Attached files

| file | filename |

|---|---|

| EX-99.4 - EX-99.4 - Eastern Bankshares, Inc. | d846554dex994.htm |

| EX-23.3 - EX-23.3 - Eastern Bankshares, Inc. | d846554dex233.htm |

| EX-3.1 - EX-3.1 - Eastern Bankshares, Inc. | d846554dex31.htm |

| EX-1.2 - EX-1.2 - Eastern Bankshares, Inc. | d846554dex12.htm |

| EX-1.1 - EX-1.1 - Eastern Bankshares, Inc. | d846554dex11.htm |

Table of Contents

As filed with the Securities and Exchange Commission on July 23, 2020

Registration No. 333-239251

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Eastern Bankshares, Inc.

Eastern Bank 401(k) Plan

(Exact Name of Registrant as Specified in Its Charter)

| Massachusetts | 6712 | 84-4199750 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code) |

(I.R.S. Employer Identification Number) |

265 Franklin Street

Boston, MA 02110

(800) 327-8376

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Mr. Robert F. Rivers

Chief Executive Officer and

Chair of the Board of Directors

265 Franklin Street

Boston, MA 02110

(800) 327-8376

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

| Michael K. Krebs, Esq. Nutter, McClennen & Fish, LLP 155 Seaport Boulevard Boston, MA 02210 (617) 439-2000 |

Kathleen C. Henry, Esq. Executive Vice President, General Counsel and Corporate Secretary 265 Franklin Street Boston, MA 02110 (800) 327-8376 |

Lee A. Meyerson, Esq. Lesley Peng, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, NY 10017 (212) 455-2000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of these securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☒

If this Form is filed to register additional shares for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement of the earlier effective registration statement for the same offering: ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of each class of securities to be registered |

Amount to be registered |

Proposed maximum offering price per share |

Proposed maximum aggregate offering price |

Amount of registration fee(3) | ||||

| Common stock, $0.01 par value per share |

210,084,636 | $10.00 | $2,100,846,360(1) | $272,689.86 | ||||

| Participation interests(2) |

11,141,591 | |||||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated solely for the purpose of calculating the registration fee. |

| (2) | The securities of Eastern Bankshares, Inc. to be purchased by the Eastern Bank 401(k) Plan are included in the amount shown for common stock. Accordingly, in accordance with Rule 457(h)(2), no separate fee is required for the participation interests. |

| (3) | Previously paid. |

The registrant hereby amends the registration on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting offers to buy these securities in any state or other jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 23, 2020

SUBSCRIPTION AND COMMUNITY

OFFERING PROSPECTUS

(Proposed holding company for Eastern Bank)

Up to 175,375,000 shares of common stock

(Subject to increase to up to 201,681,250 shares)

Eastern Bankshares, Inc., a Massachusetts corporation, is offering shares of common stock for sale in connection with the conversion of Eastern Bank Corporation, a mutual holding company, from the mutual to the stock form of organization. Eastern Bankshares, Inc. has never offered common stock for sale to the public, and consequently, there is no trading market for our common stock. We expect to list our common stock on the Nasdaq Global Select Market under the symbol “EBC.” We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012.

We are offering up to 175,375,000 shares of common stock for sale at $10.00 per share on a best efforts basis. We may sell up to 201,681,250 shares of common stock because of demand for the shares or changes in market conditions, without resoliciting subscribers. We must sell a minimum of 129,625,000 shares in order to complete the offering.

Upon the completion of the offering, we intend to donate to our charitable foundation, the Eastern Bank Charitable Foundation, a number of shares of our common stock equal to 4% of the shares that will be outstanding immediately after that donation.

The shares of common stock are first being offered in a “subscription offering” to eligible depositors and tax-qualified employee benefit plans of Eastern Bank, as well as employees, officers, trustees, directors and corporators of Eastern Bank, Eastern Insurance Group LLC, Eastern Bankshares, Inc. and Eastern Bank Corporation. Shares not purchased in the subscription offering may be offered for sale to the general public in a “community offering,” with a preference given to residents of the communities served by Eastern Bank. Any shares of common stock not purchased in the subscription or community offerings may be offered to the public through a syndicate of broker-dealers, referred to in this prospectus as the “syndicated offering.” The syndicated offering may commence before the subscription and community offerings (including any extensions) have expired. However, no shares purchased in the subscription offering or the community offering will be issued until the completion of any syndicated offering. In this prospectus, we refer to the subscription, community and syndicated offerings collectively as the “offering.”

The minimum order is 25 shares. Generally, no individual may purchase more than 200,000 shares. The subscription and community offerings are expected to expire at 2:00 p.m., Eastern Time, on [EXPIRATION DATE]. We may extend this expiration date without notice to you until [EXTENSION DATE]. Once submitted, orders are irrevocable unless the subscription and community offerings are terminated or extended, with regulatory approval, beyond [EXTENSION DATE], or the number of shares of common stock to be sold is increased to more than 201,681,250 shares or decreased to less than 129,625,000 shares. If the subscription and community offerings are extended past [EXTENSION DATE], all subscribers will be notified and given an opportunity to confirm, change or cancel their orders. If you do not respond to this notice, we will promptly return your funds with interest or cancel your deposit account withdrawal authorization. If the number of shares to be sold in the offering is increased to more than 201,681,250 shares or decreased to less than 129,625,000 shares, we will resolicit subscribers, and all funds delivered to us to purchase shares of common stock in the subscription and community offerings will be returned promptly with interest. Funds received in the subscription and the community offerings will be held in a segregated account at Eastern Bank and will earn interest at 0.02% per annum until completion or termination of the offering.

We have engaged Keefe, Bruyette & Woods, Inc. to be our selling agent, assisting us in selling the shares on a best efforts basis in the subscription and community offerings. J.P. Morgan Securities LLC is serving generally as our capital markets advisor. J.P. Morgan Securities LLC and Keefe, Bruyette & Woods, Inc. will serve as joint book-running managers for any syndicated offering. Neither Keefe, Bruyette & Woods, Inc. nor J.P. Morgan Securities LLC is required to purchase any shares of common stock that are sold in the offering.

OFFERING SUMMARY

Price: $10.00 per Share

| Minimum | Midpoint | Maximum | Adjusted Maximum |

|||||||||||||

| Number of shares |

129,625,000 | 152,500,000 | 175,375,000 | 201,681,250 | ||||||||||||

| Gross offering proceeds |

$ | 1,296,250,000 | $ | 1,525,000,000 | $ | 1,753,750,000 | $ | 2,016,812,500 | ||||||||

| Estimated offering expenses, excluding selling agent fees and expenses |

$ | 10,577,000 | $ | 10,577,000 | $ | 10,577,000 | $ | 10,577,000 | ||||||||

| Estimated selling agent fees and expenses and underwriters’ compensation (1) |

$ | 23,364,979 | $ | 27,349,042 | $ | 31,333,104 | $ | 35,914,776 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Estimated net proceeds |

$ | 1,262,308,021 | $ | 1,487,073,958 | $ | 1,711,839,896 | $ | 1,970,320,724 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Estimated net proceeds per share |

$ | 9.74 | $ | 9.75 | $ | 9.76 | $ | 9.77 | ||||||||

| (1) | Assumes 80% of shares are sold in the subscription and community offerings and 20% of shares are sold in the syndicated offering, and includes reimbursement of selling agent’s expenses. See the section of this prospectus titled “Pro Forma Data” and “The Conversion and Offering—Plan of Distribution; Selling Agent and Underwriter Compensation” for information regarding compensation to be received by Keefe, Bruyette & Woods, Inc. and J.P. Morgan Securities LLC in the subscription and community offerings and the compensation to be received by J.P. Morgan Securities LLC, Keefe, Bruyette & Woods, Inc., and other participating broker-dealers in the syndicated offering. If all shares are sold in the syndicated offering, excluding those purchased by our insiders and by our employee stock ownership plan and donated to our charitable foundation, for which no selling agent fee will be paid, the selling agent fees and expenses would be approximately $64.7 million, $77.3 million, $88.8 million and $102.1 million at the minimum, midpoint, maximum, and adjusted maximum of the offering range, respectively. |

This investment involves a degree of risk, including the possible loss of principal.

Please read “Risk Factors ” beginning on page 19.

Shares of our common stock are not deposits or accounts and are not insured or guaranteed by the Federal Deposit Insurance Corporation, or any other government agency. None of the Securities and Exchange Commission, the Board of Governors of the Federal Reserve System, the Massachusetts Commissioner of Banks, the Federal Deposit Insurance Corporation, nor any state securities regulator has approved or disapproved of these securities or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

For assistance, please contact the Stock Information Center at [stock center number].

The date of this prospectus is [prospectus date].

Table of Contents

Table of Contents

| 1 | ||||

| 19 | ||||

| 48 | ||||

| 50 | ||||

| 66 | ||||

| 67 | ||||

| 69 | ||||

| 70 | ||||

| 71 | ||||

| 72 | ||||

| 74 | ||||

| 80 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

81 | |||

| 121 | ||||

| 132 | ||||

| 143 | ||||

| 145 | ||||

| 152 | ||||

| 153 | ||||

| 161 | ||||

| 162 | ||||

| 180 | ||||

| 183 | ||||

| 187 | ||||

| 188 | ||||

| 189 | ||||

| 189 | ||||

| 190 | ||||

| F-1 | ||||

i

Table of Contents

The following summary explains material information in this prospectus. It may not contain all of the information that is important to you. Before making an investment decision, you should read this entire document carefully, including the consolidated financial statements and the notes thereto, and the section titled “Risk Factors.”

In this prospectus, the terms “we,” “our,” “us,” “Eastern” and “company” refer collectively to Eastern Bank Corporation, Eastern Bankshares, Inc., Eastern Bank and Eastern Insurance Group LLC unless the context indicates another meaning. Any reference in this prospectus to the term the “Bank” refers to Eastern Bank, and any reference to the “Foundation” refers to the Eastern Bank Charitable Foundation. Any reference in this prospectus to the term “offering” refers to the offering of Eastern Bankshares, Inc. common stock in the subscription, community and syndicated offerings described in this prospectus.

The Companies; Our Business

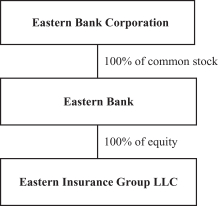

Eastern Bankshares, Inc. is a Massachusetts corporation formed in 2020 to conduct the offering. Upon completion of the offering, Eastern Bankshares, Inc. will own all of Eastern Bank’s capital stock, and through Eastern Bank and its wholly owned subsidiary Eastern Insurance Group LLC, Eastern Bankshares, Inc. will provide a variety of banking, trust and investment, and insurance services. Eastern Bankshares, Inc. currently does not intend to engage in any material business activity other than those relating to owning all of the capital stock of Eastern Bank. (Please refer to the section of this prospectus titled “The Conversion and Offering—Reorganization of Eastern Immediately Prior to Completion of Offering” for a description of the reorganization of Eastern that will occur simultaneously with the completion of the offering.)

Eastern Bankshares, Inc.’s executive offices are located at 265 Franklin Street, Boston, MA 02110, and its telephone number is 1.800.EASTERN (1.800.327.8376).

The historical financial data presented in this prospectus are derived from the financial statements of Eastern Bank Corporation, including Eastern Bank Corporation’s audited consolidated financial statements as of and for the years ended December 31, 2019 and 2018 and Eastern Bank Corporation’s unaudited consolidated financial statements as of and for the three months ended March 31, 2020 and 2019. The section of this prospectus titled “Recent Developments” includes certain unaudited financial data of Eastern Bank Corporation as of and for the six months ended June 30, 2020.

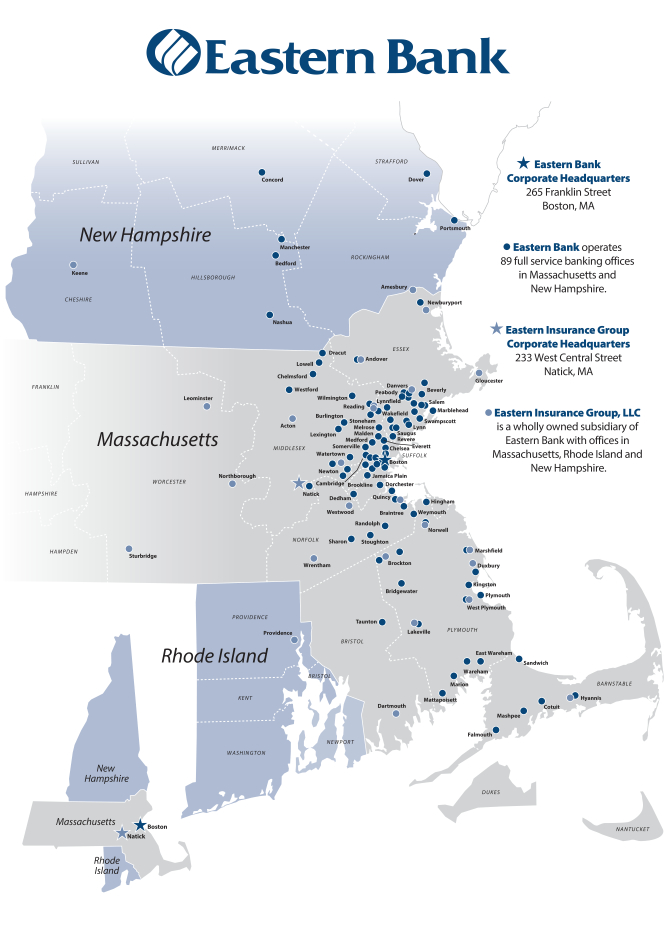

Eastern Bank is a Massachusetts-chartered bank headquartered in Boston that has served our community for over 200 years. Founded in 1818 as a local savings bank, we have evolved over the years into a diversified commercial bank, providing a broad array of products and services to retail, commercial and small business customers. We operate primarily in the greater Boston market with 89 banking offices located in eastern Massachusetts and southern and coastal New Hampshire. We have two business segments: banking and insurance agency operations. As of March 31, 2020, we had consolidated total assets of $12.3 billion, total gross loans of $9.1 billion, total deposits of $10.3 billion and total stockholders’ equity of $1.7 billion.

Our mission is to invest in our customers, communities and colleagues to help them prosper and grow. We pride ourselves on understanding our customers’ financial needs and delivering a diverse suite of tailored, high-quality solutions through a consultative approach that fosters long-term relationships. We have stayed true to our communities since 1818, especially over the last few decades through the generosity of the Eastern Bank Charitable Foundation and the robust volunteerism of our talented employees. We consistently invest in our colleagues and believe our diverse and inclusive workforce is crucial to our success. Overall, we like to think of ourselves as good people, doing good things to help people prosper.

We believe that, as a result of our differentiated approach to banking, we have established a distinctive brand and reputation in the market, contributing to Eastern having the greatest share of deposits in the Boston market for any full-service bank headquartered in Boston. (Based upon the most currently available FDIC data as of June 30, 2019, our total deposits of $8.7 billion represented 2.4% of the Boston market.) We believe our focus on long-term client

1

Table of Contents

relationships contributes to our stable, low-cost deposit base, and that our long-term presence in the market enables us to prudently underwrite and originate high-quality assets and deliver more stable returns. In addition, we believe these benefits from our focus on long-term client relationships position us well for times of stress and allow us to successfully manage through the full range of economic cycles.

For the quarter ended March 31, 2020 our annualized return on average assets was 0.29% driven by a net interest margin of 0.94%, cost of total deposits of 0.23% and fee income as a percent of revenue of 29.49%. At March 31, 2020, our ratio of common equity tier 1 capital to total assets, which we refer to as our “CET1 ratio,” was 12.42%, and our ratio of net loans to deposits was 87.03%. We are committed to expanding our business in a disciplined manner with a long-term perspective. We believe that we have prudently grown our business over the past five years, with a focus on transaction deposits and loans to commercial clients. For the five-year period from January 1, 2015 through December 31, 2019, our checking accounts (our primary relationship deposit product) grew from $4.2 billion to $5.3 billion, representing a compounded annual growth rate of 5.2%, and our commercial loans (our primary strategic focus for loan growth) grew from $4.1 billion to $6.2 billion, representing a compounded annual growth rate of 8.6%.

Our diversified products and services include lending, deposit, wealth and insurance products. Deposits obtained through our branch banking network have traditionally been the principal source of funds for use in lending and for other general business purposes. We offer a range of demand deposits, interest checking, money market accounts, savings accounts, and time certificates of deposit. Our lending focuses on the following loan categories: commercial and industrial (including our Asset Based Lending Portfolio), commercial real estate, commercial construction, small business banking, residential real estate, and home equity loans. Through Eastern Bank’s wealth management offering, we provide a wide range of trust services. Eastern Insurance Group LLC, a wholly owned subsidiary of Eastern Bank, acts as an agent in offering insurance solutions for clients with personal, commercial or employee benefits-related insurance needs. Eastern Insurance Group LLC operates through 22 non-branch offices located primarily in eastern Massachusetts.

Our website address is www.easternbank.com. Information on this website is not and should not be considered a part of this prospectus.

Eastern Insurance Group LLC, a wholly owned subsidiary of Eastern Bank, acts as an agent in offering property and casualty as well as life and health insurance to both personal and commercial customers. Personal lines insurance products include life, accident and health, automobile, and property and liability insurance including fire, condominium, home and tenants, among others. Commercial insurance products include group life and health, commercial property and liability, surety, and workers compensation insurance, among others. Eastern Insurance Group LLC operates through 22 non-branch offices in Eastern Massachusetts, one office in Keene, New Hampshire, and one office in Providence, Rhode Island. From 2004 through 2018, we expanded Eastern Insurance Group LLC by acquiring 31 independent insurance agencies, having average revenue of $1.4 million.

Regulation and Supervision

Upon the completion of the offering, Eastern Bankshares, Inc. will be subject to regulation and supervision by the Board of Governors of the Federal Reserve System, which we refer to as the Federal Reserve Board. The activities of Eastern Bank are subject to regulation and supervision by the Federal Deposit Insurance Corporation, which we refer to as the FDIC, and the Consumer Financial Protection Bureau, which we refer to as the CFPB. Eastern Bank is also subject to various Massachusetts and New Hampshire business and banking regulations, and supervision by the Massachusetts Commissioner of Banks. In addition, Eastern Bankshares, Inc. will be subject to various Massachusetts business and banking regulations. Our insurance agency, Eastern Insurance Group LLC, is subject to regulation and supervision by the Massachusetts Division of Insurance, and various state insurance regulatory authorities in other states that license, regulate and supervise insurance producers, brokers and agents. Upon the completion of the offering, we expect that Eastern Bankshares, Inc. common stock will be listed for trading on the Nasdaq Global Select Market (“Nasdaq”) and will be subject to the rules thereof for listed companies.

2

Table of Contents

Our Organizational Structure and the Proposed Offering

The following diagram shows our current organizational structure.

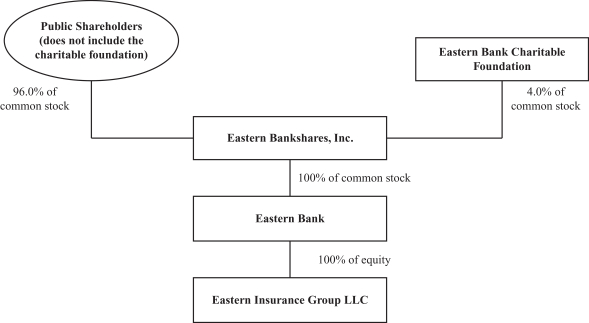

The following diagram shows our organizational structure immediately following the offering and our donation of shares of our common stock to the Eastern Bank Charitable Foundation.

Our Competitive Strengths

Abiding commitment to long-term, customer-centric relationships. We pride ourselves on understanding our customers’ financial needs and delivering a diverse suite of tailored, high-quality solutions through a consultative approach that fosters long-term relationships. We have served our communities for over 200 years, evolving from a traditional mutual savings bank serving a relatively narrow geographic region northeast of Boston to a full-service commercial bank with a presence across eastern Massachusetts and southern New Hampshire. We believe that over time we have developed long-standing customer relationships and established a distinctive brand, which emphasizes our commitment to our community and social activism.

Well-positioned in attractive greater Boston market. The Boston Metropolitan Statistical Area is one of the largest banking markets in the country with a high concentration of affluent, highly-educated individuals and

3

Table of Contents

successful businesses. It has a diverse and vibrant business community supported by world class higher education institutions. We believe we have distinguished ourselves in the market through our distinctive approach to banking, notably our focus on customers, commitment to community and diversity of our workforce. Our strong brand, reputation and client relationships have become key drivers of our performance in the market.

Stable, low-cost deposit base. We believe our business model of fostering deep client relationships and our long-standing position in our communities allows us to attract deposit customers that are focused on more than just price. As a result, we have a stable, low-cost deposit base. Our average cost of total deposits for the quarter ended March 31, 2020 was 0.23% compared to 0.84% for the peer group used by RP Financial, LC for purposes of its independent valuation discussed elsewhere in this prospectus. Our funding advantage and deep client relationships enable us to prudently deploy our liquidity into high-quality loans and generate attractive returns. Generally, we do not take brokered deposits.

Strong capital and liquidity position. At March 31, 2020, our CET1 ratio was 12.42%, and our cash and securities as a percentage of assets was 18.77%. On a pro forma basis, giving effect to the offering and the proposed use of proceeds discussed elsewhere in this prospectus, we will be the most well-capitalized and most liquid bank in the peer group used by RP Financial, LC in its appraisal. Assuming an offering at the mid-point of the valuation range, our pro forma CET1 ratio of 24.52% will be 263 bps above the next most well-capitalized bank in that peer group as of March 31, 2020. We believe our strong capital position will serve as a strong foundation in a period of significant economic uncertainty like we are experiencing today, providing us the financial flexibility to continue to invest in our businesses and execute on our strategic initiatives. A large proportion of our balance sheet will be comprised of highly liquid assets, which will allow us to continue to meet customer liquidity and funding needs in times of stress.

Disciplined underwriting and risk management. We focus on originating high-quality loans for our clients, which we believe generate stable returns. We believe our experienced credit risk professionals and conservative credit culture, combined with centralized processes and consistent underwriting standards, have generally allowed us to maintain high asset quality. We believe we have positioned the company to successfully navigate a wide range of credit and interest rate environments, including the current uncertain economic environment due to the Covid-19 pandemic and current low interest rates. We have long maintained a diversified loan portfolio with limited industry or property type concentrations. Our loans to borrowers engaged in various wholesale trade businesses, including household appliances, alcoholic beverage wholesalers, and grocery wholesalers, represent the largest concentration among our commercial borrowers, constituting 12% of our commercial portfolio at March 31, 2020. Our largest property type concentration in our commercial real estate portfolio as of March 31, 2020 is multi-family at 19%.

Culture of technological innovation. We believe our ability to innovate and integrate new products, services and technology distinguishes us from many of our similarly-sized peers. Important to our development and refinement of technology-driven products and services in recent years has been customizing the interface between our customers and our outsourced core data processing systems. By customizing the software that connects our digital platforms to our core system, we believe we are able to develop, test and deploy new features and products more quickly than many of our peers. In addition, during the Covid-19 global pandemic, we were able to quickly transition more than half our workforce to work remotely, with our technology team working closely with senior management to ensure that systems and applications were in place to support a secure remote work environment while meeting an unprecedented surge in customer needs.

Experienced management team supported by a high-performing and diverse workforce. We believe that we have a highly experienced leadership team with deep roots in our markets, which on average has 30.9 years of experience working in banking or the financial services sector, has successfully operated through the full range of economic cycles. Complementing their experience at Eastern, most of our executive officers have had prior management experience at other leading companies and institutions, including publicly-traded banking companies. Our leadership team is supported by a high quality, highly motivated, diverse set of managers and employees committed to delivering a strong customer value proposition. We are recognized as an employer of choice by providing employees with opportunities for advancement and growth in an attractive business environment.

Commitment to communities. We believe our strong commitment to our communities provides a competitive advantage by strengthening customer relationships and increasing loyalty. The communities in our footprint are one of our three core constituencies (along with our colleagues and customers). We support our communities in a number of

4

Table of Contents

ways, including: through extensive employee volunteer efforts; through our donations to the Eastern Bank Charitable Foundation, a private foundation we formed in 1994; through executives providing board leadership to community organizations; and through the Bank’s social justice advocacy work. The Eastern Bank Charitable Foundation, which had total assets of $111.8 million as of March 31, 2020, funds a range of non-profit organizations serving our communities and creates partnerships with other organizations to “scale up” key initiatives (such as enhancing early childhood education). For the three-year period ended December 31, 2019, the Eastern Bank Charitable Foundation’s annual charitable donations averaged approximately $7.6 million. Our stock donation to the Foundation upon completion of the offering will allow the Foundation, and indirectly the communities that we serve, both now and in the future, to share in our long-term growth.

Our commitment to our community also is reflected in Eastern Bank’s latest FDIC CRA rating, which was “Outstanding.”

Business Strategy

Our goal is to enhance our position as one of the leading community banking institutions in our market, providing a broad array of banking and other financial services to retail, commercial and small business customers. In recent years, we have focused significant effort on and invested heavily in our infrastructure to create sophisticated and competitive products and services, a strong, experienced work force and awareness of our banking brand.

As a result, we believe we are well positioned to capitalize on the opportunities available in our market by focusing on the following core strategies.

Develop new customer relationships and deepen existing relationships. We seek to expand our market share in existing and contiguous markets across our businesses by leveraging our distinctive brand and delivering a diverse suite of tailored, high-quality solutions through a consultative, relationship-based approach reinforced by superior customer service. We believe this will result in disciplined growth of low-cost deposits, loans with attractive risk-adjusted returns and a steady stream of fee income. Our relationship-based approach has enabled us to achieve disciplined organic growth over time, and we expect this trend to continue. We believe our support of our small business and non-profit customers in obtaining funding in April and May 2020 under the Paycheck Protection Program, also known as “PPP,” demonstrates both our commitment and capacity to meet our customers’ needs, even in the most challenging circumstances. The Small Business Administration, or “SBA,” approved all applications for PPP funding across the nation on a “first come, first served” basis. We believe that our experience as the largest SBA lender in New England made us effective in helping a large number of our customers avail themselves of the very attractive PPP terms. Through June 30, 2020, we originated approximately 8,100 PPP loans, representing $1.1 billion of aggregate PPP loans. The vast majority of our PPP borrowers are existing commercial and small business borrowers, non-profit customers, retail banking customers and clients of Eastern Wealth Management and Eastern Insurance Group LLC. Please refer to the section of this prospectus titled “Recent Developments” for additional information regarding our PPP loans as of June 30, 2020.

Pursue opportunistic acquisitions. We intend to prudently pursue opportunities to acquire banks in our existing and contiguous markets that create attractive financial returns. Our focus will primarily be on franchises that enhance our funding profile, product capabilities or geographic density, while maintaining an acceptable risk profile. We believe the vital need to make increasingly significant technological investments has greatly amplified the importance of scale in banking. In addition, we believe that the current economic recession will increase the rate of consolidation in the banking industry. We believe that after the offering we will be well-positioned as a consolidator in the banking market because of our financial strength, reputation and culture. In addition, we intend to continue to pursue opportunistic acquisitions of additional insurance agencies in existing and contiguous markets.

Leverage technology to enhance customer experience and drive operating efficiencies. We have made significant investments in our technology to ensure we can deliver high-quality, innovative products and services to our customers. For example, we have recently upgraded our Mobile Banking platform for both consumer and commercial customers. In addition, we have continued investing in our new commercial lending origination system and platform, and we intend to progressively improve our consumer lending origination platform as well. We are committed to

5

Table of Contents

regularly investing in technology and data analytics, as we are positioning our franchise for the future. We believe these investments will differentiate us with our target customers and provide a scalable platform, which will generate significant operating leverage as we grow over time.

Maintain and grow our experienced, diverse and customer focused employee base. We have an established corporate culture based on personal accountability, high ethical standards and a commitment to training and career development. We will look to opportunistically hire talented bankers and employees with a continued emphasis on recruiting highly motivated, diverse managers and employees who can establish and maintain long-term customer relationships that are key to our business, brand and culture.

Manage risk to navigate a range of economic environments, including the current Covid-19 pandemic recession. We believe that our conservative credit culture, strong capital and liquidity position and our deep client relationships are key to our long-term financial success. We believe that stable long-term growth and profitability are the result of building strong customer relationships one at a time while maintaining superior credit discipline. We supplement our conservative risk culture with a rigorous and continuous enterprise risk management program. The current Covid-19 pandemic recession is resulting in material uncertainty in the near- and medium-term future. In addition, a sustained period of low interest rates will put pressure on our net interest margin. We believe we are entering this period of stress from a position of strength, which allows us to maintain a strong balance sheet while still supporting our customers and communities in need.

Reasons for the Offering

Our strategic objective for many years has been to evolve over time into one of the leading banking institutions in our market by concentrating on achieving disciplined, profitable growth in our core business lines while maintaining an abiding commitment to our customers, colleagues and communities. Profitable growth provides us with the flexibility to pursue strategic acquisitions as opportunities arise and to make additional technological, risk management and talent investments.

We believe the additional capital provided by the offering will, when added to our existing well-capitalized balance sheet, give us a strong foundation that in the near-term will help us to remain resilient while the regional, national and global economies recover from the recession caused by Covid-19 pandemic and over the longer-term allow us to accelerate our growth—principally by:

Enhancing our capital and liquidity position to increase our resiliency in the short-term and to provide a foundation for long-term future growth. By substantially increasing our regulatory capital and liquidity, the offering will enhance our capacity to build and maintain credit reserves in the near term while maintaining the financial flexibility to support all of our stakeholders, including by continuing to work constructively with our borrowers adversely affected by the Covid-19 recession, offering payment deferrals, loan modifications and, where prudent, additional lines of credit to our business customers with proven track records. Over the longer-term, the substantial increase in our regulatory capital and liquidity will provide a foundation for us to renew our focus on pursuing profitable loan and deposit growth through disciplined organic growth in our core business lines consistent with our overarching goal of serving more people, businesses and communities for many more generations.

Enhancing our ability to make investments in new technologies to meet the ever-increasing customer demands for “ease of use” of banking and financial services. As we anticipate the competitive landscape that will emerge after our economy recovers from the negative impacts of the Covid-19 pandemic, we believe the most significant systemic challenge we will face is the accelerating pace of technological change driven by ubiquitous digital adoption by both consumer and commercial banking customers. We believe this trend has greatly amplified the importance of scale in banking, and the increasing benefit of scale exacerbates the challenge of competing with significantly larger banks and large information technology and e-commerce companies. The capital raised in the offering will allow us to increase our investments in new technologies to develop and implement an increasingly sophisticated array of banking and other financial services for retail, small business and commercial customers to meet the ever-increasing customer expectations for “ease of use” of banking and financial services and products.

6

Table of Contents

Better positioning us to pursue opportunistic strategic transactions within our existing and contiguous markets and through digital delivery channels. We believe the additional capital raised in the offering, coupled with our structure as a publicly-traded company, will make us a more attractive and competitive bidder for mergers and acquisitions of other financial institutions or business lines as opportunities arise. We will be able to structure business combinations using stock, cash or a combination of both. We believe that the current economic recession will increase the rate of consolidation in the banking industry. We have completed seven bank acquisitions or mergers since 1999, the most recent of which was our 2014 acquisition of New Hampshire-based Centrix Bank. We also expect that a portion of the proceeds of the offering will be used to fund acquisitions of independent insurance agencies by Eastern Insurance Group LLC. From 2004 through 2018, we expanded Eastern Insurance Group LLC by acquiring 31 independent insurance agencies for an aggregate price of $124.9 million. We expect to maintain a disciplined approach to strategic transactions, focusing on opportunities in or contiguous to our market that create value for our shareholders and that we believe will likely materially enhance the strength of our franchise, while maintaining an acceptable risk profile. We do not currently have any agreement or understanding regarding any specific transaction.

Expanding and retaining a talented and diverse workforce. By increasing our capital through the offering, we believe that we will be better positioned to expand and retain a talented and diverse workforce dedicated to providing superior service to our customers and to fostering a culture of compliance and accountability. In addition, we believe the offering will enhance our ability to attract and retain qualified officers and employees by allowing us to implement various stock benefit plans, including an employee stock ownership plan concurrently with the offering and one or more equity incentive plans after the offering. Through continued investments in human capital and effective technology, we can continue to advance our mission to do good things to help people prosper.

Supporting our local communities through an additional significant and immediate donation to the Eastern Bank Charitable Foundation. We intend to donate to the Eastern Bank Charitable Foundation, upon the completion of the offering, a number of shares of our authorized but previously unissued common stock that will represent 4% of the shares of Eastern Bankshares, Inc. common stock that will be outstanding immediately after that donation. The opportunity to have an outsized philanthropic impact on the Foundation and the community-orientated non-profit organizations that it supports is viewed by our Board and senior management as an important benefit of the offering. Eastern Bank formed the Eastern Bank Charitable Foundation in 1994, and to date, Eastern Bank has been the sole source of the Foundation’s funding. The Eastern Bank Charitable Foundation had total assets of approximately $111.8 million at March 31, 2020, and for the three-year period ended December 31, 2019, the Foundation’s annual charitable donations averaged approximately $7.6 million. Our stock donation to the Foundation upon completion of the offering will complement our historical charitable giving and allow the Foundation, and indirectly the communities that we serve, both now and in the future, to share in our long-term growth. Although we expect that our annual charitable contributions after the offering and excluding the stock donation will be a small percentage of our net income, we believe the impact of that reduction will be offset by our stock donation.

Enhancing our ability to positively impact local communities through expanded volunteerism and enhanced advocacy influence. We believe that with increased scale through both organic growth and opportunistic strategic acquisitions—coupled with our culture of supporting community volunteerism, where we already are a market leader—we will be able to have a broader and deeper positive impact on our local communities. We also expect that with increased scale, we will be able to have a more impactful “voice” on social justice issues. Eastern takes pride in its public advocacy regarding social justice issues that affect the communities we serve. In recent years, we have advocated in support of immigrants and their families, pay equality and the LGBTQ+ community.

Offering our depositors, employees, officers, directors, trustees and corporators an equity ownership interest in our future growth and profitability. We believe that offering stock to our depositors, employees, officers, directors, trustees and corporators will provide those constituencies with an economic interest in our future success, should they decide to invest. We believe that an ownership interest in Eastern will help to align the interests of our employees with our overall profitability, complementing our organizational focus on continuing to improve Eastern so that it remains competitive in our markets for generations to come.

7

Table of Contents

Terms of the Offering

We are offering between 129,625,000 and 175,375,000 shares of common stock in a subscription offering to eligible depositors of Eastern Bank, our tax-qualified employee benefit plans, and our employees, officers, trustees, directors and corporators, and, to the extent shares remain available, to the general public in a community offering. If necessary, we will also offer shares to the general public in a syndicated offering. The number of shares of common stock to be sold may be increased to up to 201,681,250 shares as a result of demand for the shares of common stock in the offering or changes in market conditions. Unless the number of shares of common stock to be offered is increased to more than 201,681,250 shares or decreased to fewer than 129,625,000 shares, or the subscription and community offerings are extended beyond [EXPIRATION DATE], subscribers will not have the opportunity to change or cancel their stock orders once submitted. If the subscription and community offerings are extended past [EXPIRATION DATE], all subscribers will be notified and given an opportunity to confirm, change or cancel their orders. If you do not respond to that notice, your order will be cancelled and we will promptly return your funds with interest at 0.02% per annum or cancel your deposit account withdrawal authorization. If the number of shares to be sold is increased to more than 201,681,250 shares or decreased to less than 129,625,000 shares, all subscribers’ stock orders will be canceled, all withdrawal authorizations will be canceled and funds delivered to us to purchase shares of common stock in the subscription and community offerings will be returned promptly with interest at 0.02% per annum. We will then resolicit subscribers, giving them an opportunity to place new orders for a period of time. No shares purchased in the subscription offering and community offering will be issued until the completion of any syndicated offering.

The purchase price of each share of common stock offered for sale in the offering is $10.00. All investors will pay the same purchase price per share, regardless of whether the shares are purchased in the subscription offering, the community offering or a syndicated offering. Investors will not be charged a commission to purchase shares of common stock in the offering. Our marketing agent in the subscription and community offerings, Keefe, Bruyette & Woods, Inc., will use its best efforts to assist us in selling shares of our common stock in the subscription and community offerings but is not obligated to purchase any shares of common stock in the subscription and community offerings.

How We Determined the Offering Range and the $10.00 Per Share Stock Price

The amount of common stock we are offering for sale is based on an independent appraisal of the estimated market value of Eastern Bankshares, Inc., assuming the offering has been completed. RP Financial, LC, our independent appraiser, has estimated that, as of May 21, 2020, this market value, including the shares to be issued to Eastern Bank Charitable Foundation, was $1.6 billion. Based on applicable regulations, this market value forms the midpoint of a valuation range with a minimum of $1.4 billion and a maximum of $1.8 billion. Based on this valuation range, and the $10.00 per share price, the number of shares of common stock being offered for sale by Eastern Bankshares, Inc. ranges from 129,625,000 shares to 175,375,000 shares. The $10.00 per share price was selected primarily because it is the price most commonly used in mutual-to-stock conversions of financial institutions. If demand for shares or market conditions warrant, the appraisal can be increased, without resoliciting subscribers, by up to 15%, which would result in an appraised value of up to $2.1 billion and an offering of up to 201,681,250 shares of common stock.

8

Table of Contents

The appraisal is based in part on Eastern Bankshares, Inc.’s financial condition and results of operations, the pro forma effect of the additional capital raised by the sale of shares of common stock in the offering, and an analysis of a peer group of eleven publicly traded bank holding companies and savings and loan holding companies that RP Financial, LC considers comparable to Eastern Bankshares, Inc. The appraisal peer group consists of the following companies, all of which are traded on the Nasdaq Stock Market or the New York Stock Exchange.

| Company Name |

Ticker Symbol |

Headquarters |

Total Assets (1) | |||||

| (in millions) | ||||||||

| Brookline Bancorp, Inc. |

BRKL | Boston, MA | $ | 8,462 | ||||

| Independent Bancorp, Inc. |

INDB | Rockland, MA | $ | 11,980 | ||||

| Meridian Bancorp, Inc. |

EBSB | Peabody, MA | $ | 6,349 | ||||

| Eagle Bancorp, Inc. |

EGBN | Bethesda, MD | $ | 9,992 | ||||

| Kearny Financial Corp. |

KRNY | Fairfield, NJ | $ | 6,774 | ||||

| Northwest Bancshares, Inc. |

NWBI | Warren, PA | $ | 10,681 | ||||

| OceanFirst Financial Corp. |

OCFC | Toms River, NJ | $ | 10,489 | ||||

| Provident Financial Services, Inc. |

PFS | Jersey City, NJ | $ | 10,085 | ||||

| S&T Bancorp, Inc. |

STBA | Indiana, PA | $ | 9,005 | ||||

| First Commonwealth Financial Corporation |

FCF | Indiana, PA | $ | 8,515 | ||||

| WSFS Financial Corporation |

WSFS | Wilmington, DE | $ | 12,279 | ||||

| (1) | Asset size for all companies is as of March 31, 2020 or the most recent date available. |

The following table presents a summary of selected pricing ratios for Eastern Bankshares, Inc. (on a pro forma basis assuming completion of the offering) as of and for the 12 months ended March 31, 2020, and for the peer group companies based on earnings and other information as of and for the 12 months ended March 31, 2020, with stock prices as of May 21, 2020, as reflected in the appraisal report. Compared to the average pricing of the peer group, our pro forma pricing ratios at the midpoint of the offering range indicated a discount of 31.55% on a price-to-book value basis, a discount of 41.88% on a price-to-tangible book value basis and a premium of 71.70% relative to the peer group’s average core price-to-earnings multiple.

| Eastern Bankshares, Inc. (on a pro forma basis, assuming completion of the offering) |

Price-to- earnings multiple (1) |

Price-to- book value ratio |

Price-to- tangible book value ratio |

|||||||||

| Adjusted maximum |

23.91x | 61.77 | % | 69.44 | % | |||||||

| Maximum |

20.14x | 57.57 | % | 65.32 | % | |||||||

| Midpoint |

17.05x | 53.39 | % | 61.12 | % | |||||||

| Minimum |

14.12x | 48.64 | % | 56.27 | % | |||||||

| Valuation of peer group companies, all of which are fully converted (on a historical basis) |

||||||||||||

| Averages |

9.93x | 78.00 | % | 105.16 | % | |||||||

| Medians |

8.20x | 73.88 | % | 104.34 | % | |||||||

| (1) | Price-to-earnings multiples calculated by RP Financial, LC in the independent appraisal are based on an estimate of “core” or recurring earnings. These ratios are different than those presented in “Pro Forma Data.” |

9

Table of Contents

The independent appraisal does not indicate trading market value. Do not assume or expect that our valuation as indicated in the appraisal means that after the offering the shares of our common stock will trade at or above the $10.00 per share purchase price. Furthermore, the pricing ratios presented in the appraisal were used by RP Financial, LC to estimate our pro forma appraised value for regulatory purposes and not to compare the relative value of shares of our common stock with the value of the capital stock of the peer group. The value of the capital stock of a particular company may be affected by a number of factors such as financial performance, asset size and market location.

For a more complete discussion of the amount of common stock we are offering for sale and the independent appraisal, please see the section of this prospectus titled “The Conversion and Offering—Stock Pricing and Number of Shares to be Issued.”

How We Intend to Use the Proceeds From the Offering

We intend to contribute 50% of the net proceeds from the offering to Eastern Bank’s capital. The remaining net proceeds from the offering will be used in part to fund a loan to the employee stock ownership plan to finance its purchase of shares in the offering (or possibly, after the offering, in open market purchases) and the balance will be retained by Eastern Bankshares, Inc.

Assuming we sell 152,500,000 shares of common stock in the offering at the midpoint of the offering range, and we have net proceeds of $1.5 billion, we intend to contribute $747.3 million to Eastern Bank as common equity, loan to our employee stock ownership plan $127.1 million to fund its purchase of shares of common stock and retain the remaining $620.2 million of the net proceeds at Eastern Bankshares, Inc.

Eastern Bankshares, Inc. may use the funds it retains for investment, to repurchase shares of common stock, to acquire other financial institutions or financial services companies, to pay cash dividends and for other general corporate purposes. Eastern Bank expects to use the proceeds it receives primarily to support increased lending, enhance existing, or support the development of new, products and services, enhance the development of our employees and to pursue strategic growth opportunities primarily by acquiring other banking and insurance agency businesses as opportunities arise. We do not currently have any agreement or understanding regarding any acquisition transaction.

Please see the section of this prospectus titled “How We Intend to Use the Proceeds from the Offering” for more information on the proposed use of the proceeds from the offering.

Persons Who May Order Shares of Common Stock in the Offering

We are offering the shares of common stock in a subscription offering in the following descending order of priority:

| (i) | To depositors with accounts at Eastern Bank with aggregate balances of at least $50 at the close of business on March 29, 2019. |

| (ii) | To depositors with accounts at Eastern Bank with aggregate balances of at least $50 at the close of business on March 31, 2020. |

| (iii) | To our tax-qualified employee benefit plans (including Eastern Bank’s employee stock ownership plan and Eastern Bank’s 401(k) plan which may subscribe for, in the aggregate, up to 10% of the shares of common stock sold in the offering). We expect our employee stock ownership plan to purchase 8% of the shares of our common stock outstanding immediately after the offering (including the shares we donate to the Eastern Bank Charitable Foundation). |

| (iv) | To employees, officers, directors, trustees and corporators of Eastern Bank, Eastern Bank Corporation or Eastern Insurance Group LLC who are not eligible in the first or second priority. |

10

Table of Contents

Shares of common stock not purchased in the subscription offering may be offered for sale to the general public in a community offering, with a preference given first to natural persons, and trusts of natural persons, residing in the following cities and towns:

Massachusetts

Abington, Acton, Acushnet, Amesbury, Andover, Arlington, Avon, Barnstable, Bedford, Belmont, Berkley, Beverly, Billerica, Boston, Bourne, Boxford, Braintree, Bridgewater, Brockton, Brookline, Burlington, Cambridge, Canton, Carlisle, Carver, Chelmsford, Chelsea, Cohasset, Danvers, Dedham, Dighton, Dover, Dracut, Dunstable, Duxbury, East Bridgewater, Easton, Essex, Everett, Fairhaven, Falmouth, Foxborough, Framingham, Freetown, Georgetown, Gloucester, Groton, Groveland, Halifax, Hamilton, Hanover, Hanson, Haverhill, Hingham, Holbrook, Hull, Ipswich, Kingston, Lakeville, Lawrence, Lexington, Lincoln, Littleton, Lowell, Lynn, Lynnfield, Malden, Manchester-by-the-Sea, Mansfield, Marblehead, Marion, Marshfield, Mashpee, Mattapoisett, Medford, Melrose, Merrimac, Methuen, Middleborough, Middleton, Milton, Nahant, Natick, Needham, Newbury, Newburyport, Newton, North Andover, North Reading, Norton, Norwell, Norwood, Peabody, Pembroke, Pepperell, Plymouth, Plympton, Quincy, Randolph, Raynham, Reading, Rehoboth, Revere, Rochester, Rockland, Rockport, Rowley, Salem, Salisbury, Sandwich, Saugus, Scituate, Sharon, Sherborn, Somerville, Stoneham, Stoughton, Swampscott, Taunton, Tewksbury, Topsfield, Tyngsborough, Wakefield, Walpole, Waltham, Wareham, Watertown, Wayland, Wellesley, Wenham, West Bridgewater, West Newbury, Westford, Weston, Westwood, Weymouth, Whitman, Wilmington, Winchester, Winthrop, Woburn and Yarmouth.

New Hampshire

Amherst, Atkinson, Auburn, Barrington, Bedford, Boscawen, Bow, Brentwood, Candia, Canterbury, Chester, Chichester, Concord, Danville, Derry, Dover, Durham, East Kingston, Epping, Exeter, Fremont, Goffstown, Hampstead, Hampton, Hampton Falls, Hollis, Hooksett, Hopkinton, Hudson, Kensington, Kingston, Lee, Litchfield, Londonderry, Loudon, Madbury, Manchester, Merrimack, Nashua, New Boston, New Castle, Newfields, Newington, Newmarket, Newton, North Hampton, Pelham, Pembroke, Plaistow, Portsmouth, Raymond, Rochester, Rollinsford, Rye, Salem, Sandown, Seabrook, Somersworth, South Hampton, Stratham, Webster, Warner and Windham.

The community offering may occur either concurrently with or after the subscription offering.

We also may offer for sale shares of common stock not purchased in the subscription offering and the community offering through a syndicated offering. J.P. Morgan Securities LLC and Keefe, Bruyette & Woods, Inc. will act as joint book-running managers for the syndicated offering, if any.

We have the right to accept or reject, in our sole discretion, orders received in the community offering or syndicated offering, and our interpretation of the terms and conditions of the Plan of Conversion will be final. Any determination to accept or reject stock orders in the community offering or syndicated offering will be based on the facts and circumstances available to management at the time of the determination.

If we receive orders for more shares than we are offering, we may not be able to fully or partially fill your order. A detailed description of the subscription offering, the community offering and the syndicated offering, as well as a discussion regarding allocation procedures, can be found in the section of this prospectus titled “The Conversion and Offering.”

Limits on How Much Common Stock You May Purchase

The minimum number of shares of common stock that may be purchased is 25 shares.

Generally, no individual with one or more qualifying accounts or individual exercising subscription rights through a single account held jointly may purchase more than 200,000 shares ($2,000,000) of common stock. If any of the

11

Table of Contents

following persons purchase shares of common stock, their purchases, in all categories of the offering, when combined with your purchases, cannot exceed 200,000 shares ($2,000,000) of common stock:

| • | most companies, trusts or other entities in which you are a senior officer, partner, trustee or have a substantial beneficial interest; or |

| • | your spouse or any relative of you or your spouse living in your house or who is a director, trustee, or officer of Eastern Bank Corporation, Eastern Bankshares, Inc. or Eastern Bank; or |

| • | other persons who may be your “associates” (as defined below) or persons acting in concert with you. |

Unless we determine otherwise, persons having the same address and persons exercising subscription rights through qualifying deposit accounts registered to the same address will be subject to the overall purchase limitation of 200,000 shares ($2,000,000).

The following relatives of directors, trustees and officers will be considered “associates” of these individuals regardless of whether they share a household with the director, trustee or officer: any child, stepchild, grandchild, parent, stepparent, grandparent, spouse, sibling, mother-in-law, father-in-law, son-in-law, daughter-in-law, brother-in-law or sister-in-law. This also includes adoptive relationships.

Subject to regulatory approval, we may increase or decrease the purchase limitations at any time. See the detailed description of the purchase limitations in the section of this prospectus titled “The Conversion and Offering—Additional Limitations on Common Stock Purchases.”

How You May Purchase Shares of Common Stock in the Subscription Offering and the Community Offering

In the subscription offering and community offering, you may pay for your shares only by:

| (i) | personal check, bank check or money order made payable directly to Eastern Bankshares, Inc.; or |

| (ii) | authorizing us to withdraw available funds from the types of Eastern Bank deposit account(s) designated on the stock order form. |

Eastern Bank is not permitted to lend funds to anyone to purchase shares of common stock in the offering. Additionally, you may not use a line of credit check from Eastern Bank or any type of third party check (such as a check payable to you and endorsed over to Eastern Bankshares, Inc.) to pay for shares of common stock. Please do not submit cash. You may not designate withdrawal from Eastern Bank’s accounts with check-writing privileges; instead, please submit a check. You may not authorize direct withdrawal from an individual retirement account, or IRA, held at Eastern Bank. See the section of this prospectus titled “—Using Individual Retirement Account Funds to Purchase Shares of Common Stock.”

You may subscribe for shares of common stock in the subscription and community offerings by delivering a signed and completed original stock order form, together with full payment payable to Eastern Bankshares, Inc. or authorization to withdraw funds from one or more of your deposit accounts at Eastern Bank, provided that the stock order form is received before 2:00 p.m., Eastern Time, on [SUBSCRIPTION DEADLINE], 2020, which is the end of the subscription offering period. You may submit your stock order form and payment by mail using the stock order reply envelope provided or by overnight delivery to the address indicated on the stock order form. You may also hand-deliver stock order forms to the following location: 195 Market Street, Lynn, MA 01901. Hand-delivered stock order forms will only be accepted at this location. We will not accept stock order forms at our banking offices. Please do not mail stock order forms to Eastern Bank’s offices.

Please see the section of this prospectus titled “The Conversion and Offering—Procedure for Purchasing Shares in Subscription and Community Offerings—Payment for Shares” for a complete description of how to purchase shares in the subscription and community offerings.

Using Individual Retirement Account Funds to Purchase Shares of Common Stock

You may be able to subscribe for shares of common stock using funds in your individual retirement account (“IRA”) or other retirement account. If you wish to use some or all of the funds in your IRA or other retirement

12

Table of Contents

account held at Eastern Bank, the applicable funds must be transferred to an IRA or other retirement account that can hold common stock and that is maintained by an independent custodian or trustee, such as a brokerage firm, before you place your stock order. If you do not have such an account, you will need to establish one. A one-time and/or annual administrative fee may be payable to the independent custodian or trustee. Because individual circumstances differ and the processing of retirement fund orders takes additional time, we recommend that you contact our Stock Information Center promptly, preferably at least two weeks before the [EXPIRATION DATE] offering deadline, for assistance with purchases using funds in your IRA or other retirement account held at Eastern Bank or elsewhere. Whether you may use such funds for the purchase of shares in the offering may depend on timing constraints and, possibly, limitations imposed by the institution where the funds are held.

Please see the sections of this prospectus titled “The Conversion and Offering—Procedure for Purchasing Shares in Subscription and Community Offerings—Payment for Shares” and “—Using Individual Retirement Account Funds” for a complete description of how to use IRA funds to purchase shares of common stock in the offering.

Market for Common Stock

We expect that our common stock will be listed for trading on the Nasdaq Global Select Market under the symbol “EBC.” J.P. Morgan Securities LLC and Keefe, Bruyette & Woods, Inc. have advised us that they intend to make a market in our common stock following the offering, but neither is under any obligation to do so.

Our Dividend Policy

Following completion of the offering, our Board of Directors will have the authority to declare dividends on our common stock, subject to our capital requirements, our financial condition and results of operations, tax considerations, statutory and regulatory limitations, and general economic conditions.

Eastern Bankshares, Inc. may not declare or pay a cash dividend on, or repurchase any of, its capital stock if the effect thereof would cause its net worth to be reduced below (i) the amount required for the Liquidation Account or (ii) the regulatory capital requirements of Eastern Bankshares, Inc. (to the extent applicable).

For more information regarding our proposed dividend policy, please see the section of this prospectus titled “Our Dividend Policy.”

Purchases by Directors and Executive Officers

We expect our directors and named executive officers, together with their associates, will subscribe for 1,407,500 shares of common stock in the offering, representing 1.1% of shares to be outstanding at the minimum of the offering range and 0.7% of shares to be sold in the offering at the maximum of the offering range. The purchase price paid by them will be the same $10.00 per share price paid by all other persons who purchase shares of common stock in the offering.

For more information on the proposed purchases of shares of common stock by our directors and executive officers, please see the section of this prospectus titled “Subscriptions by Directors and Executive Officers.”

Deadline for Orders of Shares of Common Stock in the Subscription and Community Offerings

The deadline for purchasing shares of common stock in the subscription and community offerings is 2:00 p.m., Eastern Time, on [SUBSCRIPTION DEADLINE], 2020, unless we extend this deadline. If you wish to purchase shares of common stock, a properly completed and signed original stock order form, together with full payment, must be received (not postmarked) by this time.

For a complete description of the deadline for purchasing shares in the offering, please see the section of this prospectus titled “The Conversion and Offering—Procedure for Purchasing Shares in Subscription and Community Offerings—Expiration Date.”

13

Table of Contents

You May Not Sell or Transfer Your Subscription Rights

Applicable regulations prohibit you from transferring your subscription rights. If you order shares of common stock in the subscription offering, you will be required to certify that you are purchasing the common stock for yourself and that you have no agreement or understanding to sell or transfer your subscription rights or the shares that you are purchasing. We intend to take legal action, including reporting persons to federal or state agencies, against anyone who we believe has sold or transferred his or her subscription rights. We will not accept your order if we have reason to believe you have sold or transferred your subscription rights. On the order form, you cannot add the names of others for joint stock registration who do not have subscription rights or who qualify only in a lower purchase priority than you do. Doing so may jeopardize your subscription rights. In addition, the stock order form requires that you list all deposit accounts, giving all names on each account and the account number at the applicable eligibility date. Failure to provide this information, or providing incomplete or incorrect information, may result in a loss of part or all of your share allocation if there is an oversubscription.

Delivery of Shares of Common Stock

All shares of common stock sold will be issued in book entry form. Stock certificates will not be issued. As soon as practicable following consummation of the offering, a statement reflecting ownership of shares of common stock issued in the subscription and community offerings will be mailed by our transfer agent to the persons entitled thereto at the registration address noted by them on their stock order form. We expect trading in the stock to begin on the day of completion of the offering or the next business day. The offering is expected to be completed as soon as practicable following satisfaction of the conditions described below in “—Conditions to Completion of the Offering.” Until a statement reflecting ownership of shares of common stock is available and delivered to purchasers, purchasers might not be able to sell the shares of common stock that they purchased, even though the common stock will have begun trading. Your ability to sell your shares of common stock before receiving your statement will depend on arrangements you may make with a brokerage firm.

Conditions to Completion of the Offering

We cannot complete the offering unless:

| • | We sell at least the minimum number of shares of common stock offered in the offering; |

| • | We receive approval from the Federal Reserve Board; and |

| • | We receive approval of the Massachusetts Commissioner of Banks to complete the offering. |

Steps We May Take if We Do Not Receive Orders for the Minimum Number of Shares

If we do not receive orders for at least 129,625,000 shares of common stock (not counting shares to be donated to the Eastern Bank Charitable Foundation), we may take several steps in order to sell the minimum number of shares of common stock in the offering range. Specifically, we may:

| (i) | increase the purchase and ownership limitations; and/or |

| (ii) | seek regulatory approval to extend the offering beyond [SUBSCRIPTION DEADLINE], 2020, so long as we resolicit subscribers who previously submitted subscriptions in the offering. |

If we extend the offering past [SUBSCRIPTION DEADLINE], 2020, all subscribers will be notified and given an opportunity to confirm, change or cancel their orders. If you do not respond to that notice, we will cancel your stock order and promptly return your funds with interest at 0.02% per annum for funds received in the subscription and community offering or cancel your deposit account withdrawal authorization. If one or more purchase limitations are increased, only those subscribers in the subscription offering who ordered the maximum amount and who indicated on their stock order form an interest in being resolicited will be given the opportunity to increase their subscriptions up to the then-applicable limit.

14

Table of Contents

Possible Change in the Offering Range

RP Financial, LC will update its appraisal before we complete the offering. If, as a result of demand for the shares or changes in market conditions or both, RP Financial, LC determines that our pro forma market value has increased, we may sell up to 201,681,250 shares in the offering without further notice to you. If our pro forma market value at that time is either below $1.4 billion or above $2.1 billion, then, after consulting with the Federal Reserve Board and the Massachusetts Commissioner of Banks, we may:

| • | terminate the offering and promptly return all funds (with interest paid on funds received in the subscription and community offerings); |

| • | set a new offering range; or |

| • | take such other actions as may be permitted by the Federal Reserve Board, the Massachusetts Commissioner of Banks and the Securities and Exchange Commission. |

If we set a new offering range, we will promptly return funds, with interest at 0.02% per annum for funds received for purchases in the subscription and community offerings, and cancel any authorization to withdraw funds from deposit accounts for the purchase of shares of common stock. We will then resolicit subscribers, allowing them time to place a new stock order.

Possible Termination of the Offering

We may terminate the offering at any time with regulatory approval. If we terminate the offering, we will promptly return your funds with interest at 0.02% per annum, and we will cancel deposit account withdrawal authorizations.

Delivery of Prospectus

To ensure that each person receives a prospectus at least 48 hours before the deadline for orders for common stock, we may not mail prospectuses any later than five days before such date or hand-deliver prospectuses later than two days before that date. Stock order forms may only be delivered if accompanied or preceded by a prospectus. We are not obligated to deliver a prospectus or stock order form by means other than U.S. mail.

We will make reasonable attempts to provide a prospectus and offering materials to holders of subscription rights. The subscription offering and all subscription rights will expire at 2:00 p.m., Eastern Time, on [EXPIRATION DATE], whether or not we have been able to locate each person entitled to subscription rights.

Our Donation of Shares of Common Stock to Eastern Bank Charitable Foundation

To further our commitment to our local community, and assuming we receive final approval from the Massachusetts Commissioner of Banks and the Federal Reserve Board, Eastern Bankshares, Inc. intends to donate to Eastern Bank Charitable Foundation a number of shares of our common stock equal to 4% of the total number of shares of common stock that will be outstanding immediately following the completion of the offering and our donation of shares to the Eastern Bank Charitable Foundation. At the minimum, midpoint, maximum and adjusted maximum of the offering range, we would donate to Eastern Bank Charitable Foundation 5,401,042, 6,354,167, 7,307,292 and 8,403,386 shares of common stock, respectively. As a result of the stock donation, we expect to record an after-tax expense of approximately $62.2 million during the quarter in which the offering is completed, assuming we sell 201,681,250 shares of common stock in the offering.

Eastern Bank Charitable Foundation is dedicated exclusively to supporting charitable and community-based organizations dedicated to social justice and otherwise serving in the communities in which we operate. The stock donation to Eastern Bank Charitable Foundation will:

| • | dilute the voting interests of purchasers of shares of our common stock in the offering; and |

| • | result in an expense, and a reduction in capital, during the quarter in which the donation is made, equal to the full amount of the donation to Eastern Bank Charitable Foundation, offset in part by a corresponding tax benefit. |

15

Table of Contents

The amount of common stock that we would offer for sale would be greater if Eastern Bankshares, Inc. was not donating shares to the Eastern Bank Charitable Foundation. For a further discussion of the financial impact of the stock donation to the Eastern Bank Charitable Foundation, including its effect on those who purchase shares in the offering, please see the sections of this prospectus titled “Risk Factors—Risks Related to the Offering—The donation to the Eastern Bank Charitable Foundation will dilute your ownership interest and adversely affect net income in 2020,” “Risk Factors—Risks Related to the Offering—Our donation to the Eastern Bank Charitable Foundation may not be tax deductible, which could reduce our profits,” “Comparison of Valuation and Pro Forma Information With and Without Stock Donation to Charitable Foundation,” and “Eastern Bank Charitable Foundation.”

Benefits to Management and Potential Dilution to Shareholders Resulting from the Offering

We expect our employee stock ownership plan, which is a tax-qualified retirement plan for the benefit of all eligible employees of Eastern Bank and Eastern Insurance Group LLC, to purchase up to 8% of the sum of the shares of common stock that are issued in the offering plus the number of shares we donate to the Eastern Bank Charitable Foundation upon completion of the offering, although the ultimate decision of whether and to what extent the employee stock ownership plan will purchase shares in the offering will be made by its trustee (initially a committee comprised of Eastern Bank executives) acting in its fiduciary capacity with respect to the employee stock ownership plan. In the event the amount purchased by the employee stock ownership plan in the offering does not equal such 8%, then if market conditions warrant, in the judgment of its trustees, the employee stock ownership plan may elect to purchase shares in the open market following the completion of the offering, subject to the approval of the Federal Reserve Board and the Massachusetts Commissioner of Banks.