Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2018

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Exact name of registrant as specified in its charter | State or other jurisdiction of incorporation or organization | Commission File Number | I.R.S. Employer Identification No. | |||

Windstream Holdings, Inc. | Delaware | 001-32422 | 46-2847717 | |||

Windstream Services, LLC | Delaware | 001-36093 | 20-0792300 | |||

4001 Rodney Parham Road | ||||

Little Rock, Arkansas | 72212 | |||

(Address of principal executive offices) | (Zip Code) | |||

(501) 748-7000 | ||||

(Registrants’ telephone number, including area code) | ||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Windstream Holdings, Inc. | ý YES ¨ NO | |||

Windstream Services, LLC | ý YES ¨ NO | |||

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Windstream Holdings, Inc. | ý YES ¨ NO | |||

Windstream Services, LLC | ý YES ¨ NO | |||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of large accelerated filer, accelerated filer, smaller reporting company, and emerging growth company in Rule 12b-2 of the Exchange Act:

Windstream Holdings, Inc. | Large accelerated filer ý | Accelerated filer ¨ | ||

Non-accelerated filer ¨ | (Do not check if a smaller reporting company) | |||

Smaller reporting company ¨ | ||||

Emerging growth company ¨ | ||||

Windstream Services, LLC | Large accelerated filer ¨ | Accelerated filer ¨ | ||

Non-accelerated filer ý | (Do not check if a smaller reporting company) | |||

Smaller reporting company ¨ | ||||

Emerging growth company ¨ | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Windstream Holdings, Inc. | ¨ YES ¨ NO | |||

Windstream Services, LLC | ¨ YES ¨ NO | |||

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act).

Windstream Holdings, Inc. | ¨ YES ý NO | |||

Windstream Services, LLC | ¨ YES ý NO | |||

As of August 6, 2018, 42,938,115 shares of common stock of Windstream Holdings, Inc.were outstanding. Windstream Holdings, Inc. holds a 100 percent interest in Windstream Services, LLC.

This Form 10-Q is a combined quarterly report being filed separately by two registrants: Windstream Holdings, Inc. and Windstream Services, LLC. Windstream Services, LLC is a direct, wholly-owned subsidiary of Windstream Holdings, Inc. Accordingly, Windstream Services, LLC meets the conditions set forth in general instruction H(1)(a) and (b) of Form 10-Q and is therefore filing this form with the reduced disclosure format. Unless the context indicates otherwise, the use of the terms “Windstream,” “we,” “us” or “our” shall refer to Windstream Holdings, Inc. and its subsidiaries, including Windstream Services, LLC, and the term “Windstream Services” shall refer to Windstream Services, LLC and its subsidiaries.

The Exhibit Index is located on page 91. | ||

WINDSTREAM HOLDINGS, INC.

WINDSTREAM SERVICES, LLC

FORM 10-Q

TABLE OF CONTENTS

Page No. | ||

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 1. | ||

Item 1A. | ||

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | * |

Item 3. | Defaults Upon Senior Securities | * |

Item 4. | Mine Safety Disclosures | * |

Item 5. | Other Information | * |

Item 6. | ||

_____________

* | No reportable information under this item. |

1

WINDSTREAM HOLDINGS, INC.

WINDSTREAM SERVICES, LLC

FORM 10-Q

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

WINDSTREAM HOLDINGS, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

(Millions, except per share amounts) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues and sales: | ||||||||||||||||

Service revenues | $ | 1,424.6 | $ | 1,465.6 | $ | 2,860.0 | $ | 2,810.0 | ||||||||

Product sales | 19.8 | 26.0 | 38.7 | 47.3 | ||||||||||||

Total revenues and sales | 1,444.4 | 1,491.6 | 2,898.7 | 2,857.3 | ||||||||||||

Costs and expenses: | ||||||||||||||||

Cost of services (exclusive of depreciation and amortization included below) | 722.8 | 750.7 | 1,459.7 | 1,434.5 | ||||||||||||

Cost of products sold | 18.2 | 29.7 | 35.0 | 50.5 | ||||||||||||

Selling, general and administrative | 224.5 | 226.4 | 453.3 | 440.2 | ||||||||||||

Depreciation and amortization | 370.7 | 362.4 | 752.5 | 700.9 | ||||||||||||

Merger, integration and other costs | 14.1 | 16.4 | 21.4 | 73.7 | ||||||||||||

Restructuring charges | 5.8 | 3.5 | 19.5 | 10.9 | ||||||||||||

Total costs and expenses | 1,356.1 | 1,389.1 | 2,741.4 | 2,710.7 | ||||||||||||

Operating income | 88.3 | 102.5 | 157.3 | 146.6 | ||||||||||||

Other income, net | 12.0 | 4.2 | 9.7 | 6.8 | ||||||||||||

Net loss on early extinguishment of debt | — | — | — | (3.2 | ) | |||||||||||

Interest expense | (224.4 | ) | (214.4 | ) | (447.5 | ) | (426.2 | ) | ||||||||

Loss before income taxes | (124.1 | ) | (107.7 | ) | (280.5 | ) | (276.0 | ) | ||||||||

Income tax benefit | (30.4 | ) | (39.6 | ) | (65.4 | ) | (96.6 | ) | ||||||||

Net loss | $ | (93.7 | ) | $ | (68.1 | ) | $ | (215.1 | ) | $ | (179.4 | ) | ||||

Basic and diluted loss per share: | ||||||||||||||||

Net loss | ($2.30 | ) | ($1.83 | ) | ($5.51 | ) | ($5.75 | ) | ||||||||

See the accompanying notes to the unaudited interim consolidated financial statements.

2

WINDSTREAM HOLDINGS, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

(Millions) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

Net loss | $ | (93.7 | ) | $ | (68.1 | ) | $ | (215.1 | ) | $ | (179.4 | ) | ||||

Other comprehensive income (loss): | ||||||||||||||||

Interest rate swaps: | ||||||||||||||||

Unrealized gain (loss) on designated interest rate swaps | 4.9 | (5.3 | ) | 19.7 | (1.9 | ) | ||||||||||

Amortization of net unrealized losses on de-designated interest rate swaps | 0.8 | 1.4 | 1.7 | 2.9 | ||||||||||||

Income tax (expense) benefit | (1.5 | ) | 1.5 | (5.5 | ) | (0.4 | ) | |||||||||

Change in interest rate swaps | 4.2 | (2.4 | ) | 15.9 | 0.6 | |||||||||||

Postretirement and pension plans: | ||||||||||||||||

Prior service credit arising during the period | 2.7 | — | 2.7 | — | ||||||||||||

Change in net actuarial gain for employee benefit plans | 5.4 | 1.4 | 5.4 | 1.4 | ||||||||||||

Amounts included in net periodic benefit cost: | ||||||||||||||||

Amortization of net actuarial loss | — | 0.1 | 0.1 | 0.1 | ||||||||||||

Amortization of prior service credits | (1.3 | ) | (0.2 | ) | (2.6 | ) | (0.4 | ) | ||||||||

Income tax expense | (0.9 | ) | (0.5 | ) | (0.6 | ) | (0.4 | ) | ||||||||

Change in postretirement and pension plans | 5.9 | 0.8 | 5.0 | 0.7 | ||||||||||||

Other comprehensive income (loss) | 10.1 | (1.6 | ) | 20.9 | 1.3 | |||||||||||

Comprehensive loss | $ | (83.6 | ) | $ | (69.7 | ) | $ | (194.2 | ) | $ | (178.1 | ) | ||||

See the accompanying notes to the unaudited interim consolidated financial statements.

3

WINDSTREAM HOLDINGS, INC.

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(Millions, except par value) | June 30, 2018 | December 31, 2017 | ||||||

Assets | ||||||||

Current Assets: | ||||||||

Cash and cash equivalents | $ | 45.3 | $ | 43.4 | ||||

Accounts receivable (less allowance for doubtful | ||||||||

accounts of $25.3 and $29.7, respectively) | 623.9 | 643.0 | ||||||

Inventories | 85.0 | 93.0 | ||||||

Prepaid expenses and other | 181.0 | 154.3 | ||||||

Total current assets | 935.2 | 933.7 | ||||||

Goodwill | 2,873.9 | 2,842.4 | ||||||

Other intangibles, net | 1,349.4 | 1,454.4 | ||||||

Net property, plant and equipment | 5,156.6 | 5,391.8 | ||||||

Deferred income taxes | 416.2 | 370.8 | ||||||

Other assets | 108.5 | 91.2 | ||||||

Total Assets | $ | 10,839.8 | $ | 11,084.3 | ||||

Liabilities and Shareholders’ Deficit | ||||||||

Current Liabilities: | ||||||||

Current maturities of long-term debt | $ | 17.9 | $ | 169.3 | ||||

Current portion of long-term lease obligations | 200.1 | 188.6 | ||||||

Accounts payable | 495.2 | 494.0 | ||||||

Advance payments and customer deposits | 199.7 | 207.3 | ||||||

Accrued taxes | 87.5 | 89.5 | ||||||

Accrued interest | 62.2 | 52.6 | ||||||

Other current liabilities | 278.9 | 342.1 | ||||||

Total current liabilities | 1,341.5 | 1,543.4 | ||||||

Long-term debt | 5,867.9 | 5,674.6 | ||||||

Long-term lease obligations | 4,540.5 | 4,643.3 | ||||||

Other liabilities | 496.4 | 521.9 | ||||||

Total liabilities | 12,246.3 | 12,383.2 | ||||||

Commitments and Contingencies (See Note 15) | ||||||||

Shareholders’ Deficit: | ||||||||

Common stock, $.0001 par value, 75.0 shares authorized, | ||||||||

42.7 and 36.5 shares issued and outstanding, respectively | — | — | ||||||

Additional paid-in capital | 1,243.2 | 1,191.9 | ||||||

Accumulated other comprehensive income | 44.0 | 21.4 | ||||||

Accumulated deficit | (2,693.7 | ) | (2,512.2 | ) | ||||

Total shareholders’ deficit | (1,406.5 | ) | (1,298.9 | ) | ||||

Total Liabilities and Shareholders’ Deficit | $ | 10,839.8 | $ | 11,084.3 | ||||

See the accompanying notes to the unaudited interim consolidated financial statements.

4

WINDSTREAM HOLDINGS, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

Six Months Ended June 30, | ||||||||

(Millions) | 2018 | 2017 | ||||||

Cash Flows from Operating Activities: | ||||||||

Net loss | $ | (215.1 | ) | $ | (179.4 | ) | ||

Adjustments to reconcile net loss to net cash provided from operations: | ||||||||

Depreciation and amortization | 752.5 | 700.9 | ||||||

Provision for doubtful accounts | 15.2 | 19.7 | ||||||

Share-based compensation expense | 18.4 | 32.4 | ||||||

Deferred income taxes | (64.7 | ) | (97.3 | ) | ||||

Net loss on early extinguishment of debt | — | 3.2 | ||||||

Other, net | 4.3 | 7.9 | ||||||

Changes in operating assets and liabilities, net | ||||||||

Accounts receivable | 5.8 | 15.7 | ||||||

Prepaid income taxes | (4.7 | ) | (5.2 | ) | ||||

Prepaid expenses and other | 7.3 | (14.3 | ) | |||||

Accounts payable | 17.2 | (56.3 | ) | |||||

Accrued interest | 9.9 | (6.8 | ) | |||||

Accrued taxes | (9.3 | ) | 2.0 | |||||

Other current liabilities | (18.7 | ) | (20.1 | ) | ||||

Other liabilities | 7.0 | 1.5 | ||||||

Other, net | 14.6 | (29.0 | ) | |||||

Net cash provided from operating activities | 539.7 | 374.9 | ||||||

Cash Flows from Investing Activities: | ||||||||

Additions to property, plant and equipment | (406.3 | ) | (507.8 | ) | ||||

Cash acquired from EarthLink | — | 5.0 | ||||||

Acquisition of MASS | (37.6 | ) | — | |||||

Other, net | (8.8 | ) | (11.8 | ) | ||||

Net cash used in investing activities | (452.7 | ) | (514.6 | ) | ||||

Cash Flows from Financing Activities: | ||||||||

Dividends paid to shareholders | — | (35.6 | ) | |||||

Proceeds from issuance of stock | 11.1 | 9.6 | ||||||

Repayments of debt and swaps | (413.1 | ) | (1,282.2 | ) | ||||

Proceeds from debt issuance | 450.0 | 1,535.6 | ||||||

Debt issuance costs | (11.6 | ) | (7.3 | ) | ||||

Payments under long-term lease obligations | (91.4 | ) | (82.2 | ) | ||||

Payments under capital lease obligations | (27.7 | ) | (22.0 | ) | ||||

Other, net | (2.4 | ) | (10.6 | ) | ||||

Net cash (used in) provided from financing activities | (85.1 | ) | 105.3 | |||||

Increase (decrease) in cash and cash equivalents | 1.9 | (34.4 | ) | |||||

Cash and Cash Equivalents: | ||||||||

Beginning of period | 43.4 | 59.1 | ||||||

End of period | $ | 45.3 | $ | 24.7 | ||||

Supplemental Cash Flow Disclosures: | ||||||||

Interest paid, net of interest capitalized | $ | 428.9 | $ | 417.7 | ||||

Income taxes (refunded) paid, net | $ | (15.1 | ) | $ | 1.3 | |||

See the accompanying notes to the unaudited interim consolidated financial statements.

5

WINDSTREAM HOLDINGS, INC.

CONSOLIDATED STATEMENT OF SHAREHOLDERS’ DEFICIT (UNAUDITED)

(Millions, except per share amounts) | Common Stock and Additional Paid-In Capital | Accumulated Other Comprehensive Income | Accumulated Deficit | Total | ||||||||||||

Balance at December 31, 2017 | $ | 1,191.9 | $ | 21.4 | $ | (2,512.2 | ) | $ | (1,298.9 | ) | ||||||

Cumulative effect adjustments, net of tax: | ||||||||||||||||

Adoption of ASU 2014-09 (See Note 1) | — | — | 35.3 | 35.3 | ||||||||||||

Adoption of ASU 2017-12 (See Note 1) | — | 1.7 | (1.7 | ) | — | |||||||||||

Net loss | — | — | (215.1 | ) | (215.1 | ) | ||||||||||

Other comprehensive income (loss), net of tax: | ||||||||||||||||

Change in postretirement and pension plans | — | 5.0 | — | 5.0 | ||||||||||||

Amortization of net unrealized losses on de-designated interest rate swaps | — | 1.2 | — | 1.2 | ||||||||||||

Change in designated interest rate swaps | — | 14.7 | — | 14.7 | ||||||||||||

Comprehensive income (loss) | — | 20.9 | (215.1 | ) | (194.2 | ) | ||||||||||

Share-based compensation | 7.4 | — | — | 7.4 | ||||||||||||

Stock issued under equity distribution agreement | 11.1 | — | — | 11.1 | ||||||||||||

Stock issued for pension contribution | 5.8 | — | — | 5.8 | ||||||||||||

Stock issued to employee savings plan | 28.3 | — | — | 28.3 | ||||||||||||

Taxes withheld on vested restricted stock and other | (1.3 | ) | — | — | (1.3 | ) | ||||||||||

Balance at June 30, 2018 | $ | 1,243.2 | $ | 44.0 | $ | (2,693.7 | ) | $ | (1,406.5 | ) | ||||||

See the accompanying notes to the unaudited interim consolidated financial statements.

6

WINDSTREAM SERVICES, LLC

CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

(Millions) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues and sales: | ||||||||||||||||

Service revenues | $ | 1,424.6 | $ | 1,465.6 | $ | 2,860.0 | $ | 2,810.0 | ||||||||

Product sales | 19.8 | 26.0 | 38.7 | 47.3 | ||||||||||||

Total revenues and sales | 1,444.4 | 1,491.6 | 2,898.7 | 2,857.3 | ||||||||||||

Costs and expenses: | ||||||||||||||||

Cost of services (exclusive of depreciation and amortization included below) | 722.8 | 750.7 | 1,459.7 | 1,434.5 | ||||||||||||

Cost of products sold | 18.2 | 29.7 | 35.0 | 50.5 | ||||||||||||

Selling, general and administrative | 223.8 | 225.6 | 452.1 | 439.1 | ||||||||||||

Depreciation and amortization | 370.7 | 362.4 | 752.5 | 700.9 | ||||||||||||

Merger, integration and other costs | 14.1 | 16.4 | 21.4 | 73.7 | ||||||||||||

Restructuring charges | 5.8 | 3.5 | 19.5 | 10.9 | ||||||||||||

Total costs and expenses | 1,355.4 | 1,388.3 | 2,740.2 | 2,709.6 | ||||||||||||

Operating income | 89.0 | 103.3 | 158.5 | 147.7 | ||||||||||||

Other income, net | 12.0 | 4.2 | 9.7 | 6.8 | ||||||||||||

Net loss on early extinguishment of debt | — | — | — | (3.2 | ) | |||||||||||

Interest expense | (224.4 | ) | (214.4 | ) | (447.5 | ) | (426.2 | ) | ||||||||

Loss before income taxes | (123.4 | ) | (106.9 | ) | (279.3 | ) | (274.9 | ) | ||||||||

Income tax benefit | (30.2 | ) | (39.3 | ) | (65.1 | ) | (96.2 | ) | ||||||||

Net loss | $ | (93.2 | ) | $ | (67.6 | ) | $ | (214.2 | ) | $ | (178.7 | ) | ||||

See the accompanying notes to the unaudited interim consolidated financial statements.

7

WINDSTREAM SERVICES, LLC

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

(Millions) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

Net loss | $ | (93.2 | ) | $ | (67.6 | ) | $ | (214.2 | ) | $ | (178.7 | ) | ||||

Other comprehensive income (loss): | ||||||||||||||||

Interest rate swaps: | ||||||||||||||||

Unrealized gain (loss) on designated interest rate swaps | 4.9 | (5.3 | ) | 19.7 | (1.9 | ) | ||||||||||

Amortization of net unrealized losses on de-designated interest rate swaps | 0.8 | 1.4 | 1.7 | 2.9 | ||||||||||||

Income tax (expense) benefit | (1.5 | ) | 1.5 | (5.5 | ) | (0.4 | ) | |||||||||

Change in interest rate swaps | 4.2 | (2.4 | ) | 15.9 | 0.6 | |||||||||||

Postretirement and pension plans: | ||||||||||||||||

Prior service credit arising during the period | 2.7 | — | 2.7 | — | ||||||||||||

Change in net actuarial gain for employee benefit plans | 5.4 | 1.4 | 5.4 | 1.4 | ||||||||||||

Amounts included in net periodic benefit cost: | ||||||||||||||||

Amortization of net actuarial loss | — | 0.1 | 0.1 | 0.1 | ||||||||||||

Amortization of prior service credits | (1.3 | ) | (0.2 | ) | (2.6 | ) | (0.4 | ) | ||||||||

Income tax expense | (0.9 | ) | (0.5 | ) | (0.6 | ) | (0.4 | ) | ||||||||

Change in postretirement and pension plans | 5.9 | 0.8 | 5.0 | 0.7 | ||||||||||||

Other comprehensive income (loss) | 10.1 | (1.6 | ) | 20.9 | 1.3 | |||||||||||

Comprehensive loss | $ | (83.1 | ) | $ | (69.2 | ) | $ | (193.3 | ) | $ | (177.4 | ) | ||||

See the accompanying notes to the unaudited interim consolidated financial statements.

8

WINDSTREAM SERVICES, LLC

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(Millions) | June 30, 2018 | December 31, 2017 | ||||||

Assets | ||||||||

Current Assets: | ||||||||

Cash and cash equivalents | $ | 45.3 | $ | 43.4 | ||||

Accounts receivable (less allowance for doubtful | ||||||||

accounts of $25.3 and $29.7, respectively) | 623.9 | 643.0 | ||||||

Inventories | 85.0 | 93.0 | ||||||

Prepaid expenses and other | 181.0 | 154.3 | ||||||

Total current assets | 935.2 | 933.7 | ||||||

Goodwill | 2,873.9 | 2,842.4 | ||||||

Other intangibles, net | 1,349.4 | 1,454.4 | ||||||

Net property, plant and equipment | 5,156.6 | 5,391.8 | ||||||

Deferred income taxes | 416.2 | 370.8 | ||||||

Other assets | 108.5 | 91.2 | ||||||

Total Assets | $ | 10,839.8 | $ | 11,084.3 | ||||

Liabilities and Member Deficit | ||||||||

Current Liabilities: | ||||||||

Current maturities of long-term debt | $ | 17.9 | $ | 169.3 | ||||

Current portion of long-term lease obligations | 200.1 | 188.6 | ||||||

Accounts payable | 495.2 | 494.0 | ||||||

Advance payments and customer deposits | 199.7 | 207.3 | ||||||

Accrued taxes | 87.5 | 89.5 | ||||||

Accrued interest | 62.2 | 52.6 | ||||||

Other current liabilities | 278.9 | 342.1 | ||||||

Total current liabilities | 1,341.5 | 1,543.4 | ||||||

Long-term debt | 5,867.9 | 5,674.6 | ||||||

Long-term lease obligations | 4,540.5 | 4,643.3 | ||||||

Other liabilities | 496.4 | 521.9 | ||||||

Total liabilities | 12,246.3 | 12,383.2 | ||||||

Commitments and Contingencies (See Note 15) | ||||||||

Member Deficit: | ||||||||

Additional paid-in capital | 1,237.5 | 1,187.1 | ||||||

Accumulated other comprehensive income | 44.0 | 21.4 | ||||||

Accumulated deficit | (2,688.0 | ) | (2,507.4 | ) | ||||

Total member deficit | (1,406.5 | ) | (1,298.9 | ) | ||||

Total Liabilities and Member Deficit | $ | 10,839.8 | $ | 11,084.3 | ||||

See the accompanying notes to the unaudited interim consolidated financial statements.

9

WINDSTREAM SERVICES, LLC

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

Six Months Ended June 30, | ||||||||

(Millions) | 2018 | 2017 | ||||||

Cash Flows from Operating Activities: | ||||||||

Net loss | $ | (214.2 | ) | $ | (178.7 | ) | ||

Adjustments to reconcile net loss to net cash provided from operations: | ||||||||

Depreciation and amortization | 752.5 | 700.9 | ||||||

Provision for doubtful accounts | 15.2 | 19.7 | ||||||

Share-based compensation expense | 18.4 | 32.4 | ||||||

Deferred income taxes | (64.7 | ) | (97.3 | ) | ||||

Net loss on early extinguishment of debt | — | 3.2 | ||||||

Other, net | 4.3 | 7.9 | ||||||

Changes in operating assets and liabilities, net | ||||||||

Accounts receivable | 5.8 | 15.7 | ||||||

Prepaid income taxes | (4.7 | ) | (5.2 | ) | ||||

Prepaid expenses and other | 7.3 | (14.3 | ) | |||||

Accounts payable | 17.2 | (56.3 | ) | |||||

Accrued interest | 9.9 | (6.8 | ) | |||||

Accrued taxes | (9.3 | ) | 2.0 | |||||

Other current liabilities | (18.6 | ) | (21.1 | ) | ||||

Other liabilities | 7.0 | 1.5 | ||||||

Other, net | 14.6 | (29.0 | ) | |||||

Net cash provided from operating activities | 540.7 | 374.6 | ||||||

Cash Flows from Investing Activities: | ||||||||

Additions to property, plant and equipment | (406.3 | ) | (507.8 | ) | ||||

Cash acquired from EarthLink | — | 5.0 | ||||||

Acquisition of MASS | (37.6 | ) | — | |||||

Other, net | (8.8 | ) | (11.8 | ) | ||||

Net cash used in investing activities | (452.7 | ) | (514.6 | ) | ||||

Cash Flows from Financing Activities: | ||||||||

Distributions to Windstream Holdings, Inc. | (1.0 | ) | (35.3 | ) | ||||

Contribution from Windstream Holdings, Inc. | 11.1 | 9.6 | ||||||

Repayments of debt and swaps | (413.1 | ) | (1,282.2 | ) | ||||

Proceeds from debt issuance | 450.0 | 1,535.6 | ||||||

Debt issuance costs | (11.6 | ) | (7.3 | ) | ||||

Payments under long-term lease obligations | (91.4 | ) | (82.2 | ) | ||||

Payments under capital lease obligations | (27.7 | ) | (22.0 | ) | ||||

Other, net | (2.4 | ) | (10.6 | ) | ||||

Net cash (used in) provided from financing activities | (86.1 | ) | 105.6 | |||||

Increase (decrease) in cash and cash equivalents | 1.9 | (34.4 | ) | |||||

Cash and Cash Equivalents: | ||||||||

Beginning of period | 43.4 | 59.1 | ||||||

End of period | $ | 45.3 | $ | 24.7 | ||||

Supplemental Cash Flow Disclosures: | ||||||||

Interest paid, net of interest capitalized | $ | 428.9 | $ | 417.7 | ||||

Income taxes (refunded) paid, net | $ | (15.1 | ) | $ | 1.3 | |||

See the accompanying notes to the unaudited interim consolidated financial statements.

10

WINDSTREAM SERVICES, LLC

CONSOLIDATED STATEMENT OF MEMBER DEFICIT (UNAUDITED)

(Millions) | Additional Paid-In Capital | Accumulated Other Comprehensive Income | Accumulated Deficit | Total | ||||||||||||

Balance at December 31, 2017 | $ | 1,187.1 | $ | 21.4 | $ | (2,507.4 | ) | $ | (1,298.9 | ) | ||||||

Cumulative effect adjustments, net of tax: | ||||||||||||||||

Adoption of ASU 2014-09 (See Note 1) | — | — | 35.3 | 35.3 | ||||||||||||

Adoption of ASU 2017-12 (See Note 1) | — | 1.7 | (1.7 | ) | — | |||||||||||

Net loss | — | — | (214.2 | ) | (214.2 | ) | ||||||||||

Other comprehensive income (loss), net of tax: | ||||||||||||||||

Change in postretirement and pension plans | — | 5.0 | — | 5.0 | ||||||||||||

Amortization of unrealized losses on de-designated interest rate swaps | — | 1.2 | — | 1.2 | ||||||||||||

Change in designated interest rate swaps | — | 14.7 | — | 14.7 | ||||||||||||

Comprehensive income (loss) | — | 20.9 | (214.2 | ) | (193.3 | ) | ||||||||||

Share-based compensation | 7.4 | — | — | 7.4 | ||||||||||||

Contributions from Windstream Holdings, Inc.: | ||||||||||||||||

Stock issued under equity distribution agreement | 11.1 | — | — | 11.1 | ||||||||||||

Stock issued for pension contribution | 5.8 | — | — | 5.8 | ||||||||||||

Stock contribution to employee savings plan | 28.3 | — | — | 28.3 | ||||||||||||

Taxes withheld on vested restricted stock and other | (1.3 | ) | — | — | (1.3 | ) | ||||||||||

Distributions payable to Windstream Holdings, Inc. | (0.9 | ) | — | — | (0.9 | ) | ||||||||||

Balance at June 30, 2018 | $ | 1,237.5 | $ | 44.0 | $ | (2,688.0 | ) | $ | (1,406.5 | ) | ||||||

See the accompanying notes to the unaudited interim consolidated financial statements.

11

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

1. Preparation of Interim Financial Statements:

In these consolidated financial statements, unless the context requires otherwise, the use of the terms “Windstream,” “we,” “us” or “our” shall refer to Windstream Holdings, Inc. and its subsidiaries, including Windstream Services, LLC, and the term “Windstream Services” shall refer to Windstream Services, LLC and its subsidiaries.

Organizational Structure – Windstream Holdings, Inc. (“Windstream Holdings”) is a publicly traded holding company incorporated in the state of Delaware on May 23, 2013, and the parent of Windstream Services, LLC (“Windstream Services”), a Delaware limited liability company organized on March 1, 2004. Windstream Holdings common stock trades on the NASDAQ Global Select Market (“NASDAQ”) under the ticker symbol “WIN”. Windstream Holdings owns a 100 percent interest in Windstream Services. Windstream Services and its guarantor subsidiaries are the sole obligors of all outstanding debt obligations and, as a result also file periodic reports with the Securities and Exchange Commission (“SEC”). Windstream Holdings is not a guarantor of nor subject to the restrictive covenants included in any of Windstream Services’ debt agreements. The Windstream Holdings board of directors and officers oversee both companies.

Description of Business – We are a leading provider of advanced network communications and technology solutions for businesses across the U.S. We also offer broadband, entertainment and security solutions to consumers and small businesses primarily in rural areas in 18 states. Additionally, we supply core transport solutions on a local and long-haul fiber network spanning approximately 150,000 miles.

Consumer service revenues are generated from the provisioning of high-speed Internet, voice and video services to consumers. Enterprise service revenues include revenues from integrated voice and data services, advanced data and traditional voice and long-distance services provided to enterprise, mid-market and small business customers. Wholesale revenues include revenues from other communications services providers for special access circuits and fiber connections, voice and data transport services, and revenues from the reselling of our services. Service revenues also include switched access revenues, federal and state Universal Service Fund (“USF”) revenues, amounts received from Connect America Fund - Phase II, USF surcharges and revenues from providing other miscellaneous services.

Basis of Presentation – The accompanying unaudited consolidated financial statements have been prepared based upon SEC rules that permit reduced disclosure for interim periods. Certain information and footnote disclosures have been condensed or omitted in accordance with those rules and regulations. The accompanying consolidated balance sheet as of December 31, 2017, was derived from audited financial statements, but does not include all disclosures required by accounting principles generally accepted in the United States. In our opinion, these financial statements reflect all adjustments that are necessary for a fair statement of results of operations and financial condition for the interim periods presented including normal recurring accruals and other items. The results for the interim periods are not necessarily indicative of results for the full year. For a more complete discussion of significant accounting policies and certain other information, this report should be read in conjunction with the consolidated financial statements and accompanying notes included in our Annual Report on Form 10-K for the year ended December 31, 2017, which was filed with the SEC on February 28, 2018.

On May 23, 2018, we amended our certificate of incorporation to decrease the number of authorized shares of our common and preferred stock from 375.0 million to 75.0 million and from 33.3 million to 6.7 million, respectively, and enacted a one-for-five reverse stock split with respect to all of our outstanding shares of common stock which became effective on May 25, 2018. All per share data of Windstream Holdings presented herein has been retrospectively adjusted to reflect the decrease in authorized shares and the reverse stock split, as appropriate.

Windstream Holdings and its domestic subsidiaries, including Windstream Services, file a consolidated federal income tax return. As such, Windstream Services and its subsidiaries are not separate taxable entities for federal and certain state income tax purposes. In instances when Windstream Services does not file a separate return, income taxes as presented within the accompanying consolidated financial statements attribute current and deferred income taxes of Windstream Holdings to Windstream Services and its subsidiaries in a manner that is systematic, rational and consistent with the asset and liability method. Income tax provisions presented for Windstream Services and its subsidiaries are prepared under the “separate return method.” The separate return method represents a hypothetical computation assuming that the reported revenue and expenses of Windstream Services and its subsidiaries were incurred by separate taxable entities.

12

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

1. Preparation of Interim Financial Statements, Continued:

The preparation of financial statements, in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”), requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses and disclosure of contingent assets and liabilities. The estimates and assumptions used in the accompanying consolidated financial statements are based upon management’s evaluation of the relevant facts and circumstances as of the date of the consolidated financial statements. Actual results may differ from the estimates and assumptions used in preparing the accompanying consolidated financial statements, and such differences could be material.

There are no significant differences between the consolidated results of operations, financial condition, and cash flows of Windstream Holdings and those of Windstream Services other than for certain expenses incurred directly by Windstream Holdings principally consisting of audit, legal and board of director fees, NASDAQ listing fees, other shareholder-related costs, income taxes, common stock activity, and payables from Windstream Services to Windstream Holdings. Earnings per share data has not been presented for Windstream Services, because that entity has not issued publicly held common stock as defined in accordance with U.S. GAAP. Unless otherwise indicated, the note disclosures included herein pertain to both Windstream Holdings and Windstream Services.

Certain prior year amounts have been reclassified to confirm to the current year financial statement presentation. These changes and reclassifications did not impact net loss or comprehensive loss.

Recently Adopted Accounting Standards

Revenue Recognition – In May 2014, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2014-09, Revenue from Contracts with Customers (Topic 606) as modified by subsequently issued ASU Nos. 2015-14, 2016-08, 2016-10, 2016-11, 2016-12 and 2016-20 (collectively “ASU 2014-09”). The core principle of the revenue model is that an entity should recognize revenue for the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled to receive for those goods or services. ASU 2014-09 also provided new accounting principles related to the deferral and amortization of contract acquisition and fulfillment costs.

On January 1, 2018, we adopted ASU 2014-09 using the modified retrospective transition method applied to those contracts which were not complete as of January 1, 2018. Under the modified retrospective transition method, we recognized the cumulative effect of initial adoption as an adjustment to our opening accumulated deficit balance. Comparative information for prior periods has not been restated and continues to be reported under the accounting standards in effect for those periods.

Under the new revenue recognition guidance, a substantial portion of our service revenues continue to be recognized when services are provided. Changes to the timing of recognition of certain installation services, discounts and promotional credits given to customers under the new guidance resulted in the recognition of incremental contract assets and liabilities in our consolidated balance sheet at the date of adoption. In addition, the new requirement to defer incremental contract acquisition and fulfillment costs, including sales commissions and installation costs, and recognize such costs over the period where control of goods and services are transferred resulted in the recognition of additional deferred contract costs in our consolidated balance sheet at the date of adoption. We evaluated the effect of the time value of money and determined it to be immaterial.

The following table presents the cumulative effect of the changes made to our consolidated balance sheet at December 31, 2017:

(Millions) | December 31, 2017 | ASU 2014-09 Adjustments | January 1, 2018 | |||||||||

Assets | ||||||||||||

Accounts receivable | $ | 643.0 | $ | — | $ | 643.0 | ||||||

Prepaid expenses and other | $ | 154.3 | $ | 26.0 | $ | 180.3 | ||||||

Other assets | $ | 91.2 | $ | 20.9 | $ | 112.1 | ||||||

Deferred income taxes | $ | 370.8 | $ | (12.0 | ) | $ | 358.8 | |||||

Liabilities | ||||||||||||

Advance payments and customer deposits | $ | 207.3 | $ | (0.5 | ) | $ | 206.8 | |||||

Other current liabilities | $ | 342.1 | $ | (0.3 | ) | $ | 341.8 | |||||

Other liabilities | $ | 521.9 | $ | 0.4 | $ | 522.3 | ||||||

Accumulated deficit | $ | (2,512.2 | ) | $ | 35.3 | $ | (2,476.9 | ) | ||||

13

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

1. Preparation of Interim Financial Statements, Continued:

The impact of adoption of ASU 2014-09 on our 2018 consolidated statements of operations and consolidated balance sheet are as follows:

Three Months Ended June 30, 2018 | |||||||||||

(Millions) | Under ASC 605 | Effect of Adoption of ASU 2014-09 | As reported | ||||||||

Revenue and sales | |||||||||||

Service revenues | $ | 1,424.5 | $ | 0.1 | $ | 1,424.6 | |||||

Product sales | $ | 19.8 | $ | — | $ | 19.8 | |||||

Costs and expenses | |||||||||||

Cost of services | $ | 722.9 | $ | (0.1 | ) | $ | 722.8 | ||||

Selling, general and administrative | $ | 225.5 | $ | (1.0 | ) | $ | 224.5 | ||||

Income tax benefit | $ | (30.7 | ) | $ | 0.3 | $ | (30.4 | ) | |||

Net loss | $ | (94.6 | ) | $ | 0.9 | $ | (93.7 | ) | |||

Six Months Ended June 30, 2018 | |||||||||||

(Millions) | Under ASC 605 | Effect of Adoption of ASU 2014-09 | As reported | ||||||||

Revenue and sales | |||||||||||

Service revenues | $ | 2,858.9 | $ | 1.1 | $ | 2,860.0 | |||||

Product sales | $ | 38.7 | $ | — | $ | 38.7 | |||||

Costs and expenses | |||||||||||

Cost of services | $ | 1,459.3 | $ | 0.4 | $ | 1,459.7 | |||||

Selling, general and administrative | $ | 453.7 | $ | (0.4 | ) | $ | 453.3 | ||||

Income tax benefit | $ | (65.7 | ) | $ | 0.3 | $ | (65.4 | ) | |||

Net loss | $ | (215.9 | ) | $ | 0.8 | $ | (215.1 | ) | |||

June 30, 2018 | |||||||||||

(Millions) | Under ASC 605 | Effect of Adoption of ASU 2014-09 | As reported | ||||||||

Assets | |||||||||||

Accounts receivable | $ | 623.9 | $ | — | $ | 623.9 | |||||

Prepaid expenses and other | $ | 149.4 | $ | 31.6 | $ | 181.0 | |||||

Other assets | $ | 92.3 | $ | 16.2 | $ | 108.5 | |||||

Deferred income taxes | $ | 428.5 | $ | (12.3 | ) | $ | 416.2 | ||||

Liabilities | |||||||||||

Advance payments and customer deposits | $ | 200.3 | $ | (0.6 | ) | $ | 199.7 | ||||

Other current liabilities | $ | 278.8 | $ | 0.1 | $ | 278.9 | |||||

Other liabilities | $ | 496.5 | $ | (0.1 | ) | $ | 496.4 | ||||

Accumulated deficit | $ | (2,729.8 | ) | $ | 36.1 | $ | (2,693.7 | ) | |||

The new revenue recognition standard also requires additional disclosures related to performance obligations; contract asset and liability balances; deferred commissions and costs to fulfill; disaggregation of revenue and use of practical expedients in applying the new guidance. See Note 2 for these additional disclosures.

14

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

1. Preparation of Interim Financial Statements, Continued:

Statement of Cash Flows – In August 2016, the FASB issued ASU No. 2016-15, Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments (“ASU 2016-15”). This standard provides guidance on how certain cash receipts and cash payments should be presented and classified in the statement of cash flows, including among others, debt prepayment and extinguishment costs, contingent consideration payments made after a business combination, proceeds from the settlement of insurance claims and distributions received from equity method investees. The standard also clarifies that when cash receipts and cash payments have aspects of more than one class of cash flows and cannot be separated, classification will depend on the predominant source or use of the underlying cash flows. ASU 2016-15 is effective for annual and interim reporting periods beginning after December 15, 2017, with early adoption permitted. We adopted this standard effective January 1, 2018. The effect of the retrospective adoption of this standard was to change previously reported amounts within the accompanying consolidated statement of cash flows for the six-month period ended June 30, 2017 due to reclassifying $21.2 million of debt prepayment penalties and fees paid to lenders in conjunction with the early termination of long-term debt obligations from operating activities to financing activities. Other than this change in classification of debt prepayment penalties and fees, adoption of this standard did not have an impact on our consolidated statement of cash flows.

The following table presents the effect of the changes made to our consolidated statement of cash flows for the six-month period ended June 30, 2017:

(Millions) | As Previously Reported | Reclassification Adjustments | As Revised | |||||||||

Cash Flows from Operating Activities: | ||||||||||||

Adjustments to reconcile net loss to net cash provided from operations: | ||||||||||||

Noncash portion of net (gain) loss on early extinguishment of debt | $ | (15.1 | ) | $ | 15.1 | $ | — | |||||

Net loss on early extinguishment of debt | $ | — | $ | 3.2 | $ | 3.2 | ||||||

Changes in operating assets and liabilities, net: | ||||||||||||

Other, net | $ | (31.9 | ) | $ | 2.9 | $ | (29.0 | ) | ||||

Net cash provided from operating activities | $ | 353.7 | $ | 21.2 | $ | 374.9 | ||||||

Cash Flows from Financing Activities: | ||||||||||||

Repayments of debt and swaps | $ | (1,261.0 | ) | $ | (21.2 | ) | $ | (1,282.2 | ) | |||

Net cash provided from financing activities | $ | 126.5 | $ | (21.2 | ) | $ | 105.3 | |||||

Definition of a Business – In January 2017, the FASB issued ASU No. 2017-01, Business Combinations (Topic 805), Clarifying the Definition of a Business (“ASU 2017-01”). The standard clarifies the definition of a business when evaluating whether transactions should be accounted for as acquisitions or disposals of assets or businesses. Under the new guidance an integrated set of activities must include, at a minimum, an input and a substantive process that together significantly contribute to the ability to create output to be considered a business. ASU 2017-01 provides a framework to assist entities in evaluating whether both an input and a substantive process are present and removes the evaluation of whether a market participant could replace missing elements. Although outputs are not required for an integrated set of activities to be a business, outputs generally are a key element of a business; therefore, the new guidance provides more stringent criteria for an integrated sets of activities without outputs. Furthermore, ASU 2017-01 narrows the definition of the term output so that it is consistent with how outputs are described in Topic 606. ASU 2017-01 is effective for annual periods beginning after December 15, 2017, including interim periods within those annual reporting periods. We adopted this standard effective January 1, 2018. Following adoption, we expect fewer transactions will be accounted for as acquisitions or disposals of businesses.

15

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

1. Preparation of Interim Financial Statements, Continued:

Presentation of Defined Benefit Retirement Costs – In March 2017, the FASB issued ASU 2017-07, Compensation-Retirement Benefits (Topic 715) Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost (“ASU 2017-07”). This standard changes the income statement presentation of defined benefit plan expense by requiring separation between operating expense (service cost component) and non-operating expense (all other components, including interest cost, amortization of prior service cost, actuarial gains and losses, curtailments and settlements). The operating expense component will be reported in the same income statement line item(s) as other employee compensation costs arising from services rendered during the period while the non-operating components will be reported in other income and expense. In addition, only the service cost component will be eligible for capitalization as part of an asset such as inventory or property, plant and equipment. Retrospective application of the change in income statement presentation is required, while the change in capitalized benefit cost is to be applied prospectively. The ASU is effective for fiscal years beginning after December 15, 2017. We adopted this standard effective January 1, 2018. The effect of the retrospective adoption of this standard was to change previously reported amounts within the accompanying consolidated statement of operations for the three and six month periods ended June 30, 2017, respectively, for operating income and other income, net, resulting in decreases in operating income from $106.8 million to $102.5 million and from $152.8 million to $146.6 million, respectively, with corresponding increases to other (expense) income, net from $(0.1) million to $4.2 million and $0.6 million to $6.8 million, respectively. There was no change to our reported net loss for the three and six month periods ended June 30, 2017. The impact of only capitalizing service cost on a prospective basis was immaterial to our consolidated financial statements as of and for the three and six month periods ended June 30, 2018.

Hedging Activities – In August 2017, the FASB issued ASU 2017-12, Derivatives and Hedging (Topic 815) Targeted Improvements to Accounting for Hedging Activities. This standard modifies hedge accounting to allow more hedging strategies to qualify for hedge accounting, amends presentation and disclosure requirements, and changes how entities assess effectiveness of their hedging transactions. ASU 2017-12 is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. Early adoption is permitted. As permitted, we early adopted this standard effective January 1, 2018. Upon adoption, we recognized a cumulative effect adjustment of $(1.7) million, net of tax, to the opening balance of our accumulated deficit with an offsetting increase to accumulated comprehensive income. Comparative prior-period information has not been restated. See Note 6 for additional information regarding our hedging activities and derivative financial instruments.

Recently Issued Authoritative Guidance

Leases – In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842), which will require that virtually all lease arrangements that do not meet the criteria of a short-term lease be presented on the lessee’s balance sheet by recording a right-of-use asset and a lease liability equal to the present value of the related future lease payments. The income statement impacts of the leases will depend on the nature of the leasing arrangement and will be similar to existing accounting for operating and capital leases. The new standard does not substantially change the accounting for lessors. The new standard will also require additional disclosures regarding an entity’s leasing arrangements and will be effective for the first interim reporting period within annual periods beginning after December 15, 2018, although early adoption is permitted. Lessees and lessors will be required to apply the new standard at the beginning of the earliest period presented in the financial statements in which they first apply the new guidance, using a modified retrospective transition method. We will adopt ASU 2016-02 effective January 1, 2019. Our existing operating lease portfolio primarily consists of network, real estate and equipment leases. Upon adoption of this standard, we expect to record in our consolidated balance sheet a right-of-use asset and liability related to substantially all of our operating lease arrangements. We have established a cross-functional team to determine the scope of arrangements subject to this standard as well as to assess the impact to our systems, processes and internal controls that will be necessary to meet the standard’s reporting and disclosure requirements.

Financial Instruments - Credit Losses – In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments (“ASU 2016-13”). This standard introduces a new forward-looking approach, based on expected losses, to estimate credit losses on certain types of financial instruments, including trade receivables. The estimate of expected credit losses will require entities to incorporate considerations of historical information, current information and reasonable and supportable forecasts. This new standard also expands the disclosure requirements to enable users of financial statements to understand the entity’s assumptions, models and methods for estimating expected credit losses. ASU 2016-13 is effective for annual and interim reporting periods beginning after December 15, 2019, and the guidance is to be applied using a modified retrospective transition approach. Early adoption is permitted for annual and interim reporting periods beginning after December 15, 2018. We intend to adopt this standard update in the first quarter of 2020. We are currently assessing the impact the new standard will have on our consolidated financial statements.

16

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

2. Revenues:

As previously discussed in Note 1, we adopted ASU 2014-09 effective January 1, 2018 using the modified retrospective transition method. The majority of our revenue is derived from providing access to or usage of our networks and facilities we operate.

Performance Obligations – A performance obligation is a promise in a contract to transfer a distinct good or service to the customer, and represents the unit of account in applying the new revenue recognition guidance. A contract’s transaction price, considering discounts given for bundled purchases and promotional credits, is allocated to each distinct performance obligation and recognized as revenue when, or as, the performance obligation is satisfied. The majority of our contracts have multiple performance obligations. While many contracts include one or more performance obligations, the revenue recognition pattern is generally not impacted by the allocation since the performance obligations are generally satisfied over the same period of time. For contracts with multiple performance obligations, we allocate the contract’s transaction price to each performance obligation based on the relative standalone selling price of each performance obligation in the contract. The standalone selling price is the estimated price we would charge for the good or service in a separate transaction with similar customers in similar circumstances. Identifying distinct performance obligations and determining the standalone selling price for each performance obligation within a contract with multiple performance obligations requires significant management judgment.

Our performance obligations are satisfied over time as services are rendered or at a point in time depending on our evaluation of when the customer obtains control of the promised goods. Revenue is recognized when obligations under the terms of a contract with our customer are satisfied; generally, this occurs when services are rendered or control of our communication products is transferred. Service revenues are recognized over the period that the corresponding services are rendered to customers. Revenues that are billed in advance include monthly recurring network access and data services, special access and monthly recurring voice, Internet and other related charges. Revenues derived from other telecommunications services, including interconnection, long-distance and enhanced service revenues are recognized monthly as services are provided. Telecommunications network maintenance revenue from indefeasible rights to use fiber optic network facility arrangements (“IRUs”) are generally recognized over the term of the related contract. Sales of communications products including customer premise equipment and modems are recognized when products are delivered to and accepted by customers.

In determining whether installation is a separate performance obligation, we evaluate, among other factors, whether other performance obligations are highly dependent upon installation requiring significant integration or customization or whether a customer can benefit from the installation with other readily available resources. In circumstances where customers can benefit from the installation with other readily available resources, installation is a separate performance obligation. We recognize installation revenue when the installation is complete. In circumstances where other telecommunication service performance obligations are highly dependent upon installation, installation is not a separate purchase obligation, and accordingly, we include the installation fees in the transaction price allocated to and recognized with other telecommunication service performance obligations.

Fees assessed to customers for service activation are considered a material right in a month-to-month contract. These service activation fees are deferred and recognized as service revenue on a straight-line basis over the estimated life of the customer.

As a practical expedient, we group similar contracts or performance obligations together into portfolios of contracts or performance obligations for the following: service activations, installation services, certain promotional credits, commissions and other costs to fulfill a contract. Portfolios are recognized over the estimated life of the customer. Determining the estimated life of the customer requires significant management judgment.

The estimated life of our customer relationships varies by business segment. Wholesale customer lives are estimated based on the average number of months each individual circuit was active. Enterprise and small business customer lives are based on average contract terms. Consumer lives are estimated based on average customer tenure.

17

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

2. Revenues, Continued:

Our contracts include discounts and promotional credits given to customers. We include discounts and promotional credits in the transaction price. These estimates are based on historical experience and anticipated performance.

In determining whether to include in revenues and expenses, the taxes and surcharges assessed and collected from customers and remitted to government authorities, including USF charges, sales, use, value added and excise taxes, we evaluate, among other factors, whether we are the primary obligor or principal tax payer for the fees and taxes assessed in each jurisdiction in which we operate. In those jurisdictions for which we are the primary obligor, we record the taxes and surcharges on a gross basis and include in revenues and costs of services and products. In jurisdictions in which we function as a collection agent for the government authority, we record the taxes on a net basis and exclude the amounts from our revenues and costs of services and products.

We offer third-party video services to our customers. The third-party service provider retains control of the service and is the primary obligor. We record commissions received on a net basis.

Accounts Receivable – Accounts receivable, principally consist of amounts billed and currently due from customers and are generally unsecured and due within 30 days. The amounts due are stated at their net estimated realizable value. We maintain an allowance for doubtful accounts to provide for the estimated amount of receivables that will not be collected. The allowance is based upon an assessment of historical collection experience, age of outstanding receivables, current economic conditions and a specific customer’s ability to meet its financial obligations. Concentration of credit risk with respect to accounts receivable is limited because a large number of geographically diverse customers make up our customer base. Due to varying customer monthly billing cycle cut-off, we must estimate service revenues earned but not yet billed at the end of each reporting period. Included in accounts receivable are unbilled revenues related to communication services and product sales of $23.7 million and $23.8 million at June 30, 2018 and December 31, 2017, respectively.

Contract Balances – Contract assets include unbilled amounts resulting when revenue recognized exceeds the amount billed to the customer, and right to payment is not just subject to the passage of time. Contract assets principally consist of discounts and promotional credits given to customers. The current and noncurrent portion of contract assets is included in prepaid expenses and other and other assets, respectively in the accompanying consolidated balance sheets.

Our contract liabilities consist of services billed in excess of revenue recognized. Our contract assets and liabilities are reported in a net position on a contract-by-contract basis at the end of each reporting period. We classify these amounts as current or noncurrent based on the timing of when we expect to recognize revenue.

The following table provides a rollforward of contract assets and liabilities from contracts with customers:

(Millions) | Contract Assets | Contract Liabilities | |||||||

Balance at January 1, 2018 | $ | 13.1 | (a) | $ | (209.3 | ) | (b) | ||

Revenue recognized included in opening contract balance | (4.8 | ) | 183.8 | ||||||

Cash received, excluding amounts recognized as revenue | — | (177.1 | ) | ||||||

Credits granted, excluding amounts recognized as revenue | 4.6 | — | |||||||

Balance at June 30, 2018 | $ | 12.9 | (a) | $ | (202.6 | ) | (b) | ||

(a) | Includes $8.5 million and $3.6 million in prepaid expense and other and $4.4 million and $9.5 million in other assets as of June 30, 2018 and January 1, 2018, respectively. |

(b) | Includes $190.0 million and $198.3 million in advance payments and customer deposits and $12.6 million and $11.0 million in other liabilities as of June 30, 2018 and January 1, 2018, respectively. |

18

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

2. Revenues, Continued:

Remaining Performance Obligations – Our remaining performance obligations represent services we are required to provide to customers under bundled or discounted arrangements, which are satisfied as services are provided over the contract term. Certain contracts provide customers the option to purchase additional services or usage based services. The fees related to the additional services or usage based services are recognized when the customer exercises the option, typically on a month-to-month basis. In determining the transaction price allocated, we do not include these non-recurring fees and estimates for usage, nor do we consider arrangements with an original expected duration of less than one year.

Remaining performance obligations reflect recurring charges billed, adjusted for discounts and promotional credits and revenue adjustments. At June 30, 2018, the aggregate amount of the transaction price allocated to remaining performance obligations was approximately $3.5 billion for contracts with original expected durations of more than one year remaining. We expect to recognize approximately 23.1 percent, 38.3 percent and 24.7 percent of our remaining performance obligations as revenue during the remainder of 2018, 2019 and 2020, with the remaining balance thereafter.

Revenue by Category – We disaggregate our revenue from contracts with customers by product type for each of our segments, as we believe it best depicts the nature, amount and timing of our revenue. Revenues recognized from contracts with customers by customer and product type for the three-month period ended June 30, 2018 was as follows:

(Millions) | Consumer & Small Business | Enterprise | Wholesale | Consumer CLEC | Total | |||||||||||||||

Revenue from contracts with customers: | ||||||||||||||||||||

Type of service: | ||||||||||||||||||||

High-speed Internet bundles | $ | 242.4 | $ | — | $ | — | $ | 23.2 | $ | 265.6 | ||||||||||

Voice and long-distance | 30.7 | 240.2 | — | — | 270.9 | |||||||||||||||

Video and miscellaneous | 11.3 | — | — | — | 11.3 | |||||||||||||||

Dial-up, e-mail and miscellaneous | — | — | — | 22.5 | 22.5 | |||||||||||||||

Data and integrated services | — | 388.4 | — | — | 388.4 | |||||||||||||||

Small business services | 75.9 | — | — | — | 75.9 | |||||||||||||||

Core wholesale (a) | — | — | 139.1 | — | 139.1 | |||||||||||||||

Resale (b) | — | — | 20.1 | — | 20.1 | |||||||||||||||

Wireless TDM (c) | — | — | 2.4 | — | 2.4 | |||||||||||||||

Switched access | 7.0 | — | 9.4 | — | 16.4 | |||||||||||||||

Miscellaneous | — | 38.8 | — | — | 38.8 | |||||||||||||||

Service revenues from contracts with customers | 367.3 | 667.4 | 171.0 | 45.7 | 1,251.4 | |||||||||||||||

Product sales | 6.6 | 13.0 | 0.1 | 0.1 | 19.8 | |||||||||||||||

Total revenue from contracts with customers | 373.9 | 680.4 | 171.1 | 45.8 | 1,271.2 | |||||||||||||||

Other service revenues (d) | 98.6 | 62.7 | 11.3 | 0.6 | 173.2 | |||||||||||||||

Total revenues and sales | $ | 472.5 | $ | 743.1 | $ | 182.4 | $ | 46.4 | $ | 1,444.4 | ||||||||||

19

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

2. Revenues, Continued:

Revenues recognized from contracts with customers by customer and product type for the six-month period ended June 30, 2018 was as follows:

(Millions) | Consumer & Small Business | Enterprise | Wholesale | Consumer CLEC | Total | |||||||||||||||

Revenue from contracts with customers: | ||||||||||||||||||||

Type of service: | ||||||||||||||||||||

High-speed Internet bundles | $ | 486.0 | $ | — | $ | — | $ | 47.6 | $ | 533.6 | ||||||||||

Voice and long-distance | 62.1 | 483.0 | — | — | 545.1 | |||||||||||||||

Video and miscellaneous | 22.7 | — | — | — | 22.7 | |||||||||||||||

Dial-up, e-mail and miscellaneous | — | — | — | 45.3 | 45.3 | |||||||||||||||

Data and integrated services | — | 776.1 | — | — | 776.1 | |||||||||||||||

Small business services | 154.0 | — | — | — | 154.0 | |||||||||||||||

Core wholesale (a) | — | — | 278.6 | — | 278.6 | |||||||||||||||

Resale (b) | — | — | 41.4 | — | 41.4 | |||||||||||||||

Wireless TDM (c) | — | — | 5.1 | — | 5.1 | |||||||||||||||

Switched access | 15.1 | — | 18.8 | — | 33.9 | |||||||||||||||

Miscellaneous | — | 77.7 | — | — | 77.7 | |||||||||||||||

Service revenues from contracts with customers | 739.9 | 1,336.8 | 343.9 | 92.9 | 2,513.5 | |||||||||||||||

Product sales | 12.1 | 26.2 | 0.2 | 0.2 | 38.7 | |||||||||||||||

Total revenue from contracts with customers | 752.0 | 1,363.0 | 344.1 | 93.1 | 2,552.2 | |||||||||||||||

Other service revenues (d) | 197.0 | 126.2 | 22.1 | 1.2 | 346.5 | |||||||||||||||

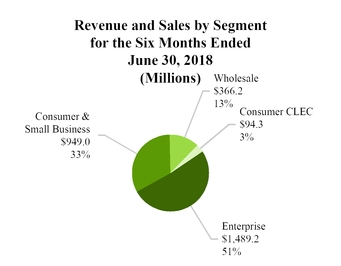

Total revenues and sales | $ | 949.0 | $ | 1,489.2 | $ | 366.2 | $ | 94.3 | $ | 2,898.7 | ||||||||||

(a) | Core wholesale revenues primarily include revenues from providing special access circuits, fiber connections, data transport and wireless backhaul services. |

(b) | Revenues represent voice and data services sold to other communications services providers on a resale basis. |

(c) | Revenues represent Time Division Multiplexing (“TDM”) private line transport services. |

(d) | Other service revenues primarily include end user surcharges, Connect America Fund Phase II funding, state USF and access recovery mechanism (“ARM”) support and lease revenue. |

Deferred Commissions and Other Costs to Fulfill a Contract – Our direct incremental costs of obtaining a contract, consisting of sales commissions, and certain costs associated with activating services, including costs to develop customized solutions and provision services, are deferred and recognized as an operating expense using a portfolio approach over the estimated life of the customer, which ranges from 18 to 36 months.

Determining the amount of costs to fulfill requires judgment. In determining costs to fulfill consideration is given to periodic time studies, management estimates and statistics from internal information systems.

Collectively, deferred commissions and other costs to fulfill a contract are referred to as deferred contract costs. We classify deferred contract costs as current or noncurrent based on the timing of when we expect to recognize the expense. The current and noncurrent portions of deferred contract costs are included in prepaid expenses and other and other assets in our consolidated balance sheets. Deferred contract costs totaled $44.7 million at June 30, 2018, of which $30.6 million and $14.1 million was included in prepaid expenses and other and other assets, respectively. At January 1, 2018, deferred contract costs were $44.6 million, of which $30.3 million and $14.3 million was included in prepaid expenses and other and other assets, respectively. Amortization of deferred contract costs was $21.3 million for the six-month period ended June 30, 2018. There was no impairment loss recognized for the six-month period ended June 30, 2018, related to deferred contract cost.

20

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

3. Acquisitions:

MASS Communications

On March 27, 2018, Windstream Holdings acquired MASS Communications (“MASS”), a privately held telecommunications network management company focused on providing custom engineered voice, data and networking solutions to small and mid-sized global enterprises in the financial, legal, healthcare, technology, education and government sectors for initial cash consideration of approximately $37.6 million, including $2.5 million of expected earn-out payments, which have been funded into an escrow account. The acquisition was accounted using the acquisition method and accordingly, the cost of the acquisition was allocated to the assets acquired and liabilities assumed based on their estimated fair values as of the acquisition date. In allocating the purchase price, we recorded approximately $2.0 million of tangible assets, consisting primarily of accounts receivable, $10.0 million associated with a customer list intangible asset, $4.1 million of trade accounts payable and other current liabilities, $2.5 million of deferred income tax liabilities, and $32.2 million of goodwill. The purchase price allocation is preliminary and subject to change based on receipt of information currently not available to us, including the tax basis of the assets acquired. Any changes to the initial estimates of the fair value of the acquired assets and liabilities assumed will be recorded as adjustments to those asset and liabilities with the offset charged to goodwill. Goodwill associated with this acquisition was primarily attributable to the MASS workforce and expected synergies. None of the goodwill recorded in this acquisition is expected to be deductible for income tax purposes. The results of MASS’ operations were not material to our consolidated results of operations, and accordingly, no pro forma financial information has been presented.

Broadview Network Holdings, Inc.

On July 28, 2017, Windstream Holdings completed its merger with Broadview Networks Holdings, Inc. (“Broadview”), pursuant to the terms of the Agreement and Plan of Merger (the “Broadview Merger Agreement”) dated April 12, 2017, whereby Broadview merged into Beethoven Merger Subsidiary, Inc., with Broadview surviving as an indirect wholly owned subsidiary of Windstream Holdings, and changing its name to Windstream BV Holdings, Inc. Broadview is a leading provider of cloud-based unified communications solutions to small and medium-sized businesses and offers a broad suite of cloud-based services, which will improve our competitiveness and ability to provide enhanced services to business customers. Upon completion of the merger, Windstream added approximately 20,000 small and medium-sized business customers and approximately 3,000 incremental route fiber miles. Pursuant to the terms of the Broadview Merger Agreement, each share of Broadview’s common stock, par value $.01 per share that was issued and outstanding immediately prior to the effective time of the merger was automatically converted into the right to receive cash consideration of $6.98 per share. In completing the merger, Windstream Services paid $69.8 million in cash to Broadview shareholders and assumed $160.2 million of Broadview’s short-term debt obligations, which Windstream Services subsequently repaid using amounts available under its senior secured revolving credit facility. The transaction is valued at approximately $230.0 million.

We accounted for the merger using the acquisition method of accounting and accordingly, the cost of the acquisition was allocated to the assets acquired and liabilities assumed based on their estimated fair values as of the merger date. During 2018, we finalized our preliminary purchase price allocation for changes in the estimated fair value of certain acquired assets, resulting from new information about facts and circumstances that existed at the time of acquisition. The adjustments primarily consisted of an increase of $4.2 million in property, plant and equipment, reflecting updates to replacement cost information applicable to the valuation of these assets. The impact of this change on depreciation expense was not material to our consolidated results of operations. We also adjusted deferred income tax assets based on receipt of the final tax basis of assets acquired and adjusted certain state gross receipts and sales tax liabilities based on additional information received subsequent to the acquisition date, resulting in increases in deferred income tax assets of $1.4 million and other current liabilities of $4.7 million. The adjustments to the estimated fair values of assets acquired and liabilities assumed resulted in an offsetting decrease to goodwill of $0.7 million.

Goodwill associated with this acquisition was primarily attributable to the Broadview workforce and expected synergies. As a result of past acquisitions completed by Broadview, approximately $10.8 million of goodwill recorded in the merger is expected to be deductible for income tax purposes.

21

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

3. Acquisitions, Continued:

The following table summarizes the preliminary fair values of the assets acquired and liabilities assumed for Broadview.

(Millions) | Allocation as of December 31, 2017 | Adjustments | Final Allocation | |||||||||

Fair value of assets acquired: | ||||||||||||

Accounts receivable | $ | 17.4 | $ | 0.2 | $ | 17.6 | ||||||

Other current assets | 7.1 | (0.3 | ) | 6.8 | ||||||||

Property, plant and equipment | 37.1 | 4.2 | 41.3 | |||||||||

Goodwill | 121.3 | (0.7 | ) | 120.6 | ||||||||

Customer lists (a) | 45.0 | — | 45.0 | |||||||||

Trade names (b) | 21.0 | — | 21.0 | |||||||||

Developed technology (c) | 10.0 | — | 10.0 | |||||||||

Deferred income taxes | 9.7 | 1.4 | 11.1 | |||||||||

Other assets | 2.6 | (0.1 | ) | 2.5 | ||||||||

Total assets acquired | 271.2 | 4.7 | 275.9 | |||||||||

Fair value of liabilities assumed: | ||||||||||||

Short-term debt obligations | 160.2 | — | 160.2 | |||||||||

Other current liabilities | 46.9 | 4.7 | 51.6 | |||||||||

Other liabilities | 0.8 | — | 0.8 | |||||||||

Total liabilities assumed | 207.9 | 4.7 | 212.6 | |||||||||

Cash paid, net of cash acquired | $ | 63.3 | $ | — | $ | 63.3 | ||||||

(a) | Customer lists are amortized using the sum-of-years digits methodology over a weighted average life of 10 years. |

(b) | Trade names are amortized on a straight-line basis over an estimated useful life of 1 and 10 years. |

(c) | Internally developed technology is amortized on a straight-line basis over an estimated useful life of 5 years. |

The fair values of the assets acquired and liabilities assumed were determined utilizing income, cost and market approaches with the assistance of a third-party valuation firm. The customer list was valued based on the present value of future cash flows and the trade names and developed technology were valued using the relief-from-royalty method, both of which are income approaches. Significant assumptions utilized in these income approaches were based on our specific information and projections, which are not observable in the market and are thus considered Level 3 measurements as defined by authoritative guidance. The cost approach, which estimates value by determining the current cost of replacing an asset with another of equivalent economic utility, was used as appropriate for valuing property, plant and equipment. The cost to replace a given asset reflects the estimated reproduction or replacement cost for the asset, less an allowance for loss in value due to depreciation. The fair value of Broadview’s short-term debt obligations, consisting of a revolving credit facility and 10.5 percent senior notes due November 15, 2017 (“Broadview 2017 Notes”), were based on redemption cost and quoted market prices, respectively.

The results of Broadview’s operations are included in our consolidated results of operations beginning on July 28, 2017. For the three and six month periods ended June 30, 2018 our consolidated results of operations include revenues and sales of $69.4 million and $138.8 million and operating income of $18.7 million and $29.4 million attributable to Broadview. We incurred $1.5 million and $3.4 million of merger and integration expenses during the three and six month periods ended June 30, 2018 related to the completion of this acquisition (see Note 10). Pro forma financial information for Broadview has not been presented because the effects of this acquisition were not material to our consolidated results of operations.

22

NOTES TO UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS

____

3. Acquisitions, Continued:

EarthLink Holdings Corp.

On February 27, 2017, Windstream Holdings completed its merger with EarthLink Holdings Corp. (“EarthLink”), pursuant to the terms of the Agreement and Plan of Merger (the “Merger Agreement”) dated November 5, 2016, whereby EarthLink merged into Europa Merger Sub, Inc., an wholly-owned subsidiary of Windstream Services, LLC, and survived, and immediately following, merged with Europa Merger Sub, LLC, a wholly-owned subsidiary of Windstream Services, LLC, with Merger Sub surviving and changing its name to EarthLink Holdings, LLC (the “Merger”). EarthLink Holdings, LLC is a direct, wholly-owned subsidiary of Windstream Services and provides data, voice and managed network services to retail and wholesale business customers and nationwide Internet access and related value-added services to residential customers. In the Merger, we added approximately 700,000 customers and approximately 16,000 incremental route fiber miles, which expanded our national footprint to approximately 150,000 fiber route miles and enhanced our ability to offer customers expanded products, services and enhanced enterprise solutions. We also expect to achieve operating expense and capital expenditure synergies in integrating the acquired operations. Pursuant to the terms of the Merger Agreement, each share of EarthLink common stock was exchanged, on a post-reverse stock split basis, for .1636 of Windstream Holdings common stock. No fractional shares were issued in the Merger, with a cash payment being made in lieu of fractional shares. Employee restricted stock units issued by EarthLink that were outstanding as of the merger date were exchanged for an equivalent number of Windstream Holdings restricted stock units based on the same exchange ratio of EarthLink common stock to Windstream Holdings common stock. The replacement restricted stock units remain subject to the vesting and other terms and conditions prescribed by the EarthLink equity plans that were assumed by us in the Merger. In the aggregate, on a post-reverse stock split basis,Windstream Holdings issued 17.6 million shares of its common stock and 1.0 million of replacement equity awards. Windstream also assumed $435.3 million aggregate principal amount of EarthLink’s long-term debt, which we refinanced, as further discussed in Note 5. The Merger qualifies as a tax-free reorganization for U.S. federal income tax purposes and is valued at approximately $1.1 billion.

The results of EarthLink’s operations are included in our consolidated results of operations beginning on February 27, 2017. For the three and six month periods ended June 30, 2017, our consolidated results of operations include revenues and sales of $225.0 million and $307.1 million and operating income of $6.8 million and $4.0 million attributable to EarthLink. We incurred $6.6 million and $11.0 million of merger and integration expenses during the three and six month periods ended June 30, 2018, respectively, as compared to $13.4 million and $66.5 million for the same period in 2017 related to the completion of the Merger (see Note 10).

The following unaudited pro forma consolidated results of operations of Windstream for the three and six month periods ended June 30, 2017 assume that the Merger occurred as of January 1, 2016:

(Millions) | Three Months Ended June 30, 2017 | Six Months Ended June 30, 2017 | ||||||||||

Revenues and sales | $ | 1,491.6 | $ | 3,006.8 | ||||||||

Operating income | $ | 104.3 | $ | 168.5 | ||||||||

Net loss | $ | (70.4 | ) | $ | (168.1 | ) | ||||||

Loss per share | ($1.89 | ) | ($4.57 | ) | ||||||||

The pro forma information presents our historical results of operations adjusted to include EarthLink, with the results prior to the merger closing date adjusted to include the pro forma effect of the elimination of transactions between Windstream and EarthLink, the adjustment to revenues and sales to change EarthLink’s reporting of USF fees billed to customers and the related payments from a net basis to a gross basis to conform to Windstream’s reporting of such customer billings, the adjustment to depreciation and amortization expense associated with the estimated acquired fair value of property, plant and equipment and intangible assets, the adjustment to interest expense to reflect the refinancing of EarthLink’s long-term debt obligations, the impact of merger expenses related to the acquisition and the related income tax effects of the pro forma adjustments.