Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - Benefit Street Partners Realty Trust, Inc. | bsprt-exhibit312_q220.htm |

| EX-32 - EXHIBIT 32 - Benefit Street Partners Realty Trust, Inc. | bsprt-exhibit32_q2.htm |

| EX-31.1 - EXHIBIT 31.1 - Benefit Street Partners Realty Trust, Inc. | bsprt-exhibit311_q220.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One) | |

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2020

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000-55188

BENEFIT STREET PARTNERS REALTY TRUST, INC.

(Exact name of registrant as specified in its charter)

Maryland | 46-1406086 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

9 West 57th Street, Suite #4920 New York, New York | 10019 | |

(Address of Principal Executive Office) | (Zip Code) | |

(212) 588-6770

(Registrant’s Telephone Number, Including Area Code)

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

None | ||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act:

Large accelerated filer o | Accelerated filer o |

Non-accelerated filer x | Smaller reporting company o |

Emerging growth filer o | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The number of shares of the registrant's common stock, $0.01 par value, outstanding as of July 31, 2020 was 44,339,023.

BENEFIT STREET PARTNERS REALTY TRUST, INC.

TABLE OF CONTENTS

Page | ||

i

PART I

Item 1. Consolidated Financial Statements and Notes (unaudited)

1

BENEFIT STREET PARTNERS REALTY TRUST, INC.

CONSOLIDATED BALANCE SHEETS

(In thousands, except share and per share data)

June 30, 2020 | December 31, 2019 | ||||||

ASSETS | (Unaudited) | ||||||

Cash and cash equivalents | $ | 111,631 | $ | 87,246 | |||

Restricted cash | 15,479 | 21,876 | |||||

Commercial mortgage loans, held for investment, net of allowance of $26,244 and $921 as of June 30, 2020 and December 31, 2019, respectively | 2,468,670 | 2,762,042 | |||||

Commercial mortgage loans, held-for-sale, measured at fair value | 69,879 | 112,562 | |||||

Real estate securities, available for sale, measured at fair value, amortized cost of $436,878 and $387,294 as of June 30, 2020 and December 31, 2019, respectively | 408,612 | 386,316 | |||||

Derivative instruments, measured at fair value | 133 | 1,119 | |||||

Other real estate investments, measured at fair value | 2,514 | 2,557 | |||||

Receivable for loan repayment (1) | 173,465 | 89,317 | |||||

Accrued interest receivable | 15,308 | 16,308 | |||||

Prepaid expenses and other assets | 4,853 | 5,322 | |||||

Intangible lease asset, net of amortization | 13,959 | 14,377 | |||||

Operating right of use asset, net of amortization | 5,825 | 5,979 | |||||

Real estate owned, net of depreciation | 35,758 | 35,333 | |||||

Real estate owned, held-for-sale | 14,000 | — | |||||

Receivable for unsettled trades | — | 266 | |||||

Total assets | $ | 3,340,086 | $ | 3,540,620 | |||

LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||

Collateralized loan obligations | $ | 1,697,666 | $ | 1,803,185 | |||

Repurchase agreements - commercial mortgage loans | 226,224 | 252,543 | |||||

Repurchase agreements - real estate securities | 335,256 | 394,359 | |||||

Mortgage note payable | 40,241 | 29,167 | |||||

Other financing and loan participation - commercial mortgage loans | 18,771 | — | |||||

Derivative instruments, measured at fair value | 4,589 | 1,581 | |||||

Interest payable | 3,566 | 4,958 | |||||

Distributions payable | 15,570 | 6,912 | |||||

Accounts payable and accrued expenses | 19,632 | 10,925 | |||||

Due to affiliates | 9,545 | 4,789 | |||||

Operating lease liabilities | 6,217 | 6,136 | |||||

Deferred rent revenue | — | 150 | |||||

Total liabilities | $ | 2,377,277 | $ | 2,514,705 | |||

Commitment and contingencies (See Note 10) | |||||||

Redeemable convertible preferred stock Series A, $0.01 par value, 60,000 authorized and 40,514 and 40,500 issued and outstanding as of June 30, 2020 and December 31, 2019, respectively | $ | 202,253 | $ | 202,144 | |||

Redeemable convertible preferred stock Series C, $0.01 par value, 20,000 authorized and 1,400 issued and outstanding as of June 30, 2020 and December 31, 2019, respectively | 6,960 | 6,966 | |||||

Equity: | |||||||

Preferred stock, $0.01 par value, 50,000,000 authorized, none issued and outstanding as of June 30, 2020 and December 31, 2019 | — | — | |||||

Common stock, $0.01 par value, 949,999,000 shares authorized, 44,395,816 and 43,916,815 shares issued and outstanding as of June 30, 2020 and December 31, 2019, respectively | 445 | 441 | |||||

Additional paid-in capital | 910,706 | 903,310 | |||||

Accumulated other comprehensive income (loss) | (28,266 | ) | (978 | ) | |||

Accumulated deficit | (129,289 | ) | (85,968 | ) | |||

Total stockholders' equity | $ | 753,596 | $ | 816,805 | |||

Total liabilities, redeemable convertible preferred stock and stockholders' equity | $ | 3,340,086 | $ | 3,540,620 | |||

(1) Includes $173.5 million and $89.3 million of cash held by servicer related to loan payoffs pledged to the CLOs as of June 30, 2020 and December 31, 2019, respectively.

The accompanying notes are an integral part of these unaudited consolidated financial statements.

2

BENEFIT STREET PARTNERS REALTY TRUST, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(In thousands, except share and per share data)

(Unaudited)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2020 | 2019 | 2020 | 2019 | ||||||||||||

Income: | |||||||||||||||

Interest income | $ | 43,241 | $ | 48,225 | $ | 91,095 | $ | 94,736 | |||||||

Less: Interest expense | 15,135 | 25,869 | 39,627 | 46,235 | |||||||||||

Net interest income | 28,106 | 22,356 | 51,468 | 48,501 | |||||||||||

Revenue from real estate owned | 828 | — | 2,457 | — | |||||||||||

Total Income | $ | 28,934 | $ | 22,356 | $ | 53,925 | $ | 48,501 | |||||||

Expenses: | |||||||||||||||

Asset management and subordinated performance fee | 3,738 | 3,805 | 7,650 | 7,449 | |||||||||||

Acquisition expenses | 175 | 270 | 317 | 518 | |||||||||||

Administrative services expenses | 2,940 | 3,556 | 7,052 | 7,519 | |||||||||||

Professional fees | 3,222 | 2,568 | 6,006 | 4,663 | |||||||||||

Real estate owned operating expenses | 1,096 | — | 2,741 | — | |||||||||||

Depreciation and amortization | 586 | — | 1,174 | — | |||||||||||

Other expenses | 1,055 | 836 | 2,642 | 1,732 | |||||||||||

Total expenses | $ | 12,812 | $ | 11,035 | $ | 27,582 | $ | 21,881 | |||||||

Other (income)/loss: | |||||||||||||||

Increase/(decrease) for credit losses | 4,042 | 573 | 18,639 | 3,068 | |||||||||||

Impairment losses on real estate owned assets | — | — | 398 | — | |||||||||||

Realized (gain)/loss on extinguishment of debt | (438 | ) | — | (438 | ) | — | |||||||||

Realized (gain)/loss on sale of real estate securities | 5,309 | — | 5,747 | — | |||||||||||

Realized (gain)/loss on sale of commercial mortgage loan held-for-sale | (252 | ) | — | (252 | ) | 25 | |||||||||

Realized (gain)/loss on sale of commercial mortgage loan, held-for-sale, measured at fair value | 238 | (7,237 | ) | (9,166 | ) | (18,418 | ) | ||||||||

Unrealized (gain)/loss on commercial mortgage loans, held-for-sale, measured at fair value | (1,595 | ) | (568 | ) | 339 | (232 | ) | ||||||||

Unrealized (gain)/loss on other real estate investments, measured at fair value | (18 | ) | — | 43 | — | ||||||||||

Unrealized (gain)/loss on derivatives | 99 | 2,004 | 4,935 | 3,070 | |||||||||||

Realized (gain)/loss on derivatives | 1,659 | 1,626 | 8,328 | 3,084 | |||||||||||

Total other (income)/loss | $ | 9,044 | $ | (3,602 | ) | $ | 28,573 | $ | (9,403 | ) | |||||

Income/(loss) before taxes | 7,078 | 14,923 | (2,230 | ) | 36,023 | ||||||||||

Provision/(benefit) for income tax | (736 | ) | 397 | (2,644 | ) | 1,607 | |||||||||

Net income/(loss) | $ | 7,814 | $ | 14,526 | $ | 414 | $ | 34,416 | |||||||

Net income/(loss) applicable to common stock | $ | 4,359 | $ | 11,036 | $ | (7,556 | ) | $ | 27,606 | ||||||

Basic earnings per share | $ | 0.10 | $ | 0.27 | $ | (0.17 | ) | $ | 0.68 | ||||||

Diluted earnings per share | $ | 0.10 | $ | 0.27 | $ | (0.17 | ) | $ | 0.68 | ||||||

Basic weighted average shares outstanding | 44,376,437 | 41,226,805 | 44,319,531 | 40,516,456 | |||||||||||

Diluted weighted average shares outstanding | 44,389,380 | 41,239,548 | 44,319,531 | 40,529,371 | |||||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

3

BENEFIT STREET PARTNERS REALTY TRUST, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(In thousands)

(Unaudited)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2020 | 2019 | 2020 | 2019 | ||||||||||||

Net income/(loss) | $ | 7,814 | $ | 14,526 | $ | 414 | $ | 34,416 | |||||||

Unrealized gain/(loss) on available-for-sale securities | 40,319 | (65 | ) | (27,288 | ) | 80 | |||||||||

Comprehensive income/(loss) attributable to Benefit Street Partners Realty Trust, Inc. | $ | 48,133 | $ | 14,461 | $ | (26,874 | ) | $ | 34,496 | ||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

4

BENEFIT STREET PARTNERS REALTY TRUST, INC.

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY

(In thousands, except share data)

(Unaudited)

Common Stock | ||||||||||||||||||||||

Number of Shares | Par Value | Additional Paid-In Capital | Accumulated Other Comprehensive Income/(Loss) | Accumulated Deficit | Total Stockholders' Equity | |||||||||||||||||

Balance, December 31, 2019 | 43,916,815 | $ | 441 | $ | 903,310 | $ | (978 | ) | $ | (85,968 | ) | $ | 816,805 | |||||||||

Issuance of common stock | 650,034 | 7 | 10,855 | — | — | 10,862 | ||||||||||||||||

Common stock repurchases | (361,829 | ) | (4 | ) | (6,711 | ) | — | — | (6,715 | ) | ||||||||||||

Common stock issued through distribution reinvestment plan | 191,326 | 1 | 3,548 | — | — | 3,549 | ||||||||||||||||

Share-based compensation | — | — | 39 | — | — | 39 | ||||||||||||||||

Offering costs | — | — | (136 | ) | — | — | (136 | ) | ||||||||||||||

Net income/(loss) | — | — | — | — | (7,400 | ) | (7,400 | ) | ||||||||||||||

Distributions declared | — | — | — | — | (20,371 | ) | (20,371 | ) | ||||||||||||||

Cumulative-effect adjustment upon adoption of ASU 2016-13 (Note 2) | — | — | — | — | (7,761 | ) | (7,761 | ) | ||||||||||||||

Other comprehensive income/(loss) | — | — | — | (67,607 | ) | — | (67,607 | ) | ||||||||||||||

Balance, March 31, 2020 | 44,396,346 | $ | 445 | $ | 910,905 | $ | (68,585 | ) | $ | (121,500 | ) | $ | 721,265 | |||||||||

Issuance of common stock | — | $ | — | $ | 25 | $ | — | $ | — | $ | 25 | |||||||||||

Common stock repurchases | (11,306 | ) | — | (192 | ) | — | — | (192 | ) | |||||||||||||

Common stock issued through distribution reinvestment plan | 6 | — | (57 | ) | — | — | (57 | ) | ||||||||||||||

Share-based compensation | 10,770 | — | 57 | — | — | 57 | ||||||||||||||||

Offering costs | — | (32 | ) | (32 | ) | |||||||||||||||||

Net income/(loss) | — | — | — | — | 7,814 | 7,814 | ||||||||||||||||

Distributions declared | — | — | — | — | (15,603 | ) | (15,603 | ) | ||||||||||||||

Other comprehensive income/(loss) | — | — | — | 40,319 | — | 40,319 | ||||||||||||||||

Balance, June 30, 2020 | 44,395,816 | $ | 445 | $ | 910,706 | $ | (28,266 | ) | $ | (129,289 | ) | $ | 753,596 | |||||||||

Balance, December 31, 2018 | 39,303,710 | $ | 395 | $ | 827,558 | $ | (459 | ) | $ | (94,266 | ) | $ | 733,228 | |||||||||

Issuance of common stock | 1,161,580 | 11 | 19,398 | — | — | 19,409 | ||||||||||||||||

Common stock repurchases | (387,530 | ) | (4 | ) | (7,203 | ) | — | — | (7,207 | ) | ||||||||||||

Common stock issued through distribution reinvestment plan | 180,906 | 2 | 3,390 | — | — | 3,392 | ||||||||||||||||

Share-based compensation | — | — | 39 | — | — | 39 | ||||||||||||||||

Offering costs | — | — | (382 | ) | — | — | (382 | ) | ||||||||||||||

Net income | — | — | — | — | 19,890 | 19,890 | ||||||||||||||||

Distributions declared | — | — | — | — | (17,449 | ) | (17,449 | ) | ||||||||||||||

Other comprehensive income/(loss) | — | — | — | 145 | — | 145 | ||||||||||||||||

Balance, March 31, 2019 | 40,258,666 | $ | 404 | $ | 842,800 | $ | (314 | ) | $ | (91,825 | ) | $ | 751,065 | |||||||||

Issuance of common stock | 1,267,833 | $ | 13 | $ | 21,175 | $ | — | $ | — | $ | 21,188 | |||||||||||

Common stock repurchases | — | — | — | — | — | — | ||||||||||||||||

Common stock issued through distribution reinvestment plan | 187,146 | 2 | 3,490 | — | — | 3,492 | ||||||||||||||||

Share-based compensation | 6,400 | — | 39 | — | — | 39 | ||||||||||||||||

5

Offering Cost | — | — | (529 | ) | — | — | (529 | ) | ||||||||||||||

Net income | — | — | — | — | 14,526 | 14,526 | ||||||||||||||||

Distributions declared | — | — | — | — | (18,298 | ) | (18,298 | ) | ||||||||||||||

Other comprehensive income/(loss) | — | — | — | (65 | ) | — | (65 | ) | ||||||||||||||

Balance, June 30, 2019 | 41,720,045 | $ | 419 | $ | 866,975 | $ | (379 | ) | $ | (95,597 | ) | $ | 771,418 | |||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

6

BENEFIT STREET PARTNERS REALTY TRUST, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

Six Months Ended June 30, | |||||||

2020 | 2019 | ||||||

Cash flows from operating activities: | |||||||

Net income/(loss) | $ | 414 | $ | 34,416 | |||

Adjustments to reconcile net income/(loss) to net cash (used in)/provided by operating activities: | |||||||

Premium amortization and (discount accretion), net | $ | (3,041 | ) | $ | (3,185 | ) | |

Accretion of deferred commitment fees | (2,664 | ) | (1,282 | ) | |||

Amortization of deferred financing costs | 6,936 | 7,072 | |||||

Share-based compensation | 96 | 78 | |||||

Realized (gain)/loss on sale of real estate securities | 5,747 | — | |||||

Unrealized (gain)/loss on commercial mortgage loans held-for-sale | 339 | (232 | ) | ||||

Unrealized (gain)/loss on derivative instruments | 4,935 | 3,070 | |||||

Unrealized losses on other real estate investments | 43 | — | |||||

Depreciation and amortization | 1,174 | — | |||||

Recognition of deferred rent revenue | (150 | ) | — | ||||

Increase/(decrease) for credit losses | 18,639 | 3,068 | |||||

Impairment losses on real estate owned assets | 398 | — | |||||

Origination of commercial mortgage loans, held-for-sale | (119,447 | ) | (324,219 | ) | |||

Proceeds from sale of commercial mortgage loans, held-for-sale | 148,020 | 297,269 | |||||

Changes in assets and liabilities: | |||||||

Accrued interest receivable | 3,664 | (462 | ) | ||||

Prepaid expenses and other assets | (1,418 | ) | (2,104 | ) | |||

Accounts payable and accrued expenses | 8,057 | 2,458 | |||||

Due to affiliates | 4,831 | 37 | |||||

Interest payable | (1,392 | ) | 370 | ||||

Net cash (used in)/provided by operating activities | $ | 75,181 | $ | 16,354 | |||

Cash flows from investing activities: | |||||||

Origination and purchase of commercial mortgage loans, held for investment | $ | (417,216 | ) | $ | (669,044 | ) | |

Principal repayments received on commercial mortgage loans, held for investment | 603,589 | 328,742 | |||||

Purchase of other real estate investments | — | (2,511 | ) | ||||

Purchase of real estate owned and capital expenditures | (1,332 | ) | — | ||||

Purchase of real estate securities | (134,823 | ) | (107,535 | ) | |||

Proceeds from sale of real estate securities | 79,404 | 249 | |||||

Purchase of derivative instruments | (697 | ) | (829 | ) | |||

Net cash (used in)/provided by investing activities | $ | 128,925 | $ | (450,928 | ) | ||

Cash flows from financing activities: | |||||||

Proceeds from issuances of common stock | $ | 10,887 | $ | 40,597 | |||

Proceeds from issuances of redeemable convertible preferred stock | 70 | 14,979 | |||||

Common stock repurchases | (6,907 | ) | (7,207 | ) | |||

Borrowings under collateralized loan obligation | — | 639,899 | |||||

Repayments of collateralized loan obligation | (110,458 | ) | (260,833 | ) | |||

Borrowings on repurchase agreements - commercial mortgage loans | 171,994 | 728,432 | |||||

Repayments of repurchase agreements - commercial mortgage loans | (198,313 | ) | (745,003 | ) | |||

Borrowings on repurchase agreements - real estate securities | 585,504 | 493,541 | |||||

7

BENEFIT STREET PARTNERS REALTY TRUST, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

Repayments of repurchase agreements - real estate securities | (644,607 | ) | (453,058 | ) | |||

Borrowing on other financing and loan participation - commercial mortgage loans | 18,771 | — | |||||

Repayments on other financing and loan participation - commercial mortgage loans | — | (10,000 | ) | ||||

Borrowing on mortgage note payable | 11,074 | — | |||||

Payments of deferred financing costs | (359 | ) | (4,395 | ) | |||

Distributions paid | (23,774 | ) | (28,563 | ) | |||

Net cash (used in)/provided by financing activities: | $ | (186,118 | ) | $ | 408,389 | ||

Net change in cash, cash equivalents and restricted cash | 17,988 | (26,185 | ) | ||||

Cash, cash equivalents and restricted cash, beginning of period | 109,122 | 204,419 | |||||

Cash, cash equivalents and restricted cash, end of period | $ | 127,110 | $ | 178,234 | |||

Supplemental disclosures of cash flow information: | |||||||

Taxes paid | $ | — | $ | — | |||

Interest paid | 34,083 | 38,793 | |||||

Supplemental disclosures of non - cash flow information: | |||||||

Distribution payable | $ | 15,570 | $ | 6,083 | |||

Common stock issued through distribution reinvestment plan | 3,492 | 6,884 | |||||

Commercial mortgage loans transferred from held for sale to held for investment | 23,390 | — | |||||

Real estate owned received in foreclosure | 14,000 | — | |||||

Reconciliation of cash, cash equivalents and restricted cash at end of period: | |||||||

Cash and cash equivalents | $ | 111,631 | $ | 164,541 | |||

Restricted cash | 15,479 | 13,693 | |||||

Cash, cash equivalents and restricted cash, end of period | $ | 127,110 | $ | 178,234 | |||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

8

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Note 1 - Organization and Business Operations

Benefit Street Partners Realty Trust, Inc. (the "Company") is a real estate finance company that primarily originates, acquires and manages a diversified portfolio of commercial real estate debt investments secured by properties located within and outside the United States. The Company was incorporated in Maryland on November 15, 2012 and commenced operations on May 14, 2013.

The Company made a tax election to be treated as a real estate investment trust (a "REIT") for U.S. federal income tax purposes commencing with its taxable year ended December 31, 2013. The Company believes that it has qualified as a REIT and intends to continue to meet the requirements for qualification and taxation as a REIT. In addition, the Company, through a subsidiary which is treated as a taxable REIT subsidiary (a "TRS") is indirectly subject to U.S federal, state and local income taxes. The majority of the Company's business is conducted through Benefit Street Partners Realty Operating Partnership, L.P. (the “OP”), a Delaware limited partnership. The Company is the sole general partner and directly or indirectly holds all of the units of limited partner interests in the OP.

The Company has no direct employees. Benefit Street Partners L.L.C. serves as the Company's advisor (the "Advisor") pursuant to an Amended and Restated Advisory Agreement, dated January 19, 2018 (the "Advisory Agreement"). The Advisor is a wholly owned subsidiary of Franklin Resources, Inc. which, together with its various subsidiaries, operates as Franklin Templeton. The Advisor, an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”), is a credit-focused alternative asset management firm. Established in 2008, the Advisor's credit platform manages funds for institutions and high-net-worth investors across various credit funds and complementary strategies including high yield, levered loans, private / opportunistic debt, liquid credit, structured credit and commercial real estate debt. These strategies complement each other as they all leverage the sourcing, analytical, compliance, and operational capabilities that encompass the platform. The Advisor manages the Company's affairs on a day-to-day basis. The Advisor receives compensation and fees for services related to the investment and management of the Company's assets and the operations of the Company.

The Company invests in commercial real estate debt investments, which may include first mortgage loans, subordinated mortgage loans, mezzanine loans and participations in such loans. The Company also originates conduit loans which the Company intends to sell through its TRS into commercial mortgage-backed securities ("CMBS") at a profit. The Company also invests in commercial real estate securities. Real estate securities may include CMBS, senior unsecured debt of publicly traded REITs, debt or equity securities of other publicly traded real estate companies and collateralized debt obligations ("CDOs"). The Company also owns real estate, which represents real estate acquired by the Company through foreclosure, deed in lieu of foreclosure, or purchase.

Note 2 - Summary of Significant Accounting Policies

Basis of Accounting

The Company's unaudited consolidated financial statements and related footnotes have been prepared on the accrual basis of accounting in conformity with accounting principles generally accepted in the United States of America ("GAAP") for interim financial statements and pursuant to the requirements for reporting on Form 10-Q and Regulation S-X, as appropriate. Accordingly, the consolidated financial statements may not include all of the information and notes required by GAAP for annual consolidated financial statements.

These financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto as of, and for the year ended December 31, 2019, which are included in the Company's Annual Report on Form 10-K/A filed with the SEC on March 19, 2020.

9

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Use of Estimates

GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reported periods. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ materially. In the opinion of management, the interim data includes all adjustments, of a normal and recurring nature, necessary for a fair statement of the results for the periods presented. The current period’s results of operations will not necessarily be indicative of results that ultimately may be achieved for the entire year or any subsequent interim periods.

In response to the global coronavirus (COVID-19) pandemic, numerous countries, including the U.S., have declared national emergencies with respect to COVID-19 and certain jurisdictions, including those where our corporate headquarters and/or properties that secure our investments, or properties that we own, are located, have at times imposed “stay-at-home” guidelines or orders or other restrictions to help prevent its spread. The disruptive economic effects of the COVID-19 pandemic and government responses thereto have significantly impacted our estimates involving credit losses and fair values during the three and six months ended June 30, 2020, including introducing a significant degree of uncertainty underlying those estimates.

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of the Company, the OP and its subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation. In determining whether the Company has a controlling financial interest in a joint venture and the requirement to consolidate the accounts of that entity, management considers factors such as ownership interest, authority to make decisions and contractual and substantive participating rights of the other partners or members, as well as whether the entity is a variable interest entity ("VIE") for which the Company is the primary beneficiary.

The Company has determined the OP is a VIE of which the Company is the primary beneficiary. Substantially all of the Company's assets and liabilities are held by the OP.

The Company consolidates all entities that it controls through either majority ownership or voting rights. In addition, the Company consolidates all VIEs of which the Company is considered the primary beneficiary. VIEs are entities in which equity investors (i) do not have the characteristics of a controlling financial interest and/or (ii) do not have sufficient equity at risk for the entity to finance its activities without additional subordinated financial support from other parties. The entity that consolidates a VIE is its primary beneficiary and is generally the entity with (i) the power to direct the activities that most significantly affect the VIE’s economic performance and (ii) the right to receive benefits from the VIE or the obligation to absorb losses of the VIE that could be significant to the VIE.

The accompanying consolidated financial statements include the accounts of collateralized loan obligations ("CLOs") issued and securitized by wholly owned subsidiaries of the Company. The Company has determined the CLOs are VIEs of which the Company's subsidiary is the primary beneficiary. The assets and liabilities of the CLOs are consolidated in the accompanying consolidated balance sheets in accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 810, Consolidation.

Acquisition Expenses

The Company capitalizes certain direct costs relating to loan origination activities and the cost is amortized over the life of the loan.

Cash and Cash Equivalents

Cash consists of amounts deposited with high quality financial institutions. These deposits are guaranteed by the Federal Deposit Insurance Company up to an insurance limit. Cash equivalents include short-term, liquid investments in money market funds with original maturities of 90 days or less when purchased.

Restricted Cash

Restricted cash primarily consists of cash pledged as margin on repurchase agreements and derivative transactions. The duration of this restricted cash generally matches the duration of the related repurchase agreements or derivative transaction.

10

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Commercial Mortgage Loans

Held for Investment - Commercial mortgage loans that are held for investment purposes and are anticipated to be held until maturity, are carried at cost, net of unamortized acquisition expenses, discounts or premiums and unfunded commitments. Commercial mortgage loans, held for investment purposes, that are deemed to be impaired are carried at amortized cost less a specific allowance for credit losses. Interest income is recorded on the accrual basis and related discounts, premiums and acquisition expenses on investments are amortized over the life of the investment using the effective interest method. Amortization is reflected as an adjustment to interest income in the Company’s consolidated statements of operations. Guaranteed loan commitment fees payable by the borrower upon maturity are accreted over the life of the investment using the effective interest method. The accretion of guaranteed loan commitment fees is recognized in interest income in the Company's consolidated statements of operations.

Held-for-Sale - Commercial mortgage loans that are intended to be sold in the foreseeable future are reported as held-for-sale and are transferred at fair value and recorded at the lower of cost or fair value with changes recorded through the statements of operations. Unamortized loan origination costs for commercial mortgage loans held-for-sale that are carried at the lower of cost or fair value are capitalized as part of the carrying value of the loans and recognized upon the sale of such loans. Amortization of origination costs ceases upon transfer of commercial mortgage loans to held-for-sale.

Held-for-Sale, Accounted for Under the Fair Value Option - The fair value option provides an option to elect fair value as an alternative measurement for selected financial assets, financial liabilities, and written loan commitments. The Company has elected to measure commercial mortgage loans held-for-sale in the Company's TRS under the fair value option. These commercial mortgage loans are included in the Commercial mortgage loans, held-for-sale, measured at fair value in the consolidated balance sheets. Interest income received on commercial mortgage loans held-for-sale, measured at fair value is recorded on the accrual basis of accounting and is included in interest income in the consolidated statements of operations. Acquisition expenses on originating these investments are expensed when incurred.

Real estate owned

Real estate owned (“REO”) represents real estate acquired by the Company through foreclosure, deed in lieu of foreclosure, or purchase. REO assets are carried at their estimated fair value at acquisition and are presented net of accumulated depreciation and impairment charges. The Company allocates the purchase price of acquired real estate assets based on the fair value of the acquired land, building, furniture, fixtures and equipment.

Real estate assets are depreciated using the straight-line method over estimated useful lives of up to 40 years for buildings and improvements and up to 15 years for furniture, fixtures and equipment. Renovations and/or replacements that improve or extend the life of the real estate asset are capitalized and depreciated over their estimated useful lives.

Real estate owned assets that are probable to be sold within one year are reported as held-for sale. Real estate owned assets classified as held-for-sale shall be measured at the lower of its carrying amount or fair value less cost to sell. Real estate owned assets shall not be depreciated or amortized while it is classified as held-for-sale. Interest and other expenses attributable to the liabilities of a disposal group classified as held-for-sale shall continue to be accrued.

Leases

Operating right of use assets "ROU" represent the Company’s right to use an underlying asset during the lease term and lease liabilities represent the Company’s obligation to make lease payments arising from the lease. ROU assets and lease liabilities are recognized at commencement date based on the present value of fixed lease payments over the lease term. Leases will be classified as either a finance or operating lease, with such classification affecting the pattern and classification of expense recognition in the consolidated statements of operations. For leases greater than 12 months, the Company determines, at the inception of the contract, if the arrangement meets the classification criteria for an operating or finance lease. For leases that have extension options, which can be exercised at the Company's discretion, management uses judgment to determine if it is reasonably certain that such extension options will be elected. If the extension options are reasonably certain to occur, the Company includes the extended term's lease payments in the calculation of the respective lease liability. Lease expense for lease payments is recognized on a straight-line basis over the lease term. The incremental borrowing rate used to discount the lease liability is determined at commencement of the lease, or upon modification of the lease, as the interest rate a lessee would have to pay to borrow on a fully collateralized basis over a similar term an amount equal to the lease payments in a similar economic environment. The Company's incremental borrowing rate considers information at both the corporate and property level and analysis of current market conditions for obtaining new financings. All leases as of June 30, 2020 were operating leases.

11

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Separately, on October 15, 2019, the Company acquired certain real estate assets which had an existing in-place lease asset. This in-place lease asset is recorded as an Intangible lease asset on the consolidated balance sheets and amortized using the straight-line method over the contractual life of the lease.

Credit Losses

In June 2016, the FASB issued Accounting Standards Update ("ASU") No. 2016-13, Financial Instruments-Credit Losses, which amends the credit impairment model for financial instruments. The Company adopted ASU 2016-13 on January 1, 2020.

Following our adoption of ASU 2016-13, our previous incurred loss model was replaced with a lifetime current expected credit loss (“CECL”) model for financial instruments carried at amortized cost and off-balance sheet credit exposures, such as loans, loan commitments, held-to-maturity (“HTM”) debt securities, financial guarantees, net investments in leases, reinsurance and trade receivables, which will generally result in earlier recognition of allowance for losses. For available for sale (“AFS”) debt securities, unrealized credit losses are recognized as allowances rather than reductions in amortized cost basis and elimination of the other than temporary impairment concept will result in more frequent estimation of credit losses. The accounting model for purchased credit impaired loans and debt securities has been simplified, including elimination of some of the asymmetrical treatment between credit losses and credit recoveries, to be consistent with the CECL model for originated and purchased non-credit impaired assets. The adopted model for ASC 326 as it applies to HTM and AFS securities, encompassing the beneficial interest model for securities that are not of high credit quality, has been clarified to include the effective interest method as a basis for the projection of cash collections method in connection with the newly adopted impairment models for HTM and AFS debt securities under ASC 326 when securities are not of high credit quality. Upon adoption of ASU 2016-13 on January 1, 2020, we recorded an additional allowance for credit losses for our outstanding loans and unfunded loan commitments of $7.8 million, or $0.18 per share, which was 0.27% of the aggregate commitment amount of the Company’s loan portfolio at December 31, 2019.

Pre-adoption | Transition Adjustment | Post-adjustment | ||||

Assets | ||||||

Commercial mortgage loans, held for investment, net of allowance | 2,762,042 | (7,211 | ) | 2,754,831 | ||

Liabilities | ||||||

Accounts payable and accrued expenses (1) | 10,925 | (550 | ) | 10,375 | ||

Equity | ||||||

Accumulated deficit | (85,968 | ) | (7,761 | ) | (93,729 | ) |

(1) Includes allowance associated with unfunded loan commitment.

The following discussion highlights changes to the Company’s accounting policies as a result of this adoption.

Allowance for credit losses

The allowance for credit losses for the Company’s financial instruments carried at amortized cost and off-balance sheet credit exposures, such as loans held for investment and unfunded loan commitments represents a lifetime estimate of expected credit losses. Factors considered by the Company when determining the allowance for credit losses reserve include loan-specific characteristics such as loan-to-value (“LTV”) ratio, vintage year, loan term, property type, occupancy and geographic location, financial performance of the borrower, expected payments of principal and interest, as well as internal or external information relating to past events, current conditions and reasonable and supportable forecasts.

The allowance for credit losses is measured on a collective (pool) basis when similar risk characteristics exist for multiple financial instruments. If similar risk characteristics do not exist, the Company measures the allowance for credit losses on an individual instrument basis. The determination of whether a particular financial instrument should be included in a pool can change over time. If a financial asset’s risk characteristics change, the Company evaluates whether it is appropriate to continue to keep the financial instrument in its existing pool or evaluate it individually.

12

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

In measuring the allowance for credit losses for financial instruments including our unfunded loan commitments that share similar risk characteristics, the Company primarily applies a probability of default (“PD”)/loss given default (“LGD”) model for instruments that are collectively assessed, whereby the allowance for credit losses is calculated as the product of PD, LGD and exposure at default (“EAD”). The Company’s model principally utilizes historical loss rates derived from a commercial mortgage backed securities database with historical losses from 1998 to 2020 provided by a reputable third party, forecasting the loss parameters using a scenario-based statistical approach over a reasonable and supportable forecast period of twelve months, followed by an immediate reversion to average historical losses. For financial instruments assessed on an individual basis, including when it is probable that the Company will be unable to collect the full payment of principal and interest on the instrument, the Company applies a discounted cash flow (“DCF”) methodology.

For financial instruments where the borrower is experiencing financial difficulty based on the Company’s assessment at the reporting date and the repayment is expected to be provided substantially through the operation or sale of the collateral, the Company may elect to use as a practical expedient the fair value of the collateral at the reporting date when determining the allowance for credit losses.

In developing the allowance for credit losses for its loans held for investment, the Company performs a comprehensive analysis of its loan portfolio and assigns risk ratings to loans that incorporate management's current judgments about their credit quality based on all known and relevant internal and external factors that may affect collectability, using similar factors as those in developing the allowance for credit losses. This methodology results in loans being segmented by risk classification into risk rating categories that are associated with estimated probabilities of default and principal loss. Risk rating categories range from "1" to "5" with "1" representing the lowest risk of loss and "5" representing the highest risk of loss with the ratings updated quarterly. At the time of origination or purchase, loans held for investment are ranked as a “2” and will move accordingly going forward based on the ratings which are defined as follows:

1. | Very Low Risk- Investment exceeding fundamental performance expectations and/or capital gain expected. Trends and risk factors since time of investment are favorable. |

2. | Low Risk- Performing consistent with expectations and a full return of principal and interest expected. Trends and risk factors are neutral to favorable. |

3. | Average Risk- Performing investments requiring closer monitoring. Trends and risk factors show some deterioration. |

4. | High Risk/Delinquent/Potential for Loss- Underperforming investment with the potential of some interest loss but still expecting a positive return on investment. Trends and risk factors are negative. |

5. | Impaired/Defaulted/Loss Likely- Underperforming investment with expected loss of interest and some principal. |

The Company also considers qualitative and environmental factors, including, but not limited to, economic and business conditions, nature and volume of the loan portfolio, lending terms, volume and severity of past due loans, concentration of credit and changes in the level of such concentrations in its determination of the allowance for credit losses.

Changes in the allowance for credit losses for the Company’s financial instruments are recorded in Increase/(decrease) for credit losses on the consolidated statements of operations with a corresponding offset to the financial instrument’s amortized cost recorded on the consolidated balance sheets, or as a component of Accounts payable and accrued expenses for unfunded loan commitments.

The Company has elected to not measure an allowance for credit losses for accrued interest receivable as it is reversed against interest income when a loan or preferred equity investment is placed on nonaccrual status. Loans are charged off against the Increase/(decrease) for credit losses when all or a portion of the principal amount is determined to be uncollectible.

Past due and nonaccrual status

Loans are placed on nonaccrual status and considered non-performing when full payment of principal and interest is unpaid for 90 days or more or where reasonable doubt exists as to timely collection, unless the loan is both well secured and in the process of collection. Interest received on nonaccrual status loans are accounted for under the cost-recovery method, until qualifying for return to accrual. Upon restructuring the nonaccrual loan, the Company may return a loan to accrual status when repayment of principal and interest is reasonably assured.

13

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Troubled Debt Restructuring (“TDR”)

The Company classifies an individual financial instrument as a TDR when it has a reasonable expectation that the financial instrument’s contractual terms will be modified in a manner that grants concession to the borrower who is experiencing financial difficulty. Concessions could include term extensions, payment deferrals, interest rate reductions, principal forgiveness, forbearance, or other actions designed to maximize the Company’s collection on the financial instrument. The Company determines the allowance for credit losses for financial instruments that are TDRs individually.

Real Estate Securities

On the acquisition date, all of the Company’s commercial real estate securities were classified as available for sale and carried at fair value, and subsequently any unrealized gains or losses are recognized as a component of accumulated other comprehensive income or loss. The Company may elect the fair value option for its real estate securities, and as a result, any unrealized gains or losses on such real estate securities will be recorded in the Company’s consolidated statements of operations. No such election has been made to date. Related discounts, premiums and acquisition expenses on investments are amortized over the life of the investment using the effective interest method. Amortization is reflected as an adjustment to interest income in the Company’s consolidated statements of operations. The Company uses the specific identification method in determining the cost relief for real estate securities sold. Realized gains and losses from the sale of real estate securities are included in the Company’s consolidated statements of operations.

AFS real estate securities which have experienced a decline in the fair value below their amortized cost basis (i.e., impairment) are evaluated each reporting period to determine whether the decline in fair value is due to credit-related factors. Any impairment that is not credit-related is recognized in other comprehensive income, while credit-related impairment is recognized as an allowance on the consolidated balance sheets with a corresponding adjustment on the consolidated statements of operations. If the Company intends to sell an impaired real estate security or more likely than not will be required to sell such a security before recovering its amortized cost basis, the entire impairment amount is recognized in the consolidated statements of operations with a corresponding adjustment to the security’s amortized cost basis.

The Company analyzes the AFS security portfolio on a periodic basis for credit losses at the individual security level using the same criteria described above for those amortized cost financial assets subject to an allowance for credit losses including but not limited to; performance of the underlying assets in the security, borrower financial resources and investment in collateral, collateral type, credit ratings, project economics and geographic location as well as national and regional economic factors.

The non-credit loss component of the unrealized loss within the Company’s AFS portfolio is recognized as an adjustment to the individual security’s asset balance with an offsetting entry to other comprehensive income in the consolidated balance sheets.

Repurchase Agreements

Commercial mortgage loans and real estate securities sold under repurchase agreements have been treated as collateralized financing transactions because the Company maintains effective control over the transferred securities. Commercial mortgage loans and real estate securities financed through a repurchase agreement remain on the Company’s consolidated balance sheets as an asset and cash received from the purchaser is recorded as a liability. Interest paid in accordance with repurchase agreements is recorded in interest expense on the Company's consolidated statements of operations.

Deferred Financing Costs

The deferred financing costs related to the Company's various Master Repurchase Agreements as well as certain prepaid subscription costs are included in Prepaid expenses and other assets on the consolidated balance sheets. Deferred financing cost on the Company's collateralized debt obligations ("CLO") are netted against the Company's CLO payable in the Collateralized debt obligations on the consolidated balance sheets. Deferred financing costs are amortized over the terms of the respective financing agreement using the effective interest method and included in interest expense on the Company's consolidated statements of operations. Unamortized deferred financing costs are generally expensed when the associated debt is refinanced or repaid before maturity.

Share Repurchase Program

The Company has a Share Repurchase Program (the "SRP"), which became effective as of February 28, 2016, that enables stockholders to sell their shares to the Company.

Subject to certain conditions, stockholders that purchased shares of our common stock or received their shares from us (directly or indirectly) through one or more non-cash transactions and have held their shares for a period of at least one year may request that we repurchase their shares of common stock so long as the repurchase otherwise complies with the provisions of Maryland law. Repurchase requests made following the death or qualifying disability of a stockholder will not be subject to any minimum holding period.

14

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

On August 10, 2017, our board of directors amended the SRP to provide that the repurchase price per share for requests will be equal to the lesser of (i) our most recent estimated per-share NAV, as approved by our board of directors from time to time, and (ii) our book value per share, computed in accordance with GAAP, multiplied by a percentage equal to (i) 92.5%, if the person seeking repurchase has held his or her shares for a period greater than one year and less than two years; (ii) 95%, if the person seeking repurchase has held his or her shares for a period greater than two years and less than three years; (iii) 97.5%, if the person seeking repurchase has held his or her shares for a period greater than three years and less than four years; or (iv) 100%, if the person seeking repurchase has held his or her shares for a period greater than four years or in the case of requests for death or disability.

Repurchases pursuant to the SRP, when requested, generally will be made semiannually (each six-month period ending June 30 or December 31, a “fiscal semester”). Repurchases for any fiscal semester will be limited to a maximum of 2.5% of the weighted average number of shares of common stock outstanding during the previous fiscal year, with a maximum for any fiscal year of 5.0% of the weighted average number of shares of common stock outstanding during the previous fiscal year. Funding for repurchases pursuant to the SRP for any given fiscal semester will be limited to proceeds received during that same fiscal semester through the issuance of common stock pursuant to any Dividend Reinvestment Plan ("DRIP") in effect from time to time, provided that the board of directors has the power, in its sole discretion, to determine the amount of shares repurchased during any fiscal semester as well as the amount of funds to be used for that purpose. Due to these limitations, we cannot guarantee that we will be able to accommodate all repurchase requests made during any fiscal semester or fiscal year. However, a stockholder may withdraw its request at any time or ask that we honor the request when funds are available. Pending repurchase requests will be honored on a pro rata basis. We will generally pay repurchase proceeds, less any applicable tax or other withholding required by law, by the 31st day following the end of the fiscal semester during which the repurchase request was made.

When a stockholder requests a redemption and the redemption is approved by the board of directors, the Company will reclassify such obligation from equity to a liability based on the settlement value of the obligation. Shares repurchased under the SRP will have the status of authorized but unissued shares.

Offering and Related Costs

The Company is currently offering shares of the Company’s common stock, Series A convertible preferred stock (“Series A Preferred Stock”) and Series C convertible preferred stock (the “Series C Preferred Stock,” and, together with the Series A Preferred stock, the “Preferred Stock”) in private placements exempt from the registration requirements of the Securities Act of 1933, as amended (the “Offering”). In connection with the Offering, the Company incurred various offering costs and will continue to incur these costs until the Offering is complete. These offering costs include but are not limited to legal, accounting, printing, mailing and filing fees, and diligence expenses of broker-dealers. Offering costs for the common stock are recorded in the Company’s stockholders’ equity, while the offering costs for the Preferred Stock are included within Redeemable convertible preferred stock Series A and Redeemable convertible preferred stock series C, respectively, on the Company’s consolidated balance sheets.

15

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Distribution Reinvestment Plan

Pursuant to the DRIP, stockholders may elect to reinvest distributions by purchasing shares of common stock in lieu of receiving cash. No dealer manager fees or selling commissions are paid with respect to shares purchased pursuant to the DRIP. Participants purchasing shares pursuant to the DRIP have the same rights and are treated in the same manner as if such shares were issued pursuant to the Offering. The board of directors may designate that certain cash or other distributions be excluded from the DRIP. The Company has the right to amend any aspect of the DRIP or terminate the DRIP with ten days’ notice to participants. Shares issued under the DRIP are recorded to equity in the consolidated balance sheets in the period distributions are declared.

Income Taxes

The Company has conducted its operations to qualify as a REIT for U.S. federal income tax purposes beginning with its taxable year ended December 31, 2013. As a REIT, if the Company meets certain organizational and operational requirements and distributes at least 90% of its "REIT taxable income" (determined before the deduction of dividends paid and excluding net capital gains) to its stockholders in a year, it will not be subject to U.S. federal income tax to the extent of the income that it distributes. However, even if the Company qualifies for taxation as a REIT, it may be subject to certain state and local taxes on income in addition to U.S. federal income and excise taxes on its undistributed income. The Company, through its TRS, is indirectly subject to U.S. federal, state and local income taxes. The Company’s TRS is not consolidated for U.S. federal income tax purposes, but is instead taxed as a C corporation. For financial reporting purposes, the TRS is consolidated and a provision for current and deferred taxes is established for the portion of earnings recognized by the Company with respect to its interest in its TRS. Total income tax expense (benefit) for the six months ended June 30, 2020 and June 30, 2019 were $(2.6) million and $1.6 million, respectively.

The Company uses a more-likely-than-not threshold for recognition and derecognition of tax positions taken or to be taken in a tax return. The Company has assessed its tax positions for all open tax years beginning with December 31, 2016 and concluded that there were no uncertainties to be recognized. The Company’s accounting policy with respect to interest and penalties related to tax uncertainties is to classify these amounts as provision for income taxes.

The Company utilizes the TRS to reduce the impact of the prohibited transaction tax and to avoid penalty for the holding of assets not qualifying as real estate assets for purposes of the REIT asset tests. Any income associated with a TRS is fully taxable because the TRS is subject to federal and state income taxes as a domestic C corporation based upon its net income.

Derivatives and Hedging Activities

In the normal course of business, the Company is exposed to the effect of interest rate changes and may undertake a strategy to limit these risks through the use of derivatives. The Company uses derivatives primarily to economically hedge against interest rates, CMBS spreads and macro market risk in order to minimize volatility. The Company may use a variety of derivative instruments that are considered conventional, including but not limited to: Treasury note futures and credit derivatives on various indices including CMBX and CDX.

The Company recognizes all derivatives on the consolidated balance sheets at fair value. The Company does not designate derivatives as hedges to qualify for hedge accounting for financial reporting purposes and therefore any net payments under, or fluctuations in the fair value of these derivatives have been recognized currently in unrealized gain/(loss) on derivative instruments in the accompanying consolidated statements of operations. The Company records derivative asset and liability positions on a gross basis with any collateral posted with or received from counterparties recorded separately within Restricted cash on the Company’s consolidated balance sheets. Certain derivatives that the Company has entered into are subject to master netting agreements with its counterparties, allowing for netting of the same transaction, in the same currency, on the same date.

Per Share Data

The Company’s Preferred Stock is considered a participating security and calculates basic earnings per share using the two-class method. The Company’s dilutive earnings per share calculation is computed using the more dilutive result of the treasury stock method, assuming the participating security is a potential common share, or the two-class method, assuming the participating security is not converted. The Company calculates basic earnings per share by dividing net income applicable to common stock for the period by the weighted-average number of shares of common stock outstanding for that period. Diluted earnings per share reflects the potential dilution that could occur from shares outstanding if potential shares of common stock with a dilutive effect have been issued in connection with the restricted stock plan or upon conversion of the outstanding shares of the Company’s Preferred Stock, except when doing so would be anti-dilutive.

16

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Reportable Segments

The Company has determined that it has four reportable segments based on how the chief operating decision maker reviews and manages the business. The four reporting segments are as follows:

• | The real estate debt business which is focused on originating, acquiring and asset managing commercial real estate debt investments, including first mortgage loans, subordinate mortgages, mezzanine loans and participations in such loans. |

• | The real estate securities business which is focused on investing in and asset managing commercial real estate securities primarily consisting of CMBS and may include unsecured REIT debt, CDO notes and other securities. |

• | The commercial conduit business in the Company's TRS, which is focused on originating and subsequently selling fixed-rate commercial real estate loans into the CMBS securitization market. |

• | The real estate owned business represents real estate acquired by the Company through foreclosure, deed in lieu of foreclosure, or purchase. |

See Note 15 - Segment Reporting for further information regarding the Company's segments.

Redeemable Convertible Preferred Stock

The Company’s Preferred Stock is classified outside of permanent equity in the consolidated balance sheets. Subject to certain conditions, the Preferred Stock is redeemable at the option of the holder of Preferred Stock, outside of the control of the Company. As set forth in the Articles Supplementary relating to each of the Series A Preferred Stock and the Series C Preferred Stock (the “Articles Supplementary”) to the Company’s Articles of Amendment and Restatement, the Preferred Stock is redeemable for shares of the Company's common stock, $0.01 par value per share (the "Common Stock") at the option of the shareholder upon a change of control (as defined in the Articles Supplementary) or after the sixth anniversary of the date of issuance. A change in control of the Company occurs if any person acquires more than 50% of the total economic interests or voting power of all securities of the Company, other than in a liquidity event.

Shares of Preferred Stock rank senior to shares of Common Stock with respect to rights to receive dividends and to participate in distributions or payments upon any voluntary or involuntary liquidation, dissolution or winding up of the Company. Dividends payable on each share of Preferred Stock will be equal to the greater of (i) an amount equal to $16.67 per share and (ii) the monthly dividend that would have been paid had such share of Preferred Stock been converted to a share of Common Stock, subject to proration in the event that such share of Preferred Stock was not outstanding for the full month.

Immediately prior to a “Liquidity Event,” each outstanding share of Series A Preferred Stock shall convert into 299.2 shares of Common Stock, subject to anti-dilution adjustments (the “Conversion Rate”). Each outstanding share of Series C Preferred Stock will convert into shares of Common Stock at the same Conversion Rate on the one-year anniversary of a Liquidity Event, subject to the Company’s right to accelerate the conversion to a date no earlier than six months after the Liquidity Event, upon at least ten days prior notice to the holders of the Series C Preferred Stock. A “Liquidity Event” is defined as (i) the listing of the Common Stock on a national securities exchange or quotation on an electronic inter-dealer quotation system; (ii) a merger or business combination involving the Company pursuant to which outstanding shares Common Stock are exchanged for securities of another company which are listed on a national securities exchange or quoted on an electronic inter-dealer quotation system; or (iii) any other transaction or series of transaction that results in all shares of Common Stock being transferred or exchange for cash or securities which are listed on a national securities exchange or quoted on an electronic inter-dealer quotation system. If there has not been a Liquidity Event within six years from the initial issuance of the Preferred Stock, each holder of Preferred Stock shall have the right to convert all, but not less than all, of the Preferred Stock held by such holder into Common Stock at the Conversion Rate. Each holder also has the option to convert its shares of Preferred Stock into Common Stock upon a change in control (as defined in the respective Articles Supplementary for the Series A Preferred Stock and Series C Preferred Stock) of the Company. In addition, neither the Company nor a holder of shares of Preferred Stock may redeem shares of the Preferred Stock until six years from the initial issuance of the Preferred Stock, except in cases of a change in control (as defined in the respective Articles Supplementary).

17

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Holders of the Preferred Stock are entitled to vote on each matter submitted to a vote of the stockholders of the Company upon which the holders of Common Stock are entitled to vote, upon which the holders of the Preferred Stock and holders of the Common Stock shall vote together as a single class. The number of votes applicable to a share of Preferred Stock will be equal to the number of shares of Common Stock a share of Preferred Stock could have been converted into as of the record date set for purposes of such stockholder vote (rounded down to the nearest whole number of shares of Common Stock). In addition, the affirmative vote of the holders of two-thirds of the outstanding shares of Preferred Stock is required to approve the issuance of any equity securities senior to the Preferred Stock and to take certain actions materially adverse to the holders of the Preferred Stock.

Accounting Pronouncements Not Yet Adopted

On March 12, 2020, the FASB issued ASU No. 2020-04, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting, which provides temporary optional expedients and exceptions to the US GAAP guidance on contract modifications and hedge accounting to ease the financial reporting burdens of the expected market transition from LIBOR and other interbank offered rates to alternative reference rates. The guidance is effective upon issuance and generally can be applied through December 31, 2022. The Company has not adopted any of the optional expedients or exceptions through June 30, 2020, but will continue to evaluate the possible adoption of any such expedients or exceptions during the effective period as circumstances evolve.

Note 3 - Commercial Mortgage Loans

The following table is a summary of the Company's commercial mortgage loans, held for investment, carrying values by class (dollars in thousands):

________________________

June 30, 2020 | December 31, 2019 | ||||||

Senior loans | $ | 2,486,919 | $ | 2,721,325 | |||

Mezzanine loans | 7,995 | 41,638 | |||||

Total gross carrying value of loans | 2,494,914 | 2,762,963 | |||||

Less: Allowance for credit losses (1) | 26,244 | 921 | |||||

Total commercial mortgage loans, held for investment, net | $ | 2,468,670 | $ | 2,762,042 | |||

(1) As of June 30, 2020 and December 31, 2019, there have been no specific reserves for loans in non-performing status.

As of June 30, 2020 and December 31, 2019, the Company's total commercial mortgage loan portfolio, excluding commercial mortgage loans accounted for under the fair value option, was comprised of 116 and 122 loans, respectively.

Allowance for Credit Losses

The following table presents the activity in the Company's allowance for credit losses, excluding the unfunded loan commitments, as of June 30, 2020 (dollars in thousands):

Three Months Ended June 30, 2020 | ||||||||||||||||||||||||||||||||||||

MultiFamily | Retail | Office | Industrial | Mixed Use | Hospitality | Self Storage | Mobile Housing | Total | ||||||||||||||||||||||||||||

Beginning Balance | $ | 12,189 | $ | 1,153 | $ | 4,573 | $ | 2,332 | $ | 41 | $ | 1,070 | $ | 276 | $ | 68 | $ | 21,702 | ||||||||||||||||||

Current Period: | ||||||||||||||||||||||||||||||||||||

Increase/(decrease) for credit losses | (1,447 | ) | (373 | ) | (223 | ) | (1,733 | ) | 2,209 | 6,173 | (56 | ) | (8 | ) | 4,542 | |||||||||||||||||||||

Write offs | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Recoveries | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Ending Balance | $ | 10,742 | $ | 780 | $ | 4,350 | $ | 599 | $ | 2,250 | $ | 7,243 | $ | 220 | $ | 60 | $ | 26,244 | ||||||||||||||||||

18

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Six Months Ended June 30, 2020 | ||||||||||||||||||||||||||||||||||||

MultiFamily | Retail | Office | Industrial | Mixed Use | Hospitality | Self Storage | Mobile Housing | Total | ||||||||||||||||||||||||||||

Beginning Balance | $ | 322 | $ | 202 | $ | 249 | $ | 23 | $ | 4 | $ | 103 | $ | — | $ | 18 | $ | 921 | ||||||||||||||||||

Cumulative-effect adjustment upon adoption of ASU 2016-13 | 3,220 | 386 | 1,966 | 434 | 9 | 739 | 399 | 58 | 7,211 | |||||||||||||||||||||||||||

Current Period: | ||||||||||||||||||||||||||||||||||||

Increase/(decrease) for credit losses | 7,200 | 192 | 2,135 | 142 | 2,237 | 6,828 | (179 | ) | (16 | ) | 18,539 | |||||||||||||||||||||||||

Write offs | — | — | — | — | — | (427 | ) | — | — | (427 | ) | |||||||||||||||||||||||||

Recoveries | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Ending Balance | $ | 10,742 | $ | 780 | $ | 4,350 | $ | 599 | $ | 2,250 | $ | 7,243 | $ | 220 | $ | 60 | $ | 26,244 | ||||||||||||||||||

The increase in the provision for credit losses during the three and six months ended June 30, 2020 of $4.5 million and $18.5 million, respectively, is primarily driven by the continuing strains on the overall economic outlook as a result of the COVID-19 pandemic.

19

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

The following table presents the activity in the Company's allowance for credit losses, for the unfunded loan commitments, as of June 30, 2020 (dollars in thousands):

Three Months Ended June 30, 2020 | ||||||||||||||||||||||||||||||||||||

MultiFamily | Retail | Office | Industrial | Mixed Use | Hospitality | Self Storage | Mobile Housing | Total | ||||||||||||||||||||||||||||

Beginning Balance | $ | 295 | $ | — | $ | 392 | $ | 287 | $ | — | $ | 174 | $ | — | $ | 2 | $ | 1,150 | ||||||||||||||||||

Current Period: | ||||||||||||||||||||||||||||||||||||

Increase/(decrease) for credit losses | (70 | ) | — | (243 | ) | (247 | ) | — | 61 | — | (1 | ) | (500 | ) | ||||||||||||||||||||||

Write offs | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Recoveries | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Ending Balance | $ | 225 | $ | — | $ | 149 | $ | 40 | $ | — | $ | 235 | $ | — | $ | 1 | $ | 650 | ||||||||||||||||||

Six Months Ended June 30, 2020 | ||||||||||||||||||||||||||||||||||||

MultiFamily | Retail | Office | Industrial | Mixed Use | Hospitality | Self Storage | Mobile Housing | Total | ||||||||||||||||||||||||||||

Beginning Balance | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||||||||||

Cumulative-effect adjustment upon adoption of ASU 2016-13 | 239 | 40 | 150 | 30 | 1 | 57 | 28 | 5 | 550 | |||||||||||||||||||||||||||

Current Period: | ||||||||||||||||||||||||||||||||||||

Increase/(decrease) for credit losses | (14 | ) | (40 | ) | (1 | ) | 10 | (1 | ) | 178 | (28 | ) | (4 | ) | 100 | |||||||||||||||||||||

Write offs | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Recoveries | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Ending Balance | $ | 225 | $ | — | $ | 149 | $ | 40 | $ | — | $ | 235 | $ | — | $ | 1 | $ | 650 | ||||||||||||||||||

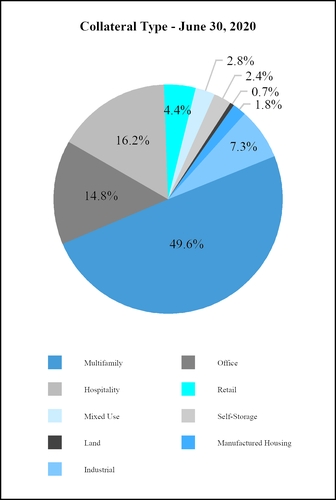

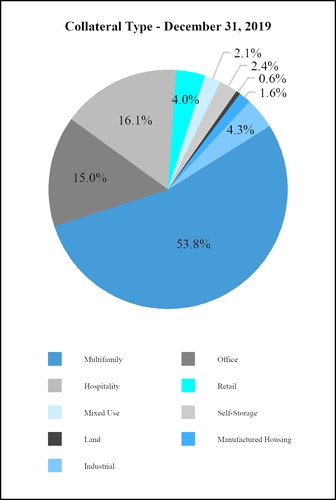

The following table represents the composition by loan type of the Company's commercial mortgage loans, held for investment portfolio (dollars in thousands):

June 30, 2020 | December 31, 2019 | |||||||||||||

Loan Type | Par Value | Percentage | Par Value | Percentage | ||||||||||

Multifamily | $ | 1,239,671 | 49.6 | % | $ | 1,491,971 | 53.9 | % | ||||||

Office | 369,472 | 14.8 | % | 414,772 | 15.0 | % | ||||||||

Hospitality | 404,517 | 16.2 | % | 446,562 | 16.1 | % | ||||||||

Industrial | 183,368 | 7.3 | % | 118,743 | 4.3 | % | ||||||||

Retail | 109,615 | 4.4 | % | 111,620 | 4.0 | % | ||||||||

Mixed Use | 69,635 | 2.8 | % | 58,808 | 2.1 | % | ||||||||

Self Storage | 62,597 | 2.4 | % | 67,767 | 2.4 | % | ||||||||

Land | 16,400 | 0.7 | % | 16,400 | 0.6 | % | ||||||||

Manufactured Housing | 46,168 | 1.8 | % | 44,656 | 1.6 | % | ||||||||

Total | $ | 2,501,443 | 100.0 | % | $ | 2,771,299 | 100.0 | % | ||||||

20

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

As of June 30, 2020 and December 31, 2019, the Company's total commercial mortgage loans, held-for-sale, measured at fair value comprised of 8 and 7 loans, respectively. As of June 30, 2020 and December 31, 2019, the contractual principal outstanding of commercial mortgage loans, held-for-sale, measured at fair value was $70.1 million and $112.5 million, respectively. As of June 30, 2020 and December 31, 2019, none of the Company's commercial mortgage loans, held-for-sale, measured at fair value were in default or greater than ninety days past due.

The following table represents the composition by loan type of the Company's commercial mortgage loans, held-for-sale, measured at fair value (dollars in thousands):

June 30, 2020 | December 31, 2019 | |||||||||||||

Loan Type | Par Value | Percentage | Par Value | Percentage | ||||||||||

Multifamily | $ | 41,100 | 58.6 | % | $ | 78,250 | 69.6 | % | ||||||

Retail | 21,193 | 30.2 | % | 2,613 | 2.3 | % | ||||||||

Office | 6,000 | 8.6 | % | — | — | % | ||||||||

Manufactured Housing | 1,850 | 2.6 | % | — | — | % | ||||||||

Hospitality | — | — | % | 8,000 | 7.1 | % | ||||||||

Industrial | — | — | % | 23,625 | 21.0 | % | ||||||||

Total | $ | 70,143 | 100.0 | % | $ | 112,488 | 100.0 | % | ||||||

Loan Credit Quality and Vintage

The following tables present the amortized cost of our commercial mortgage loans, held for investment as of June 30, 2020, by loan type, the Company’s internal risk rating and year of origination. The risk ratings are updated as of June 30, 2020.

June 30, 2020 | ||||||||||||||||||||||||||||||||

2020 | 2019 | 2018 | 2017 | 2016 | 2015 | Prior | Total | |||||||||||||||||||||||||

Multifamily: | ||||||||||||||||||||||||||||||||

Risk Rating: | ||||||||||||||||||||||||||||||||

1-2 internal grade | $ | 213,562 | $ | 438,877 | $ | 442,535 | $ | 34,875 | $ | — | $ | — | $ | 3,489 | $ | 1,133,338 | ||||||||||||||||

3-4 internal grade | — | — | 65,842 | 37,812 | — | — | — | 103,654 | ||||||||||||||||||||||||

Total Multifamily Loans | $ | 213,562 | $ | 438,877 | $ | 508,377 | $ | 72,687 | $ | — | $ | — | $ | 3,489 | $ | 1,236,992 | ||||||||||||||||

Retail: | ||||||||||||||||||||||||||||||||

Risk Rating: | ||||||||||||||||||||||||||||||||

1-2 internal grade | $ | — | $ | 36,147 | $ | 16,380 | $ | — | $ | — | $ | — | $ | 9,450 | $ | 61,977 | ||||||||||||||||

3-4 internal grade | — | 21,985 | 41,874 | — | — | — | — | 63,859 | ||||||||||||||||||||||||

Total Retail Loans | $ | — | $ | 58,132 | $ | 58,254 | $ | — | $ | — | $ | — | $ | 9,450 | $ | 125,836 | ||||||||||||||||

Office: | ||||||||||||||||||||||||||||||||

Risk Rating: | ||||||||||||||||||||||||||||||||

1-2 internal grade | $ | 56,205 | $ | 153,180 | $ | 61,323 | $ | 41,563 | $ | — | $ | — | $ | — | $ | 312,271 | ||||||||||||||||

3-4 internal grade | — | — | — | 10,480 | — | — | — | 10,480 | ||||||||||||||||||||||||

Total Office Loans | $ | 56,205 | $ | 153,180 | $ | 61,323 | $ | 52,043 | $ | — | $ | — | $ | — | $ | 322,751 | ||||||||||||||||

Industrial: | ||||||||||||||||||||||||||||||||

Risk Rating: | ||||||||||||||||||||||||||||||||

1-2 internal grade | $ | 39,847 | $ | 109,037 | $ | — | $ | — | $ | — | $ | 33,655 | $ | — | $ | 182,539 | ||||||||||||||||

3-4 internal grade | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||

Total Industrial Loans | $ | 39,847 | $ | 109,037 | $ | — | $ | — | $ | — | $ | 33,655 | $ | — | $ | 182,539 | ||||||||||||||||

21

BENEFIT STREET PARTNERS REALTY TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2020

(Unaudited)

Mixed Use: | ||||||||||||||||||||||||||||||||

Risk Rating: | ||||||||||||||||||||||||||||||||

1-2 internal grade | $ | — | $ | — | $ | 56,711 | $ | 12,924 | $ | — | $ | — | $ | — | $ | 69,635 | ||||||||||||||||

3-4 internal grade | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||

Total Mixed Use Loans | $ | — | $ | — | $ | 56,711 | $ | 12,924 | $ | — | $ | — | $ | — | $ | 69,635 | ||||||||||||||||

Hospitality: | ||||||||||||||||||||||||||||||||

Risk Rating: | ||||||||||||||||||||||||||||||||

1-2 internal grade | $ | — | $ | 10,536 | $ | — | $ | — | $ | — | $ | — | $ | — | $ | 10,536 | ||||||||||||||||

3-4 internal grade | — | 166,208 | 181,204 | 90,708 | — | — | — | 438,120 | ||||||||||||||||||||||||

Total Hospitality Loans | $ | — | $ | 176,744 | $ | 181,204 | $ | 90,708 | $ | — | $ | — | $ | — | $ | 448,656 | ||||||||||||||||

Self Storage: | ||||||||||||||||||||||||||||||||

Risk Rating: | ||||||||||||||||||||||||||||||||

1-2 internal grade | $ | — | $ | — | $ | 62,516 | $ | — | $ | — | $ | — | $ | — | $ | 62,516 | ||||||||||||||||

3-4 internal grade | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||

Total Self Storage Loans | $ | — | $ | — | $ | 62,516 | $ | — | $ | — | $ | — | $ | — | $ | 62,516 | ||||||||||||||||

Manufactured Housing: | ||||||||||||||||||||||||||||||||

Risk Rating: | ||||||||||||||||||||||||||||||||

1-2 internal grade | $ | 1,398 | $ | 44,591 | $ | — | $ | — | $ | — | $ | — | $ | — | $ | 45,989 | ||||||||||||||||

3-4 internal grade | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||