Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - EVOLUTION PETROLEUM CORP | a2020fysecrotpwith991fin.htm |

| EX-32.2 - EXHIBIT 32.2 - EVOLUTION PETROLEUM CORP | a6302020exhibit322.htm |

| EX-32.1 - EXHIBIT 32.1 - EVOLUTION PETROLEUM CORP | a6302020exhibit321.htm |

| EX-31.2 - EXHIBIT 31.2 - EVOLUTION PETROLEUM CORP | a6302020exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - EVOLUTION PETROLEUM CORP | a6302020exhibit311.htm |

| EX-23.2 - EXHIBIT 23.2 - EVOLUTION PETROLEUM CORP | dandmconsent63020exh_232.htm |

| EX-23.1 - EXHIBIT 23.1 - EVOLUTION PETROLEUM CORP | mossadamsconsent63020exh_2.htm |

| EX-21.1 - EXHIBIT 21.1 - EVOLUTION PETROLEUM CORP | listofsubs63020exh211.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended June 30, 2020

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission File Number 001-32942

EVOLUTION PETROLEUM CORPORATION

(Exact name of registrant as specified in its charter)

Nevada | 41-1781991 | |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |

1155 Dairy Ashford Road, Suite 425, Houston, Texas 77079

(Address of principal executive offices and zip code)

(713) 935-0122

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol(s) | Name of Each Exchange On Which Registered | ||

Common Stock, $0.001 par value | EPM | NYSE American | ||

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes: ☐ No: ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes: ☐ No: ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes: ☒ No: ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes: ☒ No: ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definition of "large accelerated filer", "accelerated filer", "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☒ | |

Non-accelerated filer | ☐ | Smaller reporting company | ☒ | |

Emerging growth company | ☐ | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.). Yes: ☐ No: ☒

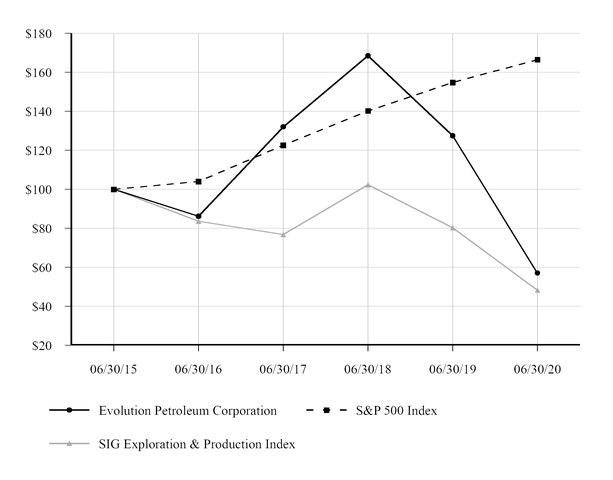

The aggregate market value of the voting and non-voting common equity held by non-affiliates on December 31, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, based on the closing price on that date of $5.47 on the NYSE American was $122,253,472.

The number of shares outstanding of the registrant's common stock, par value $0.001, as of September 1, 2020, was 32,956,469.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement related to the registrant's 2020 Annual Meeting of Stockholders to be filed within 120 days of the end of the fiscal year covered by this report are incorporated by reference into Part III of this report.

EVOLUTION PETROLEUM CORPORATION AND SUBSIDIARIES

2020 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

We use the terms, "EPM," "Company," "we," "us" and "our" to refer to Evolution Petroleum Corporation, and unless the context otherwise requires, its wholly-owned subsidiaries.

i

FORWARD-LOOKING STATEMENTS

This Form 10-K and the information referenced herein contains forward-looking statements within the meaning of the Private Securities Litigations Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The words “plan,” “expect,” “project,” “estimate,” “assume,” “believe,” “anticipate,” “intend,” “budget,” “forecast,” “predict” and other similar expressions are intended to identify forward-looking statements. These statements appear in a number of places and include statements regarding our plans, beliefs or current expectations, including the plans, beliefs and expectations of our officers and directors. When considering any forward-looking statement, you should keep in mind the risk factors that could cause our actual results to differ materially from those contained in any forward-looking statement. Important factors that could cause actual results to differ materially from those in the forward-looking statements herein include the timing and extent of changes in commodity prices for oil and natural gas, operating risks and other risk factors as described in Part I, Item 1A, "Risk Factors" and elsewhere in this report and as also may be described from time to time in our future reports we file with the Securities and Exchange Commission. You should read such information in conjunction with our consolidated financial statements and related notes and "Management's Discussion and Analysis of Financial Condition and Results of Operations" in this report. There also may be other factors that we cannot anticipate or that are not described in this report, generally because we do not currently perceive them to be material. Such factors could cause results to differ materially from our expectations.

Forward-looking statements speak only as of the date they are made, and we do not undertake to update these statements other than as required by law. You are advised, however, to review any further disclosures we make on related subjects in our periodic filings with the Securities and Exchange Commission.

ii

GLOSSARY OF SELECTED PETROLEUM INDUSTRY TERMS

Term | Definition | |

Bbls | Barrels of oil or natural gas liquids. | |

BFPD | Barrels of fluid per day. | |

BOE | Barrels of oil equivalent. BOE is calculated by converting 6 MCF of natural gas to 1 Bbl of oil which reflects energy equivalence and not price equivalence. Gas prices per MCF and NGL prices per barrel often differ significantly from the equivalent amount of oil. | |

BOPD | Barrels of oil per day. | |

BTU | British Thermal Unit: the standard unit of measure of energy equal to the amount of heat required to raise the temperature of one pound of water 1 degree Fahrenheit. One Bbl of crude is typically 5.8 MMBTU, and one standard MCF is typically one MMBTU. | |

CO2 | Carbon dioxide; CO2 is a gas that can be found in naturally occurring reservoirs, is typically associated with ancient volcanoes, is a major byproduct from manufacturing and power production, and is also utilized in enhanced oil recovery through injection into an oil reservoir. | |

Developed Reserves | Reserves of any category that can be expected to be recovered (i) through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well; and (ii) through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by a means not involving a well. | |

EOR | Enhanced Oil Recovery; projects that involve injection of heat, miscible or immiscible gas, or chemicals into oil reservoirs, typically following full primary and secondary waterflood recovery efforts, in order to gain incremental recovery of oil from the reservoir. | |

Field | An area consisting of a single reservoir or multiple reservoirs all grouped within or related to the same geologic structural features and/or stratigraphic features.* | |

Farmout | Sale or transfer of all or part of the operating rights from the working interest owner (the assignor or farm-out party), to an assignee (the farm-in party) who assumes all or some of the burden of development, in return for an interest in the property. The assignor may retain an overriding royalty or any other type of interest. For Federal tax purposes, a farm-out may be structured as a sale or lease, depending on the specific rights and carved out interests retained by the assignor. | |

Gross Acres or Gross Wells | The total acres or number of wells participated in, regardless of the amount of working interest owned. | |

Horizontal Drilling | Involves drilling horizontally out from a vertical well bore, thereby potentially increasing the area and reach of the well bore that is in contact with the reservoir. | |

Hydraulic Fracturing | Involves pumping a fluid with or without particulates into a formation at high pressure, thereby creating fractures in the rock and leaving the particulates in the fractures to ensure that the fractures remain open which potentially increases the ability of the reservoir to produce oil or gas. | |

LOE | Means lease operating expense(s), a current period expense incurred to operate a well. | |

MBO | One thousand barrels of oil. | |

MBOE | One thousand barrels of oil equivalent. | |

MCF | One thousand cubic feet of natural gas at standard conditions, being approximately sea level pressure and 60 degrees Fahrenheit temperature. | |

MMBOE | One million barrels of oil equivalent. | |

MMBTU | One million British Thermal Units. | |

MMCE | One million cubic feet of natural gas at standard temperature and pressure. | |

Mineral Royalty Interest | A royalty interest that is retained by the owner of the minerals underlying a lease. See "Royalty Interest". | |

Net Acres or Net Wells | The sum of the fractional working interests owned in gross acres or gross wells. | |

NGL | Natural gas liquids; the combination of ethane, propane, butane and natural gasoline that can be removed from natural gas through processing, typically through refrigeration plants that utilize low temperatures, or through plants that utilize compression, temperature reduction and expansion to a lower pressure. | |

NYMEX | New York Mercantile Exchange. | |

OOIP | Original Oil in Place; an estimate of the barrels originally contained in a reservoir before any production therefrom. | |

Operator | An oil and gas joint venture participant that manages the joint venture, pays venture costs and bills the venture's non-operators for their share of venture costs. The operator is also responsible to market all oil and gas production, except for those non-operators who take their production in-kind. | |

Overriding Royalty Interest or ORRI | A royalty interest that is created out of the operating or working interest. Unlike a royalty interest, an overriding royalty interest terminates with the operating interest from which it was created or carved out of. See "Royalty Interest." | |

iii

Permeability | The measure of ease with which a fluid can move through a reservoir. The unit of measure is a darcy(d), or any metric derivation thereof, such as a millidarcy(md), where one darcy equals 1,000 millidarcys. Extremely low permeability of 10 millidarcys, or less, are often associated with source rocks, such as shale. Extraction of hydrocarbons from a source rock is more difficult than a sandstone reservoir where permeability typically ranges one to two darcys or more. | |

Porosity | The relative volume of the pore space (or open area) compared to the total bulk volume of the reservoir, stated in percent. Higher porosity rocks provide more storage space for hydrocarbon accumulations than lower porosity rocks in a given cubic volume of reservoir. | |

Producing Reserves | Any category of reserves that have been developed and production has been initiated.* | |

Proved Developed Reserves | Proved Reserves that can be expected to be recovered (i) through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well; and (ii) through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by a means not involving a well. | |

Proved Developed Nonproducing Reserves | Proved Reserves that have been developed and no material amount of capital expenditures are required to bring on production, but production has not yet been initiated due to timing, markets, or lack of third party completed connection to a gas sales pipeline.* | |

Proved Developed Producing Reserves ("PDP") | Proved Reserves that have been developed and production has been initiated.* | |

Proved Reserves | Estimated quantities of crude oil, natural gas, and natural gas liquids which geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic, operating methods, and government regulations prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time.* | |

Proved Undeveloped Reserves ("PUD") | Proved Reserves that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion.* (i) Reserves on undrilled acreage shall be limited to those directly offsetting development spacing areas that are reasonably certain of production when drilled, unless evidence using reliable technology exists that establishes reasonable certainty of economic producibility at greater distances. (ii) Undrilled locations can be classified as having undeveloped reserves only if a development plan has been adopted indicating that they are scheduled to be drilled within five years, unless the specific circumstances, justify a longer time. (iii) Under no circumstances shall estimates for undeveloped reserves be attributable to any acreage for which an application of fluid injection or other improved recovery technique is contemplated, unless such techniques have been proved effective by actual projects in the same reservoir or an analogous reservoir or by other evidence using reliable technology establishing reasonable certainty. | |

Present Value | When used with respect to oil and gas reserves, present value means the estimated future net revenues computed by applying current prices of oil and gas reserves (with consideration of price changes only to the extent provided by contractual arrangements) to estimated future production of proved oil and gas reserves as of the date of the latest balance sheet presented, less estimated future expenditures (based on current costs to be incurred in developing and producing the proved reserves) computed using a discount factor and assuming continuation of existing economic conditions. | |

Productive Well | A well that is producing oil or gas or that is capable of production. | |

PV-10 | Means the present value, discounted at 10% per annum, of future net revenues (estimated future gross revenues less estimated future costs of production, development, and asset retirement costs) associated with reserves and is not necessarily the same as market value. PV-10 does not include estimated future income taxes. Unless otherwise noted, PV-10 is calculated using the pricing scheme as required by the Securities and Exchange Commission ("SEC"). PV-10 of proved reserves is calculated the same as the standardized measure of discounted future net cash flows, except that the standardized measure of discounted future net cash flows includes future estimated income taxes discounted at 10% per annum. See the definition of standardized measure of discounted future net cash flows. | |

Royalty or Royalty Interest | 1) The mineral owner's share of oil or gas production (typically between 1/8 and 1/4), free of costs, but subject to severance taxes unless the lessor is a government. In certain circumstances, the royalty owner bears a proportionate share of the costs of making the natural gas saleable, such as processing, compression and gathering. 2) When a royalty interest is coterminous with and carved out of an operating or working interest, it is an "Overriding Royalty Interest," which also may generically be referred to as a Royalty. | |

Shut-in Well | A well that is not on production, but has not been plugged and abandoned. Wells may be shut-in in anticipation of future utility as a producing well, plugging and abandonment or other use. | |

Standardized Measure | The standardized measure of discounted future net cash flows. The Standardized Measure is an estimate of future net cash flows associated with proved reserves, discounted at 10% per annum. Future net cash flows are calculated by reducing future net revenues by estimated future income tax expenses and discounting at 10% per annum. The Standardized Measure and the PV-10 of proved reserves is calculated in the same exact fashion, except that the Standardized Measure includes future estimated income taxes discounted at 10% per annum. The Standardized Measure is in accordance with accounting standards generally accepted in the United States of America ("GAAP"). | |

iv

Undeveloped Reserves | Reserves of any category that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion.* | |

Working Interest | The interest in the oil and gas in place which is burdened with the cost of development and operation of the property. Also called the operating interest. | |

Workover | A remedial operation on a completed well to restore, maintain or improve the well's production. | |

* This definition may be an abbreviated version of the complete definition as defined by the SEC in Rule 4-10(a) of Regulation S-X.

v

PART I

Item 1. Business

Note: See Glossary of Selected Petroleum Industry Terms starting on page

General

Evolution Petroleum Corporation is an oil and gas company focused on delivering a sustainable dividend yield to its shareholders through the ownership, management and development of producing oil and gas properties. The Company's long-term goal is to build a diversified portfolio of oil and gas assets primarily through acquisition, while seeking opportunities to maintain and increase production through selective development, production enhancement and other exploitation efforts on its properties.

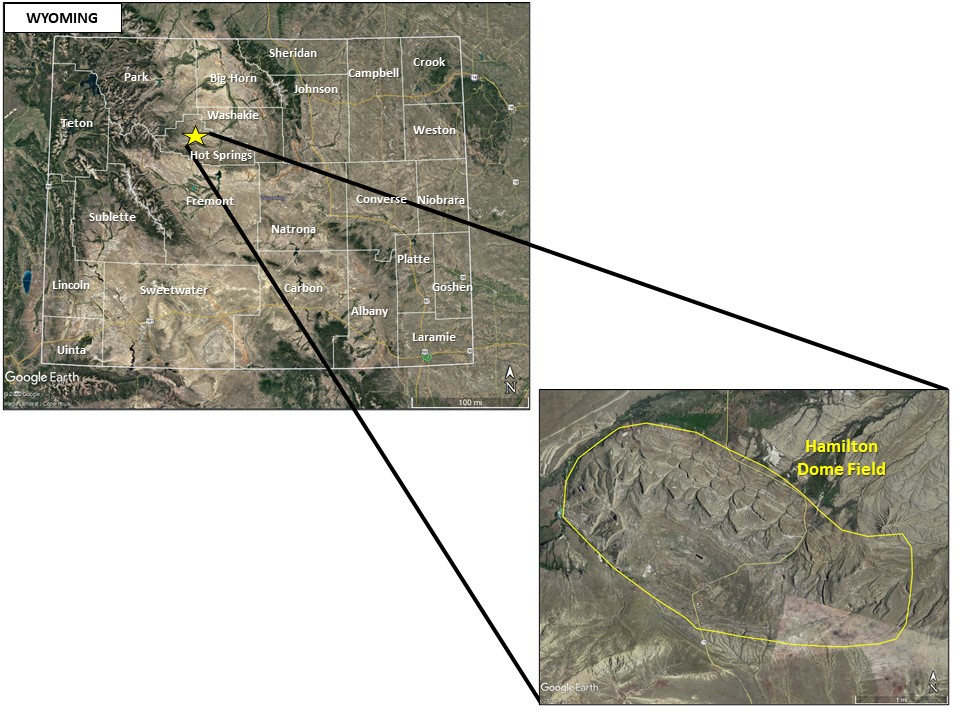

Our producing assets consist of our interests in the Delhi Holt-Bryant Unit in the Delhi field in Northeast Louisiana, a CO2 enhanced oil recovery project, and our interests in the Hamilton Dome field located in Hot Springs County, Wyoming, a secondary recovery field utilizing water injection wells to pressurize the reservoir, and overriding royalty interests in two onshore Texas wells.

Our interests in the Delhi field consist of a 23.9% working interest, with an associated 19.0% revenue interest and separate overriding royalty and mineral interests of 7.2% yielding a total net revenue interest of 26.2%. The field is operated by Denbury Onshore LLC ("Denbury"), a subsidiary of Denbury Resources, Inc.

On November 1, 2019, the Company acquired non-operated working interests in the Hamilton Dome field consisting of a 23.5% working interest, with an associated 19.7% revenue interest (inclusive of a small overriding royalty interest). The field is operated by Merit Energy Company ("Merit"), a private oil and gas company, who owns the vast majority of the remaining working interest in Hamilton Dome field. Our acquired interest in Hamilton Dome aligned with the Company's strategy of adding long lived, low decline reserves expected to be supportive of our dividend over the long-term.

Significant Activity in Fiscal 2020

• | Proved oil equivalent reserves at June 30, 2020 were 10.2 MMBOE, a 13% increase from the previous year primarily due to the acquisition of the Hamilton Dome field in November 2019. The Standardized Measure for proved reserves decreased 51% to $62 million, as the acquisition of the Hamilton Dome field was offset by the decrease in the average first day of the month net oil price from $64.54 per barrel of oil and $23.83 per barrel of natural gas liquids at June 30, 2019 to $46.37 per barrel of oil and $9.00 per barrel of natural gas liquids at June 30, 2020. Our proved reserves consist of 80% crude oil and 20% natural gas liquids, 82% are classified as proved developed producing and 18% are proved undeveloped. |

• | We recognized net income of $5.9 million, or $0.18 per diluted common share, our ninth consecutive year of reporting net income. |

• | Returned to shareholders $10.7 million in cash dividends and $2.5 million in stock repurchases in fiscal 2020. The Company has paid out to shareholders more than $70 million in cash dividends since inception of the dividend program in December 2013. |

• | Closed the acquisition of non-operating working interest in the Hamilton Dome field on November 1, 2019 which included total proved reserves of 1.47 MMBOE as of June 30, 2020 as estimated by DeGolyer & MacNaughton ("D&M"), an independent reservoir engineering firm. |

• | Reported $12.4 million of cash flows from operations for the fiscal year ended June 30, 2020. We funded all operations, including $11.8 million of capital spending inclusive of our $9.3 million acquisition of our interest in the Hamilton Dome Field, from internal resources and remain debt free at June 30, 2020. |

• | In order to mitigate the impact of the growing global COVID-19 pandemic on our employees, we continue to follow local stay-at-home orders and remotely work from home with minimal disruptions to our business operations. |

• | We entered into NYMEX WTI oil swaps covering approximately 42,000 barrels per month for the period of April 2020 through December 2020 at a fixed swap price of $32.00 per barrel, recording a loss of $1.4 million at June 30, 2020. Of this amount, $1.9 million were non-cash, unrealized mark-to-market losses as commodity prices improved from those existing at fiscal year-end, offset in part by $0.5 million in realized gains during the fiscal fourth quarter. |

1

• | We completed remaining capital expenditures for the six-well water curtain program and related infrastructure preceding the planned Delhi Phase V development, which was delayed by the operator until our fiscal fourth quarter of 2021. |

• | In July 2020, Denbury Resources announced that it had entered into a restructuring support agreement with certain of its debt holders and filed a pre-packaged voluntary petition for reorganization under Chapter 11 of the Bankruptcy Code in Texas. Denbury Resources is seeking to eliminate $2.1 billion of debt. Denbury subsequently announced on September 3, 2020 that its plan to eliminate $2.1 billion of its bond debt has been confirmed by the court which will substantially reduce its debt and strengthen its balance sheet. |

Our Reserves: Delhi Field - Enhanced Oil Recovery - Onshore Louisiana

Our independent reservoir engineering firm, D&M, assigned the estimated reserves net to our interests at Delhi as of June 30, 2020; we had 8.7 million bbls of total proved oil equivalent reserves. The following table summarizes the reserves assigned by D&M:

Reserves as of June 30, 2020 | ||

Proved | ||

Reserves MBOE | 8,746 | |

% Developed | 79 | % |

Liquids % | 100 | % |

Development History of the Delhi Field - Enhanced Oil Recovery - Onshore Louisiana

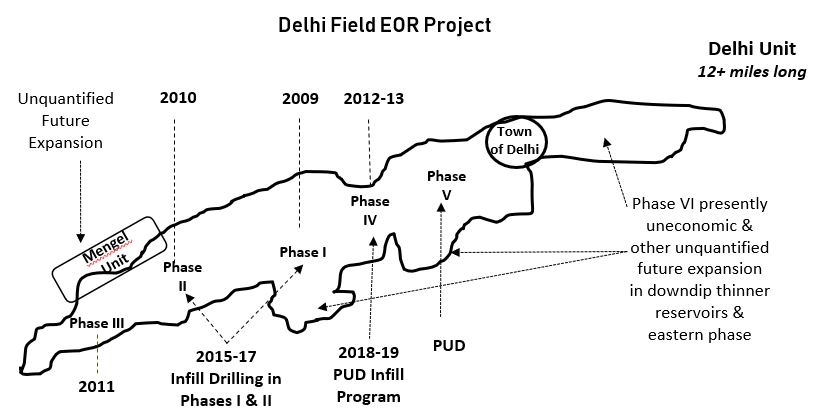

Our working and royalty interests in the Delhi field is currently our largest producing asset. The Holt-Bryant Unit ("Unit") is approximately 13,636 acres in size and has had a prolific production history totaling approximately 195 million bbls of oil through primary and limited secondary recovery operations since its discovery in the mid-1940s. At the time of our purchase of the field in 2003, the Unit had minimal production. We conveyed our working interest in the field to Denbury in May 2006 for $50 million for the purpose of installing an enhanced oil recovery ("EOR") project in the field. We retained a 23.9% reversionary working interest upon payout of the project, as defined in the purchase and sale agreements. Since EOR production began in March 2010, the Unit has produced over 21.5 million bbls of oil.

After the May 2006 conveyance, Denbury as the operator, originally planned six primary phases for the installation of the CO2 flood in the Delhi field. Four of these six phases have been completed as of June 30, 2020 and two remain undeveloped. One of the remaining two phases (Phase V) is reflected as proved undeveloped in our current reserves report and the other (Phase VI) was removed from proved reserves as it was not deemed economic under current pricing guidelines for SEC purposes.

Phase I began CO2 injection in November 2009. First oil production response occurred in March 2010 and production in the field increased to approximately 1,000 gross barrels of oil per day by December 2010.

2

Implementation of Phase II, which was more than double the size of Phase I, commenced with incremental CO2 injection at the end of December 2010. First oil production response from Phase II occurred during March 2011, and field gross production increased to more than 4,000 barrels of oil per day by June 2011.

Phase III was initially installed and subsequently expanded during calendar 2011. First oil production response from Phase III occurred during June 2011, and field gross production subsequently increased to more than 5,000 gross barrels of oil per day by December 2011.

Phase IV was installed during the first six months of calendar 2012. During early calendar 2013, the operator intensified development in the previously redeveloped western side of the field based on production results and new geological mapping that included the results of seismic data acquired over the last few years. First oil production response from Phase IV occurred during August 2012, and field gross production increased to more than 7,500 gross barrels of oil per day by February 2013.

In June 2013, following an adverse fluid release event that consisted of the uncontrolled release of CO2, water, natural gas and a small amount of oil from a previously plugged well in the southwest part of the field, the operator suspended CO2 injection in most of the southwestern tip of the field. The operator has fully remediated the affected area, has isolated that part of the field with a water curtain, thus removing the area from the CO2 flood.

Construction began on the NGL extraction plant in February 2015 and was completed and began processing in December 2016. The plant extracts methane and NGL's from the CO2 recycle stream. The methane and part of the ethane produced by the NGL extraction plant are used to generate electrical power for use in the field. The extracted NGL's are sold at the field to a purchaser who transports them by truck to a plant for further processing. In addition to the value of these hydrocarbon products, the increased purity of the CO2 stream re-injected into the field has resulted in operational benefits to the CO2 flood. To date, we have incurred a net capital cost of approximately $27.4 million for the plant, including capital upgrades since its commissioning.

Subsequent to the reversion of our working interest to us in November 2014, the operator initiated work on the Phase V expansion of the CO2 flood in the undeveloped eastern part of the field. These operations were suspended shortly after reversion when the operator significantly reduced capital spending as a result of declining oil prices. Resumption of this work has been delayed due to low prevailing oil prices and the operator's allocation of capital to other Delhi projects, primarily the large investment in the NGL plant together with the consensus that Phase V project economics would be enhanced if it were implemented after completion of the NGL plant.

An infill drilling program commenced in March 2018 to target productive oil zones in the developed areas of the field that were not being swept efficiently by the CO2 flood.During fiscal 2019 the 12 well infill program, consisting of 10 producing wells and two CO2 injection wells, was completed. Proved undeveloped reserves of 536 MBOE were converted to proved developed reserves.

Additionally during fiscal 2019, one pad of the six-well water curtain program was completed and commenced water injection during the second half of fiscal 2019. The project began late in fiscal 2017 after completion of the NGL plant with the drilling of one injection well followed by three injection wells in fiscal 2018. During fiscal 2019, the operator drilled the two remaining injection wells and proceeded with completions and injection line work. The first pad commenced operations during fiscal 2019 and the second pad began injections during our second quarter of fiscal 2020.

At June 30, 2020, we had total proved reserves of 8.7 MMBOE at Delhi, which was comprised of 6.7 MMBOE of oil and 2.0 MMBOE of NGLs as estimated by our independent petroleum engineering firm. The following table sets forth our estimated proved reserves as of June 30, 2020. For additional reserve information see Note 21 to our consolidated financial statements in Item 8.

Reserve Category | Oil (MBbls) | NGLs (MBbls) | Total Reserves (MBOE)* | |||||

PROVED | ||||||||

Developed Producing (79% of Proved) | 5,105 | 1,777 | 6,882 | |||||

Undeveloped (21% of Proved) | 1,648 | 216 | 1,864 | |||||

TOTAL PROVED | 6,753 | 1,993 | 8,746 | |||||

Product Mix | 77 | % | 23 | % | 100 | % | ||

*Equivalent oil reserves are defined as six MCF of gas and 42 gallons of natural gas liquids to one barrel of oil conversion ratio which reflects energy equivalence and not price equivalence. Gas prices per MCF and NGL prices per barrel often differ significantly from the equivalent amount of oil.

3

For fiscal 2020, average gross daily oil production at Delhi was 5,632 BOPD and 1,106 bbls NGLs per day (6,738 BOEPD). The total gross purchased CO2 volume was 19 BCF for fiscal 2020. In February 2020, the CO2 purchase line to Delhi was shut-in by the pipeline operator for extensive repairs. No CO2 was purchased from the shut-in date through June 2020. The recycle facilities continue to operate as usual providing approximately 80% of the injected CO2 volumes to Delhi with production somewhat reduced due to lower injection volumes. Per communications with Denbury, the CO2 line is currently being repaired and is projected to be completed early in the second quarter of our fiscal 2021.

Our Reserves: Hamilton Dome - Hot Springs County, Wyoming

Our independent reservoir engineering firm, D&M, assigned the estimated reserves net to our interests at Hamilton Dome as of June 30, 2020; we had 1.5 million bbls of total proved oil equivalent reserves. The following table summarizes the reserves assigned by D&M:

Reserves as of June 30, 2020 | ||

Proved | ||

Reserves MBOE | 1,473 | |

% Developed | 100 | % |

Liquids % | 100 | % |

On November 1, 2019, the Company acquired certain mineral interests in the Hamilton Dome field from Merit, who owns the vast majority of the remaining working interest in the field. The Hamilton Dome field is located in the southwest part of the Big Horn Basin in northwest Wyoming about twenty miles northwest of Thermopolis in Hot Springs County.

4

Our interest includes a 23.5% working interest and an associated 19.7% revenue interest (inclusive of a small overriding royalty interest). The Hamilton Dome field has produced over 160 MMBO over the last 100 years; Merit has operated the field over the last 25 years. Production from this field is 100% oil and is currently averaging low single-digit decline rates.

Development History of the Hamilton Dome Field - Hot Springs County, Wyoming

Oil was first discovered at the Hamilton Dome field within the Big Horn Basin in September 1918 in the Curtis/Chugwater reservoir by New York Oil Company via surface mapping. Shortly thereafter, the Phosphoria and Tensleep formations were discovered in 1919 and 1929, respectively. The field is part of an anticlinal fold with a southerly bounding fault with approximately 4,500-5,000 feet of displacement, thus providing a structural trap. The two major producing formations are the Tensleep (sandstone) and Phospohoria (limestone) reservoirs. Additional present day and historical production exists from the Curtis/Chugwater (sandstone), Amsden (sandstone), Madison (limestone), and Big Horn (dolomite) formations. These formations produce from depths ranging approximately 1,500 to 3,600 feet and have historically produced at rates of greater than 25,000 gross BOPD. The productive surface area of the field spans approximately 2,500 acres. The original oil in place of the six producing reservoirs is estimated to be at least 500 million barrels. Over the last 100 years, more than 160 million barrels have been produced from the field.

Although the Tensleep reservoir was discovered in 1929, it remained largely undeveloped until World War II. Active development of the Tensleep reservoir occurred between 1944 and 1960. The Madison and Darwin reservoirs were discovered in 1948 and 1959, respectively. These two reservoirs were developed sporadically from 1950 through the 1970’s. In 1970, 52 years after the field’s discovery, a waterflood was implemented in the Curtis/Chugwater reservoir. In 1973, the Phosphoria reservoir was unitized in order to implement a waterflood of the reservoir, this unit is still in place and is approximately 3,160 acres. In the early 1970’s, Tensleep production was down spaced to 5 acres and in the late 1970’s an isolated Tensleep waterflood was implemented. By 1981, the Tensleep reservoir had produced more than 147 million bbls. The last active development of the Curtis/Chugwater reservoir occurred in 1978 when the waterflood was ended. The Madison reservoir was further developed in the early 1990’s.

Merit Energy purchased the field in 1995 and has operated the field for 25 years; the field was unitized in 1996. The Phosphoria and Tensleep reservoirs were permitted for unlimited commingling in 1996 as well. In 1997, Merit began a capital workover program to downspace the Phosphoria reservoir to 10 acres in addition to improving the Tensleep and Phosphoria waterfloods and eliminating commingled production.

Under Merit’s operations, the wells in the Hamilton Dome field are produced via electric submersible pumps (ESP) and rod pumps. Typical workovers in the field include rod repair, ESP repair, injector acid jobs, and wellbore cleanouts.

At June 30, 2020, EPM has total net proved reserves of 1.47 MMBOE at Hamilton Dome which was entirely comprised of oil as estimated by our independent reservoir engineering firm. The following table sets forth our estimated proved reserves as of June 30, 2020 for our Hamilton Dome field. For additional reserve information see Note 21 to our consolidated financial statements in Item 8.

Reserve Category | Oil (MBbls) | NGLs (MBbls) | Total Reserves (MBOE)* | |||||

PROVED | ||||||||

Developed Producing (100% of Proved) | 1,473 | — | 1,473 | |||||

Undeveloped (0% of Proved) | — | — | — | |||||

TOTAL PROVED | 1,473 | — | 1,473 | |||||

Product Mix | 100 | % | — | % | 100 | % | ||

*Equivalent oil reserves are defined as six MCF of gas and 42 gallons of natural gas liquids to one barrel of oil conversion ratio which reflects energy equivalence and not price equivalence. Gas prices per MCF and NGL prices per barrel often differ significantly from the equivalent amount of oil.

Following acquisition in November 2019, average gross daily production was 2,048 BOPD through the end of fiscal 2020. From March to June 2020, the production rate was negatively impacted by an estimated 870 gross BOPD, or approximately 38%, due to the shut-in of 61 wells as a result of the drop in oil prices.

Estimated Oil and Natural Gas Reserves and Estimated Future Net Revenues

The SEC sets rules related to reserve estimation and disclosure requirements for oil and natural gas companies. These rules require disclosure of oil and gas proved reserves by significant geographic area, using the trailing 12-month average price,

5

calculated as the unweighted arithmetic average of the first-day-of-the-month price for each month within the 12-month period prior to the end of the reporting period, rather than year-end prices, and allows the use of new technologies in the determination of proved reserves if those technologies have been demonstrated empirically to lead to reliable conclusions about reserve volumes. Subject to limited exceptions, the rules also require that proved undeveloped reserves may only be classified as such if a development plan has been adopted indicating that they are scheduled to be drilled within five years.

There are numerous uncertainties inherent in estimating quantities of proved reserves and estimates of reserves quantities and values must be viewed as being subject to significant change as more data about the properties becomes available.

Summary of Oil & Gas Reserves for Fiscal Year Ended 2020

Our proved reserves at June 30, 2020, denominated in equivalent barrels using six MCF of gas and 42 gallons of natural gas liquids to one barrel of oil conversion ratio, were estimated by our independent reservoir engineer, DeGolyer and MacNaughton which was formed in 1936. D&M has completed more than 23,000 projects in more than 100 countries. D&M was selected to estimate reserves primarily due to their expertise in CO2-EOR projects and to ensure consistency with the operator of the Delhi field. The scope and results of their procedures are summarized in a letter from the firm, which is included as Exhibit 99.1 to this Annual Report on Form 10-K.

The following table sets forth our estimated proved reserves as of June 30, 2020. For additional reserve information see Note 21 to our consolidated financial statements in Item 8. The NYMEX previous 12-month unweighted arithmetic average first-day-of-the-month price used to calculate estimated revenues was $47.37 per barrel of crude oil. The net price per barrel of NGLs was $9.00, which does not have any single comparable reference index price. The NGL price was based on historical prices received. For periods for which no historical price information was available, we used comparable pricing in the geographic area. Pricing differentials were applied based on quality, processing, transportation, location and other pricing aspects for each individual property and product.

Reserves as of June 30, 2020

Reserve Category | Oil (MBbls) | NGLs (MBbls) | Total Reserves (MBOE)* | |||||

PROVED | ||||||||

Developed Producing (82% of Proved) | 6,578 | 1,777 | 8,355 | |||||

Undeveloped (18% of Proved) | 1,648 | 216 | 1,864 | |||||

TOTAL PROVED | 8,226 | 1,993 | 10,219 | |||||

Product Mix | 80 | % | 20 | % | 100 | % | ||

*Equivalent oil reserves are defined as six MCF of gas and 42 gallons of natural gas liquids to one barrel of oil conversion ratio which reflects energy equivalence and not price equivalence. Gas prices per MCF and NGL prices per barrel often differ significantly from the equivalent amount of oil.

.

6

The following table presents a reconciliation of changes in our proved reserves by major property, on the basis of equivalent MBOE quantities.

Reconciliation of Changes in Proved Reserves by Major Property

Delhi Field Proved Total | ||

Proved reserves, MBOE | MBOE | |

June 30, 2019 | 8,981 | |

Purchases | — | |

Production | (647 | ) |

Revisions (a) | 412 | |

Sales of minerals in place | — | |

Improved recovery, extensions and discoveries | — | |

June 30, 2020 | 8,746 | |

(a) Positive revisions of 412 MBOE at Delhi field reflect adjusted methodology of forecasting NGLs independently from the oil production forecast by our independent reservoir engineering firm.

Hamilton Dome Field Proved Total | ||

Proved reserves, MBOE | MBOE | |

June 30, 2019 | — | |

Purchases | 3,427 | |

Production | (98 | ) |

Revisions (a) | (1,856 | ) |

Sales of minerals in place | — | |

Improved recovery, extensions and discoveries | — | |

June 30, 2020 | 1,473 | |

(a) Negative revisions of 1,856 MBOE were due to the impacts of lower oil prices since the field’s November 2019 acquisition and to subsequent reduced rates of production. Responding to lower oil prices, in March, the operator shut in wells that were not economic to optimize the field's cash flow. Although some returned to production as prices improved, as of June 30, 2020, approximately 25% of the wells remained shut-in. The lowered historical production curve and lower SEC average price, resulted in the field reaching its economic limit sooner than it had when proved reserves were estimated at the acquisition date.

Internal Controls Over Reserves Estimation Process and Qualifications of Technical Persons with Oversight for the Company's Overall Reserve Estimation Process

Our policies regarding internal controls over reserves estimates require such estimates to be prepared by an independent petroleum engineering firm under the supervision of our President and Chief Executive Officer, Jason Brown, who has over 20 years of experience in the energy industry and is a Registered Professional Engineer (Petroleum) in the State of Texas. He earned his B.S. degree in chemical engineering from the University of Tulsa and his M.B.A. from the Mendoza School of Business at the University of Notre Dame. Such reserves estimates are in compliance with generally accepted petroleum engineering and evaluation principles, definitions, and guidelines as established by the SEC.

The reserves information in this filing is based on estimates prepared by D&M, our independent petroleum engineering firm, which was formed in 1936 and has completed more than 23,000 projects in more than 100 countries. The person responsible for preparing the reserves report with D&M is a Registered Professional Engineer in the State of Texas and a Vice President of the firm. He received a Bachelor of Science degree in petroleum engineering from the University of Texas in 1984, has over 35 years of experience in the energy industry and is a member of the Society of Petroleum Engineers and the Society of Petroleum Evaluation Engineers.

7

We provide D&M with our property interests, production, current operating costs, current production prices and other information in order to prepare the reserve estimates. This information is reviewed by our President and Chief Executive Officer, designated operations personnel, and other members of management to ensure accuracy and completeness of the data prior to submission to D&M. The scope and results of D&M's procedures, as well as their professional qualifications, are summarized in the letter included as Exhibit 99.1 to this Annual Report on Form 10-K.

Proved Undeveloped Reserves

Our proved undeveloped reserves were 1,864 MBOE at June 30, 2020, with associated future development costs of approximately $8.6 million, which are associated with the Phase V development of Delhi field. The Company does not have any proved undeveloped reserves associated with its Hamilton Dome field acquired in November of 2019.

During the year ended June 30, 2020 our proved undeveloped reserves changed as follows:

Oil (MBbls) | NGLs (MBbls) | Total Reserves (MBOE) | |||||||||

June 30, 2019 | 1,342 | 241 | 1,583 | ||||||||

Revisions to previous estimates | 306 | (25 | ) | 281 | |||||||

Conversion to proved developed reserves | — | — | — | ||||||||

June 30, 2020 | 1,648 | 216 | 1,864 | ||||||||

Price declines resulted in a reclassification of a small volume of oil reserves from PDP to PUD at June 30, 2020. The decline in price led to currently producing wells becoming uneconomic at an earlier point in time than previously estimated. However, when forecasted in conjunction with the PUD reserves the overall economic life of the field is extended. Due to the EOR unit nature of Delhi, this PDP reduction shifts those reserves to our PUD oil reserves as they are considered proved and expected to be recovered as a result of the development of our Phase V. NGL reserves were revised downward 25 MBbls primarily due to the adjusted methodology of projecting NGL volumes independent of oil production, shifting them into developed NGL volumes. The infill program, consisting of ten producer wells and two CO2 injection wells, was completed during 2019 resulting in the conversion of 463 MBbls of oil and and 73 MBOE of NGLs from proved undeveloped reserves to proved developed reserves. Since this project's inception in March 2018, its net capital expenditures have totaled $4.6 million.

The initial assignment of proved undeveloped reserves in the Delhi field was made on June 30, 2010, which encompassed a large scale CO2 enhanced oil recovery project. The operator’s development plans for the field have remained essentially unchanged and were originally scheduled to be completed by June 30, 2015, within five years from the initial recording of such proved reserves. However, as a result of the adverse fluid release event in the field in June 2013 and the resulting delay in reversion of our working interest, development of the field has not proceeded as originally scheduled. Expansion of the CO2 flood to the remaining undeveloped eastern portion of the field commenced subsequent to reversion of our working interest in late calendar 2014. We incurred $3.8 million of capital expenditures before the operator electively deferred this project as a result of a reduction in its cash flows and capital spending from the significant drop in oil prices. This project was further electively deferred as we began work on the NGL recovery plant field in February 2015. It was determined that the economics of development of the remaining eastern portion of the field would be significantly improved after the NGL plant was completed.

During fiscal 2015, we authorized the NGL plant project and from late in that fiscal year until January 2017 when production of NGLs began, we incurred $26.0 million of related capital expenditures. The NGL plant was completed in December 2016 and we converted approximately 1,377 MBOE of proved undeveloped reserves to proved developed reserves during fiscal 2017.

Since completion of the plant, we have resumed work that had been suspended in late 2014 and further deferred until the NGL recovery plant was complete. Cumulatively, we have spent $3.7 million as of June 30, 2020, including $0.6 million and $1.6 million in fiscal years 2020 and 2019, respectively, on the six well water curtain program and related infrastructure required to precede the development of Phase V. As of June 30, 2020 we had drilled all the injection wells, including four gross injection wells during fiscal 2019, and commenced operations for one of the program's pads. The program was configured as two pads, each having two injection wells and one water source well. The second pad was completed during fiscal 2020 and began injections during our second quarter of fiscal 2020.

As of June 30, 2020, we have estimated total future net capital expenditures of approximately $8.6 million for remaining curtain infrastructure and development of Phase V in the eastern part of the field, which we expect to commence in May 2021 based on our discussions with the operator. The timing of Phase V development is dependent on the field operator's available funds and capital spending plans and priorities within its portfolio of properties.

8

We believe this project is economic in the current oil price environment and we expect it to be completed within the next four fiscal years. We have been continuously developing the Delhi field and have spent over $48 million subsequent to reversion of our working interest in November 2014. Given the long-term nature of CO2 EOR development projects, we believe that the remaining undeveloped reserves in the Delhi field satisfy the conditions to continue to be treated as proved undeveloped reserves because (1) we initially established the development plan for the Delhi field in 2010 and continue to follow that plan, as adjusted to incorporate the completion of the NGL plant in late 2016 and delays relating to the 2013 adverse fluid release event; (2) we have had significant ongoing development activities at this project that, as budgeted and currently being expended, reflect a significant and sufficient portion of remaining capital expenditures to convert proved undeveloped reserves to proved developed reserves; and (3) the operator has a historical record of completing the development of comparable long-term projects.

As of June 30, 2020, no proved reserves were attributed to (a) the area beneath the inhabited portion of the town of Delhi in the northeast and (b) the farthest east of the two remaining undeveloped sites in the eastern portion of the field (Phase VI) due to the current economics and other technical aspects of our future development plans. In addition, no proved reserves are currently attributed to three smaller reservoirs within the Unit in similar formations with similar production history due to the lower oil price utilized in our reserves calculation. We also do not have any proved reserves associated with our interests in the Mengel Sand, a separate interval within the Unit that is not currently producing, but has produced oil in the past.

Sales Volumes, Average Sales Prices and Average Production Costs

The following table shows the Company's sales volumes and average sales prices received for crude oil, natural gas liquids, and natural gas for the periods indicated:

Year Ended June 30, 2020 | Year Ended June 30, 2019 | Year Ended June 30, 2018 | |||||||||||||||||||||

Product | Volume | Price | Volume | Price | Volume | Price | |||||||||||||||||

Crude oil (Bbls) | 638,464 | $ | 44.76 | 626,879 | $ | 65.05 | 651,931 | $ | 58.52 | ||||||||||||||

Natural gas liquids (Bbls) | 106,159 | $ | 9.59 | 112,013 | $ | 21.87 | 93,366 | $ | 28.06 | ||||||||||||||

Natural gas (Mcf) | 1,087 | $ | 1.90 | 459 | $ | 2.64 | — | $ | — | ||||||||||||||

Average price per BOE* | 744,804 | $ | 39.74 | 738,968 | $ | 58.50 | 745,297 | $ | 54.71 | ||||||||||||||

Production costs | Amount | per BOE | Amount | per BOE | Amount | per BOE | |||||||||||||||||

Production costs, excluding ad valorem and production taxes | $ | 12,966,923 | $ | 17.41 | $ | 14,027,461 | $ | 18.98 | $ | 11,497,759 | $ | 15.43 | |||||||||||

Total production costs, including ad valorem and production taxes | $ | 13,505,502 | $ | 18.13 | $ | 14,266,784 | $ | 19.31 | $ | 11,685,817 | $ | 15.68 | |||||||||||

*Equivalent oil reserves are defined as six MCF of gas and 42 gallons of natural gas liquids to one barrel of oil conversion ratio which reflects energy equivalence and not price equivalence. Gas prices per MCF and NGL prices per barrel often differ significantly from the equivalent amount of oil.

Drilling Activity

Our productive drilling activity during the past three fiscal years at Delhi field ended June 30, 2020, and was limited to five gross (1.2 net) producer wells drilled and completed in fiscal 2019 and another five (1.2 net) producer wells completed in fiscal 2018. We completed one (0.239 net) CO2 injection well during fiscal 2019 and completed one (0.239 net) CO2 injection well during fiscal 2018. No dry wells were drilled in the past three fiscal years.

In connection with establishing a six-well water curtain in advance of Phase V site development, during fiscal 2019 we drilled two (0.48 net) wells and completed three (0.72 net) wells. In fiscal 2018, we drilled three (0.72 net) wells and in fiscal 2017 one (0.239 net) well was drilled. A pad consists of one gross water source well and two gross water injector wells. The three completed wells comprise the northern pad of the water curtain program which commenced injection during fiscal 2019. The southern pad became fully operational late in the second quarter of fiscal 2020 when capital expenditures for completion work concluded.

Hamilton Dome field is considered fully developed. No wells were drilled in fiscal 2020 and there are no plans to drill wells in fiscal 2021.

9

Present Activities

The operator is completing a SCADA (supervisory control and data acquisition) well monitoring capital project at present which will improve the flow of information and assist in the real-time management of the Delhi field. There are no significant drilling plans until Phase V development, expected to commence in the fourth quarter of fiscal 2021.

For further discussion, see "Highlights for our fiscal year 2020" and "Capital Expenditures" within Item 7.

Delivery Commitments

As of June 30, 2020, we were not committed to provide a fixed and determinable quantity of oil, NGLs or gas under existing agreements, nor do we currently intend to enter into any such agreements.

If the price of oil remains above $32.00, we have a financial commitment as we entered into NYMEX WTI oil swaps covering approximately 42,000 barrels per month for the period of April 2020 through December 2020 at a fixed swap price of $32.00 per barrel.

Productive Wells

The following table sets forth the number of productive oil and gas wells in which we own a working interest as of June 30, 2020.

Company Operated | Non-Operated | Total | |||||||||||||||

Gross | Net | Gross | Net | Gross | Net | ||||||||||||

Crude oil | — | — | 315 | 74.5 | 315 | 74.5 | |||||||||||

Natural gas | — | — | — | — | — | — | |||||||||||

Total | — | — | 315 | 74.5 | 315 | 74.5 | |||||||||||

Acreage Data

The following table sets forth certain information regarding our developed and undeveloped lease acreage as of June 30, 2020. Developed acreage refers to acreage on which wells have been drilled or completed to a point that would allow production of oil and gas in commercial quantities. Undeveloped acreage refers to acreage on which wells have not been drilled or completed to a point that would permit production of oil and gas in commercial quantities whether or not the acreage contains proved reserves.

Field (1) | Developed Acreage | Undeveloped Acreage | Total | ||||||||||||||

Gross | Net | Gross | Net | Gross | Net | ||||||||||||

Delhi Field, Louisiana (2) | 9,126 | 2,180 | 4,510 | 1,077 | 13,636 | 3,257 | |||||||||||

Hamilton Dome Field, Wyoming | 5,908 | 1,389 | — | — | 5,908 | 1,389 | |||||||||||

Total | 15,034 | 3,569 | 4,510 | 1,077 | 19,544 | 4,646 | |||||||||||

(1) All acreage, including any undeveloped, nonproductive or undrilled acreage, is held by existing production as long as continuous production is maintained in the unit.

(2) This table excludes acreage attributable to small overriding royalty interests retained in various formations in the Texas Giddings Field area. Except for de minimis production that began on two leases during later fiscal 2019, none of such acreage is currently producing and our interests are subject to expiration if leases are not maintained by others or commercial production is not established. It does not currently appear likely that we will obtain any significant value from these interests and no reserves have been assigned to any of the Giddings interests.

When the Company acquired the Delhi field in 2003, the field had been fully developed through primary and secondary recovery and all of such acreage was reflected as developed acreage. With the addition of a CO2-EOR project in the field, certain acreage is now reflected as undeveloped using tertiary recovery operations. We estimate that our developed acreage currently includes 9,126 gross (2,180 net) acres in the Delhi field, with approximately 4,510 gross (1,077 net) acres attributable to the remaining undeveloped areas in the eastern part of the field. We own a 23.9% working interest in the field, along with certain mineral and royalty interests. We are not the operator of the EOR project.

10

Our interests include all depths from the surface of the earth to the top of the Massive Anhydride, including the Delhi Holt Bryant Unit, which is currently under CO2 flood, and the Mengel Sand Interval, which is within the boundary of the field, but is currently not producing. As the Delhi field is unitized per the State of Louisiana Department of Conservation order number 96-G-5, all acreage, including any undeveloped, nonproductive or undrilled acreage is held by existing production as long as continuous production is maintained in the unit.

When the Company acquired Hamilton Dome field on November, 1 2019, the field had been fully developed through primary recovery and all acreage is reflected as developed acreage. The Tensleep and Phosphoria were permitted for commingling and unitized in 1996 following purchase of the field by Merit Energy. The Company estimates that our developed acreage includes 5,908 gross (1,389 net) acres in the Hamilton Dome field, with no acres attributable as undeveloped. We own 23.5% working interest in the field, along with a small overriding royalty interest. As Hamilton Dome is unitized, all acreage is held by existing production as long as continuous production is maintained in the unit. We are not operators of Hamilton Dome field.

For more complete information regarding current year activities, including crude oil and natural gas production, refer to Item 7.

Markets and Customers

Our production is marketed to third parties in a manner consistent with industry practices. In the United States of America market, where we operate, crude oil and natural gas liquids are readily transportable and marketable. We do not currently market our share of crude oil production from Delhi nor from Hamilton Dome separately from the operators' shares of production. Although we have the right to take our working interest production in-kind, we are currently selling our production through the field operators pursuant to the delivery and pricing terms of their sales contracts. Under such arrangements we typically do not know the identity of the buyers of production except in the case of the Delhi field where there is a sole buyer for oil and another for NGL's.

The oil from Delhi is currently transported from the field by pipeline, which results in better net pricing than the alternative of transportation by truck. Delhi crude oil production sells at Louisiana Light Sweet ("LLS") pricing which generally trades at a premium to West Texas Intermediate ("WTI") crude oil pricing. The positive LLS Gulf Coast average price differential over WTI, as quoted daily on the New York Mercantile Exchange ("NYMEX"), was approximately $0.77 per barrel during our fiscal year ended June 30, 2020, compared to $4.11 per barrel for the prior year. In the current fiscal year, the differential was impacted by market conditions over the second half of the fiscal year and trucking charges that were incurred for several months while the sales pipeline underwent repair. NGL production is sold to a midstream processing company which fractionates the stream and sells the resulting hydrocarbons.

On November 1, 2019, Evolution acquired a non-operated interest in the Hamilton Dome field in Wyoming. All the field’s production is sour heavy crude oil which is the sole component of the field’s reserves. Crude oil is transported by pipeline primarily to purchasers in Casper, Wyoming. As a result of transportation differentials, the high sulfur content and low API gravity, this crude trades at a discount to WTI, averaging $17.62 lower over the last eight months. Although we have the option of taking our production in kind, we have elected to have the operator market our share of production. Our realized price is net of transportation and marketing costs.

The following table sets forth purchasers of our oil and natural gas liquid production for the years indicated:

Year Ended June 30, | |||||

Customer | 2020 | 2019 | |||

Plains Marketing L.P. (Delhi field oil) | 87 | % | 94 | % | |

Merit Energy Company (Hamilton Dome field oil) | 10 | % | — | % | |

Third Coast Midstream (Delhi field NGLs) | 3 | % | 6 | % | |

All others | — | % | — | % | |

Total | 100 | % | 100 | % | |

The loss of a purchaser at either the Delhi or Hamilton Dome fields or disruption to pipeline transportation from these fields could adversely affect our net realized pricing and potentially our near-term production levels.

11

Market Conditions

Marketing of crude oil, natural gas, and natural gas liquids and the prices we receive are influenced by many factors that are beyond our control, the exact effect of which is difficult to predict. These factors include changes in supply and demand, market prices, government regulation and actions of major foreign producers.

Oil prices over the past few years have fluctuated and been extremely volatile. For example, average daily prices for WTI crude oil ranged from a high of $74 per barrel to a low of a negative $38 per barrel over our past few fiscal years. Starting in the fourth quarter of 2014, the price of oil per barrel dropped dramatically and continuing into 2017 before recovering somewhat in late calendar 2018, then weakening again in 2019 and dropping substantially in 2020 as a result of the impact of the COVID-19 pandemic and geopolitical factors. Worldwide factors such as global health pandemics, geopolitical, international trade disruptions and tariffs, macroeconomic, supply and demand, refining capacity, petrochemical production and derivatives trading, among others, influence prices for crude oil. Local factors also influence prices for crude oil and include increasing or decreasing production trends, quality differences, regulation and transportation issues unique to certain producing regions and reservoirs.

Competition

The oil and natural gas industry is highly competitive for prospects, acreage and capital. Our competitors include major integrated crude oil and natural gas companies, numerous independent crude oil and natural gas companies, individuals, and drilling and income programs. Many of our competitors are large, well-established companies with substantially larger operating staffs and greater capital resources. Competitors are national, regional or local in scope and compete on the basis of financial resources, technical prowess or local knowledge. The principal competitive factors in our industry are expertise in given geographical areas and geological systems and the abilities to efficiently conduct operations, achieve technological advantages, identify, and acquire economically producible reserves and obtain capital at rates which allow economic investments.

Risk Management

Derivative instruments are occasionally utilized to hedge our exposure to price fluctuations and reduce the variability in our cash flows associated with anticipated sales of future oil and natural gas production. We have designed a risk management policy to use derivative instruments from time to time during periods of extraordinary price volatility and when such instruments are needed to ensure the Company can meet its current dividend policy, fund its capital expenditures commitments and maintain liquidity. We determine the duration of derivative positions to approximate the anticipated period of volatility and the percentage of our production to be hedged, based on our view of current and future market conditions. We do not enter into derivative contracts for speculative trading purposes.

While there are many different types of derivatives available, we typically use fixed-price swap and costless collars to attempt to manage price risk. The fixed-price swap agreements call for payments to, or receipts from, counterparties depending on whether the index price of oil or natural gas for the period is greater or less than the fixed price established for the period contracted under the fixed-price swap agreement. Costless collar agreements are put and call options used to establish floor and ceiling commodity prices for a fixed volume of production during a certain time period. All costless collar agreements provide for payments to counterparties if the settlement price under the agreement exceeds the ceiling and payments from the counterparties if the settlement price under the agreement is below the floor.

We entered into NYMEX WTI oil swaps covering approximately 42,000 barrels per month for the period of April 2020 through December 2020 at a fixed swap price of $32.00 per barrel. In the future we may add additional swaps or other derivative positions covering a variable portion of our anticipated future production during subsequent periods.

It is our policy to enter into derivative contracts only with counterparties that are creditworthy financial institutions deemed by management as competent and competitive market makers. As of June 30, 2020, we did not post collateral under any of our derivative contracts as they are uncollateralized trades. We will continue to evaluate the benefit of employing derivatives in the future. See Item 7A and Note 19 to our consolidated financial statements in Item 8 for additional information.

Government Regulation

Numerous federal and state laws and regulations govern the oil and gas industry, including environmental laws and regulations. These laws and regulations are often changed in response to changes in the political or economic environment. Compliance with this evolving regulatory environment is often difficult and costly; substantial penalties may be incurred for noncompliance. To the best of our knowledge, we are in compliance with all federal and state-level laws and regulations applicable to our operations. The future annual capital cost of complying with the regulations applicable to our operations is

12

uncertain and will be governed by several factors, including future changes to regulatory requirements which are unpredictable. We do not currently anticipate that continued and future compliance with existing laws and regulations will have a materially adverse effect on our consolidated financial position or results of operations.

See discussion captioned "Government regulation and liability for oil and gas operations and environmental matters may adversely affect our business and results of operations" in Item 1A.

Insurance

We maintain insurance on our oil and gas properties and operations for risks and in amounts customary in the industry. Such insurance includes general liability, excess liability, control of well, operators extra expense, casualty, fraud and directors and officer's liability coverage. Not all losses are insured, and we retain certain risks of loss through deductibles, limits and self-retentions. We do not carry lost profits coverage and we do not have coverage for consequential damages.

Employment

At June 30, 2020, we had four full-time employees, not including contract personnel and outsourced service providers. None of the Company’s employees are currently represented by a union, and the Company believes that it has excellent relations with its employees. Our team is broadly experienced in oil and gas operations, development, acquisitions and financing. We follow a strategy of outsourcing most of our property accounting, human resources, administrative and other non-core functions.

Additional Information

We file Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other reports with the Securities and Exchange Commission ("SEC") . Our reports filed with the SEC are available free of charge to the general public through our website at www.evolutionpetroleum.com. These reports are accessible on our website as soon as reasonably practicable after being filed with, or furnished to, the SEC. This Annual Report on Form 10-K and our other filings can also be obtained by contacting: Corporate Secretary, 1155 Dairy Ashford Road, Suite 425, Houston, Texas 77079, or calling (713) 935-0122. These reports are also available at the SEC Public Reference Room at 450 Fifth Street, N.W., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website at www.sec.gov that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

13

Item 1A. Risk Factors

Our business involves a high degree of risk. If any of the following risks, or any risk described elsewhere in this Annual Report on Form 10-K, actually occurs, our business, financial condition or results of operations could suffer. The risks described below are not the only ones facing us. Additional risks not presently known to us or which we currently consider to be immaterial also may adversely affect us.

Risks related to the oil and gas industry and our Company

A substantial or extended decline in oil prices may adversely affect our business, financial condition or results of operations and our ability to meet our capital expenditure obligations and financial commitments.

The price we receive for our oil significantly influences our revenue, profitability, access to capital, and future rate of growth. Oil is a commodity and its price is subject to wide fluctuations in response to relatively minor changes in supply and demand. For example, average daily prices for WTI crude oil ranged from a high of $74 per barrel to a low of a negative $38 per barrel over our past few fiscal years. Historically, the markets for oil and natural gas liquids have been volatile and these markets will likely continue to be volatile in the future. The prices we receive for our production depend on numerous factors beyond our control, including, but not limited to the following:

• | changes in global supply and demand for oil and natural gas, which has recently been negatively affected by concerns about the impact of COVID-19; |

• | worldwide and regional economic conditions impacting the global supply and demand for oil and gas; |

• | actions of OPEC or other groups of oil producing nations; |

• | the price and quantity of imports of foreign oil and natural gas; |

• | political conditions in or affecting other oil-producing and natural gas-producing countries; |

• | the level of global oil and natural gas exploration and production; |

• | the level of global oil and natural gas inventories; |

• | localized supply and demand fundamentals of regional, domestic and international transportation availability; |

• | weather conditions and natural disasters; |

• | domestic and foreign governmental regulations; |

• | speculation as to the future price of oil and the speculative trading of oil and natural gas futures contracts; |

• | price and availability of competitors' supplies of oil and natural gas; |

• | technological advances affecting energy consumption; and |

• | the price and availability of alternative fuels. |

Substantially all of our production is sold to purchasers under short-term (less than 12-month) contracts at market-based prices. A decline in oil and natural gas liquids prices will reduce our cash flows, borrowing ability, the present value of our reserves, and our ability to develop future reserves. We may be unable to obtain needed capital or financing on satisfactory terms. Low oil and natural gas liquids prices may also reduce the amount of oil and natural gas liquids that we can produce economically, which could lead to a decline in our oil and natural gas liquids reserves. Because approximately 80% of our proved reserves at June 30, 2020 are crude oil reserves and 20% are natural gas liquids reserves, we are heavily impacted by movements in crude oil prices, which also influence natural gas liquids prices. To the extent that we have not hedged our production with derivative contracts or fixed-price contracts, any significant and extended decline in oil and natural gas liquids prices may adversely affect our financial position.

Our revenues are concentrated in two assets and related declines in production or other events beyond our control could have a material adverse effect on our results of operations and financial results.

Our revenues come from our royalty, mineral and working interests in the Delhi field in Louisiana and the Hamilton Dome field in Wyoming and thus our current revenues are highly concentrated in these fields. Any significant downturn in production, oil and NGL prices, or other events beyond our control which impact these fields could have a material adverse effect on our results of operations and financial results. We are not the operator of these fields, and our revenues and future growth are heavily dependent on the success of operations, which we do not control.

Operating results from oil and natural gas production may decline; we may be unable to acquire and develop the additional oil and natural gas reserves that are required in order to sustain our business operations.

In general, the volumes of production from crude oil and natural gas properties decline as reserves are depleted, with the rate of decline depending on reservoir characteristics. Except to the extent we acquire additional properties containing proved reserves or conduct successful development activities, or both, our proved reserves will decline. Our production is heavily dependent on our interests in EOR production that began during March 2010 in the Delhi field and our newly acquired interests in the

14

Hamilton Dome field in Wyoming. Environmental or operating problems or lack of extended future investment in either of these fields could cause our net production of oil and natural gas liquids to decline significantly over time, which could have a material adverse effect on our financial condition. In fiscal 2020, our production was impacted by the operators of both fields. Delhi production volumes were negatively impacted as a result of the financial strain Denbury was under and their lack of investment in projects in the field, including the delay of our Phase V, in addition to the purchased CO2 line being shut in for repairs. In the Hamilton Dome field Merit temporarily shut in a portion of the production as it was uneconomic at the historically low prices. As of June 30, 2020, a number of these wells have returned to production and we continue to monitor their performance; however, there is no guarantee that prolonged periods of being shut in or lack of investment would not negatively impact future production.

We have limited control over the activities on properties we do not operate.

Substantially, all of our property interests are not operated by the Company and also involve other third-party working interest owners. As a result, we have limited ability to influence or control the operation or future development of such properties, including compliance with environmental, safety and other regulations, or the amount of capital expenditures that we will be required to fund with respect to such properties. Operators of these properties may act in ways that are not in our best interest. Moreover, we are dependent on the other working interest owners of such projects to fund their contractual share of the capital expenditures of such projects. These limitations and our dependence on the operator and other working interest owners for these projects could cause us to incur unexpected future costs, result in lower production, and materially and adversely affect our financial conditions and results of operations.

We are materially dependent upon our operators with respect to the successful operation of our principal assets, which consists of our interests Delhi and Hamilton Dome fields. A materially negative change in our operator’s financial condition could negatively affect operations (or timing thereof) in these fields, and consequently our income (or timing thereof) from these fields as well as the value of our interests in these fields.