Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Vertex Energy Inc. | a09302018-ex322.htm |

| EX-32.1 - EXHIBIT 32.1 - Vertex Energy Inc. | a09302018-ex321.htm |

| EX-31.2 - EXHIBIT 31.2 - Vertex Energy Inc. | a09302018-ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - Vertex Energy Inc. | a09302018-ex311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal quarter ended September 30, 2018

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM _____________ TO _____________

Commission File Number 001-11476

———————

VERTEX ENERGY, INC.

(Exact name of registrant as specified in its charter)

———————

NEVADA | 94-3439569 |

(State or other jurisdiction of | (I.R.S. Employer Identification No.) |

incorporation or organization) | |

1331 GEMINI STREET, SUITE 250 HOUSTON, TEXAS | 77058 |

(Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: 866-660-8156

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ | Accelerated filer ¨ |

Non-accelerated filer ¨ | Smaller reporting company ý |

Emerging growth ¨ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.

Yes ¨ No ý

State the number of shares of the issuer’s common stock outstanding, as of the latest practicable date: 40,007,520 shares of common stock are issued and outstanding as of November 5, 2018.

TABLE OF CONTENTS

Page | |||

PART I | |||

Item 1. | |||

Item 2 | |||

Item 3. | |||

Item 4. | |||

PART II | |||

Item 1. | |||

Item 1A. | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Item 5. | |||

Item 6. | |||

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

VERTEX ENERGY, INC.

CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

September 30, 2018 | December 31, 2017 | ||||||

ASSETS | |||||||

Current assets | |||||||

Cash and cash equivalents | $ | 1,840,345 | $ | 1,105,787 | |||

Accounts receivable, net | 14,380,264 | 11,288,991 | |||||

Federal income tax receivable | 137,212 | — | |||||

Inventory | 6,646,171 | 6,304,842 | |||||

Prepaid expenses | 3,973,105 | 1,771,832 | |||||

Total current assets | 26,977,097 | 20,471,452 | |||||

Noncurrent assets | |||||||

Fixed assets, at cost | 66,781,807 | 65,237,652 | |||||

Less accumulated depreciation | (18,671,219 | ) | (16,617,824 | ) | |||

Fixed assets, net | 48,110,588 | 48,619,828 | |||||

Goodwill and other intangible assets, net | 13,210,821 | 14,499,354 | |||||

Federal income tax receivable | 137,211 | 274,423 | |||||

Other assets | 694,059 | 440,417 | |||||

TOTAL ASSETS | $ | 89,129,776 | $ | 84,305,474 | |||

LIABILITIES, TEMPORARY EQUITY, AND EQUITY | |||||||

Current liabilities | |||||||

Accounts payable and accrued expenses | $ | 9,805,852 | $ | 10,318,738 | |||

Dividends payable | 479,311 | 420,713 | |||||

Capital leases-current | 92,900 | — | |||||

Current portion of long-term debt, net of unamortized finance costs | 2,167,171 | 1,616,926 | |||||

Derivative commodity liability | 601,534 | — | |||||

Revolving note | 5,999,733 | 4,591,527 | |||||

Total current liabilities | 19,146,501 | 16,947,904 | |||||

Long-term liabilities | |||||||

Long-term debt, net of unamortized finance costs | 14,483,702 | 13,531,179 | |||||

Capital leases-long-term | 322,538 | — | |||||

Contingent consideration | 108,564 | 236,680 | |||||

Derivative warrant liability | 4,370,379 | 2,245,408 | |||||

Total liabilities | 38,431,684 | 32,961,171 | |||||

COMMITMENTS AND CONTINGENCIES (Note 3) | — | — | |||||

TEMPORARY EQUITY | |||||||

Series B Convertible Preferred Stock, $0.001 par value per share; 10,000,000 shares designated, 3,551,549 and 3,427,597 shares issued and outstanding at September 30, 2018 and December 31, 2017, respectively with a liquidation preference of $11,009,802 and $10,625,551 at September 30, 2018 and December 31, 2017, respectively. | 8,432,160 | 7,190,467 | |||||

Series B1 Convertible Preferred Stock, $0.001 par value per share; 17,000,000 shares designated, 11,074,331 and 13,151,989 shares issued and outstanding at September 30, 2018 and December 31, 2017, respectively with a liquidation preference of $17,275,956 and $20,517,103 at September 30, 2018 and December 31, 2017, respectively. | 14,387,804 | 15,769,478 | |||||

Total Temporary Equity | 22,819,964 | 22,959,945 | |||||

F-1

September 30, 2018 | December 31, 2017 | ||||||

EQUITY | |||||||

50,000,000 of total Preferred shares authorized: | |||||||

Series A Convertible Preferred Stock, $0.001 par value; 5,000,000 shares designated, 419,859 and 453,567 shares issued and outstanding at September 30, 2018 and December 31, 2017, respectively with a liquidation preference of $625,590 and $675,815 at September 30, 2018 and December 31, 2017, respectively. | 420 | 454 | |||||

Series C Convertible Preferred Stock, $0.001 par value; 44,000 shares designated, 31,568 shares issued and outstanding at December 31, 2017, with a liquidation preference of $3,156,800 at December 31, 2017. | — | 32 | |||||

Common stock, $0.001 par value per share; 750,000,000 shares authorized; 38,840,890 and 32,658,176 shares issued and outstanding at September 30, 2018 and December 31, 2017, respectively. | 38,841 | 32,658 | |||||

Additional paid-in capital | 72,974,146 | 67,768,509 | |||||

Accumulated deficit | (45,508,871 | ) | (39,816,300 | ) | |||

Total Vertex Energy, Inc. stockholders' equity | 27,504,536 | 27,985,353 | |||||

Non-controlling interest | 373,592 | 399,005 | |||||

Total Equity | 27,878,128 | 28,384,358 | |||||

TOTAL LIABILITIES, TEMPORARY EQUITY, AND EQUITY | $ | 89,129,776 | $ | 84,305,474 | |||

See accompanying notes to the consolidated financial statements

F-2

VERTEX ENERGY, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

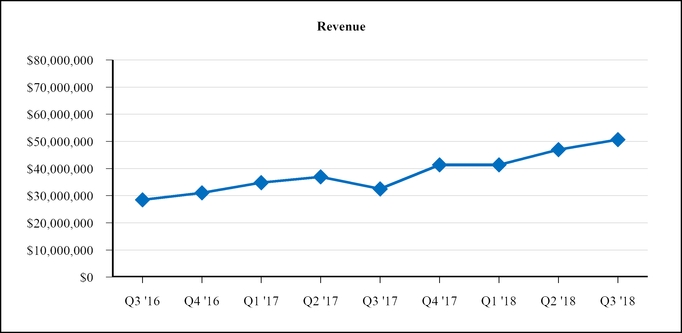

Revenues | $ | 50,632,948 | $ | 32,470,451 | $ | 138,918,913 | $ | 104,153,844 | ||||||||

Cost of revenues (exclusive of depreciation and amortization shown separately below) | 42,593,367 | 28,696,461 | 114,434,776 | 90,864,044 | ||||||||||||

Gross profit | 8,039,581 | 3,773,990 | 24,484,137 | 13,289,800 | ||||||||||||

Operating expenses: | ||||||||||||||||

Selling, general and administrative expenses | 5,658,659 | 5,690,761 | 16,668,692 | 16,280,495 | ||||||||||||

Depreciation and amortization | 1,806,839 | 1,697,821 | 5,234,014 | 4,942,911 | ||||||||||||

Total operating expenses | 7,465,498 | 7,388,582 | 21,902,706 | 21,223,406 | ||||||||||||

Income (loss) from operations | 574,083 | (3,614,592 | ) | 2,581,431 | (7,933,606 | ) | ||||||||||

Other income (expense): | ||||||||||||||||

Interest income | — | 1,519 | 659 | 5,748 | ||||||||||||

Gain (loss) on sale of assets | — | 25,693 | 51,523 | (13,806 | ) | |||||||||||

Gain (loss) on change in value of derivative warrant liability | (2,169,133 | ) | 1,371,461 | (2,124,971 | ) | 2,676,902 | ||||||||||

Interest expense | (798,800 | ) | (733,459 | ) | (2,448,771 | ) | (2,688,394 | ) | ||||||||

Total other income (expense) | (2,967,933 | ) | 665,214 | (4,521,560 | ) | (19,550 | ) | |||||||||

Income (loss) before income tax | (2,393,850 | ) | (2,949,378 | ) | (1,940,129 | ) | (7,953,156 | ) | ||||||||

Income tax benefit (expense) | — | — | — | — | ||||||||||||

Net income (loss) | (2,393,850 | ) | (2,949,378 | ) | (1,940,129 | ) | (7,953,156 | ) | ||||||||

Net income (loss) attributable to non-controlling interest | (105,970 | ) | 34,554 | 76,305 | 94,690 | |||||||||||

Net income (loss) attributable to Vertex Energy, Inc. | (2,287,880 | ) | (2,983,932 | ) | (2,016,434 | ) | (8,047,846 | ) | ||||||||

Accretion of discount on Series B and B-1 Preferred Stock | (515,698 | ) | (424,480 | ) | (1,444,376 | ) | (1,267,778 | ) | ||||||||

Accrual of dividends on Series B and B-1 Preferred Stock | (1,831,794 | ) | (420,713 | ) | (3,191,217 | ) | (1,256,921 | ) | ||||||||

Net income (loss) available to common shareholders | $ | (4,635,372 | ) | $ | (3,829,125 | ) | $ | (6,652,027 | ) | $ | (10,572,545 | ) | ||||

Income (loss) per common share | ||||||||||||||||

Basic | $ | (0.13 | ) | $ | (0.12 | ) | $ | (0.20 | ) | $ | (0.32 | ) | ||||

Diluted | $ | (0.13 | ) | $ | (0.12 | ) | $ | (0.20 | ) | $ | (0.32 | ) | ||||

Shares used in computing earnings per share | ||||||||||||||||

Basic | 35,144,113 | 32,655,135 | 33,843,721 | 32,651,961 | ||||||||||||

Diluted | 35,144,113 | 32,655,135 | 33,843,721 | 32,651,961 | ||||||||||||

See accompanying notes to the consolidated financial statements

F-3

VERTEX ENERGY, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

NINE MONTHS ENDED SEPTEMBER 30, 2018 AND 2017 (UNAUDITED)

Nine Months Ended | |||||||

September 30, 2018 | September 30, 2017 | ||||||

Cash flows from operating activities | |||||||

Net income (loss) | $ | (1,940,129 | ) | $ | (7,953,156 | ) | |

Adjustments to reconcile net loss to cash provided by (used in) operating activities | |||||||

Stock based compensation expense | 494,779 | 460,475 | |||||

Depreciation and amortization | 5,234,014 | 4,942,911 | |||||

(Gain) loss on sale of assets | (51,523 | ) | 13,806 | ||||

(Increase) decrease in fair value of derivative warrant liability | 2,124,971 | (2,676,902 | ) | ||||

Loss on commodity derivative contracts | 1,859,234 | — | |||||

Net cash settlements on commodity derivatives | (2,386,897 | ) | — | ||||

Amortization of debt discount and deferred costs | 474,360 | 571,635 | |||||

Changes in operating assets and liabilities | |||||||

Accounts receivable | (3,091,273 | ) | 2,054,774 | ||||

Inventory | (341,329 | ) | (195,977 | ) | |||

Prepaid expenses | (1,072,076 | ) | (65,603 | ) | |||

Accounts payable, accrued expenses, and other liabilities | (641,003 | ) | 329,959 | ||||

Other assets | (253,642 | ) | 129,500 | ||||

Net cash provided by (used in) operating activities | 409,486 | (2,388,578 | ) | ||||

Cash flows from investing activities | |||||||

Acquisition of SES | (269,826 | ) | — | ||||

Acquisition of Acadiana | — | (710,350 | ) | ||||

Acquisition of Nickco | — | (1,126,730 | ) | ||||

Acquisition of Ygriega | — | (162,500 | ) | ||||

Purchase of fixed assets | (1,813,904 | ) | (1,842,237 | ) | |||

Proceeds from sale of fixed assets | 6,848 | 297,718 | |||||

Net cash used in investing activities | (2,076,882 | ) | (3,544,099 | ) | |||

Cash flows from financing activities | |||||||

Payments on capital leases | (34,660 | ) | — | ||||

Payment of debt issuance costs | — | (1,718,090 | ) | ||||

Line of credit (payments) proceeds, net | 1,408,206 | 1,012,444 | |||||

Proceeds from note payable | 4,024,964 | 16,570,929 | |||||

Payments on note payable | (2,996,556 | ) | (12,013,925 | ) | |||

Net cash provided by financing activities | 2,401,954 | 3,851,358 | |||||

Net change in cash, cash equivalents and restricted cash | 734,558 | (2,081,319 | ) | ||||

Cash, cash equivalents, and restricted cash at beginning of the period | 1,105,787 | 3,206,158 | |||||

Cash, cash equivalents, and restricted cash at end of period | $ | 1,840,345 | $ | 1,124,839 | |||

F-4

SUPPLEMENTAL INFORMATION | |||||||

Cash paid for interest | $ | 2,034,275 | $ | 1,328,401 | |||

Cash paid for taxes | $ | — | $ | — | |||

NON-CASH INVESTING AND FINANCING TRANSACTIONS | |||||||

Conversion of Series A Preferred Stock into common stock | $ | 34 | $ | 36 | |||

Conversion of Series B-1 Preferred Stock into common stock | $ | 4,616,354 | $ | 119,440 | |||

Accretion of discount on Series B and B-1 Preferred Stock | $ | 1,444,376 | $ | 1,267,778 | |||

Dividends-in-kind accrued on Series B and B-1 Preferred Stock | $ | 3,191,217 | $ | 1,256,920 | |||

Equipment acquired under capital leases | $ | 450,098 | $ | — | |||

Contingent consideration on Nickco acquisition | $ | — | $ | 236,680 | |||

Common restricted shares for Nickco acquisition | $ | — | $ | 474,000 | |||

Return of common shares for sale escrow | $ | — | $ | 1,109 | |||

See accompanying notes to the consolidated financial statements

F-5

VERTEX ENERGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2018

(UNAUDITED)

NOTE 1. BASIS OF PRESENTATION AND NATURE OF OPERATIONS

The accompanying unaudited consolidated interim financial statements of Vertex Energy, Inc. (the "Company" or "Vertex Energy") have been prepared in accordance with accounting principles generally accepted in the United States of America and the rules of the Securities and Exchange Commission ("SEC") and should be read in conjunction with the audited consolidated financial statements and notes thereto for the year ended December 31, 2017, contained in the Company's annual report, as filed with the SEC on Form 10-K on March 7, 2018 (the "Form 10-K"). The December 31, 2017 balance sheet was derived from the audited financial statements of our 2017 Form 10-K. In the opinion of management all adjustments, consisting of normal recurring adjustments necessary for a fair presentation of financial position and the results of operations for the interim periods presented, have been reflected herein. The results of operations for interim periods are not necessarily indicative of the results to be expected for the full year. Notes to the consolidated financial statements which would substantially duplicate the disclosures contained in the audited consolidated financial statements for the most recent fiscal year 2017 as reported in Form 10-K have been omitted.

NOTE 2. SUMMARY OF CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Cash, Cash Equivalents and Restricted Cash

The Company considers all highly liquid investments with an original maturity of three months or less to be cash equivalents.

Inventory

Inventories of products consist of feedstocks, refined petroleum products and recovered ferrous and non-ferrous metals and are reported at the lower of cost or market. Cost is determined using the first-in, first-out (“FIFO”) method. The Company reviews its inventory commodities whenever events or circumstances indicate that the value may not be recoverable.

Impairment of long-lived assets

The Company evaluates the carrying value and recoverability of its long-lived assets when circumstances warrant such evaluation by applying the provisions of the Financial Accounting Standards Board Accounting Standards Codification ("FASB ASC") regarding long-lived assets. It requires that long-lived assets be reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable through the estimated undiscounted cash flows expected to result from the use and eventual disposition of the assets. Whenever any such impairment exists, an impairment loss will be recognized for the amount by which the carrying value exceeds the fair value. The Company determined that no long-lived asset impairment existed at September 30, 2018.

F-6

Fair value of financial instruments

Under the FASB ASC, we are permitted to elect to measure financial instruments and certain other items at fair value, with the change in fair value recorded in earnings. We elected not to measure any eligible items using the fair value option. Consistent with the Fair Value Measurement Topic of the FASB ASC, we implemented guidelines relating to the disclosure of our methodology for periodic measurement of our assets and liabilities recorded at fair market value.

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. A three-tier fair value hierarchy prioritizes the inputs used in measuring fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (level 1 measurements) and the lowest priority to unobservable inputs (level 3 measurements). These tiers include:

• | Level 1, defined as observable inputs such as quoted prices for identical instruments in active markets; |

• | Level 2, defined as inputs other than quoted prices in active markets that are either directly or indirectly observable such as quoted prices for similar instruments in active markets or quoted prices for identical or similar instruments in markets that are not active; and |

• | Level 3, defined as unobservable inputs in which little or no market data exists, therefore requiring an entity to develop its own assumptions, such as valuations derived from valuation techniques in which one or more significant inputs or significant value drivers are unobservable. |

Our Level 1 assets primarily include our cash and cash equivalents. Valuations are obtained from readily available pricing sources for market transactions involving identical assets or liabilities. The carrying amounts of accounts receivable, accounts payable and accrued liabilities approximate their fair values due to the immediate or short-term maturities of these financial instruments.

Our Level 2 liabilities include our marked to market changes in the estimated value of our open derivative contracts held at the balance sheet date.

Our Level 3 liabilities include our marked to market changes in the estimated value of our derivative warrants issued in connection with our Series B Preferred Stock and Series B1 Preferred Stock.

The Company estimates the fair values of the crude oil swaps and collars based on published forward commodity price curves for the underlying commodity as of the date of the estimate for which published forward pricing is readily available. The determination of the fair values above incorporates various factors including the impact of the Company's non-performance risk and the credit standing of the counterparty involved in the Company's derivative contracts. In addition, the Company routinely monitors the creditworthiness of its counterparty.

Nonfinancial assets and liabilities measured at fair value on a nonrecurring basis include certain nonfinancial assets and liabilities as may be acquired in a business combination and thereby measured at fair value.

Income Taxes

The Company accounts for income taxes in accordance with the FASB ASC Topic 740. The Company records a valuation allowance against net deferred tax assets if, based upon the available evidence, it is more likely than not that some or all of the deferred tax assets will not be realized. The ultimate realization of deferred tax assets is dependent upon the generation of future taxable income and when temporary differences become deductible. The Company considers, among other available information, uncertainties surrounding the recoverability of deferred tax assets, scheduled reversals of deferred tax liabilities, projected future taxable income, and other matters in making this assessment.

As part of the process of preparing its consolidated financial statements, the Company is required to estimate its income taxes in each of the jurisdictions in which it operates. This process requires the Company to estimate its actual current tax liability and to assess temporary differences resulting from differing book versus tax treatment of items, such as deferred revenue, compensation and benefits expense and depreciation. These temporary differences result in deferred tax assets and liabilities, which are included within the Company’s consolidated balance sheets. Significant management judgment is required in determining the Company’s provision for income taxes, its deferred tax assets and liabilities and any valuation allowance recorded against its net deferred tax assets. If actual results differ from these estimates or the Company adjusts these estimates in future periods, the Company may need to adjust its valuation allowance, which could materially impact the Company’s consolidated financial position and results of operations.

F-7

Tax contingencies can involve complex issues and may require an extended period of time to resolve. Changes in the level of annual pre-tax income can affect the Company’s overall effective tax rate. Furthermore, the Company’s interpretation of complex tax laws may impact its recognition and measurement of current and deferred income taxes.

Derivative Transactions

All derivative instruments are recorded on the accompanying balance sheets at fair value. These derivative transactions are not designated as cash flow hedges under FASB ASC 815, Derivatives and Hedges. Accordingly, these derivative contracts are marked-to-market and any changes in the estimated value of derivative contracts held at the balance sheet date are recognized in the accompanying statements of operations as net gain or loss on derivative contracts. The derivative assets or liabilities are classified as either current or noncurrent assets or liabilities based on their anticipated settlement date. The Company nets derivative assets and liabilities for counterparties where it has a legal right of offset.

In accordance with ASC 815-40-25 and ASC 815-10-15, Derivatives and Hedging and ASC 480-10-25, Liabilities-Distinguishing from Equity, convertible preferred shares are accounted for net, outside of shareholders' equity and warrants are accounted for as liabilities at their fair value during periods where they can be net cash settled in case of a change in control transaction. The warrants are accounted for as a liability at their fair value at each reporting period. The value of the derivative warrant liability will be re-measured at each reporting period with changes in fair value recorded in earnings. To derive an estimate of the fair value of these warrants, a Dynamic Black Scholes model is utilized which computes the impact of a possible change in control transaction upon the exercise of the warrant shares. This process relies upon inputs such as shares outstanding, our quoted stock prices, strike price and volatility assumptions to dynamically adjust the payoff of the warrants in the presence of the dilution effect.

Debt Issuance Costs

The Company follows the accounting guidance of ASC 835-30, Interest-Imputation of Interest, which requires that debt issuance costs related to a recognized debt liability be reported on the Consolidated Balance Sheet as a direct reduction from the carrying amount of that debt liability.

Reclassification of Prior Year Presentation

Certain prior period amounts have been reclassified to conform to current period presentation. These reclassifications had no effect on the reported results of operations.

Recently Issued Accounting Pronouncements

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers, which supersedes nearly all existing revenue recognition guidance under U.S. GAAP. The core principle of ASU No. 2014-09 is to recognize revenues when promised goods or services are transferred to customers in an amount that reflects the consideration to which an entity expects to be entitled for those goods or services. ASU No. 2014-09 defines a five step process to achieve this core principle and, in doing so, more judgment and estimates may be required under existing U.S. GAAP. The standard is effective for annual periods beginning after December 15, 2016, and interim periods therein, using either of the following transition methods: (i) a full retrospective approach reflecting the application of the standard in each prior reporting period with the option to elect certain practical expedients, or (ii) a retrospective approach with the cumulative effect of initially adopting ASU No. 2014-09 recognized at the date of adoption (which includes additional footnote disclosures). In July 2015, the FASB issued ASU No. 2015-14 which delayed the effective date of ASU No. 2014-09 by one year (effective for annual periods beginning after December 15, 2017). The Company adopted ASU 2014-09 in the first quarter of fiscal 2018 using the modified retrospective method. The adoption of the standard did not have a material impact on our revenue recognition policies, and the Company has concluded that the most significant impact of the standard relates to the incremental disclosures required.

In February 2016, the FASB issued ASU No. 2016-02, Leases, which requires lessees to recognize the following for all leases (with the exception of short-term leases) at the commencement date: (1) a lease liability, which is a lessee’s obligation to make lease payments arising from a lease, measured on a discounted basis; and (2) a right-of-use asset, which is an asset that represents the lessee’s right to use, or control the use of, a specified asset for the lease term. Under ASU No. 2016-02, lessor accounting is largely unchanged. ASU No. 2016-02 is effective for fiscal years beginning after December 15, 2018 with early application permitted. In February 2018, FASB issued ASU 2018-01, Leases (Topic 842): Land Easement Practical Expedient for Transition to Topic 842. The amendment clarifies that land easements are within the scope of the new leases standard (ASC 842) and introduces a new transition practical expedient allowing a company to not assess whether existing and expired land easements that were not previously accounted for as leases under current US GAAP (ASC 840) are or contain leases under ASC 842.

F-8

In July 2018, FASB issued ASU 2018-10, Codification Improvements to Topic 842, Leases. The amendment provides improvements that clarify specific aspects of the guidance in ASU 2016-02. In August 2018, FASB issued ASU 2018-11, Leases (Topic 842): Targeted Improvements. The amendment provides entities with an additional (and optional) transition method to adopt the new leases standard and provides lessors with a practical expedient, by class of underlying asset, to not separate non-lease components from the associated lease component and, instead, to account for those components as a single component if certain criteria are met. To date, certain personnel have attended technical training concerning this new standard and management is currently reviewing our various leases to identify those affected. The Company is also continuing to evaluate transition considerations such as whether to elect practical expedients, use of hindsight, and comparative reporting periods.

NOTE 3. CONCENTRATIONS, SIGNIFICANT CUSTOMERS, COMMITMENTS AND CONTINGENCIES

At September 30, 2018 and 2017 and for each of the nine months then ended, the Company’s revenues and receivables were comprised of the following customer concentrations:

Nine Months Ended September 30, 2018 | Nine Months Ended September 30, 2017 | ||||||

% of Revenues | % of Receivables | % of Revenues | % of Receivables | ||||

Customer 1 | 37% | 37% | 9% | 23% | |||

Customer 2 | —% | —% | 19% | —% | |||

Customer 3 | 8% | 3% | 13% | 3% | |||

Customer 4 | 8% | 5% | 10% | 7% | |||

At September 30, 2018 and 2017 and for each of the nine months then ended, the Company's segment revenues were comprised of the following customer concentrations:

% of Revenue by Segment | % Revenue by Segment | ||||||||||

Nine Months Ended September 30, 2018 | Nine Months Ended September 30, 2017 | ||||||||||

Black Oil | Refining | Recovery | Black Oil | Refining | Recovery | ||||||

Customer 1 | 100% | —% | —% | 100% | —% | —% | |||||

Customer 2 | —% | —% | —% | 100% | —% | —% | |||||

Customer 3 | 100% | —% | —% | 100% | —% | —% | |||||

Customer 4 | —% | 100% | —% | —% | 100% | —% | |||||

The Company had no vendors that represented 10% of total purchases or payables for the three and nine months ended September 30, 2018 and 2017.

The Company’s revenue, profitability and future rate of growth are substantially dependent on prevailing prices for petroleum-based products. Historically, the energy markets have been very volatile, and there can be no assurance that these prices will not be subject to wide fluctuations in the future. A substantial or extended decline in such prices could have a material adverse effect on the Company’s financial position, results of operations, cash flows, access to capital, and the quantities of petroleum-based products that the Company can economically produce.

Business commitment:

On June 5, 2016, Vertex Energy and Penthol C.V. (“Penthol”) of the Netherlands aka Penthol LLC (a Penthol subsidiary in the United States) reached an agreement for Vertex Energy to act as Penthol’s exclusive agent to provide marketing, sales, and logistical duties of Group III base oil from the United Arab Emirates to the United States. The start-up date was July 25, 2016, with a 5 year term through 2021 and the product ships via truck, rail and barge.

F-9

Litigation:

The Company, in its normal course of business, is involved in various claims and legal action. In the opinion of management, the outcome of these claims and actions will not have a material adverse impact upon the financial position of the Company. We are currently party to the following material litigation proceedings:

Vertex Refining LA, LLC ("Vertex Refining LA"), the wholly-owned subsidiary of Vertex Operating, LLC, our wholly-owned subsidiary ("Vertex Operating") was named as a defendant, along with numerous other parties, in five lawsuits filed on or about February 12, 2016, in the Second Parish Court for the Parish of Jefferson, State of Louisiana, Case No. 121749, by Russell Doucet et. al., Case No. 121750, by Kendra Cannon et. al., Case No. 121751, by Lashawn Jones et. al., Case No. 121752, by Joan Strauss et. al. and Case No. 121753, by Donna Allen et. al. The suits relate to alleged noxious and harmful emissions from our facility located in Marrero, Louisiana. The suits seek damages for physical and emotional injuries, pain and suffering, medical expenses and deprivation of the use and enjoyment of plaintiffs’ homes. We intend to vigorously defend ourselves and oppose the relief sought in the complaints, provided that at this stage of the litigation, the Company has no basis for determining whether there is any likelihood of material loss associated with the claims and/or the potential and/or the outcome of the litigation.

E-Source Holdings, LLC ("E-Source"), the wholly-owned subsidiary of Vertex Operating, was named as a defendant (along with Motiva Enterprises, LLC, ("Motiva")) in a lawsuit filed in the Sixtieth (60th) Judicial District, Jefferson County, Texas, on April 22, 2015. Pursuant to the lawsuit, Whole Environmental, Inc. ("Whole"), made certain allegations against E-Source and Motiva. In July 2018, the parties entered into a confidential settlement agreement and settled all previously pending claims. The settlement did not have a material impact on the consolidated financial statements.

NOTE 4. REVENUES

Revenue Recognition

We account for a contract when it has approval and commitment from both parties, the rights of the parties are identified, payment terms are identified, the contract has commercial substance and collectability of consideration is probable. Revenue is recognized when our performance obligations under the terms of a contract with our customers are satisfied. Recognition occurs when the Company transfers control by completing the specified services at the point in time the customer benefits from the services performed or once our products are delivered. Revenue is measured as the amount of consideration we expect to receive in exchange for completing our performance obligations. Sales tax and other taxes we collect with revenue-producing activities are excluded from revenue. In the case of contracts with multiple performance obligations, the Company allocates the transaction price to each performance obligation based on the relative stand-alone selling prices of the various goods and/or services encompassed by the contract. We do not have any material significant payment terms, as payment is generally due within 30 days after the performance obligation has been satisfactorily completed. The Company has elected the practical expedient to recognize the incremental costs of obtaining a contract as an expense when incurred if the amortization period of the asset that we otherwise would have recognized is one year or less. In applying the guidance in Topic 606, there were no judgments or estimates made that the Company deems significant.

For time to time, our fuel oil customers in our black oil segment may request that we store product which they purchase from us in our facilities. We recognize revenues for these “bill and hold” sales once the following criteria have been met: (1) there is a substantive reason for the arrangement, (2) the product is segregated and identified as the customer's asset, (3) the product is ready for delivery to the customer, and (4) we cannot use the product or direct it to another customer.

Disaggregation of Revenue

The following table presents our revenues disaggregated by revenue source:

F-10

Three Months Ended September 30, 2018 | |||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | ||||||||||||

Primary Geographical Markets | |||||||||||||||

Northern United States | $ | 12,361,348 | $ | — | $ | — | $ | 12,361,348 | |||||||

Southern United States | 28,038,716 | 7,313,630 | 2,919,254 | 38,271,600 | |||||||||||

$ | 40,400,064 | $ | 7,313,630 | $ | 2,919,254 | $ | 50,632,948 | ||||||||

Sources of Revenue | |||||||||||||||

Petroleum products | $ | 40,400,064 | $ | 7,313,630 | $ | 547,184 | $ | 48,260,878 | |||||||

Metals | — | — | 2,372,070 | 2,372,070 | |||||||||||

Total revenues | $ | 40,400,064 | $ | 7,313,630 | $ | 2,919,254 | $ | 50,632,948 | |||||||

Nine Months Ended September 30, 2018 | |||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | ||||||||||||

Primary Geographical Markets | |||||||||||||||

Northern United States | $ | 31,314,405 | $ | — | $ | — | $ | 31,314,405 | |||||||

Southern United States | 79,792,036 | 17,381,741 | 10,430,731 | 107,604,508 | |||||||||||

$ | 111,106,441 | $ | 17,381,741 | $ | 10,430,731 | $ | 138,918,913 | ||||||||

Sources of Revenue | |||||||||||||||

Petroleum products | $ | 111,106,441 | $ | 17,381,741 | $ | 1,607,596 | $ | 130,095,778 | |||||||

Metals | — | — | 8,823,135 | 8,823,135 | |||||||||||

Total revenues | $ | 111,106,441 | $ | 17,381,741 | $ | 10,430,731 | $ | 138,918,913 | |||||||

Three Months Ended September 30, 2017 | |||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | ||||||||||||

Primary Geographical Markets | |||||||||||||||

Northern United States | $ | 7,770,262 | $ | — | $ | — | $ | 7,770,262 | |||||||

Southern United States | 17,588,055 | 4,856,520 | 2,255,614 | 24,700,189 | |||||||||||

$ | 25,358,317 | $ | 4,856,520 | $ | 2,255,614 | $ | 32,470,451 | ||||||||

Sources of Revenue | |||||||||||||||

Petroleum products | $ | 25,358,317 | $ | 4,856,520 | $ | 284,526 | $ | 30,499,363 | |||||||

Metals | — | — | 1,971,088 | 1,971,088 | |||||||||||

Total revenues | $ | 25,358,317 | $ | 4,856,520 | $ | 2,255,614 | $ | 32,470,451 | |||||||

F-11

Nine Months Ended September 30, 2017 | |||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | ||||||||||||

Primary Geographical Markets | |||||||||||||||

Northern United States | $ | 22,305,861 | $ | — | $ | — | $ | 22,305,861 | |||||||

Southern United States | 55,240,941 | 15,436,919 | 11,170,123 | 81,847,983 | |||||||||||

$ | 77,546,802 | $ | 15,436,919 | $ | 11,170,123 | $ | 104,153,844 | ||||||||

Sources of Revenue | |||||||||||||||

Petroleum products | $ | 77,546,802 | $ | 15,436,919 | $ | 6,389,229 | $ | 99,372,950 | |||||||

Metals | — | — | 4,780,894 | 4,780,894 | |||||||||||

Total revenues | $ | 77,546,802 | $ | 15,436,919 | $ | 11,170,123 | $ | 104,153,844 | |||||||

Petroleum products- We derive a majority of our revenues from the sale of recovered/re-refined petroleum products, which include Base Oil, VGO (Vacuum Gas Oil), Pygas, Gasoline, Cutterstock and Fuel Oils.

Metals- Consist of recoverable ferrous and non-ferrous recyclable metals from manufacturing and consumption. Scrap metal can be recovered from pipes, barges, boats, building supplies, surplus equipment, tanks, and other items consisting of metal composition. These materials are segregated, processed, cut-up and sent back to a steel mill for re-purposing.

NOTE 5. ACCOUNTS RECEIVABLE

Accounts receivable, net, consists of the following at September 30, 2018 and December 31, 2017:

September 30, 2018 | December 31, 2017 | ||||||

Accounts receivable trade | $ | 15,672,859 | $ | 12,925,059 | |||

Allowance for doubtful accounts | (1,292,595 | ) | (1,636,068 | ) | |||

Accounts receivable trade, net | $ | 14,380,264 | $ | 11,288,991 | |||

Accounts receivable trade represents amounts due from customers. Accounts receivable trade are recorded at invoiced amounts, net of reserves and allowances and do not bear interest. The Company uses its best estimate to determine the required allowance for doubtful accounts based on a variety of factors, including the length of time receivables are past due, economic trends and conditions affecting its customer base, significant one-time events and historical write-off experience. Specific provisions are recorded for individual receivables when we become aware of a customer’s inability to meet its financial obligations. The Company reviews the adequacy of its reserves and allowances quarterly.

Receivable balances greater than 30 days past due are individually reviewed for collectability and if deemed uncollectible, are charged off against the allowance accounts after all means of collection have been exhausted and the potential for recovery is considered remote. The Company does not have any significant off balance sheet credit exposure related to its customers.

NOTE 6. LINE OF CREDIT AND LONG-TERM DEBT

F-12

Credit and Guaranty Agreement and Revolving Credit Facility with Encina Business Credit, LLC

Effective February 1, 2017, we, Vertex Operating, and substantially all of our other operating subsidiaries, other than E-Source Holdings, LLC ("E-Source"), entered into a Credit Agreement (the “EBC Credit Agreement”) with Encina Business Credit, LLC as agent (the “Agent” or “EBC”) and Encina Business Credit SPV, LLC and CrowdOut Capital LLC as lenders thereunder (the “EBC Lenders”). Pursuant to the EBC Credit Agreement, and the terms thereof, the EBC Lenders agreed to loan us up to $20 million, provided that the amount outstanding under the EBC Credit Agreement at any time cannot exceed 50% of the value of the operating plant facilities and related machinery and equipment owned by us (not including E-Source).

Amounts borrowed under the EBC Credit Agreement bear interest at 12%, 13% or 14% per annum, based on the ratio of (a) (i) consolidated EBITDA for such applicable period minus (ii) capital expenditures made during such period, minus (iii) the aggregate amount of income taxes paid in cash during such period (but not less than zero) to (b) the sum of (i) debt service charges plus (ii) the aggregate amount of all dividend or other distributions paid on capital stock in cash for the most recently completed 12 month period (which ratio falls into one of the three following tiers: less than 1 to 1; from 1 to 1 to less than 1.45 to 1; or equal to or greater than 1.45 to 1, which together with the value below, determines which interest rate is applicable) and average availability under the Revolving Credit Agreement (defined below) (which falls into two tiers: less than $2.5 million and greater than or equal to $2.5 million, which together with the calculation above, determines which interest rate is applicable), as described in greater detail in the EBC Credit Agreement (increasing by 2% per annum upon the occurrence of an event of default). Interest on amounts borrowed under the EBC Credit Agreement is payable by us in arrears, on the first business day of each month, beginning on the first business day of the first full month following the closing, together with required $75,000 monthly principal repayments. We also have the right to make voluntary repayments of the amount owed under the EBC Credit Agreement in amounts equal to or greater than $100,000, from time to time. The interest rate is 12% at September 30, 2018.

The EBC Credit Agreement terminates on February 1, 2020, on which date we are required to repay the outstanding balance owed thereunder and any accrued and unpaid interest thereon.

The amounts borrowed under the EBC Credit Agreement are guaranteed by us and our subsidiaries, other than E-Source, pursuant to a Guaranty and Security Agreement (the “Guaranty and Security Agreement”), whereby we also pledged substantially all of our assets and all of the securities of our subsidiaries (other than E-Source) as collateral securing the amount due under the terms of the EBC Credit Agreement. We also provided EBC mortgages on our Marrero, Louisiana, and Columbus, Ohio facilities to secure the repayment of outstanding amounts and agreed to provide mortgages on certain other real property to be delivered post-closing. The post-closing mortgage properties provided were in Baytown, Pflugerville and Corpus Christi, Texas.

The EBC Credit Agreement contains customary representations, warranties and requirements for the Company to indemnify the EBC Lenders and their affiliates. The EBC Credit Agreement also includes various covenants (positive and negative) binding upon the Company, including, prohibiting us from undertaking acquisitions or dispositions unless they meet the criteria set forth in the EBC Credit Agreement, not incurring any capital expenditures in an amount exceeding $3 million in any fiscal year that the EBC Credit Agreement is in place, and requiring us to maintain at least $2.5 million of borrowing availability under the Revolving Credit Agreement (defined below) in any 30 day period.

The EBC Credit Agreement includes customary events of default for facilities of a similar nature and size as the EBC Credit Agreement, including if an event of default occurs under any agreement evidencing $500,000 or more of indebtedness of the Company; we fail to make any payment when due under any material agreement; subject to certain exceptions, any judgment is entered against the Company in an amount exceeding $500,000; and also provides that an event of default occurs if a change in control of the Company occurs, which includes if (a) Benjamin P. Cowart, the Company’s Chief Executive Officer, Chairman of the Board and largest shareholder and Chris Carlson, the Chief Financial Officer of the Company, cease to own and control legally and beneficially, collectively, either directly or indirectly, equity securities in Vertex Energy, Inc., representing more than 15% of the combined voting power of all securities entitled to vote for members of the board of directors or equivalent on a fully-diluted basis, (b) the acquisition of ownership, directly or indirectly, beneficially or of record, by any person or group of securities representing more than 30% of the aggregate ordinary voting power represented by the issued and outstanding securities of Vertex Energy, Inc., or (c) during any period of 12 consecutive months, a majority of the members of the board of directors of the Company cease to be composed of individuals (i) who were members of that board or equivalent governing body on the first day of such period, (ii) whose election or nomination to that board or equivalent governing body was approved by individuals referred to in clause (i) above constituting at the time of such election or nomination at least a majority of that

F-13

board or equivalent governing body or (iii) whose election or nomination to that board or other equivalent governing body was approved by individuals referred to in clauses (i) and (ii) above constituting at the time of such election or nomination at least a majority of that board or equivalent governing body (collectively “Events of Default”). An event of default under the Revolving Credit Agreement (defined below), is also an event of default under the EBC Credit Agreement.

Effective February 1, 2017, we, Vertex Operating and substantially all of our operating subsidiaries, other than E-Source, entered into a Revolving Credit Agreement (the “Revolving Credit Agreement” and together with the EBC Credit Agreement, the "Credit Agreements") with Encina Business Credit SPV, LLC as lender (“Encina”) and EBC as the administrative agent. Pursuant to the Revolving Credit Agreement, and the terms thereof, Encina agreed to loan us, on a revolving basis, up to $10 million, subject to the terms of the Revolving Credit Agreement and certain lending ratios set forth therein, which provide that the amount outstanding thereunder cannot exceed an amount equal to the total of (a) the lesser of (A) the value (as calculated in the Revolving Credit Agreement) of our inventory which are raw materials or finished goods that are merchantable and readily saleable to the public in the ordinary course of our business (“EBC Eligible Inventory”), net of certain inventory reserves, multiplied by 85% of the appraised value of EBC Eligible Inventory, or (B) the value (as calculated in the Revolving Credit Agreement) of EBC Eligible Inventory, net of certain inventory reserves, multiplied by 65%, subject to a ceiling of $4 million, plus (b) the face amount of certain accounts receivables (net of certain reserves applicable thereto) multiplied by 85% (subject to adjustment as provided in the Revolving Credit Agreement); minus (c) the then-current amount of certain reserves that the agent may determine necessary for the Company to maintain. At September 30, 2018, the maximum amount available to be borrowed was $4,000,267, based on the above borrowing base calculation.

Amounts borrowed under the Revolving Credit Agreement bear interest, subject to the terms of the Revolving Credit Agreement, at the one month LIBOR interest rate then in effect, subject to a floor of 0.25% (which interest rate is currently approximately 2.10% per annum), plus an additional 6.50% per annum (increasing by 2% per annum upon the occurrence of an event of default), provided that under certain circumstances amounts borrowed bear interest at the higher of (a) the “prime rate”; (b) the Federal Funds Rate, plus 0.50%; and (c) the LIBOR Rate for a one month interest period, plus 1.00%. Interest on amounts borrowed under the Revolving Credit Agreement is payable by us in arrears, on the first business day of each month, beginning on the first business day of the first full month following the closing.

The Revolving Credit Agreement terminates on February 1, 2020, on which date we are required to repay the outstanding balance owed thereunder and any accrued and unpaid interest thereon. Borrowings under a revolving credit agreement that contain a subjective acceleration clause and also require a borrower to maintain a lockbox with the lender (whereby lockbox receipts may be applied to reduce the amount outstanding under the revolving credit agreement) are considered short-term obligations. As a result, the debt is classified as a current liability at September 30, 2018.

The amounts borrowed under the Revolving Credit Agreement are guaranteed by us and our subsidiaries, other than E-Source, pursuant to a separate Guaranty and Security Agreement, similar to the EBC Credit Agreement, described in greater detail above. We also provided Encina mortgages on our Marrero, Louisiana, and Columbus, Ohio facilities to secure the repayment of outstanding amounts.

The Revolving Credit Agreement contains customary representations, warranties and requirements for the Company to indemnify Encina and its affiliates. The Revolving Credit Agreement also includes various covenants (positive and negative) binding upon the Company, including, prohibiting us from undertaking acquisitions or dispositions unless they meet the criteria set forth in the Revolving Credit Agreement, not incurring any capital expenditures in amount exceeding $3 million in any fiscal year that the Revolving Credit Agreement is in place, and requiring us to maintain at least $2.5 million of borrowing availability under the Revolving Credit Agreement in any 30 day period.

The Revolving Credit Agreement includes customary events of default for facilities of a similar nature and size as the Revolving Credit Agreement, including the same Events of Default as are described above under the description of the EBC Credit Agreement.

The principal balances of the EBC Credit Agreement and the Revolving Credit Agreement as of September 30, 2018 are $15,575,000 and $5,999,733, respectively.

F-14

Texas Citizens Bank Loan Agreement

The Company had notes payable to Texas Citizens Bank bearing interest at 5.50% per annum, maturing on January 7, 2020. The balances of the notes payable was $834,283 at December 31, 2017. The note was paid off during the quarter ended September 30, 2018.

Insurance Premiums

The Company financed insurance premiums through various financial institutions bearing interest rates from 4.00% to 4.52%. All such premium finance agreements have maturities of less than one year and have a balance of $1,841,083 at September 30, 2018 and $803,392 at December 31, 2017.

Capital Leases

On March 1, 2018, the Company obtained one capital lease. Payments are $908 per month for three years and the amount of the capital lease obligation has been reduced to $24,829 at September 30, 2018.

On May 29, 2018, the Company obtained one capital lease. Payments are $26,305 per quarter for four years and the amount of the capital lease obligation has been reduced to $390,609 at September 30, 2018.

The Company's outstanding debt facilities as of September 30, 2018 and December 31, 2017 are summarized as follows:

Creditor | Loan Type | Origination Date | Maturity Date | Loan Amount | Balance on September 30, 2018 | Balance on December 31, 2017 | ||||||||||

Encina Business Credit, LLC | Term Loan | February 1, 2017 | February 1, 2020 | $ | 20,000,000 | $ | 15,575,000 | $ | 14,750,000 | |||||||

Encina Business Credit SPV, LLC | Revolving Note | February 1, 2017 | February 1, 2020 | $ | 10,000,000 | 5,999,733 | 4,591,527 | |||||||||

Tetra Capital Lease | Capital Lease | May, 2018 | May, 2022 | $ | 419,690 | 390,609 | — | |||||||||

Well Fargo Equipment Lease | Capital Lease | March, 2018 | March, 2021 | $ | 30,408 | 24,829 | — | |||||||||

Texas Citizens Bank | Term Note | January, 2015 | January, 2020 | $ | 2,045,500 | — | 834,283 | |||||||||

Various institutions | Insurance premiums financed | Various | < 1 year | $ | 2,902,428 | 1,841,083 | 803,392 | |||||||||

Total | 23,831,254 | 20,979,202 | ||||||||||||||

Deferred finance cost, net | (765,210 | ) | (1,239,570 | ) | ||||||||||||

Total, net of deferred finance costs | $ | 23,066,044 | $ | 19,739,632 | ||||||||||||

F-15

Future contractual maturities of notes payable as of September 30, 2018 are summarized as follows:

Creditor | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Thereafter | |||||||||||||||||

Encina Business Credit, LLC | $ | 900,000 | $ | 14,675,000 | $ | — | $ | — | $ | — | $ | — | |||||||||||

Encina Business Credit SPV, LLC | 5,999,733 | — | — | — | — | — | |||||||||||||||||

Tetra Capital Lease | 82,969 | 88,743 | 94,919 | 123,978 | — | — | |||||||||||||||||

Well Fargo Equipment Lease | 9,931 | 10,413 | 4,485 | — | — | — | |||||||||||||||||

Various institutions | 1,841,083 | — | — | — | — | — | |||||||||||||||||

Totals | 8,833,716 | 14,774,156 | 99,404 | 123,978 | — | — | |||||||||||||||||

Deferred finance costs, net | (573,912 | ) | (191,298 | ) | — | — | — | — | |||||||||||||||

Totals, net of deferred finance costs | $ | 8,259,804 | $ | 14,582,858 | $ | 99,404 | $ | 123,978 | $ | — | $ | — | |||||||||||

NOTE 7. EARNINGS PER SHARE

Basic earnings per share includes no dilution and is computed by dividing income available to common shareholders by the weighted average number of common shares outstanding for the periods presented. Diluted earnings per share reflects the potential dilution of securities that could share in the earnings of an entity, such as convertible preferred stock, stock options, warrants or convertible securities. Due to their anti-dilutive effect, the calculation of diluted earnings per share for the three months ended September 30, 2018 and 2017 excludes: 1) options to purchase 3,438,837 and 3,030,249 shares, respectively, of common stock, 2) warrants to purchase 7,353,056 and 7,353,061 shares, respectively, of common stock, 3) Series B Preferred Stock which is convertible into 3,551,549 and 3,376,938 shares, respectively, of common stock, and 4) Series B1 Preferred Stock which is convertible into 11,074,331 and 12,862,572 shares, respectively, of common stock, 5) Series A Preferred Stock which is convertible into 419,859 and 456,608 shares, respectively, of common stock, and 6) Series C Preferred Stock, which was convertible into 3,156,800 shares of common stock as of September 30, 2017. Due to their anti-dilutive effect, the calculation of diluted earnings per share for the nine months ended September 30, 2018 and 2017 excludes: 1) options to purchase 3,438,837 and 3,030,249 shares, respectively, of common stock, 2) warrants to purchase 7,353,056 and 7,353,061 shares, respectively, of common stock, 3) Series B Preferred Stock which is convertible into 3,499,059 and 3,376,938 shares, respectively, of common stock, 4) Series B1 Preferred Stock which is convertible into 13,105,989 and 12,862,572 shares, respectively, of common stock, 5) Series A Preferred Stock which is convertible into 419,859 and 456,608 shares, respectively, of common stock, and 6) Series C Preferred Stock, which was convertible into 3,156,800 shares of common stock as of September 30, 2017.

F-16

The following is a reconciliation of the numerator and denominator for basic and diluted earnings per share for the three and nine months ended September 30, 2018 and 2017:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Basic Earnings per Share | |||||||||||||||

Numerator: | |||||||||||||||

Net loss available to common shareholders | $ | (4,635,372 | ) | $ | (3,829,125 | ) | $ | (6,652,027 | ) | $ | (10,572,545 | ) | |||

Denominator: | |||||||||||||||

Weighted-average shares outstanding | 35,144,113 | 32,655,135 | 33,843,721 | 32,651,961 | |||||||||||

Basic earnings per share | $ | (0.13 | ) | $ | (0.12 | ) | $ | (0.20 | ) | $ | (0.32 | ) | |||

Diluted Earnings per Share | |||||||||||||||

Numerator: | |||||||||||||||

Net loss available to common shareholders | $ | (4,635,372 | ) | $ | (3,829,125 | ) | $ | (6,652,027 | ) | $ | (10,572,545 | ) | |||

Denominator: | |||||||||||||||

Weighted-average shares outstanding | 35,144,113 | 32,655,135 | 33,843,721 | 32,651,961 | |||||||||||

Effect of dilutive securities | |||||||||||||||

Stock options and warrants | — | — | — | — | |||||||||||

Preferred Stock A | — | — | — | — | |||||||||||

Diluted weighted-average shares outstanding | 35,144,113 | 32,655,135 | 33,843,721 | 32,651,961 | |||||||||||

Diluted earnings (loss) per share | $ | (0.13 | ) | $ | (0.12 | ) | $ | (0.20 | ) | $ | (0.32 | ) | |||

F-17

NOTE 8. COMMON STOCK

The total number of authorized shares of the Company’s common stock is 750,000,000 shares, $0.001 par value per share. As of September 30, 2018, there were 38,840,890 common shares issued and outstanding.

During the nine months ended September 30, 2018, the Company issued 6,182,473 shares of common stock in connection with the conversion of Series B1, Series B, Series C, and Series A Convertible Preferred Stock, pursuant to the terms of such securities. In addition, the Company issued 241 shares of common stock in connection with the cashless exercise of options.

F-18

NOTE 9. PREFERRED STOCK AND DETACHABLE WARRANTS

The total number of authorized shares of the Company’s preferred stock is 50,000,000 shares, $0.001 par value per share. The total number of designated shares of the Company’s Series A Convertible Preferred Stock is 5,000,000 (“Series A Preferred”). The total number of designated shares of the Company’s Series B Convertible Preferred Stock is 10,000,000. The total number of designated shares of the Company’s Series B1 Convertible Preferred Stock is 17,000,000. The number of designated shares of the Company's Series C Convertible Preferred Stock is 44,000. As of September 30, 2018 and December 31, 2017, there were 419,859 shares and 453,567 shares of Series A Preferred Stock issued and outstanding, respectively. As of September 30, 2018 and December 31, 2017, there were 3,551,549 and 3,427,597 shares of Series B Preferred Stock issued and outstanding, respectively. As of September 30, 2018 and December 31, 2017, there were 11,074,331 and 13,151,989 shares of Series B1 Preferred Stock issued and outstanding, respectively. As of September 30, 2018, there were no shares of Series C Preferred Stock issued and outstanding. As of December 31, 2017, there were 31,568 shares of Series C Preferred Stock issued and outstanding.

Series B Preferred Stock and Temporary Equity

Dividends on our Series B Preferred Stock accrue at an annual rate of 6% of the original issue price of the preferred stock ($3.10 per share), subject to increase under certain circumstances, and are payable on a quarterly basis. The dividends are payable by the Company, at the Company’s election, in registered common stock of the Company (if available), cash or in-kind in Series B Preferred Stock at $3.10 per share.

The Company has the option to redeem the outstanding shares of Series B Preferred Stock at $3.10 per share, plus any accrued and unpaid dividends on such Series B Preferred Stock redeemed, at any time beginning on June 24, 2017, and the Company is required to redeem the Series B Preferred Stock at $3.10 per share, plus any accrued and unpaid dividends, on June 24, 2020. Notwithstanding either of the foregoing, the Series B Preferred Stock may not be redeemed unless and until amounts outstanding under the Company’s senior credit facility have been paid in full.

The Warrants issued in connection with the Series B Preferred Stock (Series B Warrants) were initially valued using the Dynamic Black Scholes Merton formula pricing model that computes the impact of share dilution upon the exercise of the warrant shares at $7,028,067. In accordance with ASC 815-40-25 and ASC 815-10-15 Derivatives and Hedging and ASC 480-10-25 Liabilities-Distinguishing Liabilities from Equity, the convertible preferred shares are accounted for net outside of stockholders’ equity with the Warrants accounted for as liabilities at their fair value. The initial value assigned to the derivative warrant liability was recognized through a corresponding discount to the Series B Preferred Stock. The value of the derivative warrant liability will be re-measured at each reporting period with changes in fair value recorded in earnings. The initial valuation of the warrants resulted in a beneficial conversion feature on the convertible preferred stock of $5,737,796. The amounts related to the warrant discount and beneficial conversion feature will be accreted over the term as a deemed dividend. Fees in the amount of $1.4 million relating to the stock placement were netted against proceeds.

The following table represents the activity related to the Series B Preferred Stock, classified as Temporary Equity on the accompanying Consolidated Balance Sheet, during the nine months ended September 30, 2018 and 2017:

2018 | 2017 | ||||||

Balance at beginning of period | $ | 7,190,467 | $ | 5,676,467 | |||

Less: conversions of shares to common | (62,962 | ) | — | ||||

Plus: discount accretion | 815,373 | 643,458 | |||||

Plus: dividends in kind | 489,282 | 492,599 | |||||

Balance at end of period | $ | 8,432,160 | $ | 6,812,524 | |||

The Series B Warrants and Series B1 Warrants were revalued at September 30, 2018 and December 31, 2017 using the Dynamic Black Scholes model that computes the impact of a possible change in control transaction upon the exercise of the warrant shares at approximately $4,370,379 and $2,245,408, respectively. At September 30, 2018, the Series B Warrants and Series B1 Warrants were valued at approximately $1,357,079 and $3,013,300, respectively. The Dynamic Black Scholes Merton inputs used were: expected dividend rate of 0%, expected volatility of 76%-100%, risk free interest rate of 2.85% (Series B Warrants) and 2.95% (Series B1 Warrants), and expected term of 2.22 years (Series B Warrants) and 3.61 years (Series B1 Warrants).

At September 30, 2018 and December 31, 2017, a total of $165,162 and $139,186 of dividends were accrued on our outstanding Series B Preferred Stock, respectively. During the three months ended September 30, 2018 and 2017, we paid dividends in-kind in additional shares of Series B Preferred Stock of $162,719 and $139,186, respectively.

F-19

Series B1 Preferred Stock and Temporary Equity

Dividends on our Series B1 Preferred Stock accrue at an annual rate of 6% of the original issue price of the preferred stock ($1.56 per share), subject to increases if certain EBITDA thresholds are not met, and are payable on a quarterly basis. The dividends are payable by the Company, at the Company’s election, in registered common stock of the Company (if available), cash, or in-kind in Series B1 Preferred Stock at $1.56 per share. At March 31, 2018, and June 30, 2018, the EBITDA thresholds were not met resulting in a 9% dividend rate. At September 30, 2018, the EBITDA thresholds expired and the dividend rate of the Series B1 Preferred Stock returned to 6%.

The Company has the option to redeem the outstanding shares of Series B1 Preferred Stock at $1.72 per share, plus any accrued and unpaid dividends on such Series B1 Preferred Stock redeemed, at any time beginning on June 24, 2017, and the Company is required to redeem the Series B1 Preferred Stock at $1.56 per share, plus any accrued and unpaid dividends, on June 24, 2020. Notwithstanding either of the foregoing, the Series B1 Preferred Stock may not be redeemed unless and until amounts outstanding under the Company’s senior credit facility have been paid in full.

The Warrants issued in connection with the Series B1 Preferred Stock offering (Series B1 Warrants) were initially valued using the Dynamic Black Scholes Merton formula pricing model that computes the impact of share dilution upon the exercise of the May 2016 Warrant shares at $2,867,264. In accordance with ASC 815-40-25 and ASC 815-10-15 Derivatives and Hedging and ASC 480-10-25 Liabilities-Distinguishing Liabilities from Equity, the convertible Series B1 Preferred Stock shares are accounted for net outside of stockholders’ equity at $14,387,804 with the May 2016 Warrants accounted for as liabilities at their fair value. The initial value assigned to the derivative warrant liability was recognized through a corresponding discount to the Series B1 Preferred Stock. The value of the derivative warrant liability will be re-measured at each reporting period with changes in fair value recorded in earnings. This initial valuation of the warrants resulted in a beneficial conversion feature on the convertible preferred stock of $2,371,106. The amounts related to the warrant discount and beneficial conversion feature will be accreted over the term as a deemed dividend. Fees in the amount of $0.6 million relating to the stock placement were netted against proceeds.

The following table represents the activity related to the Series B1 Preferred Stock, classified as Temporary Equity on the accompanying Consolidated Balance Sheet, for the nine months ended September 30, 2018, and 2017:

2018 | 2017 | ||||||

Balance at beginning of period | $ | 15,769,478 | $ | 13,927,788 | |||

Less: conversions of shares to common | (3,746,917 | ) | (86,467 | ) | |||

Plus: dividends-in-kind | 1,736,240 | 848,082 | |||||

Plus: discount accretion | 629,003 | 591,347 | |||||

Balance at end of period | $ | 14,387,804 | $ | 15,280,750 | |||

As of September 30, 2018 and December 31, 2017, respectively, a total of $314,149 and $276,144 of dividends were accrued on our outstanding Series B1 Preferred Stock. During the three months ended September 30, 2018 and 2017, we paid dividends in-kind in additional shares of Series B Preferred Stock of $460,035 and $276,144, respectively.

The following is an analysis of changes in the derivative liability for the nine months ended September 30:

Level Three Roll-Forward | |||||||

2018 | 2017 | ||||||

Balance at beginning of period | $ | 2,245,408 | $ | 4,365,992 | |||

Change in valuation of warrants | 2,124,971 | (2,676,902 | ) | ||||

Balance at end of period | $ | 4,370,379 | $ | 1,689,090 | |||

F-20

NOTE 10. SEGMENT REPORTING

The Company’s reportable segments include the Black Oil, Refining & Marketing and Recovery divisions. Segment information for the three and nine months ended September 30, 2018 and 2017 is as follows:

THREE MONTHS ENDED SEPTEMBER 30, 2018 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 40,400,064 | $ | 7,313,630 | $ | 2,919,254 | $ | 50,632,948 | ||||||||

Income (loss) from operations | $ | 1,769,439 | $ | (418,482 | ) | $ | (776,874 | ) | $ | 574,083 | ||||||

THREE MONTHS ENDED SEPTEMBER 30, 2017 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 25,358,317 | $ | 4,856,520 | $ | 2,255,614 | $ | 32,470,451 | ||||||||

Income (loss) from operations | $ | (2,769,027 | ) | $ | (708,175 | ) | $ | (137,390 | ) | $ | (3,614,592 | ) | ||||

NINE MONTHS ENDED SEPTEMBER 30, 2018 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 111,106,441 | $ | 17,381,741 | $ | 10,430,731 | $ | 138,918,913 | ||||||||

Income (loss) from operations | $ | 3,979,619 | $ | (1,119,522 | ) | $ | (278,666 | ) | $ | 2,581,431 | ||||||

NINE MONTHS ENDED SEPTEMBER 30, 2017 | ||||||||||||||||

Black Oil | Refining & Marketing | Recovery | Total | |||||||||||||

Revenues | $ | 77,546,802 | $ | 15,436,919 | $ | 11,170,123 | $ | 104,153,844 | ||||||||

Income (loss) from operations | $ | (6,816,027 | ) | $ | (920,726 | ) | $ | (196,853 | ) | $ | (7,933,606 | ) | ||||

NOTE 11. INCOME TAXES

Our effective tax rate of 0% on pretax income differs from the U.S. federal income tax rate of 21% because of the change in our valuation allowance.

The year to date loss at September 30, 2018 put the Company in an accumulated loss position for the cumulative 12 quarters then ended. For tax reporting purposes, we have net operating losses ("NOLs") of approximately $57.5 million as of September 30, 2018 that are available to reduce future taxable income. In determining the carrying value of our net deferred tax asset, the Company considered all negative and positive evidence. The Company has generated a pre-tax loss of approximately $2.0 million from January 1, 2018 through September 30, 2018.

F-21

NOTE 12. COMMODITY DERIVATIVE INSTRUMENTS

The Company utilizes derivative instruments to manage its exposure to fluctuations in the underlying commodity prices of its inventory. The Company's management sets and implements hedging policies, including volumes, types of instruments and counterparties, to support oil prices at targeted levels and manage its exposure to fluctuating prices.

The Company’s derivative instruments consist of swap and futures arrangements for oil. In a commodity swap agreement, if the agreed-upon published third-party index price (“index price”) is lower than the swap fixed price, the Company receives the difference between the index price and the swap fixed price. If the index price is higher than the swap fixed price, the Company pays the difference. For futures arrangements, the Company receives the difference positive or negative between an agreed-upon strike price and the market price.

The mark-to-market effects of these contracts as of September 30, 2018, are summarized in the following table. The Company held no open contracts at December 31, 2017. The notional amount is equal to the total net volumetric derivative position during the period indicated. The fair value of the crude oil swap agreements is based on the difference between the strike price and the New York Mercantile Exchange futures price for the applicable trading months.

Contract Type | Contract Period | Weighted Average Strike Price (Barrels) | Remaining Volume (Barrels) | Fair Value | |||||

Swap | Sep. 2018- Dec. 2018 | $ | 69.93 | 120,000 | $ | 740,200 | |||

Swap | Sep. 2018- Jan. 2019 | $ | 98.79 | 20,000 | $ | (431,894 | ) | ||

Futures | Sep. 2018- Dec. 2018 | $ | 95.43 | 100,000 | $ | (874,440 | ) | ||

Futures | Sep. 2018- Nov. 2018 | $ | 73.25 | 10,000 | $ | (35,400 | ) | ||

The carrying values of the Company's derivatives positions and their locations on the consolidated balance sheets as of September 30, 2018 are presented in the table below.

Balance Sheet Classification | Contract Type | 2018 | ||

Crude oil swaps | $ | 308,306 | ||

Crude oil futures | (909,840 | ) | ||

Derivative commodity liability | $ | (601,534 | ) | |

For the three and nine months ended September 30, 2018, we recognized $647,149 and $1,859,234 loss on commodity derivative contracts on the consolidated statements of operations as part of our costs of revenues, respectively.

NOTE 12. ASSET PURCHASE

On April 30, 2018, the Company entered into and closed an Asset Purchase Agreement (the "APA") with Specialty Environmental Services ("SES") pursuant to which the Company agreed to buy substantially all of SES's customer relations, vehicles, equipment, supplies and tools in Texas for an aggregate purchase price of $269,826. We recognized most of the consideration in tangible and intangible assets as of the purchase date.

F-22

NOTE 13. SUBSEQUENT EVENTS

Issuance of Series B and B1 Preferred Stock Shares In-Kind and Common Stock

We paid the accrued dividends on our Series B Preferred Stock and Series B1 Preferred Stock, which were accrued as of September 30, 2018, in-kind by way of the issuance of 53,278 restricted shares of Series B Preferred Stock pro rata to each of the then holders of our Series B Preferred Stock in October 2018 and the issuance of 166,630 shares of common stock (at a conversion price of $1.55 per share, as calculated as provided in the designation) pro rata to each of the then holders of our Series B1 Preferred Stock, other than those due to an affiliate of Mr. Benjamin P. Cowart, our Chief Executive Officer and Chairman, whose affiliated entity was issued 567 shares of restricted Series B Preferred Stock in lieu of common stock, because of the 9.99% beneficial ownership limitation in the designation in October 2018. If converted in full, the 53,278 shares of Series B Preferred Stock would convert into 53,278 shares of common stock and the 567 shares of Series B1 Preferred Stock would convert into 567 shares of common stock.

Conversion of Series B1 Preferred Stock

On October 4, 2018, a holder of shares of Series B1 Preferred Stock converted 1,000,000 shares of our Series B1 Preferred Stock into 1,000,000 shares of our common stock, pursuant to the terms of such Series B1 Preferred Stock.

F-23

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In some cases, you can identify forward-looking statements by the following words: “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “ongoing,” “plan,” “potential,” “predict,” “project,” “should,” or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words. Forward-looking statements are not a guarantee of future performance or results, and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available at the time the statements are made and involve known and unknown risks, uncertainties and other factors that may cause our results, levels of activity, performance or achievements to be materially different from the information expressed or implied by the forward-looking statements in this Report. These factors include:

• | risks associated with our outstanding credit facilities, including amounts owed, restrictive covenants, security interests thereon and our ability to repay such facilities and amounts due thereon when due; |

• | the level of competition in our industry and our ability to compete; |

• | our ability to respond to changes in our industry; |

• | the loss of key personnel or failure to attract, integrate and retain additional personnel; |

• | our ability to protect our intellectual property and not infringe on others’ intellectual property; |

• | our ability to scale our business; |

• | our ability to maintain supplier relationships and obtain adequate supplies of feedstocks; |

• | our ability to obtain and retain customers; |

• | our ability to produce our products at competitive rates; |

• | our ability to execute our business strategy in a very competitive environment; |

• | trends in, and the market for, the price of oil and gas and alternative energy sources; |

• | our ability to maintain our relationship with KMTEX; |

• | the impact of competitive services and products; |

• | our ability to integrate acquisitions; |

• | our ability to complete future acquisitions; |

• | our ability to maintain insurance; |

• | potential future litigation, judgments and settlements; |

• | rules and regulations making our operations more costly or restrictive; |

• | changes in environmental and other laws and regulations and risks associated with such laws and regulations; |

• | economic downturns both in the United States and globally; |

• | risk of increased regulation of our operations and products; |

• | negative publicity and public opposition to our operations; |

• | disruptions in the infrastructure that we and our partners rely on; |

1

• | an inability to identify attractive acquisition opportunities and successfully negotiate acquisition terms; |

• | our ability to effectively integrate acquired assets, companies, employees or businesses; |

• | liabilities associated with acquired companies, assets or businesses; |

• | interruptions at our facilities; |

• | required earn-out payments and other contingent payments we are required to make; |

• | unexpected changes in our anticipated capital expenditures resulting from unforeseen required maintenance, repairs, or upgrades; |

• | our ability to acquire and construct new facilities; |

• | certain events of default which have occurred under our debt facilities and previously been waived; |

• | prohibitions on borrowing and other covenants of our debt facilities; |

• | our ability to effectively manage our growth; |

• | the lack of capital available on acceptable terms to finance our continued growth; and |

• | other risk factors included under “Risk Factors” in our latest Annual Report on Form 10-K. |