Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF MALONEBAILEY, LLC - ALPINE 4 HOLDINGS, INC. | exh23_1.htm |

| EX-21 - SUBSIDIARIES OF THE COMPANY - ALPINE 4 HOLDINGS, INC. | exh21.htm |

Registration No. 333-_________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Alpine 4 Technologies Ltd.

(Exact name of registrant as specified in its charter)

|

Delaware

|

3669

|

46-5482689

|

|

(State or other jurisdiction of incorporation or organization)

|

(Primary Standard Industrial Classification Code Number)

|

(I.R.S. Employer Identification Number)

|

|

2525 E Arizona Biltmore Circle Suite 237

|

|

Phoenix, AZ

|

855-777-0077 ext 801

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive

Offices)

Kent Wilson

Alpine 4 Technologies Ltd.

4742 N. 24th Street, Suite 300

Phoenix AZ 85016

855-777-0077 ext 801

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

C. Parkinson Lloyd, Esq.

Kirton | McConkie

50 East South Temple Street, Suite 400

Salt Lake City, UT 84111

(801) 328-3600

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after

this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following

box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the

Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of

the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of

the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

◻

|

Accelerated filer

|

◻

|

|

Non-accelerated filer

|

⌧

|

Smaller reporting company

|

⌧

|

|

Emerging Growth Company

|

⌧

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to be Registered

|

Amount

to be

Registered

|

Proposed

Maximum

Offering Price

Per Share

|

Proposed

Maximum

Aggregate

Offering Price

|

Amount of

Registration Fee

|

||||||||||||

|

Class A Common stock, par value $0.0001 per share

|

14,000,000

|

(1)

|

$ |

0.0773

|

|

$ |

1,082,200

|

(2)

|

$ |

141

|

|

|||||

(1) Pursuant to Rule 416 of the Securities Act of 1933, as amended (the “Securities Act”), this registration statement also covers any additional shares of common stock that become issuable by reason of any share dividend, share

split, recapitalization or any other similar transaction without receipt of consideration that results in an increase in the number of shares or common stock outstanding.

(2) Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(c) of the Securities Act based on the average of the high and low prices of the Registrant’s Common

Stock on February 10, 2020, as quoted on the OTCQB Market.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until

the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become

effective on such date as the Commission acting pursuant to said Section 8(a) may determine.

The information in this prospectus is not complete and may be changed. The selling stockholder may not sell these

securities until the Securities and Exchange Commission declares this registration statement effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or

sale is not permitted.

|

PRELIMINARY PROSPECTUS

|

SUBJECT TO COMPLETION

|

DATED FEBRUARY ___, 2020

|

This prospectus relates to the resale or other disposition from time to time of up to 14,000,000 shares of common stock, par value $0.0001, of Alpine 4

Technologies, Ltd., by Lincoln Park Capital Fund, LLC (“Lincoln Park”).

The shares of common stock being offered by Lincoln Park, the selling stockholder, have been or may be issued pursuant to the purchase agreement dated

January 16, 2020, that we entered into with Lincoln Park. See “The Lincoln Park Transaction” for a description of that agreement and “Selling Stockholder” for additional information regarding Lincoln Park. The prices at which Lincoln Park may sell

the shares will be determined by the prevailing market price for the shares or in negotiated transactions.

We are not selling any securities under this prospectus and will not receive any of the proceeds from the sale of shares by the selling stockholder.

The selling stockholder may sell or otherwise dispose of the shares of common stock described in this prospectus in a number of different ways and at

varying prices. See “Plan of Distribution” for more information about how the selling stockholder may sell or otherwise dispose of the shares of common stock being registered pursuant to this prospectus. The selling stockholder is an “underwriter”

within the meaning of Section 2(a)(11) of the Securities Act of 1933, as amended.

The selling stockholder will pay all brokerage fees and commissions and similar expenses. We will pay the expenses (except brokerage fees and commissions

and similar expenses) incurred in registering the shares, including legal and accounting fees. See “Plan of Distribution.”

Our common stock is quoted on the OTCQB Market under the symbol “ALPP.” On February 10, 2020, the last reported sale of our common stock on the OTCQB

Market was $0.0756 per share.

Investing in our common stock involves a high degree of Risk.

See "Risk Factors" beginning on page ____.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy

or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read the entire prospectus and any

amendments or supplements carefully before you make your investment decision.

The date of this prospectus is ______________, 2020.

2

TABLE OF CONTENTS

| Page | |

|

Prospectus Summary

|

4

|

|

Risk Factors

|

9

|

|

Cautionary Note Regarding Forward Looking Statements

|

16

|

|

Determination of Market Price

|

17

|

|

Use of Proceeds

|

17

|

|

Dividend Policy

|

18

|

|

Lincoln Park Transaction

|

18

|

|

Dilution

|

21

|

|

Market Price of Common Equity and Related Stockholder Matters

|

22

|

|

Business

|

23

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

27

|

|

Management

|

34

|

|

Security Ownership of Certain Beneficial Owners and Management

|

37

|

|

Certain Relationships and Related Transactions

|

38

|

|

Description of Securities

|

39

|

|

Selling Stockholder

|

44

|

|

Plan of Distribution

|

45

|

|

Legal Matters

|

46

|

|

Experts

|

46

|

|

Where You Can Find More Information

|

46

|

|

Index to Financial Statements

|

F-1

|

3

ABOUT THIS PROSPECTUS

The registration statement of which this prospectus forms a part that we have filed with the Securities and Exchange Commission, or SEC, includes exhibits that provide more detail of the matters

discussed in this prospectus. You should read this prospectus and the related exhibits filed with the SEC, together with the additional information described under the heading “Where You Can Find More Information” before making your investment

decision.

You should rely only on the information provided in this prospectus or in a prospectus supplement or any free writing prospectuses or amendments thereto. Neither we, nor the Selling Stockholder, have

authorized anyone else to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. You should assume that the information in this prospectus is accurate only as of the date

hereof. Our business, financial condition, results of operations and prospects may have changed since that date.

Neither we, nor the Selling Stockholder, are offering to sell or seeking offers to purchase these securities in any jurisdiction where the offer or sale is not permitted. We have not done anything that would permit this

offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform

themselves about, and observe any restrictions relating to, the offering of the securities as to distribution of the prospectus outside of the United States.

4

ROSPECTUS SUMMARY

The following summary highlights selected information contained in this prospectus. This

summary does not contain all the information you should consider before investing in our common stock. You should read the entire prospectus carefully, including the "Risk Factors" beginning on page 5, and our financial statements and the notes to

the financial statements included elsewhere in this prospectus. As used throughout this prospectus, the terms "Alpine 4," "Company," "we," "us," or "our" refer to Alpine 4 Technologies Ltd.

General

Company Background and History

Alpine 4 Technologies Ltd. (“Alpine 4,” the “Company,” “we,” or “our”) was incorporated under the laws of the State of Delaware on April 22, 2014. The

Company was formed to serve as a vehicle to effect an asset acquisition, merger, exchange of capital stock, or other business combination with a domestic or foreign business. As of the date this Registration Statement was filed, the Company was a

holding company that owned six operating subsidiaries: ALTIA, LLC; Quality Circuit Assembly, Inc.; American Precision Fabricators, Inc.; Morris Sheet Metal, Corp; JTD Spiral, Inc.; and Deluxe Sheet Metal, Inc. (As discussed in more detail below, we

previously had an additional subsidiary, Venture West Energy Services (formerly Horizon Well Testing, LLC) (“Venture West”). However, as of December 31, 2018, we discontinued operations on Venture West and in February 2019 Venture West filed for

Chapter 7 bankruptcy proceedings. As of March 31, 2019, Venture West’s bankruptcy was completed.

Alpine 4 maintains our corporate office located at 2525 E. Arizona Biltmore Circle, Suite C237, Phoenix, Arizona 85016. ALTIA works out of the headquarters

offices. QCA rents a location at 1709 Junction Court #380 San Jose, California 95112. American Precision Fabricators rents a property 4401 Savannah St. Fort Smith, Arkansas 72903. Deluxe Sheet Metal’s facilities

are located at 6661 Lonewolf Dr, South Bend, Indiana 46628. Morris Sheet Metal and JTD Spiral are located at 6212 Highview Dr, Fort Wayne, Indiana 46818.

Who We Are

Alexander Hamilton, in his “Federalist paper #11,” said that our adventurous spirit distinguishes the commercial character of

America. Hamilton knew that our freedom to be creative gave American businesses a competitive advantage over the rest of the world. We believe that Alpine 4 also exemplifies this spirit in our subsidiaries and that our greatest competitive

advantage is our highly diverse business structure combined with a culture of collaboration.

It is our mandate to grow Alpine 4 into a leading, multi-faceted holding company with diverse subsidiary holdings with products and

services that not only benefit from one another as a whole, but also have the benefit of independence. This type of corporate structure is about having our subsidiaries prosper through strong onsite leadership while working synergistically with

other Alpine 4 holdings. The essence of our business model is based around acquiring business-to-business (B2B) companies in a broad spectrum of industries via our acquisition strategy of DSF (Drivers, Stabilizer, Facilitator). Our DSF business

model (which is discussed more below) offers our shareholders an opportunity to own small-cap businesses that hold defensible positions in their individual market space. Further, Alpine 4’s greatest opportunity for growth exists in the smaller to

middle-market operating companies with revenues between $5 to $150 million annually. In this target-rich environment, businesses generally sell at more reasonable multiples, presenting greater opportunities for operational and strategic improvements

that have greater potential to enhance profit.

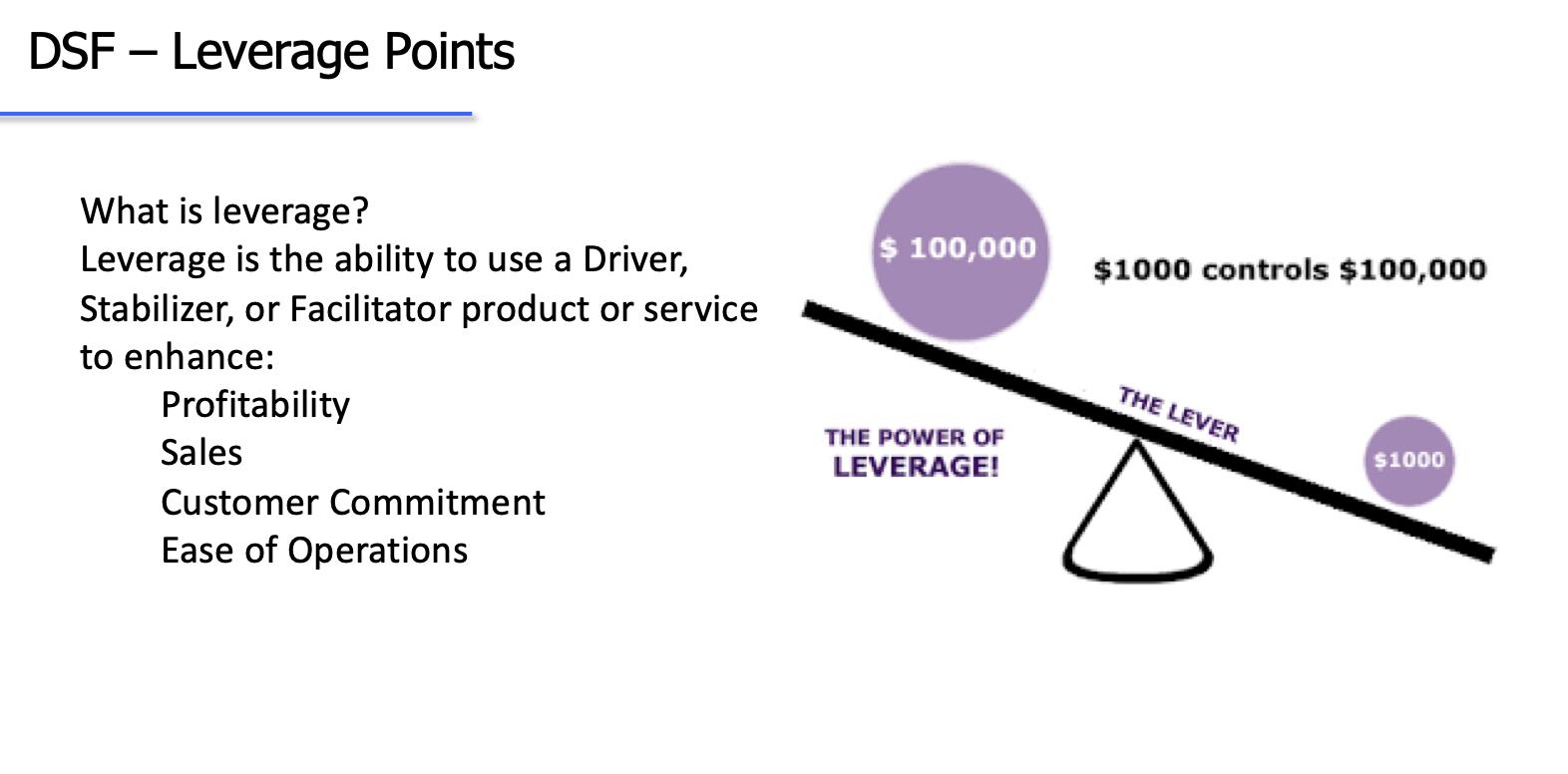

Driver, Stabilizer, Facilitator (DSF)

Driver: A Driver is a company that is in an emerging market or technology, that has enormous upside potential for revenue and

profits, with a significant market opportunity to access. These types of acquisitions are typically small, brand new companies that need a structure to support their growth.

Stabilizer: Stabilizers are companies that have sticky customers, consistent revenue and provide solid net profit returns to Alpine

4.

Facilitators: Facilitators are our “secret sauce.” Facilitators are companies that provide a product or service that an Alpine 4

sister company can use as leverage to create a competitive advantage.

Our DSF Strategy is discussed in more detail below in the section entitled “Business.”

5

Risk Factors

We face numerous risks that could materially affect our business, results of operations or financial condition. The most significant

of these risks include the following:

|

-

|

Alpine 4 is an "emerging growth company," and the reduced disclosure requirements applicable to "emerging growth companies"

could make our common stock less attractive to investors.

|

|

-

|

Growth and development of operations will depend on the acceptance of Alpine 4's proposed businesses. If Alpine 4's products

are not deemed desirable and suitable for purchase and it cannot establish a customer base, it may not be able to generate future revenues, which would result in a failure of the business and a loss of the value of your investment.

|

|

-

|

If demand for the products Alpine 4 plans to offer slows, then its business would be materially affected, which could result

in the loss of your entire investment.

|

|

-

|

Our revenue growth rate depends primarily on our ability to satisfy relevant channels and end-customer demands, identify

suppliers of our necessary ingredients and to coordinate those suppliers, all subject to many unpredictable factors.

|

|

-

|

If securities or industry analysts do not publish or cease publishing research or reports or publish misleading, inaccurate or

unfavorable research about us, our business or our market, our stock price and trading volume could decline.

|

|

-

|

Alpine 4 stockholders may have difficulty in reselling their shares due to the limited public market or state Blue Sky laws.

|

For further discussion of these and other risks, see “Risk Factors,” beginning on page 5.

The Offering

On January 16, 2020, we entered into a transaction (the “Lincoln Park Transaction”) consisting of a purchase agreement (the “Purchase

Agreement”) and a registration rights agreement (the “Registration Rights Agreement”) with Lincoln Park, pursuant to which Lincoln Park has committed to purchase up to $10.0 million worth of our Class A common stock, $0.0001 par value per share (the

“Common Stock”). A.G.P./Alliance Global Partners acted as sole placement agent for the offering.

Under the terms and subject to the conditions of the Purchase Agreement, we have the right, but not the obligation, to sell to Lincoln

Park, and Lincoln Park is obligated to purchase up to in the aggregate $10.0 million worth of shares of our Common Stock. As an initial purchase on January 17, 2020, Lincoln Park purchased 1,666,666 shares of our Common Stock (the “Initial Purchase

Shares”) at a price of $0.15 per share.

Additional sales of Common Stock by us to Lincoln Park, if any, will be subject to certain limitations, and may occur from time to

time, at our sole discretion, over the 36-month period commencing on the date that the registration statement of which this Prospectus is a part is declared effective by the U.S. Securities and Exchange Commission (the “SEC”) and a final prospectus

in connection therewith is filed and the other conditions set forth in the purchase agreement are satisfied, all of which are outside the control of Lincoln Park (the date on which all of such conditions are satisfied being the “Commencement Date”).

After the Commencement Date, under the Purchase Agreement, on any business day selected by us, we may direct Lincoln Park to purchase

up to 1,000,000 shares of our Common Stock on that business day (each, a “Regular Purchase”), provided, however, that (i) the Regular Purchase may be increased to up to 1,250,000 shares, provided that the closing sale price of the Common Stock is not

below $0.30 on the purchase date; (ii) the Regular Purchase may be increased to up to 1,500,000 shares, provided that the closing sale price of the Common Stock is not below $0.40 on the purchase date (subject to adjustment for any reorganization,

recapitalization, non-cash dividend, stock split, reverse stock split or other similar transaction as provided in the Purchase Agreement); and (iii) the Regular Purchase may be increased to up to 1,750,000 shares, provided that the closing sale price

of the Common Stock is not below $0.50 on the purchase date (each subject to adjustment for any reorganization, recapitalization, non-cash dividend, stock split, reverse stock split or other similar transaction as provided in the Purchase Agreement).

In each case, Lincoln Park’s maximum commitment in any single Regular Purchase may not exceed $1,000,000. The purchase price per share for each such Regular Purchase will be based off of prevailing market prices of Common Stock immediately preceding

the time of sale. The purchase price per share will be equitably adjusted for any reorganization, recapitalization, non-cash dividend, stock split, or other similar transaction occurring during the business days used to compute such price.

6

In addition to Regular Purchases, we may also direct Lincoln Park to purchase other amounts as accelerated purchases or as additional

accelerated purchases if the closing sale price of the common stock exceeds certain threshold prices as set forth in the Purchase Agreement.

Lincoln Park has no right to require us to sell any shares of common stock to Lincoln Park, but Lincoln Park is obligated to make

purchases as we direct, subject to certain conditions. In all instances, we may not sell shares of our Common Stock to Lincoln Park under the purchase agreement if it would result in Lincoln Park’s beneficially owning more than 4.99% of our Common

Stock. There are no upper limits on the price per share that Lincoln Park must pay for shares of Common Stock. Lincoln Park may not assign or transfer its rights and obligations under the Purchase Agreement.

There are no restrictions on future financings, rights of first refusal, participation rights, penalties or liquidated damages in the

Purchase Agreement or Registration Rights Agreement, other than a prohibition on our entering into certain types of transactions that are defined in the Purchase Agreement as “Variable Rate Transactions.”

We issued to Lincoln Park 2,275,086 shares of Common Stock (the “Commitment Shares”) as consideration for its commitment to purchase

shares of Common Stock under the Purchase Agreement.

As of February 10, 2020, we had 110,677,860 shares of our Class A Common Stock outstanding (including the 2,275,086 Commitment Shares

and the 1,666,666 Initial Purchase Shares issued to Lincoln Park), of which 106,326,000 shares were held by non-affiliates.

Although the Purchase Agreement provides that we may sell up to $10,000,000 of our common stock to Lincoln Park, only 14,000,000

shares of our common stock are being offered under this prospectus, which represents shares which have been or may be issued to Lincoln Park in the future under the Purchase Agreement. Depending on the market prices of our common stock at the time

we elect to issue and sell shares to Lincoln Park under the Purchase Agreement, we may need to register the resale of additional shares of our Common Stock under the Securities Act in order to receive aggregate gross proceeds equal to the $10,000,000

total commitment available to us under the Purchase Agreement. If all of the 14,000,000 shares offered by Lincoln Park under this prospectus were issued and outstanding as of the date hereof, such shares would represent approximately 11.23% of the

total number of shares of our common stock outstanding, and approximately 11.64% of the total number of outstanding shares excluding shares held by affiliates, in each case as of the date hereof. If we elect to issue and sell more than the

14,000,000 shares offered under this prospectus to Lincoln Park, which we have the right but not the obligation to do, we must first register for the resale of any such additional shares under the Securities Act pursuant to one or more additional

registration statements, which could cause additional substantial dilution to our stockholders. The number of shares ultimately offered for resale by Lincoln Park is dependent upon the number of shares we sell to Lincoln Park under the Purchase

Agreement.

The Purchase Agreement prohibits us from directing Lincoln Park to purchase any shares of common stock if those shares, when

aggregated with all other shares of our common stock then beneficially owned by Lincoln Park and its affiliates, would result in Lincoln Park and its affiliates having beneficial ownership, at any single point in time, of more than 4.99% of the then

total outstanding shares of our common stock, as calculated pursuant to Section 13(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and Rule 13d-3 thereunder, which limitation we refer to as the Beneficial Ownership Cap.

Issuances of our common stock in this offering will not affect the rights or privileges of our existing stockholders, except that the

economic and voting interests of each of our existing stockholders will be diluted as a result of any such issuance. Although the number of shares of common stock that our existing stockholders own will not decrease, the shares owned by our existing

stockholders will represent a smaller percentage of our total outstanding shares after any such issuance to Lincoln Park.

7

Summary of the Offering

|

Common stock offered by the Selling Stockholder

|

14,000,000 shares consisting of 2,275,086 Commitment Shares issued to Lincoln Park upon execution of the Purchase Agreement; the 1,666,666 Initial Purchase Shares; and

10,058,248 shares we may sell to Lincoln Park under the Purchase Agreement from time to time after the date of this prospectus

|

|

|

Common stock outstanding immediately prior to this offering

|

110,677,860 shares.

|

|

|

Common stock to be outstanding immediately following this offering

|

120,736,108 shares.

|

|

|

Use of proceeds

|

We will receive no proceeds from the sale of shares of common stock by Lincoln Park in this offering. We may receive up to $10,000,000 in aggregate gross proceeds under the

Purchase Agreement from any sales we make to Lincoln Park pursuant to the Purchase Agreement after the date of this prospectus. Any proceeds that we receive from sales to Lincoln Park under the Purchase Agreement will be used for working

capital and general corporate purposes. See “Use of Proceeds.”

|

|

|

OTCQB Trading Symbol

|

“ALPP”

|

|

|

Risk factors

|

You should carefully consider the information set forth in this Prospectus and, in particular, the specific factors set forth in the “Risk Factors” section beginning on page 5

of this Prospectus before deciding whether or not to invest in our common stock.

|

The number of shares of common stock to be outstanding after this offering is based on 110,677,860 shares of common stock outstanding at February 10, 2020,

(including the 2,275,086 Commitment Shares issued to Lincoln Park upon execution of the Purchase Agreement and the and the 1,666,666 Initial Purchase Shares purchased by Lincoln Park) and excludes the following:

|

-

|

779,000 shares of Class A common stock issuable upon exercise of stock options outstanding at a weighted-average exercise price of $.055 per share;

|

|

-

|

75,000 shares of Class A common stock issuable upon exercise of warrants outstanding at a weighted-average exercise price of $4.25per share; and

|

|

-

|

6,566,667 shares of Class A common stock issuable upon conversion of $985,000 convertible debt outstanding at a conversion price of $0.15 per share.

|

Unless otherwise indicated, all information in this prospectus reflects or assumes no issuance or exercise of stock options or warrants on or after September 30, 2019.

8

RISK FACTORS

Investing in our securities involves a high degree of risk. You should carefully consider and evaluate all of the information included and incorporated by reference or deemed to be

incorporated by reference in this prospectus. Our business, results of operations or financial condition could be adversely affected by any of these risks or by additional risks and uncertainties not currently known to us or that we currently

consider immaterial.

Risks Associated with Our Business and Operations

Alpine 4 is an "emerging growth company," and the reduced disclosure requirements applicable to "emerging growth companies" could make our common stock less

attractive to investors.

Alpine 4 is an "emerging growth company," as defined in the JOBS Act. For as long as we are an emerging growth company, we may take advantage of certain exemptions from various reporting

requirements that are applicable to other public companies that are not emerging growth companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act,

reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding advisory "say-on-pay" votes on executive compensation and shareholder advisory votes on

golden parachute compensation. We will remain an "emerging growth company" until the earliest of (i) the last day of the fiscal year during which we have total annual gross revenues of $1 billion or more; (ii) the last date of the fiscal year

following the fifth anniversary of the date of the first sale of common stock under the Company's first filed registration statement; (iii) the date on which we have, during the previous three-year period, issued more than $1 billion in

non-convertible debt; and (iv) the date on which we are deemed to be a "large accelerated filer" under the Exchange Act. We will be deemed a large accelerated filer on the first day of the fiscal year after the market value of our common equity

held by non-affiliates exceeds $700 million, measured on October 31.

We cannot predict if investors will find our common stock less attractive to the extent we rely on the exemptions available to emerging growth companies. If some investors find our common stock

less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for

complying with new or revised accounting standards. An emerging growth company can therefore delay the adoption of certain accounting standards until those standards would otherwise apply to private companies.

A Company that elects to be treated as an emerging growth company shall continue to be deemed an emerging growth company until the earliest of (i) the last day of the fiscal year during which it

had total annual gross revenues of $1,000,000,000 (as indexed for inflation), (ii) the last day of the fiscal year following the fifth anniversary of the date of the first sale of common stock under the Company's first filed registration statement;

(iii) the date on which it has, during the previous 3-year period, issued more than $1,000,000,000 in non-convertible debt; or (iv) the date on which is deemed to be a 'large accelerated filer' as defined by the SEC, which would generally occur

upon it attaining a public float of at least $700 million.

However, we are choosing to "opt out" of such extended transition period, and as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption of such

standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Our independent auditors have expressed substantial doubt about our ability to continue as a going concern.

Alpine 4 has incurred net losses of $28,520,094 since inception through December 31, 2018. This net loss was primarily driven in 2015 by stock issuance to employees and the ceasing of business

operations for its subsidiary Venture West Energy Services, LLC. Because we have yet to attain profitable operations, in their report on our financial statements for the period ended December 31, 2018, our independent auditors included an

explanatory paragraph regarding their substantial doubt about our ability to continue as a going concern. While management believes Alpine 4 will have net operating gains beginning in 2019, there can be no guarantee that we will be able to achieve

these net operating gains. Our ability to continue as a going concern is subject to our ability to generate a profit and/or obtain necessary funding from outside sources, including obtaining additional funding from the sale of our securities,

increasing sales or obtaining loan from various financial institutions where possible. Our net operating losses increase the difficulty in meeting such goals and there can be no assurances that such methods will prove successful. Our financial

statements contain additional note disclosures describing the management's assessment of our ability to continue as a going concern.

9

While Alpine 4 and its subsidiaries have long term Purchase Order arrangements with its large Contract Manufacturing customers and Master Service Agreements with its mechanical customers that can

provide a level of dependable revenue, there can be no assurance that Alpine 4 will be able to continue to generate revenues or that revenues will be sufficient to maintain its business. As a result, investors or shareholders could lose all of

their investment if Alpine 4 is not successful in its proposed business plans.

Alpine 4's needs could exceed the amount of time or level of experience its officers and directors may have. Alpine 4 will be dependent on key executives,

and the loss of the services of the current officers and directors could severely impact Alpine 4's business operations.

Alpine 4's business plan does not provide for the hiring of any additional employees other than outlined in its plan of operations until sales will support the expense. Until that time, the

responsibility of developing Alpine 4's business and fulfilling the reporting requirements of a public company will fall upon the officers and the directors. In the event they are unable to fulfill any aspect of their duties to Alpine 4, it may

experience a shortfall or complete lack of sales resulting in little or no profits and eventual closure of our business.

Additionally, the management of future growth will require, among other things, continued development of Alpine 4's financial and management controls and management information systems, stringent

control of costs, increased marketing activities, and the ability to attract and retain qualified management, research, and marketing personnel. The loss of key executives or the failure to hire qualified replacement personnel would compromise

Alpine 4's ability to generate revenues or otherwise have a material adverse effect on Alpine 4. There can be no assurance that Alpine 4 will be able to successfully attract and retain skilled and experienced personnel.

Significant time and management resources are required to ensure compliance with public company reporting and other obligations. Taking steps to comply with

these requirements will increase our costs and require additional management resources, and does not ensure that we will be able to satisfy them.

We are a publicly reporting company. As a public company, we are required to comply with applicable provisions of the Sarbanes-Oxley Act of 2002, as well as other federal securities laws, and

rules and regulations promulgated by the SEC and the various exchanges and trading facilities where our common stock may trade, which result in significant legal, accounting, administrative and other costs and expenses. These rules and requirements

impose certain corporate governance requirements relating to director independence, distributing annual and interim reports, stockholder meetings, approvals and voting, soliciting proxies, conflicts of interest, and codes of conduct, depending on

where our shares trade. Our management and other personnel will need to devote a substantial amount of time to ensure that we comply with all applicable requirements.

As we review our internal controls and procedures, we may determine that they are ineffective or have material

weaknesses, which could impact the market's acceptance of our filings and financial statements.

In connection with the preparation of our Annual Report for the year ended December 31, 2018, we conducted a review of our internal control over financial reporting for the purpose of providing the

management report required by these rules. During the course of our review and testing, we identified deficiencies and have been unable to remediate them before we were required to provide the required reports. Furthermore, because we have material

weaknesses in our internal control over financial reporting, we may not detect errors on a timely basis and our financial statements may be materially misstated. Even if we are able to remediate the material weaknesses, we may not be able to

conclude on an ongoing basis that we have effective internal controls over financial reporting, which could harm our operating results, cause investors to lose confidence in our reported financial information and cause the trading price of our

stock to fall. In addition, as a public company we are required to file in a timely manner accurate quarterly and annual reports with the SEC under the Securities Exchange Act of 1934 (the "Exchange Act"), as amended. Any failure to report our

financial results on an accurate and timely basis could result in sanctions, lawsuits, delisting of our shares from the market or trading facility where our shares may trade, or other adverse consequences that would materially harm our business.

10

Because Alpine 4 has shown a net loss since inception, ownership of Alpine 4 shares is highly risky and could result in a complete loss of the value of your

investment if Alpine 4 is unsuccessful in its business plans.

Based upon current plans, Alpine 4 expects to stop incurring operating losses in future periods as its subsidiaries move from their Optimization Phase to its Asset Producing Phase. However new

additional subsidiaries may incur significant expenses associated with the growth of those businesses. Further, there is no guarantee that it will be successful in realizing future revenues or in achieving or sustaining positive cash flow at any

time in the future. Any such failure could result in the possible closure of its business or force Alpine 4 to seek additional capital through loans or additional sales of its equity securities to continue business operations, which would dilute

the value of any shares you receive in connection with the Share Exchange.

Growth and development of operations will depend on the growth in the Alpine 4 acquisition model and from organic growth from its subsidiaries businesses. If

Alpine 4 cannot find desirable acquisition candidates, it may not be able to generate growth with future revenues.

Alpine 4 expects to continue its strategy of acquiring businesses, which management believes will result in significant growth in projected annualized revenue by the end of 2020. However, there is

no guarantee that it will be successful in realizing future revenue growth from its acquisition model. As such, Alpine 4 is highly dependent on suitable candidates to acquire which the supply of those candidates cannot be guaranteed and is driven

from the market for M&A. If Alpine 4 is unable to locate or identify suitable acquisition candidates, or to enter into transactions with such candidates, or if Alpine 4 is unable to integrate the acquired businesses, Alpine 4 may not be able

to grow its revenues to the extent anticipated, or at all.

Alpine 4 has limited management resources, and will be dependent on key executives. The loss of the services of the current officers and directors could

severely impact Alpine 4's business operations and future development, which could result in a loss of revenues and adversely impact the ability to ever sell any Exchange Shares received through participation in the Share Exchange.

Alpine 4 is relying on a small number of key individuals to implement its business and operations and, in particular, the professional expertise and services of Kent B. Wilson, our President, Chief

Executive Officer, and Secretary, and Charles Winters, our Chairman of the Board of Directors. Mr. Wilson intends to serve full time in his capacities with Alpine 4 to work to develop and grow the Company. Nevertheless, Alpine 4 may not have

sufficient managerial resources to successfully manage the increased business activity envisioned by its business strategy. In addition, Alpine 4's future success depends in large part on the continued service of Mr. Wilson. If he chooses not to

serve as an officer or if he is unable to perform his duties, this could have an adverse effect on Company business operations, financial condition and operating results if we are unable to replace Mr. Wilson or Mr. Winters with other individuals

qualified to develop and market our business. The loss of their services could result in a loss of revenues, which could result in a reduction of the value of any ownership of Alpine 4.

Competition that Alpine 4 faces is varied and strong.

Alpine 4's subsidiaries’ products and industries as a whole are subject to competition. There is no guarantee that we can sustain our market position or expand our business.

We compete with a number of entities in providing products to our customers. Such competitor entities include a variety of large nationwide corporations, including but not limited to public

entities and companies that have established loyal customer bases over several decades.

Many of our current and potential competitors are well established and have significantly greater financial and operational resources, and name recognition than we have. As a result, these

competitors may have greater credibility with both existing and potential customers. They also may be able to offer more competitive products and services and more aggressively promote and sell their products. Our competitors may also be able to

support more aggressive pricing than we will be able to, which could adversely affect sales, cause us to decrease our prices to remain competitive, or otherwise reduce the overall gross profit earned on our products.

Our success in business and operations will depend on general economic conditions.

The success of Alpine 4 and its subsidiaries depends, to a large extent, on certain economic factors that are beyond its control. Factors such as general economic conditions, levels of unemployment, interest rates,

tax rates at all levels of government, competition and other factors beyond Alpine 4's control may have an adverse effect on the ability of our subsidiaries to sell its products, to operate, and to collect sums due and owing to them.

11

Successful implementation of our business strategy depends on our being able to acquire additional businesses and grow our existing subsidiaries, as well as on factors specific to the industries in

which our subsidiaries operate, and the state of the financial industry and numerous other factors that may be beyond our control. Adverse changes in the following factors could undermine our business strategy and have a material adverse effect on

our business, our financial condition, and results of operations and cash flow:

|

•

|

The competitive environment in the industries in which our subsidiaries operate that may force us to reduce prices below the optimal pricing level or increase promotional spending;

|

|

•

|

Our ability to anticipate changes in consumer preferences and to meet customers' needs for our products in a timely cost effective manner; and

|

|

•

|

Our ability to establish, maintain and eventually grow market share in these competitive environments.

|

Our revenue growth rate depends primarily on our ability to satisfy relevant channels and end-customer demands, identify suppliers of our necessary

ingredients and to coordinate those suppliers, all subject to many unpredictable factors.

We may not be able to identify and maintain the necessary relationships with suppliers of product and services as planned. Delays or failures in deliveries could materially and adversely affect

our growth strategy and expected results. As we supply more customers, our rate of expansion relative to the size of such customer base will decline. In addition, one of our biggest challenges is securing an adequate supply of suitable

product. Competition for product is intense, and commodities costs subject to price volatility.

Our ability to execute our business plan also depends on other factors, including:

|

•

|

ability to keep satisfied vendor relationships

|

|

•

|

hiring and training qualified personnel in local markets;

|

|

•

|

managing marketing and development costs at affordable levels;

|

|

•

|

cost and availability of labor;

|

|

•

|

the availability of, and our ability to obtain, adequate supplies of ingredients that meet our quality standards; and

|

|

•

|

securing required governmental approvals in a timely manner when necessary.

|

Risks Related to Our Common Stock

Alpine 4 stockholders, and others who choose to purchase shares of Alpine 4 common stock if and when offered, may have difficulty in reselling their shares

due to the limited public market or state Blue Sky laws.

Our common stock is currently quoted on the OTC market. Current Alpine 4 stockholders and persons who desire to purchase them in any trading market should be aware that there might be additional

significant state law restrictions upon the ability of investors to resell our shares. Accordingly, investors should consider any secondary market for our securities to be a limited one.

Sales of our common stock under Rule 144 could reduce the price of our stock.

Under Rule 144 affiliates of Alpine 4 may not sell more than one percent of the total issued and outstanding shares in any 90-day period and must resell the shares in an unsolicited brokerage

transaction at the market price. If substantial amounts of our common stock become available for resale under Rule 144 once a market has developed for our common stock, the then-prevailing market prices for our common stock may be reduced.

12

We may, in the future, issue additional securities, which would reduce our stockholders' percent of ownership and may dilute our share value.

Our Certificate of Incorporation, as amended to date, authorizes us to issue 125,000,000 shares of Class A common stock, and 10,000,000 shares of Class B common stock and 15,000,000 Class C stock.

As of the date of this Prospectus, we had 110,677,860 shares of Class A common stock outstanding; 9,022,983 shares of Class B common stock issued and outstanding; and 11,527,268 shares of Class C common stock issued and outstanding. Accordingly, we

may issue up to an additional 14,322,140 shares of Class A common stock; up to an additional 977,017 shares of Class B common stock; and up to an additional 3,472,732 shares of Class C common stock. The future issuance of additional shares of

Class A common stock will result in additional dilution in the percentage of our Class A common stock held by our then existing stockholders. We may value any Class A common stock issued in the future on an arbitrary basis including for services or

acquisitions or other corporate actions that may have the effect of diluting the value of the shares held by our stockholders, and might have an adverse effect on any trading market for our Class A common stock. Additionally, our board of

directors may designate the rights terms and preferences of one or more series of preferred stock at its discretion including conversion and voting preferences without prior notice to our stockholders. Any of these events could have a dilutive

effect on the ownership of our shareholders, and the value of shares owned.

Raising additional capital or purchasing businesses through the issuance of common stock will cause dilution to our existing stockholders.

We may seek additional capital through a combination of private and public equity offerings, debt financings, collaborations, and strategic and licensing arrangements, as well as issuing stock to

make additional business or asset acquisitions. To the extent that we raise additional capital through the sale of common stock or securities convertible or exchangeable into common stock or through the issuance of equity for purchases of

businesses or assets, your ownership interest in Alpine 4 will be diluted.

Raising additional capital may restrict our operations or require us to relinquish rights.

We may seek additional capital through a combination of private and public equity offerings, debt financings, collaborations, and strategic and licensing arrangements. To the extent that we raise

additional capital through the sale of common stock or securities convertible or exchangeable into common stock, the terms of any such securities may include liquidation or other preferences that materially adversely affect your rights as a

stockholder. Debt financing, if available, would increase our fixed payment obligations and may involve agreements that include covenants limiting or restricting our ability to take specific actions, such as incurring additional debt, making

capital expenditures or declaring dividends. If we raise additional funds through collaboration, strategic partnerships and licensing arrangements with third parties, we may have to relinquish valuable rights to our intellectual property, future

revenue streams or grant licenses on terms that are not favorable to us.

Market volatility may affect our stock price and the value of your shares.

The market price for our common stock is likely to be volatile, in part because the volume of trades of our common stock. In addition, the market price of our common stock may fluctuate

significantly in response to a number of factors, most of which we cannot control, including, among others:

|

•

|

announcements of new products, brands, commercial relationships, acquisitions or other events by us or our competitors;

|

|

•

|

regulatory or legal developments in the United States and other countries;

|

|

•

|

fluctuations in stock market prices and trading volumes of similar companies;

|

|

•

|

general market conditions and overall fluctuations in U.S. equity markets;

|

|

•

|

variations in our quarterly operating results;

|

|

•

|

changes in our financial guidance or securities analysts' estimates of our financial performance;

|

|

•

|

changes in accounting principles;

|

|

•

|

our ability to raise additional capital and the terms on which we can raise it;

|

|

•

|

sales of large blocks of our common stock, including sales by our executive officers, directors and significant stockholders;

|

|

•

|

additions or departures of key personnel;

|

|

•

|

discussion of us or our stock price by the press and by online investor communities; and

|

|

•

|

other risks and uncertainties described in these risk factors.

|

13

If securities or industry analysts do not publish or cease publishing research or reports or publish misleading, inaccurate or unfavorable research about us,

our business or our market, our stock price and trading volume could decline.

The trading market for our common stock will be influenced by the research and reports that securities or industry analysts may publish about us, our business, our market or our competitors. We

currently have limited coverage and may never obtain increased research coverage by securities and industry analysts. If no or few securities or industry analysts cover our company, the trading price and volume of our stock would likely be

negatively impacted. If we obtain securities or industry analyst coverage and if one or more of the analysts who covers us downgrades our stock or publishes inaccurate or unfavorable research about our business, or provides more favorable relative

recommendations about our competitors, our stock price would likely decline. If one or more of these analysts ceases coverage of us or fails to publish reports on us regularly, demand for our stock could decrease, which could cause our stock price

or trading volume to decline.

Future sales of our common stock may cause our stock price to decline.

Sales of a substantial number of shares of our common stock in the public market or the perception that these sales might occur could significantly reduce the market price of our common stock and

impair our ability to raise adequate capital through the sale of additional equity securities.

Our compliance with the Sarbanes-Oxley Act and SEC rules concerning internal controls may be time consuming, difficult and costly.

Alpine 4's executive officers have limited experience being officers of a public company. It may be time consuming, difficult and costly for us to continue to implement and update the internal

controls and reporting procedures required by Sarbanes-Oxley. We may need to hire additional financial reporting, internal controls and other finance staff in order to develop and implement appropriate internal controls and reporting

procedures. If we are unable to comply with Sarbanes-Oxley's internal controls requirements, we may not be able to obtain the independent accountant certifications that Sarbanes-Oxley Act requires publicly-traded companies to obtain.

Alpine 4 may issue Preferred Stock with voting and conversion rights that could adversely affect the voting power of the holders of Common Stock.

Pursuant to our Certificate of Incorporation, our Board of Directors may issue Preferred Stock with voting and conversion rights that could adversely affect the voting power of the holders of

Common Stock. In the fourth quarter of 2019, we issued shares of a newly designated Series B Preferred Stock to members of our Board of Directors. The outstanding shares of Series B Preferred Stock have voting rights in the aggregate equal to 200%

of the total voting power of our other outstanding securities, giving our Board of Directors control over any matters submitted to the vote of the shareholders of Alpine 4. that Any such provision may be deemed to have a potential anti-takeover

effect, and the issuance of Preferred Stock in accordance with such provision may delay or prevent a change of control of Alpine 4. The Board of Directors also may declare a dividend on any outstanding shares of Preferred Stock.

Risks Related to the Offering

The sale or issuance of our common stock to Lincoln Park may cause dilution, and the sale of the shares of common stock acquired by Lincoln Park, or the perception

that such sales may occur, could cause the price of our common stock to fall.

On January 16, 2020, we entered into the Purchase Agreement with Lincoln Park, pursuant to which Lincoln Park has committed to

purchase up to $10,000,000 of our common stock. Upon the execution of the Purchase Agreement, we issued 2,275,086 Commitment Shares to Lincoln Park as a fee for its commitment to purchase shares of our common stock under the Purchase Agreement, and

immediately following execution of the Purchase Agreement, Lincoln Park purchased 1,666,666 shares of our Common Stock (the “Initial Purchase Shares”). The remaining shares of our common stock that may be issued under the Purchase Agreement may be

sold by us to Lincoln Park at our discretion from time to time over a 36-month period commencing after the satisfaction of certain conditions set forth in the Purchase Agreement, including that the SEC has declared effective the registration

statement that includes this prospectus. The purchase price for the shares that we may sell to Lincoln Park under the Purchase Agreement will fluctuate based on the price of our common stock. Depending on market liquidity at the time, sales of such

shares may cause the trading price of our common stock to fall.

14

We generally have the right to control the timing and amount of any future sales of our shares to Lincoln Park. Additional sales of

our common stock, if any, to Lincoln Park will depend upon market conditions and other factors to be determined by us. We may ultimately decide to sell to Lincoln Park all, some or none of the additional shares of our common stock that may be

available for us to sell pursuant to the Purchase Agreement. If and when we do sell shares to Lincoln Park, after Lincoln Park has acquired the shares, Lincoln Park may resell all, some or none of those shares at any time or from time to time in its

discretion. Therefore, sales to Lincoln Park by us could result in substantial dilution to the interests of other holders of our common stock. Additionally, the sale of a substantial number of shares of our common stock to Lincoln Park, or the

anticipation of such sales, could make it more difficult for us to sell equity or equity-related securities in the future at a time and at a price that we might otherwise wish to effect sales.

If we sell shares of our common stock in future financings, stockholders may experience

immediate dilution and, as a result, our stock price may decline.

We may from time to time issue additional shares of common stock at a discount from the current market price of our common stock. As a

result, our stockholders would experience immediate dilution upon the purchase of any shares of our common stock sold at such discount. In addition, as opportunities present themselves, we may enter into financing or similar arrangements in the

future, including the issuance of debt securities, preferred stock or common stock. If we issue common stock or securities convertible into common stock, our common stockholders would experience additional dilution and, as a result, our stock price

may decline.

We will have broad discretion in how we use the net proceeds of this offering. We may not use

these proceeds effectively, which could affect our results of operations and cause our stock price to decline.

We will have considerable discretion in the application of the net proceeds of this offering, including for any of the purposes

described in the section entitled “Use of Proceeds.” We intend to use the net proceeds from this offering to fund clinical development of our product candidates and working capital and other general corporate purposes. As a result, investors will be

relying upon management’s judgment with only limited information about our specific intentions for the use of the balance of the net proceeds of this offering. We may use the net proceeds for purposes that do not yield a significant return or any

return at all for our stockholders. In addition, pending their use, we may invest the net proceeds from this offering in a manner that does not produce income or that loses value.

An active trading market for our common stock may not be sustained.

Although our common stock is listed on the OTCQB Market, the market for our shares has demonstrated varying levels of trading

activity. Furthermore, the current level of trading may not be sustained in the future. The lack of an active market for our common stock may impair investors’ ability to sell their shares at the time they wish to sell them or at a price that they

consider reasonable, may reduce the fair market value of their shares and may impair our ability to raise capital to continue to fund operations by selling shares and may impair our ability to acquire additional intellectual property assets by using

our shares as consideration.

The market price for our common stock may be volatile, and an investment in our common stock could decline in value.

The stock market in general has experienced extreme price and volume fluctuations. The market prices of the securities of biotechnology and specialty pharmaceutical companies,

particularly companies like ours without product revenues and earnings, have been highly volatile and may continue to be highly volatile in the future. This volatility has often been unrelated to the operating performance of particular companies. The

following factors, in addition to other risk factors described in this section, may have a significant impact on the market price of our common stock:

15

|

-

|

announcements of technological innovations or new products by us or our competitors;

|

|

-

|

developments or disputes concerning patents or proprietary rights, including announcements of infringement, interference or other litigation against us or our potential

licensees;

|

|

-

|

developments involving our efforts to commercialize our products, including developments impacting the timing of commercialization;

|

|

-

|

actual or anticipated fluctuations in our operating results;

|

|

-

|

changes in financial estimates or recommendations by securities analysts;

|

|

-

|

developments involving corporate collaborators, if any;

|

|

-

|

changes in accounting principles; and

|

|

-

|

the loss of any of our key management personnel.

|

In the past, securities class action litigation has often been brought against companies that experience volatility in the market price of their securities. Whether or not

meritorious, litigation brought against us could result in substantial costs and a diversion of management’s attention and resources, which could adversely affect our business, operating results and financial condition.

We do not anticipate paying dividends on our common stock and, accordingly, stockholders must rely on stock

appreciation for any return on their investment.

We have never declared or paid cash dividends on our common stock and do not expect to do so in the foreseeable future. The declaration of dividends is subject to the discretion of

our board of directors and limitations under applicable law, and will depend on various factors, including our operating results, financial condition, future prospects and any other factors deemed relevant by our board of directors. You should not

rely on an investment in our company if you require dividend income from your investment in our company. The success of your investment will likely depend entirely upon any future appreciation of the market price of our common stock, which is

uncertain and unpredictable. There is no guarantee that our common stock will appreciate in value.

We expect that our quarterly results of operations will fluctuate, and this fluctuation could cause our stock price to decline.

Our quarterly operating results are likely to fluctuate in the future. These fluctuations could cause our stock price to decline. The nature of our business involves variable factors,

such as the timing of the research, development and regulatory pathways of our product candidates, which could cause our operating results to fluctuate.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. The forward-looking statements are contained principally in the sections entitled “Prospectus Summary,” “Risk Factors,”

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” These statements relate to future events or to our future financial performance and involve known and unknown risks, uncertainties and other

factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Forward-looking statements include, but

are not limited to, statements about:

|

-

|

our lack of revenues, history of operating losses, bankruptcy, limited cash reserves and ability to draw on our Purchase Agreement with Lincoln Park or obtain other capital to

develop and implement our business strategies and grow our business, and continue as a going concern;

|

|

-

|

our ability to execute our strategy and business plan regarding growth, acquisitions, and focusing on our strategy of Drivers, Stabilizers, and Facilitators;

|

|

-

|

the success, progress, timing and costs of our efforts to evaluate or consummate various strategic acquisitions, collaborations, and other alternatives if in the best

interests of our stockholders;

|

|

-

|

our ability to timely source adequate supply of our development products from third-party manufacturers on which we depend;

|

|

-

|

the potential, if any, for future development of any of our present or future products;

|

|

-

|

our ability to identify and develop additional uses for our products;

|

|

-

|

our ability to attain market exclusivity and/or to protect our intellectual property and to operate our business without infringing on the intellectual property rights of

others;

|

|

-

|

the ability of our Board of Directors to influence control over all matters put to a vote of our stockholders, including elections of directors, amendments of our

organizational documents, or approval of any merger, sale of assets, or other major corporate transaction; and

|

|

-

|

the accuracy of our estimates regarding expenses, future revenues, capital requirements and needs for additional financing.

|

16

In some cases, you can identify these statements by terms such as “anticipate,” “believe,” “could,” “estimate,” “expects,” “intend,” “may,” “plan,” “potential,” “predict,” “project,”

“should,” “will,” “would” or the negative of those terms, and similar expressions that convey uncertainty of future events or outcomes. These forward-looking statements reflect our management’s beliefs and views with respect to future events and are

based on estimates and assumptions as of the date of this prospectus and are subject to risks and uncertainties. In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These

statements are based upon information available to us as of the date of this prospectus, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not

be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements. We

discuss many of the risks associated with the forward-looking statements in this prospectus in greater detail under the heading “Risk Factors.” Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to

time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those

contained in any forward-looking statements we may make. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

You should carefully read this prospectus and the documents that we reference in this prospectus and have filed as exhibits to the registration statement of which this prospectus is a

part, completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of the forward-looking statements in this prospectus by these cautionary statements.

Except as required by law, we expressly disclaim any obligation or intention to update these forward-looking statements publicly, or to update the reasons actual results could differ

materially from those anticipated in any forward-looking statements, whether as a result of new information, future events or otherwise.

Any forward-looking statement made by us in this prospectus is based only on information currently available to us and speaks only as of the date on which it is made. We undertake no

obligation to publicly update any forward-looking statement, whether written or oral that may be made from time to time, whether as a result of new information, future developments or otherwise, except as required by applicable law.

DETERMINATION OF MARKET PRICE

The selling stockholder will determine at what price it may sell the offered shares, and such sales may be made at prevailing market prices or at privately negotiated prices. See

“Plan of Distribution” for more information.

USE OF PROCEEDS

This prospectus relates to shares of our common stock that may be offered and sold from time to time by Lincoln Park. We will receive no proceeds from the sale of shares of common

stock by Lincoln Park in this offering.

We may receive up to $10,000,000 in aggregate gross proceeds under the Purchase Agreement from any sales we make to Lincoln Park pursuant to the Purchase Agreement after the date of

this prospectus. We estimate that the net proceeds to us from the sale of our common stock to Lincoln Park pursuant to the Purchase Agreement will be up to approximately $9,500,000 over an approximately 36-month period, assuming that we sell the full

amount of our common stock that we have the right, but not the obligation, to sell to Lincoln Park under the Purchase Agreement, and after other estimated fees and expenses. See “Plan of Distribution” elsewhere in this prospectus for more

information.

We currently intend to use the estimated net proceeds we receive under the Purchase Agreement in the following order of priority: (i) Paying off liabilities incurred in connection

with business acquisitions through the date of this Prospectus; (ii) Paying off long-term liabilities; (iii) payment of other acquisition expenses; and (iv) for general working capital and general corporate purposes.

Our management will have significant discretion and flexibility in applying the net proceeds from the Purchase Agreement. Pending the application of the net proceeds, as described

above, we intend to invest the net proceeds in high-quality, short-term, interest-bearing securities.

17

DIVIDEND POLICY

As of the date of this Prospectus, we had never declared or paid a cash dividend. Our Board of Directors may elect to declare and pay a cash dividend in the future. As of the date of

this Prospectus, we had declared and issued a dividend of shares of our Class C Common Stock to the holders of our Class A Common Stock. Our Board of Directors may elect to declare and pay other similar dividends in the future.

LINCOLN PARK TRANSACTION

General

On January 16, 2020, we entered into the Purchase Agreement and the Registration Rights Agreement with Lincoln Park. Pursuant to the terms of the Purchase Agreement, Lincoln Park has

agreed to purchase from us up to $10,000,000 of our Class A common stock (subject to certain limitations) from time to time during the term of the Purchase Agreement. Pursuant to the terms of the Registration Rights Agreement, we have filed with the

SEC the registration statement that includes this prospectus to register for resale under the Securities Act the shares that have been or may be issued to Lincoln Park under the Purchase Agreement.

Pursuant to the terms of the Purchase Agreement, at the time we signed the Purchase Agreement and the Registration Rights Agreement, we issued 2,275,086 Commitment Shares to Lincoln

Park as consideration for its commitment to purchase shares of our common stock under the Purchase Agreement. Additionally, immediately following the execution of the Purchase Agreement and Registration Rights Agreement, Lincoln Park purchased

1,666,666 shares of our common stock (the “Initial Purchase Shares”) at a per share price of $0.15.

We do not have the right to commence any sales to Lincoln Park under the Purchase Agreement until certain conditions set forth in the Purchase Agreement, all of which are outside of

Lincoln Park’s control, have been satisfied, including the registration statement that includes this prospectus being declared effective by the SEC, which we refer to as the Commencement. Thereafter, we have the right, but not the obligation, to

direct Lincoln Park to purchase up to 1,000,000 Purchase Shares on any single business day from and after the Commencement, which amount may be increased up to 1,250,000 shares, 1,500,000 shares, or 1,750,000 shares, depending on the market price of

our common stock at the time of sale, subject to a maximum of [$1,000,000] per purchase.

In addition, upon notice to Lincoln Park, we may, from time to time and at our sole discretion, direct Lincoln Park to purchase additional shares of our common stock in “accelerated

purchases,” “additional accelerated purchases” and/or “additional purchases” as set forth in the Purchase Agreement. The purchase price per share is based on the market price of our common stock at the time of sale as computed under the Purchase

Agreement. Lincoln Park may not assign or transfer its rights and obligations under the Purchase Agreement.

The Purchase Agreement prohibits us from directing Lincoln Park to purchase any shares of common stock if those shares, when aggregated with all other shares of our common stock then

beneficially owned by Lincoln Park, would result in Lincoln Park and its affiliates exceeding the Beneficial Ownership Cap.

Purchase of Shares Under the Purchase Agreement

Regular Purchases

Under the Purchase Agreement, on any business day selected by us, we may direct Lincoln Park to purchase up to 1,000,000 shares of our Class A common stock, which we refer to as the

Regular Purchase Share Limit, on such business day (the “Purchase Date”) in a regular purchase (a “Regular Purchase”), provided, however, that (i) the Regular Purchase Share Limit may be increased to up to 1,250,000 shares, provided that the closing

sale price is not below $0.30 on the applicable Purchase Date, (ii) the Regular Purchase Share Limit may be increased to up to 1,500,000 shares, provided that the closing sale price is not below $0.40 on the applicable purchase date, and (iii) the

Regular Purchase Share Limit may be increased to up to 1,750,000 shares, provided that the closing sale price is not below $0.50 on the applicable Purchase Date. In each case, the maximum amount of any single Regular Purchase may not exceed

$1,000,000 per purchase. The Regular Purchase Share Limit is subject to proportionate adjustment in the event of a reorganization, recapitalization, non-cash dividend, stock split or other similar transaction; provided, that if after giving effect to

such full proportionate adjustment, the adjusted Regular Purchase Share Limit would preclude us from requiring Lincoln Park to purchase common stock at an aggregate purchase price equal to or greater than $150,000 in any single Regular Purchase, then

the Regular Purchase Share Limit will not be fully adjusted, but rather the Regular Purchase Share Limit for such Regular Purchase shall be adjusted as specified in the Purchase Agreement, such that, after giving effect to such adjustment, the

Regular Purchase Share Limit will be equal to (or as close as can be derived from such adjustment without exceeding) $1,000,000.

18

The purchase price per share for each such Regular Purchase will be equal to 95% of the lower of:

|

-

|

the lowest sale price for our common stock on the purchase date of such shares; and

|

|

-

|

the arithmetic average of the three lowest closing sale prices for our common stock during the 12 consecutive business days ending on the business day immediately preceding

the purchase date of such shares.

|

Accelerated Purchases

On any Purchase Date on which the last closing trade price of the Company’s common stock is not below $0.05 per share and the Company has directed Lincoln Park to purchase the full Regular Share

Purchase Limit, the Company also has the right, in its sole discretion, to direct Lincoln Park to purchase an amount of stock (an “Accelerated Purchase”) equal to up to the lesser of (i) two times the number of shares purchased pursuant to such