Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FLUSHING FINANCIAL CORP | ffic-20210204x8k.htm |

Exhibit 99.1

| Piper Sandler Investor Meetings February 4, 2021 contact: susan.cullen@flushingbank.com | phone: 718.961.5400 | website: www.flushingbank.com |

| Safe Harbor Statement 2 “Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995: Statements in this Presentation relating to plans, strategies, economic performance and trends, projections of results of specific activities or investments and other statements that are not descriptions of historical facts may be forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking information is inherently subject to risks and uncertainties, and actual results could differ materially from those currently anticipated due to a number of factors, which include, but are not limited to, risk factors discussed in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2019 and in other documents filed by the Company with the Securities and Exchange Commission from time to time, as well as the possibility that the proposed expected benefits of the Empire merger may not materialize in the timeframe expected or at all, or may be more costly to achieve. These proposed risks, as well as other risks associated with the transaction, are more fully discussed in the proxy statement/prospectus that is included in the registration statement on Form S-4 filed with the SEC in connection with the transaction, as amended and supplemented from time to time. Forward-looking statements may be identified by terms such as “may”, “will”, “should”, “could”, “expects”, “plans”, “intends”, “anticipates”, “believes”, “estimates”, “predicts”, “forecasts”, “goals”, “potential” or “continue” or similar terms or the negative of these terms. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. The Company has no obligation to update these forward-looking statements. |

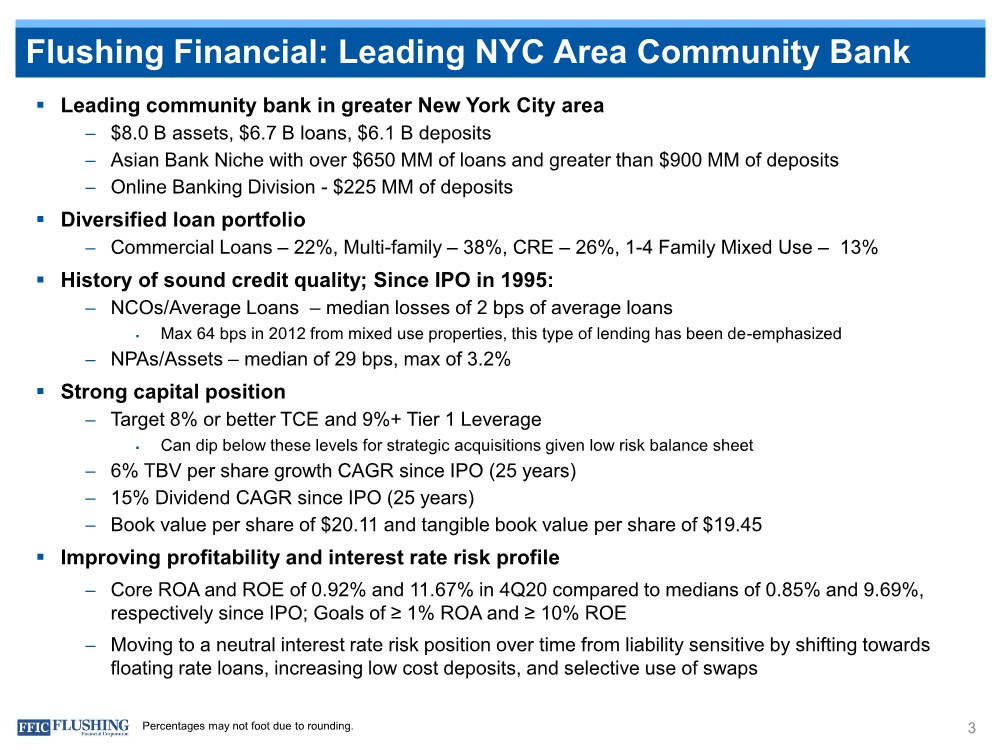

| Flushing Financial: Leading NYC Area Community Bank 3 . Leading community bank in greater New York City area – $8.0 B assets, $6.7 B loans, $6.1 B deposits – Asian Bank Niche with over $650 MM of loans and greater than $900 MM of deposits – Online Banking Division - $225 MM of deposits . Diversified loan portfolio – Commercial Loans – 22%, Multi-family – 38%, CRE – 26%, 1-4 Family Mixed Use – 13% . History of sound credit quality; Since IPO in 1995: – NCOs/Average Loans – median losses of 2 bps of average loans . Max 64 bps in 2012 from mixed use properties, this type of lending has been de-emphasized – NPAs/Assets – median of 29 bps, max of 3.2% . Strong capital position – Target 8% or better TCE and 9%+ Tier 1 Leverage . Can dip below these levels for strategic acquisitions given low risk balance sheet – 6% TBV per share growth CAGR since IPO (25 years) – 15% Dividend CAGR since IPO (25 years) – Book value per share of $20.11 and tangible book value per share of $19.45 . Improving profitability and interest rate risk profile – Core ROA and ROE of 0.92% and 11.67% in 4Q20 compared to medians of 0.85% and 9.69%, respectively since IPO; Goals of ≥ 1% ROA and ≥ 10% ROE – Moving to a neutral interest rate risk position over time from liability sensitive by shifting towards floating rate loans, increasing low cost deposits, and selective use of swaps Percentages may not foot due to rounding. |

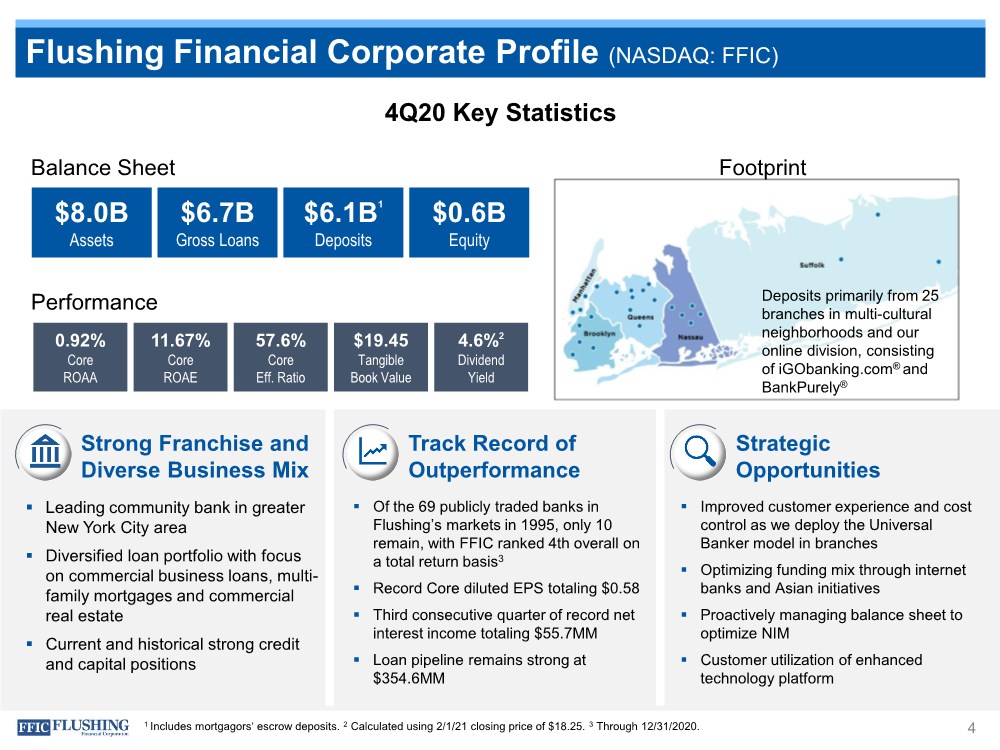

| Flushing Financial Corporate Profile (NASDAQ: FFIC) 4 4Q20 Key Statistics Strong Franchise and Diverse Business Mix . Leading community bank in greater New York City area . Diversified loan portfolio with focus on commercial business loans, multi- family mortgages and commercial real estate . Current and historical strong credit and capital positions Track Record of Outperformance . Of the 69 publicly traded banks in Flushing’s markets in 1995, only 10 remain, with FFIC ranked 4th overall on a total return basis3 . Record Core diluted EPS totaling $0.58 . Third consecutive quarter of record net interest income totaling $55.7MM . Loan pipeline remains strong at $354.6MM Strategic Opportunities . Improved customer experience and cost control as we deploy the Universal Banker model in branches . Optimizing funding mix through internet banks and Asian initiatives . Proactively managing balance sheet to optimize NIM . Customer utilization of enhanced technology platform Deposits primarily from 25 branches in multi-cultural neighborhoods and our online division, consisting of iGObanking.com® and BankPurely® Footprint Balance Sheet $8.0B Assets $6.7B Gross Loans $6.1B1 Deposits $0.6B Equity Performance 0.92% Core ROAA 11.67% Core ROAE 57.6% Core Eff. Ratio $19.45 Tangible Book Value 4.6%2 Dividend Yield 1 Includes mortgagors‘ escrow deposits. 2 Calculated using 2/1/21 closing price of $18.25. 3 Through 12/31/2020. |

| Strong Asian Banking Market Focus . Asian Bank within Flushing Bank . Loans in the Asian communities total over $650MM with deposits exceeding $900MM . Multilingual branch staff serves our diverse customer base in New York City market area . Growth aided by the Asian Advisory Board . Sponsorships of cultural activities support new and existing opportunities 5 |

| Experienced Executive Leadership Team 6 John Buran President and CEO FFIC: 19 years Industry: 43 years Maria Grasso SEVP, COO, Corporate Secretary FFIC: 14 years Industry: 34 years Susan Cullen SEVP, CFO, Treasurer FFIC: 5 years Industry: 29 years Francis Korzekwinski SEVP, Chief of Real Estate FFIC: 27 years Industry: 31 years Michael Bingold SEVP, Chief Retail and Client Development Officer FFIC: 7 years Industry: 37 years Tom Buonaiuto SEVP, Chief of Staff, Deposit Channel Executive FFIC: 12 years1 Industry: 29 years Allen Brewer SEVP, Chief Information Officer FFIC: 12 years Industry: 47 years Vincent Giovinco EVP, Commercial Real Estate Lending FFIC: 1 year Industry: 23 years Jeoung Jin EVP, Residential and Banking FFIC: 22 years Industry: 24 years Theresa Kelly EVP, Business Banking FFIC: 14 years Industry: 36 years Patricia Mezeul EVP, Director of Government Banking FFIC: 12 years Industry: 40 years 1 Previously President and COO of Empire Bancorp and Empire National Bank from its inception in February 2008 until the sale to Flushing in October 2020. |

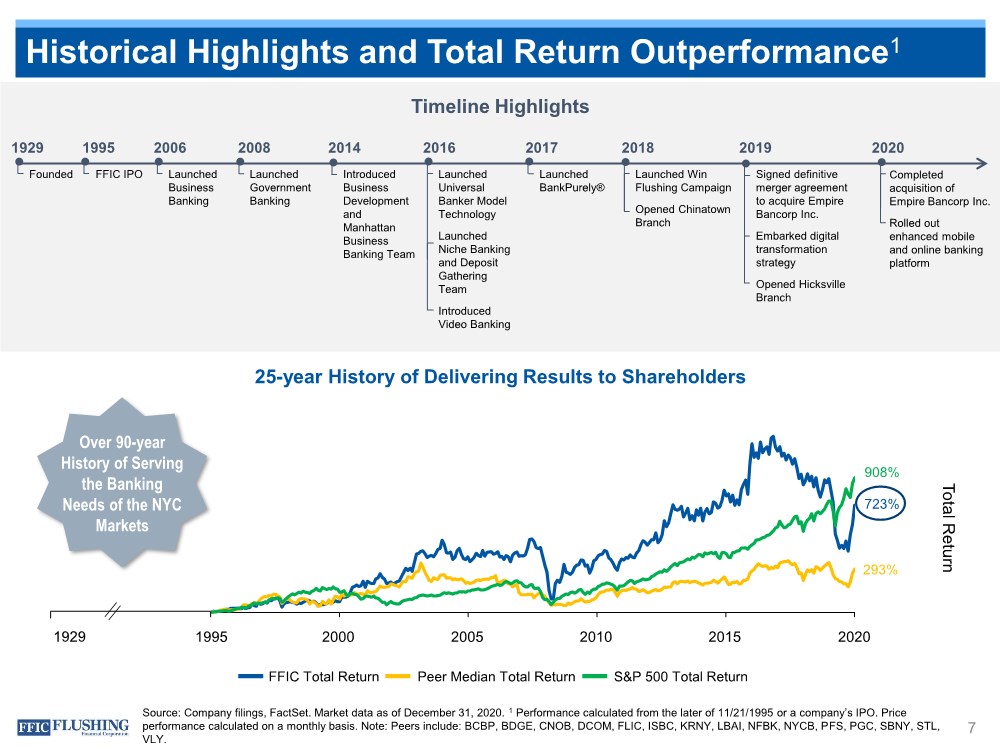

| Historical Highlights and Total Return Outperformance1 7 Timeline Highlights 1929 2018 2017 2014 2016 2008 2006 1995 2019 Source: Company filings, FactSet. Market data as of December 31, 2020. 1 Performance calculated from the later of 11/21/1995 or a company’s IPO. Price performance calculated on a monthly basis. Note: Peers include: BCBP, BDGE, CNOB, DCOM, FLIC, ISBC, KRNY, LBAI, NFBK, NYCB, PFS, PGC, SBNY, STL, VLY. 2020 Signed definitive merger agreement to acquire Empire Bancorp Inc. Embarked digital transformation strategy Opened Hicksville Branch Introduced Business Development and Manhattan Business Banking Team FFIC IPO Founded Launched Win Flushing Campaign Opened Chinatown Branch Launched Universal Banker Model Technology Launched Niche Banking and Deposit Gathering Team Introduced Video Banking Launched Business Banking Launched Government Banking Launched BankPurely® 25-year History of Delivering Results to Shareholders Over 90-year History of Serving the Banking Needs of the NYC Markets FFIC Total Return Peer Median Total Return S&P 500 Total Return Total Return 1929 723% 293% 908% 1995 2000 2005 2010 2015 2020 1995 2000 2005 2010 2015 Completed acquisition of Empire Bancorp Inc. Rolled out enhanced mobile and online banking platform 2020 |

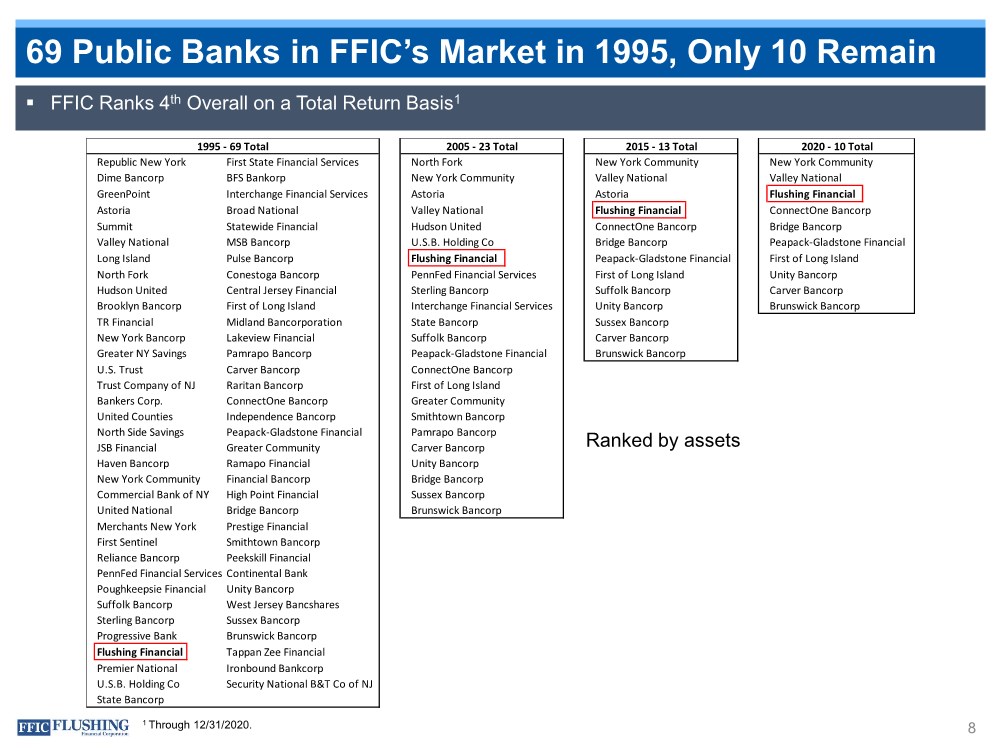

| Republic New York First State Financial Services North Fork New York Community New York Community Dime Bancorp BFS Bankorp New York Community Valley National Valley National GreenPoint Interchange Financial Services Astoria Astoria Flushing Financial Astoria Broad National Valley National Flushing Financial ConnectOne Bancorp Summit Statewide Financial Hudson United ConnectOne Bancorp Bridge Bancorp Valley National MSB Bancorp U.S.B. Holding Co Bridge Bancorp Peapack-Gladstone Financial Long Island Pulse Bancorp Flushing Financial Peapack-Gladstone Financial First of Long Island North Fork Conestoga Bancorp PennFed Financial Services First of Long Island Unity Bancorp Hudson United Central Jersey Financial Sterling Bancorp Suffolk Bancorp Carver Bancorp Brooklyn Bancorp First of Long Island Interchange Financial Services Unity Bancorp Brunswick Bancorp TR Financial Midland Bancorporation State Bancorp Sussex Bancorp New York Bancorp Lakeview Financial Suffolk Bancorp Carver Bancorp Greater NY Savings Pamrapo Bancorp Peapack-Gladstone Financial Brunswick Bancorp U.S. Trust Carver Bancorp ConnectOne Bancorp Trust Company of NJ Raritan Bancorp First of Long Island Bankers Corp. ConnectOne Bancorp Greater Community United Counties Independence Bancorp Smithtown Bancorp North Side Savings Peapack-Gladstone Financial Pamrapo Bancorp JSB Financial Greater Community Carver Bancorp Haven Bancorp Ramapo Financial Unity Bancorp New York Community Financial Bancorp Bridge Bancorp Commercial Bank of NY High Point Financial Sussex Bancorp United National Bridge Bancorp Brunswick Bancorp Merchants New York Prestige Financial First Sentinel Smithtown Bancorp Reliance Bancorp Peekskill Financial PennFed Financial Services Continental Bank Poughkeepsie Financial Unity Bancorp Suffolk Bancorp West Jersey Bancshares Sterling Bancorp Sussex Bancorp Progressive Bank Brunswick Bancorp Flushing Financial Tappan Zee Financial Premier National Ironbound Bankcorp U.S.B. Holding Co Security National B&T Co of NJ State Bancorp 1995 - 69 Total 2005 - 23 Total 2015 - 13 Total 2020 - 10 Total 69 Public Banks in FFIC’s Market in 1995, Only 10 Remain 8 . FFIC Ranks 4th Overall on a Total Return Basis1 1 Through 12/31/2020. Ranked by assets |

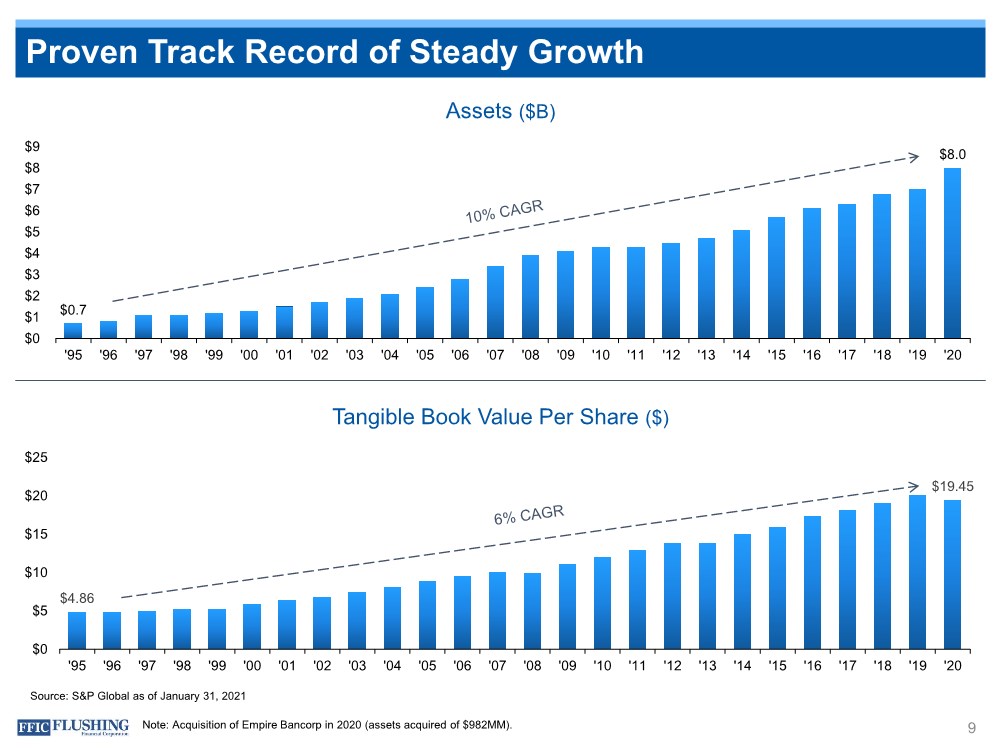

| $4.86 $19.45 $0 $5 $10 $15 $20 $25 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 $0.7 $8.0 $0 $1 $2 $3 $4 $5 $6 $7 $8 $9 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 Proven Track Record of Steady Growth 9 Assets ($B) Tangible Book Value Per Share ($) Note: Acquisition of Empire Bancorp in 2020 (assets acquired of $982MM). Source: S&P Global as of January 31, 2021 |

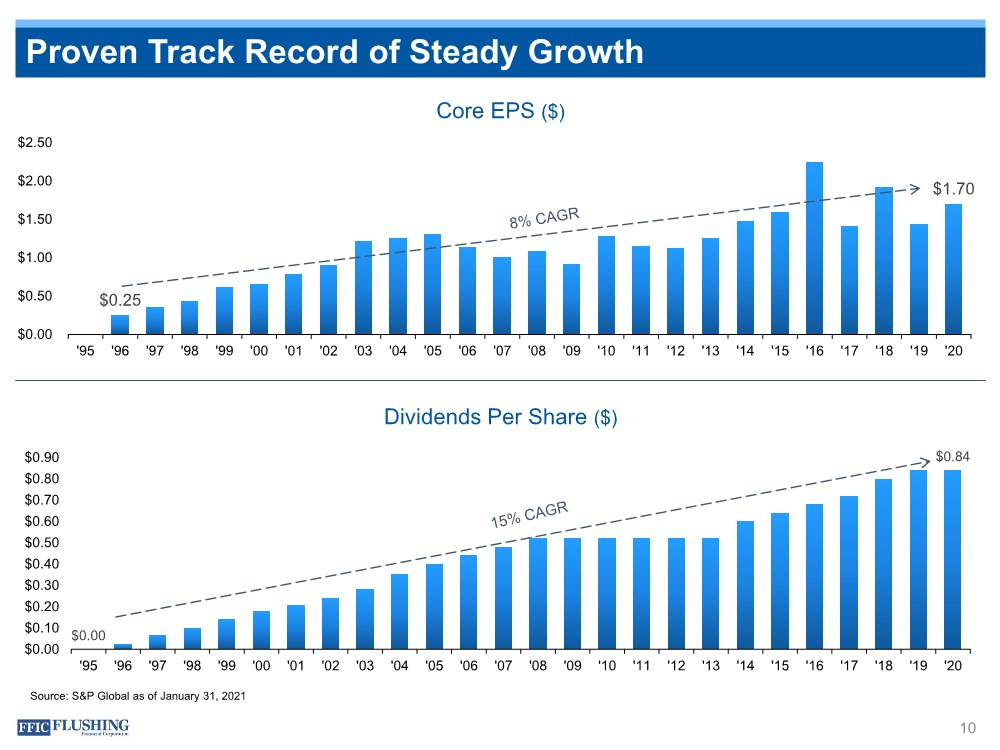

| $0.00 $0.84 $0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 $0.80 $0.90 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 $0.25 $1.70 $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 Proven Track Record of Steady Growth 10 Core EPS ($) Dividends Per Share ($) Source: S&P Global as of January 31, 2021 |

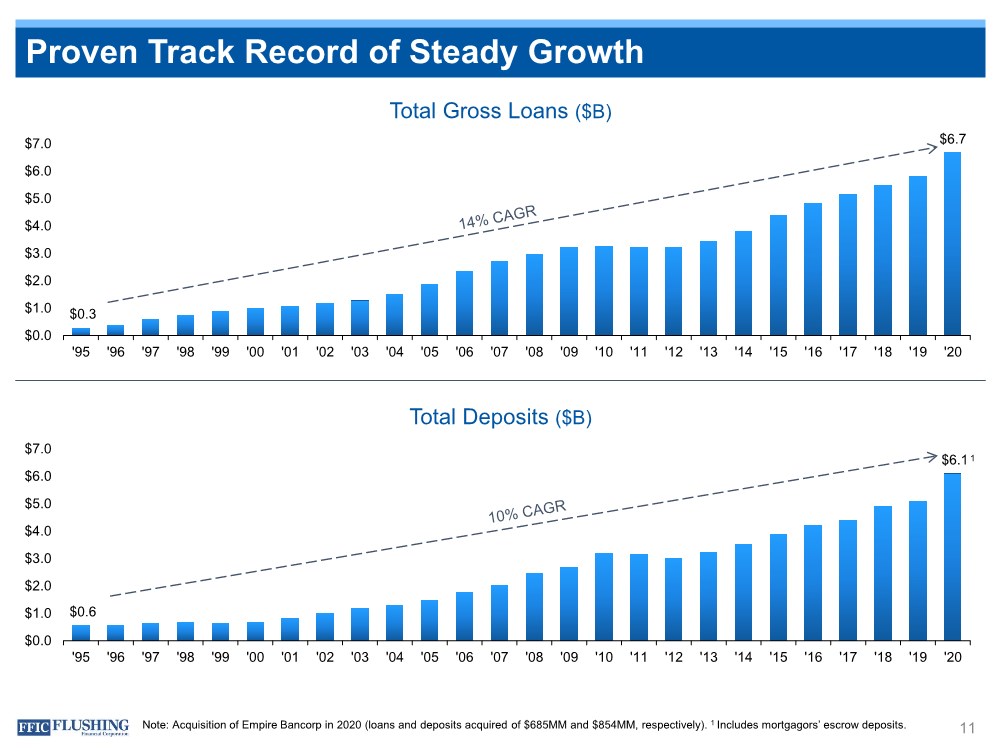

| $0.6 $6.1 $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 $7.0 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 $0.3 $6.7 $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 $7.0 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 Proven Track Record of Steady Growth 11 Total Gross Loans ($B) Total Deposits ($B) Note: Acquisition of Empire Bancorp in 2020 (loans and deposits acquired of $685MM and $854MM, respectively). 1 Includes mortgagors’ escrow deposits. 1 |

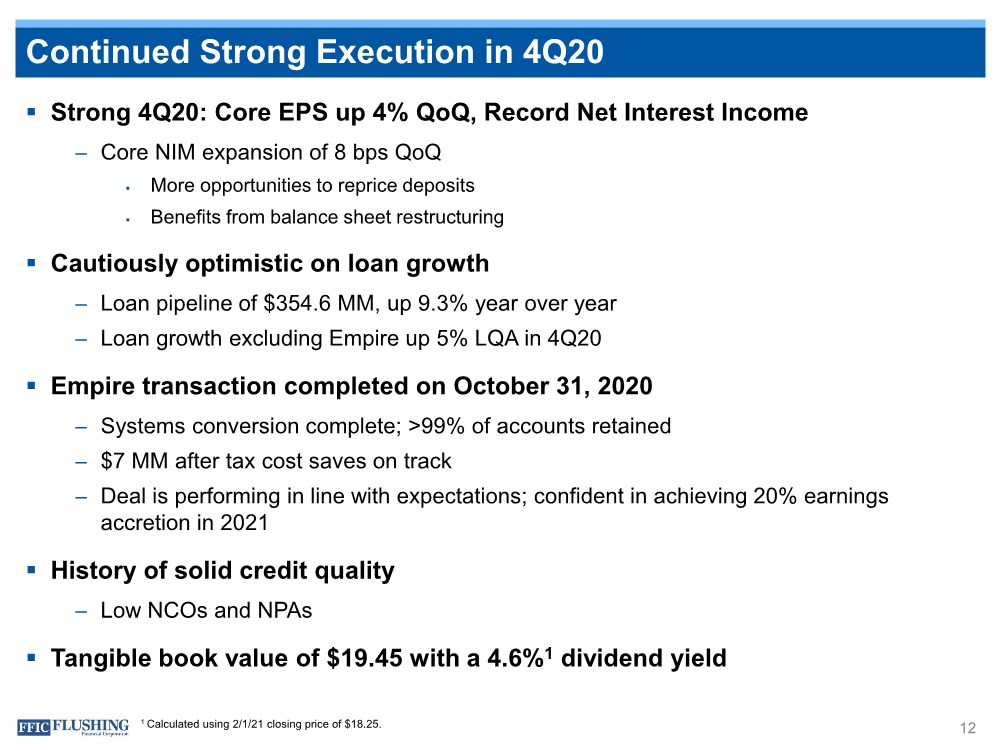

| Continued Strong Execution in 4Q20 12 . Strong 4Q20: Core EPS up 4% QoQ, Record Net Interest Income – Core NIM expansion of 8 bps QoQ . More opportunities to reprice deposits . Benefits from balance sheet restructuring . Cautiously optimistic on loan growth – Loan pipeline of $354.6 MM, up 9.3% year over year – Loan growth excluding Empire up 5% LQA in 4Q20 . Empire transaction completed on October 31, 2020 – Systems conversion complete; >99% of accounts retained – $7 MM after tax cost saves on track – Deal is performing in line with expectations; confident in achieving 20% earnings accretion in 2021 . History of solid credit quality – Low NCOs and NPAs . Tangible book value of $19.45 with a 4.6%1 dividend yield 1 Calculated using 2/1/21 closing price of $18.25. |

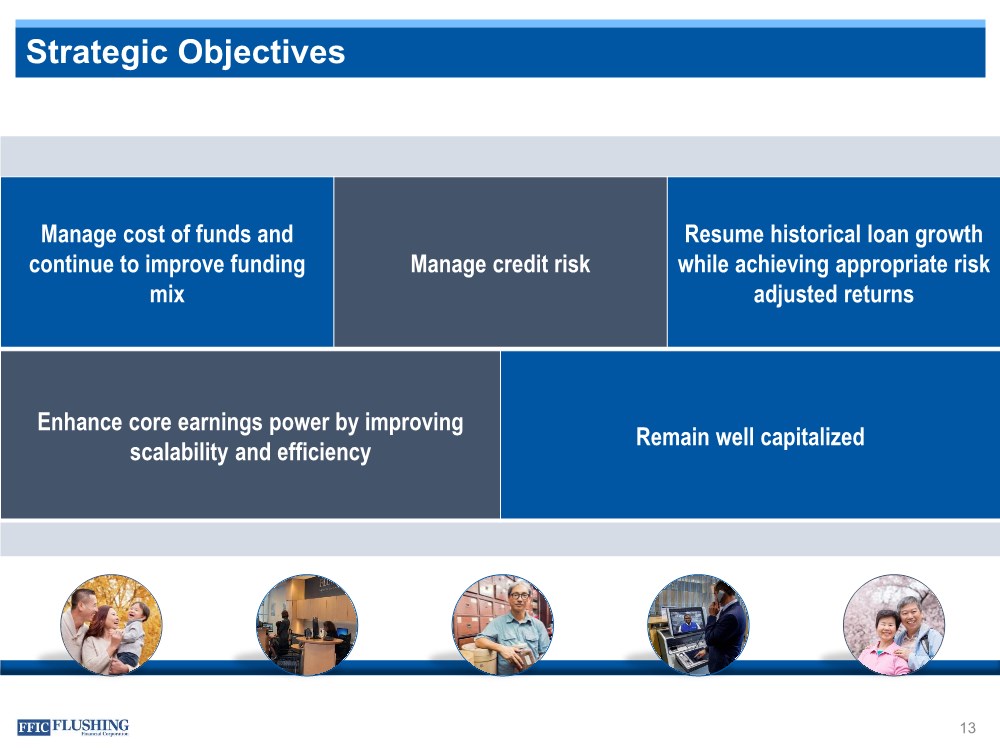

| Strategic Objectives 13 Manage cost of funds and continue to improve funding mix Manage credit risk Resume historical loan growth while achieving appropriate risk adjusted returns Enhance core earnings power by improving scalability and efficiency Remain well capitalized |

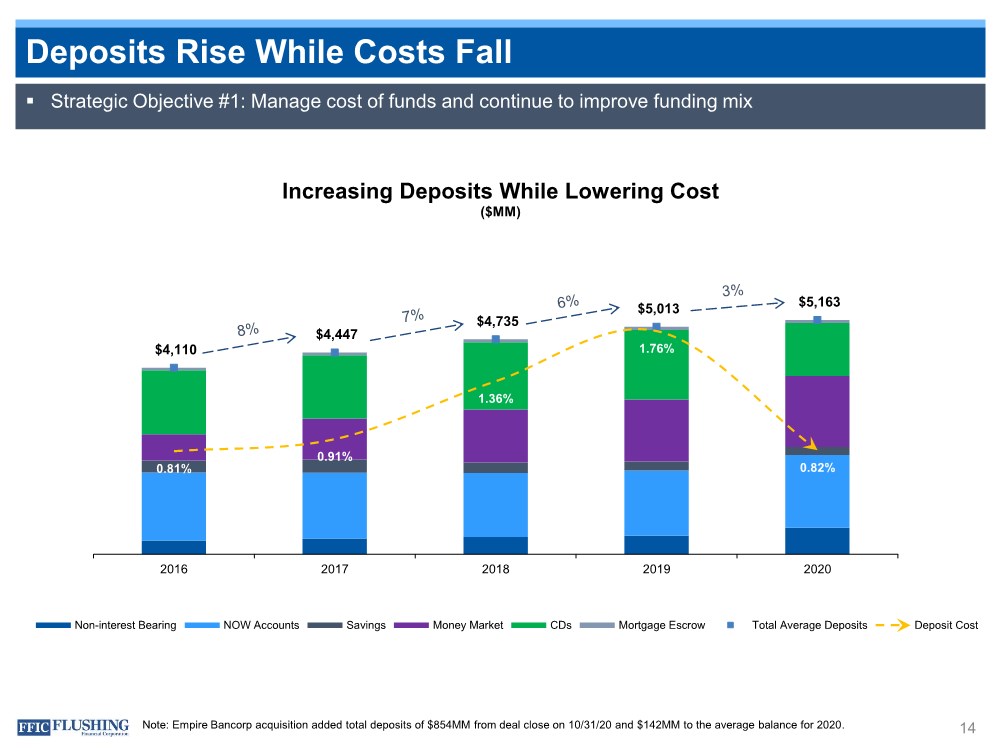

| Deposits Rise While Costs Fall 14 $4,110 $4,447 $4,735 $5,013 $5,163 0.81% 0.91% 1.36% 1.76% 0.82% 2016 2017 2018 2019 2020 Increasing Deposits While Lowering Cost ($MM) Non-interest Bearing NOW Accounts Savings Money Market CDs Mortgage Escrow Total Average Deposits Deposit Cost . Strategic Objective #1: Manage cost of funds and continue to improve funding mix Note: Empire Bancorp acquisition added total deposits of $854MM from deal close on 10/31/20 and $142MM to the average balance for 2020. |

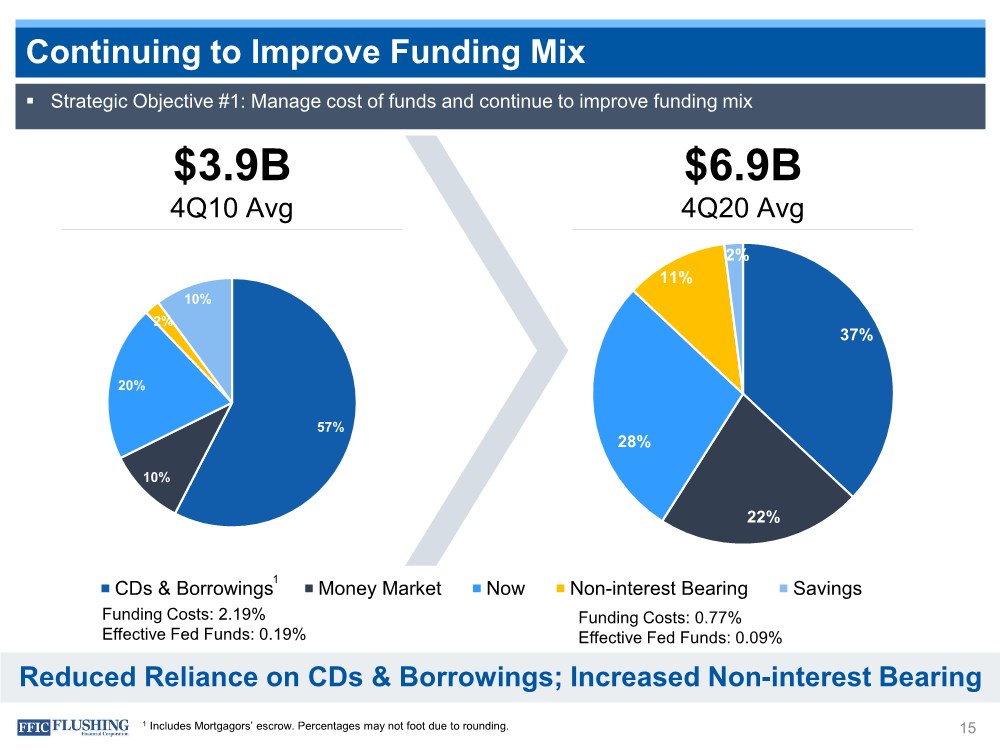

| Continuing to Improve Funding Mix 15 Reduced Reliance on CDs & Borrowings; Increased Non-interest Bearing 57% 10% 20% 2% 10% 37% 22% 28% 11% 2% $3.9B 4Q10 Avg $6.9B 4Q20 Avg CDs & Borrowings Money Market Now Non-interest Bearing Savings 1 1 Includes Mortgagors’ escrow. Percentages may not foot due to rounding. Funding Costs: 2.19% Effective Fed Funds: 0.19% Funding Costs: 0.77% Effective Fed Funds: 0.09% . Strategic Objective #1: Manage cost of funds and continue to improve funding mix |

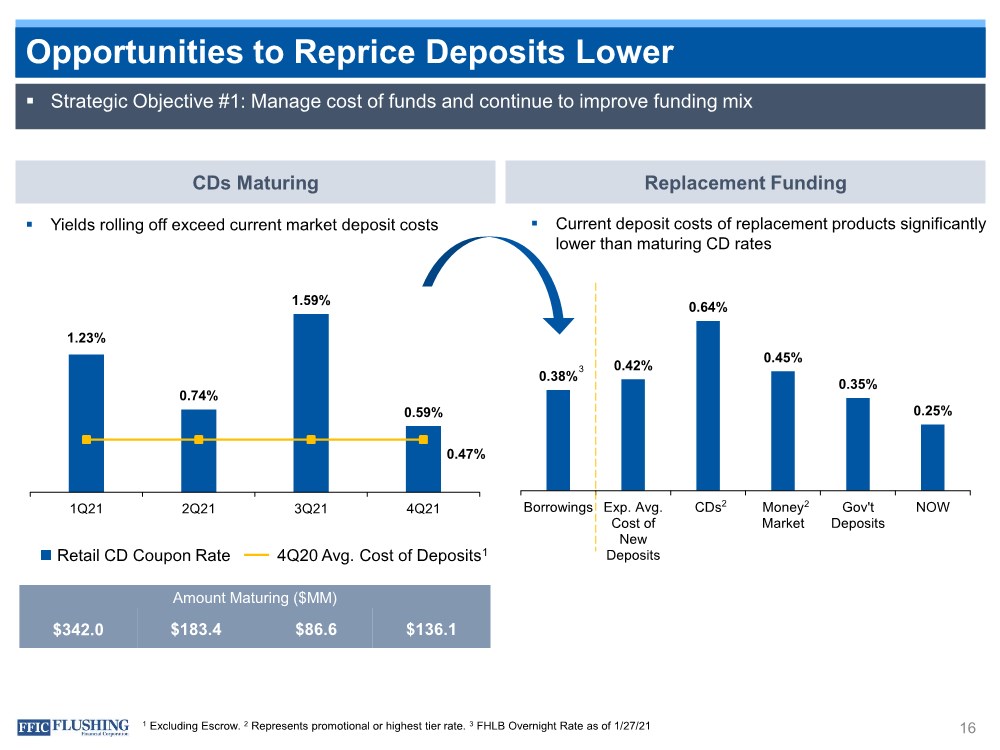

| 16 CDs Maturing Replacement Funding . Current deposit costs of replacement products significantly lower than maturing CD rates . Yields rolling off exceed current market deposit costs 1.23% 0.74% 1.59% 0.59% 0.47% 1Q21 2Q21 3Q21 4Q21 0.38% 0.42% 0.64% 0.45% 0.35% 0.25% Borrowings Exp. Avg. Cost of New Deposits CDs Money Market Gov't Deposits NOW Retail CD Coupon Rate 4Q20 Avg. Cost of Deposits1 Amount Maturing ($MM) $342.0 $183.4 $86.6 $136.1 3 2 2 1 Excluding Escrow. 2 Represents promotional or highest tier rate. 3 FHLB Overnight Rate as of 1/27/21 Strategic Objective #1: Manage cost of funds and continue to improve funding mix Opportunities to Reprice Deposits Lower . Strategic Objective #1: Manage cost of funds and continue to improve funding mix |

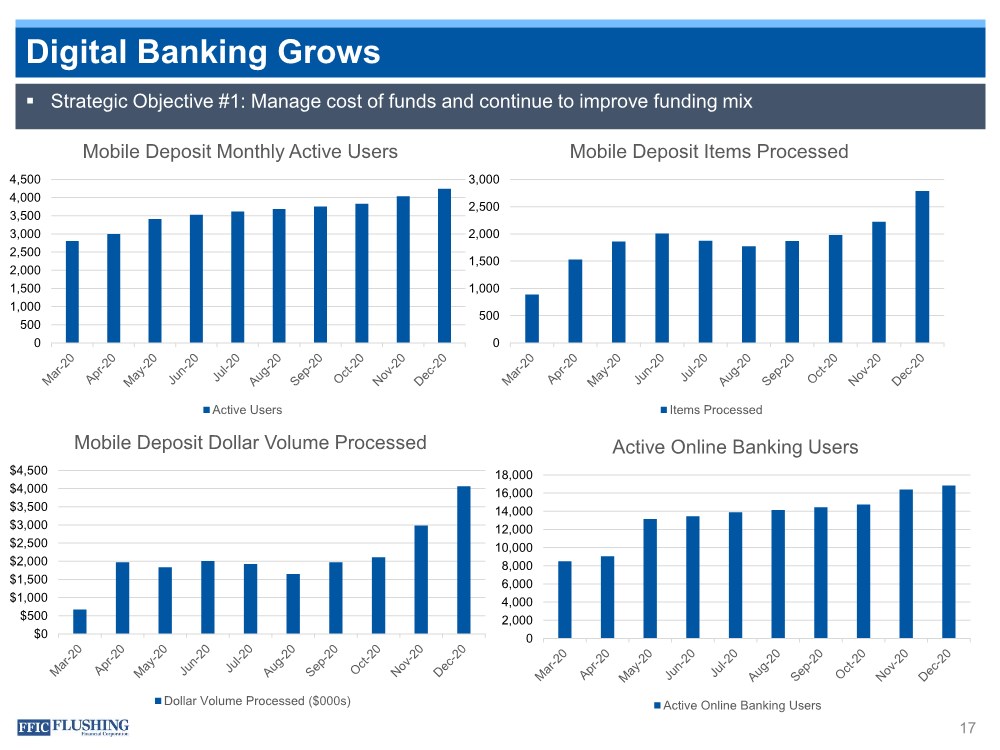

| Digital Banking Grows 17 . Strategic Objective #1: Manage cost of funds and continue to improve funding mix 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 Mobile Deposit Monthly Active Users Active Users 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 Active Online Banking Users Active Online Banking Users 0 500 1,000 1,500 2,000 2,500 3,000 Mobile Deposit Items Processed Items Processed $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 $4,500 Mobile Deposit Dollar Volume Processed Dollar Volume Processed ($000s) |

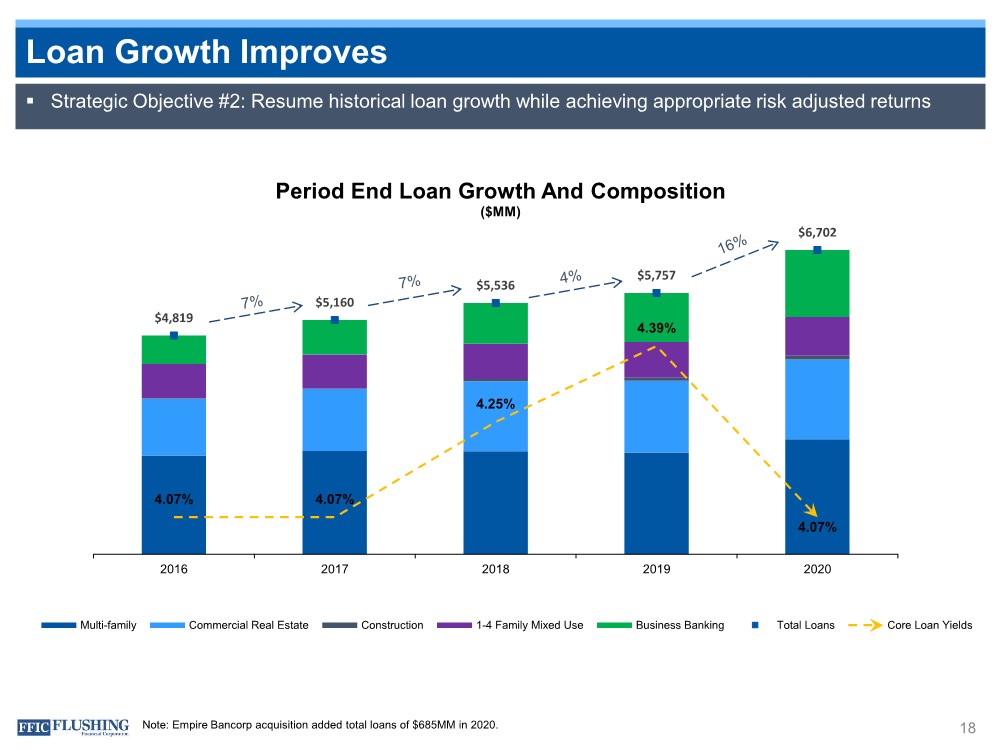

| $4,819 $5,160 $5,536 $5,757 $6,702 4.07% 4.07% 4.25% 4.39% 4.07% 2016 2017 2018 2019 2020 Period End Loan Growth And Composition ($MM) Multi-family Commercial Real Estate Construction 1-4 Family Mixed Use Business Banking Total Loans Core Loan Yields 18 Loan Growth Improves . Strategic Objective #2: Resume historical loan growth while achieving appropriate risk adjusted returns Note: Empire Bancorp acquisition added total loans of $685MM in 2020. |

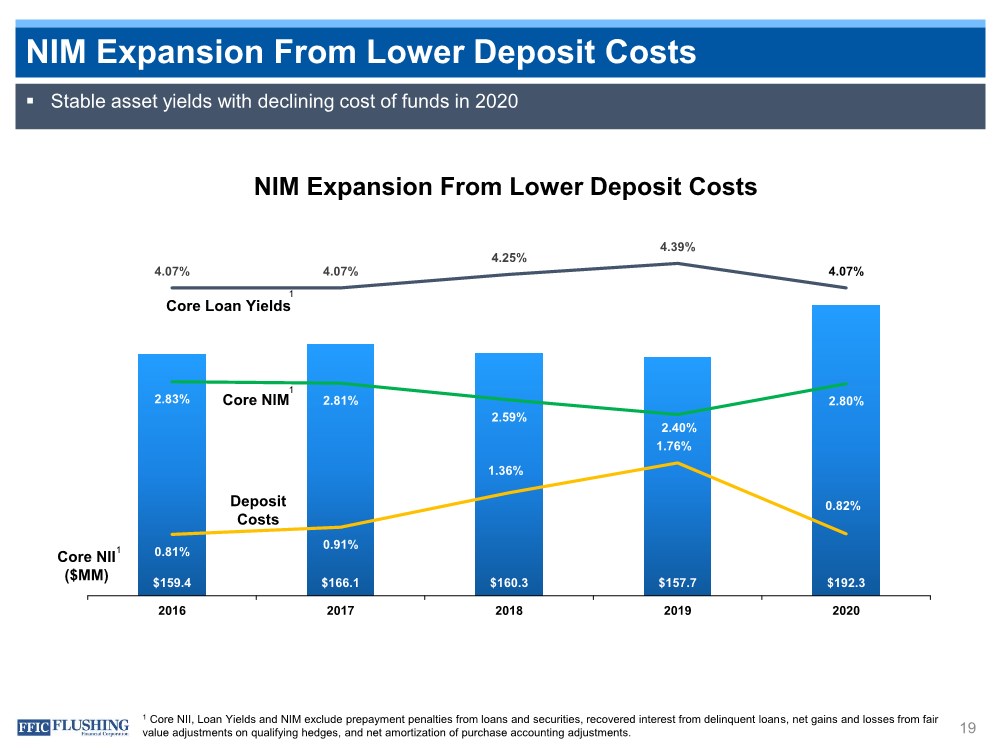

| NIM Expansion From Lower Deposit Costs 19 1 Core NII, Loan Yields and NIM exclude prepayment penalties from loans and securities, recovered interest from delinquent loans, net gains and losses from fair value adjustments on qualifying hedges, and net amortization of purchase accounting adjustments. $159.4 $166.1 $160.3 $157.7 $192.3 2.83% 2.81% 2.59% 2.40% 2.80% 4.07% 4.07% 4.25% 4.39% 4.07% 0.81% 0.91% 1.36% 1.76% 0.82% 2016 2017 2018 2019 2020 NIM Expansion From Lower Deposit Costs Core NIM Deposit Costs Core Loan Yields . Stable asset yields with declining cost of funds in 2020 Core NII ($MM) 1 1 1 |

| 20% Earnings Accretion in 2021 From Empire Expected 20 . Strategic Objective #3: Enhance core earnings power by improving scalability and efficiency . Closed the Empire transaction on October 31, 2020 – This added $982MM of assets, $685MM of loans and $854MM of deposits – Recorded goodwill of $1.5MM, CDI of $3.3MM and approximately 2.0% loan portfolio purchase accounting mark – Systems conversion completed in November – Targeted costs savings are $7MM after-tax, most of which will start in 1Q21 – Merger costs were approximately $5.0MM – The system conversion and integration are complete . Overall, the deal is in line with expectations and we are confident in achieving 20% earnings accretion in 2021 |

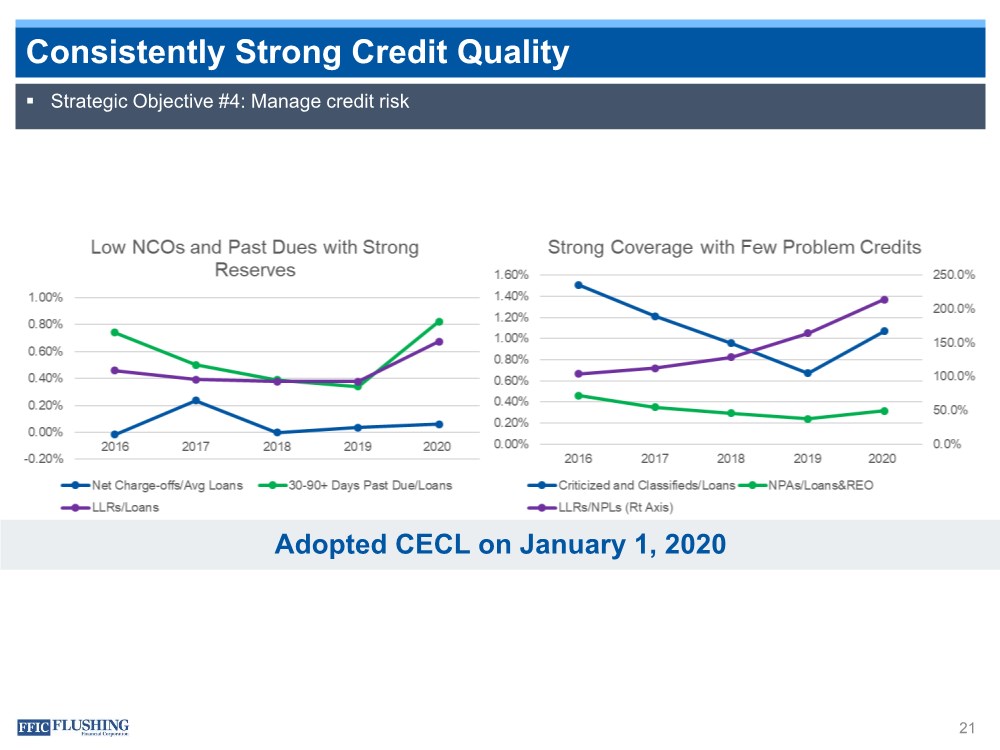

| Consistently Strong Credit Quality 21 $216.3MM . Strategic Objective #4: Manage credit risk Adopted CECL on January 1, 2020 |

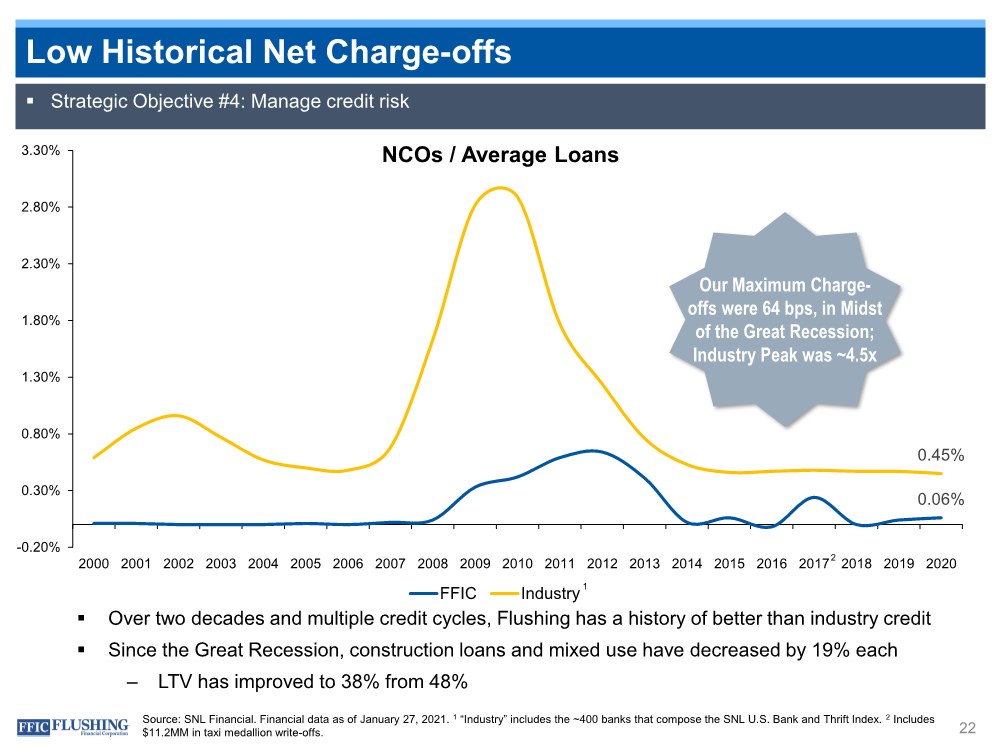

| 0.06% 0.45% -0.20% 0.30% 0.80% 1.30% 1.80% 2.30% 2.80% 3.30% 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 FFIC Industry Low Historical Net Charge-offs NCOs / Average Loans Our Maximum Charge- offs were 64 bps, in Midst of the Great Recession; Industry Peak was ~4.5x 1 Source: SNL Financial. Financial data as of January 27, 2021. 1 “Industry” includes the ~400 banks that compose the SNL U.S. Bank and Thrift Index. 2 Includes $11.2MM in taxi medallion write-offs. 22 . Over two decades and multiple credit cycles, Flushing has a history of better than industry credit . Since the Great Recession, construction loans and mixed use have decreased by 19% each ‒ LTV has improved to 38% from 48% 2 . Strategic Objective #4: Manage credit risk |

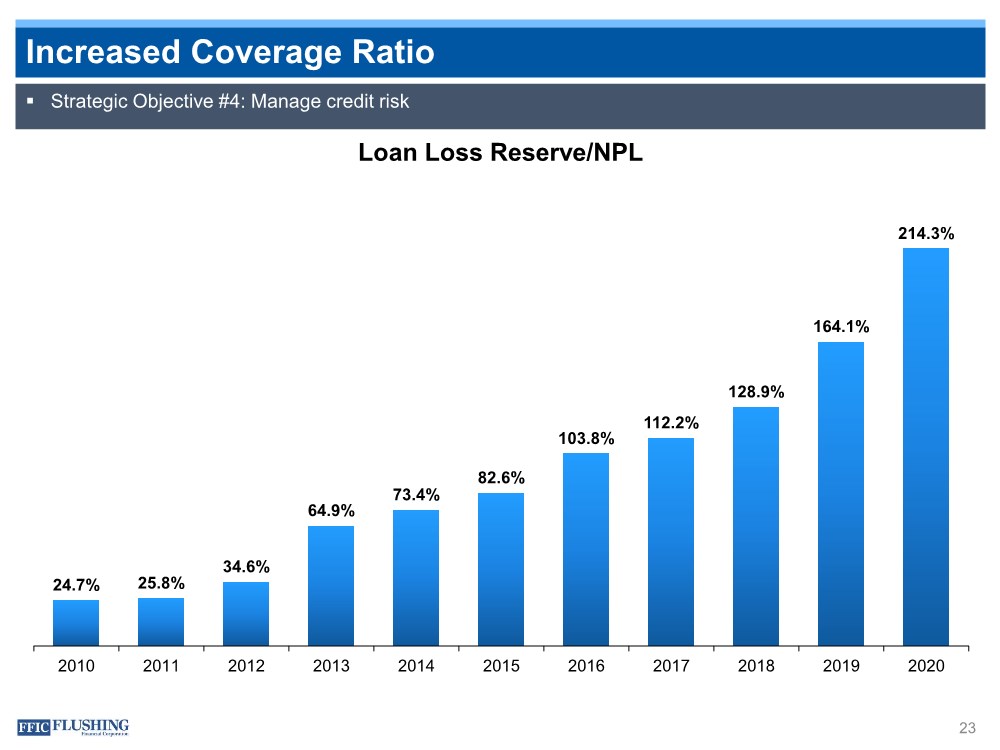

| Increased Coverage Ratio 23 24.7% 25.8% 34.6% 64.9% 73.4% 82.6% 103.8% 112.2% 128.9% 164.1% 214.3% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Loan Loss Reserve/NPL . Strategic Objective #4: Manage credit risk |

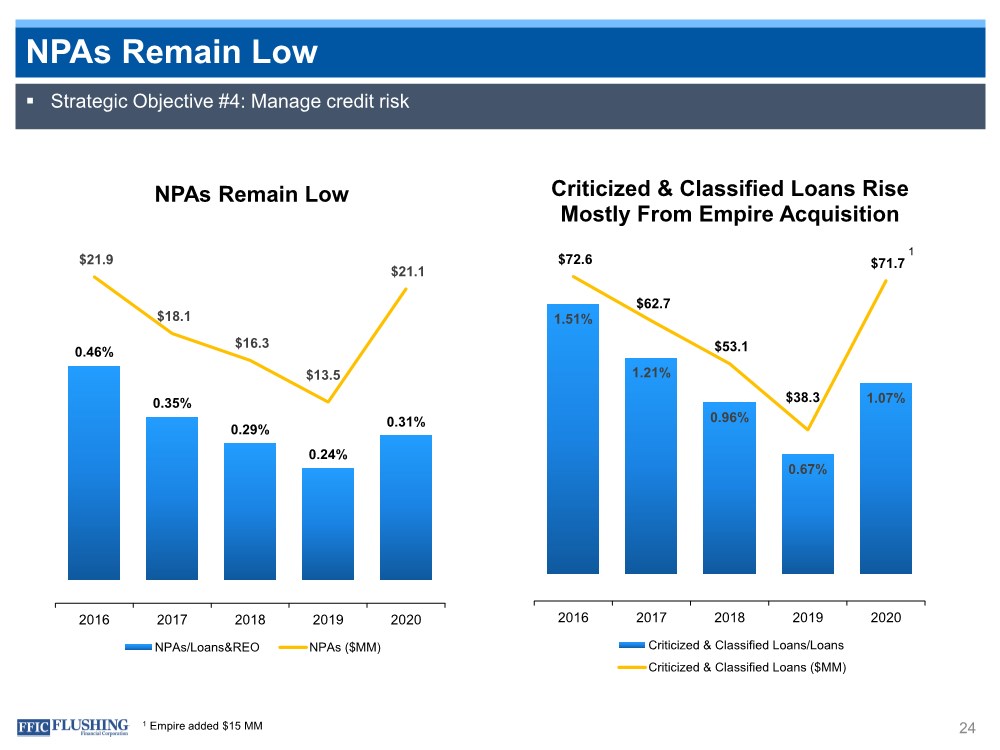

| NPAs Remain Low 24 0.46% 0.35% 0.29% 0.24% 0.31% $21.9 $18.1 $16.3 $13.5 $21.1 2016 2017 2018 2019 2020 NPAs Remain Low NPAs/Loans&REO NPAs ($MM) 1.51% 1.21% 0.96% 0.67% 1.07% $72.6 $62.7 $53.1 $38.3 $71.7 2016 2017 2018 2019 2020 Criticized & Classified Loans Rise Mostly From Empire Acquisition Criticized & Classified Loans/Loans Criticized & Classified Loans ($MM) . Strategic Objective #4: Manage credit risk 1 Empire added $15 MM 1 |

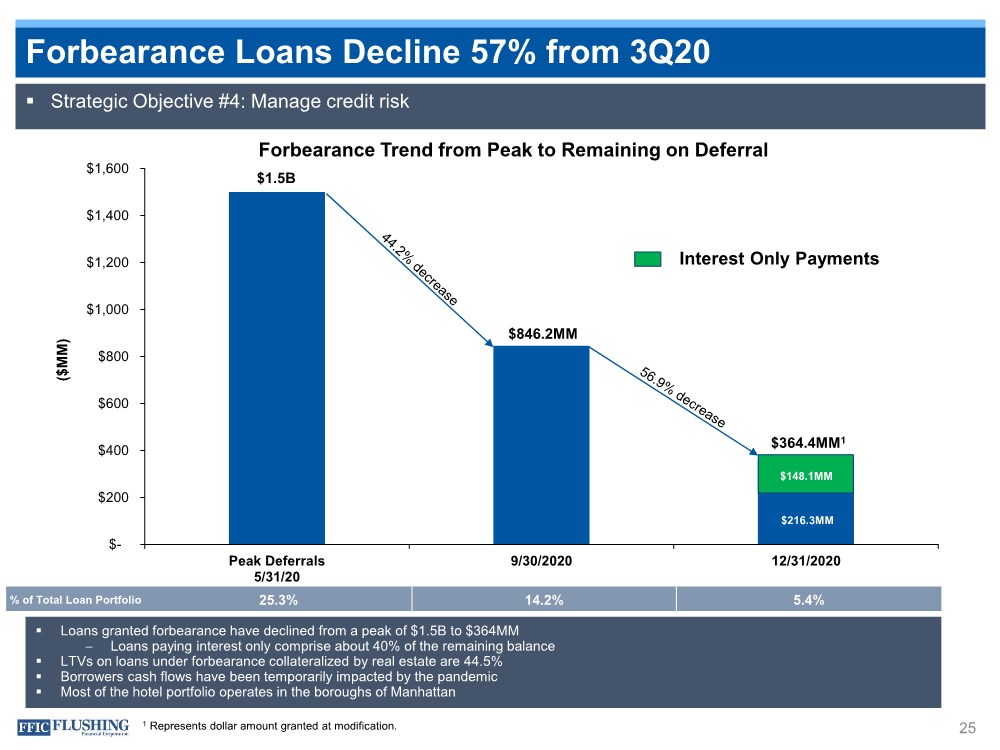

| Forbearance Loans Decline 57% from 3Q20 25 Forbearance Trend from Peak to Remaining on Deferral $- $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 Peak Deferrals 5/31/20 9/30/2020 12/31/2020 ($MM) $1.5B $846.2MM $364.4MM1 % of Total Loan Portfolio 25.3% 14.2% 5.4% $148.1MM $216.3MM Interest Only Payments . Strategic Objective #4: Manage credit risk . Loans granted forbearance have declined from a peak of $1.5B to $364MM – Loans paying interest only comprise about 40% of the remaining balance . LTVs on loans under forbearance collateralized by real estate are 44.5% . Borrowers cash flows have been temporarily impacted by the pandemic . Most of the hotel portfolio operates in the boroughs of Manhattan 1 Represents dollar amount granted at modification. |

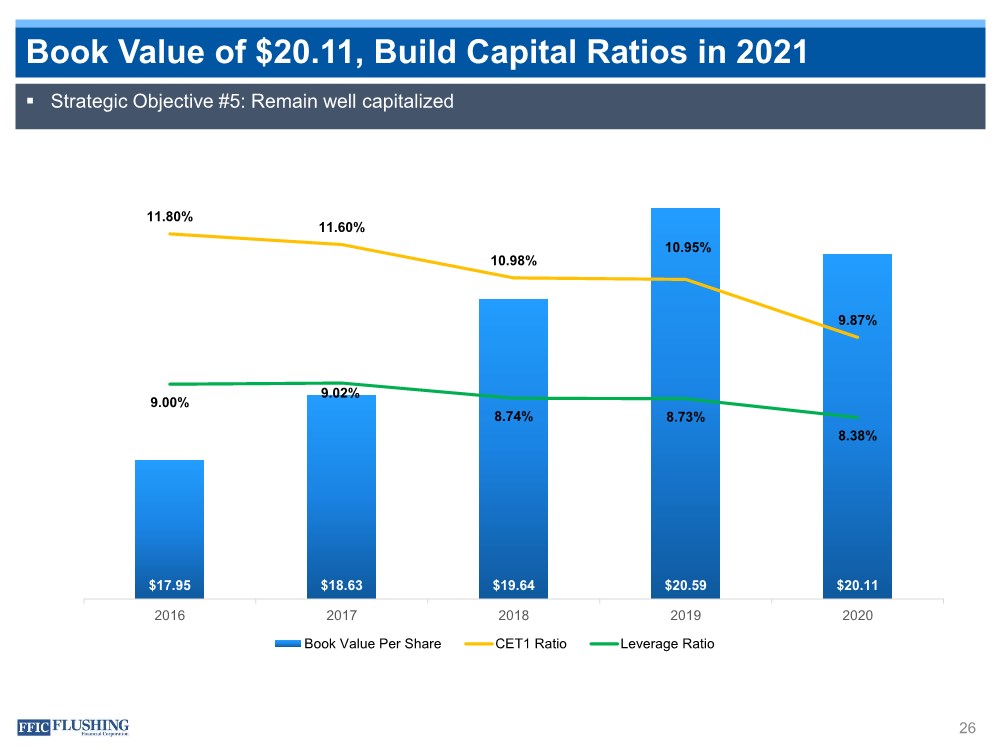

| Book Value of $20.11, Build Capital Ratios in 2021 26 $17.95 $18.63 $19.64 $20.59 $20.11 11.80% 11.60% 10.98% 10.95% 9.87% 9.00% 9.02% 8.74% 8.73% 8.38% 2016 2017 2018 2019 2020 Book Value Per Share CET1 Ratio Leverage Ratio . Strategic Objective #5: Remain well capitalized |

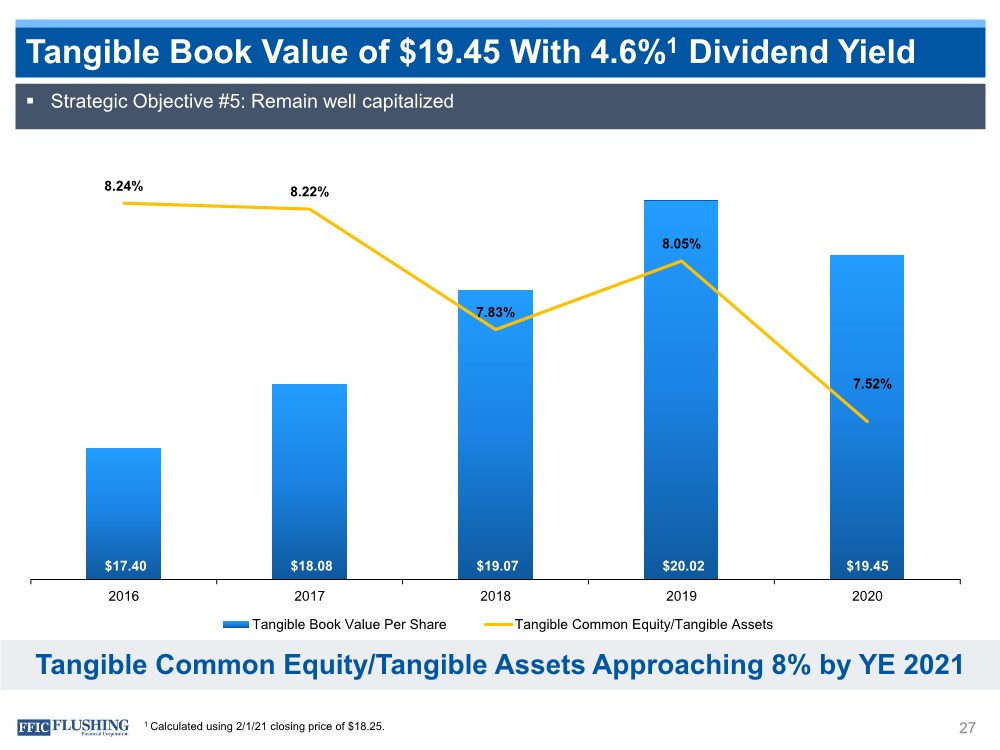

| Tangible Book Value of $19.45 With 4.6%1 Dividend Yield 27 $17.40 $18.08 $19.07 $20.02 $19.45 8.24% 8.22% 7.83% 8.05% 7.52% 2016 2017 2018 2019 2020 Tangible Book Value Per Share Tangible Common Equity/Tangible Assets . Strategic Objective #5: Remain well capitalized 1 Calculated using 2/1/21 closing price of $18.25. Tangible Common Equity/Tangible Assets Approaching 8% by YE 2021 |

| Outlook 28 . We are cautiously optimistic about the operating environment – Steeper yield curve – Fiscal stimulus and vaccine roll out should have a positive impact on the economy and borrowers . We are concerned about – Rising COVID cases near term and what that might mean for the local economy – Potential tax policy and regulatory changes . Loan pipelines are solid . Empire integration is complete and performance is in line with expectations . We remain very comfortable with our credit profile . Overall, we are on the right path to reach our LT goals of having an ROA ≥1% and ROE ≥10% |

| Appendix |

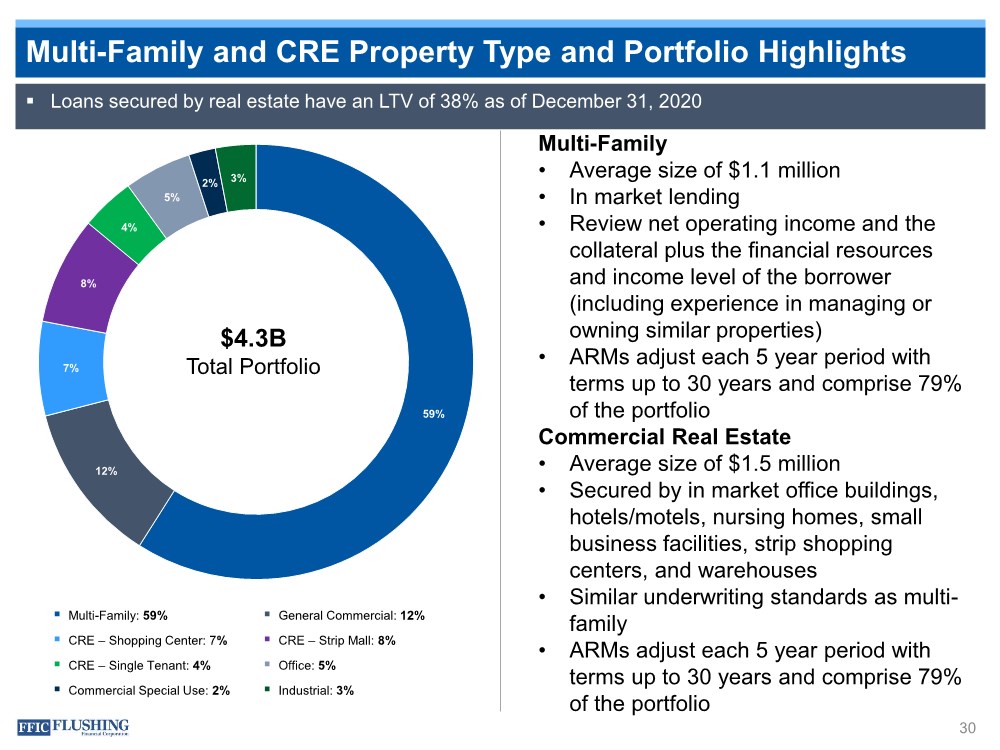

| Multi-Family and CRE Property Type and Portfolio Highlights 30 59% 12% 7% 8% 4% 5% 2% 3% $4.3B Total Portfolio . Multi-Family: 59% . General Commercial: 12% . CRE – Shopping Center: 7%. CRE – Strip Mall: 8% . CRE – Single Tenant: 4% . Office: 5% . Commercial Special Use: 2% . Industrial: 3% Multi-Family • Average size of $1.1 million • In market lending • Review net operating income and the collateral plus the financial resources and income level of the borrower (including experience in managing or owning similar properties) • ARMs adjust each 5 year period with terms up to 30 years and comprise 79% of the portfolio Commercial Real Estate • Average size of $1.5 million • Secured by in market office buildings, hotels/motels, nursing homes, small business facilities, strip shopping centers, and warehouses • Similar underwriting standards as multi- family • ARMs adjust each 5 year period with terms up to 30 years and comprise 79% of the portfolio . Loans secured by real estate have an LTV of 38% as of December 31, 2020 |

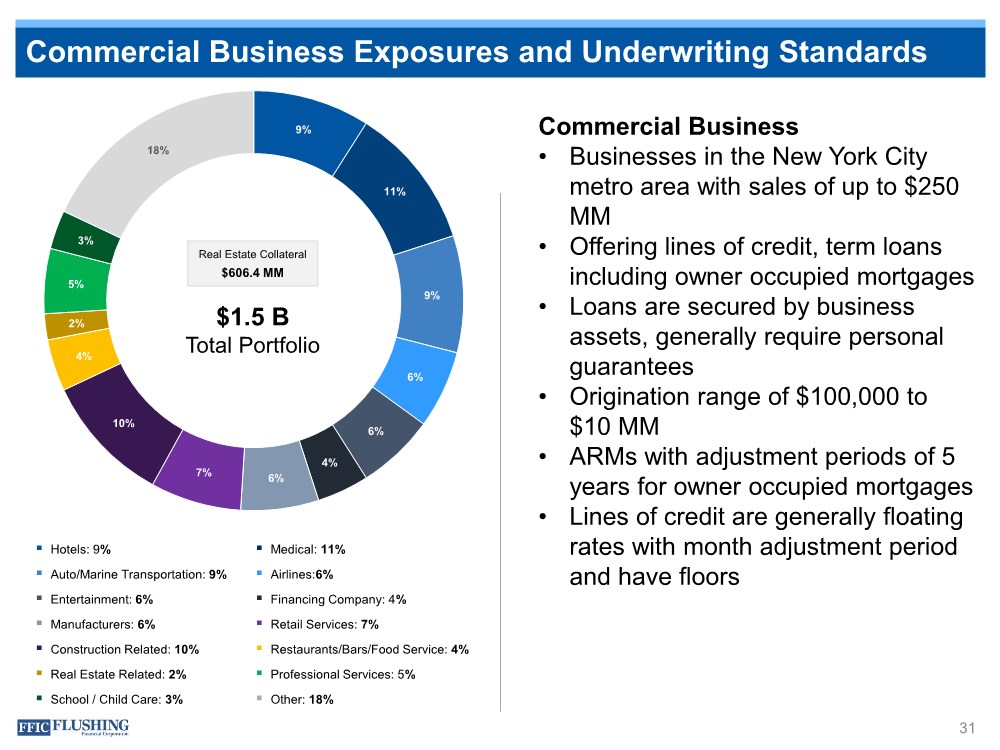

| Commercial Business Exposures and Underwriting Standards 31 9% 11% 9% 6% 6% 4% 6% 7% 10% 4% 2% 5% 3% 18% $1.5 B Total Portfolio Real Estate Collateral $606.4 MM . Hotels: 9%. Medical: 11% . Auto/Marine Transportation: 9% . Airlines:6% . Entertainment: 6% . Financing Company: 4% . Manufacturers: 6% . Retail Services: 7% . Construction Related: 10% . Restaurants/Bars/Food Service: 4% . Real Estate Related: 2% . Professional Services: 5% . School / Child Care: 3% . Other: 18% Commercial Business • Businesses in the New York City metro area with sales of up to $250 MM • Offering lines of credit, term loans including owner occupied mortgages • Loans are secured by business assets, generally require personal guarantees • Origination range of $100,000 to $10 MM • ARMs with adjustment periods of 5 years for owner occupied mortgages • Lines of credit are generally floating rates with month adjustment period and have floors |

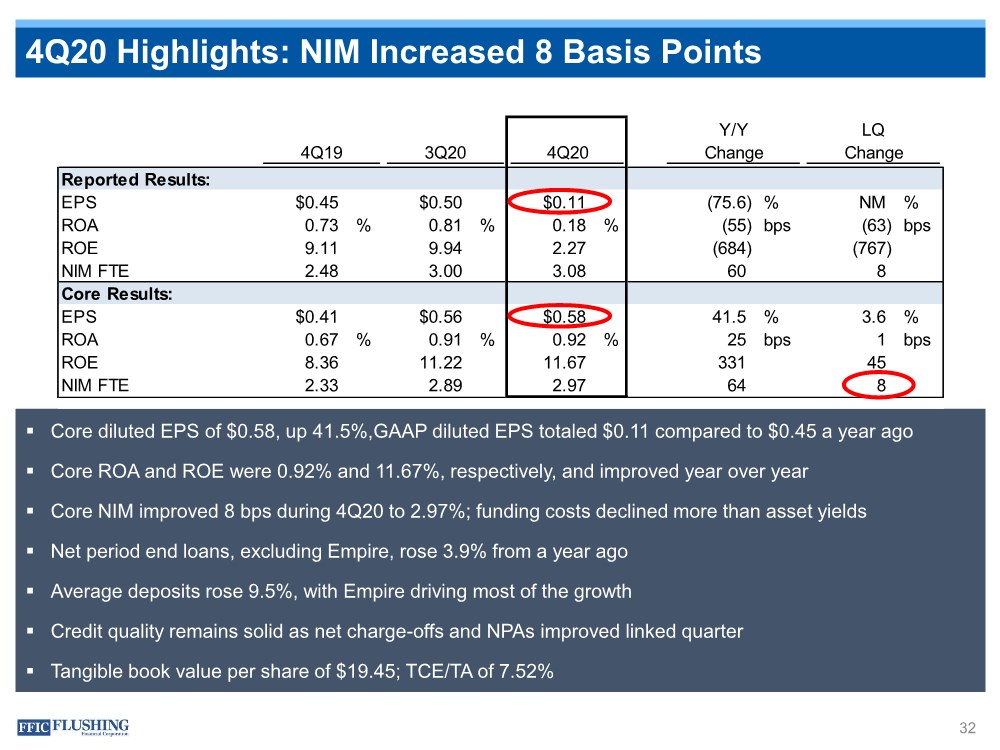

| 4Q20 Highlights: NIM Increased 8 Basis Points 32 . Core diluted EPS of $0.58, up 41.5%,GAAP diluted EPS totaled $0.11 compared to $0.45 a year ago . Core ROA and ROE were 0.92% and 11.67%, respectively, and improved year over year . Core NIM improved 8 bps during 4Q20 to 2.97%; funding costs declined more than asset yields . Net period end loans, excluding Empire, rose 3.9% from a year ago . Average deposits rose 9.5%, with Empire driving most of the growth . Credit quality remains solid as net charge-offs and NPAs improved linked quarter . Tangible book value per share of $19.45; TCE/TA of 7.52% Reported Results: EPS $0.45 $0.50 $0.11 (75.6) % NM % ROA 0.73 % 0.81 % 0.18 %(55) bps (63) bps ROE 9.11 9.94 2.27 (684) (767) NIM FTE 2.48 3.00 3.08 60 8 Core Results: EPS $0.41 $0.56 $0.58 41.5 % 3.6 % ROA 0.67 % 0.91 % 0.92 % 25 bps 1 bps ROE 8.36 11.22 11.67 331 45 NIM FTE 2.33 2.89 2.97 64 8 4Q19 3Q20 4Q20 Y/Y LQ Change Change |

| Flushing Financial Corporation and Subsidiaries Reconciliation of GAAP Earnings and Core Earnings 33 Non-cash Fair Value Adjustments to GAAP Earnings The variance in GAAP and core earnings is primarily due to the impact of non-cash net gains and losses from fair value adjustments. These fair value adjustments relate primarily to swaps designated to protect against rising rates and borrowing carried at fair value under the fair value option. As the swaps get closer to maturity, the volatility in fair value adjustments will dissipate. In a declining interest rate environment, the movement in the curve exaggerates our mark-to-market loss position. In a rising interest rate environment or a steepening of the yield curve, the loss position would experience an improvement. Core Diluted EPS, Core ROAE, Core ROAA, Core Net Interest Income, Core Yield on Total Loans, Core Net Interest Margin and tangible book value per common share are each non-GAAP measures used in this presentation.A reconciliation to the most directly comparable GAAP financial measures appears below in tabular form. The Company believes that these measures are useful for both investors and management to understand the effects of certain interest and non-interest items and provide an alternative view of the Company's performance over time and in comparison to the Company's competitors. These measures should not be viewed as a substitute for net income. The Company believes that tangible book value per common share is useful for both investors and management as these are measures commonly used by financial institutions, regulators and investors to measure the capital adequacy of financial institutions. The Company believes these measures facilitate comparison of the quality and composition of the Company's capital over time and in comparison to its competitors. These measures should not be viewed as a substitute for total shareholders' equity. These non-GAAP measures have inherent limitations, are not required to be uniformly applied and are not audited. They should not be considered in isolation or as a substitute for analysis of results reported under GAAP. These non-GAAP measures may not be comparable to similarly titled measures reported by other companies. |

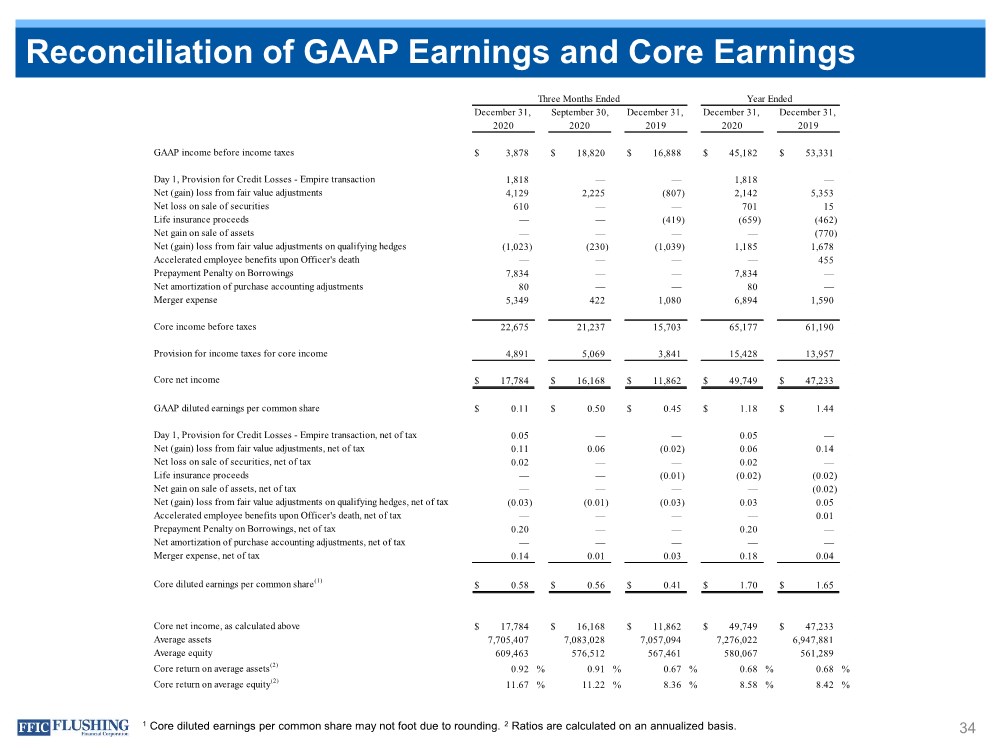

| Reconciliation of GAAP Earnings and Core Earnings 34 1 Core diluted earnings per common share may not foot due to rounding. 2 Ratios are calculated on an annualized basis. GAAP income before income taxes $ 3,878 $ 18,820 $ 16,888 $ 45,182 $ 53,331 Day 1, Provision for Credit Losses - Empire transaction 1,818 — — 1,818 — Net (gain) loss from fair value adjustments 4,129 2,225 (807) 2,142 5,353 Net loss on sale of securities 610 — — 701 15 Life insurance proceeds — — (419) (659) (462) Net gain on sale of assets — — — — (770) Net (gain) loss from fair value adjustments on qualifying hedges (1,023) (230) (1,039) 1,185 1,678 Accelerated employee benefits upon Officer's death — — — — 455 Prepayment Penalty on Borrowings 7,834 — — 7,834 — Net amortization of purchase accounting adjustments 80 — — 80 — Merger expense 5,349 422 1,080 6,894 1,590 Core income before taxes 22,675 21,237 15,703 65,177 61,190 Provision for income taxes for core income 4,891 5,069 3,841 15,428 13,957 Core net income $ 17,784 $ 16,168 $ 11,862 $ 49,749 $ 47,233 GAAP diluted earnings per common share $ 0.11 $ 0.50 $ 0.45 $ 1.18 $ 1.44 Day 1, Provision for Credit Losses - Empire transaction, net of tax 0.05 — — 0.05 — Net (gain) loss from fair value adjustments, net of tax 0.11 0.06 (0.02) 0.06 0.14 Net loss on sale of securities, net of tax 0.02 — — 0.02 — Life insurance proceeds — — (0.01) (0.02) (0.02) Net gain on sale of assets, net of tax — — — — (0.02) Net (gain) loss from fair value adjustments on qualifying hedges, net of tax (0.03) (0.01) (0.03) 0.03 0.05 Accelerated employee benefits upon Officer's death, net of tax — — — — 0.01 Prepayment Penalty on Borrowings, net of tax 0.20 — — 0.20 — Net amortization of purchase accounting adjustments, net of tax — — — — — Merger expense, net of tax 0.14 0.01 0.03 0.18 0.04 Core diluted earnings per common share(1) $ 0.58 $ 0.56 $ 0.41 $ 1.70 $ 1.65 Core net income, as calculated above $ 17,784 $ 16,168 $ 11,862 $ 49,749 $ 47,233 Average assets 7,705,407 7,083,028 7,057,094 7,276,022 6,947,881 Average equity 609,463 576,512 567,461 580,067 561,289 Core return on average assets(2) 0.92 % 0.91 % 0.67 % 0.68 % 0.68 % Core return on average equity(2) 11.67 % 11.22 % 8.36 % 8.58 % 8.42 % 2020 September 30, December 31, 2020 Three Months Ended December 31, 2019 Year Ended December 31, 2020 2019 December 31, |

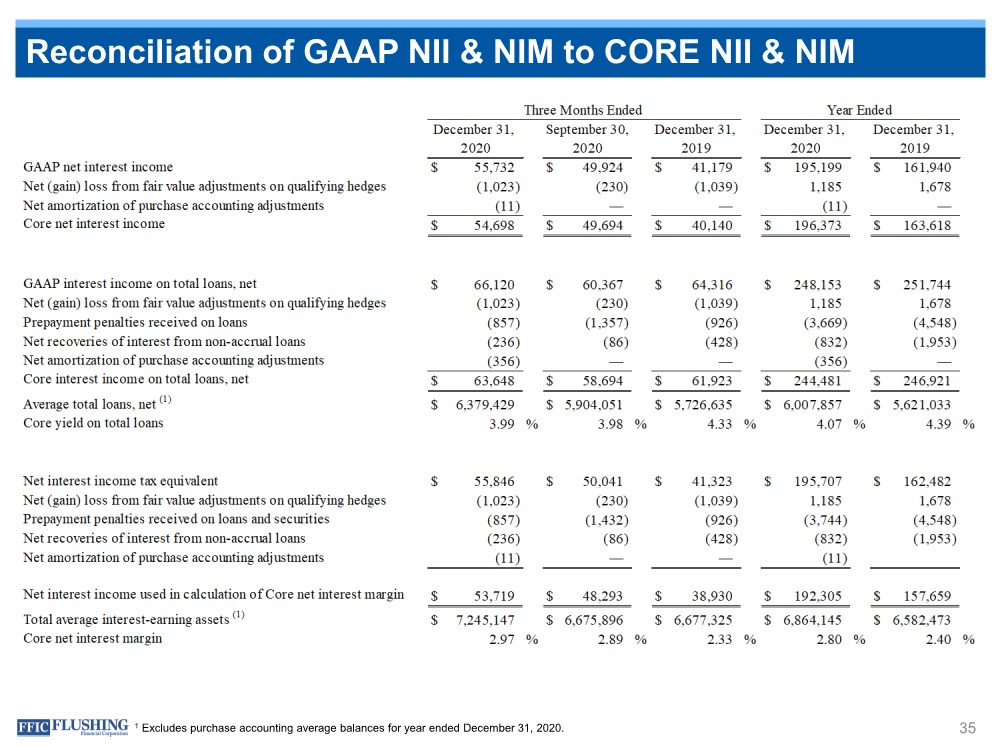

| Reconciliation of GAAP NII & NIM to CORE NII & NIM 35 1 Excludes purchase accounting average balances for year ended December 31, 2020. |

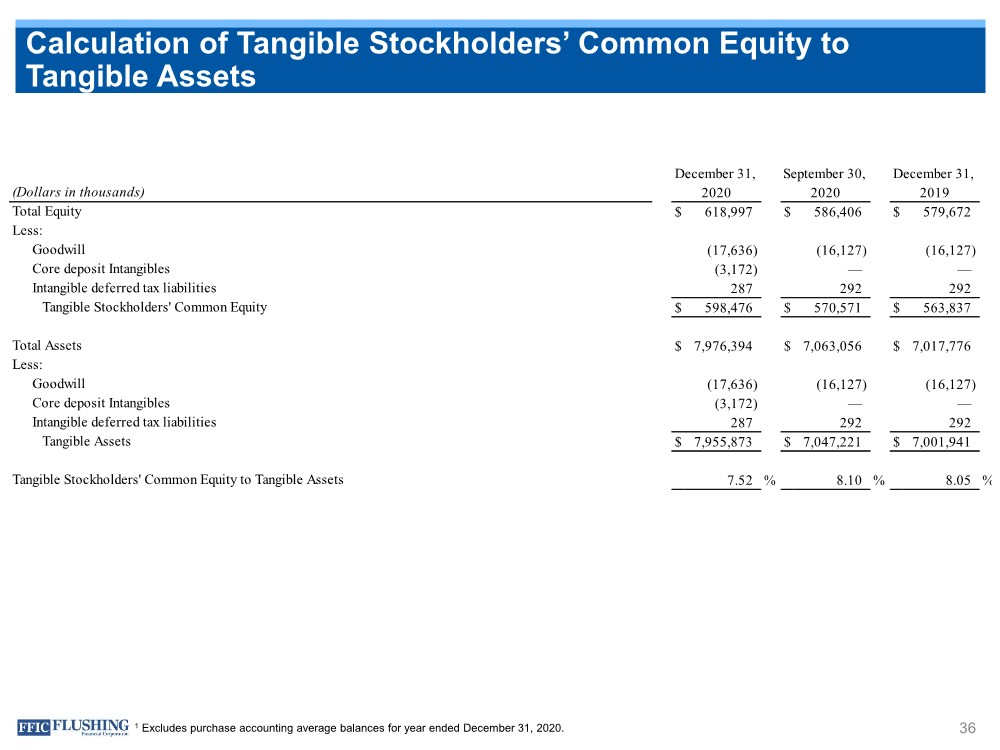

| Calculation of Tangible Stockholders’ Common Equity to Tangible Assets 36 (Dollars in thousands) Total Equity $ 618,997 $ 586,406 $ 579,672 Less: Goodwill (17,636) (16,127) (16,127) Core deposit Intangibles (3,172) — — Intangible deferred tax liabilities 287 292 292 Tangible Stockholders' Common Equity $ 598,476 $ 570,571 $ 563,837 Total Assets $ 7,976,394 $ 7,063,056 $ 7,017,776 Less: Goodwill (17,636) (16,127) (16,127) Core deposit Intangibles (3,172) — — Intangible deferred tax liabilities 287 292 292 Tangible Assets $ 7,955,873 $ 7,047,221 $ 7,001,941 Tangible Stockholders' Common Equity to Tangible Assets 7.52 % 8.10 % 8.05 % 2020 September 30, December 31, 2019 2020 December 31, 1 Excludes purchase accounting average balances for year ended December 31, 2020. |

| Contact Details | Flushing Financial Corporation 37 Susan Cullen SEVP, CFO & Treasurer (516) 209-3622 susan.cullen@flushingbank.com NASDAQ: FFIC |

|