Attached files

UNITED

STATES

SECURITIES AND

EXCHANGE COMMISSION

Washington, DC

20549

FORM

10-K

☑ ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

FOR THE YEAR ENDED: DECEMBER 31,

2019

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number

000-53088

HIREQUEST,

INC.

(Exact name of registrant as

specified in its charter)

|

Delaware

|

|

91-2079472

|

|

(State of

incorporation or organization)

|

|

(I.R.S.

Employer Identification no.)

|

|

|

|

|

|

111 Springhall Drive, Goose Creek, SC, 29445

|

||

|

(Address of

principal executive offices) (Zip code)

|

||

|

|

|

|

|

Registrant’s telephone number, including

area code: (843)

723-7400

|

||

Securities

registered pursuant to Section 12(b) of the Act:

|

Common Stock,

$0.001 par value

|

|

HQI

|

|

The Nasdaq Stock

Market LLC

|

|

Title of each class

|

|

Trading symbol(s)

|

|

Name of each exchange on which

registered

|

Securities registered pursuant to section 12(g) of

the Act: None

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the

Securities Act. Yes ☐ No

☑

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of

the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1)

has filed all reports required to be filed by Section 13 or 15(d)

of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required

to file such reports) and (2) has been subject to such filing

requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has

submitted electronically every Interactive Data File required to be

submitted pursuant to Rule 405 of Regulation S-T (§232.405 of

this chapter) during the preceding 12 months (or for such shorter

period that the registrant was required to submit such

files). Yes ☑ No ☐

Indicate by check mark whether the

Registrant is a large accelerated filer ☐ , an accelerated filer ☐ , a non-accelerated filer ☑ , a smaller

reporting company ☑ , or an emerging

growth company ☐ (as defined in Rule

12b-2 of the Exchange Act).

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 13(a) of the Exchange

Act. ☐

Indicate by check mark whether the Registrant is a

shell company (as defined in Rule 12b-2 of the Exchange

Act). Yes ☐ No ☑

The aggregate

market value of the voting and non-voting common equity held by

non-affiliates computed by reference to the price at which the

common equity was last sold, or the average bid and asked price of

such common equity, as of the last business day of the

Registrant’s most recently completed second fiscal quarter

was $5,737,000.

Number

of shares of issuer's common stock outstanding at

March 27, 2020 was 13,536,472.

Portions of the

Registrant’s definitive proxy statement for the annual

meeting of stockholders to be filed pursuant to Regulation 14A or

an amendment to this Annual Report on Form 10-K are incorporated by

reference into Items 10, 11, 12, 13, and 14 of Part III of this

report. The Registrant will file its definitive proxy statement or

an amendment to this Annual Report on Form 10-K with the Securities

and Exchange Commission within 120 days of December 31,

2019.

HireQuest,

Inc.

2019 Annual

Report on Form 10-K

Table of

Contents

|

|

|

Page

|

|

PART

I

|

||

|

|

|

|

|

PART

II

|

||

|

|

|

|

|

PART

III

|

||

|

|

|

|

|

PART

IV

|

||

|

|

||

2

Special Note

Regarding Forward-Looking Statements

This Annual

Report on Form 10-K for the year ended December 31, 2019 and other

documents incorporated herein by reference include, and our

officers and other representatives may sometimes make or provide

certain estimates and other forward-looking statements within the

meaning of the safe harbor provisions of the U.S. Private

Securities Litigation Reform Act of 1995, Section 27A of the

Securities Act, and Section 21E of the Exchange Act, including,

among others, statements with respect to future revenue, franchise

sales, system-wide sales, and the growth thereof; the impact of any global

pandemic including the novel coronavirus disease

("COVID-19"); operating results; anticipated benefits of the

merger with Command Center, Inc., or the conversion to the

franchise model; intended office openings; expectations of the

effect on our financial condition of claims and litigation;

strategies for customer retention and growth; strategies for risk

management; and all other statements that are not purely historical

and that may constitute statements of future expectations.

Forward-looking statements can be identified by words such as:

“anticipate,” “intend,” “plan,”

“goal,” “seek,” “believe,”

“project,” “estimate,”

“expect,” “strategy,” “future,”

“likely,” “may,” “should,”

“will,” and similar references to future

periods.

While we

believe these statements are accurate, forward-looking statements

are not historical facts and are inherently uncertain. They are

based only on our current beliefs, expectations, and assumptions

regarding the future of our business, future plans and strategies,

projections, anticipated events and trends, the economy, and other

future conditions. We cannot assure you that these expectations

will occur, and our actual results may be significantly different.

Therefore, you should not place undue reliance on these

forward-looking statements. Important factors that may cause actual

results to differ materially from those contemplated in any

forward-looking statements made by us include the following: the

level of demand and financial performance of the temporary staffing

industry; the financial performance of our franchisees; changes in

customer demand; the extent to which we are successful in gaining

new long-term relationships with customers or retaining existing

ones, and the level of service failures that could lead customers

to use competitors’ services; significant investigative or

legal proceedings including, without limitation, those brought

about by the existing regulatory environment or changes in the

regulations governing the temporary staffing industry and those

arising from the action or inaction of our franchisees and

temporary employees; strategic actions, including acquisitions and

dispositions and our success in integrating acquired businesses

including, without limitation, successful integration following the

merger with Command Center, Inc.; disruptions to our technology

network including computer systems and software; natural events

such as severe weather, fires, floods, and earthquakes, or man-made

or other disruptions of our operating systems; and the factors

discussed in the “Risk Factors” section and elsewhere

in this Annual Report on Form 10-K.

Any

forward-looking statement made by us in this Annual Report on Form

10-K is based only on information currently available to us and

speaks only as of the date on which it is made. The Company

disclaims any obligation to update or revise any forward-looking

statement, whether written or oral, that may be made from time to

time, based on the occurrence of future events, the receipt of new

information, or otherwise, except as required by law.

PART

I

Item 1. Business

Our

Company

HireQuest, Inc. (collectively with its subsidiaries, the

“Company,” “we,” “us,” or

“our”) is a Delaware corporation originally organized

in Washington as Command Staffing, LLC in 2002. In 2005, Temporary

Financial Services, Inc., a public company, acquired the assets of

Command Staffing, LLC, and the combined entity changed its name to

Command Center, Inc. On September 11, 2019, Command Center, Inc.

reincorporated in Delaware and changed its name to Hire Quest, Inc.

following its acquisition of Hire Quest Holdings, LLC (“Hire

Quest Holdings,” and together with its subsidiary, Hire

Quest, LLC, “Legacy HQ”). This acquisition is

sometimes referred to as the “Merger.” Hire Quest, LLC

was formed as a Florida limited liability company in 2002. Hire

Quest Holdings, LLC was formed as a Florida limited liability

company in 2017.

Our common stock trades on the

Nasdaq Market under the symbol “HQI.” Command Center

previously traded on the Nasdaq Market under the symbol

"CCNI."

3

More information about the Merger

and other recent developments can be found in Part II, Item 7. Management’s Discussion and

Analysis of Financial Conditions and Results of Operations of this

Annual Report on Form 10-K under the heading “Recent

Developments” which is incorporated herein by

reference.

More information about us may be

found at www.hirequest.com. The information on our website is not

incorporated by reference in this Annual Report on Form

10-K.

Our

Model

We are a

nationwide franchisor of temporary staffing offices providing

on-demand labor solutions primarily in the light industrial and

blue-collar segments of the staffing industry. We provide our

customers with seamless access to a contingent workforce whenever

they need it. Our daily dispatch model, in which we match temporary

employees with openings every day, allows us to be responsive to

our customers’ dynamic needs. Our flexible staffing solutions

permit our customers to focus on their underlying operations and to

expand or contract their workforce quickly to meet fluctuating

demands. We assist our employees in arranging transportation

amongst themselves to ensure timely arrival of the right number of

employees at the scheduled starting time. In addition, we pay our

employees daily which attracts workers who cannot wait up to three

weeks for their first paycheck under a traditional

model.

Our revenue,

which is largely comprised of royalty fees and interest on overdue

accounts that we charge our franchisees, was $16.2 million in 2019.

Our system-wide sales, which we define as sales at all office

locations, whether owned and operated by us or by our franchisees,

were $241.6 million. System-wide sales for 2019 include $227.7

million attributable to franchisee-owned offices and $13.9 million

attributable to offices we owned for a portion of the year before

selling them to franchisees. Currently all of our offices are

franchised. We employed 67,000 temporary employees in 2019. At

December 31, 2019, we had 147 franchisee-owned offices operating in

32 states and the District of Columbia.

Our franchisees

operate through one of our two owned brands: HireQuest Direct and

HireQuest. HireQuest Direct, which represents the great majority of

our franchises, focuses on daily-work-daily-pay jobs in the

construction and light industrial segments. HireQuest, focuses on

longer-term staffing positions in the light industrial and

administrative arenas.

On a

net basis, we added 50 offices in 2019 (opening 60 and closing 10),

most of them via the July 2019 Merger. We provide incentives to our

existing franchisees, including assistance with start-up funding

and acquisition costs, to encourage them to open in new markets.

While staffing industry growth has outpaced overall economic and

employment growth, the industry still employs only 2% of the United

States’ non-farm workforce.1 We believe

that the low percentage of the total workforce that is currently

contingent, when combined with potential shifts towards a more

contingent workforce in the overall economy, provides an

opportunity for future organic growth.

Our

differentiated services are driven by two key

elements:

●

Local

ownership and dedicated responsiveness. Our offices are franchisee-owned. We believe that

ownership at the local level – where the vast majority of

customer communication occurs – allows our organization to be

agile and responsive to customer needs. Since our franchisees have

personal financial stakes directly tied to the success of their

offices, our customers interface with owners who are incentivized

to deliver excellent customer service and resolve issues

efficiently. Responsiveness promotes customer retention. Each

franchisee is incentivized to acquire new business to help grow his

or her personal income.

●

Direct

dispatch from our offices. The majority of our employees are dispatched from

our offices every day. This allows our franchisees and their staff

to qualify the employees for work, provide them with any necessary

personal protective equipment, assist our employees in arranging

transportation amongst themselves, and ensure we deliver the right

number of qualified individuals at the right time. We believe that

employee dispatch from franchise offices increases consistency as

our employees are sent to a particular jobsite without having to

rely on potentially less reliable means of verification, such as

telephone calls. Once we and our customers have developed a rapport

with particular employees, we will sometimes dispatch these

employees directly to a customer location.

4

Our Industry

Temporary Staffing

According to the American Staffing Association,

the staffing and recruiting industry employed approximately 16

million people and accounted for $167 billion of sales in

2018.2 We focus

primarily on the largest segment, light industrial and blue collar

work, which accounts for roughly 37% of the temporary staffing

industry.3

The on-demand labor industry has

developed based on business needs for flexible staffing solutions.

The industry provides contingent workforce solutions as an

alternative to the costs and efforts that are required for

recruiting, hiring and managing permanent employees. Many of the

customers we target operate in a cyclical production environment

and find it difficult to staff according to their changing business

requirements. Companies also desire a way to maintain consistent

staffing levels when full-time employees are absent due to illness,

vacation, or unplanned terminations. On-demand labor offers

customers the opportunity to respond immediately to changes in

staffing needs, to reduce the costs associated with recruiting and

interviewing, to eliminate unemployment and workers’

compensation exposure, and to draw from a larger pool of potential

employees. We have found that staffing firms provide particular

value in assisting customers with filling mundane or repetitive

jobs, high turnover positions, staffing for project specific needs,

and filling other short duration positions such as special events,

disaster recovery, and seasonal jobs.

Historically,

our business has been bolstered by declining unemployment rates as

our customers find it more difficult and more expensive to recruit,

interview, hire, and train qualified staff. As employers look for

alternatives to combat these increasing costs and administrative

burdens, opportunities arise for the temporary staffing industry.

In addition, worker attitudes have changed from one which idealized

extended tenure with a single employer to one which is more open to

temporary or transient employment. This shift has increased the

availability of temporary workers in the economy as a

whole.

Government Regulation

As a large

employer, we are subject to a significant number of employment laws

at the state, federal, and local levels. We are required to comply

with all applicable federal and state laws and regulations relating

to employment, including verification of eligibility for

employment, occupational safety and health provisions, wage and

hour requirements, employment insurance, and laws relating to equal

opportunity employment. In addition to federal and state laws

and regulations, many counties and cities have become active in

regulating various aspects of employment, including minimum wages,

paid sick leave, retirement savings programs, transportation

benefits, application forms and background checks, and required

notices to employees, among others. Regulatory compliance creates a

barrier to entry to many would-be smaller competitors as they

cannot profitably comply with the administrative burden of new and

voluminous regulations.

In addition,

fourteen states and the Federal Trade Commission impose pre-sale

franchise registration or disclosure requirements on franchisors. A

number of states also regulate substantive aspects of our

relationship with our franchisees such as termination, nonrenewal,

transfer, no-poach and non-competition provisions, discrimination

among franchisees, and other aspects of the relationships between

and with franchisees. Additional legislation, which we cannot

predict, could expand these requirements imposed on

us.

Working Capital Practices

Our working capital requirements,

and the working capital requirements of our competition, are driven

largely by temporary employee payroll and accounts receivable from

customers. Since receipts lag behind employee pay – which is

typically daily or weekly – our working capital requirements

increase as system-wide sales increase.

We obtain our

working capital largely from cash produced by our daily operations.

In addition, we have obtained a line of credit from Branch Bank

& Trust Company, now called Truist Bank ("BB&T"), for $30

million with a $15 million sublimit for letters of credit. In our

experience, it is common for staffing firms to utilize cash

produced from operations along with credit facilities to finance

working capital requirements.

2 Id.

3 American Staffing Association,

Staffing Industry

Statistics (published May 2019). Available at: https://americanstaffing.net/staffing-research-data/fact-sheets-analysis-staffing-industry-trends/staffing-industry-statistics/#tab:tbs_nav_item_0

5

Our Competitive Strengths

We attribute

our success to the following strengths:

●

Nationwide

footprint with differentiated business model. We believe we are one of the largest providers

of on-demand temporary staffing solutions in the light industrial

and blue-collar segments of the staffing industry measured by

number of office locations. Our nationwide footprint allows us to

compete for national account relationships when our competitors

that are local or regional operators are simply too small. Our size

also allows us to obtain favorable terms on our workers’

compensation insurance program. Our franchise model has many

advantages as well. Most of our competitors utilize a company-owned

office model in which the management of day-to-day interactions

with customers is handled by individuals who do not have the

incentives to succeed that comes only from ownership. On the other

hand, our offices are owned and operated by franchisees whose

personal financial success is directly tied to the success or

failure of their local franchised office. The company-owned model

typically requires significant investment in middle management. We

largely avoid this expense because our franchisees are independent

business owners responsible for their own financial

well-being.

●

A franchise

system with expansion capabilities. We incentivize our franchisees to expand their own

businesses through our Franchise Expansion Incentive Program. Under

this program, we offer assistance overcoming the startup costs of

an office in a new metropolitan area by providing our existing

franchisees with credits on the royalty fees they pay in their

existing offices. Under certain circumstances, we will provide

assistance in acquisition funding or financing. In addition, our

Risk Management Incentive Program allows us to reward franchisees

who are successful in keeping their workers' compensation loss

ratios below certain thresholds by paying to franchisees an amount

equivalent to a portion of their premiums. We believe that this

incentivizes our franchisees to encourage workplace safety and

provides successful franchisees with capital to reinvest in or

expand their businesses.

●

Responsible

capital allocation with very little debt. As of December 31, 2019, we were debt free.

Financing our day-to-day needs with cash produced from operations

allows us to continue building cash reserves which we can use, in

addition to our line of credit with BB&T, to finance

significant transactions such as major reinvestments in our

business, strategic acquisitions, share buybacks, or stockholder

dividends, depending on the opportunities that present themselves.

Compared to company-owned offices, our franchise model allows us to

employ relatively fewer full-time staff at our corporate

headquarters decreasing the working capital needed for

operations.

Our Growth Strategy

We believe

there are opportunities to grow our business and brand. While the

onset of COVID-19 has made the economic future unpredictable, we

believe the following to be key components of our growth

strategy:

●

Continue to

grow the number of offices our franchisees

operate. We believe attractive

returns at the franchisee level should allow us to continue to

attract new franchisees and encourage our existing franchisees to

open new offices. In addition, we encourage our existing

franchisees to explore new potential markets through our Franchise

Expansion Incentive Program. When combined with the back-office

support that we provide franchisees, we believe we are poised to

expand into unserved or underserved markets like the Upper

Midwestern United States.

●

Capitalize

on our national footprint to grow same store and

system-wide sales. We

anticipate that our enhanced scale combined with our royalty

business model will contribute to growth in our access to and

profitability from national accounts. Traditionally, these larger

national accounts have the leverage to impose lower margins on

their temporary staffing providers. Our royalty-driven business

model, in which we earn a percentage of gross billings or payroll

funded regardless of margins, partially insulates stockholders from

margin volatility inherent in the ownership of the traditional

company-owned model for temporary staffing (although royalty

revenue from our HireQuest business line depends in part on the

gross margin of the franchisee). In addition, we have a strategic

relationship with Dock Square HQ, LLC, an entity with connections

at many of the largest users of temporary staffing in the country,

which increases the prospects of introduction to the decision

makers at these traditionally harder-to-reach potential

customers.

●

Increase

our brand awareness. As we

continue to develop new markets and to serve our existing markets,

we expect our brand to become more recognizable and a greater asset

to us in driving repeat customers, encouraging customers to expand

their use of our services across multiple markets, and increasing

new customer development.

6

Our

Offices

We had 147

offices located in 32 states and the District of Columbia as of

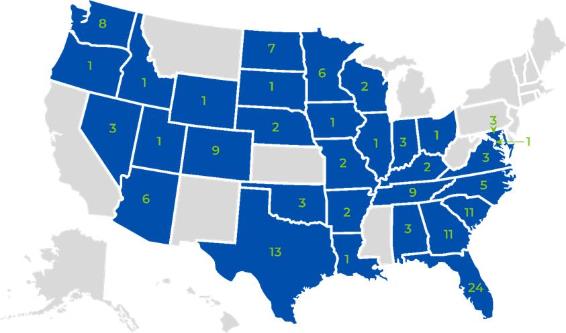

December 31, 2019. All were franchised. The map below provides the

number of offices we had in each state on December 31,

2019.

Number of Offices By State

December 31, 2019

We have a

strong concentration of offices in established and emerging regions

such as the Southeast, Texas, Colorado, and Washington. These

regional office concentrations allow for greater local brand

recognition and ease of oversight in those regions while we

continue to add offices in unserved and underserved communities.

These concentrations also allow us to better recognize local and

regional market trends and to centralize our administrative

functions. Since January 1, 2020, our franchisees have closed or

consolidated a small number of offices. These were largely

satellite offices or in markets already served by another office.

Accordingly, we do not expect these closures to materially impact

our revenue.

We encourage

our franchisees to locate in areas with access to public

transportation and major thoroughfares. Such locations facilitate

employee ease in reaching the office and increase their ability to

efficiently get to their work assignments. We also encourage our

franchisees to locate offices in areas between 1,000 and 1,500

square feet. Most of our offices are located near areas of

concentrated construction or major manufacturing and industrial

sites.

7

Our Franchise Program

Our

franchised offices are a key component of our success. We

urge our franchisees to customize their services according to the

unique opportunities and assets presented by each of their offices,

while also leveraging the overall size of the organization when

possible. This approach allows for each office to have a unique

blend of customers and emphases while also reducing overhead costs,

improving economies of scale, establishing procedural uniformity

and controls, and creating a predictable internal environment for

temporary employees.

A typical

franchised office location is managed by an owner with the

assistance of in-office personnel. Many offices hire business

development staff to help drive business to the offices. We provide

advice and guidance from our corporate headquarters.

Franchising Strategy

As of December

31, 2019, there were 147 franchised HireQuest and HireQuest Direct

offices operated by 57 franchisees. 29.3% of our franchisees owned

multiple offices. Our largest franchisee owned 13 offices, and

17.2% of our franchisees owned more than 5 offices. One individual

owned significant interests in 6 franchisees that operated 27

offices. 20 of our franchisees were Worlds Franchisees, those

franchisees that share common ownership with significant

stockholders, directors, and officers of the Company. The Worlds

Franchisees operated 57 offices as of December 31,

2019.

Our approach to

the franchise model creates what we believe to be superior

office-level economics. We finance many of the initial working

capital needs of our franchisees, including costs of new office

openings, through our ownership of franchisee accounts receivable

which we acquire through our franchise agreements. This is a

relatively inexpensive source of capital for our franchisees and

allows them to expand more freely. In addition, our Risk Management

Incentive Program lowers the effective cost of workers’

compensation insurance at the franchisee level – a

significant expense for many of our competitors. Through the Risk

Management Incentive Program, we pay franchisees who keep their

workers’ compensation loss ratios below a specific loss

threshold an amount equivalent to a portion of the premium they pay

for workers’ compensation coverage. We thereby eliminate for

our franchisees two of the strongest barriers to entry: financing

and workers’ compensation, and enable potentially higher

operating margins at the office level.

Franchise Agreements

For each

metropolitan area in which we have an office, we enter into a

franchise agreement with standard terms and conditions. Our

franchisees are granted the exclusive right to operate their chosen

brand, either HireQuest or HireQuest Direct, in their protected

territory. Typically, a protected territory corresponds with the

metropolitan statistical area where the office is located. We also

grant a franchisee a three-year right of first refusal on opening

an office using the other brand in that same protected

territory.

On December 31,

2019, our franchisees operated under 88 executed franchise

agreements. Our franchise agreements grant us the right to charge a

royalty fee of between 6% and 8%, depending on sales volume, on the

gross sales of our HireQuest Direct franchisees. For our HireQuest

business line, we charge a royalty fee of 4.5% of the payroll we

fund plus 18% of the gross margin for the territory.

Our typical

franchise agreement has a term of five years. We own the accounts

receivable of our franchisees pursuant to the franchise agreements.

We collect these and, after subtracting our royalty fees, payroll

and taxes funded for temporary employees, interest on overdue

accounts, and other fees and costs, we remit the remainder to our

franchisees. Our franchisees also gain access to our proprietary

software, HQ Webconnect, which we update regularly through a

dedicated staff of developers. Finally, in states that do not

require participation in a state-run policy, our franchisees gain

access to our workers’ compensation policy. By entering a

franchise agreement with us, our owner/operators remove some of the

most significant barriers to entry in our industry – payroll

funding and dedicated software, in addition to the workers’

compensation insurance premium benefits, and startup cost

assistance discussed above.

The table below

displays the number of franchise agreements scheduled to renew each

year:

|

Year

|

|

Renewals

|

|

2020

|

|

6

|

|

2021

|

|

9

|

|

2022

|

|

13

|

|

2023

|

|

12

|

|

2024

|

|

42

|

|

2029

|

|

6

|

The large number of renewals in 2024

arose because of the significant number of new franchisees we added

in 2019 as a result of the Merger.

Franchisees

receive initial and ongoing training in our proven methods of

operation. We provide support personnel on an as-needed basis to

our franchisees. We have a comprehensive brand standards manual

which explains our policies on key operational, financial, and

regulatory compliance issues. Under the franchise agreement,

beneficial owners of our franchisees guaranty all debts and

obligations of the franchise to us. Still, we have less control

over a franchisee’s operations than we would if we owned and

operated an office ourselves.

8

Our Employees

Temporary Employees

Our

temporary employees are also a key component of our success. They

perform the services we provide. Hire Quest, LLC, our

wholly-owned subsidiary, is the employer of record of all of our

temporary employees. In 2019, we

employed approximately 67,000 temporary employees and issued

approximately 1.4 million paychecks. The vast majority of these

payments were made via electronic paycard. We anticipate these

numbers to be larger in 2020 as we will operate for a full year

with the legacy Command Center offices and their corresponding

employees under the HireQuest umbrella. Given the nature of

temporary employment, it is difficult for us to determine the exact

number of full time employees on a given day, however, 451

temporary employees worked at least 2,000 hours in

2019.

These temporary employees served

thousands of customers, primarily in the construction,

industrial/manufacturing, warehousing, disaster recovery,

hospitality, and recycling/waste management industries. Our

customers range in size from small businesses to large corporate

enterprises. Most of our work assignments are short-term, and many

are filled on little advance notice from customers.

We continuously recruit temporary

staff so we can respond to customer needs quickly. We attract our

employees through various means, including in-person recruitment,

online resources, cell phone texting services, our large and

ever-growing internal database, job fairs, word-of-mouth,

advertisements, and a number of other methods. Our success is

dependent, in part, on our ability to attract and retain temporary

employees. To that end, we have implemented a robust health

insurance program giving qualifying temporary employees a list of

plans to choose from.

We remain committed to worker

safety. We regularly provide safety and skills training. We also

aggressively manage our workers' compensation program to identify

trends in injuries and limit our losses and exposure. Through our

Risk Management Incentive Program, our franchisees are incentivized

to ensure safe working environments and to achieve quick

resolutions of workers' compensation claims when they do

arise.

Corporate Employees

In addition to

the temporary staff, we employ approximately fifty corporate

employees through HQ LTS Corporation, our wholly-owned subsidiary.

Most of these individuals were employed at our corporate

headquarters in Goose Creek, South Carolina. The vast majority of

these employees are full-time. These employees provide back office

support, including financing, insurance, accounting, operations,

national sales, information technology, legal, and human resources

services to our franchisees and temporary employees.

Executive Officers

Information

about our executive officers follows:

|

Name

|

Age

|

Position

|

|

Richard

Hermanns

|

56

|

President, Chief

Executive Officer, and Chairman of the Board

|

|

John D.

McAnnar

|

37

|

Vice President,

Secretary, and General Counsel

|

|

Cory

Smith

|

43

|

Treasurer and Chief

Financial Officer

|

Richard Hermanns has

served as President and Chief Executive Officer, as well as

Chairman of the Board of Directors, of HireQuest, Inc. since the

Merger. Mr. Hermanns has nearly thirty years of experience in the

temporary staffing industry. He has served as Chief Executive

Officer and Secretary of Hire Quest, LLC, now a wholly-owned

subsidiary of HireQuest, Inc., since the company’s founding

in 2002. He served in the same capacities for predecessor entities

since July 1991. He is also Chairman of the Board of Directors and

President of Hirequest Insurance Company and has been since its

founding in 2010. He has been Chief Executive Officer of Hire Quest

Financial, LLC since its founding in 2006. Together with Edward

Jackson, Mr. Hermanns owns a majority stake in Bass Underwriters,

Inc., a large managing general insurance agent. Prior to founding

Hire Quest and its related entities, Mr. Hermanns served as Chief

Financial Officer of Outsource International, and as an Assistant

Vice President for NCNB National Bank (now Bank of America). Mr.

Hermanns obtained his Bachelor of Science degree in Economics and

Finance from Barry University, and his Masters of Business

Administration in Finance from the University of Southern

California. Mr. Hermanns is also active in the charitable realm.

Among his charitable pursuits, he founded the Higher Quest

Foundation, a non-profit organization dedicated to fighting global

hunger in a more sustainable way.

9

John D. McAnnar is

the General Counsel, Vice President, and Secretary of HireQuest,

Inc. He has served as General Counsel and Vice President for

HireQuest, LLC, now a wholly-owned subsidiary of HireQuest, Inc.,

since 2014. He manages a broad range of legal affairs in the

securities, employment, construction, insurance, finance, workers'

compensation, intellectual property, and other realms. He

previously served in the litigation departments of Carmody

MacDonald, P.C. and Armstrong Teasdale, LLP, where he focused on

complex commercial litigation, corporate, and employment law. Mr.

McAnnar is an adjunct professor at the Charleston School of Law. He

co-founded ArchCity Defenders, Inc., a non-profit organization in

St. Louis, Missouri, that led the push for change in

Missouri’s municipal court system following the Ferguson

unrest. For this work, Mr. McAnnar has received awards including

the National Legal Aid & Defenders Association New Leaders

in Advocacy Award, the Ina M. Boon Social Justice Award, and many

others. He served on St. Louis Mayor Francis Slay’s Vanguard

Cabinet and was a Commissioner on the St. Louis Developmental

Disability Resources Commission, a body that oversaw millions of

dollars of taxpayer funds. John graduated magna cum laude from the St. Louis

University School of Law, where he was inducted into the Alpha

Sigma Nu Jesuit Honor Society and the Order of the Woolsack. He

graduated cum

laude from the University of Pittsburgh with a Bachelor

of Arts degree.

Cory

Smith is the Treasurer and

Chief Financial Officer of HireQuest, Inc. He was appointed as

Command Center’s Chief Financial Officer on July 22, 2017.

Mr. Smith was previously employed by Command Center from 2010

through 2015, serving as Controller during the final two years of

his tenure. Before rejoining Command Center, he was employed

by Southeast Staffing beginning in 2015, where he served as the

Vice President of Finance. From 2005 to 2010, Mr. Smith worked as a

Certified Public Accountant, primarily performing attestation work.

Mr. Smith graduated cum laude from Lewis-Clark College with a Bachelor of

Science in Business Administration.

Our Competition

The manual labor sector of the

on-demand labor industry is largely fragmented and highly

competitive, with relatively low barriers to entry aside from

payroll funding, workers’ compensation premiums, and startup

costs. No single staffing company dominates the industry. Our

competitors range in size from small, local or regional operators

with five or fewer locations to large, multi-national companies

with hundreds of locations. Our strongest competition in any market

comes from companies that have established long-lasting

relationships with their clients. Competition in the industry tends

to track the overall strength of the economy and trends in

workforce flexibility. As the economy grows, the number of

competitors generally increases.

The primary competitive factors in

our market segments include price, the ability to timely provide

the requested workers, and success in meeting customer

expectations. Secondary factors include name recognition,

established reputation, and customer relationships. Businesses

operating in these segments of the on-demand labor industry require

access to significant working capital to pay temporary employees,

particularly in the spring and summer when seasonal staffing

requirements are highest, and to fund workers' compensation

premiums or claims. Lack of working capital can be a significant

impediment to growth for small, local, and regional on-demand labor

providers. A second barrier to entry is an affordable

workers’ compensation policy. Small entrants usually do not

have the scale necessary to secure a policy on terms similar to

ours. Regulatory compliance is becoming more burdensome,

particularly for smaller firms that cannot profitably comply with

the increasing number of federal, state, and local employment laws

and regulations.

We also face

increasing competition from “gig-economy” companies who

are attempting to monetize the temporary staffing industry through

smartphone applications. We believe these apps, however, will not

be a major source of successful competition in the commoditized

section of the labor spectrum where we specialize. The apps, which

operate on a broad-blast, first-come-first-served basis, often

result in too many or too few workers arriving at a jobsite as well

as other problems such as improper personal protective equipment or

employees arriving at a jobsite unwilling or unable to perform the

assigned tasks. In contrast, our direct dispatch model allows us to

screen employees’ readiness for work every day, assist with

arranging transportation to and from jobsites, and match employees

with company-provided personal protective equipment before they

leave the office.

10

Our Cyclicality and Seasonality

The temporary staffing industry has

historically been cyclical. Success tends to track the economy.

When our franchisees’ customers expect to have long-term

permanent needs, they tend to increase their use of temporary

employees. Our revenue tends to increase as the economy expands.

During economic downturns, our revenue tends to

diminish.

Some of the industries in which we

operate are subject to seasonal fluctuation. Many of the jobs

filled by temporary employees are outdoors and generally performed

during the warmer months of the year. As a result, activity

increases in the spring and continues at higher levels through the

summer, then begins to taper off during fall and through winter. In

addition, demand by industrial customers tends to slow after the

holiday season and pick up again in the third and fourth quarters

– peaking in the third quarter. Our exposure to seasonality

is tempered, in part, by our strong presence in the Southern United

States. Seasonal fluctuations are typically less pronounced in the

more temperate parts of the United States, where many of our

franchised offices are located. Fluctuations in seasonal business

affect financial performance from period to period. Severe weather

in a location for prolonged periods has the potential to impair

business within those geographies, given the outdoor nature of many

of its assignments. However, natural disasters also sometimes lead

to additional assignments in the disaster recovery

industry.

Our Intellectual Property

We own the

rights to all of our key trademarks including

“HireQuest,” “HireQuest Direct,” “The

Right People at the Right Time,” and all of our stylized

logos. We also own the rights to trademarks we have utilized in the

past. We license the use of our marks to our franchisees via the

franchise agreements.

We have developed and own our

proprietary software, HQ Webconnect, to handle most aspects of

operations, including temporary employee dispatch and payroll,

invoicing, and accounts receivable. Our software system also allows

us to produce internal reports necessary to track and manage

financial performance of franchisees, trends in customers, to root

out potential fraud, and to examine other vital metrics

efficiently. We believe that our software facilitates customer

interaction, allowing for online bill payment, invoice review, and

other important functions. Because we developed a proprietary

system and have a dedicated IT development staff, we constantly

refine our software based on feedback from franchisees, customers,

and employees. We license the use of our software to franchisees

via our franchise agreements. The system is not patented. We have

invested in off-site back-up and storage systems that we believe

provide reasonable protections for our electronic information

systems against breakdowns as well as other disruptions and

unauthorized intrusions.

We rely on

common law protection of our copyrighted works. These works include

advertising and marketing materials and other items that are not

material to our business. We license some intellectual property

from third parties for use in our corporate headquarters, but such

licenses are not material to our business.

Our Organizational Structure

HireQuest, Inc.

is a holding company. It is the corporate parent of a series of

wholly-owned subsidiaries including: (1) HQ LTS Corporation, which

employs the staff of our corporate headquarters; (2) HQ Financial

Corporation, which provides financing and related services to our

franchisees; (3) Hire Quest, LLC, which is the employer of record

of our temporary employees; (4) HQ Franchising Corporation, which

assuming all proper regulatory approval, is expected to become the

franchisor of HireQuest and HireQuest Direct franchises in 2020;

(5) HQ Real Property Corporation, which, as of December 31, 2019,

owns our corporate headquarters and two adjacent parcels of real

property; and (6) HQ Insurance Corporation, which currently has no

operations but may serve a role related to our workers'

compensation program in the future.

11

Organization as of December 31, 2019

In addition,

Command Center had two wholly-owned subsidiaries which we dissolved

in December 2019: (1) Command Florida, LLC, and (2) ComStaff

Transport, Inc. Command Florida facilitated the Merger and served

no ongoing purpose. ComStaff had no operations in 2019 or

2018.

We

underwent the following significant changes in 2019: (1) we

completed the Merger between Legacy HQ and Command Center and

subsequently reincorporated in Delaware, (2) in connection with the

Merger, we entered into a new credit facility; (3) we entered into

a consulting agreement with Dock Square HQ, LLC, (4) we converted

all of the Command Center company-owned offices, acquired during

the Merger, to our franchise model, and (5) we exited the

California market for strategic reasons. For more information on

these transactions, please see Part II, Item 7. Management’s Discussion and

Analysis of Financial Conditions and Results of Operations under

the heading “Recent Developments” which is incorporated

herein by reference.

Our Securities Exchange Act Reports

We maintain a

website at the following address: www.hirequest.com. The

information on our website is not incorporated by reference in this

Annual Report on Form 10-K.

We make

available on our website certain reports and amendments to those

reports that we file with or furnish to the Securities and Exchange

Commission (the “SEC”) in accordance with the

Securities Exchange Act of 1934, as amended (the “Exchange

Act”). These include our annual reports on Form 10-K, our

quarterly reports on Form 10-Q, our current reports on Form 8-K,

and Section 16 filings by our officers, directors and 10%

stockholders. We make this information available on our website

free of charge as soon as reasonably practicable after we or they

electronically file the information with, or furnish it to, the

SEC.

Item 1A. Risk Factors

Our common stock value and our business, results of operations,

cash flows, and financial condition are subject to various risks,

including, but not limited to, those set forth below. If any of

these risks actually occur, our common stock, business, results of

operations, cash flows, and financial condition could be materially

adversely affected. In such case, the value of your investment

could decline and you may lose all or part of the money you paid to

buy our common stock. These risk factors should be carefully

considered together with the other information in this Form 10-K,

including the risks and uncertainties described under the heading

“Special Note Regarding Forward-Looking

Statements.”

Risks Related to Our Business and Industry

Fluctuations in general economic conditions, including those caused

by the novel coronavirus disease ("COVID-19"), may significantly

impact demand for our services, system-wide sales, and

profitability.

The demand for

temporary staffing is highly dependent upon the state of the

economy and upon the workforce needs of our clients, which creates

uncertainty and volatility. National and global economic activity

can be slowed by many factors, including the economic impact of

COVID-19, fluctuating markets and interest rates and global trade

uncertainties. As economic activity slows, companies tend to reduce

their use of temporary workers and reduce their recruitment of new

employees, and permanent full-time and part-time workers are

generally inclined to work more hours and overtime, resulting in

fewer available vacancies and less demand for our services.

Significant declines in demand of any region or industry in which

we have a major presence may severely reduce the demand for our

services and thereby significantly decrease our revenue and

profits. Deterioration in economic conditions or the financial or

credit markets could also have an adverse impact on our

clients’ ability to pay for services we have already

provided.

12

The

coronavirus pandemic is an emerging serious threat to health and

economic wellbeing affecting our franchisees, employees, customers

and the overall economy.

On March 11, 2020, the World Health

Organization announced that infections of COVID-19 had become

pandemic, and on March 13, 2020, the President of the United States

announced a National Emergency relating to the disease. Since March

13, several state and local authorities have taken dramatic action

including, without limitation, ordering the workforce to stay home,

banning all non-essential businesses from operating, refusing to

issue new building permits, and invalidating current building

permits causing work to stop. There has been widespread infection

in the United States and abroad, with the potential for

catastrophic impact on human lives, including those of our

franchisees and employees, and the economy as a whole, including

our customers. In addition to the actions described above,

national, state, and local authorities have recommended social

distancing and imposed or are considering quarantine and isolation

measures on large portions of the population and additional

mandatory business closures. These measures, while intended to

protect human life, are expected to have serious adverse impacts on

domestic and foreign economies of uncertain severity and duration.

The effectiveness of economic stabilization efforts, including

proposed government payments to affected citizens and industries,

is uncertain. Some economists are predicting the United States will

soon enter a recession.

The sweeping nature of the COVID-19

pandemic makes it extremely difficult to predict how our business

operations will be affected long term. But the likely overall

economic impact of the pandemic is viewed as highly negative to the

general economy. Already, the COVID-19 outbreak has begun to

negatively impact our operations and revenue as well as those of

our franchisees. We expect the effects to become more acute in the

next few months. It is possible that a number of our offices may be

forced to close. To date, our franchisees have closed or

consolidated a small number of offices at least, in part, due to

the potential financial impacts of COVID-19. Some of our

franchisees may experience economic hardship or even failure. We

may be classified as a non-essential business in some or all of the

jurisdictions that impose a ban on non-essential businesses. If

that were to occur, we may be forced to temporarily or permanently

close offices in those jurisdictions. Our customers may choose to

voluntarily close their worksites. Already, we have witnessed a

significant drop in the amount of hospitality, event service, and

catering business that we do. We may experience a shortage of

temporary employees as a result of the spread of the

disease.

Any of the above factors, or other

cascading effects of the coronavirus pandemic that are not

currently foreseeable, could materially increase our costs,

severely negatively impact our revenue, net income, and other

results of operations, reduce system-wide sales, cause office

closings or cause us to lose franchisees, and impact our liquidity

position, possibly significantly. The duration of any such impacts

cannot be predicted.

We may be unable to attract sufficient qualified candidates to meet

the needs of our clients.

We compete to

meet our clients’ needs for workforce solutions and,

therefore, we must continually attract qualified candidates to fill

positions. Attracting qualified candidates depends on factors such

as desirability of the assignment, location, the health of our

workforce, and the associated wages and other benefits. We have

experienced shortages of qualified candidates and we may experience

such shortages in the future due to a number of factors including,

without limitation, as a result of the COVID-19 pandemic. Further,

if there is a shortage, the cost to employ or recruit these

individuals could increase. If we are unable to pass those costs

through to our clients, it could materially and adversely affect

our business.

We are

vulnerable to seasonal fluctuations with lower demand in the fall

and winter months.

Royalty fees

generated from office sales in markets subject to seasonal

fluctuations will be less stable and may be lower than in other

markets. Locating offices in highly seasonal markets involves

higher risks. Individual franchisee revenue can fluctuate

significantly on both a quarter over quarter and year over year

basis thereby impacting our royalty and service revenue, depending

on the local economic conditions and need for temporary labor

services in the local economy. Weather can also have a significant

impact on our operations as there is typically lower demand for

staffing services during adverse weather conditions in the winter

months. To the extent that seasonal fluctuations become more

pronounced, our royalty fees could fluctuate materially from period

to period.

We are critically dependent on workers’ compensation

insurance coverage at commercially reasonable terms, and unexpected

changes in claim trends on our workers’ compensation may

negatively impact our financial condition.

We employ

workers for whom we provide workers’ compensation insurance.

Our workers’ compensation insurance policies are renewed

annually. The majority of our insurance policies are with Chubb/Ace

American. Our insurance carriers require us to collateralize a

significant portion of our workers’ compensation obligation.

We currently collateralize our policies largely with a letter of

credit from Branch Banking and Trust Company, now Truist Bank

(“BB&T”). If we no longer had access to that

collateral, we could not be certain we would be able to obtain

appropriate types or levels of insurance in the future or that

adequate replacement policies would be available on acceptable

terms. As our business grows or if our financial results

deteriorate, the amount of collateral required will likely increase

and the timing of providing collateral could be accelerated.

Resources to meet these requirements may not be available to us in

a timely manner or at all. The loss of our workers’

compensation insurance coverage would prevent us from operating as

a staffing services business in the majority of our markets.

Further, we cannot be certain that our current and former insurance

carriers will be able to pay claims we make under such

policies.

We are

responsible for a significant portion of expected losses under our

workers’ compensation program. Unexpected changes in claim

trends, including the severity and frequency of claims, changes in

state laws regarding benefit levels and allowable claims, actuarial

estimates, or medical cost inflation, could result in costs that

are significantly higher. There can be no assurance that we will be

able to increase the fees charged to our clients in a timely manner

and in a sufficient amount to cover increased costs as a result of

any changes in claims-related liabilities.

Our efforts to

actively manage the safety of our temporary workers and actively

control costs with internal staff and our network of workers’

compensation related service providers may not be sufficient to

prevent material increases to our workers’ compensation

costs.

13

We are dependent on a small number of individuals who constitute

our current management.

We are highly

dependent on the services of our senior management team and other

key employees at our corporate headquarters and on our

franchisees’ ability to recruit, retain, and motivate key

employees. Competition for such employees can be intense, and the

inability to attract and retain the additional qualified employees

required to expand our activities, or the loss of current key

employees including, without limitation, as a result of the

COVID-19 pandemic, could adversely affect our and our

franchisees’ operating efficiency and financial condition. In

addition, our growth strategy may place strains on our management

who may become distracted from day-to-day duties.

Our industry is subject to extensive government regulation and the

imposition of additional regulations, which could materially harm

our future earnings.

Our workforce

solutions are subject to extensive government regulation. In

particular, we are subject to a significant number of employment

laws due to our being a large employer. Additionally, there are

state and federal rules regarding disclosure requirements to

potential franchisees and regulations regarding our relationship

with existing franchisees. The cost to comply, and any inability to

comply with government regulation, could have a material adverse

effect on our business and financial results. Increases or changes

in government regulation of the workplace or of the

employer-employee relationship, or judicial or administrative

proceedings related to such regulation, could materially harm our

business.

We offer our

qualifying temporary workers government-mandated health insurance

in compliance with the Patient Protection and Affordable Care Act

and the Health Care and Education Reconciliation Act of 2010

(collectively, the “ACA”). We cannot be certain that

compliant insurance coverage will remain available to us on

reasonable terms, and we could face additional risks arising from

future changes to or repeal of the ACA or changed interpretations

of our obligations under the ACA.

Recently, Congress enacted the

Families First Coronavirus Response Act which, among other things,

requires certain employers under certain circumstances to pay their

employees emergency paid sick leave and pay further leave under an

extension of the Family Medical Leave Act. It is possible that the

payments required by this law will have a significant negative

impact on many of our franchisees. We cannot predict whether

Congress will enact additional legislation in response to COVID-19

or whether additional legislation will impact us and our

franchisees positively or negatively.

We may incur employment related claims or other types of claims and

costs that could materially harm our business.

We are in the

business of employing people in the workplaces of our clients. We

incur a risk of liability for claims for personal injury, wage and

hour violations, immigration, discrimination, harassment, and other

liabilities arising from the actions of our clients and/or

temporary workers. Some or all of these claims may give rise to

negative publicity, litigation, settlements, or investigations. As

a result, we may incur costs, charges or other material adverse

impacts on our financial statements.

We maintain

insurance with respect to some potential claims and costs with

deductibles. We cannot be certain that our insurance will be

available, or if available, will be of a sufficient amount or scope

to cover claims that may be asserted against us. Should the

ultimate judgments or settlements exceed our insurance coverage,

they could have a material effect on our business. We cannot be

certain we will be able to obtain appropriate types or levels of

insurance in the future, that adequate replacement policies will be

available on acceptable terms, or at all, or that our insurance

providers will be able to pay claims we make under such

policies.

We operate in a highly competitive industry and may be unable to

retain clients or market share.

Our industry is

highly competitive and rapidly innovating. We compete in national,

regional and local markets with full-service and specialized

temporary staffing companies. Our competitors offer a variety of

flexible workforce solutions. Therefore, there is no assurance

that we will be able to retain clients or market share in the

future, nor can there be any assurance that we will, in light of

competitive pressures, be able to remain profitable or maintain our

current profit margins.

If we fail successfully to implement our growth strategy, which

includes new office development by existing and new franchisees,

our ability to increase our revenue and operating profits could be

adversely affected.

Portions of our growth strategy rely

on new office development by existing and new franchisees. Our

franchisees may face many challenges in opening new offices

including:

14

●

Availability and cost of financing;

●

Negotiation of acceptable lease and financing

terms;

●

Trends in the overall and local economy of the

target market;

●

Recruitment, training, and retention of

qualified core staff and temporary personnel; and

●

General economic and business conditions

(including those resulting from the effects of the coronavirus

global pandemic (COVID-19)).

These factors are outside of our

control and could hinder our franchisees from opening new offices

or expanding existing ones. This could prevent us from successfully

implementing our growth strategy.

Changes in our industry could place strains on our management,

employees, information systems, and internal controls, which may

adversely impact our business.

Changes in the temporary staffing

industry and how our customers utilize, order, and pay for

temporary staffing services, particularly through new and

innovative uses of technology, may place significant demands on our

administrative, operational, financial, and other resources or

require us to obtain different or additional resources. Any failure

to respond to or manage such changes effectively could adversely

affect our business. To be successful, we will need to continue to

implement management information systems and improve our operating,

administrative, financial, and accounting systems and controls in

order to adapt quickly to such changes. These changes may be

time-consuming and expensive, increase management responsibilities,

and divert management attention, and we may not realize a return on

our investment in these changes.

The loss of or damage to key relationships, including with Dock

Square, may adversely affect the Company’s

business.

The Company’s business is

dependent on its relationships with clients and collaboration

partners. On July 15, 2019, the Company entered into a consulting

arrangement with Dock Square HQ, LLC (“Dock Square”),

an organization with connections at

many of the largest users of temporary staffing in the country.

Pursuant to this consulting arrangement, Dock Square introduces

prospective customers and expands relationships with existing

customers of the Company in return for which it is

eligible to receive unregistered shares of the Company’s

common stock, subject to certain performance metrics and vesting

terms. The loss of or damage to the Company’s

consulting arrangement with Dock Square may adversely affect the Company’s business

and revenue.

Shifts in attitudes towards contingent workforces could negatively

impact our results of operations and financial

condition.

Attitudes and beliefs about

contingent workforces could change such that our customers no

longer desire to utilize our services. If this occurs, it could

negatively impact our financial condition and results of

operations. Such a shift could also make it challenging or

impossible for us to successfully implement our growth

strategies.

Difficult political or market conditions, natural disasters, global

pandemics, or other unpredictable matters could affect our business

in many ways including by reducing the amount of available

temporary employees, reducing the amount of customer projects, or

harming the overall economy which could materially reduce our

revenue, earnings and cash flow and adversely affect our financial

condition.

Our business is linked to conditions

in the overall economy, such as those impacting the ability of our

customers to obtain financing, the availability of temporary

employees, changes in laws, and catastrophic events such as fires,

floods, earthquakes, tornadoes, hurricanes, and pandemics. In

particular, the recent outbreak of COVID-19 could materially affect

our business to the extent it affects the economy overall,

negatively impacts the industries our customers are in, or infects

a large number of temporary employees removing them from the

available worker pool. These factors are unpredictable and outside

of our control. They may affect the level and volatility of

securities prices and the liquidity and value of investments,

including investments in our common stock.

Our credit facility contains operating and financial covenants that

may restrict our business and financing activities.

On July 11,

2019, in connection with the Merger, we, along with our

subsidiaries, entered into a loan agreement with BB&T for a $30

million line of credit with a $15 million sublimit for letters of

credit. The loan agreement and other loan documents contain

customary events of default and negative covenants, including but

not limited to those governing indebtedness, liens, fundamental

changes, transactions with affiliates, and sales of assets. The

loan agreement also requires us to comply with a fixed charge

coverage ratio of at least 1.10:1.00.

15

The agreements limit, among

other things, our ability to:

●

Sell, lease, license, or

otherwise dispose of assets;

●

Undergo a change in

control;

●

Consolidate and merge with

other entities; or

●

Create, incur, or assume

liens, debt, and other encumbrances.

The operating

and other restrictions and covenants in the agreements and in any

future financing arrangement that we may enter into, may restrict

our ability to finance our operations, engage in certain business

activities, or expand or fully pursue our business strategies, or

otherwise limit our discretion to manage our business. Our ability

to comply with these restrictions and covenants may be affected by

events beyond our control, and we may not be able to meet those

restrictions and covenants. A breach of any of the restrictions and

covenants could result in a default under our agreements which

could cause any outstanding indebtedness under the agreements or

under any future financing arrangements to become immediately due

and payable, and result in the termination of commitments to extend

further credit.

The phase-out of the London Interbank Offered Rate

(“LIBOR”), or the replacement of LIBOR with a different

reference rate, may adversely affect interest rates.

Borrowings

under our credit facility bear interest at rates determined using

LIBOR as the reference rate. On July 27, 2017, the Financial

Conduct Authority (the authority that regulates LIBOR) announced

that it would phase-out LIBOR by the end of 2021. It is unclear

whether new methods of calculating LIBOR will be established such

that it continues to exist after 2021, or if alternative rates or

benchmarks will be adopted, and currently it appears highly likely

that LIBOR will be discontinued or substantially modified by 2021.

Changes in the method of calculating LIBOR, or the replacement of

LIBOR with an alternative rate or benchmark, may adversely affect

interest rates and result in higher borrowing costs. This could

materially and adversely affect our results of operations, cash

flows, and liquidity. We cannot predict the effect of the potential

changes to LIBOR or the establishment and use of alternative rates

or benchmarks. Furthermore, we may need to renegotiate our

revolving credit facility or incur other indebtedness, and changes

in the method of calculating LIBOR, or the use of an alternative

rate or benchmark, may negatively impact the terms of such

indebtedness.

Risks Related to

Our Franchisees and Business Model

Converting our company-owned offices to franchises has multiple

risks.

We believe that

the franchise model is superior to the company-owned store model.

To that end, we converted the remaining company-owned offices to

franchises in the third quarter of 2019. However, we will have less

control over the day-to-day operations of the offices and the

franchisees may operate in a manner that is counter to our

interests or introduce risks to our business by departing from our

operating norms. Further, franchises are generally regulated at

both the federal and the state level, so operating as franchises

will introduce additional regulatory risk. In addition, the new

franchisees will need to adapt to a new operating model, a new IT

system, and new business processes.

Our operating and financial results and growth strategies are

closely tied to the success of our franchisees.

With all of our

offices being operated by franchisees, we are dependent on the

financial success and cooperation of our franchisees. We have

limited control over how our franchisees’ businesses are run,

and the inability of franchisees to operate successfully could

adversely affect our operating and financial results through

decreased royalty payments or otherwise. If our franchisees incur

too much debt, if their operating expenses increase, or if economic

or sales trends deteriorate (including as a result of the global

pandemic caused by COVID-19) such that they are unable to operate

profitably or repay existing debt, it could result in their

financial distress, including insolvency or bankruptcy. If a

significant franchisee or a significant number of franchisees

become financially distressed, our operating and financial results

could be impacted through reduced or delayed royalty payments. A

franchisee bankruptcy could have a substantial negative impact on

our ability to collect payments due under such franchisee’s

franchise agreement. Our success also depends on the willingness

and ability of our franchisees to be incentivized to deliver

excellent customer service, resolve any issues efficiently, and

ensure customer retention. In addition, our success depends on the

willingness and ability of our franchisees to implement major

initiatives, which may include financial investment. Our

franchisees may be unable to successfully implement strategies that

we believe are necessary for their further growth, which in turn

may harm our growth prospects and financial condition.

16

Our franchisees could take action that could harm our

business.

Our franchisees

are contractually obligated to operate their offices in accordance

with the operations standards set forth in our agreements with them

and applicable laws. However, although we attempt to properly train

and support all our franchisees, they are independent third parties

whom we do not control. The franchisees own, operate, and oversee

the daily operations of their offices, and their core office

employees are not our employees. While we have the ability to

enforce our franchise agreements, many of our franchisees’

actions are outside of our control. Although we have developed

criteria to evaluate and screen prospective franchisees, we cannot

be certain that our franchisees will have the business acumen or

financial resources necessary to operate successful franchises at

their approved locations, and state franchise laws may limit our

ability to terminate or not renew these franchise agreements.

Moreover, despite our training, support, and monitoring,

franchisees may not successfully operate offices in a manner

consistent with our standards and requirements or may not hire and

adequately train qualified office personnel. The failure of our

franchisees to operate their franchises in accordance with our

standards or applicable law, actions taken by their employees or a

negative publicity event at one of our franchisees’ offices

or involving one of our franchisees could have a material adverse

effect on our reputation, our brands, our ability to attract

prospective franchisees, and our business, financial condition, or

results of operations.

If we fail to identify, recruit, and contract with a sufficient

number of qualified franchisees, our ability to open new offices

and increase our revenue could be materially adversely

affected.