Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Item 9 Labs Corp. | inlb0112form10kexh32_2.htm |

| EX-32.1 - EXHIBIT 32.1 - Item 9 Labs Corp. | inlb0112form10kexh32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - Item 9 Labs Corp. | inlb0112form10kexh31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - Item 9 Labs Corp. | inlb0112form10kexh31_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

☑ ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 (FEE REQUIRED)

For the fiscal year ended September 30, 2019

☐ TRANSACTION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 (NO FEE REQUIRED)

For the transaction period from ________ to ________

ITEM 9 LABS CORP.

(Exact name of registrant as specified in its charter)

| Delaware | 000-54730 | 96-0665018 | ||

| (State of other jurisdiction | (Commission | (IRS Employer | ||

| of incorporation) | File Number) | Identification No.) |

2727 North 3rd Street, Suite 201 Phoenix, Arizona 85004

(Address of principal executive offices and zip code)

1-833-867-6337

(Registrant’s telephone number, including area code)

1709 East Bethany Home Road, Phoenix, AZ 85016

(Former name or former address, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| N/A | N/A | N/A |

Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $0.0001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☑ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act: ☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer (Do not check if a smaller reporting company) | ☐ | Smaller reporting company | ☑ |

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

As of March 31, 2019 (the last business day of our most recently completed second fiscal quarter), based upon the last reported trade on that date, the aggregate market value of the voting and non-voting common equity held by non-affiliates (for this purpose, all outstanding and issued common stock minus stock held by the officers, directors and known holders of 10% or more of the Company’s common stock) was $43,679,785.50.

As of January 13, 2020, there were 63,652,620 shares of the issuer’s common stock, $0.0001 par value per share, outstanding.

FORWARD LOOKING STATEMENTS

The following discussion, in addition to the other information contained in this report, should be considered carefully in evaluating us and our prospects. This report (including without limitation the following factors that may affect operating results) contains forward-looking statements (within the meaning of Section 27A of the Securities Act of 1933, as amended ("Securities Act") and Section 21E of the Securities Exchange Act of 1934, as amended ("Exchange Act") regarding us and our business, financial condition, results of operations and prospects. Words such as "expects," "anticipates," "intends," "plans," "believes," "seeks," "estimates" and similar expressions or variations of such words are intended to identify forward-looking statements, but are not the exclusive means of identifying forward-looking statements in this report. Additionally, statements concerning future matters such as revenue projections, projected profitability, growth strategies, development of new products, enhancements or technologies, possible changes in legislation and other statements regarding matters that are not historical are forward-looking statements.

Forward-looking statements in this report reflect the good faith judgment of our management and the statements are based on facts and factors as we currently know them. Forward-looking statements are subject to risks and uncertainties and actual results and outcomes may differ materially from the results and outcomes discussed in the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, but are not limited to, those discussed below and in "Management's Discussion and Analysis of Financial Condition and Results of Operations" as well as those discussed elsewhere in this report. Readers are urged not to place undue reliance on these forward-looking statements which speak only as of the date of this report. We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report.

|

TABLE OF CONTENTS |

| Page | ||

| PART 1 | ||

| ITEM 1. | Description of Business | 4 |

| ITEM 1A. | Risk Factors | 10 |

| ITEM 1B | Unresolved Staff Comments | 17 |

| ITEM 2. | Properties | 18 |

| ITEM 3. | Legal Proceedings | 18 |

| ITEM 4. | Mine Safety Disclosures | 18 |

| PART II | ||

| ITEM 5. | Market for Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 19 |

| ITEM 6. | Selected Financial Data | 21 |

| ITEM 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 21 |

| ITEM 7A. | Quantitative and Qualitative Disclosures About Market Risk | 28 |

| ITEM 8. | Financial Statements and Supplementary Data | 28 |

| ITEM 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 28 |

| ITEM 9A. | Controls and Procedures | 29 |

| ITEM 9B. | Other Information | 29 |

| PART III | ||

| ITEM 10. | Directors, Executive Officers and Corporate Governance | 30 |

| ITEM 11. | Executive Compensation | 33 |

| ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 36 |

| ITEM 13. | Certain Relationships and Related Transactions, and Director Independence | 37 |

| ITEM 14. | Principal Accounting Fees and Services | 38 |

| PART IV | ||

| ITEM 15. | Exhibits, Financial Statement Schedules | 39 |

| SIGNATURES | 60 |

PART I

Item 1. Description Of Business

Corporate history

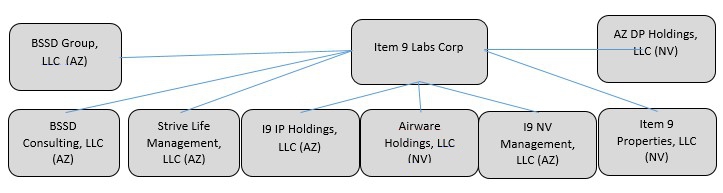

Item 9 Labs Corp. (“Item 9 Labs” or the “Company”), was incorporated under the laws of the State of Delaware on June 15, 2010 as Crown Dynamics Corp. On October 26, 2012, the Company changed its name to Airware Labs Corp. On April 2, 2018, the Company changed its name to Item 9 Labs Corp. to better reflect its business following the acquisition of BSSD, as discussed below.

On March 20, 2018, the Company closed on an Agreement and Plan of Exchange to acquire all of the membership interests of BSSD Group, LLC (“BSSD”), an Arizona limited liability company formed on May 2, 2017, in exchange for newly issued restricted shares of the Company’s common stock (the “Shares”), which represent approximately 75% of the issued and outstanding shares of the Company’s common stock on a fully-diluted basis. The 40,355,771 shares were distributed pro-rata to the BSSD members.

Effective October 18, 2018, the Company completed a 1-for-20 reverse split of its issued and outstanding common stock.

On November 26, 2018, the company’s wholly owned subsidiary AZ DP Holdings, LLC (“AZ DP”) closed on an asset acquisition of the majority of the assets of Arizona DP Consulting, LLC, a consulting firm specializing in obtaining marijuana dispensary permits and developing cannabis related business plans. The purchase price was $1,500,000 in cash and 3,000,000 shares of restricted common stock having an aggregate value of $7,770,000 or $2.59 per share based on current market price of the Company shares at time asset purchase agreement was executed.

On September 12, 2018, the Company executed a $1,500,000 promissory note (see Note 8) which was used to make a capital contribution into Strive Management, LLC, a Nevada limited liability company (“Strive Management”). In exchange for the contribution, the Company received a 20% membership interest in Strive Management. The remaining interests are held by three individuals, Sara Gullickson, Larry Lemons, and Donnie Burton. Through a management agreement with Strive Wellness of Nevada, LLC, a related party Strive Management will facilitate the cultivation, processing and distribution of marijuana in Nevada. Strive Wellness of Nevada, LLC has been allocated cultivation, processing and distribution licenses from the State of Nevada. Additionally, the Company will acquire an additional 31% ownership of Strive Management upon the approval from the State of Nevada to operate the cultivation and processing facility.

Our principal offices are located at 2727 N 3rd Street, Phoenix AZ 85004 Suite 201. Our registered agent for service of process in Delaware is located at 108 West 13th St., Wilmington, DE 19801, and our registered agent is Business Filings Incorporated. Our fiscal year end is September 30.

All references to “we,” “us,” “our,” “Item 9,” “Item 9 Labs,” or similar terms used in this Registration Statement refer to Item 9 Labs Corp.

Corporate Structure

The following chart illustrates, as of the date of this Registration Statement, the Company's wholly-owned subsidiaries, including their respective jurisdictions of incorporation and percentage of voting securities of each that are beneficially owned, controlled or directed by the Company.

Additionally, the Company currently owns a 20% ownership in Strive Management, LLC as discussed in Note 1 of our Notes to Financials (see Note 1). The Company has the right to acquire an additional 31% ownership of Strive Management if certain conditions are met. The Company will raise funds as necessary (approximately $5,500,000) to construct the facility in Nevada, which will be wholly owned by a subsidiary of Item 9 Labs Corp and leased to Strive Management, LLC. $3,000,000 has been raised as of the date of this filing. If the funds are not raised, the additional 31% interest due to the Company upon operational approval from the State of Nevada would be subject to reclamation by the other members of Strive Management.

Overview

Item 9 Labs creates comfortable cannabis health solutions for the modern consumer. The Company is bringing best of industry practices to markets from coast to coast through cultivation and production, distinctive retail environments, licensing services, and diverse product suites catering to different medical and adult use cannabis demographics. Item 9 Labs is headquartered in Phoenix, Arizona, with medical cannabis operations in multiple U.S. markets.

Item 9 Labs’ asset portfolio includes Dispensary Permits, Dispensary Templates, and Strive Life. These assets provide services specific to different stakeholder groups. Dispensary Permits is the Company’s consulting firm specializing in strategic license application and compliance. Dispensary Templates, a subdivision of the firm, is a technology platform with an extensive digital library of licensing and business planning resources. Strive Life is a turnkey dispensary model for the retail sector, elevating the patient experience with consistent and superior service, high-end design, and precision-tested products. It is currently being implemented in North Dakota.

In addition, Item 9 Labs is advancing the industry with its dynamic product suites. The Company has created complementary brands Item 9 Labs and Strive Wellness to channel consumer diversity. Propriety delivery platforms include the Apollo Vape and Pod system, as well as a pioneering intra-nasal device. The Company has received multiple accolades for its medical-grade flower and concentrates.

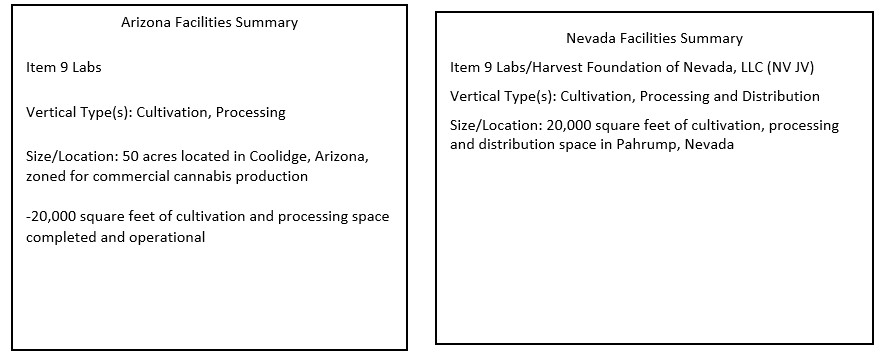

Item 9 Labs anticipates it will be managing cultivation, processing, distribution, and dispensary operations in up to seven U.S. markets by the end of 2020. Current facilities include Cultivation, Processing and Distribution for Strive Wellness of Nevada, as well as dispensary Strive Life North Dakota.

| 4 |

Mission and Vision

The Company is leading a new era of wellness by creating comfortable health solutions for modern consumers through the development of innovative products and proprietary delivery platforms.

Item 9 Labs will facilitate national expansion by combining our award-winning manufacturing brand and product offerings with the strategic licensing and consulting brand of Dispensary Permits, in conjunction with the luxury retail and distribution brand of Strive Life.

This powerful combination provides national scalability and produces the highest quality marijuana, product knowledge, and experience of top professionals to consumers and patients.

Cannabis Verticals

To date, Item 9 Labs has proven models for the following cannabis verticals:

- Cultivation: Growing of award winning, high-grade boutique cannabis.

- Production: Producing a wide variety of Marijuana Products. Each facility product line is developed in compliance with the local rules and regulations.

- Dispensary: Medical and Adult use retail dispensary facilities.

- Distribution: Providing Sales, Marketing and Distribution support to other cultivators, processors and potential to integrate patient delivery in the coming months.

Company Assets

A company asset of Item 9 Labs, Dispensary Permits is one of the most established marijuana business consultancies in the United States. Dispensary Permits offers expert advice in obtaining cultivation, dispensing, processing, and transporting permits in the Cannabis industry, with a proven track record in successfully obtaining marijuana business permits for clientele in over 13 different states. Visit www.dispensarypermits.com for more information.

Dispensary Templates, a division of Dispensary Permits, is an extensive template library and resource to help those navigating the application process without a consultant to obtain a marijuana business license or to build upon their existing marijuana business. Think LegalZoom for the Marijuana Industry – Dispensary Templates’ online store offers template products that guide customers through the application process to cultivation, processing and dispensary operations. Visit www.dispensarytemplates.com to view all tools and resources.

Strive Life, the company’s “franchise style” dispensary model, aims to elevate any marijuana market by offering the documents and systems necessary for launching a successful dispensary. The model includes a Project Plan, Welcome Kit, Brand Guidelines, Interior Concept, and Policy and Procedures for the facility. The Strive vision is to implement best industry practices from across the United States to offer optimal medical services and support through the dispensing and sale of medical marijuana.

| 5 |

Products and Facilities.

The Company is focused on the development of technology and products that administer high-quality medical marijuana through novel and proprietary delivery devices including an intra-nasal delivery system to deliver significant health benefits. The Company is headquartered in Phoenix, Arizona where it owns and operates 50 acres.

Currently, Item 9 is utilizing five acres and intends to implement the remaining 45 acres in accordance with its three-year strategic plan. The property includes a 10,000 square foot, state-of-the-art indoor manufacturing facility with 10,000 square feet of additional cultivation capacity which received approval to operate on June 4, 2019 and is currently producing premium flower. As part of its growth strategy, the Company is in the process of opening additional cultivation and extraction locations with Nevada near completion.

Item 9 Labs produces premium cannabis and cannabis related products in a rapidly growing market. We currently offer more than 300 products that we group in the following categories: flower; concentrates; distillates; and hardware. Our product offerings will continue to grow as we develop new products to meet the needs of the end-users. We make our products available to consumers through licensed dispensaries in Arizona. Item 9 products can be found in over 70 dispensaries throughout Arizona, covering 75% of the retail medical cannabis market. The following is a summary of the Company’s Product Line:

| 6 |

Strategy of our Brands

Item 9 Labs Concepts

Marijuana Growing & Processing

Product offerings include over 70 medical marijuana strains, shatter, crumble, badder, THCA, Delta 8 THC, broad spectrum distillate and live resin terpene sauce. Item 9 owns 50 acres, one of the largest properties in the U.S. zoned to grow and cultivate the medical marijuana flower. Most recently, on June 4, 2019, the Company passed inspections to operate custom 10,000 square-foot construction and is currently in production . The facility now totals 20,000 square-feet consisting of 8 flower rooms, just over 1,000 square-feet of nursery space and an updated or upgraded extraction laboratory for increased manufacturing capabilities. The Company’s products can be found in over 70 dispensaries in Arizona.

Strive Concepts

Strive is a branded medical marijuana “franchise- style” solution with a proven concept operating dispensaries in multiple states including Illinois, Delaware and Pennsylvania. The advance model offers the documents and systems necessary for launching a successful dispensary. The model includes a project plan, welcome kit, brand guidelines, interior concept, & policy and procedures for the facility.

Combined brands

Currently, we have two brands, both brands encompass our corporate vision and uphold our 5 core competencies which include: Care, Compliance, Customers, Community, and Culture. To achieve optimal balance between brands, Item 9 Labs was designed to be minimalistic with defined lines and shapes while Strive Concepts, was designed with the cannabis mother plant in mind, the brand colors are derived from the cannabis plant, the imagery includes other plant such as Aspen leaves and succulents and many interior textures derived from the “Franchise Style” Dispensary Model.

Growth Objectives and National Expansion Plans for 2020-2021

Our mission is to provide good times and good health for cannabis consumers in legal medical and adult use cannabis markets across the United States. We strive to elevate any market we enter through the development of high caliber, precision tested, cannabis products designed with consistency and adaptability in mind. We will accomplish this through the acquisition of numerous medical marijuana business licenses located all throughout the United States, from the East Coast to the West Coast. Our goal is to hold 10 – 12 licenses by the end of 2021, including through the provision of management services over joint ventures for outstanding license applications. Other plans for 2021 include:

- Replicate Nevada expansion in other key states through

management services joint ventures

- Purchase Licenses: 30+ existing markets

- Each deal will be vetted individually to ensure it’s in line with our mission, vision and capital structure.

Employees and Independent Contractors

As of January 13, 2020, we had sixty seven full time employees, including our executive officers, one full-time consultant, and two part-time employees. We plan to hire additional employees and engage consultants on an as-needed basis. Our employees are not represented by any unions and we consider our relationship with our employees to be great. We also have relationships with several independent contractors who provide services on a regular basis to us.

Research and Development

Going forward, we intend to continue focusing adequate resources on research and development . Allocation of research and development funds may be dependent on the perceived likelihood of legalization or a significant change in the treatment of cannabis in a given geographic market. Funds may also be used for both product and market development in the hemp and cannabis industries. Given the emergent nature of these industries, we recognize the needs of today may not be the needs of the future and some capital investment will be necessary to meet changing demands.

| 7 |

Intellectual Property

We generally rely upon copyright, trademark and trade secret laws to protect and maintain our proprietary rights for our technology, brands, and products. We currently hold several trademarks including various goods and services of “Item 9 Labs” (serial numbers 87940264, 87940227, 87940254 and 87940239), “Delta 8” (serial numbers 88004775, 88004789, 88004799, 88004812) and Strive Life (88/144,717), as well as several domains, including but not limited to, arizonadispensarypermits.com, dispernsarytemplates.com, and wegrowstore.com.

We maintain a policy requiring our employees, consultants and other third parties to enter into confidentiality and proprietary rights agreements and to control access to software, documentation and other proprietary information.

Notwithstanding the steps we have taken to protect our intellectual property rights, third parties may infringe or misappropriate our proprietary rights. Competitors may also independently develop products and models that are substantially equivalent or superior to our products and services.

Competition

We compete in markets where cannabis has been legalized and regulated, which includes various states within the United States. We expect that the quantity and composition of our competitive environment will continue to evolve as the industry matures. Additionally, increased competition is possible to the extent that new states and geographies enter the marketplace as a result of continued enactment of regulatory and legislative changes that de-criminalize and regulate cannabis products. We believe that by diligently establishing and expanding our brands, product offerings and services in new and existing locations, we will become established in the industry. Additionally, we expect that establishing our product offerings in new and existing locations are factors that mitigate the risk associated with operating in a developing competitive environment. Additionally, the contemporaneous growth of the industry as a whole will result in new customers entering the marketplace, thereby further mitigating the impact of competition on our operations and results.

In our opinion, we are currently competing with cannabis cultivators, manufacturers, and retailers in our local jurisdictions as well as international enterprises as set forth below, among many others. Many of our competitors are substantially larger than us and have significantly greater name recognition, sales and marketing, financial, technical, customer support and other resources. These competitors also may have more established distribution channels and stronger relationships with local, long distance and Internet service providers. These competitors may be able to respond more rapidly to new or emerging technologies and changes in customer requirements or to devote greater resources to the development, promotion and sale of their products.

These competitors may enter our existing or future markets with products that may be less expensive, that may provide higher performance or additional features or that may be introduced more quickly than our products.

With respect to our operations, including consulting services, we may face competition with any one of the following:

| • | Harvest Health & Recreation Inc. (CNSX: HARV, OTCQX: HTHHF), an Arizona based vertically integrated cannabis company with as many as 60 licensees across 12 states, 525 employees, and planned expansion for the future. |

| • | Curaleaf Hldgs Inc. (OTCQ: CURLF), a Massachusetts based fully integrated life science company with a presence in 12 states, operating 43 dispensaries, 12 cultivation sites and 11 processing sites. |

| • | Green Thumb Industries, Inc. (CSE: GTII, OTCQX:GTBIF),a vertically integrated cannabis operator with presence in twelve state markets and also provides management services and solutions to state licensed cultivators and dispensaries. |

| • | American Cannabis Company, Inc. (OTCQB:AMMJ), a Denver based company that provides advisory and consulting services specific to this industry, designs industry specific products and facilities, and manages a strategic group partnership that offers both exclusive and nonexclusive customer products. |

We do not expect to face competition with respect to our branded apparel, however, other corporations may sell apparel that incorporates other logos or trademarks associated with the cannabis industry.

We believe that we compete favorably with our competitors on the basis of these factors. However, if we are unable to compete successfully against our current and future competitors, it will be difficult to acquire and retain customers, and we may experience revenue declines, thereby resulting in reduced operating margins, loss of market share and diminished value in our services.

Government Regulation of Cannabis

Cannabis is currently a Schedule I controlled substance under the Controlled Substances Act (21 U.S.C. § 811) (“CSA”) and is, therefore, illegal under federal law. Even in those states in which the use of cannabis has been legalized pursuant to state law, its use, possession or cultivation remains a violation of federal law. A Schedule I controlled substance is defined as one that has no currently accepted medical use in the United States, a lack of safety for use under medical supervision and a high potential for abuse. The U.S. Department of Justice (the “DOJ”) defines Schedule I controlled substances as “the most dangerous drugs of all the drug schedules with potentially severe psychological or physical dependence.” If the federal government decides to enforce the CSA, persons that are charged with distributing, possessing with intent to distribute or growing cannabis could be subject to fines and/or terms of imprisonment, the maximum being life imprisonment and a $50 million fine, even though these persons are in compliance with state law.

In light of such conflict between federal laws and state laws regarding cannabis, the previous administration under President Obama had effectively stated that it was not an efficient use of resources to direct federal law enforcement agencies to prosecute those lawfully abiding by state-designated laws allowing the use and distribution of medical cannabis. The new administration under President Trump has indicated that he will strongly enforce the federal laws applicable to cannabis. Any such change in the federal government’s enforcement of current federal laws could cause significant financial damage to us. As we currently directly harvest, distribute and/or sell cannabis, we may be irreparably harmed by a change in enforcement policies of the federal government (see Risk Factors).

The Company and our licensed products will also be subject to a number of other federal, state and local laws, rules and regulations. We anticipate that our vendors and us will be required to manufacture our products in accordance with the Good Manufacturing Practices guidelines and will be subject to regulations relating to employee safety, working conditions, protection of the environment, and other items. The current administration has indicated that it will closely scrutinize the cannabis industry, in particular, recreational marijuana. Changes in laws, rules and regulations or the recall of any product by a regulatory authority, could have a material adverse effect on our business and financial condition.

The United States federal government regulates drugs through the Controlled Substances Act (21 U.S.C. § 811), which places controlled substances, including cannabis, in a schedule. Currently, cannabis and CBD (0.3 percent THC or more) are classified as Schedule I drugs, which are viewed as highly addictive and having no medical value and is illegal to distribute and use. The United States Federal Drug Administration has not approved the sale of marijuana or CBD (0.3 percent THC or more) for any medical application. Doctors may not prescribe cannabis or CBD (0.3 percent THC or more) for medical use under federal law, however they can recommend its use under the First Amendment. In 2010, the United States Veterans Affairs Department clarified that veterans using medicinal cannabis or CBD (0.3 percent THC or more) will not be denied services or other medications that are denied to those using illegal drugs.

| 8 |

Currently, fourty seven States and the District of Columbia have laws legalizing marijuana and CBD in some form. In November 2016, California, Massachusetts, Maine and Nevada all passed measures legalizing recreational marijuana. California’s Prop. 64 measure allows adults 21 and older to possess up to one ounce of marijuana and grow up to six plants in their homes. Other tax and licensing provisions of the law didn’t take effect until January 2018.

These noted state laws, both proposed and enacted, are in direct conflict with the federal Controlled Substances Act, which makes cannabis use and possession illegal on a national level. However, on August 29, 2013, the U.S. Department of Justice issued a memorandum providing that where states and local governments enact laws authorizing cannabis-related use, and implement strong and effective regulatory and enforcement systems, the federal government will rely upon states and local enforcement agencies to address cannabis activity through the enforcement of their own state and local narcotics laws. The memorandum further stated that the U.S Justice Department’s limited investigative and prosecutorial resources will be focused on eight priorities to prevent unintended consequences of the state laws, including distribution of cannabis to minors, preventing the distribution of cannabis from states where it is legal to states where it is not, and preventing money laundering, violence and impaired driving.

On December 11, 2014, the U.S. Department of Justice issued another memorandum with regard to its position and enforcement protocol with regard to Indian Country, stating that the eight priorities in the previous federal memo would guide the United States Attorneys' cannabis enforcement efforts in Indian Country. On December 16, 2014, as a component of the federal spending bill, the Obama administration enacted regulations that prohibit the Department of Justice from using funds to prosecute state-based legal medical cannabis programs.

On January 4, 2018, The Department of Justice lead by Jeff Sessions issued a memo on federal marijuana enforcement policy announcing a return to the rule of law and the rescission of previous guidance documents. Since the passage of the Controlled Substances Act (CSA) in 1970, Congress has generally prohibited the cultivation, distribution, and possession of marijuana.

However, on January 18, 2019, the new Attorney General, William Barr, stated in front of the Senate Judiciary Committee that he does not plan on using federal resources to "go after" companies if they are complying with state law. That would be a reversal from the approach taken by his predecessor, former Attorney General Jeff Sessions, who vowed to pursue federal violations more aggressively. According to Erik Altieri, executive director of the National Organization for the Reform of Marijuana Laws (NORML), Barr's stance is a good sign for advocates but it remains to be seen if his actions will follow through on his pledge. Our business could end and investors could lose their total investment in the company if there is no reversal in Sessions’ approach.

On June 20, 2019, the United States House of Representatives passed a historic bipartisan amendment to the fiscal year 2020 Commerce-Justice-Science spending bill. By a vote of 267-165, the House approved the Blumenauer-McClintock-Norton Amendment which would protect state-legal cannabis programs from interference by the United States Department of Justice (DOJ). The amendment is named after the three individuals who submitted it for consideration: Representative Earl Bluemenauer, a Democrat from Oregon, Tom McClintock, a Republican from California, and Eleanor Norton, a delegate from Washington D.C.

Currently, the spending bill does provide protection for state-legal medical cannabis programs from DOJ interference – but this amendment would protect both medical and recreational cannabis programs that are legal at the state level. The amendment would prohibit the DOJ from using funds to prevent any American state, territory, and Washington D.C. from approving and implementing laws authorizing marijuana use, distribution, possession, and cultivation. What remains uncertain is whether the current Republican-controlled Senate will support the amendment. Further, if the amendment makes it into the final spending bill approved by Congress, it will only remain in effect for one year. If the amendment does not garner approval from the Senate, then the DOJ will maintain the right to use its funding to prevent the approval and implementation of laws regarding recreational cannabis use at the state level, which could affect our business, and could impact our investors’ investment in the Company.

Where You Can Find More Information

We are required to file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). These filings are not deemed to be incorporated by reference into this Form 10-K. You may read and copy any documents filed by us at the Public Reference Room of the SEC, 100 F Street, NE, Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Our filings with the SEC are also available to the public through the SEC’s website at http://www.sec.gov.

| 9 |

Item 1A. Risk Factors .

There are certain inherent risks which will have an effect on our development in the future and the most significant risks and uncertainties known and identified by our management are described below.

Risks Related to Our Company and Our Business

We compete for market share with other companies, including other licensed entities in the United States, some of which have longer operating histories and more financial resources and experience than we have.

We face, and we expect to continue to face, intense competition from licensed cannabis operators, both public and private, and other potential competitors, some of which have longer operating histories and more financial resources and experience than we have. In addition, it is possible that the medical cannabis industry will undergo consolidation, creating larger companies with financial resources, capabilities and product offerings that are superior ours by virtue of size alone. As a result of this competition, we may be unable to maintain our operations or develop them as currently proposed, on terms we consider acceptable, or at all.

There are currently hundreds of applications for cannabis licenses being processed across a number of states. The number of licenses granted and the number of ultimately authorized by each state could have an adverse impact on our ability to compete for market share in the medical cannabis and recreational/adult use cannabis industry. We expect to face additional competition from new market entrants that are granted licenses or existing license holders that are not yet active in the industry in the states in which we currently operate or plan to operate. If a significant number of new licenses are granted in any given market which we participate in, we may experience increased competition for market share and may experience downward price pressure on our medical cannabis products as new entrants increase production.

If the number of users of cannabis for medical and/or recreational purposes increases, the demand for products will increase. This could result in the competition in the cannabis industry becoming more intense as current and future competitors begin to offer an increasing number of diversified cannabis products. Conversely, if there is a contraction in the medical market for cannabis, resulting from the legalization of adult-use cannabis or otherwise, competition for market share may increase.

We face intense competition which could prohibit us from developing a customer base and generating revenue.

The industries within which we plan to compete are highly competitive with companies that have greater capital resources, facilities and greater diversity of operations. More established companies with much greater financial resources which do not currently compete with us may be able to easily adapt their existing operations to our lines of business. Due to this competition, there is no assurance that we will not encounter difficulties in obtaining revenues and market share or in the positioning of our products or that competition in the industry will not lead to reduced prices for our products. Our competitors may also introduce new strains, use competitive, organic techniques or novel application that could also increase competition, decrease demand for our business, and render our methods and craft products obsolete.

If we fail to raise additional capital, our ability to implement our business model and strategy could be compromised.

We have limited capital resources. To date, our operations have been funded by and through our operations, private placements of our securities, and financing from our financing partners. We expect to require substantial additional capital in the near future in order to execute our businesses as planned, to develop and expand our operations, expand our brand in the marketplace, and to establish the targeted levels of production. We may not be able to obtain additional financing on terms acceptable to us, or at all. Even if we obtain financing for our near term operations, we expect that we will require additional capital beyond the near term. If we are unable to raise capital when needed, our business, financial condition and results of operations would be materially adversely affected, and we could be forced to reduce or discontinue our operations.

If we need additional capital to fund our growing operations, we may not be able to obtain sufficient capital and may be forced to limit the scope of our operations.

If adequate additional financing is not available on reasonable terms, we may not be able to expand our business operations and we would have to modify our business plans accordingly. There is no assurance that additional financing will be available to us.

In connection with our growth strategies, we may experience increased capital needs and accordingly, we may not have sufficient capital to fund our future operations without additional capital investments. Our capital needs will depend on numerous factors, including: (i) our profitability; (ii) the release of competitive products by our competition; (iii) the level of our investment in marketing and branding our products; and (iv) the amount of our capital expenditures. We cannot assure you that we will be able to obtain capital in the future to meet our needs.

In recent years, the securities markets in the United States have experienced a high level of price and volume volatility, and the market price of securities of many companies have experienced wide fluctuations that have not necessarily been related to the operations, performances, underlying asset values or prospects of such companies. For these reasons, our securities can also be expected to be subject to volatility resulting from purely market forces over which we will have no control. If we need additional funding we will, most likely, seek such funding in the United States and the market fluctuations effect on our stock price could limit our ability to obtain equity financing.

If we cannot obtain additional funding, we may be required to: (i) limit our expansion; (ii) limit our marketing efforts; and (iii) decrease or eliminate capital expenditures. Such reductions could materially adversely affect our business and our ability to compete.

Even if we do find a source of additional capital, we may not be able to negotiate terms and conditions for receiving the additional capital that are favorable to us. Any future capital investments could dilute or otherwise materially and adversely affect the holdings or rights of our existing shareholders. In addition, new equity or convertible debt securities issued by us to obtain financing could have rights, preferences and privileges senior to our common stock shares. We cannot give you any assurance that any additional financing will be available to us, or if available, will be on terms favorable to us.

| 10 |

The failure to hire additional employees could harm our business.

Our future success also depends upon our continuing ability to attract and retain highly qualified personnel. Expansion of our business and the management and operation will require additional managers, officers, directors and employees with industry experience, and our success will be highly dependent on our ability to attract and retain skilled management personnel and other employees. There can be no assurance that we will be able to attract or retain highly qualified personnel. Competition for honest, diligent and skilled personnel in our industry is significant. This competition may make it more difficult and expensive to attract, hire and retain qualified managers and employees.

If we are unable to deliver consistent, high quality products at sufficient volumes, our relationship with our customers may suffer and our operating results will be adversely affected.

Our customers will expect us to be able to consistently deliver our products at sufficient volumes, while meeting the established quality standards desired to maintain their loyalty to our brands. If we are unable to consistently deliver, our relationship with these customers could be adversely affected, which could have a negative impact on our operating results.

Failure to effectively manage growth of internal operations and business may strain our financial resources.

We intend to significantly expand the scope of our business operations in the near term. Our growth rate may place a significant strain on our financial resources for a number of reasons, including, but not limited to, the following:

| • | The need for continued development of our financial reporting and information management systems; |

| • | The need to manage strategic relationships and agreements with manufacturers, suppliers, customers and partners; and |

| • | Difficulties in hiring and retaining skilled management, technical and other personnel necessary to support and manage our business. |

Additionally, our strategy envisions a period of rapid growth that may impose a significant burden on our administrative and operational resources. Our ability to effectively manage growth will require us to substantially expand the capabilities of our administrative and operational resources and to attract, train, manage and retain qualified management and other personnel. Our failure to successfully manage growth could result in our sales not increasing commensurately with capital investments. Our inability to successfully manage growth could materially adversely affect our business.

If we are unable to continually innovate and increase efficiencies, our ability to attract new customers may be adversely affected.

In the area of innovation, we must be able to develop new management strategies, strains, techniques, products and creative branding that appeal to our customers. This depends, in part, on the technological and creative skills of our personnel and on our ability to protect our intellectual property rights. We may not be successful in the development, introduction, and marketing and sourcing that satisfy customer needs, achieve market acceptance or generate satisfactory financial returns.

Global economic conditions may adversely affect our industry, business and result of operations.

Disruptions in the global credit and financial markets could result in diminished liquidity and credit availability, a decline in consumer confidence, a decline in economic growth, an increased unemployment rate, and uncertainty about economic stability. These economic uncertainties can affect businesses such as ours in a number of ways, making it difficult to accurately forecast and plan our future business activities. Such conditions can lead consumers to postpone spending, which can cause our vendors, suppliers, distributors and retailers to cancel, decrease or delay orders with us. We are unable to predict the likelihood of the occurrence, duration or severity of such disruptions in the credit and financial markets and adverse global economic conditions and such economic conditions could materially and adversely affect our business and the results of operations.

Our business depends substantially on the continuing efforts of our management team and our business may be severely disrupted if we lose their services.

Our current and future success depends substantially on the continued services of our management team, Andrew Bowden, Bryce Skalla, Chris Wolven, Robert Mikkelsen, Ronald L. Miller, Jr., and Jeffrey Rassas. Each brings a unique blend of skill and experience that is essential to the success of our business. We do not maintain key man life insurance for our management team at this time. If our management team is unable or unwilling to continue in their present positions, we may not be able to replace them readily, if at all. Therefore, our business may be severely disrupted, and we may incur additional expenses to recruit and retain new management.

| 11 |

Litigation may adversely affect our business, financial condition and results of operations.

From time to time in the normal course of our business operations, we may become subject to litigation that may result in liability material to our financial statements as a whole or may negatively affect our operating results if changes to our business operation are required. The cost to defend such litigation may be significant and may require a diversion of our resources. There also may be adverse publicity associated with litigation that could negatively affect customer perception of our business, regardless of whether the allegations are valid or whether we are ultimately found liable. As a result, litigation may adversely affect our business, financial condition and results of operations.

Confidentiality agreements with employees and others may not adequately prevent disclosure of our trade secrets and other proprietary information.

Our success depends upon the skills, knowledge and experience of our technical personnel, our consultants and advisors as well as our licensors and contractors. Because we operate in a highly competitive field, we will rely significantly on trade secrets to protect our proprietary techniques and processes. However, trade secrets are difficult to protect. We plan to enter into confidentiality and intellectual property assignment agreements with our corporate partners, employees, consultants, outside scientific collaborators, developers and other advisors. These agreements generally require that the receiving party keep confidential and not disclose to third parties confidential information developed by us during the course of the receiving party’s relationship with us. These agreements also generally provide that inventions conceived by the receiving party in the course of rendering services to us will be our exclusive property. However, these agreements may be breached and may not effectively assign intellectual property rights to us. Our trade secrets also could be independently discovered by competitors, in which case we would not be able to prevent the use of such trade secrets by our competitors. The enforcement of a claim alleging that a party illegally obtained and was using our trade secrets could be difficult, expensive and time consuming and the outcome would be unpredictable. In addition, courts outside the United States may be less willing to protect trade secrets. The failure to obtain or maintain meaningful trade secret protection could adversely affect our competitive position.

Risks Related to Cannabis Industry

Cannabis remains illegal under federal law, and any change in the enforcement priorities of the federal government could render our current and planned future operations unprofitable or even prohibit such operations.

We operate both directly and indirectly in the cannabis industry, which is dependent on state laws and regulations pertaining to such industry; however, under federal law, cannabis remains illegal.

The United States federal government regulates drugs through the Controlled Substances Act (the “CSA”), which places controlled substances, including cannabis, on one of five schedules. Cannabis is currently classified as a Schedule I controlled substance, which is viewed as having a high potential for abuse and having no currently accepted medical use in treatment in the United States. No prescriptions may be written for Schedule I substances, and such substances are subject to production quotas imposed by the United States Drug Enforcement Administration (the “DEA”). Because of this, doctors may not prescribe cannabis for medical use under federal law, although they can recommend its use under the First Amendment.

Currently, 33 U.S. states, the District of Columbia and the U.S. territories of Guam and Puerto Rico allow the use of medical cannabis and 10 states and the District of Columbia have legalized cannabis for “adult use” or recreational use. State and territorial laws are in conflict with the federal CSA, which makes cannabis use and possession illegal at the federal level. Because cannabis is a Schedule I controlled substance, however, the development of a legal cannabis industry under the laws of these states is in conflict with the CSA, which makes cannabis use and possession illegal on a national level. The United States Supreme Court has confirmed that the federal government has the right to regulate and criminalize cannabis, including for medical purposes, and that federal law criminalizing the use of cannabis preempts state laws that legalize its use.

In light of such conflict between federal laws and state laws regarding cannabis, the previous administration under President Obama had effectively stated that it was not an efficient use of resources to direct law federal law enforcement agencies to prosecute those lawfully abiding by state-designated laws allowing the use and distribution of medical cannabis. For example, the prior DOJ Deputy Attorney General of the Obama administration, James M. Cole, issued a memorandum (the “Cole Memo”) to all United States Attorneys providing updated guidance to federal prosecutors concerning cannabis enforcement under the CSA (see “Business—Government and Industry Regulation—The Cole Memo”) [see further discussion below]. In addition, the Financial Crimes Enforcement Network (“FinCEN”) provided guidelines (the “FinCEN Guidelines”) on February 14, 2014, regarding how financial institutions can provide services to cannabis-related businesses consistent with their Bank Secrecy Act (“BSA”) obligations (see “Business—Government and Industry Regulation—FinCEN”).

In 2014, the United States House of Representatives passed an amendment (the “Rohrabacher-Farr Amendment”) to the Commerce, Justice, Science, and Related Agencies Appropriations Bill, which funds the United States Department of Justice (the “DOJ”). The Rohrabacher-Farr Amendment prohibits the DOJ from using funds to prevent states with medical cannabis laws from implementing such laws. In August 2016, a 9th Circuit federal appeals court ruled in United States v. McIntosh that the Rohrabacher-Farr Amendment bars the DOJ from spending funds on the prosecution of conduct that is allowed by state medical cannabis laws, provided that such conduct is in strict compliance with applicable state law. In March 2015, bipartisan legislation titled the Compassionate Access, Research Expansion, and Respect States Act (the “CARERS Act”) was introduced, proposing to allow states to regulate the medical use of cannabis by changing applicable federal law, including by reclassifying cannabis under the Controlled Substances Act to a Schedule II controlled substance and thereby changing the plant from a federally-criminalized substance to one that has recognized medical uses. More recently, the Respect State Marijuana Laws Act of 2017 has been introduced in the U.S. House of Representatives, which proposes to exclude persons who produce, possess, distribute, dispense, administer or deliver marijuana in compliance with state laws from the regulatory controls and administrative, civil and criminal penalties of the CSA.

Although these developments have been met with a certain amount of optimism in the cannabis industry, neither the CARERS Act nor the Respect State Marijuana Laws Act of 2017 have yet been adopted. In addition, the Rohrabacher-Farr Amendment, being an amendment to an appropriations bill that must be renewed annually, has not been renewed beyond December 7, 2018. Furthermore, the ruling in United States v. McIntosh is only applicable in the 9th Circuit, which does include California, Hawaii and Arizona, where we currently primarily operate. The Trump administration could change this policy and decide to strongly enforce the federal laws applicable to cannabis. Any such change in the federal government’s enforcement of current federal laws could cause significant financial damage to us. Because we grow, harvest, distribute or sell cannabis directly, we may be irreparably harmed by a change in enforcement policies of the federal government.

| 12 |

Approach to the Enforcement of Cannabis Laws is Subject to Change

Given the conflicting opinions between state legislatures and the federal government regarding cannabis, investments in United States cannabis businesses are subject to varying legislation and regulation. The Cole Memorandum (the “Cole Memo”), issued in 2013 by former Deputy Attorney General of the United States James M. Cole, served as the response to these inconsistencies, and recognized that notwithstanding the classification of cannabis as a controlled substance at the United States federal level, several states have enacted laws relating to cannabis for medical purposes.

The Cole Memo outlined certain priorities for the Department of Justice relating to the prosecution of cannabis offenses. Particularly, the Cole Memo noted that in those jurisdictions that have enacted laws legalizing cannabis in some form and that have also implemented robust and effective regulatory and enforcement mechanisms to control the cultivation, distribution, sale, and possession of cannabis, conduct in compliance with those laws and regulations is less likely to be a priority at the federal level. Notably, however, the Department of Justice did not provide specific guidelines for what regulatory and enforcement systems it deemed sufficient under the Cole Memo standard.

Considering the limited investigative and prosecutorial resources at hand, the Cole Memo concluded that the Department of Justice should only be focused on addressing the most serious cannabis related threats. Consequently, states where cannabis had been legalized were not branded as a high priority. In March 2017, newly appointed Attorney General Jeff Sessions again noted limited federal resources and acknowledged that much of the Cole Memo had merit; however, he disagreed that the Cole Memo had been successfully implemented. On January 4, 2018, Attorney General Sessions issued the Sessions Memorandum, which effectively rescinded the Cole Memo. The Sessions Memorandum withdrew previous nationwide guidance specific to the prosecutorial authority of United States Attorneys relative to cannabis enforcement on the basis that they are unnecessary, given the well-established principles governing federal prosecution already in place. Those principles are included in Chapter 9.27.000 of the United States Attorneys’ Manual and require federal prosecutors deciding which cases to prosecute to weigh all relevant considerations, including federal law enforcement priorities set by the Attorney General, the seriousness of the crime, the deterrent effect of criminal prosecution, and the cumulative impact of particular crimes on the community.

With the issuance of the Sessions Memorandum, federal prosecutors will now be free to utilize their prosecutorial discretion to decide whether to prosecute cannabis activities despite the existence of state-level laws that may be inconsistent with federal prohibitions. The Sessions Memorandum gave no direction to federal prosecutors as to the priority they should ascribe to such cannabis activities. Therefore, it is ultimately uncertain how active federal prosecutors will be with respect to such activities. Furthermore, the Sessions Memorandum did not how federal prosecutors should treat medical cannabis. At present, medical cannabis is protected against enforcement by United States Congressional legislation through the Leahy Amendment to H.R.1625 – a vehicle for the Consolidated Appropriations Act of 2018 which similarly averts federal prosecutors from applying federal funds to impede the implementation of medical cannabis laws enacted at the state level, subject to Congress’ restoration of such funding. Given the ambiguity of the Sessions Memorandum, there can be no guarantee that the federal government will not seek to prosecute cases involving cannabis businesses that are otherwise compliant with state law.

Such potential proceedings could impose significant restrictions upon the Company, thereby diverting the attention of key executives. In addition, such proceedings could materially adversely affect the Company business, revenues, operating results, and financial condition as well as the Company’s reputation and prospects, even if such proceedings were concluded successfully in the Resulting Issuer’s favor. In the extreme case, such proceedings could ultimately involve the prosecution of key executives of the Company, or the seizure of the corporate assets.

As the possession and use of cannabis is illegal under the CSA, we may be deemed to be engaging in illegal activities through the growth and sales of our products in the future. As a result, we may be subject to enforcement actions by law enforcement authorities, which would materially and adversely affect our business.

Under Federal law, specifically the CSA, the possession, use, cultivation, and transfer of cannabis is illegal. Our business directly involves the possession, use, cultivation, manufacturing and/or transfer of cannabis and derivative therefrom. As a result, law enforcement authorities, in their attempt to regulate the illegal use of cannabis and related products, may seek to bring an action or actions against us and or the businesses who are integral to our supply chain, including, but not limited, to a claim of aiding and abetting another’s criminal activities. The Federal aiding and abetting statute provides that anyone who “commits an offense against the United States or aids, abets, counsels, commands, induces or procures its commission, is punishable as a principal.” 18 U.S.C. §2(a). As a result of such an action, we may be forced to cease operations and our investors could lose their entire investment. Such an action would have a material negative effect on our business and operations.

| 13 |

However, on January 18, 2019, the new Attorney General, William Barr, stated in front of the Senate Judiciary Committee that he doesn't plan on using federal resources to "go after" companies if they are complying with state law. That would be a reversal from the approach taken by his predecessor, former Attorney General Jeff Sessions, who vowed to pursue federal violations more aggressively. According to Erik Altieri, executive director of the National Organization for the Reform of Marijuana Laws (NORML), Barr's stance is a good sign for advocates but it remains to be seen if his actions will follow through on his pledge. Our business could end and investors could lose their total investment in the company if there is no reversal in Sessions’ approach.

On June 20, 2019, the United States House of Representatives passed a historic bipartisan amendment to the fiscal year 2020 Commerce-Justice-Science spending bill. By a vote of 267-165, the House approved the Blumenauer-McClintock-Norton Amendment which would protect state-legal cannabis programs from interference by the United States Department of Justice (DOJ). The amendment is named after the the three individuals who submitted it for consideration: Representative Earl Bluemenauer, a Democrat from Oregon, Tom McClintock, a Republican from California, and Eleanor Norton, a delegate from Washington D.C.

Currently, the spending bill does provide protection for state-legal medical cannabis programs from DOJ interference – but this amendment would protect both medical and recreational cannabis programs that are legal at the state level. The amendment would prohibit the DOJ from using funds to prevent any American state, territory, and Washington D.C. from approving and implementing laws authorizing marijuana use, distribution, possession, and cultivation. What remains uncertain is whether the current Republican-controlled Senate will support the amendment. Further, if the amendment makes it into the final spending bill approved by Congress, it will only remain in effect for one year. If the amendment does not garner approval from the Senate, then the DOJ will maintain the right to use its funding to prevent the approval and implementation of laws regarding recreational cannabis use at the state level, which could affect our business, and could impact our investors’ investment in our Company.

Our business is primarily dependent on state laws pertaining to the cannabis industry.

Currently, fourty-seven states and the District of Columbia currently have laws legalizing marijuana and CBD in some form. Continued development of the cannabis industry is dependent upon continued legislative authorization of cannabis at the state level. Any number of factors could slow or halt progress in this area. Further, progress in the cannabis industry, while encouraging, is not assured. While there may be ample public support for legislative action, numerous factors impact the legislative process. Further legalization attempts at the state level that creates bad public policy could slow or stop further development of the cannabis industry. Any one of these or other factors could slow or halt use of cannabis, which would negatively impact our business model.

The medical and recreational use cannabis industry presents substantial risks and uncertainty.

We plan to be engaged directly in business related to licensed medical cannabis industry in the State of Arizona and medical and recreational in Nevada, among other states. The relatively new development of the medical and recreational use cannabis industry presents numerous and material risks. Many of those risks are not inherent in other developing or mature industries. Many of the risks are unknown and the consequences to our business are speculative. The risks range from the uncertainty as to how the laws and regulations will be applied, to the potential catastrophic collapse of the medical and recreational use cannabis industry nationally or in the states we operate in that might result from changes in laws or the enforcement of existing laws, for example, to the failure of individual businesses that might result from the volatile market conditions that sometimes accompany the development of new markets and industries. Included in the risks is the potential that regulatory authorities could conclude that we provide products and/or engage in other activities that are illegal under the applicable state laws despite the company’s intentions and efforts to not engage in any illegal activities. Such numerous and material risks, the diversity of those risks, and the uncertainty associated with those risks, will likely cause an investment in the Company to be highly speculative and significantly more risky than other similar investments.

We may be unable to secure a local and/or State license to conduct our business, which could lead to a loss in your investment.

Businesses that wish to conduct commercial cannabis operations, either for medicinal or adult-use cannabis, are required to obtain the pertinent municipal and State licenses, dependent on the state. License applications for new operations in each state maintain stringent requirements and are highly competitive; as such, there are no guarantees of license issuance for a license. Failure to secure and maintain a license for our operations would prevent us from legally conducting any commercial cannabis operations in the jurisdictions in which we operate, and thus an investment in our Company carries a great amount of risk.

Our business may be negatively impacted by environmental factors, including unfavorable weather patterns and pesticide contamination.

Cannabis cultivation is an extensive, complicated, and delicate process, and a successful harvest is reliant on a myriad factors including, but not limited to,: lighting, fertilization, technique, sunlight, temperature, and proper application of pesticides. Variance in any one of these factors may result in a tainted or destroyed harvest that will be unfit for distribution. Further, pesticide contamination may prompt recall and public-safety alerts, and any contamination detected may also result in product removal from retail dispensaries.

| 14 |

We may have difficulty accessing the service of banks, which may make it difficult for us to operate.

On February 14, 2014, the U.S. government issued rules allowing banks to legally provide financial services to state-licensed cannabis businesses. A memorandum issued by the Justice Department to federal prosecutors reiterated guidance previously given, this time to the financial industry that banks can do business with legal marijuana businesses and “may not” be prosecuted. The Treasury Department's Financial Crimes Enforcement Network (FinCEN) issued guidelines to banks noting that it is possible to provide financial services to state-licensed cannabis businesses and still be in compliance with federal anti-money laundering laws. The guidance, however, falls short of the explicit legal authorization that banking industry officials had requested the government provide, and, to date, it is not clear if any banks have relied on the guidance to take on legal cannabis companies as clients. The aforementioned policy can be changed, including in connection with the recent change in presidential administration, and any policy reversal and or retraction could result in legal cannabis businesses losing access to the banking industry.

Because the use, sale and distribution of cannabis remains illegal under federal law, most banks will not accept deposits from or provide other bank services to businesses involved with cannabis, and the banks that do provide banking services to companies related to the cannabis industry do not advertise their position and require greater oversight of the depositor relationship. The limited ability to open bank accounts may make it difficult for us to operate.

Although we currently have a bank account, our ability to open additional bank accounts or maintain our current accounts is subject to change. In the future may be difficult or impossible to deposit cannabis related funds and other amounts owed to the Company which may make it difficult for us to do business under the current business plans.

Our insurance coverage may be inadequate to cover all significant risk exposures.

Our business will be exposed to liabilities that are unique to the industry we operate in. While we intend to maintain insurance for certain risks, the amount of our insurance coverage may not be adequate to cover all claims or liabilities, and we may be forced to bear substantial costs resulting from risks and uncertainties of our business. It is also not possible to obtain insurance to protect against all operational risks and liabilities. The failure to obtain adequate insurance coverage on terms favorable to us, or at all, could have a material adverse effect on our business, financial condition and results of operations. Further, we do not have any business interruption insurance. Any business disruption or natural disaster could result in substantial costs and diversion of resources.

Additionally, we may have a more difficult time acquiring insurance that is otherwise readily available, such as property insurance, workers compensation, general liability, and directors and officers insurance, and may become more expensive because we may be deemed to participate either directly or indirectly in the cannabis industry. There are no guarantees that we will be able to find such insurances in the future, or that the cost will be affordable to them. If we are forced to go without such insurances, it may affect our decision business, may inhibit our growth, and may expose us to additional risk and financial liabilities.

Risks Associated with Our Capital Stock

Because we became a reporting company under the Exchange Act by means other than a traditional underwritten initial public offering, we may not be able to attract the attention of research analysts at major brokerage firms.

Because we did not become a reporting company by conducting an underwritten initial public offering, or IPO, of our common stock, and because we will not be listed on a national securities exchange, security analysts of brokerage firms may not provide coverage of our company. In addition, investment banks may be less likely to agree to underwrite secondary offerings on our behalf than they might if we were to become a public reporting company by means of an IPO because they may be less familiar with our company as a result of more limited coverage by analysts and the media, and because we became public at an early stage in our development.

| 15 |

Our common stock may become subject to the SEC's penny stock rules, which may make it difficult for broker-dealers to complete customer transactions and could adversely affect trading activity in our securities.

The SEC has adopted regulations which generally define "penny stock" to be an equity security that has a market price of less than $5.00 per share, subject to specific exemptions. The market price of our common stock may be less than $5.00 per share for some period of time and therefore would be a "penny stock" according to SEC rules, unless we are listed on a national securities exchange. Under these rules, broker-dealers who recommend such securities to persons other than institutional accredited investors must:

| • | make a special written suitability determination for the purchaser; | |

| • | receive the purchaser's prior written agreement to the transaction; | |

| • | provide the purchaser with risk disclosure documents which identify certain risks associated with investing in "penny stocks" and which describe the market for these "penny stocks" as well as a purchaser's legal remedies; and | |

| • | obtain a signed and dated acknowledgment from the purchaser demonstrating that the purchaser has actually received the required risk disclosure document before a transaction in a "penny stock" can be completed. |

If required to comply with these rules, broker-dealers may find it difficult to effectuate customer transactions and trading activity in our securities may be adversely affected.

The market price of our common stock may be volatile and may fluctuate in a way that is disproportionate to our operating performance.

Our stock price may experience substantial volatility as a result of a number of factors, including:

| • | sales or potential sales of substantial amounts of our common stock; | |

| • | the success of competitive products or technologies; | |

| • | announcements about us or about our competitors, including new product introductions and commercial results; | |

| • | the recruitment or departure of key personnel; | |

| • | developments concerning our licensors or manufacturers; | |

| • | litigation and other developments; | |

| • | actual or anticipated changes in estimates as to financial results, development timelines or recommendations by securities analysts; | |

| • | variations in our financial results or those of companies that are perceived to be similar to us; and | |

| • | general economic, industry and market conditions. |

Many of these factors are beyond our control. The stock markets in general, and the market for cannabis companies in particular, have historically experienced extreme price and volume fluctuations. These fluctuations often have been unrelated or disproportionate to the operating performance of these companies. Broad market and industry factors could reduce the market price of our common stock, regardless of our actual operating performance.

We have never paid and do not intend to pay cash dividends.

We do not intend to declare dividends for the foreseeable future, as we anticipate that we will reinvest any future earnings in the development and growth of our business.

Our executive officers and directors, and affiliate shareholders, have the ability to control all matters submitted to stockholders for approval.

Our executive officers, directors, and affiliate shareholders hold collectively 28,324,488 shares of our outstanding common stock or 44.51% of the total vote, and as such, they would be able to control all matters submitted to our stockholders for approval, as well as our management and affairs. For example, these persons, if they choose to act collectively, would control the election of directors and approval of any merger, consolidation or sale of all or substantially all of our assets. This concentration of voting power could delay or prevent an acquisition of our company on terms that other stockholders may desire.

| 16 |

Provisions under Delaware law could make an acquisition of our company more difficult, limit attempts by our stockholders to replace or remove our current management.

In addition to our corporate charter and our bylaws, because we are incorporated in Delaware, we are subject to the provisions of Section 203 of the Delaware General Corporation Law, which generally prohibits a Delaware corporation from engaging in any of a broad range of business combinations with any holder of at least 15% of our capital stock for a period of three years following the date on which the stockholder became a 15% stockholder.

We will incur increased costs as a result of operating as a public reporting company, and our management will be required to devote substantial time to new compliance initiatives.

As a public reporting company, we will incur significant legal, accounting and other expenses that we did not incur as a private company. In addition, the Sarbanes-Oxley Act of 2002 and rules subsequently implemented by the SEC, have imposed various requirements on public companies, including establishment and maintenance of effective disclosure and financial controls and corporate governance practices. Our management and other personnel will need to devote a substantial amount of time to these compliance initiatives. Moreover, these rules and regulations will increase our legal and financial compliance costs and will make some activities more time consuming and costly. For example, we expect that these rules and regulations may make it more difficult and more expensive for us to obtain director and officer liability insurance.

We currently have outstanding, and we may, in the future issue instruments which are convertible into shares of common stock, which will result in additional dilution to you.

We currently have an outstanding instrument which is convertible into shares of common stock, and we may need to issue similar instruments in the future. In the event that these convertible instruments are converted into shares of common stock outstanding stock, or that we make additional issuances of other convertible or exchangeable securities, you could experience additional dilution. Furthermore, we cannot assure you that we will be able to issue shares or other securities in any other offering at a price per share that is equal to or greater than the price per share paid by investors or the then current market price.

Item 1B. Unresolved Staff Comments.

None

| 17 |

Item 2. Properties.