Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - Focus Financial Partners Inc. | focs-20191231ex321c7cd9b.htm |

| EX-31.2 - EX-31.2 - Focus Financial Partners Inc. | focs-20191231ex312ab3aae.htm |

| EX-31.1 - EX-31.1 - Focus Financial Partners Inc. | focs-20191231ex311db9c96.htm |

| EX-23.1 - EX-23.1 - Focus Financial Partners Inc. | focs-20191231ex231d9335d.htm |

| EX-21.1 - EX-21.1 - Focus Financial Partners Inc. | focs-20191231ex2114a48ff.htm |

| EX-10.32 - EX-10.32 - Focus Financial Partners Inc. | focs-20191231ex1032e3dbc.htm |

| EX-10.31 - EX-10.31 - Focus Financial Partners Inc. | focs-20191231ex1031896e6.htm |

| EX-10.19 - EX-10.19 - Focus Financial Partners Inc. | focs-20191231ex1019204ea.htm |

| EX-10.18 - EX-10.18 - Focus Financial Partners Inc. | focs-20191231ex1018fd12b.htm |

| EX-4.2 - EX-4.2 - Focus Financial Partners Inc. | focs-20191231ex42537e53e.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File No. 001-38604

Focus Financial Partners Inc.

(Exact Name of Registrant as Specified in its Charter)

|

Delaware |

47‑4780811 |

|

(State or Other Jurisdiction |

(I.R.S. Employer |

|

|

|

|

875 Third Avenue, 28th Floor |

10022 |

|

(Address of Principal Executive Offices) |

(Zip Code) |

(646) 519‑2456

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

Class A common stock, par value $0.01 per share |

|

FOCS |

|

Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S -T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☒ |

Accelerated filer ☐ |

Non-accelerated filer ☐ |

Smaller reporting company ☐ |

|

|

|

|

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b -2 of the Exchange Act): ☐ Yes ☒ No

The aggregate market value of the Class A common stock held by non-affiliates was $829,203,698 on June 28, 2019, the last business day of the registrant’s most recently completed second fiscal quarter.

As of February 20, 2020, the registrant had 47,421,315 shares of Class A common stock and 22,075,749 shares of Class B common stock outstanding.

Documents incorporated by reference:

The registrant’s definitive proxy statement relating to the annual meeting of shareholders (to be held June 3, 2020) will be filed with the Securities and Exchange Commission within 120 days after the close of the registrant’s fiscal year ended December 31, 2019 and is incorporated by reference in Part III to the extent described herein.

FOCUS FINANCIAL PARTNERS INC.

FOR THE YEAR ENDED DECEMBER 31, 2019

| 1 | ||

| 2 | ||

| 3 | ||

| 3 | ||

| 18 | ||

| 39 | ||

| 39 | ||

| 39 | ||

| 39 | ||

| 40 | ||

| 40 | ||

| 40 | ||

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

42 | |

| 63 | ||

| 64 | ||

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

64 | |

| 64 | ||

| 66 | ||

| 67 | ||

| 67 | ||

| 67 | ||

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

67 | |

|

Certain Relationships and Related Transactions, and Director Independence |

67 | |

| 67 | ||

|

PART IV |

|

|

| 67 | ||

| 71 | ||

|

F-1 |

||

i

CAUTIONARY STATEMENT REGARDING FORWARD‑LOOKING STATEMENTS

Some of the information in this Annual Report on Form 10‑K (this “Annual Report”) may contain forward‑looking statements. Forward‑looking statements give our current expectations, contain projections of results of operations or of financial condition, or forecasts of future events. Words such as “may,” “assume,” “forecast,” “position,” “predict,” “strategy,” “expect,” “intend,” “plan,” “estimate,” “anticipate,” “believe,” “project,” “budget,” “potential,” “continue,” “will” and similar expressions are used to identify forward‑looking statements. They can be affected by assumptions used or by known or unknown risks or uncertainties. Consequently, no forward‑looking statements can be guaranteed. When considering these forward‑looking statements, you should keep in mind the risk factors and other cautionary statements described under “Part I, Item 1A, Risk Factors.” Actual results may vary materially. You are cautioned not to place undue reliance on any forward‑looking statements. You should also understand that it is not possible to predict or identify all such factors and should not consider the following list to be a complete statement of all potential risks and uncertainties. Factors that could cause our actual results to differ materially from the results contemplated by such forward‑looking statements include:

|

· |

fluctuations in wealth management fees; |

|

· |

our reliance on our partner firms and the principals who manage their businesses; |

|

· |

our ability to make successful acquisitions; |

|

· |

unknown liabilities of or poor performance by acquired businesses; |

|

· |

harm to our reputation; |

|

· |

our inability to facilitate smooth succession planning at our partner firms; |

|

· |

our inability to compete; |

|

· |

our reliance on key personnel and principals; |

|

· |

our inability to attract, develop and retain talented wealth management professionals; |

|

· |

our inability to retain clients following an acquisition; |

|

· |

our reliance on key vendors; |

|

· |

write down of goodwill and other intangible assets; |

|

· |

our failure to maintain and properly safeguard an adequate technology infrastructure; |

|

· |

cyber‑attacks; |

|

· |

our inability to recover from business continuity problems; |

|

· |

inadequate insurance coverage; |

|

· |

the termination of management agreements by management companies; |

|

· |

our inability to generate sufficient cash to service all of our indebtedness or our ability to access additional capital; |

|

· |

the failure of our partner firms to comply with applicable U.S. and non‑U.S. regulatory requirements and the highly regulated nature of our business; |

|

· |

legal proceedings, governmental inquiries; and |

1

|

· |

other factors discussed in this Annual Report. |

All forward‑looking statements are expressly qualified in their entirety by the foregoing cautionary statements. Our forward‑looking statements speak only as of the date of this Annual Report or as of the date as of which they are made. Except as required by applicable law, including federal securities laws, we do not intend to update or revise any forward‑looking statements.

The following terms are used throughout this Annual Report:

Base Earnings. This is a percentage of the estimated operating cash flow earnings before partner compensation (i.e. Target Earnings) upon which we apply a multiple to determine acquisition prices. We retain a cumulative preferred position in Base Earnings.

Commission‑based. Commission‑based revenue is derived from commissions paid by clients or payments from third parties for sales of investment or insurance products.

Fee‑based. Fee‑based services are those for which a partner firm primarily charges a fee directly to the client for wealth management services, recordkeeping and administration services and other services rather than being primarily compensated through commissions from third parties for recommending financial products.

Fiduciary Duty. A fiduciary duty is a legal duty to act in another party’s interests, with utmost good faith, to make full and fair disclosure of all material facts and to exercise all reasonable care to avoid misleading clients.

GAAP. Accounting principles generally accepted in the United States of America.

High Net Worth. High net worth individuals are generally defined in the financial industry as those with liquid financial assets, excluding primary residence, in excess of $1 million.

Lift Out. The circumstance when a group of wealth management professionals, already working as a team, seeks to leave their current employer and join another employer or start their own registered investment advisor firm.

Open‑architecture. An investment platform that grants clients access to a wide range of investment funds and products offered by third parties. By contrast, a closed architecture is an investment platform that grants clients access only to proprietary investment funds and products.

Partnership. The term we use to refer to our business and relationship with our partner firms. It is not intended to describe a particular form of legal entity or a legal relationship.

Target Earnings. The estimated operating cash flow earnings before partner compensation.

Ultra‑High Net Worth. Ultra‑high net worth individuals are generally defined in the financial industry as those with liquid financial assets, excluding primary residence, in excess of $30 million.

Wealth Management. Comprehensive professional services that combine investment advice, financial and tax planning, consulting, tax return preparation, family office services and other services that help clients achieve their objectives regarding accumulation, preservation and distribution of long‑term wealth.

Wirehouse. Brokerage firm that provides a full range of investment, research, trading and wealth management services to clients. The term originated prior to the advent of modern wireless communications, when brokerage firms were connected to their branches primarily through telephone and telegraph wires.

2

Unless otherwise indicated or the context requires, all references to “we”, “us”, “our”, the “Company”, “Focus Inc.” and similar terms for periods prior to our initial public offering (“IPO”) and related reorganization transactions (the “Reorganization Transactions”) refer to Focus Financial Partners, LLC and its subsidiaries. For periods subsequent to the IPO and Reorganization Transactions, these terms refer to Focus Financial Partners Inc. and its consolidated subsidiaries. “Focus LLC” refers to Focus Financial Partners, LLC, a Delaware limited liability company and a consolidated subsidiary of ours following the IPO and Reorganization Transactions.

The term “partner firms” refers to our consolidated subsidiaries engaged in wealth management and related services, the businesses of which are typically managed by the principals. The term “principals” refers to the wealth management professionals who manage the businesses of our partner firms pursuant to the relevant management agreement. The term “our partnership” refers to our business and relationship with our partner firms and is not intended to describe a particular form of legal entity or a legal relationship.

Corporate Structure

Focus Inc. was incorporated as a Delaware corporation on July 29, 2015 for the purpose of completing the IPO and Reorganization Transactions. On July 30, 2018, we completed our IPO of 18,648,649 shares of Class A common stock, par value $0.01 per share. The shares began trading on the NASDAQ Global Select Market on July 26, 2018 under the ticker symbol “FOCS.” We used the proceeds from the IPO to purchase certain outstanding Focus LLC units, to reduce indebtedness under our credit facility and for acquisitions and general corporate business purposes.

In connection with the IPO and Reorganization Transactions, Focus Inc. became a holding company whose most significant asset is a membership interest in Focus LLC. Focus LLC directly or indirectly owns all of the outstanding equity interests in our partner firms. Focus Inc. is the sole managing member of Focus LLC and is responsible for all operational, management and administrative decisions of Focus LLC. Subject to certain restrictions, unitholders of Focus LLC (other than Focus Inc. and any of its subsidiaries) may receive shares of our Class A common stock pursuant to the exercise of an exchange right or a call right.

Our Company

We are a leading partnership of independent, fiduciary wealth management firms operating in the highly fragmented registered investment adviser (“RIA”) industry, with a footprint of over 60 partner firms primarily in the United States. We have achieved this market leadership by positioning ourselves as the partner of choice for many firms in an industry where a number of secular trends are driving consolidation. Our partner firms primarily service ultra‑high net worth and high net worth individuals and families by providing highly differentiated and comprehensive wealth management services. Our partner firms benefit from our intellectual and financial resources, operating as part of a scaled business model with aligned economic interests, while retaining their entrepreneurial culture and independence.

3

Our partnership is built on the following principles, which enable us to attract and retain high‑quality wealth management firms and accelerate their growth:

|

Entrepreneurship: |

Maintain the entrepreneurial spirit, independence and unique culture of each partner firm. |

|

|

|

|

Fiduciary Standard: |

Partner with wealth management firms that are held to the fiduciary standard in serving their clients. |

|

|

|

|

Alignment of Interests: |

Align principals’ interests with our interests through our differentiated partnership and economic model. |

|

|

|

|

Value‑Add Services: |

Empower our partner firms through collaboration on strategy, growth and acquisition opportunities, marketing, technology and operational expertise, best practices, cash and credit solutions. Provide access to world‑class intellectual resources and capital to fund expansion and acquisitions. |

We were founded by entrepreneurs and began revenue‑generating and acquisition activities in 2006. Since that time, we have:

|

· |

created a partnership of over 60 partner firms, the substantial majority of which are RIAs registered with the Securities and Exchange Commission (the “SEC”) pursuant to the Investment Advisers Act of 1940 (the “Advisers Act”); |

|

· |

built a business with revenues in excess of $1.2 billion for the year ended December 31, 2019; |

|

· |

increased revenues at a compound annual growth rate of 35.1% since 2006; |

|

· |

established an attractive revenue model whereby in excess of 95% of our revenues for the year ended December 31, 2019 were fee‑based and recurring in nature; |

|

· |

built a partnership currently comprised of approximately 4,000 wealth management‑focused principals and employees; and |

|

· |

established a national footprint across the United States and expanded our presence internationally with partner firms in the United Kingdom, Canada and Australia. |

We are in the midst of a fundamental shift in the growing wealth management services industry. The delivery of wealth management services is moving from traditional brokerage, commission‑based platforms to a fiduciary, open‑architecture and fee‑based structure. This shift has resulted in a significant transfer of client assets and wealth management professionals out of traditional brokerage, commission‑based platforms to independent wealth management practices. We believe that our leading partnership of independent, fiduciary wealth management firms positions us to benefit from these trends.

The independent wealth management industry, including RIAs, is highly fragmented, which we believe enables us to continue our growth strategy of acquiring high‑quality independent wealth management firms, directly and through acquisitions by our partner firms. We have a track record of enhancing the competitive position of our partner firms by providing them with access to the intellectual expertise, resources and network benefits of our large organization. Our scale enables us to help our partner firms achieve operational efficiencies and ensure organizational continuity. Additionally, our scale, resources and value‑added services increase our partner firms’ ability to achieve growth through a variety of tactical, operational and strategic initiatives, as well as the consummation of their own acquisitions. As our existing partner firms benefit from these growth initiatives, we continue to focus on acquisitions of new partner firms.

4

Our partnership is comprised of trusted professionals providing comprehensive wealth management services through a largely recurring, fee‑based model, which differentiates our partner firms from the traditional brokerage platforms whose revenues are largely derived from commissions. We derive a substantial majority of our revenues from wealth management fees for investment advice, financial and tax planning, consulting, tax return preparation, family office services and other services. We also generate other revenues from recordkeeping and administration service fees, commissions and distribution fees and outsourced services.

Our Growth Strategy

We believe we are well‑positioned to take advantage of favorable trends in the wealth management industry, including the migration of wealth management professionals from traditional brokerage, commission‑based platforms to a fiduciary, open‑architecture and fee‑based structure. We plan to grow our business through the growth of our existing partner firms and the expansion of our partnership.

Growth of Our Existing Partner Firms

High‑Quality, Growth‑Oriented Partner Firms

Our goal has been and continues to be to acquire high‑quality, entrepreneurial wealth management firms that have built their businesses through a proven track record of growth. We believe that our partner firms will continue to take advantage of the shift in client assets to the RIA space and grow organically through acquisitions of wealth management practices and customer relationships, by attracting new clients, adding new wealth management professionals, increasing client assets from existing clients and through financial market appreciation over time. The economic arrangements put in place at the time of acquisition through our management agreements incentivize the principals of our partner firms to continue executing on their growth plans.

Value‑Added Services

We have a team of over 80 professionals who support our partner firms by providing value‑added services, including marketing and business development support; human resources support, including adviser coaching and development and structuring compensation and incentive models, career path planning and succession planning advice; operational and technology expertise, cash and credit solutions, legal and regulatory support and providing negotiating leverage with vendors. Our value‑added services also include access to our M&A expertise, which facilitates acquisition opportunities for our partner firms through a proactive outreach program, structuring, executing and funding transactions and providing guidance to partner firms to facilitate their integration into our partnership as well as integration of mergers they execute. We assign a relationship leader to each partner firm who is responsible for coordinating our value‑added services to assist that partner firm in accelerating its growth. These services are provided to our partner firms at no additional cost. Our partner firms also have access to our intellectual expertise and partner firm network, which ultimately enhance their operations, enabling them to better serve their clients.

Some of our key value‑added services are described in detail below.

Marketing and Business Development. We offer marketing and business development coaching to our partner firms on topics including referral programs, revenue enhancement measures, communications, website and social media, brand strategy and public relations support. Our marketing team works closely with each of our partner firms to understand their unique value proposition and help them better market themselves to their clients and their centers of influence, including accounting and law firms who serve as potential referral sources. To further support our partner firms, in June 2018 we completed a minority investment in Financial Insight Technology, Inc. (known as SmartAsset), a New York‑based fintech company that connects prospective clients with financial advisers and provides tools to help individuals make more informed financial decisions.

Talent Management. We support the mentoring of next‑generation talent at each of our partner firms through continuous coaching programs that we organize and execute. These programs emphasize key learnings gained from observing top talent across our organization, allowing our firms to benefit from best practices across our talent pool.

5

Compensation Structures and Succession Planning. We help our partner firms align their compensation models to further incentivize their teams. We also facilitate wealth management professional career path planning and advise on principal promotions to the respective management company. These services allow our partner firms to attract and retain the highest quality wealth management professionals. Our acquisition structure facilitates succession planning by maintaining the partner firm and management company as separate entities, thereby allowing for the principals owning the management company to transition over time without disrupting client relationships at the partner firm.

Operations and Technology. We assist partner firms in selecting and implementing third‑party technology solutions that strengthen each firm’s operational performance. Our partner firms can request that our operations team conduct detailed operational assessments to determine their staffing and operating efficiency. Additionally, our operations team provides partner firms negotiating leverage with vendors and cost‑efficient access to third‑party technology.

Cash and Credit Solutions. Through Focus Client Solutions we have created a network of third-party banks and non-bank lenders to provide a competitive array of cash and credit solutions. These alternatives enable our partner firms to proactively help their clients achieve higher yields on cash, as well as unlock home equity and business opportunities through refinancing, commercial lending and other options.

Legal and Regulatory Support. We have an experienced team of legal professionals in place to help support our partner firms in fulfilling their regulatory responsibilities by providing subject matter guidance and expertise. We also have relationships with numerous legal and compliance advisers to help each of our partner firms maintain a robust compliance culture.

Sharing of Best Practices / Collaboration with Other Partner Firms. Our partner firms have access to networking opportunities, best practices roundtable discussions and training seminars. We offer offsite meetings, seminars and other forums for partner firms to learn and adopt best practices. We host partners meetings each year where wealth management professionals from our partner firms have opportunities to meet face to face to collaborate and share ideas. In addition we host periodic summits for chief investment officers, chief compliance officers, chief operating officers, chief financial officers and chief marketing officers, where our partner firms can gather and share specialized expertise and business development practices. Our partner firms are also encouraged to share best practices regularly in order to enhance their collective ability to better serve their clients.

Acquisitions by Our Partner Firms

We are instrumental and support the acquisition of wealth management practices and customer relationships by our partner firms to further expand their businesses. Partner firms pursue acquisitions for a variety of reasons, including geographic expansion, acquisition of new talent and/or specific expertise and succession planning. Acquisitions by our partner firms allow them to add new talent and services to better support their client base while simultaneously capturing synergies from the acquired businesses. We believe there are currently approximately 5,000 firms in the United States that are suitable targets for our partner firms. We have an experienced team of professionals with deep industry relationships to assist in identifying potential acquisition targets for our partner firms. Through our proprietary in‑house sourcing effort, we frequently identify acquisition opportunities for our partner firms. Additionally, many of our partner firms are well‑known in the industry and have developed extensive relationships. In recent years, principals and employees of our partner firms have identified attractive merger candidates, and we believe this trend will continue as our partner firms continue to build scale.

In addition to sourcing opportunities, we are actively involved through each stage of the process to provide legal, financial, tax, compliance and operational expertise to guide our partner firms through the acquisition due diligence process and execution. We provide the funding for acquisitions in the same manner that a parent company would typically fund acquisitions by its subsidiaries.

Our partner firms typically acquire substantially all of the assets of a target firm for cash or a combination of cash and equity and the right to receive contingent consideration. In certain situations, when the acquisition involves a merger with a corporation, and the consideration includes our Class A common stock, Focus Inc. may purchase all of the

6

equity of a target firm and then contribute the assets to our partner firm. In certain instances, our partner firms may acquire only the customer relationships. At the time a partner firm consummates an acquisition, we amend our management agreement with the partner firm to adjust Base Earnings and Target Earnings to reflect the projected post‑acquisition Earnings Before Partner Compensation (“EBPC”) of the partner firm.

Our partner firms completed 15 transactions in 2017, 17 transactions in 2018 and 28 transactions in 2019. With our approval and support, our partner firms may choose to merge with each other as well. Consolidation of our existing partner firms leads to efficiencies and incremental growth in our cash flows. Since January 2017, three partner firms have consummated mergers with other partner firms.

Expansion of Our Partnership

Acquisitions of New Partner Firms

Since inception, a fundamental aspect of our growth strategy has been the acquisition of high‑quality, independent wealth management firms to expand our partnership. We believe that there are approximately 1,000 firms in the United States that are high‑quality targets for future acquisitions. While most of our acquisitions have taken place in the United States, we also see opportunities in several countries where market and regulatory trends toward the fiduciary standard and open‑architecture access mirror those occurring in the United States. We have already begun expansion into the United Kingdom, Canada and Australia.

Our differentiated partnership model and track record have allowed us to grow and enhance our leadership position in the independent wealth management industry.

We are highly selective in choosing our partner firms and conduct extensive financial, legal, tax, operational and business due diligence. We evaluate a variety of criteria including the quality of the wealth management professionals, client characteristics, historical revenues and cash flows, the recurring nature of the revenues, compliance policies and procedures and the alignment of interests between wealth management professionals and clients. We focus on firms with owners who are committed to the long‑term management and growth of their businesses.

With limited exceptions, our partner firm acquisitions have been structured as acquisitions of substantially all of the assets of the firm we choose to partner with but only a portion of the underlying economics in order to align the principals’ interests with our own objectives. To determine the acquisition price, we first estimate the operating cash flow of the business based on current and projected levels of revenue and expense, before compensation and benefits to the selling principals or other individuals who become principals. We refer to the operating cash flow of the business as Earnings Before Partner Compensation or EBPC, and to this EBPC estimate as Target Earnings. In economic terms, we typically purchase 40% to 60% of the partner firm’s EBPC. We refer to the corresponding percentage of Target Earnings on which we base the purchase price as “Base Earnings.” Under a management agreement between our operating subsidiary and the management company and the principals, the management company is entitled to management fees typically consisting of all future EBPC of the acquired wealth management firm in excess of Base Earnings up to Target Earnings, plus a percentage of any EBPC in excess of Target Earnings. Through the management agreement, we create downside protection for ourselves by retaining a cumulative preferred position in Base Earnings.

7

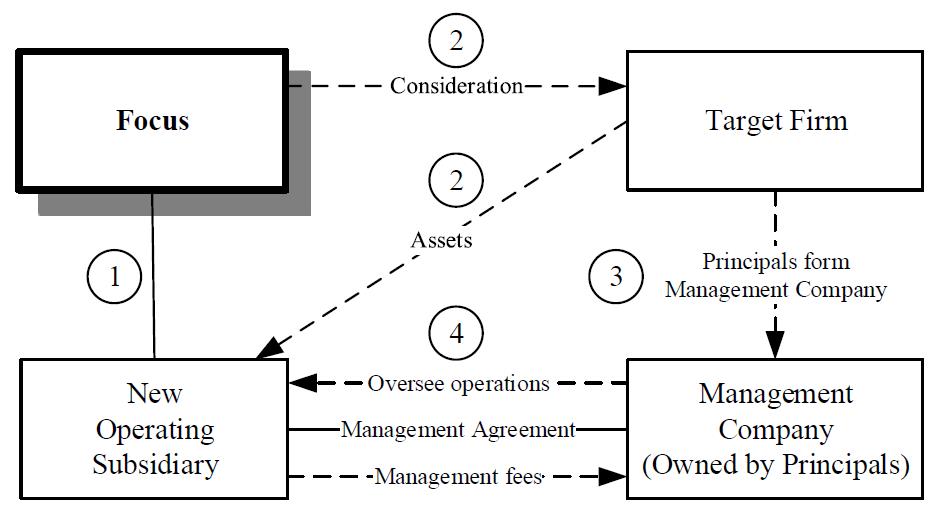

Since 2006, when we began revenue‑generating and acquisition activities, we have grown to a partnership with over 60 partner firms. Acquisitions of partner firms to date have been structured as illustrated below, with limited exceptions. Subsidiary mergers at the partner firm level have been structured differently, and in the future we may structure acquisitions in foreign jurisdictions differently depending on legal and tax considerations.

|

(1) |

Focus LLC forms a wholly owned subsidiary. |

|

(2) |

In exchange for cash or a combination of cash and equity and the right to receive contingent consideration, the new operating subsidiary acquires substantially all of the assets of the target firm, which is owned by the selling principals, and becomes the successor firm. |

|

(3) |

The selling principals form a management company. In addition to the selling principals, the management company may include non‑selling principals who become newly admitted in connection with the acquisition or thereafter. |

|

(4) |

The new operating subsidiary, the principals and the management company enter into a management agreement which typically has an initial term of six years subject to automatic renewals for consecutive one‑year terms, unless earlier terminated by either the management company or us in certain limited situations. Under the management agreement, the management company is entitled to management fees typically consisting of all future EBPC of the new operating subsidiary in excess of Base Earnings up to Target Earnings, plus a percentage of any EBPC in excess of Target Earnings. Pursuant to the management agreement, the management company provides the personnel who conduct the day‑to‑day operations of the new operating subsidiary. Through the management agreement, we create downside protection for ourselves by retaining a cumulative preferred position in each partner firm’s Base Earnings. |

In connection with a typical acquisition, we enter into an acquisition agreement with the target firm and its selling principals pursuant to which we purchase substantially all of the assets of the target firm. The purchase price is a multiple of Base Earnings, which is a percentage of Target Earnings. The purchase price is comprised of a base purchase price and a right to receive contingent consideration in the form of earn out payments. The contingent consideration for acquisitions of new partner firms is generally paid over a six-year period upon the satisfaction of specified growth thresholds in years three and six. These growth thresholds are typically tied to the compounded annual growth rate (“CAGR”) of the partner firm’s earnings. Such growth thresholds can be set annually over the six-year period as well. The contingent consideration for acquisitions made by our partner firms is paid upon the satisfaction of specified financial thresholds, which are typically annual. These thresholds are typically tied to revenue as adjusted for certain criteria or other operating metrics, based on the retention or growth of the business acquired. These arrangements may

8

result in the payment of additional purchase price consideration to the sellers for periods following the closing of an acquisition. Contingent consideration payments are typically payable in cash and, in some cases, equity.

The acquisition agreements contain customary representations and warranties of the parties, and closing is generally conditioned on the delivery of certain ancillary documents, including an executed management agreement, a confidentiality and non‑solicitation agreement, a non‑competition agreement and a notice issued by the acquired firm to its clients notifying them of the acquisition and requesting their consent for the assignment of any agreements to the successor firm.

In connection with the acquisition, management companies and selling principals agree to non‑competition and non‑solicitation provisions of the management agreement, as well as standalone non‑competition and non‑solicitation agreements required by the acquisition agreement. Such non‑competition and non‑solicitation agreements typically have five‑year terms. The non‑competition and non‑solicitation provisions of the management agreement continue during the term of the management agreement and for a period of two years thereafter.

Our partner firms are primarily overseen by the principals who own the management company formed concurrently with the acquisition. Our operating subsidiary, the management company and the principals enter into a long‑term management agreement pursuant to which the management company provides the personnel responsible for overseeing the day‑to‑day operations of the partner firm. The term of the management agreement is generally six years subject to automatic renewals for consecutive one‑year terms, unless earlier terminated by either the management company or us. Subject to applicable cure periods, we may terminate the management agreement upon the occurrence of an event of cause, which may include willful misconduct by the management company or any principal that is reasonably likely to result in a material adverse effect, the failure of the management company to comply with regulatory or other governmental compliance procedures or a material breach of the agreement by the management company or the principals. In some cases, we may have the right to terminate the agreement if any principal ceases to be involved on a full‑time basis in the management of the management company or the performance of services under the agreement. Generally, the management company may terminate the management agreement upon a material breach of the agreement by us and the expiration of the applicable cure period.

This ownership and management structure allows the principals to maintain their entrepreneurial spirit through autonomous day‑to‑day decision making, while gaining access to our extensive resources and preserving the principals’ long‑term economic incentive to continue to grow the business. The management company structure provides both flexibility to us and stability to our partner firms by permitting the principals to continue to build equity value in the management company as the partner firm grows and to control their internal economics and succession plans within the management company.

9

The following table provides an illustrative example of our economics, including management fees earned by the management company, for periods of projected revenues, +10% growth in revenues and −10% growth in revenues. This example assumes (i) Target Earnings of $3.0 million; (ii) Base Earnings acquired of 60% of Target Earnings or $1.8 million; and (iii) a percentage of earnings in excess of Target Earnings retained by the management company of 40%.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Projected |

|

+10% Growth |

|

−10% Growth |

|

|||

|

|

|

|

Revenues |

|

in Revenues |

|

in Revenues |

|

|||

|

|

|

|

(in thousands) |

|

|||||||

|

|

New Partner Firm |

|

|

|

|

|

|

|

|

|

|

|

|

New partner firm revenues |

|

$ |

5,000 |

|

$ |

5,500 |

|

$ |

4,500 |

|

|

|

Less: |

|

|

|

|

|

|

|

|

|

|

|

|

Operating expenses (excluding management fees) |

|

|

(2,000) |

|

|

(2,000) |

|

|

(2,000) |

|

|

|

EBPC |

|

$ |

3,000 |

|

$ |

3,500 |

|

$ |

2,500 |

|

|

|

Base Earnings to Focus Inc. (60%) |

|

|

1,800 |

|

|

1,800 |

|

|

1,800 |

|

|

|

Management fees to management company (40%) |

|

|

1,200 |

|

|

1,200 |

|

|

700 |

|

|

|

EBPC in excess of Target Earnings: |

|

|

|

|

|

|

|

|

|

|

|

|

To Focus Inc. (60%) |

|

|

— |

|

|

300 |

|

|

— |

|

|

|

To management company as management fees (40%) |

|

|

— |

|

|

200 |

|

|

— |

|

|

|

Focus Inc. |

|

|

|

|

|

|

|

|

|

|

|

|

Focus Inc. revenues |

|

$ |

5,000 |

|

$ |

5,500 |

|

$ |

4,500 |

|

|

|

Less: |

|

|

|

|

|

|

|

|

|

|

|

|

Operating expenses (excluding management fees) |

|

|

(2,000) |

|

|

(2,000) |

|

|

(2,000) |

|

|

|

Less: |

|

|

|

|

|

|

|

|

|

|

|

|

Management fees to management company |

|

|

(1,200) |

|

|

(1,400) |

|

|

(700) |

|

|

|

Operating income |

|

$ |

1,800 |

|

$ |

2,100 |

|

$ |

1,800 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In certain circumstances, the structure of our relationship with partner firms may differ from the typical structure described above. In addition, our future international acquisitions may not be structured like our typical partner firm acquisitions. For example, the structure of our ownership interests in non‑U.S. partner firms may differ from the way in which we own our U.S. partner firms.

Lift Outs of Established Wealth Management Professionals

From time to time, through Focus Independence, we offer teams of wealth management professionals at traditional brokerage firms and wirehouses with attractive track records and books of business the opportunity to establish their own independent wealth management firm and ultimately join our partnership as a new partner firm. This program gives these professionals the opportunity to build a business largely unencumbered by the conflicts of interest they face at traditional brokerage firms and wirehouses and with more favorable economics. Focus Independence is a targeted approach to lift out teams of wealth management professionals from traditional brokerage firms and wirehouses with attractive track records and books of business and make them entrepreneurs within our partnership. The program has been successful, with the substantial majority of ultra‑high net worth and high net worth clients retained by the newly formed partner firm. We have completed 14 acquisitions of new partner firms through Focus Independence.

We work with each team of wealth management professionals to establish a new RIA business and provide consultation as needed on virtually everything needed to transition to and operate the new RIA as a full‑service firm, including technology, personnel and office space. With many teams, we enter into an option agreement, which provides us with the option to acquire substantially all of the assets of the RIA 12 to 13 months after the team’s resignation date from the brokerage firm or wirehouse. The option agreement provides a purchase price formula, typically equal to a multiple of the portion of the new RIA’s run-rate EBPC at the time of acquisition closing. The option agreement also

10

establishes the portion of the purchase price to be paid in cash and equity. Transactions with teams where we do not enter into an option agreement may be structured more like a typical acquisition.

Our Partner Firms

Our partner firms provide comprehensive wealth management services to ultra‑high net worth and high net worth individuals and families, as well as business entities, under a largely recurring, fee‑based model. Our partner firms provide these services across a diverse range of investment styles, asset classes and clients. The substantial majority of our partner firms are RIAs, and certain of our partner firms also have affiliated broker‑dealers and/or insurance brokers. Several of our partner firms and their principals have been recognized as leading wealth management firms and advisers by financial publications such as Barron’s, The Financial Times and Forbes.

Our partner firms derive a substantial majority of their revenues from wealth management fees for investment advice, financial and tax planning, consulting, tax return preparation, family office services and other services. Wealth management fees are primarily based either on a contractual percentage of the client assets, a flat fee, an hourly rate or a combination of such fees and are billed either in advance or arrears on a monthly, quarterly or semiannual basis. We also generate other revenue from recordkeeping and administration service fees, commissions and distribution fees and outsourced services.

We currently have over 60 partner firms. All of our partner firm acquisitions have been paid for with cash or a combination of cash and equity and the right to receive contingent consideration. We have to date, with limited exceptions, acquired substantially all of the assets of the firms we choose to partner with and have assumed only post‑closing contractual obligations, not any material existing liabilities.

11

The following is a list of our partner firms as of February 25, 2020:

|

|

|

|

|

Joined through |

|

Acquisition(s) |

|

|

|

Partner |

|

Focus |

|

Completed by |

|

Partner Firm |

|

Firm Since |

|

Independence |

|

Partner Firm |

|

|

|

2006 |

|

|

|

|

|

StrategicPoint |

|

January |

|

|

|

|

|

HoyleCohen |

|

May |

|

|

|

|

|

|

|

2007 |

|

|

|

|

|

Sentinel Benefits & Financial Group |

|

January |

|

|

|

|

|

Buckingham |

|

February |

|

|

|

|

|

Benefit Financial Services Group |

|

March |

|

|

|

|

|

JFS Wealth Advisors |

|

August |

|

|

|

|

|

Atlas Private Wealth Management |

|

September |

|

|

|

|

|

GW & Wade |

|

September |

|

|

|

|

|

|

|

2008 |

|

|

|

|

|

Greystone |

|

April |

|

|

|

|

|

WESPAC |

|

July |

|

|

|

|

|

|

|

2009 |

|

|

|

|

|

Joel Isaacson & Co. |

|

November |

|

|

|

|

|

Coastal Bridge Advisors |

|

December |

|

|

|

|

|

|

|

2010 |

|

|

|

|

|

Pettinga |

|

December |

|

|

|

|

|

|

|

2011 |

|

|

|

|

|

Sapient Private Wealth Management |

|

September |

|

|

|

|

|

The Colony Group |

|

October |

|

|

|

|

|

LVW Advisors |

|

October |

|

|

|

|

|

|

|

2012 |

|

|

|

|

|

Vestor Capital |

|

October |

|

|

|

|

|

Merriman |

|

December |

|

|

|

|

|

The Portfolio Strategy Group |

|

December |

|

|

|

|

|

|

|

2013 |

|

|

|

|

|

LaFleur & Godfrey |

|

August |

|

|

|

|

|

Telemus Capital |

|

August |

|

|

|

|

|

|

|

2014 |

|

|

|

|

|

Summit Financial |

|

April |

|

|

|

|

|

Flynn Family Office |

|

June |

|

|

|

|

|

Gratus Capital |

|

October |

|

|

|

|

|

Strategic Wealth Partners |

|

November |

|

|

|

|

|

|

|

2015 |

|

|

|

|

|

IFAM Capital |

|

February |

|

|

|

|

|

Dorchester Wealth Management |

|

April |

|

|

|

|

|

The Fiduciary Group |

|

April |

|

|

|

|

|

Quadrant Private Wealth |

|

July |

|

|

|

|

|

Relative Value Partners |

|

July |

|

|

|

|

|

Fort Pitt Capital Group |

|

October |

|

|

|

|

|

Patton Albertson Miller Group |

|

October |

|

|

|

|

|

|

|

2016 |

|

|

|

|

|

Douglas Lane & Associates |

|

January |

|

|

|

|

|

Kovitz Investment Group Partners |

|

January |

|

|

|

|

|

Waddell & Associates |

|

April |

|

|

|

|

|

Transform Wealth |

|

April |

|

|

|

|

|

GYL Financial Synergies |

|

August |

|

|

|

|

|

XML Financial Group |

|

October |

|

|

|

|

|

|

|

2017 |

|

|

|

|

|

Crestwood Advisors |

|

January |

|

|

|

|

|

CFO4Life |

|

February |

|

|

|

|

|

One Charles Private Wealth |

|

February |

|

|

|

|

|

Bordeaux Wealth Advisors |

|

March |

|

|

|

|

|

Gelfand, Rennert & Feldman |

|

April |

|

|

|

|

|

Lake Street Advisors |

|

April |

|

|

|

|

|

Financial Professionals |

|

May |

|

|

|

|

|

SCS Financial Services |

|

July |

|

|

|

|

|

Brownlie & Braden |

|

July |

|

|

|

|

|

Eton Advisors |

|

September |

|

|

|

|

|

|

|

2018 |

|

|

|

|

|

Cornerstone Wealth |

|

January |

|

|

|

|

|

Fortem Financial |

|

February |

|

|

|

|

|

Bartlett Wealth Management |

|

April |

|

|

|

|

|

Campbell Deegan Financial |

|

April |

|

|

|

|

|

Nigro, Karlin, Segal, Feldstein & Bolno (NKSFB) |

|

April |

|

|

|

|

|

TrinityPoint Wealth |

|

May |

|

|

|

|

|

Asset Advisors Investment Management |

|

July |

|

|

|

|

|

Edge Capital Group |

|

August |

|

|

|

|

|

Vista Wealth Management |

|

August |

|

|

|

|

|

|

|

2019 |

|

|

|

|

|

Altman, Greenfield & Selvaggi |

|

January |

|

|

|

|

|

Prime Quadrant |

|

February |

|

|

|

|

|

Foster, Dykema & Cabot |

|

March |

|

|

|

|

|

Escala Partners |

|

April |

|

|

|

|

|

Sound View Wealth Advisors |

|

April |

|

|

|

|

|

Williams Jones |

|

August |

|

|

|

|

|

|

|

2020 |

|

|

|

|

|

Nexus Investment Management |

|

February |

|

|

|

|

|

|

|

|

|

|

|

|

12

The following shows certain of the value‑added services we have provided to our partner firms through February 25, 2020:

|

|

|

Value‑Added Services |

||||||||

|

|

|

|

|

Operational |

|

|

|

|

|

|

|

|

|

Marketing and |

|

and |

|

Legal and |

|

|

|

|

|

|

|

Business |

|

Technology |

|

Compliance |

|

Talent |

|

Succession |

|

Partner Firm |

|

Development |

|

Enhancements |

|

Support |

|

Management |

|

Planning |

|

StrategicPoint |

|

|

|

|

|

|

|

|

|

|

|

HoyleCohen |

|

|

|

|

|

|

|

|

|

|

|

Sentinel Benefits & Financial Group |

|

|

|

|

|

|

|

|

|

|

|

Buckingham |

|

|

|

|

|

|

|

|

|

|

|

Benefit Financial Services Group |

|

|

|

|

|

|

|

|

|

|

|

JFS Wealth Advisors |

|

|

|

|

|

|

|

|

|

|

|

Atlas Private Wealth Management |

|

|

|

|

|

|

|

|

|

|

|

GW & Wade |

|

|

|

|

|

|

|

|

|

|

|

Greystone |

|

|

|

|

|

|

|

|

|

|

|

WESPAC |

|

|

|

|

|

|

|

|

|

|

|

Joel Isaacson & Co. |

|

|

|

|

|

|

|

|

|

|

|

Coastal Bridge Advisors |

|

|

|

|

|

|

|

|

|

|

|

Pettinga |

|

|

|

|

|

|

|

|

|

|

|

Sapient Private Wealth Management |

|

|

|

|

|

|

|

|

|

|

|

The Colony Group |

|

|

|

|

|

|

|

|

|

|

|

LVW Advisors |

|

|

|

|

|

|

|

|

|

|

|

Vestor Capital |

|

|

|

|

|

|

|

|

|

|

|

Merriman |

|

|

|

|

|

|

|

|

|

|

|

The Portfolio Strategy Group |

|

|

|

|

|

|

|

|

|

|

|

LaFleur & Godfrey |

|

|

|

|

|

|

|

|

|

|

|

Telemus Capital |

|

|

|

|

|

|

|

|

|

|

|

Summit Financial |

|

|

|

|

|

|

|

|

|

|

|

Flynn Family Office |

|

|

|

|

|

|

|

|

|

|

|

Gratus Capital |

|

|

|

|

|

|

|

|

|

|

|

Strategic Wealth Partners |

|

|

|

|

|

|

|

|

|

|

|

IFAM Capital |

|

|

|

|

|

|

|

|

|

|

|

Dorchester Wealth Management |

|

|

|

|

|

|

|

|

|

|

|

The Fiduciary Group |

|

|

|

|

|

|

|

|

|

|

|

Quadrant Private Wealth |

|

|

|

|

|

|

|

|

|

|

|

Relative Value Partners |

|

|

|

|

|

|

|

|

|

|

|

Fort Pitt Capital Group |

|

|

|

|

|

|

|

|

|

|

|

Patton Albertson Miller Group |

|

|

|

|

|

|

|

|

|

|

|

Douglas Lane & Associates |

|

|

|

|

|

|

|

|

|

|

|

Kovitz Investment Group Partners |

|

|

|

|

|

|

|

|

|

|

|

Waddell & Associates |

|

|

|

|

|

|

|

|

|

|

|

Transform Wealth |

|

|

|

|

|

|

|

|

|

|

|

GYL Financial Synergies |

|

|

|

|

|

|

|

|

|

|

|

XML Financial Group |

|

|

|

|

|

|

|

|

|

|

|

Crestwood Advisors |

|

|

|

|

|

|

|

|

|

|

|

CFO4Life |

|

|

|

|

|

|

|

|

|

|

|

One Charles Private Wealth |

|

|

|

|

|

|

|

|

|

|

|

Bordeaux Wealth Advisors |

|

|

|

|

|

|

|

|

|

|

|

Gelfand, Rennert & Feldman |

|

|

|

|

|

|

|

|

|

|

|

Lake Street Advisors |

|

|

|

|

|

|

|

|

|

|

|

Financial Professionals |

|

|

|

|

|

|

|

|

|

|

|

SCS Financial Services |

|

|

|

|

|

|

|

|

|

|

|

Brownlie & Braden |

|

|

|

|

|

|

|

|

|

|

|

Eton Advisors |

|

|

|

|

|

|

|

|

|

|

|

Cornerstone Wealth |

|

|

|

|

|

|

|

|

|

|

|

Fortem Financial |

|

|

|

|

|

|

|

|

|

|

|

Bartlett Wealth Management |

|

|

|

|

|

|

|

|

|

|

|

Campbell Deegan Financial |

|

|

|

|

|

|

|

|

|

|

|

Nigro, Karlin, Segal, Feldstein, & Bolno (NKSFB) |

|

|

|

|

|

|

|

|

|

|

|

TrinityPoint Wealth |

|

|

|

|

|

|

|

|

|

|

|

Asset Advisors Investment Management |

|

|

|

|

|

|

|

|

|

|

|

Edge Capital Group |

|

|

|

|

|

|

|

|

|

|

|

Vista Wealth Management |

|

|

|

|

|

|

|

|

|

|

|

Altman, Greenfield & Selvaggi |

|

|

|

|

|

|

|

|

|

|

|

Prime Quadrant |

|

|

|

|

|

|

|

|

|

|

|

Foster, Dykema & Cabot |

|

|

|

|

|

|

|

|

|

|

|

Escala Partners |

|

|

|

|

|

|

|

|

|

|

|

Sound View Wealth Advisors |

|

|

|

|

|

|

|

|

|

|

|

Williams Jones |

|

|

|

|

|

|

|

|

|

|

|

Nexus Investment Management |

|

|

|

|

|

|

|

|

|

|

13

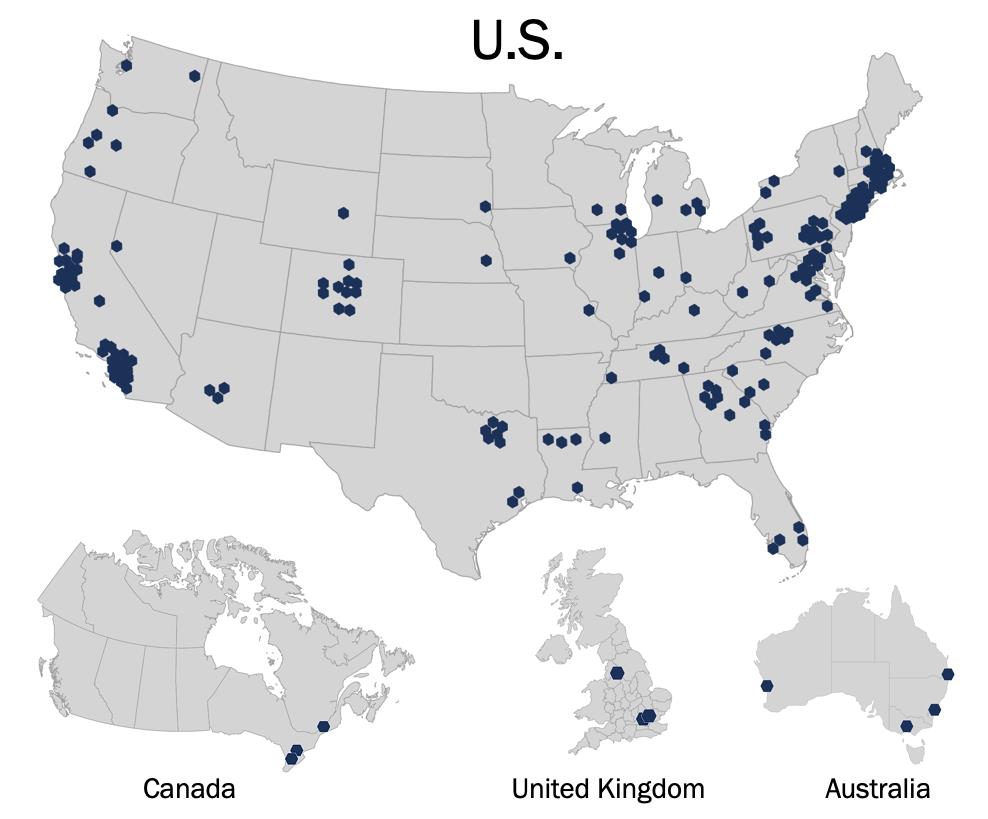

Our partner firms are primarily located in the United States. In addition, we have one partner firm, Greystone, in the United Kingdom, two partner firms, Dorchester Wealth Management and Prime Quadrant, in Canada and two partner firms, Escala Partners and Financial Professionals, in Australia. The following table shows our domestic and international revenues for the years ended December 31, 2017, 2018 and 2019:

|

|

|

Year Ended December 31, |

|

|||||||||||||

|

|

|

2017 |

|

2018 |

|

2019 |

|

|||||||||

|

|

|

(dollars in thousands) |

|

|||||||||||||

|

Domestic revenue |

|

$ |

643,077 |

|

97.0 |

% |

$ |

889,166 |

|

97.6 |

% |

$ |

1,170,169 |

|

96.0 |

% |

|

International revenue |

|

|

19,810 |

|

3.0 |

% |

|

21,714 |

|

2.4 |

% |

|

48,172 |

|

4.0 |

% |

|

Total revenue |

|

$ |

662,887 |

|

100.0 |

% |

$ |

910,880 |

|

100.0 |

% |

$ |

1,218,341 |

|

100.0 |

% |

In February 2020, we acquired an additional partner firm in Canada, Nexus Investment Management.

The maps below show the locations of our partner firms as of February 25, 2020. The majority of our partner firms operate multiple offices and in multiple states.

Upon joining our partnership, each partner firm transitions its operations to our common general ledger, payroll and cash management systems. Our common general ledger system provides us access to financial information of each partner firm and is designed to accommodate the varied needs of each individual business. We control payroll and payment of management fees for partner firms through a common disbursement process. The common payroll system allows us to effectively monitor compensation, new hires, terminations and other personnel changes. We employ a cash management system under which cash held by partner firms above a threshold is transferred into our centralized accounts. The cash management system enables us to control and secure our cash flow and more efficiently monitor partner firm earnings and financial position.

14

We and our partner firms devote substantial time and effort to remaining current on, and addressing, regulatory and compliance matters. Each of our registered partner firms has its own chief compliance officer and has established a compliance program to help detect and prevent compliance violations.

While the chief compliance officers at our partner firms are principally responsible for maintaining their respective compliance programs and for tailoring them to the specifics of their partner firms’ businesses, we have an experienced team of legal professionals in place at the holding company to support our partner firms in fulfilling their regulatory responsibilities by providing additional guidance and expertise. We collaborate with each of our partner firms in its completion of an annual compliance risk assessment, which is conducted by an outside law firm or a compliance consulting firm. We also engage third‑party firms to conduct periodic cybersecurity audits and help coordinate completion of certain other employee training. We also monitor how our partner firms address risk assessment recommendations and regulatory exam findings. We also work with our partner firms to assist them in identifying qualified legal and compliance advisers by leveraging our extensive relationships.

Competition

The wealth management industry is very competitive. We compete with a broad range of wealth management firms, including public and privately held investment advisers, traditional brokerage firms and wirehouses, firms associated with securities broker‑dealers, financial institutions, private equity firms and insurance companies. We believe that important factors affecting our partner firms’ ability to compete for clients include the ability to attract and retain key wealth management professionals, investment performance, wealth management fee rates, the quality of services provided to clients, the depth and continuity of client relationships, adherence to the fiduciary standard and reputation.

We strategically built a leading partnership of independent, fiduciary wealth management firms led by entrepreneurs through a unique, disciplined and proven acquisition strategy. Our differentiated partnership model has allowed us to grow and enhance our leadership position in the wealth management industry. As we continue our growth strategy of acquiring high‑quality partner firms, we believe that important factors affecting our ability to compete for future acquisitions include:

|

· |

the degree to which target wealth management firms view our partnership model as preferable, financially and operationally or otherwise, to acquisition or other arrangements offered by other potential purchasers; |

|

· |

the reputation and performance of our existing and future partner firms, by which target wealth management firms may judge us and our future prospects; and |

|

· |

the quality and breadth of our value‑added services. |

Employees

As of December 31, 2019, we had over 3,400 employees, 83 of whom were employed at the holding company.

Additionally, as of December 31, 2019, there were over 500 principals who were part of the management companies that oversaw partner firms and were not our employees.

Trademarks

We own many registered trademarks and service marks in the United States. We believe the Focus Financial Partners name and the many distinctive marks associated with it are of significant value and are very important to our business. Accordingly, as a general policy, we monitor the use of our marks and vigorously oppose any unauthorized use of them.

We register some of our copyrighted material and otherwise rely on common law protection of our copyrighted materials, but these are not material to our business.

15

Available Information

We are required to file annual, quarterly and current reports, proxy statements and certain other information with the SEC. The SEC maintains a website at www.sec.gov that contains reports, proxy and information statements and other information regarding registrants that file electronically with the SEC. Any documents filed by us with the SEC, including this Annual Report, can be downloaded from the SEC’s website.

We also make available free of charge through our website, www.focusfinancialpartners.com, electronic copies of certain documents that we file with the SEC, including our Annual Reports on Form 10‑K, Quarterly Reports on Form 10‑Q, Current Reports on Form 8‑K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC.

Regulatory Environment

Existing Regulation

Our partner firms are subject to extensive regulation in the United States. In addition, Greystone, Dorchester, Prime Quadrant, Nexus Investment Management, Financial Professionals and Escala are subject to extensive regulation in the United Kingdom, Canada and Australia, as applicable. In the United States, our partner firms are subject to regulation primarily at the federal level, including regulation by the SEC under the Advisers Act, by the U.S. Department of Labor (the “DOL”) under the Employee Retirement Income Security Act of 1974, as amended (“ERISA”), and by the SEC and the Financial Industry Regulatory Authority (“FINRA”) for our partner firm subsidiaries that are broker‑dealers. Our partner firms may also be subject to regulation by state regulators for insurance and several other aspects of our partner firms’ activities. Outside of the United States, Greystone is primarily regulated by the Financial Conduct Authority in the United Kingdom, Dorchester, Prime Quadrant and Nexus Investment Management are primarily regulated by the securities regulators of Canada’s provinces, and Financial Professionals and Escala are primarily regulated by the Australian Securities & Investments Commission (“ASIC”).

Our U.S. based partner firms that are investment advisers are registered with the SEC under the Advisers Act. The Advisers Act imposes numerous obligations on RIAs, including fiduciary duties, compliance and disclosure obligations, recordkeeping requirements and operational requirements. Certain of our partner firms sponsor unregistered and registered funds in the United States and certain foreign jurisdictions. These activities subject those partner firms to additional regulatory requirements in those jurisdictions. In addition, many state securities commissions impose filing requirements on investment advisers that operate or have places of business in their states. Similarly, many states require certain client facing employees of RIAs and FINRA‑registered broker‑dealers to become state-licensed.

Certain of our partner firms have affiliated SEC registered broker‑dealers for the purpose of distributing funds or other securities products or facilitating securities transactions. Broker‑dealers and their personnel are regulated, to a large extent, by the SEC and self‑regulatory organizations, principally FINRA. In addition, state regulators have supervisory authority over broker‑dealer activities conducted in their states. Broker‑dealers are subject to regulations which cover virtually all aspects of their business, including sales practices, trading practices, use and safekeeping of clients’ funds and securities, recordkeeping and the conduct of directors, officers, employees and representatives. Broker‑dealers are also subject to net capital rules that mandate that they maintain certain levels of capital. Certain partner firms have employees who are registered representatives with either affiliated or unaffiliated broker‑dealers.

Certain of our partner firms have licensed insurance affiliates. State insurance laws grant state insurance regulators broad administrative powers. These supervisory agencies regulate many aspects of the insurance business, including the licensing of insurance brokers and agents and other insurance intermediaries, and trade practices such as marketing, advertising and compensation arrangements entered into by insurance brokers and agents.

Our partner firms are also subject to regulation by the DOL under ERISA and related regulations with respect to investment advisory and management services provided to participants in retirement plans covered by ERISA and subject to regulation by the Internal Revenue Service (“IRS”) with respect to individual retirement accounts (“IRAs”)

16

pursuant to comparable provisions within the Internal Revenue Code (“IRC”). Among other requirements, ERISA and the IRC imposes duties on persons who are fiduciaries under ERISA and the IRC, respectively, and prohibit certain transactions involving related parties.

Additionally, we and our partner firms are subject to various state, federal and international data privacy and cybersecurity laws designed to protect client and employee personally identifiable information. These laws and regulations are increasing in complexity and number, which has resulted in greater compliance risk and cost for us. The unauthorized access, use, theft or destruction of client or employee personal, financial or other data could expose us to potential financial penalties and legal liability.

Additional Regulatory Reform

Our partner firms are subject to the numerous regulatory reform initiatives in the United States and in international jurisdictions where they operate. New laws or regulations, or changes in enforcement of existing laws or regulations, could have a material and adverse impact on the scope or profitability of our partner firms’ business activities or require us and/or our partner firms to change business practices and incur additional costs as well as potential reputational harm.

As examples, on June 5, 2019, the SEC adopted a package of rulemakings and interpretations that impose a best interest standard of conduct for broker‑dealers, requires investment advisers and broker-dealers to deliver short‑form disclosure documents to retail investors and clarifies the SEC’s views on the fiduciary duty that investment advisers owe to their clients. Our partner firms are developing their required short-form disclosure document by the June 30, 2020 compliance date. The impact of other elements of the rulemakings and interpretations on our partner firms and the industry is unclear at this time.

On November 4, 2019, the SEC proposed new rules regarding investment adviser advertisements and payments to solicitors. These proposed rules, if adopted, would largely replace the current advertising rules’ broad prohibitions and limitations with principles-based regulation. The rules would also extend the current solicitation rule to cover non-cash as well as cash compensation. While initially the impact of these rules appears positive for the business of our partner firms, the ultimate impact will be uncertain until any final rules are adopted and fully implemented.

On February 1, 2019, a Royal Commission in Australia issued a highly publicized report following a 12‑month inquiry of misconduct in the banking, superannuation and financial services industry. The report makes many recommendations that, if adopted into law or regulations, could impact our existing or any future Australian partner firms or investments. Some of the regulations include a new system of registration for financial advisers to be overseen by a new regulatory body and the repeal of carve‑outs and grandfathering of certain conflicted remuneration prohibitions.

In December 2019, the Canadian Securities Administrators adopted amendments to National Instrument 31-103 and its related Companion Policy which will impose new heightened requirements on our Canadian partner firms with respect to conflicts of interest, know your client, know your product and suitability obligations. In addition, in December 2019, our U.K. wealth management partner firm became subject to the new Senior Managers and Certification Regime which provides for additional firm and individual responsibilities and enhanced oversight by the U.K. Financial Conduct Authority.

Of the many data privacy and cybersecurity laws being enacted or considered, the California Consumer Privacy Act became effective on January 1, 2020. This act requires certain partner firms to review and enhance their governance regarding the collection and categorizing of certain personal information. They were also required to develop procedures to respond to consumer requests to be informed of their personal information that is collected and to have such information deleted if desired, among other elements.

In addition, financial regulators are increasing their enforcement and examination attention across a wide range of activities and business practices, including disclosure, conflicts of interest, cybersecurity, business continuity and succession planning. Such enhanced scrutiny may increase the likelihood of enforcement actions or violation findings, or

17

cause us or our partner firms to change business practices or incur additional costs. It is also not possible to predict how such changes may impact the businesses of our competitors and the competitive dynamics of the industry.

You should carefully consider the information in this Annual Report and the following risks. Our business, financial condition and results of operations could be materially and adversely affected by any of these risks. The risks described below are not the only ones facing us. Additional risks not presently known to us or which we consider immaterial also may adversely affect us.

Risks Related to Capital Markets and Competition

Our financial results largely depend on wealth management fees received by our partner firms, which are impacted by market fluctuations.