Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Douglas Emmett Inc | a2018q2exhibit322-cfo906ce.htm |

| EX-32.1 - EXHIBIT 32.1 - Douglas Emmett Inc | a2018q2exhibit321-ceo906ce.htm |

| EX-31.2 - EXHIBIT 31.2 - Douglas Emmett Inc | a2018q2exhibit312-cfo302ce.htm |

| EX-31.1 - EXHIBIT 31.1 - Douglas Emmett Inc | a2018q2exhibit311-ceo302ce.htm |

United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2018

Commission file number 001-33106

Douglas Emmett, Inc.

(Exact name of registrant as specified in its charter)

Maryland | 20-3073047 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

808 Wilshire Boulevard, Suite 200, Santa Monica, California | 90401 |

(Address of principal executive offices) | (Zip Code) |

(310) 255-7700

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of "large accelerated filer", "accelerated filer", "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer ¨ |

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Emerging growth company ¨ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

Class | Outstanding at | July 27, 2018 | |

Common Stock, $0.01 par value per share | 169,917,966 | shares | |

1

DOUGLAS EMMETT, INC. FORM 10-Q | ||

Table of Contents | ||

Page | ||

2

Glossary

Abbreviations used in this Report:

AOCI | Accumulated Other Comprehensive Income (Loss) |

ASU | Accounting Standards Update |

ATM | At-the-Market |

BOMA | Building Owners and Managers Association |

CEO | Chief Executive Officer |

CFO | Chief Financial Officer |

Code | Internal Revenue Code of 1986, as amended |

DEI | Douglas Emmett, Inc. |

EPS | Earnings Per Share |

Exchange Act | Securities Exchange Act of 1934, as amended |

FASB | Financial Accounting Standards Board |

FDIC | Federal Deposit Insurance Corporation |

FFO | Funds from Operations |

Fund X | Douglas Emmett Fund X, LLC |

Funds | Unconsolidated institutional real estate funds (Fund X, Partnership X and Opportunity Fund) |

GAAP | Generally Accepted Accounting Principles (United States) |

JV | Joint Venture |

LIBOR | London Interbank Offered Rate |

LTIP Units | Long-Term Incentive Plan Units |

NAREIT | National Association of Real Estate Investment Trusts |

OCI | Other Comprehensive Income (Loss) |

OP Units | Operating Partnership Units |

Operating Partnership | Douglas Emmett Properties, LP |

Opportunity Fund | Fund X Opportunity Fund, LLC |

Partnership X | Douglas Emmett Partnership X, LP |

PCAOB | Public Company Accounting Oversight Board (United States) |

REIT | Real Estate Investment Trust |

Report | Quarterly Report on Form 10-Q |

SEC | Securities and Exchange Commission |

Securities Act | Securities Act of 1933, as amended |

TRS | Taxable REIT subsidiary(ies) |

US | United States |

VIE | Variable Interest Entity(ies) |

3

Glossary

Defined terms used in this Report:

Annualized Rent | Annualized cash base rent (excluding tenant reimbursements, parking and other income) before abatements under leases commenced as of the reporting date. Annualized rent for our triple net office leases is calculated by adding expense reimbursements and estimates of normal building expenses paid by tenants to base rent. Annualized rent does not include lost rent recovered from insurance and rent for building management use. |

Consolidated Portfolio | Includes the properties in our consolidated results, which includes the properties owned by our consolidated JVs. |

Funds From Operations (FFO) | We calculate FFO in accordance with the standards established by NAREIT by excluding gains (or losses) on sales of investments in real estate, real estate depreciation and amortization (other than amortization of deferred loan costs) from our net income (including adjusting for the effect of such items attributable to consolidated joint ventures and unconsolidated real estate funds, but not for noncontrolling interests included in our Operating Partnership). FFO is a Non-GAAP supplemental financial measure that we report because it is useful to our investors. See Management’s Discussion and Analysis of Financial Condition and Results of Operations in Item 2 for a discussion of FFO. |

Net Operating Income (NOI) | We calculate NOI, a Non-GAAP measure, as revenue less operating expenses attributable to the properties that we own and operate. NOI is calculated by excluding the following from our net income: general and administrative expense, depreciation and amortization expense, other income, other expense, income, including depreciation, from unconsolidated real estate funds, interest expense, gains (or losses) on sales of investments in real estate and net income attributable to noncontrolling interests. NOI is a Non-GAAP supplemental financial measure that we report because it is useful to our investors. See Management’s Discussion and Analysis of Financial Condition and Results of Operations in Item 2 for a discussion of our Same Properties NOI. |

Occupancy Rate | The percentage leased, excluding signed leases not yet commenced, as of the reporting date. Management space is considered leased and occupied, while space taken out of service during a repositioning is excluded from both the numerator and denominator for calculating percentage leased and occupied. |

Recurring Capital Expenditures | Building improvements required to maintain revenues once a property has been stabilized, and excludes capital expenditures for (i) acquired buildings being stabilized, (ii) newly developed space, (iii) upgrades to improve revenues or operating expenses, (iv) casualty damage or (v) bringing the property into compliance with governmental requirements. |

Rentable Square Feet | Based on the BOMA remeasurement and consists of leased square feet (including square feet with respect to signed leases not commenced as of the reporting date), available square feet, building management use square feet and square feet of the BOMA adjustment on leased space. |

Same Properties | Our wholly-owned properties that have been owned and operated by us in a consistent manner, and reported in our consolidated results during the entire span of both periods being compared. We exclude from our same property subset any properties (i) acquired during the comparative periods; (ii) sold, held for sale, contributed or otherwise removed from our consolidated financial statements during the comparative periods; or (iii) that underwent a major repositioning project that we believed significantly affected its results during the comparative periods. |

Short-Term Leases | Represents leases that expired on or before the reporting date or had a term of less than one year, including hold over tenancies, month to month leases and other short term occupancies. |

Total Portfolio | Includes our Consolidated Portfolio plus the properties owned by our Funds. |

4

This Report contains forward-looking statements within the meaning of the Section 27A of the Securities Act and Section 21E of the Exchange Act. You can find many (but not all) of these statements by looking for words such as “believe”, “expect”, “anticipate”, “estimate”, “approximate”, “intend”, “plan”, “would”, “could”, “may”, “future” or other similar expressions in this Report. We claim the protection of the safe harbor contained in the Private Securities Litigation Reform Act of 1995. We caution investors that any forward-looking statements used in this Report, or those that we make orally or in writing from time to time, are based on our beliefs and assumptions, as well as information currently available to us. Actual outcomes will be affected by known and unknown risks, trends, uncertainties and factors beyond our control or ability to predict. Although we believe that our assumptions are reasonable, they are not guarantees of future performance and some will inevitably prove to be incorrect. As a result, our future results can be expected to differ from our expectations, and those differences may be material. Accordingly, investors should use caution when relying on previously reported forward-looking statements, which were based on results and trends at the time they were made, to anticipate future results or trends. Some of the risks and uncertainties that could cause our actual results, performance or achievements to differ materially from those expressed or implied by forward-looking statements include the following:

• | adverse economic or real estate developments affecting Southern California or Honolulu, Hawaii; |

• | competition from other real estate investors in our markets; |

• | decreasing rental rates or increasing tenant incentive and vacancy rates; |

• | defaults on, early terminations of, or non-renewal of leases by tenants; |

• | increases in interest rates or operating costs; |

• | insufficient cash flows to service our outstanding debt or pay rent on ground leases; |

• | difficulties in raising capital; |

• | inability to liquidate real estate or other investments quickly; |

• | adverse changes to rent control laws and regulations; |

• | environmental uncertainties; |

• | natural disasters; |

• | insufficient insurance, or increases in insurance costs; |

• | inability to successfully expand into new markets and submarkets; |

• | difficulties in identifying properties to acquire and failure to complete acquisitions successfully; |

• | failure to successfully operate acquired properties; |

• | risks associated with property development; |

• | risks associated with JVs; |

• | conflicts of interest with our officers and reliance on key personnel; |

• | changes in zoning and other land use laws; |

• | adverse results of litigation or governmental proceedings; |

• | failure to comply with laws, regulations and covenants that are applicable to our properties; |

• | possible terrorist attacks or wars; |

• | possible cyber attacks or intrusions; |

• | adverse changes to accounting rules; |

• | weaknesses in our internal controls over financial reporting; |

• | failure to maintain our REIT status under federal tax laws; and |

• | adverse changes to tax laws, including those related to property taxes. |

For further discussion of these and other risk factors see Item 1A. "Risk Factors” in our 2017 Annual Report on Form 10-K for the fiscal year ended December 31, 2017. This Report and all subsequent written and oral forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. We do not undertake any obligation to release publicly any revisions to our forward-looking statements to reflect events or circumstances after the date of this Report.

5

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

Douglas Emmett, Inc. Consolidated Balance Sheets (In thousands, except share data) | |||||||

June 30, 2018 | December 31, 2017 | ||||||

Unaudited | |||||||

Assets | |||||||

Investment in real estate: | |||||||

Land | $ | 1,064,189 | $ | 1,062,345 | |||

Buildings and improvements | 7,945,119 | 7,886,201 | |||||

Tenant improvements and lease intangibles | 802,868 | 756,190 | |||||

Property under development | 111,760 | 124,472 | |||||

Investment in real estate, gross | 9,923,936 | 9,829,208 | |||||

Less: accumulated depreciation and amortization | (2,136,480 | ) | (2,012,752 | ) | |||

Investment in real estate, net | 7,787,456 | 7,816,456 | |||||

Cash and cash equivalents | 170,391 | 176,645 | |||||

Tenant receivables, net | 3,261 | 2,980 | |||||

Deferred rent receivables, net | 115,211 | 106,021 | |||||

Acquired lease intangible assets, net | 3,741 | 4,293 | |||||

Interest rate contract assets | 116,090 | 60,069 | |||||

Investment in unconsolidated real estate funds | 109,835 | 107,735 | |||||

Other assets | 11,999 | 18,442 | |||||

Total Assets | $ | 8,317,984 | $ | 8,292,641 | |||

Liabilities | |||||||

Secured notes payable and revolving credit facility, net | $ | 4,106,495 | $ | 4,117,390 | |||

Interest payable, accounts payable and deferred revenue | 125,419 | 103,947 | |||||

Security deposits | 50,509 | 50,414 | |||||

Acquired lease intangible liabilities, net | 62,789 | 75,635 | |||||

Interest rate contract liabilities | — | 807 | |||||

Dividends payable | 42,486 | 42,399 | |||||

Total liabilities | 4,387,698 | 4,390,592 | |||||

Equity | |||||||

Douglas Emmett, Inc. stockholders' equity: | |||||||

Common Stock, $0.01 par value, 750,000,000 authorized, 169,917,966 and 169,564,927 outstanding at June 30, 2018 and December 31, 2017, respectively | 1,699 | 1,696 | |||||

Additional paid-in capital | 3,277,643 | 3,272,539 | |||||

Accumulated other comprehensive income | 87,486 | 43,099 | |||||

Accumulated deficit | (905,085 | ) | (879,810 | ) | |||

Total Douglas Emmett, Inc. stockholders' equity | 2,461,743 | 2,437,524 | |||||

Noncontrolling interests | 1,468,543 | 1,464,525 | |||||

Total equity | 3,930,286 | 3,902,049 | |||||

Total Liabilities and Equity | $ | 8,317,984 | $ | 8,292,641 | |||

See accompanying notes to the consolidated financial statements.

6

Douglas Emmett, Inc.

Consolidated Statements of Operations

(Unaudited; in thousands, except per share data)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues | |||||||||||||||

Office rental | |||||||||||||||

Rental revenues | $ | 150,161 | $ | 135,665 | $ | 297,932 | $ | 268,681 | |||||||

Tenant recoveries | 14,654 | 12,801 | 25,707 | 23,851 | |||||||||||

Parking and other income | 28,946 | 27,076 | 57,455 | 53,358 | |||||||||||

Total office revenues | 193,761 | 175,542 | 381,094 | 345,890 | |||||||||||

Multifamily rental | |||||||||||||||

Rental revenues | 23,655 | 22,237 | 46,716 | 44,478 | |||||||||||

Parking and other income | 2,053 | 1,853 | 3,906 | 3,745 | |||||||||||

Total multifamily revenues | 25,708 | 24,090 | 50,622 | 48,223 | |||||||||||

Total revenues | 219,469 | 199,632 | 431,716 | 394,113 | |||||||||||

Operating Expenses | |||||||||||||||

Office expenses | 61,818 | 57,887 | 122,174 | 112,772 | |||||||||||

Multifamily expenses | 6,908 | 5,878 | 13,606 | 11,825 | |||||||||||

General and administrative | 9,437 | 8,592 | 19,004 | 18,748 | |||||||||||

Depreciation and amortization | 73,379 | 68,793 | 145,877 | 136,167 | |||||||||||

Total operating expenses | 151,542 | 141,150 | 300,661 | 279,512 | |||||||||||

Operating income | 67,927 | 58,482 | 131,055 | 114,601 | |||||||||||

Other income | 2,792 | 2,331 | 5,422 | 4,493 | |||||||||||

Other expenses | (2,086 | ) | (1,773 | ) | (3,819 | ) | (3,497 | ) | |||||||

Income, including depreciation, from unconsolidated real estate funds | 1,668 | 1,113 | 3,174 | 3,290 | |||||||||||

Interest expense | (33,268 | ) | (38,000 | ) | (66,168 | ) | (74,954 | ) | |||||||

Net income | 37,033 | 22,153 | 69,664 | 43,933 | |||||||||||

Less: Net income attributable to noncontrolling interests | (5,349 | ) | (1,909 | ) | (9,774 | ) | (4,640 | ) | |||||||

Net income attributable to common stockholders | $ | 31,684 | $ | 20,244 | $ | 59,890 | $ | 39,293 | |||||||

Net income attributable to common stockholders per share – basic | $ | 0.19 | $ | 0.13 | $ | 0.35 | $ | 0.25 | |||||||

Net income attributable to common stockholders per share – diluted | $ | 0.19 | $ | 0.13 | $ | 0.35 | $ | 0.25 | |||||||

Dividends declared per common share | $ | 0.25 | $ | 0.23 | $ | 0.50 | $ | 0.46 | |||||||

See accompanying notes to the consolidated financial statements.

7

Douglas Emmett, Inc.

Consolidated Statements of Comprehensive Income

(Unaudited and in thousands)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Net income | $ | 37,033 | $ | 22,153 | $ | 69,664 | $ | 43,933 | |||||||

Other comprehensive income (loss): cash flow hedges | 18,994 | (4,193 | ) | 63,363 | 5,636 | ||||||||||

Comprehensive income | 56,027 | 17,960 | 133,027 | 49,569 | |||||||||||

Less: Comprehensive (income) loss attributable to noncontrolling interests | (10,878 | ) | 297 | (28,750 | ) | (4,561 | ) | ||||||||

Comprehensive income attributable to common stockholders | $ | 45,149 | $ | 18,257 | $ | 104,277 | $ | 45,008 | |||||||

See accompanying notes to the consolidated financial statements.

8

Douglas Emmett, Inc.

Consolidated Statements of Cash Flows

(Unaudited and in thousands)

Consolidated Statements of Cash Flows

(Unaudited and in thousands)

Six Months Ended June 30, | |||||||

2018 | 2017 | ||||||

Operating Activities | |||||||

Net income | $ | 69,664 | $ | 43,933 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Income, including depreciation, from unconsolidated real estate funds | (3,174 | ) | (3,290 | ) | |||

Depreciation and amortization | 145,877 | 136,167 | |||||

Net accretion of acquired lease intangibles | (12,295 | ) | (8,476 | ) | |||

Straight-line rent | (9,191 | ) | (6,030 | ) | |||

Increase in the allowance for doubtful accounts | 1,335 | 504 | |||||

Deferred loan costs amortized and written off | 4,279 | 4,522 | |||||

Amortization of loan premium | (102 | ) | — | ||||

Non-cash market value adjustments on interest rate contracts | — | 25 | |||||

Amortization of stock-based compensation | 5,964 | 5,311 | |||||

Operating distributions from unconsolidated real estate funds | 3,174 | 3,290 | |||||

Change in working capital components: | |||||||

Tenant receivables | (1,616 | ) | (868 | ) | |||

Interest payable, accounts payable and deferred revenue | 4,974 | 16,718 | |||||

Security deposits | 95 | 2,392 | |||||

Other assets | 6,896 | 4,404 | |||||

Net cash provided by operating activities | 215,880 | 198,602 | |||||

Investing Activities | |||||||

Capital expenditures for improvements to real estate | (73,127 | ) | (51,370 | ) | |||

Capital expenditures for developments | (26,474 | ) | (23,646 | ) | |||

Property acquisitions | — | (354,023 | ) | ||||

Deposits for property acquisitions | — | (10,000 | ) | ||||

Acquisitions of additional interests in unconsolidated real estate funds | — | (2,571 | ) | ||||

Capital distributions from unconsolidated real estate funds | 3,774 | 39,962 | |||||

Net cash used in investing activities | (95,827 | ) | (401,648 | ) | |||

Financing Activities | |||||||

Proceeds from borrowings | 535,000 | 933,000 | |||||

Repayment of borrowings | (546,979 | ) | (986,069 | ) | |||

Loan cost payments | (2,924 | ) | (6,889 | ) | |||

Contributions from noncontrolling interests in consolidated JVs | — | 188,248 | |||||

Distributions paid to noncontrolling interests | (26,114 | ) | (19,202 | ) | |||

Dividends paid to common stockholders | (84,868 | ) | (70,075 | ) | |||

Taxes paid on exercise of stock options | (314 | ) | (52,704 | ) | |||

Repurchase of OP Units | (108 | ) | — | ||||

Proceeds from issuance of common stock, net | — | 276,961 | |||||

Net cash (used in) provided by financing activities | (126,307 | ) | 263,270 | ||||

(Decrease) increase in cash and cash equivalents and restricted cash | (6,254 | ) | 60,224 | ||||

Cash and cash equivalents and restricted cash - beginning balance | 176,766 | 113,048 | |||||

Cash and cash equivalents and restricted cash - ending balance | $ | 170,512 | $ | 173,272 | |||

9

Douglas Emmett, Inc.

Consolidated Statements of Cash Flows

(Unaudited and in thousands)

Consolidated Statements of Cash Flows

(Unaudited and in thousands)

Supplemental Cash Flows Information

Six Months Ended June 30, | |||||||

2018 | 2017 | ||||||

Operating Activities | |||||||

Cash paid for interest, net of capitalized interest | $ | 61,228 | $ | 69,001 | |||

Capitalized interest paid | $ | 1,558 | $ | 1,150 | |||

Non-cash Investing Transactions | |||||||

Accrual for additions to real estate and developments | $ | 16,329 | $ | 417 | |||

Capitalized stock-based compensation for improvements to real estate and developments | $ | 948 | $ | 475 | |||

Removal of fully depreciated and amortized tenant improvements and lease intangibles | $ | 22,157 | $ | 22,077 | |||

Removal of fully amortized acquired lease intangible assets | $ | 1,180 | $ | 71 | |||

Removal of fully accreted acquired lease intangible liabilities | $ | 8,899 | $ | 2,935 | |||

Non-cash Financing Transactions | |||||||

Gain recorded in AOCI - Adoption of ASU 2017-12 - consolidated derivatives | $ | 211 | $ | — | |||

Gain (loss) recorded in AOCI - consolidated derivatives | $ | 58,890 | $ | (4,016 | ) | ||

Gain recorded in AOCI - unconsolidated Funds' derivatives (our share) | $ | 6,404 | $ | 867 | |||

Dividends declared | $ | 84,955 | $ | 72,194 | |||

Common stock issued in exchange for OP Units | $ | 5,481 | $ | 8,856 | |||

See accompanying notes to the consolidated financial statements.

10

1. Overview

Organization and Business Description

Douglas Emmett, Inc. is a fully integrated, self-administered and self-managed REIT. We are one of the largest owners and operators of high-quality office and multifamily properties in Los Angeles County, California and Honolulu, Hawaii. Through our interest in our Operating Partnership and its subsidiaries, consolidated JVs and unconsolidated Funds, we focus on owning, acquiring, developing and managing a significant market share of top-tier office properties and premier multifamily communities in neighborhoods that possess significant supply constraints, high-end executive housing and key lifestyle amenities. The terms "us," "we" and "our" as used in the financial statements refer to Douglas Emmett, Inc. and its subsidiaries on a consolidated basis. At June 30, 2018, our Consolidated Portfolio consisted of (i) a 16.6 million square foot office portfolio, (ii) 3,522 multifamily apartment units and (iii) fee interests in two parcels of land from which we receive rent under ground leases. We also manage and own equity interests in unconsolidated Funds which, at June 30, 2018, owned an additional 1.8 million square feet of office space. We manage our unconsolidated Funds alongside our Consolidated Portfolio, and we therefore present the statistics for our office portfolio on a Total Portfolio basis. As of June 30, 2018, our portfolio (not including two parcels of land from which we receive rent under ground leases), consisted of the following office and multifamily properties (both of which include ancillary retail space):

Consolidated Portfolio | Total Portfolio | ||

Office | |||

Wholly-owned properties | 53 | 53 | |

Consolidated JV properties | 10 | 10 | |

Unconsolidated Fund properties | — | 8 | |

63 | 71 | ||

Multifamily | |||

Wholly-owned properties | 10 | 10 | |

Total | 73 | 81 | |

Basis of Presentation

The accompanying financial statements are the consolidated financial statements of Douglas Emmett, Inc. and its subsidiaries, including our Operating Partnership and our consolidated JVs. All significant intercompany balances and transactions have been eliminated in our consolidated financial statements. Our Operating Partnership and consolidated JVs are VIEs of which we are the primary beneficiary. As of June 30, 2018, the total consolidated assets, liabilities and equity of the VIEs was $8.32 billion (of which $7.79 billion related to investment in real estate), $4.39 billion and $3.93 billion (of which $1.47 billion related to noncontrolling interests), respectively.

The accompanying unaudited interim financial statements have been prepared pursuant to the rules and regulations of the SEC. Certain information and footnote disclosures normally included in the financial statements prepared in accordance with GAAP may have been condensed or omitted pursuant to SEC rules and regulations, although we believe that the disclosures are adequate to make their presentation not misleading. The accompanying unaudited interim financial statements include, in our opinion, all adjustments, consisting of normal recurring adjustments, necessary to present fairly the financial information set forth therein. The results of operations for the interim periods are not necessarily indicative of the results that may be expected for the year ending December 31, 2018. The interim financial statements should be read in conjunction with the consolidated financial statements in our 2017 Annual Report on Form 10-K and the notes thereto. References in this Report to the number of properties, square footage, per square footage amounts, apartment units and geography, are outside the scope of our independent registered public accounting firm’s review of our financial statements in accordance with the standards of the PCAOB.

11

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

2. Summary of Significant Accounting Policies

We adopted ASUs during the six months ended June 30, 2018 that changed our accounting policies for revenue recognition and hedge accounting disclosed in our 2017 Annual Report on Form 10-K - see "New Accounting Pronouncements" below. The adoption of these ASUs did not have a material impact on our financial statements. We have not made any other changes to our significant accounting policies disclosed in our 2017 Annual Report on Form 10-K.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make certain estimates that affect the reported amounts in the consolidated financial statements and accompanying notes. Actual results could differ materially from those estimates.

Income Taxes

We have elected to be taxed as a REIT under the Code. Provided that we qualify for taxation as a REIT, we are generally not subject to corporate-level income tax on the earnings distributed currently to our stockholders that we derive from our REIT qualifying activities. We are subject to corporate-level tax on the earnings that we derive through our TRS.

New Accounting Pronouncements

Changes to GAAP are implemented by the FASB in the form of ASUs. We consider the applicability and impact of all ASUs. Other than the ASUs discussed below, the FASB has not issued any other ASUs during 2018 that we expect to be applicable and have a material impact on our financial statements.

Adopted ASUs

During the six months ended June 30, 2018 we adopted the ASUs listed below:

Revenue from Contracts with Customers

In May 2014, the FASB issued ASU No. 2014-09, "Revenue from Contracts with Customers" (Topic 606), which provides guidance for the accounting of revenue from contracts with customers, and supersedes Topic 605, "Revenue Recognition", and most industry-specific guidance throughout the industry topics of the Codification. In March 2016, the FASB issued ASU No. 2016-08, "Principal versus Agent Considerations (Reporting Revenue Gross versus Net)", which amends Topic 606 and clarifies the guidance for principal versus agent considerations. In April 2016, the FASB issued ASU No. 2016-10, "Identifying Performance Obligations and Licensing" which amends Topic 606 and provides guidance for identifying performance obligations and licensing. In May 2016, the FASB issued ASU No. 2016-12, "Narrow-Scope Improvements and Practical Expedients" which amends Topic 606 and provides guidance for a variety of revenue recognition related topics. In February 2017, the FASB issued ASU No. 2017-05 "Other Income - Gains and Losses from the Derecognition of Nonfinancial Assets" (Subtopic 610-20), which provides guidance for recognizing gains and losses from the transfer of nonfinancial assets in contracts with non-customers. Sales of real estate are now accounted for under Subtopic 610-20 which focuses on a transfer of control. The amendments in these ASUs were effective in the first quarter of 2018 and were required to be applied on a retrospective basis.

Most of our revenues are derived from lease contracts with tenants and are not within the scope of the respective ASUs. Although our office parking revenues are within the scope of the respective ASUs, the timing and pattern of revenue recognition was not impacted. However, the scoping of our revenues could be impacted by ASU No. 2016-02, "Leases" (Topic 842), which we plan to adopt in the first quarter of 2019 - see "Recently Issued Accounting Pronouncements" further below.

Our office parking revenues are mostly derived from lease contracts with our office tenants. The lease contracts generally make a specified number of parking spaces available to the tenant, and we bill and recognize parking revenues on a monthly basis in accordance with the lease agreements generally using the monthly parking rates in effect at the time of billing. Office parking revenues were $25.7 million and $24.0 million for the three months ended June 30, 2018 and 2017, and $50.8 million and $47.2 million for the six months ended June 30, 2018 and 2017, respectively, and are included in Office parking and other income in our consolidated statements of operations. Office parking receivables were $1.0 million as of June 30, 2018 and December 31, 2017. Office parking receivables are included in Tenant receivables in our consolidated balance sheets.

12

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

Derivatives and Hedging

In August 2017, the FASB issued ASU No. 2017-12, "Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities". The ASU requires the entire change in the fair value of the hedging instrument included in the assessment of hedge effectiveness be recorded in other comprehensive income. GAAP historically provided special hedge accounting only for the portion of the hedge deemed to be “highly effective” and requires an entity to separately reflect the amount by which the hedging instrument does not offset the hedged item, which is referred to as the “ineffective” amount. The amendments are effective in the first quarter of 2019 and are required to be applied on a prospective basis. We early adopted the ASU and it did not have a material impact on our financial statements. The ASU requires the cumulative effect of initially applying the ASU as an adjustment to AOCI with a corresponding adjustment to the opening balance of retained earnings as of the beginning of the fiscal year in which the ASU is adopted. On January 1, 2018, we recorded such an adjustment to AOCI and accumulated deficit of $211 thousand. See Note 10.

ASUs Not Yet Adopted

Leases

In February 2016, the FASB issued ASU No. 2016-02, "Leases" (Topic 842). The primary difference between Topic 842 and current GAAP is the recognition of lease assets and liabilities on the balance sheet by lessees for leases classified as operating leases under current GAAP. The accounting applied by lessors is largely unchanged from current GAAP, for example, the vast majority of operating leases will remain classified as operating leases, and lessors will continue to recognize lease income for those leases on a straight-line basis over the lease term.

Topic 842 requires separation of the lease from the non-lease components (for example, maintenance services or other activities that transfer a good or service to the customer) in a contract. Only the lease components should be accounted for in accordance with Topic 842. The consideration in the contract is allocated to the lease and non-lease components on a relative standalone selling price basis and the non-lease component would be accounted for in accordance with ASC 606 ("Revenue from Contracts with Customers"). In July 2018, the FASB issued ASU No. 2018-11 which includes an optional practical expedient for lessors to elect, by class of underlying asset, to not separate the lease from the non-lease components if certain criteria are met.

Topic 842 defines initial direct costs of a lease (which we have historically capitalized) as costs that would not have been incurred had the lease not been executed. Costs to negotiate a lease that would have been incurred regardless of whether the lease was executed, such as employee salaries, are not considered to be initial direct costs, and may not be capitalized.

We pay rent under a ground lease which expires on December 31, 2086. See Note 15 for more information regarding this ground lease. We currently account for the lease as an operating lease. We are currently evaluating the ASUs to determine if this ground lease should be accounted for as a finance lease with a corresponding right-of-use asset.

The ASUs are effective in the first quarter of 2019 and are required to be adopted using a modified retrospective approach, which includes optional practical expedients related to leases that commenced before the effective date. ASU No. 2018-11 includes an optional practical expedient which allows the new requirements to be applied on the date of adoption rather than the beginning of the earliest comparative period presented.

We are in the process of evaluating the impact of the ASUs, and the related practical expedients, on our financial statements and we plan to adopt the ASUs in the first quarter of 2019.

13

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

3. Investment in Real Estate

Property previously held for sale

During the first quarter we actively marketed for sale an 80,000 square foot Class A office property and a health club located in Honolulu, Hawaii. We partially own the assets through a consolidated joint venture in which we own a two-thirds interest. The net assets were presented in our first quarter balance sheet as property held-for-sale. During the second quarter we ceased marketing the assets for sale and reclassified the net assets in our balance sheet to investment in real estate.

Acquisitions during the six months ended June 30, 2017

We account for our property acquisitions as asset acquisitions. Prior to January 1, 2017, we accounted for our property acquisitions as business combinations. The acquired properties results of operations are included in our results of operations from the respective acquisition dates.

On April 25, 2017, a consolidated JV that we manage and in which we own an equity interest acquired two Class A office properties. The table below summarizes the purchase price allocations for the acquisitions. The contract and purchase prices differ due to prorations and similar matters:

(In thousands) | 1299 Ocean | 429 Santa Monica | |||||

Submarket | Santa Monica | Santa Monica | |||||

Acquisition date | April 25 | April 25 | |||||

Contract price | $ | 275,800 | $ | 77,000 | |||

Building square footage | 206 | 87 | |||||

Investment in real estate: | |||||||

Land | $ | 22,748 | $ | 4,949 | |||

Buildings and improvements | 260,188 | 69,286 | |||||

Tenant improvements and lease intangibles | 5,010 | 3,248 | |||||

Acquired above- and below-market leases, net | (10,683 | ) | (722 | ) | |||

Net assets and liabilities acquired | $ | 277,263 | $ | 76,761 | |||

14

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

4. Acquired Lease Intangibles

Summary of our Acquired Lease Intangibles

The table below summarizes our above- and below-market leases:

(In thousands) | June 30, 2018 | December 31, 2017 | |||||

Above-market tenant leases | $ | 5,997 | $ | 7,177 | |||

Above-market tenant leases - accumulated amortization | (3,209 | ) | (3,846 | ) | |||

Above-market ground lease where we are the lessor | 1,152 | 1,152 | |||||

Above-market ground lease - accumulated amortization | (199 | ) | (190 | ) | |||

Acquired lease intangible assets, net | $ | 3,741 | $ | 4,293 | |||

Below-market tenant leases | $ | 118,707 | $ | 127,606 | |||

Below-market tenant leases - accumulated accretion | (59,350 | ) | (55,428 | ) | |||

Above-market ground lease where we are the tenant | 4,017 | 4,017 | |||||

Above-market ground lease - accumulated accretion | (585 | ) | (560 | ) | |||

Acquired lease intangible liabilities, net | $ | 62,789 | $ | 75,635 | |||

Impact on the Consolidated Statements of Operations

The table below summarizes the net amortization/accretion related to our above- and below-market leases :

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

(In thousands) | 2018 | 2017 | 2018 | 2017 | |||||||||||

Net accretion of above- and below-market tenant lease assets and liabilities(1) | $ | 6,134 | $ | 4,275 | $ | 12,277 | $ | 8,458 | |||||||

Amortization of an above-market ground lease asset(2) | (4 | ) | (4 | ) | (8 | ) | (8 | ) | |||||||

Accretion of an above-market ground lease liability(3) | 13 | 13 | 26 | 26 | |||||||||||

Total | $ | 6,143 | $ | 4,284 | $ | 12,295 | $ | 8,476 | |||||||

______________________________________________

(1) | Recorded as a net increase to office and multifamily rental revenues. |

(2) | Recorded as a decrease to office parking and other income. |

(3) | Recorded as a decrease to office expense. |

15

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

5. Investments in Unconsolidated Real Estate Funds

Description of our Funds

We manage and own equity interests in three unconsolidated Funds, the Opportunity Fund, Fund X and Partnership X, through which we and investors own eight office properties totaling 1.8 million square feet. At June 30, 2018, we held direct and indirect equity interests of 6.2% of the Opportunity Fund, 69.4% of Fund X and 24.3% of Partnership X. Our Funds pay us fees and reimburse us for certain expenses related to property management and other services we provide. We also receive distributions based on invested capital and on any profits that exceed certain specified cash returns to the investors. The table below presents cash distributions received from our Funds:

Six Months Ended June 30, | |||||||

(In thousands) | 2018 | 2017 | |||||

Operating distributions received | $ | 3,174 | $ | 3,290 | |||

Capital distributions received | 3,774 | 39,962 | |||||

Total distributions received | $ | 6,948 | $ | 43,252 | |||

Summarized Financial Information for our Funds

The tables below present selected financial information for the Funds on a combined basis. The amounts presented reflect 100% (not our pro-rata share) of amounts related to the Funds, and are based upon historical acquired book value:

(In thousands) | June 30, 2018 | December 31, 2017 | |||||

Total assets | $ | 708,436 | $ | 704,186 | |||

Total liabilities | $ | 525,144 | $ | 523,767 | |||

Total equity | $ | 183,292 | $ | 180,419 | |||

Six Months Ended June 30, | |||||||

(In thousands) | 2018 | 2017 | |||||

Total revenues | $ | 38,963 | $ | 37,071 | |||

Operating income | $ | 11,504 | $ | 9,723 | |||

Net income | $ | 3,180 | $ | 2,853 | |||

6. Other Assets

Other assets consisted of the following:

(In thousands) | June 30, 2018 | December 31, 2017 | |||||

Restricted cash | $ | 121 | $ | 121 | |||

Prepaid expenses | 2,952 | 9,235 | |||||

Other indefinite-lived intangibles | 1,988 | 1,988 | |||||

Furniture, fixtures and equipment, net | 839 | 1,155 | |||||

Other | 6,099 | 5,943 | |||||

Total other assets | $ | 11,999 | $ | 18,442 | |||

16

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

7. Secured Notes Payable and Revolving Credit Facility, Net

The following table summarizes our secured notes payable and revolving credit facility:

Description | Maturity Date(1) | Principal Balance as of June 30, 2018 (In thousands) | Principal Balance as of December 31, 2017 (In thousands) | Variable Interest Rate | Fixed Interest Rate(2) | Swap Maturity Date | ||||||||||

Wholly Owned Subsidiaries | ||||||||||||||||

Term loan(3) | — | $ | — | $ | 146,974 | — | — | — | ||||||||

Term loan(3) | — | — | 280,721 | — | — | — | ||||||||||

Fannie Mae loan | 10/1/2019 | 145,000 | 145,000 | LIBOR + 1.25% | N/A | N/A | ||||||||||

Term loan(4) | 4/15/2022 | 340,000 | 340,000 | LIBOR + 1.40% | 2.77% | 4/1/2020 | ||||||||||

Term loan(4) | 7/27/2022 | 180,000 | 180,000 | LIBOR + 1.45% | 3.06% | 7/1/2020 | ||||||||||

Term loan(4) | 11/1/2022 | 400,000 | 400,000 | LIBOR + 1.35% | 2.64% | 11/1/2020 | ||||||||||

Term loan(4) | 6/23/2023 | 360,000 | 360,000 | LIBOR + 1.55% | 2.57% | 7/1/2021 | ||||||||||

Term loan(4) | 12/23/2023 | 220,000 | 220,000 | LIBOR + 1.70% | 3.62% | 12/23/2021 | ||||||||||

Term loan(4) | 1/1/2024 | 300,000 | 300,000 | LIBOR + 1.55% | 3.46% | 1/1/2022 | ||||||||||

Term loan(4) | 3/3/2025 | 335,000 | — | LIBOR + 1.30% | 3.84% | 3/1/2023 | ||||||||||

Fannie Mae loan(4) | 4/1/2025 | 102,400 | 102,400 | LIBOR + 1.25% | 2.84% | 3/1/2020 | ||||||||||

Fannie Mae loans(4) | 12/1/2025 | 115,000 | 115,000 | LIBOR + 1.25% | 2.76% | 12/1/2020 | ||||||||||

Fannie Mae loans(4) | 6/1/2027 | 550,000 | 550,000 | LIBOR + 1.37% | 3.16% | 6/1/2022 | ||||||||||

Term loan(5) | 6/1/2038 | 31,929 | 32,213 | N/A | 4.55% | N/A | ||||||||||

Revolving credit facility(6) | 8/21/2020 | 81,000 | — | LIBOR + 1.40% | N/A | N/A | ||||||||||

Total Wholly Owned Subsidiary Debt | 3,160,329 | 3,172,308 | ||||||||||||||

Consolidated JVs | ||||||||||||||||

Term loan(4) | 2/28/2023 | 580,000 | 580,000 | LIBOR + 1.40% | 2.37% | 3/1/2021 | ||||||||||

Term loan(4) | 12/19/2024 | 400,000 | 400,000 | LIBOR + 1.30% | 3.47% | 1/1/2023 | ||||||||||

Total Consolidated Debt(7) | 4,140,329 | 4,152,308 | ||||||||||||||

Unamortized loan premium, net | 4,089 | 4,191 | ||||||||||||||

Deferred loan costs, net | (37,923 | ) | (39,109 | ) | ||||||||||||

Total Consolidated Debt, net | $ | 4,106,495 | $ | 4,117,390 | ||||||||||||

___________________________________________________

Except as noted below, each loan (including our revolving credit facility) is non-recourse and secured by one or more separate collateral pools consisting of one or more properties, and requires monthly payments of interest only with the outstanding principal due upon maturity.

(1) | Maturity dates include the effect of extension options. |

(2) | Includes the effect of interest rate swaps and excludes the effect of prepaid loan fees. See Note 9 for details of our interest rate swaps. |

(3) | At June 30, 2018, this loan had been paid off. |

(4) | Loan agreement includes a zero-percent LIBOR floor. The corresponding swaps do not include such a floor. |

(5) | Requires monthly payments of principal and interest. Principal amortization is based upon a 30-year amortization schedule. |

(6) | $400.0 million revolving credit facility. Unused commitment fees range from 0.15% to 0.20%. |

(7) | See Note 12 for our fair value disclosures. |

17

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

Debt Statistics

The following table summarizes our fixed and floating rate debt:

(In thousands) | Principal Balance as of June 30, 2018 (In thousands) | Principal Balance as of December 31, 2017 (In thousands) | ||||||

Aggregate swapped to fixed rate loans | $ | 3,882,400 | $ | 3,547,400 | ||||

Aggregate fixed rate loans | 31,929 | 459,908 | ||||||

Aggregate floating rate loans | 226,000 | 145,000 | ||||||

Total Debt | $ | 4,140,329 | $ | 4,152,308 | ||||

The following table summarizes certain debt statistics at June 30, 2018:

Statistics for consolidated loans with interest fixed under the terms of the loan or a swap | |

Principal balance (in billions) | $3.91 |

Weighted average remaining life (including extension options) | 5.9 years |

Weighted average remaining fixed interest period | 3.2 years |

Weighted average annual interest rate | 3.07% |

Future Principal Payments

At June 30, 2018, the minimum future principal payments due on our secured notes payable and revolving credit facility were as follows:

Twelve months ending June 30: | Excluding Maturity Extension Options | Including Maturity Extension Options(1) | ||||||

(In thousands) | ||||||||

2019 | $ | 702 | $ | 702 | ||||

2020 | 145,735 | 145,735 | ||||||

2021 | 376,769 | 81,769 | ||||||

2022 | 640,805 | 340,805 | ||||||

2023 | 1,675,842 | 1,520,842 | ||||||

Thereafter | 1,300,476 | 2,050,476 | ||||||

Total future principal payments | $ | 4,140,329 | $ | 4,140,329 | ||||

____________________________________________

(1) | Our loan agreements generally require that we meet certain minimum financial thresholds to be able to extend the loan maturity. |

Loan Costs

Deferred loan costs are net of accumulated amortization of $20.2 million and $18.0 million at June 30, 2018 and December 31, 2017, respectively. The table below presents loan costs which are included in Interest expense in our consolidated statements of operations:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

(In thousands) | 2018 | 2017 | 2018 | 2017 | |||||||||||

Loan costs expensed | $ | — | $ | 376 | $ | 404 | $ | 376 | |||||||

Deferred loan cost amortization | 1,970 | 2,424 | 3,875 | 4,522 | |||||||||||

Total | $ | 1,970 | $ | 2,800 | $ | 4,279 | $ | 4,898 | |||||||

18

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

8. Interest Payable, Accounts Payable and Deferred Revenue

Interest payable, accounts payable and deferred revenue consisted of the following:

(In thousands) | June 30, 2018 | December 31, 2017 | |||||

Interest payable | $ | 10,592 | $ | 9,829 | |||

Accounts payable and accrued liabilities | 75,748 | 62,741 | |||||

Deferred revenue | 39,079 | 31,377 | |||||

Total interest payable, accounts payable and deferred revenue | $ | 125,419 | $ | 103,947 | |||

9. Derivative Contracts

We make use of interest rate swap and cap contracts to manage the risk associated with changes in interest rates on our floating-rate debt. When we enter into a floating-rate term loan, we generally enter into an interest rate swap agreement for the equivalent principal amount, for a period covering the majority of the loan term, which effectively converts our floating-rate debt to a fixed-rate basis during that time. In limited instances, we also make use of interest rate caps to limit our exposure to interest rate increases on our floating-rate debt. We do not speculate in derivatives and we do not make use of any other derivative instruments. See Note 7 regarding our debt, and our consolidated JVs debt, that is hedged. See Note 16 regarding our unconsolidated Funds debt that is hedged.

Derivative Summary

As of June 30, 2018, all of our interest rate swaps, which include the interest rate swaps of our consolidated JVs and our unconsolidated Funds, were designated as cash flow hedges:

Number of Interest Rate Swaps | Notional (In thousands) | ||||

Consolidated derivatives(1)(3) | 27 | $ | 3,882,400 | ||

Unconsolidated Funds' derivatives(2)(3) | 4 | $ | 510,000 | ||

___________________________________________________

(1) | The notional amount reflects 100%, not our pro-rata share, of our consolidated JVs' derivatives. |

(2) | The notional amount reflects 100%, not our pro-rata share, of our unconsolidated Funds' derivatives. |

(3) | See Note 12 for our derivative fair value disclosures. |

Credit-risk-related Contingent Features

We have agreements with each of our interest rate swap counterparties that contain a provision under which we could also be declared in default on our derivative obligations if we default on the underlying indebtedness that we are hedging. As of June 30, 2018, there have been no events of default with respect to our interest rate swaps or our consolidated JVs' or unconsolidated Funds' interest rate swaps. We do not post collateral for our interest rate swap contract liabilities. As of June 30, 2018, we, including our consolidated JVs' and our unconsolidated Funds, did not have any interest rate swaps with fair values that were in a liability position.

19

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

Counterparty Credit Risk

We are subject to credit risk from the counterparties on our interest rate swap contract assets because we do not receive collateral. We seek to minimize that risk by entering into agreements with a variety of high quality counterparties with investment grade ratings. The fair value of our interest rate swap contract assets, including accrued interest and excluding credit risk adjustments, were as follows:

(In thousands) | June 30, 2018 | December 31, 2017 | |||||

Consolidated derivatives(1) | $ | 117,876 | $ | 60,093 | |||

Unconsolidated Funds' derivatives(2) | $ | 19,582 | $ | 9,350 | |||

___________________________________________________

(1) | The amounts reflect 100%, not our pro-rata share, of our consolidated JVs' derivatives. |

(2) | The amounts reflect 100%, not our pro-rata share, of our unconsolidated Funds' derivatives. |

Impact of Hedges on AOCI and the Consolidated Statements of Operations

The table below presents the effect of our derivatives on our AOCI and the consolidated statements of operations:

(In thousands) | Six Months Ended June 30, | ||||||

2018 | 2017 | ||||||

Derivatives Designated as Cash Flow Hedges: | |||||||

Consolidated derivatives: | |||||||

Gain recorded in AOCI - adoption of ASU 2017-12(1)(2) | $ | 211 | $ | — | |||

Gain (loss) recorded in AOCI(1)(2) | $ | 58,890 | $ | (4,016 | ) | ||

(Gain) loss reclassified from AOCI to Interest Expense(1) | $ | (2,063 | ) | $ | 8,955 | ||

Total Interest Expense presented in the consolidated statements of operations | $ | (66,168 | ) | $ | (74,954 | ) | |

Gain related to ineffectiveness recorded in Interest Expense | $ | — | $ | 25 | |||

Unconsolidated Funds' derivatives (our share)(3): | |||||||

Gain recorded in AOCI(1) | $ | 6,404 | $ | 867 | |||

Gain reclassified from AOCI to Income, including depreciation, from unconsolidated real estate funds(1) | $ | (79 | ) | $ | (170 | ) | |

Total Income, including depreciation, from unconsolidated real estate funds presented in the consolidated statements of operations | $ | 3,174 | $ | 3,290 | |||

___________________________________________________

(1) | See Note 10 for our AOCI reconciliation. |

(2) | See Note 2 regarding the ASU adoption. |

(3) | We calculate our share by multiplying the total amount for each Fund by our equity interest in the respective Fund. |

Future Reclassifications from AOCI

At June 30, 2018, our estimate of the AOCI related to derivatives designated as cash flow hedges, that will be reclassified to earnings during the next twelve months as interest rate swap payments are made is as follows:

(In thousands) | |||

Consolidated derivatives: | |||

Gains to be reclassified from AOCI to Interest Expense | $ | 30,465 | |

Unconsolidated Funds' derivatives (our share): | |||

Gains to be reclassified from AOCI to Income, including depreciation, from unconsolidated real estate funds | $ | 2,053 | |

20

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

10. Equity

Transactions

During the six months ended June 30, 2018, we (i) acquired 339 thousand OP Units in exchange for issuing an equal number of shares of our common stock to the holders of the OP Units, (ii) acquired 3 thousand OP Units for $108 thousand in cash and (iii) issued 14 thousand shares of our common stock for the exercise of 32 thousand stock options on a net settlement basis (net of the exercise price and related taxes).

During the six months ended June 30, 2017, we (i) acquired 659 thousand OP Units in exchange for issuing an equal number of shares of our common stock to the holders of the OP Units, (ii) issued 1.3 million shares of our common stock for the exercise of 3.9 million stock options on a net settlement basis (net of the exercise price and related taxes) and (iii) issued 9.1 million shares of our common stock under our ATM program for net proceeds of $346.0 million.

Condensed Consolidated Statements of Equity

The tables below present our condensed consolidated statements of equity:

(In thousands) | DEI Stockholders' Equity | Noncontrolling Interests | Total Equity | ||||||||

Balance as of January 1, 2018 | $ | 2,437,524 | $ | 1,464,525 | $ | 3,902,049 | |||||

Adjustment to opening balance of accumulated deficit(1) | (211 | ) | — | (211 | ) | ||||||

Net income | 59,890 | 9,774 | 69,664 | ||||||||

Cash flow hedge fair value adjustments | 44,387 | 18,976 | 63,363 | ||||||||

Dividends and distributions | (84,955 | ) | (26,114 | ) | (111,069 | ) | |||||

Exchange of OP units for common stock | 5,481 | (5,481 | ) | — | |||||||

OP Units redeemed with cash | (59 | ) | (49 | ) | (108 | ) | |||||

Exercise of stock options(2) | (314 | ) | — | (314 | ) | ||||||

Stock-based compensation | — | 6,912 | 6,912 | ||||||||

Balance as of June 30, 2018 | $ | 2,461,743 | $ | 1,468,543 | $ | 3,930,286 | |||||

__________________________________________________

(1) Reflects the adoption of ASU No. 2017-12. See Note 2 for details.

(2) Reflects withholding taxes. We issued shares of our common stock for the exercise of stock options on a net settlement basis (net of the exercise price and related taxes).

(In thousands) | DEI Stockholders' Equity | Noncontrolling Interests | Total Equity | ||||||||

Balance as of January 1, 2017 | $ | 1,921,143 | $ | 1,092,928 | $ | 3,014,071 | |||||

Net income | 39,293 | 4,640 | 43,933 | ||||||||

Cash flow hedge fair value adjustments | 5,715 | (79 | ) | 5,636 | |||||||

Contributions to consolidated JV | — | 188,248 | 188,248 | ||||||||

Dividends and distributions | (72,194 | ) | (19,202 | ) | (91,396 | ) | |||||

Exchange of OP units for common stock | 8,856 | (8,856 | ) | — | |||||||

Exercise of stock options(1) | (52,704 | ) | — | (52,704 | ) | ||||||

Stock-based compensation | — | 5,786 | 5,786 | ||||||||

Sale of common stock, net of offering costs | 276,961 | — | 276,961 | ||||||||

Balance as of June 30, 2017 | $ | 2,127,070 | $ | 1,263,465 | $ | 3,390,535 | |||||

__________________________________________________

(1) Reflects withholding taxes. We issued shares of our common stock for the exercise of stock options on a net settlement basis (net of the exercise price and related taxes).

21

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

Noncontrolling Interests

Our noncontrolling interests consist of interests in our Operating Partnership and consolidated JVs which are not owned by us. Noncontrolling interests in our Operating Partnership consist of OP Units and fully-vested LTIP Units, and represented approximately 14% of our Operating Partnership's total interests as of June 30, 2018 when we and our Operating Partnership had 169.9 million shares of common stock and 27.4 million OP Units and fully-vested LTIP Units outstanding. A share of our common stock, an OP Unit and an LTIP Unit (once vested and booked up) have essentially the same economic characteristics, sharing equally in the distributions from our Operating Partnership. Investors who own OP Units have the right to cause our Operating Partnership to acquire their OP Units for an amount of cash per unit equal to the market value of one share of our common stock at the date of acquisition, or, at our election, exchange their OP Units for shares of our common stock on a one-for-one basis. LTIP Units have been granted to our key employees and non-employee directors as part of their compensation. These awards generally vest over a service period and once vested can generally be converted to OP Units provided our stock price increases by more than a specified hurdle.

Changes in our Ownership Interest in our Operating Partnership

The table below presents the effect on our equity from net income attributable to common stockholders and changes in our ownership interest in our Operating Partnership:

Six Months Ended June 30, | |||||||

(In thousands) | 2018 | 2017 | |||||

Net income attributable to common stockholders | $ | 59,890 | $ | 39,293 | |||

Transfers from noncontrolling interests: | |||||||

Exchange of OP Units with noncontrolling interests | 5,481 | 8,856 | |||||

Repurchase of OP Units from noncontrolling interests | (59 | ) | — | ||||

Net transfers from noncontrolling interests | 5,422 | 8,856 | |||||

Change from net income attributable to common stockholders and transfers from noncontrolling interests | $ | 65,312 | $ | 48,149 | |||

22

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

AOCI Reconciliation(1)

The table below presents a reconciliation of our AOCI, which consists solely of adjustments related to derivatives designated as cash flow hedges:

Six Months Ended June 30, | |||||||

(In thousands) | 2018 | 2017 | |||||

Beginning balance | $ | 43,099 | $ | 15,156 | |||

Adoption of ASU 2017-12 - cumulative opening balance adjustment(2) | 211 | — | |||||

Consolidated derivatives: | |||||||

Other comprehensive income (loss) before reclassifications | 58,890 | (4,016 | ) | ||||

Reclassification of (gains) losses from AOCI to Interest Expense | (2,063 | ) | 8,955 | ||||

Unconsolidated Funds' derivatives (our share): | |||||||

Other comprehensive income before reclassifications | 6,404 | 867 | |||||

Reclassification of gains from AOCI to Income, including depreciation, from unconsolidated real estate funds | (79 | ) | (170 | ) | |||

Net current period OCI | 63,363 | 5,636 | |||||

OCI attributable to noncontrolling interests | (18,976 | ) | 79 | ||||

OCI attributable to common stockholders | 44,387 | 5,715 | |||||

Ending balance | $ | 87,486 | $ | 20,871 | |||

___________________________________________________

(1) | See Note 9 for the details of our derivatives and Note 12 for our derivative fair value disclosures. |

(2) | See Note 2 regarding our adoption of the ASU on January 1, 2018. |

Equity Compensation

On June 2, 2016, the Douglas Emmett 2016 Omnibus Stock Incentive Plan ("2016 Plan") became effective after receiving stockholder approval, superseding our prior plan, the Douglas Emmett 2006 Omnibus Stock Incentive Plan ("2006 Plan"), both of which allow for awards to our directors, officers, employees and consultants. The key terms of the two plans are substantially identical, except for the date of expiration, the number of shares authorized for grants and various technical provisions. Grants after June 2, 2016 were awarded under the 2016 Plan, while grants prior to that date were awarded under the 2006 Plan (grants under the 2006 Plan remain outstanding according to their terms). Both plans are administered by the compensation committee of our board of directors.

Total net stock-based compensation expense was $2.9 million and $2.6 million for the three months ended June 30, 2018 and 2017, and $6.0 million and $5.3 million for the six months ended June 30, 2018 and 2017 respectively. These amounts are net of capitalized stock-based compensation of $496 thousand and $247 thousand for the three months ended June 30, 2018 and 2017, and $948 thousand and $475 thousand for the six months ended June 30, 2018 and 2017 respectively. No options were exercised for the three months ended June 30, 2018 and 2017. The intrinsic value of options exercised was $803 thousand and $102.1 million for the six months ended June 30, 2018 and 2017 respectively.

23

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

11. EPS

We calculate basic EPS by dividing the net income attributable to common stockholders for the period by the weighted average number of common shares outstanding during the period. We calculate diluted EPS by dividing the net income attributable to common stockholders for the period by the weighted average number of common shares and dilutive instruments outstanding during the period using the treasury stock method. We account for unvested LTIP awards that contain nonforfeitable rights to dividends as participating securities and include these securities in the computation of basic and diluted EPS using the two-class method. The table below presents the calculation of basic and diluted EPS:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Numerator (In thousands): | |||||||||||||||

Net income attributable to common stockholders | $ | 31,684 | $ | 20,244 | $ | 59,890 | $ | 39,293 | |||||||

Allocation to participating securities: Unvested LTIP Units | (156 | ) | (97 | ) | (294 | ) | (196 | ) | |||||||

Numerator for basic and diluted net income attributable to common stock holders | $ | 31,528 | $ | 20,147 | $ | 59,596 | $ | 39,097 | |||||||

Denominator (In thousands): | |||||||||||||||

Weighted average shares of common stock outstanding - basic | 169,916 | 155,898 | 169,759 | 154,203 | |||||||||||

Effect of dilutive securities: Stock options(1) | 10 | 54 | 17 | 607 | |||||||||||

Weighted average shares of common stock and common stock equivalents outstanding - diluted | 169,926 | 155,952 | 169,776 | 154,810 | |||||||||||

Basic EPS: | |||||||||||||||

Net income attributable to common stockholders per share | $ | 0.19 | $ | 0.13 | $ | 0.35 | $ | 0.25 | |||||||

Diluted EPS: | |||||||||||||||

Net income attributable to common stockholders per share | $ | 0.19 | $ | 0.13 | $ | 0.35 | $ | 0.25 | |||||||

____________________________________________________

(1) | The following securities were excluded from the calculation of diluted EPS because including them would be anti-dilutive to the calculation: |

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||

(In thousands) | 2018 | 2017 | 2018 | 2017 | |||||||

OP Units | 26,637 | 24,797 | 26,790 | 24,730 | |||||||

Vested LTIP Units | 807 | 313 | 803 | 536 | |||||||

24

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

12. Fair Value of Financial Instruments

Our estimates of the fair value of financial instruments were determined using available market information and widely used valuation methods. Considerable judgment is necessary to interpret market data and determine an estimated fair value. The use of different market assumptions or valuation methods may have a material effect on the estimated fair values. The FASB fair value framework hierarchy distinguishes between assumptions based on market data obtained from sources independent of the reporting entity, and the reporting entity’s own assumptions about market-based inputs. The hierarchy is as follows:

Level 1 - inputs utilize unadjusted quoted prices in active markets for identical assets or liabilities.

Level 2 - inputs are observable either directly or indirectly for similar assets and liabilities in active markets.

Level 3 - inputs are unobservable assumptions generated by the reporting entity

As of June 30, 2018, we did not have any fair value estimates of financial instruments using Level 3 inputs.

Financial instruments disclosed at fair value

Short term financial instruments: The carrying amounts for cash and cash equivalents, tenant receivables, revolving credit line, interest payable, accounts payable, security deposits and dividends payable approximate fair value because of the short-term nature of these instruments.

Secured notes payable: See Note 7 for the details of our secured notes payable. We estimate the fair value of our consolidated secured notes payable (excluding our revolving credit facility) by calculating the credit-adjusted present value of the principal and interest payments for each secured note payable. The calculation incorporates observable market interest rates which we consider to be Level 2 inputs, assumes that the loans will be outstanding through maturity, and excludes any maturity extension options. The table below presents the estimated fair value of our secured notes payable:

(In thousands) | June 30, 2018 | December 31, 2017 | |||||

Fair value | $ | 4,090,917 | $ | 4,195,489 | |||

Carrying value | $ | 4,063,418 | $ | 4,156,499 | |||

Financial instruments measured at fair value

Derivative instruments: See Note 9 for the details of our derivatives. We present our derivatives on the balance sheet at fair value, on a gross basis, excluding accrued interest. We estimate the fair value of our derivative instruments by calculating the credit-adjusted present value of the expected future cash flows of each derivative. The calculation incorporates the contractual terms of the derivatives, observable market interest rates which we consider to be Level 2 inputs, and credit risk adjustments to reflect the counterparty's as well as our own nonperformance risk. Our derivatives are not subject to master netting arrangements. The table below presents the estimated fair value of our derivatives:

(In thousands) | June 30, 2018 | December 31, 2017 | |||||

Derivative Assets: | |||||||

Fair value - consolidated derivatives(1) | $ | 116,090 | $ | 60,069 | |||

Fair value - unconsolidated Funds' derivatives(2) | $ | 19,308 | $ | 9,437 | |||

Derivative Liabilities: | |||||||

Fair value - consolidated derivatives(1) | $ | — | $ | 807 | |||

Fair value - unconsolidated Funds' derivatives(2) | $ | — | $ | — | |||

____________________________________________________

(1) | Consolidated derivatives, which include 100%, not our pro-rata share, of our consolidated JVs' derivatives, are included in interest rate contracts in our consolidated balance sheets. The fair values exclude accrued interest which is included in interest payable in the consolidated balance sheets. |

(2) | Reflects 100%, not our pro-rata share, of our unconsolidated Funds' derivatives. Our pro-rata share of the amounts related to the unconsolidated Funds' derivatives is included in our Investment in unconsolidated real estate funds in our consolidated balance sheets. See Note 16 regarding our unconsolidated Funds debt and derivatives. |

25

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

13. Segment Reporting

Segment information is prepared on the same basis that our management reviews information for operational decision-making purposes. We operate in two business segments: (i) the acquisition, development, ownership and management of office real estate and (ii) the acquisition, development, ownership and management of multifamily real estate. The services for our office segment primarily include rental of office space and other tenant services, including parking and storage space rental. The services for our multifamily segment include rental of apartments and other tenant services, including parking and storage space rental. Asset information by segment is not reported because we do not use this measure to assess performance or make decisions to allocate resources. Therefore, depreciation and amortization expense is not allocated among segments. General and administrative expenses and interest expense are not included in segment profit as our internal reporting addresses these items on a corporate level. The table below presents the operating activity of our reportable segments:

(In thousands) | Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Office Segment | |||||||||||||||

Total office revenues | $ | 193,761 | $ | 175,542 | $ | 381,094 | $ | 345,890 | |||||||

Office expenses | (61,818 | ) | (57,887 | ) | (122,174 | ) | (112,772 | ) | |||||||

Office segment profit | 131,943 | 117,655 | 258,920 | 233,118 | |||||||||||

Multifamily Segment | |||||||||||||||

Total multifamily revenues | 25,708 | 24,090 | 50,622 | 48,223 | |||||||||||

Multifamily expenses | (6,908 | ) | (5,878 | ) | (13,606 | ) | (11,825 | ) | |||||||

Multifamily segment profit | 18,800 | 18,212 | 37,016 | 36,398 | |||||||||||

Total profit from all segments | $ | 150,743 | $ | 135,867 | $ | 295,936 | $ | 269,516 | |||||||

The table below presents a reconciliation of the total profit from all segments to net income attributable to common stockholders:

(In thousands) | Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Total profit from all segments | $ | 150,743 | $ | 135,867 | $ | 295,936 | $ | 269,516 | |||||||

General and administrative | (9,437 | ) | (8,592 | ) | (19,004 | ) | (18,748 | ) | |||||||

Depreciation and amortization | (73,379 | ) | (68,793 | ) | (145,877 | ) | (136,167 | ) | |||||||

Other income | 2,792 | 2,331 | 5,422 | 4,493 | |||||||||||

Other expenses | (2,086 | ) | (1,773 | ) | (3,819 | ) | (3,497 | ) | |||||||

Income, including depreciation, from unconsolidated real estate funds | 1,668 | 1,113 | 3,174 | 3,290 | |||||||||||

Interest expense | (33,268 | ) | (38,000 | ) | (66,168 | ) | (74,954 | ) | |||||||

Net income | 37,033 | 22,153 | 69,664 | 43,933 | |||||||||||

Less: Net income attributable to noncontrolling interests | (5,349 | ) | (1,909 | ) | (9,774 | ) | (4,640 | ) | |||||||

Net income attributable to common stockholders | $ | 31,684 | $ | 20,244 | $ | 59,890 | $ | 39,293 | |||||||

26

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

14. Future Minimum Lease Rental Receipts

We lease space to tenants primarily under non-cancelable operating leases that generally contain provisions for a base rent plus reimbursement of certain operating expenses, and we own fee interests in two parcels of land from which we receive rent under ground leases. The table below presents the future minimum base rentals on our non-cancelable office tenant and ground leases at June 30, 2018:

Twelve months ending June 30: | (In thousands) | ||

2019 | $ | 563,563 | |

2020 | 527,436 | ||

2021 | 456,384 | ||

2022 | 364,772 | ||

2023 | 291,970 | ||

Thereafter | 670,467 | ||

Total future minimum base rentals(1) | $ | 2,874,592 | |

_____________________________________________________

(1) | Does not include (i) residential leases, which typically have a term of one year or less, (ii) holdover rent, (iii) other types of rent such as storage and antenna rent, (iv) tenant reimbursements, (v) straight- line rent, (vi) amortization/accretion of acquired above/below-market lease intangibles and (vii) percentage rents. The amounts assume that early termination options held by tenants are not exercised. |

15. Future Minimum Lease Rental Payments

We pay rent under a ground lease which expires on December 31, 2086. The rent is fixed at $733 thousand per year until February 28, 2019, and will then reset to the greater of the existing ground rent or market. We incurred ground rent expense of $183 thousand for the three months ended June 30, 2018 and 2017 and $366 thousand for the six months ended June 30, 2018 and 2017 respectively. The table below, which assumes that the ground rent payments will continue to be $733 thousand per year after February 28, 2019, presents the future minimum ground lease payments as of June 30, 2018:

Twelve months ending June 30: | (In thousands) | ||

2019 | $ | 733 | |

2020 | 733 | ||

2021 | 733 | ||

2022 | 733 | ||

2023 | 733 | ||

Thereafter | 46,544 | ||

Total future minimum lease payments | $ | 50,209 | |

27

Douglas Emmett, Inc.

Notes to Consolidated Financial Statements (unaudited) (continued)

16. Commitments, Contingencies and Guarantees

Legal Proceedings

From time to time, we are party to various lawsuits, claims and other legal proceedings that arise in the ordinary course of our business. Excluding ordinary, routine litigation incidental to our business, we are not currently a party to any legal proceedings that we believe would reasonably be expected to have a materially adverse effect on our business, financial condition or results of operations.

Concentration of Risk

We are subject to credit risk with respect to our tenant receivables and deferred rent receivables related to our tenant leases. Our tenants' ability to honor the terms of their respective leases remains dependent upon economic, regulatory and social factors. We seek to minimize our credit risk from our tenant leases by (i) targeting smaller, more affluent tenants, from a diverse mix of industries, (ii) performing credit evaluations of prospective tenants and (iii) obtaining security deposits or letters of credit from our tenants. For the six months ended June 30, 2018 and 2017, no tenant accounted for more than 10% of our total revenues.

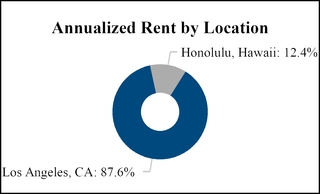

All of our properties, including the properties of our consolidated JVs and unconsolidated Funds, are located in Los Angeles County, California and Honolulu, Hawaii, and we are therefore susceptible to adverse economic and regulatory developments, as well as natural disasters, in those markets.

We are subject to credit risk with respect to our interest rate swap counterparties that we use to manage the risk associated with our floating rate debt. We do not post or receive collateral with respect to our swap transactions. See Note 9 for the details of our interest rate contracts. We seek to minimize our credit risk by entering into agreements with a variety of high quality counterparties with investment grade ratings.

We have significant cash balances invested in a variety of short-term money market funds that are intended to preserve principal value and maintain a high degree of liquidity while providing current income. These investments are not insured against loss of principal and there is no guarantee that our investments in these funds will be redeemable at par value. We also have significant cash balances in bank accounts with high quality financial institutions with investment grade ratings. Interest bearing bank accounts at each U.S. banking institution are insured by the FDIC up to $250 thousand.

Asset Retirement Obligations