Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - NATIONAL RURAL UTILITIES COOPERATIVE FINANCE CORP /DC/ | nrufy2021q1exhibit322.htm |

| EX-32.1 - EXHIBIT 32.1 - NATIONAL RURAL UTILITIES COOPERATIVE FINANCE CORP /DC/ | nrufy2021q1exhibit321.htm |

| EX-31.2 - EXHIBIT 31.2 - NATIONAL RURAL UTILITIES COOPERATIVE FINANCE CORP /DC/ | nrufy2021q1exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - NATIONAL RURAL UTILITIES COOPERATIVE FINANCE CORP /DC/ | nrufy2021q1exhibit311.htm |

| EX-3.2 - EXHIBIT 3.2 - NATIONAL RURAL UTILITIES COOPERATIVE FINANCE CORP /DC/ | nrufy2021q1exhibit32.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________

FORM 10-Q

__________________________

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended August 31, 2020

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 1-7102

__________________________

NATIONAL RURAL UTILITIES

COOPERATIVE FINANCE CORPORATION

(Exact name of registrant as specified in its charter)

__________________________

District of Columbia | 52-0891669 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

20701 Cooperative Way, Dulles, Virginia, 20166 |

(Address of principal executive offices) (Zip Code) |

Registrant’s telephone number, including area code: (703) 467-1800

__________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

7.35% Collateral Trust Bonds, due 2026 | NRUC 26 | New York Stock Exchange |

5.50% Subordinated Notes, due 2064 | NRUC | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Smaller reporting company ¨ Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transaction period for complying with any new or revised financial accounting standards provided pursuant to Section13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

TABLE OF CONTENTS

Page | ||||

i

MD&A TABLE CROSS REFERENCE INDEX

Table | Description | Page | |||

1 | Summary of Selected Financial Data | 3 | |||

2 | Average Balances, Interest Income/Interest Expense and Average Yield/Cost | 11 | |||

3 | Rate/Volume Analysis of Changes in Interest Income/Interest Expense | 13 | |||

4 | Non-Interest Income | 15 | |||

5 | Derivative Gains (Losses) | 16 | |||

6 | Derivative Cash Settlements Expense—Average Notional Amounts and Interest Rates | 17 | |||

7 | Non-Interest Expense | 18 | |||

8 | Loans Outstanding by Member Class and Loan Type | 19 | |||

9 | Historical Retention Rate and Repricing Selection | 20 | |||

10 | Total Debt Outstanding | 21 | |||

11 | Member Investments | 22 | |||

12 | Collateral Pledged | 23 | |||

13 | Unencumbered Loans | 24 | |||

14 | Equity | 25 | |||

15 | Guarantees Outstanding | 26 | |||

16 | Maturities of Guarantee Obligations | 27 | |||

17 | Unadvanced Loan Commitments | 27 | |||

18 | Unadvanced Loan Commitments Maturities of Notional Amount | 28 | |||

19 | Unconditional Committed Lines of Credit Maturities of Notional Amount | 29 | |||

20 | Loan Portfolio Security Profile | 31 | |||

21 | Loan Exposure to 20 Largest Borrowers | 32 | |||

22 | Troubled Debt Restructured Loans | 33 | |||

23 | Allowance for Credit Losses | 35 | |||

24 | Rating Triggers for Derivatives | 37 | |||

25 | Available Liquidity | 38 | |||

26 | Committed Bank Revolving Line of Credit Agreements | 38 | |||

27 | Short-Term Borrowings—Funding Sources | 40 | |||

28 | Short-Term Borrowings | 40 | |||

29 | Long-Term and Subordinated Debt Issuances and Repayments | 41 | |||

30 | Long-Term and Subordinated Debt Principal Maturity | 41 | |||

31 | Projected Sources and Uses of Liquidity from Debt and Investment Activity | 42 | |||

32 | Credit Ratings | 43 | |||

33 | Interest Rate Gap Analysis | 45 | |||

34 | Adjusted Financial Measures—Income Statement | 46 | |||

35 | TIER and Adjusted TIER | 47 | |||

36 | Adjusted Financial Measures—Balance Sheet | 47 | |||

37 | Debt-to-Equity Ratio and Adjusted Debt-to-Equity Ratio | 48 | |||

38 | Members’ Equity | 48 | |||

ii

PART I—FINANCIAL INFORMATION

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) |

FORWARD-LOOKING STATEMENTS |

This Quarterly Report on Form 10-Q for the quarterly period ended August 31, 2020 (“this Report”) contains certain statements that are considered “forward-looking statements” as defined and within the meaning of the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements do not represent historical facts or statements of current conditions. Instead, forward-looking statements represent management’s current beliefs and expectations, based on certain assumptions and estimates made by, and information available to, management at the time the statements are made, regarding our future plans, strategies, operations, financial results or other events and developments, many of which, by their nature, are inherently uncertain and outside our control. Forward-looking statements are generally identified by the use of words such as “intend,” “plan,” “may,” “should,” “will,” “project,” “estimate,” “anticipate,” “believe,” “expect,” “continue,” “potential,” “opportunity” and similar expressions, whether in the negative or affirmative. All statements about future expectations or projections, including statements about loan volume, the adequacy of the allowance for credit losses, operating income and expenses, leverage and debt-to-equity ratios, borrower financial performance, impaired loans, and sources and uses of liquidity, are forward-looking statements. Although we believe that the expectations reflected in our forward-looking statements are based on reasonable assumptions, actual results and performance may differ materially from our forward-looking statements. Therefore, you should not place undue reliance on any forward-looking statement and should consider the risks and uncertainties that could cause our current expectations to vary from our forward-looking statements including, but not limited to, general economic conditions, legislative changes including those that could affect our tax status, governmental monetary and fiscal policies, demand for our loan products, lending competition, changes in the quality or composition of our loan portfolio, changes in our ability to access external financing, changes in the credit ratings on our debt, valuation of collateral supporting impaired loans, charges associated with our operation or disposition of foreclosed assets, technological changes within the rural electric utility industry, regulatory and economic conditions in the rural electric industry, nonperformance of counterparties to our derivative agreements, the costs and impact of legal or governmental proceedings involving us or our members, the occurrence and effect of natural disasters or public health emergencies, such as the emergence in 2019 and continued spread of a novel coronavirus that causes coronavirus disease 2019 (“COVID-19”), which was declared a global pandemic by the World Health Organization (“WHO”) in March 2020, and the factors identified under “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended May 31, 2020 (“2020 Form 10-K”), as well as any risk factors identified under “Part II—Item 1A. Risk Factors” in this Report. Forward-looking statements speak only as of the date they are made, and, except as required by law, we undertake no obligation to update any forward-looking statement to reflect the impact of events, circumstances or changes in expectations that arise after the date the forward-looking statement is made.

INTRODUCTION |

National Rural Utilities Cooperative Finance Corporation (“CFC”) is a member-owned cooperative association incorporated under the laws of the District of Columbia in April 1969. CFC’s principal purpose is to provide its members with financing to supplement the loan programs of the Rural Utilities Service (“RUS”) of the United States Department of Agriculture (“USDA”). CFC makes loans to its rural electric members so they can acquire, construct and operate electric distribution systems, generation and transmission (“power supply”) systems and related facilities. CFC also provides its members with credit enhancements in the form of letters of credit and guarantees of debt obligations. As a cooperative, CFC is owned by and exclusively serves its membership, which consists of not-for-profit entities or subsidiaries or affiliates of not-for-profit entities. CFC is exempt from federal income taxes under Section 501(c)(4) of the Internal Revenue Code. As a member-owned cooperative, CFC’s objective is not to maximize profit, but rather to offer members cost-based financial products and services. CFC funds its activities primarily through a combination of public and private issuances of debt securities, member investments and retained equity. As a Section 501(c)(4) tax-exempt, member-owned cooperative, we cannot issue equity securities.

Our financial statements include the consolidated accounts of CFC, National Cooperative Services Corporation (“NCSC”), Rural Telephone Finance Cooperative (“RTFC”) and subsidiaries created and controlled by CFC to hold foreclosed assets resulting from defaulted loans or bankruptcy. NCSC is a taxable member-owned cooperative that may provide financing to

1

members of CFC, government or quasi-government entities which own electric utility systems that meet the Rural Electrification Act definition of “rural,” and for-profit and nonprofit entities that are owned, operated or controlled by, or provide significant benefits to certain members of CFC. RTFC is a taxable Subchapter T cooperative association that provides financing for its rural telecommunications members and their affiliates. CFC and its consolidated entities have not held any foreclosed assets since fiscal year 2017. See “Item 1. Business—Overview” in our 2020 Form 10-K for additional information on the business activities of each of these entities. Unless stated otherwise, references to “we,” “our” or “us” relate to CFC and its consolidated entities. All references to members within this document include members, associates and affiliates of CFC and its consolidated entities, except where indicated otherwise.

We conduct our operations through three business segments, which are based on of the legal entities included in our consolidated financial statements: CFC, NCSC and RTFC. CFC’s business operations account for the substantial majority of our loans and revenue. Loans to members totaled $26,929 million as of August 31, 2020, of which 96% was attributable to CFC. We generated total revenue, which consists of net interest income and fee and other income, of $103 million for the three months ended August 31, 2020 (“current quarter”), compared with $88 million for the three months ended August 31, 2019 (“same prior-year quarter”). Our adjusted total revenue was $76 million for the current quarter, compared with $77 million for the same prior-year quarter. We provide information on the financial performance of our business segments in “Note 14—Business Segments.”

Management monitors a variety of key indicators to evaluate our business performance. In addition to financial measures determined in accordance with generally accepted accounting principles in the United States (“GAAP”), management also evaluates performance based on certain non-GAAP measures and metrics, which we refer to as “adjusted” measures. The following MD&A is intended to provide the reader with an understanding of our consolidated results of operations, financial condition and liquidity by discussing the factors influencing changes from period to period and key measures used by management to evaluate performance, including, among others, net interest income, net interest yield, debt-to-equity ratio and the related non-GAAP adjusted measures, loan activity and credit quality metrics. Our MD&A is provided as a supplement to, and should be read in conjunction with the unaudited consolidated financial statements and related notes in this Report, our audited consolidated financial statements and related notes in our 2020 Form 10-K and additional information contained in our 2020 Form 10-K, including the risk factors identified under “Part I—Item 1A. Risk Factors,” as well as additional information contained elsewhere in this Report.

SUMMARY OF SELECTED FINANCIAL DATA |

Table 1 provides a summary of consolidated selected financial data for the three months ended August 31, 2020 and 2019, and as of August 31, 2020 and May 31, 2020. In addition to financial measures determined in accordance with GAAP, management also evaluates performance based on certain non-GAAP measures, which we refer to as “adjusted” measures. Our key non-GAAP financial measures are adjusted net income, adjusted net interest income, adjusted interest expense, adjusted net interest yield, adjusted TIER and adjusted debt-to-equity ratio. The most comparable GAAP measures are net income, net interest income, interest expense, net interest yield, TIER and debt-to-equity ratio, respectively. The primary adjustments we make to calculate these non-GAAP measures consist of: (i) adjusting interest expense and net interest income to include the impact of net periodic derivative cash settlements expense; (ii) adjusting net income, total liabilities and total equity to exclude the non-cash impact of the accounting for derivative financial instruments; (iii) adjusting total liabilities to exclude the amount that funds CFC member loans guaranteed by RUS, subordinated deferrable debt and members’ subordinated certificates; and (iv) adjusting total equity to include subordinated deferrable debt and members’ subordinated certificates and exclude cumulative derivative forward value gains and losses and accumulated other comprehensive income (“AOCI”). We believe our non-GAAP adjusted measures, which are not a substitute for GAAP and may not be consistent with similarly titled non-GAAP measures used by other companies, provide meaningful information and are useful to investors because management evaluates performance based on these metrics for purposes of: (i) budgeting and forecasting; (ii) comparing period-to-period operating results, analyzing changes in results and identifying potential trends; (iii) making compensation decisions; and (iv) informing the establishment of short- and long-term strategic goals. In addition, certain of the financial covenants in our committed bank revolving line of credit agreements and debt indentures are based on these non-GAAP adjusted measures. We provide a reconciliation of our non-GAAP adjusted measures to the most comparable GAAP measures in the section “Non-GAAP Financial Measures.”

2

Table 1: Summary of Selected Financial Data(1)

Three Months Ended August 31, | ||||||||||

(Dollars in thousands) | 2020 | 2019 | Change | |||||||

Statement of operations | ||||||||||

Interest income | $ | 279,584 | $ | 290,015 | (4)% | |||||

Interest expense | (179,976 | ) | (213,271 | ) | (16) | |||||

Net interest income | 99,608 | 76,744 | 30 | |||||||

Fee and other income | 3,516 | 10,941 | (68) | |||||||

Total revenue | 103,124 | 87,685 | 18 | |||||||

Provision for credit losses | (326 | ) | (30 | ) | 987 | |||||

Derivative gains (losses)(2) | 60,276 | (395,725 | ) | ** | ||||||

Investment securities gains | 4,659 | 1,620 | 188 | |||||||

Operating expenses(3) | (22,663 | ) | (25,329 | ) | (11) | |||||

Other non-interest (expense) income(1) | (332 | ) | 7,179 | ** | ||||||

Income (loss) before income taxes | 144,738 | (324,600 | ) | ** | ||||||

Income tax (provision) benefit | (151 | ) | 521 | ** | ||||||

Net income (loss) | $ | 144,587 | $ | (324,079 | ) | ** | ||||

Adjusted operational financial measures | ||||||||||

Adjusted interest expense(4) | $ | (206,948 | ) | $ | (224,314 | ) | (8) | |||

Adjusted net interest income(4) | 72,636 | 65,701 | 11 | |||||||

Adjusted total revenue(4) | 76,152 | 76,642 | (1) | |||||||

Adjusted net income(4) | 57,339 | 60,603 | (5) | |||||||

Selected ratios | ||||||||||

Fixed-charge coverage ratio/TIER(5) | 1.80 | — | 180 bps | |||||||

Adjusted TIER(4) | 1.28 | 1.27 | 1 | |||||||

Net interest yield(6) | 1.42 | % | 1.14 | % | 28 | |||||

Adjusted net interest yield(4)(7) | 1.04 | 0.97 | 7 | |||||||

Net charge-off rate(8) | 0.00 | 0.00 | — | |||||||

3

August 31, 2020 | May 31, 2020 | Change | ||||||||

Balance sheet | ||||||||||

Cash, cash equivalents and restricted cash | $ | 357,194 | $ | 680,019 | (47)% | |||||

Investment securities | 589,792 | 370,135 | 59 | |||||||

Loans to members(9) | 26,928,877 | 26,702,380 | 1 | |||||||

Allowance for credit losses(10) | (57,351 | ) | (53,125 | ) | 8 | |||||

Loans to members, net | 26,871,526 | 26,649,255 | 1 | |||||||

Total assets | 28,262,621 | 28,157,605 | — | |||||||

Short-term borrowings | 4,553,491 | 3,961,985 | 15 | |||||||

Long-term debt | 19,181,520 | 19,712,024 | (3) | |||||||

Subordinated deferrable debt | 986,166 | 986,119 | — | |||||||

Members’ subordinated certificates | 1,298,845 | 1,339,618 | (3) | |||||||

Total debt outstanding | 26,020,022 | 25,999,746 | — | |||||||

Total liabilities | 27,531,117 | 27,508,783 | — | |||||||

Total equity | 731,504 | 648,822 | 13 | |||||||

Guarantees(11) | 683,246 | 820,786 | (17) | |||||||

Selected ratios period end | ||||||||||

Allowance coverage ratio(10)(12) | 0.21 | % | 0.20 | % | — | |||||

Debt-to-equity ratio(13) | 37.64 | 42.40 | (476) | |||||||

Adjusted debt-to-equity ratio(4) | 5.96 | 5.85 | 11 | |||||||

** Calculation of percentage change is not meaningful.

(1)Certain reclassifications have been made to prior periods to conform to the current period presentation.

(2)Consists of net periodic contractual interest amounts on our interest rate swaps, which we refer to as derivatives cash settlements interest (expense) income, and derivative forward value gains (losses) on derivatives not designated for hedge accounting. Derivative forward value gains (losses) represent changes in fair value during the period, excluding net periodic contractual interest amounts, related to derivatives not designated for hedge accounting and amounts reclassified into income related to the cumulative transition adjustment amount recorded in accumulated other comprehensive income as of June 1, 2001, the adoption date of the derivative accounting guidance requiring derivatives to be reported at fair value on the balance sheet.

(3)Consists of salaries and employee benefits and the other general and administrative expenses components of non-interest expense, each of which are presented separately on our consolidated statements of operations.

(4)See “Non-GAAP Financial Measures” for details on the calculation of these non-GAAP adjusted measures and the reconciliation to the most comparable GAAP measures.

(5)Calculated based on net income (loss) plus interest expense for the period divided by interest expense for the period. The fixed-charge coverage ratios and TIER were the same during each period presented because we did not have any capitalized interest during these periods.

(6)Calculated based on annualized net interest income for the period divided by average interest-earning assets for the period.

(7)Calculated based on annualized adjusted net interest income for the period divided by average interest-earning assets for the period.

(8)Calculated based on annualized net charge-offs (recoveries) for the period divided by average total outstanding loans for the period.

(9)Consists of the outstanding principal balance of member loans plus unamortized deferred loan origination costs, which totaled $12 million as of both August 31, 2020 and May 31, 2020.

(10)On June 1, 2020, we adopted Accounting Standards Update (“ASU”) 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which replaces the incurred loss methodology previously used for estimating our allowance for credit losses with an expected loss methodology referred to as the current expected credit loss (“CECL”) model. At adoption, we recorded an increase in our allowance for credit losses of $4 million and a corresponding decrease in retained earnings through a cumulative-effect adjustment.

(11)Reflects the total amount of member obligations for which CFC has guaranteed payment to a third party as of the end of each period. This amount represents our maximum exposure to loss, which significantly exceeds the guarantee liability recorded on our consolidated balance sheets. See “Note 11—Guarantees” for additional information.

(12)Calculated based on the allowance for credit losses at period end divided by total outstanding loans at period end.

(13)Calculated based on total liabilities at period end divided by total equity at period end.

4

EXECUTIVE SUMMARY |

Our primary objective as a member-owned cooperative lender is to provide cost-based financial products to our rural electric members while maintaining a sound financial position required for investment-grade credit ratings on our debt instruments. Our objective is not to maximize profit; therefore, the rates we charge our member-borrowers reflect our funding costs plus a spread to cover our operating expenses, a provision for credit losses and earnings sufficient to achieve interest coverage to meet our financial objectives. Our goal is to earn an annual minimum adjusted TIER of 1.10 and to maintain an adjusted debt-to-equity ratio at approximately 6.00-to-1 or below.

We are subject to period-to-period volatility in our reported GAAP results due to changes in market conditions and differences in the way our financial assets and liabilities are accounted for under GAAP. Our financial assets and liabilities expose us to interest-rate risk. We use derivatives, primarily interest rate swaps, as part of our strategy in managing this risk. Our derivatives are intended to economically hedge and manage the interest-rate sensitivity mismatch between our financial assets and liabilities. We are required under GAAP to carry derivatives at fair value on our consolidated balance sheets; however, the financial assets and liabilities for which we use derivatives to economically hedge are carried at amortized cost. Changes in interest rates and the shape of the swap curve result in periodic fluctuations in the fair value of our derivatives, which may cause volatility in our earnings because we do not apply hedge accounting for our interest rate swaps. As a result, the mark-to-market changes in our interest rate swaps are recorded in earnings. Because our derivative portfolio consists of a higher proportion of pay-fixed swaps than receive-fixed swaps, we generally record derivative losses when interest rates decline and derivative gains when interest rates rise. This earnings volatility generally is not indicative of the underlying economics of our business, as the derivative forward fair value gains or losses recorded each period may or may not be realized over time, depending on the terms of our derivative instruments and future changes in market conditions that impact the periodic cash settlement amounts of our interest rate swaps. As such, management uses our non-GAAP adjusted results to evaluate our operating performance. Our adjusted results include realized net periodic interest rate swap settlement amounts but exclude the impact of unrealized forward fair value gains and losses. Certain of the financial covenants in our committed bank revolving line of credit agreements and debt indentures are also based on our non-GAAP adjusted results, as the forward fair value gains and losses related to our interest rate swaps do not affect our cash flows, liquidity or ability to service our debt.

Financial Performance

Reported Results

We reported net income of $145 million and a TIER of 1.80 for the current quarter. In comparison, we reported a net loss of $324 million for the same prior-year quarter, which resulted in no TIER coverage. The significant variance between our reported results for the current quarter and the same prior-year quarter was attributable to mark-to-market changes in the fair value of our derivative instruments. Our debt-to-equity ratio decreased to 37.64 as of August 31, 2020, from 42.40 as of May 31, 2020, primarily due to an increase in equity from our reported net income of $145 million, which was partially offset by a decrease in equity as a result of the CFC Board of Directors’ authorization in the current quarter to retire patronage capital of $60 million, which we returned to members in September 2020.

The variance of $469 million between our reported net income of $145 million for the current quarter and our reported net loss of $324 million for the same prior-year quarter was driven by a shift of $456 million in the derivative fair value changes recorded in each period. We recorded net derivative gains of $60 million for the current quarter due to a net increase in the fair value of our swap portfolio, which consists predominately of pay-fixed swaps, primarily attributable to an increase in long-term swap interest rates. In comparison, we recorded net derivative losses of $396 million for the same prior-year quarter due to a net decrease in the fair value of our swap portfolio primarily attributable to a decline in interest rates across the swap curve, with medium- and longer-term interest rates experiencing a steeper decline than short-term rates. Net interest income increased $23 million, or 30%, to $100 million for the current quarter, attributable to an increase in the net interest yield of 28 basis points, or 25%, to 1.42% and an increase in our average interest-earning assets of $947 million, or 4%. The increase in the net interest yield was largely due to a reduction in our average cost of borrowings of 61 basis points to 2.75%, partially offset by a decrease in the average yield on interest-earning assets of 31 basis points to 3.99%. The reduction in the overall average cost of borrowings was driven by a decrease in the average cost of our short-term borrowings of 213 basis points to 0.45% for the current quarter.

5

The decreases in our average borrowing cost and average yield on interest-earning assets reflect in part the impact of the overall lower interest rate environment. Since August 31, 2019, the end of the same prior-year quarter, the Federal Open Market Committee (“FOMC”) of the Federal Reserve has lowered the benchmark federal funds rate by 200 basis points, including a 150 basis point reduction in March 2020 to a near zero target range of 0% to 0.25% as part of a series of measures implemented to ease the economic impact of the COVID-19 crisis. Over the last 12 months, the 3-month London Interbank Offered Rate (“LIBOR”) decreased by190 basis points to 0.24% as of August 31, 2020. Medium- and longer-term interest rates also fell during this 12-month period, but the decreases were not as pronounced as the decrease in short-term interest rates.

Other factors affecting the variance between our results for the current quarter and the same prior-year quarter include a decrease in fee income of $7 million due to a reduction in prepayment fees and the absence of a gain of $8 million recorded in connection with the sale of land in the same prior-year quarter.

Adjusted Non-GAAP Results

Adjusted net income totaled $57 million and adjusted TIER was 1.28 for the current quarter, compared with adjusted net income of $61 million and adjusted TIER of 1.27 for the same prior-year quarter. Our adjusted debt-to-equity ratio increased to 5.96 as of August 31, 2020, from 5.85 as of May 31, 2020, primarily attributable to a reduction in adjusted equity due to the maturity of subordinated certificates and the authorized patronage capital retirement amount, partially offset by adjusted net income for the current quarter. Our adjusted debt-to-equity ratio of 5.96 as of August 31, 2020, remained below our targeted threshold of 6.00-to-1.

The decrease in adjusted net income of $4 million in the current quarter from the same prior-year quarter was largely attributable to the combined impact of the decrease in fee income of $7 million due to a reduction in prepayment fees and the absence of the gain of $8 million recorded in connection with the sale of land in the same prior-year quarter, which was partially offset by an increase in adjusted net interest income of $7 million, or 11%, to $73 million for the current quarter. The increase in adjusted net interest income was driven by an increase in the adjusted net interest yield of 7 basis points, or 7%, to 1.04% and an increase in average interest-earning assets of $947 million, or 4%. The increase in our adjusted net interest yield reflected the favorable impact of a reduction in our adjusted average cost of borrowings of 37 basis points to 3.16%, which was partially offset by a decrease in the average yield on interest-earning assets of 31 basis points to 3.99%. As noted above, the lower interest rate environment had a favorable impact on our adjusted average cost of borrowings and contributed to the decrease in the average yield on interest-earnings assets.

See “Non-GAAP Financial Measures” for additional information on our adjusted measures, including a reconciliation of these measures to the most comparable GAAP measures.

Lending Activity

Loans to members totaled $26,929 million as of August 31, 2020, an increase of $227 million, or 1%, from May 31, 2020. The increase was driven by an increase in long-term loans of $385 million, partially offset by a decrease in line of credit loans of $159 million. CFC distribution loans and RTFC loans increased by $242 million and $11 million, respectively. NCSC loans, CFC statewide and associate loans and CFC power supply loans decreased by $17 million, $8 million and $2 million, respectively.

Long-term loan advances totaled $807 million during the current quarter, of which approximately 93% was provided to members for capital expenditures and approximately 4% was provided for the refinancing of loans made by other lenders. In comparison, long-term loan advances totaled $888 million during the same prior-year quarter, of which approximately 73% was provided to members for capital expenditures and approximately 19% was provided for the refinancing of loans made by other lenders. CFC had long-term fixed-rate loans totaling $79 million that were scheduled to reprice during the current quarter. Of this total, $78 million repriced to a new long-term fixed rate and the remainder either repriced to a long-term variable rate or were repaid in full. In comparison, CFC had long-term fixed-rate loans totaling $110 million that were scheduled to reprice during the same prior-year quarter, of which $109 million repriced to a new long-term fixed rate and $1 million was repaid in full.

6

Credit Quality

Despite the economic disruption caused by COVID-19, the overall credit quality of our loan portfolio remained high as of August 31, 2020, as evidenced by our continued strong credit performance metrics. We had no delinquent loans as of August 31, 2020 or May 31, 2020, and we have not experienced any loan defaults or charge-offs since fiscal year 2017. During the fourth quarter of fiscal year 2020, we classified one loan to a CFC power supply borrower with an outstanding balance of $168 million as of May 31, 2020, as nonperforming, placed the loan on nonaccrual status and established an asset-specific allowance for credit losses of $34 million as of May 31, 2020. We received payments from the borrower on this loan during the current quarter, which reduced the outstanding balance to $161 million as of August 31, 2020. The asset-specific allowance for credit losses for this loan, which we continue to report as nonperforming and remains on nonaccrual status, was $33 million as of August 31, 2020. We had no other loans classified as nonperforming or on nonaccrual status as of August 31, 2020 or May 31, 2020.

Loans outstanding to electric utility organizations represented approximately 99% of total loans outstanding as of both August 31, 2020 and May 31, 2020. We historically have had limited defaults and losses on loans in our electric utility loan portfolio largely because of the essential nature of the service provided by electric utility cooperatives as well as other factors, such as limited rate regulation and competition, which we discuss further in the section “Credit Risk—Loan Portfolio Credit Risk.” We generally lend to members on a senior secured basis, which reduces the risk of loss in the event of a borrower default. Of our total loans outstanding, 94% were secured as of August 31, 2020 and May 31, 2020.

On June 1, 2020, we adopted ASU 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which replaces the incurred loss methodology for estimating credit losses with an expected loss methodology that is referred to as the current expected credit loss (“CECL”) model. The incurred loss model delayed the recognition of credit losses until it was probable that a loss had occurred, while the CECL model requires the immediate recognition of expected credit losses over the contractual term, adjusted as appropriate for estimated prepayments, of financial instruments that fall within the scope of CECL at the date of origination or purchase of the financial instrument. The CECL model, which is applicable to the measurement of credit losses on financial assets measured at amortized cost and certain off-balance sheet credit exposures, affects our estimates of the allowance for credit losses for our loan portfolio and our off-balance sheet credit exposures related to unadvanced loan commitments and financial guarantees.The adoption of CECL resulted in an increase in our allowance for credit losses for our loan portfolio of $4 million and a corresponding decrease to retained earnings of $4 million recorded through a cumulative-effect adjustment. The impact on the allowance for credit losses for our off-balance sheet credit exposures related to unadvanced loan commitments and financial guarantees was not material. While the adoption of CECL had no impact on our earnings, subsequent to our adoption on June 1, 2020, lifetime expected credit losses for newly recognized loans, unadvanced loan commitments and financial guarantees, as well as changes during the period in our estimate of lifetime expected credit losses for existing financial instruments subject to CECL, will be recognized in earnings.

The allowance for credit losses for our loan portfolio increased to $57 million as of August 31, 2020, from $53 million as of May 31, 2020, and the allowance coverage ratio increased to 0.21% from 0.20%, primarily due to the increase in the allowance of $4 million recorded at adoption of CECL on June 1, 2020. We discuss our methodology for estimating the allowance for credit losses under the CECL model in “Note 1—Summary of Significant Accounting Policies” of this Report. We also provide information on the allowance for credit losses below in the section “Credit Risk—Allowance for Credit Losses” and in “Note 5—Allowance for Credit Losses.”

7

Financing Activity

We issue debt primarily to fund growth in our loan portfolio. As such, our outstanding debt volume generally increases and decreases in response to member loan demand. Total debt outstanding was $26,020 million as of August 31, 2020, an increase of $20 million from May 31, 2020. Debt activity during the current quarter consisted of net increases in outstanding member commercial paper, select notes and daily liquidity fund notes of $297 million and dealer commercial paper of $300 million, which together totaled $597 million. This increase was partially offset by net decreases in collateral trust bonds of $396 million, medium-term notes of $86 million, borrowings under the United States Department of Agriculture (“USDA”) Guaranteed Underwriter Program (“Guaranteed Underwriter Program”) of $35 million and Federal Agricultural Mortgage Corporation (“Farmer Mac”) notes payable of $18 million, which together totaled $535 million. Outstanding dealer commercial paper totaled $300 million as of August 31, 2020, below our targeted maximum threshold of $1,250 million.

Liquidity

As of August 31, 2020, our sources of liquidity readily available for access totaled $6,956 million, consisting of (i) $348 million in cash and cash equivalents; (ii) $528 million in debt investment securities; (iii) up to $2,722 million available for access under committed bank revolving line of credit agreements; (iv) up to $900 million available under committed loan facilities under the Guaranteed Underwriter Program; and (v) up to $2,458 million available under a revolving note purchase agreement with Farmer Mac, subject to market conditions.

The face value of long-term debt scheduled to mature over the next 12 months totaled $2,269 million as of August 31, 2020, consisting of fixed-rate debt of $1,395 million with a weighted average cost of 2.35%, variable-rate debt of $645 million and scheduled amortization on borrowings under the Guaranteed Underwriter Program and notes payable to Farmer Mac of $229 million. Our available liquidity of $6,956 million as of August 31, 2020, was $4,687 million, or 2.1 times, in excess of our long-term debt obligations of $2,269 million over the next 12 months. We currently believe that our available liquidity along with our ability to access the capital markets as a well-known seasoned issuer of debt and to issue debt to our members and in private placements will be more than sufficient to cover our debt obligations to meet the borrowing needs of our members and satisfy our obligations to repay long-term debt maturing over the next 12 months subsequent to August 31, 2020.

Our members historically have maintained a relatively stable level of short-term investments in CFC in the form of commercial paper, select notes, daily liquidity fund notes and medium-term notes. We believe we can continue to roll over outstanding member short-term debt of $4,003 million as of August 31, 2020, based on our expectation that our members will continue to reinvest their excess cash in our commercial paper, daily liquidity fund notes, select notes and medium-term notes. We expect to continue accessing the dealer commercial paper market as a cost-effective means of satisfying our short-term liquidity needs. Although the intra-period amount of outstanding dealer commercial paper may fluctuate based on our liquidity requirements, we intend to manage our short-term wholesale funding risk by maintaining outstanding dealer commercial paper at an amount near or below $1,250 million for the foreseeable future. We expect to continue to be in compliance with the covenants under our committed bank revolving line of credit agreements, which will allow us to mitigate roll-over risk, as we can draw on these facilities to repay dealer or member commercial paper that cannot be refinanced with similar debt.

We provide additional information on our primary sources and uses of liquidity and our liquidity profile below in the section “Liquidity Risk.”

COVID-19

We continue to adhere to the COVID-19 guidelines established by the Centers for Disease Control and Prevention and the World Health Organization and orders issued by state and local governments where we operate. In mid-June 2020, following the announcement by the governor of phased reopening dates and guidelines for Virginia, we implemented a return-to-work policy that included, as part of our physical distancing measures, assigning employees to physically separate teams and a staggered weekly in-office rotation schedule for each team to limit the number of employees present at any given time, face mask covering requirements and an enhanced cleaning program to maintain the well-being of our employees as well as comply with Virginia’s reopening guidelines. Our current expectation is that we will maintain the return-to-work policy

8

implemented in mid-June for the near term. To date, our business resiliency plans and technology systems have effectively supported both remote and on-site operations.

We have been working with our members not only as a lender, but also by offering a full range of products, services, tools and training designed to help cooperatives continue to deliver uninterrupted, essential utility services to their customers and successfully manage the ongoing challenges of the COVID-19 pandemic.

Outlook for the Next 12 Months

We have been able to navigate the challenges of the COVID-19 pandemic reasonably well to date. As noted above, we currently believe that we have sufficient cash flow and liquidity to cover our debt obligations as well as meet the borrowing needs of our members. While there continues to be uncertainty about the duration and severity of the COVID-19 pandemic and the extent of its future economic impact, our borrowers operate in an industry sector that historically has been resilient to economic downturns. Our electric utility cooperative members, which have a strong track record in preparing for and responding to emergencies, thus far, have been able to manage the challenges and pressures presented by the COVID-19 pandemic. To date, the COVID-19 pandemic has not had a material adverse impact on the operations and financial performance of the substantial majority of our borrowers. Thus far, we have not experienced any delinquencies in scheduled loan payments from our borrowers or received requests for payment deferrals or covenant relief.

While the overall credit quality of our loan portfolio remains high, we continue to actively monitor conditions and developments, including key credit metrics of our borrowers, to facilitate the timely identification of loans with potential credit weaknesses and assess any notable shifts in the credit quality of our loan portfolio as well as any impact on our financial position. Assuming no material adverse change in the overall credit quality of our borrowers, we expect that our financial performance for fiscal year 2021 will be comparable to or slightly better than our financial performance for fiscal year 2020, absent the impact of (i) the non-cash impairment charge of $31 million recorded in the fourth quarter of fiscal year 2020 resulting from the abandonment of an internal-use software project; (ii) the loan impairment charge of $34 million recorded in the fourth quarter of fiscal year 2020 due to the establishment of an asset-specific allowance for the outstanding loan to the CFC power supply borrower noted above; and (iii) changes in the fair value of our derivatives and investment securities that are driven by changes in market interest rates and prices, which we are unable to predict.

See “Item 1A. Risk Factors” in our 2020 Form 10-K for a discussion of the potential adverse impact of COVID-19 on our business, results of operations, financial condition and liquidity.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES |

The preparation of financial statements in accordance with GAAP requires management to make a number of judgments, estimates and assumptions that affect the reported amount of assets, liabilities, income and expenses in our consolidated financial statements. Understanding our accounting policies and the extent to which we use management’s judgment and estimates in applying these policies is integral to understanding our financial statements. We provide a discussion of our significant accounting policies under “Note 1—Summary of Significant Accounting Policies” in our 2020 Form 10-K. Pursuant to our June 1, 2020 adoption of the CECL accounting standard, we have provided updates to certain of our significant accounting policies, including the allowance for credit losses, in “Note 1—Summary of Significant Accounting Policies” of this Report.

We have identified certain accounting policies as critical because they involve significant judgments and assumptions about highly complex and inherently uncertain matters, and the use of reasonably different estimates and assumptions could have a material impact on our results of operations or financial condition. Our most critical accounting policies and estimates involve the determination of the allowance for credit losses and fair value. Below we have updated our critical accounting policy for the allowance for credit losses under the CECL model, which involves additional areas involving significant management judgment.

Prior to the adoption of CECL on June 1, 2020, we maintained an allowance based on an estimate of probable incurred losses inherent in our loan portfolio as of each balance sheet date. Under CECL, we are required to maintain an allowance based on a current estimate of credit losses that are expected to occur over the remaining contractual life of the loans in our

9

portfolio. The methods utilized to estimate the allowance for credit losses, key assumptions and quantitative and qualitative information considered by management in determining the appropriate allowance for credit losses is discussed in “Note 1—Summary of Significant Accounting Policies” of this Report. The determination of allowance for credit losses entails significant judgment on various risk factors, including our historical loss data, third-party default data and the assessment of a borrower’s capacity to meet its financial obligations. While our estimate of lifetime credit losses is sensitive to each of these inputs, the most notable input that affects the sensitivity of the allowance is the internal risk ratings assigned to each borrower.

We evaluate our critical accounting estimates and judgments required by our policies on an ongoing basis and update them as necessary based on changing conditions. Management has discussed significant judgments and assumptions in applying our critical accounting policies with the Audit Committee of the CFC Board of Directors. We provide information on the significant judgments and assumptions in measuring fair value under “MD&A—Critical Accounting Policies and Estimates” in our 2020 Form 10-K. See “Item 1A. Risk Factors” in our 2020 Form 10-K for a discussion of the risks associated with management’s judgments and estimates in applying our accounting policies and methods.

RECENT ACCOUNTING CHANGES AND OTHER DEVELOPMENTS |

Recent Accounting Changes

See “Note 1—Summary of Significant Accounting Policies” for information on accounting standards adopted during the current fiscal year, as well as recently issued accounting standards not yet required to be adopted and the expected impact of the adoption of these accounting standards. To the extent we believe the adoption of new accounting standards has had or will have a material impact on our consolidated results of operations, financial condition or liquidity, we also discuss the impact in the applicable section(s) of this MD&A.

CONSOLIDATED RESULTS OF OPERATIONS |

The section below provides a comparative discussion of our consolidated results of operations between the three months ended August 31, 2020 and 2019. Following this section, we provide a comparative analysis of our consolidated balance sheets as of August 31, 2020 and May 31, 2020. You should read these sections together with our “Executive Summary—Outlook for the Next 12 Months” where we discuss trends and other factors that we expect will affect our future results of operations.

Net Interest Income

Net interest income represents the difference between the interest income earned on our interest-earning assets, which includes loans and investment securities, and the interest expense on our interest-bearing liabilities. Our net interest yield represents the difference between the yield on our interest-earning assets and the cost of our interest-bearing liabilities plus the impact from non-interest bearing funding. We expect net interest income and our net interest yield to fluctuate based on changes in interest rates and changes in the amount and composition of our interest-earning assets and interest-bearing liabilities. We do not fund each individual loan with specific debt. Rather, we attempt to minimize costs and maximize efficiency by proportionately funding large aggregated amounts of loans.

Table 2 presents average balances for the three months ended August 31, 2020 and 2019, and for each major category of our interest-earning assets and interest-bearing liabilities, the interest income earned or interest expense incurred, and the average yield or cost. Table 2 also presents non-GAAP adjusted interest expense, adjusted net interest income and adjusted net interest yield, which reflect the inclusion of net accrued periodic derivative cash settlements expense in interest expense. We provide reconciliations of our non-GAAP adjusted measures to the most comparable GAAP measures under “Non-GAAP Financial Measures.”

10

Table 2: Average Balances, Interest Income/Interest Expense and Average Yield/Cost

Three Months Ended August 31, | ||||||||||||||||||||||

(Dollars in thousands) | 2020 | 2019 | ||||||||||||||||||||

Assets: | Average Balance | Interest Income/Expense | Average Yield/Cost | Average Balance | Interest Income/Expense | Average Yield/Cost | ||||||||||||||||

Long-term fixed-rate loans(1) | $ | 24,607,166 | $ | 263,184 | 4.24 | % | $ | 23,358,728 | $ | 258,528 | 4.40 | |||||||||||

Long-term variable-rate loans | 686,024 | 4,400 | 2.54 | 993,105 | 9,756 | 3.91 | ||||||||||||||||

Line of credit loans | 1,416,678 | 8,242 | 2.31 | 1,712,082 | 16,033 | 3.73 | ||||||||||||||||

Troubled debt restructuring (“TDR”) loans | 10,781 | 207 | 7.62 | 11,786 | 206 | 6.95 | ||||||||||||||||

Nonperforming loans | 164,758 | — | — | — | — | — | ||||||||||||||||

Other, net(2) | — | (335 | ) | — | — | (334 | ) | — | ||||||||||||||

Total loans | 26,885,407 | 275,698 | 4.07 | 26,075,701 | 284,189 | 4.34 | ||||||||||||||||

Cash, time deposits and investment securities | 906,308 | 3,886 | 1.70 | 768,763 | 5,826 | 3.01 | ||||||||||||||||

Total interest-earning assets | $ | 27,791,715 | $ | 279,584 | 3.99 | % | $ | 26,844,464 | $ | 290,015 | 4.30 | % | ||||||||||

Other assets, less allowance for credit losses | 476,024 | 605,697 | ||||||||||||||||||||

Total assets | $ | 28,267,739 | $ | 27,450,161 | ||||||||||||||||||

Liabilities: | ||||||||||||||||||||||

Short-term borrowings | $ | 3,864,887 | $ | 4,341 | 0.45 | % | $ | 3,513,191 | $ | 22,822 | 2.58 | % | ||||||||||

Medium-term notes | 3,684,835 | 29,887 | 3.22 | 3,571,967 | 32,076 | 3.57 | ||||||||||||||||

Collateral trust bonds | 6,850,779 | 62,593 | 3.62 | 7,385,085 | 65,381 | 3.52 | ||||||||||||||||

Guaranteed Underwriter Program notes payable | 6,242,813 | 42,413 | 2.70 | 5,398,324 | 40,433 | 2.98 | ||||||||||||||||

Farmer Mac notes payable | 3,052,451 | 13,933 | 1.81 | 3,031,600 | 25,074 | 3.29 | ||||||||||||||||

Other notes payable | 11,625 | 87 | 2.97 | 22,529 | 254 | 4.49 | ||||||||||||||||

Subordinated deferrable debt | 986,136 | 12,890 | 5.19 | 986,014 | 12,882 | 5.20 | ||||||||||||||||

Subordinated certificates | 1,307,879 | 13,832 | 4.20 | 1,356,145 | 14,349 | 4.21 | ||||||||||||||||

Total interest-bearing liabilities | $ | 26,001,405 | $ | 179,976 | 2.75 | % | $ | 25,264,855 | $ | 213,271 | 3.36 | % | ||||||||||

Other liabilities | 1,591,883 | 1,012,301 | ||||||||||||||||||||

Total liabilities | 27,593,288 | 26,277,156 | ||||||||||||||||||||

Total equity | 674,451 | 1,173,005 | ||||||||||||||||||||

Total liabilities and equity | $ | 28,267,739 | $ | 27,450,161 | ||||||||||||||||||

Net interest spread(3) | 1.24 | % | 0.94 | % | ||||||||||||||||||

Impact of non-interest bearing funding(4) | 0.18 | 0.20 | ||||||||||||||||||||

Net interest income/net interest yield(5) | $ | 99,608 | 1.42 | % | $ | 76,744 | 1.14 | % | ||||||||||||||

Adjusted net interest income/adjusted net interest yield: | ||||||||||||||||||||||

Interest income | $ | 279,584 | 3.99 | % | $ | 290,015 | 4.30 | % | ||||||||||||||

Interest expense | 179,976 | 2.75 | 213,271 | 3.36 | ||||||||||||||||||

Add: Net periodic derivative cash settlements interest expense(6) | 26,972 | 1.16 | 11,043 | 0.41 | ||||||||||||||||||

Adjusted interest expense/adjusted average cost(7) | $ | 206,948 | 3.16 | % | $ | 224,314 | 3.53 | % | ||||||||||||||

Adjusted net interest spread(5) | 0.83 | % | 0.77 | % | ||||||||||||||||||

Impact of non-interest bearing funding(4) | 0.21 | % | 0.20 | % | ||||||||||||||||||

Adjusted net interest income/adjusted net interest yield(8) | $ | 72,636 | 1.04 | % | $ | 65,701 | 0.97 | % | ||||||||||||||

____________________________

(1)Interest income on long-term, fixed-rate loans includes loan conversion fees, which are generally deferred and recognized as interest income using the effective interest method.

(2)Consists of late payment fees and net amortization of deferred loan fees and loan origination costs.

11

(3)Net interest spread represents the difference between the average yield on total average interest-earning assets and the average cost of total average interest-bearing liabilities. Adjusted net interest spread represents the difference between the average yield on total average interest-earning assets and the adjusted average cost of total average interest-bearing liabilities.

(4)Includes other liabilities and equity.

(5)Net interest yield is calculated based on annualized net interest income for the period divided by total average interest-earning assets for the period.

(6)Represents the impact of net periodic contractual interest amounts on our interest rate swaps during the period. This amount is added to interest expense to derive non-GAAP adjusted interest expense. The average (benefit)/cost associated with derivatives is calculated based on the annualized net periodic swap settlement interest amount during the period divided by the average outstanding notional amount of derivatives during the period. The average outstanding notional amount of interest rate swaps was $9,225 million and $10,752 million for the three months ended August 31, 2020 and 2019, respectively.

(7)Adjusted interest expense consists of interest expense plus net periodic derivative cash settlements interest expense during the period. Net periodic derivative cash settlement interest amounts are reported on our consolidated statements of operations as a component of derivative gains (losses). Adjusted average cost is calculated based on annualized adjusted interest expense for the period divided by total average interest-bearing liabilities during the period.

(8)Adjusted net interest yield is calculated based on annualized adjusted net interest income for the period divided by total average interest-earning assets for the period.

Table 3 displays the change in net interest income between periods and the extent to which the variance is attributable to:

(i) changes in the volume of our interest-earning assets and interest-bearing liabilities or (ii) changes in the interest rates of these assets and liabilities. The table also presents the change in adjusted net interest income between periods. Changes that are not solely due to either volume or rate are allocated to these categories on a pro-rata basis based on the absolute value of the change due to average volume and average rate.

12

Table 3: Rate/Volume Analysis of Changes in Interest Income/Interest Expense

Three Months Ended August 31, | ||||||||||||

2020 versus 2019 | ||||||||||||

Total | Variance Due To:(1) | |||||||||||

(Dollars in thousands) | Variance | Volume | Rate | |||||||||

Interest income: | ||||||||||||

Long-term fixed-rate loans | $ | 4,656 | $ | 14,564 | $ | (9,908 | ) | |||||

Long-term variable-rate loans | (5,356 | ) | (2,998 | ) | (2,358 | ) | ||||||

Line of credit loans | (7,791 | ) | (2,730 | ) | (5,061 | ) | ||||||

TDR loans | 1 | (17 | ) | 18 | ||||||||

Other, net | (1 | ) | — | (1 | ) | |||||||

Total loans | (8,491 | ) | 8,819 | (17,310 | ) | |||||||

Cash, time deposits and investment securities | (1,940 | ) | 1,061 | (3,001 | ) | |||||||

Total interest income | (10,431 | ) | 9,880 | (20,311 | ) | |||||||

Interest expense: | ||||||||||||

Short-term borrowings | (18,481 | ) | 2,353 | (20,834 | ) | |||||||

Medium-term notes | (2,189 | ) | 1,104 | (3,293 | ) | |||||||

Collateral trust bonds | (2,788 | ) | (4,564 | ) | 1,776 | |||||||

Guaranteed Underwriter Program notes payable | 1,980 | 6,453 | (4,473 | ) | ||||||||

Farmer Mac notes payable | (11,141 | ) | 242 | (11,383 | ) | |||||||

Other notes payable | (167 | ) | (123 | ) | (44 | ) | ||||||

Subordinated deferrable debt | 8 | 37 | (29 | ) | ||||||||

Subordinated certificates | (517 | ) | (473 | ) | (44 | ) | ||||||

Total interest expense | (33,295 | ) | 5,029 | (38,324 | ) | |||||||

Net interest income | $ | 22,864 | $ | 4,851 | $ | 18,013 | ||||||

Adjusted net interest income: | ||||||||||||

Interest income | $ | (10,431 | ) | $ | 9,880 | $ | (20,311 | ) | ||||

Interest expense | (33,295 | ) | 5,029 | (38,324 | ) | |||||||

Net periodic derivative cash settlements interest expense(2) | 15,929 | (1,542 | ) | 17,471 | ||||||||

Adjusted interest expense(3) | (17,366 | ) | 3,487 | (20,853 | ) | |||||||

Adjusted net interest income | $ | 6,935 | $ | 6,393 | $ | 542 | ||||||

____________________________

(1)The changes for each category of interest income and interest expense are divided between the portion of change attributable to the variance in volume and the portion of change attributable to the variance in rate for that category. The amount attributable to the combined impact of volume and rate has been allocated to each category based on the proportionate absolute dollar amount of change for that category.

(2)For the net periodic derivative cash settlements interest amount, the variance due to average volume represents the change in the net periodic derivative cash settlements interest amount resulting from the change in the average notional amount of derivative contracts outstanding. The variance due to average rate represents the change in the net periodic derivative cash settlements amount resulting from the net difference between the average rate paid and the average rate received for interest rate swaps during the period.

(3)See “Non-GAAP Financial Measures” for additional information on our adjusted non-GAAP measures.

Reported Net Interest Income

Reported net interest income of $100 million for the current quarter increased $23 million, or 30%, from the same prior-year quarter, driven by an increase in the net interest yield of 28 basis points, or 25%, to 1.42% and an increase in average interest-earning assets of 4%.

13

• | Net Interest Yield: The increase in the net interest yield of 28 basis points, or 25%, was largely due to a reduction in our average cost of borrowings of 61 basis points to 2.75%, partially offset by a decrease in the average yield on interest-earning assets of 31 basis points to 3.99%. The reduction in our average cost of borrowings was primarily driven by a decrease in the average cost of our short-term and variable-rate borrowings due to a decrease in short-term interest rates as the FOMC lowered the benchmark federal funds rate by 200 basis points over the last 12 months, including a 150 basis point reduction in March 2020 to a near zero target range of 0% to 0.25% as part of a series of measures implemented to ease the economic impact of the COVID-19 crisis. The average cost of our short-term borrowings decreased 213 basis points to 0.45% for the current quarter. The decrease in the average yield on interest-earning assets reflected the combined impact of a reduction in the average yield on our long-term fixed-rate loan portfolio, as the maturity and pay-off of loan advances at higher rates were replaced with new loan advances at lower rates due to the lower interest rate environment, and a reduction in the average yield on our long-term variable-rate and line of credit loan portfolios due to the decline in short-term interest rates over the last 12 months. |

• | Average Interest-Earning Assets: The increase in average interest-earning assets of 4% was primarily driven by growth in average total loans of $810 million, or 3%, largely attributable to an increase in average long-term fixed-rate loans of $1,248 million, or 5%, as the lower interest rate environment presented an opportunity for members to obtain advances to fund capital investments and refinance with us loans made by other lenders at a reduced fixed rate of interest. |

Adjusted Net Interest Income

Adjusted net interest income of $73 million for the current quarter increased $7 million, or 11%, from the same prior-year quarter, driven by an increase in the adjusted net interest yield of 7 basis points, or 7%, to 1.04%, and the increase in average interest-earning assets of $947 million, or 4%.

• | Adjusted Net Interest Yield: The increase in the adjusted net interest yield 7 basis points, or 7%, reflected the favorable impact of a reduction in our adjusted average cost of borrowings of 37 basis points to 3.16%, which was partially offset by the decrease in the average yield on interest-earning assets of 31 basis points to 3.99%. The reduction in our adjusted average cost of borrowings was largely attributable to the decrease in the average cost of our short-term and variable-rate borrowings and a partially offsetting increase in net periodic derivative cash settlements expense, both of which resulted from the decline in short-term interest rates over the last 12 months. As noted above, the decrease in the average yield on interest-earning assets reflected the combined impact of a reduction in the average yield on our long-term fixed-rate loan portfolio, as the maturity and pay-off of loan advances at higher rates were replaced with new loan advances at lower rates due to the lower interest rate environment, and a reduction in the average yield on our long-term variable-rate and line of credit loan portfolios from the decline in short-term interest rates over the last 12 months. |

• | Average Interest-Earning Assets: The increase in average interest-earning assets of 4% was primarily driven by the growth in average total loans of $810 million, or 3%. |

We include the net periodic derivative interest settlement amounts on our interest rate swaps in the calculation of our adjusted average cost of borrowings, which, as a result, also impacts the calculation of adjusted net interest income and adjusted net interest yield. We recorded net periodic derivative cash settlements interest expense of $27 million for the current quarter, an increase of $16 million from the $11 million recorded for the same prior-year quarter. Because our derivative portfolio consists of a higher proportion of pay-fixed swaps than receive-fixed swaps, we generally record derivative losses when interest rates decline and derivative gains when interest rates rise. The floating-rate payments on our interest rate swaps are typically based on the 3-month LIBOR, which decreased by 190 basis points over the last 12 months to 0.24% as of August 31, 2020. The decrease in the 3-month LIBOR drove the increase of $16 million in the net periodic derivative cash settlements interest expense recorded in the current quarter. See “Non-GAAP Financial Measures” for additional information on our adjusted measures, including a reconciliation of these measures to the most comparable GAAP measures.

14

Provision for Credit Losses

We recorded a provision for credit losses of less than $1 million for the current quarter under the CECL model for estimating our allowance for credit losses. We also recorded a provision for credit losses of less than $1 million for the same prior-year quarter under the incurred model for estimating our allowance for credit losses.

Under CECL, we are required to maintain an allowance based on a current estimate of credit losses that are expected to occur over the remaining contractual term of the loans in our portfolio. Prior to the adoption of CECL on June 1, 2020, we maintained an allowance based on an estimate of probable incurred losses inherent in our loan portfolio as of each balance sheet date.

As discussed above in “Executive Summary—Credit Quality,” the adoption of CECL resulted in an increase in our allowance for credit losses for our loan portfolio of $4 million and a corresponding decrease to retained earnings of $4 million recorded through a cumulative-effect adjustment. While the adoption of CECL had no impact on our earnings, subsequent to our adoption on June 1, 2020, lifetime expected credit losses for newly recognized loans, unadvanced loan commitments and financial guarantees, as well as changes during the period in our estimate of lifetime expected credit losses for existing financial instruments subject to CECL, will be recognized in earnings.

The allowance for credit losses for our loan portfolio increased to $57 million as of August 31, 2020, from $53 million as of May 31, 2020, and the allowance coverage ratio increased to 0.21% from 0.20%, primarily due to the increase in the allowance of $4 million recorded at adoption of CECL on June 1, 2020.

We discuss our methodology for estimating the allowance for credit losses under the CECL model in “Note 1—Summary of Significant Accounting Policies” of this Report. We also provide information on the allowance for credit losses below in the section “Credit Risk—Allowance for Credit Losses” and in “Note 5—Allowance for Credit Losses.”

Non-Interest Income

Non-interest income consists of fee and other income, gains and losses on derivatives not accounted for in hedge accounting relationships and gains and losses on equity and debt investment securities. In the fourth quarter of fiscal year 2020, we transferred all of the debt securities in our held-to-maturity investment portfolio to trading. As a result, we discontinued the reporting of our debt securities at amortized cost and began reporting these securities at fair value and recognizing the related unrealized gains and losses in earnings.

Table 4 presents the components of non-interest income (expense) for the three months ended August 31, 2020 and 2019.

Table 4: Non-Interest Income

Three Months Ended August 31, | ||||||||

(Dollars in thousands) | 2020 | 2019 | ||||||

Non-interest income: | ||||||||

Fee and other income | $ | 3,516 | $ | 10,941 | ||||

Derivative gains (losses) | 60,276 | (395,725 | ) | |||||

Investment securities gains | 4,659 | 1,620 | ||||||

Total non-interest income (loss) | $ | 68,451 | $ | (383,164 | ) | |||

The significant variance between non-interest income for the current quarter and the same prior-year quarter was attributable to the mark-to-market changes in the fair value of our derivative instruments. In addition, fee and other income decreased $7 million due to a reduction in prepayment fees.

Derivative Gains (Losses)

Our derivative instruments are an integral part of our interest rate risk management strategy. Our principal purpose in using derivatives is to manage our aggregate interest rate risk profile within prescribed risk parameters. The derivative instruments

15

we use primarily include interest rate swaps, which we typically hold to maturity. In addition, we may on occasion use treasury locks to manage the interest rate risk associated with debt that is scheduled to reprice in the future. The primary factors affecting the fair value of our derivatives and derivative gains (losses) recorded in our results of operations include changes in interest rates, the shape of the swap curve and the composition of our derivative portfolio. We generally do not designate our interest rate swaps, which currently account for all our derivatives, for hedge accounting. Accordingly, changes in the fair value of interest rate swaps are reported in our consolidated statements of operations under derivative gains (losses). However, we typically designate treasury locks as cash flow hedges. We did not have any derivatives designated as accounting hedges as of August 31, 2020 or May 31, 2020.

We currently use two types of interest rate swap agreements: (i) we pay a fixed rate of interest and receive a variable rate of interest (“pay-fixed swaps”); and (ii) we pay a variable rate of interest and receive a fixed rate of interest (“receive-fixed swaps”). The interest amounts are based on a specified notional balance, which is used for calculation purposes only. The benchmark variable rate for the substantial majority of the floating rate payments under our swap agreements is 3-month LIBOR. As interest rates decline, pay-fixed swaps generally decrease in value and result in the recognition of derivative losses, as the amount of interest we pay remains fixed, while the amount of interest we receive declines. In contrast, as interest rates rise, pay-fixed swaps generally increase in value and result in the recognition of derivative gains, as the amount of interest we pay remains fixed, but the amount we receive increases. With a receive-fixed swap, the opposite results occur as interest rates decline or rise. Because our pay-fixed and receive-fixed swaps are referenced to different maturity terms along the swap curve, different changes in the swap curve—parallel, flattening, inversion or steepening—will also impact the fair value of our derivatives.

Table 5 presents the components of net derivative gains (losses) recorded in our consolidated statements of operations for the three months ended August 31, 2020 and 2019. Derivative cash settlements interest expense represents the net periodic contractual interest amount for our interest-rate swaps during the reporting period. Derivative forward value gains (losses) represent the change in fair value of our interest rate swaps during the reporting period due to changes in expected future interest rates over the remaining life of our derivative contracts. We generally record derivative losses when interest rates decline and derivative gains when interest rates rise, as our derivative portfolio consists of a higher proportion of pay-fixed swaps than receive-fixed swaps.

Table 5: Derivative Gains (Losses)

Three Months Ended August 31, | ||||||||

(Dollars in thousands) | 2020 | 2019 | ||||||

Derivative gains (losses) attributable to: | ||||||||

Derivative cash settlements interest expense | $ | (26,972 | ) | $ | (11,043 | ) | ||

Derivative forward value gains (losses) | 87,248 | (384,682 | ) | |||||

Derivative gains (losses) | $ | 60,276 | $ | (395,725 | ) | |||

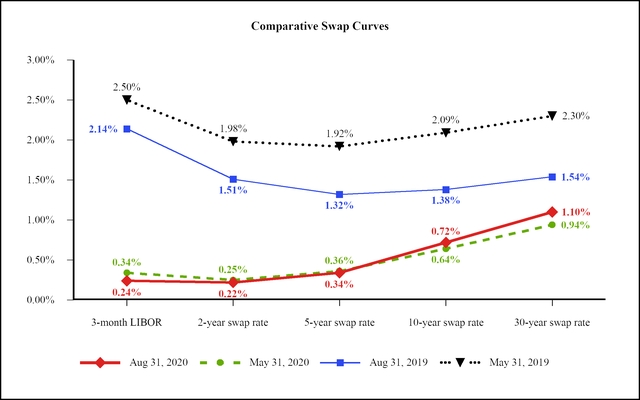

The net derivative gains of $60 million for the current quarter were due to a net increase in the fair value of our swap portfolio, primarily attributable to an increase in long-term swap interest rates as depicted by the August 31, 2020 and May 31, 2020 swap curves displayed below in the “Comparative Swap Curves” chart.

The net derivative losses of $396 million for the same prior-year quarter were due to a net decrease in the fair value of our swap portfolio, primarily attributable to a decline in interest rates across the swap curve, with medium- and longer-term interest rates experiencing a steeper decline than short-term rates as depicted by the August 31, 2019 and May 31, 2019 swap curves displayed below in the “Comparative Swap Curves” chart.

Pay-fixed swaps accounted for approximately 72% and 71% of the outstanding notional amount of our derivative portfolio as of August 31, 2020 and May 31, 2020, respectively. The profile of our derivative portfolio, however, may change as a result of changes in market conditions and actions taken to manage exposure to interest rate risk. The average remaining maturity of our pay-fixed and receive-fixed swaps was 19 years and four years, respectively, as of August 31, 2020. In comparison, the average remaining maturity of our pay-fixed and receive-fixed swaps was 18 years and four years, respectively, as of August 31, 2019.

16

Derivative Cash Settlements

As indicated in Table 5 above, we recorded net periodic derivative cash settlements interest expense of $27 million for the current quarter, an increase of $16 million from the $11 million recorded for the same prior-year quarter. The increase was driven by the decrease in the 3-month LIBOR of 190 basis points over the last 12 months to 0.24% as of August 31, 2020. Table 6 displays, by interest rate swap agreement type, the average notional amount outstanding and the weighted-average interest rate paid and received for the net periodic derivative cash settlements interest expense during each respective period.

Table 6: Derivative Cash Settlements Expense—Average Notional Amounts and Interest Rates

Three Months Ended August 31, | ||||||||||||||||||||

2020 | 2019 | |||||||||||||||||||

(Dollars in thousands) | Average Notional Balance | Weighted- Average Rate Paid | Weighted- Average Rate Received | Average Notional Balance | Weighted- Average Rate Paid | Weighted- Average Rate Received | ||||||||||||||

Pay-fixed swaps | $ | 6,579,420 | 2.78 | % | 0.38 | % | $ | 7,353,402 | 2.84 | % | 2.39 | % | ||||||||

Receive-fixed swaps | 2,646,826 | 1.21 | 2.76 | 3,399,000 | 3.09 | 2.56 | ||||||||||||||

Total | $ | 9,226,246 | 2.33 | % | 1.06 | % | $ | 10,752,402 | 2.92 | % | 2.44 | % | ||||||||

Comparative Swap Curves

The chart below provides comparative swap curves as of August 31, 2020, May 31, 2020, August 31, 2019 and May 31, 2019.

____________________________

Benchmark rates obtained from Bloomberg.

See “Note 9—Derivative Instruments and Hedging Activities” for additional information on our derivative instruments.

17

Non-Interest Expense

Non-interest expense consists of salaries and employee benefit expense, general and administrative expenses, gains and losses on the early extinguishment of debt and other miscellaneous expenses.

Table 7 presents the components of non-interest expense recorded in our consolidated statements of operations for the three months ended August 31, 2020 and 2019.

Table 7: Non-Interest Expense

Three Months Ended August 31, | ||||||||

(Dollars in thousands) | 2020 | 2019 | ||||||

Non-interest expense: | ||||||||

Salaries and employee benefits | $ | (13,133 | ) | $ | (12,942 | ) | ||

Other general and administrative expenses | (9,530 | ) | (12,387 | ) | ||||

Other non-interest (expense) income | (332 | ) | 7,179 | |||||

Total non-interest expense | $ | (22,995 | ) | $ | (18,150 | ) | ||

Non-interest expense of $23 million for the current quarter increased $5 million, or 27%, from the same prior-year quarter, primarily due to the absence of a gain of $8 million recorded in connection with the sale of land in the same prior-year quarter.

Net Income (Loss) Attributable to Noncontrolling Interests

Net income (loss) attributable to noncontrolling interests represents 100% of the results of operations of NCSC and RTFC, as the members of NCSC and RTFC own or control 100% of the interest in their respective companies. The fluctuations in net income (loss) attributable to noncontrolling interests are primarily due to changes in the fair value of NCSC’s derivative instruments recognized in NCSC’s earnings.

We recorded net income attributable to noncontrolling interests of less than $1 million for the current quarter, compared with a net loss of $2 million for the same prior-year quarter.

CONSOLIDATED BALANCE SHEET ANALYSIS |

Total assets of $28,263 million as of August 31, 2020 increased $105 million from May 31, 2020, primarily due to growth in our loan portfolio. Total liabilities of $27,531 million as of August 31, 2020 was relatively unchanged from May 31, 2020. Total equity increased $83 million to $732 million as of August 31, 2020, attributable to our reported net income of $145 million for the current quarter, which was partially offset by the retirement of patronage capital of $60 million authorized by the CFC Board of Directors during the current quarter and a decrease to retained earnings of $4 million from the cumulative-effect adjustment recorded at adoption of the CECL accounting standard on June 1, 2020.