Attached files

| file | filename |

|---|---|

| EX-32 - CERTIFICATION - THUNDER MOUNTAIN GOLD INC | ex32b.htm |

| EX-32 - CERTIFICATION - THUNDER MOUNTAIN GOLD INC | ex32a.htm |

| EX-31 - CERTIFICATION - THUNDER MOUNTAIN GOLD INC | ex31b.htm |

| EX-31 - CERTIFICATION - THUNDER MOUNTAIN GOLD INC | ex31a.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2018

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-08429

THUNDER MOUNTAIN GOLD INC

(Exact name of Registrant as specified in its charter)

Nevada |

| 91-1031015 |

(State or other jurisdiction of incorporation or organization) |

| (IRS identification No.) |

|

|

|

11770 W President Dr. STE F |

|

|

Boise, Idaho |

| 83713-8986 |

(Address of Principal Executive Offices) |

| (Zip Code) |

| ||

(208) 658-1037 | ||

(Registrant’s Telephone Number, including Area Code) | ||

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes¨ No

Indicate by check mark whether the Registrant is ¨ a large accelerated filer, ¨ an accelerated file, ¨ a non-accelerated filer, x a smaller reporting company (as defined in Rule 12b-2 of the Exchange Act) or ¨ an emerging growth company

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

¨ Yes x No

Number of shares of issuer’s common stock outstanding at October 22, 2018: 57,645,579

1

TABLE OF CONTENTS

PART I – FINANCIAL INFORMATION3

Item 2. Management's Discussion and Analysis or Plan of Operation14

Item 3. Quantitative and Qualitative Disclosures about Market Risk22

Item 4. Controls and Procedures23

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds.24

Item 3. Defaults Upon Senior Securities.24

Item 4. Mine Safety Disclosures24

2

PART I – FINANCIAL INFORMATION

Thunder Mountain Gold, Inc. Consolidated Balance Sheets September 30, 2018 and December 31, 2017 Unaudited | ||||||||

|

| September 30, 2018 |

| December 31, 2017 | ||||

ASSETS |

|

|

|

| ||||

Current assets: |

|

|

|

| ||||

Cash and cash equivalents | $ | 30,115 | $ | 36,454 | ||||

Prepaid expenses and other assets |

| 32,176 |

| 28,473 | ||||

Total current assets |

| 62,291 |

| 64,927 | ||||

|

|

|

|

| ||||

Property and Equipment: |

|

|

|

| ||||

Land |

| 280,333 |

| 280,333 | ||||

Equipment, net of accumulated depreciation of $113,161 and $75,959, respectively |

| 69,444 |

| 106,646 | ||||

Total property and equipment |

| 349,777 |

| 386,979 | ||||

|

|

|

|

| ||||

Mineral interests (Note 3) |

| 479,477 |

| 479,477 | ||||

Total assets | $ | 891,545 | $ | 931,383 | ||||

|

|

|

|

| ||||

LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT) |

|

|

|

| ||||

Current liabilities: |

|

|

|

| ||||

Accounts payable and other accrued liabilities | $ | 129,929 | $ | 92,311 | ||||

Accrued related party liability (Note 6) |

| 241,685 |

| 181,313 | ||||

Accrued interest payable to related parties (Note 5) |

| 48,240 |

| 36,949 | ||||

Deferred payroll (Note 6) |

| 1,041,500 |

| 871,500 | ||||

Related party notes payable (Note 5) |

| 126,576 |

| 217,688 | ||||

Total current liabilities |

| 1,587,930 |

| 1,399,761 | ||||

|

|

|

|

| ||||

Accrued reclamation costs |

| 65,000 |

| 65,000 | ||||

|

|

|

|

| ||||

Total liabilities |

| 1,652,930 |

| 1,464,761 | ||||

|

|

|

|

| ||||

Commitments and Contingencies (Notes 2, 3) |

|

|

|

| ||||

|

|

|

|

| ||||

Stockholders' equity (deficit): |

|

|

|

| ||||

Preferred stock; $0.0001 par value, 5,000,000 shares authorized; no shares issued or outstanding |

| - |

| - | ||||

Common stock; $0.001 par value; 200,000,000 shares authorized, 57,645,579 and 55,095,579, respectively, shares issued and outstanding |

| 57,646 |

| 55,096 | ||||

Additional paid-in capital |

| 5,811,988 |

| 5,457,538 | ||||

Less: 11,700 shares of treasury stock, at cost |

| (24,200) |

| (24,200) | ||||

Accumulated deficit |

| (6,780,509) |

| (6,195,923) | ||||

Total Thunder Mountain Gold, Inc. stockholders' equity (deficit) |

| (935,073) |

| (707,489) | ||||

Noncontrolling interest in Owyhee Gold Trust (Note 3) |

| 173,690 |

| 174,111 | ||||

Total stockholders' equity (deficit) |

| (761,385) |

| (533,278) | ||||

Total liabilities and stockholders' equity (deficit) | $ | 891,545 | $ | 931,383 | ||||

The accompanying notes are an integral part of these consolidated financial statements.

3

Thunder Mountain Gold, Inc. Consolidated Statements of Operations (Unaudited)

| ||||||||

|

| Three Months Ended |

| Nine Months Ended | ||||

|

| September 30, |

| September 30, | ||||

|

| 2018 |

| 2017 |

| 2018 |

| 2017 |

|

|

|

|

|

|

|

|

|

Expenses: |

|

|

|

|

|

|

|

|

Exploration | $ | 21,470 | $ | 46,613 | $ | 197,543 | $ | 144,881 |

Legal and accounting |

| 5,489 |

| 9,728 |

| 113,524 |

| 48,975 |

Management and administrative |

| 53,986 |

| 69,354 |

| 214,170 |

| 284,074 |

Loss on sale of equipment |

| - |

| 1,021 |

| - |

| 1,021 |

Depreciation |

| 12,193 |

| 15,003 |

| 37,202 |

| 57,582 |

Total expenses |

| 93,138 |

| 141,719 |

| 562,440 |

| 536,533 |

|

|

|

|

|

|

|

|

|

Other income (expense): |

|

|

|

|

|

|

|

|

Interest expense, related parties |

| (4,547) |

| (4,612) |

| (24,191) |

| (12,454) |

Miscellaneous income (expense) |

| 1,337 |

| 1,200 |

| 2,044 |

| 1,295 |

Total other income (expense) |

| (3,210) |

| (3,412) |

| (22,147) |

| (11,159) |

Net Loss |

| (96,348) |

| (145,1310 |

| (584,586) |

| (547,692) |

Net Income (loss) – noncontrolling interest in Owyhee Gold Trust |

| - |

| - |

| - |

| - |

Net Loss – Thunder Mountain Gold, Inc. | $ | (96,348) | $ | (145,131) |

| (584,586) |

| (547,692) |

|

|

|

|

|

|

|

|

|

Net Loss per common share – basic and diluted | $ | 0.00 | $ | 0.00 | $ | (0.01) | $ | (0.01) |

Weighted average common shares outstanding – basic and diluted |

| 57,645,579 |

| 54,864,185 |

| 57,554,653 |

| 54,791,550 |

|

|

|

|

|

|

|

|

|

The accompanying notes are an integral part of these consolidated financial statements.

4

|

Consolidated Statements of Cash Flows (Unaudited) | ||||||

|

| Nine Months Ended |

| |||

|

| September 30, |

| |||

|

| 2018 |

| 2017 |

| |

|

|

|

|

|

| |

Cash flows from operating activities: |

|

|

|

|

| |

Net loss | $ | (584,586) | $ | (547,692) |

| |

Adjustments to reconcile net loss to net cash used by operating activities: |

|

|

|

|

| |

Depreciation |

| 37,202 |

| 57,582 |

| |

Loss on sale of Equipment |

| - |

| 1,021 |

| |

Common stock options issued for services |

| - |

| 53,558 |

| |

Amortization of related party notes payable discount |

| 8,888 |

| - |

| |

Change in: |

|

|

|

|

| |

|

|

|

|

|

| |

Accounts payable and other accrued liabilities |

| 37,618 |

| 2,384 |

| |

Accrued related party liability |

| 60,372 |

| - |

| |

Accrued interest payable to related parties |

| 15,303 |

| 12,453 |

| |

Deferred payroll |

| 170,000 |

| 234,000 |

| |

Net cash used by operating activities |

| (258,906) |

| (182,971) |

| |

|

|

|

|

|

| |

Cash flows from investing activities: |

|

|

|

|

| |

Proceeds from sale of equipment |

| - |

| 41,000 |

| |

Net cash provided by investing activities |

| - |

| 41,000 |

| |

|

|

|

|

|

| |

Cash flows from financing activities: |

|

|

|

|

| |

Proceeds from sale of common stock and warrants |

| 252,988 |

| - |

| |

Proceeds from exercise of common stock options |

| - |

| 20,550 |

| |

Borrowing on related parties notes payable |

| - |

| 20,000 |

| |

Distribution to noncontrolling interest |

| (421) |

| - |

| |

Net cash provided by financing activities |

| 252,567 |

| 40,550 |

| |

|

|

|

|

|

| |

Net increase (decrease) in cash and cash equivalents |

| (6,339) |

| (101,421) |

| |

Cash and cash equivalents, beginning of period |

| 36,454 |

| 108,184 |

| |

Cash and cash equivalents, end of period | $ | 30,115 | $ | 6,763 |

| |

|

|

|

|

|

| |

|

|

|

|

|

| |

Noncash financing and investing activities: |

|

|

|

|

| |

Common stock and warrants issued for payment of related parties notes payable and accrued interest | $ | 104,012 |

| - |

| |

Stock options exercised in exchange for payment of related parties notes payable and related accrued interest |

| - | $ | 20,125 |

| |

|

|

|

|

|

| |

The accompanying notes are an integral part of these consolidated financial statements.

5

1. Summary of Significant Accounting Policies and Business Operations

Business Operations

Thunder Mountain Gold, Inc. (“Thunder Mountain” or “the Company”) was originally incorporated under the laws of the State of Idaho on November 9, 1935, under the name of Montgomery Mines, Inc. In April 1978, the Montgomery Mines Corporation was obtained by a group of the Thunder Mountain property holders and changed its name to Thunder Mountain Gold, Inc., with the primary goal to further develop their holdings in the Thunder Mountain Mining District, located in Valley County, Idaho. Thunder Mountain Gold, Inc. takes its name from the Thunder Mountain Mining District, where its principal lode mining claims were located. For several years, the Company’s activities were restricted to maintaining its property position and exploration activities. During 2005, the Company sold its holdings in the Thunder Mountain Mining District. During 2007, the Company acquired the South Mountain Mines property in southwest Idaho and initiated exploration activities on that property, which continue today.

Basis of Presentation and Going Concern

These unaudited interim consolidated financial statements have been prepared by the management of the Company in accordance with accounting principles generally accepted in the United States of America for interim financial information. Accordingly, they do not include all the information and footnotes required by generally accepted accounting principles for complete consolidated financial statements. In the opinion of the Company’s management, all adjustments (consisting of only normal recurring accruals) considered necessary for a fair presentation of the interim consolidated financial statements have been included.

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities known to exist as of the date the financial statements are published, and the reported amounts of revenues and expenses during the reporting period. Uncertainties with respect to such estimates and assumptions are inherent in the preparation of the Company's financial statements; accordingly, it is possible that the actual results could differ from these estimates and assumptions, which could have a material effect on the reported amounts of the Company's financial position and results of operations. Operating results for the nine months ended September 30, 2018 are not necessarily indicative of the results that may be expected for the full year ending December 31, 2018.

For further information refer to the financial statements and footnotes thereto in the Company’s audited financial statements for the year ended December 31, 2017 as filed with the Securities and Exchange Commission.

The accompanying consolidated financial statements have been prepared under the assumption that the Company will continue as a going concern. The Company has historically incurred losses and does not have sufficient cash at September 30, 2018 to fund normal operations for the next 12 months. The Company has no recurring source of revenue and its ability to continue as a going concern is dependent on the Company’s ability to raise capital to fund its future exploration and working capital requirements. The Company’s plans for the long-term return to and continuation as a going concern include financing the Company’s future operations through sales of its common stock and/or debt and the eventual profitable exploitation of its mining properties. These factors raise substantial doubt about the Company’s ability to continue as a going concern. The Company is currently investigating a number of alternatives for raising additional capital with potential investors, lessees and joint venture partners.

The consolidated financial statements do not include any adjustments that might be necessary should the Company be unable to continue as a going concern. If the going concern basis was not appropriate for these financial statements, adjustments would be necessary to the carrying value of assets and liabilities, the reported expenses and the balance sheet classifications used.

6

Reclassifications

Certain reclassifications have been made to conform prior period’s data to the current presentation. These reclassifications have no effect on previously reported operations, stockholders’ equity (deficit) or cash flows.

Principles of Consolidation

The consolidated financial statements include the accounts of the Company; its wholly owned subsidiaries, Thunder Mountain Resources, Inc. and South Mountain Mines, Inc. (“SMMI”); and Owyhee Gold Trust, LLC (“OGT”) a company in which the Company has majority control. Intercompany accounts are eliminated in consolidation.

Accounting Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The more significant areas requiring the use of management estimates and assumptions include the carrying value of properties and mineral interests, environmental remediation liabilities, deferred tax assets, and stock-based compensation. Management’s estimates and assumptions are based on historical experience and other assumptions believed to be reasonable under the circumstances. Actual results could differ from those estimate.

Cash and cash equivalents

For the purposes of the balance sheet and statement of cash flows, the Company considers all highly liquid investments with a maturity of three months or less when purchased to be a cash equivalent.

Income Taxes

The Company recognizes deferred income tax liabilities or assets at the end of each period using the tax rate expected to be in effect when the taxes are actually paid or recovered. A valuation allowance is recognized on deferred tax assets when it is more likely than not that some or all of the deferred tax assets will not be realized.

Fair Value Measurements

When required to measure assets or liabilities at fair value, the Company uses a fair value hierarchy based on the level of independent, objective evidence surrounding the inputs used. The Company determines the level within the fair value hierarchy in which the fair value measurements in their entirety fall. The categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value measurement. Level 1 uses quoted prices in active markets for identical assets or liabilities, Level 2 uses significant other observable inputs, and Level 3 uses significant unobservable inputs. The amount of the total gains or losses for the period are included in earnings that are attributable to the change in unrealized gains or losses relating to those assets and liabilities still held at the reporting date. The Company has no financial assets or liabilities that are adjusted to fair value on a recurring basis.

Financial Instruments

The Company’s financial instruments include cash and cash equivalents and related party notes payable the carrying value of which approximates fair value based on the nature of those instruments.

Mineral Interests

The Company capitalizes costs for acquiring mineral interests and expenses costs to maintain mineral rights and leases as incurred. Exploration costs are expensed in the period in which they occur. Should a property reach the production stage, these capitalized costs would be amortized using the units-of-production method based on periodic estimates of ore reserves. Mineral properties are periodically assessed for impairment of value and any subsequent losses are charged to operations at the time of impairment. If a property is abandoned or sold, its capitalized costs are charged to operations.

7

Investments in Joint Venture

The Company’s accounting policy for joint ventures is as follows:

1.The Company uses the cost method when it does not have joint control or significant influence in a joint venture. Under the cost method, these investments are carried at cost. If other than temporary impairment in value is determined, it would then be charged to current net income or loss.

2.If the Company enters into a joint venture in which there is joint control between the parties or the Company has significant influence, the equity method is utilized whereby the Company’s share of the venture’s earnings and losses is included in the statement of operations as earnings in joint ventures and its investments therein are adjusted by a similar amount. If other than temporary impairment in value is determined, it would then be charged to current net income or loss.

3.In a joint venture where the Company holds more than 50% of the voting interest and has significant influence, the joint venture is typically consolidated with the presentation of non-controlling interest. In determining whether significant influences exist, the Company considers its participation in policy-making decisions and its representation on the venture’s management committee. See Note 3 regarding the Company’s investment in Owyhee Gold Trust, LLC.

Reclamation and Remediation

The Company’s operations have been, and are subject to, standards for mine reclamation that have been established by various governmental agencies. The Company would record the fair value of an asset retirement obligation as a liability in the period in which the Company incurred a legal obligation for the retirement of tangible long-lived assets. A corresponding asset would also be recorded and depreciated over the life of the asset.

After the initial measurement of the asset retirement obligation, the liability is adjusted at the end of each reporting period to reflect changes in the estimated future cash flows underlying the obligation.

Determination of any amounts recognized upon adoption is based upon numerous estimates and assumptions, including future retirement costs, future inflation rates and the credit-adjusted risk-free interest rates.

For non-operating properties, the Company accrues costs associated with environmental remediation obligations when it is probable that such costs will be incurred, and they are reasonably estimable. Such costs are based on management’s estimate of amounts expected to be incurred when the remediation work is performed.

Share-Based Compensation

Share-based payments to employees and directors, including grants of employee stock options, are measured at fair value and expensed in the statement of operations over the vesting period.

Recent Accounting Pronouncements

In August 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2016-15 Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments. The update provides guidance on classification for cash receipts and payments related to eight specific issues. The update is effective for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years, with early adoption permitted. The adoption of this update on January 1, 2018 had no impact on the Company’s consolidated financial statements.

8

In November 2016, the FASB issued ASU No. 2016-18 Statement of Cash Flows (Topic 230): Restricted Cash. The update requires that a statement of cash flows explain the change during the period in the total of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents. The update is effective for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years, with early adoption permitted. The adoption of this update on January 1, 2018 had no impact on the Company’s consolidated financial statements.

In January 2017, the FASB issued ASU No. 2017-01 Business Combinations (Topic 805): Clarifying the Definition of a Business. The update clarifies the definition of a business with the objective of adding guidance to assist entities with evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses. The update is effective for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years. The Company will apply the provisions of the update to potential future acquisitions occurring after January 1, 2018.

Other accounting standards that have been issued or proposed by FASB that do not require adoption until a future date are not expected to have a material impact on the consolidated financial statements upon adoption. The Company does not discuss recent pronouncements that are not anticipated to have an impact on or are unrelated to its financial condition, results of operations, cash flows or disclosures.

Net Income (Loss) Per Share

The Company is required to have dual presentation of basic earnings per share (“EPS”) and diluted EPS. Basic EPS is computed as net income divided by the weighted average number of common shares outstanding for the period. Diluted EPS is calculated based on the weighted average number of common shares outstanding during the period plus the effect of potentially dilutive common stock equivalents, including options and warrants to purchase the Company’s common stock. As of September 30, 2018, and 2017, potentially dilutive common stock equivalents not included in the calculation of diluted earnings per share as their effect would have been anti-dilutive are:

2018 | 2017 | |

Stock options | 3,710,000 | 4,700,000 |

Warrants | 1,275,000 | - |

Total possible dilution | 4,985,000 | 4,700,000 |

2. Commitments

The Company has two lease arrangements with land owners that own land parcels adjacent to the Company’s South Mountain patented and unpatented mining claims. The leases were originally for a seven-year period, with annual payments of $20 per acre. The leases were renewed for an additional 10 years at $30 per acre paid annually; committed payments are listed in the table below. The lease payments have no work requirements.

| Annual Payment |

Acree Lease (June) | $ 3,390 |

Lowry Lease (October) | 11,280 |

Total | $ 14,670 |

9

The Company has 78 unpatented claims (1,600 acres) in the Trout Creek area and 21 unpatented claims in the South Mountain area. The claim fees are paid on these unpatented claims annually as follows:

Target Area | 2018 |

|

|

Trout Creek -State of Nevada | $ 12,090 |

Trout Creek -Lander County | 940 |

South Mountain-State of Idaho | 3,255 |

Total | $ 16,285 |

3.South Mountain Project

The Company’s wholly-owned subsidiary SMMI is the sole manager of the South Mountain Project in its entirety through a separate Mining Lease with Option to Purchase (“Lease Option”) with the Company’s majority-owned subsidiary OGT. The Lease Option includes a capped $5 million less, net returns royalties paid through the date of exercise. The Lease Option expires in November 2026. If SMMI exercises the option, the option payment of $5 million less advance royalties will be distributed 100% by OGT to OGT’s minority member. Under the Lease Option, SMMI pays an advance $5,000 net returns royalty to OGT annually on November 4 which is distributed to OGT’s minority member.

OGT’s financial information is included 100% in the Company’s consolidated financial statements and reflects its minority member’s non-controlling interest. Changes in the non-controlling interest equity balance is as follows:

|

| Nine Months Ended September 30, | ||

|

| 2018 |

| 2017 |

Balance at beginning of period | $ | 174,111 | $ | 178,702 |

Distribution to non-controlling interest |

| (421) |

| - |

Net income (loss) attributable to noncontrolling interest |

| - |

| - |

Balance at end of period | $ | 173,690 | $ | 178,702 |

4. Property and Equipment

The Company’s property and equipment are as follows:

|

| September 30, 2018 |

| December 31, 2017 | |

|

|

| |||

Vehicles | $ | 22,441 | $ | 22,441 | |

Buildings |

| 65,071 |

| 65,071 | |

Construction Equipment |

| 36,447 |

| 36,447 | |

Mining Equipment |

| 58,646 |

| 58,646 | |

|

| 182,605 |

| 182,605 | |

Accumulated Depreciation |

| (113,161) |

| (75,959) | |

|

| 69,444 |

| 106,646 | |

Land |

| 280,333 |

| 280,333 | |

Total Property and Equipment | $ | 349,777 | $ | 386,979 | |

10

5. Related Parties Notes Payable

At both September 30, 2018 and December 31, 2017, the Company had notes payable balances of $56,768 and $69,808 with Eric Jones, the Company’s President and Chief Executive Officer and Jim Collard, the Company’s Vice President and Chief Operating Officer, respectively. These notes, as amended, are due December 31, 2018.

On October 25, 2017 the Company received $100,000 from Paul Beckman, a director of the Company, under a convertible promissory note. Terms of the note called for interest at 1% per month, with the entire balance of principal and interest due in full on April 24, 2018. The convertible promissory note contained the option for the holder to convert any portion of the principal and interest into Company common stock at $0.15 per common share (a total of 666,667 shares). At inception, the market price for the Company’s common stock was $0.17 per common share which exceeded the conversion price. As such, the convertible note contained a beneficial conversion feature of $13,333 which was recognized as a discount on the note on the date of issuance. The discount was being amortized over the note term using the straight-line method, which approximates the effective interest method.

On February 26, 2018, Mr. Beckman participated in the Company’s Private Placement (see Note 7) and acquired 1,000,000 Units for $140,000. A portion of this amount was in exchange for retirement of Mr. Beckman’s convertible note payable of $100,000 and accrued interest payable of $4,012. Upon the retirement of Mr. Beckman’s convertible promissory note, the Company recognized the unam ortized portion of the discount of $5,100 as interest expense. After this transaction, the Company has no remaining obligation under the convertible note agreement with Mr. Beckman.

During the nine months ended September 30, 2018 and 2017, the Company recognized a total of $24,191 and 12,454, respectively, in interest expense for the notes discussed above. Accrued interest payable was $48,240 and $36,949 at September 30, 2018 and December 31, 2017, respectively.

6.Related Party Transactions

In addition to the related parties notes payable discussed in Note 5, the Company had the following related party transactions.

Three of the Company’s officers had been deferring compensation for services The officer’s balances at September 30, 2018 are as follows: Eric Jones, President and Chief Executive Officer - $420,000 (December 31, 2017 – $350,000), Jim Collord, Vice President and Chief Operating Officer - $420,000 (December 31, 2017 – $350,000), and Larry Thackery, Chief Financial Officer - $201,500 (December 31, 2017 – $171,500). On July 31, 2018 the Company stopped expensing and deferring compensation for the three Company officers in the interest of marketing the SMMI project.

The Company engages Baird Hanson LLP (“Baird”), a company owned by one of the Company’s directors, to provide legal services. During the nine-month periods ended September 30, 2018, the Company incurred $65,530 in legal expense with Mr. Baird. There was no expense for the comparable periods in 2017. At September 30, 2018 and December 31, 2017, the balance due to Baird was $241,685 and $181,313, respectively.

During 2017, Eric Jones advanced funds to the Company for operating expenses. The balance of Mr. Jones’ advance at both December 31, 2017 and September 30, 2018 was $10,971 and is included in accounts payable and other accrued liabilities on the consolidated balance sheet.

11

7. Stockholders’ Equity

The Company’s common stock has a par value of $0.001 with 200,000,000 shares authorized. The Company also has 5,000,000 authorized shares of preferred stock with a par value of $0.0001.

The Company’s common stock has a par value of $0.001 with 200,000,000 shares authorized. The Company also has 5,000,000 authorized shares of preferred stock with a par value of $0.0001.

On February 20, 2018, the Board of Directors approved a Private Placement financing of up to $750,000 from the sale of equity units at a price of $0.14 per unit. Each unit consists of one share of the Company’s common stock and one-half of one common share purchase warrant. Each whole warrant entitles the holder to purchase one additional share of common stock of the Company at a price of $0.20 for a period of 12 months. Through March 31, 2018, the Company has sold Units representing a total of 2,050,000 in shares of common stock and 1,025,000 common stock purchase warrants for total proceeds of $287,000. Of this amount, $182,988 was received in cash and $104,012 was in exchange for retirement of Mr. Beckman’s convertible note payable and related accrued interest payable See Note 5.

At September 30, 2018, the Company has outstanding warrants for 1,275,000 shares of common stock with an exercise price of $0.20 that expire in 2019. There were no outstanding warrants at December 31, 2017.

8.Stock Options

In March 2017, the Company granted 600,000 stock options to three directors of the Company. The options are exercisable on or before March 31, 2022 at a price of $0.10 for 200,000 shares, and at a price of $0.09 for the remaining 400,000 shares. The fair value of the options was determined to be $53,558 using the Black Scholes model. The options were fully vested upon grant and the entire fair value was recognized as compensation expense during the three and nine months ended September 30, 2017.

The fair value of each option award granted in March 2017 was estimated on the date of the grant using the assumptions noted in the following table:

| |

Number of Options | 600,000 |

Stock price | $0.09 - $0.10 |

Exercise price | $0.09 - $0.10 |

Expected volatility | 235.5% |

Expected dividends | - |

Expected terms (in years) | 5.0 |

Risk-free rate | 1.96% |

12

The following is a summary of the Company’s options issued under the Stock Option Incentive Plan:

| Shares |

| Weighted Average Exercise Price |

Outstanding and exercisable at December 31, 2016 | 4,515,000 |

| $0.08 |

Granted | 600,000 |

| 0.09 |

Exercised | (415,000) |

| 0.10 |

Outstanding and exercisable at December 31, 2017 | 4,700,000 |

| 0.09 |

Granted | - |

| - |

Expired | (990,000) |

| (0.07) |

Outstanding and exercisable at September 30, 2018 | 3,710,000 |

| $0.09 |

The average remaining contractual term of the options outstanding and exercisable at September 30, 2018 was 2.23 years. As of September 30, 2018, options outstanding and exercisable had an aggregate intrinsic value of approximately $79,500 based on the Company’s stock price of $0.11.

13

Item 2. Management's Discussion and Analysis or Plan of Operation

The following Management’s Discussion and Analysis of Financial Condition and Results of Operation (“MD&A”) is intended to help the reader understand our financial condition. MD&A is provided as a supplement to, and should be read in conjunction with, our financial statements and the accompanying integral notes (“Notes”) thereto. The following statements may be forward-looking in nature and actual results may differ materially.

Plan of Operation:

FORWARD LOOKING STATEMENTS: The following discussion may contain forward-looking statements that involve a number of risks and uncertainties. Factors that could cause actual results to differ materially include the following: inability to locate property with mineralization, lack of financing for exploration efforts, competition to acquire mining properties; risks inherent in the mining industry, and risk factors that are listed in the Company's reports and registration statements filed with the Securities and Exchange Commission.

The Company’s financial position remained unchanged during the first nine months of 2018. Junior mining equity markets, in the future, may strengthen periodically in response to favorable price movements in certain metal. During the first 4 months of 2018 base metal prices were strong, providing some companies access to equity financing. However, metal prices declined starting in May in response the U.S. trade policies with China and other countries. Until capital markets in the Junior Mining space become favorable, equity financing in the mining industry will remain challenging. Analyst estimates for the remainder of 2018 are for stabilizing and strengthening precious metals markets, along with stable and improving prices for zinc, copper and lead.

The Company operated on a limited budget during the first nine months of 2018, funding the maintenance and completing an updated NI-43-101 Technical Report for the South Mountain Project, while continuing to search for additional financing to advance the Project. The Company’s plan of operation for the next twelve months, subject to business conditions, will be to continue to advance the South Mountain Project and complete an industry standard Feasibility Study. The completion of any such study is highly dependent on the ability of the Company to secure additional financing.

The Trout Creek Project will remain inactive in 2018 while the South Mountain Project continues to remain the focus. The Company has identified pre-defined drill targets during the Joint Exploration Agreement with Newmont Mining. Atoka Gold, who owns significant claim package adjacent to the Companies Trout Creek project, has expressed an interest, to adjoin their claim package, with the Trout Creek project, through a joint venture. The Company perceives advantages to a joint venture, as Trout Creek resembles a large pediment play in the Reese River Valley. There have been no details discussed of a structured agreement but talks continue with Atoka Gold.

South Mountain Project, Owyhee County, Idaho

The South Mountain Project is considered an advanced stage, high-grade zinc-silver exploration or pre-development project. The land package at South Mountain consists of a total of approximately 1,518 acres, consisting of (i) 17 patented claims (326 acres) and 360 acres of private land (mill site); (ii) lease on private ranch land (542 acres); and, (iii) 21 unpatented lode mining claims on BLM managed land (290 acres). All holdings are located in the South Mountain Mining District, Owyhee County, Idaho.

The property is located approximately 70 air miles southwest of Boise, Idaho and approximately 24 miles southeast of Jordan Valley, Oregon. It is accessible by highway 95 driving south from the Boise area to Jordan Valley Oregon, then by traveling southeast approximately 22 miles back into Idaho, via Owyhee County road that is dirt and improved to within 4 miles of historic mine site. The last 4 miles up the South Mountain Mine road are unimproved dirt road. The property is accessible year-round to within 4 miles of the property, where the property is accessible from May thru October without plowing snow. There is power distribution within 4 miles of the site as well. The climate is considered high desert. The Company has water rights on the property, and there is a potable spring on the property that once supplied water to the main camp.

14

Property History

The limited historic production peaked during World War II when, based on smelter receipts, the production of direct shipped ore totaled 53,653 tons containing 3,118 ounces of gold, 566,439 ounces of silver, 13,932 pounds of copper, 2,562,318 pounds of lead and 15,593,061 pounds of zinc. In addition to the direct-ship ore, a flotation mill was constructed and operated during the late-1940s and early-1950s.

Metal | Grade | Total Metal |

Gold Silver Copper Lead Zinc | 0.058 opt 10.6 opt 1.4% 2.4% 14.5% | 3,120 ozs 566,440 ozs 1,485,200 lbs 2,562,300 lbs 15,593,100 lbs |

Anaconda Crude Ore Shipments: 1941-1953 Total Tons: 53,653

South Mountain Mines Inc. (an Idaho Corporation) owned the patented claims from 1975 to the time the Company purchased the entity in 2007. They conducted extensive exploration work including extending the Sonneman Level by approximately 1,500 feet to intercept the down-dip extension of the Texas sulfide mineralization mined on the Laxey Level approximately 400 feet up-dip from the Sonneman. High grade sulfide mineralization was intercepted and confirmed on the Sonneman Extension. In 1985 South Mountain Mines Inc. completed a feasibility study based on historic and newly developed ore zones exposed in their underground workings and drilling. This resulted in a historic resource of approximately 470,000 tons containing 23,500 ounces of gold, 3,530,000 ounces of silver, 8,339,000 pounds of copper, 13,157,000 pounds of lead and 91,817,000 pounds of zinc. Although they determined positive economics, and that the resource was still open at depth with a large upside potential, the project was shut down and placed into care and maintenance.

In 2008, the Company contracted Kleinfelder, Inc., a nationwide engineering and consulting firm, to complete a technical report “Resources Data Evaluation, South Mountain Property, South Mountain Mining District, Owyhee County, Idaho”. The technical report was commissioned by Thunder Mountain Resources, Inc. to evaluate all the existing data available on the South Mountain property. Kleinfelder utilized a panel modeling method using this data to determine potential mineralized material remaining and to make a comparison with the resource determined by South Mountain Mines in the mid-1980s.

Additional drilling and sampling will be necessary before the resource can be classified as a mineable reserve, but Kleinfelder’s calculations provided a potential resource number that is consistent with South Mountain Mines’ (Bowes 1985) reserve model.

Late in 2009, the Company contracted with Northwestern Groundwater & Geology to incorporate all the new drill and sampling data into an NI 43-101 Technical Report. This report was completed as part of the Company’s dual listing on the TSX Venture Exchange in 2010.

In January of 2018, the Company engaged Hard Rock Consulting LLC (HRC) from Denver Colorado to update the South Mountain Project 43-101. HRC concluded that significant potential exists to increase the known mineral resource with additional drilling, as well as to upgrade existing mineral resource classifications with additional infill drilling. HRC also determined that the conceptual geologic model is sound, and, in conjunction with drilling results, indicates that mineralization is essentially open in all directions, and is continuous between underground levels and extends to the surface.

HRC also noted that:

THMG technical staff has thorough understanding of the geology of the South Mountain Project, and that the appropriate deposit model is being applied for exploration.

Because the Project is largely located on and surrounded by private land, it greatly simplifies Project approvals compared to mining projects involving public lands.

15

Initial metallurgical testing demonstrates that the South Mountain massive sulfide/skarn mineralization is amenable to differential flotation and concentrated.

The current mineral resource at the South Mountain Project more than sufficient to warrant continued planning and development to further advance the Project.

The Technical Report was authored by Ms. J.J. Brown, P.G., SME-RM, Mr. Jeffrey Choquette, P.E., and Mr. Randy Martin, SME-RM, all of Hard Rock Consulting, each of whom is an independent qualified person for the purposes of NI 43-101 The NI 43-101 Technical Report has an effective date of April 7, 2018 and has been filed in Canada on SEDAR in accordance with NI 43-101. The Report can be reviewed on the Company`s website at www.thundermountaingold.com.

Highlights of South Mountain NI-43-101 Report:

The most recent THMG drilling program was successful in defining the geometry and confirming the grades of the DMEA and Texas massive sulfide zones. Confirmed intercepts within the model include:

DMEA core hole DM2UC13-13, returned a 91.5-foot true width intercept of 13.79% Zn, 12.75 o.p.t. Ag, 0.08 o.p.t. Au, 0.45% Cu, and 7.07% Pb;

Texas core hole TX13-03 drilled from the surface across the zone, returned 11.8 feet true width, assaying 14.08% Zn, 9.01 o.p.t. Ag, 0.01 o.p.t. Au, 1.43% Cu, and 0.35% Pb

DMEA core hole DM2UC13-17, includes a 42-foot true width intercept of 17.86% Zn, 2.98 o.p.t. Ag, 0.13 o.p.t. Au, 0.18% Cu, and 0.47% Pb;

Rib channel samples across the DMEA zone on the Sonneman of 130 feet true width, assaying 16.76% Zn, 4.11 o.p.t Ag, 0.09 o.p.t. Au, 0.78% Cu, and 0.38% Pb (pg.38 of the report), including 60 feet true width intercept assaying 25.00% Zn, 3.80 o.p.t Ag, 0.130 o.p.t. Au, 0.38% Cu, and 0.41% Pb.

Details of the Technical Report:

The Table below outlines the Mineral Resource Statement for the South Mountain Project as of April 7, 2018.

Mineral Resources at 6.04% ZnEq Cut-off | |||||||||||||

Classification | Zinc Equivalent Resource | Contained Metal | |||||||||||

Short Tons | ZnEq lbs | ZnEq % | Zn lbs | Zn% | Ag oz | Ag opt | Au oz | Au opt | Pb lbs | Pb % | Cu lbs | Cu % | |

x1000 | x1000 | x1000 | x1000 | x1000 | x1000 | x1000 | |||||||

Measured | 63.2 | 22,200 | 17.57 | 14,700 | 11.64 | 237 | 3.745 | 4.0 | 0.063 | 600 | 0.483 | 700 | 0.566 |

Indicated | 106.7 | 37,800 | 17.72 | 21,500 | 10.08 | 576 | 5.398 | 7.0 | 0.066 | 2,100 | 0.983 | 1,600 | 0.766 |

Measured + Indicated | 169.9 | 60,000 | 17.66 | 36,200 | 10.66 | 813 | 4.783 | 11.0 | 0.065 | 2,700 | 0.797 | 2,300 | 0.692 |

Inferred massive sulfide | 363.2 | 120,800 | 16.63 | 70,500 | 9.70 | 2,029 | 5.585 | 16.3 | 0.045 | 8,700 | 1.202 | 5,200 | 0.696 |

Notes:

1.The effective date of the mineral resource estimate is April 7th, 2018. The QP for the estimate is Mr. Randall K. Martin, of Hard Rock Consulting, LLC. and is independent of THMG.

2.Mineral resources that are not mineral reserves do not have demonstrated economic viability. Inferred mineral resources are that part of the mineral resource for which quantity and grade or quality are estimated on the basis of limited geologic evidence and sampling, which is sufficient to imply but not verify grade or quality continuity. Inferred mineral resources may not be converted to mineral reserves. It is reasonably expected, though not guaranteed, that the majority of Inferred mineral resources could be upgraded to Indicated mineral resources with continued exploration.

3.The mineral resource is reported at an underground mining cutoff of 6.04% Zinc Equivalent Grade (“ZnEq”) within coherent wireframe models. The ZnEq calculation and cutoff is based on the following assumptions: an Au price of $1,231/oz, Ag price of $16.62/oz, Pb price of $0.93/lb., Zn price of $1.10/lb. and Cu price of $2.54/lb.; metallurgical recoveries of 75% for Au, 70% for Ag, 87% for Pb, 96% for Zn and 56% for Cu, assumed mining cost of $70/ton, process costs of $25/ton, general

16

and administrative costs of $7.5/ton, smelting and refining costs of $25/ton. Based on the stated prices and recoveries the ZnEq formula is calculated as follows; ZnEq = (Au grade * 43.71) + (Ag grade * 0.55) + (Pb grade * 0.77) + (Cu grade * 1.35) + (Zn grade)

4.Rounding may result in apparent differences when summing tons, grade and contained metal content. Tonnage and grade measurements are in imperial units.

The updated resource model does not include any of the remaining polymetallic massive sulfide left in the upper part of the Laxey zone. Available historic smelter records indicate that approximately 53,642 tons of polymetallic massive sulfide were mined and direct shipped, mostly from this Zone. Historical smelter records indicate zinc values averaging 14.5%, lead 2.4%, copper 1.4%, silver at 10.6 opt, and gold at 0.058 opt (Table 6-2 of the Technical Report).

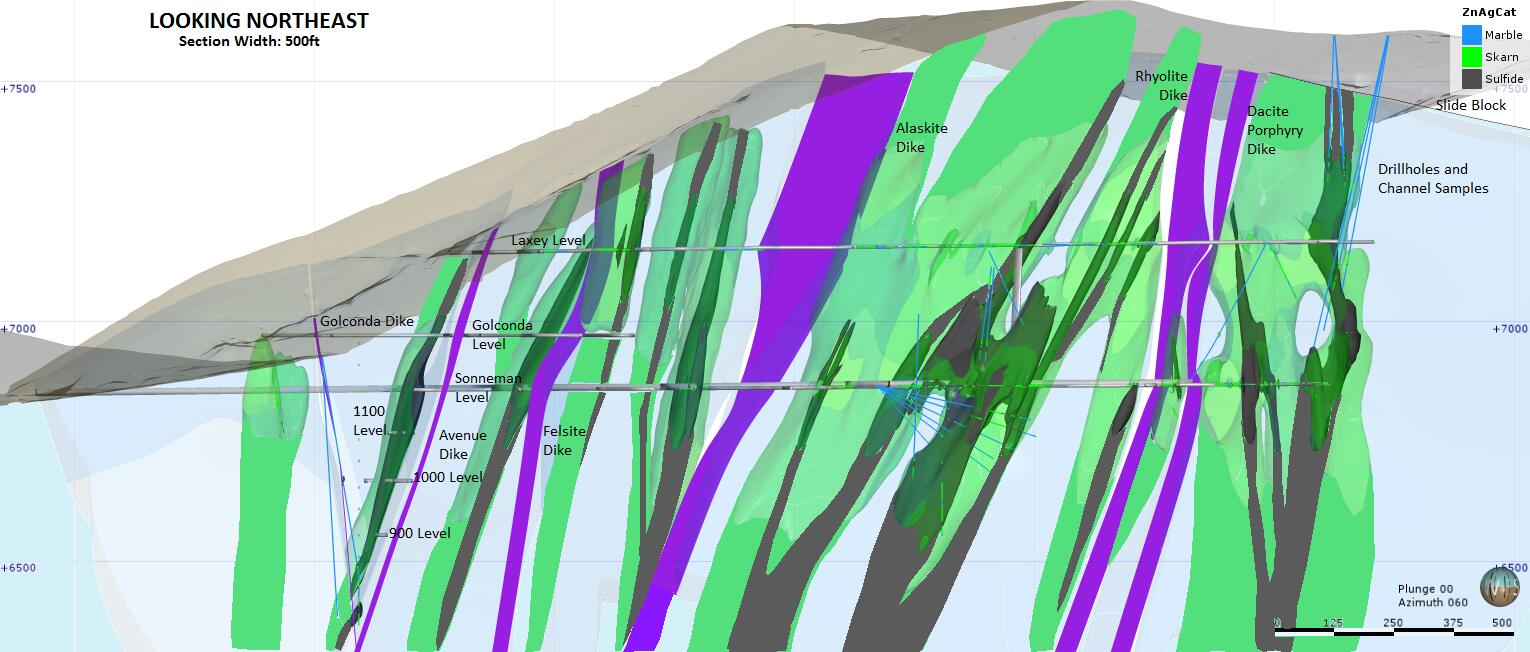

Long Section View of Modeled Estimation Domains. The deposit remains open along strike and down dip in the Laxey marble as shown in Figure 7-4 of the updated NI 43-101 Report.

Schematic Long Section of South Mountain Skarn Deposits

17

Underground Pre-Development Work Completed Since the Previous Technical Reports

The reconstruction of the Sonneman and Laxey drifts continued successfully until January 2014 when the Project went into care and maintenance. The Sonneman Level advanced 2,711 feet from the portal and is constructed to 12 feet by 12 feet for future development and mining. Approximately 350 feet of drift remains to be rehabilitated to reach the historic Texas massive sulfide zone located at the end of the old workings. This advance through this zone will allow for the drill stations and underground drilling to further define the high-grade resource encountered by William Bowes group in the 1980s.

The historic 2,200-foot long Laxey Level drift has been rehabilitated to 10 feet by 10 feet for approximately 720 feet. At that point the old tunnel had recently collapsed at an intrusive dike and preparations were being made to advance through the caved area. This old tunnel was rehabilitated and accessed along its full length in 2008, at which point it intercepted the Texas massive sulfide zone, one of many that had limited mining during and after the World War II period. Excellent high-grade massive sulfide is exposed in this area, and the core drilling during 2013 proved its continuity between the Laxey Level and the surface, an up-dip distance of nearly 400 feet.

During the development of the Sonneman Level during 2012-2013 several massive sulfide mineralized zones were mined through. Detailed rib sampling along some of these zones yielded the following results:

Significant THMG Channel Sample Intervals– Sonneman Drift

ID | From | To | Length | Ag (opt) | Zn % | Au (opt) | Cu % | Pb % |

OGT161671-02 | 30.0 | 160.0 | 130.00 | 4.11 | 16.76 | 0.09 | 0.78 | 0.38 |

OGT161671-02 | 209.2 | 230.2 | 21.00 | 3.14 | 14.02 | 0.26 | 0.31 | 0.37 |

OGT161671-02 | 270.2 | 275.0 | 4.80 | 3.21 | 13.80 | 0.24 | 0.14 | 1.10 |

OGT161714-22 | 9.0 | 32.0 | 23.00 | 7.18 | 14.69 | 0.01 | 1.17 | 0.65 |

OGT161714-22 | 76.9 | 92.0 | 15.10 | 8.24 | 14.04 | 0.01 | 2.30 | 0.59 |

OGT161735-9 | 0.0 | 40.0 | 40.00 | 13.97 | 16.44 | 0.02 | 0.70 | 0.86 |

OGT161724-30 | 0.0 | 40.0 | 40.00 | 5.80 | 5.63 | 0.00 | 0.28 | 2.83 |

Underground core drilling is planned for extending and upgrading the South Mountain resource - testing the continuity and down-dip extensions of the high-grade polymetallic massive sulfide zones. One core drill will begin on the DMEA and Laxey zones to complete the confirmation and extensional drilling, while the other core drill will focus primarily on the Texas zone to extend resources at depth beyond the current inferred resource area. In Addition, bulk samples will be mined for metallurgical test work. More than 15,000 feet (4,500 meters) have been drilled at South Mountain and included in the model. The South Mountain historic ore zones remain open down-dip on the zones encountered. The successful drilling and development work prove that the South Mountain resource continues to grow with potential to increase the resource substantially.

HRC also reviewed the data on the anomalous gold-bearing multilithic breccia that was identified by THMG conducting reconnaissance work at South Mountain. In 2010, five holes were drilled in the anomaly for a total footage of 3,530 feet, and 705 total samples taken every five feet of drill hole. Of the 705 samples taken, 686 samples contained anomalous gold, or 97% of the samples. The highest-grade intercept ran 0.038 ounce per ton. HRC reviewed the reports done on the breccia completed by both Kinross and Newmont; of note was Newmont’s comparison of the geology to the Battle Mountain Complex in Nevada.

Qualified Person – Edward D. Fields is the Qualified Person as defined by National Instrument 43-101 responsible for the technical data reported in this news release.

This property is without known reserves and the proposed program is exploratory in nature according to Instruction 3 to paragraph (b)(5) of Industry Guide 7. There are currently no permits required for conducting exploration in accordance with the Company`s current board approved exploration plan.

18

Trout Creek Project, Lander County, Nevada

The Trout Creek gold exploration project is a pediment target located along the western flank of the Shoshone Mountain Range in the Reese River Valley in Lander County, Nevada. The claim package consists of 78 unpatented mining claims (approximately 1560 acres) that are situated along a recognizable structural zone in the Eureka-Battle Mountain mineralized gold trend. Thunder Mountain maintained a joint venture agreement with Newmont Mining on some of their adjoining mineral rights sections and aliquot parcels from 2011 thru 2016. On October 27, 2016 the Company terminated the exploration agreement with Newmont Mining Corporation to concentrate their efforts on the South Mountain Project. The Company retained the 78-claim package by paying annual fees to BLM of $3,255 and Lander County $940 fees.

The Project is located approximately 155 air miles northeast of Reno, Nevada, or approximately 20 miles south of Battle Mountain, Nevada, in Sections 10, 11, 14, 16, 21, 22, 27; T.29N.; R.44E. Mount Diablo Baseline & Meridian, Lander County, Nevada. Latitude: 40 23’ 36” North, Longitude: 117 00’ 58” West. The property is accessible by traveling south from Battle Mountain Nevada on state highway 305, which is paved. The project is generally accessible year-round and there are no improvements on the property.

The Trout Creek target is anchored by a regional gravity anomaly on a well-defined northwest-southeast trending break in the alluvial fill thickness and underlying bedrock. Previous geophysical work in the 1980s revealed an airborne magnetic anomaly associated with the same structure, and this was further verified and outlined in 2008 by Company personnel using a ground magnetometer. The target is covered by alluvial fan deposits of generally unknown thickness shed from the adjacent Shoshone Range, a fault block mountain range composed of Paleozoic sediments of both upper and lower plate rocks of the Roberts Mountains thrust.

An extensive data package on the area was made available to Thunder Mountain Gold by Newmont during the joint exploration agreement period (2011-2016) that significantly enhanced the target area. This, along with fieldwork consisting of mapping and sampling the altered and mineralized structures that can be followed through the Shoshone Range. Of importance is that these structures align with the Cortez-Pipeline deposits and the Phoenix deposit (part of the Eureka-Battle Mountain-Getchell Trend).

In addition to the geologic fieldwork, Wright Geophysics conducted a ground gravity survey and CSMAT over the pediment target area and this provided insight into the gravel-bedrock contact as well as defining the favorable structural setting within the buried bedrock. An untested drill target was identified under the gravel pediment along these structures, and the geophysics showed that the bedrock was within a reasonable depth for exploration drilling and potential mining if a significant mineralization is encountered.

Thunder Mountain Gold identified pre-defined drill targets during the Joint Exploration Agreement with Newmont Mining. Atoka Gold, a private Nevada corporation, owns significant claims adjacent to the Trout Creek project, has expressed an interest to combine their claim package with the Trout Creek project through a joint venture. The Company perceives advantages to a joint venture, as it resembles a large pediment play in the Reese River Valley. There have been no details discussed of a structured agreement but talks continue with Atoka Gold. A detailed list of claims controlled by the Company can be found in the Company`s Form 10K filed on Edgar.

The ongoing exploration field work, including claim maintenance and assessment, is financed by the Company through sales of unregistered common stock funded by the Company through private placements with accredited investors. Future work will be funded in the same manner or through a strategic partnership with another mining company.

There are currently no environmental permits required for the planned exploration work on the property. In the future, a notice of intent may be required with the Bureau of Land Management. This property is without known reserves and the proposed program is exploratory in nature according to Instruction 3 to paragraph (b)(5) of Industry Guide 7.

19

Competition

We are an exploration stage company. We compete with other mineral resource exploration and development companies for financing and for the acquisition of new mineral properties. Many of the mineral resource exploration and development companies with whom we compete have greater financial and technical resources than us. Accordingly, these competitors may be able to spend greater amounts on acquisitions of mineral properties of merit, on exploration of their mineral properties and on development of their mineral properties. In addition, they may be able to afford greater geological expertise in the targeting and exploration of mineral properties. This competition could result in competitors having mineral properties of greater quality and interest to prospective investors who may finance additional exploration and development. This competition could adversely impact on our ability to finance further exploration and to achieve the financing necessary for us to develop our mineral properties.

Employees

Three of the Company’s officers had been deferring compensation for services . At September 30, 2018, SMMI has deferred payroll of $1,041,500. These salaries were earned in accordance with the OGT LLC operating agreement. OGT management includes SMMI`s Eric Jones, Jim Collord, and Larry Thackery as CFO. On July 31, 2018 the Company stopped expensing deferring compensation for the three Company officers, in the interest of marketing the SMMI project. There will be no recognized officer salaries until available funds are raised.

Results of Operations:

The Company recognized no revenues and had no production for the nine months ending September 30, 2018. Total operating expenses for the nine months ending September 30, 2018 of $562,440 increased from the same respective time frame ending 2017 by $25,907 or 5%. Exploration expenses for the nine months ended September 30, 2018 increased by $52,662 when compared to same period in 2017. This increase can be attributed to the engagement of Hard Rock Consulting LLC to update the NI 43-101. Legal and accounting costs increased from the same period in 2017 by $64,549 for a total of $113,524. The Company engages Baird Hanson LLP (“Baird”), a company owned by one of the Company’s directors, to provide legal services. During the nine-month period ended September 30, 2018, the Company incurred $65,372 in legal expense with Mr. Baird. There was no expense for the comparable periods in 2017. Management and administrative expense decreased by $69,904 or 25% mostly due to stock options compensation of $53,558 issued to our directors in March 2017, and the discontinued deferred salaries.

Liquidity and Capital Resources:

The consolidated financial statements for the three and nine-month periods ending September 30, 2018 disclose a ‘going concern’ qualification to our ability to continue in business. The consolidated financial statements for the period then ended have been prepared under the assumption that we will continue as a going concern. Such assumption contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the consolidated financial statements for the period ended September 30, 2018, we did not have sufficient cash reserves to cover normal operating expenditures for the following 12 months. These factors raise substantial doubt about our ability to continue as a going concern. The consolidated financial statements do not include any adjustments that might be necessary should we be unable to continue as a going concern.

Our continuation as a going concern is dependent upon our ability to generate enough cash flow to meet our obligations on a timely basis, to obtain additional financing as may be required, or ultimately to attain profitability. Potential sources of cash, or relief of demand for cash, include additional external debt, the sale of shares of our stock or alternative methods such as mergers or sale of our assets. No assurances can be given, however, that we will be able to obtain any of these potential sources of cash. We currently require additional cash funding from outside sources to sustain existing operations and to meet current obligations and ongoing capital requirements.

Our plans for the long-term continuation as a going concern include financing our future operations through sales of our common stock and/or debt and the eventual profitable exploitation of our mining properties. Our plans may also, at some future point, include the formation of mining joint ventures with senior mining company partners on specific mineral properties whereby the joint venture partner would provide the necessary financing in return for equity in the property.

20

While the Company does not currently have cash sufficient to support the currently planned aggressive exploration work at South Mountain, we believe that the survivability of Thunder Mountain Gold can be assisted by the following:

October 22, 2018, we had $11,560 cash in our bank accounts.

Management and the Board have not undertaken plans or commitments that exceed the cash available to the Company beyond fiscal quarter ending September 30, 2018. We do not include in this consideration any additional investment funds mentioned below. Management is committed to manage expenses of all types to not exceed the on-hand cash resources of the Company at any point in time, now or in the future.

The Company will also consider other sources of funding, including potential mergers and/or additional farm-out of some of its exploration properties.

For the nine months ended September 30, 2018, net cash used for operating activities was $258,906, consisting of net loss of $584,586 reduced by non-cash expenses and changes in current assets and current liabilities. Cash provided by financing activities for nine months ended September 30, 2018 totaled $252,567 principally from the sale of our common stock.

Our future liquidity and capital requirements will depend on many factors, including timing, cost and progress of our exploration efforts, our evaluation of, and decisions with respect to, our strategic alternatives, and costs associated with the regulatory approvals. If it turns out that we do not have enough money to complete our exploration programs, we will attempt to raise additional funds from a public offering, a private placement, mergers, farm-outs or loans.

We know that additional financing will be required in the future to fund our planned operations. We do not know whether additional financing will be available when needed or on acceptable terms, if at all. If we are unable to raise additional financing when necessary, we may have to delay our exploration efforts or any property acquisitions or be forced to cease operations. Collaborative arrangements may require us to relinquish our rights to certain of our mining claims.

Private Placement

On February 20, 2018, the Board of Directors approved a Private Placement financing of up to $750,000 from the sale of equity units at a price of $0.14 per unit. Each unit consists of one share of the Company’s common stock and one-half of one common share purchase warrant. On April 27, 2018 the Company closed its Private Placement. In total, 2,550,000 units were sold representing 2,550,000 shares of common stock and 1,275,000 warrants to purchase common stock for $0.20 over the next 12 months. Total proceeds were $357,000. Of this amount, $252,988 was received in cash and $104,012 was in exchange for retirement of a related party convertible note payable and related accrued interest payable.

The offering was believed exempt from registration pursuant to the exemption for transactions by an issuer not involving any public offering under Section 4(6) the Securities Act of 1933, as amended. The securities offered, sold, and issued in connection with the private placement have not been or are not registered under the Securities Act of 1933, as amended, or any state securities laws and may not be offered or sold in the United States absent registration with the Securities and Exchange Commission or an applicable exemption from the registration requirements.

Subsequent Events

None to Report

Contractual Obligations

During 2008 and 2009, three lease arrangements were made with land owners that own land parcels adjacent to the Company’s South Mountain patented and unpatented mining claims. The leases were for a seven-year period, with options to renew, with annual payments (based on $20 per acre) listed in the following table. The leases have no work requirements.

21

Payments due by period | |||||

Total* | Less than 1 year | 2-3 years | 4-5 years | More than 5 years | |

Acree Lease (yearly, June)(1) | $27,120 | $3,390 | $6,780 | $6,780 | $10,170 |

Lowry Lease (yearly, October)(1)(2) | $90,240 | $11,280 | $22,560 | $22,560 | $33,840 |

OGT LLC(3) | $50,000 | $5,000 | $10,000 | $10,000 | $25,000 |

Total | $167,360 | $19,670 | $39,340 | $39,340 | $69,010 |

(1)Amounts shown are for the lease periods years 4 through 7, a total of 1 years that remains after 2013, the second year of the lease period. Lease was extended an additional 10 years at $30/acre.

(2)The Lowry lease has an early buy-out provision for 50% of the remaining amounts owed in the event the Company desires to drop the lease prior to the end of the first seven-year period.

(3) OGT LLC, managed by the Company’s wholly-owned subsidiary SMMI, receives a $5,000 per year payment for up to 10 years, or until a $5 million capped NPI Royalty is paid.

Critical Accounting Policies

We have identified our critical accounting policies, the application of which may materially affect the financial statements, either because of the significance of the financials statement item to which they relate, or because they require management’s judgment in making estimates and assumptions in measuring, at a specific point in time, events which will be settled in the future. The critical accounting policies, judgments and estimates which management believes have the most significant effect on the financial statements are set forth below:

a)Estimates. Our management routinely makes judgments and estimates about the effect of matters that are inherently uncertain. As the number of variables and assumptions affecting the future resolution of the uncertainties increase, these judgments become even more subjective and complex. Although we believe that our estimates and assumptions are reasonable, actual results may differ significantly from these estimates. Changes in estimates and assumptions based upon actual results may have a material impact on our results of operation and/or financial condition.

b)Stock-based Compensation. The Company records stock-based compensation in accordance with ASC 718, “Compensation – Stock Compensation” using the fair value method. All transactions in which goods or services are the consideration received for the issuance of equity instruments are accounted for based on the fair value of the consideration received or the fair value of the equity instrument issued, whichever is more reliably measurable.

c)Income Taxes. We have current income tax assets recorded in our financial statements that are based on our estimates relating to federal and state income tax benefits. Our judgments regarding federal and state income tax rates, items that may or may not be deductible for income tax purposes and income tax regulations themselves are critical to the Company’s financial statement income tax items.

Item 3. Quantitative and Qualitative Disclosures about Market Risk

Not required for smaller reporting companies.

22

Item 4. Controls and Procedures

Evaluation of Disclosure Controls and Procedures

At the end of the period covered by this report, an evaluation was carried out under the supervision of, and with the participation of, the Company’s Management, including the Chief Executive Officer and Chief Financial Officer, of the effectiveness of the design and operation of the Company’s disclosure controls and procedures (as defined in Rule 13a – 15(e) and Rule 15d – 15(e) of the Securities and Exchange Act of 1934, as amended). Based on that evaluation, the Chief Executive Officer and Chief Financial Officer have concluded that as of the end of the period covered by this report, the Company’s disclosure controls and procedures were adequately designed and effective in ensuring that information required to be disclosed by the Company in its reports that it files or submits to the SEC under the Exchange Act, is recorded, processed, summarized and reported within the time period specified in applicable rules and forms.

Changes in Internal Controls Over Financial Reporting

During the quarter covered by this report, there have been no changes in the Company’s internal control over financial reporting that have materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting.

23

None.

Not required for smaller reporting companies.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds.

On February 20, 2018, the Board of Directors approved a Private Placement financing of up to $750,000 from the sale of equity units at a price of $0.14 per unit. Each unit consists of one share of the Company’s common stock and one-half of one common share purchase warrant. Each whole warrant entitles the holder to purchase one additional share of common stock of the Company at a price of $0.20 for a period of 12 months. No finder’s fees were to be paid. Thunder Mountain Gold will utilize the net proceeds from this financing for working capital, mineral leases, and administrative expenses.

Item 3. Defaults Upon Senior Securities.

None.

Item 4. Mine Safety Disclosures

Pursuant to Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”), issuers that are operators, or that have a subsidiary that is an operator, of a coal or other mine in the United States are required to disclose in their periodic reports filed with the SEC information regarding specified health and safety violations, orders and citations, related assessments and legal actions, and mining-related fatalities.

During the three months and nine-month periods ended September 30, 2018, the Company did not have any operating mines and therefore had no such specified health and safety violations, orders or citations, related assessments or legal actions, mining-related fatalities, or similar events in relation to the Company’s United States operations requiring disclosure pursuant to Section 1503(a) of the Dodd-Frank Act.

None.

24

(a) Documents which are filed as a part of this report:

Exhibits:

31.1 – Certification Required by Rule 13a-14(a) or Rule 15d-14(a). Jones

31.2 – Certification Required by Rule 13a-14(a) or Rule 15d-14(a). Thackery

101*The following financial information from our Quarterly Report on Form 10-Q for the quarter ended September 30, 2018 formatted in Extensible Business Reporting Language (XBRL): (i) the Consolidated Balance Sheets, (ii) the Consolidated Statements of Operations, (iii) the Consolidated Statements of Cash Flows, and (iv) Consolidated Notes to Financial Statements

25

Pursuant to the requirements of Section 13 or 15(b) of the Securities and Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf of the undersigned, thereunto duly authorized.

THUNDER MOUNTAIN GOLD, INC.

/s/ Eric T. Jones

By

Eric T. Jones

President and Chief Executive Officer

Date: November 13, 2018

Pursuant to the requirements of the Securities Act of 1934 this report signed below by the following person on behalf of the Registrant and in the capacities on the date indicated.

/s/ Larry Thackery

By

Larry Thackery

Chief Financial Officer

Date; November 13, 2018

26