Attached files

| file | filename |

|---|---|

| EX-99.3 - EX-99.3 - CONNECTICUT WATER SERVICE INC / CT | d573502dex993.htm |

| EX-99.1 - EX-99.1 - CONNECTICUT WATER SERVICE INC / CT | d573502dex991.htm |

| EX-2.1 - EX-2.1 - CONNECTICUT WATER SERVICE INC / CT | d573502dex21.htm |

| 8-K - 8-K - CONNECTICUT WATER SERVICE INC / CT | d573502d8k.htm |

Exhibit 99.2 Creating a Leading National Water Utility: Revised Merger Terms August 6, 2018 Exhibit 99.2 Creating a Leading National Water Utility: Revised Merger Terms August 6, 2018

Safe Harbor Statement Cautionary Statement Regarding Forward-Looking Statements This document contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. Some of these forward-looking statements can be identified by the use of forward-looking words such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “approximately,” “intends,” “plans,” “estimates,” “projects,” “strategy,” or “anticipates,” or the negative of those words or other comparable terminology. The accuracy of such statements is subject to a number of risks, uncertainties and assumptions including, but not limited to, the following factors: (1) the risk that the conditions to the closing of the transaction are not satisfied, including the risk that required approval from the shareholders of CTWS for the transaction is not obtained; (2) the risk that the regulatory approvals required for the transaction are not obtained, on the terms expected or on the anticipated schedule; (3) the effect of water, utility, environmental and other governmental policies and regulations; (4) litigation relating to the transaction; (5) the ability of the parties to the transaction to meet expectations regarding the timing, completion and accounting and tax treatments of the proposed transaction; (6) the occurrence of any event, change or other circumstance that could give rise to the termination of the transaction agreement between the parties to the proposed transaction; (7) changes in demand for water and other products and services of CTWS; (8) unanticipated weather conditions; (9) catastrophic events such as fires, earthquakes, explosions, floods, ice storms, tornadoes, terrorist acts, physical attacks, cyber attacks, or other similar occurrences that could adversely affect CTWS’s facilities, operations, financial condition, results of operations, and reputation; (10) risks that the proposed transaction disrupts the current plans and operations of CTWS; (11) potential difficulties in employee retention as a result of the proposed transaction; (12) unexpected costs, charges or expenses resulting from the transaction; (13) the effect of the announcement or pendency of the proposed transaction on CTWS’s business relationships, operating results, and business generally, including, without limitation, competitive responses to the proposed transaction; (14) risks related to diverting management’s attention from ongoing business operations of CTWS; (15) the trading price of CTWS’s common stock; and (16) legislative and economic developments. In addition, actual results are subject to other risks and uncertainties that relate more broadly to CTWS’s overall business and financial condition, including those more fully described in CTWS’s filings with the U.S. Securities and Exchange Commission (the “SEC”), including, without limitation, its annual report on Form 10-K for the fiscal year ended December 31, 2017. Forward looking statements are not guarantees of performance, and speak only as of the date made, and none of SJW, its management, CTWS or its management undertakes any obligation to update or revise any forward-looking statements except as required by law. 2 Safe Harbor Statement Cautionary Statement Regarding Forward-Looking Statements This document contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. Some of these forward-looking statements can be identified by the use of forward-looking words such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “approximately,” “intends,” “plans,” “estimates,” “projects,” “strategy,” or “anticipates,” or the negative of those words or other comparable terminology. The accuracy of such statements is subject to a number of risks, uncertainties and assumptions including, but not limited to, the following factors: (1) the risk that the conditions to the closing of the transaction are not satisfied, including the risk that required approval from the shareholders of CTWS for the transaction is not obtained; (2) the risk that the regulatory approvals required for the transaction are not obtained, on the terms expected or on the anticipated schedule; (3) the effect of water, utility, environmental and other governmental policies and regulations; (4) litigation relating to the transaction; (5) the ability of the parties to the transaction to meet expectations regarding the timing, completion and accounting and tax treatments of the proposed transaction; (6) the occurrence of any event, change or other circumstance that could give rise to the termination of the transaction agreement between the parties to the proposed transaction; (7) changes in demand for water and other products and services of CTWS; (8) unanticipated weather conditions; (9) catastrophic events such as fires, earthquakes, explosions, floods, ice storms, tornadoes, terrorist acts, physical attacks, cyber attacks, or other similar occurrences that could adversely affect CTWS’s facilities, operations, financial condition, results of operations, and reputation; (10) risks that the proposed transaction disrupts the current plans and operations of CTWS; (11) potential difficulties in employee retention as a result of the proposed transaction; (12) unexpected costs, charges or expenses resulting from the transaction; (13) the effect of the announcement or pendency of the proposed transaction on CTWS’s business relationships, operating results, and business generally, including, without limitation, competitive responses to the proposed transaction; (14) risks related to diverting management’s attention from ongoing business operations of CTWS; (15) the trading price of CTWS’s common stock; and (16) legislative and economic developments. In addition, actual results are subject to other risks and uncertainties that relate more broadly to CTWS’s overall business and financial condition, including those more fully described in CTWS’s filings with the U.S. Securities and Exchange Commission (the “SEC”), including, without limitation, its annual report on Form 10-K for the fiscal year ended December 31, 2017. Forward looking statements are not guarantees of performance, and speak only as of the date made, and none of SJW, its management, CTWS or its management undertakes any obligation to update or revise any forward-looking statements except as required by law. 2

Creating a Leading National Water Utility Geographic Diversity, Local Expertise Transaction Highlights • Incremental scale creates a significantly stronger platform for long-term water utility growth • SJW Group (NYSE:SJW) and Connecticut Water Service, Inc. • Diversifies utility footprint spanning four states with constructive regulatory mechanisms in each (Nasdaq:CTWS) announcing revised merger • Combines best-in-class operational and customer service practices Strategic • Underscores commitment to realizing benefits of combination Benefits and • Strengthens position as an industry leader to affect positive changes in federal and state water • Cash consideration of $70.00/share Industrial Logic utility policies • Represents 33% premium to CTWS’ unaffected share price as • Enhances value proposition as combined company is better-positioned to identify and compete for of March 14, 2018 attractive growth opportunities • Exceeds CTWS’ all-time high price of $69.72/share • Accretive to EPS in first full year, increasing to mid-to-high single-digit percentage accretion thereafter rd • Creates 3 largest investor-owned water and wastewater utility SJW states of operation • Significant rate base expansion expected to drive long-term EPS growth with footprint across four states CTWS states of operation • SJW’s attractive dividend policy supported by more diverse and stable earnings • Immediately accretive to EPS in 2019, increasing thereafter to Corporate headquarters 1 high single-digit percentage accretion in subsequent years Investor Benefits • Immediate dividend uplift of approximately 7% for CTWS shareholders New England headquarters • Substantial upfront value to shareholders with 18% premium to current CTWS share price • Enhanced growth platform as a result of increased scale, geographic diversity and strong financial foundation • Financial and operational scale improves cost of capital, market access and liquidity • Combines leadership teams with strong records of strategic execution and value creation • Improves cash flow stability and maintains SJW’s commitment to a strong investment grade credit rating of at least “A-” 3 Creating a Leading National Water Utility Geographic Diversity, Local Expertise Transaction Highlights • Incremental scale creates a significantly stronger platform for long-term water utility growth • SJW Group (NYSE:SJW) and Connecticut Water Service, Inc. • Diversifies utility footprint spanning four states with constructive regulatory mechanisms in each (Nasdaq:CTWS) announcing revised merger • Combines best-in-class operational and customer service practices Strategic • Underscores commitment to realizing benefits of combination Benefits and • Strengthens position as an industry leader to affect positive changes in federal and state water • Cash consideration of $70.00/share Industrial Logic utility policies • Represents 33% premium to CTWS’ unaffected share price as • Enhances value proposition as combined company is better-positioned to identify and compete for of March 14, 2018 attractive growth opportunities • Exceeds CTWS’ all-time high price of $69.72/share • Accretive to EPS in first full year, increasing to mid-to-high single-digit percentage accretion thereafter rd • Creates 3 largest investor-owned water and wastewater utility SJW states of operation • Significant rate base expansion expected to drive long-term EPS growth with footprint across four states CTWS states of operation • SJW’s attractive dividend policy supported by more diverse and stable earnings • Immediately accretive to EPS in 2019, increasing thereafter to Corporate headquarters 1 high single-digit percentage accretion in subsequent years Investor Benefits • Immediate dividend uplift of approximately 7% for CTWS shareholders New England headquarters • Substantial upfront value to shareholders with 18% premium to current CTWS share price • Enhanced growth platform as a result of increased scale, geographic diversity and strong financial foundation • Financial and operational scale improves cost of capital, market access and liquidity • Combines leadership teams with strong records of strategic execution and value creation • Improves cash flow stability and maintains SJW’s commitment to a strong investment grade credit rating of at least “A-” 3

rd SJW + CTWS: 3 Largest Water and Wastewater Utility 1 Investor-Owned Water Utilities by Enterprise Value ($B) $23.7 $8.8 $3.0 $2.7 $2.6 $1.8 $1.1 $0.9 $0.5 $0.5 2 AWK WTR Pro forma CWT AWR SJW CTWS MSEX YORW ARTNA 3 Investor-Owned Water Utilities by Rate Base ($B) $11.6 $4.1 $1.3 $1.1 $0.8 $0.8 $0.6 $0.5 $0.3 $0.2 AWK WTR Pro forma CWT AWR SJW MSEX CTWS YORW ARTNA 1 Source: SEC filings, FactSet as of 07/31/2018 2 Pro forma enterprise value based on pro forma equity value, new HoldCo debt issued to fund purchase price, and standalone SJW and CTWS non-equity capitalization; pro forma equity value calculated using median water utility 2019E P/E (excluding SJW and CTWS) and 2019E pro forma net income 3 2017 rate base per company investor presentations and regulatory filings. 2017 net utility plant from SEC filings used in lieu of rate base for MSEX and ARTNA due to lack of recent rate base disclosure 4 rd SJW + CTWS: 3 Largest Water and Wastewater Utility 1 Investor-Owned Water Utilities by Enterprise Value ($B) $23.7 $8.8 $3.0 $2.7 $2.6 $1.8 $1.1 $0.9 $0.5 $0.5 2 AWK WTR Pro forma CWT AWR SJW CTWS MSEX YORW ARTNA 3 Investor-Owned Water Utilities by Rate Base ($B) $11.6 $4.1 $1.3 $1.1 $0.8 $0.8 $0.6 $0.5 $0.3 $0.2 AWK WTR Pro forma CWT AWR SJW MSEX CTWS YORW ARTNA 1 Source: SEC filings, FactSet as of 07/31/2018 2 Pro forma enterprise value based on pro forma equity value, new HoldCo debt issued to fund purchase price, and standalone SJW and CTWS non-equity capitalization; pro forma equity value calculated using median water utility 2019E P/E (excluding SJW and CTWS) and 2019E pro forma net income 3 2017 rate base per company investor presentations and regulatory filings. 2017 net utility plant from SEC filings used in lieu of rate base for MSEX and ARTNA due to lack of recent rate base disclosure 4

93% Regulated Earnings Across Diversified Geographic and Regulatory Markets + Unregulated Unregulated Unregulated 9% 5% 7% Net Income by Segment Regulated Regulated Regulated 91% 95% 93% TX ME 8% 15% CT 30% Net Income by CA CA CT State 60% 92% 85% ME 5% TX 5% Note: Based on 2017 net income 5 93% Regulated Earnings Across Diversified Geographic and Regulatory Markets + Unregulated Unregulated Unregulated 9% 5% 7% Net Income by Segment Regulated Regulated Regulated 91% 95% 93% TX ME 8% 15% CT 30% Net Income by CA CA CT State 60% 92% 85% ME 5% TX 5% Note: Based on 2017 net income 5

Revised Transaction Overview • Offer price of $70.00/CTWS share in cash • Represents a 33% premium to CTWS’ unaffected share price as of March 14, 2018 Key Terms & • Equity purchase price of $843mm; transaction value of $1,138mm Financing • Financing strategy consistent with SJW’s strong credit profile • Immediately and increasingly accretive to SJW EPS • Eric Thornburg to serve as Chairman, President and CEO Management & • New England Region President based in Connecticut Governance • Current SJW Board of Directors to be expanded by 2 seats, which will be filled by current CTWS Directors selected by SJW • Maintain SJW current annual dividend per share and policy of dividend growth Dividend • Closing expected by Q1 2019 • HSR waiting period terminated on April 27, 2018 Approvals and 1 Timing • Subject to approvals from the Connecticut Public Utilities Regulatory Authority, the Maine Public Utilities Commission, and the Federal Communications Commission 1 The California Public Utilities Commission (CPUC) previously instituted an investigation into whether the transaction is subject to its approval and anticipated impacts in California, planning to complete its inquiry in time to allow the acquisition to go forward, if appropriate, by the end of 2018; it is anticipated that consideration of the revised transaction will not substantially extend the current CPUC investigation 6 Revised Transaction Overview • Offer price of $70.00/CTWS share in cash • Represents a 33% premium to CTWS’ unaffected share price as of March 14, 2018 Key Terms & • Equity purchase price of $843mm; transaction value of $1,138mm Financing • Financing strategy consistent with SJW’s strong credit profile • Immediately and increasingly accretive to SJW EPS • Eric Thornburg to serve as Chairman, President and CEO Management & • New England Region President based in Connecticut Governance • Current SJW Board of Directors to be expanded by 2 seats, which will be filled by current CTWS Directors selected by SJW • Maintain SJW current annual dividend per share and policy of dividend growth Dividend • Closing expected by Q1 2019 • HSR waiting period terminated on April 27, 2018 Approvals and 1 Timing • Subject to approvals from the Connecticut Public Utilities Regulatory Authority, the Maine Public Utilities Commission, and the Federal Communications Commission 1 The California Public Utilities Commission (CPUC) previously instituted an investigation into whether the transaction is subject to its approval and anticipated impacts in California, planning to complete its inquiry in time to allow the acquisition to go forward, if appropriate, by the end of 2018; it is anticipated that consideration of the revised transaction will not substantially extend the current CPUC investigation 6

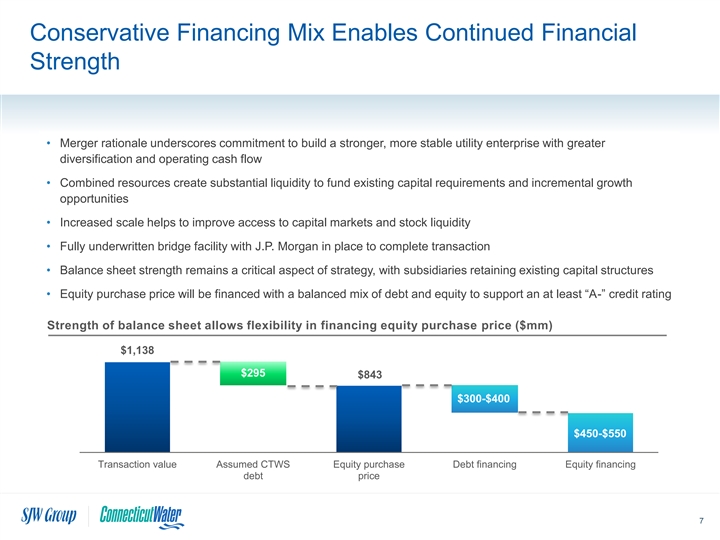

Conservative Financing Mix Enables Continued Financial Strength • Merger rationale underscores commitment to build a stronger, more stable utility enterprise with greater diversification and operating cash flow • Combined resources create substantial liquidity to fund existing capital requirements and incremental growth opportunities • Increased scale helps to improve access to capital markets and stock liquidity • Fully underwritten bridge facility with J.P. Morgan in place to complete transaction • Balance sheet strength remains a critical aspect of strategy, with subsidiaries retaining existing capital structures • Equity purchase price will be financed with a balanced mix of debt and equity to support an at least “A-” credit rating Strength of balance sheet allows flexibility in financing equity purchase price ($mm) $1,138 $295 $843 $300-$400 $450-$550 Transaction value Assumed CTWS Equity purchase Debt financing Equity financing debt price 7 Conservative Financing Mix Enables Continued Financial Strength • Merger rationale underscores commitment to build a stronger, more stable utility enterprise with greater diversification and operating cash flow • Combined resources create substantial liquidity to fund existing capital requirements and incremental growth opportunities • Increased scale helps to improve access to capital markets and stock liquidity • Fully underwritten bridge facility with J.P. Morgan in place to complete transaction • Balance sheet strength remains a critical aspect of strategy, with subsidiaries retaining existing capital structures • Equity purchase price will be financed with a balanced mix of debt and equity to support an at least “A-” credit rating Strength of balance sheet allows flexibility in financing equity purchase price ($mm) $1,138 $295 $843 $300-$400 $450-$550 Transaction value Assumed CTWS Equity purchase Debt financing Equity financing debt price 7

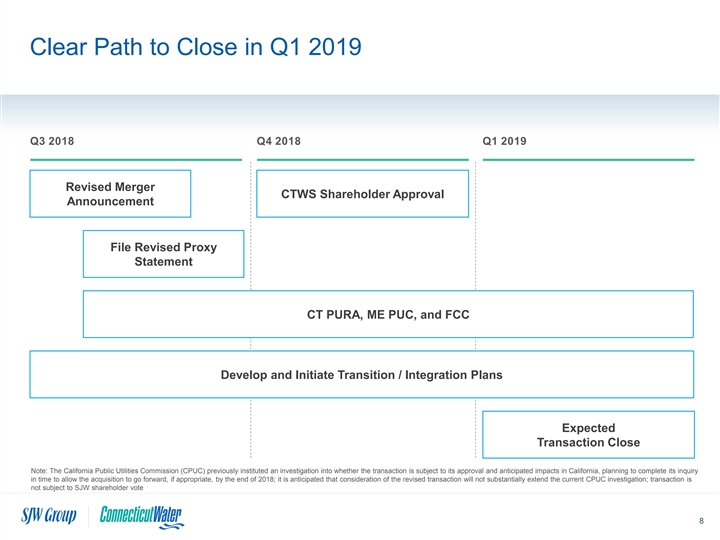

Clear Path to Close in Q1 2019 Q3 2018 Q4 2018 Q1 2019 Revised Merger CTWS Shareholder Approval Announcement File Revised Proxy Statement CT PURA, ME PUC, and FCC Develop and Initiate Transition / Integration Plans Expected Transaction Close Note: The California Public Utilities Commission (CPUC) previously instituted an investigation into whether the transaction is subject to its approval and anticipated impacts in California, planning to complete its inquiry in time to allow the acquisition to go forward, if appropriate, by the end of 2018; it is anticipated that consideration of the revised transaction will not substantially extend the current CPUC investigation; transaction is not subject to SJW shareholder vote 8 Clear Path to Close in Q1 2019 Q3 2018 Q4 2018 Q1 2019 Revised Merger CTWS Shareholder Approval Announcement File Revised Proxy Statement CT PURA, ME PUC, and FCC Develop and Initiate Transition / Integration Plans Expected Transaction Close Note: The California Public Utilities Commission (CPUC) previously instituted an investigation into whether the transaction is subject to its approval and anticipated impacts in California, planning to complete its inquiry in time to allow the acquisition to go forward, if appropriate, by the end of 2018; it is anticipated that consideration of the revised transaction will not substantially extend the current CPUC investigation; transaction is not subject to SJW shareholder vote 8

Creating a Leading Water Utility Company • Well positioned to deliver continued superior shareholder returns and best-in- class customer service • More diverse, stable and higher earnings growth profile than could be achieved standalone • Ability to leverage nationwide footprint to pursue attractive capital deployment opportunities • Robust dividend growth supported by solid investment grade balance sheet • Experienced management teams with proven track records of success • Advantages of geographic diversity, while maintaining local focus and expertise 9 Creating a Leading Water Utility Company • Well positioned to deliver continued superior shareholder returns and best-in- class customer service • More diverse, stable and higher earnings growth profile than could be achieved standalone • Ability to leverage nationwide footprint to pursue attractive capital deployment opportunities • Robust dividend growth supported by solid investment grade balance sheet • Experienced management teams with proven track records of success • Advantages of geographic diversity, while maintaining local focus and expertise 9

Additional Information Additional Information and Where to Find It This communication may be deemed to be solicitation material in respect of the proposed acquisition of CTWS by SJW. In connection with the proposed transaction, SJW and CTWS intend to file relevant materials with the SEC, including CTWS’s proxy statement on Schedule 14A. SHAREHOLDERS OF CTWS ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING CTWS’S PROXY STATEMENT, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors and security holders will be able to obtain the documents free of charge at the SEC’s web site, http://www.sec.gov, and CTWS’s shareholders will receive information at an appropriate time on how to obtain transaction-related documents free of charge from CTWS. Such documents are not currently available. Participants in Solicitation SJW and its directors and executive officers, and CTWS and its directors and executive officers, may be deemed to be participants in the solicitation of proxies from the holders of CTWS’s common stock in respect of the proposed transaction. Information about the directors and executive officers of SJW is set forth in the proxy statement for SJW’s 2018 Annual Meeting of Stockholders, which was filed with the SEC on March 6, 2018. Information about the directors and executive officers of CTWS is set forth in the proxy statement for CTWS’s 2018 Annual Meeting of Shareholders, which was filed with the SEC on April 6, 2018. Investors may obtain additional information regarding the interest of such participants by reading the proxy statement regarding the acquisition when it becomes available. 10 Additional Information Additional Information and Where to Find It This communication may be deemed to be solicitation material in respect of the proposed acquisition of CTWS by SJW. In connection with the proposed transaction, SJW and CTWS intend to file relevant materials with the SEC, including CTWS’s proxy statement on Schedule 14A. SHAREHOLDERS OF CTWS ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING CTWS’S PROXY STATEMENT, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors and security holders will be able to obtain the documents free of charge at the SEC’s web site, http://www.sec.gov, and CTWS’s shareholders will receive information at an appropriate time on how to obtain transaction-related documents free of charge from CTWS. Such documents are not currently available. Participants in Solicitation SJW and its directors and executive officers, and CTWS and its directors and executive officers, may be deemed to be participants in the solicitation of proxies from the holders of CTWS’s common stock in respect of the proposed transaction. Information about the directors and executive officers of SJW is set forth in the proxy statement for SJW’s 2018 Annual Meeting of Stockholders, which was filed with the SEC on March 6, 2018. Information about the directors and executive officers of CTWS is set forth in the proxy statement for CTWS’s 2018 Annual Meeting of Shareholders, which was filed with the SEC on April 6, 2018. Investors may obtain additional information regarding the interest of such participants by reading the proxy statement regarding the acquisition when it becomes available. 10