Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - HF Foods Group Inc. | ex_176637.htm |

| EX-32.1 - EXHIBIT 32.1 - HF Foods Group Inc. | ex_176636.htm |

| EX-31.2 - EXHIBIT 31.2 - HF Foods Group Inc. | ex_176635.htm |

| EX-31.1 - EXHIBIT 31.1 - HF Foods Group Inc. | ex_176634.htm |

| EX-23.1 - EXHIBIT 23.1 - HF Foods Group Inc. | ex_177380.htm |

| EX-21 - EXHIBIT 21 - HF Foods Group Inc. | ex_177170.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

|

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____________to____________

COMMISSION FILE NO. 001-38180

HF Foods Group Inc.

(Exact Name of Registrant as Specified in Its Charter)

|

Delaware |

81-2717873 |

|

(State or Other Jurisdiction of |

(I.R.S. Employer |

|

6001 W. Market Street Greensboro, NC |

27409 |

|

(Address of Principal Executive Offices) |

(Zip Code) |

(Registrant’s Telephone Number, Including Area Code): (336) 268-2080

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each Class |

Trading Symbols |

Name of each Exchange on which registered |

|

Common Stock, par value $0.0001 per share |

HFFG |

Nasdaq Capital Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☒ |

|

Non-accelerated filer |

☐ |

|

Smaller reporting company |

☐ |

|

|

|

|

Emerging growth company |

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes ☐ No ☒

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant on June 28, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $771,650,187.66 based on the closing price of $34.81 per share as reported on the Nasdaq Capital Market on June 28, 2019.

As of March 13, 2020, the registrant had 52,145,096 shares of common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Part III of this Annual Report on Form 10-K incorporates by reference certain portions of the registrant’s definitive proxy statement for its 2020 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission not later than 120 days after the end of the fiscal year covered by this report.

HF FOODS GROUP INC.

ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended December 31, 2019

Table of Contents

|

|

Page No. |

|

|

PART I |

|

|

|

Cautionary Note About Forward-Looking Statements |

2 | |

|

Item 1. Business |

3 | |

|

Item 1A. Risk Factors |

14 | |

|

Item 2. Properties |

26 | |

|

Item 3. Legal Proceedings |

27 | |

|

Item 4. Mine Safety Disclosures |

27 | |

|

|

||

|

PART II |

||

|

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

27 | |

| Item 6. Selected Financial Data | 27 | |

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations |

27 | |

| Item 7A. Quantitative and Qualitative Disclosures About Market Risk | 40 | |

|

Item 8. Financial Statements and Supplementary Data |

40 | |

|

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

69 | |

|

Item 9A. Controls and Procedures |

69 | |

|

Item 9B. Other Information |

69 | |

|

|

||

|

PART III |

||

|

Item 10. Directors, Executive Officers and Corporate Governance |

70 | |

|

Item 11. Executive Compensation |

70 | |

|

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Matters |

70 | |

|

Item 13. Certain Relationships and Related Transactions, and Director Independence |

70 | |

|

Item 14. Principal Accounting Fees and Services |

70 | |

|

|

||

|

PART IV |

||

|

Item 15. Exhibits and Financial Statement Schedules |

70 | |

|

Item 16. Form 10-K Summary |

72 | |

CAUTIONARY NOTE ABOUT FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K for HF Foods Group Inc. (“HF Group,” the “Company,” “we,” “us,” or “our”) contains forward-looking statements. Forward-looking statements include statements about our expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts. Words or phrases such as “anticipate,” “believe,” “continue,” “estimate,” “expect,” “intend,” “may,” “ongoing,” “plan,” “potential,” “predict,” “project,” “will” or similar words or phrases, or the negatives of those words or phrases, may identify forward-looking statements, but the absence of these words does not necessarily mean that a statement is not forward-looking. We derive many of our forward-looking statements from our operating budgets and forecasts, which are based on many detailed assumptions. While we believe that our assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors, and it is impossible for us to anticipate all factors that could affect our actual results. All forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that we expected. Important factors that could cause actual results to differ materially from our expectations, or cautionary statements, include without limitation:

|

● |

Unfavorable macroeconomic conditions in the United States; |

|

● |

Competition in the food service distribution industry particularly the entry of new competitors into the Chinese/Asian restaurant market niche; |

|

● |

Increases in fuel costs; |

|

● |

Increases in commodity prices; |

|

● |

Disruption of relationships with vendors and increases in product prices; |

|

● |

US government tariffs on products imported into the United States, particularly from China; |

|

● |

Changes in consumer eating and dining out habits; |

|

● |

Disruption of relationships with or loss of customers; |

|

● |

Our ability to execute our acquisition strategy; |

|

● |

Availability of financing to execute our acquisition strategy; |

|

● |

Our success at integrating B&R Global Holdings, Inc. (“B&R Global”) into HF Group; |

|

● |

Our ability to renew or replace our current leases; |

|

● |

Control of the Company by our Chief Executive Officer and principal stockholder; |

|

● |

Failure to retain our senior management and other key personnel particularly; |

|

● |

Our ability to attract, train and retain employees; |

|

● |

Changes in and enforcement of immigration laws; |

|

● |

Failure to comply with various federal, state and local rules and regulations regarding food safety, sanitation, transportation, minimum wage, overtime and other health and safety laws; |

|

● |

Product recalls, voluntary recalls or withdrawals if any of the products we distribute are alleged to have caused illness, been mislabeled, misbranded or adulterated or to otherwise have violated applicable government regulations; |

|

● |

Failure to protect our intellectual property rights; |

|

● |

Any cyber security incident, other technology disruption or delay in implementing our information technology systems; |

|

● |

The development of an active trading market for our common stock; and |

|

● |

other factors discussed in “Item 1A. Risk Factors.” and “Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations.” in this Annual Report on Form 10-K. |

All written and oral forward-looking statements attributable to us, or persons acting on our behalf, are expressly qualified in their entirety by these cautionary statements as well as other cautionary statements that are made from time to time in our other filings with the Securities and Exchange Commission (the "SEC") and public communications. We caution you that the important factors referenced above may not contain all of the factors that are important to you. In addition, we cannot assure you that we will realize the results or developments we expect or anticipate or, even if substantially realized, that they will result in the consequences or affect us or our operations in the way we expect. The forward-looking statements included in this Annual Report on Form 10-K are made only as of the date hereof. Except as otherwise required by law, we undertake no obligation to update or revise any forward-looking statement as a result of new information, future events or otherwise.

PART I.

|

ITEM 1. |

BUSINESS. |

Overview

HF Foods Group Inc. acting through its subsidiaries (“HF Group,” the “Company,” “we,” “us,” or “our”), is a leading Asian foodservice distributor to Asian restaurants, primarily Chinese restaurants located in the southeastern, Pacific and mountain west regions of the United States. HF Group is the result of successful merger between 2 two complementary market leaders, HF Foods Group and B&R Global Holdings on November 4, 2019.

The company now has 14 distribution centers strategically located across the east and west coasts of the United States in California, Arizona, Colorado, Florida, Georgia, Montana, Nevada, North Carolina, Oregon, Utah, and Washington, and a fleet of over 340 refrigerated vehicles. Capitalizing on its deep understanding of the Chinese culture and with 960 employees supported by two call centers in China, HF Group has become a trusted partner serving over 10,000 Asian restaurants in 21 states and provides round-the-clock sales and service support to its customers who mainly converse in Mandarin or Chinese dialects. Operating through its subsidiaries, the Company is dedicated to serving the vast array of Asian and Chinese restaurants in need of high-quality food ingredients at competitive prices.

HF Foods is committed to providing excellent customer service by delivering a distinctive product portfolio built from an indelible partnership with both foreign and domestic suppliers. These relationships, coupled with state-of-the-art technology, ensure that we deliver an outstanding array of products at unbeatable prices. The Company also utilizes a centralized inventory procurement system for all its distribution centers which provides great negotiating power with suppliers resulting in competitive prices for its customers. This proprietary system helps to better manage customer relationships and inventory while providing a solid platform for expansion from acquisition of smaller companies in this fast growing yet fragmented niche market.

Recent Developments

Business Combination with B&R Global

On November 4 2019, the Company completed the transactions contemplated by that certain the merger agreement dated as of June 21, 2019 (the “Merger Agreement”) by and among the Company, B&R Merger Sub Inc., a Delaware corporation (“Merger Sub”), B&R Global, the stockholders of B&R Global (the “B&R Global Stockholders”), and Xiao Mou Zhang (aka Peter Zhang), as representative of the stockholders (the “Business Combination”). Capitalized terms used herein without definition have the meaning given to them in the Merger Agreement.

Pursuant to the Merger Agreement, Merger Sub merged with and into B&R Global, resulting in B&R Global becoming a wholly owned subsidiary of HF Group. In connection with the closing, HF Group issued 30.7 million of its shares of common stock to the B&R Global Stockholders.

Pursuant to the Amendment to HF Group’s certificate of incorporation, HF Group currently has authorized share capital of 101,000,000 shares consisting of 100,000,000 shares of common stock with a par value of $0.0001 per share and 1,000,000 shares of preferred stock with a par value of $0.0001 per share.

Immediately after the Business Combination, HF Group’s pre-Business Combination public shareholders owned approximately 12% of HF Group, HF Group’s pre-Business Combination directors, officers and affiliates owned approximately 29.1% of HF Group, and the B&R Global Stockholders owned approximately 58.9% of HF Group.

In connection with the Business Combination:

|

● |

HF Group, Xiao Mou Zhang, as representative of the stockholders of B&R Group, and Loeb & Loeb LLP, as escrow agent, entered into an Escrow Agreement pursuant to which HF Group deposited shares of HF Group common stock representing 5% of the aggregate amount of shares issued to the B&R Global Stockholders pursuant to the Merger, to secure the indemnification obligations of the B&R Global Stockholders as contemplated by the Merger Agreement. |

|

● |

Certain shareholders of HF Group and certain of the B&R Global Stockholders entered into a Tag-Along Agreement, which provides the stockholder parties thereto with tag-along rights in the event any such stockholder desires to sell his or her HF Group securities in a private transaction, or enter into any transaction that would have the same effect as a sale, or enter into any swap, hedge or other arrangement that transfers, in whole or in part, any of the economic consequences of ownership of such shares, or to enter into any transaction, swap, hedge or other arrangement, or engage in any short sales with respect to any such securities. |

|

● |

HF Group and the B&R Global Stockholders entered into a Registration Rights Agreement to provide for the registration of the common stock issued to the B&R Global Stockholders in connection with the Business Combination. The B&R Global Stockholders will be entitled to “piggy-back” registration rights with respect to registration statements filed following the consummation of the Business Combination, and will have certain demand rights for registration. HF Group will bear the expenses incurred in connection with the filing of any such registration statements. |

|

● |

HF Group, B&R Global, and certain of the B&R Global Stockholders entered into a five year Voting Agreement, which provided that, immediately after the closing of the Business Combination, (i) Zhou Min Ni, the prior Chief Executive Officer of HF Group, would continue to serve as a director and the chairman of the board of the Company and as its Co-CEO; (ii) Xiao Mou Zhang, the pre-Business Combination Chief Executive Officer of B&R Global, would begin serving as a director of HF Group and its Co-CEO; (iii) Zhou Min Ni would select one person to serve as an independent director of the Company, (iv) Xiao Mou Zhang would select one person to serve as an independent director, and (v) Zhou Min Ni and Xiao Mou Zhang would jointly select one person to serve as an independent director. |

Acquisition of Warehouse Facilities

On January 17, 2020, the Company completed the transactions contemplated by that certain membership interest purchase agreement dated the same date (the “Purchase Agreement”) by and among its subsidiary B&R Global, B&R Group Realty, and nine subsidiary limited liability companies wholly owned by B&R Group Realty (the “B&R Realty Subsidiaries”) (the “Acquisition”). Capitalized terms used herein without definition have the meaning given to them in the Purchase Agreement

Pursuant to the Purchase Agreement, B&R Global acquired all equity membership interests in the B&R Realty Subsidiaries, which own warehouse facilities that were being leased by the Company for its operations in California, Arizona, Utah, Colorado, Washington, and Montana. Co-CEO of the Company, Peter Zhang, managed and owned an 8.91% interest in B&R Group Realty. The total purchase price for the Acquisition was set at $101,269,706. Financing for the Acquisition was provided under the Second Amended and Restated Credit Agreement, the terms of which are set forth below, and the lender parties thereto relied upon the appraisals in determining to provide such financing. Based in part on the foregoing, the special transactions review committee, composed of the Company’s independent directors, reviewed and approved the Acquisition and the related financing on behalf of HF Group’s board.

Consideration for the Acquisition was a funded by (i) $75.6 million in mortgage-backed term loans financed under the Second Amended and Restated Credit Agreement, (ii) issuance by B&R Global and the Company of a $7.0 million Unsecured Subordinated Promissory Note (the “Note”) to B&R Group Realty, and (iii) payment of $18.7 million from funds drawn from the Company’s revolving credit facility. The restatement of the mortgage-backed term loans released B&R Group Realty from its obligations to the lenders under the First Amended Credit Agreement and predecessor financing arrangements.

Amendment to Credit Facility

On November 4, 2019, the Company, B&R Global, and certain of the wholly-owned subsidiaries and affiliates of the Company (collectively with the Company, the “Borrowers”), as borrowers, and certain material subsidiaries of the Company as guarantors, entered into an Amended and Restated Credit Agreement (the “Amended Credit Agreement”) with JPMorgan Chase Bank, N.A. (“JPMorgan”), as Administrative Agent, and certain lender parties thereto. The Amended Credit Agreement provided for (a) a $100 million asset-secured revolving credit facility maturing on November 4, 2022, and (b) mortgage-secured Term Loans of $55.4 million, and amended and restated the existing $75 million secured revolving credit facility and $60 million of real estate term loans evidenced by that certain Credit Agreement, dated as of November 6, 2017, among B&R Global, its affiliates and JP Morgan Chase Bank, N.A., as the sole lender.

On January 17, 2020, the Company, B&R Global, and the Borrowers, and certain material subsidiaries of the Company as guarantors, entered into a Second Amended and Restated Credit Agreement (the “Second Amended Credit Agreement”) by and among JPMorgan, as Administrative Agent, and certain lender parties thereto, including Comerica Bank. The Second Amended Credit Agreement provided for (a) a $100 million asset-secured revolving credit facility maturing on November 4, 2022 (the “Facility”), and (b) mortgage-secured Term Loans of $75.6 million. The Second Amended Credit Agreement amended and restated the existing $55.0 million of real estate term loans under the Amended Credit Agreement. As of January 17, 2020, the existing balance of revolving debt under the Amended Credit Agreement, $41.2 million, was rolled over, and an additional $18.7 million available to the Company under the Facility was drawn. The Company used the $75.6 million in mortgage-secured term loans and $18.7 million drawn from the revolving credit facility to fund in part the Acquisition.

Borrowings under the Second Amended Credit Agreement may be used for, among other things, working capital and other general corporate purposes of the Company and its subsidiaries (including permitted acquisitions). The Borrowers have the ability to increase the amount of the Facility, which increases may take the form of increases to the revolving credit commitments, by an aggregate amount of up to $30 million upon satisfaction of customary conditions precedent for such increases, or incremental loans and receipt of additional commitments by one or more existing or new lenders.

Borrowings under the Facility bear interest at a floating rate which will be, at the Borrowers’ option, either LIBOR plus 1.375%, or a base rate of prime rate minus 1.125%. The Term Loans bear interest at a floating rate which will be, at the Borrowers’ option, either LIBOR plus 1.875%, or a base rate of prime rate minus 0.625%. A commitment fee of 0.15% is payable monthly in arrears based on the daily amount of the undrawn portion of each lender’s revolving credit commitments under the Facility.

Business Model and Competitive Advantage

We are committed to providing our customers with a wide range of products at competitive prices. Since inception, we have differentiated ourselves from our competitors with our distinctive product portfolio, supplier relationships, strategic locations, and technology. Our wide range of Asian Specialty product offerings sets us apart from other mainstream competitors such as Sysco and US Foods, as many of the items we offer are specific to the Chinese restaurant industry. More importantly, our relationships with our suppliers allow us to procure a large variety of products in volume at a low cost. We also import specialized items that would be difficult to procure domestically. With fourteen warehouses and over three hundred trucks executing daily routes within 300 miles of our distribution centers, we offer our customers prompt delivery of high-quality products.

We believe that the following elements of our business model provide us with a competitive advantage and has contributed greatly to our success:

|

● |

We offer a wide array of specialty products that are not commonly provided by large distributors serving the mainstream market. |

|

● |

We have a deep understanding of Chinese culture and most of our employees can speak the native language of our customers. |

|

● |

We lower administrative expenses by outsourcing our telephone-based sales and customer service directly to a call center located in China, which serves our customers with Chinese speaking agents. |

|

● |

We capitalize on economies of scale and have strong negotiating power with our suppliers. |

|

● |

We have strategically placed distribution centers and with a trucking fleet with routes limited to 3 to 5 hours of driving time. Our customers receive their orders quickly. |

|

● |

With our self-developed proprietary information system, we are able to manage our customer relationships and inventory efficiently and reduce operating expenses. |

|

● |

Employees’ bilingual capabilities provide a competitive advantage against other major providers in the industry. |

We plan to strategically consolidate our market segment by acquiring competitors, including other distributors and wholesalers, to expand our business into untapped regions around the United States and to eventually grow into a nationwide foodservice distributor. We will continue develop our management technology systems to further improve our operational efficiency, accuracy and customer satisfaction. We will also explore providing value-added items such as semi-prepared food products to help our customers upgrade their service.

Industry and Market Analysis

We distribute food and supplies to Chinese/Asian restaurants, primarily Chinese restaurants that mainly serve non-Chinese Americans, which is a niche market segment of the foodservice distribution industry. The foodservice industry in the U.S. is generally large and has a long history, with several large players such as Sysco Corporation, US Foods Holding Corp. and Performance Food Group Company, each serving a significant market share of the industry by offering a food related products and services, or carrying specific products for large chains. However, the Chinese restaurants are generally not well served by these mainstream players which open up opportunity for specialty players like HF Foods Group.

Features of Chinese Restaurants

Set forth below are the principal characteristics of the Chinese/Asian restaurants we serve.

Primarily Serving Non-Chinese Americans. There are tens of thousands of Chinese restaurants spread throughout the U.S., which primarily serve non-Chinese American customers. Although the dishes they serve cater to the preferences of American mainstream customers and are more simply and quickly prepared as compared to traditional full-service Chinese restaurant cuisine, they still require typical Chinese ingredients utilizing traditional cooking styles.

Operated by Chinese Individual Families. Most Chinese restaurants serviced by HF Group are operated and owned by individual families with very few workers, who are usually immigrants from China or second generation Chinese Americans. These restaurant owners have very limited resources and appreciate value-added services to help them improve their operational efficiency. The owners and workers in the Chinese restaurants usually speak Mandarin or other regional dialects of the Chinese language. Understanding the Chinese culture and language is paramount to facilitating efficient communications with customers.

Close-Knit Chinese American Community. Second or third generation Chinese Americans living in the U.S. inherit their traditional cultural, and ethnic languages, and our experience has been that people in these communities prefer to do business with Chinese Americans as opposed to other ethnic groups.

Unique Cooking Style and Ingredients for Chinese Cuisines. Chinese cuisine requires unique cooking styles such as steaming and wokking, and requires specialty ingredients and vegetables such as bitter melons, Chinese yams, vine spinach, Chinese cabbage and winter melon. It also requires Chinese and Asian seasonings and spices, including peanut oil, cooking wine, vinegar, dark soy source, black bean sauce, pepper oil and chili oil. Most of the unique ingredients for Chinese cuisine are not widely available from mainstream U.S. suppliers, but are staple supplies of HF Group.

Growth Potential

Growing Consumption Trend for Food Away from Home. According to National Restaurant Association, the percentage of Americans which prefer food away from home increased from 41.2% in 2014 to 43.8% in 2018. We believe the trend of consuming food away from home likely represents a potential increase of demand for Chinese restaurants.

Increased Recognition of Chinese Cuisines by Americans. With the growing influence of China’s economy and culture, more and more Americans are consuming Chinese cuisines. The management of the Company has seen regularly increasing demand for Chinese cuisine and believes this will result in expanded opportunities for Chinese restaurants, and thus the food distribution industry that supplies them.

Current Industry Landscape and Opportunities

Natural Culture Barriers to Entry. Understanding Chinese cooking culture is important to run a Chinese restaurant and, therefore, most Chinese restaurants are operated by Chinese Americans. It is very difficult for mainstream food distributors to serve these restaurants because of various cultural and language barriers.

Highly Fragmented Market Segment. The market is currently highly fragmented with many unsophisticated competitors and there is no recognized industry leader nationwide. Most participants are small players such as wholesalers, specialty import brokers, farmers markets, and local produce retailers without the support of sophisticated logistics infrastructure. We believe we are the only Chinese food distributor operating in the United States with such a well-developed logistics infrastructure and experienced management team and that the fragmented market gives us the opportunity to consolidate supply and further develop a dominant market position.

Infrastructure Barriers for New Entrants. The food distribution industry requires large capital investments and resources to build the necessary logistics infrastructure including warehouses and a fleet of trucks to cover its distribution network. In addition, the size of HF Group gives us greater negotiating power with vendors, resulting in price advantages for our customers which we believe are simply not achievable by smaller suppliers.

Demand for Value-Added Services. Our customers are Chinese/Asian restaurants, primarily takeout restaurants. These customers are price and quality sensitive and prefer large suppliers with scale economies providing competitive prices for products. Given the limited labor forces and resources of these restaurants, most desire to have more value-added services from the suppliers to help them to operate more efficiently.

In sum, we see a great opportunity for market consolidation. We believe we have numerous advantages to address the current market imperfections and become a national leader in this niche market. With economies of scale, we can provide high quality products at competitive prices in an efficient way.

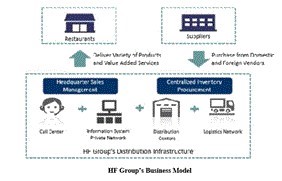

Business Model

Our business model features an integrated structure with fourteen distribution centers with one million square feet of total storage space, a fleet of over 340 vehicles for short-distance delivery, and centralized inventory management and procurement, supported by an outsourced call center located in China for customer relationship management. We offer a variety of high-quality products at competitive prices to our customers. Customers can benefit from our efficient supply chain to support their own growth.

We offer one-stop service to Chinese restaurants with over 1,500 types of products, including fresh and frozen meats, Chinese specialty vegetables, sauces, and packaging materials for takeout restaurants. Chinese restaurants, especially small or takeout restaurants, can find virtually all the products they need in our product lists, which can help minimize the effort involved in managing their purchase of inventory. We use an outsourced call center in Fuzhou, China, with 24-hour availability for sales and marketing, order placement and post-sales service, which reduces our operating costs, and offers service to our customers in Mandarin, Cantonese and regional Chinese dialects, in addition to English.

With 20 years of operations, we have established a large supplier network and we maintain long-term relationships with many major suppliers. The procurement team is led by Zhou Min Ni and Peter Zhang, co-CEOs of the Company, who have a deep insight in the industry. The centralized procurement management system gives us increased negotiating power given the large procurement quantities, improves our turnover of inventory and account payables, and reduces our operating costs.

The graph below depicts our business model:

Products

We offer over 1,500 different products for our clients, primarily Chinese/Asian restaurants, which includes virtually all items needed to operate their business. Products range from perishable produce to takeout food packaging materials. To meet our customers’ demands, we have a large variety and a complete line of products in our inventory. Eighty percent of our sales volume currently consists of domestic goods such as frozen meat and vegetables, which are procured through large suppliers or directly from the producer. The remaining twenty percent are imported specialty products. We provide full service one-stop-shop for our customers by providing most or all of the products they need, from order placement to delivery and post-sales services. Services to customers are supported by our plentiful physical facilities, vehicles, material handling equipment and techniques, and administrative and operating staffs.

The products we distribute include:

|

● |

Asian specialty food items: Asian specialty encompasses any product that has an Asian flair or flavor, including a multitude of noodles, rice, dry goods (dried mushrooms, and dried beans), specialty sauces/ seasonings, spring rolls, and canned products (such as preserved vegetables, bamboo shoots and water chestnut). |

|

● |

Meat and Poultry: We provide our customers with a variety of beef, pork, chicken and duck products with different brands to choose from, such as Smithfield, Teys Australia and Tyson. |

|

● |

Seafood: We are committed to providing our customers with the freshest possible seafood. We provide our clients with all sorts of seafood including lobster, shrimp, crab, scallops and flavorful fish such as tuna and Alaskan salmon, with different brands to choose from, like Asian Star and Atlantic Bay. |

|

● |

Fresh Produce: We offer fresh, seasonal fruits and vegetables including celery, Chinese cabbage, and winter melon, which is widely used in Chinese cuisines. |

|

● |

Packaging and Other Items: We offer a wide range of take-out accessories for customers, from bamboo chopsticks to takeout containers, plastic cups and sushi combo boxes. |

|

● |

Commodities: True commodity products such as regular rice, flour, sugar and oil are classified as “commodity”. |

The following table sets forth sales percentage by category for the year ended December 31, 2019 (pro-forma together with B&R Global Foods for the period prior to the closing of the merger):

|

Category |

|

Percentage |

|

|

|

Asian Specialty |

28 |

% |

||

|

Meat and Poultry |

24 |

% |

||

|

Seafood |

|

|

20 |

% |

|

Fresh Produce |

|

|

13 |

% |

|

Packaging and Others |

|

|

9 |

% |

|

Commodity |

|

|

6 |

% |

Customer Service

We use an outsourced call center located in China to manage our sales order, customer development, sales promotion and post-sales services. The outsourced call center is located in Fuzhou, the capital city of Fujian Province of China, with local employees speaking Mandarin, Cantonese, regional Chinese dialects and English. By offering the customer service in their native language, the sales staff can communicate smoothly and efficiently with our clients and understand what they need. With cultural understanding and a common language, salespeople can design a product portfolio for our customers and use a precision marketing strategy to promote our products. The location of the outsourced call center controls costs by employing skilled salespersons at lower wages in China as compared with the U.S.

We also have a sales team in the U.S., with sales agents that make on-site visits to our customers’ restaurants, in order to gain a better understanding of our customers’ operations and needs.

Currently, we maintain our sales department, which involves decision-making for sales strategies and supervision of sales performance by our key sales managers, in our headquarters in Greensboro, North Carolina and City of Industry, California. The sales managers work closely with the sales staff in China to ensure our market strategies are precisely implemented. Our plan is to further integrate our operating model with the outsourced call center to expand our business and operate even more efficiently.

A proprietary information system is used to maintain each customer’s records, including location, size, contact information, purchasing history, preferences, orders and payment records. Customers can directly call the outsourced call center in China to inquire about products and to place orders. Once orders are confirmed, electronic sales orders are generated by the information system and sent to the distribution center closest to the customer. Upon receipt of the sales orders, products are pulled from the shelves and moved to a staging area at the loading docks. Products are then loaded into delivery vehicles in preparation for delivery. Products are generally delivered to customers within only two days of an order. Customer analysis can be generated through the information system and prompts the salesperson to follow up with customers for product promotion, post-sales services and the taking of new orders.

We offer a refund policy for non-satisfaction without penalty, which many of our small competitors in the market segment are unable to provide. We provide a 100% satisfaction guarantee to our customer. When a shipment is made and the products are not to the standards of the customer, we allow our customers to reject the order in whole or in part with no penalty within 24 hours. The non-penalty refund policy works to help us earn the trust and loyalty of our customers.

Inventory Procurement

The Company utilizes centralized procurement on bulk and frequently sold items. Subsidiaries send their inventory procurement requests to headquarters where the operations team is responsible for fulfillment in the most cost-effective way. The centralized procurement allows HF Group to establish a meaningful vendor relationship under one brand.

We maintain a large supplier network through a vendor pool with a carefully selected group of suppliers to ensure product quality, availability and competitive pricing. Eighty percent of sales volume currently consists of domestic goods such as frozen meat and vegetables, which are procured through large suppliers or directly from the producer. The remaining twenty percent are imported specialty products. To minimize costs, the procurement team directly manages our major vendors for large and frequent purchases and engages brokers for our smaller suppliers of specialty goods. Utilizing brokers allows us to maintain lower costs due to the brokers’ volume.

The key procurement team members closely monitor the supply market for seasonal products such as vegetables and make procurement adjustments according to market conditions. In addition, they use a dual-sourcing method for their suppliers and can negotiate lower prices for comparable products. For high volume sale products such as certain vegetables and meats, we usually negotiate long term agreements with its suppliers to ensure stabile pricing and minimize risk due to market fluctuations.

Each distribution center reviews the inventory level in the information system on a daily basis and submits purchase requests as needed to the procurement team at headquarters. The procurement at headquarters also can alter or adjust purchasing decisions based on an analysis of the inventory data in the system. Upon receipt of ordered products, the delivery schedule is determined based on the needs of each location. The lead-time for products is dependent on the product category and need. For perishable goods, products are usually delivered by suppliers within 72 hours of placing the order. Products that are ordered through import brokers have lead times of up to seven days.

We employ a large supplier network to ensure product availability and low pricing. These suppliers range from small importers of specialty goods to large produce and meat suppliers. JBS USA LLC accounted for approximately 13.2% of our aggregate purchases during the year ended December 31, 2018. None of our suppliers accounted for more than 10% of our aggregate purchases during the year ended December 31, 2019.

Warehousing

We use our information system for warehouse management with daily inventory monitoring. The system allows us to manage our inventory in an efficient way. It optimizes the inventory level and turnover, reducing waste, and helps to reduce labor costs to track and record the inventory.

Inventory levels are maintained based on the category of products. Perishable goods are kept in the refrigerated warehouse for a period of no more than seven days. This includes fresh produce and fresh meat products. Frozen produce, seafood and meat products are kept in the freezer to extend shelf life. Frozen products usually turn over between 30 and 60 days. Non-perishable goods are held in greater quantities of inventory based on the pricing of the market. Non-perishable items are carefully monitored for pricing changes. As they have an extended shelf life, there is an advantage to ordering larger quantities of stock. Non-perishable goods generally turn over in approximately three weeks, which we believe is average for distributors of similar size. Maintaining this level of inventory allows us to manage any surges in demand.

Products are stored throughout warehouses in our various distribution centers. A routine inventory count is taken weekly to ensure stock quantity and replenishment needs. Forty percent of the inventory consists of fresh meats and produce; this inventory is counted daily and turns over on average in about ten days. The other sixty percent consists of frozen and dry goods with interim cycle counts every two weeks and an average turnover of about 30 days. Non-perishable items are stored on racks until their shelf life is reached or the product is sold, whichever comes first. Products are broken down from their pallets and sold in their original packaging. Items stored in the warehouses are not removed from their original packaging. Each package is sold as one unit and priced accordingly.

Locations

We currently have fourteen distribution centers with a total of over one million square feet of storage, including refrigerated storage of over 320,000 square feet. The distribution centers are located on the route of many of our suppliers; delivery of each truckload can be made to each location with one large order. Each warehouse is equipped with multiple loading docks, allowing parallel methods of loading goods to the trucks during the start of each shift. Warehouse locations are also located in industrial regions, allowing large delivery trucks to enter without the need of acquiring permits.

It is important for us to strategically place our warehouses within certain markets to maximize our market share. We currently strategically place our warehouses within markets that are not saturated and have limited competitors. This allows us to quickly penetrate the market and develop customer relationships that will assist in promotion of products and services. Upon penetrating the market, we seek to expand our warehouses into regional areas in order to streamline our distribution network. This strategy is designed to improve the delivery routes and maximize the utilization of our delivery vehicles.

The table below summarizes certain details of our distribution centers:

|

Location |

Total Size |

Size of Cooler and |

Year |

Number of |

||||||||||||

|

Phoenix, AZ |

68,000 | 14,000 | 2011 | 18 | ||||||||||||

|

City of Industry, CA |

128,000 | 35,000 | 2013 | 87 | ||||||||||||

|

Fresno, CA |

10,000 | 3,000 | 2011 | ---- | ||||||||||||

|

Hayward, CA |

108,000 | 36,000 | 2012 | 29 | ||||||||||||

|

Irwindale, CA |

85,000 | 45,000 | 2006 | 29 | ||||||||||||

|

West Sacramento, CA |

25,000 | 8,000 | 2011 | 19 | ||||||||||||

|

Aurora, CO |

55,000 | 16,000 | 2010 | 18 | ||||||||||||

|

Ocala, FL |

130,000 | 30,000 | 2008 | 35 | ||||||||||||

|

Atlanta, GA |

100,000 | 25,000 | 2006 | 20 | ||||||||||||

|

Hardin, MT |

16,000 | 5,000 | 2011 | --- | ||||||||||||

|

Greensboro, NC |

170,000 | 45,000 | 2002 | 50 | ||||||||||||

|

Murray, UT |

59,000 | 14,000 | 2013 | 14 | ||||||||||||

|

West Jordan, UT |

34,000 | 10,000 | 2006 | --- | ||||||||||||

|

Renton, WA |

70,000 | 40,000 | 2015 | 24 | ||||||||||||

|

Total: |

1,058,000 | 326,000 | 343 | |||||||||||||

Fleet Management

We currently own a fleet of over 340 refrigerated vehicles. Vehicles range from vans, 26-foot semi-delivery trucks, to 53-foot long refrigerated trucks and trailer units. These vehicles are maintained by both in-house and external mechanics and follow a strict maintenance schedule. Each vehicle has a 7-year life cycle of approximately 250,000 miles. Each vehicle is refueled daily upon return from its delivery route. When smaller delivery vehicle reaches the end of their usable life, they will be retired and replaced with larger vehicles that are 53 feet long and have a capacity of 40,000 lbs.

Promotion and Marketing

We don’t advertise in the media or magazines. We believe that it is more efficient and cost effective to promote our business through telemarketing and have our drivers promote our business while executing deliveries. Our drivers visit the Chinese/Asian restaurants along their delivery route and are trained to market our products to non-customers along their route. Telemarketing is conducted by salespersons from the outsourced call center in China.

Competitive Strengths

We believe we have the following competitive strengths that give us an advantage over our competitors in the niche industry sector of food service distribution to Chinese restaurants:

A Large Array of Products to Meet the Demands of Customers. We offer over 1,500 products ranging from meats, vegetables and specialty products to packaging materials. Compared with the mainstream foodservice distributors in the United States, our products are selected to meet the specific demands of Chinese restaurants. A large array of products allows Chinese restaurants to purchase from us virtually all of the products they need for operation, and receive one-stop service, which can help them run their business more efficiently with limited operation resources.

Cultural Understanding and Language Advantages. By offering customers service in their native language, the salespersons can communicate smoothly and efficiently with our customers and understand what the customers need. With cultural understanding and a common language, our sales staff can design a product portfolio for our customers and use a precision marketing strategy to promote our products. The location of the outsourced call center controls costs by employing skilled salespersons at lower wages in China as compared with the U.S.

Outsourced Customer Call Center with Low Costs. We use an outsourced call center in China to manage our sales order, customer development, sales promotion, and post-sales services. The outsourced call center is located in Fuzhou, the capital city of Fujian Province of China, with local employees speaking Mandarin, Cantonese, regional Chinese dialects and English. In addition to the advantage provided by interacting with customers in their native language, the location of the outsourced call center also helps us control costs by employing skilled salespersons at lower wages in China as compared with the U.S.

Cost Efficiency with Economies of Scale. We have developed our business around our three distribution centers serving over 3,200 Chinese restaurants in ten states in the southeastern United States and eleven distribution centers serving over 6800 customers in over ten states in the Western United States. We believe we are the only Asian/Chinese food service distributor with a well-developed logistic infrastructure and experienced management team in the regions covered by our distribution network. Compared with small and local distributors, we operate in a more cost-efficient manner and have generated economies of scale, which allows us to offer products with competitive prices to our customers.

Strong Negotiation Power with Vendors. With a large purchase volume and a centralized procurement management, we have strong negotiating power with our vendors and are able to source high quality products at lower prices than many competitors. With a developed inventory procurement system supported by strong negotiating power and an experienced management team, we can offer our customers high quality products at competitive prices.

Developed Logistics Infrastructure. We have developed a sophisticated infrastructure with fourteen distribution centers in the U.S. having a total storage capacity of over one million square feet and a fleet of over 300 vehicles. The Company operates three distribution centers in the, southeastern United States, serving North Carolina, South Carolina, Georgia, Florida, Alabama, Virginia, West Virginia, Tennessee, Kentucky, and Mississippi. We have eleven additional distribution centers in the Western United States, serving customers in Arizona, California, Colorado, Montana, Nevada, Oregon, Utah, Washington, and elsewhere. In conjunction with the development of our logistics infrastructure and business expansion, we have also developed our proprietary information system to manage our customer relationships and inventory. The logistics infrastructure provides efficiency and economies of scale resulting in significant advantages for us and creates a high entry barrier for potential competitors.

Proprietary Information System. We have developed a proprietary electronic information system for our customer relationship and inventory management. All customer information including preferences, purchases and payment history is recorded in the system and can be used to provide post-sales services and promotion. We use this system to monitor our inventory daily, which provides prompt management of inventory and access to important historical information to make operating decisions quickly. The use of the electronic information system improves our management efficiency and reduces operating costs and makes us more competitive in the industry.

Experienced Management and Proven Growth. Key management personnel include Mr. Zhou Min Ni, Co-Chief Executive Officer, and Peter Zhang, Co-Chief Executive Officer, each of whom founded the respective east- and west-coast operations of the current Company, which has have grown it into a regional industry leader serving over 11,000 Chinese restaurants in more than twenty states in the southeastern and western U.S. over the past 20 years. The Company has also built a top-tier management team with operational experience, financial expertise and IT knowledge to grow the business. We believe that we are well-positioned to expand our business into other underserved regions through consolidation of small competitors.

Competition

The foodservice distribution industry is large and highly competitive. There are a few very large distributors serving the mainstream U.S. market. However, with natural cultural barriers, the mainstream foodservice distributors haven’t yet earned a significant market share for Chinese restaurants. Management believes that the market participants in the niche market segment that we are serving is highly fragmented and immature. With the continuing growth of demand for Chinese cuisine, we believe that this industry sector has significant opportunity for consolidation.

The competitors serving the industry sector for Chinese restaurants include a large number of small wholesalers, some medium-sized distributors, as well as large established market players. However, we believe there is no dominating market provider in this segment. Our customers also make purchases from local farms, retailers and grocery stores. Small wholesalers sometimes supply the same specialized items such as spices, specialized sauces, and specialty foods, which we carry, but these small suppliers are not able to offer the same broad base and wide array of products that we do. Compared with the medium-sized distributors and large mainstream market players, we have the advantages of offering a broad line of both staple and niche products, efficient operation infrastructure, and cultural understanding to maintain our market position and continue to grow our business.

Trademarks and Other Intellectual Property

We own several registered trademarks, including the following word marks -- : Han Feng, Inc., Green Leave, Rong, 333, Sea888 (U.S. Regis. No. 5520118), and Sea333 (U.S. Regis. No. 5503974), and the following design/combined marks -- SEA333 (U.S. Regis. No. 5713248), HF [Color Logo] (U.S. Regis. No. 5888817) and HF [B/W Logo] (U.S. Regis. No. 5985676).

Insurance

We use insurance to provide coverage for potential liability for workers compensation, automobile and general liability, product liability, director and officer’s liability, employee health care benefits and other casualty and property risks coverage. Changes in legal trends and interpretations, variability in inflation rates, changes in the nature and method of claims settlement, benefit level changes due to changes in applicable laws, insolvency or insurance carriers, and changes in discount rates could all affect the ultimate settlements of various claims. We evaluate our insurance requirements on an ongoing basis to ensure we maintain adequate levels of coverage.

Employees

As of December 31, 2019, we had a workforce of approximately 1,000 persons, including both our employees and workers engaged through agency placements, 900 of whom are full-time associates and the remaining 100 of whom work part-time. We have over 150 employees who have worked for us for ten years or more. Our workforce is not unionized and we are not aware of any plans for them to unionize. We have never experienced a strike or significant work stoppage. We regard our employee relations to be good.

Government Regulation

Legal compliance is important to our operations. We are required to comply, and it is our policy to comply, with all applicable laws in the numerous jurisdictions in which we do business.

As a marketer and distributor of food products in the United States, we are subject to the Federal Food, Drug and Cosmetic Act and regulations promulgated thereunder by the U.S. Food and Drug Administration (FDA). The FDA regulates food safety and quality through various statutory and regulatory mandates, including manufacturing and holding requirements for foods through good manufacturing practice regulations, hazard analysis and critical control point (HACCP) requirements for certain foods, and the food and color additive approval process. The agency also specifies the standards of identity for certain foods, prescribes the format and content of information required to appear on food product labels, regulates food contact packaging and materials, and maintains a Reportable Food Registry for the industry to report when there is a reasonable probability that an article of food will cause serious adverse health consequences. For certain product lines, we are also subject to the Federal Meat Inspection Act, the Poultry Products Inspection Act, the Perishable Agricultural Commodities Act, the Packers and Stockyard Act and regulations promulgated by the U.S. Department of Agriculture (USDA) to interpret and implement these statutory provisions. The USDA imposes standards for product safety, quality and sanitation through the federal meat and poultry inspection program. The USDA reviews and approves the labeling of these products and also establishes standards for the grading and commercial acceptance of produce shipments from our suppliers. We are also subject to the Public Health Security and Bioterrorism Preparedness and Response Act of 2002, which imposes certain registration and record keeping requirements on facilities that manufacture, process, pack or hold food for human or animal consumption.

The recently published and pending rules under the Food Safety Modernization Act (FSMA) will significantly expand food safety requirements, including those of the Company. Among other things, FDA regulations implementing the FSMA require us to establish and maintain comprehensive, prevention-based controls across the food supply chain that are both verified and validated. The FSMA also imposes new requirements for food products imported into the U.S. and provides the FDA with mandatory recall authority.

The Company and our products are also subject to state and local regulation through such measures as the licensing of our facilities; enforcement by state and local health agencies of state and local standards for our products; and regulation of our trade practices in connection with the sale of our products. Our facilities are subject to regulations issued pursuant to the U.S. Occupational Safety and Health Act by the U.S. Department of Labor. These regulations require us to comply with certain manufacturing, health and safety standards to protect employees from accidents and to establish hazard communication programs to transmit information on the hazards of certain chemicals which may be present in products that we distribute.

Our distribution facilities must be registered with the FDA biennially and are subject to periodic government agency inspections by the FDA and USDA. Our facilities are generally inspected at least annually by federal and/or state authorities. Further, we are required to establish communication programs to transmit information about the hazards of certain chemicals present in some of the products we distribute.

Our business and employment practices are also subject to regulation by numerous federal, state and local regulatory agencies, including, but not limited to, the U.S. Department of Labor, which sets employment practice standards for workers, and the U.S. Department of Transportation, as well as its agencies, the Surface Transportation Board, the Federal Highway Administration, the Federal Motor Carrier Safety Administration, and the National Highway Traffic Safety Administration, which collectively regulate our trucking business through the regulation of operations, safety, insurance and hazardous materials. We must comply with the safety and fitness regulations promulgated by the Federal Motor Carrier Safety Administration, including those relating to drug and alcohol testing and hours-of service. Such matters as weight and dimension of equipment also fall under federal and state regulations. In addition, we are subject to the U.S. False Claims Act, and similar state statutes, which prohibit the submission of claims for payment to the government that are false and the knowing retention of overpayments.

Our operations are also subject to a broad range of U.S. federal, state, and local environmental laws and regulations, as well as zoning and building regulations. Environmental laws and regulations cover a variety of procedures, including appropriately managing wastewater and stormwater; complying with clean air laws, including those governing vehicle emissions; properly handling and disposal of solid and hazardous wastes; protecting against and appropriately investigating and remediating spills and releases; and monitoring and maintaining underground and aboveground storage tanks for diesel fuel and other petroleum products. As of December 31, 2019, the costs of managing our compliance with environmental laws and regulations was nominal.

The U.S. Foreign Corrupt Practices Act (FCPA) prohibits bribery of public officials to obtain or retain business in foreign jurisdictions. The FCPA also requires us to keep accurate books and records and to maintain internal accounting controls to detect and prevent bribery and to ensure that transactions are properly authorized. We will be required to implement and continue to develop a robust anti-corruption compliance program applicable to our operations which will allow us to detect and prevent bribery and to comply with these and other anti-corruption laws in countries where we operate.

For the purchase of items produced, harvested or manufactured outside of the United States, we are subject to applicable customs laws regarding the import and export of various products. Certain activities, including working with customs brokers and freight forwarders, are subject to applicable regulation by U.S. Customs and Border Protection, which is a part of the Department of Homeland Security.

|

ITEM 1A. |

RISK FACTORS. |

The following are significant factors known to us that could materially adversely affect our business, reputation, operating results, industry, financial position and/or future financial performance.

Risk Factors Relating to Our Business

Unfavorable macroeconomic conditions in the U.S. may adversely affect the results of operations and financial condition of the Company.

The operating results of the Company are substantially affected by the operating and economic conditions in the regions in which we operate. Economic conditions can affect us in the following ways:

|

● |

A reduction in discretionary spending by consumers could adversely impact sales of Chinese/Asian restaurants, and their purchases from us. Future economic conditions affecting disposable consumer income, such as employment levels, business conditions, changes in housing market conditions, the availability of consumer credit, interest rates, tax rates and fuel and energy costs, could reduce overall consumer spending. |

|

● |

Food cost and fuel cost inflation experienced by consumers can lead to reductions in the frequency of and the amount spent by consumers for food-away-from-home purchases, which could negatively impact our business by reducing demand for our products. |

|

● |

Heightened uncertainty in the financial markets negatively affects consumer confidence and discretionary spending, which can cause disruptions with our customers and suppliers. |

|

● |

Liquidity issues and the inability of our customers to consistently access credit markets to obtain cash to support their operations can cause temporary interruptions in our ability to conduct day-to-day transactions involving the collection of funds from such customers. |

|

● |

Liquidity issues and the inability of suppliers to consistently access credit markets to obtain cash to support their operations can cause temporary interruptions in our ability to obtain the foodservice products and supplies needed by us in the quantities and at the prices requested. |

In addition, our existing operations are mainly located in the Southeastern and Western United States. The geographic concentration of our operations creates an exposure to the economy of those regions and any financial downturn in these areas could materially adversely affect our financial condition and results of operations.

Competition may increase intensively in the future, which may adversely impact our margins and ability to retain customers, and make it difficult to maintain our market share, growth rate and profitability.

The foodservice distribution industry in the United States is fragmented and highly competitive, with local, regional, multi-regional distributors, and specialty competitors. However, we believe that the market participants serving Chinese restaurants are highly fragmented. Currently, we face competition from smaller and/or dispersed competitors focusing on the niche market serving Chinese/Asian restaurants, especially Chinese takeout restaurants. However, with the growing demand for Chinese cuisines, others may also begin operating in this niche market in the future. Those potential competitors include: (i) national and regional foodservice distributors, (ii) local wholesalers and brokers, (iii) food retailers, and (iv) farmers’ markets. The national and regional distributors are experienced in operating multiple distribution locations and expanding management, and they have greater marketing and financial resources than we do. Even though they currently offer only a limited selection of Chinese and Asian specialty foods, they may be able to devote greater resources to sourcing, promoting and selling their products if they choose to do so. Conversely, the local wholesalers and brokers are small in size with a deep understanding of local preferences, but their lack of scale results in high risk and limited growth potential.

If more competitors enter this market segment aiming to serve Chinese/Asian restaurants in the future, our operating results may be negatively impacted through a loss of sales, reduction in margins from competitive price changes, and/or greater operating costs, such as marketing costs, due to the increase of competition.

We may not be able to fully compensate for increases in fuel costs when fuel prices experience high volatility, and our operating results would be adversely affected.

Volatile fuel prices have a direct impact on the industry served by us. We require significant quantities of fuel for delivery vehicles and are exposed to the risk associated with fluctuations in the market price for fuel. The price and supply of fuel can fluctuate significantly based on international, political and economic circumstances, as well as other factors outside our control, such as actions by the Organization of the Petroleum Exporting Countries, or OPEC, and other oil and gas producers, regional production patterns, weather conditions and environmental concerns. The cost of fuel affects the price paid by us for products, as well as the costs we incur to deliver products to the customers. Although we have been able to pass along a portion of increased fuel costs to our customers in the past, there is no guarantee that we will be able to do so in the future. If fuel costs increase in the future, we may experience difficulties in passing all or a portion of these costs along to its customers, which may have a negative impact on our results of operations.

Disruption of relationships with vendors could negatively affect our business. Suppliers may increase product prices, which could increase our product costs.

We purchase our food items and related products from third-party suppliers. Although our purchasing volume can provide benefits when dealing with suppliers, suppliers may not provide the products and supplies needed by us in the quantities and at the prices requested. The cancellation of our supply arrangement with any of our suppliers or the disruption, delay and/or inability to supply the requested products by our suppliers could adversely affect our sales. If our suppliers fail to comply with food safety or other laws and regulations, or face allegations of non-compliance, their operations may be disrupted. We cannot assure you that we would be able to find replacement suppliers on commercially reasonable terms.

In addition, we purchase seasonal Chinese vegetables and fruits from farms and other vendors. Increased frequency or duration of extreme weather conditions could impair production capabilities, disrupt our supply chain or impact demand for our products. Input costs could increase at any point in time for a large portion of the products that we sell for a prolonged period. Our inability to obtain adequate supplies of food items and related products as a result of any of the foregoing factors or otherwise could mean that we are unable to fulfill our obligations to customers, and customers may turn to other distributors.

The purchase prices of our products vary from time to time, which is subject to market conditions and negotiation with our suppliers. The prices of some of our products, especially seasonal products, such as vegetables and fruits, have significant fluctuation. We can mitigate the risk of fluctuation in the purchasing and distribution costs by either fixing a price for a certain supply period through negotiation with our suppliers, streamlining our inventory turnover, and passing portions of the price fluctuation to our customers. However, we may not always be able to do that if there are significant and frequent fluctuations. If we are unable to mitigate these price fluctuations, our performance results will be adversely affected.

As a foodservice distributor, it is necessary for us to maintain an inventory of products that may have declines in product pricing levels between the time we purchase the product from suppliers and the time we sell the product to customers, which could reduce the margin on that inventory, adversely affecting our results of operations.

Our relationships with customers may be materially diminished or terminated. The loss of customers could adversely affect our business, financial condition, and results of operations.

We have maintained long-standing relationships with a number of our customers. However, those customers could unilaterally terminate their relationship with us or materially reduce the amount of business they conduct with us at any time. Our customers may shift their purchase orders from us to other competitors due to market competition, change of customer requirements and preferences, or because of the customer’s financial condition. There is no guarantee that we will be able to maintain relationships with any of our customers on acceptable terms, or at all. The loss of a number of customers could adversely affect our business, financial condition, and results of operations.

Changes in consumer eating habits could materially and adversely affect our business, financial condition, and results of operations.

We provide foodservice distribution to Chinese/Asian restaurants, primarily Chinese takeout restaurants, which focus on serving Chinese food to non-Chinese Americans. Changes in consumer eating habits (such as a decline in consuming food away from home, a decline in portion sizes, or a shift in preferences toward western foods) could reduce demand for our products. Consumer eating habits could be affected by a number of factors, including attitudes regarding diet and health or new information regarding the health effects of consuming certain foods. If consumer eating habits change significantly, we may be required to modify or discontinue sales of certain items in our product portfolio, and we may experience higher costs and/or supply shortages associated with our efforts to accommodate those changes as our suppliers adapt to new eating preferences. Additionally, changes in consumer eating habits may result in the enactment or amendment of laws and regulations that impact the ingredients and nutritional content of our food products, or laws and regulations requiring us to disclose the nutritional content of our food products. Compliance with these laws and regulations, as well as others regarding the ingredients and nutritional content of food products, may be costly and time-consuming. We cannot make any assurances regarding our ability to effectively respond to changes in consumer culture preference, health perceptions or resulting new laws or regulations or to adapt our product offerings to trends in eating habits.

The coronavirus pandemic may adversely affect our sources of supply and our sales.

The impact on our business of the coronavirus outbreak is unknown at this time, but the developing situation could have some negative effect on the operations of our suppliers and services vendors, both domestically and in China, as well as on our US domestic sales revenue in the event that consumer behaviors change in response to the public health epidemic.

We may not be able to achieve the financial targets in the projections disclosed in our June 18, 2018 Proxy Statement.

Our ability to meet the financial targets as disclosed in our June 18, 2018 Proxy Statement depends largely on our successful execution of business plan including various related initiatives. There are various risks related to these efforts, including the risk that these efforts may not provide the expected benefits in our anticipated time frame, if at all, and may prove costlier than expected; and the risk of adverse effects to our business, results of operations and liquidity if past and future undertakings, and the associated changes to our business, do not prove to be cost effective or do not result in the cost savings and other benefits at the levels that we anticipate. Our intentions and expectations with regard to the execution of our business plan, and the timing of any related initiatives, are subject to change at any time based on management’s subjective evaluation of our overall business needs. If we are unable to successfully execute our business plan, whether due to the failure to realize the anticipated benefits from our various business initiatives in the anticipated time frame or otherwise, we may be unable to achieve these financial targets.

We may be unable to protect or maintain our intellectual property, which could result in customer confusion, a negative perception of our brand and adversely affect our business.

We believe that our intellectual property has substantial value and has contributed significantly to the success of our business. In particular, our “HF” logo trademarks and the name “Han Feng,” are valuable assets that reinforce our customers’ favorable perception of our products. Our trademark rights and related registrations may be challenged in the future and could be canceled or narrowed. Failure to protect our trademark rights could cause customer confusion or negatively affect customers’ perception of our brand and products, and eventually adversely affect our sales and profitability. Moreover, intellectual property disputes and proceedings and infringement claims may result in a significant distraction for management and significant expense, which may not be recoverable regardless of whether we are successful. Such proceedings may be protracted with no certainty of success, and an adverse outcome could subject us to liability, force us to cease use of certain trademarks or other intellectual property or force us to enter into licenses with others. Any one of these occurrences may have a material adverse effect on our business, results of operations and financial condition.

If we are unable to renew or replace our current leases on favorable terms, or any of our current leases are terminated prior to expiration of their stated terms, and we cannot find suitable alternate locations, our operations and profitability could be negatively impacted.

We currently have leases for some of our warehouses. Our ability to re-negotiate favorable terms on an expiring lease or to negotiate favorable terms for a suitable alternate location, and our ability to negotiate favorable lease terms for additional locations, could depend on conditions in the real estate market, competition for desirable properties, our relationships with current and prospective landlords, and/or other factors that are not within our control. Any or all of these factors and conditions could negatively impact our growth and profitability.

Failure to retain our senior management and other key personnel may adversely affect our operations.

Our success is substantially dependent on the continued service of our senior management and other key personnel. These executives have been primarily responsible for determining the strategic direction of our business and for executing our growth strategy and are integral to our brand and culture, and the reputation the Company enjoys with suppliers and consumers. The loss of the services of any of these executives and other key personnel could have a material adverse effect on our business and prospects, as we may not be able to find suitable individuals to replace them on a timely basis, if at all. In addition, any such departure could be viewed in a negative light by investors and analysts, which may cause our stock price to decline. The loss of key employees could negatively affect our business.

If we are unable to attract, train and retain employees, we may not be able to grow or successfully operate our business.