Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - PPD, Inc. | ppdex322cfo.htm |

| EX-32.1 - EXHIBIT 32.1 - PPD, Inc. | ppdex321ceo.htm |

| EX-31.2 - EXHIBIT 31.2 - PPD, Inc. | ppdext312cfo.htm |

| EX-31.1 - EXHIBIT 31.1 - PPD, Inc. | ppdex311ceo.htm |

| EX-23.1 - EXHIBIT 23.1 - PPD, Inc. | ppdex231consent.htm |

| EX-4.5 - EXHIBIT 4.5 - PPD, Inc. | ppdex45.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number: 001-39212

PPD, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 45-3806427 | ||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||

929 North Front Street, Wilmington, North Carolina 28401 | |||

(Address of Principal Executive Offices) (Zip Code) | |||

910-251-0081

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock, par value $0.01 per share | PPD | The NASDAQ Stock Market LLC (Nasdaq Global Select Market) |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes o No x

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | o | Accelerated filer | o |

Non-accelerated filer | x | Smaller reporting company | o |

Emerging growth company | o | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

As of June 28, 2019, the last business day of the registrant’s most recently completed second quarter, the registrant’s common stock was not publicly traded. The registrant's common stock, $0.01 par value per share, began trading on The Nasdaq Global Select Market (“Nasdaq”) on February 6, 2020. As of February 27, 2020, the aggregate market value of the registrant’s common stock held by non-affiliates was approximately $2,001.7 million (based upon the closing sale price of the common stock on that date on Nasdaq). For purposes of this computation, shares of the registrant’s common stock held by affiliates, including executive officers, directors and certain holders known to the registrant, have been excluded.

As of February 27, 2020, the registrant had outstanding 348,580,422 shares of common stock.

DOCUMENTS INCORPORATED BY REFERENCE

No items are incorporated by reference into this Annual Report on Form 10-K.

PPD, INC.

ANNUAL REPORT ON FORM 10-K

FOR FISCAL YEAR ENDED DECEMBER 31, 2019

TABLE OF CONTENTS

Item | Page | |

PART I | ||

1. | Business | |

1A. | Risk Factors | |

1B. | Unresolved Staff Comments | |

2. | Properties | |

3. | Legal Proceedings | |

4. | Mine Safety Disclosures | |

PART II | ||

5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

6. | Selected Financial Data | |

7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

7A. | Quantitative and Qualitative Disclosures About Market Risk | |

8. | Financial Statements and Supplementary Data | |

9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | |

9A. | Controls and Procedures | |

9B. | Other Information | |

PART III | ||

10. | Directors and Executive Officers of the Registrant and Corporate Governance | |

11. | Executive Compensation | |

12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

13. | Certain Relationships and Related Transactions, and Director Independence | |

14. | Principal Accountant Fees and Services | |

PART IV | ||

15. | Exhibits and Financial Statement Schedules | |

Exhibit Index | ||

16. | Form 10-K Summary | |

Signatures | ||

2

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Such forward-looking statements reflect, among other things, our current expectations and anticipated results of operations, all of which are subject to known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements, market trends, or industry results to differ materially from those expressed or implied by such forward-looking statements. Therefore, any statements contained herein that are not statements of historical fact may be forward-looking statements and should be evaluated as such. Without limiting the foregoing, the words “anticipate,” “expect,” “suggest,” “plan,” “believe,” “intend,” “project,” “forecast,” “estimates,” “targets,” “projections,” “should,” “could,” “would,” “may,” “might,” “will,” and the negative thereof and similar words and expressions are intended to identify forward-looking statements. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in “Risk Factors” in Part I, Item 1A of this report. Unless legally required, we assume no obligation to update any such forward-looking information to reflect actual results or changes in the factors affecting such forward-looking information.

When we use the terms “PPD,” the “Company,” “we,” “us” or “our” in this Annual Report on Form 10-K, we mean PPD, Inc. and its subsidiaries on a consolidated basis, unless the context indicates otherwise.

WEBSITE AND SOCIAL MEDIA DISCLOSURE

We use our website (www.ppdi.com) and our corporate Facebook, LinkedIn, and Twitter accounts as channels of distribution of Company information. The information we post through these channels may be deemed material. Accordingly, investors should monitor these channels, in addition to following our press releases, Securities and Exchange Commission (the “SEC”) filings and public conference calls and webcasts. The contents of our website and social media channels are not, however, a part of this Annual Report on Form 10-K.

TRADEMARKS AND SERVICE MARKS

All trademarks, trade names, product names, graphics and logos of PPD contained herein are trademarks or registered trademarks of PPD, Inc. or its subsidiaries, as applicable, in the United States and/or other countries. All other party trademarks, trade names, product names, graphics and logos contained herein are the property of their respective owners. The use or display of other parties’ trademarks, trade names, product names, graphics or logos is not intended to imply, and should not be construed to imply, a relationship with, or endorsement or sponsorship of PPD, Inc. or its subsidiaries by such other party. Solely for convenience, we may refer to trademarks in this Annual Report on Form 10-K without the TM and ® symbols. Such references are not intended to indicate, in any way, that we will not assert, to the fullest extent permitted by law, our rights to our trademarks. Other trademarks appearing in this Annual Report on Form 10-K are the property of their respective owners.

INDUSTRY AND MARKET DATA

Market data used throughout this Annual Report on Form 10-K is based on management’s knowledge of the industry and the good faith estimates of management. All of management’s estimates presented herein are based on industry sources, including analyst reports and management’s knowledge. We also relied, to the extent available, upon management’s review of independent industry surveys and publications prepared by a number of sources and other publicly available information. We are responsible for all of the disclosure in this Annual Report on Form 10-K and while we believe that each of the publications, studies and surveys used throughout this Annual Report on Form 10-K are prepared by reputable sources and are generally reliable, we have not independently verified market and industry data from third-party sources. All of the market data used in this Annual Report on Form 10-K involves a number of assumptions and limitations and therefore is inherently uncertain and imprecise, and you are cautioned not to give undue weight to such estimates. Projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors” in Part I, Item 1A of this Annual Report on Form 10-K and elsewhere in this Annual Report on Form 10-K. These and other factors could cause results to differ materially from those expressed in our estimates and beliefs and in the estimates prepared by independent parties.

3

Part I

Item 1. Business

Our Company

We are a leading provider of drug development services to the biopharmaceutical industry, focused on helping our customers bring their new medicines to patients around the world. We have been in the drug development services business for more than 30 years, providing a comprehensive suite of clinical development and laboratory services to pharmaceutical, biotechnology, medical device and government organizations, as well as other industry participants. Over that time, we have developed a track record of consistent quality, delivery and continuous innovation that has enabled us to grow faster than our underlying market over the past five years and deliver strong financial results. In 2019, we served all of the top 50 biopharmaceutical companies in the world, as ranked by 2018 research and development (“R&D”) spending, and, in 2018, were involved in 66 drug approvals. We also participated in the development of all of 2018’s top ten selling drugs, as ranked by 2018 revenue. Since 2014, we have also worked with over 300 companies in the growing biotechnology sector through our PPD Biotech model, which was built specifically to serve the unique needs of this customer segment. We have two reportable segments, Clinical Development Services and Laboratory Services.

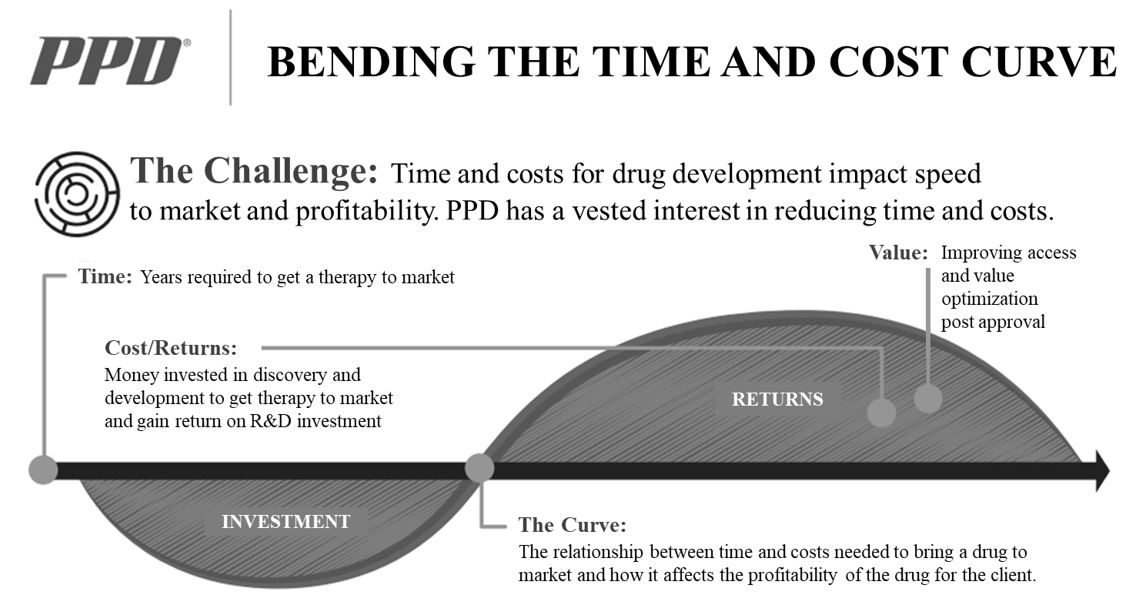

Our purpose and mission are to improve health by helping our customers deliver life-changing therapies to patients. We pursue our purpose and mission through our clinical development and laboratory services and our strategy to bend the cost and time curve of drug development and optimize value for our customers.

Our customers benefit from accelerated time to market because it results in lengthened periods of market exclusivity, and our real-world evidence solutions support the superior efficacy and health economics of their novel therapies. We believe our medical, scientific and drug development expertise, along with our innovative technologies and knowledge of global regulatory requirements help our customers accelerate the development of safe and effective therapeutics and maximize returns on their R&D investments.

Our service offerings include both clinical development and laboratory services. Our clinical development services include all phases of development (i.e., Phase I-IV), peri- and post-approval and site and patient access services. Our laboratory services offer a range of high-value, advanced testing services, including bioanalytical, biomarker, vaccine, good manufacturing practice (“GMP”) and central laboratory services. We have deep experience across a broad range of rapidly growing areas of drug development and engage with customers through a variety of commercial models, including both full-service and functional service partnerships and other offerings tailored to address the specific needs of our customers.

We have developed significant expertise in the design and execution of complex global clinical trials, a result of conducting studies on global, national, regional and local levels across a wide spectrum of therapeutic areas for more than 30 years and in over 100 countries. Our customers entrust us to design, execute and deliver results on some of the most critical aspects of the drug development process for the key assets in their pipelines.

4

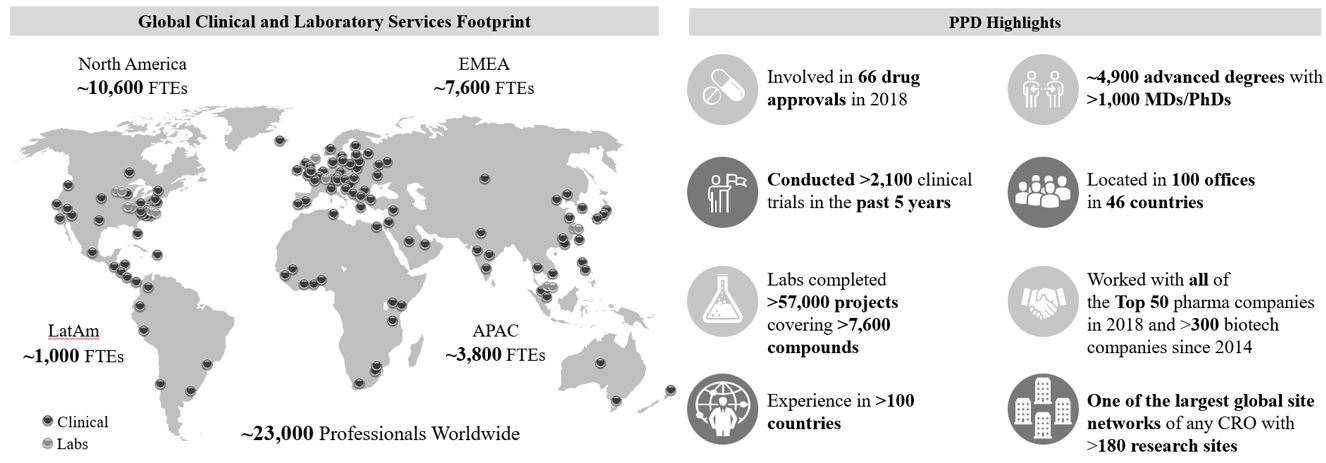

As of December 31, 2019, we had more than 23,000 employees worldwide, approximately 5,100 of whom hold advanced degrees, and we had 100 offices in 46 countries. Over the last five years, we have conducted more than 2,100 clinical trials, and our laboratory scientists have completed more than 57,000 pharmaceutical development projects and worked with more than 7,600 compounds. Among other elements, our ability to successfully assess feasibility in the context of study design, recruit for increasingly specialized patient populations and devise optimal regulatory strategies is essential to our competitive advantage in winning new studies.

Our deep understanding of the drug development process has allowed us to effectively invest in and evolve our service offerings to meet the needs of our customers. We have developed a differentiated site and patient access capability, built a delivery model for biotechnology companies, invested in advanced laboratory testing, broadened the scope of our peri- and post-approval services and expanded our global presence. Specific examples of some of our recent initiatives and investments include:

• | Innovative site and patient access. We have developed differentiated capabilities that meaningfully address two of the biggest challenges that our customers face: patient enrollment and site performance. Through our Accelerated Enrollment Solutions (“AES”) delivery model, we focus on meeting the unique feasibility, site start-up and patient recruitment needs of each study. We address these complex needs by leveraging (i) large data sets, including identified and consented personal data on 100 million U.S. households and health information on approximately 20 million previously screened study candidates and (ii) our global site network of over 180 research sites across five continents and 17 countries. |

• | Purpose-built PPD Biotech. Over the past five years, we pioneered the development, implementation and scaling of a purpose-built, customer-facing delivery model to address the specific needs of the increasingly relevant biotechnology sector. Our model is founded on (i) dedicating commercial, medical, operational and functional leaders to our biotechnology customers and (ii) allocating the right mix of experienced resources to drive their drug development programs. |

• | Advanced laboratory services. Over the last five years, in response to strong customer demand for our services (over $1 billion of laboratory services in our backlog as of December 31, 2019), we have invested over $200 million to significantly increase the size and operating capacity of our laboratory facilities, acquire innovative laboratory equipment, expand our test menus and build out differentiated IT systems and laboratory automation. |

• | Innovative peri-and post-approval studies. Our customers increasingly require evidence-based solutions to help them demonstrate the real-world effectiveness, safety and value of newly approved therapies, which are essential to optimize the commercial potential of their products. We have significantly expanded our capabilities in this growing area, providing our customers with service offerings in areas such as (i) market access, (ii) health economics modeling and (iii) patient-centered research. |

• | Targeted geographic expansion. We maintain a strong presence of experienced professionals in all key regions and countries necessary to support our customers’ global drug development programs. In response to the growing importance of conducting global studies that include cohorts in Japan and China and the opportunity to serve local customers in those geographies with their global drug development needs, we have significantly increased the size and scale of our operations in those countries while maintaining the quality and operating standards demanded by our customers and regulatory authorities alike. |

We believe these investments in our businesses and our innovative solutions have enhanced the strength of our clinical development and laboratory services and further differentiated our offerings from other clinical development organizations, providing us with meaningful competitive advantages and growth opportunities.

Our Industry

The drug development process involves the testing of drug candidates to demonstrate safety and efficacy in order to meet regulatory requirements. Developing new drugs for the treatment of human disease is an extremely expensive, complex, high-risk and time-consuming process. It is estimated that bringing a new drug or medical device to market can take up to 15 years and cost $2.5 billion or more.

5

The Drug Development Process

The drug development process consists of two stages: pre-clinical and clinical. In the pre-clinical stage, the new drug candidate is tested in vitro and in vivo in animals, generally over a one- to three-year period, to assess and optimize potential use in humans. After successful pre-clinical testing and receipt of required regulatory authorizations, the new drug candidate can be advanced to the clinical development stage, which involves testing in humans. As we do not participate in the pre-clinical market, the following discussion describes the clinical drug development process in the context of the U.S. regulatory framework. The clinical drug development process and regulatory frameworks in other countries can vary from the United States framework, but in many ways are substantially similar.

Prior to commencing human clinical trials in the United States, a company must file with the U.S. Food and Drug Administration (“FDA”) an investigational new drug application (“IND”) containing information about animal toxicity and distribution studies, manufacturing and control data, stability data, a clinical development plan and a study protocol for the initial proposed clinical trial. The design of these trials, described in the study protocols, is essential to the success of the drug development effort. The studies are designed to generate the type of clinical data that will support the development of the drug candidate and, ultimately, potentially support regulatory approval. An IND must become effective in order for human clinical trials to begin. If the FDA does not place the IND on clinical hold within 30 days after an IND filing, human clinical trials may begin upon expiration of the 30-day period or upon earlier notification by the FDA that the clinical investigations may begin.

The clinical stage is the most time-consuming and expensive part of the drug development process. During the clinical stage, the drug candidate undergoes a series of tests in humans, including healthy volunteers, as well as participants with the targeted disease or condition. Human trials usually start on a small scale to assess safety, efficacy and dosage (Phase I-II) and then expand to larger trials (Phase III) to test efficacy and safety in the target population. These trials are generally conducted in the following sequential phases, which may overlap or be combined:

• | Phase I trials involve testing the drug candidate on a limited number of healthy individuals, typically 20 to 80 people, to determine the drug candidate’s basic safety data, including tolerance, absorption, metabolism and excretion. This phase lasts an average of six months to one year. In some therapeutic areas such as oncology, where cytotoxic compounds are being investigated, it is sometimes necessary to run Phase I trials in diagnosed patients instead of healthy individuals. |

• | Phase II trials involve testing a small number of volunteer participants, typically 100 to 200 people, who suffer from the targeted disease or condition, to assess the drug candidate’s effectiveness and how different doses work. This phase lasts an average of one to two years. |

• | Phase III trials involve testing large numbers of participants, typically several hundred to several thousand people, to evaluate efficacy on a large scale, as well as long-term safety. These trials involve numerous sites and generally last two to three years, but can be shorter or longer. |

• | Phase IV or post-approval clinical trials involve monitoring or verifying the risks and benefits of a drug product. |

• | Real-world data and evidence studies, meaning data and evidence gathered outside of the context of clinical trials, are often used to assess usage, potential benefits or risks, safety, effectiveness and health economics to achieve successful market access and product uptake. |

Our Markets

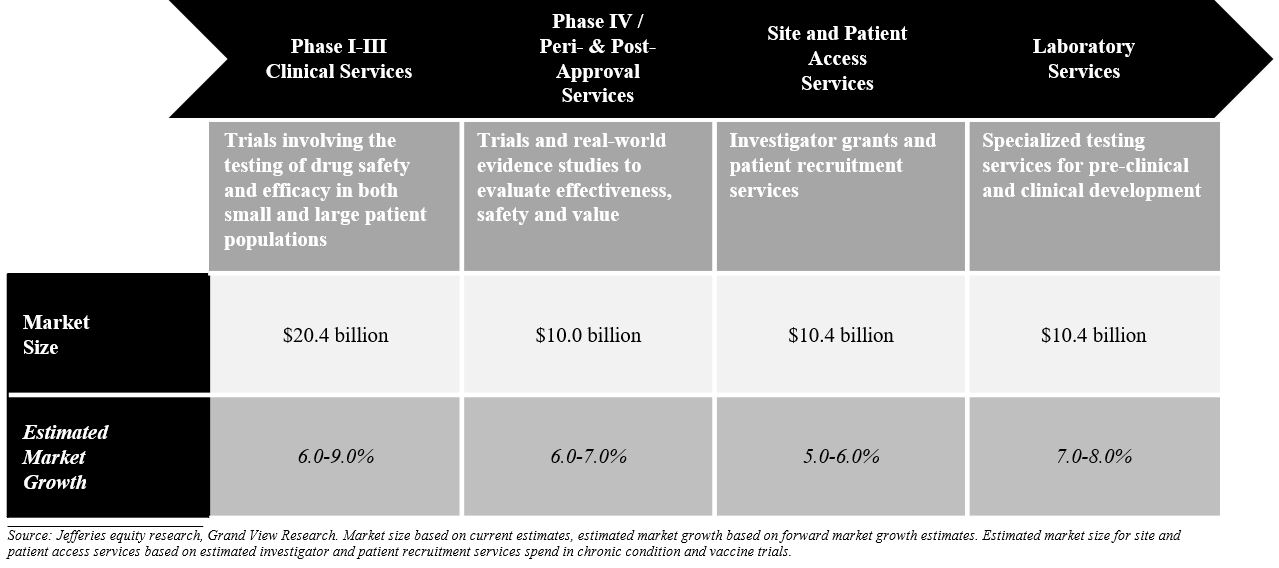

As of December 31, 2019, our total addressable market was greater than $51 billion, consisting of clinical development services, including peri- and post-approval services and site and patient enrollment services, and laboratory services. We believe the clinical development services (Phase I–III), or clinical research organization (“CRO”), market to be an approximately $20.4 billion market as of December 31, 2019 and expect this market to continue to grow at an average annual growth rate of approximately 6-9%. We have expanded our capabilities in the $10.0 billion Phase IV and peri- and post-approval services market, which we anticipate will grow at an annual growth rate of approximately 6-7%. Our AES delivery model has allowed us to participate in the economics and growth of the investigator and patient recruitment market that otherwise would represent pass-through revenues, as it does for most other CROs. We expect this to be an approximately $10.4 billion market and anticipate it to grow at an annual growth rate of approximately 5-6%. In addition to competing in the CRO market, through our strategic investments we have strengthened our position in the laboratory services market and expanded our addressable market to include the markets for investigator and patient recruitment and peri- and post-approval services. In laboratory services, in addition to the $4.3 billion central laboratory market, we compete in the $6.0 billion market for advanced laboratory testing, which we anticipate will grow at an annual growth rate of 7-8%.

6

We believe there are five key trends affecting our end markets that will create increasing demand for our offering of services:

• | Growth in R&D spending. Biopharmaceutical companies must continually invest in drug development in order to create innovative new therapies or use existing drugs to treat new indications, to address unmet medical needs and to replace lost revenues when their currently marketed drugs lose patent protection. From 2008 to 2018, R&D spending increased approximately 3.3% annually, driven by long-term secular fundamentals including a 30% increase in active INDs and an approximately 80% increase in average annual FDA approvals from 2008 to 2018. |

• | Increased levels of outsourcing by biopharmaceutical companies. As biopharmaceutical companies continue to seek ways to reduce clinical development costs and focus resources on core competencies, we believe they will continue to increase the amount of clinical development work they outsource to CROs. Outsourcing penetration as a percentage of total development spending by biopharmaceutical companies increased from approximately 36% in 2007 to approximately 49% in 2018. Drivers of increased outsourcing include: |

• | biopharmaceutical companies’ desire for flexible cost structures and focus on core competencies; |

• | experience, expertise, capability and value provided by CROs; |

• | difficulty conducting large, global and complex clinical trials required by the current regulatory environment; |

• | ability to generate real-world data and evidence; and |

• | desire to address declining R&D productivity by utilizing more efficient means of conducting clinical trials. |

• | Increased complexity in clinical development. Clinical trials continue to increase in complexity due to a confluence of factors including, but not limited to, (i) new therapeutic modalities, (ii) the collection of more clinical trial endpoints, (iii) more specific patient inclusion/exclusion criteria, (iv) ever-changing regulatory requirements and (v) an expansion of evidence generation methods, such as electronic patient-reported outcomes and virtual clinical trials. All of these factors result in more complex trial design, challenges in enrolling protocol-eligible patients, longer duration of clinical trials and greater overall clinical trial cost. As a result, we expect biopharmaceutical companies to increasingly seek partners that have the experience and expertise to conduct cost-effective clinical studies. In particular, we believe large CROs who possess scale, geographic reach and differentiated capabilities to manage the complexity of clinical trials will continue to grow at a higher rate and take market share versus the overall industry. |

7

• | Biotechnology sector growth. The U.S. biotechnology sector has grown rapidly over the last decade and has emerged as a key customer segment for the drug development services industry. The rate of biotechnology companies’ R&D spending growth has been higher than that of traditional pharmaceutical companies in recent years, and we believe that over the last five years, innovative biotechnology companies have accounted for approximately 40% of new drug approvals (“NDAs”). This has largely been fueled by a robust funding environment, both public and private, with over $150 billion of capital raised for biotechnology companies in the last three years. Today, we believe the majority of biotechnology companies have enough cash on hand to fund R&D expenditures for two to three years. Many biotechnology companies are smaller, discovery research-focused organizations that do not find it economically attractive to invest in the infrastructure and personnel necessary to conduct their clinical development programs on their own, and we believe they will continue to rely on CROs, like us, for their global drug development needs. |

• | Increasing importance to prove value of new therapies. As participants in the healthcare industry are increasingly focused on managing costs, biopharmaceutical companies need to find alternatives to align market constituents on the value of their treatments. The ability to perform peri- and post-approval studies to transform real-world data (such as medical claims data or electronic medical records) into real-world evidence provides biopharmaceutical companies a solution to quantify the value of new therapies to market constituents. Real-world data and evidence enable biopharmaceutical companies to develop better therapies and optimize the commercial potential of their new therapies. With increased R&D activity and competition among newly approved therapies in similar indications, we anticipate the continued adoption of real-world data and evidence to demonstrate the value of new medicines. |

Our Competitive Strengths

We believe we are well-positioned to serve the global biopharmaceutical industry in obtaining the approval for, and maximizing the market access and value of, their new medicines. We differentiate ourselves from others in our industry through our competitive strengths, which include:

Leading Drug Development Expertise with Scale and a Long Track Record of Excellence

We are one of the world’s largest providers of clinical development services, with the scale to leverage investments in capabilities and innovative solutions to serve the increasingly complex and diverse needs across our extensive customer base. As of December 31, 2019, we had more than 23,000 employees worldwide and 100 offices in 46 countries, allowing us to offer our customers global infrastructure and deep expertise across a broad range of therapeutic areas and all stages of clinical development.

Through our integrated global platform and workforce, we provide our customers with consistent quality and operating standards worldwide, thereby minimizing risks in, and maintaining the integrity of, the evidence generation process without the need to rely on local sub-contractors or vendors. We have developed our scale, capabilities and track record of quality and innovation over a more than 30-year history, earning us a reputation as a leading global partner to the most sophisticated biopharmaceutical companies. In 2019, for the eighth consecutive year, we were recognized by Life Science Leader magazine for excellence in clinical research. We believe the combination of our scale, expertise, track record and innovative offerings positions us to continue to grow and take market share within the industry.

8

Differentiated Clinical Development Services

Building on our solid foundation, we have invested heavily in recent years to further strengthen our competitive position through differentiated clinical development solutions designed to address our customers’ needs and bend the time and cost curve of their clinical trials. Our key clinical development investments include:

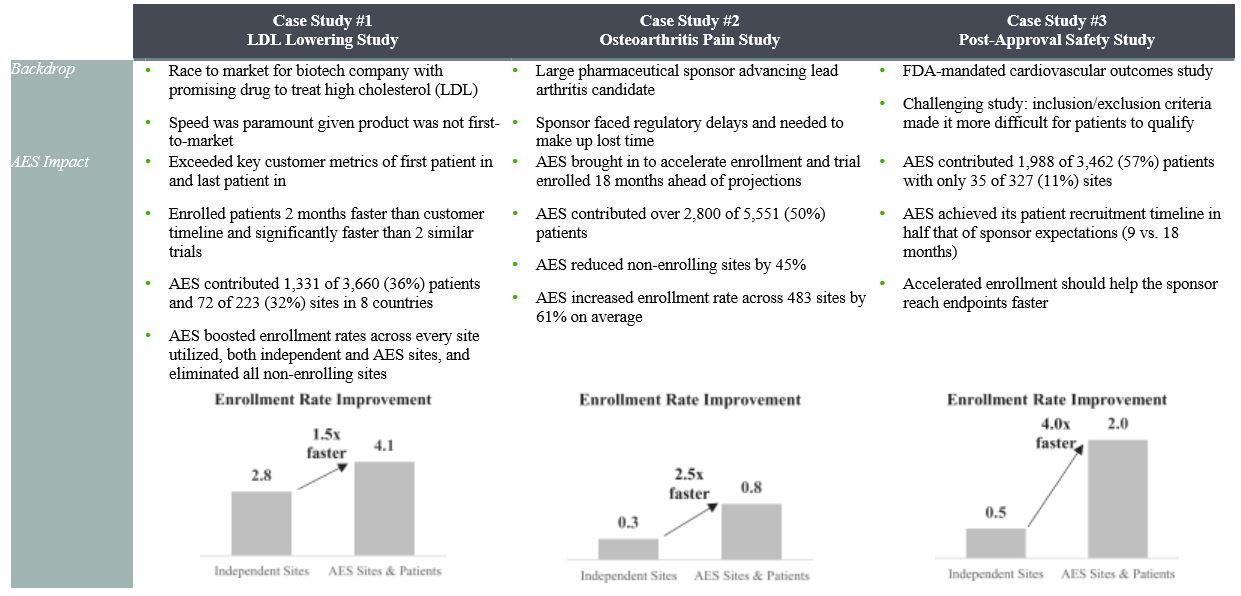

• | Study start-up. We have acquired and embedded leading technologies and tools in our global start-up processes to (i) improve feasibility by helping our customers assess trial viability quickly and effectively and (ii) reduce study start-up timelines. Due to the substantial costs and investments associated with clinical trial starts, our ability to reduce key cycle times to below-industry averages addresses a critical need of our customers. For example, our median cycle time from final protocol received (“FPR”) to first site activated is more than 10% faster than industry benchmark cycle times. Similarly, our median time from FPR to the milestone of 50% of sites activated is more than 10% faster than industry benchmarks. This accelerated site activation, coupled with our clinical operations, has also resulted in significantly improved patient enrollment timelines: FPR to first patient, first visit is more than 10% faster and FPR to 50% patients enrolled is more than 30% faster than benchmarks. |

• | Accelerated Enrollment Solutions: Our AES delivery model aligns the fundamental components of the clinical trial execution process and extends across five continents, 17 countries and over 180 research sites. In the past five years, AES has participated in over 750 studies, including trials conducted by us, our customers and other CROs. Since 2013, we have deployed over $600 million making strategic acquisitions and bringing together complementary capabilities to create a delivery model which would be difficult to replicate. We believe our AES delivery model represents the industry’s largest aggregation of fully identified data on individuals who have provided their consent and indicated an interest in participating, or have participated, in clinical trials. With our AES delivery model, we are able to provide significant flexibility to our customers, giving them the ability to engage us for (i) discrete components of our AES service offerings, (ii) the full suite of AES capabilities or (iii) wholly integrated constructs which combine our AES offerings with our clinical development services. Through this model, we have been able to deliver compelling value propositions to our customers, including: |

◦ | significant percentages (e.g., 30% - 80%) of their trial enrollment with fewer sites, in less time and under one contract and uniform procedures and quality standards; and |

◦ | significantly faster start-up times and higher enrollment rates than the independent site model. |

9

• | Site monitoring. We have built and implemented a global risk-based monitoring model designed to efficiently focus site monitoring resources on key risks. Driven by an adaptive and intelligent monitoring model powered by real-time data analytics and remote site monitoring, we are able to provide an efficient and cost-effective study monitoring solution focused on the prevention and mitigation of protocol compliance risks in our customers’ clinical development programs. By focusing our on-site monitors on key risks, our differentiated site monitoring solution enables us to reduce our monitors’ time on site, translating to faster and lower-cost clinical trials with better quality oversight. |

• | Peri- and post-approval services. We are a leading provider of real-world research and evidence-based solutions designed to help sponsors support the real-world effectiveness, safety and value of biopharmaceutical and biotechnology products with capabilities in 35 countries. Through this offering, we provide our customers with critical scientific expertise and global operational capabilities to help generate the evidence needed to optimize the market access and commercial potential of their products. As of December 31, 2019, we had over 450 scientists and consultants conducting real-world, patient-centered, health economics, epidemiological and market access research. We specialize in engaging with key market constituents early in the drug development process to create an evidence strategy that will meet the needs of all relevant stakeholders. We develop evidence to demonstrate the safety, effectiveness and value of over 150 drugs and therapies per year across more than 20 countries. We have also contributed to a number of payer submissions, including the reversal of multiple decisions by the U.K.’s National Institute for Health and Care Excellence. |

Comprehensive and Growing Laboratory Services

We own and operate an integrated and scaled suite of laboratory services. We offer a range of high-value, advanced testing services, including bioanalytical, biomarker, vaccines, GMP and central laboratory infrastructure to support R&D. We believe our scientific employee base with advanced degrees provides us with a competitive advantage – of our approximately 480 laboratory services scientists with advanced degrees, approximately 180 have PhDs and approximately 300 have MSs. Since 2015, we have invested an aggregate of over $200 million in capital expenditures to expand and enhance our global laboratory services capabilities and capacity. We believe we are differentiated from other laboratory providers by our global scale and the comprehensiveness of our service offering and focus on servicing the research needs of the biopharmaceutical industry. The breadth of our test menus, efficient technology and instrumentation platforms and global facility footprint allow us to offer a comprehensive set of scientific laboratory services. The ability to integrate patient data from the clinical trial and associated laboratory results has also contributed to increased customer wallet share. Our laboratory facilities have been successfully audited by customers and regulatory authorities over 1,100 times since 2014, and our track record of quality has significant reputational value. We believe we are one of the leading providers in each of the GMP, bioanalytical and central laboratory services sectors as well as in the growing vaccines market. In 2019, for the second time in three years, we were named Best CRO Provider at the World ADC Awards, a recognition of our efforts to help customers advance their antibody drug conjugates (“ADC”) research to develop new anticancer therapies.

Large and Growing Diversified Customer Base

Our leading capabilities are evidenced by the quality, scale and diversity of our customers. Over the past five years, we have provided services to all of the top 50 biopharmaceutical companies in the world, as ranked by 2018 R&D spending, small and mid-size pharmaceutical companies and over 300 biotechnology customers as well as government, academic and non-profit organizations. We have long-standing relationships with our customers as demonstrated by having provided services for a decade or more to each of our top ten customers by revenue for the year ended December 31, 2019. These relationships tend to have larger and longer-term contracts, which provide stability and visibility to our revenues. In addition, our customer base continues to grow and is very diverse, spanning key geographies, therapeutic areas and clinical stages of development. This diversity enables us to continuously develop and refine our expertise and enhance our ability to bend the cost and time curve of drug development and optimize value for our customers. We have also strategically positioned ourselves to benefit from the rapid growth of the biotechnology market through the formation and build-out of PPD Biotech where nearly 80% of our biotechnology awards are for Phase IIb-IV, post proof of concept drug development. As a result of our diversified customer base, no one customer accounted for more than 10% of our 2019 revenue.

10

Experienced, Highly Technical Organization with a Culture of Excellence and Industry-Leading Retention

We are led by an experienced and talented team of individuals who collectively have extensive experience in the CRO and biopharmaceutical industries. Many of our senior leaders previously worked for our biopharmaceutical customers, and as such have first-hand knowledge of the challenges our customers face in today’s clinical development environment. To achieve our goal of delivering best-in-class services to our customers, our management team has built a culture of excellence based on a set of defining principles by which we hire, develop and compensate our talent. The result is a company-wide culture focused on the pursuit of industry leadership, innovation and excellence aimed at our purpose and mission. We believe the technical and therapeutic expertise of our dedicated employees provides us with a competitive advantage—of our more than 23,000 employees as of December 31, 2019, approximately 5,100 hold advanced, masters or equivalent degrees, including over 1,100 MDs and PhDs. As a result, we have industry-shaping domain expertise and thought leadership, including in key areas such as product development strategy, protocol design, outcomes and patient-centered research and health economics. In recent years, we have made significant investments to build capabilities to effectively recruit, train, develop and retain talented individuals and teams. Our consistent focus on talent and culture has contributed to both overall retention and retention in key operational roles, such as project managers, that is significantly ahead of industry averages. Our low turnover rates in key operational roles provides our customers consistency in their study teams and is an important differentiator for us. For example, our project manager turnover rates have ranged from 8.9% in 2017 to 8.0% in 2019, which we believe is lower than industry averages. Our investment in these areas has been recognized by industry publications. In 2018, for the eighth consecutive year, we received honors from Training magazine for our employee training and development programs while Forbes magazine named us to their list of America’s Best Employers in the large company category in 2018 and 2019.

Disciplined Operational and Financial Approach

We have strategically oriented our business towards the largest and highest growth areas of the drug development services market, including key therapeutic areas, the biotechnology end market and peri- and post-approval services, in order to position ourselves to win high value-add business. Our operating model is focused on providing our customers with a mix of full-service contracts and select functional service provider (“FSP”) commercial arrangements in differentiated value-add areas. We have also leveraged our track record of operational discipline and expertise around contract pricing and backlog policy to create a highly visible and stable revenue base. Furthermore, we have focused our operations on key initiatives, including optimal utilization of billable staff and prudent cost management. Our positive historical operating results have allowed us to deploy significant capital into our business through strategic investments and acquisitions while also returning capital to our stockholders. We believe our strong financial profile demonstrates the quality and efficiency of our operating model and positions us for continued growth.

Our Growth Strategy

The key elements of our growth strategy to help our customers bend the cost and time curve of drug development include:

Further Strengthen Our Offerings in Existing and New Markets

Our global footprint, scale, integrated systems and deep scientific expertise enable us to conduct complex, multi-center clinical trials simultaneously throughout the world. We have a well-established presence in all of the major biopharmaceutical markets, including the United States, Europe and Asia, with nearly 3,800 professionals in the latter region and scale and differentiation in Japan and China, two countries of increasingly strategic importance for drug development programs. As a result, we continue to gain share within the CRO market as biopharmaceutical customers continue to look for strategic partners with global scale and service offerings to conduct complex global trials. We plan to further strengthen our leadership position by investing in geographies that are critical to address the needs of our customers and their drug development pipelines.

Expand Leading Therapeutic Expertise in Existing and Novel Areas

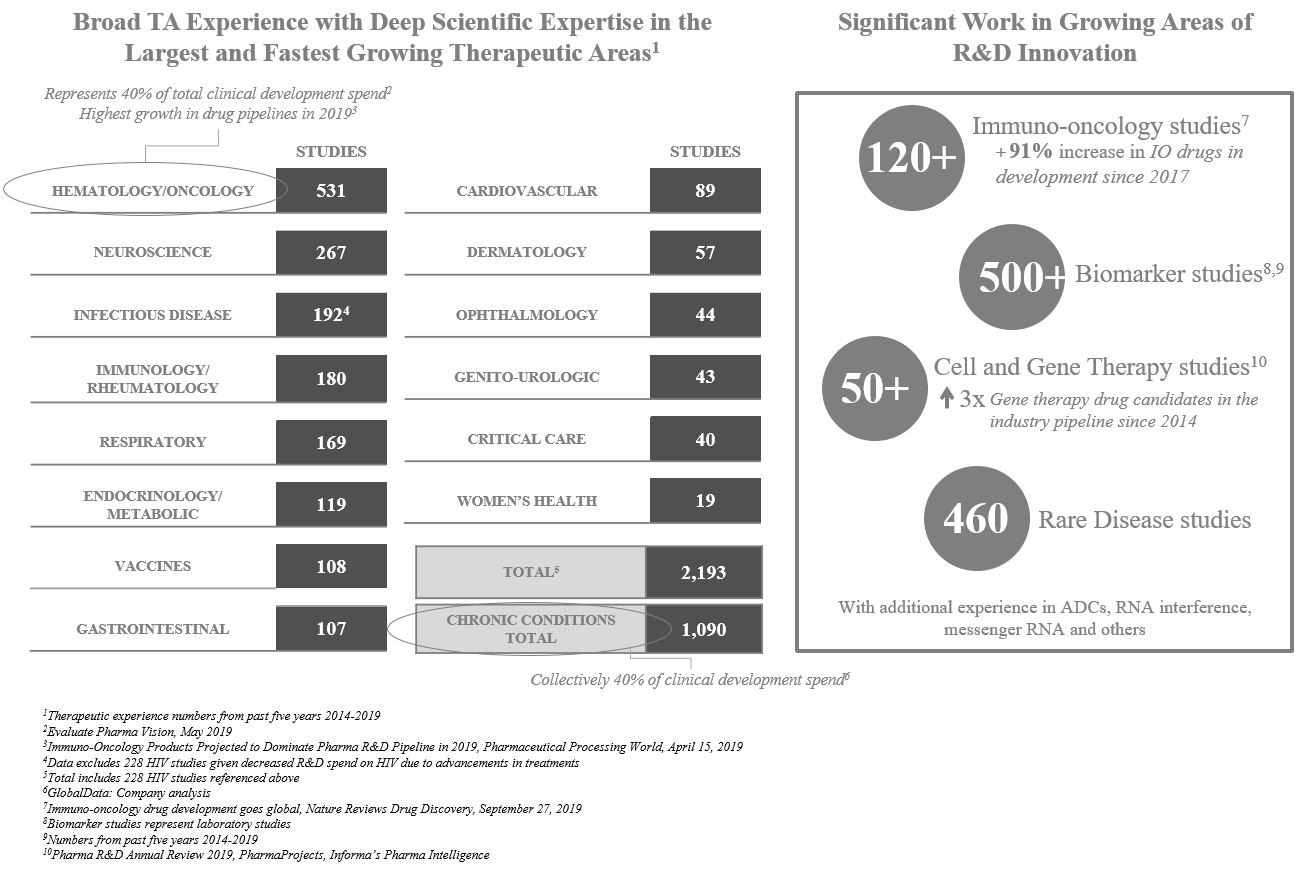

We have amassed deep scientific expertise in the largest and fastest growing therapeutic areas. In addition, we have developed specific capabilities in disciplines that cross therapeutic areas, such as rare diseases, vaccines and a broad array of chronic conditions. Over 75% of total R&D spend on late stage clinical trials conducted from 2015 through 2018 related to hematology/oncology and chronic conditions. Over the last five years, we have performed a significant amount of work in both of these areas, having provided services in over 500 hematology/oncology studies and over 1,000 chronic condition studies in the last five years.

11

We are also conducting significant work in growing areas of R&D innovation, such as immuno-oncology, which has experienced a 91% increase in the number of drugs in development since 2017, and cell and gene therapy, for which the industry pipeline of drugs has more than tripled since 2014. In addition, customers are hiring us to run their programs in other areas of innovative R&D, such as ADC’s, ribonucleic acid (“RNA”) interference, messenger RNA and others. We intend to continue investing in our scientific and operational capabilities to further strengthen our leadership position in key therapeutic areas and position ourselves to take advantage of the evolving trends in the biopharmaceutical industry.

Build Upon Our Existing Dedicated Biotech Offering

Over the last five years, innovative biotechnology companies focused on new and complex therapies have accounted for approximately 40% of NDAs and have driven significant growth in related R&D spending. Large biopharmaceutical companies have had to fill gaps in their pipelines through strategic collaborations with, and acquisitions of, biotechnology companies, further increasing growth in the number of innovative, complex and global clinical trials. We were at the forefront of realizing these trends and formed our dedicated PPD Biotech model in 2014. Since that time, we have more than doubled PPD Biotech annual authorizations and grown revenue by over 80%. We continue to leverage our sophisticated customer development activities within PPD Biotech, which include early identification of novel molecules and extensive pre-trial consultative advisory engagement with customers, to optimally position ourselves to win new business. PPD Biotech’s success is evidenced by the increase in our win rates from biotechnology companies whereby we have increased our average win rate from approximately 26% in 2016 to over 40% in 2019. We believe that our track record of serving biotechnology companies through our PPD Biotech model has earned us a reputation as the strategic partner of choice. Since the beginning of 2014, we have worked with some of the most innovative companies to help bring disease-modifying therapies to the market for patients. We believe our differentiated offering will enable us to continue to capture share within the biotechnology market.

12

Increase Use of Our Innovative Site Network and Patient Enrollment Platform

Through our AES delivery model, we have developed an approach to directly serve our customers’ needs by addressing patient enrollment and site performance challenges, which are two of the biggest challenges our customers face in clinical development. We believe our integrated strategy of using technology and identified and consented data, our global site network and support for leading independent sites, is the ideal approach to serving our customers. To date, AES has played a critical role in completing some of the most important and complex clinical trials for our customers. We plan to continue to build out our AES capabilities and further strengthen the value propositions we offer and deliver to our customers through this differentiated model.

In addition to providing us with a competitively advantaged asset, our AES delivery model is financially attractive as it allows us to participate in the economics and growth of the market for investigator and patient recruitment services that otherwise would represent pass-through revenues, as is the case for most other CROs.

Capitalize on our Growing Laboratory Segment

Our laboratory services offering is focused on the high-growth, innovative segment of laboratory services through its diverse range of high-value, advanced testing services. As an example, we have developed a significant and growing number of assays to address the testing needs of gene therapy. Our Laboratory Services segment represents approximately 19.0% of our 2019 total direct revenues and increased approximately 19.3% for the year ended December 31, 2019 as compared to the same period in 2018. It also affords us significant operating leverage and diversification, and provides higher backlog visibility and related conversion rates. Our Laboratory Services segment allows us to provide integrated offerings to customers that need both clinical development and laboratory services.

Continue to Invest in Innovation

We have consistently been and are committed to spending our time and resources on adding to and improving on our capabilities and service offerings. We assess the need to add new and innovative capabilities to reduce the cost and time required to generate evidence for our customers’ product candidates. We believe that the biopharmaceutical industry is constantly evolving and we are focused on evaluating opportunities in a disciplined manner that is both capital efficient and flexible in approach. We are adept at successfully identifying and executing on acquisitions, joint ventures and strategic venture investments to pursue and amplify nascent technologies and capabilities for our customers’ benefit, as evidenced by our investments in Science 37, Inc. and Medable, Inc.

Our Services

We are a leading provider of drug development services to the biopharmaceutical industry, offering comprehensive, integrated clinical development and laboratory services to our customers. We provide our services through our Clinical Development Services and Laboratory Services segments. Within each segment, we offer numerous services and solutions for our customers, and across segments our offerings are complementary so that customers may optimize their development programs and maximize value and outcomes by accessing our full suite of offerings.

Clinical Development Services

Our Clinical Development Services offerings span the lifecycle of clinical product development and include:

Product development and consulting services. We specialize in developing integrated product development strategies that provide biopharmaceutical companies with interdisciplinary preclinical, chemistry, manufacturing and controls, clinical and regulatory road maps for the development and marketing of their products and product candidates through the global product life cycle. Our services are designed to speed our customers’ product candidates to market with reduced operational risk and increased commercial potential. Our team of physicians, scientists, regulatory professionals and biostatisticians with pharmaceutical expertise offers specialized guidance across all major therapeutic areas, including oncology, cardiovascular disease and critical care, neurology and psychiatry, infectious diseases, rheumatology and metabolic diseases and across a range of specialized disciplines, including advanced therapies, biosimilars, pediatrics and rare diseases.

Early development services. We provide comprehensive support to early clinical development programs, including Phase I trials. We conduct early-phase studies at our 185-bed clinic in Austin, Texas for healthy volunteer studies, our 24-bed hospital-adjacent facility in Las Vegas, Nevada for both healthy and patient volunteer studies and our 52-bed hospital-adjacent facility in Orlando, Florida for healthy volunteer studies. Our Orlando facility also has two ten-bed intensive treatment rooms. We complement these Phase I units with a global network of affiliated clinical trial sites which provide access to numerous special populations and disease indications and a fully integrated early development services team providing streamlined program management, clinical monitoring, data management, biostatistics, clinical pharmacology, medical writing, regulatory and pharmacovigilance support. We have particular experience in the conduct of first in human studies and have specialized capabilities for flow cytometry measurement, allowing rapid measurement of cell surface biomarkers and conducting glucose clamp and other endocrinology and metabolic studies.

13

Phases II-IV clinical trial management. We provide full service protocol management for Phase II-IV clinical research studies for investigational new drugs, biologics and medical devices. The core of our Clinical Development Services offering is a comprehensive global suite of services for Phase II-IV clinical trials. These services include:

• | Protocol design; |

• | Clinical trial strategic feasibility and investigator site selection; |

• | Project management; |

• | Site study startup activities; |

• | Clinical monitoring and data capture; |

• | Data management; |

• | Biostatistics; |

• | Safety medical monitoring/pharmacovigilance; |

• | Regulatory affairs; |

• | Medical writing; |

• | Global clinical supplies – including depots in Kiev, Ukraine; Moscow, Russia; Johannesburg, South Africa; and Athlone, Ireland; |

• | eClinical services; |

• | Quality assurance; and |

• | Virtual and digitally-enabled solutions. |

We provide these services under a variety of outsourcing models, including the traditional full-service model in which we provide all or substantially all of these services to our customers by trial or asset. We also offer our services through a FSP model in which we provide specific services by function ranging from staff augmentation to functional services across trials, globally or by region. We are able to provide custom-built offerings with tailored services that are flexible and innovative to meet the specific needs of our customers.

In addition to managing trials for biopharmaceutical and biotechnology customers, we also provide clinical trial services to the U.S. government, including the National Institute of Allergy and Infectious Diseases (“NIAID”) under the National Institute of Health. We provide support to the NIAID Division of AIDS, including monitoring services at domestic and international sites, laboratory audits, Good Laboratory Practice (“GLP”) training and quality management, biostatistics and data management. We also support other U.S. government research priorities, such as developing a vaccine for the Zika virus, through subcontracts with other U.S. government contractors.

We have extensive expertise and experience in numerous therapeutic areas, including oncology/hematology, metabolic/endocrine, neuroscience, pediatric, cardiovascular, analgesia, gastroenterology, rare diseases, chronic diseases, urology and vaccines.

Accelerated Enrollment Solutions. We believe our AES delivery model provides the largest global dedicated site network, extending across five continents, 17 countries and over 180 research sites combined with the industry’s largest aggregation of fully identified and consented data on individuals interested or having participated in clinical trials. Through AES, we offer services to replace or complement the traditional site selection model, focusing on maximizing patient delivery through efficient and predictive centralized recruitment, having the ability to provide patient enrollment at significantly higher rates than the independent site model. Our SynexusPlus offering is an adaptable solution that allows us to meet customers’ needs, including more patients per site, faster startup and reduction in the number of sites or enrollment completion within a specific timeframe, all under a results-based single-price-per-patient model. SynexusPlus may be combined with our core global clinical trial management services to create PatientAdvantage, a fully outsourced trial solution that is designed to offer patient enrollment and budget certainty, as well as speed and cost savings, through streamlined contracting terms, capitated budget constructs, fewer sites and reduced recruiting time.

14

Peri- and post-approval services. We are a leading provider of real-world research and evidence-based solutions to demonstrate the real-world effectiveness, safety and value of biopharmaceutical and biotechnology products with capabilities in 35 countries and, since 2015, have invested over $200 million to enhance our peri- and post-approval services. Through this offering, we provide our customers with critical scientific expertise and global operational capabilities to help generate the evidence needed to optimize the market access and commercial potential of their products. As of December 31, 2019, we had over 450 scientists and consultants conducting real-world, patient-centered, health economics, epidemiological and market access research. We provide our customers with critical scientific expertise and insight across the development continuum of a product, from early development through loss of exclusivity, with a primary focus on demonstrating the real-world effectiveness, safety and value of treatments. We specialize in engaging with key market constituents early in the development process to create an evidence strategy that will meet the needs of all relevant stakeholders. We develop evidence to demonstrate the safety, effectiveness and value of over 150 drug therapies per year across more than 20 countries. We have also contributed to a number of payer submissions, including the reversal of multiple decisions by the U.K.’s National Institute for Health and Care Excellence.

Medical communications. We provide industry inbound and outbound peri- and post-approval contact center solutions focused on medical and clinical support to the biopharmaceutical industry. Our multidisciplinary team, consisting of over 800 highly trained health care professionals, including physicians, pharmacists, nurses and life science graduates, provides medical and technical information to our customers’ patients with a focus on compliance, quality and delivery of what we believe to be best-in-class customer experiences. We support full portfolios of marketed products, providing local language expertise as well as a global reach. Live customer question and answering services are provided in multiple languages covering the major markets in which our customers sell their pharmaceutical products from 11 locations in North America, Latin America, Europe and Asia-Pacific. Using dedicated teams, our programs are customized and flexible to meet each customer’s evolving needs.

Laboratory Services

We own and operate an integrated and scaled suite of laboratory services. We offer a range of high value, advanced testing services, including bioanalytical, biomarker, vaccines, GMP and central laboratory infrastructure to support R&D. Throughout the drug development cycle, our customers benefit from global, comprehensive laboratory services spanning bioanalytical, biomarker, vaccines, GMP and central laboratory. Our laboratory services accelerate drug development for small molecules, biologics and cell and gene therapies which we believe allows customers to make faster decisions about their products. We believe we are one of the leading providers in each of the GMP, bioanalytical and central laboratory services sectors, as well as in the growing vaccines market. In 2019, for the second time in three years, we were named Best CRO Provider at the World ADC Awards, a recognition of our efforts to help customers advance their ADC research to develop new anticancer therapies.

Bioanalytical laboratory services. We provide bioanalytical services through our highly automated locations in Richmond, Virginia and Middleton, Wisconsin that are designed to be compliant with GLPs. Our bioanalytical laboratories analyze drug and metabolite concentrations from biological fluid and tissue samples within preclinical and human clinical studies. Our bioanalytical methods include: liquid chromatography combined with mass spectrometry (“LC-MS”) and high-resolution mass spectrometry, high performance liquid chromatography, ligand-binding, enzyme-linked immunosorbent assay, radioimmunoassay, flow cytometry and cell-based assay support. Our bioanalytical laboratories support the complete service necessary for biologic, small molecule, oligonucleotide and cell and gene therapy development. This includes pharmacokinetic evaluation of the therapeutic agent, immunogenicity testing to determine the presence of antibodies, and cell-based assays to determine the neutralizing antibody effect of the antibodies. We have the proven ability to handle an increasingly diverse range of large molecules, which include therapeutic peptides, monoclonal antibodies and ADC’s, as well as new areas such as glycans and biotransformation.

Biomarker laboratory services. Our biomarker laboratory core facility is located in Richmond, Virginia. The laboratory is closely aligned with both the central laboratories and bioanalytical laboratories to provide customized solutions for biomarker projects. The capabilities include LC-MS, ligand binding, flow cytometry and molecular genomics. Our technologies and applications enable the biomarker laboratory to develop or transfer methods and either perform sample analysis within the biomarker laboratory or transfer validated methods to the central laboratory or Phase I clinic as needed.

Vaccine science services. We perform testing for vaccines in our dedicated facility located in Richmond, Virginia. Our scientists perform immunogenicity testing to evaluate the efficacy of vaccines in inducing cellular and humoral immune responses and employ molecular detection methods, such as polymerase chain reaction testing to detect the absence of pathogens or to characterize attenuated vaccine strains following administration of a vaccine. Our service offering also includes providing dedicated laboratory space to conduct complex proprietary assays in support of multiple vaccine programs.

15

GMP laboratory services. We provide early preclinical development through post-approval testing services and product analysis laboratory services through our locations in Middleton, Wisconsin and Athlone, Ireland that are designed to be compliant with GMPs. Our product analysis services include analytical method development and validation, stability and quality control testing of product and pharmaceutical ingredients and impurities characterization for small molecules and biologics for all dosage forms, as well as analytical testing of biopharmaceuticals, inhalation devices and cell and gene therapies. Our Athlone laboratory offers the advantage of proximity to our growing number of European customers and allows us to conduct release testing of products to be marketed in Europe for our global customers.

Central laboratory services. With facilities in Highland Heights, Kentucky, Brussels, Belgium, Singapore and Shanghai, China, our central laboratories provide highly standardized safety and biomarker testing services with customized results databases for our customers. We focus on providing long-term, large-scale studies where laboratory measurement of clinically relevant endpoints is critical. Our central laboratories utilize the same standard operating procedures and maintain identical instruments in every facility. All of our facilities are College of American Pathologists (“CAP”) accredited, and National Glycohemoglobin Standardization Program (“NGSP”) and Centers of Disease Control and Prevention (“CDC”) lipid standardization survey (“LSP”) certified. All our facilities run the same CAP proficiency tests on a quarterly basis. In addition to these industry quality standards, we run our own unique global laboratory assay standardization survey program monthly on our most common analyses, ensuring continuity and consistency of data at all stages of a clinical project. We also standardize data collection and reporting on a global basis utilizing the same software platform, our Preclarus central laboratory database. This platform provides real-time data and eliminates the need to merge data sets from different regions. Our laboratories provide on-site biorepository services that enable storage and archiving of samples for future testing, including specialized biomarker testing of specific patient populations to speed drug discovery and development efforts. In 2018, we formed a global strategic alliance for pathology and molecular testing solutions with NeoGenomics to provide a fully integrated global pathology and molecular testing solution to our customers, further expanding our central laboratory services related to oncology clinical trial activities.

Customers

Our customers consist predominantly of large biopharmaceutical companies and small to mid-size biotechnology and pharmaceutical companies. We also serve governmental organizations, medical device companies and other industry participants. We participated in the development of all of 2018’s top ten selling drugs, as ranked by 2018 revenue, and, in 2019, we served all of the top 50 biopharmaceutical companies in the world, as ranked by 2018 R&D spending. Since 2014, we have also worked with over 300 companies in the growing biotechnology sector, with no one customer accounting for more than 10% of our revenue in 2019. We seek to meet the individual needs of each of our customers by tailoring our services to address their specific objectives and offering a competitive commercial structure. We customize our offerings based on numerous factors, including the particular therapeutic area, trial type, trial size, study complexity, competitive landscape and unique customer needs. We believe that we are recognized among our customers as a leading provider of drug development services to the biopharmaceutical industry, differentiated on the basis of our expertise, global scale, track record, differentiated service offerings, comprehensive laboratory services and dedicated workforce.

Sales and Marketing

Our approach to sales and marketing to both biopharmaceutical and biotechnology companies involves the coordinated approach of a team of internal scientific, operational and other technical experts as well as our business development team members, building multi-faceted relationships and designing solutions tailored to the specific customer’s pipeline and other particular needs, and often includes members of our senior leadership team. For those large biopharmaceutical customers with which we have, or seek to have, a strategic partnership arrangement, a dedicated strategic account management team supports all aspects of the relationship. For small and mid-size biotechnology and pharmaceutical companies, we developed our PPD Biotech business model which is built specifically to serve the unique needs of this customer segment and is comprised of business development personnel and leaders from our commercial operational, medical and functional groups dedicated to working with customers in this customer segment.

Our Laboratory Services segment has a dedicated business development group that is organized into three separate teams focused on (i) central laboratory services, (ii) bioanalytical, biomarker and vaccines testing and (iii) GMP testing. The group has representatives in North America, Europe and Asia and is further supplemented by a laboratory partnerships group that ensures operational delivery. In addition to calling on biopharmaceutical and biotechnology companies directly, the Laboratory Services segment business development teams coordinate efforts with our other business development teams for customers that are interested in buying services across our segments.

16

Our corporate marketing team supports the activities of our business development staff. Our global marketing initiatives include integrated, multi-channel campaigns designed to help differentiate and promote our expertise and services and strengthen our corporate brand. We provide our perspective on current industry challenges and developments to create an ongoing dialogue with our customers and prospective customers and to promote our scientific expertise, differentiated service offerings, quality, technology and innovation. In support of these efforts, we exhibit, provide speakers, present papers and host customer meetings at key industry events, and publish scientific articles in industry, trade, medical and pharmaceutical journals.

Backlog and Authorizations

Our backlog represents anticipated direct revenue for work not yet completed or performed (i) under signed contracts, letters of intent and, in some cases, awards that are supported by other forms of written communication and (ii) where there is sufficient or reasonable certainty about the customer’s ability and intent to fund and commence the services within six months. Our backlog excludes anticipated third-party pass-through and out-of-pocket revenue.

Backlog and backlog conversion to direct revenue vary from period to period depending upon new authorizations, contract modifications, cancellations and the amount of direct revenue recognized under existing contracts. The weighted-average duration of contracts in our backlog fluctuates from period to period based on the contracts constituting our backlog at any given time. We adjust backlog for foreign currency fluctuations and exclude direct revenue that has been recognized as revenue in our statements of operations.

Although an increase in backlog will generally result in an increase in future direct revenue to be recognized over time (depending on future contract modifications, contract cancellations and other adjustments), an increase in backlog at a particular point in time does not necessarily correspond to an increase in direct revenue during a particular period. The timing and extent to which backlog will result in direct revenue depends on many factors, including the timing of commencement of work, the rate at which we perform services, scope changes, cancellations, delays, receipt of regulatory approvals and the nature, duration, size, complexity and phase of the studies. Our contracts generally have terms ranging from several months to several years. In addition, delayed projects remain in backlog until they are canceled. As a result of these factors, our backlog might not be a reliable indicator of future direct revenue and we might not realize all or any part of the direct revenue from the authorizations in backlog as of any point in time. Our backlog was $7,066.3 million at December 31, 2019 and $6,313.7 million at December 31, 2018.

We add new authorizations to backlog based on the aforementioned criteria for backlog. New authorizations vary from period to period depending on numerous factors, including customer authorization volume, sales performance and overall health of the biopharmaceutical industry, among others. New authorizations have and will continue to vary significantly from quarter to quarter and from year to year. Once work begins, we recognize direct revenue over the life of the contract based on our performance of services under the contract. Our net authorizations were $3,827.3 million, $3,421.0 million, and $2,485.4 million, respectively, for the years ended December 31, 2019, 2018 and 2017.

Competition

The drug development services industry is highly competitive, consisting of hundreds of small, limited-scope service providers and a limited number of large full-service global development companies. While the industry has seen an increasing level of consolidation over the past several years, largely driven by the larger full-service providers, it remains highly fragmented.

Our Clinical Development Services segment competes primarily with a small number of other global, full-service CROs, although we also compete against small and medium-sized niche CROs, in-house R&D departments of biopharmaceutical companies, universities and teaching hospitals. We generally compete on the basis of scientific and therapeutic experience, project team expertise, qualifications and experience, ability to recruit patients, price, quality and the ability to innovate to achieve time and cost savings for our customers, amongst other factors. Our major competitors include IQVIA Holdings, Inc. (“IQVIA”), ICON plc (“ICON”), PAREXEL International Corporation, PRA Health Sciences, Inc. (“PRA Health Sciences”), the Covance Drug Development business of Laboratory Corporation of America Holdings (“Covance”), Syneos Health, Inc. (“Syneos Health”) and Medpace Holdings, Inc.

Our Laboratory Services segment competes primarily with the laboratory businesses of other large CROs, large global laboratory organizations, specialty laboratories and in-house laboratories of biopharmaceutical companies. We generally compete on the basis of testing capability, scientific and therapeutic experience, global footprint, price, quality and speed. Our major competitors include the advanced and central laboratory segments of Laboratory Corporation of America Holdings and Syneos Health, Q2 Solutions, ICON, Eurofins Scientific, WuXi AppTec, BioAgilytix and SGS.

We believe that our competitive position is generally strong and that we are able to effectively compete in both the clinical development and laboratory services markets.

17

Intellectual Property

In the course of conducting our business, we have developed, and continue to develop and use proprietary software, systems, processes, databases and other intellectual property. We seek to protect our proprietary and confidential information and trade secrets through confidentiality agreements with employees, customers and other third parties, as well as administrative and technical safeguards. We rely on patent, copyright and trademark laws, as may be appropriate and applicable, to protect our other intellectual property rights. For example, we have applied for and/or obtained and maintain registration in the United States and other countries for numerous trademarks, including PPD®, PPD® Biotech, PPD® Laboratories and Preclarus®. We also enter into agreements with third-parties for the license and use of their intellectual property, although no one such license is considered to be material to the business as a whole. We do not have any material patents.

Government Regulation

Regulation of Drugs and Biologics

The development, testing, manufacturing, labeling, storage, approval, promotion, marketing, distribution and post-approval monitoring and reporting of pharmaceutical, biological and medical device products are subject to rigorous regulation by numerous governmental authorities in the United States at the federal, state and local level, including the FDA, as well as those of other countries, such as the European Medicines Agency (the “EMA”) in the European Union and the Medicines and Healthcare products Regulatory Agency (the “MHRA”) in the United Kingdom. These regulations apply to our customers and are generally applicable to us when we are providing services to our customers, either as a result of their direct applicability, through a transfer of regulatory obligations from our customers, or as a consequence of acting as local legal representative on behalf of our customers in a particular country or countries. Consequently, we must comply with all relevant laws and regulations in the conduct of our Clinical Development Services and Laboratory Services segments. The following discussion describes the role of the FDA in the clinical drug development process in the United States. Clinical trials conducted outside the United States are subject to the laws and regulations of the country where the trials are conducted. These laws and regulations might not be similar to the laws and regulations administered by the FDA and other laws and regulations regarding the protections of patient safety and privacy and the control of study pharmaceuticals, medical devices or other materials. FDA laws and regulations may apply to clinical studies conducted outside the United States if, for example, such studies are conducted under an IND or offered as support for an IND.

Prior to commencing human clinical trials, a company developing a new drug must file an IND with the FDA. The IND must include information about pre-clinical tests, manufacturing and control data, and a study protocol for the proposed clinical trial of the drug in humans. If the FDA does not object in writing within 30 days after filing the IND becomes effective and the clinical trial may begin. A separate submission to an existing IND must also be made for each successive clinical trial conducted during product development. Each clinical trial must be conducted in accordance with an effective IND.

The study protocol must also be reviewed and approved by an institutional review board/independent ethics committee (“IRB/IEC”) for each institution in which a study is proposed to be conducted and each IRB/IEC may impose additional requirements on the conduct of the study in its institution. IRB/IECs have the authority to review, approve and monitor clinical trials, and clinical trials are subject to oversight by IRB/IECs. The industry standard for the conduct of clinical trials is embodied in the FDA’s regulations for IRB/IECs, investigators and sponsor/monitors, which regulations collectively are termed Good Clinical Practices (“GCP”) by industry, and the GCP guidelines issued by the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (“ICH”), which have been agreed upon by industry and regulatory representatives from the United States, the European Union and Japan. GCP requirements address, among other things, IRBs, qualified investigators, informed consent, recordkeeping and reporting. Regulatory authorities enforce GCP requirements through periodic inspections, and violations of GCP requirements could result in enforcement actions including the issuance of warning letters, civil penalties, product recalls, criminal prosecutions or debarment from involvement in the submission of NDAs. Our global standard operating procedures are written in accordance with all applicable FDA, EMA, MHRA, ICH and GCP requirements. This enables our work to be conducted locally, regionally and globally to standards that meet all currently applicable regulatory requirements. We must also maintain reports in compliance with applicable regulatory requirements for each study for auditing by the customer and regulatory authorities.

In order to comply with GCP and other regulations, sponsors of clinical trials must, among other things:

• | comply with specific requirements governing the selection of qualified investigators; |

• | obtain specific written commitments from the investigators; |

• | obtain IRB review and approval of the clinical trial; |

• | verify that appropriate patient informed consent is obtained before the patient participates in a clinical trial; |

• | ensure adverse drug reactions resulting from the administration of a drug or biologic during a clinical trial are medically evaluated and reported in a timely manner; |

18