Attached files

| file | filename |

|---|---|

| EX-32.2 - CERTIFICATION - ShiftPixy, Inc. | pixy_ex322.htm |

| EX-32.1 - CERTIFICATION - ShiftPixy, Inc. | pixy_ex321.htm |

| EX-31.2 - CERTIFICATION - ShiftPixy, Inc. | pixy_ex312.htm |

| EX-31.1 - CERTIFICATION - ShiftPixy, Inc. | pixy_ex311.htm |

| EX-23 - CONSENT - ShiftPixy, Inc. | pixy_ex23.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended August 31, 2019 |

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from _____________ to _____________ |

SEC File No. 024-10557

SHIFTPIXY, INC. |

(Exact name of registrant as specified in its charter) |

Wyoming |

| 47-4211438 |

(State of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

| ||

1 Venture Suite 150, Irvine CA |

| 92618 |

(Address of principal executive offices) |

| (Zip Code) |

Registrant’s telephone number:(888) 798-9100

Securities to be registered pursuant to Section 12(b) of the Act:

Common Stock, par value $0.0001 per share |

| The NASDAQ Stock Market LLC |

Title of each class registered |

| Name of each exchange on which each class is registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | ¨ |

Non-accelerated filer | x | Smaller reporting company | x |

Emerging growth company | x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter ($1.53 on February 28, 2019) was approximately $6,980,000.

The number of outstanding shares of Registrant’s Common Stock, $0.0001 par value, was 36,593,762 shares as of December 13, 2019.

| 2 |

| Table of Contents |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS AND INFORMATION

This Annual Report on Form 10-K, the other reports, statements, and information that we have previously filed or that we may subsequently file with the Securities and Exchange Commission (“SEC”), and public announcements that we have previously made or may subsequently make include, may include, incorporate by reference or may incorporate by reference certain statements that may be deemed to be “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and are intended to enjoy the benefits of that act. Unless the context is otherwise, the forward-looking statements included or incorporated by reference in this Form 10-K and those reports, statements, information and announcements address activities, events or developments that ShiftPixy, Inc. (hereinafter referred to as “we,” “us,” “our,” “our Company” or “ShiftPixy”), expects or anticipates will or may occur in the future. Any statements in this document about expectations, beliefs, plans, objectives, assumptions or future events or performance are not historical facts and are forward-looking statements. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “will continue,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would” and “outlook,” and similar expressions. Accordingly, these statements involve estimates, assumptions and uncertainties, which could cause actual results to differ materially from those expressed in them. Any forward-looking statements are qualified in their entirety by reference to the factors discussed throughout this document. All forward-looking statements concerning economic conditions, rates of growth, rates of income or values as may be included in this document are based on information available to us on the dates noted, and we assume no obligation to update any such forward-looking statements. It is important to note that our actual results may differ materially from those in such forward-looking statements due to fluctuations in interest rates, inflation, government regulations, economic conditions and competitive product and pricing pressures in the geographic and business areas in which we conduct operations, including our plans, objectives, expectations and intentions and other factors discussed elsewhere in this Report.

Certain risk factors could materially and adversely affect our business, financial conditions and results of operations and cause actual results or outcomes to differ materially from those expressed in any forward-looking statements made by us, and you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and we do not undertake any obligation to update any forward-looking statement or statements to reflect events or circumstances after the date on which such statement is made or to reflect the occurrence of unanticipated events. The risks and uncertainties we currently face are not the only ones we face. New factors emerge from time to time, and it is not possible for us to predict which will arise. There may be additional risks not presently known to us or that we currently believe are immaterial to our business. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. If any such risks occur, our business, operating results, liquidity and financial condition could be materially affected in an adverse manner. Under such circumstances, you may lose all or part of your investment.

The industry and market data contained in this report are based either on our management’s own estimates or, where indicated, independent industry publications, reports by governmental agencies or market research firms or other published independent sources and, in each case, are believed by our management to be reasonable estimates. However, industry and market data is subject to change and cannot always be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey of market shares. We have not independently verified market and industry data from third-party sources. In addition, consumption patterns and customer preferences can and do change. As a result, you should be aware that market share, ranking and other similar data set forth herein, and estimates and beliefs based on such data, may not be verifiable or reliable.

| 3 |

| Table of Contents |

Item 1. Description of Business

Company Information

ShiftPixy, Inc (PIXY-Nasdaq), “ShiftPixy”, or the “Company” was incorporated under the laws of the State of Wyoming on June 3, 2015. Our principal executive office is located at 1 Venture, Suite 150, Irvine, CA 92618, and our telephone number is (888) 798-9100. Our website address is www.shiftpixy.com. We do not incorporate the information on or accessible through our website into this Report, and you should not consider any information on, or that can be accessed through our website as a part of this Report.

ShiftPixy Human Capital Management Inc., d/b/a ShiftableHR

In December, 2015 we formed Shift Human Capital Management Inc., d/b/a/ ShiftableHR, (“SHCM”) a wholly owned subsidiary. We formed this subsidiary in response to the need to have workers’ compensation policies written in the names of the clients (as may be required by some states) and otherwise in response to client needs for only administrative and processing services rather than the assignment of employees, particularly temporary employees, as offered by ShiftPixy. Under this subsidiary, under circumstances wherein the client remains as the sole employer of the subject employees, we act as a payroll processor, human resources consultant, and administrator of workers’ compensation coverages and claims (providing “administrative services only”). For administrative reasons, we believe that providing these services through a separate legal entity seemed advisable and required, and thus we formed the subsidiary to provide these services. Our goal is to migrate these clients to ShiftPixy. We consolidate all operations of SCHM into the financial statements of ShiftPixy.

Business Overview

Our current business, and the primary source of our revenues to date, has been under a traditional staffing services business model. Our initial market focus is to use this traditional approach, coupled with developed technology, and address an underserved market containing predominately lower wage employees with high turnover, in light industrial, services, and food and hospitality. The Company provides Human Resources, employment compliance, insurance, payroll, and operational employment services solutions for our business clients (“clients”) and shift work or “gig” opportunities for worksite employees (“WSEs”). We receive admin or processing fees as a percentage of a business client’s gross payroll, process and file payroll taxes and payroll tax returns, provide workers compensation insurance, and provide employee benefits. We have built a substantial business on a recurring revenue model since our inception in 2015 and we currently process in excess of $400 million of annualized payroll billings, based on $105 million of payroll billings for our fourth fiscal quarter of 2019. Our business grew in both billings and billable worksite employees in excess of 50% year over year for each year since inception and is expected to continue a high degree of growth. We have experienced losses to date as we have invested in both our technology solutions as well as the back-office operations required to service a large employee base under a traditional staffing model.

We provide services to businesses and we define a “client” as any business paying us to provide employee related services. We are currently focused on clients in the restaurant and hospitality industries, traditionally market segments with high employee turnover and low pay rates; however, we have clients in a variety of other industries as well. All have written client service agreements. The basic client agreement is substantially similar for all clients, with minor modifications to fit each client’s specific situation, and some differences to account for whether the engagement is with ShiftPixy or its wholly owned subsidiary, Shift Human Capital Management Inc.

Our founders’ initial goal was to bring Employment Administration Services (“EAS”) and traditional staffing services (“Staffing”) to an underserved segment of the market; namely small businesses who lack HR and Payroll infrastructure and therefore struggle with the HR compliance requirements and high turnover that is prevalent for many businesses who employ lower income and part time workers. Since our inception in 2015, we have built a client employee pool of over 25,000 persons that is populated by lower wage employees, averaging approximately $22,000 per year and for personnel typically under 35 years of age. We believe that by accumulating together a large number of low-wage and younger employee population, we will obtain a competitive advantage and increase revenues and profits through increased services over and above our base service offering to better serve the younger demographic through our technology solution.

| 4 |

| Table of Contents |

Beginning in 2015, our core business model is to provide payroll services and to facilitate workers compensation insurance to small businesses in exchange for an administration fee calculated as a percentage of their gross payroll. Our initial market focus was to provide a suite of payroll services for small businesses who hire lower income and part-time workers in a high employee turnover environment and struggle to comply with costly employee related “soft” costs such as workers compensation and governmental compliance. We provide such services by employing an operations team consisting of taxation, customer service, HR Compliance, benefits, and workers compensation specialists and which allows us to deliver “best practices” HR, tax compliance, workers compensation insurance, and payroll services at a lower cost than it would cost our clients to provide on their own.

Our revenues through the end of fiscal 2019 primarily consist of admin fees calculated as a percentage of gross payroll processed, payroll taxes due on worksite employees billed to the client and remitted to the taxation authority, and workers compensation premiums billed to the client for which we facilitate workers compensation coverage. Our costs of revenues consist of the accrued and paid payroll taxes and our costs to provide the workers compensation coverage including premiums and loss reserves. A significant portion of our assets and liabilities is for our workers compensation reserves, carried as cash balances, and our estimates of projected workers compensation claims, carried as liabilities. For 2019, we provide a self-funded workers compensation policy up to $500,000 and purchase reinsurance for claims in excess of $500,000. As of August 31, 2019, we have workers compensation related assets that are approximately $1.9 million higher than our projected workers compensation losses, or approximately 25% of the asset total as of August 31, 2019. We also actively and closely monitor and manage our clients and worksite employees’ workers compensation claims which allow us to provide a lower cost option for our clients than they would otherwise be able to purchase on their own. We believe that our customer value proposition is to provide the combination of overall net cost savings to the client as follows:

· Payroll tax compliance and management services · Governmental HR compliance such as for the Affordable Care Act compliance requirements · Reduced client workers compensation premiums or enhanced coverage · Access to an employee pool of potential applicants to reduce turnover costs · Offset by increased administrative fee cost to the client payable to ShiftPixy

Our founders believed that providing this baseline business, coupled with a technology solution to address additional concerns such as employee scheduling and turnover, would provide a unique, cost effective solution to the HR compliance, staffing, and scheduling problems that faced these businesses. Our next goal, currently underway, is to match the small business needs of companies with paying “gigs” with a fully compliant and lower cost staffing solution. For this, we need to acquire a significant number of worksite employees (“WSE”) to provide our paying clients with a variety of solutions for their unique staffing needs and facilitate the employment relationship.

Managing, recruiting, and scheduling a large number of low wage employees can be both difficult and expensive. The acquisition and recruiting of such an employee population is highly labor intensive and therefore have high customer acquisition costs in part due to high onboarding and maintenance costs such as tax information capture or I-9 verification. Early in our history, we evaluated these costs and determined that proper process flows, automated with blockchain and cloud technology and coupled with access to lower cost workers compensation policies resulting from economies of scale could result in a profitable and low-cost scalable business model. To that end,

over the past four years, the Company has invested heavily in a robust, cloud-based Human Resources Information System (HRIS) platform in order to:

· reduce WSE management costs, · automate new WSE and client onboarding, and · provide additional value-add services for our business clients resulting in additional revenue streams to the Company

Beginning in 2017, we began to develop our HRIS database and front-end desktop and mobile phone application to facilitate a lower and easier WSE and client onboarding as well as for additional client functionality and the opportunity for WSEs to find shift work. We outsourced the development and had delays in the launch of our application during 2018 into early 2019 due to delays with our outsourced development partner. Beginning in March 2019, we brought the development of our application in house to complete and launched the initial phase in 2019. As of August 31, 2019, the initial launch was completed and we began to provide some of the HRIS and application services to selected legacy customers on a test basis late in our fiscal year ending August 31, 2019. Subsequent to year end, we continued working to implement additional mobile application and HRIS functionality in delivery, “gig” intermediation services, and scheduling. We expect to launch some of these additional features and services in the fourth calendar quarter of 2019. We see these technology based services as multiple potential revenue drivers with limited additional costs.

| 5 |

| Table of Contents |

Our cloud-based HRIS platform captures, holds, and processes HR and payroll information for the clients and WSEs through an easy to use customized front end interface coupled with a secure, remotely hosted database. The HRIS system can be accessed by either a desktop computer or an easy to use electronic mobile phone application designed with legally binding HR workflows in mind. Once fully implemented, we expect to reduce the time, expense, and error rate for on boarding our client employees into our HRIS ecosystem and thereby have created a technological solution for employers and their workers. Once onboarded, the client employees are included as our worksite employees and who are available for shift work within our business ecosystem. This allows our HRIS platform to serve as a “gig” marketplace for WSEs and clients and allows for client businesses to better manage their staffing needs.

As of August 31, 2018, ShiftableHR and ShiftPixy had a combined client list of 193 clients with approximately 8,500 worksite employees. As of August 31, 2019, we had 246 clients with over 13,000 WSEs and processed payroll of over $350 million during our fiscal year ending August 31, 2019, an increase of nearly 60% from August 2018 . Of these WSEs, approximately 60% represent workers in the restaurant industry. We have an additional 12,000 WSEs as of August 31, 2019 that were retained in our HRIS system that were not active WSEs as of August 31, 2019 but which are available for “gig” opportunities.

Our Services:

To date, and throughout fiscal 2019, the core ShiftPixy client services were to provide regular payroll processing services under an employer administration services (“EAS”) model with “a la carte” additional services added as can be seen illustrated. Our payroll processing fee is typically a percentage of the gross payroll processed. We also provide workers compensation and payroll tax remittance and reporting as core services for most of our clients with additional services such as benefits administration and human resources services for additional fees. Beginning in fiscal 2020, with the full commercial launch of our mobile application software, we will provide additional services for employee scheduling and delivery as described in greater detail below.

|

| Figure 1

|

Our core EAS services are provided via standard legal contracts with our business clients, customized for each client’s specific needs and that are typically one year in length and are cancelable with 30 days’ notice. Through August 31, 2019, we have not had any material revenues or billings generated within our HRIS from additional value-added services. We consider our future service offering to be the future of the company and which will provide for additional revenue streams and support cost reductions for existing and future business clients. Future services, including technology based services provided through our HRIS system and mobile application will be through “a la carte” pricing via customizable on-line contracts.

We provide our solution in the developing nextGEN or “gig” economy primarily by absorbing our clients’ workers, who we call worksite employees (WSEs) but may also be called “shift workers,” “shifters,” “gig workers,” or “assigned employees.” WSEs are carried under a ShiftPixy corporate employee umbrella and we shoulder certain employment-related compliance responsibilities for our business clients as part of our services provided. This arrangement benefits the WSEs by opening additional work opportunities through access to other shift work with other ShiftPixy clients. The WSE further benefits from employee status benefits through ShiftPixy’s benefit plan offerings, including minimum essential health insurance coverage plans and a 401(k) plan while enjoying the protections of workers’ compensation coverage and employment laws.

| 6 |

| Table of Contents |

Technological Solution:

At the heart of ShiftPixy’s employment service solutions is a secure, cloud-based HRIS database accessible by a desktop or mobile device through which ShiftPixy worksite employees will be enabled to find available shift work at ShiftPixy client locations. This solution solves a problem of finding available shift work for both the shifters looking for additional shift work and business clients looking to fill open shifts. For new WSEs, the mobile platform includes an easy to use WSE onboarding functionality which we believe will increase our WSE pool of workers that will provide a deep bench of worker talent for our business clients. The onboarding feature of our software enables us to capture all application process related data regarding our assigned employees and to introduce employees to and integrate them into the ShiftPixy Ecosystem. The mobile platform features a Pixy chatbot that leverages artificial intelligence to aid in gathering the data from workers via a series of questions designing to capture all required information, including customer specific and governmental information. Final onboarding steps requiring signatures can also be prepared from the HRIS onboarding module. |

| Figure 2

|

In 2019, we implemented additional functionality to provide a scheduling component of our software, which enables each client worksite to schedule workers and to identify shift gaps that need to be filled. We utilize artificial intelligence to maintain schedules and fulfillment, using an active methodology to engage and move people to action. We began using this functionality at the end of fiscal 2019 on a test basis.

The final phase of our initial platform, deployed in late fiscal 2019 on a test basis, consists of our “shift intermediation” functionality, which is designed to enable our WSE shift workers to receive information regarding and to accept available shift work opportunities. The intermediation functionality becomes useful only to the extent that we have meaningful numbers of available workers and client shift opportunities in the same geographic region. We reached geographical concentration in Southern California during 2019 and we activated these key features in August 2019 to a limited group of customers on a test basis.

Our goal is to have a mature and robust hosted cloud based HRIS platform coupled with a seamless and technically sophisticated mobile phone application (“App”) that will act as both a revenue generation system as well as a “viral” customer acquisition engine through the combination of the scheduling, delivery, and intermediation features and interactions. We believe that once a critical mass of clients and WSEs is achieved, additional shift opportunities will be created pulling in additional WSEs and additional client businesses in food service and hospitality industries. Our approach to achieving this critical mass is to market our services to restaurant owners and franchisees, focusing on specific brands and geographical locations. We expect critical mass to be a function of both geography, such as in Southern California for viral adoption by WSEs and clients, or by adoption within franchise brands for viral adoption by clients.

| 7 |

| Table of Contents |

Markets and Marketing

Our initial market focus was chosen based on our understanding of the issues and challenges facing “Quick Service Restaurants” (“QSRs”), including fast food franchises and local restaurants. We have chosen to invest in two key features of our mobile application to this end consisting of: i) scheduling functionality, designed to enhance the client’s experience through scheduling of employees and reducing the impact of turnover and ii) delivery functionality, designed to increase revenues through delivery fulfillment as well as to bring “in house” the delivery fulfillment and thereby reducing delivery costs.

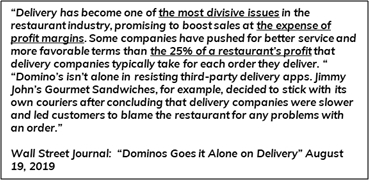

One of the most recent developments in the food and hospitality industry is the rapid rise of third-party restaurant delivery providers such as Uber Eats, GrubHub, and DoorDash. These providers have successfully increased QSR revenue in many local markets by providing food delivery to a wide-scale audience using contract delivery drivers. We have observed two significant issues with our clients and third-party delivery providers which is increasingly being reported in the news media with companies like Dominos Pizza and Jimmy Johns franchises providing their own delivery services and avoiding third party delivery services. The first issue is the very large revenue share typically being paid to many of these third-party delivery providers as delivery fees. These additional costs erode the profit for the QSRs from those additional sales made through this delivery channel. The second is that our QSR customers have encountered problematic deliveries of their food products - late deliveries, cold food, missing accessories, and unfriendly delivery people. This in turn has caused significant “brand erosion” in many cases and has caused these clients to reconsider third-party delivery. |

| Figure 3

|

We provide a solution to the third-party delivery issues. We designed our HRIS platform to manage food deliveries by the QSRs using internal personnel and a customized “white label” smart phone App. Our recently released delivery feature links this “white label” delivery ordering system to our delivery solution, thereby freeing the QSR to have their own brand showcasing an ordering APP but retaining similar back-office delivery technology including scheduling, ordering, and delivery status pushed to a customer’s smart phone. Our technology and approach to human capital management allows the company a unique window into the daily demands of QSR operators and the ability to extend our technology and engagement to enable this unique self-delivery proposition. ShiftPixy’s new driver management layer for operators in the ShiftPixy ecosystem will now allow clients to use their own team members to deliver a brand intended customer experience. ShiftPixy’s mobile platform now provides the HR compliance, management and insurance solutions necessary to the support of a delivery option and created a turnkey self-delivery opportunity for the individual QSR operator. Our solution saves delivery costs to the QSR client and allows them to retain the customer information and quality control over the food delivery.

The first phase of this component of our platform is the driver onboarding, which was completed in 2019. The enhanced features will also “micro meter” the essential commercial insurance coverages required by our operator clients on a delivery-by-delivery basis (workers’ compensation and auto coverages) which has been a significant barrier for some QSRs to provide their own delivery services. We began using the “delivery features” of our mobile platform for selected customers on a trial basis in the fourth quarter of fiscal 2019 and expect to fully deploy the solution in fiscal 2020.

| 8 |

| Table of Contents |

A significant problem for small businesses and in particular businesses in the food service industry such as QSRs, involve compliance with employment related regulations imposed by federal, state and local governments. Requirements associated with workers’ compensation insurance, and other traditional employment compliance issues, including the employer mandate provisions of the Patient Protection and Affordable Care Act (the “ACA”) create compliance challenges and increased costs. The compliance challenges are often complicated by “workaround” solutions that many employers resort to in order to avoid characterizing employees as “full-time” and which in turn requires increased compliance to avoid fines and penalties. To date, the U.S. Congress has considered but not passed an amendment to replace the ACA other than the removal of the individual mandate provision in 2017. Despite the removal of the individual mandate, employers still face regulatory issues and overhead costs for which we believe our services are a cost-effective solution.

Other regulation is prevalent at the State and Local levels. Recently in California, where most of our worksite employees reside, legislation was passed that more clearly defines “Gig” workers for companies such as Lyft or Uber as employees rather than their previous classification as independent contractors. We believe that legislation such as this is a direct response to a considerable loss of tax revenue from the “Gig” companies’ contract employees, and that there is an increasing likelihood that workers in other states will have to be treated as employees within the next few years. The effective date for the California legislation is January 2020, although both Lyft and Uber are aggressively filing appeals to avoid these reclassifications. By comparison, we have designed our HRIS platform solution to classify our WSEs as employees and thereby be well positioned to provide HR services for companies that are impacted by the change from independent contractors to employees.

Figure 4

The worldwide trend toward a Gig Economy resulting from the market adoption of smart phones and mobile telephones and remote office workers moving away from the traditional 9 to 5 office or factory workplace. For our target worksite employee audience, as of February 2019, over 92% of 18-30-year-old workers have, or use, a “smart” mobile telephone. This development has created opportunities for companies catering to the use of these devices. We have designed our mobile application (“App”) to utilize the mobile smart phone adoption to create an easy to use on-boarding tool for potential employees. The migration towards a Gig Economy trend is also significant and according to a 2016 study conducted by Ardent partners, nearly 42% of the world’s total workforce is now considered ‘non-employee,’ which includes contingent/contract workers, temporary staff, gig workers, freelancers, professional services, and independent contractors. (Ardent Partners Ltd. “The State of Contingent Workforce Management 2016-2017: Adapting to a New World of Work.” October 2016). Our initial focus in the marketing of our product to the larger Gig Economy is to small and medium sized businesses with high worker turnover such as the restaurant and hospitality industries who have high turnover and often contract with independent contractor workers to perform less than full-time gig engagements, primarily in the form of shift work.

We are also joining the hot topic dialogue currently going on in the nextGEN Gig Economy about companies such as Uber and others and we see a potential new market based upon the issue of worker misclassification in the Gig Economy. Gig Economy companies such as Uber may typically classify the people working for them as “independent contractors” rather than “employees” for jobs (gigs). The companies can pay much less for services and in regulatory requirements if their workers are classified as independent contractors. Under state and federal employment laws, workers classified as employees are much more expensive for these companies. However, increasing legal and regulatory pressure against Uber and others has increased awareness about this issue. Most recently, in the State of California, legislation has passed that would require Uber, Lyft, and other shift companies to convert their previously classified independent contractors to employee status. ShiftPixy management foresaw this regulatory change and provides a solution by absorbing workers for these types of Gig Economy companies as employees of ShiftPixy, eliminating any risk of litigation, fines and other worker misclassification problems for these types of Gig Economy companies to the extent they become ShiftPixy clients.

| 9 |

| Table of Contents |

Figure 5

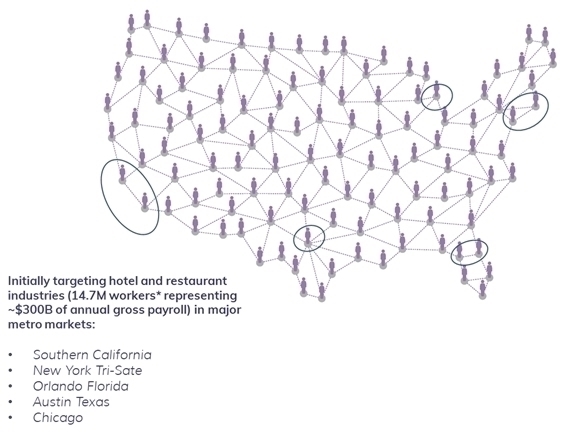

ShiftPixy’s headquarters is currently situated in Irvine, California, from which it can reach the Southern California market and has a geographical presence via sales offices in New York, Austin, Texas, Chicago and the Orlando area from which its local sales/services representatives will secure and service clients in those areas, and it plans to open additional physical offices in San Francisco and Miami. Through these office locations, we plan to engage more actively with clients through sales, marketing, employee onboarding, training and payroll processing, in each instance as necessary and appropriate to the applicable market. These markets collectively account for or allow us to cover approximately 53% of our target market in the restaurant/hospitality sectors. (U.S. Department of Labor. Bureau of Labor Statistics. May 2015. Occupational Employment and Wages.).

| 10 |

| Table of Contents |

We believe ShiftPixy will experience business and revenue growth in the nextGEN Gig Economy from the following factors:

| · | Large Potential Market. Current statistics show that there are over 14.7 million employees working in our current target market--the restaurant and hospitality industries representing over $300 billion of annual revenues. (U.S. Department of Labor. Bureau of Labor Statistics. February 2018). Compared to the total workforce in all industries, workers in the restaurant industry have a notably higher percentage of part-time workers. (National Restaurant Association. “News & Research: Restaurant middle class job growth 4x stronger than overall economy.” 13 January 2016). At our current monetization rate per employee, this represents an annual revenue opportunity of over $9 billion per year for the United States. Our current geographic presence in California, New York City and parts of Texas, Illinois, and Florida provides coverage of over 50% of this opportunity. Our intention is to expand both our geographic footprint and our service offerings into other industries, particularly where part-time work is a significant component of the applicable labor force, including the retail and health care sectors. |

| · | Rapid Rise of Independent Workers. The number of independent workers, totaling approximately 41 million in 2018, is expected to increase to 40% of the private, non-farm U.S. workforce by 2021. (MBO Partners. “America’s Independents / A Rising Economic Force / 2016 State of Independence in America Report / Sixth Annual.” 2016.). As of early 2019, approximately 48% of the U.S. workforce has worked as an independent employee as either part time or on a contract basis (Source: http://www.mbopartners.com/state-of-independence). |

| · | Technology Affecting and Attitudes towards Employment Related Engagements. Gig-economy platforms have changed the way part-time workers can identify and connect to work opportunities, and Millennials and others have embraced such technologies as a means to secure short-term employment related engagements. The significant increase in the adoption of smart phone devices has provided the “last mile” platform to enable technology solutions such as ours to provide a gig economy platform. Most importantly, for our target audience of 18-35 year old workers as of February 2019, 92% of these workers regularly use a smart phone (Source: Pew Research Center). |

| · | New ShiftPixy Mobile App is Designed to Provide Additional Benefits to Employers and NextGen Shift Workers. Millennials represent approximately 40% of the independent workforce who are over the age of 21 and who work 15 hours or more each week. (MBO Partners. “America’s Independents / A Rising Economic Force / 2016 State of Independence in America Report / Sixth Annual.” 2016.) Mindful that most of its shifters will be Millennials who connect with the outside world primarily through a mobile device, ShiftPixy is poised to significantly expand its business through the ShiftPixy mobile app. The ShiftPixy mobile app is a proprietary application downloaded to mobile devices, allowing ShiftPixy’s shifters to access shift work opportunities at all of ShiftPixy’s clients, not just their current restaurant or hospitality provider, and with an added feature, anticipated to be available in the first calendar quarter of 2020, also allowing shift employees not working at its clients to access shift work opportunities at all of its clients. |

| 11 |

| Table of Contents |

Figure 6

The ShiftPixy Ecosystem Solution: ShiftPixy has developed an HRIS Ecosystem comprised of a closed proprietary operating and processing information system that provides a tool for businesses needing staffing flexibility to schedule existing employees and to post open schedule slots to be filled by an available pool of shift workers. The ShiftPixy Ecosystem provides the following benefits to our clients:

| 1. | Compliance: ShiftPixy assumes a substantial portion of a business’s employment regulatory compliance issues by having all of client shifter employees become employees of ShiftPixy. As the employer of the WSEs, ShiftPixy can assist its clients with the staffing of their shift employee requirements by providing a qualified pool of potential applicants or as shift workers. The individual WSE is a legal employee of ShiftPixy and ShiftPixy thereby provides employment regulatory compliance reporting, taking this burden away from the ShiftPixy client. The client’s management time spent on compliance issues substantially reduced and allows client management to focus on their business. |

|

|

|

| 2. | Operational improvements: Our service can reduce the impact of high turnover, which is a consistent problem across the restaurant industry and a significant issue to our clients. Our service provides pre-screened applicants for permanent positions as well as the access to the ShiftPixy Ecosystem population of potential shift workers. The flexibility inherent in the Ecosystem approach can better tailor the staffing needs of a client to the talent pool available. |

|

|

|

| 3. | Cost Savings: The payroll and related costs associated WSEs such as workers compensation and benefits are consolidated and charged, in effect, in conjunction with the shifters’ applicable rates of pay, allowing the clients to fund the employment related costs as the services are used--thereby avoiding various lump sum employment-related cost impositions. Cost savings for our clients can be varied but in general we see cost reductions in reduced overhead costs related to HR compliance, payroll processing, and elimination of non-compliance fines and related penalties. We also see a reduction in the impact of high turnover and the related costs of that high turnover. ShiftPixy is able to use economies of scale in purchasing employer related solutions such as workers’ compensation and other benefits and in general can provide a shift worker to a business at a lower cost than the business can otherwise typically staff a particular position. |

|

|

|

| 4. | Improved human resources management: By having access to ShiftPixy’s entire part-time workforce, a client business is enabled to scale up or down more rapidly, making it easier to contain and manage operational costs. The two largest costs for a restaurant are food and labor. (National Restaurant Association “Restaurant Operations Report 2013-2014.) ShiftPixy charges a fixed percentage on wages that allows the client business to budget and plan more effectively without the full weight associated with the threats of penalties or missteps in dealing with employment law compliance related issues. |

ShiftPixy and its subsidiary collectively serve, as of August 31, 2019 an aggregate of 246 clients, with an aggregate of approximately 13,000 employees. None of these clients represents more than 10% of our revenues for fiscal year 2019.

| 12 |

| Table of Contents |

Competition

We see two primary sources of competition with no one competitor addressing both. Competitors to our “gig” business model include businesses such as ShiftGig, Instawork, Snag, Jobletics and other comparable businesses that seek to arrange short-term work assignments for both employees and independent contractors. Competitors to our HRIS Ecosystem, which encompasses on a broad scale, the assignment of a workforce to businesses on a long-term basis, include businesses such as Insperity, TriNet Group, and Just Works, and the assignment of individual workers to businesses generally on a short-term basis include businesses such as Kelly Services, ManpowerGroup, and Barrett Business Services.

We believe our service offering competes effectively based on our strategy of combining an Ecosystem of employment services with the individualized ability to link trained workers to specific shift work opportunities.

Governmental Regulation

Our business operates in an environment that is affected by numerous federal, state and local laws and regulations relating to labor and employment matters, benefit plans and income and employment taxes. Moreover, because our client engagements involve some form of co-employer relationship with regard to the employees who provide services in employment to our clients, the application of such laws to these non-traditional employer relationships can become complex. Nearly all states have adopted laws or regulations regarding the licensure, registration or certifications of organizations that engage in co-employer relationships. While our model is currently not included in such regulations, we may become subject to such laws and regulations when we enter into co-employer relationships with regard to employees providing services in the jurisdictions where such laws and regulations apply.

The following summarizes what we believe are the most important legal and regulatory aspects of our business:

Federal Regulations

Employer Status

We sponsor certain employee benefit plan offerings as the “employer” of our shift workers under the Internal Revenue Code of 1986 (the “Code”) and ERISA. The multiple definitions of “employer” under both the Code and ERISA are not clear and most are defined in part by complex multi-factor tests under common law. We believe that we qualify as an “employer” of our shift workers under both the Code and ERISA, as well as various state regulations, but this status could be subject to challenge by various regulators. For additional information on employer status and its impact on our business and results of operations, refer to Item 1A of this Form 10-K, under the heading, “If ShiftPixy is not recognized as an employer of worksite employees under federal and state regulations, or we are deemed to be an insurance agent or third-party administrator, we and our clients could be adversely impacted.”

Affordable Care Act and Health Care Reform

The Patient Protection and Affordable Care Act (the “ACA”) was signed into law in March 2010. The ACA implemented substantial health care reforms with staggered effective dates continuing through 2020, and many provisions in the Act require the issuance of additional guidance from applicable federal government agencies and the states. There could be significant changes to the ACA and health care in general, including the potential modification, amendment or repeal of the ACA. For additional information on the ACA and its impact on our business and results of operations, refer to Item 1A of this Form 10-K, under the heading, “Failure to comply with, or changes in, laws and regulations applicable to our business, particularly potential changes to the ACA, could have a materially adverse effect on our marketing plan as well as our reputation, results of operations or financial condition, or have other adverse consequences.” As of the date of this filing, the ACA has not been formally amended or repealed; however, the Tax Cuts and Jobs Act of 2017 effectively eliminates the individual mandate provisions of the ACA, beginning in 2019.

| 13 |

| Table of Contents |

Health Insurance Portability and Accountability Act

Maintaining the security of information regarding our employees is important to us as we sponsor employee benefit plans and may have access to personal health information of our employees. The manner in which we manage protected health information (PHI) is subject to the Health Insurance Portability and Accountability Act of 1996 (HIPAA), and the Health Information Technology for Economic and Clinical Health Act of 2009 (HITECH Act). HIPAA contains substantial restrictions and health data privacy, security and breach notification requirements with respect to the use and disclosure of PHI. Further, under the HITECH Act there are steep penalties and fines for HIPAA violations. Our health plans are covered entities under HIPAA, and we are therefore required to comply with HIPAA’s portability, privacy, and security requirements. For additional information regarding the information we collect, how we maintain the confidentiality of our clients’ and employees’ confidential information and the potential impact to our business if we fail to protect the confidentiality of such data, refer to Item 1A of this Form 10-K, under the heading, “We host, collect, use, transmit and store personal and business information, and a security or privacy breach may damage or disrupt our businesses, result in the disclosure of confidential information, damage our reputation, increase our costs and cause losses.”

State Regulations

Nearly all states have adopted provisions for licensing, registration, certification or other formal recognition of co-employers. Such laws vary from state to state but generally provide for monitoring or ensuring the fiscal responsibility of a professional employer organization, and in some cases codify and clarify the co-employment relationship for unemployment, workers’ compensation and other purposes under state laws. The scope of the laws and regulations of states is such that it encompasses the activities of ShiftPixy, Inc., as well as its subsidiary, ShiftableHR. In addition, many state laws require guarantees by ShiftPixy, Inc. of the activities of its subsidiary, ShiftableHR, and in some states we may seek licensure, registration or certification, as applicable, of ShiftPixy, Inc., with its subsidiary, ShiftableHR, because the financials for both organizations are consolidated. We believe we are in compliance in all material respects with the requirements in the states wherein we are conducting business.

We must also comply with state unemployment tax requirements where our clients are located. State unemployment taxes are based on taxable wages and tax rates assigned by each state. The tax rates vary by state and are determined, in part, based on our prior years’ compensation and unemployment claims experience in each state. Certain rates are also determined, in part, by each client’s own compensation and unemployment claims experience. In addition, states have the ability under law to increase unemployment tax rates, including retroactively, to cover deficiencies in the unemployment tax funds.

| 14 |

| Table of Contents |

Intellectual Property

ShiftPixy has registered a trademark in its name, and a copyright in its “Pixy” image. In addition, the company has submitted a patent application in connection with certain features of its mobile application. ShiftPixy has other intellectual property and related rights as well, particularly in connection with our software. We believe that our intellectual property is of considerable importance to our business.

Employees

As of August 31, 2019, we employed 67 people on a full-time basis in our corporate offices, and we served approximately 13,000 active, paid worksite employees with an additional 12,000 inactive worksite employees carried within our HRIS platform.

Available Information

We are a public company and file annual, quarterly and special reports and other information with the SEC. We are not required to, and do not intend to, deliver an annual report to security holders. You may read and copy any document we file at the SEC’s public reference room at 100 F Street, N.E., Washington, D.C. 20549. You can request copies of these documents by writing to the SEC and paying a fee for the copying cost. Please call the SEC at 1-800-SEC-0330 for more information about the operation of the public reference room. Our filings are also available, at no charge, to the public at http://www.sec.gov.

Information Disclosures

Consistent with the SEC’s April 2013 guidance on using social media outlets like Facebook and Twitter to make corporate disclosures and announce key information in compliance with Regulation FD, ShiftPixy is alerting investors and other members of the general public that ShiftPixy will provide updates on operations and progress required to be disclosed under Regulation FD through its social media on Facebook, Twitter and YouTube. Investors, potential investors, shareholders and individuals interested in our Company are encouraged to keep informed by following us on Twitter, YouTube or Facebook.

Facebook: http://www.facebook.com/shiftpixy

Twitter: http://www.twitter.com/shiftpixy

YouTube: http://www.youtube.com/shiftpixy

Our operations and financial results are subject to various risks and uncertainties, including those described below, that could adversely affect our business, financial condition, results of operations, cash flows, and the trading price of our common stock. Some statements in this Report, including statements in the following risk factors, constitute forward-looking statements. Please refer to the section entitled “Cautionary Statement Regarding Forward-Looking Statements.”

| 15 |

| Table of Contents |

Risks Relating to Our Business

We have limited operating history, which makes it difficult for us to evaluate our future business prospects and make decisions based on those estimates of our future performance.

We are an emerging business and are in the process of developing our products and services. We have been in business for 50 months as of August 31, 2019. Although we have now processed gross billings of over $350 million for the fiscal year ended August 31, 2019 it is still difficult, if not impossible, to forecast our future results based upon our limited but now improving historical operating data. Because of the related uncertainties, we may be hindered in our ability to anticipate and timely adapt to increases or decreases in sales, revenues or expenses. If we make poor budgetary decisions as a result of unreliable data, our gross billings in the future may decline, which may result in a decline in our stock price.

There is uncertainty regarding our ability to implement our business plan and to grow our business to a greater extent than we can with our existing financial resources without additional financing. Except from the proceeds of our initial public offering (“IPO”) and our recent private placements of senior secured convertible notes to institutional investors raising $13 million of gross proceeds ($11.9 million net of costs), we have no binding agreements, commitments or understandings to secure additional financing at this time. We have no binding agreements, commitments or understandings to acquire any other businesses or assets. Our long-term future growth and success is dependent upon our ability to generate cash from operating activities. There is no assurance that we will be able to generate sufficient cash from operations, to borrow additional funds or to raise additional equity capital. Our inability to obtain additional cash could have a material adverse effect on our ability to fully implement our business plan as described herein and grow our business to a greater extent than we can with our existing financial resources.

We have incurred net losses in recent periods and may require additional financing. If financing is not available, we may be required to further downsize or discontinue operations.

As of August 31, 2019, the Company had cash of $1.6 million and a working capital deficiency of $15.9 million. During the year ended August 31, 2019, the Company used approximately $2.4 million of cash in operations and an additional $1.1 million on capitalized software and fixed asset purchases. The Company has incurred recurring losses resulted in an accumulated deficit of $45 million as of August 31, 2019. These conditions raise substantial doubt as to the Company’s ability to continue as going concern within one year from issuance date of the financial statements, and our independent registered public accounting firm has included an explanatory paragraph regarding going concern qualification in its audit report. Management has prepared a liquidity plan to address the going concern and while we believe that these liquidity plan measures will be adequate to satisfy our liquidity requirements for the twelve months ending November 28, 2020, there is no assurance that the liquidity plan will be successfully implemented. Failure to successfully implement the liquidity plan may have a material adverse effect on our business, results of operations and financial position, and may adversely affect our ability to continue as a going concern. If we do not become consistently profitable, our accumulated deficit will grow larger and our cash balances will decline further, and we will require additional financing to continue operations. Any such financing may not be accessible on acceptable terms, if at all. If we cannot generate sufficient cash or obtain additional financing, we may be required to downsize our business further or discontinue our operations altogether.

| 16 |

| Table of Contents |

Our success depends on adoption of our products and services by our various types of customers, and if these potential customers do not accept and acquire our products and services then our revenue will be severely limited.

The major customer groups to whom we believe our products and services will appeal, both employers and employees, particularly related to shift work, may not embrace our products and services. Acceptance of our products and services will depend on several factors, including: cost, ease of use, familiarity of use, convenience, timeliness, strategic partnerships, and reliability. If we fail to adequately meet our customers’ needs and expectations, our product offerings may not be competitive and our ability to commence or continue generating revenues could be reduced. We also cannot be sure that our business model will gain wide acceptance among all targeted customer groups. If the market fails to continue to develop, or develops more slowly than we expect, our ability to continue generating revenues could be reduced.

The Company assumes the obligation to make wage, tax, and regulatory payments for our shifter employees, and, as a result, is exposed to client credit risks.

Under the Contract Service Agreement (“CSA”), we become a co-employer of worksite employees and assume the obligations to pay the salaries, wages and related benefits costs and payroll taxes of such worksite employees. We assume such obligations as an agent, not as a principal, of the client. Our obligations include responsibility for:

| · | payment of the salaries and wages for work performed by worksite employees, regardless of whether the client timely pays us the associated service fee |

| · | withholding and payment of federal and state payroll taxes with respect to wages and salaries reported by the Company. |

If a client does not pay us, our ultimate liability for worksite employee payroll and benefits costs could have a material adverse effect on our financial condition or results of operations.

If we are unable to effectively manage growth and maintain low operating costs, our results of operations and financial condition may be adversely affected.

We have experienced rapid growth since our inception, and our plans contemplate significant expansion of our business. If we are unable to manage our growth effectively, including having geographically dispersed offices and employees or to anticipate and manage our future growth accurately, our business may be adversely affected. If we are unable to manage our expansion and growth effectively, we may be unable to keep our operating costs low or effectively meet the requirements of an ever-growing, geographically dispersed client base. Our business relies on data systems, billing systems and financial reporting and control systems, procedures and controls. Our success in managing our expansion and growth in a cost-effective manner will require us to upgrade and improve these systems, procedures and controls. If we are unable to adapt our systems and put adequate controls in place in a timely manner, our business may be adversely affected. In addition, our growth may place significant demands on our management, and our overall operational and financial resources. A failure on our part to meet any of the foregoing challenges inherent in our growth strategy may have an adverse effect on our results of operations and financial condition.

Our targeted customer base is diverse, and we face a challenge in adequately meeting each group’s needs.

Because we will serve both employers and employees, we must work constantly to understand the needs, standards and requirements of each group and must devote significant resources to developing products and services for their interests. If we do not accurately predict our customers’ needs and expectations, we may expend valuable resources in developing products and services that do not achieve broad acceptance across the markets, and we may fail to grow our business.

| 17 |

| Table of Contents |

We face intense competition across all markets for our services, which may lead to lower revenue or operating margins. Competing forms of Gig Economy oriented staffing management products and services may be more desirable to consumers or may make our products and services obsolete.

Our competitors range in size from diversified global companies with significant research and development resources to small, specialized firms whose narrower service lines may let them be more effective in deploying technical, marketing, and financial resources. Barriers to entry in many of our businesses are low and many of the areas in which we compete evolve rapidly with changing and disruptive technologies, shifting user needs, and frequent introductions of new products and services. Our ability to remain competitive depends on our success in making innovative products, devices, and services that appeal to customers.

Companies compete with us based on a growing variety of business models. The competitive pressures described above may cause decreased sales volumes, price reductions, and/or increased operating costs, such as for research and development, marketing, and sales incentives. This may lead to lower revenue, gross margins, and operating income.

There are currently several different competing Gig Economy oriented staffing management product and service technologies that are being marketed to our potential customers. Further development of any of these technologies may lead to advancements in technology that will make our products and services obsolete. Consumers may prefer alternative technologies and products and services. We cannot guarantee that users of Gig Economy oriented staffing management products and services who will be using our products and services will continue to grow within the industry as a whole. Any developments that contribute to the obsolescence of our products and services may substantially impact our business, reducing our ability to sustain generating revenues.

Providing specialized Gig Economy oriented staffing management products and services is an emerging yet competitive business, and many of our competitors have greater resources that may enable them to compete more effectively.

We will compete in the same markets with many companies that offer not only staffing management products and services focused on the Gig Economy but also more traditional staffing management products and services. There are limited barriers to entry. Price competition in the industry, particularly from larger, more traditional industry model competitors, is intense, and pricing pressures from competitors and clients are increasing. New competitors entering our markets may further increase pricing pressures.

Clients may competitively bid new contracts; a trend is expected to continue for the foreseeable future. Some of our competitors have greater resources than we do, which may enable them to compete more effectively in this market. Our competitors may devote their resources to developing and marketing products and services that will directly compete with our product lines, and new, more efficient competitors may enter the market. If we are unable to successfully compete with existing companies and new entrants to the market this will have a negative impact on our business and financial condition.

We operate in an immature and rapidly evolving industry and have a relatively new business model, which makes it difficult to evaluate our business and prospects.

The industry in which we operate is characterized by rapidly changing regulatory requirements, evolving industry standards and shifting user and client demands. Our business model is also evolving and is different from models used by other companies in our industry. As a result of these factors, the success and future revenue and income potential of our business is uncertain. Any evaluation of our business and our prospects must be considered in light of these risks and uncertainties, some of which relate to our ability to:

| · | Expand employer and employee client relationships; |

| · | Increase the number of our employer clients and grow a shifter employee base; |

| · | Develop relationships with third-party vendors such as insurance companies; |

| · | Expand operations and implement and improve our operational, financial and management controls; |

| · | Raise capital at attractive costs, or at all; |

| · | Attract and retain qualified management, employees and independent service providers; |

| · | Successfully introduce new processes, technologies products and services and upgrade our existing processes, technologies, products and services; |

| · | Protect our proprietary processes and technologies and our intellectual property rights; and |

| · | Respond to government regulations relating to the internet, personal data protection, email, software technologies, cyber security and other regulated aspects of our business. |

If we are unable to successfully address the challenges posed by operating in an immature and rapidly evolving industry and having a relatively new business model, our business could suffer.

| 18 |

| Table of Contents |

We have claims and lawsuits against us that may result in adverse outcomes.

We are subject to a variety of claims and lawsuits. These claims may arise from a wide variety of business practices, significant business transactions, operational claims, and employment practices. Adverse outcomes in some or all of these claims may result in significant monetary damages or injunctive relief that could adversely affect our ability to conduct our business. The litigation and other claims are subject to inherent uncertainties and management’s view of these matters may change in the future. A material adverse impact on our consolidated financial statements could occur for the period in which the effect of an unfavorable outcome becomes probable and reasonably estimable.

We have identified material weaknesses in our internal control over financial reporting. If our internal control over financial reporting is not effective, we may not be able to accurately report our financial results or file our periodic reports in a timely manner, which may cause adverse effects on our business and may cause investors to lose confidence in our reported financial information and may lead to a decline in stock price.

Effective internal control over financial reporting is necessary in order to provide reliable financial reports in a timely manner. In connection with the audit of our consolidated financial statements for the year ended August 31, 2019, we concluded that there were material weaknesses in our internal control over financial reporting relating to our IT environment, controls over cut-off procedures, a related party transaction, accounting for certain litigation accruals, segregation of duties and corporate oversight functions. A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the annual or interim financial statements will not be prevented or detected on a timely basis.

If we are unable to successfully remediate our material weaknesses or identify any future significant deficiencies or material weaknesses, the accuracy and timing of our financial reporting may be adversely affected, a material misstatement in our consolidated financial statements could occur, we may be unable to maintain compliance with securities law requirements regarding timely filing of periodic reports, which may adversely affect our business and our stock price may decline as a result. In addition, even if we remediate our material weaknesses, we will be required to expend significant time and resources to further improve our internal controls over financial reporting, including by further expanding our finance and accounting staff to meet the demands that are placed upon us as a public company, including the requirements of the Sarbanes-Oxley Act. If we fail to adequately staff our accounting and finance function to remediate our material weaknesses, or fails to maintain adequate internal control over financial reporting, any new or recurring material weaknesses could prevent us from concluding our internal control over financial reporting is effective and impair our ability to prevent material misstatements in our consolidated financial statements, which could cause our business to suffer.

If we are unable to secure or pay for the insurance coverage required for our business operations, or if we lose any existing coverage, we may not be able to offer some of our services and our revenues could be reduced.

We are required to obtain and maintain various types of insurance coverage for our business, in particular health and workers’ compensation insurance related to our employees. Although we have contracts with all types of providers currently necessary for our business, if in the future we are unable to secure the insurance coverage required for our business operations, or if we lose any existing coverage, we may not be able to offer some of our services and our revenues could be reduced. In addition, any increases in the cost of insurance coverage we are required to maintain could reduce profitability (or increase net losses).

We provide limited self- insurance for our workers compensation services provided to our clients. If we have claims in excess of our collected premiums we may incur additional losses. Workers’ compensation costs for shifter employees may rise and reduce our margins and require more liquidity.

The Company is responsible for and pays workers’ compensation costs for its shift workers. We currently provide self-insurance for up to $500,000 per occurrence and purchase reinsurance for claims in excess of $500,000. Our workers compensation billings are designed to cover expected claims based on insurance annuity calculations. These calculations are based on our limited operating history and claims experiences due to our limited operating history. At times, these costs have risen substantially as a result of increased claims and claim trends, general economic conditions, changes in business mix, increases in healthcare costs, and government regulations. Although the Company carries insurance and currently has reserves in excess of projected losses, unexpected changes in claim trends, including the severity and frequency of claims, actuarial estimates, and medical cost inflation could result in costs that are significantly different than initially reported. If future claims-related liabilities increase due to unforeseen circumstances, or if new laws, rules, or regulations are passed, costs could increase significantly. There can be no assurance that the Company will be able to increase the fees charged to clients in a timely manner and in a sufficient amount to cover increased costs as a result of any changes in claims-related liabilities.

| 19 |

| Table of Contents |

We may be subject to penalties and interest payable on taxes as a result of data entry into our software or manual error.

Our input of data in our tax processing software must be entered properly in order to process the data and payments correctly with regard to clients, employees and applicable tax agencies. If we input incorrect data or input accurate data incorrectly, we could inadvertently overbill or underbill our clients or overpay or underpay applicable taxes, resulting in the loss of net income and/or clients and/or the incurrence of tax penalties and interest. Despite our efforts to reconcile taxes on a monthly basis, we may incur additional taxes, penalties and interest for which we may or may not bill the clients.

Our Ability to Adjust and Collect Service Fees for Increases in Unemployment Tax Rates May be Limited

We record our State Unemployment Tax (“SUI”) expense based on taxable wages and tax rates assigned by each state. SUI tax rates vary by state and are determined, in part, based on prior years’ compensation experience in each state. Prior to the receipt of final tax rate notices, we estimate our expected SUI tax rate in those states for which tax rate notices have not yet been received for purposes of pricing. In a period of adverse economic conditions state unemployment funds may experience a significant increase in the number of unemployment claims. Accordingly, SUI tax rates would likely increase substantially. Some states have the ability under law to increase SUI tax rates retroactively to cover deficiencies in the unemployment fund.

In addition, FUTA may be retroactively increased in certain states in the event the state fails to timely repay federal unemployment loans. Employers in such states are experiencing higher FUTA tax rates as a result of not repaying their unemployment loans from the federal government in a timely manner. The credit reduction is an additional tax on the FUTA wage base for employers in states that continue to have outstanding federal unemployment insurance loans beginning with the fifth year in which there is a balance due on the loan. States have the option to apply for a waiver before July 1st of the year in which the credit reduction is applicable.

Generally, our contractual agreements allow us to incorporate such statutory tax increases into our service fees upon the effective date of the rate change. However, our ability to fully adjust service fees in our billing systems and collect such increases over the remaining term of the clients’ contracts could be limited, resulting in a potential tax increase not being fully recovered. As a result, such increases could have a material adverse effect on our financial condition or results of operations.

Financial Market Risks

We have warrants and convertible debt that may be converted into shares issued in the future, which would dilute your ownership in the Company

On June 4, 2018, December 20, 2018, and March 12, 2019 the Company issued senior secured convertible note agreements with certain institutional investors in which, at any time while there is an outstanding balance, the notes may be converted, at the option of the holders at a conversion price for the principal and interest, subject to adjustment from down round price protection. As of the date of this report, these notes were in default and therefore subject to a conversion price of 75% of the lowest volume weighted average price on any given trading day for the June 2018, December 2018 notes the March 2019 notes. As of the August 31, 2019 date, those notes, if converted at the applicable discount price, would be convertible into approximately 19.7 million shares of common stock. In conjunction with the above transactions, the Company also granted warrants to purchase up to 4.2 million shares of common stock, which may be exercised for up to five years from their issuance date. These warrants may also include the requirement for the Company to issue additional warrants if a future financing is entered into at a price per share below the warrant exercise price. Further, any additional financing that we secure may require the granting of rights, preferences or privileges senior to those of our common stock and which result in additional dilution of the existing ownership of our common shareholders.

The agreements governing our senior convertible notes contain a mandatory default amount when an event of default occurs

The indentures governing our senior secured convertible notes, contain mandatory default amounts when an event of default occurs. In general, interest is to be accrued at 18% annual rate from the date of default, the conversion feature is modified to be a discount of between 15% and 25% to the volume weighted average price on the date of conversion, and a mandatory redemption may be demanded at up to 130% of the remaining principal balance. We have been notified that our June 2018, December 2018, and March 2019 notes are in default by one of our noteholders for failure to honor a conversion notice sent in June 2019 for the March 2019 notes. We are currently in litigation with our note holders for this failure to honor conversions for the June 2018, December 2018, and March 2019 series. If we remain in default, one or a combination of the following could occur: i) we could have to repay a portion of the outstanding notes at a premium to the total non-default outstanding principal balance of approximately $6.8 million, the conversion price could be reduced resulting in additional shares issued which could cause dilution to common shareholders, and iii) additional cash interest may be due.

Our Common Stock is thinly traded, which can cause volatility in its price.

Our Common Stock is listed for trading on the Nasdaq Stock Market, LLC, and is thinly traded. Thinly traded stock can be more susceptible to market volatility. This market volatility could significantly affect the market price of our common stock without regard to our operating performance. Securities markets worldwide experience significant price and volume fluctuations. In addition, the price of our common stock could be subject to wide fluctuations in response to the following factors, among others:

| · | a deviation in our results from the expectations of public market analysts and investors; |

| · | statements by research analysts about our common stock, our company or our industry; |

| · | changes in market valuations of companies in industries to which our company is compared and market evaluations of our industries in which our company is deemed to be operating generally; |

| · | actions taken by our competitors; |