Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - YETI Holdings, Inc. | a2236927zex-23_2.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on October 23, 2018

Registration No. 333-227578

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

YETI Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

3949 (Primary Standard Industrial Classification Code Number) |

45-5297111 (I.R.S. Employer Identification Number) |

7601 Southwest Parkway

Austin, Texas 78735

(512) 394-9384

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Matthew J. Reintjes

President and Chief Executive Officer, Director

7601 Southwest Parkway

Austin, Texas 78735

(512) 394-9384

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||||

Timothy R. Curry Kimberly J. Pustulka Jones Day 901 Lakeside Avenue Cleveland, Ohio 44114 (216) 586-3939 |

Bryan C. Barksdale Senior Vice President, General Counsel and Secretary YETI Holdings, Inc. 7601 Southwest Parkway Austin, Texas 78735 (512) 394-9384 |

Michael Benjamin Latham & Watkins LLP 885 Third Avenue New York, New York 10022 (212) 906-1200 |

||

Approximate date of commencement of proposed sale to the public:

As soon as practicable, after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý |

Smaller reporting company o Emerging growth company ý |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. o

CALCULATION OF REGISTRATION FEE

|

||||||||

| Title of Each Class of Securities to be Registered |

Amount to be registered(1)(2) |

Proposed Maximum Offering Price Per Share |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) |

||||

|---|---|---|---|---|---|---|---|---|

Common Stock, par value $0.01 per share |

23,000,000 | $21.00 | $483,000,000 | $58,540 | ||||

|

||||||||

- (1)

- Estimated

solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended.

- (2)

- Includes

the aggregate offering price of additional shares that the underwriters have the option to purchase. See "Underwriting."

- (3)

- Of this amount $58,540 was previously paid in connection with prior filings of this registration statement.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject To Completion, Dated October 23, 2018

PROSPECTUS

20,000,000 Shares

Common Stock

This is the initial public offering of shares of common stock of YETI Holdings, Inc. We are selling 2,500,000 shares of our common stock and the selling stockholders identified in this prospectus are selling 17,500,000 shares of our common stock. We will not receive any proceeds from the sale of shares of our common stock by the selling stockholders.

We expect the public offering price to be between $19.00 and $21.00 per share. Currently, no public market exists for the shares. We have been approved to list our shares on the New York Stock Exchange under the symbol "YETI."

We are an "emerging growth company" under the federal securities laws and, as such, will be subject to reduced public company reporting requirements. See "Prospectus Summary—Implications of Being an Emerging Growth Company."

After the completion of this offering, Cortec Group Fund V, L.P. and its affiliates will control a majority of the voting power of our common stock with respect to the election of our directors. As a result, we will be a "controlled company" within the meaning of the New York Stock Exchange listing standards. See "Management—Controlled Company Exemption."

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 17 of this prospectus.

|

||||

| |

Per share |

Total |

||

|---|---|---|---|---|

Public offering price |

$ | $ | ||

Underwriting discounts and commissions(1) |

$ | $ | ||

Proceeds, before expenses, to us |

$ | $ | ||

Proceeds, before expenses, to the selling stockholders |

$ | $ | ||

|

||||

- (1)

- See "Underwriting" for additional information regarding total underwriter compensation.

The underwriters may also exercise their option to purchase up to an additional 3,000,000 shares from the selling stockholders, at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2018.

| BofA Merrill Lynch | Morgan Stanley | Jefferies |

| Baird | Piper Jaffray |

| Citigroup | Goldman Sachs & Co. LLC |

| KeyBanc Capital Markets | William Blair | Raymond James | Stifel | Academy Securities |

, 2018

You should rely only on the information contained in this prospectus and in any related free writing prospectus prepared by or on behalf of us and the selling stockholders. Neither we, the selling stockholders, nor the underwriters have authorized anyone to provide you with information different from, or in addition to, the information contained in this prospectus or any related free writing prospectus. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our common stock. Our business, financial condition, results of operations, and prospects may have changed since that date.

For Investors Outside the United States

Neither we, the selling stockholders, nor the underwriters have taken any action that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. Persons outside the United States are required to inform themselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

Trademarks, Trade Names, and Service Marks

We use various trademarks, trade names, and service marks in our business, including, without limitation, YETI®, Tundra®, Hopper®, Hopper Flip®, YETI TANK®, Rambler®, Colster®, Roadie®, BUILT FOR THE WILD®, LOAD-AND-LOCK®, YETI Authorized™, YETI PRESENTS™, YETI Custom Shop™, Panga™, LoadOut™, Camino™, Hondo™, SideKick™, SideKick Dry™, Silo™, YETI ICE™, EasyBreathe™, FlexGrid™, PermaFrost™, T-Rex™, Haul™, NeverFlat™, StrongArm™, Vortex™, SteadySteel™, Hopper BackFlip™, ThickSkin™, DryHaul™, SureStrong™, LipGrip™, No Sweat™,

i

Boomer™, Tocayo™, Lowlands™, TripleGrip™, TripleHaul™, Over-the-Nose™, FatLid™, MagCap™, DoubleHaul™, HydroLok™, and ColdCell™. YETI also uses trade dress for its distinctive product designs. For convenience, we may not include the ® or ™ symbols in this prospectus, but such omission is not meant to and does not indicate that we would not protect our intellectual property rights to the fullest extent allowed by law. Any other trademarks, trade names, or service marks referred to in this registration statement and the prospectus that are not owned by us are the property of their respective owners.

Industry, Market, and Other Data

This prospectus includes estimates, projections, and other information concerning our industry and market data, including data regarding the estimated size of the market, projected growth rates, and perceptions and preferences of consumers. We obtained this data from industry sources, third-party studies, including market analyses and reports, and internal company surveys. Industry sources generally state that the information contained therein has been obtained from sources believed to be reliable. Although we are responsible for all of the disclosure contained in this prospectus, and we believe the industry and market data to be reliable as of the date of this prospectus, this information could prove to be inaccurate.

Effective January 1, 2017, we converted our fiscal year end from a calendar year ending December 31 to a "52-53 week" year ending on the Saturday closest in proximity to December 31, such that each quarterly period will be 13 weeks in length, except during a 53 week year when the fourth quarter will be 14 weeks. This did not have a material effect on our consolidated financial statements and, therefore, we did not retrospectively adjust our financial statements. References herein to "2017" relate to the 52 weeks ended December 30, 2017, and references herein to "2016" and "2015" relate to the years ended December 31, 2016 and December 31, 2015, respectively. The second quarter of 2018 ended on June 30, 2018, and the second quarter of 2017 ended on July 1, 2017. In this prospectus, unless otherwise noted, when we compare a metric between one period and a "prior period," we are comparing it to the corresponding period from the prior fiscal year.

ii

The following summary highlights selected information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should carefully read the entire prospectus, including the consolidated financial statements and the related notes included in this prospectus and the information set forth under the headings "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations." Unless the context requires otherwise, the words "YETI," "we," "company," "us," and "our" refer to YETI Holdings, Inc. and its subsidiaries, as applicable.

YETI: Built for the Wild

We believe that by consistently designing and marketing innovative and outstanding outdoor products, we make an active lifestyle more enjoyable and cultivate a growing group of passionate and loyal customers.

Our Founders, Roy and Ryan Seiders, are avid outdoorsmen who were frustrated with equipment that could not keep pace with their interests in hunting and fishing. By utilizing forward-thinking designs and advanced manufacturing techniques, they developed a nearly indestructible hard cooler with superior ice retention. Our original cooler not only delivered exceptional performance, it anchored an authentic, passionate, and durable bond among customers and our company.

Today, we are a rapidly growing designer, marketer, retailer, and distributor of a variety of innovative, branded, premium products to a wide-ranging customer base. Our brand promise is to ensure each YETI product delivers exceptional performance and durability in any environment, whether in the remote wilderness, at the beach, or anywhere else life takes you. By consistently delivering high-performing products, we have built a following of engaged brand loyalists throughout the United States, Canada, Australia, and elsewhere, ranging from serious outdoor enthusiasts to individuals who simply value products of uncompromising quality and design. Our relationship with customers continues to thrive and deepen as a result of our innovative new product introductions, expansion and enhancement of existing product families, and multifaceted branding activities.

Our diverse product portfolio includes:

1

We bring our products to market through a diverse and powerful omni-channel strategy, comprised of our select group of national and independent retail partners and our direct-to-consumer and corporate sales, or DTC, channel. Our DTC channel is comprised of YETI.com, YETIcustomshop.com, YETI Authorized on the Amazon Marketplace, corporate sales, and our flagship store in Austin, Texas. Our DTC channel provides authentic, differentiated brand experiences, customer engagement, and expedited customer feedback, enhancing the product development cycle while providing diverse avenues for growth.

The broadening demand for our innovative and distinctive products is evidenced by our net sales growth from $89.9 million in 2013 to $639.2 million in 2017, representing a compound annual growth rate, or CAGR, of 63%. Over the same period, operating income grew from $15.2 million to $64.0 million, representing a CAGR of 43%, net income grew from $7.3 million to $15.4 million, representing a CAGR of 21%, Adjusted Operating Income grew from $16.3 million to $76.0 million, representing a CAGR of 47%, Adjusted Net Income grew from $8.0 million to $23.1 million, representing a CAGR of 30%, and our Adjusted EBITDA increased from $21.8 million to $97.5 million, representing a CAGR of 45%.

See "—Summary Consolidated Financial and Other Data" for a reconciliation of Adjusted Operating Income, Adjusted Net Income, and Adjusted EBITDA, each a non-GAAP (as defined below) measure, to operating income, net income, and net income, respectively.

How is YETI different?

We believe the following strengths fundamentally differentiate us from our competitors and drive our success:

Influential, Growing Brand with Passionate Following. The YETI brand stands for innovation, performance, uncompromising quality, and durability. We believe these attributes have made us the preferred choice of a wide variety of customers, from professional outdoors people to those who simply appreciate product excellence. Our products are used in and around an expanding range of pursuits, such as fishing, hunting, camping, climbing, snow sports, surfing, barbecuing, tailgating, ranch and rodeo, and general outdoors, as well as in life's daily activities. We support and build our brand through a multifaceted strategy, which includes innovative digital, social, television, and print media, our YETI Dispatch magalog, and several grass-roots initiatives that foster customer engagement. Our brand is embodied and personified by our YETI Ambassadors, a diverse group of men and women from throughout the United States and select international markets, comprised of world-class anglers, hunters, rodeo cowboys, barbecue pitmasters, surfers, and outdoor adventurers who embody our brand. The success of our brand-building strategy is partially demonstrated by our approximately 1.4 million new customers to YETI.com since 2013 and approximately 1.0 million Instagram followers as of June 30, 2018. In 2017 and the first six months of 2018, we added approximately 0.5 million and 0.2 million new customers to YETI.com, respectively.

Our loyal customers act as brand advocates. YETI owners often purchase and proudly wear YETI apparel and display YETI banners and decals. As evidenced by the respondents to our May 2018 YETI owner study, 95% say they have proactively recommended our products to their friends, family, and others through social media or by word-of-mouth. Their brand advocacy, coupled with our varied marketing efforts, has consistently extended our appeal to the broader "YETI Nation." As we have expanded our product lines, extended our YETI Ambassador base, and broadened our marketing messaging, we have cultivated an audience of both men and women living throughout the United States and, increasingly, in international markets. Based on our annual owner studies, from 2015 to 2018 our customer base has evolved from 9% female to 34%, and from 64% aged 45 and under to 70%. While we have continued to invest in and remain true to our heritage hunting and fishing communities, our customer base evolved from 69% hunters to 38% during that same time period as our appeal broadened beyond those heritage communities. Further, based on our quarterly Brand Tracking Study, our unaided brand awareness in the coolers and drinkware markets in the United States has grown from 7% in 2015 to 24% in 2017,

2

representing 243% growth during that period and indicating significant opportunity for future expansion, particularly in more densely populated United States markets.

Superior Design Capabilities and Product Development. At YETI, product is at our core and innovation fuels us. By employing an uncompromising approach to product performance and functionality, we have expanded on our original hard cooler offering and extended beyond our hunting and fishing heritage by introducing innovative new products, including soft coolers, drinkware, travel bags, backpacks, multipurpose buckets, outdoor chairs, blankets, dog bowls, apparel, and accessories. We believe that our new products appeal to our long-time customers as well as customers first experiencing our brand. We carefully design and rigorously test all new products, both in our innovation center and in the field, consistent with our commitment to delivering outstanding functional performance.

We believe our products continue to set new performance standards in their respective categories. Our expansive team of in-house engineers and designers develops our products using a comprehensive stage-gate process that ensures quality control and optimizes speed-to-market. We use our purpose-built, state-of-the-art research and development center to rapidly generate design prototypes and test performance. Our global supply chain group, with offices in Austin, Texas and mainland China, sources and partners with qualified suppliers to manufacture our products to meet our rigorous specifications. As a result, we control the innovation process from concept through design, production, quality assurance, and launch. To ensure we benefit from the significant investment we make in product innovation, we actively manage and aggressively protect our intellectual property.

We have a history of developing innovative products, including new products in existing product families, product line expansions, and accessories, as well as products that bring us into new categories. Our current product portfolio gives customers access to our brand at multiple price points, ranging from a $20 Rambler tumbler to a $1,300 Tundra hard cooler. We expand our existing product families and enter new product categories by creating solutions grounded in consumer insights and relevant market knowledge. We believe our product families, extensions, variations, and colorways, in addition to new product launches, result in repeat purchases by existing customers and consistently attract new customers to YETI.

Balanced, Omni-Channel Distribution Strategy. We distribute our products through a balanced omni-channel platform, consisting of our wholesale and DTC channels. In our wholesale channel, we sell our products through select national and regional accounts and an assemblage of independent retail partners throughout the United States and, more recently, Australia, Canada, and Japan. We carefully evaluate and select retail partners that have an image and approach that are consistent with our premium brand and pricing. Our domestic national and regional specialty retailers include Dick's Sporting Goods, REI, Academy Sports + Outdoors, Bass Pro Shops, and Ace Hardware. As of June 30, 2018, we also sold through a diverse base of nearly 4,800 independent retail partners, including outdoor specialty, hardware, sporting goods, and farm and ranch supply stores, among others. Our DTC channel consists primarily of online and inbound telesales and has grown from 8% of our net sales in 2015 to 30% in 2017. On YETI.com and at our flagship store, we showcase the entirety of our extensive product portfolio. Through YETIcustomshop.com and our corporate sales programs, we offer customers and businesses the ability to customize many of our products with licensed marks and original artwork. Our DTC channel enables us to directly interact with our customers, more effectively control our brand experience, better understand consumer behavior and preferences, and offer exclusive products, content, and customization capabilities. We believe our control over our DTC channel provides our customers the highest level of brand engagement and further builds customer loyalty, while generating attractive margins. As part of our commitment to premium positioning, we maintain supply discipline, consistently enforce our minimum advertised pricing, or MAP, policy across our wholesale and DTC channels, and sell primarily through one-step distribution.

3

Scalable Infrastructure to Support Growth. As we have grown, we have worked diligently and invested significantly to further build our information technology capabilities, while improving business process effectiveness. This robust infrastructure facilitates our ability to manage our global manufacturing base, optimize complex distribution logistics, and effectively serve our consistently expanding customer base. We believe our global team, sophisticated technology backbone, and extensive experience provide us with the capabilities necessary to support our future growth.

Experienced Management Team. Our senior management team, led by our President and Chief Executive Officer, or CEO, Matt Reintjes, is comprised of experienced executives from large global product and services businesses and publicly listed companies. They have proven track records of scaling businesses, leading innovation, expanding distribution, and managing expansive global operations. Our culture is an embodiment of the values of our Founders who continue to work as a member of our product development team and a YETI Ambassador and help to identify new opportunities and drive innovation.

Our Growth Strategies

We plan to continue growing our customer base by driving YETI brand awareness, introducing new and innovative products, entering new product categories, accelerating DTC sales, and expanding our international presence.

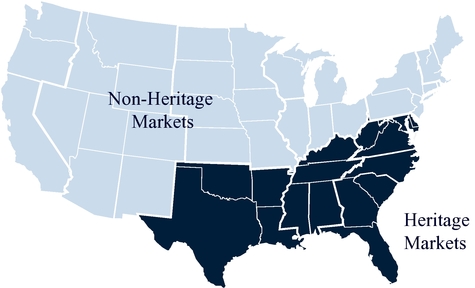

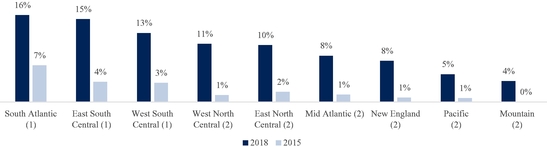

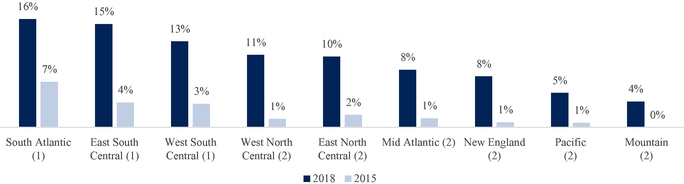

Expand Our Brand Awareness and Customer Base. Creating brand awareness among new customers and in new geographies has been, and remains, central to our growth strategy. We drive our brand through multilayered marketing programs, word-of-mouth referral, experiential brand events, YETI Ambassador reach, and product use. We have significantly invested in increasing brand awareness, spending $156.5 million in marketing initiatives from 2013 to 2017, including $50.7 million in 2017. This growth is illustrated by the increase in our gross sales derived from outside our heritage markets, which have increased significantly since 2013. We define our heritage markets as the South Atlantic, East South Central, and West South Central, as defined by the U.S. Census Bureau.

While we have meaningfully grown and expanded our brand reach throughout the United States and developed an emerging international presence, according to our quarterly brand study, unaided brand awareness, or consumers' awareness of our brand without prompt, in non-heritage markets remains meaningfully below unaided brand awareness in heritage markets. We believe our sales growth will be driven, in part, by continuing to grow YETI's brand awareness in non-heritage markets. For example, based on our quarterly Brand Tracking Study, our unaided brand awareness in the premium outdoor company and brand markets in the United States has grown from 2% in October 2015 to 10% in July 2018,

4

indicating there may be significant opportunity for future expansion, particularly in more densely populated United States markets. Our unaided brand awareness in the premium outdoor company and brand markets by region as of October 2015 and as of July 2018 is set forth below based on our quarterly Brand Tracking Study:

Domestic Unaided Brand Awareness by Region

- (1)

- Heritage market region

- (2)

- Non-heritage market region

Introduce New and Innovative Products. We have a track record of consistently broadening our high performance, premium-priced product portfolio to meet our expanding customer base and their evolving pursuits. Our culture of innovation and success in identifying customer needs and wants drives our robust product pipeline. We typically enter a product line by introducing anchor products, followed by product expansions, such as additional sizes and colorways, and then accessories, as exemplified by our current product portfolio. In 2017, we expanded our Drinkware line to new colorways, launched our Hopper Two soft cooler, and added new Hopper Flip sizes and colors. We added to our Coolers & Equipment offering with the introductions of our Panga submersible duffel and LoadOut multipurpose bucket. In 2018, we introduced our Camino Carryall bag, Hondo base camp chair, Hopper Backflip backpack, Rambler wine tumblers, Haul wheeled cooler, Silo water cooler, Panga submersible backpack, Tocayo backpack, Boomer dog bowl, and Lowlands blanket. We have also meaningfully enhanced our customization capabilities through YETIcustomshop.com, which offers a broad assortment of custom logo Drinkware and coolers to individual and corporate clients.

As we have done historically, we have identified several opportunities in new, adjacent product categories where we believe we can redefine performance standards and offer superior quality and design to customers. We believe these new opportunities will further bridge the connection between indoor and outdoor life and are consistent with our objective to have YETI products travel with customers wherever they go.

Increase Direct-to-Consumer and Corporate Sales. DTC represents our fastest growing sales channel, with net sales increasing from $14.1 million in 2013 to $194.4 million in 2017. Our DTC channel provides customers and businesses ready access to our brand, branded content, and full product assortment. We intend to continue to drive direct sales to our varied customers through: YETI.com; YETIcustomshop.com; YETI Authorized on the Amazon Marketplace; our corporate sales initiatives; increasing the number of our own retail stores; and our international YETI websites. In 2017, we had nearly 29.5 million visits to YETI.com and YETIcustomshop.com, of which 16.7 million were unique visitors and 0.8 million resulted in purchases. We believe we will continue to grow visitors to YETI.com and convert a portion of them to our customers. With YETIcustomshop.com, we believe there are significant opportunities to expand our licensing portfolio in sports and entertainment, along with numerous opportunities to further drive customized consumer and corporate sales. We began selling

5

through YETI Authorized on the Amazon Marketplace in late 2016 and have enjoyed rapid reach expansion and sales growth since that time. Based upon our growth to date, we are optimistic about continued expansion through this important distribution channel. In 2017, we opened our flagship retail store in Austin, which is a showroom for our products as well as an event space. Sales from our flagship store have continued to grow since its opening. Building on the strong response to our flagship store, we intend to open a company store for employees and additional retail stores in the second half of 2018 or in 2019.

Increasing sales through these various DTC channels enables us to control our product offering and how it is communicated to new and existing customers, fosters customer engagement, provides rapid feedback on new product launches, and enhances our demand forecasting. Further, our DTC channels provide customers an immersive and YETI-only experience, which we believe strengthens our brand.

Expand into International Markets. We believe we have the opportunity to continue to diversify and grow sales into existing and new international markets. In 2017, we successfully entered Canada and Australia, and 2018 net sales have continued to grow in both of these countries. In 2018, we successfully entered Japan. Our focus is on driving brand awareness, dealer expansion, and our DTC channel in these new markets. We believe there are meaningful growth opportunities by expanding into additional international markets, such as Europe and Asia, including China, as many of the market dynamics and premium, performance-based consumer needs that we have successfully identified domestically are also valued in these markets.

Our Market

Our premium products are designed for use in a wide variety of activities, from professional to recreational and outdoor to indoor, and can be used all year long. As a result, the markets we serve are broad as well as deep, including, for example, outdoor, housewares, home and garden, outdoor living, industrial, and commercial. While our product reach extends into numerous and varied markets, as of today, we primarily serve the United States outdoor recreation market. The outdoor recreation products market is a large, growing, and diverse economic super sector, which includes consumers of all genders, ages, ethnicities, and income levels. According to the Outdoor Industry Association's Outdoor Recreation Economy Reports, which are published every five years, outdoor recreation product sales in the United States grew from a total of approximately $120.7 billion in 2011 to a total of approximately $184.5 billion in 2016, representing a 9% CAGR.

Preliminary Third Quarter Results

We have not yet completed our closing procedures for the three months ended September 29, 2018. Set forth below are selected unaudited, preliminary, estimated financial results for the third quarter ended September 29, 2018. These estimated financial results are preliminary and subject to change. Our independent registered public accountants have not audited, reviewed, compiled, or performed any procedures with respect to these estimated financial results and, accordingly, do not express an opinion or any other form of assurance with respect to these preliminary estimates.

We expect net sales and gross profit to increase to approximately $196.1 million and $97.5 million for the three months ended September 29, 2018, respectively, compared to $183.0 million and $82.2 million for the three months ended September 30, 2017, respectively. We expect net income and Adjusted EBITDA to increase to approximately $17.0 million and $38.4 million for the three months ended September 29, 2018, respectively, compared to $11.3 million and $30.5 million for the three months ended September 30, 2017, respectively. We expect Adjusted EBITDA to represent approximately 19.6% of net sales for the three months ended September 29, 2018 compared to 16.7% for the three months ended September 30, 2017. We expect our cash to be approximately $52.0 million at September 29, 2018. We expect our long-term

6

debt, excluding debt issuance costs, to be approximately $394.0 million at September 29, 2018, which reflects additional debt payments of $41.4 million during the three months ended September 29, 2018.

The following table provides a preliminary reconciliation of net income to Adjusted EBITDA, as net income is the most directly comparable financial measure presented in accordance with GAAP. All line items are estimated approximations.

| |

Three Months Ended | ||||||

|---|---|---|---|---|---|---|---|

| (dollars in thousands) |

September 29, 2018 |

September 30, 2017 |

|||||

Net income |

$ | 17,030 | $ | 11,271 | |||

Interest expense |

7,756 | 8,351 | |||||

Income tax expense |

3,125 | 5,208 | |||||

Depreciation and amortization expense(a) |

6,333 | 5,815 | |||||

Non-cash stock-based compensation expense(b)(c) |

2,923 | 2,678 | |||||

Early extinguishment of debt(d) |

614 | — | |||||

Investments in new retail locations and international market expansion(b)(e) |

52 | — | |||||

Transition to Cortec majority ownership(b)(f) |

— | — | |||||

Transition to the ongoing senior management team(b)(g) |

350 | 90 | |||||

Transition to a public company(b)(h) |

232 | (2,935 | ) | ||||

| | | | | | | | |

Adjusted EBITDA |

$ | 38,415 | $ | 30,478 | |||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Net sales |

$ | 196,100 | $ | 183,032 | |||

Adjusted EBITDA as a % of net sales |

19.6% | 16.7% | |||||

- (a)

- These

costs are reported in SG&A expenses and cost of goods sold.

- (b)

- All

of these costs are reported in SG&A expenses.

- (c)

- Represents

our preliminary non-cash stock-based compensation for the three months ended September 29, 2018 of $2.9 million, compared to

$2.7 million for the three months ended September 30, 2017.

- (d)

- Represents

preliminary accelerated amortization of deferred financing fees caused by early debt paydown of the Credit Facility during the three months ended

September 29, 2018.

- (e)

- Represents

retail store pre-opening expenses and costs for expansion into new international markets.

- (f)

- Represents

management fees and expenses associated with contingent consideration.

- (g)

- Represents

severance, recruiting, and relocation costs related to the transition to our ongoing senior management team.

- (h)

- Represents fees and expenses in connection with our transition to a public company, including consulting fees, recruiting fees, salaries, and travel costs related to members of our Board of Directors, fees associated with Sarbanes-Oxley Act compliance, and incremental audit and legal fees associated with being a public company.

We include Adjusted EBITDA in this prospectus for the reasons described in "—Summary Consolidated Financial and Other Data." Adjusted EBITDA has certain limitations in that it does not reflect all expense items that affect our results. These and other limitations are described in "—Summary Consolidated Financial and Other Data." We encourage you to review our financial information in its entirety and not rely on a single financial measure.

We have provided the preliminary estimated results described above as our financial closing procedures for the month and three months ended September 29, 2018 are not yet complete. As a result,

7

there is a possibility that our final financial results will vary from these preliminary estimates. However, we currently expect that our final financial results will be materially consistent with the amounts described above. We undertake no obligation to update or supplement the information provided above until we release our final financial results for the three months ended September 29, 2018.

Selected Risks Associated with Our Business

Our business is subject to a number of risks and uncertainties, including those highlighted in the section titled "Risk Factors" immediately following this prospectus summary. Some of these principal risks include the following:

- •

- our business depends on maintaining and strengthening our brand and generating and maintaining ongoing demand for our products, and a

significant reduction in demand could harm our results of operations;

- •

- if we are unable to successfully design and develop new products, our business may be harmed;

- •

- we may not be able to effectively manage our growth;

- •

- our growth depends in part on expanding into additional consumer markets, and we may not be successful in doing so;

- •

- our plans for international expansion may not be successful;

- •

- the outdoor and recreation market is highly competitive and includes numerous other brands and retailers that offer a wide variety of products

that compete with our products; if we fail to compete effectively, or fail to protect our brand, our business would be harmed;

- •

- we rely on third-party contract manufacturers and problems with, or loss of, our suppliers or an inability to obtain raw materials could harm

our business and results of operations;

- •

- fluctuations in the cost and availability of raw materials, equipment, labor, and transportation could cause manufacturing delays or increase

our costs;

- •

- our business could be harmed if we are unable to accurately forecast demand for our products or our results of operations;

- •

- a significant portion of our sales are to national, regional, and independent retail partners and our business could be harmed if these retail

partners decide to emphasize products from our competitors, to redeploy their retail floor space to other product categories, to take other actions that reduce their purchases of our products, or if

they are disproportionately affected by economic conditions;

- •

- our future success depends on the continuing efforts of our management and key employees and our ability to attract and retain highly-skilled

personnel and senior management;

- •

- our indebtedness may limit our ability to invest in the ongoing needs of our business and if we are unable to comply with the covenants in the

Credit Agreement, dated as of May 19, 2016, by and among YETI Holdings, Inc., the lenders from time to time party thereto and Bank of America, N.A., as administrative agent, as amended,

which we refer to as the Credit Facility, our liquidity and results of operations could be harmed; and

- •

- we will be a "controlled company" and, as a result, we intend to rely on exemptions from certain corporate governance requirements.

8

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last completed fiscal year, we qualify as an "emerging growth company" as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of certain reduced reporting requirements that are otherwise applicable generally to public companies. These reduced reporting requirements include:

- •

- an exemption from compliance with the auditor attestation requirement on the effectiveness of our internal control over financial reporting;

- •

- an exemption from compliance with any requirement that the Public Company Accounting Oversight Board, or PCAOB, may adopt regarding mandatory

audit firm rotation or a supplement to the auditor's report providing additional information about the audit and the financial statements;

- •

- reduced disclosure about our executive compensation arrangements;

- •

- an exemption from the requirements to obtain a non-binding advisory vote on executive compensation or any golden parachute arrangements;

- •

- extended transition periods for complying with new or revised accounting standards; and

- •

- the ability to present more limited financial data, including presenting only three years of selected financial data in this registration statement, of which this prospectus is a part.

We will remain an emerging growth company until the earliest to occur of: (i) the end of the first fiscal year in which our annual gross revenue is $1.07 billion or more; (ii) the end of the fiscal year in which the market value of our common stock that is held by non-affiliates is at least $700 million as of the last business day of our most recently completed second fiscal quarter; (iii) the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt securities; and (iv) the end of the fiscal year during which the fifth anniversary of this offering occurs. We may choose to take advantage of some, but not all, of the available benefits under the JOBS Act.

We currently intend to take advantage of all of the exemptions discussed above. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you invest.

Our Sponsor

Cortec Group Fund V, L.P. and its affiliates, or Cortec, has been our principal stockholder since its initial investment in 2012.

After the closing of this offering, Cortec will own approximately 51.4% of our outstanding common stock (or approximately 48.7% if the underwriters exercise their option to purchase additional shares in full). In addition, Cortec will have the right to vote in the election of our directors the shares of common stock held by Roy Seiders, Ryan Seiders, their respective affiliates, and certain other stockholders pursuant to a voting agreement, or the Voting Agreement, to be entered into upon the pricing of this offering. As a result, upon the completion of this offering, the group formed by the Voting Agreement will control more than 50% of the total voting power of our common stock with respect to the election of our directors.

In May 2016, we declared and paid a dividend, or the Special Dividend, as a partial return of capital to our stockholders. The Special Dividend totaled $451.3 million, of which Cortec received $312.1 million.

9

Corporate Information

We were founded in 2006 by brothers Roy and Ryan Seiders in Austin, Texas and were subsequently incorporated as YETI Coolers, Inc., a Texas corporation, in 2010. In 2012, Cortec became our principal stockholder. In connection with Cortec's investment in YETI in 2012, YETI Coolers, Inc. was converted into YETI Coolers, LLC, a Delaware limited liability company, and subsequently YETI Coolers, LLC was acquired by an indirect subsidiary of YETI Holdings, Inc., a Delaware corporation incorporated in 2012 by Cortec. Thereafter, through two subsequent mergers, YETI Coolers, LLC became a wholly owned subsidiary of YETI Holdings, Inc. As part of the acquisition of YETI Coolers, LLC, our Founders and certain other equity holders exchanged a portion of their proceeds from the sale of YETI Coolers, LLC for equity in YETI Holdings, Inc. As a result, YETI Holdings, Inc. is currently majority owned by Cortec, with the remaining ownership being shared by our Founders, certain other management equity holders and select investors.

Our principal executive and administrative offices are located at 7601 Southwest Parkway, Austin, Texas 78735, and our telephone number is (512) 394-9384. Our website address is YETI.com. The information on, or that can be accessed through, our website is not incorporated by reference into this prospectus and should not be considered to be a part of this prospectus.

10

Common stock offered by us |

2,500,000 shares | |

Common stock offered by the selling stockholders |

17,500,000 shares (20,500,000 shares if the underwriters exercise their option to purchase additional shares in full) |

|

Underwriters' option to purchase additional shares from the selling stockholders |

The underwriters have a 30-day option to purchase up to 3,000,000 additional shares of our common stock from the selling stockholders at the public offering price less estimated underwriting discounts and commissions. |

|

Common stock to be outstanding after this offering |

83,647,425 shares |

|

Use of proceeds |

We estimate that we will receive net proceeds from the sale of shares of our common stock that we are selling in this offering of approximately $41.5 million, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us, based upon an assumed initial public offering price of $20.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus. We currently intend to use the net proceeds from this offering to repay $41.5 million of outstanding borrowings under the Credit Facility. We will not receive any proceeds from the sale of shares of our common stock by the selling stockholders. See "Use of Proceeds" for a complete description of the intended use of proceeds from this offering. |

|

Controlled company |

Pursuant to the Voting Agreement, upon the closing of this offering, Cortec will control more than 50% of the total voting power of our common stock with respect to the election of our directors. As a result, we will be a "controlled company" within the meaning of the New York Stock Exchange, or NYSE, listing standards, and therefore will be exempt from certain NYSE corporate governance requirements. |

|

Risk factors |

Investing in shares of our common stock involves a high degree of risk. See "Risk Factors" beginning on page 17 and the other information included in this prospectus for a discussion of factors you should carefully consider before investing in shares of our common stock. |

|

NYSE symbol |

"YETI" |

The number of shares of our common stock that will be outstanding after this offering is based on 81,147,425 shares of our common stock outstanding as of October 1, 2018, and excludes:

- •

- 2,675,780 shares of our common stock issuable upon the exercise of outstanding but unexercised options, of which 2,281,956 are vested, to purchase shares of our common stock as of October 1, 2018 under the YETI Holdings, Inc. 2012 Equity and Performance Incentive Plan, as amended and restated June 20, 2018, or the 2012 Plan, with a weighted average exercise price of $2.04 per share;

11

- •

- 1,410,718 shares of our common stock issuable upon the settlement of restricted stock units outstanding as of October 1, 2018 under the

2012 Plan, with an estimated grant date fair value of $31.74 per share;

- •

- 2,217,236 shares of our common stock reserved for future issuance under the 2012 Plan which, upon the effectiveness of the YETI Holdings, Inc.

2018 Equity and Incentive Compensation Plan, or the 2018 Plan, will no longer be available for awards under the 2012 Plan or the 2018 Plan; and

- •

- 4,764,000 shares of our common stock reserved for future issuance under the 2018 Plan.

Except as otherwise indicated, all information in this prospectus assumes or reflects:

- •

- no exercise of the underwriters' option to purchase additional shares from the selling stockholders;

- •

- no exercise or settlement of outstanding stock options;

- •

- the filing and effectiveness of an amendment to our certificate of incorporation prior to the completion of this offering to effect a

0.397-for-1 reverse split of our common stock, and all share, option, and per share information in this prospectus has been adjusted to reflect the split on a retroactive basis;

- •

- the filing and effectiveness of our amended and restated certificate of incorporation, including an increase in the authorized shares of our

capital stock, and the effectiveness of our amended and restated bylaws, each of which will occur prior to the completion of this offering; and

- •

- the amendment of our certificate of incorporation on May 5, 2016 to effect a 2,000-for-1 forward split of our common stock, including an increase in the authorized shares of our capital stock, and all share, option, and per share information in this prospectus has been adjusted to reflect the split on a retroactive basis.

12

Summary Consolidated Financial and Other Data

The following tables set forth a summary of our historical summary consolidated financial data for the periods and at the dates indicated. Effective January 1, 2017, we converted our fiscal year end from a calendar year ending December 31 to a "52-53 week" year ending on the Saturday closest in proximity to December 31, such that each quarterly period will be 13 weeks in length, except during a 53-week year when the fourth quarter will be 14 weeks. This did not have a material effect on our consolidated financial statements and, therefore, we did not retrospectively adjust our financial statements. Fiscal year 2017 included 52 weeks, and the first six months of fiscal 2018 and fiscal 2017 included 26 weeks. The following table sets forth consolidated financial data for 2017, 2016, and 2015, which have been derived from our audited consolidated financial statements included elsewhere in this prospectus. The consolidated financial data as of and for the six months ended June 30, 2018 and for the six months ended July 1, 2017 have been derived from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. In the opinion of management, our unaudited condensed consolidated financial statements were prepared on the same basis as our audited consolidated financial statements and include all adjustments necessary for a fair presentation of this information. The percentages below indicate the statement of operations data as a percentage of net sales. You should read this data together with our audited financial statements, our unaudited financial statements, and related notes appearing elsewhere in this prospectus and the information included under the caption "Management's Discussion and Analysis of Financial Condition and Results of Operations." Our historical results are not necessarily indicative of our future results.

| |

Six Months Ended | Fiscal Year Ended | |||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

(in thousands, except per share data) |

June 30, 2018 |

July 1, 2017 |

December 30, 2017 |

December 31, 2016 |

December 31, 2015 |

||||||||||||||||||||||||||

Statements of Operations |

|||||||||||||||||||||||||||||||

Net sales |

$ | 341,545 | 100 | % | $ | 254,108 | 100 | % | $ | 639,239 | 100 | % | $ | 818,914 | 100 | % | $ | 468,946 | 100 | % | |||||||||||

Cost of goods sold |

183,786 | 54 | % | 134,822 | 53 | % | 344,638 | 54 | % | 404,953 | 49 | % | 250,245 | 53 | % | ||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Gross profit |

157,759 | 46 | % | 119,286 | 47 | % | 294,601 | 46 | % | 413,961 | 51 | % | 218,701 | 47 | % | ||||||||||||||||

Selling, general and administrative expenses |

121,329 | 36 | % | 103,908 | 41 | % | 230,634 | 36 | % | 325,754 | 40 | % | 90,791 | 19 | % | ||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating income |

36,430 | 11 | % | 15,378 | 6 | % | 63,967 | 10 | % | 88,207 | 11 | % | 127,910 | 27 | % | ||||||||||||||||

Interest expense |

(16,719 | ) | 5 | % | (15,610 | ) | 6 | % | (32,607 | ) | 5 | % | (21,680 | ) | 3 | % | (6,075 | ) | 1 | % | |||||||||||

Other (expense) income |

(111 | ) | 0 | % | 1,150 | 0 | % | 699 | 0 | % | (1,242 | ) | 0 | % | (6,474 | ) | 1 | % | |||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income before income taxes |

19,600 | 6 | % | 918 | 0 | % | 32,059 | 5 | % | 65,285 | 8 | % | 115,361 | 25 | % | ||||||||||||||||

Income tax expense |

(4,036 | ) | 1 | % | (762 | ) | 0 | % | (16,658 | ) | 3 | % | (16,497 | ) | 2 | % | (41,139 | ) | 9 | % | |||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income |

$ | 15,564 | 5 | % | $ | 156 | 0 | % | $ | 15,401 | 2 | % | $ | 48,788 | 6 | % | $ | 74,222 | 16 | % | |||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income attributable to noncontrolling interest |

— | 0 | % | — | 0 | % | — | 0 | % | (811 | ) | 0 | % | — | 0 | % | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income to YETI Holdings, Inc. |

15,564 | 5 | % | 156 | 0 | % | 15,401 | 2 | % | 47,977 | 6 | % | 74,222 | 16 | % | ||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Adjusted Operating Income(1) |

46,642 | 14 | % | 23,343 | 9 | % | 76,003 | 12 | % | 221,429 | 27 | % | 136,043 | 29 | % | ||||||||||||||||

Adjusted Net Income(1) |

23,453 | 7 | % | 5,267 | 2 | % | 23,126 | 4 | % | 134,559 | 16 | % | 79,484 | 17 | % | ||||||||||||||||

Adjusted EBITDA(1) |

$ | 58,416 | 17 | % | $ | 33,849 | 13 | % | $ | 97,471 | 15 | % | $ | 231,862 | 28 | % | $ | 137,101 | 29 | % | |||||||||||

Net income to YETI Holdings, Inc. per share |

|||||||||||||||||||||||||||||||

Basic |

$ | 0.19 | $ | — | $ | 0.19 | $ | 0.59 | $ | 0.93 | |||||||||||||||||||||

Diluted |

$ | 0.19 | $ | — | $ | 0.19 | $ | 0.58 | $ | 0.92 | |||||||||||||||||||||

Adjusted Net Income per share(2) |

|||||||||||||||||||||||||||||||

Diluted |

$ | 0.28 | $ | 0.06 | $ | 0.28 | $ | 1.63 | $ | 0.99 | |||||||||||||||||||||

Weighted average common shares outstanding |

|||||||||||||||||||||||||||||||

Basic |

81,283 | 81,451 | 81,479 | 81,097 | 79,775 | ||||||||||||||||||||||||||

Diluted |

82,956 | 83,029 | 82,972 | 82,755 | 80,665 | ||||||||||||||||||||||||||

13

| |

|

As of June 30, 2018 |

|||||

|---|---|---|---|---|---|---|---|

| |

As of June 30, 2018 |

||||||

(dollars in thousands)

|

Pro Forma(3)(4)(5) | ||||||

Balance Sheet and Other Data |

|||||||

Inventory |

$ | 149,368 | $ | 149,368 | |||

Property and equipment, net |

71,101 | 71,101 | |||||

Total assets |

510,397 | 510,397 | |||||

Long-term debt including current maturities |

427,863 | 386,363 | |||||

Total stockholders' deficit |

(56,801 | ) | (15,301 | ) | |||

Additions to property and equipment |

7,067 | 7,067 | |||||

- (1)

- Adjusted

Operating Income and Adjusted Net Income are defined as operating income and net income adjusted for non-cash stock-based compensation expense, early

extinguishment of debt, asset impairment charges, investments in new retail locations and international market expansion, transition to Cortec majority ownership, transition to the ongoing senior

management team, and transition to a public company, and, in the case of Adjusted Net Income, net of the tax impact of such adjustments. Adjusted EBITDA is defined as net income before interest

expense, income tax expense, depreciation and amortization expense, non-cash stock-based compensation expense, early extinguishment of debt, asset impairment charges, investments in new retail

locations and international market expansion, transition to Cortec majority ownership, transition to the ongoing senior management team, and transition to a public company. The expenses incurred

related to these transitional events include: management fees and contingent consideration related to the transition to Cortec majority ownership; severance, recruiting, and relocation costs related

to the transition to our ongoing senior management team; consulting fees, recruiting fees, salaries and travel costs related to members of our Board of Directors, fees associated with Sarbanes-Oxley

Act compliance, and incremental audit and legal fees in connection with our transition to a public company. All of these transitional costs are reported in selling, general, and administrative, or

SG&A, expenses.

Adjusted Operating Income, Adjusted Net Income, and Adjusted EBITDA are not defined under GAAP and may not be comparable to similarly titled measures reported by other entities. We use these non-GAAP measures, along with GAAP measures, as a measure of profitability. These measures help us compare our performance to other companies by removing the impact of our capital structure; the effect of operating in different tax jurisdictions; the impact of our asset base, which can vary depending on the book value of assets and methods used to compute depreciation and amortization; the effect of non-cash stock-based compensation expense, which can vary based on plan design, share price, share price volatility, and the expected lives of equity instruments granted; as well as certain expenses related to what we believe are events of a transitional nature. We also disclose Adjusted Operating Income, Adjusted Net Income, and Adjusted EBITDA as a percentage of net sales to provide a measure of relative profitability.

We believe these non-GAAP measures, when reviewed in conjunction with GAAP financial measures, and not in isolation or as substitutes for analysis of our results of operations under GAAP, are useful to investors as they are widely used measures of performance and the adjustments we make to these non-GAAP measures provide investors further insight into our profitability and additional perspectives in comparing our performance to other companies and in comparing our performance over time on a consistent basis. Adjusted Operating Income, Adjusted Net Income, and Adjusted EBITDA have limitations as profitability measures in that they do not include the interest expense on our debts, our provisions for income taxes, and the effect of our expenditures for capital assets and certain intangible assets. In addition, all of these non-GAAP measures have limitations as profitability measures in that they do not include the effect of non-cash stock-based compensation expense, the effect of asset impairments, the effect of investments in new retail locations and international market expansion, and the impact of certain expenses related to transitional events that are settled in cash. Because of these limitations, we rely primarily on our GAAP results.

14

In the future, we may incur expenses similar to those for which adjustments are made in calculating Adjusted Operating Income, Adjusted Net Income, and Adjusted EBITDA. Our presentation of these non-GAAP measures should not be construed as a basis to infer that our future results will be unaffected by extraordinary, unusual, or non-recurring items.

The following tables reconcile operating income to Adjusted Operating Income, net income to Adjusted Net Income, and net income to Adjusted EBITDA for the periods presented.

| |

Six Months Ended | Fiscal Year Ended | |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

(dollars in thousands)

|

June 30, 2018 |

July 1, 2017 |

December 30, 2017 |

December 31, 2016 |

December 31, 2015 |

|

|||||||||||

Operating income |

$ | 36,430 | $ | 15,378 | $ | 63,967 | $ | 88,207 | $ | 127,910 | |||||||

Adjustments: |

|||||||||||||||||

Non-cash stock-based compensation expense(a)(b) |

7,108 | 6,508 | 13,393 | 118,415 | 624 | ||||||||||||

Early extinguishment of debt(c) |

— | — | — | 1,221 | — | ||||||||||||

Investments in new retail locations and international market expansion(a)(d) |

240 | — | — | — | — | ||||||||||||

Transition to Cortec majority ownership(a)(e) |

750 | 750 | 750 | 750 | 7,224 | ||||||||||||

Transition to the ongoing senior management team(a)(f) |

1,344 | — | 90 | 2,824 | 285 | ||||||||||||

Transition to a public company(a)(g) |

770 | 707 | (2,197 | ) | 10,012 | — | |||||||||||

| | | | | | | | | | | | | | | | | | |

Adjusted Operating Income |

$ | 46,642 | $ | 23,343 | $ | 76,003 | $ | 221,429 | $ | 136,043 | |||||||

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

Net income |

$ | 15,564 | $ | 156 | $ | 15,401 | $ | 48,788 | $ | 74,222 | |||||||

Adjustments: |

|||||||||||||||||

Non-cash stock-based compensation expense(a)(b) |

7,108 | 6,508 | 13,393 | 118,415 | 624 | ||||||||||||

Early extinguishment of debt(c) |

— | — | — | 1,221 | — | ||||||||||||

Investments in new retail locations and international market expansion(a)(d) |

240 | — | — | — | — | ||||||||||||

Transition to Cortec majority ownership(a)(e) |

750 | 750 | 750 | 750 | 7,224 | ||||||||||||

Transition to the ongoing senior management team(a)(f) |

1,344 | — | 90 | 2,824 | 285 | ||||||||||||

Transition to a public company(a)(g) |

770 | 707 | (2,197 | ) | 10,012 | — | |||||||||||

Tax impact of adjusting items(h) |

(2,323 | ) | (2,854 | ) | (4,311 | ) | (47,451 | ) | (2,871 | ) | |||||||

| | | | | | | | | | | | | | | | | | |

Adjusted Net Income |

$ | 23,453 | $ | 5,267 | $ | 23,126 | $ | 134,559 | $ | 79,484 | |||||||

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

Net income |

$ | 15,564 | $ | 156 | $ | 15,401 | $ | 48,788 | $ | 74,222 | |||||||

Adjustments: |

|||||||||||||||||

Interest expense |

16,719 | 15,610 | 32,607 | 21,680 | 6,075 | ||||||||||||

Income tax expense |

4,036 | 762 | 16,658 | 16,497 | 41,139 | ||||||||||||

Depreciation and amortization expense(i) |

11,885 | 9,356 | 20,769 | 11,675 | 7,532 | ||||||||||||

Non-cash stock-based compensation expense(a)(b) |

7,108 | 6,508 | 13,393 | 118,415 | 624 | ||||||||||||

Early extinguishment of debt(c) |

— | — | — | 1,221 | — | ||||||||||||

Investments in new retail locations and international market expansion(a)(d) |

240 | — | — | — | — | ||||||||||||

Transition to Cortec majority ownership(a)(e) |

750 | 750 | 750 | 750 | 7,224 | ||||||||||||

Transition to the ongoing senior management team(a)(f) |

1,344 | — | 90 | 2,824 | 285 | ||||||||||||

Transition to a public company(a)(g) |

770 | 707 | (2,197 | ) | 10,012 | — | |||||||||||

| | | | | | | | | | | | | | | | | | |

Adjusted EBITDA |

$ | 58,416 | $ | 33,849 | $ | 97,471 | $ | 231,862 | $ | 137,101 | |||||||

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

Net sales |

$ | 341,545 | $ | 254,108 | $ | 639,239 | $ | 818,914 | $ | 468,946 | |||||||

Net income as a % of net sales |

4.6 | % | 0.1 | % | 2.4 | % | 6.0 | % | 15.8 | % | |||||||

Adjusted operating income as a % of net sales |

13.7 | % | 9.2 | % | 11.9 | % | 27.0 | % | 29.0 | % | |||||||

Adjusted net income as a % of net sales |

6.9 | % | 2.1 | % | 3.6 | % | 16.4 | % | 16.9 | % | |||||||

Adjusted EBITDA as a % of net sales |

17.1 | % | 13.3 | % | 15.2 | % | 28.3 | % | 29.2 | % | |||||||

- (a)

- All of these costs are reported in SG&A expenses.

15

- (b)

- For

the six months ended June 30, 2018 and July 1, 2017, non-cash stock-based compensation expense was $7.1 million and $6.5 million,

respectively. For 2017, 2016, and 2015, compensation expense was $13.4 million, $118.4 million, and $0.6 million, respectively.

- (c)

- For

2016, represents the unamortized deferred financing fees associated with our prior credit facility, or the 2012 Credit Facility, which were outstanding at the

time of repayment in May 2016.

- (d)

- Represents

retail store pre-opening expenses and costs for expansion into new international markets.

- (e)

- Represents

management fees of $0.8 million and $0.8 million and expenses associated with contingent consideration of $0 and $0 for the six months ended

June 30, 2018 and July 1, 2017, respectively. For 2017, 2016, and 2015, annual management fees to Cortec were $0.8 million and contingent consideration was $0, $0, and

$6.5 million, respectively.

- (f)

- Represents

severance, recruiting, and relocation costs related to the transition to our ongoing senior management team.

- (g)

- Represents

fees and expenses in connection with our transition to a public company, including consulting fees, recruiting fees, salaries, and travel costs related to

members of our Board of Directors, fees associated with Sarbanes-Oxley Act compliance, and incremental audit and legal fees associated with being a public company.

- (h)

- Tax

impact of adjustments calculated at a 23% and 36% effective tax rate for the six months ended June 30, 2018 and July 1, 2017, respectively. For

2017, 2016, and 2015, the effective tax rate used to calculate the tax impact of adjustments was 36%, 36%, and 35%, respectively.

- (i)

- These costs are reported in SG&A expenses and cost of goods sold.

- (2)

- Adjusted Net Income per share is calculated using Adjusted Net Income, as defined above, and diluted weighted average shares

outstanding. Adjusted Net Income per share is not a presentation made in accordance with GAAP, and our use of the term Adjusted Net Income per share may vary from similar measures reported by others

in our industry due to the potential differences in the method of calculation. Adjusted Net Income per share should not be considered as an alternative to earnings per share derived in accordance with

GAAP. Adjusted Net Income per share has important limitations as an analytical tool and should not be considered in isolation or as a substitute for analysis of our results as reported under GAAP.

Because of these limitations, we rely primarily on our GAAP results. However, we believe that presenting Adjusted Net Income per share is appropriate to provide investors with useful information

regarding our historical operating results.

- (3)

- Reflects our total assets and total stockholders' equity (deficit) as of June 30, 2018 on a pro forma basis to give

effect to the filing and effectiveness of our amended and restated certificate of incorporation, including an increase in the authorized shares of our capital stock, as if such event had

occurred on June 30, 2018.

- (4)

- Reflects the sale by us of shares of common stock in this offering at an assumed initial public offering price of $20.00 per

share, the midpoint of the price range set forth on the cover page of this prospectus, after deducting underwriting discounts and commissions and estimated offering expenses payable by us and the

application of the net proceeds from this offering as described in "Use of Proceeds."

- (5)

- Each $1.00 increase (decrease) in the assumed initial public offering price of $20.00 per share, the midpoint of the price range set forth on the cover page of this prospectus, would increase (decrease) each of total assets and total stockholders' equity (deficit) by approximately $2.4 million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same, and after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We may also increase or decrease the number of shares we are offering. Each increase (decrease) of 100,000 shares in the number of shares offered by us would increase (decrease) each of total assets and total stockholders' equity by approximately $1.9 million, assuming that the assumed initial price to the public remains the same, and after deducting the underwriting discounts and commissions and estimated offering expenses payable by us. The pro forma information discussed above is illustrative only and will adjust based on the actual initial public offering price and other terms of this offering determined at pricing.

16

Investing in our common stock involves a high degree of risk. These risks include, but are not limited to, those described below, each of which may be relevant to an investment decision. You should carefully consider the risks and uncertainties described below, together with all of the other information contained in this prospectus, including the section titled "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and the related notes, before deciding whether to invest in shares of our common stock. If any of the following risks or other risks actually occur, our business, financial condition, results of operations, and future prospects could be materially harmed. In that event, the market price of our common stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business and Industry

Our business depends on maintaining and strengthening our brand and generating and maintaining ongoing demand for our products, and a significant reduction in such demand could harm our results of operations.

The YETI name and premium brand image are integral to the growth of our business, as well as to the implementation of our strategies for expanding our business. Our success depends on the value and reputation of our brand, which, in turn, depends on factors such as the quality, design, performance, functionality, and durability of our products, the image of our e-commerce platform and retail partner floor spaces, our communication activities, including advertising, social media, and public relations, and our management of the customer experience, including direct interfaces through customer service. Maintaining, promoting, and positioning our brand are important to expanding our customer base, and will depend largely on the success of our marketing and merchandising efforts and our ability to provide consistent, high quality customer experiences. We intend to make substantial investments in these areas in order to maintain and enhance our brand, and such investments may not be successful. Ineffective marketing, negative publicity, product diversion to unauthorized distribution channels, product or manufacturing defects, counterfeit products, unfair labor practices, and failure to protect the intellectual property rights in our brand are some of the potential threats to the strength of our brand, and those and other factors could rapidly and severely diminish customer confidence in us. Furthermore, these factors could cause our customers to lose the personal connection they feel with the YETI brand. We believe that maintaining and enhancing our brand image in our current markets and in new markets where we have limited brand recognition is important to expanding our customer base. If we are unable to maintain or enhance our brand in current or new markets, our growth strategy and results of operations could be harmed.

If we are unable to successfully design and develop new products, our business may be harmed.

To maintain and increase sales we must continue to introduce new products and improve or enhance our existing products. The success of our new and enhanced products depends on many factors, including anticipating consumer preferences, finding innovative solutions to consumer problems, differentiating our products from those of our competitors, and maintaining the strength of our brand. The design and development of our products is costly and we typically have several products in development at the same time. Problems in the design or quality of our products, or delays in product introduction, may harm our brand, business, financial condition, and results of operations.

Our business could be harmed if we are unable to accurately forecast demand for our products or our results of operations.

To ensure adequate inventory supply, we forecast inventory needs and often place orders with our manufacturers before we receive firm orders from our retail partners or customers. If we fail to accurately forecast demand, we may experience excess inventory levels or a shortage of product to deliver to our retail partners and through our DTC channel.

17

If we underestimate the demand for our products, our manufacturers may not be able to scale to meet our demand, and this could result in delays in the shipment of our products and our failure to satisfy demand, as well as damage to our reputation and retail partner relationships. If we overestimate the demand for our products, we could face inventory levels in excess of demand, which could result in inventory write-downs or write-offs and the sale of excess inventory at discounted prices, which would harm our gross margins. For example, driven by strong customer demand and a shortage of product in 2015, retailers aggressively stocked our products during 2016, which led to excess inventory in our wholesale channel and drove many of our retail partners to reduce purchases in the first half of 2017. In addition, failures to accurately predict the level of demand for our products could cause a decline in sales and harm our results of operations and financial condition.

In addition, we may not be able to accurately forecast our results of operations and growth rate. Forecasts may be particularly challenging as we expand into new markets and geographies and develop and market new products. Our historical sales, expense levels, and profitability may not be an appropriate basis for forecasting future results.

Failure to accurately forecast our results of operations and growth rate could cause us to make poor operating decisions and we may not be able to adjust in a timely manner. Consequently, actual results could be materially lower than anticipated. Even if the markets in which we compete expand, we cannot assure you that our business will grow at similar rates, if at all.

We may not be able to effectively manage our growth.

As we grow our business, slower growing or reduced demand for our products, increased competition, a decrease in the growth rate of our overall market, failure to develop and successfully market new products, or the maturation of our business or market could harm our business. We expect to make significant investments in our research and development and sales and marketing organizations, expand our operations and infrastructure both domestically and internationally, design and develop new products, and enhance our existing products. In addition, in connection with operating as a public company, we will incur significant additional legal, accounting, and other expenses that we did not incur as a private company. If our sales do not increase at a sufficient rate to offset these increases in our operating expenses, our profitability may decline in future periods.

We have expanded our operations rapidly since our inception. Our employee headcount and the scope and complexity of our business have increased substantially over the past several years. We have only a limited history operating our business at its current scale. Our management team does not have substantial tenure working together. Consequently, if our operations continue to grow at a rapid pace, we may experience difficulties in managing this growth and building the appropriate processes and controls. Continued growth may increase the strain on our resources, and we could experience operating difficulties, including difficulties in sourcing, logistics, recruiting, maintaining internal controls, marketing, designing innovative products, and meeting consumer needs. If we do not adapt to meet these evolving challenges, the strength of our brand may erode, the quality of our products may suffer, we may not be able to deliver products on a timely basis to our customers, and our corporate culture may be harmed.

Our marketing strategy of associating our brand and products with activities rooted in passion for the outdoors may not be successful with existing and future customers.