Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - ETF Managers Group Commodity Trust I | s112215_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - ETF Managers Group Commodity Trust I | s112215_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - ETF Managers Group Commodity Trust I | s112215_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - ETF Managers Group Commodity Trust I | s112215_ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

for the fiscal year ended June 30, 2018.

or

| ☐ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

for the transition period from to .

Commission file number: 001-36851

ETF Managers Group Commodity Trust I

(Exact name of registrant as specified in its charter)

| Delaware | 36-4793446 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

30 Maple Street – Suite 2

Summit, NJ 07901

(Address of principal executive offices) (Zip code)

(908) 897-0518

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Shares of Sit Rising Rate ETF | NYSE Arca, Inc. |

| (Title of each class) | (Name of exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ | Smaller reporting company ☒ |

| Emerging Growth Company ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected to not use the extend transition period for complying with any new or revised financial reporting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

The aggregate market value of the registrant’s shares held by non-affiliates of the registrant as of June 30, 2018 was: $9,974,970. (RISE)

The aggregate market value of the registrant’s shares held by non-affiliates of the registrant as of June 30, 2018 was: $3,306,000. (BDRY)

The registrant had 2,100,040 outstanding shares as of September 1, 2018. (RISE)

The registrant had 150,040 outstanding shares as of September 1, 2018. (BDRY)

ETF Managers Group Commodity Trust I

Table of Contents

The Trust and the Funds

ETF Managers Group Commodity Trust I (the “Trust”) was organized as a Delaware statutory trust on July 23, 2014. The Trust is a series trust formed pursuant to the Delaware Statutory Trust Act and currently includes two separate series. Sit Rising Rate ETF (“RISE”) is the first series of the Trust and is a commodity pool that continuously issues common shares of beneficial interest that may be purchased and sold on the NYSE Arca, Inc. stock exchange (“NYSE Arca”). The second series of the Trust, Breakwave Dry Bulk Shipping ETF (“BDRY,” and together with RISE, each, a “Fund” and collectively, the “Funds”), is also a commodity pool that continuously issues shares of beneficial interest that may be purchased and sold on NYSE Arca.

RISE commenced investment operations on February 19, 2015. RISE commenced trading on NYSE Arca on February 19, 2015 and trades under the symbol “RISE.” BDRY commenced investment operations on March 22, 2018. BDRY commenced trading on NYSE Arca on March 22, 2018 and trades under the symbol “BDRY.”

The principal office of the Trust and the Funds is located at 30 Maple Street, Suite 2, Summit, NJ 07901. The telephone number is (844) 383-6477.

The Sponsor

The Funds are each managed and controlled by ETF Managers Capital LLC (the “Sponsor”), a single member limited liability company that was formed in the state of Delaware on June 12, 2014. Each Fund pays the Sponsor a management fee. The Sponsor maintains its main business office at 30 Maple Street, Suite 2, Summit, NJ 07901. The Sponsor’s telephone number is (844) 383-6477.

The Funds are each a “commodity pool” as defined by the Commodity Exchange Act (“CEA”). Consequently, the Sponsor has registered as a commodity pool operator (“CPO”) with the Commodity Futures Trading Commission (“CFTC”) and is a member of the National Futures Association (“NFA”).

The Sponsor is a wholly-owned subsidiary of Exchange Traded Managers Group LLC (“ETFMG”), a limited liability company domiciled and headquartered in New Jersey.

Sit Rising Rate ETF

RISE Investment Objective

RISE’s investment objective is to profit from rising interest rates by tracking the performance of a portfolio (the “RISE Benchmark Portfolio”) consisting of exchange traded futures contracts and options on futures on 2, 5 and 10 year U.S. Treasury securities (“Treasury Instruments”) weighted to achieve a targeted negative 10 year average effective portfolio duration (the “RISE Benchmark Component Instruments”). RISE seeks to achieve its investment objective by investing in the RISE Benchmark Component Instruments currently constituting the RISE Benchmark Portfolio. The RISE Benchmark Portfolio is maintained by Sit Fixed Income Advisors II, LLC (“Sit”), which also serves as RISE’s commodity trading advisor (“CTA”). The RISE Benchmark Portfolio will be rebalanced, reconstituted, or both, monthly (typically on the 15th of each month, or on the next business day if the 15th is a holiday, weekend, or other day on which the national stock exchanges are closed) to maintain a negative 10 year average effective duration. The RISE Benchmark Portfolio and RISE will each maintain a short position in Treasury Instruments. RISE does not use futures contracts or options to obtain leveraged investment results. RISE will not invest in swaps or other over-the-counter derivative instruments.

1

RISE Commodity Trading Advisor

Sit serves as RISE’s CTA. Sit is a Delaware limited liability company and a subsidiary of Sit Investment Associates, Inc. Sit Investment Associates, Inc. was founded in July 1981 by Eugene C. Sit and is a Minnesota corporation.

Sit is registered as a CTA with the CFTC and is a member of the NFA.

Sit provides its services to RISE under a Licensing and Services Agreement with the Sponsor. Under this agreement, Sit has agreed to compose and maintain the RISE Benchmark Portfolio and license to the Sponsor the use of the RISE Benchmark Portfolio.

RISE Significant Shareholders

Prior to RISE’s commencing operations, Sit made an initial investment of $5,000,000 in exchange for 200,000 shares of RISE. As of June 30, 2018, Sit was RISE’s primary shareholder. The shares purchased by Sit are redeemable by Sit on the same terms and conditions as those applicable to firms authorized to purchase and redeem RISE shares. If Sit were to redeem its shares before RISE sells sufficient additional shares, such sale could have a material adverse affect on RISE and its shareholders, including its ability to achieve its investment objective.

RISE Investing Strategy

RISE seeks to achieve its investment objective by investing in the RISE Benchmark Component Instruments currently constituting the RISE Benchmark Portfolio. The weighting of the Treasury Instruments constituting the RISE Benchmark Component Instruments will be based on each maturity’s duration contribution. The expected range for the duration weighted percentage of the 2 year and 5 year maturity Treasury Instruments will be from 30% to 70%. The expected range for the duration weighted percentage of the 10 year maturity Treasury Instruments will be from 5% to 25%.

The relative weightings of the RISE Benchmark Component Instruments will be shifted between maturities when there are material changes in the shape of the yield curve, for example, if the Federal Reserve began raising short term interest rates more than long term interest rates. In such an instance, Sit, which maintains the RISE Benchmark Portfolio, will increase the weightings of the 2 year and reduce the weighting in the 10 year maturity Treasury Instruments. Conversely, Sit will do the opposite if the Federal Reserve began raising long term interest rates more than short term interest rates. Reconstitution, rebalancing, or both, each will occur monthly as discussed above or if there are radical changes in the yield curve such that effective duration is outside of a range from negative nine to negative 11-year average effective duration, in which case Sit will adjust the maturities of the Treasury Instruments before the next expected monthly reconstitution.

The Sponsor anticipates that approximately 5% to 15% of RISE’s assets will be used as payment for or collateral for Treasury Instruments. RISE will post margin from such assets to its futures commission merchant (“FCM”), SG Americas Securities, LLC (“SGAS”), in an amount equal to the margin required by the relevant exchange, and transfer to its FCM any additional amounts that may be separately required by the FCM. When establishing positions in Treasury Instruments, RISE will be required to deposit initial margin with a value of approximately 3% to 10% of the value of each Treasury Instrument position at the time it is established. These margin requirements are subject to change from time to time by the exchange or the FCM. On a daily basis, RISE will be obligated to pay, or entitled to receive, variation margin in an amount equal to the change in the daily settlement level of its Treasury Instruments positions. Any assets not required to be posted as margin with RISE’s FCM will be held at RISE’s custodian in cash or cash equivalents.

The RISE Benchmark Portfolio will consist of the RISE Benchmark Component Instruments and rebalanced, reconstituted, or both to maintain a negative average effective portfolio duration of approximately 10 years. Duration is a measure of estimated price sensitivity relative to changes in interest rates. Portfolios with longer durations are typically more sensitive to changes in interest rates. For example, if interest rates rise by 1%, the market value of a security with an effective duration of 5 years would decrease by 5%, with all other factors being constant, and likewise, if interest rates decline by 1%, the market value of a security with an effective duration of negative 5 years would increase by 5%, with all other factors being constant. Duration estimates are based on assumptions by Sit and are subject to a number of limitations. Duration is a more accurate estimate of price sensitivity provided interest rate changes are small and occur equally in short-term and long-term securities. Investments in debt securities typically decrease in value when interest rates rise. The risk of a decrease in value is usually greater for longer-term debt securities.

2

RISE will incur certain expenses in connection with its operations. RISE will hold cash or cash equivalents such as U.S. Treasuries or other high credit quality, short-term fixed-income or similar securities for direct investment or as collateral for the Treasury Instruments and for other liquidity purposes and to meet redemptions that may be necessary on an ongoing basis. These expenses and income from the cash and cash equivalent holdings may cause imperfect correlation between changes in RISE’s net asset value (“NAV”) and changes in the RISE Benchmark Portfolio, because the RISE Benchmark Portfolio does not reflect expenses or income.

Sit expects that it will generally seek to close out its positions in Treasury futures contracts prior to such contracts maturing and enter into new positions in Treasury futures contracts. In connection with this process, natural market forces may affect RISE’s NAV positively or negatively. This is because each time RISE seeks to rebalance or reconstitute its positions, even absent movement in the underlying Treasury Instruments, the prices of new futures and option prices may be higher or lower than the prices of those that were closed out. Such differences in price, barring a movement in the price of the underlying security, will constitute “roll yield” and may inhibit RISE’s ability to achieve its investment objective.

Several factors may determine the total return from investing in a futures contract position. One factor that impacts the total return, which will result from investing in near month futures contracts and “rolling” those contracts forward each month, is the price relationship between the current near month contract and the next month contract. Among other such factors, when RISE purchases an option that expires “out of the money,” RISE will realize a loss. Additionally, RISE may not be able to invest its assets in futures and options contracts having an aggregate notional amount exactly equal to that which is required to achieve a negative 10 year average effective duration. For example, as standardized contracts, Treasury futures contracts are denominated in specific dollar amounts, and RISE’s NAV and the proceeds from the sale of a creation basket (a “Creation Basket”) are unlikely to be an exact multiple of the amounts of those contracts. As a result, in such circumstances, RISE may be better able to achieve the exact amount of exposure desired through the use of other investments.

Sit will close existing positions when it determines it would be appropriate to do so and reinvest the proceeds in other positions. Positions may also be closed out to meet orders for a redemption basket (a “Redemption Basket”).

RISE Benchmark Portfolio

The RISE Benchmark Portfolio is maintained by Sit and will be rebalanced, reconstituted, or both, monthly (typically on the 15th of each month or on the next business day if the 15th is a holiday, weekend, or other day on which the national exchanges are closed) to maintain a negative 10 year average effective duration. The RISE Benchmark Portfolio and RISE will each maintain a short position in Treasury Instruments. RISE does not use futures contracts or options to obtain leveraged investment results. The RISE Benchmark Component Instruments currently constituting the RISE Benchmark Portfolio as of June 30, 2018 include:

| Name | Ticker | Market Value (USD) | ||||

| UNITED STATES TREASURY BILLS | 912796QB8 | $ | 50,447,201 | |||

| U.S. 5 YR FUTR OPTN AUG 18 C $113.50 | FVQ8C 113.50 | (70,664 | ) | |||

| U.S. 5 YR NOTE (CBT) SEP 18 | FVU8 | (53,400,078 | ) | |||

| U.S. 2 YR NOTE (CBT) SEP 18 | TUU8 | (98,711,907 | ) | |||

| U.S. 10 YR FUT OPTN AUG 18 P $120.00 | TYQ8P 120 | 53,547 | ||||

The RISE Benchmark Component Instruments currently constituting the RISE Benchmark Portfolio and anticipated rebalancing dates, as well as the daily holdings of RISE, are available on RISE’s website at www.risingrateetf.com.

3

RISE Trading Policies

Liquidity

RISE invests principally in exchange traded futures and options on futures on U.S. Treasuries that, in the opinion of the Sponsor, are traded in sufficient volume to permit the ready taking of orders and liquidation of positions in these financial instruments.

Borrowings

Borrowings are not undertaken by RISE.

Breakwave Dry Bulk Shipping ETF

BDRY Investment Objective

BDRY’s investment objective is to provide investors with exposure to the daily change in the price of dry bulk freight futures by tracking the performance of a portfolio (the “BDRY Benchmark Portfolio” and, collectively with the RISE Benchmark Portfolio, the “Benchmark Portfolios”) consisting of exchange-cleared futures contracts on the cost of shipping dry bulk freight (“Freight Futures”). BDRY seeks to achieve its investment objective by investing substantially all of its assets in the Freight Futures currently constituting the BDRY Benchmark Portfolio.

The BDRY Benchmark Portfolio is maintained by Breakwave Advisors LLC (“Breakwave”), which also serves as BDRY’s CTA. The BDRY Benchmark Portfolio is maintained by Breakwave and will be rebalanced annually.

BDRY Commodity Trading Advisor

Breakwave serves as BDRY’s CTA. Breakwave is a Delaware limited liability company.

Breakwave is registered as a CTA with the CFTC and is a member of the NFA.

Breakwave provides its services to BDRY under a Services Agreement with the Sponsor. Under this agreement, Breakwave has agreed to compose and maintain the BDRY Benchmark Portfolio and license to the Sponsor the use of the BDRY Benchmark Portfolio.

BDRY Investing Strategy

BDRY seeks to achieve its investment objective by investing substantially all of its assets in the Freight Futures currently constituting the BDRY Benchmark Portfolio. The BDRY Benchmark Portfolio will include all existing positions to maturity and settle them in cash. During any given calendar quarter, the BDRY Benchmark Portfolio will progressively increase its position to the next calendar quarter three-month strip, thus maintaining constant exposure to the Freight Futures market as positions mature.

The BDRY Benchmark Portfolio will maintain long-only positions in Freight Futures. The BDRY Benchmark Portfolio will include a combination of Capesize, Panamax and Supramax Freight Futures. More specifically, the BDRY Benchmark Portfolio will include 50% exposure in Capesize Freight Futures contracts, 40% exposure in Panamax Freight Futures contracts and 10% exposure in Supramax Freight Futures contracts. The BDRY Benchmark Portfolio will not include and BDRY will not invest in swaps, non-cleared dry bulk freight forwards or other over-the-counter derivative instruments that are not cleared through exchanges or clearing houses. BDRY may hold exchange-traded options on Freight Futures. The BDRY Benchmark Portfolio is maintained by Breakwave and will be rebalanced annually. The Freight Futures currently constituting the BDRY Benchmark Portfolio, as well as the daily holdings of BDRY will be available on BDRY’s website at www.drybulketf.com.

4

When establishing positions in Freight Futures, BDRY will be required to deposit initial margin with a value of approximately 10% to 40% of the notional value of each Freight Futures position at the time it is established. These margin requirements are established and subject to change from time to time by the relevant exchanges, clearing houses or BDRY’s FCM. On a daily basis, BDRY will be obligated to pay, or entitled to receive, variation margin in an amount equal to the change in the daily settlement level of its Freight Futures positions. Any assets not required to be posted as margin with BDRY’s FCM will be held at BDRY’s custodian in cash or cash equivalents, as discussed below.

BDRY will hold cash or cash equivalents such as U.S. Treasuries or other high credit quality, short-term fixed-income or similar securities for direct investment or as collateral for the U.S. Treasuries and for other liquidity purposes and to meet redemptions that may be necessary on an ongoing basis. BDRY may also realize interest income from its holdings in U.S. Treasuries or other market rate instruments.

BDRY Benchmark Portfolio

The BDRY Benchmark Portfolio is maintained by Breakwave, which also serves as BDRY’s CTA. The BDRY Benchmark Portfolio consists of the Freight Futures, which are a three-month strip of the nearest calendar quarter of futures contracts on specified indexes (each a “Reference Index”) that measure rates for shipping dry bulk freight. Each Reference Index is published each United Kingdom business day by the London-based Baltic Exchange Ltd. (the “Baltic Exchange”) and measures the charter rate for shipping dry bulk freight in a specific size category of cargo ship – Capesize, Panamax or Supramax. The three Reference Indexes are as follows:

| ● | Capesize: the Capesize 5TC Index; |

| ● | Panamax: the Panamax 4TC Index; and |

| ● | Supramax: the Supramax 6TC Index. |

The Freight Futures currently constituting the BDRY Benchmark Portfolio as of June 30, 2018 include:

| Name | Ticker | Market Value USD | ||||

| BALTIC EXCHANGE PANAMAX T/C AVERAGE SHIPPING ROUTE INDEX - JUL 18 | BFFAP N18 Index | $ | 348,300 | |||

| BALTIC EXCHANGE PANAMAX T/C AVERAGE SHIPPING ROUTE INDEX - AUG 18 | BFFAP Q18 Index | 368,250 | ||||

| BALTIC EXCHANGE PANAMAX T/C AVERAGE SHIPPING ROUTE INDEX - SEP 18 | BFFAP U18 Index | 390,600 | ||||

| BALTIC EXCHANGE SUPRAMAX T/C AVERAGE SHIPPING ROUTE - JUL 18 | BFFAS N18 Index | 114,210 | ||||

| BALTIC EXCHANGE SUPRAMAX T/C AVERAGE SHIPPING ROUTE - AUG 18 | BFFAS Q18 Index | 117,760 | ||||

| BALTIC EXCHANGE SUPRAMAX T/C AVERAGE SHIPPING ROUTE - SEP 18 | BFFAS U18 Index | 120,160 | ||||

| BALTIC CAPESIZE TIME CHARTER - JUL 18 | BFFATC N18 Index | 543,300 | ||||

| BALTIC CAPESIZE TIME CHARTER - AUG 18 | BFFATC Q18 Index | 561,300 | ||||

| BALTIC CAPESIZE TIME CHARTER - SEP 18 | BFFATC U18 Index | 642,300 | ||||

The value of the Capesize 5TC Index is disseminated at 11:00 a.m., London Time and the value of the Panamax 4TC Index and the Supramax 6TC Index each is disseminated at 1:00 p.m., London Time. The Reference Index information disseminated by the Baltic Exchange also includes the components and value of each component in each Reference Index. Such Reference Index information also is widely disseminated by Reuters and/or other major market data vendors.

BDRY Trading Policies

Liquidity

BDRY invests principally in exchange cleared futures that, in the opinion of the Sponsor, are traded in sufficient volume to permit the ready taking of orders in these financial interests.

Leverage

The Sponsor endeavors to have the value of the Fund’s Treasury Securities, cash and cash equivalents, whether held by the Fund or posted as margin or collateral, at all times approximate the aggregate market value of its obligations under the Fund’s Freight Futures interests, adjusted for the proportion of the current month’s Freight Futures contracts whose value has already been assessed.

5

Borrowings

BDRY does not intend to or foresee the need to borrow money or establish lines of credit.

Pyramiding

BDRY does not and will not employ the technique, commonly known as pyramiding, in which the speculator uses unrealized profits on existing positions as variation margin for the purchase of additional positions in the same commodity interest.

No Distributions

The Sponsor has discretionary authority over all distributions made by BDRY. In view of BDRY’s objective of seeking significant capital appreciation, the Sponsor currently does not intend to make any distributions, but, has the sole discretion to do so from time to time.

Margin Requirements and Marking-to-Market Futures Positions

“Initial margin” is an amount of funds that must be deposited by a commodity trader with the trader’s broker to initiate an open position in futures contracts. A margin deposit is like a cash performance bond. It helps assure the trader’s performance of the futures contracts that he or she purchases or sells. Futures contracts are customarily bought and sold on initial margin that represents a small percentage of the aggregate purchase or sales price of the contract. The amount of margin required in connection with a particular futures contract is set by the exchange on which the contract is traded. Brokerage firms, such as BDRY’s clearing broker, carrying accounts for traders in commodity interest contracts may require higher amounts of margin as a matter of policy to further protect themselves.

Futures contracts are marked to market at the end of each trading day and the margin required with respect to such contracts is adjusted accordingly. This process of marking-to-market is designed to prevent losses from accumulating in any futures account. Therefore, if BDRY’s futures positions have declined in value, BDRY may be required to post “variation margin” to cover this decline. Alternatively, if BDRY’s futures positions have increased in value, this increase will be credited to BDRY’s account.

Futures Contracts

The Funds enter into futures contracts to gain exposure to changes in the value of the Benchmark Portfolios. A futures contract obligates the seller to deliver (and the purchaser to accept) the future cash settlement of a specified quantity and type of a treasury futures contract at a specified time and place. The contractual obligations of a buyer or seller of a treasury futures contract may generally be satisfied by making an offsetting sale or purchase of an identical futures contract on the same or linked exchange before the designated date of delivery.

Upon entering into a futures contract, the Funds are each required to deposit and maintain as collateral at least such initial margin as required by the exchange on which the transaction is affected. The initial margin is segregated as cash held by broker, as disclosed in the Combined Statements of Assets and Liabilities, and is restricted as to its use. Pursuant to the futures contract, the Funds each agree to receive from or pay to the broker an amount of cash equal to the daily fluctuation in value of the futures contract. Such receipts or payments are known as variation margin and are recorded by the Funds as unrealized gains or losses. The Funds will realize a gain or loss upon closing a futures transaction.

Futures contracts involve, to varying degrees, elements of market risk (specifically treasury price risk) and exposure to loss in excess of the amount of variation margin. The face or contract amounts reflect the extent of the total exposure the Funds have in the particular classes of instruments. Additional risks associated with the use of futures contracts include imperfect correlation between movements in the price of the futures contracts and the market value of the underlying securities and the possibility of an illiquid market for a futures contract. With futures contracts, there is minimal counterparty risk to the Funds since futures contracts are exchange-traded and the exchange’s clearinghouse, as counterparty to all exchange-traded futures contracts, guarantees the futures contracts against default.

6

The Funds’ Service Providers

Administrator, Custodian, Fund Accountant, and Transfer Agent

The Funds have each appointed U.S. Bank, a national banking association, with its principal office in Milwaukee, Wisconsin, as the custodian (the “Custodian”). Its affiliate, U.S. Bancorp Fund Services, is the Fund accountant (the “Fund Accountant”) of the Funds, transfer agent (the “Transfer Agent”) for the Funds’ shares and administrator for the Funds (the “Administrator”). It performs certain administrative and accounting services for the Funds and prepares certain SEC, NFA and CFTC reports on behalf of the Funds. (U.S. Bank and U.S. Bancorp Fund Services are referred to collectively hereinafter as “U.S. Bank”).

Distributor

Effective April 1, 2017, ETFMG Financial LLC, a wholly-owned subsidiary of ETFMG (the “Distributor”), provides statutory and wholesaling distribution services to RISE. The Distributor has provided statutory and wholesaling distribution services to BDRY since it commenced trading on NYSE Arca on March 22, 2018.

The Funds pay the Distributor an annual fee for statutory and wholesaling distribution services and related administrative services equal to the greater of $15,000 or 0.02% of the Funds’ average daily net assets, payable monthly. Pursuant to the respective Marketing Agent Agreement between the Sponsor, each Fund and the Distributor, the Distributor assists the Sponsor and the applicable Fund with certain functions and duties relating to distribution and marketing services to the applicable Fund, including reviewing and approving marketing materials and certain regulatory compliance matters. The Distributor also assists with the processing of creation and redemption orders.

ALPS Distributors, Inc. (“ALPS”) provided statutory and wholesaling distribution services to RISE from December 1, 2015 through March 31, 2017. RISE paid an annual fee for such distribution services and related administrative services equal to $15,000 plus 0.02% of RISE’s average daily net assets, payable monthly. This fee had two components, with a portion of the fee paid to ALPS for the statutory distribution services and a portion paid to the Sponsor for the related administrative services. Pursuant to the Marketing Agent Agreement between the Sponsor, RISE and ALPS, the former distributor assisted the Sponsor and RISE with certain functions and duties relating to distribution and marketing services to RISE, including reviewing and approving marketing materials and certain regulatory compliance matters. ALPS also assisted with the processing of creation and redemption orders.

In no event will the aggregate compensation paid to the Distributor and any affiliate of the Sponsor for distribution-related services in connection with the offering of shares exceed ten percent (10%) of the gross proceeds of the offering. The Distributor’s principal business address is 30 Maple Street, Suite 2, Summit, New Jersey, 07901.

Trustee

Under the respective Amended and Restated Declaration of Trust and Trust Agreement (each, a “Trust Agreement”) for each Fund, Wilmington Trust Company, the Trustee of each of the Funds (the “Trustee”) serves as the sole trustee of each Fund in the State of Delaware. The Trustee will accept service of legal process on the Funds in the State of Delaware and will make certain filings under the Delaware Statutory Trust Act. Under the respective Trust Agreement for each Fund, the Sponsor has the exclusive management and control of all aspects of the business of the Fund. The Trustee does not owe any other duties to the Funds, the Sponsor or the Shareholders of the Funds. The Trustee has no duty or liability to supervise or monitor the performance of the Sponsor, nor does the Trustee have any liability for the acts or omissions of the Sponsor.

7

RISE Futures Commission Merchant

SG Americas Securities, LLC, a Delaware limited liability company, serves as RISE’s clearing broker to execute and clear RISE’s futures and options transactions and provide other brokerage-related services. SGAS is an FCM and broker dealer registered with the CFTC and the U.S. Securities and Exchange Commission (the “SEC”), and is a member of the Financial Industry Regulatory Authority (“FINRA”). SGAS is a clearing member of all principal futures exchanges located in the United States as well as a member of the Chicago Board Options Exchange, International Securities Exchange, New York Stock Exchange, Options Clearing Corporation, and Government Securities Clearing Corporation. RISE has estimated that it will pay 0.09% of RISE’s NAV in brokerage fees for execution and clearing services on behalf of RISE.

SGAS is headquartered at 245 Park Avenue, New York, NY 10167 with a branch office in Chicago and, as securities only branches, in Houston, Boston and Dallas.

On January 2, 2015, Newedge USA, LLC (“Newedge USA”) merged with and into SGAS, with the latter as the surviving entity.

In February 2015, SGAS, as successor to Newedge USA, settled, without admitting or denying the allegations, a matter brought by the CME Group alleging that on multiple occasions between 2010 and 2012, Newedge USA employees executed certain customers’ orders as EFRPs, instead of on CME Group’s GLOBEX platform. The settlement also included allegations that the subject EFRPs were non bona fide and/or inadequately documented. In connection with this matter, SGAS paid a fine of $1,100,000 to Comex and $650,000 to NYMEX.

In October 2015, SGAS, as successor to Newedge USA, settled, without admitting or denying the allegations, a matter brought by ICE Futures U.S. that was based on alleged failures by Newedge USA to report an open interest in three energy futures contracts in accordance with the rules of the exchange over a period of approximately twenty-two business days in May and June 2014. In connection with the settlement of this matter, SGAS paid a $100,000 fine.

Beginning in late 2013, the SEC reviewed transactions by SGAS’s Non-Agency Mortgage Desk in which SGAS bought baskets of securities from a counterparty and sold the securities back to the same counterparty, and also reviewed communications with counterparties regarding certain riskless principal trades. The SEC reviewed transactions that occurred between approximately December 2011 and June 2013. SGAS cooperated with the investigation and disciplined the trader involved and her supervisor. In December 2015, SGAS paid $1,011,093 to settle the matter, consisting of a $800,000 fine and $211,093 in disgorgement including interest.

In June 2016, SGAS, as successor to Newedge USA, settled, without admitting or denying the allegations, a matter brought by the Chicago Board of Trade alleging that on six days between November 2013 and January 2014, three traders for Newedge (one employed by Newedge and two by its Canadian affiliate) entered into separate transactions with third parties prior to consummating the block trade with the counterparty in violation of CBOT Rules 432.W. and 526. The settlement included a fine in the amount of $100,000 and a disgorgement of profits in the amount of $19,502.50.

8

In September 2016, SGAS, as successor to Newedge USA, settled, without admitting or denying the allegations, a matter brought by the CFTC alleging Newedge USA violated Section 4C(A) of the CEA and Regulations 1.38 and 166.3 by executing and confirming numerous exchange for physical transactions in agricultural and soft commodities for and on behalf of its clients that were for the same contract, quantity and same or similar price with the buyer and seller for each transaction under the same common control and ownership. The settlement includes a $750,000 civil penalty and an undertaking to implement policies, procedures and training programs reasonably designed to prevent the execution, clearing and reporting to an exchange of non-bona fide exchange of futures for physical transactions.

In April 2017, SGAS settled, without admitting or denying the allegations, a matter brought by the Chicago Board of Options Exchange and NYSE ARCA, Inc. for failing to report, or accurately report, “reportable positions” on its large option position report in violation of Exchange Rules 4.2 and 4.13. In connection with this matter, SGAS paid a fine of $100,000 to each of the Chicago Board of Options Exchange and NYSE ARCA, Inc.

In April 2017, SGAS, as successor to Newedge USA settled, without admitting or denying the findings, a matter brought by FINRA for failing to establish and maintain a supervisory system reasonably designed to ensure that customers were sent account statements, notified of availability of statements on its customer portal, agreed to receive statements and confirmations electronically, and were sent confirmations which contained all of the required information. The settlement included payment of a fine in the amount of $100,000.

In July 2017, SGAS settled, without admitting or denying the findings, a matter with the CME Group where the CME alleged SGAS violated CME Rules 9.70.A., 971.A.2.A., B. and C., 980.A. and 980.B.1 and 2. The settlement related to two separate CME exam findings: 1) balances were not consistently identifiable in the general ledger and 2) procedures for resolving the general ledger suspense balances were not sufficient. In connection with this matter, SGAS paid a fine of $150,000.

In January 2018, SGAS, without admitting or denying the findings, settled a matter with FINRA in which FINRA alleged SGAS failed to meet certain FINRA trade reporting requirements and also disclosed the incorrect capacity on certain customer confirmations, in violation of various FINRA and NASD rules. In connection with this matter, SGAS paid a fine of $200,000 and also undertook to re-report certain trades, pay associated transaction fees not previously paid due to the reporting issues, and revise certain of its written supervisory procedures.

Other than the foregoing proceedings, which did not have a material adverse effect upon the financial condition of SGAS, there have been no material administrative, civil or criminal actions brought, pending or concluded against SGAS or its principals in the past five years.

Neither SGAS nor any affiliate, officer, director or employee thereof has passed on the merits of the Prospectus or offering, or given any guarantee as to the performance or any other aspect of the Trust or RISE.

SGAS is not affiliated with RISE or the Sponsor. Therefore, the Sponsor and RISE do not believe that RISE has any conflicts of interest with SGAS or its trading principals arising from their acting as RISE’s FCM.

BDRY Futures Commission Merchant

Macquarie Futures USA LLC (“Macquarie”) serves as BDRY’s broker clearing broker to execute and clear BDRY’s futures and options transactions and provide other brokerage-related services. Macquarie is an FCM registered with the CFTC. BDRY has estimated that it will pay 0.40% of BDRY’s NAV in brokerage fees for execution and clearing services on behalf of BDRY.

Macquarie’s head office is at 125 West 55th Street, New York, NY 10019.

There have been no material administrative, civil or criminal actions brought, pending or concluded against Macquarie or its principals in the past five years.

Neither Macquarie nor any affiliate, officer, director or employee thereof have passed on the merits of this prospectus or offering, or give any guarantee as to the performance or any other aspect of BDRY.

Macquarie is not affiliated with either BDRY or the Sponsor. Therefore, the Sponsor and BDRY do not believe that BDRY has any conflicts of interest with Macquarie or its trading principals arising from their acting as BDRY’s FCM.

Legal Counsel

Sullivan & Worcester LLP serves as legal counsel to the Trust and the Funds.

9

Fees of the Funds

Management and CTA Fees

RISE and BDRY each pay the Sponsor a management fee (the “Sponsor Fee”) in consideration of the Sponsor’s advisory services to the Funds. Additionally, RISE and BDRY each pays its respective commodity trading advisor a license and service fee (the “CTA Fee”).

RISE pays the Sponsor Fee monthly in arrears, in an amount equal to the greater of 0.15% per annum of the value of RISE’s average daily net assets or $75,000 effective January 1, 2018. The Sponsor Fee is paid in consideration of the Sponsor’s management services to RISE. RISE also pays Sit a CTA Fee monthly in arrears, for the use of the RISE Benchmark Portfolio in an amount equal to 0.20% effective January 1, 2018 (0.50% prior to January 1, 2018) per annum of RISE’s average daily net assets. Prior to January 1, 2018, RISE’s Sponsor Fee was calculated as the greater of 0.15% per annum of the value of RISE’s average daily net assets or, $18,750 for the year ended December 31, 2017, $75,000 for the period from February 20, 2016 through December 31, 2016 and $56,350 prior to February 20, 2016.

As of January 1, 2018, the Sponsor has contractually agreed to waive RISE’s Sponsor Fee and/or assume RISE’s remaining expenses so that RISE’s expenses do not exceed an annual rate of 1.00%, excluding brokerage commissions, interest expense, and extraordinary expenses, of the value of RISE’s average daily net assets (the “RISE Expense Cap”). The assumption of expenses and waiver of RISE’s Sponsor fee are contractual on the part of the Sponsor, through September 30, 2019. If after that date, the Sponsor no longer assumed expenses or waived RISE’s Sponsor Fee, RISE could be adversely impacted, including in its ability to achieve its investment objective.

For the period from the inception of RISE through December 31, 2017, Sit had agreed to waive the CTA Fee and the Sponsor agreed to correspondingly assume the remaining expenses of RISE so that RISE expenses did not exceed an annual rate of 1.50%, excluding brokerage commissions, interest expense, and extraordinary expenses, of the value of RISE’s average daily net assets.

The waiver of RISE’s Sponsor Fee, pursuant to the contractual RISE Expense Cap, amounted to $24,657 and $-0- for the years ended June 30, 2018 and 2017, respectively. The waiver of RISE’s CTA fee amounted to $49,453 and $71,035 for the years ended June 30, 2018 and 2017, respectively. RISE currently accrues its daily expenses up to the RISE Expense Cap. At the end of each month, the accrued amount is remitted to the Sponsor as the Sponsor is responsible for the payment of the routine operational, administrative and other ordinary expenses of RISE. RISE’s total expenses amounted to $606,334 and $542,088, for the years ended June 30, 2018 and 2017, respectively, of which $87,625 and $230,689, respectively, was absorbed by the Sponsor pursuant to the RISE Expense Cap.

BDRY pays the Sponsor Fee, monthly in arrears, in an amount equal to the greater of 0.15% per year of BDRY’s average daily net assets; or $125,000. BDRY’s Sponsor Fee is paid in consideration of the Sponsor’s management services to BDRY. BDRY also pays Breakwave the CTA Fee monthly in arrears, for the use of BDRY’s Benchmark Portfolio in an amount equal to 1.45% per annum of BDRY’s average daily net assets.

Breakwave has agreed to waive its CTA Fee and the Sponsor has agreed to correspondingly assume the remaining expenses of BDRY so that BDRY’s expenses do not exceed an annual rate of 3.50%, excluding brokerage commissions, interest expense, and extraordinary expenses, of the value of BDRY’s average daily net assets (the “BDRY Expense Cap”). The assumption of expenses and waiver of BDRY’s CTA Fee are contractual on the part of the Sponsor and Breakwave, respectively, through September 30, 2019. If after that date, the Sponsor and/or Breakwave no longer assumed expenses or waived the CTA Fee, respectively, BDRY could be adversely impacted, including in its ability to achieve its investment objective.

The assumption of expenses by the Sponsor for BDRY, pursuant to the BDRY Expense Cap, amounted to $165,676 for the period from March 22, 2018 to June 30, 2018, as disclosed in the Combined Statements of Operations. The waiver of Breakwave’s CTA fees, pursuant to the undertaking, amounted to $14,567 for the period from March 22, 2018 to June 30, 2018, as disclosed in the Combined Statements of Operations. BDRY currently accrues its daily expenses up to the BDRY Expense Cap. At the end of each month, the accrued amount is remitted to the Sponsor as the Sponsor is responsible for the payment of the routine operational, administrative and other ordinary expenses of the Fund. BDRY’s total expenses amounted to $231,538 for the period from March 22, 2018 to June 30, 2018.

10

Administrator, Custodian, Fund Accountant, and Transfer Agent Fees

RISE has agreed to pay U.S. Bank 0.05% of assets under management (“AUM”), with a $50,000 minimum annual fee payable for its administrative, accounting and transfer agent services and 0.01% of AUM, with an annual minimum of $4,800 for custody services.

Effective March 22, 2018, BDRY has agreed to pay U.S. Bank 0.05% of AUM, with a $55,000 minimum annual fee payable for its administrative, accounting and transfer agent services and 0.01% of AUM, with an annual minimum of $4,800 for custody services.

Distribution Fees

RISE and BDRY each pay the Distributor an annual fee for statutory and wholesaling distribution services and related administrative services equal to the greater of $15,000 or 0.02% of RISE and BDRY’s, respectively, average daily net assets, payable monthly. Pursuant to the applicable Marketing Agent Agreement between the Sponsor, each Fund and the Distributor, the Distributor assists the Sponsor and the applicable Fund with certain functions and duties relating to distribution and marketing services to the applicable Fund, including reviewing and approving marketing materials and certain regulatory compliance matters. The Distributor also assists with the processing of creation and redemption orders.

ALPS provided statutory and wholesaling distribution services to RISE from December 1, 2015 through March 31, 2017. RISE paid an annual fee for such distribution services and related administrative services equal to $15,000 plus 0.02% of RISE’s average daily net assets, payable monthly. This fee had two components, with a portion of the fee paid to ALPS for the statutory distribution services and a portion paid to the Sponsor for the related administrative services. Pursuant to the Marketing Agent Agreement between the Sponsor, RISE and the ALPS, the former distributor assisted the Sponsor and RISE with certain functions and duties relating to distribution and marketing services to RISE, including reviewing and approving marketing materials and certain regulatory compliance matters. ALPS also assisted with the processing of creation and redemption orders.

RISE incurred $17,494 and $17,605 in distribution and related administrative services for the year ended June 30, 2018 and 2017, respectively. BDRY incurred $4,520 in distribution and related administrative services for the period from March 22, 2018 to June 30, 2018, as disclosed in the Combined Statements of Operations.

RISE also pays the Sponsor an annual fee for wholesale support services equal to 0.1% of RISE’s average daily net assets, payable monthly. BDRY pays the Sponsor for wholesale support services $25,000 plus 0.12% of BDRY’s average daily net assets, payable monthly.

RISE incurred $33,720 and $14,202 in wholesale support fees for the year ended June 30, 2018 and 2017, respectively. BDRY incurred $9,680 in wholesale support fees for the period from March 22, 2018 to June 30, 2018, as disclosed in the Combined Statements of Operations.

Futures Commission Merchant Fees

RISE and BDRY each pay respective brokerage commissions, including applicable exchange fees, NFA fees, give–up fees, pit brokerage fees and other transaction related fees and expenses charged in connection with trading activities in CFTC regulated investments. Brokerage commissions on futures contracts are recognized on a half-turn basis.

The Sponsor does not expect brokerage commissions and fees to exceed 0.09% for RISE, and 0.40% for BDRY, of the NAV of the applicable Fund for execution and clearing services on behalf of the applicable Fund, although the actual amount of brokerage commissions and fees in any year or any part of any year may be greater. The effects of trading spreads, financing costs associated with financial instruments, and costs relating to the purchase of Treasury Instruments or similar high credit quality short-term fixed-income or similar securities are not included in the foregoing analysis. RISE incurred $42,798 and $27,257 in brokerage commissions and fees for the year ended June 30, 2018 and 2017, respectively, as disclosed in the Combined Statements of Operations. BDRY incurred $16,135 in brokerage commissions and fees for the period from March 22, 2018 to June 30, 2018, as disclosed in the Combined Statements of Operations.

11

Other Fees

RISE and BDRY each are responsible for certain other expenses, including professional services (e.g., outside auditor’s fees and legal fees and expenses), shareholder Form K-1’s, tax return preparation, regulatory compliance, and other services provided by affiliated and non-affiliated service providers. The fees for Principal Financial Officer and Chief Compliance Officer services provided to the Funds by the Sponsor amount to $25,000 per annum. Certain additional fees paid to the Sponsor by the Funds for tax return preparation and regulatory reporting fees amount to $100,000 and $25,000, respectively, per annum.

Extraordinary fees

RISE and BDRY each pay all of their extraordinary fees and expenses, if any. Extraordinary fees and expenses are fees and expenses which are non-recurring and unusual in nature, such as legal claims and liabilities, litigation costs or indemnification or other unanticipated expenses. Extraordinary fees and expenses are fees and expenses which are nonrecurring and unusual in nature, such as legal claims and liabilities, litigation costs or indemnification or other unanticipated expenses. Such extraordinary fees and expenses, by their nature, are unpredictable in terms of timing and amount.

Form of Shares

Registered Form

Shares of the Funds are issued in registered form in accordance with the respective Trust Agreement for each Fund. U.S. Bank has been appointed registrar and transfer agent for the purpose of transferring shares in certificated form. U.S. Bank keeps a record of all limited partners and holders of the shares in certificated form in the registry (the “Register”). The Sponsor recognizes transfers of shares in certificated form only if done in accordance with the respective Trust Agreement for each Fund. The beneficial interests in such shares are held in book-entry form through participants and/or accountholders in the Depository Trust Company (“DTC”).

Book Entry

Individual certificates are not issued for the shares. Instead, shares are represented by one or more global certificates, which are deposited by the Administrator with, or on behalf of, DTC and registered in the name of Cede & Co., as nominee for DTC. The global certificates evidence all of the shares outstanding at any time. Shareholders are limited to (1) participants in DTC such as banks, brokers, dealers and trust companies (“DTC Participants”), (2) banks, brokers, dealers and trust companies who maintain, either directly or indirectly, a custodial relationship with, or clear through, a DTC Participant (“Indirect Participants”), and (3) persons holding interests in the shares through DTC Participants or Indirect Participants, in each case who satisfy the requirements for transfers of shares.

Shareholders will be shown on, and the transfer of Shares will be effected only through, in the case of DTC Participants, the records maintained by the Depository and, in the case of Indirect Participants and Shareholders holding through a DTC Participant or an Indirect participant, through those records or the records of the relevant DTC Participants or Indirect participants. Shareholders are expected to receive, from or through which the Shareholder has purchased Shares, a written confirmation relating to their purchase of Shares.

DTC

DTC is a limited purpose trust company organized under the laws of the State of New York and is a member of the Federal Reserve System, a “clearing corporation” within the meaning of the New York Uniform Commercial Code and a “clearing agency” registered pursuant to the provisions of Section 17A of the Exchange Act. DTC holds securities for DTC Participants and facilitates the clearance and settlement of transactions between DTC Participants through electronic book-entry changes in accounts of DTC Participants.

12

Calculating NAV

Each of the Funds’ NAV is calculated by:

| ● | Taking the current market value of its total assets; |

| ● | Subtracting any liabilities; and |

| ● | Dividing that total by the total number of outstanding shares. |

The Administrator calculates the NAV of the Funds once each NYSE Arca trading day. The NAV for a particular trading day is released after 4:00 p.m. E.T. Regular trading on the NYSE Arca typically closes at 4:00 p.m. E.T. In the case of RISE, the Administrator uses the CME closing price (determined at the earlier of the close of the CME or 2:30 p.m. E.T.) for the contracts traded on the CME. In the case of BDRY, the Administrator uses the Baltic Exchange settlement price for the Freight Futures and option contracts. The Administrator calculates or determines the value of all other RISE and BDRY investments using market quotations, if available, or other information customarily used to determine the fair value of such investments as of the earlier of the close of the NYSE Arca, in the case of RISE, and as of the close of the NYSE Arca (typically 4:00 p.m. E.T.), in the case of BDRY, in accordance with the current applicable Administrative Agency Agreement among U.S. Bancorp Fund Services, the Sponsor and RISE or BDRY, respectively. For purposes of calculating the NAV of RISE, “other information” customarily used in determining fair value includes information consisting of market data in the relevant market supplied by one or more third parties including, without limitation, relevant rates, prices, yields, yield curves, volatilities, spreads, correlations or other market data in the relevant market; or information of the types described above from internal sources if that information is of the same type used by RISE in the regular course of its business for the valuation of similar transactions. The information may include costs of funding, to the extent costs of funding are not and would not be a component of the other information being utilized. Third parties supplying quotations or market data may include, without limitation, dealers in the relevant markets, end-users of the relevant product, information vendors, brokers and other sources of market information.

In addition, in order to provide updated information relating to the Funds for use by investors and market professionals, an updated indicative fund value (“IFV”) is made available through on-line information services throughout the trading hours of 9:30 a.m. E.T. to 4:00 p.m. E.T. on each trading day. In the case of RISE, IFV is calculated by using the prior day’s closing NAV per share of RISE as a base and updating that value throughout the trading day to reflect changes in the most recently reported trade price for the futures and options held by RISE traded on the CME. In the case of BDRY, the IFV is calculated by using the prior day’s closing NAV per share of BDRY as a base and updating that value throughout the trading day to reflect changes in the most recently reported trade price for the futures and/or options held by BDRY. Certain Freight Futures brokers provide real time pricing information to the general public either through their websites or through data vendors such as Bloomberg or Reuters. The IFV disseminated during NYSE Arca regular trading hours should not be viewed as an actual real time update of the NAV, because the NAV is calculated only once at the end of each trading day based upon the relevant end of day values of the Funds’ investments.

The IFV is disseminated on a per share basis every 15 seconds during NYSE Arca regular trading hours. The normal trading hours of the CME are 10:00 a.m. E.T. to 2:30 p.m. E.T. The customary trading hours of the Freight Futures trading are 3:00 a.m. E.T. to 12:00 p.m. E.T. This means that there is a gap in time at the beginning and/or the end of each day during which a Fund’s shares are traded on the NYSE Arca, but real-time trading prices for contracts are not available. During such gaps in time the IFV will be calculated based on the end of day price of such contracts from the CME’s or Baltic Exchange’s, immediately preceding trading session, as applicable. In addition, other investments and U.S. Treasuries held by the Funds will be valued by the Administrator, using rates and points received from client-approved third party vendors (such as Reuters and WM Company) and advisor or broker-dealer quotes. These investments will not be included in the IFV.

13

The NYSE Arca disseminates the IFV through the facilities of CTA/CQ High Speed Lines. In addition, the IFV is published on the NYSE Arca’s website and is available through on-line information services such as Bloomberg and Reuters.

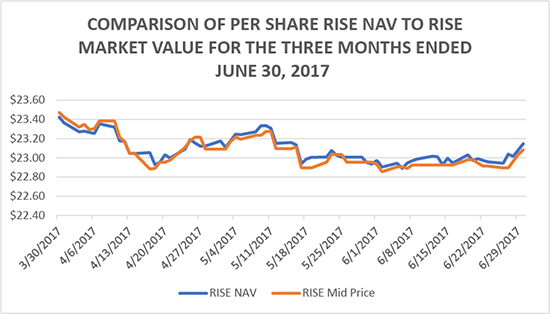

Dissemination of the IFV provides additional information that is not otherwise available to the public and is useful to investors and market professionals in connection with the trading of a Fund’s shares on the NYSE Arca. Investors and market professionals are able throughout the trading day to compare the market price of a Fund’s shares and the IFV. If the market price of a Fund’s shares diverges significantly from the IFV, market professionals will have an incentive to execute arbitrage trades. For example, if RISE’s or BDRY’s shares appear to be trading at a discount compared to the IFV, a market professional could buy RISE’s or BDRY’s shares on the NYSE Arca and take the opposite position in Treasury Instruments or Freight Futures, as applicable. Such arbitrage trades can tighten the tracking between the market price of a Fund’s shares and the IFV and thus can be beneficial to all market participants.

Creation and Redemption of Shares

The Funds create and redeem shares from time to time, but only in one or more Creation Baskets or Redemption Baskets. The creation and redemption of baskets are only made in exchange for delivery to the Funds or the distribution by the Funds of the amount of U.S. Treasuries and/or any cash represented by the baskets being created or redeemed, the amount of which is based on the combined NAV of the number of shares included in the baskets being created or redeemed determined as of 4:00 p.m. E.T. on the day the order to create or redeem baskets is properly received.

Authorized Participants are the only persons that may place orders to create and redeem baskets. Authorized Participants must be (1) registered broker-dealers or other securities market participants, such as banks and other financial institutions, that are not required to register as broker-dealers to engage in securities transactions described below, and (2) DTC Participants. To become an Authorized Participant, a person must enter into an Authorized Participant Agreement with the Sponsor. The Authorized Participant Agreement provides the procedures for the creation and redemption of baskets and for the delivery of the U.S. Treasuries and any cash required for such creation and redemptions. The Authorized Participant Agreement and the related procedures attached thereto may be amended by the respective Funds, without the consent of any limited partner or shareholder or Authorized Participant. Authorized Participants will pay a transaction fee of $500 to the Custodian for each order they place to create or redeem one or more baskets. Authorized Participants who make deposits with a Fund in exchange for baskets receive no fees, commissions or other form of compensation or inducement of any kind from either the respective Fund or the Sponsor, and no such person will have any obligation or responsibility to the Sponsor or the respective Fund to effect any sale or resale of shares.

With respect to RISE, certain Authorized Participants are expected to be capable of participating directly in the Treasury market and the related derivatives market. In some cases, Authorized Participants or their affiliates may from time to time buy or sell Treasuries and related derivatives and may profit in these instances. The Sponsor believes that the size and operation of the Treasury market make it unlikely that an Authorized Participant’s direct activities in such markets will significantly affect the price of Treasuries, related derivatives or the price of the shares.

Each Authorized Participant is required to be registered as a broker-dealer under the Exchange Act and be a member in good standing with FINRA, or exempt from being or otherwise not required to be registered as a broker-dealer or a member of FINRA, and qualified to act as a broker or dealer in the states or other jurisdictions where the nature of its business so requires. Certain Authorized Participants may also be regulated under federal and state banking laws and regulations. Each Authorized Participant has its own set of rules and procedures, internal controls and information barriers as it determines is appropriate in light of its own regulatory regime.

Under the Authorized Participant Agreements, the Sponsor has agreed to indemnify the Authorized Participants against certain liabilities, including liabilities under the 1933 Act, and to contribute to the payments the Authorized Participants may be required to make in respect of those liabilities.

14

Creation Procedures

On any business day, an Authorized Participant may place an order with the Transfer Agent, and accepted by the Distributor, to create one or more baskets. For purposes of processing purchase and redemption orders, a “business day” means any day other than a day when any of the NYSE Arca, the New York Stock Exchange or the CME, in the case of RISE, or the Baltic Exchange, in the case of BDRY, is closed for regular trading. Purchase orders must be placed by 12:00 p.m. E.T. or 1:00 p.m. E.T., in the case of RISE or BDRY, respectively, or the close of NYSE Arca core trading session, whichever is earlier. The day on which a valid purchase order is received in accordance with the terms of the applicable “Authorized Participant Agreement” is referred to as the purchase order date. Purchase orders are irrevocable. Prior to the delivery of baskets for a purchase order, the Authorized Participant will be charged a non-refundable transaction fee due for the purchase order.

The manner by which creations are made is dictated by the terms of the applicable Authorized Participant Agreement. By placing a purchase order for Creation Baskets of RISE, an Authorized Participant agrees to deposit U.S. Treasuries, cash, or a combination of U.S. Treasuries and cash with the Custodian of RISE. If an Authorized Participant fails to so deposit, the order shall be cancelled.

Determination of Required Deposits (RISE only)

The total deposit required to create each basket (“Creation Basket Deposit”) is the amount of U.S. Treasuries and/or cash that is in the same proportion to the total assets of the Fund (net of estimated accrued but unpaid fees, expenses and other liabilities) on the purchase order date as the number of shares to be created under the purchase order is in proportion to the total number of shares outstanding on the purchase order date. The Sponsor determines, directly in its sole discretion or in consultation with the Administrator, the requirements for U.S. Treasuries and the amount of cash, including the maximum permitted remaining maturity of a Treasury and proportions of each Treasury and cash that may be included in deposits to create baskets. The Distributor will publish such requirements at the beginning of each business day. The amount of cash deposit required is the difference between the aggregate market value of the U.S. Treasuries required to be included in a Creation Basket Deposit as of 4:00 p.m. E.T. on the date the order to purchase is properly received and the total required deposit.

Determination of Required Payment (BDRY only)

The Creation Basket Deposit for BDRY is the NAV of 25,000 shares on the purchase order date, but only if the required payment is timely received. To calculate the NAV, the Administrator will use the Baltic Exchange settlement price (typically determined after 2:00 p.m. E.T.) for the Freight Futures.

Because orders to purchase Creation Baskets must be placed no later than 1:00 p.m. E.T., but the total payment required to create a Creation Basket typically will not be determined until after 2:00 p.m. E.T., on the date the purchase order is received, Authorized Participants will not know the total amount of the payment required to create a Creation Basket at the time they submit an irrevocable purchase order. The NAV and the total amount of the payment required to create a Creation Basket could rise or fall substantially between the time an irrevocable purchase order is submitted and the time the amount of the purchase price in respect thereof is determined.

Delivery of Required Deposits (RISE only)

An Authorized Participant who places a purchase order is responsible for transferring to the Fund’s account with the Custodian the required amount of U.S. Treasuries and cash by the end of the third business day following the purchase order date. Upon receipt of the deposit amount, the Administrator directs DTC to credit the number of shares represented by the baskets ordered to the Authorized Participant’s DTC account on the third business day following the purchase order date. The expense and risk of delivery and ownership of U.S. Treasuries until such U.S. Treasuries have been received by the Custodian on behalf of the Fund is borne solely by the Authorized Participant.

Because orders to purchase baskets must be placed by 12:00 p.m., E.T., but the total payment required to create a basket during the continuous offering period will not be determined until after 4:00 p.m., E.T., on the date the purchase order is received, Authorized Participants will not know the total amount of the payment required to create a basket at the time they submit an irrevocable purchase order for the basket. The Fund’s NAV and the total amount of the payment required to create a basket could rise or fall substantially between the time a purchase order is submitted and the time the amount of the purchase price in respect thereof is determined.

15

Delivery of Required Payment (BDRY only)

An Authorized Participant who places a purchase order shall transfer to the Administrator the required amount of U.S. Treasuries and/or cash, by the end of the next business day following the purchase order date. Upon receipt of the deposit amount, the Administrator will direct DTC to credit the number of Creation Baskets ordered to the Authorized Participant’s DTC account on the next business day following the purchase order date.

Suspension of Purchase Orders

The Sponsor acting by itself or through the Administrator or the Distributor may suspend the right of purchase, or postpone the purchase settlement date, for any period during which the NYSE Arca or other exchange on which the shares are listed is closed, other than for customary holidays or weekends, or when trading is restricted or suspended. None of the Sponsor, the Marketing Agent or the Administrator will be liable to any person or in any way for any loss or damages that may result from any such suspension or postponement.

Rejection of Purchase Orders

The Sponsor acting by itself or through the Distributor shall have the absolute right but no obligation to reject a purchase order or a Creation Basket Deposit if:

| ● | it determines that the investment alternative available to the Fund at that time will not enable it to meet its investment objective (RISE only); |

| ● | it determines that the purchase order or the purchase order or Creation Basket Deposit is not in proper form; |

| ● | it believes that the purchase order or the Creation Basket Deposit would have adverse tax consequences to the Fund, the limited partners or its shareholders (RISE only); |

| ● | the acceptance or receipt of the purchase order or Creation Basket Deposit would, in the opinion of counsel to the Sponsor, be unlawful; or |

| ● | circumstances outside the control of the Sponsor, Distributor or Custodian make it, for all practical purposes, not feasible to process creations of baskets. |

None of the Sponsor, Distributor or Custodian will be liable for the rejection of any purchase order or Creation Basket Deposit.

Redemption Procedures

The procedures by which an Authorized Participant can redeem one or more baskets mirror the procedures for the creation of baskets. On any business day, an Authorized Participant may place an order with the Distributor to redeem one or more baskets. Redemption orders must be placed by 12:00 p.m. E.T., with respect to RISE, or 1:00 p.m., with respect to BDRY, or the close of the core trading session on the NYSE Arca, whichever is earlier. A redemption order so received will be effective on the date it is received in satisfactory form by the Distributor. The redemption procedures allow Authorized Participants to redeem baskets and do not entitle an individual shareholder to redeem any shares in an amount less than a Redemption Basket, or to redeem baskets other than through an Authorized Participant. Redemption orders are irrevocable.

16

The manner by which redemptions are made is dictated by the terms of the Authorized Participant Agreement. By placing an order for Redemption Baskets of RISE, an Authorized Participant agrees to (1) deliver the Redemption Basket to be redeemed through DTC’s book-entry system to the Fund’s account with the Custodian not later than 3:00 p.m. E.T. on the third business day following the effective date of the redemption order, and (2) if required by the Sponsor in its sole discretion, enter into or arrange for a block trade, an exchange for related position, or any other transaction (through itself or a designated acceptable broker) with the Fund for the sale of a number and type of futures contracts at the closing settlement price for such contracts on the redemption order date. If an Authorized Participant fails to consummate (1) and (2) above, the order shall be cancelled. The number and type of contracts specified shall be determined by the Sponsor, in its sole discretion, to meet the Fund’s investment objective and shall be sold as a result of the Authorized Participant’s redemption of shares. By placing an order for Redemption Baskets of BDRY, an Authorized Participant agrees to deliver the Redemption Baskets to be redeemed through DTC’s book-entry system to the Fund not later than 1:00 p.m. E.T., on the next business day immediately following the redemption order date. Prior to the delivery of redemption distribution or proceeds, the Authorized Participant will be charged a non-refundable transaction fee due for the redemption order.

Determination of Redemption Distribution (RISE only)

The redemption distribution from the Fund consists of a transfer to the redeeming Authorized Participant of an amount of U.S. Treasuries and/or cash that is in the same proportion to the total assets of the Fund (net of estimated accrued but unpaid fees, expenses and other liabilities) on the date the order to redeem is properly received as the number of shares to be redeemed under the redemption order is in proportion to the total number of shares outstanding on the date the order is received. The Sponsor, directly or in consultation with the Administrator, determines the requirements for U.S. Treasuries and the amounts of cash, including the maximum permitted remaining maturity of a Treasury, and the proportions of U.S. Treasuries and cash that may be included in distributions to Redeem Baskets. The Distributor will publish an estimate of the redemption distribution per basket as of the beginning of each business day.

Determination of Redemption Proceeds (BDRY only)

The redemption proceeds from the Fund consist of a cash redemption amount equal to the NAV of the number of Baskets requested in the Authorized Participant’s redemption order on the redemption order date. To calculate the NAV, the Administrator will use the Baltic Exchange settlement price (typically determined after 2:00 p.m. E.T.) for the Freight Futures.

Because orders to redeem baskets must be placed no later than 1:00 p.m. E.T., but the total amount of redemption proceeds typically will not be determined until after 2:00 p.m. E.T., on the date the redemption order is received, Authorized Participants will not know the total amount of the redemption proceeds at the time they submit an irrevocable redemption order. The NAV and the total amount of redemption proceeds could rise or fall substantially between the time an irrevocable redemption order is submitted and the time the amount of redemption proceeds in respect thereof is determined.

Delivery of Redemption Distribution (RISE only)

The redemption distribution due from the Fund will be delivered to the Authorized Participant by 3:00 p.m. E.T. on the third business day following the redemption order date if, by 3:00 p.m. E.T. on such third business day, the Fund’s DTC account has been credited with the shares represented by the baskets to be redeemed. If the Fund’s DTC account has not been credited with all of the shares represented by the baskets to be redeemed by such time, the redemption distribution will be delivered to the extent of whole baskets received. Any remainder of the redemption distribution will be delivered on the next business day to the extent of remaining shares represented by the whole baskets received if the Fund receives the fee applicable to the extension of the redemption distribution date which the Sponsor may, from time to time, determine and the remaining baskets to be redeemed are credited to the Fund’s DTC account by 3:00 p.m. E.T. on such next business day. Any further outstanding amount of the redemption order will be cancelled. Pursuant to information from the Sponsor, the Custodian will also be authorized to deliver the redemption distribution notwithstanding that the baskets to be redeemed are not credited to the Fund’s DTC account by 3:00 p.m. E.T. on the third business day following the redemption order date if the Authorized Participant has collateralized its obligation to deliver the baskets through DTC’s book entry-system on such terms as the Sponsor may from time to time determine.

17

Delivery of Redemption Proceeds (BDRY only)

The redemption proceeds due from the Fund will be delivered to the Authorized Participant at 1:00 p.m. E.T., on the next business day immediately following the redemption order date if, by such time, the Fund’s DTC account has been credited with the baskets to be redeemed. If the Fund’s DTC account has not been credited with all of the baskets to be redeemed by such time, the redemption distribution is delivered to the extent of whole baskets received. Any remainder of the redemption distribution is delivered on the next business day to the extent of remaining whole baskets received if the Fund receives the fee applicable to the extension of the redemption distribution date which the Sponsor may, from time to time, determine and the remaining baskets to be redeemed are credited to the Fund’s DTC account by 1:00 p.m. E.T., on such next business day. Any further outstanding amount of the redemption order shall be cancelled. The Sponsor may cause the redemption distribution to be delivered notwithstanding that the baskets to be redeemed are not credited to the Fund’s DTC account by 12:00 p.m. E.T., on the next business day immediately following the redemption order date if the Authorized Participant has collateralized its obligation to deliver the Baskets through DTC’s book entry system on such terms as the Sponsor may from time to time determine.

Suspension or Rejection of Redemption Orders

The Sponsor may, in its discretion, suspend the right of redemption, or postpone the redemption settlement date, (1) for any period during which the NYSE Arca, or the CME in the case of RISE, is closed other than customary weekend or holiday closings, or trading on the NYSE Arca, or the CME, in the case of RISE, is suspended or restricted, (2) for any period during which an emergency exists as a result of which delivery, disposal or evaluation of the redemption distribution or redemption proceeds, as applicable, is not reasonably practicable, or (3) for such other period as the Sponsor determines to be necessary for the protection of the limited partners or shareholders. For example, the Sponsor may determine that it is necessary to suspend redemptions to allow for the orderly liquidation of a Fund’s assets at an appropriate value to fund a redemption. If the Sponsor has difficulty liquidating its positions, e.g., because of a market disruption event in the futures markets or a suspension of trading by the exchange where the futures contracts are listed, it may be appropriate to suspend redemptions until such time as such circumstances are rectified. None of the Sponsor, the Distributor, the Transfer Agent, the Administrator, or the Custodian will be liable to any person or in any way for any loss or damages that may result from any such suspension or postponement.

Redemption orders must be made in whole baskets. The Sponsor will reject a redemption order if the order is not in proper form as described in the applicable Authorized Participant Agreement or if the fulfillment of the order, in the opinion of its counsel, might be unlawful. The Sponsor may also reject a redemption order if the number of shares being redeemed would reduce the remaining outstanding shares to 50,000 shares (minimum NYSE Arca listing requirement) or less, unless the Sponsor has reason to believe that the placer of the redemption order does in fact possess all the outstanding shares and can deliver them.

Creation and Redemption Transaction Fee