Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SANDY SPRING BANCORP INC | tm2016738d1_8k.htm |

Exhibit 99.1

1 st Quarter Supplemental Information April 23, 2020

Our Commitment We are laser focused on doing all that we can do to ensure everyone’s safety and to seamlessly continue to serve you. Sandy Spring Bank has more than 150 years of experience and we have weathered challenging times before. We are committed to using our experience to best serve you and to continue to earn and keep your trust . - March 13, 2020 message to c lients 2

Protecting Our Employees, Clients and Community ▪ Suspended all business - related travel, limited in - person meetings with outside parties, asked employees to postpone non - essential personal travel. ▪ Implemented enhanced cleaning and disinfecting procedures. ▪ Closed branch lobbies to the public, established a process for clients to schedule appointments for critical needs, made a wider range of transactions possible in drive - thru facilities. ▪ Closed the majority of branches that do not have drive - thru facilities. ▪ Transitioned approximately 85% of non - branch personnel to teleworking. ▪ D eveloped comprehensive guidance for responding to any COVID - 19 diagnoses or exposures in our operations. In response to the emerging public health crisis, we took the following steps to safeguard our community and help stop the spread of COVID - 19. 3

Taking Care of Our Employees Enhanced P ersonal Leave : Two weeks of paid time off is available to employees who are unable to work for reasons related to COVID - 19. Appreciation Bonus : Branch personnel and support staff whose responsibilities do not permit them to work remotely were awarded a bonus of up to $1,200. Redeploying Employees : Nearly two dozen retail employees transitioned to roles within mortgage, consumer lending and the call center. Those employees who cannot be redeployed will continue to be paid. Open Lines of Communication : Executive management communicates several times a week with employees, providing regular updates regarding safety measures, and the resources and benefits available during this time. 4

Advocating for Our Clients ▪ Launched a webpage with the latest information, resources, federal relief program details, and all client communications to date. ▪ We are working with clients on a case - by - case basis to provide fee waivers, structure loan payment deferrals or other accommodations . ▪ Our bankers are working to make clients aware of resources available inside the bank, programs in MD , VA and DC, and loans from the Small Business Administration (SBA)’s Paycheck Protection Program. ▪ Established a moratorium on foreclosures and repossessions . ▪ We are waiving: ▪ ATM fees for all Sandy Spring Bank cardholders, including refunding ATM fees charged by other banks or networks. ▪ C ertain penalties for early CD withdrawals less than $ 10,000. ▪ Fees for remote check deposits by our business clients . We are helping our individual and business clients deal with the enormous financial impact of the corona virus. . 5

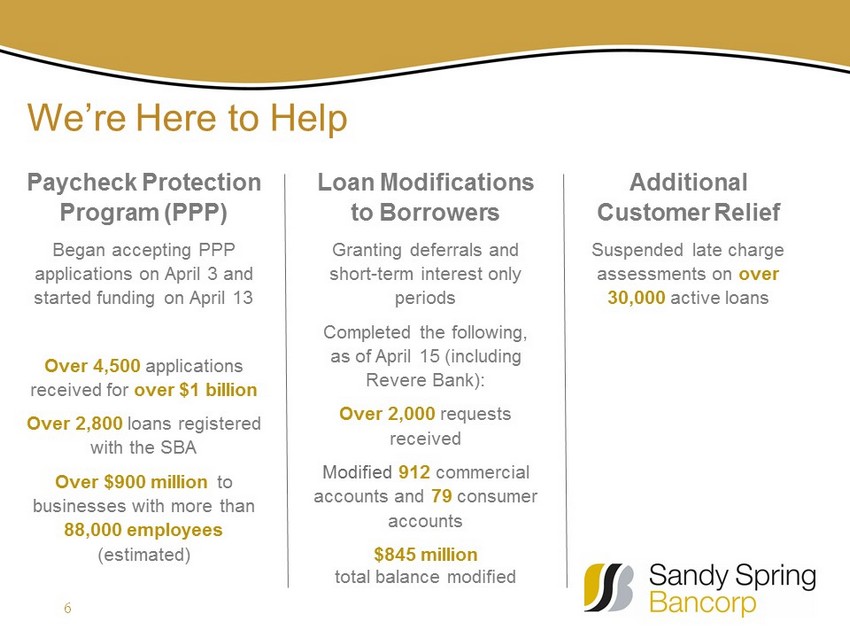

We’re Here to Help Paycheck Protection Program (PPP) Began accepting PPP applications on April 3 and started funding on April 13 Over 4,500 applications received for over $1 billion Over 2,800 loans registered with the SBA Over $900 million to businesses with more than 88,000 employees (estimated) Loan Modifications to Borrowers Granting deferrals and short - term interest only periods Completed the following, as of April 15 (including Revere Bank): Over 2,000 requests received Modified 912 commercial accounts and 79 consumer accounts $845 million total balance modified Additional Customer Relief Suspended late charge assessments on over 30,000 active loans 6

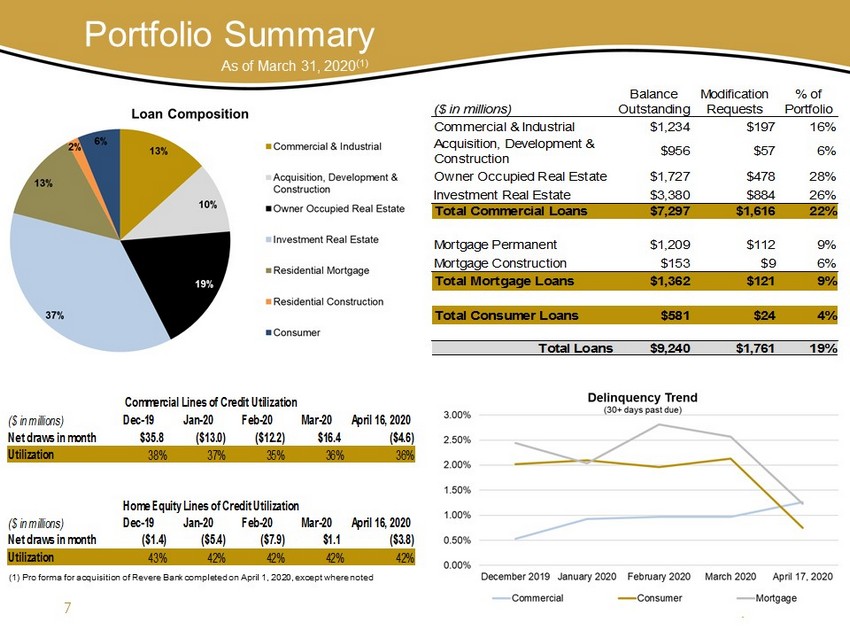

Portfolio Summary As of March 31, 2020 (1) (1) Pro forma for acquisition of Revere Bank completed on April 1, 2020, except where noted Balance Modification % of ($ in millions) Outstanding Requests Portfolio Commercial & Industrial $1,234 $197 16% Acquisition, Development & Construction $956 $57 6% Owner Occupied Real Estate $1,727 $478 28% Investment Real Estate $3,380 $884 26% Total Commercial Loans $7,297 $1,616 22% Mortgage Permanent $1,209 $112 9% Mortgage Construction $153 $9 6% Total Mortgage Loans $1,362 $121 9% Total Consumer Loans $581 $24 4% Total Loans $9,240 $1,761 19% As of March 31, 2020 (1) 7 ($ in millions) Dec-19 Jan-20 Feb-20 Mar-20 April 16, 2020 Net draws in month $35.8 ($13.0) ($12.2) $16.4 ($4.6) Utilization 38% 37% 35% 36% 36% ($ in millions) Dec-19 Jan-20 Feb-20 Mar-20 April 16, 2020 Net draws in month ($1.4) ($5.4) ($7.9) $1.1 ($3.8) Utilization 43% 42% 42% 42% 42% Home Equity Lines of Credit Utilization Commercial Lines of Credit Utilization

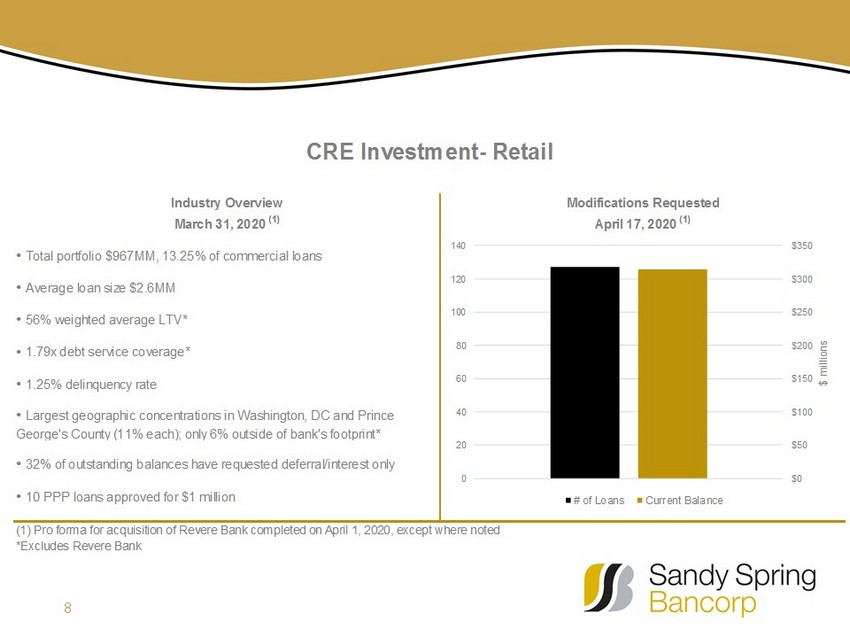

8 • Total portfolio $967MM, 13.25% of commercial loans • Average loan size $2.6MM • 56% weighted average LTV* • 1.79x debt service coverage* • 1.25% delinquency rate • 32% of outstanding balances have requested deferral/interest only • 10 PPP loans approved for $1 million (1) Pro forma for acquisition of Revere Bank completed on April 1, 2020, except where noted *Excludes Revere Bank CRE Investment- Retail Industry Overview • Largest geographic concentrations in Washington, DC and Prince George's County (11% each); only 6% outside of bank's footprint* Modifications Requested March 31, 2020 (1) April 17, 2020 (1) $0 $50 $100 $150 $200 $250 $300 $350 0 20 40 60 80 100 120 140 $ millions # of Loans Current Balance

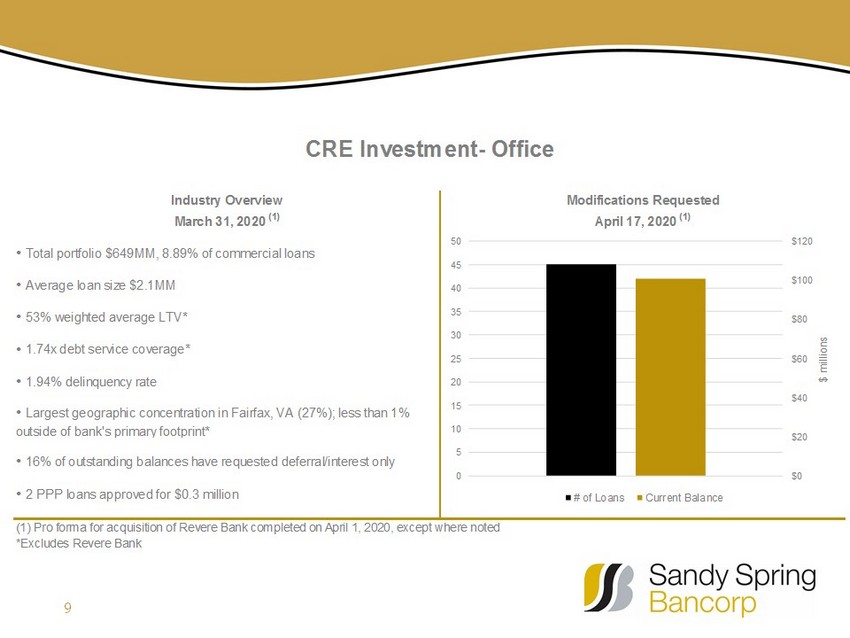

9 • Total portfolio $649MM, 8.89% of commercial loans • Average loan size $2.1MM • 53% weighted average LTV* • 1.74x debt service coverage* • 1.94% delinquency rate • 16% of outstanding balances have requested deferral/interest only • 2 PPP loans approved for $0.3 million (1) Pro forma for acquisition of Revere Bank completed on April 1, 2020, except where noted *Excludes Revere Bank CRE Investment- Office Industry Overview • Largest geographic concentration in Fairfax, VA (27%); less than 1% outside of bank's primary footprint* Modifications Requested March 31, 2020 (1) April 17, 2020 (1) $0 $20 $40 $60 $80 $100 $120 0 5 10 15 20 25 30 35 40 45 50 $ millions # of Loans Current Balance

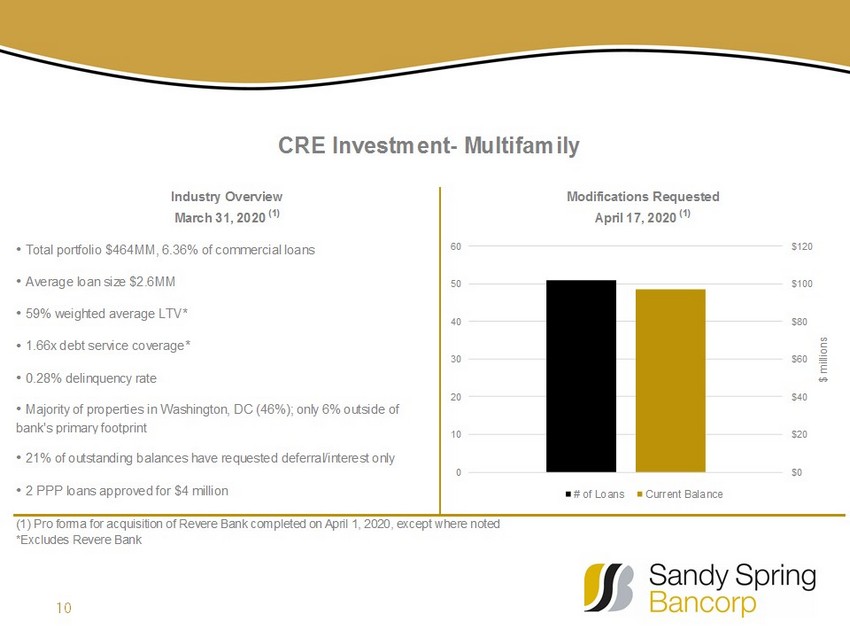

10 • Total portfolio $464MM, 6.36% of commercial loans • Average loan size $2.6MM • 59% weighted average LTV* • 1.66x debt service coverage* • 0.28% delinquency rate • 21% of outstanding balances have requested deferral/interest only • 2 PPP loans approved for $4 million (1) Pro forma for acquisition of Revere Bank completed on April 1, 2020, except where noted *Excludes Revere Bank CRE Investment- Multifamily Industry Overview • Majority of properties in Washington, DC (46%); only 6% outside of bank's primary footprint Modifications Requested March 31, 2020 (1) April 17, 2020 (1) $0 $20 $40 $60 $80 $100 $120 0 10 20 30 40 50 60 $ millions # of Loans Current Balance

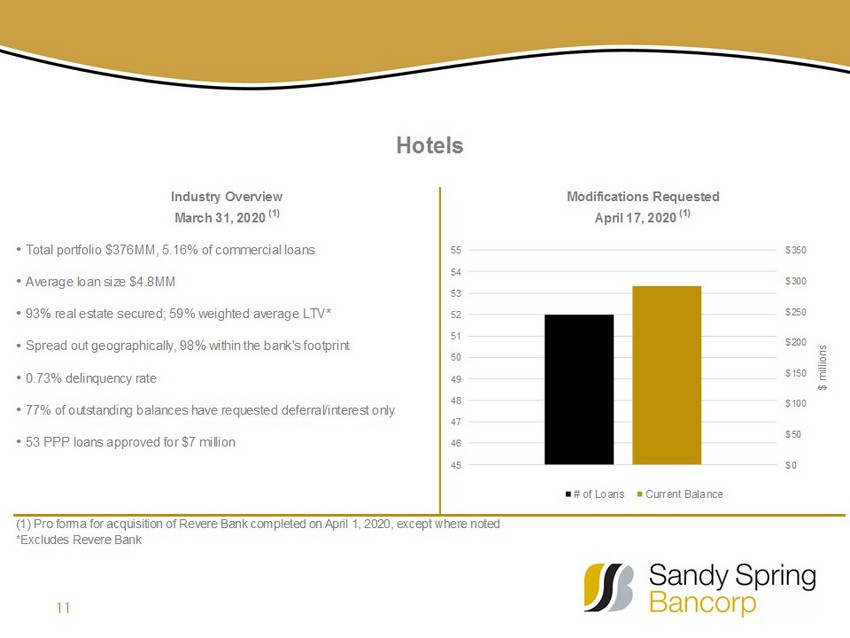

11 • Total portfolio $376MM, 5.16% of commercial loans • Average loan size $4.8MM • 93% real estate secured; 59% weighted average LTV* • Spread out geographically, 98% within the bank's footprint • 0.73% delinquency rate • 77% of outstanding balances have requested deferral/interest only • 53 PPP loans approved for $7 million (1) Pro forma for acquisition of Revere Bank completed on April 1, 2020, except where noted *Excludes Revere Bank Hotels Industry Overview March 31, 2020 (1) Modifications Requested April 17, 2020 (1) $0 $50 $100 $150 $200 $250 $300 $350 45 46 47 48 49 50 51 52 53 54 55 $ millions # of Loans Current Balance

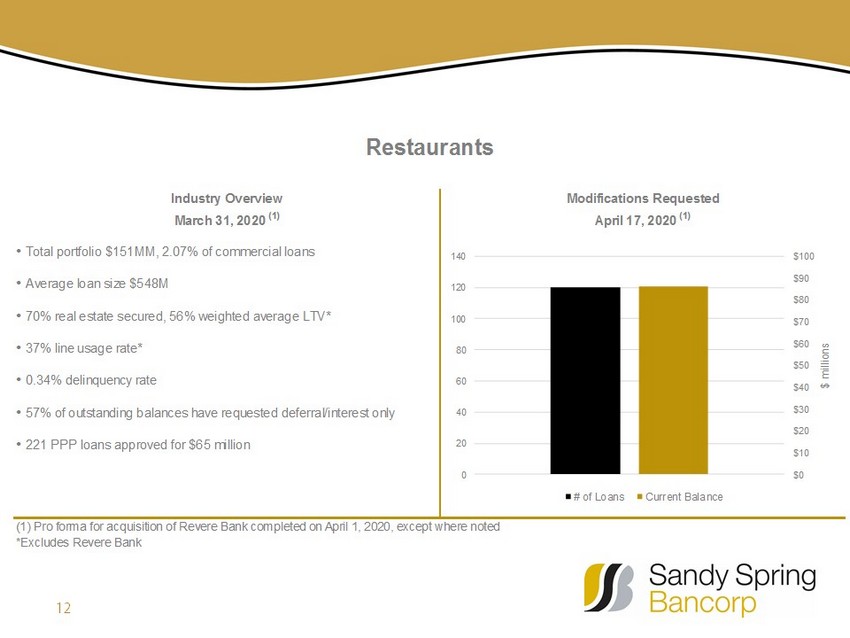

12 • Total portfolio $151MM, 2.07% of commercial loans • Average loan size $548M • 70% real estate secured, 56% weighted average LTV* • 37% line usage rate* • 0.34% delinquency rate • 57% of outstanding balances have requested deferral/interest only • 221 PPP loans approved for $65 million (1) Pro forma for acquisition of Revere Bank completed on April 1, 2020, except where noted *Excludes Revere Bank Restaurants Industry Overview March 31, 2020 (1) Modifications Requested April 17, 2020 (1) $0 $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 0 20 40 60 80 100 120 140 $ millions # of Loans Current Balance

Allowance for Credit Losses – Q1 2020 • Balances in millions. • Day 1 adjustment includes initial allowance on purchased credit deteriorated loans (formerly purchased credit impaired loans) and transitional impact of adopting ASC 326. • Q1 increase in ACL impacted by the economic downturn and changes in economic outlook particularly related to unemployment rate and expected levels of business bankruptcies caused by the coronavirus pandemic. 13 $56.1 $85.8 $5.8 $2.0 $2.8 $19.1 ALLL 12/31/19 Day 1 Adjustment Other factors Change in portfolio composition Change in economic forecast ACL 3/31/20 Drivers of change in Q1 ACL reserve

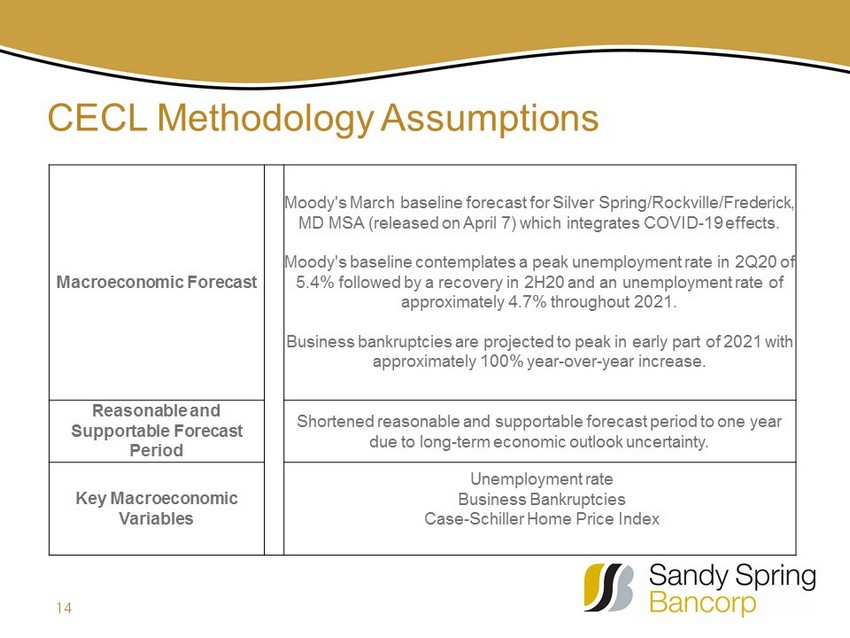

CECL Methodology Assumptions 14 Macroeconomic Forecast Moody's March baseline forecast for Silver Spring/Rockville/Frederick, MD MSA (released on April 7) which integrates COVID - 19 effects. Moody's baseline contemplates a peak unemployment rate in 2Q20 of 5.4% followed by a recovery in 2H20 and an unemployment rate of approximately 4.7% throughout 2021. Business bankruptcies are projected to peak in early part of 2021 with approximately 100% year - over - year increase. Reasonable and Supportable Forecast Period Shortened reasonable and supportable forecast period to one year due to long - term economic outlook uncertainty. Key Macroeconomic Variables Unemployment rate Business Bankruptcies Case - Schiller Home Price Index

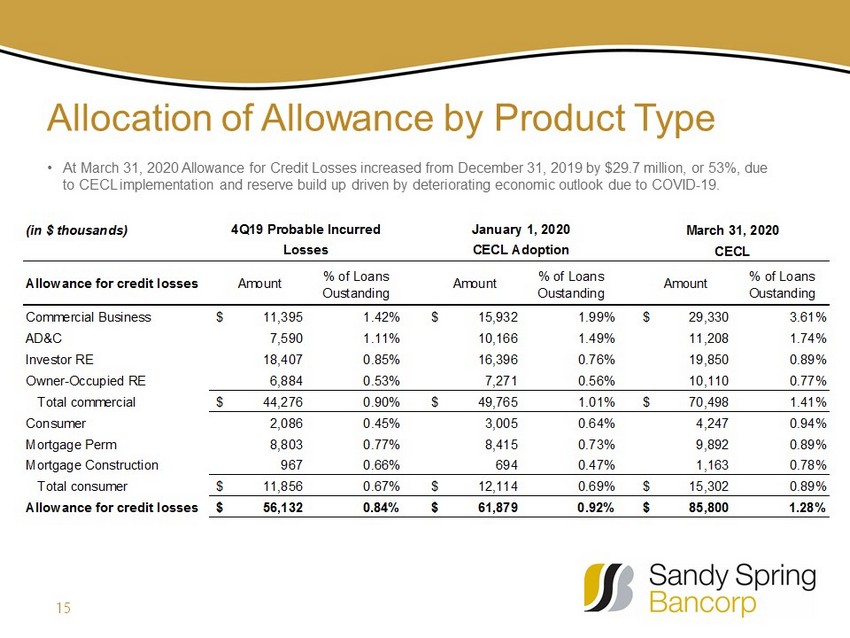

Allocation of Allowance by Product Type • At March 31, 2020 Allowance for Credit Losses increased from December 31, 2019 by $29.7 million, or 53%, due to CECL implementation and reserve build up driven by deteriorating economic outlook due to COVID - 19. 15 (in $ thousands) Allowance for credit losses Amount % of Loans Oustanding Amount % of Loans Oustanding Amount % of Loans Oustanding Commercial Business 11,395$ 1.42% 15,932$ 1.99% 29,330$ 3.61% AD&C 7,590 1.11% 10,166 1.49% 11,208 1.74% Investor RE 18,407 0.85% 16,396 0.76% 19,850 0.89% Owner-Occupied RE 6,884 0.53% 7,271 0.56% 10,110 0.77% Total commercial 44,276$ 0.90% 49,765$ 1.01% 70,498$ 1.41% Consumer 2,086 0.45% 3,005 0.64% 4,247 0.94% Mortgage Perm 8,803 0.77% 8,415 0.73% 9,892 0.89% Mortgage Construction 967 0.66% 694 0.47% 1,163 0.78% Total consumer 11,856$ 0.67% 12,114$ 0.69% 15,302$ 0.89% Allowance for credit losses 56,132$ 0.84% 61,879$ 0.92% 85,800$ 1.28% 4Q19 Probable Incurred Losses January 1, 2020 CECL Adoption March 31, 2020 CECL

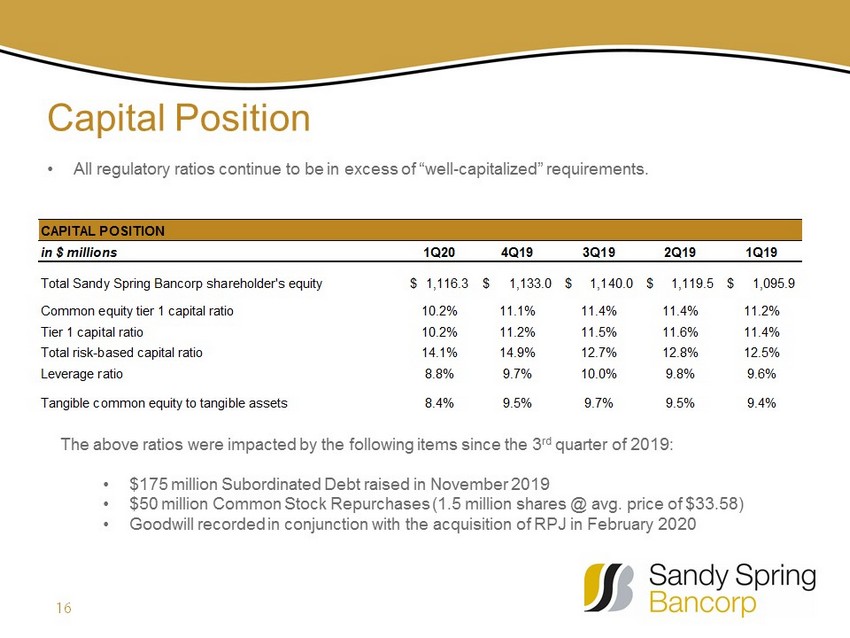

Capital Position • All regulatory ratios continue to be in excess of “well - capitalized” requirements. CAPITAL POSITION in $ millions 1Q20 4Q19 3Q19 2Q19 1Q19 Total Sandy Spring Bancorp shareholder's equity 1,116.3$ 1,133.0$ 1,140.0$ 1,119.5$ 1,095.9$ Common equity tier 1 capital ratio 10.2% 11.1% 11.4% 11.4% 11.2% Tier 1 capital ratio 10.2% 11.2% 11.5% 11.6% 11.4% Total risk-based capital ratio 14.1% 14.9% 12.7% 12.8% 12.5% Leverage ratio 8.8% 9.7% 10.0% 9.8% 9.6% Tangible common equity to tangible assets 8.4% 9.5% 9.7% 9.5% 9.4% 16 The above ratios were impacted by the following items since the 3 rd quarter of 2019: • $175 million Subordinated Debt raised in November 2019 • $50 million Common Stock Repurchases (1.5 million shares @ avg. price of $33.58) • Goodwill recorded in conjunction with the acquisition of RPJ in February 2020

Forward Looking Statements Sandy Spring Bancorp’s forward - looking statements are subject to the following principal risks and uncertainties: risks, uncertainties and other factors relating to the COVID - 19 pandemic, including the length of time that the pandemic continues, the duration of shelter in place orders and the potential imposition of further restrictions on travel in the future; the effect of the pandemic on the general economy and on the businesses of our borrowers and their ability to make payments on their obligations; the remedial actions and stimulus measures adopted by federal, state and local governments, the inability of employees to work due to illness, quarantine, or government mandates; general economic conditions and trends, either nationally or locally; conditions in the securities markets; changes in interest rates; changes in deposit flows, and in the demand for deposit, loan, and investment products and other financial services; changes in real estate values; changes in the quality or composition of the Company’s loan or investment portfolios; changes in competitive pressures among financial institutions or from non - financial institutions; the Company’s ability to retain key members of management; changes in legislation, regulations, and policies; the possibility that any of the anticipated benefits of acquisitions will not be realized or will not be realized within the expected time period; and a variety of other matters which, by their nature, are subject to significant uncertainties. Sandy Spring Bancorp provides greater detail regarding some of these factors in its Form 10 - K for the year ended December 31, 2019, including in the Risk Factors section of that report, and in its other SEC reports. Sandy Spring Bancorp’s forward - looking statements may also be subject to other risks and uncertainties, including those that it may discuss elsewhere in this news release or in its filings with the SEC, accessible on the SEC’s Web site at www.sec.gov . 17