Attached files

| file | filename |

|---|---|

| EX-32.1 - Surna Inc. | ex32-1.htm |

| EX-32.2 - Surna Inc. | ex32-2.htm |

| EX-31.2 - Surna Inc. | ex31-2.htm |

| EX-31.1 - Surna Inc. | ex31-1.htm |

| EX-23.1 - Surna Inc. | ex23-1.htm |

| EX-21.1 - Surna Inc. | ex21-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2019

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM ____ TO _______

Commission File Number: 000-54286

SURNA INC.

(Exact name of registrant as specified in its charter)

| Nevada | 27-3911608 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 1780 55th Street, Boulder, Colorado | 80301 | |

| (Address of principal executive offices) | (Zip code) |

(303) 993-5271

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| N/A | N/A | N/A |

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class Registered

Common stock, par value $0.00001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X].

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X].

Indicate by check mark whether the issuer (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the last 90 days. Yes [X] No [ ].

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [X] No [ ].

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer, “accelerated filer,” “non-accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | [ ] | Accelerated Filer | [ ] |

| Non-accelerated Filer | [ ] | Smaller Reporting Company | [X] |

| Emerging Growth Company | [ ] | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X].

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately $8,757,000 based upon a closing price of $0.039 reported for such date on the OTCMarkets.

As of March 23, 2020, the number of outstanding shares of common stock of the registrant was 236,526,638.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Surna Inc.

Annual Report on Form 10-K

For Fiscal Year Ended December 31, 2019

Table of Contents

| 2 |

In this Annual Report, unless otherwise indicated, the “Company”, “we”, “us” or “our” refer to Surna Inc. and, where appropriate, its wholly-owned subsidiary.

Hemp and marijuana are technically both part of the “Cannabis sativa L.” plant. “Hemp” is a term used to classify varieties of cannabis that contain 0.3% or less tetrahydrocannabinol (“THC”) content (by dry weight), the principal psychoactive constituent of cannabis. Hemp and its derivatives were federally legalized in the United States as part the Agricultural Act of 2018. “Marijuana” is a term used to classify varieties of cannabis that contain more than 0.3% THC (by dry weight). Marijuana is not federally legal in the United States. Many states, however, have taken action to make marijuana legal for all purposes, made it available for medical uses, decriminalized it or a combination thereof. We currently provide nearly all of our products and services to customers that cultivate marijuana. In this Annual Report, unless otherwise indicated, “cannabis” refers to “marijuana.”

CAUTIONARY STATEMENT

This Annual Report on Form 10-K, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7, contains forward-looking statements that involve substantial risks and uncertainties. These forward-looking statements are not historical facts, but are based on current management expectations that involve substantial risks, uncertainties, and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed in, or implied by, these forward-looking statements. Forward-looking statements relate to future events or our future financial performance. We generally identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these terms or other similar words. All statements, other than statements of historical fact, are statements that could be deemed forward-looking statements including, but not limited to, any projections of revenue, gross profit, earnings or loss, tax provisions, cash flows or other financial items; any statements of the plans, strategies or objectives of management for future operations; any statements regarding current or future macroeconomic or industry-specific trends or events and the impact of those trends and events on us or our financial performance; any statements regarding pending investigations, legal claims or tax disputes; any statements of expectation or belief; and any statements of assumptions underlying any of the foregoing.

These forward-looking statements are subject to known and unknown risks, uncertainties, assumptions and other factors that could cause our actual results of operations, financial condition, liquidity, performance, prospects, opportunities, achievements or industry results, as well as those of the markets we serve or intend to serve, to differ materially from those expressed in, or suggested by, these forward-looking statements. These forward-looking statements are based on assumptions regarding our present and future business strategies and the environment in which we operate. Important factors that could cause those differences include, but are not limited to:

| ● | our business prospects and the prospects of our existing and prospective customers; |

| ● | the inherent uncertainty of product development; |

| ● | regulatory, legislative and judicial developments, especially those related to changes in, and the enforcement of, cannabis laws; |

| ● | increasing competitive pressures in our industry; |

| ● | the ability to effectively operate our business, including servicing our existing customers and obtaining new business, as a result of our recent workforce reduction; |

| ● | our relationships with our customers and suppliers; |

| ● | the continuation of normal payment terms and conditions with our customers and suppliers, including our ability to obtain advance payments from our customers; |

| ● | general economic conditions, our customers’ operations and access to capital, and market and business disruptions including severe weather conditions, natural disasters, health hazards, terrorist activities, financial crises, political crises or other major events, or the prospect of these events, adversely affecting demand for the products and services offered by us in the markets in which we operate; |

| ● | changes in our business strategy or development plans, including our expected level of capital expenses and working capital; |

| ● | our ability to attract and retain qualified personnel; |

| ● | our ability to raise equity and debt capital to fund our operations and growth strategy, including possible acquisitions; |

| ● | our ability to identify, complete and integrate potential strategic acquisitions; |

| ● | future revenue being lower than expected; |

| ● | our ability to convert our backlog into revenue in a timely manner, or at all; and |

| ● | our intention not to pay dividends. |

| 3 |

Although we believe that the assumptions on which these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions also could be inaccurate. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this annual report on Form 10-K should not be regarded as a representation by us that our plans and objectives will be achieved. These risks and uncertainties include those described or identified in “Risk Factors” in this Annual Report on Form 10-K. You should not place undue reliance on these forward-looking statements, which apply only as of the date of this Annual Report on Form 10-K. Except as required by the federal securities laws, we undertake no obligation to revise or update any forward-looking statements, whether as a result of new information, future events or otherwise, to reflect events or circumstances occurring after the date of this Annual Report on Form 10-K. The forward-looking statements and projections contained in this Annual Report on Form 10-K are excluded from the safe harbor protection provided by Section 27A of the Securities Act.

Non-GAAP Financial Measures

To supplement our financial results on U.S. generally accepted accounting principles (“GAAP”) basis, we use non-GAAP measures including net bookings, backlog, as well as adjusted net income (loss) which reflects adjustments for certain non-cash expenses such as stock-based compensation, certain debt-related items and depreciation expense. We believe these non-GAAP measures are helpful in understanding our past performance and are intended to aid in evaluating our potential future results. The presentation of these non-GAAP measures should be considered in addition to our GAAP results and are not intended to be considered in isolation or as a substitute for financial information prepared or presented in accordance with GAAP. We believe these non-GAAP financial measures reflect an additional way to view aspects of our operations that, when viewed with our GAAP results, provide a more complete understanding of factors and trends affecting our business. For purposes of this Annual Report, (i) “adjusted net income (loss)” and “adjusted operating income (loss)” mean GAAP net income (loss) and operating income (loss), respectively, after adjustment for non-cash equity compensation expense, debt-related items and depreciation expense, and (ii) “net bookings” means new sales contracts executed during the quarter for which we received an initial deposit, net of any adjustments including cancelations and change orders during the quarter.

Our backlog, remaining performance obligations and net bookings may not be indicative of future operating results, and our customers may attempt to renegotiate or terminate their contracts for a number of reasons, including delays in or inability to obtain project financing or licensing or abandonment of the project entirely. Accordingly, there can be no assurance that contracts included in the backlog or remaining performance obligations will actually generate revenues or when the actual revenues will be generated.

| 4 |

Overview

We design, engineer and sell cultivation technologies for controlled environment agriculture including: (i) liquid-based process cooling systems and other climate control systems, (ii) air handling equipment and systems, (iii) a full-service engineering package for designing and engineering commercial scale thermodynamic systems specific to cannabis cultivation facilities, and (iv) automation and control devices, systems and technologies used for environmental, lighting and climate control. Our customers include commercial, state- and provincial-regulated cannabis growers in the U.S. and Canada as well as other international locations, including those growers building new facilities and those expanding or retrofitting existing facilities. Currently, our revenue stream is derived primarily from supplying our products, services and technologies to commercial indoor and hybrid sealed greenhouse facilities ranging from several thousand to more than 100,000 square feet.

Headquartered in Boulder, Colorado, we leverage our experience in this space to bring value-added climate control solutions to our customers that help improve their overall crop quality and yield, optimize energy and water efficiency, and satisfy the evolving state and local codes, permitting and regulatory requirements. Although our customers do, we neither produce nor sell cannabis.

Indoor cannabis cultivators are facing multiple headwinds of high energy costs, increasingly rigorous quality standards and declining cannabis prices. To be competitive, among other things, our customers must develop innovative ways to meet the demands of their business and reduce energy costs, 90% of which is typically related to their HVAC (50%) and lighting systems (40%). HVAC systems have historically been our focus. We often have the advantage of early engagement with our customers at the pre-build and construction phases and the corresponding opportunity to build longer-term relationships with our existing customers and their facilities. Going forward, our plan is to leverage our existing customer relationships and attempt to sell them additional products and services, thereby becoming “stickier” to our customers, in an effort to generate incremental revenue.

We have three core assets that we believe are important to our going forward business strategy. First, we have multi-year relationships with customers and others in the cannabis industry. Second, we have specialized engineering know-how and experience gathered from designing environmental control systems for cannabis cultivation facilities since 2016. Third, we have a line of proprietary environmental control products, which we are in the process of expanding.

We are an integrated provider of mechanical engineering design, proprietary environmental control equipment and a controls and automation offering serving the cannabis space. We believe our employees have more experience than most other mechanical engineering firms serving this industry. Our customers engage us for their environmental and climate control systems because they want experts to design their facilities, and they come to us because of our reputation. We leverage our reputation and know-how against the many local contractors and mechanical engineers who collectively constitute our largest competitors.

A number of recent events have had an adverse impact on our operations and financial condition, including constraints on capital availability for our customers and prospects who have commenced, or are contemplating, new and expanded cannabis cultivation facilities and the recent outbreak of COVID-19, a novel strain of coronavirus first identified in China, which has spread across the globe including the U.S. Most recently, the response to this coronavirus by federal, state and local governments in the U.S. has resulted in significant market and business disruptions across many industries and affecting businesses of all sizes. This pandemic has also caused significant stock market volatility and further tightened capital access for most businesses.

As a result of these events, we assessed our near-term operations, working capital, finances and capital formation opportunities, and implemented, in late March 2020, a downsizing of our operations, including workforce reductions, reductions of salaried employee compensation and a reduction of hours worked to preserve cash resources, cut costs and focus our operations on customer-centric sales and project management activities. In addition, any potential government mandate to limit non-essential work would have a material adverse effect on management’s revised plans. The extent to which COVID-19 will impact our business and financial results will depend on future developments, which are uncertain and cannot be predicted at this time.

The duration and likelihood of success of our downsizing effort, workforce reduction and cost-cutting measures are uncertain. If these actions do not meet our expectations, or additional capital is not available, we may not be able to continue our operations. Other factors that will affect our ability to continue operations include the market demand for our products and services, our ability to service the needs of our customers and prospects with a reduced workforce, potential contract cancellations, project scope reductions and project delays, our ability to fulfill our current backlog, management of our working capital, the availability of cash to fund our operations, and the continuation of normal payment terms and conditions for purchase of our products. Due to the heightened uncertainty relating to the potential impacts of the coronavirus on our business operations, we believe our cash balances and cash flow from operations will be insufficient to fund our operations for the next twelve months. If our customers or prospects are unable to obtain project financing and we are unable to increase revenues, or otherwise generate cash flows from operations, we will not be able to successfully execute on the various strategies and initiatives we have set forth in this Annual Report to grow our business.

Shares of our common stock are traded on The OTC Markets under the ticker symbol “SRNA.”

Our Growth Strategy

We believe there are fundamentally three ways to grow a business: (i) increase the number of customers, (ii) increase the average revenue per order, or (iii) increase the frequency of orders. Our growth strategy is threefold:

| 1. | Sell proverbial “Chevys.” In addition to “Cadillac” -level products, sell “Chevy” or equivalent products to satisfy a wider range of points along the demand curve. Anticipated result: Increase the number of customers. |

We have a sales and marketing program that generates many prospective customer relationships. However, our limited range of higher cost products, mostly chilled water systems, reduces the number of customer prospects who can afford to buy from us. We will broaden our product line to include lower- and mid-cost products, such as split systems and packaged roof top units, as well as other technology solutions, so that a broader group of growers can take advantage of our engineering expertise and capabilities. We believe these new products and services will increase our addressable market and increase sales, further leveraging our investment in sales and marketing.

| 5 |

| 2. | Sell proverbial “steering wheels.” Sell our customers the automated facilities control systems they need—directly. Anticipated result: Increase average order size. |

Growing live plants indoors in a controlled environment is a technically demanding business, and a failed crop can cost a grower significant foregone revenue. We believe our licensed professional engineers are some of the industry’s leading experts in the design of such facilities, and we seek to extend that leadership into more advanced technology products.

Last year we introduced our SentryIQ™ control system. If our climate control design and products are the proverbial car, then SentryIQ™ is the proverbial steering wheel—one is needed to direct the car where to go. Before SentryIQ™, we had to send our customers elsewhere for controls to regulate their cultivation environments, but we now have the ability to capture that revenue.

Our next step down this technology and innovation road will be the eventual development of the equivalent of a self-driving car. Growers will tell the control system what they want to achieve, and the system will sense the environment and direct the climate control system to achieve the grower’s goals. These systems will be able to integrate data analytics—and eventually deploy artificial intelligence—to optimize multiple variables to maximize the grower’s profits. While we are in the early stages of development of these technology-driven systems, we believe it is important for us to become a player in this market because it expands our addressable market for both sensors and software while offering the possibility of higher margins and recurring revenue over time.

| 3. | Add more proverbial “dealers.” Engage in one or more strategic relationships with other technology leaders that serve our industry. Anticipated result: Increase the number of customers. |

Such relationships might include referral marketing agreements, co-development of unique integrated solutions with best-in-class partners, and acquisitions. To extend the automotive analogy, engaging in these types of relationships is like adding more dealers to sell our products, at little cost to us.

********

Our Key Initiatives

Our goal for the immediate future is to grow organically, strategically and profitably. We believe the worldwide market for indoor-grown cannabis products will grow substantially for the foreseeable future, and we hope this will lead to more new build projects to drive our continued growth. Here are some of the initiatives we pursued in 2019, and where more work is needed to progress each of these initiatives.

Focus on Multi-facility Operators. In 2019, in addition to independent smaller growers, we actively pursued business from multi-facility operators (MFOs), which we define as businesses that own and operate two or more cannabis cultivation facilities in either the U.S. or Canada. These MFOs are typically larger and have greater financial and organizational wherewithal to buy more and larger systems and are less prone to project delays and cancellations, compared to the smaller (and riskier) independent cultivators that had been our primary customers in the past. We enjoyed success in this effort, booking seven projects with MFOs, representing $8.3 million in revenue, or 55% of our total 2019 revenue. However, three of these projects, generating a total of $6.7 million in revenue, were with a single MFO. Going forward, we will conduct our operations to seek a sales pipeline with MFO customers that we believe will result in more consistent and predictable revenue and cash flow. Because MFOs are typically more sophisticated and may, in many cases, have in-house engineering teams, such MFOs may not need the expertise and experience we offer. This contrasts with the independent smaller grower market that places significant value in our cannabis-specific expertise and experience and continues to represent an important market segment for us.

| 6 |

The table below shows our 2019 full year results for commercial-scale projects, which we define as contracts with a value over $100,000, by project and customer type.

To achieve profitability in the future, we must first be able to generate a more consistent and predictable revenue stream. To do so, we must: (i) maximize our new build facility projects, and (ii) supplement those projects with an increased number of retrofit and expansion projects—which typically have shorter completion cycles and fewer external contingencies that we do not control. Historically, whenever a new build project has been delayed or cancelled, which can occur often, our revenue and cash flow has taken a corresponding dramatic hit.

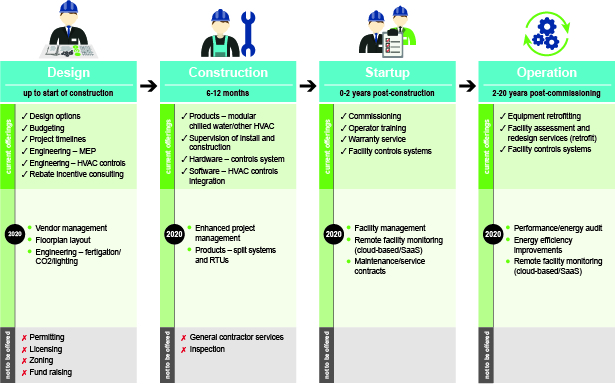

Offer a Broader Range of Products and Services Across the Cultivation Facility Lifecycle. During 2019, we fulfilled the first step of this goal with the introduction of our SentryIQ™ controls package. We also began offering full mechanical, electrical, and plumbing engineering services, developed and sold a four-pipe environmental control system with Surna branded fan coil units and custom air handlers, developed a proprietary destratification fan, and performed facility retrofit services. Our new custom air handlers alone generated $2.3 million in revenue in 2019.

Following up on our product launch successes in 2019, we plan to address facility lifecycle revenue opportunities by leveraging our strong brand name and positioning ourselves as the “trusted advisor” in environmental controls management. Our expanded product offering is illustrated by the following 4-phase matrix of product/service depth and facility lifecycle participation.

| 7 |

Our plan is to attempt to become “stickier” to our customers by providing climate control products and services across the entire 4-phase facility lifecycle. Each phase of the facility lifecycle has many activities that present potential opportunities for us, some of which we will pursue. We do not intend to offer products and services in all activities in each phase, but rather we will focus on technology and innovation that provide value-add to our customers as they attempt to seek out “best-in-class” partners to automate and control the indoor grow facilities of the future. We believe, if successful, this could possibly translate into greater demand for our proprietary, customized equipment, technology and software solutions.

Enter Strategic Alliances to Expand our Marketing and Sales Reach. Although we explored a few acquisitions and strategic alliance opportunities in 2019, we did not attract partners of the caliber or business segment that we are seeking. We have identified several business verticals that we believe are logical and natural complements to our climate control business, such as: lighting, fertigation (automated process of delivering nutrients and water to plants), benches (customized systems to optimize use of the growing space), cultivation management technology (software), consumables (growing, packaging, facility and lab supplies), and operational improvement analytics (modeling, data aggregation and artificial intelligence). We also believe we should consider strategic alliances, such as distribution, reseller, co-marketing or product development agreements, with select companies which are consistent with our strategic direction. Our strategic alliances will likely involve development of more comprehensive, end-to-end, integrated solutions for our customers, as well as specialized products and services that help cultivators compete in the market, whether through automation, software or operating efficiencies.

If some of these strategic alliances are successful in driving top-line revenue for us and our partners, over time these relationships could develop into more exclusive arrangements or evolve into possible acquisitions or a source of strategic capital for us. There can be no assurance that we will be able to successfully execute any of these strategic initiatives. Efforts will be primarily focused on working with new strategic partners to co-market each other’s products and services and possibly jointly develop new and improved products and services with cannabis-specific applications, as opposed to exclusively seeking acquisitions.

Cash and Dilution. We started 2019 with just over $250,000 in cash but, with a new discipline on cost control and strong revenue growth, we were able to increase our cash to $922,000 at the end of 2019. We were self-sustaining during 2019, having used operating cash flows to support our operations, and we did not require any outside capital. By contrast, in 2017 and 2018, we experienced losses and cash flow deficits that had to be financed with a series of dilutive capital raises. In 2019, we exercised strict financial discipline to achieve the goal of cash operating profitability and cash flow sustainability—in part of sheer necessity, and in part to simply validate that we had a financially viable business model. We believe we do, with our first two profitable quarters ever in both the second and third quarter of 2019, and adjusted net income in 2019 of $92,000 compared to an adjusted net loss in 2018 of $2,592,000. Our adjusted net income (loss) is our GAAP net income (loss) after addback for our non-cash equity compensation expenses, debt-related items and depreciation expense.

Though improved in 2019, our working capital remains negative, which is a constant impediment to the overall viability of our business as planned, so we must land more MFO and other contracts and we may have to raise capital again to fund our working capital need and future growth. As discussed above, due to the heightened uncertainty relating to the potential impacts of the coronavirus on our business operations, we implemented a workforce reduction in late March 2020 to preserve cash resources and focus our operations on customer-centric sales and project management activities. We do not know the duration or the likelihood of success of this downsizing effort. However, if our customers and customer prospects are unable to obtain project financing and we are unable to increase revenues, we may not be able to continue our operations.

Investor Relations. We previously had limited investor relations activities of any kind prior to 2019. Now, we have a clear plan designed to create an actively traded, widely held, and fully valued stock over time—and in concert with our achievement of consistent financial goals. In 2019 we took the required initial steps of hosting regular earnings calls and attending a select number of investor conferences.

| 8 |

Products and Services

We now offer a deeper range of products and services than the mechanical engineering and modular chilled water systems we historically offered. This includes products and services targeting smaller indoor grow facilities and commercial-scale facilities as well as sealed greenhouse, or hybrid, facilities.

Services: Engineering and Design. Previously, we provided basic engineering and design work. Currently, we believe we have leading edge, sophisticated engineering capabilities which we attempt to leverage with independent small growers as well as MFOs that are building larger and more sophisticated commercial projects. As evidenced by our 2019 success penetrating the MFO market, our reputation today reflects this reality.

Going forward, we will: (i) emphasize our strong mechanical engineering team that includes an in-house staff of degreed engineers including an experienced licensed professional engineer (PE), (ii) offer pre-construction energy modeling to help our customers and enhance our sales closing rate, (iii) develop an engineering, design and audit services program for the expanding retrofit market, which remediates existing grow facilities that suffer from sub-optimal performance, and (iv) potentially offer other facility management programs.

Our technical experience and know-how in designing indoor cannabis cultivation facilities allow us to deliver to our customers practical solutions to complicated problems in three primary areas: (i) precision climate and environmental controls, (ii) energy and water efficiency, and (iii) building code and permitting. Our engineering design typically includes all mechanical components of a climate control system: cooling and heating, dehumidification, ventilation, air sanitation and odor control. We provide load calculations, equipment specifications, and engineered systems drawings for both the cultivation and comfort cooling portions of our customers’ facilities. We also have experience in, or knowledge of, state and local permitting and code compliance for cannabis facilities in states and provinces where cannabis has been legalized for either recreational or medical use or is expected to be legalized, and we provide stamped, engineered drawings in all states and provinces where we operate.

Our competitive advantages are our experience and reputation. Since 2006, we have been continuously improving our facility designs which we believe distinguishes us from our competition, including local heating, ventilation and air conditioning (“HVAC”) contractors, traditional HVAC design consultants, and others who may lack our cannabis-specific expertise. Indoor sealed grow facilities present a very difficult mechanical engineering challenge, and traditional mechanical engineers, without our cannabis experience, are typically unfamiliar with the precise climate and air control requirements needed for such facilities. As important, they may be unable to effectively navigate the local code and permitting rules which did not contemplate cannabis cultivation facilities when enacted. With our engineering design resources and experience, we are able to provide a code-compliant mechanical plan set in any state or province by collaborating with local regulators and our customers to engineer creative solutions that not only meet the intent of the local codes but also address concerns about the growing energy and resource usage of these facilities.

Energy use is, and will increasingly become, a primary concern for regulators and indoor cultivators. Two states, Massachusetts and Illinois, have already placed regulatory caps on energy density in cannabis cultivation facilities and we expect this trend to continue. Energy costs are frequently the second largest operating expense for a cultivation facility, after labor, with HVAC and lighting comprising approximately 50% and 40%, respectively, of a facility’s energy use.

As a result, licensed producers are adopting practices to maximize energy efficiency and thereby reduce operating costs, which will become even more important as the industry matures and wholesale prices continue to decline. These practices include more efficient uses of water, more efficient lighting (typically LED lighting), and renewable energy alternatives. Sealed greenhouses, or hybrid facilities—which are insulated for energy efficiency and combine natural light with the use of artificial lights—also provide a more economical way to grow cannabis compared to warehouse type indoor production. But regardless of whether an indoor or a hybrid facility is the grow venue, precise environmental controls are required to deliver consistent product quality and yield. We are evaluating possible strategic relationships with providers that are seeking an environmental controls partner for these specific facility applications.

We believe the right solution for our cultivation customers must include: (i) precise temperature/humidity control; (ii) reduced fungus, pollen, pesticide and insect contamination risk (“bio-security”); (iii) controlled regulatory compliance risk; and (iv) lower maintenance complexity, costs and downtime.

Our bio-security program uses a combination of a sealed facility and customized approaches to air sterilization to maintain facility standards, while destroying harmful airborne microbes without the production of byproducts. Additionally, our ductless modular chilled water systems—using fan coil units within each grow room—isolate the air and potential contaminants within each room, while taking advantage of the energy efficiencies and redundancies offered by such systems. Our experience has shown that our precision environmental controls can reduce the reliance on the use of harmful pesticides and fungicides. We also believe our experience in the tightly regulated Canadian market where pharmaceutical-like standards (including Good Manufacturing Practice standards) exist for filtration, air quality and post-harvest plant quality gives us an advantage over our competitors, especially as product quality testing regulations continue to be enacted and made more stringent by state, provincial and local agencies.

| 9 |

The following perspectives explain and help conceptualize the complexity of the environmental controls systems that need to be deployed by indoor cultivators:

| ● | Lighting. Lighting demand is 70 times more energy intensive than commercial office buildings. This lighting intensity creates heat, which when combined with plant transpiration to create humidity, creates the need for dehumidification and corresponding additional energy demand. Further complicating matters, lighting schedules and density must be adjusted for the clone, vegetative and flowering stages of cannabis cultivation, and associated variances in watering rates and temperature and humidity targets. | |

| ● | HVAC. HVAC energy use is driven by the need to remove the heat emitted from lighting and the moisture released during the plant’s evapotranspiration process, coupled with air circulation and odor and contaminant filtration requirements. | |

| ● | Legacy Systems. Mechanical systems are often designed and/or installed poorly, which can increase energy consumption and inconsistencies in environmental conditions. Reasons include: (i) cultivators deploying HVAC systems without an understanding of how the HVAC system impacts the growing environment, (ii) cultivators failing to understand the criticality of proper installation, commissioning and servicing of the equipment, even if properly designed, (iii) HVAC systems selected without understanding the interrelationship between sensible (cooling) and latent (moisture) factors, and (iv) most HVAC systems are designed for human occupied spaces, not process loads to accommodate plants. |

New technologies and applications, coupled with emerging cultivation innovations, are providing opportunities for increased efficiency, which we are positioned to deliver to our customers. Our engineering and product development teams, which currently consist of nine people, are fully qualified and committed to delivering energy and resource efficient solutions to commercial cultivators. Leveraging their technical competence, and our customers’ increasing focus on energy efficiency, quality and yield, in the future we intend to offer retrofit/design, energy audit, energy efficiency improvement, and performance audit services.

Products: Environmental Control Systems. Previously, we exclusively sold modular chilled water systems. In the future, we intend to expand our product offering to include other HVAC solutions, such as custom air handling units, split systems, packaged roof-top units, self-contained and complex water chilled systems. During 2019, we launched upgraded equipment lines of fan coils and air handlers. This expanded product line will allow us in the future to offer less expensive products that can help us serve customers who are more cost sensitive.

We are now offering various configurations of our new Surna-branded fan coil units, which provide greater efficiency, design flexibility and control for growers using modular chilled water systems. During 2019, we delivered our first custom-designed ducted air handling system, which is another alternative to our new and improved ductless fan coil units.

We are capable of offering a utility rebate consulting service to help our new build customers obtain utility rebates. While this service is not expected to generate significant revenue, it should help us sell our environmental controls systems because our customers will be able to use these rebates to offset some of their capital costs.

There can be no assurance that we will be able to successfully execute any of these product initiatives, or identify, test and develop improved products or services, or that such products or services will generate revenue or profitability at the levels we expect. We also intend to work with select “best-in-class” vendors and partners that may be interested in jointly developing and marketing new and improved products and services with cannabis-specific applications.

Technology: Sensors, Controls and Automation Business. One of our key initiatives for 2019 was the development of a branded, proprietary controls and monitoring offering (consisting of sensors, controllers, software, monitoring and a user interface). We accomplished this and launched in April 2019 our SentryIQTM sensors, controls and automation (“SCA”) platform—a turnkey, single-vendor HVAC equipment and controls integration solution to new build projects as well as existing facilities in the startup and operation phases. We have now entered into seven contracts with six different companies to implement our SentryIQTM SCA platform covering a combined total of over 212,000 square feet of cultivation space. This product line is important for tactical and strategic reasons, and we hope to offer this as a standalone offering in the future.

| 10 |

Cultivation facilities must have SCA to operate their HVAC equipment. In simple form, SCA is the thermostat in the room, with the occupant selecting the desired temperature set point, the wall thermostat (Sensor) detecting the actual temperature, and when the space temperature deviates from the desired set point the thermostat (Control) commands the furnace or air-conditioner to supply heated or cooled air to bring the room temperature back to the set point. In the case of the cultivation facilities that we serve, there are more environmental conditions to monitor and control (such as temperature, relative humidity, CO2, lighting, vapor pressure deficit status, and more) than in a typical residential home.

Indoor cannabis growers also need to vary and tightly control environmental conditions depending on the stage of plant growth (i.e., clone, vegetative and flowering stages of cannabis cultivation), the time of day, and the plant genetics. In a cultivation facility the desired conditions change many times during the plant’s growth cycle and even within a day, and this is most easily accomplished with a programmable environmental control system (Automation), not unlike a simple programmable thermostat in a home.

Our SentryIQTM SCA package includes precision sensors to measure temperature, humidity, and CO2 levels—more accurately than typical HVAC sensors and within tighter tolerance levels. Our controllers are purpose-built computers programmed by us to ensure our industrial environmental control equipment follows the engineered sequences of operation to obtain desired setpoints. Our sensors connect to our branded controllers through wires installed in the facility, and similarly they are wired to our HVAC equipment (e.g., chillers, fan coils and dehumidifiers) to direct these pieces of equipment. The controllers also provide a user interface on a screen so that they can be easily programmed and controlled to achieve the customer’s environmental objectives, and also giving the cultivator the ability to access this data and react to alerts remotely.

We have entered this business to satisfy our customer’s needs that we did not previously address and that historically was provided by third-party controls contractors. Our entry into the SCA market helps both our customers’ and our business. Our customers benefit because they are saved the extra work of finding and engaging a controls contractor, which allows them to get their facility up and running more quickly by taking one decision off the table and thereby establishing a single point of responsibility for controls implementation. We are also in a position to provide SCA because we know our proprietary equipment better than anyone, thereby ensuring smooth integration with our equipment with no work scope shortcomings, what we refer to as “scope gap.”

From a tactical perspective, with limited incremental selling costs, our current sales team can now offer our SCA package to nearly every prospect since every cultivation facility should have SCA technology. We believe this technology value-added solution gives us an opportunity to achieve incremental project revenue. Strategically, through our SCA package, we are also able to deepen our ongoing relationship with the customer which positions us for a long-term customer relationship by tethering us to the customer through a controls interface (dashboard) to their facility and, eventually, allow our customer to use artificial intelligence (AI) by aggregating environment and growing data to optimize energy use, operating efficiency, and product quality and yield. While there are several other total controls systems providers, we believe that our industry know-how, experience and reputation with climate control equipment may give us a compelling and competitive SCA offering.

Sales and Marketing

Multi-Facility Operator Focus

We plan to have our sales and marketing efforts include a focus on MFOs. However, we face multiple sources of competition in our attempt to penetrate the MFO market.

| ● | First, some companies with multiple cultivation facilities have internal staffs with the requisite expertise to manage their environmental control needs, and who are able to access and engage vendors for both engineering services and equipment without external help. | |

| ● | Second, some large, multi-state and multi-national engineering and construction firms, which have deep engineering and construction management experience and expertise, have entered this market. | |

| ● | Third, we compete with other cannabis-focused service providers, that like us promote their industry expertise and experience. | |

| ● | Fourth, several larger, brand name HVAC equipment manufacturers are now pursuing the cannabis cultivation market directly through their own sales forces. |

| 11 |

We believe we can compete in the MFO market for the following reasons:

| ● | We are one of the oldest and most experienced specialty engineering firms serving the indoor cannabis cultivation market, and we believe that MFOs will value the expertise we have gained from designing environmental control systems for cannabis cultivation facilities since 2016. | |

| ● | Unlike the local and regional engineering firms operating in the market, we have the capability and experience to perform work across the U.S. and Canada, thereby matching the facilities footprint of our MFO prospects. | |

| ● | We believe that the MFOs value the range of experience and expertise that our personnel provide. Our professional staff has expertise covering the gamut, including commercial agriculture, engineering and facility design, HVAC technology, applications and controls, energy efficiency, and sustainability. | |

| ● | We have deep networks with cannabis cultivators, HVAC technical experts, AgTech experts, sustainability leaders, and agricultural resources that we can easily access and bring to bear for the benefit of our customers. | |

| ● | And finally, our 2019 business with four MFOs, covering a total of seven projects with an average contract value of $1.4 million, provides important validation and enhances our credibility in the eyes of other MFOs that we are pursuing. |

Our ability to develop relationships with, and obtain new business from, other MFOs will be critical to generating consistent revenues quarter-over-quarter. During the second half of 2019, we believe certain Canadian MFOs delayed new or expansion projects as access to capital had tightened due to market conditions in that country. Notwithstanding our efforts, there is no assurance that we will be successful in growing and maintaining our business with these MFOs, especially in light of the uncertainty surrounding the potential impact of the coronavirus on our business and the business of our customers and customer prospects.

New Commercial-Scale Projects Driven by Cannabis Legalization

The demand for our environmental control systems is driven primarily by the construction of new cannabis cultivation facilities in the U.S. and Canada. New construction activity is, in turn, driven by state legislation approving either medical or recreational cannabis use. Recent regulatory changes involving medical and/or recreational cannabis use in various jurisdictions, such as California, Michigan, Oklahoma, Utah, Missouri, Illinois and Canada, tend to be a leading indicator for the granting of licenses for new facility construction. As more new cultivation facilities become licensed, we in turn have an expanded set of potential customers that might buy our environmental control systems. However, since both medical and recreational cannabis use remains prohibited under U.S. federal law, uncertainty continues and tends to unfavorably impact the development and financing of new cannabis cultivation facilities in the U.S.

| ● | In the U.S., a total of 33 states (and the District of Columbia) have legalized the medical use of cannabis for over 60 qualifying conditions. Currently, 11 states (and the D.C.), have legalized access to cannabis for recreational use. Now, 68% of the U.S. population is living in a state that has legalized some form of medical or recreational cannabis. | |

| ● | 67% of Americans support full legalization of cannabis, more than double the 31% support in 2000. With increasing consumer acceptance of cannabis and the growth of the industry as a whole, we believe the number of states that allow cannabis use will likely jump even higher in 2020. Consider the following data gathered from various industry sources and publications: In the U.S., more than 24 million persons, or 9.9% of adults age 18 and over consume cannabis regularly, and 115 million report consuming it in their lifetime. There were 2.3 million registered U.S. medical cannabis patients in 2019, up 31% since 2014. | |

| ● | In states where cannabis is currently legal, sales of medical and recreational cannabis are forecasted to grow from $17 billion in 2020 to $30 billion in 2025. | |

| ● | Currently, 18 states are actively debating whether to legalize cannabis for medical or adult-use. There is legislation or referenda being considered in 11 states to legalize cannabis for recreational purposes, including Arizona, New Jersey and New York. There is also legislation or referendums being considered in 7 states to legalize cannabis for medicinal purposes, including South Dakota, Virginia and Georgia. If all 18 states in question were to legalize programs, industry sources believe these states could collectively add $11.4 billion in annual sales to the legal U.S. market by their fourth year of operation. | |

| ● | As of January 16, 2020, there were 975 cannabis-related bills moving through state legislatures and Congress for 2020 sessions. |

| 12 |

The following table sets forth our commercial-scale project bookings, which we define as contracts executed with a value over $100,000 for which we received an initial deposit, by country/state for the years 2016 through 2019. Based on the current economic climate and our downsizing measures, there is no assurance that we will be able to continue to obtain the level of bookings that we had in the past.

| Number of New Commercial-Scale Project Bookings | ||||||||||||||||||||

| 2019 | 2018 | 2017 | 2016 | Total | ||||||||||||||||

| Canada | 9 | 10 | 7 | 1 | 27 | |||||||||||||||

| California | 4 | 3 | - | 3 | 10 | |||||||||||||||

| Michigan | 6 | 4 | - | - | 10 | |||||||||||||||

| Colorado | 1 | - | 2 | 3 | 6 | |||||||||||||||

| Washington | - | 2 | 1 | 3 | 6 | |||||||||||||||

| Oregon | - | - | 2 | 2 | 4 | |||||||||||||||

| Alaska | 1 | - | 1 | 2 | 4 | |||||||||||||||

| Arizona | - | - | 2 | 1 | 3 | |||||||||||||||

| Nevada | 1 | - | 1 | 1 | 3 | |||||||||||||||

| Ohio | 1 | 1 | - | - | 2 | |||||||||||||||

| Rhode Island | - | 1 | 1 | - | 2 | |||||||||||||||

| New Mexico | 1 | 1 | - | - | 2 | |||||||||||||||

| Massachusetts | - | 1 | - | - | 1 | |||||||||||||||

| Texas | - | - | 1 | - | 1 | |||||||||||||||

| Hawaii | - | - | - | 1 | 1 | |||||||||||||||

| Wisconsin | - | - | - | 1 | 1 | |||||||||||||||

| Maryland | - | 1 | - | - | 1 | |||||||||||||||

| Arkansas | - | 1 | - | - | 1 | |||||||||||||||

| Oklahoma | 1 | - | - | - | 1 | |||||||||||||||

| Minnesota | 1 | - | - | - | 1 | |||||||||||||||

| Total | 26 | 25 | 18 | 18 | 87 | |||||||||||||||

Depending on the state of our operations, our marketing efforts will be targeted at MFOs, smaller independent growers, architects working in the cannabis industry, investors and cannabis consulting firms that are actively seeking licenses to produce cannabis in California, Michigan, Missouri, Oklahoma, Massachusetts, Florida, Utah and Illinois. We believe these represent the largest markets, based on the state and local regulatory framework, for our products and services. However, as and when new states pass legislation, we will shift our priorities and/or add new salespeople to pursue new facility construction at the early stage. We believe our marketing efforts will be curtailed for the foreseeable future due to our recent workforce reduction and our efforts to preserve our cash resources as we deal with the uncertainty surrounding the coronavirus.

In the second half of 2019, we noticed softening demand from Canadian prospects due, in part, to limited capital being available for new facilities and an overbuilding of cultivation capacity following federal legalization in October 2018. As a result, Canada now appears to be in a period of correction. By contrast, cultivators in the United States were unable to raise capital so readily, and thus some states are under supplied with cannabis product. We believe this supply imbalance could bode well for companies such as ours as we expect that additional cultivation capacity will be required to meet demand.

Retrofit Market

Existing commercial retrofit projects also represent a business opportunity. The estimated 3,000+ existing commercial grow facilities in North America are easier to identify than new build projects. We believe, based on evidence and our market knowledge, that some of these exiting facilities are operating sub-optimally and have environmental control problems that our products can help remediate. We also believe that the energy consumption of these facilities can be reduced, and we have commenced developing services and products to help them realize savings. We have a full product and service offering in mind, but we expect that the roll-out will take up to two years. However, to expedite this roll-out, we are evaluating possible strategic partners that could add products and services that are an immediate value-add to our customers.

We believe the industry is beginning to recognize the need for our specialized know-how and experience. Although we began targeting this retrofit market segment in 2019, we have only completed one retrofit project to date. We plan to continue our targeted outreach to the operators of these first-generation facilities, although this outreach may be limited based on the current economic climate and our recent downsizing. These facility retrofit projects do not typically carry the uncertainties associated with new build projects such as licensing, permitting and funding. In the future, we also hope to launch an internally developed facility assessment and analysis tool to assist existing facilities in solving their environmental controls challenges.

| 13 |

Our Sales Team

Following our downsizing, our sales team consists of two national accounts representatives, one regional salesperson and our Chief Executive Officer.

Marketing Strategy

Our marketing outreach is conducted primarily through five primary channels: print advertisement, digital advertisement, our website, social media and industry trade shows.

Print Advertisement. We advertise in major industry trade publications such as Cannabis Business Times, Cannabis Tech, Grow Opportunity (Canada), and MJBiz Daily.

Digital Advertisement. We use digital advertising across a larger array of publications. Digital advertising may consist of Surna banners, newsletters, e-blasts and leaderboards on MJBiz Daily, Grow Opportunity, Cannabis Prospect, Cannabis Tech, Contact Canada, Cannabis Business Times, Cultivate and MMJ Daily.

Website. Our website is a consistent source of leads. We revamped our website in 2019 consistent with our new marketing methodology to better identify customer prospects earlier in the cultivator’s vendor decision-making and engagement process.

Social Media. While there are still challenges in this industry to fully take advantage of social media advertising, it is still a meaningful channel to communicate directly with our customers and prospects, we continue to grow our follower base and regularly communicate via Facebook, Twitter, LinkedIn and Instagram.

Trade Shows. We display at industry trade shows and conventions and conduct speaking engagements to achieve industry visibility and presence in a cost-effective manner.

New Build Facility Sales Cycle and Risks

The sales cycles for our new build commercial projects can vary significantly. From pre-sales and technical advisory meetings to sales contract execution, to engineering and design services and equipment delivery, and all the way through installation and commissioning of the installed system, the full cycle can range from six months to two years. Since we do not install the climate control systems, our customers are required to use third-party installation contractors, which adds to the variability of the sales cycle.

The length of our sales cycle for new facilities is driven by numerous factors including:

| ● | the large number of first-time participants interested in the indoor cannabis cultivation business; | |

| ● | the complexities and uncertainties involved in obtaining state and local licensure and permitting; | |

| ● | local and state government delays in approving licenses and permits due to lack of staff or the large number of pending applications, especially in states where there is no cap on the number of cultivators; | |

| ● | the customer’s need to obtain cultivation facility financing; | |

| ● | the time needed, and coordination required, for our customers to acquire real estate and properly design and build the facility (to the stage where climate control systems can be installed); | |

| ● | the large price tag and technical complexities of the climate control and air sanitation system; | |

| ● | availability of power; and | |

| ● | delays that are typical in completing any commercial construction project. |

As a result of the foregoing, there are risks that we may not realize the full contract value of our backlog in a timely manner, or at all. The performance of our obligations under a sales contract, and the timing of our revenue recognition, is dependent upon our customers’ ability to secure funding and real estate, obtain a license and then build their cultivation facility so they can take possession of the equipment—each of which are outside of our control. More recently, as some of our new construction facility projects have become larger and more complex, the likelihood of delays—due to licensing and permitting, lack of or delay in funding, staged facility construction, and/or the shifting priorities of certain customers with multiple facility projects in progress at one time—has increased.

| 14 |

In order to address these risks, the obligations under our sales contracts are generally allocated into the following types of deliverables, and we typically require non-refundable payments from our customers in advance of our performance of services or delivery of equipment. However, in certain situations, especially as we expand our products and services offering for a customer’s entire facility lifecycle, we may extend credit to our customers in which case we are at risk for the collection of account receivables.

Engineering Services. We provide our customer with engineering and design services and drawings. In many cases, the engineering phase is done as part of the license application or building permit process and takes approximately six to eight weeks to complete. Our strategy is to secure the sales contract and commence the engineering and design portion of the project early in the customer’s planning phase of the project. This is important for a number of reasons: (i) we can assist our customers with their engineering and design plans as part of their licensing application process as well as better assure the customer has the right-sized equipment for their application, leading to a higher probability of a successful grow, (ii) we are better positioned to utilize our proprietary equipment for the project at an earlier stage, and (iii) we are able to help reduce a customer’s time to market. Before we commence the engineering phase of the project, we will generally require an advanced payment intended to cover the engineering value of the contract.

Surna Manufactured Equipment. Upon completion of the engineering and design phase, it may take our customer on average six to 12 months to complete the facility build-out, with possible delays due to financing or other aspects which are beyond our control as discussed above. Customer delays in obtaining financing and completing facility build-out make the completion timing of our sales contract unpredictable. For this reason, we require an additional advance payment before we begin manufacturing our proprietary equipment items.

Third-Party Manufactured Equipment. The final phase of our contract typically involves the delivery of third-party manufactured equipment items and other equipment to complete the project. We typically will not deliver until we receive a final advance payment for the remaining contract value. After the project is completed and the environmental control system has been fully installed by third-party installation contractors, we will deploy our technicians to the customer’s cultivation facility to “commission” the system. Commissioning involves testing that the equipment has been properly assembled and installed by the installation contractor and assuring the equipment is operating within the agreed specifications.

Given the timing of the deliverables of our sales contracts, we have often experienced large variances in quarterly revenue. Our revenue recognition is dependent upon shipment of the equipment portions of our sales contracts, which, in many cases, may be delayed while our customers complete permitting, prepare their facilities for equipment installation or obtain project financing.

Competition

Our environmental control systems and our related engineering and design services compete with various national and local HVAC contractors and traditional HVAC equipment suppliers who traditionally resell, design, and implement climate control systems for commercial and industrial facilities, most of whom do not have the specific knowledge that we have about the complexities and challenges of cannabis cultivation. We have positioned ourselves to differ from these competitors by providing engineering and design services and environmental control systems, across all HVAC solutions, including modular chilled water systems, custom air handling units, split systems, packaged roof-top units, and self-contained and complex chilled-water systems, each tailored specifically for managing the distinct challenges involved in indoor cannabis cultivation. We believe our cannabis-specific applications and experience in this market allow us to deliver the right solution to our cultivation customers. Unlike many of our competitors, our solutions are designed specifically for cultivators to provide tight temperature/humidity control, reduce bio-security risk, reduce energy requirements, and minimize maintenance complexity, costs and downtime. However, we are seeing more direct competitors enter into the cannabis market offering the same cannabis-specific climate control systems and engineering services that we offer. We believe this increased competition may adversely impact our ability to obtain new facility projects from both MFOs and independent smaller growers and could require us to accept lower gross margins on our projects.

Intellectual Property

We rely on a combination of patent and trademark rights, licenses, trade secrets, laws that protect intellectual property, confidentiality procedures, and contractual restrictions with our employees and others to establish and protect our intellectual property rights. We have several issued patents and pending patent applications; however, we do not believe that these issued and pending patents currently provide us with any competitive advantage. We have registered trademark registrations around our core Surna brand (“Surna”) in the United States and select foreign jurisdictions, as well as the Surna logo and the combined Surna logo and name in the United States. Our trademark is also registered in the European Union and Canada. Subject to ongoing use and renewal, trademark protection is potentially perpetual. We actively protect our inventions, new technologies, and product developments by maintaining trade secrets and, in limited circumstances, filing for patent protection.

| 15 |

Employees

Following our workforce reduction, we currently have 15 active full-time employees and eight part-time employees. However, we may engage, and have in the past utilized, the services of consultants, independent contractors, and other non-employee professionals. Additional employees may be hired in the future depending on need, available resources, and our achieved growth.

Government Regulation

The use, possession, cultivation, and distribution of marijuana is prohibited by U.S. federal law for medical and recreational purposes. Although certain states have legalized medical and recreational cannabis, companies and individuals involved in the sector are still at risk of being prosecuted by federal authorities. Further, the landscape in the cannabis industry changes rapidly. This means that at any time the city, county, or state where cannabis is permitted can change the current laws and/or the federal government can supersede those laws and take prosecutorial action. Given the uncertain legal nature of the cannabis industry, it is imperative that investors understand that investments in the cannabis industry should be considered very high risk. A change in the current laws or enforcement policy can negatively affect the status and operation of our business, require additional fees, stricter operational guidelines and unanticipated shut-downs.

See the “Risks Related to the Cannabis Industry” set forth in Item 1A of this Annual Report which addresses various risks related to U.S. and foreign regulation and enforcement of cannabis laws and regulations and their potential impact on our business.

Available Information

Our website address is www.surna.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are filed with the U.S. Securities and Exchange Commission (the “SEC”). Such reports and other information filed by us with the SEC are available free of charge through our website when such reports are available on the SEC’s website.

The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov.

The contents of the websites referred to above are not incorporated into this filing. Further, references to the URLs for these websites are intended to be inactive textual references only.

Investing in our common stock involves significant risks. Certain factors may have a material adverse effect on our business, financial condition, and results of operations. You should consider carefully the risks and uncertainties described below, in addition to other information contained in this Annual Report on Form 10-K, including our consolidated financial statements and related notes. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. If any of the following risks actually occurs, our business, financial condition, results of operations, and future prospects could be materially and adversely affected. In that event, the trading price of our common stock could decline, and you could lose part or all of your investment.

Risks Relating to Our Business

Our revenues have been limited, and we will need to obtain financing for future growth, and possibly our operations, which may not be available to us and could dilute the ownership of current shareholders.

Historically, we have raised equity and debt capital to support our operations. We anticipate we will require additional cash resources to finance our growth or other future developments, including the launch of any new products and services and any investments or acquisitions we may decide to pursue. As of December 31, 2019, we had a working capital deficit of approximately $1,437,000 and our cash balance was $922,000. We are likely to need additional funds to complete further development of our business plan to achieve a sustainable sales level where ongoing operations can be funded from operations. We currently have no debt obligations. We will likely need to raise debt or equity financing in the future in order to continue our operations and achieve our growth targets. However, there can be no assurance that such financing will be available in sufficient amounts and on acceptable terms, when and if needed, or at all. The precise amount and timing of our funding needs cannot be determined accurately at this time, and will depend on a number of factors, including market demand for our products and services, the success of our product development efforts, the timing of receipts for customer payments, the management of working capital, and the continuation of normal payment terms and conditions for our purchase of goods and services. The continuation of normal payment terms and conditions with our customers and suppliers, including our ability to obtain advance payments from our customers, significantly impacts our ability to fund our ongoing operations. We believe our cash balances and cash flow from operations will be insufficient to fund our operations and growth for the next 12 months.

| 16 |

To the extent that we raise additional equity capital, existing shareholders will experience a dilution in the voting power and ownership of their common stock, and earnings per share, if any, would be negatively impacted. Our inability to use our equity securities to finance our operations could materially limit our growth. Any borrowings made to finance operations, which are difficult to obtain from most traditional banks due to the federal laws prohibiting cannabis use, could make us more vulnerable to a downturn in our operating results, a downturn in economic conditions, or increases in interest rates on borrowings that are subject to interest rate fluctuations. The amount and timing of such additional financing needs will vary principally depending on the timing of new product launches, investments and/or acquisitions, and the amount of cash flow from our operations. If our resources are insufficient to satisfy our cash requirements, we may seek to issue additional equity or debt securities or obtain a credit facility.

Due to the heightened uncertainty relating to the potential impacts of the coronavirus on our business operations and other headwinds affecting the cannabis industry, we recently implemented a workforce reduction which could adversely impact our day-to-day operations, including our sales and project management activities, and we may not be able to continue our operations.

A number of recent events have had an adverse impact on our operations and financial condition, including constraints on capital availability for our customers and prospects who have commenced, or are contemplating, new and expanded cannabis cultivation facilities and the recent outbreak of COVID-19, a novel strain of coronavirus first identified in China, which has spread across the globe including the U.S. Most recently, the response to this coronavirus by federal, state and local governments in the U.S. has resulted in significant market and business disruptions across many industries and affecting businesses of all sizes. This pandemic has also caused significant stock market volatility and further tightened capital access for most businesses.

As a result of these events, we assessed our near-term operations, working capital, finances and capital formation opportunities, and implemented, in late March 2020, a downsizing of our operations and workforce to preserve cash resources and focus our operations on customer-centric sales and project management activities. The duration and likelihood of success of this workforce reduction are uncertain. If this downsizing effort does not meet our expectations, or additional capital is not available, we may not be able to continue our operations. Other factors that will affect our ability to continue operations include the market demand for our products and services, our ability to service the needs of our customers and prospects with a reduced workforce, potential contract cancellations, project scope reductions and project delays, our ability to fulfill our current backlog, management of our working capital, the availability of cash to fund our operations, and the continuation of normal payment terms and conditions for purchase of our products. In light of these extenuating circumstances, there is no assurance that we will be successful in growing and maintaining our business with MFOs and independent smaller growers. Due to the heightened uncertainty relating to the potential impacts of the coronavirus on our business operations, we believe our cash balances and cash flow from operations will be insufficient to fund our operations for the next twelve months. If our customers or prospects are unable to obtain project financing and we are unable to increase revenues, or otherwise generate cash flows from operations, we will not be able to successfully execute on the various strategies and initiatives we have set forth in this Annual Report to grow our business. The extent to which the coronavirus will impact our business and our financial results will depend on future developments, which are uncertain and cannot be predicted at this time.

Our independent registered public accounting firm has expressed substantial doubt about our ability to continue as a going concern.

We have determined that our ability to continue as a going concern is dependent on raising additional capital to fund our operations and ultimately on generating future profits. Our independent registered public accounting firm has also included a “going concern” explanatory paragraph in its opinion on our financial statements, expressing substantial doubt that we can continue as an ongoing business for the next 12 months. Our financial statements do not include any adjustments that may result from the outcome of this uncertainty. If we are unable to successfully raise the capital we need, we may need to and believe we can reduce the scope of our business to fully satisfy our future short-term liquidity requirements. If we cannot raise additional capital or reduce the scope of our business, we may be otherwise unable to achieve our goals or continue our operations. While we believe that we will be able to raise the capital we need to continue our operations, there can be no assurances that we will be successful in these efforts or will be able to resolve our liquidity issues or eliminate our operating losses.

Even if we obtain more customers, there is no assurance that we will be able to convert our backlog into revenue or make a profit.

We may be unable to convert the full contract value of our backlog in a timely manner, or at all. The performance of our obligations under a sales contract, and the timing of our revenue recognition, is dependent upon our customers’ ability to secure funding and real estate, obtain a license and then build their cultivation facility so they can take possession of the equipment. Our sales contracts currently are not time specific as to when our customers are required to take delivery of our services and equipment. More recently, we determined that some of our new construction facility projects are becoming larger and more complex and, as a result, delays were more likely due to licensing and permitting, lack of or delay in funding, staged facility construction, and/or the shifting priorities of certain customers with multiple facility projects in progress at one time. Even if we obtain more customers, or increase the average size of our projects, there is no guarantee that we will be able to generate a profit. Because we are a small company with limited capital, limited products and services, and limited marketing activities, we may not be able to generate sufficient revenue to operate profitably. If we cannot operate profitably, we may have to suspend or cease operations.

We may extend credit to our customers in the future and, if we are unable to collect these accounts receivable, our future profitability could be adversely impacted.