Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - Vaulted Gold Bullion Trust | ex32_1.htm |

| EX-31.1 - EXHIBIT 31.1 - Vaulted Gold Bullion Trust | ex31_1.htm |

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________________

Form 10-Q

____________________________________

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended April 30, 2020

OR

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from ________ to ________

Commission File Number: 333-194144

____________________________________

VAULTED GOLD BULLION TRUST

(Exact name of registrant as specified in its charter)

____________________________________

| Delaware | 46-7176227 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

c/o Bank of Montreal

3 Times Square

New York, New York 10036

Attention: Legal Department

(Address of principal executive offices)

(212) 885-4000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Not applicable | Not applicable | Not applicable |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer o | |

| Non-accelerated filer x |

Smaller reporting company o Emerging growth company x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of April 30, 2020, there were 576 Gold Deposit Receipts outstanding.

VAULTED GOLD BULLION TRUST

FORM 10-Q

FOR THE QUARTER ENDED APRIL 30, 2020

INDEX

| Page No. | |||

| PART I. FINANCIAL INFORMATION | |||

| Item 1. | Financial Statements (Unaudited) | 4 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 17 | |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 22 | |

| Item 4. | Controls and Procedures | 22 | |

| PART II. OTHER INFORMATION | |||

| Item 1. | Legal Proceedings | 23 | |

| Item 1A. | Risk Factors | 23 | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 23 | |

| Item 3. | Defaults Upon Senior Securities | 23 | |

| Item 4. | Mine Safety Disclosures | 23 | |

| Item 5. | Changes in and Disagreements with Accounting and Financial Disclosure | 23 | |

| Item 6. | Directors, Executive Officers and Corporate Governance | 23 | |

| Item 7. | Executive Compensation | 24 | |

| Item 8. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 24 | |

| Item 9. | Certain Relationships and Related Transactions, and Director Independence | 24 | |

| Item 10. | Principal Accounting Fees and Services | 24 | |

| Item 11. | Other Information | 24 | |

| Item 12. | Exhibits | 24 | |

| Signatures | 25 | ||

| 2 |

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

The statements contained in this report that are not purely historical are forward-looking statements. The Vaulted Gold Bullion Trust’s (the “Trust”) forward-looking statements include, but are not limited to, statements regarding its expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predicts,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this report may include, for example, statements about:

| · | The gold industry; | |

| · | Sources of and demand for gold bullion; and | |

| · | The performance of the gold market. |

The forward-looking statements contained in this report are based on the Trust’s current expectations and beliefs concerning future developments and their potential effects on the Trust. There can be no assurance that future developments affecting the Trust will be those that it has anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Trust’s control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include those factors described under the heading “Risk Factors” in the Trust’s Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on January 29, 2020. Should one or more of these risks or uncertainties materialize, or should any of the Trust’s assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. The Trust undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

| 3 |

PART I. FINANCIAL INFORMATION

| Item 1. | Financial Statements (Unaudited) |

VAULTED GOLD BULLION TRUST

Financial Statements

Statements of Assets and Liabilities

| (Amounts in US$, except for Receipt data) | As of April 30, 2020 | As of October 31, 2019 | ||||||

| ASSETS | ||||||||

Investment in gold (Cost: $886,320 and $203,584,099, respectively) (see Notes 2.2, 2.5) | $ | 980,784 | $ | 231,758,577 | ||||

| Total assets | $ | 980,784 | $ | 231,758,577 | ||||

Paid In Capital | $ | 886,320 | 203,584,099 | |||||

Unrealized gain (loss) on investment in gold | $ | 94,464 | 28,174,478 | |||||

| NET ASSETS | 980,784 | 231,758,577 | ||||||

| Receipts issued, issuable and outstanding (see Note 2.3) | 576 | 153,386 | ||||||

| Net Asset Value per Receipt | $ | 1,702.75 | $ | 1,510.95 | ||||

See Notes to the Unaudited Financial Statements

| 4 |

VAULTED GOLD BULLION TRUST

Schedules of Investments

(Amounts in US$, except for Troy oz data) | As of April 30, 2020 (Unaudited)

| |||||||||||||||

| Description | Troy Oz | Cost | Fair Value | % of Net Assets (1) | ||||||||||||

| Investment in gold | ||||||||||||||||

| Gold | 576 | $ | 886,320 | $ | 980,784 | 100 | % | |||||||||

| Total investment in gold | 576 | $ | 886,320 | $ | 980,784 | 100 | % | |||||||||

| As of October 31, 2019 | ||||||||||||||||

| Description | Troy Oz | Cost | Fair Value | % of Net Assets (1) | ||||||||||||

| Investment in gold | ||||||||||||||||

| Gold | 153,386 | $ | 203,584,099 | $ | 231,758,577 | 100 | % | |||||||||

| Total investment in gold | 153,386 | $ | 203,584,099 | $ | 231,758,577 | 100 | % | |||||||||

| (1) | Calculated as investment in gold at fair value divided by net assets |

See Notes to the Unaudited Financial Statements

| 5 |

VAULTED GOLD BULLION TRUST

Statements of Operations

(Unaudited)

| (Amounts in US$) | ||||||||||||||||

| Three Months Ended April 30, 2020 | Three Months Ended April 30, 2019 | Six Months Ended April 30, 2020 | Six Months Ended April 30, 2019 | |||||||||||||

Net realized gain (loss) on redemption of Receipts | $ | 37,134,501 | $ | - | $ | 37,134,635 | $ | (434 | ) | |||||||

Net change in unrealized gain (loss) on investment in gold | (39,316,596 | ) | (6,279,471 | ) | (28,080,014 | ) | 10,324,734 | |||||||||

Total gain (loss) on investment in gold | (2,182,095 | ) | (6,279,471 | ) | 9,054,621 | 10,324,300 | ||||||||||

Increase (decrease) in net assets from operations | (2,182,095 | ) | (6,279,471 | ) | 9,054,621 | 10,324,300 | ||||||||||

Increase (decrease) in net assets from | (97.39) | (40.95) | 102.18 | 67.34 | ||||||||||||

Weighted average number of receipts | 22,405 | 153,338 | 88,618 | 153,321 | ||||||||||||

* - Based on weighted average number of Receipts issued and outstanding over the period

See Notes to the Unaudited Financial Statements

| 6 |

VAULTED GOLD BULLION TRUST

Statements of Changes in Net Assets

(Unaudited)

| Three Months Ended April 30, 2020 | Three Months Ended April 30, 2019 | Six Months Ended April 30, 2020 | Six Months Ended April 30, 2019 | |||||||||||||||||||||||||||||

| (Amounts in US$, except for Receipt data) | Receipts | Amount | Receipts | Amount | Receipts | Amount | Receipts | Amount | ||||||||||||||||||||||||

| Opening balance | 153,395 | $ | 243,008,359 | 153,336 | $ | 202,901,862 | 153,386 | $ | 231,758,577 | 153,304 | $ | 186,256,695 | ||||||||||||||||||||

| From Operations: | ||||||||||||||||||||||||||||||||

| Net change in unrealized gain (loss) on investment in gold | (39,316,596 | ) | (6,279,471 | ) | (28,080,014 | ) | 10,324,734 | |||||||||||||||||||||||||

| Net realized gain (loss) on redemption of Receipts | 37,134,501 | - | 37,134,635 | (434 | ) | |||||||||||||||||||||||||||

| From Trust Receipt activity: | ||||||||||||||||||||||||||||||||

| Issuances | 299 | 513,032 | 10 | 13,185 | 309 | 527,574 | 47 | 60,860 | ||||||||||||||||||||||||

| Redemptions | (153,118 | ) | (240,358,512 | ) | - | - | (153,119 | ) | (240,359,988 | ) | (5 | ) | (6,279 | ) | ||||||||||||||||||

| Closing balance at period end | 576 | $ | 980,784 | 153,346 | $ | 196,635,576 | 576 | $ | 980,784 | 153,346 | $ | 196,635,576 | ||||||||||||||||||||

See Notes to the Unaudited Financial Statements

| 7 |

VAULTED GOLD BULLION TRUST

April 30, 2020

(Unaudited)

Notes to the Financial Statements

| 1. | Organization |

The Vaulted Gold Bullion Trust (the “Trust”) was initially formed on December 10, 2013. The Trust is governed by the second amended and restated Depositary Trust Agreement, dated May 11, 2017 (the “Depositary Trust Agreement”). Commencement of operations occurred on August 5, 2016. The Bank of New York Mellon is the trustee (the “Trustee”) and BNY Mellon Trust of Delaware is the Delaware trustee (the “Delaware Trustee”). The Bank of Montreal (the “Initial Depositor”) sells Gold Bullion (“Gold”) to the Trust, arranges custodial services through its storage account and provides administrative services from time to time. The Vaulted Gold Bullion Trust is not a registered investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

The Trust is intended to hold Gold for the benefit of owners of Gold Deposit Receipts (“Receipts”). One Receipt represents the undivided beneficial ownership of one troy ounce of Gold. Investors (through registered broker-dealers, or banks or trust companies that become party to the distribution agreement (“Authorized Participants”)) are able to acquire, hold, transfer and surrender only whole Receipts (i.e., no fractional interests), with a minimum of one Receipt per transaction. The Trustee performs only administrative and ministerial acts. The property of the Trust consists of the Gold and all monies or other property, if any, received by the Trustee. The fiscal year end for the Trust is October 31.

| 8 |

VAULTED GOLD BULLION TRUST

April 30, 2020

(Unaudited)

| 2. | Significant Accounting Policies |

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America (“GAAP”) requires those responsible for preparing financial statements to make estimates and assumptions that affect the reported amounts and disclosures. Actual results could differ from those estimates. The following is a summary of significant accounting policies followed by the Trust.

| 2.1. | Basis of Accounting |

The Trust is an investment company for financial reporting purposes in accordance with GAAP and is not registered as an investment company under the 1940 Act nor is it required to register under such act.

| 9 |

VAULTED GOLD BULLION TRUST

April 30, 2020

(Unaudited)

| 2.2. | Valuation of Gold |

The Gold is held for the benefit of holders of the Receipts in a custodial account operated by Bank of Montreal at the Royal Canadian Mint (the “Mint”) and is valued, for financial statement purposes, at fair value. Fair value is determined by the London Bullion Market Association (“LBMA”) (PM) Gold Price, which is set using the afternoon session of the ICE Benchmark Administration (“IBA”) equilibrium auction.

The Trust follows GAAP guidance for determining fair value and GAAP requires disclosure regarding the inputs to valuation techniques used to measure fair value. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

The Trust records its investment in gold at fair value and recognizes changes in fair value of the investment in gold as changes in unrealized gains or losses on investment in gold through the Statement of Operations. Realized gains and losses on the redemption of Receipts, are calculated as the difference between the fair value and cost of gold redeemed. Realized gains and losses are recorded using the specific identification method for cost relief.

| 10 |

VAULTED GOLD BULLION TRUST

April 30, 2020

(Unaudited)

| 2.2. | Valuation of Gold (continued) |

Valuation Techniques and Significant Inputs

A valuation hierarchy exists that prioritizes inputs to valuation techniques used to measure fair value. The three levels of inputs are as follows:

| – | Level 1. Unadjusted quoted prices in active markets for identical assets or liabilities that the Trust has the ability to access. |

| – | Level 2. Observable inputs other than quoted prices in an active market that are observable for the asset or liability either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments and similar data. |

| – | Level 3. Unobservable inputs for the asset or liability to the extent that relevant observable inputs are not available, representing the Trust’s own assumptions about the assumptions that a market participant would use in valuing the asset or liability, and that would be based on the best information available. |

The Trust classifies its investment in gold as Level 1 of the fair value hierarchy. There were no re-allocations or transfers between levels during the period.

| 11 |

VAULTED GOLD BULLION TRUST

April 30, 2020

(Unaudited)

| 2.3. | Issuance and Redemption of Receipts |

The Trust issues Receipts on a continuous basis pursuant to the Depositary Trust Agreement. Authorized capital is unlimited. There were 576 Receipts issued and outstanding on April 30, 2020 (153,386 Receipts issued and outstanding on October 31, 2019).

Holders of Receipts will receive no distributions.

Subject to certain exceptions, holders of Receipts have the option to redeem their Receipts for physical gold (to be delivered directly to them by the service carrier) subject to payment of a withdrawal and delivery fee to the Initial Depositor, or exchange their Receipts for cash. Changes in the Receipts for the six months ended April 30, 2020 and April 30, 2019 are set out below:

| Six Months Ended April 30, 2020 | Six Months Ended April 30, 2019 | |||||||

(Amounts in US$ except for Number of Receipts and per Receipt data) | ||||||||

| Number of Receipts Transactions | ||||||||

| Opening balance | 153,386 | 153,304 | ||||||

| Receipts issued | 309 | 47 | ||||||

| Receipts redeemed | (153,119 | ) | (5 | ) | ||||

| Closing balance | 576 | 153,346 | ||||||

| Amount of Receipts (at cost) | ||||||||

| Opening balance | $ | 203,584,099 | $ | 203,470,539 | ||||

| Issuances | 527,574 | 60,860 | ||||||

| Redemptions | (203,225,353 | ) | (6,713 | ) | ||||

| Closing balance | $ | 886,320 | $ | 203,524,686 | ||||

| Net Asset Value per Receipt at period end | $ | 1,702.75 | $ | 1,282.30 | ||||

| 12 |

VAULTED GOLD BULLION TRUST

April 30, 2020

(Unaudited)

| 2.4. | Income Taxes |

The Trust is classified as a “grantor trust” for U.S. federal income tax purposes. As a result, the Trust itself is not subject to U.S. federal income tax.

The Trustee has evaluated whether or not there are uncertain tax positions that require financial statement recognition and has determined that no reserves for uncertain tax positions are required as of April 30, 2020 and October 31, 2019.

| 2.5. | Investment in Gold |

Changes in ounces of the Trust’s investment in gold and the respective values for the three and six months ended April 30, 2020 and April 30, 2019 are set out below:

(Amounts in US$ except for ounces data) | Three Months Ended April 30, 2020 | Three Months Ended April 30, 2019 | Six Months Ended April 30, 2020 | Six Months Ended April 30, 2019 | ||||||||||||

| Ounces of gold | ||||||||||||||||

| Opening balance | 153,395 | 153,336 | 153,386 | 153,304 | ||||||||||||

| Purchases | 299 | 10 | 309 | 47 | ||||||||||||

| Redemptions | (153,118 | ) | - | (153,119 | ) | (5 | ) | |||||||||

| Closing balance | 576 | 153,346 | 576 | 153,346 | ||||||||||||

| Investment in gold | ||||||||||||||||

| Opening balance | $ | 243,008,359 | $ | 202,901,862 | $ | 231,758,577 | $ | 186,256,695 | ||||||||

| Net change in unrealized gain (loss) on investment in gold | (39,316,596 | ) | (6,279,471 | ) | (28,080,014 | ) | 10,324,734 | |||||||||

| Net realized gain (loss) on redemption of Receipts | 37,134,501 | - | 37,134,635 | (434 | ) | |||||||||||

| Purchases | 513,032 | 13,185 | 527,574 | 60,860 | ||||||||||||

| Redemptions | (240,358,512 | ) | - | (240,359,988 | ) | (6,279 | ) | |||||||||

| Closing balance | $ | 980,784 | $ | 196,635,576 | $ | 980,784 | $ | 196,635,576 | ||||||||

| 13 |

VAULTED GOLD BULLION TRUST

April 30, 2020

(Unaudited)

| 2.6. | Fees and Expenses |

The expenses of the Trust are borne by the Initial Depositor.

The expenses of the Trust are expected to include, but are not limited to, the following:

• any expenses or liabilities of the Trust;

• any taxes and other governmental charges that may fall on the Trust or its property; and

• fees and expenses of the Trustee and any indemnification of the Trustee.

Additionally, the Trustee’s and Mint’s fees are paid by the Initial Depositor and are not separate expenses of the Trust.

| 2.7. | Related Party Transactions |

On May 11, 2017, the Trust entered into the Depositary Trust Agreement with The Bank of New York Mellon, BNY Trust of Delaware, Bank of Montreal and BMO Capital Markets Corp. On July 11, 2018, the Trust entered into the Second Amended and Restated Distribution Agreement with Bank of Montreal and BMO Capital Markets Corp (the “Distribution Agreement”).

Bank of Montreal acts as the Initial Depositor of the Trust and holds gold that it transfers to the Trust from time to time in connection with the sale by the Trust of Receipts. Pursuant to the Depositary Trust Agreement and the Distribution Agreement, the offering price for each Receipt consists of the spot price at the time of sale to an investor for one troy ounce of gold, plus: (1) in the case of a Class A Gold Deposit Receipt, a deposit fee of 2.00%, payable to Bank of Montreal, plus a sales fee of 2.00% to any participating broker-dealer that sells Gold Deposit Receipts to an investor; (2) in the case of a Class F Gold Deposit Receipt, which is sold only through fee-based programs, a deposit fee of 2.00%, payable to Bank of Montreal, plus a sales fee of 0.25%; (3) in the case of a Class F-1 Gold Deposit Receipt, which is sold to trust or fiduciary accounts, a deposit fee of 2.00%, payable to Bank of Montreal, and no sales fee; (4) in the case of a Class F-2 Gold Deposit Receipt, which is sold solely to an Institutional Account, a deposit fee of 1.50%, payable to Bank of Montreal, and no sales fee; (5) in the case of a Class F-3 Gold Deposit Receipt, which is sold solely to an Institutional Account, a deposit fee of 1.00%, payable to Bank of Montreal, and no sales fee; and (6) in the case of a Class S Gold Deposit Receipt, which is sold solely to an Institutional Account, neither a deposit fee nor a sales fee. The deposit fee and the sales fee are not expenses of the Trust and have no impact on the financial highlights of the Trust. The Trust uses the proceeds of the issuance of Receipts, net of these fees, to purchase gold from Bank of Montreal in an amount that corresponds to the amount of Receipts.

Bank of Montreal charges holders of Receipts a withdrawal and delivery fee if physical delivery of the gold is requested (the “Withdrawal and Delivery Fee”). Bank of Montreal additionally reserves the right to charge the holders of Receipts a custody fee, not to exceed 0.50% per annum of the daily average closing price of gold represented by the Receipts, as calculated by the Initial Depositor, acting in good faith (the “Custody Fee”). Bank of Montreal did not charge any Custody Fee during the three or six months ended April 30, 2020 or for the fiscal year ended October 31, 2019. None of the Deposit Fee, Withdrawal and Delivery Fee or Custody Fee is paid by the Trust to Bank of Montreal.

Pursuant to the terms of the Distribution Agreement, BMO Capital Markets Corp., one of Bank of Montreal’s affiliates, acts as the Underwriter of the continuous offerings of Receipts and as the calculation agent responsible for calculating the spot price at which Receipts are offered to the public.

| 14 |

Further Bank of Montreal or its affiliates may acquire Receipts of the Trust on behalf of its private clients.

BMO Financial Group (“BMO”) held no Receipts as at April 30, 2020, after redeeming 153,118 Receipts in February 2020. BMO held 153,118 Receipts as at October 31, 2019 with a total market value of $231,353,642 (Cost: $203,243,629).

| 2.8. | New Accounting Pronouncement |

In August 2018, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework --Changes to the Disclosure Requirements for Fair Value Measurement (“ASU 2018-13”). The update provides guidance that eliminates, adds and modifies certain disclosure requirements for fair value measurements. ASU 2018-13 is effective for annual periods beginning after December 15, 2019. Management is currently assessing the potential impact of these changes to future financial statements.

| 3. | Concentration of Risk |

The Trust’s sole business activity is the investment in gold, and substantially all the Trust’s assets are holdings of gold which creates a concentration of risk associated with fluctuations in the price of gold. Several factors could affect the price of gold, including: (i) global gold supply and demand, which is influenced by factors such as forward selling by gold producers, purchases made by gold producers to unwind gold hedge positions, central bank purchases and sales, and production and cost levels in major gold-producing countries; (ii) investors’ expectations with respect to the rate of inflation; (iii) currency exchange rates; (iv) interest rates; (v) investment and trading activities of hedge funds and commodity funds; and (vi) global or regional political, economic or financial events and situations. In addition, there is no assurance that gold will maintain its long-term value in terms of purchasing power in the future. In the event that the price of gold declines, the value of an investment in the Receipts will decline proportionately. Subject to certain restrictions, Receipts may be redeemed after notice at the option of the holder. Each of these events could have a material effect on the Trust’s financial position and results of operations.

| 4. | Indemnification |

Under the Trust’s organizational documents, the Trustee (and its directors, employees and agents) and the Initial Depositor (and its members, managers, directors, officers, employees and affiliates) are indemnified by the Trust against any liability, cost or expense it incurs without gross negligence, bad faith or willful misconduct on its part and without reckless disregard on its part of its obligations and duties under the Trust’s organizational documents. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred.

| 15 |

VAULTED GOLD BULLION TRUST

April 30, 2020

(Unaudited)

| 5. | Financial Highlights |

The Trust is presenting the following financial highlights related to investment performance and operations of a Receipt outstanding for the three and six months ended April 30, 2020 and April 30, 2019.

| Net Asset Value | Three Months 2020 | Three Months 2019 | Six Months 2020 | Six Months 2019 | ||||||||||||

| Net asset value per Receipt, beginning of period | $ | 1,584.20 | $ | 1,323.25 | $ | 1,510.95 | $ | 1,214.95 | ||||||||

| Change in unrealized investment in gold | $ | 118.55 | $ | (40.95 | ) | $ | 191.80 | $ | 67.35 | |||||||

| Net Asset Value per Receipt, end of period | $ | 1,702.75 | $ | 1,282.30 | $ | 1,702.75 | $ | 1,282.30 | ||||||||

| Total Return* | 7.48 | % | (3.09 | )% | 12.69 | % | 5.54 | % | ||||||||

| Portfolio Turnover | 0.77 | % | 0.00 | % | 0.35 | % | 0.00 | % | ||||||||

* Not annualized

| 6. | Subsequent Events |

The Trust evaluated subsequent events through the date the financial statements were issued. The Trust concluded that no subsequent events have occurred that would require recognition or disclosure in the financial statements.

| 16 |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Overview

The Trust holds Gold Bullion for the benefit of owners of Gold Deposit Receipts. One Gold Deposit Receipt represents the undivided beneficial ownership of one troy ounce of Gold Bullion. The Trustee performs only administrative and ministerial acts. The property of the Trust consists of the Gold Bullion and all monies or other property, if any, received by the Trustee. The Initial Depositor sells Gold Bullion to the Trust and arranges custodial services through its gold storage account. As of April 30, 2020, there were 576 Gold Deposit Receipts outstanding.

The Trust is not managed like a corporation or an active investment vehicle. It does not have any officers, directors, or employees and is administered by the Trustee pursuant to the Depositary Trust Agreement. The expenses of the Trust are borne by the Initial Depositor.

The fiscal year end for the Trust is October 31.

Gold Industry

The participants in the gold industry may be classified in the following sectors: (1) mining and producer; (2) banking; (3) official; (4) investment; and (5) manufacturing. The following is a brief description of each of the sectors.

Mining and Producer Sector. This group includes mining companies that specialize in gold and silver production; mining companies that produce gold as a byproduct of other production (such as a copper or silver producer); scrap merchants; and recyclers.

Banking Sector. Bullion banks provide a variety of services to the gold industry and its participants, thereby facilitating interactions between other parties. Services provided by the bullion banking community include traditional banking products as well as mine financing, physical gold purchases and sales, hedging and risk management, inventory management for industrial users and consumers, and gold deposit and loan instruments.

The Official Sector. The official sector encompasses the activities of the various central banking operations of gold-holding countries. In September 1999, a group of 15 central banks acting to clarify their intentions with respect to their gold holdings signed the Central Bank Gold Agreement commonly called the “Washington Agreement on Gold.” The signatories included the European Central Bank (the “ECB”) and the central banks of Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Sweden, Switzerland, and England. The original agreement limited incremental sales by the 15 signatories to 400 tonnes per annum over the ensuing five-year period. The original Washington Agreement on Gold expired in September 2004, and was renewed by almost all of the original signatories for a second five-year period (England did not renew in 2004). The second Washington Accord Agreement expired in September 2009 and was renewed again by all signatories of the second agreement for a third agreement to last another five-year period. In addition, the central banks of Cyprus, Greece, Malta, Slovakia and Slovenia signed in 2009. The annum limit on gold sales under the third agreement was 400 tonnes, with total sales not to exceed 2,000 tonnes in the five-year period. In May 2014, before the third agreement was set to expire in September 2014, a fourth agreement was reached between the ECB and the central banks of Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia, Spain, Sweden and Switzerland, which will expire after a five-year period. The signatories agreed to, among other things, continue to coordinate their gold transactions to avoid disturbances to the gold market and have acknowledged that they each do not have plans to sell significant amounts of gold. On July 26, 2019, the ECB announced that it and the 21 other central bank signatories have decided not to renew the fourth agreement upon its expiry in September 2019, citing that they no longer see the need for a formal agreement as the market has developed and matured. The signatories confirmed that gold remains an important element of global monetary reserves and none of them currently has plans to sell significant amounts of gold.

| 17 |

The Investment Sector. This sector includes the investment and trading activities of both professional and private investors and speculators. These participants range from large hedge and mutual funds to day-traders on futures exchanges and retail-level coin collectors.

The Manufacturing Sector. The fabrication and manufacturing sector represents all the commercial and industrial users of gold for whom gold is a daily part of their business. The jewelry industry is a large user of gold. Other industrial users of gold include the electronics and dental industries.

World Gold Supply and Demand (from calendar year 2009-2019)

The following table sets forth a summary of the world gold supply and demand from calendar year 2009-2019:

| WORLD GOLD SUPPLY AND DEMAND (tonnes)(1) |

2009† | 2010† | 2011† | 2012† | 2013† | 2014† | 2015† | 2016† | 2017† | 2018† | Q1 2019* |

Q2 2019* |

Q3 2019* |

Q4 2019* |

| Supply | ||||||||||||||

| Mine Production | 2,651 | 2,771 | 2,868 | 2,882 | 3,076 | 3,180 | 3,222 | 3,252 | 3,259 | 3,332 | 831 | 838 | 884 | 868 |

| Scrap | 1,765 | 1,743 | 1,698 | 1,700 | 1,303 | 1,159 | 1,180 | 1,306 | 1,210 | 1,178 | 306 | 308 | 331 | 301 |

| Net Hedging Supply |

-234 | -106 | 18 | -40 | -39 | 108 | 21 | 32 | -41 | 8 | -25 | 70 | -15 | 15 |

| Total Supply | 4,182 | 4,407 | 4,584 | 4,543 | 4,340 | 4,446 | 4,422 | 4,590 | 4,428 | 4,518 | 1,112 | 1,216 | 1,200 | 1,185 |

| Demand | ||||||||||||||

| Jewelry | 1,879 | 2,096 | 2,109 | 2,075 | 2,737 | 2,569 | 2,474 | 1,962 | 2,222 | 2,129 | 455 | 469 | 332 | 471 |

| Industrial Fabrication |

426 | 480 | 470 | 432 | 428 | 411 | 376 | 366 | 380 | 391 | 92 | 92 | 95 | 95 |

| …of which Electronics |

295 | 346 | 342 | 310 | 306 | 297 | 267 | 264 | 277 | 288 | 67 | 68 | 70 | 70 |

| …of which Dental & Medical |

53 | 48 | 43 | 39 | 36 | 34 | 32 | 30 | 29 | 29 | 7 | 7 | 7 | 7 |

| …of which Other Industrial |

79 | 86 | 85 | 84 | 85 | 80 | 76 | 71 | 73 | 74 | 18 | 18 | 18 | 18 |

| Net Official Sector |

-34 | 77 | 457 | 544 | 409 | 466 | 443 | 253 | 366 | 536 | 145 | 210 | 136 | 132 |

| Retail Investment | 866 | 1,263 | 1,617 | 1,407 | 1,871 | 1,165 | 1,172 | 1,051 | 1,031 | 1,097 | 273 | 244 | 188 | 297 |

| …of which Bars | 562 | 946 | 1,248 | 1,057 | 1,444 | 886 | 875 | 785 | 771 | 800 | 194 | 173 | 133 | 217 |

| …of which Coins | 304 | 317 | 369 | 350 | 426 | 279 | 296 | 266 | 261 | 297 | 79 | 71 | 55 | 80 |

| Physical Demand |

3,138 | 3,915 | 4,652 | 4,458 | 5,445 | 4,611 | 4,464 | 3,631 | 3,999 | 4,154 | 1,014 | 1,049 | 814 | 1,033 |

| Physical Surplus/Deficit |

1,044 | 492 | -69 | 85 | -1,105 | -164 | -42 | 959 | 429 | 365 | 98 | 167 | 386 | 151 |

| ETF Inventory Build |

623 | 384 | 189 | 279 | -879 | -155 | -117 | 539 | 177 | 59 | 32 | 92 | 231 | 35 |

| Exchange Inventory Build |

39 | 54 | -6 | -10 | -98 | 1 | -48 | 86 | 0 | -21 | -11 | -13 | 14 | 17 |

| Net Balance | 382 | 54 | -251 | -185 | -129 | -10 | 124 | 334 | 252 | 327 | 78 | 87 | 140 | 99 |

| Gold Price (London PM, US$/oz) |

972.35 | 1,224.52 | 1,571.69 | 1,668.98 | 1,411.23 | 1,266.40 | 1,160.06 | 1,250.80 | 1,257.15 | 1,268.49 | 1,303.8 | 1,309.4 | 1,472.5 | 1,479.9 |

Note: Totals may not add due to independent rounding. Net producer hedging is the change in the physical market impact of mining companies’ gold loans, forwards and options positions. Implied net investment is the residual from combining all other Thomson Reuters GFMS data on the gold supply/demand as shown in the Summary Table. As such, it captures the net physical impact of all transactions not covered by the other supply/demand variables.

(1) “Tonne” refers to one metric ton. This is equal to 1,000 kilograms or 32,150.7465 troy ounces.

† Source: Gold Survey 2019, GFMS, Refinitiv

* Source: Gold Survey H2 2019 Update and Outlook, GFMS, Refinitiv

| 18 |

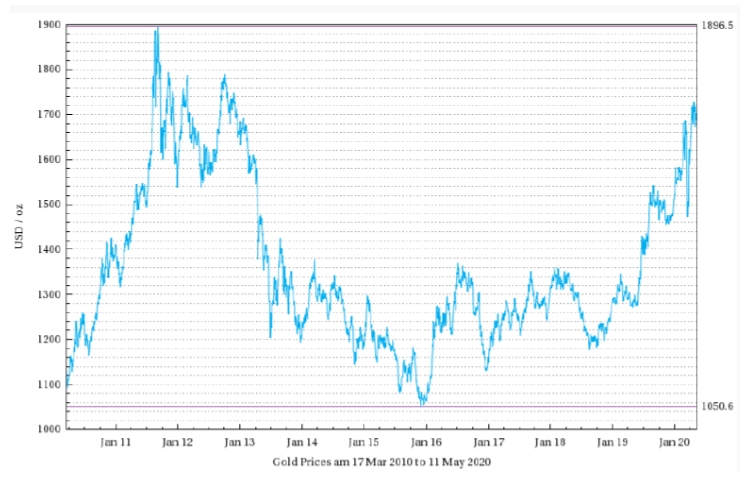

Historic Movements in the Price of Gold

As movements in the price of gold are expected to directly affect the price of the Gold Deposit Receipts, investors should understand what the recent movements in the price of gold have been. Investors, however, should also be aware that past movements in the gold price are not indicators of future movements.

The following chart provides historical background on the price of gold. The chart illustrates movements in the price of gold in U.S. dollars per ounce over the period from April 2010 to April 2020, and is based on the LBMA (PM) Gold Price, an offering of ICE Benchmark Administration.

Source: LBMA.org.uk (accessed June 2020)

The price of gold followed an upward trend in 2010, reaching a new pre-inflation adjusted record high of $1,421.00 per ounce on November 9, 2010 and closing at $1,405.50 per ounce on December 30, 2010. In August 2011, the price of gold experienced a notable increase partially due to the first U.S. downgrade by Standard & Poor’s, reaching a high of $1,895.00 per ounce on September 5, 2011. By December 29, 2011, the price of gold had fallen to $1,531.00 per ounce. The annual average price of gold in 2012 was 6.2 percent higher than 2011, reaching a high of $1,791.75 on October 4, 2012. In particular, uncertainty over U.S. monetary policy became an increasingly significant driver of market appetite towards the end of 2012, and on December 28, 2012, the price of gold had fallen slightly to $1,657.50 per ounce.

| 19 |

In 2013, the twelve-year bull run of gold ended. 2013 opened near the annual high, and the price declined approximately 29 percent over the year to $1,204.50 per ounce on December 30, 2013. For 2013, the price of gold was impacted, in part, by improving sentiment towards the U.S. economy, which contributed to a strengthening of the U.S. dollar and equities, luring investors away from gold in the process. During 2014, the underlying driver behind investor sentiment of gold was global monetary policy. On one end, the improving economic conditions in the United States (along with the announcement of the Federal Reserve Board’s tapering measures at the end of 2013) diminished demand for gold for U.S. investors, while loosening of monetary policy in other advanced and emerging markets enhanced demand for gold globally, causing gold prices to fluctuate between a low of $1,132.00 and a high of $1,392.00 per ounce. Gold prices deteriorated throughout 2015, in part as a result of the Federal Reserve Board’s announcement that it would raise interest rates as well as a significant rally of the U.S. dollar index, falling to $1,060.00 per ounce on December 30, 2015. However, the price of gold rebounded during the first half of 2016. In July 2016, gold prices experienced a rapid increase following the United Kingdom’s referendum held on June 23, 2016 to leave the European Union (i.e., “Brexit”), reaching a 28-month high of $1,366.25 per ounce on July 6, 2016. The initial market volatility and negative sentiment in connection with Brexit has somewhat subsided and gold prices have receded from the high prices displayed during July 2016, leveling off at prices similarly exhibited during the beginning of 2016. Gold prices rallied robustly in the first seven months of 2016 before leveling off for much of the third calendar quarter. Gold hit a near eleven-month low price of $1,125.70 per ounce in late December and ended the year 8 percent higher than it started. This lower price followed a few days after the Federal Reserve raised interest rates on December 15, 2016.

In the first half of 2017, physical demand was up 17 percent compared to the same period a year earlier. In September 2017, gold prices rose to their highest level for thirteen months, but then slipped to a near five-month low by mid-December. Gold prices near $1,300.00 per ounce in the later half of 2017 indicated that physical demand had slipped compared to prior calendar quarters. The final weeks of 2017 saw gold prices recover the bulk of previous losses as the dollar weakened against other major currencies after the Federal Reserve reiterated that a gradual path of rate increases remained appropriate even in light of the new tax reform. Gold closed at $1,291.00 per ounce on December 28, 2017.

Gold started 2018 strongly, extending the rally that followed the Federal Reserve’s interest rate hike in December 2017. This rally hit a barrier just below $1,360.00 in late January. While gold started off to a positive year in 2018, a recovery in the U.S. dollar weakened prices and uncertainty on the U.S-China trade front weakened the yuan, further pulling gold down. In mid-August 2018, the price of gold was at $1,178.40, which was both the lowest price point for the year-to-date and the lowest since the start of 2017. By the end of August, gold prices had gone down approximately 7.7 percent in 2018. Investment sector demand grew in the fourth calendar quarter of 2018, as a short covering rally in net managed positions on COMEX pushed up net short positions into net long positions for the first time since July 2018. Official sector purchases rose to 196 tonnes in the last calendar quarter of 2018, their highest quarterly level in 50 years. A January 2019 study by the World Gold Council, an industry trade group, reported that the amount of gold purchased by central banks reached 651 tonnes in 2018, the highest level since 1967. Gold closed at $1,279.00 per ounce on December 28, 2018.

On January 30, 2019, the Federal Reserve announced it would keep its target range for its benchmark interest rate at 2.25% to 2.5% and declared it would be patient in deciding when to raise interest rates again. Gold closed at $1,323.25 per ounce on January 31, 2019. By the end of the first calendar quarter in 2019, gold demand grew to 1.053 tonnes, up approximately 7% from the first calendar quarter of 2018. While demand grew, supply remained relatively unchanged throughout the first calendar quarter of 2019, flatlining at approximately 1,150 tonnes. Gold reached a high of $1,343.75 in the first calendar quarter of 2019, but fell to around $1,295.40 by the end of March.

In the second calendar quarter of 2019, gold demand was 1,123 tonnes, up 8% from the prior year period, while gold supply grew 6% to 1,186.7 tonnes. For the first half of 2019, gold demand grew to a three-year high of 2,181.7 tonnes, largely due to central bank purchases and ETF inflows, while gold supply reached 2,323.9 tonnes, the highest since 2016. The price of gold broke through the $1,430 per ounce level in late June, trading at a then six-year high, as the Federal Reserve re-opened the door for interest rate cuts amid rising global economic and political uncertainties. Gold closed at $1,409 per ounce on June 28, 2019. On July 31, 2019, the Federal Reserve lowered the target range for its benchmark interest rate to 2% to 2.25% (from 2.25% to 2.5%) and declared it would continue to monitor the implications of incoming information for the economic outlook. During the third calendar quarter, gold demand grew modestly to 1,107.9 tonnes mainly due to the largest ETF inflows since 2016. The price of gold rose by 5% during the third calendar quarter of 2019. On September 4, 2019, the price of gold broke through the $1,546.10 per ounce level, its highest mark for 2019. The primary factors behind this price momentum continued to be ongoing geopolitical tensions, concerns of a slowdown in economic growth, lower interest rates and the level of negative yielding debt. In the fourth calendar quarter of 2019, gold price averaged $1,481 per ounce, the highest average price since the first calendar quarter of 2013. Global demand in the second half of 2019 was down 10% compared to the same period of 2018. Gold closed at $1,514.75 per ounce on December 30, 2019 and at $1,584.20 per ounce on January 31, 2020.

| 20 |

In the first calendar quarter of 2020, gold demand grew marginally to 1,083.8 tonnes. The global COVID-19 pandemic, which impacted the world in first calendar quarter of 2020, fueled safe-haven investment demand for gold, offsetting market weakness in consumer-focused sectors of the economy. These investment inflows helped push the US dollar gold price to an eight-year high. Consequently, global gold demand in value terms reached US$55 billion – the highest since the second quarter of 2013. Total supply in the first calendar quarter of 2020 fell 4% as COVID-19 lockdowns impacted mine production and gold recycling. Central banks continued to buy significant quantities of gold in the same period. Amid heightened volatility and uncertainty, global gold reserves grew by 145 tonnes in in the first calendar quarter of 2020. Gold closed at $1,702.75 per ounce on April 30, 2020.

As of June 12, 2020, the price of gold was $1,733.50 per ounce.

Results of Operations for the Three Months and Six Months Ended April 30, 2020

The Trust’s Net Asset Value decreased from $231,758,577 at October 31, 2019 to $980,784 at April 30, 2020, a 99.58% decrease for the period.

Net Asset Value per Receipt increased 12.69% from $1,510.95 at October 31, 2019 to $1,702.75 at April 30, 2020.

Net Asset Value per Receipt increased 7.48% from $1,584.20 at January 31, 2020 to $1,702.75 at April 30, 2020.

For the six months ended April 30, 2020, the Trust issued 309 Receipts (cost — $527,574) and redeemed 153,119 Receipts (cost — $203,225,353), resulting in a decrease in the number of Receipts issued and outstanding from 153,386 Receipts at October 31, 2019 to 576 Receipts at April 30, 2020.

For the three months ended April 30, 2020, the Trust issued 299 Receipts (cost — $513,032) and redeemed 153,118 Receipts (cost — $203,224,011), resulting in a decrease in the number of Receipts issued and outstanding from 153,395 Receipts at January 31, 2020 to 576 Receipts at April 30, 2020.

The increase in net assets from operations for the six months ended April 30, 2020 was $9,054,621, resulting from a change in unrealized loss on investment in gold of $28,080,014 and a net realized gain of $37,134,635 on the redemption of receipts.

The decrease in net assets from operations for the three months ended April 30, 2020 was $2,182,095, resulting from a change in unrealized loss on investment in gold of $39,316,596 and a net realized gain of $37,134,501 on the redemption of receipts.

Liquidity and Capital Resources

The Trust is not aware of any trends, demands, commitments, conditions, events or uncertainties that are reasonably likely to result in material changes to its liquidity needs. In exchange for the Initial Depositor’s fee, the Initial Depositor has agreed to assume the expenses incurred by the Trust.

Off-Balance Sheet Arrangements

The Trust has no off-balance sheet arrangements.

Critical Accounting Policies

The Trust prepares its financial statements in accordance with GAAP.

| 21 |

The Trust has adopted the provisions of Financial Accounting Standards Board Accounting Standards Codification Topic 946, Financial Services—Investment Companies, and follows specialized accounting. As a result of the adoption of this provision, the Trust records its investment in gold at fair value and expects that there will be fluctuations in the value of investments based on changes in the price of gold.

Item 3. Quantitative and Qualitative Disclosures About Market Risk

The Trust does not engage in transactions in foreign currencies which could expose the Trust or holders of Gold Deposit Receipts to any foreign currency related market risk. The Trust does not invest in any derivative financial instruments or long-term debt instruments. The Trust’s sole business activity is the investment in gold, and substantially all the Trust’s assets are holdings of gold which creates a concentration of risk associated with fluctuations in the price of gold.

Item 4. Controls and Procedures

The Trust maintains disclosure controls and procedures that are designed to ensure that information required to be disclosed in its reports under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), is recorded, processed, summarized and reported within the time periods specified in the rules and forms of the SEC, and that such information is accumulated and communicated to an executive or senior officer of the Initial Depositor familiar with and responsible for supervising the Trust and its operations, as appropriate, to allow timely decisions regarding required disclosure.

Under the supervision and with the participation of an executive or senior officer of the Initial Depositor, the Initial Depositor conducted an evaluation of the Trust’s disclosure controls and procedures, as defined under Exchange Act Rules 13a-15(e) and 15d-15(e). Based on this evaluation, the designated officer of the Initial Depositor concluded that, as of April 30, 2020, the Trust’s disclosure controls and procedures were effective.

There have been no changes in the Trust’s or Initial Depositor’s internal control over financial reporting that occurred during the Trust’s most recent fiscal quarter ended April 30, 2020 that have materially affected, or are reasonably likely to materially affect, the Trust’s or Initial Depositor’s internal control over financial reporting.

| 22 |

PART II. OTHER INFORMATION

| Item 1. | Legal Proceedings |

None.

Item 1A. Risk Factors

There have been no material changes to the risk factors previously disclosed in the Trust’s Form 10-K filed with the SEC on January 29, 2020, except for the following:

The Trust, the Initial Depositor, BMO Financial Group (“BMO”) and their respective service providers are vulnerable to the effects of public health crises, including the ongoing novel coronavirus pandemic (the “COVID-19 pandemic”).

Pandemics and other public health crises may cause a curtailment of business activities which may potentially impact the ability of the Initial Depositor, BMO and their respective service providers to operate. The World Health Organization declared COVID-19 a global pandemic on March 11, 2020. The COVID-19 pandemic has negatively impacted the global economy and economic outlook, including with respect to the jurisdictions in which the Trust, the Initial Depositor and BMO operate, disrupted global supply chains, lowered equity market valuations, lowered interest rates, created significant volatility and disruption in financial markets, increased unemployment levels and increased credit and market risk. In addition, governments and regulatory bodies have implemented several measures, including temporary closures of a number of businesses and the institution of social distancing and sheltering in place requirements in many of these jurisdictions. Governments, monetary authorities and regulators have also taken actions to support individuals, the economy, capital markets, and the financial system, including taking fiscal and monetary measures to support incomes, businesses, liquidity, and regulatory actions in respect of financial institutions. The COVID-19 pandemic or a similar public health threat could adversely impact the Trust by causing operating delays and disruptions, market disruption and shutdowns, including as a result of government regulation and prevention measures. A prolonged outbreak could also result in an increase of the costs of the Trust, affect liquidity in the market for gold as well as the correlation between the price of the Receipts and the net asset value of the Trust. The extent to which the COVID-19 pandemic impacts the Trust’s business, results of operations and financial condition, including the potential from loss from higher credit, counterparty or mark-to-market losses, will depend on future developments, which are highly uncertain and cannot be predicted, including the scope and duration of the pandemic and actions taken by governmental and regulatory authorities, which could vary by country, and other third parties in response to the pandemic.

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds |

Not applicable.

| Item 3. | Defaults Upon Senior Securities |

None.

| Item 4. | Mine Safety Disclosures |

Not applicable.

| Item 5. | Changes in and Disagreements with Accounting and Financial Disclosure |

There have been no changes in auditors and no disagreements with auditors during the Trust’s fiscal quarter ended April 30, 2020.

| Item 6. | Directors, Executive Officers and Corporate Governance |

Not applicable.

| 23 |

| Item 7. | Executive Compensation |

Not applicable.

Item 8. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

Not applicable.

| Item 9. | Certain Relationships and Related Transactions, and Director Independence |

On May 11, 2017, the Trust entered into the Second Amended and Restated Depositary Trust Agreement with The Bank of New York Mellon, BNY Trust of Delaware, Bank of Montreal and BMO Capital Markets Corp. On July 11, 2018, the Trust entered into the Second Amended and Restated Distribution Agreement with Bank of Montreal and BMO Capital Markets Corp.

| Item 10. | Principal Accounting Fees and Services |

Audit Fees. Bank of Montreal, as the Initial Depositor, was billed $20,000 for professional services rendered by KPMG LLP.

All Other Fees. There were no other fees billed for products or services provided by KPMG LLP, other than those reported in this Item 10.

| Item 11. | Other Information |

Not applicable.

Item 12. Exhibits

* Previously filed.

| 24 |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this annual report to be signed on its behalf by the undersigned in the capacities thereunto duly authorized.

| BANK OF MONTREAL Initial Depositor of the Vaulted Gold Bullion Trust (Registrant) | |

| Date: June 15, 2020 | /s/ Rob Yeung |

| *Head, Global FICC | |

| BMO Capital Markets | |

| Date: June15, 2020 | /s/ Neil Puddicombe |

| *Assistant Corporate Secretary |

__________

* The Registrant is a trust and the persons are signing in their capacities as officers of Bank of Montreal, the Initial Depositor of the Registrant.

25