Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Livent Corp. | liventex322123119.htm |

| EX-32.1 - EXHIBIT 32.1 - Livent Corp. | liventex321123119.htm |

| EX-31.2 - EXHIBIT 31.2 - Livent Corp. | liventex312123119.htm |

| EX-31.1 - EXHIBIT 31.1 - Livent Corp. | liventex311123119.htm |

| EX-23.3 - EXHIBIT 23.3 - Livent Corp. | ex233roskillconsentlette.htm |

| EX-23.2 - EXHIBIT 23.2 - Livent Corp. | ex232bloombergconsenlett.htm |

| EX-23.1 - EXHIBIT 23.1 - Livent Corp. | ex231kpmgconsentletter1.htm |

| EX-21.1 - EXHIBIT 21.1 - Livent Corp. | liventex21123119.htm |

| EX-18.1 - EXHIBIT 18.1 - Livent Corp. | ex181preferabilityletter.htm |

| EX-10.24 - EXHIBIT 10.24 - Livent Corp. | sponessaformofexecsevagr.htm |

| EX-10.20 - EXHIBIT 10.20 - Livent Corp. | pgravesformofexecutivese.htm |

| EX-4.2 - EXHIBIT 4.2 - Livent Corp. | ex42descriptionofsecurities.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________________________________________

FORM 10-K

_______________________________________________________________________

x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2019

or

¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from _______ to _______

Commission File Number 001-38694

__________________________________________________________________________

LIVENT CORPORATION

(Exact name of registrant as specified in its charter)

__________________________________________________________________________

Delaware | 82-4699376 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

2929 Walnut Street Philadelphia, Pennsylvania | 19104 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: 215-299-6000

__________________________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol (s) | Name of each exchange on which registered |

Common Stock, $0.001 par value per share | LTHM | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Emerging growth company | ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ¨ | |||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ¨ No x

The aggregate market value of voting stock held by non-affiliates of the registrant as of June 30, 2019, the last day of the registrant’s second fiscal quarter was $1,002,722,733. The market value of voting stock held by non-affiliates excludes the value of those shares held by executive officers and directors of the registrant.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date

Class | December 31, 2019 | |

Common Stock, par value $0.001 per share | 145,981,684 | |

DOCUMENTS INCORPORATED BY REFERENCE

DOCUMENT | FORM 10-K REFERENCE | |

Portions of Proxy Statement for 2020 Annual Meeting of Stockholders | Part III | |

Livent Corporation

2019 Form 10-K

Table of Contents

Page | |

3

Glossary of Terms

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

AOCI | Accumulated other comprehensive income |

ARO | Asset retirement obligation |

ASC | Accounting Standards Codification, under U.S. GAAP |

ASU | Accounting Standards Update, under U.S. GAAP |

BEAT | Base erosion and anti-abuse tax |

Brexit | The withdrawal of the United Kingdom from the European Union |

CERCLA | Comprehensive Environmental Response, Compensation and Liability Act |

Distribution | On March 1, 2019, FMC made a tax-free distribution to its stockholders of all its remaining interest in Livent Corporation |

Exchange Act | Securities and Exchange Act of 1934 |

EV | Electric vehicle |

FASB | Financial Accounting Standards Board |

FDII | Foreign-derived intangible income |

FMC | FMC Corporation |

FMC Plan | FMC Corporation Incentive Compensation and Stock Plan |

GDP | Gross domestic product |

GILTI | Global intangible low-taxed income |

IPO | Initial public offering |

kMT | Thousand metric tons |

LCE | Lithium carbonate equivalent |

Livent NQSP | Livent Nonqualified Savings Plan |

Livent Plan | Livent Corporation Incentive Compensation and Stock Plan |

MdA | Minera del Altiplano SA, our local operating subsidiary in Argentina |

MT | Metric ton |

NPI | Net parent investment |

NYSE | New York Stock Exchange |

OCI | Other comprehensive income |

OM&M | Operation, maintenance and monitoring of site environmental remediation |

Prospectus | The final Prospectus included in our Registration on Form S-1 originally filed with the SEC on October 12, 2018 |

RCRA | Resource Conservation and Recovery Act |

REACH | Registration, Evaluation, Authorization and Restriction of Chemicals |

REMSA | Recursos Energeticos y Mineros Salta, S.A., local natural-gas sub-distributor in Argentina |

Revolving Credit Facility | Livent's $400 million senior secured revolving credit facility |

ROU Asset | Right-of-use asset |

RSU | Restricted stock unit |

SEC | Securities and Exchange Commission |

Securities Act | Securities Act of 1933 |

Separation Date | On October 15, 2019, Livent Corporation completed the IPO and sold 20 million shares of Livent common stock to the public at a price of $17.00 per share |

Tax Act | Tax Cuts and Jobs Act |

TMA | Tax Matters Agreement |

TSA | Transaction Services Agreement |

U.S. GAAP | United States Generally Accepted Accounting Principles |

VAT | Value-added tax |

4

PART I

ITEM 1. | BUSINESS |

Livent Corporation was formed and incorporated by FMC Corporation as FMC Lithium USA Holding Corp. in the State of Delaware on February 27, 2018, and was subsequently renamed Livent Corporation ("Livent"). Livent's principal executive offices are located at 2929 Walnut Street, Philadelphia, Pennsylvania, 19104. Throughout this Annual Report on Form 10-K, except where otherwise stated or indicated by the context, “Livent”, the "Company", “we,” “us,” or “our” means Livent Corporation and its consolidated subsidiaries and their predecessors after giving effect to the transactions described under “The Separation" and "The Distribution" below, and references to “FMC” refer to FMC Corporation and its consolidated subsidiaries. Unless the context requires otherwise, statements relating to our history throughout this Annual Report on Form 10-K describe the history of FMC’s lithium segment. Copies of the annual, quarterly and current reports we file with the Securities and Exchange Commission (“SEC”), and any amendments to those reports, are available on our website at www.livent.com as soon as practicable after we furnish such materials to the SEC.

The Separation and Distribution

On March 31, 2017, FMC publicly announced a plan to separate Livent into a publicly traded company (the “Separation”). Prior to the completion of the initial public offering ("IPO") on October 15, 2018 (the "Separation Date"), we were a wholly owned subsidiary of FMC, and all of our outstanding shares of common stock were owned by FMC. Following a series of restructuring steps, on October 1, 2018, prior to the IPO of Livent common stock, FMC transferred to us substantially all of the assets and liabilities of its lithium business (the “Lithium Business”). In exchange, we issued to FMC 123 million shares of our common stock.

In connection with the Separation and completion of the IPO, we entered into certain agreements with FMC that govern various relationships between the parties. These agreements include a separation and distribution agreement, a transition services agreement, a shareholders’ agreement, a tax matters agreement, a registration rights agreement, an employee matters agreement and a trademark license agreement.

On March 1, 2019, FMC completed the spin-off distribution of 123 million shares of common stock of Livent as a pro rata dividend on shares of FMC common stock outstanding at the close of business on the record date of February 25, 2019 (the “Distribution”). Effective upon completion of the Distribution, we became an independent company and FMC no longer owns any shares of Livent common stock.

General

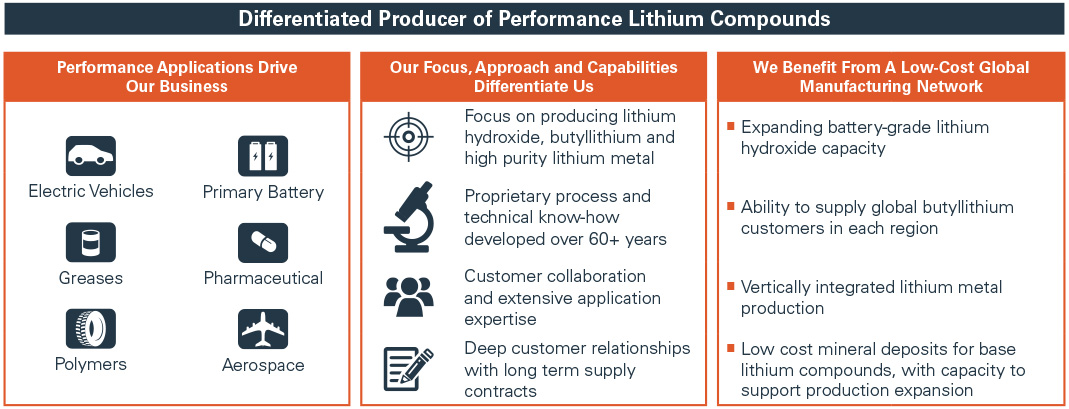

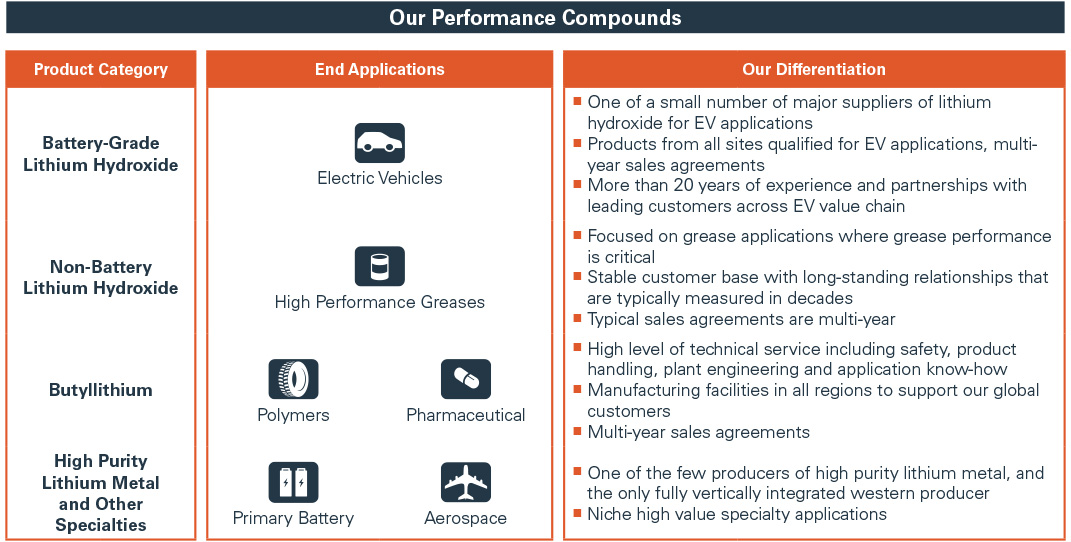

We are a pure-play, fully integrated lithium company, with a long, proven history of producing performance lithium compounds. Our primary products, namely battery-grade lithium hydroxide, lithium carbonate, butyllithium and high purity lithium metal are critical inputs used in various performance applications. Our strategy is to focus on supplying high performance lithium compounds to the fast- growing electric vehicle ("EV") battery market, while continuing to maintain our position as a leading global producer of butyllithium and high purity lithium metal. With extensive global capabilities, over 60 years of continuous production experience, applications and technical expertise and deep customer relationships, we believe we are well positioned to capitalize on the accelerating trend of vehicle electrification.

5

We produce lithium compounds for use in applications that have specific performance requirements, including battery-grade lithium hydroxide for use in high performance lithium-ion batteries. We believe the demand for our compounds will continue to grow as the electrification of transportation accelerates, and as the use of high nickel content cathode materials increases in the next generation of battery technology products. We also supply butyllithium, which is used in the production of polymers and pharmaceutical products, as well as a range of specialty lithium compounds including high purity lithium metal, which is used in the production of lightweight materials for aerospace applications and non-rechargeable batteries. It is in these applications that we have established a differentiated position in the market through our ability to consistently produce and deliver performance lithium compounds.

Livent Strategy

We believe that growth in EV sales will drive significant growth in demand for performance lithium compounds. We believe that we are well positioned to benefit from this trend thanks to our leading position and long-standing customer relationships. To fully capitalize on this opportunity, our strategy will involve investing in our assets, our technology capabilities and our people to ensure we can continue to meet our customers’ demands.

Expand our Production Capacities

We intend to expand our lithium hydroxide capacity at multiple locations in order to meet customer demands globally, as our customers expand their own production networks around the globe. To support our lithium hydroxide expansion and reduce our need to procure lithium carbonate from third party suppliers, we started a project to expand annual lithium carbonate production at our existing operations in Argentina in addition to seeking alternative lithium resources.

We will continue to evaluate our butyllithium capacity regionally and add capacity as our demand continues to increase. For high purity lithium metal, we are evaluating expansion opportunities to align with the potential increase in demand for lithium metal as our customers develop next generation battery technologies.

The timing and scope of our capacity expansion plans will be determined by market conditions, capital considerations, and anticipated customer commitments, among other factors. Based on current lithium market trends, we have slowed the pace of our carbonate expansion in Argentina resulting in the delay of phase 1 completion to the middle of 2021 and will be pausing our current lithium hydroxide expansion project to align its completion with that of phase 1 in Argentina.

Diversify our Sources of Supply

We continue to pursue additional sources of lithium products, which may include further expansion in Argentina, acquisition and development of new resources, entering into long-term supply agreements with other producers or some combination thereof. We will continually assess new resources that offer the potential to provide alternative sources of lithium products and will look to invest in developing such resources where it makes sense to do so.

Expand our Application and Process Technology Capabilities

Our market position today is built upon our ability to consistently provide our customers with the products they need. To maintain this position, we are continuously investing in our application and process technologies. As we work with our customers to understand their evolving lithium needs, we will focus on improving our own abilities to adapt the properties of our products, whether physical or chemical, to meet those needs. This may require us to invest in and potentially acquire new capabilities, hire people or acquire new technical resources.

Develop Next Generation Lithium Compounds

We believe that the evolution of battery technologies will lead to the adoption of lithium-based applications in the anode and electrolyte within the battery. This evolution will require new forms of lithium to be produced, such as new lithium metal powders or printable lithium products. We will continue to invest in our research and development efforts to help us create new products, and will also invest with and partner alongside our customers to further their own research and development efforts.

Invest in Our People

Our business requires that we hire and retain the best research scientists, engineers and technical salesforce in our industry. We will continue to invest in our people through training and developing our employees to ensure we retain the best talent in the industry.

Financial Information About Our Business

We operate as one reportable segment based on the commonalities among our products and services, the types of customers we serve and the manner in which we review and evaluate operating performance. As we earn substantially all of our revenues through the sale of lithium products, we have concluded that we have one operating segment for reporting purposes.

6

Business Overview

As a result of our focus on supplying performance lithium compounds for use in the rapidly growing EV market, we expect the shares of lithium hydroxide, lithium-based batteries and Asia as percentages of our total revenue by product, application and geography, respectively, to increase. We intend to maintain our leadership positions in other high performance markets such as greases and polymers.

We believe that we have earned a reputation as a leading supplier in the markets we serve, based on the performance of our products in our customers’ production processes and our ability to provide application know-how and technical support. In the EV market, we are one of a small number of lithium suppliers whose battery-grade lithium hydroxide has been qualified by customers for use in their cathode material production processes. Throughout our history, as end market application technologies have evolved, we have worked closely with our customers to understand their changing performance requirements and have developed products to address their needs.

As a vertically integrated producer, we benefit from operating one of the lowest cost lithium mineral deposits in the world. We have been extracting lithium brine at our operations at the Salar del Hombre Muerto in Argentina for more than 20 years, and have been producing lithium compounds for over 60 years. Our operational history provides us with a deep understanding of the process to extract lithium compounds from brine safely and sustainably. We have developed proprietary process knowledge that enables us to produce high quality, low impurity lithium carbonate and lithium chloride. We source the majority of our base lithium compounds for use in the production of performance lithium compounds from these low cost operations in Argentina. Our operations in Argentina are expandable, giving us the ability to increase our lithium carbonate and lithium chloride production to meet increasing demand. We also have the operational flexibility to procure lithium carbonate from third party suppliers, which we do from time to time and expect to do in 2020. This strategy allows us to manage our production requirements as well as to produce more end products for customers than we would have the ability to do with lithium carbonate derived solely from our internal sources of supply.

We are one of a few lithium compound producers with global manufacturing capabilities. We use the majority of the lithium carbonate we produce in the production of battery-grade lithium hydroxide in the United States and China. We use the lithium chloride we produce in the production of butyllithium products in the United States, the United Kingdom, China and India, as well as in the production of high purity lithium metal in the United States. We have significant know-how and experience in the lithium hydroxide, butyllithium and high purity lithium metal production processes and product applications, which we believe provides us with a competitive advantage in these markets.

Capacity and Production

The chart below presents a breakdown of our capacity and production by product type and category presented in product basis metric tons ("MT") for the years ended December 31, 2019, 2018 and 2017:

Product Category | Product | 2019 | 2018 | 2017 | ||||||||||||||||

Capacity | Production | Capacity | Production | Capacity | Production | |||||||||||||||

Performance Lithium | Lithium Hydroxide | 25,000 | 21,348 | 18,500 | 15,936 | 18,500 | 13,057 | |||||||||||||

Butyllithium | 3,265 | 2,437 | 3,265 | 2,389 | 3,265 | 2,218 | ||||||||||||||

High Purity Lithium Metal (1) | 250 | 167 | 250 | 140 | 250 | 101 | ||||||||||||||

Base Lithium | Lithium Carbonate (2) | 18,000 | 16,785 | 18,000 | 17,238 | 16,000 | 15,153 | |||||||||||||

Lithium Chloride (2) | 9,000 | 4,284 | 9,000 | 5,005 | 9,000 | 4,501 | ||||||||||||||

____________________

(1) | Excludes other specialty product capacities and production. |

(2) | Represents theoretical capacity for lithium carbonate and lithium chloride. Actual combined production of both products is lower and limited by the total capacity of lithium brine production. Lithium brine production was approximately 20,000 MT on a lithium carbonate equivalent ("LCE") basis for 2019, approximately 21,000 MT for 2018 and approximately 18,000 MT for 2017, resulting in the total production shown in the chart. |

7

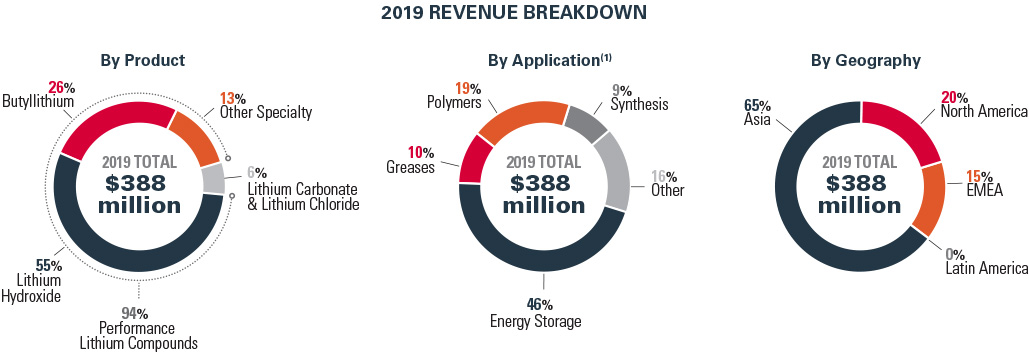

The charts below detail our 2019 revenues by product, application and geography.

____________________

(1) | Company internal estimates |

8

Products and Markets

Our performance lithium compounds are frequently produced to meet specific customer application and performance requirements. We have developed our capabilities in producing performance lithium compounds through decades of interaction with our customers, and our products are key inputs into their production processes. Our customer relationships provide us with first-hand insight into our customers’ production objectives and future needs in terms of products and specifications, which we in turn use to further develop our products.

Other specialties include lithium phosphate, pharmaceutical-grade lithium carbonate, high purity lithium chloride and specialty organics. In addition to performance lithium compounds, we also produce lithium carbonate and lithium chloride, both of which we largely consume as feedstock in the process of producing our performance lithium compounds.

Competition and Industry Overview

We sell our performance lithium compounds worldwide. Most markets for lithium compounds are global, with significant growth occurring in Asia, driven primarily by the development and manufacture of lithium-ion batteries. The market for lithium compounds also faces some barriers to entry, including access to an adequate and stable supply of lithium, technical expertise and development lead time. According to Roskill's 2018 estimates, we are one of the five largest producers, including SQM, Albemarle, Sichuan Tianqi and Jiangxi Ganfeng Lithium, that accounted for approximately 69% of the global refined lithium production as measured by lithium carbonate equivalent ("LCE"). We expect capacity to be added by new and existing producers over time. We believe our lithium brines in Salar del Hombre Muerto, Argentina, considered by the industry to be one of the lowest cost sources of lithium, provide us with a distinct competitive advantage against these current or future entrants.

We compete by providing advanced technology, high product quality, reliability, quality customer and technical service, and by operating in a cost-efficient manner and prioritizing safety and sustainability. We believe we are a leading provider of battery-grade lithium hydroxide in EV battery applications and in performance grease applications and benefit from low production costs and a history of efficient capital deployment. We also believe we are one of only two global suppliers of butyllithium. According to Roskill, we are one of the two largest producers of downstream lithium chemicals outside of China. Our primary competitor for performance lithium compounds is Albemarle Corporation. We are the only fully integrated producer of high purity lithium metal in the Western Hemisphere and enjoy competitive advantages from our vertically integrated manufacturing approach and low production costs. Our primary competitors within the lithium metal product category include Jiangxi Ganfeng Lithium and other Chinese producers.

Growth

According to Bloomberg New Energy Finance's May 2019 EV Outlook, EV (battery electric and plug-in hybrid) sales are expected to exceed 56.2 million units in 2040, representing a penetration rate of 57% of all vehicles sold. Automotive OEMs have announced plans to introduce longer-range EV models using higher energy density batteries and are increasingly doing so by moving to high nickel content cathode materials. According to Bloomberg New Energy Finance’s January 2020 report, the average range for

9

battery electric vehicles rose from 112km (~70 miles) for models launched in 2011 to 294km (~183 miles) for models launched in 2019. The average range for upcoming battery electric vehicle models launching in 2020 is even higher at 379km (~235 miles). The increasing range of EVs has generally been due to the use of larger battery packs, which require more lithium content. Bloomberg also estimates over 95% of all passenger EVs in 2025 to have high (>60%) nickel content cathodes compared to 46% of all passenger EVs in 2018. This shift will increasingly require battery-grade lithium hydroxide in the production of cathode materials.

As an existing, proven global producer of battery-grade lithium hydroxide, we are well positioned to benefit from this expected increase in lithium demand from EV growth. As one of the pioneers in the lithium industry, we have relationships throughout the lithium-ion battery value chain. Across the battery value chain, product performance requirements have continued to evolve since the first lithium-ion batteries were introduced in the early 1990s. We have developed our application and materials knowledge by working with our customers over time to produce performance lithium compounds which meet evolving customer needs.

Our growth efforts focus on developing environmentally compatible and sustainable lithium products. We are committed to providing unique, differentiated products to our customers by acquiring and further developing technologies as well as investing in innovation to extend product life cycles.

__________________________

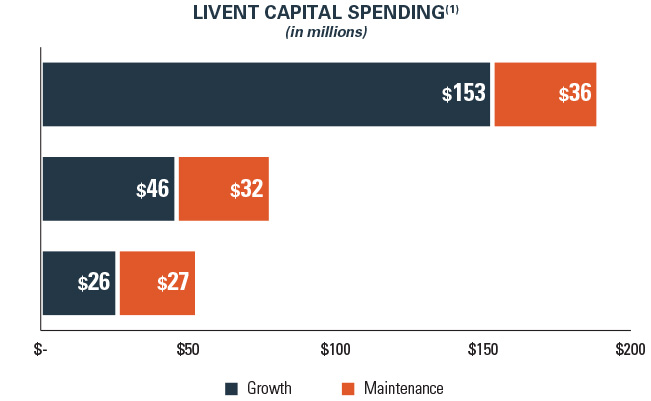

(1) | Includes capital expenditures and other investing activities. See our consolidated and combined statements of cash flows in Part II, Item 8 of this Form 10-K for further details. |

Raw Materials

Lithium

Our primary raw material is lithium, and we obtain the substantial majority of our lithium from our operations in Argentina. We extract lithium from naturally occurring lithium-rich brines located in the Andes Mountains of Argentina, which are believed to be one of the world’s most significant and lowest cost sources of lithium, through a proprietary selective adsorption and solar evaporation process. We process the brine into lithium carbonate at our co-located manufacturing facility in Fénix, Argentina and into lithium chloride at our nearby manufacturing facility in Güemes, Argentina. In 2019, 2018 and 2017, we expanded capacity of lithium carbonate at these facilities through debottlenecking projects.

For the years ended December 31, 2019, 2018 and 2017, our Argentine operations extracted and processed approximately 17 kMT, 17 kMT and 15 kMT of lithium carbonate, respectively, and approximately 4 kMT, 5 kMT and 5 kMT of lithium chloride, respectively. For the years ended December 31, 2019, 2018 and 2017, lithium brine production from both lithium carbonate and lithium chloride, on a lithium carbonate equivalent ("LCE") basis, was approximately 20 kMT, 21 kMT and 18 kMT, respectively.

We also purchase a portion of our lithium carbonate raw materials from other suppliers.

10

Salar del Hombre Muerto

We conduct our Argentine operations through Minera del Altiplano SA ("MdA"), our local operating subsidiary. We extract lithium from naturally occurring lithium-rich brines in Salar del Hombre Muerto, an area covering approximately 600 square kilometers in a region of the Andes Mountains of northwest Argentina known as the “lithium triangle.” This area of the Central Andes is within an arid plateau with numerous volcanic peaks and salt flats known as “salars” and is the principal lithium-bearing region of South America.

Salar del Hombre Muerto consists of evaporite deposits formed within an isolated basin depression. Fault-bounded bedrock hills occur within and along the margins of the salar basin, subdividing the Salar del Hombre Muerto into two separate sub-basins (eastern and western), each with different evaporite sediment compositions. The eastern sub-basin is dominated by borate evaporites, whereas the western sub-basin is relatively free of clastic sediment (such as sand, silts and clays) and is dominated by halite (sodium chloride) evaporite deposits.

We performed initial geological investigations of the Salar del Hombre Muerto in the early 1990s, prior to development of our lithium production facilities. We commenced commercial extraction operations in Salar del Hombre Muerto in 1998. Lithium extract is processed into lithium carbonate at our co-located manufacturing facility in Fénix, Argentina and into lithium chloride at our nearby manufacturing facility in Güemes, Argentina. These facilities were opened in conjunction with the commencement of our extraction operations and are in good working condition. MdA owns these facilities. We use natural gas and diesel to generate electricity, which is the principal source of power at our facilities. From time to time, we experience interruptions in the supply of electricity, but we do not believe these interruptions materially impact our operations.

Brine containing approximately 600 parts per million ("ppm") lithium is pumped from saltwater aquifers using extraction wells. The brine is then diverted to an evaporation pond system. We have also developed a proprietary lithium concentration and purification process for brine operations that significantly reduces the time from pumping brine from the Salar to processing it into lithium carbonate or lithium chloride. This reduction in processing time compares favorably to a conventional solar evaporation process, while effectively removing impurities and providing increased process control. During evaporation, other minerals, such as sodium, potassium and magnesium, which are typically contained in brine, are concentrated and removed through processing. The resulting lithium chloride brine from the terminal pond of the system is then routed to our processing plants.

We access our extraction sites and nearby manufacturing facilities by local roadway, which is a suitable transportation alternative. We transport the brine extract from our Fénix facility by truck to our Güemes facility for processing. We then transport the processed lithium carbonate and lithium chloride by truck to ports in Argentina and Chile, where it is shipped by vessel to our manufacturing facilities and customers.

Mineral concession rights

MdA holds title to mineral concession rights for its extraction activities in Salar del Hombre Muerto. These mineral concession rights cover an area of approximately 327 square kilometers and are granted to MdA pursuant to the Argentine Mining Code. See subsection “Argentine Law and Regulation” to this Item 1 for more information. Pursuant to the Argentine Mining Code, MdA’s mineral concession rights are valid until the deposit is depleted of all minerals. The concession rights may be rescinded if we fail to pay fees or do not actively extract minerals for a period lasting more than four years.

In 1991, MdA entered into an ongoing agreement, for so long a time as our mineral concession is valid, with the Argentine federal government and the Catamarca province in connection with the development of the Salar del Hombre Muerto exploration site. Following legislative and constitutional reforms in 1993 and 1994, the Argentine federal government assigned all of its rights and obligations under the agreement to the Catamarca province. The agreement governs limited matters relating to our production activities and grants to the Catamarca province an immaterial minority ownership stake in MdA, which enables the province to receive certain dividends and to appoint two of MdA’s ten member Board of Directors and one of MdA’s three member audit committee. The term of the agreement expires when MdA ceases to extract and produce lithium compounds from Salar del Hombre Muerto.

MdA is required to pay the Catamarca province an immaterial semi-annual “canon” fee pursuant to the Argentine Mining Code and royalties equal to 3% of the pithead value of the minerals extracted by MdA pursuant to the Argentine Mining Investment Law and Catamarca provincial law. Under an amendment to its long-term agreement with Catamarca entered into on January 25, 2018, and contingent upon the receipt of certain required permits, MdA will instead pay the Catamarca province a monthly contribution and royalty payment. Together, the contribution and royalty amount will equal 2% of sales of products in a given month measured at the higher of MdA’s average invoice price or an average international price for similar products, net of tax. Royalty payments to the province are netted to give effect to any dividends it receives as a result of its ownership stake in MdA. Total payments to the Catamarca province, including "canon" fee, royalties, water trust and CSR payments, would have been approximately $7.6 million, $9.2 million and $6.5 million for the years ended December 31, 2019, 2018 and 2017 had the amendment described above been in effect for all twelve months for such years.

11

A portion of the territory governed by our concession rights is subject to a longstanding border dispute between Catamarca and the adjacent Salta province. The border dispute has not impacted our operations for the 21 years we have been operating in Argentina and we do not expect that it will impact our operations going forward. We estimate the total area in dispute represents approximately 7.6% of our concession (approximately 25 square kilometers). We do not view this as material, especially considering that the area in question is largely at the fringe of the salar, where the deposits are not as thick and the grade of lithium concentration is much lower.

Salta province claims that it is entitled to royalties from us for the minerals extracted within the small portion of our concession that falls within the disputed territory, although under Argentine law we cannot be charged duplicate royalties for the same minerals. In addition, the Salta province has granted and may grant mineral concessions in the disputed territory to other parties, although to date Catamarca authorities have not permitted any others to extract lithium from within the boundaries of our concession. We are engaged in judicial proceedings in Argentina with the Salta province. The outcome of these proceedings is not expected to have a material impact on our financial position or results of operations.

In December 2019, the provinces of Catamarca and Salta entered into an agreement to create an interprovincial commission to: evaluate projects and programs for mining activity in the area subject to the border dispute; prepare a technical report to set the border between both provinces; and submit a bill to the Congress on the matter.

Water

Our Argentine operations require fresh water. We have water rights for the supply of fresh water from the Trapiche aquifer, from which water is pumped through a battery of wells to our facilities. We and the Catamarca province regularly monitor the water and salinity levels of the aquifer.

We have only once had to temporarily suspend water extraction, which was due to a dispute with the Catamarca province, and our access to our water source was quickly restored. We also regularly evaluate supplemental supplies of fresh water. The grant of water concessions and other water rights is subject to local governmental approvals, the timing and availability of which are uncertain and may be subject to delay or denial.

In October 2015, MdA entered into a trust agreement with the Catamarca province that was amended in 2018. Under the amended trust agreement, MdA is obligated to pay an amount equal to 1.2% of its annual sales determined in a manner consistent with the contribution and royalty payments described above in the "Mineral Concession Rights" subsection to this Item 1, which payment obligations are fully reflected in our financial statements, in lieu of any water use fees.

Energy

Our Argentine operations rely on a steady source of energy. In 2015, we completed construction of a 135 kilometer natural gas pipeline from Pocitos, within the Salta province, to our Fénix facilities at Salar del Hombre Muerto, which eliminated our reliance on natural gas shipments by truck. This pipeline is governed by various agreements between MdA and Recursos Energeticos y Mineros Salta, S.A., or REMSA, a local natural gas sub-distributor, including a subdistribution agreement providing for contracted capacity through 2027. We are in discussions to increase our contracted capacity in advance of our needs for all phases of our expansion plans and may need to invest in additional infrastructure to support this expansion. REMSA or Gasnor S.A., another local natural gas distributor that operates in the northeast of Argentina, have no obligation to provide us the additional capacity on a timely basis or at all. If we cannot obtain such additional capacity, we would need to secure alternative arrangements to meet the increased energy needs of the planned expansion and such alternative arrangements may be less cost effective.

MdA also has a natural gas supply contract with Pluspetrol providing for the supply of natural gas for our Fénix manufacturing facility. This supply agreement expires in April 2020 and is typically renewed on an annual basis. We also have a purchase agreement with YPF SA for the supply of diesel fuel and gasoline to our Fénix and Güemes manufacturing facilities, pursuant to which we submit monthly purchase orders.

Other raw materials

We purchase raw materials and chemical intermediates for use in our production processes, including materials for use in our production of the proprietary adsorbent used to selectively extract lithium from our brine in Argentina, soda ash, or sodium carbonate, for use in our production of lithium carbonate, and lithium metal for our production of butyllithium. In 2019, 2018 and 2017, costs of major raw materials represented 11%, 9% and 11% of our total revenues, respectively. Major raw materials include soda ash, solvents, butyl chloride, hydrochloric acid, quicklime and caustic soda. We generally satisfy our requirements through spot purchases and medium- or long-term contractual relationships. In general, where we have limited sources of raw materials, we have developed contingency plans to minimize the effect of any interruption or reduction in supply, such as sourcing from other suppliers or maintaining safety stocks.

Temporary shortages of raw materials may occasionally occur and cause temporary price increases. For example, we have had past regional interruptions in raw material supply, notably in China. In recent years, these shortages have not resulted in any material unavailability of raw materials. However, the continuing availability and price of raw materials are affected by many factors, including domestic and world market and political conditions, as well as the direct or indirect effect of governmental

12

regulations. During periods of high demand, our raw materials are subject to significant price fluctuations, and such fluctuations may have an adverse impact on our results of operations. The impact of any future raw material shortages on our business as a whole or in specific geographic regions, including China, or in specific business lines cannot be accurately predicted.

Seasonality

Our operations in Argentina are seasonally impacted by weather, including varying evaporation rates and amounts of rainfall during different seasons. These changes impact the concentration in large evaporation ponds and can have an impact on the downstream processes to produce lithium carbonate and lithium chloride. Our operations team continuously measures pond concentrations and models how they will change based on operating decisions. Our processes use proprietary and traditional technologies to minimize the variation of concentrations at the inlet to our plants. In the first quarter of 2019, there was an abnormally large rain event, resulting in an approximate 1,000 MT reduction in lithium carbonate production in 2019.

Argentine Law and Regulation

We are subject to various regulatory requirements in Argentina under the Argentine Mining Code, the Argentine Mining Investment Law and certain federal and provincial regulations, including with respect to environmental compliance. In addition, the relationship between us, MdA and the Catamarca provincial government is regulated through a contractual framework.

The Argentine Mining Code, which sets forth the rights and obligations of both mining companies and their workers, is the principal regulatory framework under which we conduct our operations in Argentina. The Argentine Mining Code provides for the terms under which the provinces regulate and administer the granting of mining rights to third parties.

The Argentine Mining Code establishes two basic means of granting title to mining property: the exploration permit and the mining concession, both of which convey valid mining title in Argentina.

Exploration permits grant their holders the right to freely explore for minerals within the boundaries of the territory covered by that permit as well as to request the mining concession for any discoveries within the covered territory.

Once a mining concession is granted, the recipient owns all in-place mineral deposits within the boundaries of the territory covered by the concession. Mining concessions are freely tradable by the title holder and can be sold, leased or otherwise transferred to third parties. Two requirements must be met to keep a mining concession in good standing: (i) the concession holder must make regular payments of a semi-annual fee known as a canon; and (ii) the concession holder must file and perform an initial five year expenditure plan. In addition, prior to commencing mining activities, the concession holder must submit environmental impact studies, which must be renewed at least every two years, for approval by the relevant environmental authorities.

In addition to the Argentine Mining Code, we are also subject to the Argentine Mining Investment Law. The Argentine Mining Investment Law offers specific financial incentives to mining investors, including a 30 year term fiscal stability of national, provincial and municipal tax rates; a deduction from income tax for prospecting, exploration and feasibility study expenditures; a refund of Value Added Tax fiscal credits resulting from exploration works; accelerated depreciation of fixed assets; and a 3% cap on royalties payable out of production to the province where the deposit is located. Our 30 year term fiscal stability certificate expires in 2026.

Our fiscal stability rights under the Argentine Mining Investment Law have been challenged by the imposition of certain export taxes on our lithium chloride and carbonate exports that did not exist at the time we obtained our 30 year term fiscal stability certificate. For instance, in 2018, the Federal Government imposed another export duty on lithium carbonate and chloride through Decree No. 793/2018, which is to be in effect until December 31, 2020. Furthermore, in December 2019, after the change of Presidential administration, the Congress passed Law No. 27,541 creating a new legal framework for export duties and establishing a new rate for mining and hydrocarbon exports. However, the Executive Power has not yet exercised its power under the Law No. 27,541 to modify the regime set under Decree No. 793/2018.

Under our 30 year term fiscal stability certificate, we are entitled to reimbursement or set-off (against other federal taxes) of any amount paid in excess of the total federal taxable burden applicable to us under such certificate. Although we are litigating to exercise our fiscal stability rights with respect to the imposition of certain of such export taxes, there can be no assurance that we will seek, or be able to obtain, reimbursement or set-off.

Environmental Laws and Regulations

We are subject to and incur capital and operating costs to comply with, numerous foreign, U.S. federal, state and local environmental, health and safety laws and regulations, including those governing employee health and safety, the composition of our products, the discharge of pollutants into the air and water, the management and disposal of hazardous substances and wastes, the usage and availability of water, the cleanup of contaminated properties and the reclamation of our mines, brine extraction operations and certain other assets at the end of their useful life.

Our business and our customers are subject to significant requirements under the European Community Regulation for the Registration, Evaluation, Authorization and Restriction of Chemicals (“REACH”). REACH imposes obligations on European Union manufacturers and importers of chemicals and other products into the European Union to compile and file comprehensive

13

reports, including testing data, on each chemical substance, and perform chemical safety assessments. Additionally, substances of high concern, as defined under REACH, are subject to an authorization process. Authorization may result in restrictions in the use of products by application or even in banning of the product. REACH regulations impose significant additional responsibilities and costs on chemical producers, importers, downstream users of chemical substances and preparations, and the entire supply chain. Our manufacturing presence and sales activities in the European Union may result in increases in the costs of raw materials we purchase and the products we sell. Increases in the costs of our products could result in a decrease in their overall demand; additionally, customers may seek products that are not regulated by REACH, which could also result in a decrease in the demand of certain products subject to the REACH regulations.

In June 2016, modifications to the Toxic Substances Control Act in the U.S. were signed into law, requiring chemicals to be assessed against a risk-based safety standard and for the elimination of unreasonable risks identified during risk evaluation. Other pending initiatives potentially will require toxicological testing and risk assessments of a wide variety of chemicals, including chemicals used or produced by us. These initiatives include the Voluntary Children’s Chemical Evaluation Program, and High Production Volume Chemical Initiative in the U.S., as well as new initiatives in Asia and other regions. These assessments may result in heightened concerns about the chemicals involved and additional requirements being placed on the production, handling, labeling or use of the subject chemicals. Such concerns and additional requirements could also increase the cost incurred by our customers to use our chemical products and otherwise limit the use of these products, which could lead to a decrease in demand for these products.

Liabilities associated with the investigation and cleanup of hazardous substances and wastes, as well as personal injury, property damages or natural resource damages arising from the release of, or exposure to, such hazardous substances and wastes, may be imposed in many situations without regard to violations of laws or regulations or other fault, and may also be imposed jointly and severally. Such liabilities may be imposed on entities that formerly owned or operated the property affected by the hazardous substances and wastes, entities that arranged for the disposal of the hazardous substances and wastes at the affected property, and entities that currently own or operate such property. Our Bessemer City, North Carolina facility is currently undergoing monitoring and remediation of contamination pursuant to a Resource Conservation and Recovery Act Part B corrective action permit. In addition, we currently have, and may in the future incur, liability as a potentially responsible party with respect to third party locations under CERCLA or state and foreign equivalents, including potential joint and several liability requiring us to pay in excess of our pro rata share of remediation costs.

We use and generate hazardous substances and wastes in our operations and may become subject to claims and substantial liability for personal injury, property damage, wrongful death, loss of production, pollution and other environmental damages relating to the release of such substances into the environment. In addition, some of our current properties are, or have been, used for industrial purposes, which could contain currently unknown contamination that could expose us to governmental requirements or claims relating to environmental remediation, personal injury and/or property damage. Depending on the frequency and severity of such incidents, it is possible that the Company’s revenues, operating costs, insurability and relationships with customers, employees and regulators could be impaired.

We record accruals for environmental matters when it is probable that a liability has been incurred and the amount of the liability can be reasonably estimated. It is possible that new information or future developments could require us to reassess our potential exposure related to environmental matters. We may incur significant costs and liabilities in order to comply with existing environmental laws and regulations. It is also possible that other developments, such as increasingly strict environmental laws, regulations and orders of regulatory agencies, as well as claims for damages to property and the environment or injuries to employees and other persons resulting from our current or past operations, could result in substantial costs and liabilities in the future.

A discussion of environmental related factors and related reserves can be found in Note 8 “Environmental Obligations” in the notes to our consolidated financial statements included in this Form 10-K.

Employees

As of December 31, 2019, we employed approximately 800 people, with approximately 300 people in our domestic operations and 500 people in our foreign operations. We believe we have a good relationship with our employees.

Approximately 190 of our Argentine employees are represented by collective bargaining agreements. To date, we have not faced any material work stoppages. We cannot predict, however, the outcome of future contract negotiations or the effect any future work stoppage may have on our results of operations. We also utilize approximately 50 independent contractors in our facility in Patancheru, India pursuant to a manufacturing services agreement that expires in 2022.

14

ITEM 1A. | RISK FACTORS |

Among the factors that could have an impact on our ability to achieve operating results and meet our other goals are:

Growth Strategy and Market Risks:

Our growth depends upon the continued growth in demand for electric vehicles with high performance lithium compounds.

We are one of a few producers of performance lithium compounds that are a critical input in current and next generation high energy density batteries used in electric vehicle applications. Our growth is dependent upon the continued adoption by consumers of electric vehicles. If the market for electric vehicles does not develop as we expect, or develops more slowly than we expect, our business, prospects, financial condition and results of operations will be affected. The market for electric vehicles is relatively new, rapidly evolving, and could be affected by numerous external factors, such as:

• | government regulations and automakers' responses to those regulations; | ||

• | tax and economic incentives; | ||

• | rates of consumer adoption, which is driven in part by perceptions about electric vehicle features (including range per charge), quality, safety, performance, cost and charging infrastructure; | ||

• | competition, including from other types of alternative fuel vehicles, plug-in hybrid electric vehicles, and high fuel-economy internal combustion engine vehicles; and | ||

• | volatility in the cost of battery materials, oil and gasoline; | ||

• | rates of customer adoption of higher performance lithium compounds; and | ||

• | rates of development and adoption of next generation high nickel battery technologies. | ||

Lithium prices can be volatile, especially due to changes in supply.

The prices of lithium have been, and may continue to be, volatile. We seek to manage volatility through the sale of performance lithium compounds and by entering into long term contracts with our customers across a range of applications, geographies and industries; however, such efforts may not be successful. Since late 2018, we have experienced significant pricing pressures, which we attribute to the oversupply of lithium compounds in the worldwide lithium industry, and we expect such pricing pressures to continue throughout 2020. We expect that prices for the performance lithium compounds we manufacture will continue to be influenced by various factors, including regional and global demand-supply balance as well as the business strategies of major producers. Some of the major producers (including us) have increased production, which increases overall global supply and can drive down prices. Certain market analysts predict a significant increase in global lithium capacity over the short and medium term. However, there is a high degree of uncertainty about the ability of our current and potential competitors to develop new lithium production capacity expansion projects given the substantial capital costs involved in such projects, the potential need for third party financing which may not be available, and the time and uncertainty involved in achieving product qualities at a level that will be qualified by customers. Further declines in lithium prices could have a material adverse effect on our business, financial condition and results of operations.

Adverse conditions in the economy and volatility and disruption of financial markets can negatively impact our customers, and downturns in our customers’ end-markets could adversely affect our sales and profitability.

We produce performance lithium compounds for application in a diverse range of end-products, including electric vehicle batteries and for a wide variety of industrial, pharmaceutical, aerospace, electronic, agricultural and polymer applications. Deterioration in the global economy or in the specific industries in which our customers compete could adversely affect the demand for our customers’ products, which, in turn, could negatively affect our sales and profitability. Many of our customers’ end-markets are cyclical in nature or are subject to secular downturns. Historically, cyclical or secular end-market downturns have resulted in diminished demand for our performance lithium compounds and have caused a decline in average selling prices, and we may experience similar problems in the future.

We face competition in our business.

We compete globally against a number of other lithium producers. Competition is based on several key criteria, including technological capabilities, service, product performance and quality, cost and price. Some of our competitors are larger than we are and may have greater financial resources. These competitors may also be able to maintain greater operating and financial

15

flexibility. If we fail to compete effectively, we may be unable to retain or expand our market share, which could have a material adverse effect on our business, results of operations and financial condition.

Our operating results are subject to substantial quarterly and annual fluctuations.

Our revenue and operating results have fluctuated in the past and are likely to fluctuate in the future. These fluctuations may occur on a quarterly and annual basis and are due to a number of factors, many of which are beyond our control. These factors include, among others:

•changes in our product mix or customer mix;

•the oversupply of lithium compounds in the global lithium industry;

•the timing of receipt, reduction or cancellation of significant product orders by customers;

•the timing, duration and pricing terms of new customer contracts and renewals;

• | our ability to adapt to changes in technology trends affecting the lithium industry, including new manufacturing processes; |

•fluctuations in currency exchange and interest rates;

•the effects of competitive pricing pressures, including decreases in average selling prices of our products; and

• | the extent to which we are required to purchase third party lithium carbonate to supplement our internally produced lithium carbonate from our company-owned mineral deposits in Argentina, as purchasing from third parties leads to higher production costs and reduced margins. |

In addition, a significant amount of our operating expenses are relatively fixed in nature due to our significant sales, research and development, and internal manufacturing overhead costs. As a result, we believe that quarter-to-quarter comparisons of our revenue and operating results may not be meaningful or a reliable indicator of our future performance. If our operating results in one or more future quarters fail to meet the expectations of securities analysts or investors, a significant decline in the trading price of our common stock may occur, which may happen immediately or over time.

Our production expansion efforts are complex projects that will require significant capital expenditures and are subject to significant risks and uncertainties.

In order to meet growing and forecasted demands for our performance lithium compounds, particularly lithium hydroxide, we intend to expand our lithium hydroxide capacity in order to meet customer demands globally, as our customers expand their own production networks around the globe. To support our lithium hydroxide expansion, we started a project to expand annual lithium carbonate production at our existing operations in Argentina in addition to seeking alternative lithium resources. Our expansion projects are complex undertakings, and there can be no assurance that we will be able to complete these projects within our projected budget and schedule or that we will be able to achieve the anticipated benefits from them. Unforeseen technical or construction difficulties, regulatory requirements, labor or civil/political unrest, community relations or logistical issues, or local hiring and procurement policies and requirements (discussed further under the below risk factor “Our lithium extraction and production operations in Argentina expose us to specific political, financial and operational risks”) could increase the cost of these projects, delay the projects or render them infeasible. Any significant delay in the completion of the projects or increased costs could have an adverse effect on our business, financial condition and results of operations.

The development and adoption of new battery technologies that rely on inputs other than lithium compounds could significantly impact our prospects and future revenues.

Current and next generation high energy density batteries for use in electric vehicles rely on lithium compounds as a critical input. The development and adoption of new battery technologies that rely on inputs other than lithium compounds or a delay in the development and adoption of next generation high nickel battery technologies that utilize lithium hydroxide could significantly impact our prospects and future revenues. Many materials and technologies are being researched and developed with the goal of making batteries lighter, more efficient, faster charging and less expensive, and some of these could be less reliant on lithium hydroxide or other lithium compounds. We cannot predict which new technologies may ultimately prove to be commercially viable and on what time horizon. Commercialized battery technologies that use less lithium compounds could materially and adversely impact our prospects and future revenues.

16

We may have difficulty accessing global capital and credit markets.

We expect to rely on cash generated from operations and external financing to fund our growth and ongoing capital needs. The expansion of our business or other business opportunities may require significant amounts of working capital. While we believe that our cash from operations, together with borrowing availability under our Revolving Credit Facility and other potential working capital financing strategies that may be available to us, will be sufficient to meet these needs in the foreseeable future, if we need additional external financing, our access to credit markets and the pricing of our capital will be dependent upon maintaining sufficiently strong credit metrics and the state of the capital markets generally. There can be no assurances that we would be able to obtain equity or debt financing on terms we deem acceptable, and it is possible that the cost of any financings could increase significantly, thereby increasing our expenses and decreasing our net income. If we are unable to generate sufficient cash flow or raise adequate external financing, including as a result of significant disruptions in the global credit markets, we could be forced to restrict our operations and growth opportunities, which could adversely affect our operating results.

We expect recent market factors, including industry oversupply conditions and decreased pricing levels, to continue in 2020 as we continue our expansion and we expect our net leverage ratio under our Revolving Credit Facility covenants to increase during the next 12 months from the date of this filing. Compliance with our debt covenants will continue to be determined, in large part, by our ability to manage the timing and amount of our capital expenditures, which is within our control; as well as by our ability to achieve forecasted operating results and to pursue other working capital financing strategies that may be available to us, which is less certain and outside our control. As a result, we have slowed the pace of our carbonate expansion in Argentina resulting in the delay of phase 1 completion to the middle of 2021 and will be pausing our current lithium hydroxide expansion project to align its completion with that of phase 1 in Argentina. We also plan to pursue additional working capital financing strategies, including potential amendments or waivers to our Revolving Credit Facility, among others. Projected 2020 capital expenditures and expenditures related to contract manufacturers are expected to be between $200 million to $230 million but may need to be reduced significantly depending on the timing and success of management’s planned additional working capital financing strategies and future operating results.

Our research and development efforts may not succeed, and our competitors may develop more effective or successful products.

The industries and the end markets into which we sell our products experience regular technological change and product improvement. Our ability to compete successfully depends in part upon our ability to maintain a superior technological capability and to continue to identify, develop and commercialize new and innovative performance lithium compounds for use in our customers’ products in the electric vehicle, aerospace and other sectors. There is no assurance that our research and development efforts will be successful or that any newly developed products will pass our customers’ qualification processes or achieve market-wide acceptance. If we fail to keep pace with evolving technological innovations in our customers’ end markets, our business, financial condition and results of operations could be adversely affected. In addition, existing or potential competitors may develop products which are similar or superior to our products or are more competitively priced. If our product launching efforts are unsuccessful, our financial condition and results of operations may be adversely affected.

We may make future acquisitions which may be difficult to integrate, divert management and financial resources and result in unanticipated costs.

As part of our continuing business strategy, we may make acquisitions of, or investments in, companies or technologies that complement our current products, enhance our market coverage, technical capabilities or production capacity, or offer growth opportunities. We do not have specific timetables for these plans and we cannot be certain that we will be able to identify suitable acquisition or investment candidates for sale at reasonable prices.

Future acquisitions could pose numerous risks to our operations, including difficulty integrating the acquired operations, products, technologies or personnel; substantial unanticipated integration costs; diversion of significant management attention and financial resources from our existing operations; a failure to realize the potential cost savings or other financial benefits and/or the strategic benefits of the acquisitions; and the incurrence of liabilities from the acquired businesses for environmental matters, infringement of intellectual property rights or other claims (for which we may not be successful in seeking indemnification). These and other risks relating to acquiring, integrating and operating acquired assets or companies could cause us not to realize the anticipated benefits from such activity and could have a material adverse effect on our business, financial condition and results of operations.

Operational Risks:

We have substantial international operations and sales, and the risks of doing business in foreign countries could adversely affect our business, financial condition and results of operations.

We conduct a substantial portion of our business outside the United States. For the years ended December 31, 2019, 2018 and 2017, approximately 80%, 81% and 77% of our revenues, respectively, were derived from sales outside of the United States. In addition, for the years ended December 31, 2019, 2018 and 2017 approximately 26%, 38% and 44% of our revenues, respectively, were denominated in a currency other than the U.S. Dollar (primarily the Chinese yuan and Euro) and approximately 33%, 26% and 28% of our costs, respectively, were denominated in a currency other than the U.S. Dollar (primarily the Argentine peso,

17

Chinese yuan and British pound). Accordingly, our business is subject to risks related to foreign exchange as well as risks related to the differing legal, political, social and regulatory requirements and economic conditions of the many jurisdictions where we conduct business.

Changes in exchange rates between foreign currencies and the U.S. Dollar will affect the recorded levels of our assets, liabilities, net sales, cost of goods sold and operating margins and could result in exchange losses. Our results of operations may be adversely affected by any volatility in currency exchange rates and our ability to manage effectively our currency transaction and translation risks. Foreign currency debt and foreign exchange forward contracts may be used in countries where we do business, thereby reducing our net asset exposure. Foreign exchange forward contracts are also used to hedge firm and highly anticipated foreign currency cash flows. The Argentine peso has recently declined significantly in value, and we currently do not hedge foreign currency risks associated with the Argentine peso due to the limited availability and high cost of suitable derivative instruments.

In addition, it may be more difficult for us to enforce agreements or collect receivables through foreign legal systems. There is a risk that foreign governments may nationalize private enterprises in certain countries where we operate. In certain countries or regions, terrorist activities and the response to such activities may threaten our operations more than in the United States. Social and cultural norms in certain countries may not support compliance with our corporate policies including those that require compliance with substantive laws and regulations. Also, changes in general economic and political conditions in countries where we operate are a risk to our financial performance and future growth. Our sales depend on international trade and moves to impose tariffs and other trade barriers, as is happening in various countries including the United States, could negatively affect our sales and have a material adverse effect on our business, financial condition and results of operations.

We and our subsidiaries are also subject to rules and regulations related to anti-bribery, anti-corruption (such as the U.S. Foreign Corrupt Practices Act), anti-money laundering, trade sanctions and export controls. Compliance with such laws may be costly and violations of such laws may carry substantial penalties.

As we continue to operate our business globally, our success will depend, in part, on our ability to anticipate and effectively manage these and other related risks. There can be no assurance that the consequences of these and other factors relating to our international operations will not have an adverse effect on our business, financial condition or results of operations.

In particular, one of our key manufacturing facilities is located in the United Kingdom. Following a referendum in June 2016 in which a majority of voters in the United Kingdom approved an exit from the European Union, the United Kingdom initiated the formal process to leave the European Union (often referred to as “Brexit”) which occurred on January 31, 2020. At this stage, it is unclear how Brexit will affect economic conditions in the United Kingdom, the European Union, or globally. Brexit could adversely affect European and worldwide economic and market conditions and could contribute to instability in global financial and foreign exchange markets, including volatility in the value of the euro and the British pound. In addition, Brexit could lead to legal uncertainty and potentially divergent national laws and regulations, as the United Kingdom determines which European Union laws to replace or replicate. While we actively monitor for developments and update our contingency plans, any of these effects of Brexit, and others we cannot anticipate, could adversely affect our business, financial condition or results of operations.

Our lithium extraction and production operations in Argentina expose us to specific political, financial and operational risks.

We obtain the substantial majority of our lithium from our operations in Argentina. Our operations in Argentina expose us to the following risks, and the occurrence of any of these risks could have a material adverse effect on our business, financial condition or results of operations:

• | Political and financial risks that are typical of developing countries. Such risks include: high rates of inflation; risk of expropriation and nationalization or changes in or nullification of concession rights; changes in taxation policies; restrictions on foreign exchange and repatriation; labor unrest; changing political norms and currency controls; and governmental policies and regulations that favor or require us or our contractors and subcontractors to award contracts in, employ citizens of, or purchase supplies from, Argentina and the local provinces where we operate. In addition, changes in mining or investment policies or shifts in political attitude in Argentina concerning mining may adversely affect our operations or profitability. There can be no assurance that the new or future governments of Argentina will not impose greater state control of lithium resources, or take other actions that are adverse to us. | ||

18

• | Risks associated with changes in tax laws. On December 20, 2019 the Argentine Congress declared an economic emergency and introduced new export duties on hydrocarbon and mining goods, a special tax on foreign exchange transactions, changes to taxes on bank accounts, the Argentine income tax, and internal taxes. The previously approved reduction of the corporate tax rate from 30% to 25% that would have been effective January 1, 2020 has been suspended for a year. The implementing regulations regarding export duties have not yet been published, so the extent of the impact of this new law to our activity in Argentina cannot yet be determined. Under the tax stability certificate we have with the Argentine federal government, we are entitled to reimbursement or set-off (against other federal taxes) of any amount paid in excess of the total federal taxable burden applicable to us under such certificate. However, there can be no assurance that we will seek, or be able to obtain, such reimbursement or set-off. | ||

• | Operational risks stemming from our dependence upon mining concessions granted to us under the Argentine Mining Code. We hold title to these mining concessions in perpetuity until the deposit is exhausted of all minerals, provided that we pay annual mining fees and keep the mining concessions active in accordance with the Argentine Mining Code. Failure to pay the annual fees or to keep the mining concessions active may result in revocation of our mining concessions. In addition, Argentinian federal and provincial mining authorities retain broad discretion in the enforcement of mining and environmental regulations, including through imposition of fines or suspension of mining extraction or related water rights. | ||

• | Risks associated with the loss or depletion of our mineral deposit. Our primary source for lithium is our current brine site at Salar del Hombre Muerto. In order to maintain our production capabilities, we will need to replace or supplement our lithium resources there in the event our access is disrupted or lost, whether due to a natural disaster, depletion or otherwise. Although we seek to reduce dependence on this primary source of supply for lithium, there is no assurance we will be able to do so in a timely manner or on commercially favorable terms. In addition, due to the current trend of growth in the lithium industry, there is no assurance that we will be able to discover or acquire new and valuable lithium resources, or that the actual production results will match the expected results. | ||

• | Risks of certain natural disasters. Our lithium brines and related production facilities are located in a seismically active region in northwest Argentina. A major earthquake could have adverse consequences for our operations and for general infrastructure, such as roads, rail, and access to goods in Argentina. Our production operations in Argentina could also be subject to significant rain events, as our production processes rely on natural evaporation and a significant rain event could impact our production. In the first quarter of 2019, we experienced a significant rain event in Argentina, which disrupted our supply chain and required that we purchase additional third party lithium carbonate for use in our lithium hydroxide production operations. If our brine site in Argentina were to suffer another significant rain event, or if any of our operating facilities in Argentina were to suffer an earthquake or other natural disaster, this could have a material adverse effect on our business, financial condition and results of operations. | ||

• | Risks associated with water rights and our access to water. Access to fresh water is essential to our production operations in Argentina; we hold water use rights granted to us by provincial Argentine authorities and will need to secure additional water rights for our planned production expansion. (See Part I, Item 1 Business-Raw Materials-Water section of this Annual Report on Form 10-K). Our operations take place in a dry, mountainous region that has limited access to fresh water and where competition among users for continuing access to water is significant. The governmental authority may seek to suspend or alter our rights or the applicable water rights code may change, each of which may limit our access to fresh water. In addition, our access to water may be impacted by changes in geology, climate change (including the potential effects of climate change such as drought, changes in precipitation patterns, and severe weather events) or other natural factors, such as wells drying up or reductions in the amount of water available in the wells or sources from which we obtain water, that we cannot control. There can be no assurance that we will have access to sufficient quantities of water to support our production operations, either at current capacities or our planned production expansion, in the future. | ||

19

• | Risks associated with foreign exchange controls and restrictions. On September 1, 2019, the Argentine Government reinstated certain foreign exchange restrictions that will remain in place indefinitely. The restrictions that may impact our Argentina operations relate to: (i) a requirement that Argentinian exporters repatriate proceeds allocated or earned abroad and convert them into Argentinian pesos within a specified time-frame; and (ii) limitations on the payment of dividends and payment for services performed by related parties, which would now generally require prior written authorization from the Argentinian Central Bank. There can be no assurance that these foreign exchange restrictions will not be modified to be even more restrictive. A new Presidential administration took office on December 10, 2019, and there is a risk that the Argentine Foreign Exchange regulations will become even more restrictive. | ||