Attached files

| file | filename |

|---|---|

| EX-4.7 - DESCRIPTION OF SECURITIES REGISTERED PURSUANT TO SECTION 12 OF THE SECURITIES EX - East Stone Acquisition Corp | f10k2020ex4-7_eaststone.htm |

| EX-32.2 - CERTIFICATION - East Stone Acquisition Corp | f10k2020ex32-2_eaststone.htm |

| EX-32.1 - CERTIFICATION - East Stone Acquisition Corp | f10k2020ex32-1_eaststone.htm |

| EX-31.2 - CERTIFICATION - East Stone Acquisition Corp | f10k2020ex31-2_eaststone.htm |

| EX-31.1 - CERTIFICATION - East Stone Acquisition Corp | f10k2020ex31-1_eaststone.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2020

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-39233

East Stone Acquisition Corporation

(Exact name of registrant as specified in its charter)

| British Virgin Islands | N/A | |

| (State or other jurisdiction of | (IRS Employer | |

| incorporation or organization) | Identification No.) | |

25 Mall Road, Suite 330 Burlington, MA |

01803 | |

| (Address of principal executive offices) | (Zip Code) |

(781) 202-9128

(Registrant’s telephone number, including area code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Units, each consisting of one Ordinary Share, one Right and one Warrant | ESSCU | The Nasdaq Stock Market LLC | ||

| Ordinary Shares, no par value | ESSC | The Nasdaq Stock Market LLC | ||

| Rights, exchangeable into one-tenth of one Ordinary Share | ESSCR | The Nasdaq Stock Market LLC | ||

| Warrants, each exercisable for one-half of one Ordinary Share, each whole Ordinary Share exercisable for $11.50 per share | ESSCW | The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☒ No ☐

As of December 31, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, the registrant’s securities were not publicly traded. The registrant’s units began trading on The Nasdaq Capital Market on February 20, 2020 and the registrant’s ordinary shares, warrants and rights began trading on The Nasdaq Capital Market on March 17, 2020. The aggregate market value of the ordinary shares outstanding, other than shares held by persons who may be deemed affiliates of the registrant, computed by reference to the closing sales price for the ordinary shares on June 30, 2020, as reported on the Nasdaq Capital Market, was $138,892,890. Ordinary shares held by each officer and director and by each person known to the registrant who owned 10% or more of the outstanding voting and non-voting ordinary shares have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of September 17, 2020, there were 17,703,500 ordinary shares, no par value, of the registrant issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

i

Unless otherwise stated in this annual report on Form 10-K:

| ● | references to “we,” “us,” “the Company” or “our company” refer to East Stone Acquisition Corporation, a BVI business company with limited liability; |

| ● | references to our “anchor investors” refer to Hua Mao and Cheng Zhao, who purchased our anchor units; |

| ● | references to our “anchor units” refer to an aggregate of 108,000 units we sold to the anchor investors simultaneously with the closing of our initial public offering; |

| ● | references to the “BVI” refer to the British Virgin Islands; |

| ● | references to the “Companies Act” and the “Insolvency Act” refer to the BVI Business Companies Act, 2004 and the Insolvency Act, 2003 of the British Virgin Islands, respectively and in each case as amended; |

| ● | references to “founder shares” refer to the 3,450,000 ordinary shares currently held by the initial shareholders (as defined below); |

| ● | references to “I-Bankers” refer I-Bankers Securities, Inc.; |

| ● | references to the “I-Bankers units” or “representative units” refer to the 75,000 private units we sold privately to I-Bankers and/or its designees simultaneously with the closing of our initial public offering; |

| ● | references to our “initial shareholders” refer to our sponsor (as defined below), Navy Sail International Limited, a BVI business company with limited liability, of which our Chairman and Chief Financial Officer, Mr. Chunyi (Charlie) Hao, is the sole director, and any of our officers or directors that hold founder shares; |

| ● | references to our “insider units” refer to the 167,000 units we sold privately to our sponsor and/or its designees simultaneously with the closing of our initial public offering; |

| ● | references to our “management” or our “management team” refer to our officers and directors; |

| ● | references to “private units” refer to the insider units, the anchor units and the I-Bankers units; |

| ● | references to “ordinary shares” refer to the ordinary shares of no par value in our company; |

| ● | references to “private shares,” “private rights” and “private warrants” refer to the ordinary shares, rights and warrants, respectively, included within the private units; |

| ● | references to “public rights” refer to the rights sold as part of the units in our initial public offering (whether they were subscribed for in our initial public offering or in the open market); |

| ● | references to our “public shares” refer to ordinary shares sold as part of the units in our initial public offering (whether they were purchased in our initial public offering or thereafter in the open market) and references to “public shareholders” refer to the holders of our public shares, including our initial shareholders to the extent our initial shareholders purchase public shares, provided that their status as “public shareholders” shall exist only with respect to such public shares; |

| ● | references to our “public warrants” refer to the redeemable warrants sold as part of the units in our initial public offering (whether they were subscribed for in our initial public offering or in the open market); |

| ● | references to “public units” refer to the units in our initial public offering (whether they were subscribed for in our initial public offering or in the open market); |

| ● | references to our “rights” refers to the rights sold as part of the units in our initial public offering as well as the concurrent private placement; |

| ● | references to our “sponsor” refer to Double Ventures Holdings Limited, a BVI business company with limited liability, the sole director of which is Chunyi (Charlie) Hao, our Chairman and Chief Financial Officer; and |

| ● | references to our “warrants” refer to our redeemable warrants, which includes the public warrants as well as the private warrants and warrants underlying units issued upon conversion of working capital loans to the extent they are no longer held by the initial purchasers of the private warrants or members of our management team (or their permitted transferees), in each case after our initial business combination. |

ii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report, including, without limitation, statements under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements can be identified by the use of forward-looking terminology, including the words “believes,” “estimates,” “anticipates,” “expects,” “intends,” “plans,” “may,” “will,” “potential,” “projects,” “predicts,” “continue,” or “should,” or, in each case, their negative or other variations or comparable terminology. There can be no assurance that actual results will not materially differ from expectations. Such statements include, but are not limited to, any statements relating to our ability to consummate any acquisition or other business combination and any other statements that are not statements of current or historical facts. These statements are based on management’s current expectations, but actual results may differ materially due to various factors, including, but not limited to:

| ● | our ability to complete our initial business combination; |

| ● | our success in retaining or recruiting, or changes required in, our officers, key employees or directors following our initial business combination; |

| ● | our officers and directors allocating their time to other businesses and potentially having conflicts of interest with our business or in approving our initial business combination, as a result of which they would then receive expense reimbursements; |

| ● | our potential ability to obtain additional financing to complete our initial business combination; |

| ● | the ability of our officers and directors to generate a number of potential acquisition opportunities; | |

| ● | our pool of prospective target businesses; |

| ● | the ability of our officers and directors to generate a number of potential acquisition opportunities; |

| ● | our public securities’ potential liquidity and trading; |

| ● | the lack of a market for our securities; |

| ● | the use of proceeds not held in the trust account or available to us from interest income on the trust account balance; or |

| ● | our financial performance. |

The forward-looking statements contained in this report are based on our current expectations and beliefs concerning future developments and their potential effects on us. Future developments affecting us may not be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors.” Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

iii

Overview

We are an early stage blank check company recently incorporated as a British Virgin Islands business company and formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses, which we refer to throughout this report as our initial business combination. Although we are not limited to a particular industry or geographic region for purposes of consummating an initial business combination, we intend to focus on businesses primarily operating in the financial services industry or businesses providing technological services to the financial industry, commonly known as fintech, in North America and Asia-Pacific.

We believe the financial services industry has experienced a significant amount of change over the last several years as new companies providing technology, software, and digital platforms have entered the market. According to an article titled “Global Fintech Investment Hits Record $111.8B in 2018” published by KPMG in February 2019, there was over $31 billion invested in fintech companies in 2017 alone. Fintech companies exist across many industries within financial services, including banking technology, payment and financial transaction processing, capital markets, wealth management, insurance, and financial management systems. We believe that fintech companies have proven to be successful with multiple business models and strategic objectives. The objective of fintech companies can range from improving the efficiency of traditional financial services companies, to introducing new products and creating new markets, to those focused on disrupting traditional financial services companies with competitive products. Fintech is impacting the financial services sector broadly in the following aspect:

| ● | Fintech companies tend to snatch away the revenues of traditional financial institutions and force them to be more competitive and vibrant; |

| ● | Technology disrupts the logic of traditional financial institutions and empowers them to adjust their strategic direction; |

| ● | Electronic channel services occupy the entrance, driving traditional financial institutions to achieve full channel integration and coordination; |

| ● | Innovations in fintech companies have sprung up, inspiring traditional financial institutions to innovate their business models; |

| ● | Business innovation drives management innovation, forcing traditional financial institutions to reform their organizational model and IT architecture. |

We intend to capitalize on the ability of our management team and the broad network our management team and members of the board of directors have built up over their respective professional career to identify, acquire, and operate a business in the proposed business of our initial business combination that may provide opportunities for attractive long-term risk-adjusted returns, though we reserve the right to pursue an acquisition opportunity in any business or industry.

Business Strategy

Our business strategy is to utilize our management team’s past to identify and complete our initial business combination with a company that our management believes, with proper utilization of our network and experience, has compelling potential for value creation.

We believe our management team and members of our board have experience in:

| ● | Operating companies, setting and changing strategies, and identifying, mentoring and recruiting exceptional talent; |

| ● | Developing and growing companies, both organically and through strategic transactions and acquisitions, and expanding the product range and geographic footprint of a number of target businesses; |

1

| ● | Investing in leading private and public technology companies to accelerate their growth and maturation; and |

| ● | Accessing the capital markets, including financing businesses and helping companies transition to public ownership. |

Market Opportunity

Although we are not limited to a particular industry or geographic region for purposes of consummating an initial business combination, we intend to focus on businesses within the fintech business with an overall transaction value between $300 million and $1.0 billion. Broadly, fintech can refer to any innovation in how people transact business, from money transfers, check deposit over smartphone, bypassing a bank for credit application, loaning money for small business instantly, or investing into money market fund without in-person assistance. According to “2018 US Fintech Market Report” by S&P Global, capital has been pouring into the fintech industry where payments, insurance technology, investment and capital technology, digital lending, banking technology and financial media are taking the center stage. As indicated in the article titled Global Fintech Investment Hits Record $111.8B in 2018 by KPMG, global fintech investment in 2018 reached $111.8 billion with investment in Asia taking the lead up to $22.7 billion. The chart below presents an evolved ecosystem of financial services.

Source: Capgemini Financial Services Analysis, 2019

2

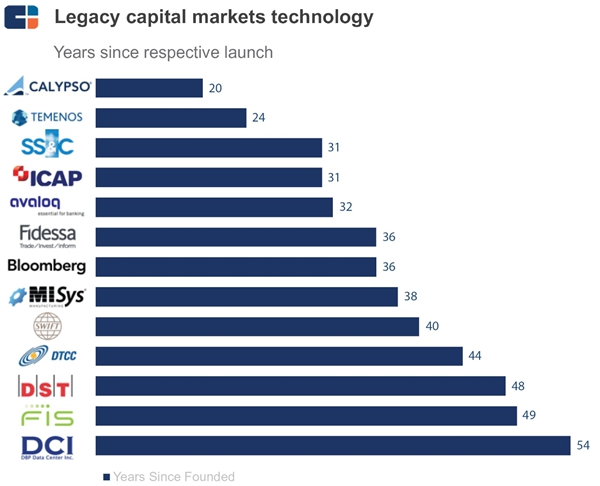

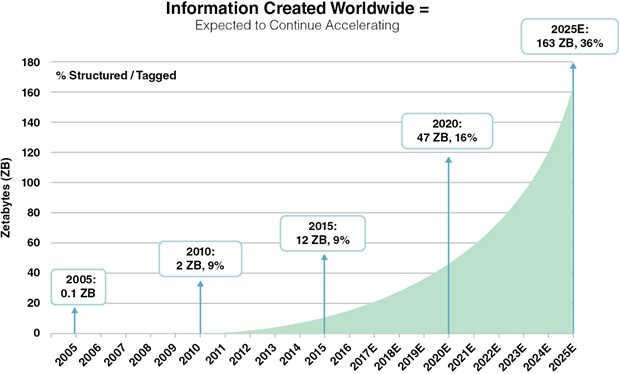

Investment in core and infrastructure technology for the financial services sector is needed to keep pace with innovation. According to the CB Report, the capital markets ecosystem suffers from a current over-reliance on legacy technologies, which are on average 38 years old. In contrast, the “information explosion” is causing increasing challenges with the management of data and information, as shown in the charts below.

Source: Global Intech Report Q3 2019 by CB Insight

3

Source: IDC “Data Age 2025 Study” (sponsored by Seagate)

4

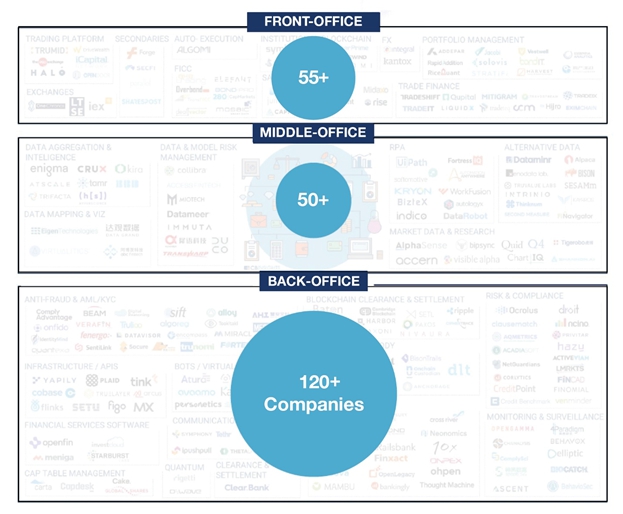

The rapid evolution of the capital markets technology landscape has translated into significant investment in companies focused on back-office applications and functions, as indicated by the number of capital investments made in the front office, middle office and back office within the same time frame in the chart below.

Source: Global Intech Report Q3 2019 by CB Insight

We have not narrowed our business combination target in any particular fintech business, however, we do believe the following areas of the fintech business are exposed to exponential growth.

Online Lending. Online lending based on big data analytics has grown where traditional bank lending fails to cover or under covers. Around 2 billion people worldwide are unbanked, ignored or technically not accessible by traditional banks or mainstream financial services companies, per Accenture analysis of World Bank and UN figures in its May 2017 report titled Fintech — Did Someone Cancel the Revolution. Those who are ignored or out of reach by traditional financial services are being served by advanced online lending technologies.

Big Data, Cloud Computing and Credit Analytics. Big data powered by cloud computing provides financial lenders the power to enhance credit rating and credit risk control. Bid data opens up a frontier to financial institutions to service those unbanked and/or underbanked customers.

Mobile Phone Payment. Mobile phone payment has been deployed quickly where cash payment can be eliminated creating fast and efficient transactions. However, smart phone payment is regulated differently in different countries by their respective financial authorities causing deployment of the technology unevenly worldwide.

Smart Contract. Smart contract utilizes computer programs, often in block chain, to automatically execute contracts between two or more parties in a variety of business in financial services, commercial transactions, B to B services, or B to C services, in lending, loan repayment, mortgaging, reducing costs in the conventional flow of documents and enhancing accuracy and security of the flow of documents.

5

Insurtech. Insurtech is short for “insurance technology.” It represents the emergence of new technologies that are transforming the insurance industry by reducing costs for consumers and insurance companies, improving efficiency, and enhancing customer satisfaction. Insurtech is seen to be a disruptor to the property and casualty homogenous insurance segment. Mass computing ability, scenario-based setting and growth are key strengths of Insurtech companies. Insurtech incorporates AI and online-to-offline (O2O) integration by tapping into casualty P&C homogeneous-like auto insurance and health insurance segments.

Insurtech has been applied in areas such as AI-powered anti-fraud solutions for the P&C insurance industry. Insurtech provides a digitized platform allowing customers to acquire all of their P&C in one place, suitable to small businesses. This digitalized market place is designed to improve insurance agency processes and efficiency.

According to KPMG’s March 2019 report titled “Insurtech 10: Trends for 2019,” insurtech trends in the arears of digital risk reduction, digitizing customers, behaviorial science, AI and machine learning, vehicle-focused coverage (as opposed to driver-focused insurance), and big data.

As reported by Insurance Journal in May 2019, more than $1 billion was invested in 85 insurtech deals in the first quarter of 2019.

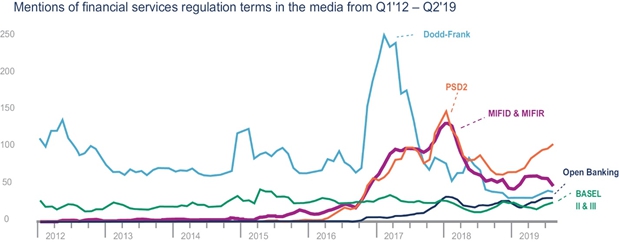

According to a March 2019 report titled Regulation and Supervision of Fintech by KPMG, fintech is moving from “under the regulatory” and is attracting growing responses and supervisory scrutiny, and according to the CB Report, the regulatory landscape is more complex than ever, giving rise to new business opportunities. The chart below presents the number of mentions of financial service regulation terms in the media from the beginning of 2012 to the first half of 2019.

Acquisition Criteria

We seek to identify companies that have compelling market presence and a combination of the following characteristics. We use these criteria and guidelines in evaluating acquisition opportunities, but we may decide to enter our initial business combination with a target business that does not meet these criteria and guidelines. We intend to acquire companies or assets that we believe have the following attributes:

| ● | Strong and noticeable presence in its market. We intend to focus on investment in an industry segment that has a noticeable presence in its market; |

| ● | First mover in its niche market. When pursuing our business combination, we look for targets that are early leaders in their niche market and which set trends in their products and/or services; |

| ● | Differentiated products or services. A company with differentiated products or services offers investors a long term investment opportunity and we certainly spend time and resources to assess our business combination in this regard; |

6

| ● | Seasoned management team. We intend to spend significant time assessing a company’s leadership and personnel and evaluating what we can do to augment and/or upgrade the team over time if needed; |

| ● | Widely-applicable technology & scalable model offering appealing growth potential. Our management believes that technology-driven solutions that are widely applicable and scalable have a unique window of opportunity to create advantages that will grow with the industry; |

| ● | Stable and reputable customer base. We seek target businesses that have a stable and reputable customer base, with systematic advantages which are generally able to employ risk management measures to endure economic downturns, industry consolidation, changing business preferences and other unfavorable business environments that may negatively impact their customers, suppliers and competitors. |

These criteria are not intended to be exhaustive. Any evaluation relating to the merits of a particular initial business combination may be based, to the extent relevant, on these general guidelines as well as other considerations, factors and criteria that our management may deem relevant.

Status as a Public Company

We believe our structure makes us an attractive business combination partner to target businesses. As an existing public company, we offer a target business an alternative to the traditional initial public offering through a merger or other business combination. In this situation, the owners of the target business would exchange their shares of stock in the target business for shares of our stock or for a combination of shares of our stock and cash, allowing us to tailor the consideration to the specific needs of the sellers. Although there are various costs and obligations associated with being a public company, we believe target businesses will find this method a more certain and cost effective method to becoming a public company than the typical initial public offering. In a typical initial public offering, there are additional expenses incurred in marketing, road show and public reporting efforts that may not be present to the same extent in connection with a business combination with us.

Furthermore, once a proposed business combination is completed, the target business will have effectively become public, whereas an initial public offering is always subject to the underwriters’ ability to complete the offering, as well as general market conditions, which could delay or prevent the offering from occurring or could have negative valuation consequences. Once public, we believe the target business would then have greater access to capital and an additional means of providing management incentives consistent with shareholders’ interests. It can offer further benefits by augmenting a company’s profile among potential new customers and vendors and aid in attracting talented employees.

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act, as modified by the JOBS Act. As such, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a non-binding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. If some investors find our securities less attractive as a result, there may be a less active trading market for our securities and the prices of our securities may be more volatile.

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We intend to take advantage of the benefits of this extended transition period.

We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following February 24, 2025, (b) in which we have total annual gross revenue of at least $1.07 billion, or (c) in which we are deemed to be a large accelerated filer, which means the market value of our ordinary shares that is held by non-affiliates exceeds $700 million on the last day of the second fiscal quarter of any given fiscal year, and (2) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the prior three-year period.

7

Financial Position

With a trust account in the amount of $138,826,973 as of June 30, 2020, we can offer a target business a variety of options to facilitate a business combination and fund future expansion and growth of its business. This amount is after payments of $402,500 to the underwriters in our initial public offering for deferred underwriting commissions and $3,795,000 to I-Bankers, the representative of the underwriters, for certain business combination-related advisory fees. Because we are able to consummate a business combination using the cash proceeds from our initial public offering, our share capital, debt or a combination of the foregoing, we have the flexibility to use an efficient structure allowing us to tailor the consideration to be paid to the target business to address the needs of the parties. However, if a business combination requires us to use substantially all of our cash to pay for the purchase price, we may need to arrange third party financing to help fund our business combination. Since we have no specific business combination under consideration, we have not taken any steps to secure third party financing. Accordingly, our flexibility in structuring a business combination may be subject to these constraints.

Effecting Our Initial Business Combination

We are not presently engaged in, and we will not engage in, any operations for an indefinite period of time. We intend to complete our initial business combination using cash from the proceeds of our initial public offering and the private placement of the private placement units, our capital stock, debt or a combination of these as the consideration to be paid in our initial business combination. We may seek to complete our initial business combination with a company or business that may be financially unstable or in its early stages of development or growth, which would subject us to the numerous risks inherent in such companies and businesses, although we will not be permitted to effectuate our initial business combination with another blank check company or a similar company with nominal operations.

If our initial business combination is paid for using equity or debt securities, or not all of the funds released from the trust account are used for payment of the consideration in connection with our business combination or used for redemptions of our ordinary shares, we may apply the balance of the cash released to us from the trust account for general corporate purposes, including for maintenance or expansion of operations of the post-transaction company, the payment of principal or interest due on indebtedness incurred in completing our initial business combination, to fund the purchase of other assets, companies or for working capital.

We may seek to raise additional funds through a private offering of debt or equity securities in connection with the completion of our initial business combination (which may include a specified future issuance), and we may complete our initial business combination using the proceeds of such offering rather than using the amounts held in the trust account. Subject to compliance with applicable securities laws, we would expect to complete such financing only simultaneously with the completion of our business combination. In the case of an initial business combination funded with assets other than the trust account assets, our tender offer documents or proxy materials disclosing the business combination would disclose the terms of the financing and, only if required by law, we would seek shareholder approval of such financing. There are no prohibitions on our ability to raise funds privately, including pursuant to any specified future issuance, or through loans in connection with our initial business combination.

The time required to select and evaluate a target business and to structure and complete our initial business combination, and the costs associated with this process, are not currently ascertainable with any degree of certainty. Any costs incurred with respect to the identification and evaluation of a prospective target business with which our business combination is not ultimately completed will result in our incurring losses and will reduce the funds we can use to complete another business combination.

Sources of Target Businesses

We expect to receive a number of proprietary transaction opportunities to originate as a result of the business relationships, direct outreach, and deal sourcing activities from the network built up by our management team and by the members of our Board. We also anticipate that target business candidates will be brought to our attention from various unaffiliated sources, including investment banking firms, consultants, accounting firms, private equity groups, large business enterprises, and other market participants. These sources may also introduce us to target businesses in which they think we may be interested on an unsolicited basis, since many of these sources will have read this report and know what types of businesses we are targeting. Some of our officers and directors may enter into employment or consulting agreements with the post-transaction company following our initial business combination. The presence or absence of any such fees or arrangements will not be used as a criterion in our selection process of an acquisition candidate. In no event will our sponsor or any of our existing officers or directors, or any entity with which they are affiliated, be paid any finder’s fee, consulting fee or other compensation prior to, or for any services they render in order to effectuate, the completion of our initial business combination (regardless of the type of transaction that it is).

8

We are not prohibited from pursuing an initial business combination with a business combination target that is affiliated with our sponsor, officers or directors. In the event we seek to complete our initial business combination with a business combination target that is affiliated with our sponsor, officers or directors, we, or a committee of independent directors, would obtain an opinion from an independent investment banking firm which is a member of FINRA or an independent accounting firm that such an initial business combination is fair to our company from a financial point of view. We are not required to obtain such an opinion in any other context. If any of our officers or directors becomes aware of a business combination opportunity that falls within the line of business of any entity to which he or she has pre-existing fiduciary or contractual obligations, he or she may be required to present such business combination opportunity to such entity prior to presenting such business combination opportunity to us.

Lack of Business Diversification

For an indefinite period of time after the completion of our initial business combination, the prospects for our success may depend entirely on the future performance of a single business. Unlike other entities that have the resources to complete business combinations with multiple entities in one or several industries, it is probable that we will not have the resources to diversify our operations and mitigate the risks of being in a single line of business. In addition, we intend to focus our search for an initial business combination in a single industry. By completing our business combination with only a single entity, our lack of diversification may:

| ● | subject us to negative economic, competitive and regulatory developments, any or all of which may have a substantial adverse impact on the particular industry in which we operate after our initial business combination, and |

| ● | cause us to depend on the marketing and sale of a single product or limited number of products or services. |

Limited Ability to Evaluate the Target’s Management Team

Although we intend to closely scrutinize the management of a prospective target business when evaluating the desirability of effecting our business combination with that business, our assessment of the target business’ management may not prove to be correct. In addition, the future management may not have the necessary skills, qualifications or abilities to manage a public company. Furthermore, the future role of members of our management team or of our board, if any, in the target business cannot presently be stated with any certainty. While it is possible that one or more of our directors will remain associated in some capacity with us following our business combination, it is presently unknown if any of them will devote their full efforts to our affairs subsequent to our business combination. Moreover, we cannot assure you that members of our management team will have significant experience or knowledge relating to the operations of the particular target business. The determination as to whether any members of our board of directors will remain with the combined company will be made at the time of our initial business combination.

Following a business combination, to the extent that we deem it necessary, we may seek to recruit additional managers to supplement the incumbent management team of the target business. We cannot assure you that we will have the ability to recruit additional managers, or that additional managers will have the requisite skills, knowledge or experience necessary to enhance the incumbent management.

Selection of a Target Business and Structuring of a Business Combination

Subject to the requirement that, so long as our securities are listed on Nasdaq, our initial business combination must be with one or more target businesses or assets having an aggregate fair market value of at least 80% of the value of the trust account (less any deferred underwriting commissions, certain advisory fees to I-Bankers and taxes payable on interest earned and less any interest earned thereon that is released to us for taxes) at the time of the agreement to enter into such initial business combination, our management have virtually unrestricted flexibility in identifying and selecting one or more prospective target businesses, although we are not permitted to effectuate our initial business combination with another blank check company or a similar company with nominal operations. In any case, we will only consummate an initial business combination in which we become the majority shareholder of the target (or control the target through contractual arrangements in limited circumstances for regulatory compliance purposes as discussed below) or are otherwise not required to register as an investment company under the Investment Company Act. To the extent we effect our initial business combination with a company or business that may be financially unstable or in its early stages of development or growth, we may be affected by numerous risks inherent in such company or business. Although our management endeavor to evaluate the risks inherent in a particular target business, we may not properly ascertain or assess all significant risk factors.

9

In evaluating a prospective target business, we have conducted and will continue to conduct an extensive due diligence review which encompasses, among other things, meetings with incumbent management and inspection of facilities, as well as review of financial and other information which is made available to us. This due diligence review are conducted either by our management or by unaffiliated third parties we may engage, although we have no current intention to engage any such third parties.

The time and costs required to select and evaluate a target business and to structure and complete the business combination cannot presently be ascertained with any degree of certainty. Any costs incurred with respect to the identification and evaluation of a prospective target business with which a business combination is not ultimately completed will result in a loss to us and reduce the amount of capital available to otherwise complete a business combination.

Fair Market Value of Target Business or Businesses

So long as our securities are listed on Nasdaq, the target business or businesses or assets with which we effect our initial business combination must have a collective fair market value equal to at least 80% of the value of the trust account (less any deferred underwriting commissions, certain advisory fees to I-Bankers and taxes payable on interest earned and less any interest earned thereon that is released to us for taxes) at the time of the agreement to enter into such initial business combination. So long as our securities are listed on Nasdaq, if we acquire less than 100% of one or more target businesses in our initial business combination, the aggregate fair market value of the portion or portions we acquire must equal at least 80% of the value of the trust account (less any deferred underwriting commissions, certain advisory fees to I-Bankers and taxes payable on interest earned and less any interest earned thereon that is released to us for taxes) at the time of the agreement to enter into such initial business combination. However, we will always acquire at least a controlling interest in a target business. The fair market value of a portion of a target business or assets will likely be calculated by multiplying the fair market value of the entire business by the percentage of the target we acquire. We may seek to consummate our initial business combination with an initial target business or businesses with a collective fair market value in excess of the balance in the trust account. In order to consummate such an initial business combination, we may issue a significant amount of debt, equity or other securities to the sellers of such business and/or seek to raise additional funds through a private offering of debt, equity or other securities (although our memorandum and articles of association provides that we may not issue securities that can vote with ordinary shareholders on matters related to our pre-initial business combination activity). If we issue securities in order to consummate such an initial business combination, our shareholders could end up owning a minority of the combined company’s voting securities as there is no requirement that our shareholders own a certain percentage of our company (or, depending on the structure of the initial business combination, an ultimate parent company that may be formed) after our business combination. Since we have no specific business combination under consideration, we have not entered into any such arrangement to issue our debt or equity securities and have no current intention of doing so.

We anticipate structuring our initial business combination to acquire 100% of the equity interest or assets of the target business or businesses. We may, however, structure our initial business combination to acquire less than 100% of such interests or assets of the target business, but we will only consummate such business combination if we will become the majority shareholder of the target (or control the target through contractual arrangements in limited circumstances for regulatory compliance purposes) or are otherwise not required to register as an “investment company” under the Investment Company Act. Even though we will own a majority interest in the target, our shareholders prior to the business combination may collectively own a minority interest in the post business combination company, depending on valuations ascribed to the target and us in the business combination transaction. For example, we could pursue a transaction in which we issue a substantial number of new shares in exchange for all of the outstanding capital stock of a target. In this case, we would acquire a 100% controlling interest in the target. However, as a result of the issuance of a substantial number of new shares, our shareholders immediately prior to our initial business combination could own less than a majority of our outstanding shares subsequent to our initial business combination.

10

The fair market value of a target business or businesses or assets will be determined by our board of directors based upon standards generally accepted by the financial community, such as actual and potential gross margins, the values of comparable businesses, earnings and cash flow, book value and, where appropriate, upon the advice of appraisers or other professional consultants. If our board of directors is not able to independently determine that the target business or assets has a sufficient fair market value to meet the threshold criterion, we will obtain an opinion from an unaffiliated, independent investment banking firm or an independent accounting firm with respect to the satisfaction of such criterion. Notwithstanding the foregoing, unless we consummate a business combination with an affiliated entity, we are not required to obtain an opinion from an independent investment banking firm or an independent accounting firm that the price we are paying is fair to our shareholders.

Shareholders May Not Have the Ability to Approve Our Initial Business Combination

Although we may seek shareholder approval before we effect our initial business combination, we may not do so for business or legal reasons (so long as such transaction does not require shareholder approval under the Companies Act or the rules of Nasdaq). Presented in the table below is a graphic explanation of the types of initial business combinations we may consider and whether we expect shareholder approval would be required under the Companies Act for each such transaction.

| Type of Transaction | Whether Shareholder Approval is Required | |

| Purchase of assets | No | |

| Purchase of stock of target not involving a merger with the company | No | |

| Merger of target with a subsidiary of the company | No | |

| Merger of the company with a target | Yes | |

| Entering into contractual agreements with a target to obtain control | No |

Additionally, under Nasdaq’s listing rules, shareholder approval would be required for our initial business combination if, for example:

| ● | we issue ordinary shares that will be equal to or in excess of 20% of the number of ordinary shares then outstanding (other than in a public offering); |

| ● | any of our directors, officers or substantial shareholders (as defined by Nasdaq rules) has a 5% or greater interest (or such persons collectively have a 10% or greater interest), directly or indirectly, in the target business or assets to be acquired or otherwise and the present or potential issuance of ordinary shares could result in an increase in outstanding ordinary shares or voting power of 5% or more; or |

| ● | the issuance or potential issuance of ordinary shares will result in our undergoing a change of control. |

We also may be required to obtain shareholder approval if we wish to take certain actions in connection with our initial business combination such as adopting an incentive stock plan or amending our charter. So long as we maintain a listing of our securities on Nasdaq, we are required to comply with such rules.

Ability to Extend Time to Complete Business Combination

We have until May 24, 2021 to consummate our initial business combination. However, if we anticipate that we may not be able to consummate our initial business combination by May 24, 2021, we may, by resolution of our board if requested by our sponsor, extend such date to consummate a business combination up to two times, each by an additional three months (up until November 24, 2021 to complete a business combination), subject to the sponsor depositing additional funds into the trust account as set out below. Pursuant to the terms of our amended and restated memorandum and articles of association and the trust agreement entered into between us and Continental Stock Transfer & Trust Company, LLC, in order to extend the time available for us to consummate our initial business combination, our initial shareholders or their affiliates or designees, upon five days advance notice prior to the applicable deadline, must deposit into the trust account for each three-month extension $1,380,000 (or $0.10 per share) on or prior to the date of the applicable deadline, up to an aggregate of $2,760,000, or approximately $0.20 per share. In the event that we receive notice from our sponsor five days prior to the applicable deadline of its wish for us to effect an extension, we intend to issue a press release announcing such intention at least three days prior to the applicable deadline. In addition, we intend to issue a press release the day after the applicable deadline announcing whether or not the funds had been timely deposited. Our sponsor and its affiliates or designees are not obligated to fund the trust account to extend the time for us to complete our initial business combination.

11

Redemption Rights for Public Shareholders upon Consummation of Our Initial Business Combination

We will provide our public shareholders with the opportunity to redeem all or a portion their shares upon the consummation of our initial business combination at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the trust account, including interest (net of taxes payable), divided by the number of then outstanding public shares, subject to the limitations described herein. The amount in the trust account as of June 30, 2020 is approximately $10.00 per share (subject to increase of up to an additional approximately $0.20 per share in the event that our sponsor elects to extend such date to consummate a business combination, as described in more detail in this report). The per-share amount we will distribute to investors who properly redeem their shares will not be reduced by certain advisory fees we will pay to I-Bankers. Our initial shareholders have agreed to waive their right to receive liquidating distributions if we fail to consummate our initial business combination within the requisite time period. However, if our initial shareholders or any of our officers, directors or affiliates acquires public shares in or after our initial public offering, they will be entitled to receive liquidating distributions with respect to such public shares if we fail to consummate our initial business combination within the required time period.

Manner of Conducting Redemptions

We will provide our public shareholders with the opportunity to redeem all or a portion of their public shares upon the completion of our initial business combination either (i) in connection with a shareholder meeting called to approve the business combination or (ii) by means of a tender offer.

We intend to hold a shareholder vote in connection with our business combination. In such case, we will:

| ● | conduct the redemptions in conjunction with a proxy solicitation pursuant to Regulation 14A of the Exchange Act, which regulates the solicitation of proxies, and not pursuant to the tender offer rules, and |

| ● | file proxy materials with the SEC. |

In the event that we seek shareholder approval of our initial business combination, we will distribute proxy materials and, in connection therewith, provide our public shareholders with the redemption rights described above upon consummation of the initial business combination.

If we seek shareholder approval, we will consummate our initial business combination only if a majority of the outstanding ordinary shares voted are voted in favor of the business combination. In such case, our initial shareholders have agreed to vote their founder shares, private shares and any public shares purchased during or after the offering in favor of our initial business combination and our officers and directors have also agreed to vote any public shares purchased during or after the offering in favor of our initial business combination. As a result, we would need only 4,307,376 of the 13,800,000 public shares, or approximately 31.2%, sold in our initial public offering to be voted in favor of a transaction in order to have our initial business combination approved. Each public shareholder may elect to redeem their public shares irrespective of whether they vote for or against the proposed transaction. In addition, our initial shareholders have agreed to waive their redemption rights with respect to their founder shares, private shares and public shares in connection with the consummation of our initial business combination.

In no event will we redeem our public shares in an amount that would cause our net tangible assets to be less than $5,000,001 prior to or upon the consummation of our initial business combination after payment of the deferred underwriting commission. Furthermore, the redemption threshold may be further limited by the terms and conditions of our initial business combination. If too many public shareholders exercise their redemption rights so that we cannot satisfy the net tangible asset requirement or any net worth or cash requirements, we would not proceed with the redemption of our public shares and the related business combination, and instead may search for an alternate business combination.

12

Notwithstanding the foregoing, if we do not decide to hold a shareholder vote in conjunction with their initial business combination for business or other legal reasons (so long as shareholder approval is not required by the Companies Act or the rules of Nasdaq), we will conduct redemptions pursuant to the tender offer rules of the SEC and our memorandum and articles of association. In such case, we will:

| ● | offer to redeem our public shares pursuant to Rule 13e-4 and Regulation 14E of the Exchange Act, which regulate issuer tender offers, and |

| ● | file tender offer documents with the SEC prior to consummating our initial business combination which will contain substantially the same financial and other information about the initial business combination and the redemption rights as is required under Regulation 14A of the Exchange Act, which regulates the solicitation of proxies, and we will not be permitted to consummate our initial business combination until the expiration of the tender offer period. |

In the event we conduct redemptions pursuant to the tender offer rules, our offer to redeem shall remain open for at least 20 business days, in accordance with Rule 14e-1(a) under the Exchange Act.

In connection with the successful consummation of our business combination, we may redeem pursuant to a tender offer up to that number of ordinary shares that would permit us to maintain net tangible assets of at least $5,000,001 prior to or upon the consummation of our initial business combination after payment of the deferred underwriting commission. However, the redemption threshold may be further limited by the terms and conditions of our proposed initial business combination. For example, the proposed business combination may require: (i) cash consideration to be paid to the target or members of its management team, (ii) cash to be transferred to the target for working capital or other general corporate purposes or (iii) the allocation of cash to satisfy other conditions in accordance with the terms of the proposed business combination. In the event the aggregate cash consideration we would be required to pay for all shares that are validly tendered plus any amount required to satisfy cash conditions pursuant to the terms of the proposed business combination exceed the aggregate amount of cash available to us, we will not consummate the business combination, we will not purchase any shares pursuant to the tender offer and all shares will be returned to the holders thereof following the expiration of the tender offer. Additionally, since we are required to maintain net tangible assets of at least $5,000,001 prior to or upon the consummation of our initial business combination after payment of the deferred underwriting commission (which may be substantially higher depending on the terms of our potential business combination), the chance that the holders of our ordinary shares electing to redeem in connection with a redemption conducted pursuant to the proxy rules will cause us to fall below such minimum requirement is increased.

When we conduct a tender offer to redeem our public shares upon consummation of our initial business combination, in order to comply with the tender offer rules, the offer will be made to all of our shareholders, not just our public shareholders. Our initial shareholders have agreed to waive their redemption rights with respect to their founder shares, private shares and public shares in connection with any such tender offer.

Limitation on Redemption Rights upon Consummation of Our Initial Business Combination If We Seek Shareholder Approval

If we seek shareholder approval of our initial business combination and we do not conduct redemptions in connection with our business combination pursuant to the tender offer rules, our memorandum and articles of association provides that a public shareholder, individually or together with any affiliate of such shareholder or any other person with whom such shareholder is acting in concert or as a “group” (as defined under Section 13 of the Exchange Act), will be restricted from seeking redemption rights with respect to more than an aggregate of 15% of the shares sold in our initial public offering. We believe this restriction will discourage shareholders from accumulating large blocks of shares, and subsequent attempts by such holders to use their ability to exercise their redemption rights as a means to force us or our management to purchase their shares at a significant premium to the then-current market price or on other undesirable terms. Absent this provision, a public shareholder holding more than an aggregate of 15% of the shares sold in our initial public offering could threaten to exercise its redemption rights if such holder’s shares are not purchased by us or our management at a premium to the then-current market price or on other undesirable terms. By limiting our shareholders’ ability to redeem no more than 15% of the shares sold in our initial public offering, we believe we will limit the ability of a small group of shareholders to unreasonably attempt to block our ability to consummate our initial business combination, particularly in connection with our initial business combination with a target that requires as a closing condition that we have a minimum net worth or a certain amount of cash. However, we would not be restricting our shareholders’ ability to vote all of their shares (including all shares held by those shareholders that hold more than 15% of the shares sold in our initial public offering) for or against our initial business combination. We will resolve any disputes relating to whether a public shareholder is acting in concert or as a “group” either by requiring certifications under the penalty of perjury to such effect by public shareholders or via adjudication in court.

13

Permitted Purchases of Our Securities by Our Affiliates

If we seek shareholder approval of our business combination and we do not conduct redemptions in connection with our business combination pursuant to the tender offer rules, our sponsor, directors, officers or their affiliates may purchase shares in privately negotiated transactions or in the open market either prior to or following the consummation of our initial business combination. Such a purchase would include a contractual acknowledgement that such shareholder, although still the record holder of our shares is no longer the beneficial owner thereof and therefore agrees not to exercise its redemption rights. In the event that our sponsor, directors, officers or their affiliates purchase shares in privately negotiated transactions from public shareholders who have already elected to exercise their redemption rights, such selling shareholders would be required to revoke their prior elections to redeem their shares. Although very unlikely, our initial shareholders, officers, directors and their affiliates could purchase sufficient shares so that the initial business combination may be approved without the majority vote of public shares held by non-affiliates. It is intended that purchases will comply with Rule 10b-18 under the Exchange Act, which provides a safe harbor for purchases made under certain conditions, including with respect to timing, pricing and volume of purchases.

The purpose of such purchases would be to (1) increase the likelihood of obtaining shareholder approval of the business combination or (2) to satisfy a closing condition in an agreement with a target that requires us to have a minimum net worth or a certain amount of cash at the closing of the business combination, where it appears that such requirement would otherwise not be met. This may result in the consummation of an initial business combination that may not otherwise have been possible.

As a consequence of any such purchases, the public “float” of our ordinary shares may be reduced and the number of beneficial holders of our securities may be reduced, which may make it difficult to maintain the listing or trading of our securities on a national securities exchange following consummation of a business combination.

Tendering Share Certificates in Connection With a Tender Offer or Redemption Rights

We will require our public shareholders seeking to exercise their redemption rights, whether they are record holders or hold their shares in “street name,” to either tender their certificates to our transfer agent prior to the expiration date set forth in the tender offer documents mailed to such holders, or in the event we distribute proxy materials, up to two business days prior to the vote on the proposal to approve the business combination, or to deliver their shares to the transfer agent electronically using The Depository Trust Company’s DWAC (Deposit/Withdrawal At Custodian) System, at the holder’s option. Accordingly, a public shareholder would have from the time we send out our tender offer materials until the close of the tender offer period, or up to two days prior to the vote on the business combination if we distribute proxy materials, as applicable, to tender its shares if it wishes to seek to exercise its redemption rights. Given the relatively short exercise period, it is advisable for shareholders to use electronic delivery of their public shares.

There is a nominal cost associated with the above-referenced tendering process and the act of certificating the shares or delivering them through the DWAC System. The transfer agent will typically charge the tendering broker $45.00 and it would be up to the broker whether or not to pass this cost on to the redeeming holder. However, this fee would be incurred regardless of whether or not we require holders seeking to exercise redemption rights to tender their shares. The need to deliver shares is a requirement of exercising redemption rights regardless of the timing of when such delivery must be effectuated.

The foregoing is different from the procedures used by many blank check companies. In order to perfect redemption rights in connection with their business combinations, many blank check companies would distribute proxy materials for the shareholders’ vote on our initial business combination, and a holder could simply vote against a proposed business combination and check a box on the proxy card indicating such holder was seeking to exercise his redemption rights. After the business combination was approved, the company would contact such shareholder to arrange for him to deliver his certificate to verify ownership. As a result, the shareholder then had an “option window” after the consummation of the business combination during which he could monitor the price of the company’s shares in the market. If the price rose above the redemption price, he could sell his shares in the open market before actually delivering his shares to the company for cancellation. As a result, the redemption rights, to which shareholders were aware they needed to commit before the shareholder meeting, would become “option” rights surviving past the consummation of the business combination until the redeeming holder delivered its certificate. The requirement for physical or electronic delivery at or prior to the meeting ensures that a redeeming holder’s election to redeem is irrevocable once the business combination is approved.

14

Any request to redeem such shares, once made, may be withdrawn at any time up to the date set forth in the tender offer materials or the date of the shareholder meeting set forth in our proxy materials, as applicable. Furthermore, if a holder of a public share delivered its certificate in connection with an election of redemption rights and subsequently decides prior to the applicable date not to elect to exercise such rights, such holder may simply request that the transfer agent return the certificate (physically or electronically). It is anticipated that the funds to be distributed to holders of our public shares electing to redeem their shares will be distributed promptly after the completion of our initial business combination.

If the initial business combination is not approved or completed for any reason, then our public shareholders who elected to exercise their redemption rights would not be entitled to redeem their shares for the applicable pro rata share of the trust account. In such case, we will promptly return any certificates delivered by public holders who elected to redeem their shares.

If our initial proposed business combination is not consummated, we may continue to try to consummate our initial business combination with a different target by May 24, 2021 (or up to November 24, 2021 if we extend such date to consummate a business combination, as described in more detail in this report).

Redemption of Public Shares and Liquidation If No Initial Business Combination

Our sponsor, officers and directors have agreed that we must complete our initial business combination by May 24, 2021 (or up to November 24, 2021 if we extend such date to consummate a business combination, as described in more detail in this report). We may not be able to find a suitable target business and consummate our initial business combination by such dates. If we are unable to consummate our initial business combination by May 24, 2021 (or up to November 24, 2021 from the closing of our initial public offering if we extend such date to consummate a business combination, as described in more detail in this report), we will, as promptly as reasonably possible but not more than five business days thereafter, distribute the aggregate amount then on deposit in the trust account (net of taxes payable, and less up to $50,000 of interest to pay liquidation expenses), pro rata to our public shareholders by way of redemption and cease all operations except for the purposes of winding up of our affairs. This redemption of public shareholders from the trust account shall be effected as required by function of our memorandum and articles of association and prior to any voluntary winding up, although at all times subject to the Companies Act.

Following the redemption of public shares, we intend to enter “voluntary liquidation” which is the statutory process for formally closing and dissolving a company under the laws of the British Virgin Islands. Given that we intend to enter voluntary liquidation following the redemption of public shareholders from the trust account, we do not expect that the voluntary liquidation process will cause any delay to the payment of redemption proceeds from our trust account. In connection with such a voluntary liquidation, the liquidator would give notice to creditors inviting them to submit their claims for payment, by notifying known creditors (if any) who have not submitted claims and by placing a public advertisement in at least one newspaper published in the British Virgin Islands and in at least one newspaper circulating in the location where the company has its principal place of business, and taking any other steps he considers appropriate to identify the company’s creditors, after which our remaining assets would be distributed. As soon as the affairs of the company are fully wound-up, the liquidator must complete his statement of account and file notice with the Registrar that the liquidation is complete. We would be dissolved once the Registrar issues a Certificate of Dissolution.

Our initial shareholders have agreed to waive their redemption rights with respect to their founder shares and private units if we fail to consummate our initial business combination within the applicable period from the closing of our initial public offering.

15

However, if our initial shareholders, or any of our officers, directors or affiliates acquire public shares in or after our initial public offering, they will be entitled to redemption rights with respect to such public shares if we fail to consummate our initial business combination within the required time period. There will be no redemption rights or liquidating distributions with respect to our rights and warrants, which will expire worthless in the event we do not consummate our initial business combination by May 24, 2021 (or up to November 24, 2021 if we extend such date to consummate a business combination, as described in more detail in this report). We will pay the costs of our liquidation from our remaining assets outside of the trust account or interest earned on the funds held in the trust account. However, the liquidator may determine that he or she requires additional time to evaluate creditors’ claims (particularly if there is uncertainty over the validity or extent of the claims of any creditors). Also, a creditor or shareholder may file a petition with the BVI court which, if successful, may result in our liquidation being subject to the supervision of that court. Such events might delay distribution of some or all of our remaining assets.

Additionally, in any liquidation proceedings of the company under British Virgin Islands law, the funds held in our trust account may be included in our estate and subject to the claims of third parties with priority over the claims of our shareholders. To the extent any such claims deplete the trust account we may not be able to return to our public shareholders the liquidation amounts payable to them.

If we were to expend all of the net proceeds of our initial public offering, other than the proceeds deposited in the trust account, and without taking into account interest, if any, earned on the trust account, the per-share redemption amount received by shareholders upon our dissolution would be approximately $10.00 (based on the trust account balance as of June 30, 2020). The proceeds deposited in the trust account could, however, become subject to the claims of our creditors, which would have higher priority than the claims of our public shareholders. The actual per-share redemption amount received by shareholders may be less than $10.00, plus interest (net of taxes payable, and less up to $50,000 of interest to pay liquidation expenses).

Although we have sought and will continue to seek to have all vendors, service providers (other than our independent auditor), prospective target businesses or other entities with which we do business execute agreements with us waiving any right, title, interest or claim of any kind in or to any monies held in the trust account for the benefit of our public shareholders, there is no guarantee that they will execute such agreements or even if they execute such agreements that they would be prevented from bringing claims against the trust account including but not limited to fraudulent inducement, breach of fiduciary responsibility or other similar claims, as well as claims challenging the enforceability of the waiver, in each case in order to gain an advantage with respect to a claim against our assets, including the funds held in the trust account. If any third party refuses to execute an agreement waiving such claims to the monies held in the trust account, our management will perform an analysis of the alternatives available to it and will only enter into an agreement with a third party that has not executed a waiver if management believes that such third party’s engagement would be significantly more beneficial to us than any alternative. Examples of possible instances where we may engage a third party that refuses to execute a waiver include the engagement of a third party consultant whose particular expertise or skills are believed by management to be significantly superior to those of other consultants that would agree to execute a waiver or in cases where management is unable to find a service provider willing to execute a waiver. WithumSmith+Brown, PC, our independent registered public accounting firm, will not execute agreements with us waiving such claims to the monies held in the trust account. In addition, there is no guarantee that such entities will agree to waive any claims they may have in the future as a result of, or arising out of, any negotiations, contracts or agreements with us and will not seek recourse against the trust account for any reason. In order to protect the amounts held in the trust account, our sponsor and our officers agreed that they will be liable to us, if and to the extent any claims by a vendor for services rendered or products sold to us, or a prospective target business with which we have discussed entering into a transaction agreement, reduce the amounts in the trust account to below $10.00 per share, except as to any claims by a third party who executed a waiver of any and all rights to seek access to the trust account and except as to any claims under our indemnity of the underwriters of our initial public offering against certain liabilities, including liabilities under the Securities Act. In the event that an executed waiver is deemed to be unenforceable against a third party, our sponsor will not be responsible to the extent of any liability for such third party claims. However, our sponsor may not be able to satisfy those obligations. Other than as described above, none of our other officers or directors will indemnify us for claims by third parties including, without limitation, claims by vendors and prospective target businesses. We have not independently verified whether our sponsor has sufficient funds to satisfy his indemnity obligations and believe that our sponsor’s only assets are securities of our company. We believe the likelihood of our sponsor having to indemnify the trust account is limited because we will endeavor to have all vendors and prospective target businesses as well as other entities execute agreements with us waiving any right, title, interest or claim of any kind in or to monies held in the trust account.

16

In the event that the proceeds in the trust account are reduced below $10.00 per share and our sponsor asserts that it is unable to satisfy any applicable obligations or that it has no indemnification obligations related to a particular claim, our independent directors would determine whether to take legal action against our sponsor to enforce its indemnification obligations. While we currently expect that our independent directors would take legal action on our behalf against our sponsor to enforce its indemnification obligations to us, it is possible that our independent directors in exercising their business judgment may choose not to do so in any particular instance. Accordingly, due to claims of creditors, the actual value of the per-share redemption price may be less than $10.00 per share.

We seek to reduce the possibility that our sponsor has to indemnify the trust account due to claims of creditors by endeavoring to have all vendors, service providers (other than our independent auditor), prospective target businesses or other entities with which we do business execute agreements with us waiving any right, title, interest or claim of any kind in or to monies held in the trust account. Our sponsor will also not be liable as to any claims under our indemnity of the underwriters of our initial public offering against certain liabilities, including liabilities under the Securities Act. As of September 18, 2020, we had access to up to approximately $780,000 not placed in the trust account (approximately $389,000 as of June 30, 2020) with which to pay any such potential claims (including costs and expenses incurred in connection with our liquidation, currently estimated to be more than approximately $50,000). In the event that we liquidate and it is subsequently determined that the reserve for claims and liabilities is insufficient, shareholders who received funds from our trust account could be liable for claims made by creditors.