Attached files

| file | filename |

|---|---|

| EX-95 - MINE SAFETY DISCLOSURE EXHIBIT - Western Uranium & Vanadium Corp. | f10k2019ex95_western.htm |

| EX-32 - CERTIFICATION - Western Uranium & Vanadium Corp. | f10k2019ex32_western.htm |

| EX-31.2 - CERTIFICATION - Western Uranium & Vanadium Corp. | f10k2019ex31-2_western.htm |

| EX-31.1 - CERTIFICATION - Western Uranium & Vanadium Corp. | f10k2019ex31-1_western.htm |

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________________ to ___________________

Commission file number: 000-55626

Western Uranium & Vanadium Corp.

(Exact Name of Registrant as Specified in its Charter)

| Ontario, Canada | 98-1271843 | |

| (State

or other jurisdiction of incorporation or organization) |

(I.R.S.

Employer Identification No.) | |

| 330 Bay Street, Suite 1400 | ||

| Toronto, Ontario, Canada | M5H 2S8 | |

| (Address of Principal Executive Offices) | (Zip Code) |

(970)

864-2125

(Registrant’s Telephone Number, including Area Code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| Title of Each Class | Name of Each Exchange on Which Registered | |

| None |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

Common Shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large Accelerated Filer ☐ | Accelerated Filer ☐ |

| Non-Accelerated Filer ☐ | Smaller Reporting Company ☒ |

| Emerging Growth Company ☒ |

If an emerging growth company, indicate by checkmark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of June 30, 2019, the aggregate market value of the common shares held by non-affiliates of the registrant was $25,190,414.

As of April 13, 2020, there were 30,083,747 common shares, no par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

WESTERN URANIUM & VANADIUM CORP.

FORM 10-K

TABLE OF CONTENTS

i

As used in this Annual Report on Form 10-K, unless the context otherwise requires, the terms “we,” “us,” “our,” “Western” and “WUC”, or the “Company” refer to Western Uranium & Vanadium Corp., an Ontario Canadian corporation, and its subsidiaries.

The accounts of the Company are reported in U.S. dollars. Unless otherwise specified, all dollar amounts referenced in this Annual Report on Form 10-K and the consolidated financial statements are stated in U.S. dollars.

FORWARD-LOOKING STATEMENTS AND INTRODUCTION

The statements contained in this document that are not purely historical are “forward-looking statements.” Although we believe that the expectations reflected in such forward-looking statements, including those regarding future operations, are reasonable, we can give no assurance that such expectations will prove to be correct. Forward-looking statements are not guarantees of future performance and they involve various risks and uncertainties. Forward-looking statements contained in this document include statements regarding our proposed services, market opportunities and acceptance, expectations for revenues, cash flows and financial performance, and intentions for the future. Such forward-looking statements are included under Item 1. “Business” and Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations”. All forward-looking statements included in this document are made as of the date hereof, based on information available to us as of such date, and we assume no obligation to update any forward-looking statement. It is important to note that such statements may not prove to be accurate and that our actual results and future events could differ materially from those anticipated in such statements. Among the factors that could cause actual results to differ materially from our expectations are those described under Item 1. “Business,” Item 1A. “Risk Factors” and Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations”. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by this section and other factors included elsewhere in this document.

ii

CORPORATE HISTORY

Western Uranium & Vanadium Corp. (formerly known as Western Uranium Corporation) was incorporated in December 2006 under the Ontario Business Corporations Act and was formerly a non-listed reporting issuer subject to the rules and regulations of the Ontario Securities Commission. On November 20, 2014, the Company completed a listing process on the Canadian Securities Exchange (“CSE”). As part of that process, the Company acquired 100% of the issued and outstanding shares of Pinon Ridge Mining LLC (“PRM”), a Delaware limited liability company. The transaction constituted a reverse takeover of Western by PRM. After obtaining appropriate shareholder approvals, the Company subsequently reconstituted its Board of Directors and senior management team.

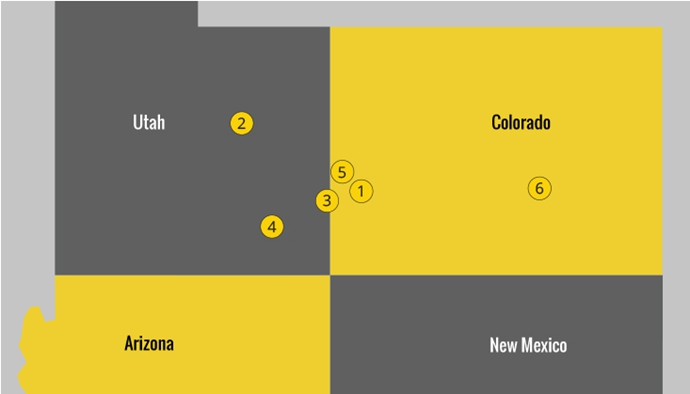

On August 18, 2014, the Company closed on the purchase of certain mining properties in Colorado and Utah from Energy Fuels Holding Corp. Assets purchased included both owned and leased lands in Utah and Colorado and all represent properties that have been previously mined for uranium to varying degrees in the past. The acquisition included the purchase of the Sunday Mine Complex. The Sunday Mine Complex is located in western San Miguel County, Colorado. The complex consists of the following five individual mines: the Sunday mine, the Carnation mine, the Saint Jude mine, the West Sunday mine and the Topaz mine. The operation of each of these mines requires a separate permit and all such permits have been obtained by Western and are currently valid. In addition, each of the mines has good access to a paved highway, electric power to existing mine workings, office/storage/shop and change buildings, and extensive underground haulage development with multiple vent shafts complete with exhaust fans. The Sunday Mine Complex is where the Company anticipates it would start mining operations.

On September 16, 2015, Western completed its acquisition of Black Range, an Australian company that was listed on the Australian Securities Exchange until the acquisition was completed. The acquisition terms were pursuant to a definitive Merger Implementation Agreement entered into between Western and Black Range. Pursuant to the agreement, Western acquired all of the issued shares of Black Range by way of Scheme of Arrangement (“the Scheme”) under the Australian Corporation Act 2001 (Cth) (the “Black Range Transaction”), with Black Range shareholders being issued common shares of Western on a 1 for 750 basis. On August 25, 2015, the Scheme was approved by the shareholders of Black Range and on September 4, 2015, Black Range received approval by the Federal Court of Australia. In addition, Western issued to certain employees, directors and consultants options to purchase Western common shares. Such stock options were intended to replace Black Range stock options outstanding prior to the Black Range Transaction on the same 1 for 750 basis.

In connection with the Black Range Transaction, Western acquired the net assets of Black Range. These net assets consist principally of interests in a large uranium resource located in Colorado (the “Hansen-Taylor Complex”) and a 100% interest in a 25 year license for Kinetic Separation technologies (“Kinetic Separation”, formerly known as “Ablation”) and related patents from Ablation Technologies, LLC. The Hansen-Taylor Complex is principally a sandstone-hosted deposit that was discovered in 1977.

Furthermore, related to Kinetic Separation in connection with the acquisition of Black Range Minerals Ltd. (“Black Range”), the Company assumed a call option agreement between Black Range and Mr. George Glasier. Prior to the Black Range Transaction, George Glasier, the Company’s CEO, who is also a director (“Seller”), transferred his interest in a former joint venture with Ablation Technologies, LLC to Black Range. In connection with the transfer, Black Range issued 25 million shares of Black Range common shares to Seller and committed to pay $500,000 AUD ($351,099 USD as of December 31, 2019) to Seller within 60 days of the first commercial application of the Kinetic Separation. Western assumed this contingent payment obligation in connection with the Black Range Transaction.

The Kinetic Separation process is dramatically different from conventional mining techniques. Subject to regulatory approvals for the use of Kinetic Separation, the benefits of Kinetic Separation are as follows:

| ● | Mining, crushing, and separation of waste from minerals (uranium and vanadium), used most effectively, occurs underground (inside the mine). Under this approach the costs of moving material to the surface are less as 85%-90% of the mined material remains underground and is never brought outside the mine. |

| ● | Less radiometric exposure throughout the process due to reduced waste rock on the surface and after the milling process less tailings. Overall surface waste material is reduced and the time duration of material handling is reduced. |

| ● | Lower costs for transportation of post-kinetically separated material from the mine site to the mill site because 85-90% of the mined material would not be taken to the mill. |

| ● | Once the kinetically separated material reaches the mill, the acid consumption at the mill and power is much less due to the lower quantity and more concentrated material moving through the milling process. |

1

Kinetic Separation can be used on legacy uranium stockpiles in the western United States. WUC would kinetically separate these stockpiles, removing 85-90% of the uranium. This is an application through which Kinetic Separation could positively contribute to the ‘greening of the environment’. According to a study there are approximately 4,225 legacy uranium mines from the 1940-1970 period throughout the Western United States, most of which have waste stockpiles.

In the estimation of management, Kinetic Separation mining allows the cost of production of uranium to be reduced by 44-53%.

Our common shares are listed on the Canadian Securities Exchange, also known as the “CSE,” under the symbol “WUC”, and are also quoted in the United States on the OTCQX Best Market under the symbol “WSTRF.” We are headquartered in Ontario, Canada with mining operations in the two U.S. states of Utah and Colorado. We have three full-time employees and one part-time employee. The mailing address of our headquarters is 330 Bay Street, Suite 1400, Toronto, Ontario, M5H2S8, Canada, and the telephone number is (970) 864-2125. Our corporate website is located at http://www.western-uranium.com/.

We are an “emerging growth company” as that term is defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). The JOBS Act defines an “emerging growth company” as one that had total annual gross revenues of less than $1,000,000,000 during the last fiscal year. Section 102(b) (1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Securities Exchange Act) are required to comply with the new or revised financial accounting standard. The JOBS Act also provides that a company can elect to opt out of the extended transition period provided by Section 102(b)(1) of the JOBS Act and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable.

Our wholly-owned subsidiaries are Western Uranium Corp., Pinon Ridge Mining LLC, Black Range Minerals Limited, Black Range Copper Inc., Ranger Resources Inc., Black Range Minerals Inc., Black Range Minerals Colorado LLC, Black Range Minerals Wyoming LLC, Haggerty Resources LLC, Ranger Alaska LLC, Black Range Minerals Utah LLC, Black Range Minerals Ablation Holdings Inc. and Black Range Development Utah LLC.

OUR COMPANY

Western is in the business of exploring, developing, mining and production of its uranium and vanadium resource properties.

Western is an exploration stage company for purposes of Industry Guide 7 of the U.S. Securities and Exchange Commission (“SEC”). Industry Guide 7 states that mining companies like ours can be classified into three stages: exploration, development, or production. Exploration stage includes all companies engaged in the search for mineral deposits, which are not in either the development or production stage. In order to be classified as a development or production stage company, the Company must have already established reserves. The Company has not established reserves for purposes of Industry Guide 7.

Our mineral properties are located in western Colorado and eastern Utah and adjacent areas of the western United States. Our primary focus is bringing the fully permitted Sunday Mine Complex into production, permitting the San Rafael Project and the commercialization of Kinetic Separation.

The Sunday Mine Complex is located in western San Miguel County, Colorado. The complex consists of the following five individual mines: the Sunday mine, the Carnation mine, the Saint Jude mine, the West Sunday mine and the Topaz mine. The operation of each of these mines requires a separate permit and all such permits have been obtained by Western and are currently valid. In addition, each of the mines has good access to a paved highway, electric power to existing mine workings, office/storage/shop and change buildings, and extensive underground haulage development with multiple vent shafts complete with exhaust fans.

We have acquired a license (“Kinetic Separation”), which provides a low cost, purely physical, method of separating uranium and vanadium mineralization from waste. No chemicals are added in the process, yet very high mineral recoveries can be achieved with considerable mass reduction; facilitating the separation of a high-value, high-grade ore product from a coarse-grained barren “clean sand” product.

Application of Kinetic Separation is expected to have a very positive effect on the development of not only our Sunday Mine Complex, but also most of our and others’ deposits, because it significantly reduces both capital and operating costs. Extensive test work has shown that from amenable sandstone-hosted ore types, typically more than 90% of the mineralization can be separated into 10-20% of the initial sample mass.

2

OUR STRATEGY

Our vision is to become a leading uranium and vanadium developer and producer. Our strategy is to build value for stockholders by advancing our projects towards scaled-up production. The increase in vanadium price levels during 2017/2018 has increased the relative importance of this resource to the Company. Hence, Western is increasingly able to baseload mine production with vanadium as a co-product. As a result, during 2019 Western implemented a mine re-opening project at the Sunday Mine Complex to identify high-grade vanadium ore, followed by bulk sampling and development drilling. Active mining was conducted and the extracted ore was stockpiled underground in the mines. The project has continued in 2020 as multiple surface infrastructure projects were completed to meet Colorado Division of Reclamation, Mining and Safety (CRDMS) requirements. Completion of the CDRMS prerequisites will enable the newly mined and stockpiled underground ore to be brought to the surface in 2020. Ore pad construction, the last of the surface projects, was completed; however, CDRMS inspection has been delayed due to a no-travel policy which was instituted in response to the COVID-19 outbreak. The Company holds an exclusive 25-year license to use Kinetic Separation, a proven technology that we anticipate will improve the efficiency of the mining from Western’s sandstone-hosted ore. The license agreement was entered into on March 17, 2015 and expires on March 16, 2040. There are no remaining license fee obligations and there are no future royalties due under the agreement. The Company has the right to sub-license the technology to third parties. The Company may not sell or assign the Kinetic Separation license; however, it could be transferred in the sale of Western or the subsidiary holding the license.

At any time we may have acquisition or partnering opportunities in various stages of active review, including, for example, our engagement of consultants and advisors to analyze particular opportunities, analysis of technical, financial and other confidential information, submission of indications of interest, participation in preliminary discussions and negotiations and involvement as a bidder in competitive processes.

Capital Raising

On May 4, 2018, the Company completed a private placement of 909,622 units at a price of CAD $0.68 (USD $0.53) per unit for gross proceeds of CAD $618,543 (USD $481,560). Each unit consisted of one common share and a warrant to purchase one-half of one common share. Each warrant is exercisable at a price of CAD $1.15 and expires two years from the date of issuance.

On July 27, 2018, the Company completed a private placement of 2,525,526 units at a price of CAD $0.68 (USD $0.52) per unit for gross proceeds of CAD $1,717,358 (USD $1,319,096). Each unit consisted of one common share and a warrant to purchase one-half of one common share. Each warrant is exercisable at a price of CAD $1.15 and expires two years from the date of issuance.

On August 9, 2018, the Company completed a private placement of 1,907,088 units at a price of CAD $0.68 (USD $0.52) per unit for gross proceeds of CAD $1,296,820 (USD $1,000,000). Each unit consisted of one common share and a warrant to purchase one-half of one common share. Each warrant is exercisable at a price of CAD $1.15 and expires two years from the date of issuance.

On April 16, 2019, the Company completed a private placement of 3,914,632 units at a price of CAD $0.98 (USD $0.73) per unit for net proceeds of CAD $3,836,340 (USD $2,856,356). Each unit consisted of common share and a warrant to purchase one-half of one common share. Each warrant is exercisable at a price of CAD $1.70 and expires three years from the date of issuance.

On June 17, 2019, the Company completed a private placement of 192,278 units at a price of CAD $0.98 (USD $0.73) per unit for gross proceeds of CAD $188,432 (USD $140,555). Each unit consisted of one common share and a warrant to purchase one-half of one common share. Each warrant is exercisable at a price of CAD $1.70 and expires three years from the date of issuance.

During the year ended December 31, 2019, the Company issued an aggregate of 4,106,910 common shares in connection with these private placements.

Uranium/Vanadium Production

Western historically positioned itself for operational flexibility with the goal of beginning production as expeditiously as possible once market conditions for uranium and/or vanadium were favorable. The recent vanadium price rally brought about those conditions, thus catalyzing the Sunday Mine Complex project. Western reinitiated active mining operations at the Sunday Mine Complex project with its infrastructure and exploratory projects, which culminated in the commencement of production with the mining and stockpiling of the extracted uranium/vanadium ore. The well maintained existing infrastructure from years of previous production allowed the Company to quickly advance the mine to production ready status. As the mining team refocused on surface infrastructure projects required by the CDRMS, the mines were shut; mining operations and transporting extracted ore to the surface could commence after CDRMS inspection of the newly constructed ore pads. The impact of COVID-19 has become an additional timing consideration. With the decline in vanadium prices during calendar year 2019, the economics of the Sunday Mine Complex have shifted from an emphasis on vanadium production back toward co-production of uranium/vanadium. The recent rally in uranium prices has become an increasingly important driver for scaled up production.

3

Western believes that its mineral resources have a reasonable prospect for economic extraction. However, the Company has not yet completed a Preliminary Economic Assessment (“PEA”).

URANIUM MARKET OUTLOOK

World demand for clean, reliable, and affordable electricity is growing. Given the expected construction of nuclear reactors and the expected growth of nuclear energy, we believe that the future for uranium is positive. Further, recently announced production cuts in response to COVID-19 by four global uranium producers has been projected to take approximately 50% of the 2020 uranium production offline, which will reduce available supply. The U.S. section 232 petition and Nuclear Fuel Working Group process has the potential to increase U.S. domestic uranium production and create economic pricing levels for U.S. domestic producers. We believe these factors will provide the price levels needed to support the additional production and supply that will be required. Currently, excess (secondary) supplies are being drawn down, and additional primary production will be needed to meet long-term demand.

Once prices rise, it may be difficult for most suppliers to respond in a timely manner, as it requires many years of permitting and development to bring new mines into production. These lead times will put further upward pressure on prices.

Western has a competitive advantage, as our mining properties are permitted and ready to scale-up production on short notice.

Despite current market uncertainty and depressed prices, we believe we have begun to see certain early signs of a market recovery; the spot uranium price declined from $29 to $24 during 2019, but has quickly rebounded to $29 in response to the COVID-19 production cuts. Japanese utilities have 42 nuclear reactors in the process of restarting (according to the World Nuclear Association (“WNA”)). According to data from the WNA, Chinese utilities continue to aggressively build new reactors and buy uranium, with the goal of having more nuclear capacity than any country except the USA and France by 2020. In total, according to the WNA, there are about 50 new reactors under construction in 13 countries and in all there are about 160 reactors on order or being planned, and over 300 more are proposed.

However, in the short- and medium-terms, market challenges remain. The world continues to be oversupplied with uranium, mainly due to large quantities of secondary uranium supplies, high levels of excess inventories, premature reactor shutdowns, delays in new reactor construction, and decreased demand due to Japanese reactors remaining offline for longer than expected. In addition, there is a great deal of uncertainty in uranium prices regarding the timing and level of the recovery, as fundamental, political, technical, and other factors could cause prices to be significantly above or below currently expected ranges.

In the United States, an investigation under Section 232 of the Trade Expansion Act of 1962 (U.S.) was undertaken in 2018 to assess the impact to national security of the importation of the vast majority of uranium utilized by the ~100 operating civilian nuclear reactors within the United States. The U.S. Department of Commerce provided a report containing a recommendation to the White House in April 2018; President Trump considered the findings of the Section 232 report and disseminated a Presidential Memoranda on July 12, 2019. At that time, the President did not implement the quota solution proposed by the petitioners. Instead, to address the concerns of the Department of Commerce, the President formed the U.S. Nuclear Fuel Working Group (“NFWG”) and charged them with finding solutions for reviving and expanding domestic nuclear fuel production and reinvigorating the entire nuclear fuel supply chain. The group was required to submit a report containing findings and recommendations on or before October 10, 2019, but President Trump granted a 30 day extension on the delivery of that report. As a first step in addressing this issue, President Trump’s Fiscal Year 2021 budget, released February 10, 2020, included a $150 million line item each year for the next decade to establish a Uranium Reserve. In a February 27, 2020 hearing U.S. Energy Secretary Dan Brouillette stated the NFWG was preparing to release its recommendations on the upcoming Monday or Tuesday. Notably, the timing was such that it immediately preceded the Coronavirus outbreak which has become the near exclusive focus of the Trump Administration and all levels/branches of government. As of the day that is one day before the filing of this report, there has been no official U.S. government update as to the status or content of the NFWG’s report. Since neither the Department of Commerce nor NFWG reports compiled for the White House have been shared with Congress, in February Congress called for the Department of Energy to oversee the compilation of a report on Key Challenges in Reconstituting Uranium Mining and Conversion Capabilities in the United States. The extended deadline for industry to supply responses to the Request For Information was March 30, 2020. Thus, three separate initiatives have been pursued by the U.S. government. The Company has participated at each stage of this process and its efforts are ongoing.

While there is no guarantee as to outcome, we believe the petition is compelling given the dynamics of uranium markets and the participation of state-owned and state-subsidized entities, which has caused the shutdown of nearly all U.S. uranium production. Further, the question of U.S. national security now hinges upon the degree that counterparties in Russia, Kazakhstan, Uzbekistan, and China have infiltrated the U.S. nuclear fuel cycle. The underlying thesis has been increasingly affirmed during the COVID-19 crisis as the U.S. has been directly damaged by Chinese dependent supply chains and Russia initiating an oil price war which turned energy into a geopolitical weapon. A positive outcome would provide relief for the U.S. uranium industry whereby U.S. domestic uranium production should have the opportunity to be sold at a price above production cost and at a profit to the producer. Western is one of very few uranium companies holding previously producing permitted and developed mines in the United States and thus is well positioned to benefit in the short-term from a favorable outcome.

4

OVERVIEW OF THE URANIUM INDUSTRY

Spot prices rose from $21 per pound in January 2005 to a high of $136 per pound in June 2007 in anticipation of sharply higher projected demand as a result of a resurgence in nuclear power and the depletion of secondary supplies. Secondary supplies are inventories of uranium not publicly available for sale, they are primarily held by utility companies and governments. The sharp price increase was driven in part by high levels of buying by utility companies, which resulted in most utilities covering their requirements through 2009. A decrease in near-term utility demand coupled with rising levels of supplies from producers and traders have led to downward pressure on uranium prices since the third quarter of 2007. A rebound in uranium prices in conjunction with a recovery in commodities in 2010 was curtailed by the Fukushima disaster in Japan.

Since the Fukushima disaster in 2011, uranium prices entered a steady decline until June 2014, when they rebounded slightly and peaked again in March 2015 at $39 per pound. After that peak, prices again began to fall steadily reaching their lowest point of $18 per pound in November 2016 before moving upward in 2017 and ending the year at the higher year over year level of $22 per pound. Uranium prices continued to steady in 2019 ending at $25 per pound on December 31, 2019.

The only significant commercial use for uranium is as a fuel for nuclear power plants for the generation of electricity. According to the WNA, at the end of February 2018, there were 449 nuclear reactors operable worldwide, with annual requirements of about 143.3 million pounds of uranium.

From the reports of leading investment banks, the macroeconomic conditions driving uranium prices are as follows:

| ● | WNA reports 55 nuclear reactors under construction with most projects China, India, Russia and South Korea. |

| ● | Decrease in primary supply due to global producers shutting down mining operations that weren’t profitable at current pricing levels and recent larger production shutdowns in response to COVID-19 |

| ● | Decreasing secondary supplies (excess reserves and supplies generally held by governments and utilities). |

| ● | The Section 232 Uranium investigation and Nuclear Fuel Working Group outcome. |

| ● | Increasing uncovered demand opportunities for future uranium demand as nuclear utilities have decreased their contracting levels |

Across the ten banks and analysts most active in the sector, a term structure of rising uranium spot prices which are significantly above today’s prices are forecast almost across the board from 2020 to 2024. The Company obtained analyst estimates that were publicly released before the COVID-19 outbreak impacted world markets and cause global production cuts. These projected increases are primarily due to two factors. The first is expected reduction in uranium production due to the low price environment. The second is continued growth in nuclear energy, fueled primarily by new plants with the greatest number located in China, Russia, and India over the next 5 years. Further, small modular reactors and advanced reactors are expected to begin coming online during the next decade. This should lead to excess reserves and inventories drying up and causing a shortage in the coming years, as historical contracts roll-off. Recently, due to mine closures in response to COVID-19, the market price of uranium has increased sharply, in contrast to other commodities.

Based upon these pricing factors specific to the uranium industry, we believe that uranium prices will improve over the coming years for Western to initiate full-scale production in its best properties.

Vanadium

With the exception of the Hansen/Taylor Deposit, most of the Company’s mining assets, including the Sunday Mine Complex, contain vanadium either as a stand-alone product or a co-product to uranium.

Conventional and new vanadium applications include steelmaking, aerospace, stationary energy storage, batteries, and chemicals.

When a very small amount of vanadium is added to steel the hardening effect greatly increases its strength. And while steelmaking accounts for roughly 90% of all vanadium currently consumed, it’s estimated that vanadium is only used in about 9% of all steels today.

In a research report, BMO Capital Markets identified a structural change in the vanadium markets. China, the largest vanadium producer in the world, has seen supply disrupted by environmental monitoring and rules while domestic demand was increasing. During 2017, BMO observed ferrovanadium exports falling by 30% year over year and projected that China would become a net importer of ferrovanadium. In 2018, this forecast was validated as China which had been a net vanadium exporter became a net vanadium importer. On the demand side, China announced a new high strength rebar standard to increase earthquake resistance in February 2018 that became effective on November 1, 2018. On the supply side in its efforts to fight pollution, Chinese environmental inspections resulted in the closing of dirty processes in which vanadium was recovered as a byproduct. These policy changes were very positive for vanadium prices. As a result of these structural changes, vanadium demand exceeded vanadium supply putting the market into a deficit and pushing the prices to all-time highs during the fourth quarter of 2018.

The substantial appreciation in vanadium price during 2018 catalyzed the Company to pursue the Sunday Mine Complex Vanadium Project during 2019.

5

After steelmaking, the second largest market for vanadium is that of catalysts and chemical applications. Significant new sources of demand for vanadium are also expected to originate from vanadium redox flow batteries (VRFB).

The current vanadium market price is $6.10 per pound as of December 31, 2019 which is a decrease from the December 31, 2018 price when the price was $18.80 per pound. New vanadium supply came online after vanadium prices reached all-time highs.

COMPETITION

There is global competition for uranium properties, capital, customers and the employment and retention of qualified personnel. We compete with multiple exploration companies for both properties as well as skilled personnel. In the production and marketing of uranium, there are a number of producing entities globally, some of which are government controlled and several of which are significantly larger and better capitalized than we are. Several of these organizations also have substantially greater financial, technical, manufacturing and distribution resources than we have.

Our future uranium production may also compete with uranium from secondary supplies, including the sale of uranium inventory held by the U.S. Department of Energy. At the current time, DOE uranium sales have been suspended. In addition, there are numerous entities in the market that compete with us for properties and operate in situ recovery (“ISR”) facilities. If we are unable to successfully compete for properties, capital, customers or employees or with alternative uranium sources, it could have a material adverse effect on our results of operations.

With respect to sales of uranium, the Company competes primarily based on price. We will market uranium to utilities and commodity brokers. We are in direct competition with supplies available from various sources worldwide. We believe we compete with multiple operating uranium companies.

With respect to sales of vanadium, the Company will compete primarily based upon availability and secondarily on price. There will be direct competition with primary production, secondary production, and co-production from various companies and processors worldwide as individual entities come online or increase production to address the supply deficit.

ENVIRONMENTAL CONSIDERATIONS AND PERMITTING

United States

Uranium extraction is regulated by the federal government, states and, in some cases, by Indian tribes. Compliance with such regulation has a material effect on the economics of our operations and the timing of project development. Our primary regulatory costs have been related to obtaining licenses and permits from federal and state agencies before the commencement of production activities. The environmental regulatory requirements for the ISR industry are well established. Many ISR projects have gone a full life cycle without any significant environmental impact. However, the process can make environmental permitting difficult and timing unpredictable. Western does not plan to utilize an ISR mining process on its properties.

Mining Permits are disclosed on a per mine basis in the “Properties” section, below.

Reclamation and Restoration Costs and Bonding Requirements

At the conclusion of conventional mining, a site is decommissioned and reclaimed. Reclamation involves removing evidence of surface disturbance. The reclamation liabilities of the US mines are subject to legal and regulatory requirements. Estimates of the costs of reclamation are reviewed periodically by the applicable regulatory authorities. The reclamation liability represents the Company’s best estimate of the present value of future reclamation costs in connection with the mineral properties. The Company determined the gross reclamation liabilities at December 31, 2019 of the mineral properties to be approximately $897,662.

The Company is required by State regulatory agencies to obtain financial surety relating to certain of its future restoration and reclamation obligations. The Company has provided performance bonds issued for the benefit of the Company in the amount of $897,662 to satisfy such regulatory requirements.

6

Risks Related to Our Business

Our business activities are subject to significant risks, including those described below. Every investor or potential investor in our securities should carefully consider these risks. If any of the described risks actually occurs, our business, financial position and results of operations could be materially adversely affected. Such risks are not the only ones we face and additional risks and uncertainties not presently known to us or that we currently deem immaterial may also affect our business.

The uranium/vanadium ore that we have mined remains stockpiled underground at the Sunday Mine Complex. As a result, we have no saleable product and currently have no sources of operating cash. If we cannot access additional sources of private or public capital, partner with another company that has cash resources and/or find other means of generating revenue other than uranium or vanadium sales, we may not be able to remain in business.

Until we begin either uranium or vanadium sales, we have no way to generate cash inflows unless we monetize certain of our assets or obtain additional financing. We can provide no assurance that our properties will produce saleable production or that we will be able to continue to find, develop, acquire and finance additional reserves. If we cannot monetize certain existing assets, partner with another company that has cash resources, find other means of generating revenue other than uranium or vanadium production and/or access additional sources of private or public capital, we may not be able to remain in business and our stockholders may lose their entire investment.

Our ability to function as an operating mining company will be dependent on our ability to mine our properties at a profit sufficient to finance further mining activities and for the acquisition and development of additional properties. The volatility of uranium prices makes long-range planning uncertain and raising capital difficult.

Our ability to operate on a positive cash flow basis will be dependent on mining sufficient quantities of uranium or vanadium at a profit sufficient to finance our operations and for the acquisition and development of additional mining properties. Any profit will necessarily be dependent upon, and affected by, the long and short term market prices of uranium and vanadium, which are subject to significant fluctuation. Uranium prices have been and will continue to be affected by numerous factors beyond our control. These factors include the demand for nuclear power, political and economic conditions in uranium producing and consuming countries, uranium supply from secondary sources and uranium production levels and costs of production. A significant, sustained drop in uranium prices may make it impossible to operate our business at a level that will permit us to cover our fixed costs or to remain in operation.

Evaluating our future performance may be difficult since we have a limited financial and operating history, with significant negative cash flow and an accumulated deficit to date. Furthermore, there is no assurance that we will be successful in securing any form of additional financing in the future, therefore substantial doubt exists as to whether our cash resources and working capital will be sufficient to enable the Company to continue its operations over the next twelve months. Our long-term success will depend ultimately on our ability to achieve and maintain profitability and to develop positive cash flow from our mining activities.

As more fully described within this annual report, we acquired our first mineral properties in November of 2014. To date, we have been acquiring additional mineral properties and raising capital. We hold uranium projects in various stages of exploration in the States of Colorado and Utah.

As more fully described under “Liquidity and Capital Resources” of Item 7. “Management’s Discussion and Analysis of Financial Condition and Result of Operations”, we have a history of significant negative cash flow and net losses, with an accumulated deficit balance of $8.7 million and $6.6 million at December 31, 2019 and 2018, respectively. We have been reliant on equity financings from the sale of our common shares and on debt financing in order to fund our operations. We do not expect to achieve profitability or develop positive cash flow from operations in the near term. As a result of our limited financial and operating history, including our significant negative cash flow and net losses to date, it may be difficult to evaluate our future performance.

At December 31, 2019 and December 31, 2018, we had working capital of $1,678,747 and $597,669, respectively. The continuation of the Company as a going concern is dependent upon our ability to obtain adequate additional financing which we have successfully secured since inception. However, there is no assurance that we will be successful in securing any form of additional financing in the future, therefore substantial doubt exists as to whether our cash resources and working capital will be sufficient to enable the Company to continue its operations over the next twelve months. The consolidated financial statements for the two years ended December 31, 2019 and 2018 were prepared assuming that the Company would continue as a going concern. The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. The Company has incurred continuing losses from operations and is dependent upon future sources of equity or debt financing in order to fund its operations. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

7

Our reliance on equity and debt financings is expected to continue for the foreseeable future, and their availability whenever such additional financing is required, will be dependent on many factors beyond our control including, but not limited to, the market price of uranium, the continuing public support of nuclear power as a viable source of electricity generation, the volatility in the global financial markets affecting our stock price and the status of the worldwide economy, any one of which may cause significant challenges in our ability to access additional financing, including access to the equity and credit markets. We may also be required to seek other forms of financing, such as asset divestitures or joint venture arrangements to continue advancing our uranium projects, which would depend entirely on finding a suitable third party willing to enter into such an arrangement, typically involving an assignment of a percentage interest in the mineral project.

Our long-term success, including the recoverability of the carrying values of our assets and our ability to acquire additional uranium projects and continue with exploration and pre-extraction activities and mining activities on our existing uranium projects, will depend ultimately on our ability to achieve and maintain profitability and positive cash flow from our operations by establishing ore bodies that contain commercially recoverable uranium and to develop these into profitable mining activities. The economic viability of our mining activities has many risks and uncertainties. These include, but are not limited to: (i) a significant, prolonged decrease in the market price of uranium; (ii) difficulty in marketing and/or selling uranium concentrates; (iii) significantly higher than expected capital costs to construct the mine and/or processing plant; (iv) significantly higher than expected extraction costs; (v) significantly lower than expected uranium extraction; (vi) significant delays, reductions or stoppages of uranium extraction activities; and (vi) the introduction of significantly more stringent regulatory laws and regulations. Our mining activities may change as a result of any one or more of these risks and uncertainties and there is no assurance that any ore body that we extract mineralized materials from will result in achieving and maintaining profitability and developing positive cash flow.

Our operations are capital intensive, and we will require significant additional financing to acquire additional uranium/vanadium projects, continue with our exploration and begin pre-extraction activities on our existing uranium/vanadium projects.

Our operations are capital intensive and future capital expenditures are expected to be substantial. We will require significant additional financing to fund our operations, including acquiring additional uranium/vanadium projects, continuing with our exploration and beginning pre-extraction activities which include assaying, drilling, geological and geochemical analysis and mine construction costs. In the absence of such additional financing, we would not be able to fund our operations, including continuing with our exploration and pre-extraction activities, which may result in delays, curtailment or abandonment of any one or all of our uranium projects.

Uranium/vanadium exploration and pre-extraction programs and mining activities are inherently subject to numerous significant risks and uncertainties, and actual results may differ significantly from expectations or anticipated amounts. Furthermore, exploration programs conducted on our uranium/vanadium projects may not result in the establishment of ore bodies that contain commercially recoverable uranium/vanadium.

Uranium/vanadium exploration and pre-extraction programs and mining activities are inherently subject to numerous significant risks and uncertainties, many beyond our control, including, but not limited to: (i) unanticipated ground and water conditions and adverse claims to water rights; (ii) unusual or unexpected geological formations; (iii) metallurgical and other processing problems; (iv) the occurrence of unusual weather or operating conditions and other force majeure events; (v) lower than expected ore grades; (vi) industrial accidents; (vii) delays in the receipt of or failure to receive necessary government permits; (viii) delays in transportation; (ix) availability of contractors and labor; (x) government permit restrictions and regulation restrictions; (xi) unavailability of materials and equipment; and (xii) the failure of equipment or processes to operate in accordance with specifications or expectations. These risks and uncertainties could result in delays, reductions or stoppages in our mining activities; increased capital and/or extraction costs; damage to, or destruction of, our mineral projects, extraction facilities or other properties; personal injuries; environmental damage; monetary losses; and legal claims.

Success in uranium/vanadium exploration is dependent on many factors, including, without limitation, the experience and capabilities of a company’s management, the availability of geological expertise and the availability of sufficient funds to conduct the exploration program. Even if an exploration program is successful and commercially recoverable uranium/vanadium is established, it may take a number of years from the initial phases of drilling and identification of the mineralization until extraction is possible, during which time the economic feasibility of extraction may change such that the uranium ceases to be economically recoverable. Uranium/vanadium exploration is frequently non-productive due, for example, to poor exploration results or the inability to establish ore bodies that contain commercially recoverable uranium, in which case the uranium project may be abandoned and written-off. Furthermore, we will not be able to benefit from our exploration efforts and recover the expenditures that we incur on our exploration programs if we do not establish ore bodies that contain commercially recoverable uranium/vanadium and develop these uranium/vanadium projects into profitable mining activities, and there is no assurance that we will be successful in doing so for any of our uranium/vanadium projects.

8

Whether an ore body contains commercially recoverable uranium/vanadium depends on many factors including, without limitation: (i) the particular attributes, including material changes to those attributes, of the ore body such as size, grade, recovery rates and proximity to infrastructure; (ii) the market price of uranium, which may be volatile; and (iii) government regulations and regulatory requirements including, without limitation, those relating to environmental protection, permitting and land use, taxes, land tenure and transportation.

We have established the existence of mineralized materials for uranium properties. We have not established proven or probable reserves, as defined by the SEC under Industry Guide 7, through the completion of a “final” or “bankable” feasibility study for any of our uranium properties. Furthermore, we have no current plans to establish proven or probable reserves for any of our uranium properties as it doesn’t serve a business purpose at the present time.

We may not be able to realize anticipated benefits of the Kinetic Separation process due to uncertainties associated with that process.

In order to utilize Kinetic Separation to process uranium/vanadium bearing ore there are uncertainties that must be overcome which include the uncertainty as to the evolution of the regulatory framework and technological considerations. Either may cause delays in start-up, and/or increase costs, and may preclude the realization of the anticipated benefits of the Kinetic Separation process. Use of Kinetic Separation represents an additional processing step, requiring additional equipment, support, material handling and a potential increase in water usage requirements.

We do not insure against all of the risks we face in our operations.

In general, where coverage is available and not prohibitively expensive relative to the perceived risk, we will maintain insurance against such risk, subject to exclusions and limitations. We currently maintain insurance against certain risks including securities and general commercial liability claims and certain physical assets used in our operations, subject to exclusions and limitations; however, we do not maintain insurance to cover all of the potential risks and hazards associated with our operations. We may be subject to liability for environmental, pollution or other hazards associated with our exploration, pre-extraction and extraction activities, which we may not be insured against, which may exceed the limits of our insurance coverage or which we may elect not to insure against because of high premiums or other reasons. Furthermore, we cannot provide assurance that any insurance coverage we currently have will continue to be available at reasonable premiums or that such insurance will adequately cover any resulting liability.

Our inability to obtain financial surety would threaten our ability to continue in business.

Future financial surety requirements to comply with federal and state environmental and remediation requirements and to secure necessary licenses and approvals may increase significantly as future development and production occurs at certain of our sites in the United States. The amount of the financial surety for each producing property is subject to annual review and revision by regulators. We expect that the issuer of the financial surety instruments will require us to provide cash collateral for a significant amount of the face amount of the bond to secure the obligation. In the event we are not able to raise, secure or generate sufficient funds necessary to satisfy these requirements, we will be unable to develop our sites and bring them into production, which inability will have a material adverse impact on our business and may negatively affect our ability to continue to operate.

Acquisitions that we may make from time to time could have an adverse impact on us.

From time to time, we examine opportunities to acquire additional mining assets and businesses. Any acquisition that we may choose to complete may be of a significant size, may change the scale of our business and operations, and may expose us to new geographic, political, operating, financial and geological risks. Our success in our acquisition activities depends on our ability to identify suitable acquisition candidates, negotiate acceptable terms for any such acquisition, and integrate the acquired operations successfully with those of our Company. Any acquisitions would be accompanied by risks which could have a material adverse effect on our business. For example, there may be a significant change in commodity prices after we have committed to complete the transaction and established the purchase price or exchange ratio; a material ore body may prove to be below expectations; we may have difficulty integrating and assimilating the operations and personnel of any acquired companies, realizing anticipated synergies and maximizing the financial and strategic position of the combined enterprise, and maintaining uniform standards, policies and controls across the organization; the integration of the acquired business or assets may disrupt our ongoing business and our relationships with employees, customers, suppliers and contractors; and the acquired business or assets may have unknown liabilities which may be significant. In the event that we choose to raise debt capital to finance any such acquisition, our leverage will be increased. If we choose to use equity as consideration for such acquisition, existing shareholders may suffer dilution. Alternatively, we may choose to finance any such acquisition with our existing resources. There can be no assurance that we would be successful in overcoming these risks or any other problems encountered in connection with such acquisitions.

9

The uranium industry is subject to numerous stringent laws, regulations and standards, including environmental protection laws and regulations. If any changes occur that would make these laws, regulations and standards more stringent, it may require capital outlays in excess of those anticipated or cause substantial delays, which would have a material adverse effect on our operations.

Uranium exploration and pre-extraction programs and mining activities are subject to numerous stringent laws, regulations and standards at the federal, state, and local levels governing permitting, pre-extraction, extraction, exports, taxes, labor standards, occupational health, waste disposal, protection and reclamation of the environment, protection of endangered and protected species, mine safety, hazardous substances and other matters. Our compliance with these requirements requires significant financial and personnel resources.

The laws, regulations, policies or current administrative practices of any government body, organization or regulatory agency in the United States or any other applicable jurisdiction, may change or be applied or interpreted in a manner which may also have a material adverse effect on our operations. The actions, policies or regulations, or changes thereto, of any government body or regulatory agency or special interest group, may also have a material adverse effect on our operations.

Uranium exploration and pre-extraction programs and mining activities are subject to stringent environmental protection laws and regulations at the federal, state, and local levels. These laws and regulations, which include permitting and reclamation requirements, regulate emissions, water storage and discharges and disposal of hazardous wastes. Uranium mining activities are also subject to laws and regulations which seek to maintain health and safety standards by regulating the design and use of mining methods. Various permits from governmental and regulatory bodies are required for mining to commence or continue, and no assurance can be provided that required permits will be received in a timely manner.

Our compliance costs including the posting of surety bonds associated with environmental protection laws and regulations and health and safety standards have been significant to date, and are expected to increase in scale and scope as we expand our operations in the future. Furthermore, environmental protection laws and regulations may become more stringent in the future, and compliance with such changes may require capital outlays in excess of those anticipated or cause substantial delays, which would have a material adverse effect on our operations.

To the best of our knowledge, our operations are in compliance, in all material respects, with all applicable laws, regulations and standards. We may not be able or may elect not to insure against the risk of liability for violations of such laws, regulations and standards, due to high insurance premiums or other reasons. Where coverage is available and not prohibitively expensive relative to the perceived risk, we will maintain insurance against such risk, subject to exclusions and limitations. However, we cannot provide any assurance that such insurance will continue to be available at reasonable premiums or that such insurance will be adequate to cover any resulting liability.

We may not be able to obtain, maintain or amend rights, authorizations, licenses, permits or consents required for our operations.

Our exploration and mining activities are dependent upon the grant of appropriate rights, authorizations, licenses, permits and consents, as well as continuation and amendment of these rights, authorizations, licenses, permits and consents already granted, which may be granted for a defined period of time, or may not be granted or may be withdrawn or made subject to limitations. There can be no assurance that all necessary rights, authorizations, licenses, permits and consents will be granted to us, or that authorizations, licenses, permits and consents already granted will not be withdrawn or made subject to limitations.

Closure and remediation costs for environmental liabilities may exceed the provisions we have made.

Natural resource companies are required to close their operations and rehabilitate the lands in accordance with a variety of environmental laws and regulations. Estimates of the total ultimate closure and rehabilitation costs for uranium operations are significant and based principally on current legal and regulatory requirements and closure plans that may change materially. Any underestimated or unanticipated rehabilitation costs could materially affect our financial position, results of operations and cash flows. Environmental liabilities are accrued when they become known, are probable and can be reasonably estimated. Whenever a previously unrecognized remediation liability becomes known, or a previously estimated reclamation cost is increased, the amount of that liability and additional cost will be recorded at that time and could materially reduce our consolidated net income in the related period.

10

The laws and regulations governing closure and remediation in a particular jurisdiction are subject to review at any time and may be amended to impose additional requirements and conditions which may cause our provisions for environmental liabilities to be underestimated and could materially affect our financial position or results of operations.

Major nuclear incidents may have adverse effects on the nuclear and uranium industries.

The

nuclear incident that occurred in Japan in March 2011 had significant and adverse effects on both the nuclear and uranium industries.

If another nuclear incident were to occur, it may have further adverse effects for both industries. Public opinion of nuclear

power as a source of electricity generation may be adversely affected, which may cause governments of certain countries to further

increase regulation for the nuclear industry, reduce or abandon current reliance on nuclear power or reduce or abandon existing

plans for nuclear power expansion. Any one of these occurrences has the potential to reduce current and/or future demand for nuclear

power, resulting in lower demand for uranium and lower market prices for uranium, adversely affecting the Company’s operations

and prospects. Furthermore, the growth of the nuclear and uranium industries is dependent on continuing and growing public support

of nuclear power as a viable source of electricity generation.

The marketability of uranium concentrates will be affected by numerous factors beyond our control which may result in our inability to receive an adequate return on our invested capital.

The marketability of uranium concentrates extracted by us will be affected by numerous factors beyond our control. These factors include macroeconomic factors, fluctuations in the market price of uranium, governmental regulations, land tenure and use, regulations concerning the importing and exporting of uranium and environmental protection regulations. The future effects of these factors cannot be accurately predicted, but any one or a combination of these factors may result in our inability to receive an adequate return on our invested capital.

The only significant market for uranium is nuclear power plants world-wide, and there are a limited number of customers.

We are dependent on a limited number of electric utilities that buy uranium for nuclear power plants. Because of the limited market for uranium, a reduction in purchases of newly produced uranium by electric utilities for any reason (such as plant closings) would adversely affect the viability of our business.

The price of alternative energy sources affects the demand for and price of uranium.

The attractiveness of uranium as an alternative fuel to generate electricity may be dependent on the relative prices of oil, gas, wind, solar, coal and hydro-electricity and the possibility of developing other low-cost sources of energy. If the prices of alternative energy sources decrease or new low-cost alternative energy sources are developed, the demand for uranium could decrease, which may result in a decrease in the price of uranium.

The title to our mineral property interests may be challenged.

Although we have taken reasonable measures to ensure proper title to our interests in mineral properties and other assets, there is no guarantee that the title to any of such interests will not be challenged. No assurance can be given that we will be able to secure the grant or the renewal of existing mineral rights and tenures on terms satisfactory to us, or that governments in the jurisdictions in which we operate will not revoke or significantly alter such rights or tenures or that such rights or tenures will not be challenged or impugned by third parties, including local governments, aboriginal peoples or other claimants. Our mineral properties may be subject to prior unregistered agreements, transfers or claims, and title may be affected by, among other things, undetected defects. A successful challenge to the precise area and location of our claims could result in us being unable to operate on our properties as permitted or being unable to enforce our rights with respect to our properties.

Due to the nature of our business, we may be subject to legal proceedings which may divert management’s time and attention from our business and result in substantial damage awards.

Due to the nature of our business, we may be subject to numerous regulatory investigations, securities claims, civil claims, lawsuits and other proceedings in the ordinary course of our business. The outcome of these lawsuits is uncertain and subject to inherent uncertainties, and the actual costs to be incurred will depend upon many unknown factors. We may be forced to expend significant resources in the defense of these suits, and we may not prevail. Defending against these and other lawsuits in the future may not only require us to incur significant legal fees and expenses, but may become time-consuming for us and detract from our ability to fully focus our internal resources on our business activities. The results of any legal proceeding cannot be predicted with certainty due to the uncertainty inherent in litigation, the difficulty of predicting decisions of regulators, judges and juries and the possibility that decisions may be reversed on appeal. There can be no assurances that these matters will not have a material adverse effect on our business, financial position or operating results.

11

Competition from better-capitalized companies affects prices and our ability to acquire both properties and personnel.

There is global competition for uranium properties, capital, customers and the employment and retention of qualified personnel. In the production and marketing of uranium, there are a number of producing entities, some of which are government controlled and all of which are significantly larger and better capitalized than we are. Many of these organizations also have substantially greater financial, technical, manufacturing and distribution resources than we have.

Our future uranium production will also compete with uranium recovered from the de-enrichment of highly enriched uranium obtained from the dismantling of United States and Russian nuclear weapons and imports to the United States of uranium from the former Soviet Union and from the sale of uranium inventory held by the United States Department of Energy. In addition, there are numerous entities in the market that compete with us for properties and are attempting to become licensed to operate ISR and/or underground mining facilities. If we are unable to successfully compete for properties, capital, customers or employees or with alternative uranium sources, it could have a materially adverse effect on our results of operations.

Because we have limited capital, inherent mining risks pose a significant threat to us compared with our larger competitors.

Because we have limited capital we may be unable to withstand significant losses that can result from inherent risks associated with mining, including environmental hazards, industrial accidents, flooding, earthquake, interruptions due to weather conditions and other acts of nature which larger competitors could withstand. Such risks could result in damage to or destruction of our infrastructure and production facilities, as well as to adjacent properties, personal injury, environmental damage and processing and production delays, causing monetary losses and possible legal liability. Our business could be harmed if we lose the services of our key personnel.

Our business and mineral exploration programs depend upon our ability to employ the services of geologists, engineers and other experts. In operating our business and in order to continue our programs, we compete for the services of professionals with other mineral exploration companies and businesses. In addition, several entities have expressed an interest in hiring certain of our employees. Our ability to maintain and expand our business and continue our exploration programs may be impaired if we are unable to continue to employ or engage those parties currently providing services and expertise to us or identify and engage other qualified personnel to do so in their place. To retain key employees, we may face increased compensation costs, including potential new stock incentive grants and there can be no assurance that the incentive measures we implement will be successful in helping us retain our key personnel.

If we fail to maintain proper and effective internal controls, our ability to produce accurate and timely consolidated financial statements could be impaired, which could harm our operating results, our ability to operate our business and investors’ views of us.

Ensuring that we have adequate internal financial and accounting controls and procedures in place so that we can produce accurate consolidated financial statements on a timely basis is a costly and time-consuming effort that will need to be evaluated frequently. Section 404 of the Sarbanes-Oxley Act requires public companies to conduct an annual review and evaluation of their internal controls. The Company is in the process of reviewing its internal control over financial reporting in the interest of complying with Section 404 of the Sarbanes-Oxley Act. Our failure to maintain the effectiveness of our internal controls in accordance with the requirements of the Sarbanes-Oxley Act could have a material adverse effect on our business. We could lose investor confidence in the accuracy and completeness of our financial reports, which could have an adverse effect on the price of our common shares.

The Company may be subject to certain tax consequences in its business, which may increase the cost of doing business.

The Company may not be able to structure its acquisitions to result in tax-free treatment for the companies or their stockholders, which could deter third parties from entering into certain business combinations with the Company or result in being taxed on consideration received in a transaction.

The COVID-19 coronavirus could adversely impact our business, including our mine development plans.

In December 2019, a novel strain of coronavirus, COVID-19, was reported to have surfaced in Wuhan, China. Since then, the COVID-19 coronavirus has spread to multiple countries, including the United States. As the COVID-19 coronavirus continues to spread in the United States, we may experience disruptions that could severely impact our business, including:

| ● | interruption of key mining activities due to limitations on travel, gathering, or business operations imposed or recommended by federal or state governments, employers and others. |

| ● | limitations in employee resources, including because of sickness of employees or their families or the desire of employees to avoid contact with large groups of people. |

| · | delays in financial reporting and filings due to the impact of mitigation efforts on staff and service providers |

12

| ● | changes in local regulations as part of a response to the COVID-19 coronavirus outbreak which may require us to change the ways in which mining is conducted, which may result in unexpected costs. |

| ● |

delays in necessary interactions with regulators and other important agencies and contractors due to limitations in employee resources or new procedures due to limitations imposed by COVID-19. | |

| ● | reduction in the global demand for uranium and vanadium due to reduced production levels in the primary applications of uranium and vanadium. Restrictions for COVID-19 could cause a decline in energy consumption or indirectly reduced oil prices could lessen the demand for nuclear power. | |

| ● | COVID-19 has globally resulted in uranium mine closures that have taken substantial uranium supply offline and increased the spot price of uranium to date during this crisis, there is no guarantee that this relationship will continue as the COVID-19 crisis is ongoing and the dynamic of the mine closure/spot price relationship may change. |

The global outbreak of the COVID-19 coronavirus continues to rapidly evolve. The extent to which the COVID-19 coronavirus may impact our business will depend on future developments, which are highly uncertain and cannot be predicted with confidence, such as the ultimate geographic spread of the disease, the duration of the outbreak, travel restrictions and social distancing in the United States and other countries, business closures or business disruptions and the effectiveness of actions taken in the United States and other countries to contain and treat the disease.

Risks Related to Our Stock

If we are unable to raise additional capital, our business may fail and stockholders may lose their entire investment.

We had $2,084,782 and $909,865 in cash at December 31, 2019 and December 31, 2018, respectively. There can be no assurance that we will be able to obtain additional capital after we exhaust our current cash. To the extent that we raise additional capital through the sale of equity or convertible debt securities, the issuance of such securities would likely result in substantial dilution to existing stockholders. If we borrow money, we will have to pay interest and may also have to agree to restrictions that limit our operating flexibility.

If additional capital is not available in sufficient amounts or on a timely basis, we will experience liquidity problems, and we could face the need to significantly curtail current operations, change our planned business strategies and pursue other remedial measures. Any curtailment of business operations would have a material negative effect on operating results, the value of our outstanding stock is likely to fall, and our business may fail, causing our stockholders to lose their entire investment.

Shareholders could be diluted if we were to use common shares to raise capital.

We may need to seek additional capital to carry our business plan. This financing could involve one or more types of securities including common shares, convertible debt or warrants to acquire common shares. These securities could be issued at or below the then prevailing market price for our common shares. Any issuance of additional common shares could be dilutive to existing stockholders and could adversely affect the market price of our common shares.

The Company’s common shares may be traded infrequently and in low volumes, which may negatively affect the ability to sell shares.

The Company’s common shares may trade infrequently and in low volumes on both the CSE and OTCQX, meaning that the number of persons interested in purchasing our common shares at or near bid prices at any given time may be relatively small or non-existent. This situation may be attributable to a number of factors, including the fact that we are a small company that is relatively unknown to stock analysts, stock brokers, institutional investors and others in the investment community who can generate or influence sales volume, and that even if we came to the attention of such institutionally oriented persons, they tend to be risk-averse in this environment and would be reluctant to follow an early stage company such as ours or purchase or recommend the purchase of our shares until such time as we became more advanced and viable. As a consequence, there may be periods of several days or more when trading activity in the Company’s shares is minimal or non-existent, as compared to a seasoned issuer which has a large and steady volume of trading activity that will generally support continuous sales without an adverse effect on share price. The Company cannot give you any assurance that a broader or more active public trading market for our common shares will develop or be sustained. Due to these conditions, we can give you no assurance that you will be able to sell your shares at or near bid prices or at all if you need money or otherwise desire to liquidate your shares. Further, institutional and other investors may have investment guidelines that restrict or prohibit investing in securities traded in the over-the-counter market. These factors may have an adverse impact on the trading and price of our securities, and could result in the loss by investors of all or part of their investment.

The Company’s common share price may be volatile.

The future trading price of the Company’s common shares may be volatile and may fluctuate substantially. The price of the common shares may be higher or lower than the price you pay for your shares, depending on many factors, some of which are beyond the Company’s control and may not be directly related to its operating performance. These factors include the following:

| ● | price and volume fluctuations in the overall stock market from time to time; |

| ● | significant volatility in the market price and trading volume of securities of mineral exploration and mining companies; |

13

| ● | changes in government regulations or regulatory policies with respect to mineral exploration and mining companies or in the status of our regulatory approvals; |

| ● | actual or anticipated changes in earnings or fluctuations in operating results; |