Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - CHUGACH ELECTRIC ASSOCIATION INC | c004-20191231xex32_2.htm |

| EX-32.1 - EX-32.1 - CHUGACH ELECTRIC ASSOCIATION INC | c004-20191231xex32_1.htm |

| EX-31.2 - EX-31.2 - CHUGACH ELECTRIC ASSOCIATION INC | c004-20191231xex31_2.htm |

| EX-31.1 - EX-31.1 - CHUGACH ELECTRIC ASSOCIATION INC | c004-20191231xex31_1.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number 33-42125

Chugach Electric Association, Inc.

(Exact name of registrant as specified in its charter)

|

Alaska |

92-0014224 |

|||

|

(State or other jurisdiction of |

(I.R.S. Employer |

|||

|

incorporation or organization) |

Identification No.) |

|||

|

|

||||

|

5601 Electron Dr., Anchorage, Alaska |

99518 |

|||

|

(Address of principal executive offices) |

(Zip Code) |

|||

|

|

||||

|

Registrant’s telephone number, including area code |

(907) 563-7494 |

|||

|

|

||||

|

Securities registered pursuant to Section 12(b) of the Act: |

||||

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

||

|

N/A |

N/A |

N/A |

||

|

|

||||

|

Securities registered pursuant to Section 12(g) of the Act: |

||||

|

N/A |

||||

|

(Title of class) |

||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☒ Yes ☐ No

Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☐ Yes ☒ No

(Note: The registrant is a voluntary filer and not subject to the filing requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934. Although not subject to these filing requirements, the registrant has filed all reports that would have been required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months had the registrant been subject to such requirements.)

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

Accelerated filer |

|||

|

Non-accelerated filer |

Smaller reporting company |

|||

|

|

Emerging growth company |

|||

|

|

||||

|

|

||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

☐Yes ☒ No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. N/A

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the last practicable date. NONE

CHUGACH ELECTRIC ASSOCIATION, INC.

2019 Form 10-K Annual Report

Table of Contents

|

|

|||||

|

Page |

|||||

|

|

Item 1. |

2 | |||

|

|

Item 1A. |

7 | |||

|

|

Item 1B. |

15 | |||

|

|

Item 2. |

15 | |||

|

|

Item 3. |

23 | |||

|

|

Item 4. |

23 | |||

|

|

Item 5. |

24 | |||

|

|

Item 6. |

24 | |||

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

25 | ||

|

|

Item 7A. |

42 | |||

|

|

Item 8. |

43 | |||

|

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

90 | ||

|

|

Item 9A. |

90 | |||

|

|

Item 9B. |

91 | |||

|

|

Item 10. |

91 | |||

|

|

Item 11. |

96 | |||

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

102 | ||

|

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

102 | ||

|

|

Item 14. |

102 | |||

|

|

Item 15. |

103 | |||

|

|

Item 16. |

117 | |||

|

|

118 | ||||

1

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

Statements in this report that do not relate to historical facts, including statements relating to future plans, events or performance, are forward-looking statements that involve risks and uncertainties. Actual results, events or performance may differ materially. Readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of the date of this report and the accuracy of which is subject to inherent uncertainty. Chugach Electric Association, Inc. (“Chugach”) undertakes no obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances that may occur after the date of this report or the effect of those events or circumstances on any of the forward-looking statements contained in this report, except as required by law.

General

Chugach was organized as an Alaska electric cooperative in 1948. Cooperatives are business organizations that are owned by their members. As not-for-profit organizations (Internal Revenue Code 501(c)(12)), cooperatives are structured to provide services to their members at cost, in part by eliminating the need to produce profits or a return on equity other than for reasonable reserves and margins. Today, cooperatives in general operate throughout the United States in such diverse areas as utilities, agriculture, irrigation, insurance and credit. All cooperatives are based upon similar principles and legal foundations. Because members’ equity is not considered an investment, a cooperative’s objectives and policies are oriented to serving member interests, rather than maximizing return on investment.

Chugach makes its current and periodic reports available, free of charge, on its website at www.chugachelectric.com as soon as practicable after filing with the Securities and Exchange Commission (“SEC”). The information on Chugach’s website is not a part of this Annual Report on Form 10-K. Chugach’s website also provides a link to the SEC’s website at http://www.sec.gov.

Chugach is one of the largest electric utilities in Alaska. We are engaged in the generation, transmission and distribution of electricity in the Anchorage and upper Kenai Peninsula areas. Chugach is on an interconnected regional electrical system referred to as the Alaska Railbelt, a 400-mile-long area stretching from the coastline of the southern Kenai Peninsula to the interior of the state, including Alaska’s largest cities, Anchorage and Fairbanks. Neither Chugach nor any other electric utility in Alaska’s Railbelt has any connection to the electric grid of the continental United States or Canada. Our principal executive offices are located at 5601 Electron Drive, Anchorage, Alaska 99518. Our telephone number is (907) 563-7494.

Chugach is an electric cooperative that is exempt from federal income taxation as an organization described in Section 501(c)(12) of the Internal Revenue Code. Chugach’s hydroelectric project is licensed by the Federal Energy Regulatory Commission (“FERC”). As such, Chugach is subject to FERC reporting requirements and our accounting records conform to the Uniform System of Accounts as prescribed by FERC. In lieu of state and local ad valorem, income and excise taxes, Alaska electric cooperatives must pay a gross revenue tax to the State of Alaska at the rate of $0.0005 per kilowatt-hour (kWh) of electricity sold in the retail market during the preceding year. This tax is collected monthly and remitted annually. In addition, we currently collect a regulatory

2

cost charge (“RCC”) of $0.000593 per kWh of retail electricity sold. The RCC is assessed to fund the operations of the Regulatory Commission of Alaska (“RCA”) and is collected monthly and remitted to the State of Alaska quarterly. We also collect sales tax on retail electricity sold to consumers in Whittier, seasonally (April through September), and in the Kenai Peninsula Borough, monthly. This tax is remitted to the City of Whittier monthly and to the Kenai Peninsula Borough quarterly. These taxes are a direct pass-through to consumer bills and therefore do not impact our margins.

We had 295 employees as of March 16, 2020. Approximately 70% of our employees are members of the International Brotherhood of Electrical Workers (“IBEW”). Chugach has three Collective Bargaining Unit Agreements (“CBA”) with the IBEW. We also have a CBA with the Hotel Employees and Restaurant Employees (“HERE”). All of the CBA’s have been renewed through June 30, 2021. The three IBEW CBAs provide for wage and pension contribution increases in all years and include health and welfare premium cost sharing provisions. The HERE CBA provides for wage, pension contribution, and health and welfare contribution increases in all years. We believe our relationship with our employees is good.

Our members are the consumers of the electricity sold by us. As of December 31, 2019, we had one wholesale customer, 69,320 retail members, and 84,327 service locations, including idle services. No individual retail customer accounts for more than ten percent of our revenue. Our customers’ requirements for capacity and energy generally peak in fall and winter as home heating and lighting needs rise and then decline in the spring and summer as the weather becomes milder and daylight hours increase.

We supply power to the City of Seward (“Seward”) as a wholesale customer. Occasionally we sell available generation, in excess of our own needs, to Matanuska Electric Association, Inc. (“MEA”), Homer Electric Association, Inc. (“HEA”), Golden Valley Electric Association, Inc. (“GVEA”) and Anchorage Municipal Light & Power (“ML&P”).

Our customers are billed on a monthly basis per a tariffed rate for electrical power consumed during the preceding period. Billing rates are approved by the RCA, see “Item 1 – Business – Rate Regulation and Rates.” Base rates (derived on the basis of historic cost of service including margins) are established to generate revenues in excess of current period costs in any year and such excess is designated on our Consolidated Statements of Operations, Consolidated Statements of Changes in Equities and Margins, and Consolidated Statements of Cash Flows as “Assignable margins.” Retained assignable margins are designated on our Consolidated Balance Sheet as “Patronage capital” which is assigned to each member on the basis of patronage. Patronage capital is held for the account of the members without interest and returned when the Chugach Board of Directors deems it appropriate to do so.

In 2019, we had 531.2 megawatts (“MW”) of installed generating capacity (rated capacity) provided by 16 generating units at our five owned power plants: Beluga Power Plant, International Station Power Plant (historically known as “IGT”), Cooper Lake Hydroelectric Project, Southcentral Power Project (“SPP”), in which we own a 70% interest, and Eklutna Hydroelectric Project, in which we own a 30% interest. Of the 531.2 MW of installed generating capacity, approximately 87% was fueled by natural gas. The rest of our owned generating resources were hydroelectric facilities. In 2019, 81% of Chugach’s power, including purchased power, was generated from gas. Of that gas-fired generation, 82% took place at SPP and 7% took place at Beluga. SPP furnishes up to 200.2 MW of capacity; Chugach owns 70% of this plant’s output and ML&P owns the remaining 30%. The Bradley Lake Hydroelectric Project, which is not owned by Chugach, provides up to 27.4 MW,

3

as currently operated, for our retail customers and up to 0.9 MW for our wholesale customer. For more information concerning Bradley Lake, see “Item 2 – Properties – Other Property – Bradley Lake.” In addition, we purchase up to 17.6 MW from Fire Island Wind, LLC (“FIW”), annually. We operate 1,727 miles of distribution line and 436 miles of transmission line, which includes Chugach’s share of the Eklutna transmission line. For the year ended December 31, 2019, we sold 1.1 billion kWh of electrical power.

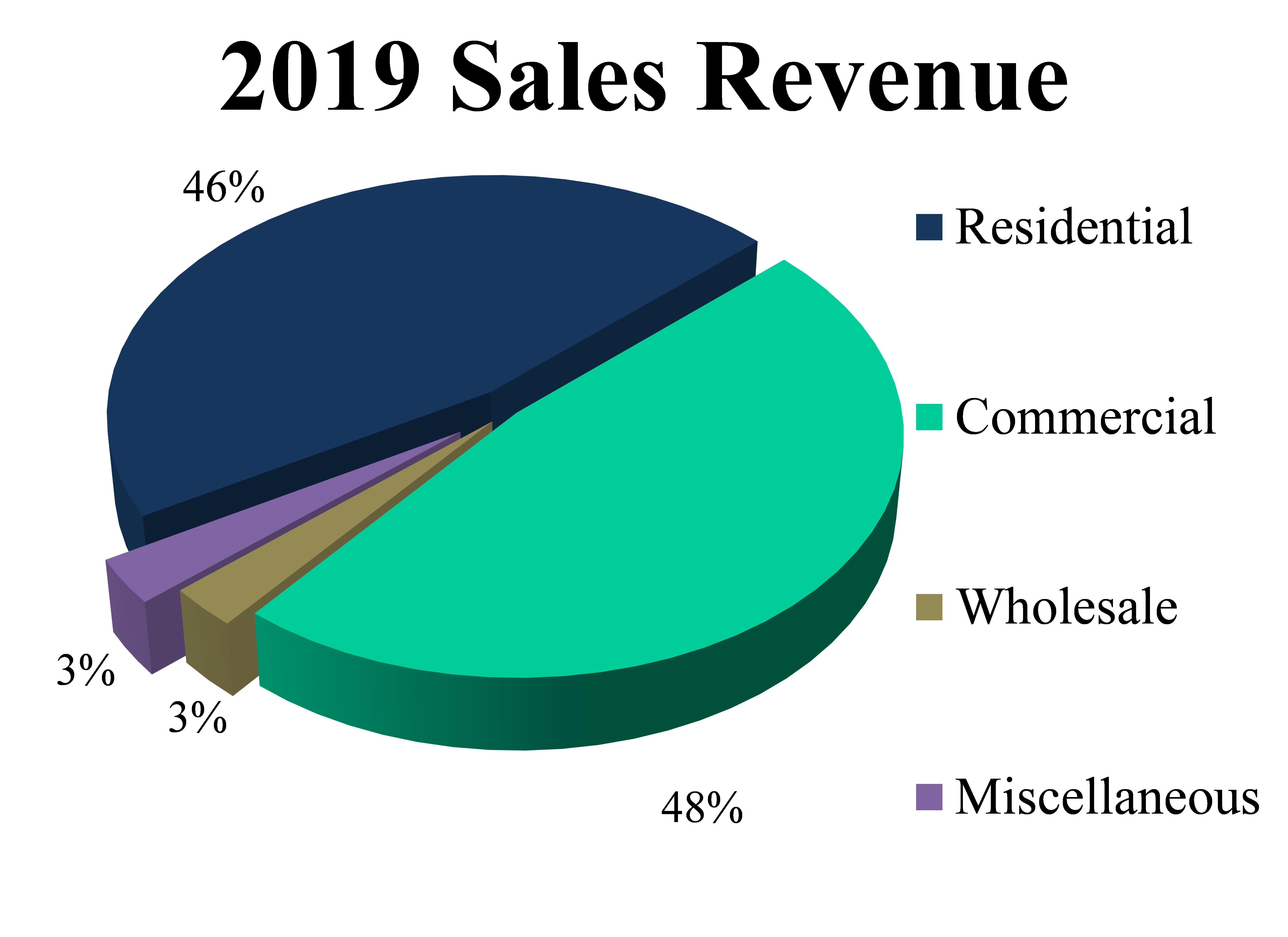

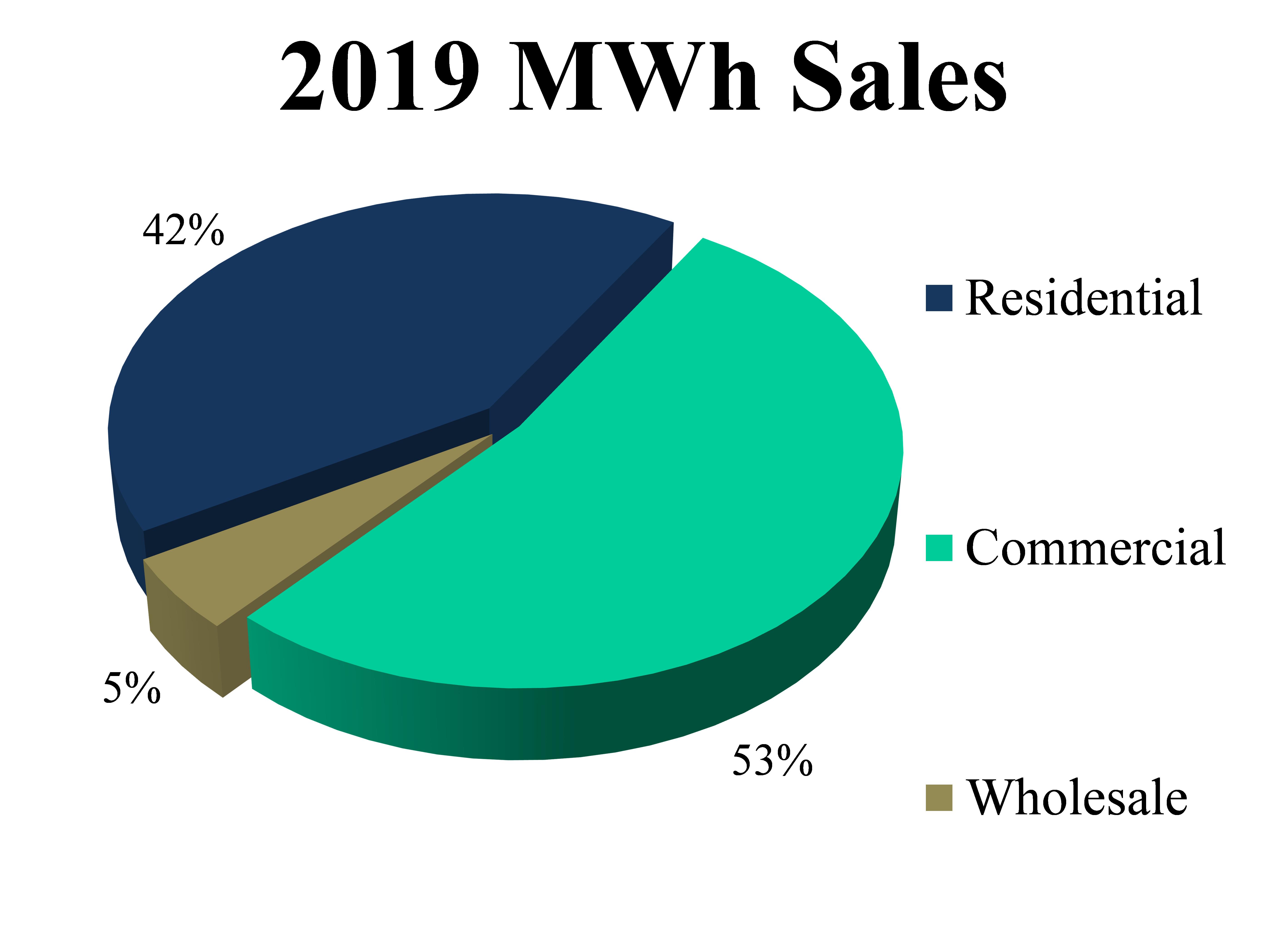

Customer Revenue from Sales

|

|

|

|

Miscellaneous revenue includes economy energy and capacity sales to GVEA, MEA, HEA and ML&P.

Retail Service Territory

Our retail service area covers most of the Municipality of Anchorage, excluding downtown Anchorage, as well as remote mountain areas and villages. The service area ranges from Anchorage to the northern Kenai Peninsula westward to Tyonek, including Fire Island, and eastward to Whittier.

Retail Customers

As of December 31, 2019, we had 69,320 members receiving power from 84,327 service locations, including idle services (some members are served by more than one service). Our customers are a mix of urban and suburban. The urban nature of our customer base means that we have a relatively high customer density per line mile. Higher customer density means that fixed costs can be spread over a greater number of customers. As a result of lower average costs attributable to each customer, we benefit from greater stability in revenue, as compared to a less dense distribution system in which each individual customer would have a more significant impact on operating results. For the past five years no retail customer accounted for more than ten percent of our revenues. The revenue contributed by retail customers for the years ended December 31, 2019, 2018 and 2017 is discussed in “Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations – Year ended December 31, 2019, compared to the year ended December 31, 2018, and the year ended December 31, 2018, compared to the year ended December 31, 2017 – Revenues.”

4

Wholesale Customers

We are the principal supplier of power to the City of Seward (“Seward”) under a wholesale power contract. Our wholesale power contract, including the fuel and purchased power components, contributed $5.8 million, $5.2 million, and $5.9 million in revenues for the years ended December 31, 2019, 2018 and 2017, respectively.

Seward

We currently provide nearly all the power needs of the City of Seward. Sales to Seward represented approximately 5% of Chugach’s total energy sales for the years ended December 31, 2019, 2018, and 2017. We entered into the 2006 Agreement for the Sale and Purchase of Electric Power and Energy between Chugach Electric Association, Inc. and the City of Seward (“2006 Agreement”), effective June 1, 2006. The 2006 Agreement contains an evergreen clause providing for two (2) automatic five-year extensions unless written notice is provided at least one year prior to the expiration date. Neither Chugach nor Seward provided written notice to terminate as both utilities desired to extend the term of the agreement. Accordingly, on June 2, 2016, Chugach submitted an updated listing of its special contracts to reflect the extension of the expiration date of the 2006 Agreement from December 31, 2016 to December 31, 2021. On July 18, 2016, the RCA approved the filing. Since both extensions provided in the 2006 Agreement have been exercised, the current contract will expire December 31, 2021, unless extended.

The 2006 Agreement is an interruptible, all-requirements/no generation capacity reserves contract. It has many of the attributes of firm service, especially in the requirement that so long as Chugach has sufficient power available, it must meet Seward’s needs for power. However, service is interruptible because Chugach is under no obligation to supply or plan for generation capacity reserves to supply Seward and there is no limit on the number of times or hours per year that the supply can be interrupted. Counterbalancing this is the requirement that Chugach must provide power to Seward if Chugach has the power available after first meeting its obligations to its retail customers for whom Chugach has an obligation to provide reserves. The price under the 2006 Agreement reflects the reduced level of service because no costs of generation in excess of that needed to meet the system peak is assigned to Seward.

Economy Customers

Occasionally, Chugach sells available generation, in excess of its own needs, to other electric utilities. Sales are made under the terms and conditions of Chugach’s economy energy sales tariff. The price includes the cost of fuel, variable operations and maintenance expense, wheeling charges and a margin.

We’ve made non-firm, economy energy sales to GVEA, HEA, MEA, and ML&P on an as needed basis. Total non-firm sales were 195 MWh, 379 MWh, and 48,526 MWh for 2019, 2018, and 2017, respectively.

5

Rate Regulation and Rates

The RCA regulates our rates. We seek changes in our base rates by submitting Simplified Rate Filings (“SRF”) or through general rate cases filed with the RCA on an as-needed basis. Chugach’s base rates, whether set under a general rate case or an SRF, are established to allow the continued recovery of our specific costs of providing electric service. In each rate filing, rates are set at levels to recover all of our specific allowable costs and those rates are then collected from our retail and wholesale customers.

Alaska Statute 42.05.175 requires the RCA to issue a final order no later than 15 months after a complete tariff filing is made for a tariff filing that changes a utility’s revenue requirement or rate design. It is within the RCA’s authority to authorize, after a notice period, rate changes on an interim, refundable basis. In addition, the RCA has been willing to open limited reviews of matters to resolve specific issues from which expeditious decisions can often be rendered.

The RCA has exclusive regulatory control of Chugach’s retail and wholesale rates, subject to appeal to the Alaska courts. The regulatory environment in Alaska requires cooperatives to use a debt service coverage approach to ratemaking. Times Interest Earned Ratio (“TIER”) is designed to ensure Chugach maintains a coverage ratio that allows Chugach to remain in compliance with its debt covenants. Under Alaska law, financial covenants of an Alaskan electric cooperative contained in a debt instrument will be valid and enforceable, and rates set by the RCA must be adequate to meet those covenants. Under Alaska law, a cooperative utility that is negotiating to enter into a mortgage or other debt instrument that provides for a TIER greater than the ratio the RCA most recently approved for that cooperative must submit the mortgage or debt instrument to the RCA before the instrument takes effect. The rate covenants contained in the instruments governing our outstanding long-term indebtedness do not impose any greater TIER requirement than those previously approved by the RCA.

Chugach expects to continue to recover changes in its fuel and purchased power expenses through routine quarterly filings with the RCA, see “Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations - Results of Operations – Overview – Rate Regulation and Rates – Fuel and Purchased Power Recovery.”

The Second Amended and Restated Indenture of Trust (“Indenture”), which became effective January 20, 2011, governs all of our outstanding bonds and requires us to set rates expected to yield margins for interest equal to at least 1.10 times total interest expense. The Second Amended and Restated Master Loan Agreement with CoBank, ACB (“CoBank”) which became effective June 30, 2016, also requires Chugach to establish and collect rates reasonably expected to yield margins for interest equal to at least 1.10 times total interest expense. The Credit Agreement with National Rural Utilities Cooperative Finance Corporation (“NRUCFC”), KeyBank National Association, Bank of America, N.A., Wells Fargo Bank N.A., and CoBank, which governs the unsecured credit facility Chugach may use to meet its obligations under its commercial paper program, also requires Chugach to maintain minimum margins for interest of at least 1.10 times interest charges for each fiscal year.

For the years ended December 31, 2019, 2018 and 2017, our Margins for Interest/Interest (“MFI/I”) was 1.23, 1.24, and 1.27, respectively. For the same periods, our TIER was 1.24, 1.26, and 1.28, respectively.

6

Our Service Areas and Local Economy

Our service areas and the service area of our wholesale customer reside within the Alaska Railbelt region of Alaska which is linked by the Alaska Railroad.

Anchorage is located in the Southcentral region of Alaska, serving as a major center for many state governmental functions. Anchorage’s economy is also supported by a large federal government and military presence. With established air, sea, and rail transportation facilities, many businesses are headquartered in Anchorage, while operating tourism, medical, educational, petroleum, mining, financial and other industries throughout the state.

Seward is a city located at the head of Resurrection Bay on the Kenai Peninsula. Seward, which is approximately 127 miles south of Anchorage, is a major fisheries port and also serves as the ocean terminus of the Alaska Railroad. Seward’s other major industry is tourism.

Sales Forecasts

The following table sets forth our projected sales forecasts for the next five years:

|

|

||||||||||

|

Sales (MWh) |

2020 |

2021 |

2022 |

2023 |

2024 |

|||||

|

Retail |

1,069,556 | 1,066,892 | 1,069,601 | 1,067,943 | 1,066,435 | |||||

|

Wholesale |

56,641 | 55,831 | 56,356 | 55,681 | 54,750 | |||||

|

Total |

1,126,197 | 1,122,723 | 1,125,957 | 1,123,624 | 1,121,185 |

Generally, energy sales are expected to slightly decline due to slow economic growth, progress in energy efficiency and conservation, and warmer than average temperatures, which creates decreased energy use in our service territory. Actual sales may vary with changing weather, end-use efficiency, and economic conditions. These projections are based on assumptions that management believes to be reasonable as of the date the projections were made. The occurrence of a significant change in any of the assumptions could affect a change in the projected sales forecast.

Chugach’s consolidated financial results will be impacted by weather, the economy of our service territory, fuel availability and prices, and the decisions of regulatory agencies. Our creditworthiness will be affected by national and international monetary trends, general market conditions and the expectations of the investment community, all of which are largely beyond our control. In addition, the following statements highlight risk factors that, in the view of management, may significantly affect our consolidated financial condition, results of operations, and cash flows. This discussion is not exhaustive. You may view risks differently than we do, or there may be other risks and uncertainties which you consider important which are not discussed. These risks, whether discussed below or those unknown, could negatively affect our business operations and financial condition. The statements below must be read together with factors discussed elsewhere in this document and in our other filings with the SEC.

7

Financing

On May 15, 2019, Chugach issued $75.0 million of First Mortgage Bonds, 2019 Series A, due May 15, 2049 (the “Bonds”). The Bonds were issued for the purpose of repaying outstanding commercial paper used to finance Chugach’s capital improvement program and for general corporate purposes. The Bonds bear interest at the rate of 3.86%. Interest on the Bonds is due each May 15 and November 15, commencing on November 15, 2019. Principal on the Bonds is due in varying installment amounts on an annual basis beginning on May 15, 2021, resulting in an average life of approximately 12.0 years. The Bonds are secured, ranking equally with all other long-term obligations, by a first lien on substantially all of Chugach’s assets, pursuant to the Seventh Supplemental Indenture to the Second Amended and Restated Indenture of Trust (“the Indenture”).

On July 30, 2019, Chugach entered into an amendment to the senior unsecured credit facility used to backstop Chugach’s commercial paper program. This amendment increased the facility from $150.0 million to $300.0 million, as well as extended the maturity date from June 13, 2021, to July 30, 2024. Chugach is expected to continue to issue commercial paper in 2020, as needed. For additional information concerning our commercial paper program, see “Item 8 – Financial Statements and Supplementary Data – Note 11 – Debt – Commercial Paper.” No assurance can be given that Chugach will be able to continue to access the commercial paper market. If Chugach were unable to access that market, this facility would effectively replace Chugach’s commercial paper program. The cost of raising money in the debt capital markets could increase while the availability of funds from those markets could diminish as a result of volatile global financial markets and economic conditions.

Credit Ratings

Changes in our credit ratings could affect our ability to access capital. We maintain a rating from Standard & Poor's Rating Services (“S&P”) of “A” (Stable). Our implied secured and unsecured ratings from Fitch Ratings (“Fitch”) of "A" (Rating Watch Evolving) were withdrawn and replaced with an Issuer Default Rating (“IDR”) of “A” (Rating Watch Negative). Fitch’s Rating Watch revision is driven by the expected higher net leverage profile following the pending acquisition of ML&P, see “Item 8 – Financial Statements and Supplementary Data – Note 16 – ML&P Acquisition.” S&P and Moody's currently rate our commercial paper at "A-1" and "P-2", respectively. If these agencies were to downgrade our ratings, particularly below investment grade, our commercial paper rates could increase immediately and we may be required to pay higher interest rates on financings. Additionally, our potential pool of investors and funding sources could decrease.

Natural disasters

Natural disasters or other catastrophic events may cause damage or disruption to our operations, and thus could have a strong negative effect on us. Our business operations are subject to interruption by natural disasters and other events beyond our control. Although we maintain crisis management and disaster response plans, such events could make it difficult or impossible for us to deliver our services to our customers. Our generation, transmission, distribution, corporate headquarters, information technology systems, and other critical business operations, are located near major seismic faults. Earthquakes and other catastrophic events, such as wild fires, floods, or other similar occurrences, could interrupt fuel supplies; affect demand for electricity or natural gas; cause unplanned outages or reduce generating output; damage

8

Chugach’s assets or operations; damage the assets or operations of third parties on which Chugach relies; damage property owned by customers or others; and cause personal injury or death. As a result, we could incur costs to purchase replacement power, to repair assets and restore service, and to compensate third parties. Because significant recovery time could be required to resume operations, our financial condition and operating results could be materially adversely affected in the event of a major earthquake or other catastrophic event.

War, acts and threats of terrorism, sabotage, and other significant events could adversely affect our operations

We cannot predict the impact that any future terrorist attacks or sabotage may have on the energy industry in general, or on our business in particular. Any such event may affect our operations in unpredictable ways, such as changes in insurance markets or instability in financial markets. Furthermore, electric generation, transmission and distribution facilities could be direct targets of, or indirect casualties of, an act of terror or sabotage. Chugach has not experienced any disruptions or significant costs associated with intentional attacks. While Chugach has numerous programs in place to safeguard our operating systems, a physical compromise of our facilities could adversely affect our ability to manage our facilities effectively.

Pandemics

In late 2019, a novel strain of the coronavirus was discovered in China. We cannot be certain if or to what extent this outbreak may impact our operations. While we do not have operations in China, the spread of this virus across the globe may impede our ability to obtain parts or have parts refurbished for our generation, transmission and distributions assets or for our fleet. If an outbreak occurred and a significant portion of our workforce fell ill, our ability to maintain operations could be materially impacted.

Cybersecurity

Data breach, system crashes and ransomware or terrorism risks are mitigated by maintaining technical systems that detect and prevent these attacks and by training employees to recognize cyber threats. Chugach has not experienced any disruptions or significant costs associated with intentional attacks or unauthorized access to any of our systems.

Chugach is working with the other Railbelt utilities to develop a set of cybersecurity standards comparable to the North American Electric Reliability Corporation/Critical Infrastructure Protection (“NERC/CIP”) standards. In June 2016, in response to RCA Docket I-16-002, Railbelt Utility Information Technology and Operations Technology leadership began meeting to discuss Railbelt Cybersecurity. The Railbelt Utilities Managers group designated the Cybersecurity Working Group to review industry standards and provide a statement of work to develop Railbelt Cybersecurity Standards. A final draft was presented to the Railbelt Utility Managers on February 14, 2019. On July 10, 2019, a status was provided to the RCA from the Railbelt Utility Managers announcing the completion of Alaska Critical Infrastructure Protection (“AKCIP”) Cybersecurity Standards, and collective agreement to adopt them effective January 1, 2020, and implement them according to the implementation schedules contained in the specific standards.

While Chugach has numerous programs in place to safeguard our operating and business systems and the personal information of our customers and employees, a cyber security compromise of our facilities could adversely affect our ability to manage our facilities and operate effectively.

9

Pension Plans

We participate in the Alaska Electrical Pension Fund (“AEPF”). The AEPF is a multiemployer pension plan to which we make fixed, per employee contributions through our collective bargaining agreement with the IBEW, which covers our IBEW-represented workforce. We do not have control over the AEPF. Chugach receives information concerning its funding status annually. There is no contingent liability at this time. If a funding shortfall in the AEPF exists, we may incur a contingent withdrawal liability.

We also participate in the National Rural Electric Cooperative Association (“NRECA”) Retirement Security Plan (“RS Plan”), a multiemployer defined benefit master pension plan maintained and administered by NRECA for the benefit of its members and their employees. All employees not covered by a union agreement become participants in the RS Plan. We do not have control over the RS Plan. The RS Plan updates contribution rates on an annual basis to maintain the health of the plan under the plans rules allowed by the Employee Retirement Income Security Act (“ERISA”). The RS Plan’s funding status is governed by plan rules as provided by ERISA. Chugach receives information concerning its funding status biannually. The RS Plan is not subject to the Pension Protection Act of 2006 under a permanent exemption from Congress as of December 16, 2014. Poor investment performance could increase our costs if underfunding occurs.

On December 14, 2016, the Chugach Board of Directors approved a prepayment of $7.9 million to the NRECA Retirement Security plan. Using the low interest rate environment, this prepayment will mitigate some of the impact of future contribution increases and will lower annual budgetary impacts of current contributions over an 11-year term.

Equipment Failures and Other External Factors

The generation and transmission of electricity requires the use of expensive and complex equipment. While we have maintenance programs for existing equipment, along with a contractual service plan in place for SPP, generating plants are subject to unplanned outages because of equipment failure or environmental disasters. In the event of unplanned outages, we must acquire power, which is not otherwise available from the fleet of Chugach generators, from other sources at unpredictable costs in order to supply our customers and comply with our contractual agreements. The fuel and purchased power rate adjustment process allows Chugach to recover current purchased power costs and to recover under-recoveries or refund over-recoveries with a three-month lag. If Chugach were to materially under-recover purchased power costs due to an unplanned outage, we would normally seek an increase in the rate adjustment to recover those costs at the time of the next quarterly fuel and purchased power rate adjustment filing. As a result, cash flows may be impacted due to the lag in payments for purchased power costs and the corresponding collection of those costs from customers. To the extent the regulatory process does not provide for the timely recovery of purchased power costs, Chugach could experience a material negative impact on its cash flows. Chugach has line of credit and commercial paper borrowing capacity to mitigate this risk.

10

Fuel Supply

In 2019, 81% of our electric energy was generated from natural gas. Our primary sources of natural gas in 2019 were Hilcorp and Chugach’s 10% share of the Beluga River Unit (“BRU”). The BRU is expected to provide approximately 15% of Chugach’s gas requirements through 2037. The BRU gas and Chugach’s current gas contracts are expected to meet 100% of Chugach’s needs through March 31, 2028. In addition to Hilcorp, Chugach has agreements with AIX Energy, LLC, Cook Inlet Energy (“CIE”), and Furie Operating Alaska, LLC (“Furie”), which provide a structure to purchase supplemental gas, adding diversity in Chugach’s sources of natural gas to meet system load requirements.

In May 2017, the RCA approved the Furie Agreement. The Furie Agreement provides Chugach with both firm and non-firm gas supplies over a 16-year period, with firm purchases beginning on April 1, 2023, and ending March 31, 2033, and interruptible gas purchases available to Chugach immediately and ending on March 31, 2033. With respect to firm purchases beginning on April 1, 2023, and ending on March 31, 2033, the Furie Agreement provides an annual gas commitment by Furie to sell and Chugach to purchase approximately 1.8 billion cubic feet (Bcf) of gas each year, which represents approximately 20% to 25% of Chugach’s projected gas requirements during this period. The Furie Agreement also provides Chugach with additional purchase options, on a firm and interruptible basis. The initial price for firm gas is $7.16 per thousand cubic feet (Mcf) beginning April 1, 2023 and escalates annually rising to $7.98 per Mcf on April 1, 2032, the last year of the contract.

Furie filed for Chapter 11 bankruptcy protection in August 2019 and is currently in ongoing negotiations. We are waiting the outcome to determine any impact to our agreement.

The State of Alaska’s Department of Natural Resources (“DNR”) published a study in March 2018, “Cook Inlet Natural Gas Availability,” to provide an estimate of additional Cook Inlet gas that could be recovered through additional investment and how long Cook Inlet gas production can continue to meet existing demand levels. The 2018 DNR study concluded there is potentially 500-800 Bcf of additional gas to be developed at the economical price range of $6-8/Mcf (using 2016 currency values); however, at a price greater than $12/Mcf as much as 800-1,000 Bcf of additional gas could be developed. The 2018 DNR study also concluded there was sufficient Cook Inlet gas to satisfy the current demand of 80 Bcf/year to meet the demand until around 2030, under the assumptions and simplifications used therein. The 2018 DNR study did not attempt to forecast Cook Inlet gas prices.

The 2015 DNR study estimated there are 1,183 Bcf of proved and probable reserves remaining in Cook Inlet’s legacy fields. The 2015 DNR estimate did not include reserves from a large gas field developed and in production by Furie and another that was developed by BlueCrest Alaska Operating, LLC. Furie constructed an offshore gas production platform, Julius R, in 2015 and achieved commercial production. The platform and other production facilities are designed for up to 200 million cubic feet (MMcf) per day.

Chugach continues to explore other alternatives to diversify its portfolio.

11

Cook Inlet Natural Gas Storage Alaska (“CINGSA”) began service April 1, 2012. The facility ensures local utilities, including Chugach, have gas available to meet deliverability requirements during peak periods and store gas during low demand periods. The RCA approved inception rates and a tariff for the CINGSA facility and a Firm Storage Service (“FSS”) Agreement between the seller and Chugach in 2011. Injections into the facility began in 2012. Chugach's share of the capacity was 1.6 Bcf in 2019. Chugach is entitled to withdraw gas at a rate of up to 31 MMcf per day.

Recovery of Fuel and Purchased Power Costs

The RCA approved inclusion of all fuel, purchased power, and transportation costs related to our current contracts and the BRU in the calculation of Chugach’s fuel and purchased power adjustment process which will ensure, in advance, that costs incurred under the contracts can be recovered from Chugach’s customers. The fuel and purchased power adjustment process collects under-recoveries and refunds over-recoveries from prior periods with minimal regulatory lag. Chugach's fuel and purchased power adjustment process includes quarterly filings with the RCA, which set the rates on projected costs, sales and system operations for the quarter. Any under- or over-recovery of costs is incorporated into the following quarterly filing. Chugach under-recovered $1.4 million at December 31, 2019, and over-recovered $3.4 million at December 31, 2018. To the extent the regulated fuel and purchased power adjustment process does not provide for the timely recovery of costs, Chugach could experience a material negative impact on its cash flows. Chugach has line of credit and commercial paper borrowing capacity to mitigate this risk.

Regulatory

Chugach’s billing rates are approved by the RCA and Chugach is required to submit filings to the RCA for approval before any rate changes can be implemented. Chugach is currently a participant in the SRF process for adjustments to base demand and energy rates for Chugach retail customers and wholesale customer, Seward. SRF is an expedited base rate adjustment process available to electric cooperatives in the State of Alaska, with filings made either on a quarterly or semi-annual basis. Chugach is a participant on a quarterly filing schedule basis. While there is no limitation on decreases, base rate increases under SRF are limited to 8% in a 12-month period and 20% in a 36-month period. Chugach is also permitted to cease participation under the SRF process and adjust rates through general rate case filings, which do not have limitations on rate adjustments. For more information see “Item 8 - Financial Statements and Supplementary Data – Note 5 – Regulatory Matters – Simplified Rate Filings.”

To the extent the RCA does not allow for the recovery of our costs associated with our current or anticipated rate cases, Chugach could experience a material negative impact on its results of operations, financial position and cash flows.

Accounting Standards or Practices

We cannot predict the impact that future changes in accounting standards or practices may have on public companies in general, the energy industry or our operations specifically. New accounting standards could be issued that could change the way we record revenues, expenses, assets and liabilities. These changes in accounting standards could adversely affect our reported earnings or could increase reported liabilities.

12

Greenhouse Gas Regulations, Carbon Emission and Climate Change

Power plants are one of the largest sources of carbon emissions in the United States. Impacts of potential regulations regarding greenhouse gases (“GHG”), carbon emissions, and climate change on Chugach’s operations remain uncertain as political momentum changed with the 2016 presidential election. An Executive Order promoting energy independence and economic growth was issued on March 28, 2017, by the President instructing the Environmental Protection Agency (“EPA”) to review the Clean Power Plan (“CPP”). On August 21, 2018, the EPA moved forward with the Affordable Clean Energy (“ACE”) proposed regulation which would establish emission guidelines for states to develop plans to address GHG emissions from existing coal-fired power plants. The final ACE rule was issued by the EPA on June 19, 2019. The final rule is certain to face legal challenge. The ACE rule, in its current form, is not expected to have a material effect on Chugach’s financial condition, results of operations, or cash flows.

Additional costs related to a GHG tax or cap and trade program, if enacted by the U.S. Congress, or other regulatory action, could affect the relative cost of the energy Chugach produces. While Chugach cannot predict the implementation of any additional new law or regulation, or the limitations thereof, it is possible that new laws or regulations could increase capital and operating costs. Chugach has obtained or applied for all Clean Air Act permits currently required for the operation of generating facilities.

Other Environmental Regulations

Chugach is currently required to comply with numerous federal, state and local laws and regulations relating to the protection of the environment. While we believe Chugach has obtained all material environmental-related approvals currently required to own and operate our facilities, Chugach may incur significant additional costs because of compliance with these requirements in addition to costs related to any costs of compliance with laws or regulations relating to GHG or carbon emissions. Failure to comply with environmental laws and regulations could have a material effect on Chugach, including potential civil or criminal liability and the imposition of fines or expenditures of funds to bring our facilities into compliance. Delay in obtaining, or failure to obtain and maintain in effect any environmental approvals, or the delay or failure to satisfy any applicable environmental regulatory requirements related to the operation of our existing facilities could result in significant additional costs to Chugach and a material adverse impact to Chugach’s results of operations, financial condition, and cash flows.

Aging Plant

Some of our facilities were constructed over 30 years ago and, as a result, may require significant capital expenditures to maintain efficiency and reliability. As plant equipment ages, the potential for operational issues such as unscheduled outages increases which could negatively impact our cost of electric service. With the addition of the SPP generating facility, which began operation in 2013, we are able to significantly reduce the reliance on some of the older facilities. The older units are used for peaking, and, in the future, may be primarily used as a reserve. Mitigating the aging risk is Chugach’s experienced work force, extensive maintenance program, and predictive maintenance measures. Also mitigating the risk of significant unanticipated capital expenditures associated with generation maintenance is a long-term service agreement smoothing major maintenance costs for our largest power producer, SPP. If approved, the ML&P acquisition will improve the efficiency and economics of power generation through the joint dispatch of the acquired generating assets.

13

Distributed Generation

Distributed generation technologies, such as combined heat and power, solar cells, micro turbines, fuel cells, batteries, and wind turbines currently exist or are in development. Significant technological advancements or positive perceptions regarding the environmentally friendly benefits of self-generation and distributed energy technologies could lead to the adoption of these technologies by our members. Increased adoption of these technologies by our members could reduce demand for electricity and the pool of customers from whom we recover fixed costs. This could have a negative impact on our business, financial condition, or cost of electric service.

Constraints on Transmission

We currently experience occasional constraints on our transmission system and those of other utilities used to transmit energy from our remote generators to loads due to periodic maintenance activities, equipment failures and other system conditions. We manage these constraints using alternative generation dispatch and energy purchasing patterns. The long-term solution for reducing transmission constraints include purchasing additional wheeling service from other utilities, or construction of additional transmission lines which would require significant capital expenditures.

Construction of new transmission lines presents numerous challenges. Environmental, state and local permitting processes can result in significant inefficiencies and delays in construction. These issues are unavoidable and are addressed through long-term planning. We typically begin planning new transmission at least 10 years in advance of the need and foster and participate in regional and interregional transmission planning and cost allocation discussions with neighboring transmission providers. In the event that we are unable to complete construction of planned transmission expansion, we must rely on purchases of electric power, which could put increased pressure on electric rates.

We also rely on transmission to access state-owned Bradley Lake power on the Kenai Peninsula. The Swan Lake fire that started in June 2019 and reached over 167,000 acres damaged this transmission line. Due to the loss of access to this power, more natural gas was consumed for generation until the line could be repaired and placed back in service.

Counterparties

We rely on other entities in the production of power and supply of fuel and therefore, we are exposed to the risk that these counterparties may default in performance of their obligations to us. As a 70% owner in SPP, a 30% owner in the Eklutna Hydroelectric Project, and a 10% owner in the Beluga River Unit (“BRU”), we rely upon the other owners to fulfill their contractual and financial obligations. Additionally we rely on numerous other entities with whom we have purchased power agreements. Failure of our counterparties to perform their obligations could increase the cost of electric service we provide to our members as we, for example, may be forced to enter into alternative contractual arrangements or purchase energy or natural gas at prices that may exceed the prices previously agreed upon with the defaulting counterparty.

14

ML&P Acquisition

In December 2017, the Mayor of Anchorage, Alaska, announced plans to place a proposition on the April 3, 2018 municipal ballot allowing the voters to authorize the sale of ML&P to Chugach. The proposition was approved by Anchorage voters 65.08% to 34.92% per the certified election results. Chugach and the Municipality of Anchorage (“MOA”) negotiated final sales agreements and associated documents. The sale of ML&P was approved by the Anchorage Assembly on December 4, 2018 and the Chugach Board of Directors gave its final approval on December 19, 2018. The agreements and associated documents were executed on December 28, 2018. For more information concerning the pending ML&P Acquisition, see “Item 8 – Financial Statements and Supplementary Data – Note 5 – Regulatory Matters and Note 16 – ML&P Acquisition.” There are many risks associated with the pending acquisition including, but not limited to, regulatory approvals, incurrence of substantial debt, interest rate risk, realization of expected benefits and savings, etc., which could have a negative impact on our business, financial condition, or cost of electric service.

Interest Rates

Chugach is exposed to a variety of risks, including changes in interest rates. The interest rates on future borrowings could be significantly higher than interest rates on our existing debt. This could have a negative impact on our business, financial condition, or cost of electric service.

Legal Proceedings

Chugach has certain litigation matters and pending claims that arise in the ordinary course of business as discussed under “Item 3 – Legal Proceedings.” We cannot predict the outcome of any current or future legal proceedings. Our business, financial condition, and results of operations could be materially adversely affected by unfavorable resolution or adverse results of legal matters.

These factors, as well as weather and economic conditions, are largely beyond our control, but may have a material adverse effect on our earnings, cash flows and financial position.

Item 1B – Unresolved Staff Comments

None

General

As of December 31, 2019, we had 531.2 MW of installed capacity consisting of 16 generating units at five power plants. These included 332.0 MW of operating capacity at the Beluga facility on the west side of Cook Inlet; 140.1 MW at SPP in Anchorage (representing our share of generation capacity of the facility which we own jointly with ML&P); 28.2 MW at IGT in Anchorage; and 19.2 MW at the Cooper Lake facility, which is on the Kenai Peninsula. We also own rights to 11.7 MW of capacity from the two Eklutna Hydroelectric Project generating units that we jointly own with MEA and ML&P.

15

In addition to our own generation, we purchase power from the 120 MW Bradley Lake Hydroelectric Project, which is owned by the Alaska Energy Authority (“AEA”), operated by HEA and dispatched by Chugach, MEA’s 171 MW Eklutna Generation Station (“EGS”), and ML&P’s 120 MW George M. Sullivan Plant 2A. We also purchase power from FIW.

The Beluga, IGT and SPP facilities are fueled by natural gas. We own our offices and headquarters, located adjacent to IGT and SPP in Anchorage. We lease warehouse space for some generation, transmission and distribution inventory (including a small amount of office space).

Generation Assets

We own the land and improvements comprising our generating facilities at Beluga, IGT and SPP. Our principal generation assets are in two plants, Beluga and SPP. With SPP in operation, the Beluga units are used for peaking, and in the future, may be primarily used as reserve. While the Beluga turbine-generators have been in service for many years, they have been maintained in good working order with scheduled inspections and periodic upgrades. All Beluga units are inspected annually with combustion and hot gas path parts replaced according to their condition or as recommended by the manufacturer. Units 3 and 5 are most often run for peak demand. In 2018, Unit 3 received major maintenance consistent with original equipment manufacturer (“OEM”) requirements for the gas turbine. Additionally, Unit 3’s generator received significant maintenance including generator testing, rotor removal and inspection, and stator re-wedge. During the third and fourth quarter of 2019, Units 1 and 2 both experienced a #2 bearing failure. The repair of these units will be completed in early 2020.

SPP began commercial operation in February 2013, contributing 200.2 MW of capacity provided by four generating units. Chugach owns 70% of this plant and ML&P owns the remaining 30%. Each owner takes a proportionate share of power from SPP. Our principal generation units at SPP are Units 10, 11, 12, and 13. Since they have been in commercial operation, SPP units have received preventative maintenance inspections consistent with OEM recommendations through 2019. The gas turbine generators of Units 11, 12, and 13 receive two internal combustion system inspections each and one full package inspection annually. In 2019, Unit 12 gas turbine was replaced with a spare gas turbine and the gas turbine that came out of Unit 12 was rebuilt and installed in Unit 11. All three steam-generating boilers were internally inspected as well as hydrotested in accordance with OEM recommendations.

The Cooper Lake Hydroelectric Project is partially located on federal lands. Chugach owns, operates and maintains the Cooper Lake project subject to a 50-year license granted to us by FERC in August of 2007.

The two generating units at Cooper Lake, Units 1 and 2, have a combined capacity of 19.2 MW. Both units were taken out of service for annual maintenance in August of 2017 and 2018. In September 2018, the powerhouse tailrace was dredged to remove accumulated sediment from decades of solid material build-up in the area. In 2019, major maintenance activities were completed on Unit 1. This included the complete disassembly of the generator and turbine, major components were refurbished, the turbine runner was replaced, and the unit was reassembled and returned to service in December. In August 2019, Unit 2 and plant auxiliary systems received annual maintenance and inspection. In 2020, an upgraded controls system is planned to be installed to replace the aging system that was originally installed in 2000.

16

The Eklutna Hydroelectric Project is located on federal land subject to a United States Bureau of Land Management right-of-way grant issued in October of 1997. The facility is jointly owned, operated and maintained by Chugach, MEA, and ML&P with ownership shares of 30%, 17%, and 53%, respectively. Chugach owns rights to 11.7 MW of capacity from the two Eklutna Hydroelectric Project generating units.

The following matrix depicts nomenclature, run hours for 2019, percentages of contribution and other historical information for all Chugach generation units.

|

|

||||||||||||

|

Facility |

Commercial Operation Date |

Nomenclature |

Rating |

Run |

Percent of Total Run Hours |

Percent of Time Available |

||||||

|

Beluga Power Plant |

||||||||||||

|

1 |

1968 |

GE Frame 5 |

19.6 | 117.8 | 0.27 | 97.3 | ||||||

|

2 |

1968 |

GE Frame 5 |

19.6 | 25.7 | 0.06 | 97.9 | ||||||

|

3 |

1973 |

GE Frame 7 |

64.8 | 1,723.6 | 3.95 | 59.9 | ||||||

|

5 |

1975 |

GE Frame 7 |

68.7 | 985.3 | 2.26 | 91.3 | ||||||

|

6 |

1976 |

GE 11DM-EV |

79.2 | 4.1 | 0.01 | 64.8 | ||||||

|

7 |

1978 |

GE 11DM-EV |

80.1 | 2.8 | 0.01 | 86.3 | ||||||

|

|

332.0 | |||||||||||

|

Cooper Lake Hydroelectric Project |

||||||||||||

|

1 |

1960 |

BBC MV 230/10 |

9.6 | 1,212.0 | 2.78 | 85.8 | ||||||

|

2 |

1960 |

BBC MV 230/10 |

9.6 | 5,525.0 | 12.68 | 85.8 | ||||||

|

|

19.2 | |||||||||||

|

IGT Power Plant |

||||||||||||

|

1 |

1964 |

GE Frame 5 |

14.1 | 71.1 | 0.16 | 91.5 | ||||||

|

2 |

1965 |

GE Frame 5 |

14.1 | 29.1 | 0.07 | 100.0 | ||||||

|

|

28.2 | |||||||||||

|

Southcentral Power Project |

||||||||||||

|

10 |

2013 |

Mitsubishi SC1F-29.5 (5) |

40.2 |

(4) |

8,750.0 | 20.08 | 99.0 | |||||

|

11 |

2013 |

GE LM6000 PF |

33.3 |

(4) |

8,363.0 | 19.19 | 95.9 | |||||

|

12 |

2013 |

GE LM6000 PF |

33.3 |

(4) |

8,417.0 | 19.31 | 97.8 | |||||

|

13 |

2013 |

GE LM6000 PF |

33.3 |

(4) |

8,354.0 | 19.17 | 96.8 | |||||

|

|

140.1 | |||||||||||

|

Eklutna Hydroelectric Project |

||||||||||||

|

1 |

1955 |

Newport News |

5.8 |

(2) |

N/A |

(3) |

94.0 | |||||

|

2 |

1955 |

Oerlikon custom |

5.9 |

(2) |

N/A |

(3) |

48.5 | |||||

|

|

11.7 | |||||||||||

|

System Total |

531.2 | 43,580.5 | 100.00 | |||||||||

|

|

||||||||||||

|

(1) Capacity rating in MW at 30 degrees Fahrenheit. |

||||||||||||

|

(2) The Eklutna Hydroelectric Project is jointly owned by Chugach, MEA and ML&P. The capacity shown is our 30% share of the plant's output under normal operating conditions. The actual nameplate rating on each unit is 23.5 MW. |

||||||||||||

|

(3) Run hours are not recorded by Chugach for the Eklutna Hydroelectric Project as it is maintained by a committee of three owners. |

||||||||||||

|

(4) The Southcentral Power Project is jointly owned by Chugach and ML&P. The capacity shown is our 70% share of the plant's output under normal operating conditions. The actual nameplate rating for the project is 200.2 MW. |

||||||||||||

|

(5) Steam-turbine powered generator with heat provided by exhaust from natural gas fueled Units 11, 12 and 13 and additional heat from supplemental duct firing in the once through steam generators associated with the respective gas turbines (combined-cycle). |

||||||||||||

|

Note: GE = General Electric, BBC = Brown Boveri Corporation |

||||||||||||

17

Transmission and Distribution Assets

As of December 31, 2019, our transmission and distribution assets included 43 substations and 436 miles of transmission lines, which included Chugach’s share of the Eklutna transmission line, 892 miles of overhead distribution lines and 835 miles of underground distribution line. We own the land on which 25 of our substations are located and a portion of the right-of-way connecting our Beluga plant to Anchorage. As part of our 1997 acquisition of 30% of the Eklutna Hydroelectric Project, we also acquired a partial interest in two substations and additional transmission facilities.

Most of Chugach’s generation sites and many of its substation sites are on Chugach-owned lands. The rights for the sites not on Chugach-owned lands are as follows: the Postmark and Point Woronzof Substations, and the Airport East Terminal Site (North - South Runway) are authorized by the State of Alaska Department of Transportation and Public Facilities, Ted Stevens Anchorage International Airport; the Six Mile East Terminal Site is under rights from Joint Base Elmendorf-Richardson; the Six Mile West Terminal Site is authorized by the Matanuska-Susitna Borough; the University Substation is on State of Alaska land under rights from the Federal Bureau of Land Management; the Hope and Daves Creek Substations are authorized by the State of Alaska; the Portage Substation has a permit from the Alaska Railroad Corporation (“ARRC”); the Summit Lake Substation and Microwave Site are on land recently conveyed to the Kenai Peninsula Borough; the Dowling and Raspberry Substations are on Municipality of Anchorage land under rights from the State of Alaska; and, the Indian Substation is authorized by FERC License, until a permit is issued by Chugach State Park. The Cooper Lake Power Plant, Quartz Creek Substation, and the 69kV transmission line between them are operated under the FERC License. Most of Chugach’s transmission, sub-transmission and distribution lines are either on public lands under rights from federal, state, municipal, borough agencies, ARRC, or on private lands via easements.

Title

On January 20, 2011, Chugach and the indenture trustee entered the Indenture, granting a lien on substantially all of Chugach’s assets to secure Chugach’s long-term debt. Assets that are generally not subject to the lien of the Indenture include cash (other than cash deposited with the indenture trustee); instruments and securities; patents, trademarks, licenses and other intellectual property; vehicles and other movable equipment; inventory and consumable materials and supplies; office furniture, equipment and supplies; computer equipment and software; office leases; other leasehold interests for an original term of less than five years; contracts (other than power sales agreements with members having an original term exceeding three years, certain contracts specifically identified in the Indenture, and other contracts relating to the ownership, operation or maintenance of generation, transmission or distribution facilities); non-assignable permits, licenses and other contract rights; timber and minerals separated from land; electricity, gas, steam, water and other products generated, produced or purchased; other property in which a security interest cannot legally be perfected by the filing of a Uniform Commercial Code financing statement, and certain parcels of real property specifically excepted from the lien of the Indenture. The lien of the Indenture may be subject to various permitted encumbrances that include matters existing on the date of the Indenture or the date on which property is later acquired; reservations in United States patents; non-delinquent or contested taxes, assessments and contractors’ liens; and various leases, rights-of-way, easements, covenants, conditions, restrictions, reservations, licenses and permits that do not materially impair Chugach’s use of the mortgaged property in the conduct of Chugach’s business.

18

Many of Chugach’s properties are burdened by easements, plat restrictions, mineral reservation, water rights and similar title exceptions common to the area or customarily reserved in conveyances from federal or state governmental entities, and by additional minor title encumbrances and defects. We do not believe that any of these title defects will materially impair the use of our properties in the operation of our business.

Under the Alaska Electric and Telephone Cooperative Act, we possess the power of eminent domain for the purpose and in the manner provided by State of Alaska condemnation laws for acquiring private property for public use.

Other Property

Bradley Lake

We are a participant in the Bradley Lake Hydroelectric Project, which is a 120 MW rated capacity hydroelectric facility near Homer on the southern end of the Kenai Peninsula that was placed into service in September 1991. The project is nominally scheduled below 90 MW to minimize losses and ensure system stability. We have a 30.4% (27.4 MW as currently operated) share in the Bradley Lake project’s output, and currently take Seward’s share which we net bill to them, for a total of 31.4% of the project’s capacity. We are obligated to pay 30.4% of the annual project costs regardless of project output.

The project was financed and built by AEA through grants from the State of Alaska and the issuance of $166.0 million principal amount of revenue bonds supported by power sales agreements with six electric utilities that share the output from the facility (ML&P, HEA and MEA (through Alaska Electric Generation & Transmission Cooperative, Inc. (“AEG&T”) and Alaska Electric and Energy Cooperative, Inc. (“AEEC”)), GVEA, Seward and us). The participating utilities have entered into take-or-pay power sales agreements under which AEA has sold percentage shares of the project capacity and the utilities have agreed to pay a like-percentage of annual costs of the project (including ownership, operation and maintenance costs, debt-service costs and amounts required to maintain established reserves). By contract, we also provide transmission and related services to all of the participants in the Bradley Lake project.

The term of our Bradley Lake power sales agreement is 50 years from the date of commercial operation of the facility (September 1991) or when the revenue bond principal is repaid, whichever is longer. The agreement may be renewed for successive 40-year periods or for the useful life of the project, whichever is shorter. We believe that so long as this project produces power taken by us for our use that this expense will be recoverable through the fuel and purchased power adjustment process. The share of Bradley Lake indebtedness for which we are responsible is approximately $10.2 million. Upon the default of a participant, and subject to certain other conditions, AEA is entitled to increase each participant’s share of costs and pro rata output, to the extent necessary to compensate for the failure of the defaulting participant to pay its share, provided that no participant’s percentage share is increased by more than 25%. Upon default, Chugach could be faced with annual expenditures of approximately $6.8 million as a result of Chugach’s Bradley Lake take-or-pay obligations.

The Battle Creek Diversion Project (“Project”) is a project to increase water available for generation by constructing a diversion on the West Fork of Upper Battle Creek to divert flows to Bradley Lake, increasing annual energy output by an estimated 37,000 MWh. The Bradley Lake Project Management Committee (“BPMC”) approved the project October 13, 2017, as amended December

19

1, 2017, and December 6, 2017. The Project cost is estimated at $47.2 million and the BPMC approved financing on December 6, 2017. Construction began in the spring of 2018 and is anticipated to be completed in the fall of 2020. Not all Bradley Lake purchasers are participating in the development and resulting benefits of the Project at this time, although they have reserved their ability to participate in the Project at a later date. Chugach would be entitled to 39.38% of the additional energy produced if no additional participants elect to join. The share of Battle Creek indebtedness for which we are responsible is approximately $16.2 million.

Eklutna

Along with two other utilities, Chugach purchased the Eklutna Hydroelectric Project from the Federal Government in 1997. Ownership was transferred from the Department of Energy’s (“DOE”) Alaska Power Administration jointly to Chugach (30%), MEA (17%) and ML&P (53%).

Beluga River Unit (“BRU”)

On April 22, 2016, Chugach commenced receiving gas from the BRU as a Working Interest Owner (“WIO”) of the gas production field. Chugach acquired a 10% working interest in the BRU by jointly purchasing, in partnership with ML&P, ConocoPhillips’ 1/3 Working Interest Ownership of the BRU. In 2019, Chugach received 0.8 Bcf from the BRU field at the field’s delivery meter as a WIO for Chugach native use in thermal generation at a weighted average transfer price of $4.07 per Mcf. In 2018, Chugach received 1.2 Bcf from the BRU field at the field’s delivery meter as a WIO for Chugach native use in thermal generation at a weighted average transfer price of $4.42 per Mcf. In 2017, Chugach received 1.4 Bcf from the BRU field at the field’s delivery meter as a WIO. Of that gas volume received Chugach allocated gas deliveries of 875 MMcf to the ConocoPhillips-ENSTAR contract (average price of $7.57 per Mcf) and retained 506 MMcf for Chugach native use in thermal generation, which had a weighted average transfer price of $4.64 per Mcf.

Fuel Supply

In 2019, 81% of our electric energy was generated from natural gas. Total gas purchased and produced during 2019 was approximately 8.4 Bcf. All of the production came from Cook Inlet, Alaska. The contract with Hilcorp provided 89%, Chugach’s 10% share of the Beluga River Unit gas field provided 10%, and minor purchases from Furie provided the balance. The current gas contract with Hilcorp began providing gas in 2011 and will expire March 31, 2028. The BRU and Hilcorp, together, fill 100% of Chugach’s firm needs through March 31, 2028. The gas contract with Furie currently provides Chugach with additional purchase options, on a firm and interruptible basis, and will provide both firm and non-firm gas supplies beginning on April 1, 2023 and ending March 31, 2033.

Hilcorp

Chugach entered into a contract with Hilcorp to provide gas beginning January 1, 2015, and through multiple amendments, now extends through March 31, 2028. The total amount of gas under contract is currently estimated to be 79.4 Bcf. Pricing for the 2019 term of the Hilcorp contract averaged $7.46 per Mcf.

20

Furie Agreement

On March 16, 2017, Chugach submitted a request to the RCA for approval of the agreement entitled, “Firm and Interruptible Gas Sale and Purchase Agreement between Furie Operating Alaska, LLC and Chugach Electric Association, Inc.” (“Furie Agreement”) dated March 3, 2017. As part of the filing, Chugach requested RCA approval to recover both firm and interruptible purchases under the agreement and all attendant transportation and storage costs through its quarterly fuel and purchased power cost adjustment process.

The Furie Agreement provides Chugach with both firm and non-firm gas supplies over a 16-year period, with firm purchases beginning on April 1, 2023, and ending March 31, 2033, and interruptible gas purchases available to Chugach immediately and ending on March 31, 2033. With respect to the firm purchases, the Furie Agreement provides an annual gas commitment by Furie to sell and Chugach to purchase approximately 1.8 Bcf of gas each year, which represents approximately 20% to 25% of Chugach’s projected gas requirements during this period. The Furie Agreement also provides Chugach with additional purchase options, on a firm and interruptible basis. The initial price for firm gas is $7.16 per Mcf beginning April 1, 2023 and escalates annually rising to $7.98 per Mcf on April 1, 2032, the last year of the Furie Agreement.

On May 1, 2017, the RCA approved the Furie Agreement. The RCA also approved recovery of costs associated with the Furie Agreement through its fuel and purchased power cost adjustment process.

Furie filed for Chapter 11 bankruptcy protection in August 2019 and is currently in ongoing negotiations. We are waiting for the outcome to determine any impact to our agreement.

Glacier Oil and Gas Corporation / Cook Inlet Energy, LLC (“CIE”)

Glacier Oil and Gas Corporation retained holdings of Miller Energy Resources Ltd, including the subsidiary CIE, following bankruptcy proceedings in 2016. Chugach entered into a Gas Sale and Purchase Agreement (“GSPA”) with CIE in 2013, to supply gas from April 1, 2014, through March 31, 2018, with an option to extend for an additional five years by mutual agreement during the term of the GSPA. In an extension letter agreement dated February 17, 2017, both parties agreed to extend the term of the agreement until March 31, 2023. The GSPA with CIE provides Chugach with an opportunity to diversify its gas supply portfolio and minimize its current dependence on the gas agreements in place with two vendors. The gas that may be purchased under the GSPA with CIE is not required, however it introduces a new pricing mechanism.

The GSPA identifies and defines two types of gas purchases. Base gas is defined by the volume of gas purchased on a firm or interruptible basis at an agreed delivery rate. Pricing for base gas purchases ranges from $6.12 to $7.31 per Mcf. Swing gas is gas sold to Chugach at a delivery rate in excess of the applicable base gas agreed delivery rate. Pricing for swing gas purchases ranges from $7.65 to $9.14 per Mcf.

AIX Energy, LLC

Chugach entered into a contract with AIX Energy, LLC (“AIX”) in 2014, to supply gas from March 1, 2015, through February 29, 2016. This agreement capped the price of gas at $6.24 per Mcf and the total volume at 300,000 Mcf. In anticipation of this agreement’s expiration, Chugach entered into another gas sale and purchase agreement with AIX in November of 2015, to provide gas beginning April 1, 2016, through March 31, 2023, with the option to extend to March 31, 2029. The

21

AIX agreements provide flexibility in both the purchase price and volumes and allow Chugach to further diversify its gas supply portfolio, with no minimum purchase requirements.

Municipality of Anchorage, dba Municipal Light and Power

Chugach entered into a contract with Municipality of Anchorage, DBA Municipal Light and Power (“ML&P”) in 2016, to supply gas beginning June 6, 2016, and expired March 31, 2017. This agreement capped the price of gas at $5.75 per Mcf and the total volume at 500,000 Mcf. The ML&P agreement provided Chugach the ability to further diversify its gas supply portfolio, with no minimum purchase requirements.

Natural Gas Transportation Contracts

The terms of the Hilcorp agreement requires Chugach to transport gas. Chugach took over the transportation obligation for natural gas shipments for gas supplied under its contracts on October 1, 2010. The following information summarizes the transportation obligations for Chugach:

ENSTAR (Alaska Pipeline Company)

ENSTAR Natural Gas Company (“ENSTAR”) has a tariff to transport our gas purchased from gas suppliers on a firm basis to our IGT and SPP facilities.

Chugach and ENSTAR entered into a Firm Transportation Service Agreement on May 21, 2012, to provide for the transportation of gas to SPP. The agreement commenced on August 1, 2012, and remains in effect until canceled upon a 12-month written notice by either party. The agreement sets a contracted peak demand of 36,300 Mcf per day.

Harvest Alaska, LLC Pipeline System

Hilcorp now operates four major gas pipelines through Harvest Alaska, LLC, in the Cook Inlet basin, including the Kenai-Nikiski Pipeline (“KNPL”), the Beluga Pipeline (“BPL”), the Cook Inlet Gas Gathering System (“CIGGS”) and the Kenai-Kachemak Pipeline (“KKPL”).

On November 1, 2014, the RCA approved consolidation of these four pipelines into a single pipeline, the Kenai-Beluga Pipeline (“KBPL”). Chugach has entered into tariff agreements to ship gas on the KBPL.

Environmental Matters

Chugach includes costs associated with environmental compliance in both our operating and capital budgets. We accrue for costs associated with environmental remediation obligations when those costs are probable and reasonably estimated. We do not anticipate that environmental related expenditures will have a material effect on our results of operations or financial condition. We cannot, however, predict the nature, extent or cost of new laws or regulations relating to environmental matters.

The three utility owners of the Eklutna Hydro Project (Chugach, ML&P, and MEA) are obligated by a 1991 Fish & Wildlife Agreement to develop and implement measures to protect, mitigate, and enhance the fish and wildlife impacted by the project (PME program). The program is to be approved by the Governor of Alaska with completion of the program no later than October of 2032, 35 years after its purchase. The owners initiated a required consultation process with key

22

government agencies and interested parties in March 2019. The agreement requires equal consideration of; 1) efficient and economical power production, 2) energy conservation, 3) protection, mitigation of damage to, and enhancement of fish and wildlife, 4) protection of recreation opportunities, 5) municipal water supplies, 6) preservation of other aspects of environmental quality, 7) other beneficial public uses, and 8) requirements of state law. The hydro project and municipal water system currently utilize 100% of the water inflows.