Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - Rush Street Interactive, Inc. | d124075dex232.htm |

| EX-23.1 - EX-23.1 - Rush Street Interactive, Inc. | d124075dex231.htm |

| EX-21.1 - EX-21.1 - Rush Street Interactive, Inc. | d124075dex211.htm |

| EX-10.9 - EX-10.9 - Rush Street Interactive, Inc. | d124075dex109.htm |

| EX-10.8 - EX-10.8 - Rush Street Interactive, Inc. | d124075dex108.htm |

| EX-5.1 - EX-5.1 - Rush Street Interactive, Inc. | d124075dex51.htm |

Table of Contents

As filed with the Securities and Exchange Commission on February 5, 2021

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

Rush Street Interactive, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 7999 | 84-3626708 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

900 N. Michigan Avenue, Suite 950

Chicago, Illinois 60611

(312) 915-2815

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Gregory A. Carlin

Rush Street Interactive, Inc.

900 N. Michigan Avenue, Suite 950

Chicago, Illinois 60611

(312) 915-2815

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

James S. Rowe

Brian Wolfe

Kirkland & Ellis LLP

300 North LaSalle

Chicago, Illinois 60654

Tel: (312) 862-2000

Approximate date of commencement of proposed sale to the public: From time to time after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

☐ |

Accelerated filer |

☐ | |||

| Non-accelerated filer |

☒ |

Smaller reporting company |

☒ | |||

| Emerging growth company |

☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Securities to be Registered | Amount to be Registered(1) |

Proposed Maximum Offering Price per Share(3) |

Proposed Maximum Aggregate Offering Price |

Amount of Registration Fee | ||||

| Class A common stock, par value $0.0001 per share(4) |

18,175,000 | $11.50(2) | $209,012,500(2) | $22,803.26 | ||||

| Class A common stock, par value $0.0001 per share(5) |

172,425,000 | $19.003) | $3,276,075,000(3) | $357,419.78 | ||||

| Warrants to purchase Class A common stock(6) |

6,675,000 | —(6) | — | — | ||||

| Total |

$3,485,087,500 | $380,223.04 | ||||||

|

| ||||||||

|

| ||||||||

| (1) | Pursuant to Rule 416 under the Securities Act of 1933, as amended (the “Securities Act”), the registrant is also registering an indeterminate number of additional shares of Class A common stock that may become issuable as a result of any stock dividend, stock split, recapitalization or other similar transaction. |

| (2) | Based upon the exercise price per share of Class A common stock, par value $0.0001 per share (“Class A Common Stock”), issuable upon exercise of the Warrants (as defined below). |

| (3) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(c) of the Securities Act, based upon the average of the high and low selling prices of the Class A Common Stock on January 29, 2021, as reported on the New York Stock Exchange (the “NYSE”), under the symbol “RSI.” |

| (4) | Consists of the following shares of Class A Common Stock that may be issued by us: (i) 11,500,000 shares of Class A common stock underlying the Public Warrants (as defined below), (ii) 6,600,000 shares of Class A Common Stock underlying the the Private Placement Warrants (as defined below) and (iii) 75,000 shares of Class A Common Stock underlying the Working Capital Warrants (as defined below). |

| (5) | Consists of the following shares of Class A Common Stock registered for resale by the Selling Holders (as defined below): (i) 6,600,000 shares of Class A Common Stock underlying the the Private Placement Warrants (as defined below); (ii) 75,000 shares of Class A Common Stock underlying the Working Capital Warrants, (iii) 160,000,000 shares of Class A Common Stock issuable upon upon conversion of the Retained RSI Units (as defined below) and (iv) 5,750,000 of Class A Common Stock issued upon the Class B Common Stock Conversion (as defined below) of the Founder Shares (as defined below). |

| (6) | Consists of (i) 6,600,000 Private Placement Warrants and (ii) 75,000 Working Capital Warrants. Pursuant to Rule 457(g), no separate registration fee is required for the Private Placement Warrants or Working Capital Warrants. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. The Selling Holders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED FEBRUARY 5, 2021

PRELIMINARY PROSPECTUS

Rush Street Interactive, Inc.

Primary Offering of

18,175,000 Shares of Class A Common Stock

Issuable Upon Exercise of Warrants

Secondary Offering of

172,425,000 Shares of Class A Common Stock

6,675,000 Warrants to Purchase Class A Common Stock

This prospectus relates to: (1) the issuance by us of up to 18,175,000 shares of our Class A common stock, par value $0.0001 per share (“Class A Common Stock”), that may be issued upon exercise of warrants to purchase Class A Common Stock at an exercise price of $11.50 per share, including the Public Warrants, Private Placement Warrants and Working Capital Warrants (each as defined below); and (2) the offer and sale, from time to time, by the selling holders identified in this prospectus (the “Selling Holders”), or their permitted transferees, of (i) up to 172,425,000 shares of our Class A Common Stock and (ii) up to 6,675,000 of Private Placement Warrants and Working Capital Warrants.

This prospectus provides you with a general description of such securities and the general manner in which we and the Selling Holders may offer or sell the securities. More specific terms of any securities that we and the Selling Holders may offer or sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the securities being offered and the terms of the offering. The prospectus supplement may also add, update or change information contained in this prospectus.

We will not receive any proceeds from the sale of shares of Class A Common Stock or Warrants by the Selling Holders pursuant to this prospectus or of the shares of Class A Common Stock by us pursuant to this prospectus, except with respect to amounts received by us upon exercise of the Warrants to the extent such Warrants are exercised for cash. However, we will pay the expenses, other than underwriting discounts and commissions, associated with the sale of securities pursuant to this prospectus.

Our registration of the securities covered by this prospectus does not mean that either we or the Selling Holders will issue, offer or sell, as applicable, any of the securities. The Selling Holders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information in the section entitled “Plan of Distribution.”

You should read this prospectus and any prospectus supplement or amendment carefully before you invest in our securities.

Our Class A Common Stock and Public Warrants are traded on the New York Stock Exchange (“NYSE”) under the symbols “RSI” and “RSI WS,” respectively. On January 29, 2021, the closing price of our Class A Common Stock was $18.17 per share and the closing price of our Warrants was $6.70 per share.

We are an “emerging growth company,” and “small reporting company” as those terms are defined under the federal securities laws and, as such, are subject to certain reduced public company reporting requirements.

INVESTING IN OUR SECURITIES INVOLVES RISKS THAT ARE DESCRIBED IN THE “RISK FACTORS” SECTION BEGINNING ON PAGE 27 OF THIS PROSPECTUS.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued under this prospectus or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2021

Table of Contents

i

Table of Contents

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using a “shelf” registration process. Under this shelf registration process, we and the Selling Holders may, from time to time, issue, offer and sell, as applicable, any combination of the securities described in this prospectus in one or more offerings. We may use the shelf registration statement to issue up to an aggregate of 18,175,000 shares of Class A Common Stock upon exercise of the Public Warrants, Private Placement Warrants and Working Capital Warrants. The Selling Holders may use the shelf registration statement to sell up to an aggregate of 172,425,000 shares of Class A Common Stock, up to 6,600,000 Private Placement Warrants and up to 75,000 Working Capital Warrants from time to time through any means described in the section entitled “Plan of Distribution.” More specific terms of any securities that the Selling Holders offer and sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the Class A Common Stock or Warrants being offered and the terms of the offering.

A prospectus supplement may also add, update or change information included in this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will be deemed not to constitute a part of this prospectus. You should rely only on the information contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. See “Where You Can Find More Information.”

Neither we nor the Selling Holders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any accompanying prospectus supplement or any free writing prospectus we have prepared. We and the Selling Holders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

On December 29, 2020 (the “Business Combination Closing Date”), Rush Street Interactive, Inc. (formerly known as dMY Technology Group, Inc.) consummated its previously announced business combination pursuant to that certain Business Combination Agreement, dated as of July 27, 2020 (as amended, amended and restated , or otherwise modified from time to time, the “Business Combination Agreement”), among dMY (as defined below), Rush Street Interactive, LP (“RSI”), the Business Combination Sellers (as defined below), dMY Sponsor, LLC (the “Sponsor”), and Rush Street Interactive GP, LLC, in its capacity as the Business Combination Sellers’ Representative (the transactions contemplated by the Business Combination Agreement, collectively, the “Business Combination”). As contemplated by the Business Combination Agreement, on the Business

ii

Table of Contents

Combination Closing Date, dMY Technology Group, Inc. changed its name to Rush Street Interactive, Inc. and RSI became an indirect subsidiary of Rush Street Interactive, Inc.

Unless the context indicates otherwise, references to “the Company,” “we,” “us” and “our” refer to Rush Street Interactive Inc., a Delaware corporation, and its consolidated subsidiaries following the Business Combination.

iii

Table of Contents

Where information has been sourced from a third-party, the source of such information has been identified. Unless otherwise indicated, the information contained in this prospectus on the market environment, market developments, growth rates, market trends and competition in the markets in which the Company operates is taken from publicly available sources, including third-party sources, or reflects the Company’s estimates that are principally based on information from publicly available sources.

We own or license numerous domestic and foreign trademarks and other proprietary rights that are important to our businesses, such as “Rush Street,” “BetRivers,” “21+3”, “Lucky Lady” and “Lucky,” which are protected under applicable intellectual property laws and are the property of the Company or its subsidiaries. This prospectus also contains trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks and trade names.

iv

Table of Contents

Unless otherwise stated in this prospectus or the context otherwise requires, references to:

“Board” means the members of the board of directors of the post-combination company.

“Business Combination” means the acquisitions and transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of July 27, 2020, by and among dMY, RSI, the Business Combination Sellers, the Sponsor and the Business Combination Sellers’ Representative, as amended and restated by the parties on October 9, 2020 and further amended on December 4, 2020.

“Business Combination Closing” means the closing of the Business Combination.

“Business Combination Closing Date” means December 29, 2020.

“Business Combination Seller” means each of Rush Street Interactive GP, LLC, Greg and Marcy Carlin Family Trust, Gregory Carlin, Rush Street Investors, LLC, Neil Bluhm, NGB 2013 Dynasty Trust, Einar Roosileht, Richard Schwartz and Mattias Stetz.

“Business Combination Sellers’ Representative” means Rush Street Interactive GP, LLC, in its capacity as the Business Combination Sellers’ representative.

“Charter” means the second amended and restated certificate of incorporation of the Company.

“Class A Common Stock” means the Class A Common Stock of the Company, par value $0.0001 per share.

“Class B Common Stock” means the Class B Common Stock of the Company, par value $0.0001 per share.

“Class B Common Stock Conversion” means the automatic conversion at the Business Combination Closing of all then-outstanding shares of Class B Common Stock into shares of Class A Common Stock on a one-for-one basis.

“Class V Voting Stock” means the Class V Voting Stock of the Company, par value $0.0001 per share.

“Company” refers (i) before the Business Combination, to dMY and (ii) immediately following the Business Combination, to Rush Street Interactive, Inc., as the context requires.

“Controlling Holders” means Neil G. Bluhm and Gregory A. Carlin and their respective trusts.

“DGCL” means the General Corporation Law of the State of Delaware.

“dMY” means, before the Business Combination, dMY Technology Group, Inc.

“Equity Incentive Plan” means the Rush Street Interactive, Inc. 2020 Omnibus Equity Incentive Plan, which became effective on the Business Combination Closing Date.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Exchange Rights” means the right of the Business Combination Sellers to exchange Retained RSI Units for either one share of Class A Common Stock or, at the election of RSI GP in its capacity as the general partner

v

Table of Contents

of RSI, depending on, among other things, the availability of cash at RSI after first considering the cash necessary at RSI to fund RSI’s outstanding and anticipated operating expenses, debt service costs and declared dividends (in each case, if any), license fees and expenses, tax obligations and capital for existing and continued growth in new jurisdictions, the cash equivalent of the market value of one share of Class A Common Stock, pursuant to the terms and conditions of the RSI A&R LPA.

“Founder Holders” means the independent directors of dMY (consisting of Darla Anderson, Francesca Luthi and Charles E. Wert) together with the Sponsor.

“Founder Shares” means the shares of Class B Common Stock purchased by the Sponsor and the following independent directors of the Company: Darla Anderson, Francesca Luthi and Charles E. Wert.

“GAAP” means generally accepted accounting principles of the United States.

“Initial Stockholders” means the Sponsor, Darla Anderson, Francesca Luthi and Charles E. Wert.

“Investor Rights Agreement” means the agreement, dated as of the Business Combination Closing Date, pursuant to which, among other things, the Sponsor has the right to nominate two directors to the Board and the Business Combination Sellers have the right (i) to nominate the remaining directors of the Board, and (ii) to appoint up to three non-voting board observers to the Board, in each case subject to certain conditions.

“Issued RSI Units” means 32,292,517 RSI Units that were issued to the Special Limited Partner pursuant to the Business Combination Agreement.

“IPO” means the Company’s initial public offering of units consummated on February 25, 2020.

“NYSE” means the New York Stock Exchange.

“PIPE” means the private placement that closed immediately prior to the Business Combination Closing, pursuant to which dMY issued and sold to the subscribers in that private placement an aggregate of 16,043,002 shares of Class A Common Stock at $10.00 per share, for an aggregate purchase price of $160,430,020.

“PIPE Shares” means the 16,043,002 shares of dMY’s Class A Common Stock previously sold by the subscribers in the PIPE.

“PIPE Subscription Agreements” means collectively, (i) a subscription agreement with certain funds and accounts managed by Fidelity Management & Research Company LLC (“Fidelity Subscription Agreement”) and (ii) the subscription agreements (the “Other Subscription Agreements”) by and among the Company, the Business Combination Sellers’ Representative and certain other subscribers, pursuant to which such investors purchased, together with the subscribers to the Fidelity Subscription Agreement, in connection with the Business Combination Closing, an aggregate of 16,043,002 shares of Class A Common Stock for a purchase price of $10.00 per share, for an aggregate purchase price of $160,430,020.

“Plan” means the Rush Street Interactive, Inc. 2020 Omnibus Equity Incentive Plan.

“Private Placement” means the private placement by dMY of 6,600,000 Private Placement Warrants to the Sponsor simultaneously with the closing of the IPO.

“Private Placement Warrants” means dMY’s 6,600,000 warrants sold to the Sponsor simultaneously with the closing of the IPO in a Private Placement at a price of $1.00 per warrant. Each Private Placement Warrant is exercisable for one share of Class A Common Stock of the Company at a price of $11.50 per share.

“public shares” means the shares of Class A Common Stock included in the units sold by dMY in its IPO.

vi

Table of Contents

“Public Warrant Holder” means a holder of Public Warrants.

“Public Warrants” means the warrants sold by dMY in the IPO (whether they were purchased in the IPO or thereafter in the open market). Each Public Warrant is exercisable for one share of Class A Common Stock of the Company at a price of $11.50 per share.

“Purchased RSI Units” means the 12,500,000 RSI Units sold by the Business Combination Sellers to the Special Limited Partner in connection with the Business Combination.

“Purchased RSI Units Cash Consideration” means an amount equal to $125,000,000.

“Retained RSI Units” means the 160,000,000 RSI Units that were retained by the Business Combination Sellers pursuant to the Business Combination Agreement.

“RSI” refers to Rush Street Interactive, L.P., a Delaware limited partnership.

“RSI A&R LPA” means the Amended and Restated Agreement of Limited Partnership of RSI.

“RSI GP” means RSI GP, LLC, a Delaware limited liability company and wholly-owned subsidiary of the Company.

“RSI Units” means the equity interests of RSI, following the transactions contemplated by the Business Combination.

“RSG” means Rush Street Gaming, LLC, a current affiliate of RSI.

“SEC” means the Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“Special Limited Partner” is a wholly-owned subsidiary of the Company that was formed in connection with the Business Combination.

“Sponsor” means the Company’s sponsor, dMY Sponsor, LLC.

“Working Capital Warrants” means the warrants issued by the Company to the Sponsor upon the Business Combination Closing in connection with the conversion of certain outstanding loans.

vii

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

The statements contained in this prospectus that are not purely historical are forward-looking statements. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. The information included in this prospectus in relation to our business has been provided by us and our management team, and forward-looking statements include statements relating to our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “will,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this prospectus may include, for example, statements about:

| • | the benefits of the Business Combination; |

| • | the future financial performance of the Company; and |

| • | expansion plans and opportunities. |

The forward-looking statements contained in this prospectus are based on our current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements.

As a result of a number of known and unknown risks and uncertainties, our results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors that could cause actual results to differ include:

| • | the ability to maintain the listing of our Class A Common Stock and Warrants on the NYSE; |

| • | our ability to raise financing in the future; |

| • | our success in retaining or recruiting, or changes required in, our officers, key employees or directors; |

| • | our officers and directors allocating their time to other businesses and potentially having conflicts of interest with our business; |

| • | our public securities’ potential liquidity and trading; |

| • | the lack of a market for our securities; |

| • | competition in the retail and online sports wagering and online gaming industry is intense and, as a result, we may fail to attract and retain users, which may negatively impact our operations and growth prospects; |

| • | economic downturns and political and market conditions beyond our control, including a reduction in consumer discretionary spending and sports leagues shortening, delaying or cancelling their seasons due to COVID-19, could adversely affect our business, financial condition, results of operations and prospects; |

| • | our projections, including for revenues, market share, expenses and profitability, are subject to significant risks, assumptions, estimates and uncertainties; |

| • | our growth prospects may suffer if we are unable to develop successful offerings, if we fail to pursue additional offerings or if we loses any of our key executives or other key employees; |

viii

Table of Contents

| • | we may be subject to litigation in the operation of our business and our insurance may not provide adequate levels of coverage against any claims; |

| • | the requirements of being a public company, including compliance with the Securities and Exchange Commission’s (the “SEC”) requirements regarding internal controls over financial reporting, may strain our resources and divert management’s attention, and increases in legal, accounting and compliance expenses that result from our recent Business Combination may be greater than we anticipate; |

| • | we are dependent on RSG and certain of its affiliates to provide us with certain services, which may not be sufficient to meet our needs, and we may have difficulty finding replacement services or be required to pay increased costs to replace these services to the extent that our services agreement with RSG terminates; |

| • | our business is subject to a variety of United States and foreign laws (including Colombia, where we have business operations), many of which are unsettled and still developing, and our growth prospects depend on the legal status of real-money gaming in various jurisdictions; |

| • | failure to comply with regulatory requirements or to successfully obtain a license or permit applied for could adversely impact our ability to comply with licensing and regulatory requirements or to obtain or maintain licenses in other jurisdictions, or could cause financial institutions, online and mobile platforms and distributors to stop providing services to us; |

| • | we rely on information technology and other systems and platforms (including reliance on third-party providers to validate the identity and identify the location of our users and to process deposits and withdrawals made by our users), and any breach or disruption of such information technology could compromise our networks and the information stored there could be accessed, publicly disclosed, lost or stolen; |

| • | we license certain trademarks and domain names to RSG and its affiliates, and RSG’s and its affiliates’ use of such trademarks and domain names, or failure to protect or enforce our intellectual property rights, could harm our business, financial condition, results of operations and prospects; |

| • | we rely on licenses and service agreements to use the intellectual property rights of third parties which are incorporated into or used in our products and services; |

| • | we may invest in or acquire other businesses, or may invest or spend the proceeds of our recent Business Combination in ways with which our investors may not agree or which may not yield a return, and our business may suffer if it we are unable to successfully integrate acquired businesses into our company or otherwise manage the growth associated with multiple acquisitions; and |

| • | other factors detailed under the section entitled “Risk Factors” herein. |

Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

ix

Table of Contents

This summary highlights selected information from this prospectus and does not contain all of the information that is important to you in making an investment decision. This summary is qualified in its entirety by the more detailed information included in this prospectus. Before making your investment decision with respect to our securities, you should carefully read this entire prospectus, including the information under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations of RSI,” and the financial statements included elsewhere in this prospectus.

Overview

We are a leading online gaming company focused primarily on online casino and online sports betting in the U.S. and Latin American markets. We provide customers an array of offerings such as real-money online casino wagering, online and retail sports wagering, and social gaming. We launched our first social gaming website in 2015 and began accepting real-money wagers in the United States in 2016. We currently operate real-money online casino and online sports wagering in Michigan, New Jersey and Pennsylvania; currently operate online sports wagering in Colorado, Illinois, Iowa, Indiana and Virginia; and currently provide retail sports wagering services in Illinois, Indiana, Michigan, New York and Pennsylvania. In addition, in 2018, we became the first United States online gaming operator to launch in Colombia, which was an early adopting Latin American country to legalize and regulate online casino wagering and sports wagering nationally. We have a market access agreement in Virginia, which has legalized online sports wagering and where we plan to launch online gaming when Virginia authorizes it. We also have a market access agreement in New York to launch online sports and online casino wagering when New York authorizes those activities.

We were founded by experienced gaming operators Neil Bluhm, Greg Carlin and Richard Schwartz, whose mission was to offer real-money online gaming products in legal and regulated markets with a particular focus on the emerging United States opportunity. In 2014, we acquired the source code that served as the starting point for our proprietary technology and has continued to develop it since then with a talented in-house product development team. Our management’s focus has always been on developing the most player-friendly online casino wagering experience in the industry. Our proprietary online gaming platform is the foundation of our digital business and reflects a suite of technologies that together provide a leading management, administrative, reporting, and regulatory compliance end-to-end solution that powers our operations. The platform incorporates multiple sophisticated technologies and provides a central back office function to manage player accounts, payments, risk, bonusing and loyalty programs, while ensuring that we can deliver a seamless experience for both players and gaming operators, as well as a wide range of proprietary player bonusing and loyalty features. This technology platform is flexible and supports both real-money online wagering and social gaming on a single code base. We began offering online casino wagering utilizing this technology in the United States in September 2016. Following, the lifting of the federal restrictions on sports wagering in May 2018 as a result of the United States Supreme Court’s repeal of the Profession and Amateur Sports Protection Act of 1992 (“PASPA”), we began offering online sports wagering utilizing the same proprietary online gaming platform with the same emphasis on player-friendly features.

Prior to the Business Combination, our founders had invested approximately $50 million into the company. This capital was primarily used to fund the development of the proprietary online gaming platform and products, recruit and grow an experienced team, and expand into new geographic and product markets. Our management has focused on being financially disciplined.

Powering our product offerings is our proprietary online gaming platform that allows us to prioritize speed to market for new gaming offerings while providing an engaging and unique user experience for its players. Since 2016, we have leveraged our platform to expand our real-money operations and launch in the markets

1

Table of Contents

listed below. Additionally, we were the first company to launch online or retail sports wagering in several of these markets, which we believe has allowed us to acquire customers at a lower cost than we could have if launching in a more mature market.

Our real-money wagering products are offered under the BetRivers & PlaySugarhouse (United States) and RushBet.co (Colombia) brands. Our social gaming products are marketed in association with each brick-and-mortar casino partner brand for business-to-business (“B2B2C”), and under the RushGames (and soon BetRivers) brands for business-to-consumer (“B2C”). The choice of branding is market-specific and partner-specific and based on brand awareness, market research, and marketing efficiency.

Our Operating Model

We leverage our proprietary online gaming platform to enter new markets. Our operating model focuses on being nimble, innovative, and “first to market” in markets where online wagering has been newly legalized. Often in advance of markets legalizing online gaming, we build relationships with brick-and-mortar casino operators and other potential partners who are looking for online gaming and sports wagering partners.

We leverage our relationships with brick-and-mortar casino operators to find stable, reliable and quality partners for online gaming collaboration. Upon securing an access partner in a local market (if required or desirable) and before we launch operations in that market, we customize our proprietary online gaming platform to the regulations of the jurisdiction. Upon entering a new market, we employ a number of marketing strategies to obtain new customers as well as leverage the database of casino partners when applicable. In addition, we also refine our product offering and marketing strategies over time based on data gleaned from each market.

We offer a loyalty program that rewards consumers in exciting, fair and transparent ways. We are dedicated to reciprocating player loyalty by ensuring there are exciting benefits at each of the ten player loyalty levels we currently offer. Based on player research, we addressed player concerns about lack of transparency when it comes to awarding, redeeming, and tracking bonuses. We enable players to easily track their loyalty and bonus progressions and give players 100% control over when and how to redeem rewards. Players have the option to ‘bank’ awarded bonuses in our proprietary ‘bonus bank’, which they can draw from whenever they wish under our industry-leading 1x wager requirement. Every player accumulates bonus store points on every real-money wager made, regardless of loyalty level. These points unlock bonuses and are used to play our fun proprietary bonus games (free scratch cards, wheel spins, and bingo games) with prizes that guarantee bonus money.

Although we have been a first-mover in many markets, we have demonstrated success even when not being first to enter a market. We entered the New Jersey online casino wagering market approximately three years after the market launched. Less than three years after beginning operations in New Jersey, we grew to operating the #4 brand in online casino wagering revenue in New Jersey, out of 19 total in the market, according to Eilers & Krejcik Gaming’s (“EKG”)’s United States Online Casino Tracker for April 2019.

Our success in New Jersey is also noteworthy because we compete with many other companies who have land-based casinos in the state. Neither we nor Rush Street Gaming, an affiliated land-based casino operator, operate a land-based casino in New Jersey. We believe our performance in New Jersey shows that we can be successful entering competitive markets without the benefit of a land-based casino presence.

Our operating model has also enabled us to become the #1 online casino wagering operator in terms of revenue in Pennsylvania as of December 31, 2020, the largest state by population in the United States where online casino wagering is currently authorized. According to the Pennsylvania Gaming Control Board, we generated 71.8% more taxable online slot machine and table games wagering revenue than the #2 operator during 2020.

2

Table of Contents

We have been the #1 operator of online slot machines and table games in terms of taxable revenue in every quarter since we launched in Pennsylvania. We believe that our performance in Pennsylvania is particularly notable as we have yet to launch online gaming via an Apple iOS App in Pennsylvania. According to the Pennsylvania Gaming Control Board, in Q4 2020, our Pennsylvania taxable slot machine and table games revenue market share was 28.6%, compared to 29.9% in Q1 2020, 34.1% in Q2 2020, and 30.6% in Q3 2020. This Q4 2020 market share includes competition from both FanDuel and DraftKings, which launched online slot machine and table games wagering in Pennsylvania in January 2020 and May 2020, respectively.

Our market share in the sub-category of online slot machines in Pennsylvania is even more pronounced. According to the Pennsylvania Gaming Control Board, in Q4 2020, despite added competition, our online slot machine taxable revenue market share was 34.8%, compared to 35.4% in Q1 2020, 38.4% in Q2 2020 and 36.6% in Q3 2020. In Q4 2020, we generated 170.3% more online slot machine taxable revenue than the #2 operator in Pennsylvania as measured by the Pennsylvania Gaming Control Board.

To further illustrate our strong performance in online slot machine revenue in Pennsylvania, we were able to achieve our #1 share of online slot machine taxable revenue during Q4 2020 while at the same time issuing fewer promotional credits than the competition. According to data from the Pennsylvania Gaming Control Board, our promotional credits as a percentage of slot machine revenue (before deducting promotional credits) was 21.3% in Q4 2020. The rest of the Pennsylvania online casinos’ promotional credits as a percentage of slot machine revenue (before deducting promotional credits) was 38.6% in Q4 2020. We believe this data point is a testament to the quality of our proprietary online gaming platform, player-friendly features, and customer service, that we can have #1 market share while offering significantly less promotional credits as a percentage of revenue than the competition.

Unlike sports wagering, which predominately appeals to males, casino wagering appeals roughly equally to both males and females. In Q3 2020, approximately 90% of our monthly unique online sports wagering-only players were male. For Q3 2020, approximately 55% of our monthly unique online casino wagering-only players were female.

It has been our experience that among casino customers, female customers are more likely to play slot machines, while male customers are more likely to play table games. We believe that we are able to achieve a strong market share in casino revenue, in general, and an even stronger market share in slot machine revenue, in particular, given that our brands, products and marketing strategies appeal to both male and female casino customers. Further, we believe that we are well positioned to continue to appeal to female slot machine customers over the long run.

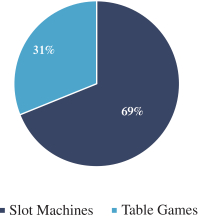

In Q4 2020, Pennsylvania marketwide slot machine taxable revenue accounted for the majority of combined online slot machine and table games taxable revenue in Pennsylvania.

3

Table of Contents

Q4 2020 Pennsylvania Marketwide Taxable Revenue Split (Online Slot Machines vs. Table Games)

Source: Company management estimates; Pennsylvania Gaming Control Board

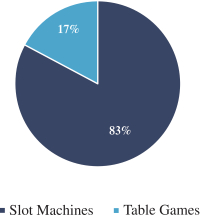

We believe that we are well positioned to be a slot machine market leader when additional markets launch. We have derived a higher percentage of our net revenues from slot machines than the market as a whole and expect this trend to continue as new states launch online.

RSI Q4 2020 Pennsylvania Taxable Revenue Split (Online Slot Machines vs. Table Games)

Source: Company management estimates; Pennsylvania Gaming Control Board

In the long run, we believe that slot machines will be a larger contributor to online casino wagering revenue than table games, just as slot machines have been a larger contributor than table games to land-based casino revenue. As an example, in Q4 2020, Pennsylvania land-based casino slot machines generated $326 million of revenue, about 2.5 times more than the $133 million of land-based casino revenue generated by table games according to data from the Pennsylvania Gaming Control Board.

We believe our online casino wagering customers are also older on average than those of our competitors. We believe that on average, customers who are 40 – 70 years of age generally have more disposable income, which they can spend on entertainment such as online gaming, than younger customers. Through Q4 2020, our online casino wagering-only customers in New Jersey and Pennsylvania averaged 43.3 years of age.

4

Table of Contents

In addition to online casino wagering, we have generated more than our fair share of online sports wagering taxable revenues since launching in Pennsylvania in 2019. We have ranked in the top 3 in online sports wagering taxable revenue in all but three months. In Q4 2020, we have generated a 7.9% share of the online sports wagering taxable revenue in Pennsylvania according to data from the Pennsylvania Gaming Control Board.

We have experienced significant success with retail sports wagering as casinos using our retail sports wagering services generated the most sports wagering revenue of any casino in each of New York and Pennsylvania in the twelve months ending September 2020 (per the New York State Gaming Commission and Pennsylvania Gaming Control Board, respectively).

Outside of the United States, we have experienced strong growth in our Colombia business. We entered the Colombia market in 2018 and gained valuable operational experience with respect to online sports wagering. When PASPA was struck down in the United States, we were able to leverage the operational experience gained in Colombia and quickly apply that knowledge to the United States market. Our business in Colombia has grown strongly since we entered the market. While 2020, especially the second quarter, was impacted by the lack of live sporting events, online casino revenue has risen almost enough to make up for the loss in online sports wagering revenue.

Lastly, with minimal marketing spend to acquire users, our social gaming business has grown significantly in the last two years.

While we have experienced strong market share and revenue growth as discussed above, we have also incurred significant increases in its cost of revenue and other operating costs and expenses to support this growth. Our comprehensive loss for the first nine months of 2019 as compared to the first nine months of 2020 increased from $7.17 million to $94.76 million.

Our People

We have built a team of industry professionals focused on technology and operations, with a highly experienced senior management team with significant experience in the online and retail gaming industries. Our culture focuses on valuing employees and enabling them to grow and take on roles that suit their strengths. We believe our culture combined with our growth and success has created very high rates of employee retention. As of February 1, 2021, we had approximately 249 employees and consultants.

Our Products and Economic Model

Our Revenue-Generating Product Offerings

B2C Operations. We currently have four main B2C product offerings — online casino wagering, online sports wagering, retail sports wagering and social gaming. In its B2C offerings, we offer products to users. In most markets, we pay a fee to third-party license holders to offer online casino wagering and online sports wagering. In the case of retail sports wagering, we make payments to the hosting property to have the right to conduct B2C operations. In the case of social games, we are able to conduct operations in jurisdictions without third-party licenses unless prohibited by law. B2C will be our primary business model on a go-forward basis in new jurisdictions.

B2B2C Operations. We currently have three main business-to-business-to-consumer (“B2B2C”) product offerings: online casino wagering, online sports wagering and social gaming. In our B2B2C offerings, we offer products to users on behalf of third-party land-based casinos in Pennsylvania and Illinois. This business model

5

Table of Contents

works the same way as B2C operations where we supply the platform and provide all of the necessary services for the operation (“managed services”). The only exception is that any operator license fees, hardware costs and expenses from the operations including marketing expenses are absorbed by partners after we receive a platform and managed services fee calculated as a percentage of the revenue less certain deductions.

In Pennsylvania and Illinois, the partner properties have paid upfront license fees required to operate sports wagering and online gaming in those states. In Pennsylvania, the partner casinos paid a total of $30 million in upfront license fees—$20 million for sports wagering and $10 million for online casino wagering. In the case of Pennsylvania, the gaming tax rates for online slot machines (54%) and online sports wagering (36%) are high. In Illinois, the partner casino paid a $10 million upfront license fee for sports wagering.

Outside of Pennsylvania and Illinois, we do not have any other agreements for B2B2C operations of real-money online gaming.

We also operate social gaming on behalf of third-party partner casinos whereby we split the revenue with the partner casino.

B2B Services. We offer business-to-business (“B2B”) services to third parties to enable them to operate retail sports wagering under their own brand. In the case of B2B operations, we provide services and is typically paid by partners based on a percentage of revenue. Current B2B customers for retail sports wagering include land-based casinos in Pennsylvania, New York, Illinois and Michigan.

Online Casino Wagering

Online casino wagering offerings typically include the full suite of games available in land-based casinos, such as blackjack, roulette and slot machines. For these offerings, we function similarly to land-based casinos, generating revenue through hold, or gross winnings, as users play against the house. There is volatility with online casino wagering, as with land-based casino wagering, but as the volume of wagers placed increases, the revenue retained from wagers placed becomes easier to predict. Our experience has been that online casino wagering is less volatile than online sports wagering.

Our online casino offering consists of a combination of licensed content from leading suppliers in the industry and a small number of games that we have developed in-house. Third-party content is subject to standard revenue-sharing agreements specific to each supplier, whereby the supplier receives a percentage of the net gaming revenue generated from the casino games played on our platform (dependent on our overall gross gaming revenue for online casino wagering). In exchange, we receive a limited license to offer the games on its platform to users in jurisdictions where use is approved by the regulatory authorities. Revenue generated through our self-developed major casino games such as our multi-bet blackjack (with licensed side bets: 21+3, Lucky Lady, Lucky Lucky), and our single deck blackjack results in us making decreased revenue share payments as a percent of revenue.

Sports Wagering

Sports wagering, whether the wager is placed online or in a retail (i.e., land-based) environment, involves a user placing a wager on an event at some fixed odds (a “Proposition”) determined by us. In the event the user wins, we pay out the bet. We take some risk on the wager. Our revenue is generated by setting odds such that there is a built-in theoretical margin in each Proposition offered to our users. While different outcomes of the events may cause volatility in our revenue, we believe we can deliver a fairly stable wagering win margin over the long term.

6

Table of Contents

Integrated into our online sports wagering platform is a third-party risk and trading platform currently provided by Kambi. In addition to traditional fixed-odds wagering, we offer other sports wagering products including in-game wagering and multi-sport parlay wagering. We have also incorporated live streaming of sporting events into our sports wagering offering.

Our online sports wagering business experiences seasonality based on the relative popularity of certain sports. Although exciting sporting events occur throughout the year, our online sports wagering users are most active during the American football season as well as during the basketball seasons (NBA and NCAA).

Social Gaming

Our social gaming business has three main goals: building online databases in key markets ahead of and post-legalization and regulation, increasing engagement and visitation to our brick-and-mortar casino partner properties, and generating revenues. The social gaming product is a marketing tool that keeps the brands present in mind and engaging with customers through another channel while providing the entertainment value the patrons seek. While the vast majority of our social gaming players enjoy engaging with the site without paying, there are a number of players that top-up their virtual coins through our social gaming cashier with a variety of packages for sale. The virtual currency can only be used within our social games sites and has no monetary value outside of the game. We pay a percentage of the social gaming revenue derived from the purchase of the virtual coins with content suppliers. In B2B2C partnerships, the net social revenue is split between the partner and us.

We also utilize our social gaming products to cross-sell to real-money wagering products in jurisdictions where real-money wagering is authorized.

Cost of Revenue

In addition to the casino content costs and costs that we pay to our sports wagering trading and risk provider, we have four main elements of cost of revenue: payment processing fees and chargebacks, product taxes, platform and content costs and revenue share/market access arrangements. We incur payment processing costs on user deposits and occasionally chargebacks. Our primary product taxes are state taxes, which are determined on a jurisdiction-by-jurisdiction basis and range from 6.75% to 54% of gross revenue minus applicable deductions. Excluding Pennsylvania, the tax rate for sports wagering ranges from 6.75% to 17% and the tax rate for online casino wagering ranges from 15% to 28% in the markets where we are currently operating. Importantly, each state defines “gross revenue” differently based on the deductibility of promotion expenses. In addition to state taxes in the United States, we pay a federal excise tax of 0.25% of United States sports wagering handle. Our platform and content fees are primarily driven by costs for use of casino content, costs for sports betting trading services and hosting, third-party vendors that provide certain elements of our platform technology (such as geolocation and know-your-customer). Finally, our revenue share fees are primarily driven by arrangements with land-based casinos in states where land-based casinos have the rights (including many times the exclusive rights) to online casino and sports wagering.

Advertising & Marketing

Our ability to effectively market is critical to operational success. Using experience, dynamic learnings and analytics, we leverage marketing to acquire, convert and retain customers. We use a variety of paid marketing channels, in combination with compelling offers and unique game and site features, to attract and engage customers as well as earned media. Furthermore, we optimize our marketing spend using data collected since the beginning of our operations. Our marketing spend is based on a return-on-investment model that considers a variety of factors, including the products offered in the jurisdiction, the performance of different marketing channels, predicted lifetime value, marginal costs and expenses and behavior of users across various product offerings.

7

Table of Contents

Where paid marketing is concerned, we leverage a broad array of advertising channels, including television, radio, social media platforms, sponsorships, affiliates and paid and organic search, and other digital channels. These efforts are concentrated within the specific jurisdictions where we operate or intend to operate. We believe that there is significant benefit to having a flexible approach to advertising spending as we can move our advertising spending around based on dynamic testing of what advertising methods and channels are working and what channels and methods are not working.

Distribution

We distribute our product offerings through various channels, including websites (traditional and mobile), direct application downloads and global direct-to-consumer digital platforms such as the Apple App Store.

B2C Market Access. We have developed proprietary technology, product offerings and partnerships to create a sustainable advantage in the sports wagering and online gaming industry. Strategic multi-year arrangements with casinos enable us to offer our products to users. We have entered into the following arrangements where legislation or regulations require it us enter the market through a relationship with a land-based casino:

| • | In September 2015, we entered into an agreement with Golden Nugget Casino in Atlantic City, which enabled us to operate online casino wagering and subsequently the agreement was amended to include online sports wagering in New Jersey. We subsequently terminated the portion of the agreement related to online sports wagering. |

| • | In October 2018, we entered into an agreement with Monmouth Racetrack in New Jersey, which enabled us to operate online sports wagering in New Jersey. |

| • | In June 2019, we entered into an agreement with French Lick Casino & Resort in Indiana, which enabled us to operate online and retail sports wagering in Indiana and online casino wagering if authorized in Indiana. |

| • | In August 2019, we entered into an agreement with Wild Rose casino group in Iowa, which enabled us to operate online sports wagering in Iowa and online casino wagering if authorized in Iowa. |

| • | In January 2020, we entered into an agreement with J.P. McGill’s Hotel & Casino in Colorado, which enabled us to operate online sports wagering in Colorado. |

| • | In March 2020, we entered into an agreement with The Little River Band of Ottawa Indians of Michigan, which enabled us to operate online and retail sports wagering and online casino wagering in Michigan. |

| • | In October 2020, we entered into an agreement with Rivers Casino & Resort Schenectady (“Rivers Schenectady”) to enable us to offer online sports wagering and online casino wagering if either or both of those activities are authorized in New York. |

| • | In October 2020, we entered into an agreement with Rivers Casino Portsmouth to conduct online sports wagering in Virginia and online casino wagering if authorized in Virginia. |

| • | In December 2020, we entered into an agreement with Mountaineer Casino, Racetrack & Resort to conduct online casino wagering in West Virginia. |

B2B2C and B2B Distribution. We have relationships with the following casino partners:

| • | In November 2018, we entered into an agreement with SugarHouse Casino (since renamed Rivers Casino Philadelphia) to provide retail sports wagering services at SugarHouse Casino in Philadelphia. |

8

Table of Contents

| • | In November 2018, we entered into an agreement with Rivers Casino Pittsburgh to provide retail sports wagering services at Rivers Casino Pittsburgh. In May 2019, we entered into an agreement to conduct online sports wagering through SugarHouse Casino throughout Pennsylvania. In June 2019, we also entered into an agreement to conduct online sports wagering through Rivers Philadelphia throughout Pennsylvania. |

| • | In July 2019, we entered into an agreement with Rivers Casino & Resort Schenectady to provide retail sports wagering services at Rivers Casino & Resort Schenectady in New York. |

| • | In March 2020, we entered into an agreement with Rivers Casino Des Plaines to provide retail sports wagering services at Rivers Casino Des Plaines in Illinois. We expect to enter into an agreement with Rivers Casino Des Plaines to provide Rivers Casino Des Plaines with software and services for its online sports wagering and online gaming sites in Illinois. We have begun providing the services for online sports wagering to Rivers Casino Des Plaines in anticipation of the agreement. |

| • | In March 2020, we entered into an agreement with The Little River Band of Ottawa Indians of Michigan to provide retail sports wagering services at their Little River casino. |

| • | In May 2020, we entered into an agreement with Coushatta Casino Resort, a gaming enterprise owned and operated by the Coushatta Tribe of Louisiana to offer customer-branded free-to-play social casino services. |

| • | We entered into an agreement in October 2020 with Rivers Casino Portsmouth to provide retail sports wagering services at the yet-to-be-developed Rivers Portsmouth Casino in Virginia. |

Company Development Team

Our development team is led by our Chief Information Officer, Einar Roosileht, and consists of team members with expertise in system architecture, client & server-side product engineering, database architecture, product engineering management, site/app design and development, project management, security, and technical support. The team constantly aims to innovate and differentiate our product offering.

9

Table of Contents

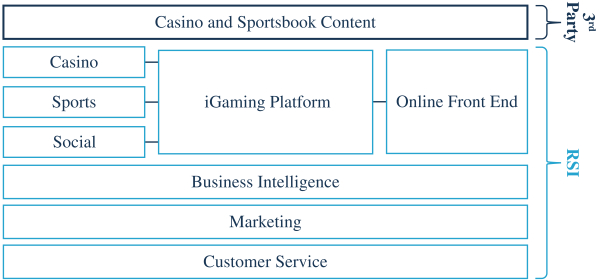

Proprietary Online Gaming Platform Overview

Our proprietary online gaming platform has been developed and is operated by a seasoned online gaming executive team with global experience operating all product categories, with particular expertise in the two largest online/mobile product categories: casino and sports wagering. Our proprietary online gaming platform and technology stack give us the ability and flexibility to develop and provide a personalized and data driven player journey. We are able to develop and implement new features in real-time, which enhance the customer experience and increase customer retention. A key feature of the proprietary platform is the ability to customize the playing experience for each player. We achieve player customization by analyzing player history and transactions and offering customized promotions and real-time betting driven bonusing.

By owning its own proprietary online gaming platform, we have been able to improve the user experience and incorporate key aspects of its operational services into our product offering:

| • | Payments & Risk Management |

| • | Regulatory Online Reporting & Accounting / iGaming Compliance |

| • | Website Management / Games Management / Live Tech Ops / Security |

| • | Online Affiliate Management & Tracking |

| • | Retention / CRM / Business Intelligence & Analytics |

| • | Customer Service |

Our Industry and Opportunity

We currently operate within the online gaming industry. The global gaming industry includes a wide array of products from lotteries to bingo, slot machines, casino games and sports wagering, across land-based and online platforms. The industry has various operators and stakeholders across the private and public sectors, including traditional brick-and-mortar casinos, state-run lottery operators, Native American tribes, legacy online gaming operators, racetracks/racinos/video lottery terminals and gaming technology companies.

Recently, online gaming has seen outsized growth and increased penetration. Per EKG, regulated online gaming grew in Europe, the most mature online gaming market in the world, at an annual rate of 11% from 2018 to 2019.

10

Table of Contents

The following trends are potential drivers of growth in this industry:

| • | New jurisdictions in the United States and internationally authorizing and/or privatizing their online casino wagering and online sports wagering industries. |

| • | Increased consumer adoption of digital activities including casino and sports wagering. While many other large United States industries (i.e. banks, retail stores, movies, etc.) digitalized over a decade ago, the United States gaming industry is just starting to do so now. |

In the past decade, there has been significant regulatory momentum with respect to online gaming across the globe. This momentum has been particularly relevant in developed nations whose citizens have disposable income to spend on entertainment and gaming. For example, United Kingdom, Denmark, France, Spain, Italy, Ireland, Denmark, Poland, Sweden, and Switzerland have legalized and regulated online casino and online sports wagering. All of the aforementioned countries are classified in the “high income” income group according to the World Bank. We expect this trend to continue moving forward, most notably in the United States.

United States Gaming Industry

We see tremendous opportunity in the United States market. As United States jurisdictions become regulated and mature, online gaming penetration may approach that of other developed nations. For example, the UK Gambling Commission (“UKGC”) reported that approximately 39% of the U.K.’s gross gaming revenue comes from online wagering. To put that U.K. figure into context, Pennsylvania, which launched online casino and sports wagering in H1 2019, generated a combined $1.71 billion in taxable revenue from land-based casino and online casino and online sports wagering revenue in H2 2019 according to data from the Pennsylvania Gaming Control Board. Of this amount, only approximately 4.5% came from online casino and online sports wagering. Although the United States has a much more significant land-based casino industry than the U.K., the statistic shows the future opportunity for online gaming in the United States.

United States Online Casino Wagering

Currently, online casino wagering has been authorized in fewer states than sports wagering. Online casino wagering is authorized in only six states: Delaware, Michigan, New Jersey, Pennsylvania, West Virginia and Nevada (although regulators have not authorized online casino wagering outside of physical casinos in Nevada). We believe there is great potential for revenue growth as new markets open in the United States online casino wagering industry. As an example, the mature land-based casino industry in the United States is substantial. The American Gaming Association estimated that United States land-based commercial and tribal casinos combined for $75.4 billion in revenue in 2018.

Online casino wagering was first launched in New Jersey in the latter half of 2013. The market got off to a slow start; however, revenue has risen steadily over the last several years. Online casino wagering also was not negatively impacted when online sports wagering was introduced in New Jersey in 2018. Online casino wagering revenue from slot machines and table games in New Jersey grew from $277.3 million in 2018 to $461.8 million in 2019 to $931.5 million in 2020 according to the New Jersey Division of Gaming Enforcement. Furthermore, land-based casino revenue in New Jersey grew from $2.51 billion in 2018 to $2.69 billion in 2019 according to the New Jersey Division of Gaming Enforcement, showing that land-based casino revenue can grow at the same time that online casino wagering revenue grows. However, it should be noted that the land-based casino revenue in New Jersey decreased to $1.51 billion in 2020, likely in large part due to stay-at-home orders and similar effects of the COVID-19 pandemic and related economic uncertainty. This fact may serve as a catalyst for lawmakers in other states with land-based casinos to consider authorizing online casino wagering.

11

Table of Contents

We believe that more states have and will consider authorizing online casino wagering for the following reasons.

| • | We believe that COVID-19 has reduced tax revenue in many states, increasing the need for new sources of tax revenue. |

| • | In states that have land-based casinos, COVID-19 caused temporary casino closures, which reduced tax revenue. |

| • | We believe that COVID-19 has caused increased general consumer adoption of digital activity including online gaming. |

| • | Online casino wagering generated more tax revenue compared to online sports wagering in New Jersey in 2019, meaning authorizing online sports wagering alone may not optimize tax revenue. |

| • | Land-based casino revenue grew as online casino wagering grew in New Jersey from 2018 to 2019, demonstrating that land-based casino revenue can grow with online casino wagering revenue (although it did not grow in 2020 likely in large part due to the COVID-19 pandemic and related economic uncertainty). |

| • | We believe that the land-based casino industry, an important stakeholder in many states, generally has shown a wider acceptance of online casino wagering. |

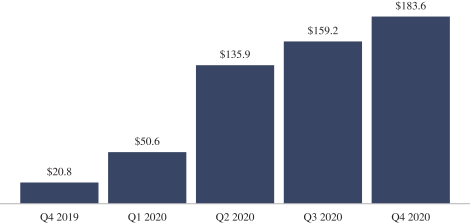

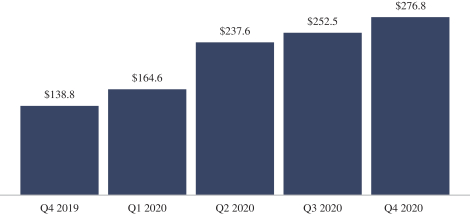

Both Pennsylvania and New Jersey were each experiencing online casino wagering taxable revenue growth prior to COVID-19; however, that growth accelerated in March 2020 into Q4 2020. The charts below highlight the growth of online slot and table games taxable revenue in New Jersey and Pennsylvania since Q4 2019:

Pennsylvania Online Slot and Table Taxable Revenue ($ in millions)

Source: Pennsylvania Gaming Control Board

12

Table of Contents

New Jersey Online Slot and Table Gross Revenue ($ in millions)

Source: New Jersey Division of Gaming Enforcement

United States Sports Wagering

On May 14, 2018, the United States Supreme Court ruled that PASPA — a nationwide ban of sports wagering — was unconstitutional, thereby allowing states (beyond the few states that were grandfathered into the PASPA law by virtue of authorizing sports wagering prior to PASPA) to enact their own sports wagering laws. In the two years since the United States Supreme Court’s decision, 22 states and the District of Columbia have legalized sports wagering. Of those 23 jurisdictions, 15 states have authorized statewide online sports wagering while eight remain retail-only at casinos or retail locations.

According to data compiled by EKG, the United States generated approximately $492 million in online sports wagering revenue in 2019. While the overall industry is still nascent, growth has been strong. For example, December 2019 online sports wagering revenue in New Jersey, the first state to regulate sports wagering after PASPA was struck down, grew 41% year-over-year including 74% growth in online sports wagering revenue according to data compiled from the New Jersey Division of Gaming Enforcement.

According to data compiled by EKG, the United States generated $268.6 million in legal wagers on Super Bowl LIV held in February 2020. Of that amount, only 47% came from outside of Nevada, showing the opportunity for future growth for online sports wagering in the United States.

13

Table of Contents

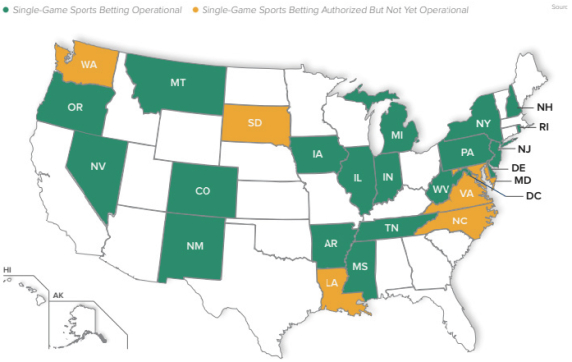

United States Sports Wagering Market Landscape

Source: EKG United States Sports Betting Policy Monitor – Released January 21, 2021

We believe the United States sports wagering market still has significant opportunity for growth. Only approximately 35% of the United States currently has access to online sports wagering, per EKG. This fact is significant when one considers that according to the New Jersey Division of Gaming Enforcement, more than 80% of New Jersey sports wagering revenue in February 2020, the last month not impacted by COVID-19, came via online wagering. We note that states such as California, Florida, New York and Texas still have not legalized online sports wagering. We believe the sports wagering industry will grow significantly over the next five years as more states authorize sports wagering and as current operating markets mature.

14

Table of Contents

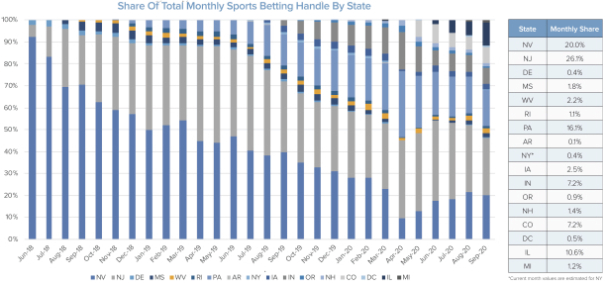

Share of Total Monthly Sports Wagering Handle (September 2020)

Source: EKG United States Sports Betting Market Monitor – Released November 2020

New Jersey and Pennsylvania, two states that offer online sports wagering, accounted for approximately 42% of all sports wagering handle across the United States in November 2020 according to EKG. Online sports wagering handle outperforms retail handle; however, some states have only legalized retail sports wagering (e.g., New York and Arkansas) and other states have legalized restricted forms of online sports wagering (e.g., in-person registration required in Nevada and for a period of time in Iowa, Illinois and Rhode Island). As more states legalize and loosen restrictions around online sports wagering, New Jersey and Pennsylvania will hold less dominant positions across the United States

United States Online Gaming: Estimating the Total Addressable Industry Size

If every state in the United States were to legalize online casino wagering, based on state level projections from EKG, it is projected that the United States market would generate approximately $20 billion in revenue.

If every state in the United States were to legalize online sports wagering, based on state level projections from EKG, it is projected that the United States market would generate approximately $15 billion in revenue.

Latin America Gaming Industry

Latin America is another area of focus for us. Since 2018, we have been operating online gaming in Colombia, a country with a population of approximately 49 million. We believe this experience will enable us to expand further in Latin America as more markets become regulated. We plan to expand further across Latin America and begin operating in other countries. Online gaming is also authorized in Mexico and Brazil, which have populations of approximately 129 million and 212 million, respectively. Both Mexico and Brazil still have relatively low internet penetration, with 60% of both populations having internet access compared to 76% in the US and 95% in the UK, so the expansion of internet penetration in these countries will allow us to grow our revenues from online wagering.

15

Table of Contents

The highest populated country in Latin America, Brazil, legalized sports wagering in December 2018. While the government has been in the process of creating a regulatory framework since then, Brazil recently moved to “privatize” its impending sports wagering market in response to the COVID-19 pandemic. By including sports wagering in its Council of Investment Partnerships Program (IPP), Brazil will allow potential operators to bid on a limited number of sports wagering licenses instead of the previous plan that called for an “unlimited” number of operators and tax revenue dispensed to the government. We believe given our experience and success in neighboring Colombia, we will be well-qualified to obtain a sports wagering license in Brazil.

Competitive Strengths

As we expand and launch in new states and territories, we are well-positioned to maintain and build upon our accomplishments by virtue of our competitive strengths:

Proprietary Online Gaming Platform. We acquired our proprietary platform in 2014 and have refined it since then. Owning a proprietary online gaming platform has allowed us to innovate quickly and introduce numerous player-friendly features. We believe that these features have led to increased conversion rates from registrations to first-time depositors, increased levels of customer engagement and retention and increased player spending. Further, we are capable of making changes to our proprietary online gaming platform at a rate that management believes is among the fastest in the industry. As the United States industry develops, our proprietary online gaming platform should help us better cater to the evolving needs of the consumer. In the long run, we believe that our proprietary online gaming platform will lead to reduced costs and improved revenue per customer relative to peers, many of which license their technology from third parties.

Unique and Diversified Product Offering. We have prioritized the customization of its products and platform. For example, we create our own online casino games, which are higher margin to us than those licensed from third parties. We have also developed and incorporated numerous proprietary bonusing features that appeal to casino and sports wagering customers alike.