Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION - Pacific Green Technologies Inc. | f10q0618ex32-1_pacific.htm |

| EX-31.1 - CERTIFICATION - Pacific Green Technologies Inc. | f10q0618ex31-1_pacific.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2018

or

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission File Number 000-54756

| PACIFIC GREEN TECHNOLOGIES INC. |

| (Exact name of registrant as specified in its charter) |

| Delaware | N/A | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

| 5205 Prospect Road, Suite 135-226, San Jose, CA | 95129 | |

| (Address of principal executive offices) | (Zip Code) |

| (408) 538-3373 |

| (Registrant’s telephone number, including area code) |

| N/A |

| (Former name, former address and former fiscal year, if changed since last report) |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ YES ☐ NO

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒ YES ☐ NO

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| (Do not check if smaller reporting company) | Emerging growth company | ☐ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) ☐ YES ☒ NO

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS

Check whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Exchange Act after the distribution of securities under a plan confirmed by a court. ☐ YES ☐ NO

APPLICABLE ONLY TO CORPORATE ISSUERS

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

43,208,923 common shares issued and outstanding as of August 15, 2018.

TABLE OF CONTENTS

| PART I – FINANCIAL INFORMATION | 1 | |

| ITEM 1. FINANCIAL STATEMENTS | 1 | |

| ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 2 | |

| ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 17 | |

| ITEM 4. CONTROLS AND PROCEDURES | 17 | |

| PART II – OTHER INFORMATION | 18 | |

| ITEM 1. LEGAL PROCEEDINGS | 18 | |

| ITEM 1A. RISK FACTORS | 18 | |

| ITEM 2. UNREGISTERED SALES OF EQUITY SECURITIES | 18 | |

| ITEM 3. DEFAULTS UPON SENIOR SECURITIES | 18 | |

| ITEM 4. MINE SAFETY DISCLOSURES | 18 | |

| ITEM 5. OTHER INFORMATION | 18 | |

| ITEM 6. EXHIBITS | 19 |

i

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

Our unaudited interim consolidated financial statements for the three month period ended June 30, 2018 form part of this quarterly report. They are stated in United States Dollars (US$) and are prepared in accordance with United States generally accepted accounting principles for interim financial information and with the instructions to Form 10-Q and Article 8 of Regulation S-X.

| 1 |

PACIFIC GREEN TECHNOLOGIES INC.

Condensed Consolidated Financial Statements

June 30, 2018

(Expressed in US dollars)

(unaudited)

| Index | |

| Condensed Consolidated Balance Sheets | F–2 |

| Condensed Consolidated Statements of Operations and Comprehensive Loss | F–3 |

| Condensed Consolidated Statements of Cash Flows | F–4 |

| Notes to the Condensed Consolidated Financial Statements | F–5 |

| F-1 |

PACIFIC GREEN TECHNOLOGIES INC.

Condensed Consolidated Balance Sheets

(Expressed in U.S. dollars)

| June 30, 2018 $ | March 31, 2018 $ | |||||||

| (unaudited) | ||||||||

| ASSETS | ||||||||

| Cash | 2,307,735 | 229,882 | ||||||

| Amounts receivable | 6,354 | 4,912 | ||||||

| Prepaid expenses and deposits | 524,994 | 72,032 | ||||||

| Due from related parties (Note 8) | 25,101 | 25,101 | ||||||

| Total Current Assets | 2,864,184 | 331,927 | ||||||

| Lease receivable (Note 3) | 1,995,000 | 1,995,000 | ||||||

| Property and equipment (Note 4) | 13,444 | 15,800 | ||||||

| Intangible assets (Note 5) | 10,403,115 | 10,622,068 | ||||||

| Total Assets | 15,275,743 | 12,964,795 | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Accounts payable and accrued liabilities (Note 8) | 714,130 | 888,760 | ||||||

| Convertible debenture (Note 6) | 30,000 | 30,000 | ||||||

| Due to related parties (Note 8) | 79,724 | 229,544 | ||||||

| Derivative liability (Note 7) | 220,652 | 75,505 | ||||||

| Total Liabilities | 1,044,506 | 1,223,809 | ||||||

| Nature of Operations and Continuance of Business (Note 1) | ||||||||

| Commitments (Note 13) | ||||||||

| Stockholders’ Equity | ||||||||

| Preferred stock, 10,000,000 shares authorized, $0.001 par value Nil shares issued and outstanding | – | – | ||||||

| Common stock, 500,000,000 shares authorized, $0.001 par value 43,208,923 and 40,757,415 shares issued and outstanding, respectively | 43,209 | 40,757 | ||||||

| Common stock issuable (Note 9) | – | 206,675 | ||||||

| Additional paid-in capital | 82,647,069 | 78,989,346 | ||||||

| Accumulated other comprehensive income | 154,029 | 268,259 | ||||||

| Deficit | (68,613,070 | ) | (67,764,051 | ) | ||||

| Total Stockholders’ Equity | 14,231,237 | 11,740,986 | ||||||

| Total Liabilities and Stockholders’ Equity | 15,275,743 | 12,964,795 | ||||||

(The accompanying notes are an integral part of these condensed consolidated financial statements)

| F-2 |

PACIFIC GREEN TECHNOLOGIES INC.

Condensed Consolidated Statements of Operations and Comprehensive Loss

(Expressed in U.S. dollars)

(unaudited)

| Three Months Ended June 30, 2018 $ | Three Months Ended June 30, 2017 $ | |||||||

| Operating expenses | ||||||||

| Advertising and promotion | 34,517 | 15,850 | ||||||

| Amortization of intangible assets | 218,953 | 218,953 | ||||||

| Consulting fees (Note 8) | 357,084 | 101,803 | ||||||

| Depreciation | 2,356 | 2,356 | ||||||

| Foreign exchange loss (gain) | (144,729 | ) | 98,471 | |||||

| Office and miscellaneous | 62,643 | 46,831 | ||||||

| Professional fees | 69,542 | 39,529 | ||||||

| Research and development | – | 52,304 | ||||||

| Transfer agent and filing fees | 17,022 | 13,301 | ||||||

| Travel | 83,494 | 50,419 | ||||||

| Total operating expenses | 700,882 | 639,817 | ||||||

| Loss before other expenses | (700,882 | ) | (639,817 | ) | ||||

| Other expenses | ||||||||

| Loss on change in fair value of derivative liability (Note 7) | (145,147 | ) | (105,060 | ) | ||||

| Interest expense | (2,990 | ) | (268,703 | ) | ||||

| Total other expenses | (148,137 | ) | (373,763 | ) | ||||

| Net loss for the period | (849,019 | ) | (1,013,580 | ) | ||||

| Other comprehensive income (loss) | ||||||||

| Foreign currency translation gain (loss) | (114,230 | ) | 44,050 | |||||

| Comprehensive loss for the period | (963,249 | ) | (969,530 | ) | ||||

| Net loss per share, basic and diluted | (0.02 | ) | (0.04 | ) | ||||

| Weighted average number of shares outstanding | 41,641,116 | 26,467,393 | ||||||

(The accompanying notes are an integral part of these condensed consolidated financial statements)

| F-3 |

PACIFIC GREEN TECHNOLOGIES INC.

Condensed Consolidated Statements of Cash Flows

(Expressed in U.S. dollars)

(unaudited)

| Three Months Ended June 30, 2018 $ | Three Months Ended June 30, 2017 $ | |||||||

| Operating Activities | ||||||||

| Net loss for the period | (849,019 | ) | (1,013,580 | ) | ||||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Accretion of discount on note payable and convertible debentures | – | 33,438 | ||||||

| Amortization of intangible assets | 218,953 | 218,953 | ||||||

| Depreciation | 2,356 | 2,356 | ||||||

| Imputed interest | – | 225,000 | ||||||

| Loss on change in fair value of derivative liability | 145,147 | 105,060 | ||||||

| Stock issued for services | 189,467 | – | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Amounts receivable | (1,442 | ) | 20,723 | |||||

| Prepaid expenses and deposits | (124,929 | ) | (135,567 | ) | ||||

| Due from related parties | – | (94 | ) | |||||

| Accounts payable and accrued liabilities | (174,629 | ) | (137,618 | ) | ||||

| Due to related parties | (124,719 | ) | 63,837 | |||||

| Net Cash Used In Operating Activities | (718,815 | ) | (617,492 | ) | ||||

| Investing Activities | ||||||||

| Additions of property and equipment | – | (87,647 | ) | |||||

| Net Cash Used In Investing Activities | – | (87,647 | ) | |||||

| Financing Activities | ||||||||

| Repayments to related parties | – | (331,783 | ) | |||||

| Repayment of loan payable | – | (30,917 | ) | |||||

| Proceeds from issuance of common stock | 2,936,000 | 1,170,000 | ||||||

| Net Cash Provided by Financing Activities | 2,936,000 | 807,300 | ||||||

| Effect of Foreign Exchange Rate Changes on Cash | (139,332 | ) | 43,311 | |||||

| Change in Cash | 2,077,853 | 145,472 | ||||||

| Cash, Beginning of Period | 229,882 | 382,167 | ||||||

| Cash, End of Period | 2,307,735 | 527,639 | ||||||

| Non-cash Investing and Financing Activities: | ||||||||

| Stock issued for services included in prepaid expenses | 328,033 | – | ||||||

| Supplemental Disclosures: | ||||||||

| Interest paid | – | – | ||||||

| Income taxes paid | – | – | ||||||

(The accompanying notes are an integral part of these condensed consolidated financial statements)

| F-4 |

PACIFIC GREEN TECHNOLOGIES INC.

Notes to the Condensed Consolidated Financial Statements

June 30, 2018

(Expressed in U.S. Dollars)

(unaudited)

| 1. | Nature of Operations and Continuance of Business |

Pacific Green Technologies Inc. (the “Company”) was incorporated in the state of Delaware on March 10, 1994, under the name of Beta Acquisition Corp. In September 1995, the Company changed its name to In-Sports International, Inc. In August 2002, the Company changed its name to ECash, Inc. On June 13, 2012, the Company changed its name to Pacific Green Technologies Inc. The Company is in the business of acquiring, developing, and marketing emission control technologies.

The accompanying condensed consolidated financial statements of the Company should be read in conjunction with the consolidated financial statements and accompanying notes filed with the U.S. Securities and Exchange Commission in the Company’s Annual Report on Form 10-K for the fiscal year ended March 31, 2018. In the opinion of management, the accompanying condensed consolidated financial statements reflect all adjustments of a recurring nature considered necessary to present fairly the Company’s financial position and the results of its operations and its cash flows for the periods shown.

The preparation of these condensed consolidated financial statements in accordance with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the amounts reported. Actual results could differ materially from those estimates. The results of operations and cash flows for the periods shown are not necessarily indicative of the results to be expected for the full year.

These condensed consolidated financial statements have been prepared on a going concern basis, which implies the Company will continue to realize its assets and discharge its liabilities in the normal course of business. The continuation of the Company as a going concern is dependent upon the continued financial support from its shareholders, creditors, and related parties, and the ability of the Company to generate profitable operations. As at June 30, 2018, the Company has begun commercial sales generating revenues; the Company has an accumulated deficit of $68,613,070 since inception. A history of significant losses raises doubts regarding the Company’s ability to continue as a going concern. These consolidated financial statements do not include any adjustments to the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern.

| 2. | Significant Accounting Policies |

| (a) | Basis of Presentation |

These consolidated financial statements and related notes are presented in accordance with accounting principles generally accepted in the United States, and are expressed in U.S. dollars. These consolidated financial statements include the accounts of the Company and the following entities:

| Pacific Green Marine Technologies Ltd. (“PGMTL”) | Wholly-owned subsidiary | ||

Pacific Green Technologies International Limited (“PGTIL”) PGT Technologies (Canada) Ltd (“PGT CAN”) |

Wholly-owned subsidiary Wholly-owned subsidiary | ||

| Energy Park Sutton Bridge Ltd. (“EPSB”) | Wholly-owned subsidiary of PGTIL | ||

| Pacific Green Technologies Asia Limited (“PGTA”) | Wholly-owned subsidiary of PGTIL | ||

| Pacific Green Technologies China Limited (“PGTC”) | Wholly-owned subsidiary of PGTA |

All inter-company balances and transactions have been eliminated.

| (b) | Financial Instruments and Fair Value Measurements |

ASC 820, “Fair Value Measurements and Disclosures” requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. ASC 820 establishes a fair value hierarchy based on the level of independent, objective evidence surrounding the inputs used to measure fair value. A financial instrument’s categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value measurement. ASC 820 prioritizes the inputs into three levels that may be used to measure fair value:

Level 1

Level 1 applies to assets or liabilities for which there are quoted prices in active markets for identical assets or liabilities.

Level 2

Level 2 applies to assets or liabilities for which there are inputs other than quoted prices that are observable for the asset or liability such as quoted prices for similar assets or liabilities in active markets; quoted prices for identical assets or liabilities in markets with insufficient volume or infrequent transactions (less active markets); or model-derived valuations in which significant inputs are observable or can be derived principally from, or corroborated by, observable market data.

| F-5 |

PACIFIC GREEN TECHNOLOGIES INC.

Notes to the Condensed Consolidated Financial Statements

June 30, 2018

(Expressed in U.S. Dollars)

(unaudited)

| 2. | Significant Accounting Policies (continued) |

| (b) | Financial Instruments and Fair Value Measurements (continued) |

Level 3

Level 3 applies to assets or liabilities for which there are unobservable inputs to the valuation methodology that are significant to the measurement of the fair value of the assets or liabilities.

The Company’s financial instruments consist principally of cash, amounts receivable, lease receivable, amounts due from and to related parties, accounts payable and accrued liabilities, convertible debenture, and derivative liability. The recorded values of these financial instruments approximate their current fair values because of their nature and respective maturity dates or durations.

The following table represents assets and liabilities that are measured and recognized at fair value as of June 30, 2018, on a recurring basis:

| Level 1 $ | Level 2 $ | Level 3 $ | |||||||||||

| Cash | 2,307,735 | – | – | ||||||||||

| Derivative liability | – | 220,652 | – | ||||||||||

| Total | 2,307,735 | 220,652 | – | ||||||||||

During the three months ended June 30, 2018, the Company recognized a loss on the change in fair value of derivative liability of $145,147 (2017 – $105,060).

| (c) | Recent Accounting Pronouncements |

In February 2016, the FASB issued new lease accounting guidance in ASU No. 2016-02, “Leases”. This new guidance was initiated as a joint project with the International Accounting Standards Board to simplify lease accounting and improve the quality of and comparability of financial information for users. This new guidance would eliminate the concept of off-balance sheet treatment for “operating leases” for lessees for the vast majority of lease contracts. Under ASU No. 2016-02, at inception, a lessee must classify all leases with a term of over one year as either finance or operating, with both classifications resulting in the recognition of a defined “right-of-use” asset and a lease liability on the balance sheet. However, recognition in the income statement will differ depending on the lease classification, with finance leases recognizing the amortization of the right-of-use asset separate from the interest on the lease liability and operating leases recognizing a single total lease expense. Lessor accounting under ASU No. 2016-02 would be substantially unchanged from the previous lease requirements under GAAP. ASU No. 2016-02 will take effect for public companies in fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. Early adoption is permitted and for leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements, lessees and lessors must apply a modified retrospective transition approach. The Company is currently evaluating the new guidance and has not determined the impact this standard may have on the consolidated financial statements.

The Company has implemented all new accounting pronouncements that are in effect and that may impact its consolidated financial statements and does not believe that there are any other new accounting pronouncements that have been issued that might have a material impact on its financial position or results of operations.

| 3. | Lease Receivable |

In December 2017, the Company completed the installation and the accounting sale of a constructed scrubber system. The Company’s investment in sales-type lease as at June 30, 2018, consists of an amount due from the customer under a long-term lease arrangement. No amount has been allocated to residual value or other deliverables; accordingly, the amount presented in the balance sheet represents the present value of amounts due under the energy management contract. The entire amount is presented as a long-term receivable.

| F-6 |

PACIFIC GREEN TECHNOLOGIES INC.

Notes to the Condensed Consolidated Financial Statements

June 30, 2018

(Expressed in U.S. Dollars)

(unaudited)

| 4. | Property and Equipment |

| Cost $ | Accumulated amortization $ | June 30, 2018 Net carrying value $ | March 31, 2018 Net carrying value $ | ||||||||||||||

| Furniture and equipment | 4,155 | 1,454 | 2,701 | 2,908 | |||||||||||||

| Leasehold improvements | 25,784 | 15,041 | 10,743 | 12,892 | |||||||||||||

| Total | 29,939 | 16,495 | 13,444 | 15,800 | |||||||||||||

| 5. | Intangible Assets |

| Cost $ | Accumulated amortization $ | Impairment $ | June 30, 2018 Net carrying value $ | March 31, 2018 Net carrying value $ | |||||||||||||||||

| Patents and technical information | 35,852,555 | (4,992,185 | ) | (20,457,255 | ) | 10,403,115 | 10,622,068 | ||||||||||||||

On May 17, 2013, the Company entered into an Assignment of Assets agreement with EnviroTechnologies, Inc. (“Enviro”), a non-related party, whereby the Company acquired various patents and technical information related to the manufacture of a wet scrubber for removing sulphur, other pollutants, and the particulate matter from diesel engine exhaust. In exchange for these assets, the Company waived all obligations owing to the Company as well as agreed to return a total of 88,876,443 of Enviro’s shares back to Enviro. The obligations waived consisted of $237,156 owing to the Company as well as $93,721 of debt owing to Pacific Green Group Limited (“PGG”), a company controlled by a shareholder of the Company who has a significant influence on the Company’s operations, which was assigned to the Company. The Company entered into share exchange agreements with Enviro shareholders pursuant to which it issued shares of its common stock in exchange for shares of Enviro on a one-for-ten basis. The intangible assets acquired were recorded at cost and is being amortized using the straight-line method over the estimated useful life of 17 years.

| 6. | Convertible Debenture |

On November 10, 2015, the Company entered into a $110,000 convertible debenture with a non-related party, in exchange for $100,000, net of $10,000 for legal fees which was deferred and amortized over the term of the debenture. Under the terms of the debenture, the amount is unsecured, bears guaranteed interest at 10% and default interest at 20% per annum, and was due on November 10, 2016. The note is convertible into shares of common stock of the Company equal to the lower of: (a) $0.40 or (b) 60% of the lowest trading price of the Company’s common stock during the 20 consecutive trading days prior to the date of conversion. In the event of a default, the discount shall be permanently increased by 10%.

The Company analyzed the conversion option under ASC 815, and determined that the conversion feature should be classified as a liability and recorded at fair value due to there being no explicit limit to the number of shares to be delivered upon settlement of the conversion option. In accordance with ASC 815, the Company recognized the intrinsic value of the embedded beneficial conversion feature of $110,000. On February 22, 2017, the Company issued 50,000 shares of common stock for the conversion of $20,000 of this debenture. On August 10, 2017, the Company issued 100,000 shares of common stock for the conversion of $20,000 of this debenture. On October 4, 2017, the Company issued 320,000 shares of common stock for the conversion of $40,000 of this debenture. As at June 30, 2018, the carrying value of the debenture was $30,000 (March 31, 2018 - $30,000) and the fair value of the derivative liability was $220,652 (March 31, 2018 - $75,505).

| 7. | Derivative Liability |

The Company records the fair value of the conversion price of the convertible debenture disclosed in Note 7 in accordance with ASC 815. The fair value of the derivative liability was calculated using a binomial option pricing model. The fair value of the derivative liability is revalued on each balance sheet date with corresponding gains and losses recorded in the consolidated statement of operations. During the three months ended June 30, 2018, the Company recorded a loss on the change in fair value of derivative liability of $145,147 (2017 – $105,060). As at June 30, 2018, the Company recorded derivative liability of $220,652 (March 31, 2018 - $75,505).

| F-7 |

PACIFIC GREEN TECHNOLOGIES INC.

Notes to the Condensed Consolidated Financial Statements

June 30, 2018

(Expressed in U.S. Dollars)

(unaudited)

| 7. | Derivative Liability (continued) |

The following inputs and assumptions were used to calculate the fair value of the beneficial conversion feature of the convertible debenture outstanding as at June 30, 2018, assuming no expected dividends:

| As at June 30, 2018 | |||||

| Estimated common stock issuable upon conversion | 163,322 | ||||

| Estimated exercise price per common share | 0.40 | ||||

| Risk-free interest rate | 1.0 | % | |||

| Expected volatility | 106 | % | |||

| Expected life (in years) | 0.25 | ||||

A summary of the activity of the derivative liability is shown below:

| $ | |||||

| Balance, March 31, 2018 | 75,505 | ||||

| Mark to market adjustment | 145,147 | ||||

| Balance, June 30, 2018 | 220,652 | ||||

| 8. | Related Party Transactions |

| (a) | As at June 30, 2018, the Company was owed $25,101 (March 31, 2018 - $25,101) from a shareholder of the Company who has a significant influence on the Company’s operations. The amount owed is unsecured, non-interest bearing, and due on demand. |

| (b) | As at June 30, 2018, the Company owed $19,737 (March 31, 2018 – $198,175) to PGG, a company controlled by a shareholder of the Company who has a significant influence on the Company’s operations, of which $nil (March 31, 2018 - $28,618) was recorded in accounts payable and accrued liabilities. The amounts owing are unsecured, non-interest bearing, and due on demand. |

| (c) | As at June 30, 2018, the Company owed $67,905 (March 31, 2018 – $64,195) to directors of the Company, of which $7,918 (March 31, 2018 - $4,208) was recorded in accounts payable and accrued liabilities. The amounts owing are unsecured, non-interest bearing, and due on demand. |

| (d) | During the three months ended June 30, 2018, the Company incurred $65,000 (2017 – $60,000) in consulting fees to PGG, a company controlled by a shareholder of the Company who has a significant influence on the Company’s operations. |

| (e) | During the three months ended June 30, 2018, the Company incurred $60,000 (2017 – $20,000) in consulting fees to a company controlled by a director of the Company. |

| (f) | During the three months ended June 30, 2018, the Company incurred $3,750 (2017 – $3,837) in consulting fees to a company controlled by a director of the Company. |

| F-8 |

PACIFIC GREEN TECHNOLOGIES INC.

Notes to the Condensed Consolidated Financial Statements

June 30, 2018

(Expressed in U.S. Dollars)

(unaudited)

| 9. | Common Stock |

| (a) | On April 28, 2018, the Company issued 206,675 shares of common stock relating to a non-brokered private placement at a price of $1.00 per share for proceeds of $206,675, which was recorded as common stock issuable as at March 31, 2018. |

| (b) | On May 28, 2018, the Company entered into securities purchase agreements (“SPA’s”) with seven investors. The SPA’s include subscription agreements for 1,957,333 shares of common stock and 1,957,333 share purchase warrants exercisable at a price of $2.50 per share expiring on July 1, 2020 for proceeds of $2,936,000. Upon the Company meeting a specified sales target by December 31, 2018, the investors must complete conditional subscriptions of an additional 1,342,665 shares of common stock and 1,342,665 share purchase warrants exercisable at a price of $2.50 per share expiring on July 1, 2020 at $1.50 per unit on or before January 10, 2019. If the Company fails to achieve the specified sales target, then the investors have the option to complete the conditional subscription agreements for the purchase of an additional 1,853,998 shares of common stock and 1,853,998 share purchase warrants exercisable at $2.00 per share expiring on July 1, 2020 for $1.00 per unit on or before January 15, 2019. |

| (c) | On June 12, 2018, the Company issued 287,500 shares of common stock with a fair value of $517,500 to three consultants, in lieu of a cash payment, for six months of consulting services. As at June 30, 2018, $328,033 of the value of the shares remains in prepaid expenses to be recognized over the remaining term of service. |

| 10. | Share Purchase Warrants |

| Number of warrants | Weighted average exercise price $ | ||||||||

| Balance, March 31, 2018 | 1,500,000 | 1.00 | |||||||

| Issued | 1,957,333 | 2.50 | |||||||

| Balance, June 30, 2018 | 3,457,333 | 1.85 | |||||||

As at June 30, 2018, the following share purchase warrants were outstanding:

| Number of warrants outstanding | Exercise price $ | Expiry date | |||||||

| 500,000 | 1.00 | November 23, 2018 | |||||||

| 1,000,000 | 1.00 | November 23, 2019 | |||||||

| 1,957,333 | 2.50 | July 1, 2020 | |||||||

| 3,457,333 | |||||||||

| F-9 |

PACIFIC GREEN TECHNOLOGIES INC.

Notes to the Condensed Consolidated Financial Statements

June 30, 2018

(Expressed in U.S. Dollars)

(unaudited)

| 11. | Stock Options |

The following table summarizes the continuity of stock options issued and outstanding:

| Number of options | Weighted average exercise price $ | Weighted average remaining contractual life (years) | Aggregate intrinsic value $ | ||||||||||||||

| Balance, March 31, 2018 | 537,500 | 0.01 | 0.7 | 478,375 | |||||||||||||

| Balance, June 30, 2018 | 537,500 | 0.01 | 0.4 | 935,250 | |||||||||||||

Additional information regarding stock options outstanding as at June 30, 2018 is as follows:

| Outstanding and exercisable | |||||||||||||||

| Range of exercise prices $ | Number of shares | Weighted average remaining contractual life (years) | Weighted average exercise price $ | ||||||||||||

| 0.01 | 537,500 | 0.4 | 0.01 | ||||||||||||

| 12. | Segmented Information |

The Company is located and operates in the United States and its subsidiaries are primarily located and operating in the United Kingdom and China.

| June 30, 2018 | |||||||||||||

| United States $ | Europe $ | Total $ | |||||||||||

| Lease receivable | – | 1,995,000 | 1,995,000 | ||||||||||

| Property and equipment | 13,444 | – | 13,444 | ||||||||||

| Intangible assets | 10,403,115 | – | 10,403,115 | ||||||||||

| Total non-current assets | 10,416,559 | 1,995,000 | 12,441,559 | ||||||||||

| F-10 |

PACIFIC GREEN TECHNOLOGIES INC.

Notes to the Condensed Consolidated Financial Statements

June 30, 2018

(Expressed in U.S. Dollars)

(unaudited)

| 13. | Commitments |

| (a) | On November 17, 2015, PGTC entered into a commercial joint venture agreement (the “Agreement”) with a non-related party (the “Supplier”) wherein the Supplier would receive and process orders, manufacture, and install products for the Company’s customers. In return, the Company agreed to design the product and provide a technology license and technical support (the “Technology”) to the Supplier. During the term of the Agreement, the Company will provide the Supplier with a non-transferrable right and license to use the Technology to manufacture and install the product within the Peoples’ Republic of China. |

Upon receiving each order from the Company, the Supplier and the Company shall submit to each other the respective estimated budgets. For each project, after receipt of the revenue from the relevant customer, the expenses of the Company and the Supplier shall be deducted and reimbursed from the revenue proportionally. The parties have agreed to share the gross profits at an even split of 50% each.

| (b) | On August 4, 2016, the Company entered into a three year lease agreement commencing November 15, 2016. The minimum lease payments over the remaining term of the lease are as follows: |

| Fiscal Year | $ | ||||

| 2019 | 61,229 | ||||

| 2020 | 39,339 | ||||

| 100,568 | |||||

| (c) | On January 1, 2017, PGTC entered into a one year tooling development agreement with a non-related party to begin tooling for pending projects in advance of orders to facilitate shorter delivery times. Pursuant to the agreement, PGTC will pay $160,198 (RMB1,050,000), on the one year anniversary of the acceptance of the system. |

| (d) | On January 1, 2017, PGTC entered into a nine month sales and marketing agreement with a non-related party to conduct sales and marketing services for the scrubber system in China. Pursuant to the agreement, PGTC will pay $160,198 (RMB1,050,000), on the nine month anniversary of the acceptance of the system. |

| (e) | On July 14, 2017, the Company entered into a new memorandum of understanding to establish a new joint venture company in China with a non-related party (the “Supplier”) wherein the Supplier would receive and process orders, manufacture, and install products for the Company’s customers. In return, the Company agreed to design the product, provide strategic pricing, sales and marketing direction, as well as provide technology licenses and technical support (the “Technology”) to the Supplier. During the term of the agreement, the Company will provide the Supplier with a non-transferrable right and license to use the Technology to manufacture and install the product within the Asia and Russia region. |

| F-11 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

FORWARD-LOOKING STATEMENTS

This quarterly report contains forward-looking statements. These statements relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “could”, “may”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “estimate”, “predict”, “potential” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable laws, including the securities laws of the United States, we do not intend to update any of the forward-looking statements so as to conform these statements to actual results.

Our unaudited consolidated financial statements are stated in U.S. dollars and are prepared in accordance with generally accepted accounting principles in the United States. The following discussion should be read in conjunction with our financial statements and the related notes that appear elsewhere in this quarterly report.

As used in this current report and unless otherwise indicated, the terms “we”, “us”, “our” and “our company” mean Pacific Green Technologies Inc., a Delaware corporation, and our wholly owned subsidiaries, Pacific Green Marine Technologies Ltd, a United Kingdom corporation, Pacific Green Technologies International Limited, a British Virgin Islands corporation, and its wholly owned subsidiary, Energy Park Sutton Bridge, a United Kingdom corporation, PGT Technologies (Canada) Ltd, a Canadian corporation, Pacific Green Technologies Asia Limited, and its wholly owned subsidiary, Pacific Green Technologies China Limited, both Hong Kong companies.

Corporate History

Our company was incorporated in Delaware on March 10, 1994, under the name of Beta Acquisition Corp. In September 1995, we changed our name to In-Sports International, Inc. In August 2002, we changed our name from In-Sports International, Inc. to ECash, Inc. In 2007, due to limited financial resources, we discontinued our operations. Over the course of the last five years, we have sought new business opportunities.

On June 13, 2012, we changed our name to Pacific Green Technologies Inc. and effected a reverse split of our common stock following which we had 27,002 shares of common stock outstanding with $0.001 par value.

Effective December 4, 2012, we filed with the Delaware Secretary of State a Certificate of Amendment of Certificate of Incorporation, wherein we increased our authorized share capital to 510,000,000 shares of stock as follows:

| ● | 500,000,000 shares of common stock with a par value of $0.001; and | |

| ● | 10,000,000 shares of preferred stock with a par value of $0.001. |

The increase of authorized capital was approved by our board of directors on July 1, 2012 and by a majority of our stockholders by a resolution dated July 1, 2012.

Historical Business Overview

On May 1, 2010 we entered into a consulting agreement with Sichel Limited. Sichel has investigated new opportunities for us and has subscribed for new shares of our company’s common stock. The consulting agreement entitles Sichel to $20,000 per calendar month. With an effective date of March 31, 2013, the consulting agreement, along with all amounts owed to Sichel, were assigned to Pacific Green Group Limited (“PGG”). As at our year ended March 31, 2017 we owed Sichel $nil and we owed PGG approximately $3,945,833 in loans and unpaid management fees. Pursuant to the terms of the consulting agreement, if we are unable to pay the monthly consulting fee, PGG may elect to be paid in shares of stock, and if we are unable to pay the monthly consulting fee, PGG may elect to be paid in shares of stock.

Details of other material contracts and commitments follows the New Strategy and Current business section.

| 2 |

New Strategy and Current business

Since 2012, the Company has focused on marketing, developing and acquiring technologies designed to improve the environment by reducing pollution. The Company has acquired technologies, patents and intellectual property from EnviroTechnologies Inc. through share transfer, assignment and representation agreements entered into during 2012 and 2013. Following those acquisitions, management has expanded the registration of intellectual property rights around the world and pursued opportunities globally for the development and marketing of the emission control technologies.

Working with a worldwide network of agents to market the ENVI-Systems™ emission control technologies, the Company has focused on three applications of the technology:

ENVI-Marine TM

Diesel exhaust from ships, ferries and tankers includes ash and soot as particulate components and sulphur dioxide as an acid gas. Testing has been conducted on diesel shipping to confirm the application of seawater as a neutralizing agent for sulphur emissions as well as capturing particulate matter. In addition to marine applications, these tests also showed applicability of the system for large displacement engines such as stationary generators, compressors, container handling, heavy construction and mining equipment.

The Company manufactured the components for an ENVI-Marine unit that was installed in Union Maritimes’ (Union) MV Westminster chemical ship during the summer of 2017. Under the terms of an Energy Management Lease dated December 16, 2016, Union will make quarterly payments to the Company determined on their savings realized by the ENVI-Marine units’ operation up to an aggregate of $1,995,000.

The Company has been actively marketing its ENVI-Marine™ units to ship brokers and ship owners.

ENVI-Pure TM

Increasing legislation relating to landfill of municipal solid waste has led to the emergence of increasing numbers of waste to energy plants (“WtE”). A WtE plant obviates the need for landfill, burning municipal waste for conversion to electricity. A WtE plant is typically 45-100MW. The ENVI-Clean™ system is particularly suited to WtE as it cleans multiple pollutants in a single system.

ENVI-Clean TM

EnviroTechnologies Inc. has successfully conducted sulphur dioxide demonstration tests at the American Bituminous Coal Partners power plant in Grant Town, West Virginia. The testing achieved a three test average of 99.3% removal efficiency. The implementation of US Clean Air regulations in July 2010 has created additional demand for sulphur dioxide removal in all industries emitting sulphur pollution. Furthermore, China consumes approximately one half of the world’s coal, but introduced measures designed to reduce energy and carbon intensity in its 12th Five Year Plan. Applications include regional power facilities and heating for commercial buildings and greenhouses. Typical applications range in size from 1 to 20 megawatts (MW) with power generation occupying the larger end of the range.

Following the signing of a joint venture agreement with Power China SPEM, an ENVI-Clean™ was sold to a steelworks company in Yancheng to remove SO2 from its 93MW gas combustion powerplant.

The ENVI-Clean™ system removes most of the sulphur dioxide, particulate matter, greenhouse gases and other hazardous air pollutants from the flue gases produced by the combustion of coal, biomass, municipal solid waste, diesel and other fuels.

| 3 |

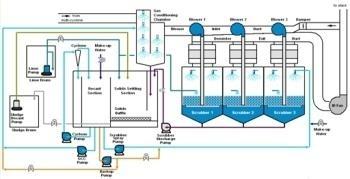

The ENVI-Clean™ system is comprised of five components:

| ● | an induced draft fan (“ID fan”); | |

| ● | a gas conditioning chamber; | |

| ● | the ENVI-Clean™ unit; | |

| ● | a demister; and | |

| ● | settling tanks. |

The ID fan creates the pressure differential required to force the gas through the scrubbing fluid suspended on each head and move it through the other components in the system. The gas conditioning chamber cools the hot flue gas prior to entering the ENVI-Clean™ System. The ENVI-Clean™ System contains the heads and the demister pads at the exhaust exit. The neutralizing fluid is constantly circulated and cleaned by mechanical means with the contaminated component of the separation going to a settling tank prior to dewatering. The settled solids are disposed of with the bottom ash produced by the combustion process.

The ENVI-CES™ technology forces 100% of the polluted exhaust flue gas into the neutralizing fluid to produce a highly turbulent interaction between the target pollutants and the fluid. The aggressive mixing produces small bubbles which create a very high surface contact area between the exhaust gas and fluid to enhance the transfer of particulate and targeted gaseous and hazardous pollutants from the exhaust to the fluid.

Schematic of the ENVI-Clean™ Emission’s System as installed for Biomass applications

Unique to the ENVI approach is the introduction of the gas in the lower section of the ENVI-Clean™ unit which makes the greatest portion of its cross section available for fluid–gas interaction. This permits a smaller and highly flexible footprint. Furthermore, the system design allows for multiple heads each containing different neutralizing fluids to remove various pollutants from the flue gas. The ordered removal of acid and greenhouse gases within a single unit makes the system highly desirable by industries whose fuels contain multiple contaminants. The resulting ENVI-Clean™ unit has high efficiency and is very simple to operate.

The neutralizing solution is selected to remove targeted pollutants: limestone and hydrated lime are used to neutralize the scrubbing solution for the removal of acid gases such as sulphur dioxide, hydrogen chloride and hydrogen fluoride. The unique design of the ENVI system allows for the sequential removal of pollutants by stacking heads and utilizing different neutralizing chemistry in each operating unit. This provides industry with a system that fulfills multiple applications.

| 4 |

The ENVI-Clean™ system has numerous new and retrofit applications:

| ● | coal and coal waste fuelled CFBC boilers; | |

| ● | pulverized coal and stoker-grate boilers; | |

| ● | heavy oil fired boilers; | |

| ● | biomass and waste to energy boilers; | |

| ● | lime kilns, dryers, shredders and foundries; | |

| ● | industrial exhaust scrubbing of particulates and acid gases; | |

| ● | diesel engines, large marine and stationary engines; and | |

| ● | sewage sludge, hazardous waste and MSW incinerators. |

Significant transactions

Management, assisted by PGG, identified an opportunity to build a business focused on marketing, developing and acquiring technologies designed to improve the environment by reducing pollution. To this end, we entered into and closed an assignment and share transfer agreement, on June 14, 2012, for the assignment of a representation agreement and the acquisition of a company involved in the environmental technology industry.

The assignment and share transfer agreement provided for the acquisition of 100% of the issued and outstanding shares of Pacific Green Technologies Limited, formerly PGG’s subsidiary in the United Kingdom. Additionally, PGG has assigned to our company a ten year exclusive worldwide representation agreement with EnviroTechnologies Inc., (formerly EnviroResolutions, Inc.), a Delaware corporation, to market and sell EnviroTechnologies’ current and future environmental technologies. The representation agreement entitles PGG to a commission of 20% of all sales (net of taxes) generated by EnviroTechnologies. Pursuant to the terms of the assignment and share transfer agreement, all rights and obligations under the representation agreement have been transferred to our company. We currently anticipate that sales under the representation agreement will be our sole source of revenue for the foreseeable future. We had intended to complete an acquisition of EnviroTechnologies, as this would have been a logical step in our development. However, as discussed herein, we have settled with EnviroTechnologies as an alternative.

Both Sichel and PGG are wholly owned subsidiaries of the Hookipa Trust. PGG’s wholly owned subsidiary was Pacific Green Technologies Limited. As a result, we acquired Pacific Green Technologies Limited from PGG. Sichel is a significant shareholder of our company and also provides us with consulting services. The sole director of Sichel is also the sole director of PGG. Further, PGG is a significant shareholder of EnviroTechnologies.

The assignment and share transfer agreement closed on June 14, 2012 via the issuance of 5,000,000 shares of our common stock as well as a $5,000,000 promissory note to PGG. We have consequently undertaken the operations of Pacific Green Technologies Limited and PGG’s obligations under the representation agreement.

Full consideration contemplated by the assignment and share transfer agreement was $25,000,000 satisfied through the issue of 5,000,000 new shares of our common stock at a price of $4 per share with the balance of $5,000,000 structured as a promissory note over the next five years as follows:

| ● | June 12, 2013, $1,000,000; | |

| ● | June 12, 2014, $1,000,000; | |

| ● | June 12, 2015, $1,000,000; | |

| ● | June 12, 2016, $1,000,000 and; | |

| ● | June 12, 2017, $1,000,000. |

| 5 |

Under the terms of the promissory note, the loan repayments specified above shall not exceed the amount we earn under the terms of the representation agreement. If we are unable to meet the repayment schedule set out above, PGG will have the option to either roll over any unpaid portion to the following payment date or to convert the outstanding amount into new shares of our common stock. However, the entire amount of the promissory note is due upon the maturity date on the fifth anniversary. On September 25, 2017, the Company and PGG agreed to a settlement of the outstanding promissory by way of a subscription agreement for 5,000,000 shares of common stock at $1.00 per share.

The initial total consideration of $25,000,000 was a purchase price not determined under U.S. GAAP, and both the $25,000,000 total price and the deemed price of $4 per share does not represent the fair value of the stock issued or a value used in accounting for the acquisition. The number of shares issued and the terms of the promissory note were negotiated between the parties and are intended to represent full consideration for the acquisition of Pacific Green Technologies Limited and the representation agreement.

Our management believes that the ENVI-Clean™ system has significant competitive advantages in the market for emission control systems including:

| 1. | Efficiency: tests performed at an 84MW coal power plant in West Virginia (USA) indicate that the ENVI-Clean™ system removed on average 99.3% of sulfur dioxide over a three day period from the plant’s emissions; | |

| 2. | Low Capital Cost: the system has a compact and flexible footprint relative to competitive products. For electricity generation applications, EnviroTechnologies’ system is priced for market at approximately $90 per kilowatt of electricity generation. In comparison, industry consultants state that comparable systems in North America are typically priced at $300-500 per kilowatt (Source: High Energy Services/Babcock & Wilson-wet scrubber systems for S02 removal in North America); | |

| 3. | Low Ongoing Operating Cost: the ENVI-Clean™ system is more affordable in the long term for customers compared to competitor products; | |

| 4. | New and Retrofit Applications: for retrofit applications in particular (as required by the 2011 EPA Boiler MACT Requirements), the system is considered by management to be more compact and adaptable than rival systems; | |

| 5. | Scalability: the ENVI-Clean™ system can be adapted for the largest power stations but also smaller applications such as diesel marine engines. It can also remove multiple pollutants in a single system, unlike much of the competition. |

On October 5, 2011, EnviroResolutions, a British Columbia corporation, signed a contract to supply the ENVI-Clean™ system to a new waste to energy plant being built in Peterborough, United Kingdom (the “Peterborough Contract”). The initial material term and condition of the contract was that EnviroResolutions demonstrate testing of the system that achieved the performance levels represented in regards to emissions by March 31, 2012. This condition was successfully satisfied and confirmed with Peterborough Renewable Energy Limited (“PREL”) prior to the required date. The Peterborough Contract entitles us, as the holder of the representation agreement, to a commission of approximately $4,600,000 before third party agency fees.

Effective March 5, 2013, we entered into a supplemental agreement with EnviroTechnologies and EnviroResolutions. The supplemental agreement amends the representation agreement between PGG and EnviroTechnologies dated June 7, 2010, which was later assigned to us from PGG in connection with an assignment and share transfer agreement dated June 14, 2012. The supplemental agreement entitles our company to a commission of equal to 50% (previously 20%) of any licensing revenue that may be generated by EnviroTechnologies Inc. in respect of its existing and future technologies.

In addition, pursuant to the supplemental agreement, we will receive from EnviroResolutions an amount equal to 50% of any assets or consideration received as compensation from PREL for PREL’s failure to perform under a contingent sale agreement dated October 5, 2011 between EnviroResolutions and PREL. We will receive the fee for our assistance to EnviroResolutions during their negotiations with PREL regarding PREL’s failure to perform. The fee, if any, provided to us will not constitute any repayment of our loans that were made to EnviroResolutions.

The supplemental agreement supplements the Peterborough Contract dated October 5, 2011 entered into among EnviroResolutions, PREL and GEPL. Pursuant to the Peterborough Contract, EnviroResolutions was to supply PREL with a wet scrubbing emission control system to a proposed waste to energy plant being built in Peterborough, United Kingdom.

| 6 |

Information on Pacific Green Technologies Limited

Pacific Green Technologies Limited is a limited liability company incorporated under the laws of England and Wales on April 5, 2011 (“PGT”). The director of PGT was Mr. Joseph Grigor Kelly. On November 7, 2012, Mr. Joseph Grigor Kelly tendered his resignation to the board of directors. PGT has no employees. Concurrently, Neil Carmichael consented to and was appointed as the sole director and chief executive and financial officer of PGT.

The purpose of incorporating PGT was to utilize local knowledge and contacts to build a platform for sales in the following regions: Western Europe, Eastern Europe, Russian Federation, Turkey, Middle East, Azerbaijan, Kazakhstan and Africa. However, our company has found that the cost to have physical presence in England far out weights the benefit. As a result, PGT is now in the process of being dissolved as of the date of the filing of this annual report.

Information on Pacific Green Energy Parks Limited

Pacific Green Energy Parks Limited (“PGEP”) sees an opportunity to develop renewable power stations with capacities up to 50MW in the biomass and waste to energy sectors. In addition to their positive impact on the world’s environment, these projects have the potential to deliver a sustainable post-tax equity IRR and may provide our company with an opportunity to deploy its technologies. To this end our company has been identifying and investigating appropriate projects worldwide.

On March 26, 2012, PGEP reached an agreement with the shareholders of Energy Park Sutton Bridge Limited (“EPSB”), whereby PGEP would fund a planning application for the development of a biomass energy plant in return for a 75% shareholding in EPSB. EPSB was incorporated in the UK in 2009 to develop a 49 MW biomass energy plant in Sutton Bridge, Lincolnshire, UK. A planning application for EPSB was submitted to South Holland District Council (“SHDC”) on September 4, 2012.

On March 5, 2013, PGEP acquired the remaining 25% of EPSB. On May 8, 2013, EPSB secured planning permission for a 49MW biomass power plant at Sutton Bridge, Lincolnshire.

The facility will have an installed energy capacity of 49MW. The export capacity of the facility will be circa 44MW. The electricity will be supplied to the National Grid. Heat from the operation will be used within the facility and the ancillary buildings whilst off-take points will be provided for future combined heat and power needs in the area. The location of the plant alongside an existing industrial estate and in proximity of an area proposed for future industrial expansion makes the realization of the potential for combined heat and power more likely than in other possible locations. EPSB has secured options to purchase the freehold of the Energy Park site from the land owners.

Biomass is considered to be carbon neutral because the quantity of CO2 released during combustion is the same as that absorbed by plants as a result of photosynthesis during their growth. This differs from fossil fuels in that, although both originating from organic matter, the carbon in fossil fuels has been locked away for millions of years, and when released during combustion, results in a net increase in CO2 levels in the atmosphere.

Biomass is also considered environmentally sustainable as in many cases it is derived from by-products of other industries such as agriculture and forestry management. This contains a closed carbon cycle with no net increase in atmospheric CO2 levels. As a result, EPSB will be entitled to renewables obligation certificates (“ROCs”) under the UK’s Renewable Obligation regime. As of April 2016, pure biomass will be afforded 1.4 ROCs/MWh of electricity produced, for a 20 year tariff period. EPSB’s forecasts assume:

EPSB will recover energy from virgin wood using steam turbine technology. The plant will require approximately 325,000 tonnes of virgin wood per annum (“Feedstock”).

Following discussions with industry experts, engineers, consultants and financiers, our company estimates that EPSB should cost approximately £165,000,000 to construct. Once the project is “spade ready”, construction should take 2 years. Previously, we anticipated that the project would be “spade ready” by March 2014. However, our company’s application for planning consent was not accepted by council and we resubmitted our application on June 20, 2014. The EPC contractor will provide a fixed cost turnkey completion guarantee. Planning consent was again turned down April 2015.

| 7 |

A detailed carbon assessment has been submitted within the EIA presenting the carbon savings offered by the operation of the facility.

The project will deliver combined heat and power (“CHP”) infrastructure. Our company is investigating potential opportunities for supplying local heat customers at both existing and potential new developments off site. EPSB will maintain an open dialogue with the local authority and will ensure that an appropriate boiler and turbine design is selected to facilitate the distribution of heat.

Currently our company is identifying and assessing further renewable power plant developments that are complimentary to the use of ENVI-Emissions Systems where possible.

Securing additional financial and human capital

We have limited capital and four directors. It is anticipated that we will expand our management team to fully exploit the representation agreement and it will also therefore be necessary to raise financial capital. We anticipate that we will need to raise additional financial capital through equity issuances, debt instruments and guarantees.

Form of any subsequent acquisitions

The manner in which we participate in an opportunity will depend upon the nature of the opportunity, our respective needs and desires and those of the promoters of the opportunity, and our relative negotiating strength compared to that of such promoters.

It is likely that we will acquire further participations in business opportunities through the issuance of our common stock, or other of our securities. Although the terms of any such transaction cannot be predicted, it should be noted that in certain circumstances the criteria for determining whether or not an acquisition is a so-called “tax free” reorganization under Section 368(a)(1) of the Internal Revenue Code of 1986, as amended, or the Code, depends upon whether the owners of the acquired business own 80% or more of the voting stock of the surviving entity. If a transaction were structured to take advantage of these provisions rather than other “tax free” provisions provided under the Code, all prior stockholders would in such circumstances retain 20% or less of the total issued and outstanding shares of the surviving entity. Under other circumstances, depending upon the relative negotiating strength of the parties, prior stockholders may retain substantially less than 20% of the total issued and outstanding shares of the surviving entity. This could result in substantial additional dilution to the equity of those who were our stockholders prior to such reorganization.

Our stockholders will likely not have control of a majority of our voting securities following a reorganization transaction. As part of such a transaction, our directors may resign and one or more new directors may be appointed without any vote by stockholders.

In the case of an acquisition, the transaction may be accomplished upon the sole determination of management without any vote or approval by our stockholders. In the case of a statutory merger or consolidation directly involving our company, it will likely be necessary to call a stockholders’ meeting and obtain the approval of the holders of a majority of our outstanding securities. The necessity to obtain such stockholder approval may result in delay and additional expense in the consummation of any proposed transaction and will also give rise to certain appraisal rights to dissenting stockholders. Most likely, management will seek to structure any such transaction so as not to require stockholder approval.

It is anticipated that the investigation of specific business opportunities and the negotiation, drafting and execution of relevant agreements, disclosure documents and other instruments will require substantial management time and attention and substantial cost for accountants, attorneys and others. If a decision is made not to participate in a specific business opportunity, the costs theretofore incurred in the related investigation might not be recoverable. Furthermore, even if an agreement is reached for the participation in a specific business opportunity, the failure to consummate that transaction may result in the loss to us of the related costs incurred.

| 8 |

Other Business Matters

On April 3, 2013, we entered into and closed a share exchange agreement with certain shareholders of EnviroTechnologies. Pursuant to the terms of the share exchange agreement, we agreed to acquire 17,653,872 issued and outstanding common shares of EnviroTechnologies from the shareholders in exchange for the issuance of 1,765,395 shares of the common stock of our company. We issued an aggregate of 1,765,395 common shares to 47 shareholders.

On April 25, 2013, we entered into and closed share exchange agreements with certain shareholders of EnviroTechnologies. Pursuant to the terms of the share exchange agreement, we agreed to acquire 6,682,357 issued and outstanding common shares of EnviroTechnologies from the shareholders in exchange for the issuance of 668,238 shares of common stock of our company. We issued an aggregate of 668,238 common shares to 20 shareholders.

On May 15, 2013, we entered into and closed a stock purchase agreement with all five of the shareholders of Pacific Green Energy Parks Limited (“PGEP”), a company incorporated in the British Virgin Islands. PGEP is the sole shareholder of Energy Park Sutton Bridge Limited, a company incorporated in the United Kingdom. PGEP is developing a biomass power plant facility and holds an option to purchase the real property upon which the facility will be built.

Pursuant to the stock purchase agreement, we agreed to acquire all of the 1,752 issued and outstanding common shares of PGEP from the shareholders in exchange for:

| 1. | a payment of $100 upon execution of the stock purchase agreement, which has been paid by us; |

| 2. | $14,000,000 paid in common shares in our capital stock at a deemed price at the lower of $4 per share or the average closing price per share of our capital stock in the ten trading days immediately preceding the date of closing of the stock purchase agreement, which have been issued by us; |

| 3. | $3,000,000 payable in common shares of our capital stock at a deemed price at the lower of $4 per share or the average closing price per share of our capital stock in the ten trading days immediately preceding the date upon which PGEP either purchases the property or secures a lease permitting PGEP to operate the facility on the property, which has not yet occurred; and |

| 4. | subject to leasing or purchasing the property and PGEP securing sufficient financing for the construction of the facility, $33,000,000 payable in common shares of our capital stock at a deemed price at the lower of $4 per share or the average closing price per share of our capital stock in the ten trading days immediately preceding the date that PGEP secures sufficient financing for the construction of the facility, which has not yet occurred. |

All consideration from our company to the shareholders has been and will be issued on a pro-rata, pari-passu basis in proportion to the respective number of shares of PGEP sold by each respective shareholder. On May 15, 2013, pursuant to the stock purchase agreement, we issued an aggregate of 3,500,000 common shares, at an agreed upon deemed price of $4 per share, to the five shareholders.

Pacific Green Energy Parks Limited and its wholly owned subsidiary, Energy Park Sutton Bridge, are now subsidiaries of our company.

On May 17, 2013, we entered into a debt settlement agreement with EnviroTechnologies and EnviroResolutions (collectively, the “Debtors”). Pursuant to the terms of the debt settlement agreement, we agreed to release and waive all obligations of the Debtors to repay debts, in the aggregate of $293,406 and CAD$38,079, to us and agreed to return an aggregate of 88,876,443 common shares of EnviroTechnologies to EnviroResolutions. The 88,876,443 common shares of EnviroTechnologies were returned as of June 30, 2016. As consideration for this release and waiver and return of shares, the Debtors agreed to transfer all rights, interests and title to certain intellectual property, the physical embodiments of such intellectual property, and to the supplemental agreement dated March 5, 2013 among EnviroResolutions, PREL and Green Energy Parks Limited (“GEPL”) (collectively, the “Debtors’ Assets”).

| 9 |

The Debtors’ Assets include the intellectual property rights throughout most of the world for the ENVI-Clean™ system, the ENVI-Pure™ system and the ENVI-SEA™ scrubber. The ENVI-Clean™ system removes most of the sulphur dioxide, particulate matter, greenhouse gases and other hazardous air pollutants from the flue gases produced by the combustion of coal, biomass, municipal solid waste, diesel and other fuels. The ENVI-Pure™ emission system combines the ENVI-Clean™ highly effective patent-pending wet scrubbing technology with an innovative wet electrostatic precipitator and a granular activated carbon adsorber to remove particulate matter, acid gases, regulated metals, dioxins and VOCs from the flue gas to levels significantly below those required by strictest international regulations. The ENVI-SEA™ scrubber can be applied to diesel exhaust emissions that require sulphur and particulate matter abatement. Using seawater on a single-pass basis as the scrubbing fluid in combination with its patent pending scrubbing head will provide a highly interactive zone of turbulent mixing for absorption of SO2, particulate matter and other pollutants from the engine’s exhaust.

The following is a brief description of further terms and conditions of the debt settlement agreement that are material to our company:

| 1. | We pay 25% of all funds, if any, received under the supplemental agreement to the Debtors within 14 days upon receipt of funds, if any, pursuant to the supplemental agreement; |

| 2. | We enter into definitive agreements with the Debtors to: |

| a. | license the Debtors’ Assets back to the Debtors, under arm’s length commercial terms, for use in the USA and Canada, with the exception of NRG Energy, Inc. and Edison Mission and affiliates; and | |

| b. | have the Debtors provide engineering services to us on terms to be agreed upon, acting reasonably; |

| 3. | The Debtors pay pro-rata any third party broker fees and legal fees, if any, that are subsequent costs associated with the Supplemental Agreement; and | |

| 4. | the Debtors retain possession of, yet make a pilot-scale scrubber available for rental to our company at a nominal cost. |

On June 11, 2013, we submitted 24,336,229 common shares of EnviroTechnologies to EnviroTechnologies for cancellation pursuant to our debt settlement agreement with EnviroTechnologies and EnviroResolutions dated May 17, 2013.

Pursuant to a debt settlement agreement dated May 17, 2013 among our company, EnviroTechnologies and EnviroResolutions, on November 22, 2013, our company was transferred a 40% shareholding in PREL by GEPL (who had, prior to this transfer, held all the issued and outstanding shares of PREL). PREL is a limited liability company incorporated under the laws of the United Kingdom.

PREL was incorporated by GEPL to develop a 79MWe waste to energy power station at Peterborough, United Kingdom (the “Peterborough Plant”). The Peterborough Plant has full planning permission at 79MWe and environmental agency permits. It is understood that the Peterborough Plant will be built in two stages at a total capital cost of approximately GBP£500 million (approximately US$824,534,442). As of May 17, 2013, PREL owned 20% of Energy Park Investments Limited, the holding company that is currently intended to finance the development of the Peterborough Plant in turn through its wholly owned operating subsidiary Energy Park Peterborough Limited.

On June 17, 2013, we entered into and closed share exchange agreements with certain shareholders of EnviroTechnologies. Pursuant to the terms of the share exchange agreements we acquired 8,061,286 issued and outstanding common shares of EnviroTechnologies from the shareholders in exchange for the issuance of 806,132 shares of common stock of our company. We issued as aggregate of 806,132 shares of common stock to 19 shareholders

| 10 |

On August 6, 2013, we entered into two share exchange agreements with two shareholders of EnviroTechnologies. Pursuant to the terms of the agreements, we acquired 440,000 issued and outstanding common shares of EnviroTechnologies from one shareholder in exchange for shares of common stock of our company on a 1 for 10 basis. Pursuant to the terms of the other agreement, we acquired 600,000 issued and outstanding common shares of EnviroTechnologies from one shareholder in exchange for shares of common stock of our company on a 1 for 15 basis.

On August 27, 2013, we entered into share exchange agreements with certain shareholders of EnviroTechnologies. Pursuant to the terms of the agreements, we acquired 32,463,489 issued and outstanding common shares of EnviroTechnologies from the shareholders in exchange for shares of common stock of our company on a 1 for 10 basis.

On September 13, 2013, we submitted 41,564,775 common shares of EnviroTechnologies to EnviroTechnologies for cancellation pursuant to our debt settlement agreement with EnviroTechnologies and EnviroResolutions dated May 17, 2013.

On September 26, 2013, we entered into an agreement with Andrew Jolly, wherein Dr. Jolly agreed to serve as a director of our company. Pursuant to the agreement, our company is to compensate Dr. Jolly for serving as a director of our company at GBP£2,000 (approximately $3,235) per calendar month. Effective October 1, 2013, we appointed Dr. Jolly as a director of our company. Effective September 1, 2014, the monthly fee for Mr. Jolly was reduced to GBP£1,000 (approximately $1,617).

On October 11, 2013, we entered into share exchange agreements with certain shareholders of EnviroTechnologies. Pursuant to the terms of the agreements, we agreed to acquire 674,107 issued and outstanding common shares of EnviroTechnologies from the shareholders in exchange for shares of common stock of our company on a 1 for 10 basis.

On December 18, 2013, we announced that our company engaged BlueMount Capital to spearhead the development of its proprietary emission control technologies, ENVI-Clean™ and ENVI-Pure™, in the People’s Republic of China (“PRC”). In addition to corporate finance advisory services both within and outside China, BlueMount offers a tailored service to clients wishing to enter the PRC market with a particular emphasis on companies that own proprietary technology, intellectual property and expertise. To that end, BlueMount provides a comprehensive suite of services to enhance the effectiveness and long-term sustainability of foreign brands entering the PRC market via: Our company’s strategic objective is to establish an operating presence in China with established local partners and rapidly rollout its technologies.

On December 27, 2013, we entered into and closed share exchange agreements with certain shareholders of EnviroTechnologies. Pursuant to the terms of the share exchange agreements, we acquired 130,000 issued and outstanding common shares of EnviroTechnologies from the shareholders in exchange for shares of common stock of our company on a 1 for 10 basis. On December 27, 2013, we issued an aggregate of 13,000 common shares to the shareholders of EnviroTechnologies.

On January 27, 2014, we entered into an agreement with Pöyry Management Consulting (UK) Limited. Pursuant to the agreement, Pöyry is to provide consulting services to us. Our company has agreed to compensate Pöyry a minimum of £5,000 (approximately $ 8,293) as consulting fees for the first year of the agreement and a variable hourly rate as set out in the agreement.

On May 27, 2014, we entered into a $200,000 convertible debenture with Intrawest Overseas Limited. Under the terms of the debenture, the amount is unsecured, bears interest at 10% per annum, and is due on May 27, 2015. Pursuant to the agreement, should any portion of loan remain outstanding past maturity the interest will increase to 15% per annum. The note is convertible into shares of common stock 180 days after the date of issuance (November 27, 2014) until maturity at a conversion rate of 75% of the average offer price of our company’s common stock for the 45 days ending one trading day prior to the date the conversion notice is sent by the holder to our company.

| 11 |

Our company analyzed the conversion option under ASC 815, “Accounting for Derivative Instruments and Hedging Activities”, and determined that the conversion feature should be classified as a liability and recorded at fair value due to there being no explicit limit to the number of shares to be delivered upon settlement of the conversion option. In accordance with ASC 815, our company recognized the intrinsic value of the embedded beneficial conversion feature of $33,922. On November 27, 2014, the note became convertible resulting in our company recording a derivative liability of $33,922 with a corresponding adjustment to loss on change in fair value of derivative liabilities.

On June 12, 2014, we entered into a $100,000 convertible debenture with Gerstle Consulting Pty Limited. Under the terms of the debenture, the amount is unsecured, bears interest at 10% per annum, and is due on June 12, 2015. Pursuant to the agreement, should any portion of loan remain outstanding past maturity the interest will increase to 15% per annum. The note is convertible into shares of common stock 180 days after the date of issuance (December 12, 2014) until maturity at a conversion rate of 75% of the average closing bid prices of our company’s common stock for the 45 days ending one trading day prior to the date the conversion notice is sent by the holder to our company.

Our company analyzed the conversion option under ASC 815, “Accounting for Derivative Instruments and Hedging Activities”, and determined that the conversion feature should be classified as a liability and recorded at fair value due to there being no explicit limit to the number of shares to be delivered upon settlement of the conversion option. In accordance with ASC 815, our company recognized the intrinsic value of the embedded beneficial conversion feature of $9,793. On December 12, 2014, the note became convertible resulting in our company recording a derivative liability of $9,793 with a corresponding adjustment to loss on change in fair value of derivative liabilities.

On June 30, 2015, through our wholly owned subsidiary, Pacific Green Energy Parks Limited, we purchased all of the issued and outstanding shares in Pacific Green Technologies Asia Limited for $1.00 from Alexander Shead.

We entered into an agreement dated July 20, 2015 with Mr. Alexander Shead. Pursuant to this agreement, Mr. Shead has agreed to serve as a director of our company. As a director of our company, Mr. Shead shall be compensated $1,000 for every calendar month of the term of the agreement. The term of the agreement is for 12 months. On July 20, 2015, we appointed Mr. Shead as a director of our company.

On September 22, 2015, our company entered into a consulting agreement (the “Agreement”) with Midam Ventures, LLC (“Midam”) wherein Midam will provide investor relations and business advisory services to us from September 23, 2015 to March 23, 2016. Any compensation described in the Agreement shall be deemed earned and vested by Midam even in the case of early termination of the Agreement.

Pursuant to the terms of the Agreement, we will to pay $30,000 in cash and 200,000 common restricted shares of our company to Midam. Effective October 20, 2015, we issued all of the shares pursuant to an exemption from registration relying on the provisions of Rule 506 of Regulation D promulgated under the Securities Act of 1933, as amended.

On October 24, 2015, our company entered into a marketing and consulting agreement with Red Rock Marketing Media, Inc. (“Red Rock”) wherein Red Rock will provide investor relations and business advisory services to us for a period of 40 business days starting on or before the 10 business days after Red Rock receives compensation from our company. Pursuant to the terms of the Agreement, we will to pay $100,000 in cash by October 29, 2015.

On October 27, 2015, our company entered into a loan agreement with a significant shareholder for proceeds of approximately $4,231. The loan is unsecured, bears an interest rate of US Prime Rate plus 4%, and is due on demand.