Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - CURTISS WRIGHT CORP | a51842901ex99_1.htm |

| 8-K - CURTISS-WRIGHT CORPORATION 8-K - CURTISS WRIGHT CORP | a51842901.htm |

1 | July 26, 2018 | © 2018 Curtiss-Wright 2Q 2018 Earnings Conference Call July 26, 2018 NYSE: CW

2 | July 26, 2018 | © 2018 Curtiss-Wright Safe Harbor Statement Please note that the information provided in this presentation is accurate as of the date of the original presentation. The presentation will remain posted on this website from one to twelve months following the initial presentation, but content will not be updated to reflect new information that may become available after the original presentation posting. The presentation contains forward-looking statements including, among other things, management's estimates of future performance, revenue and earnings, our management's growth objectives, our management’s ability to integrate our acquisition, and our management's ability to produce consistent operating improvements. These forward-looking statements are based on expectations as of the time the statements were made only, and are subject to a number of risks and uncertainties which could cause us to fail to achieve our then-current financial projections and other expectations. This presentation also includes certain non-GAAP financial measures with reconciliations to GAAP financial measures being made available in the earnings release that is posted to our website and furnished with the SEC. We undertake no duty to update this information. More information about potential factors that could affect our business and financial results is included in our filings with the Securities and Exchange Commission, including our Annual Reports on Form 10-K and Quarterly Reports on Form 10-Q, including, among other sections, under the captions, "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations," which is on file with the SEC and available at the SEC's website at www.sec.gov.

3 | July 26, 2018 | © 2018 Curtiss-Wright 2018 Second Quarter Performance and Full-Year Business Outlook Net Sales up 9% overall (4% organic) – Driven by strong demand in defense and industrial markets Adjusted Operating Income up 28%; Adjusted Operating Margin of 17.6%, up 260 basis points – Driven by favorable overhead absorption on higher sales and benefits of ongoing margin improvement initiatives – Excludes first year purchase accounting costs associated with the acquisition of Dresser-Rand’s government business (“DRG”) Adjusted Diluted EPS of $1.80, up 49% – Reflects higher sales and strong growth in profitability in C/I and Defense segments Free Cash Flow of $87 million, up 19% New Orders of $700 million, up 28%, led by strong demand in naval defense Second Quarter 2018 Highlights (1) (2) FY 2018 Guidance Highlights (1) (2) Introduced Adjusted Full-Year 2018 Diluted EPS range of $6.00 to $6.15 – Increased Reported GAAP Sales, Operating Income, Operating Margin and EPS (+$0.28) – Reflects $0.25 adjustment for first year acquisition-related purchase accounting costs – Expect higher sales in all end markets – Double-digit growth in operating income and continued margin expansion Increased Adjusted Free Cash Flow guidance by $10 million to new range of $300 - $320 million Notes: 1) Any references to organic growth exclude the effects of foreign currency translation, acquisitions and divestitures, unless otherwise noted. 2) Adjusted operating income, operating margin and diluted EPS exclude first year purchase accounting costs, specifically one-time inventory step-up, backlog amortization and transaction costs, for current and prior year acquisitions.

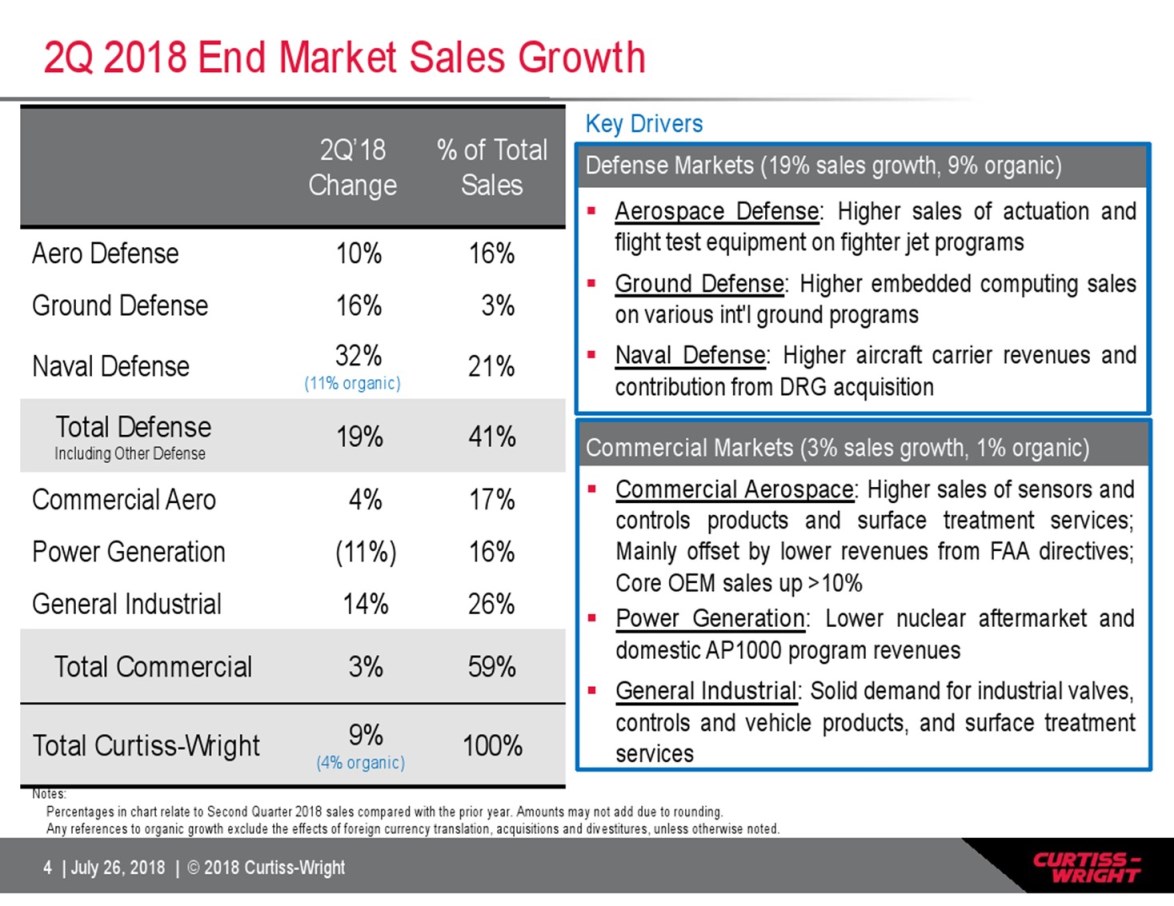

4 | July 26, 2018 | © 2018 Curtiss-Wright Key Drivers Defense Markets (19% sales growth, 9% organic) Aerospace Defense: Higher sales of actuation and flight test equipment on fighter jet programs Ground Defense: Higher embedded computing sales on various int'l ground programs Naval Defense: Higher aircraft carrier revenues and contribution from DRG acquisition 2Q 2018 End Market Sales Growth Notes: Percentages in chart relate to Second Quarter 2018 sales compared with the prior year. Amounts may not add due to rounding. Any references to organic growth exclude the effects of foreign currency translation, acquisitions and divestitures, unless otherwise noted. 2Q’18 Change % of Total Sales Aero Defense 10% 16% Ground Defense 16% 3% Naval Defense 32% (11% organic) 21% Total Defense Including Other Defense 19% 41% Commercial Aero 4% 17% Power Generation (11%) 16% General Industrial 14% 26% Total Commercial 3% 59% Total Curtiss-Wright 9% (4% organic) 100% Commercial Markets (3% sales growth, 1% organic) Commercial Aerospace: Higher sales of sensors and controls products and surface treatment services; Mainly offset by lower revenues from FAA directives; Core OEM sales up >10% Power Generation: Lower nuclear aftermarket and domestic AP1000 program revenues General Industrial: Solid demand for industrial valves, controls and vehicle products, and surface treatment services

5 | July 26, 2018 | © 2018 Curtiss-Wright 2Q 2018 Operating Income / Margin Drivers ($ in millions) 2Q’18 Adjusted(1) 2Q’17 Adjusted(1) Change vs. 2017 Adjusted(1) Key Drivers Commercial / Industrial Margin $51.7 16.6% $43.6 15.0% 19% 160 bps Higher sales and favorable absorption Benefit of Op margin improvement initiatives, including savings from prior restructuring actions Defense Margin 38.6 26.4% 26.3 20.8% 47% 560 bps Higher sales (partly timing) and favorable absorption Favorable contract adjustments (naval business) Benefit of Op margin improvement initiatives Power Margin 26.2 16.2% 23.9 15.9% 10% 30 bps Higher sales and favorable absorption (naval business) AP1000 CD: Improved YOY profitability despite flat sales Lower sales and unfavorable absorption in domestic nuclear aftermarket Reduced domestic AP1000 production revenues Total Segments Adjusted Operating Income $116.6 $93.8 24% Corp & Other ($7.5) ($8.9) 16% Total CW Adjusted Op Income Margin $109.1 17.6% $85.0 15.0% 28% 260 bps 1) Adjusted operating income and operating margin exclude first year purchase accounting costs, specifically one-time inventory step-up, backlog amortization and transaction costs associated with the acquisitions of DRG in 2018 (Power segment) and TTC in 2017 (Defense segment). Note: Amounts may not add down due to rounding.

6 | July 26, 2018 | © 2018 Curtiss-Wright 2018E End Market Sales Growth (Guidance as of July 25, 2018) FY2018E (Prior) FY2018E (Current) % of Total Sales Aero Defense 8 - 10% 11 - 13% 16% Ground Defense 0 - 2% No change 4% Naval Defense 16 - 18% 20 - 22% 20% Total Defense Including Other Defense 9 - 11% 13 - 15% (6 - 8% organic) 41% Commercial Aero 0 - 2% No change 17% Power Generation 6 - 8% 2 - 4% 17% General Industrial 4 - 6% 8 - 10% 25% Total Commercial 3 - 5% No change 59% Total Curtiss-Wright 6 - 8% 8 - 9% (5 - 6% organic) 100% Note: Amounts may not add down due to rounding. Updated (in blue)

7 | July 26, 2018 | © 2018 Curtiss-Wright ($ in millions) 2017 Adjusted (Non-GAAP) (1) 2018 Prior Reported (GAAP) Operational Changes 2018 Updated Reported (GAAP) Adjustments(1) 2018 Current Adjusted (Non-GAAP) (1) 2018 Change vs 2017 Adjusted(1) Commercial / Ind $1,163 $1,193 - 1,213 $20 $1,213 - 1,233 $1,213 - 1,233 4 - 6% Defense $555 $565 - 575 $10 $575 - 585 $575 - 585 4 - 5% Power $553 $657 - 667 $657 - 667 $657 - 667 19 - 21% Total Sales $2,271 $2,415 - 2,455 $30 $2,445 - 2,485 $2,445 - 2,485 8 - 9% Commercial / Ind Margin $168 14.5% $177 – 182 14.8% - 15.0% $6 $183 – 188 15.1% - 15.2% $183 – 188 15.1% - 15.2% 9 - 12% +60 - 70 bps Defense Margin $119 21.4% $121 – 124 21.3% - 21.5% $3 $124 – 127 21.5% - 21.7% $124 – 127 21.5% - 21.7% 4 - 6% +10 - 30 bps Power Margin $81 14.7% $80 – 83 12.2% - 12.4% $4 $85 – 87 12.9% - 13.1% $14 $99 – 102 15.1% - 15.3% 22 - 26% +40 - 60 bps Corporate and Other ($34) ($34 - 35) ($34 - 35) ($34 - 35) - Total Op. Income CW Margin $335 14.7% $343 – 353 14.2% - 14.4% $13 +40 bps $357 – 367 14.6% - 14.8% $14 +60 bps $371 – 382 15.2% - 15.4% 11 - 14% +50 - 70 bps 2018E Financial Outlook (Guidance as of July 25, 2018) Note: Amounts may not add down due to rounding. 1) Adjusted operating income and operating margin exclude first year purchase accounting costs, specifically one-time inventory step-up, backlog amortization and transaction costs associated with the acquisitions of DRG in 2018 (Power segment) and TTC in 2017 (Defense segment). Updated (in blue)

8 | July 26, 2018 | © 2018 Curtiss-Wright 2018E Financial Outlook (Guidance as of July 25, 2018) Note: Amounts may not add down due to rounding. 1) Adjusted operating income and diluted EPS exclude first year purchase accounting costs, specifically one-time inventory step-up, backlog amortization and transaction costs, for current and prior year acquisitions. 2) Full-year 2018 effective tax rate guidance includes the impacts of the Tax Cuts and Jobs Act. Updated (in blue) ($ in millions, except EPS) 2017 Adjusted (Non-GAAP) (1) 2018 Prior Reported (GAAP) Operational Changes 2018 Updated Reported (GAAP) Adjustments(1) 2018 Current Adjusted (Non-GAAP) (1) 2018 Change vs 2017 Adjusted (1) Total Operating Income $335 $343 - 353 $13 $357 - 367 $14 $371 - 382 11 - 14% Other Income/(Expense) $16 $14 $1 $15 $15 Interest Expense ($41) ($36 - 37) $1 ($35 - 36) ($35 - 36) Provision for Income Taxes(2) ($88) ($77 - 79) ($4) ($81 - 83) ($3) ($84 - 87) Effective Tax Rate(2) 28.3% 24.0% 24.0% 24.0% Diluted EPS(2) $4.96 $5.47 - 5.62 $0.28 $5.75 - 5.90 $0.25 $6.00 - 6.15 21 - 24% Diluted Shares Outstanding 44.8 44.7 (0.1) 44.6 44.6

9 | July 26, 2018 | © 2018 Curtiss-Wright 2018E Financial Outlook (Guidance as of July 25, 2018) Updated (in blue) ($ in millions) 2018 Prior Reported (GAAP) Operational Changes 2018 Updated Reported (GAAP) Adjustments(2) 2018 Current Adjusted (Non-GAAP) (2) Free Cash Flow(1) $240 - 260 $10 $250 - 270 $50 $300 – 320 Free Cash Flow Conversion(1) 98 - 103% 93 - 98% 112 - 117% Capital Expenditures $50 - 60 $50 - 60 $50 – 60 Depreciation & Amortization $105 - 115 $105 - 115 $105 – 115 Notes: 1) Free Cash Flow is defined as cash flow from operations less capital expenditures. Free Cash Flow Conversion is calculated as free cash flow divided by net earnings from continuing operations. 2) Adjusted Free Cash Flow excludes a voluntary contribution to the Company’s corporate defined benefit pension plan of $50 million in 2018. Adjusted free Cash Flow Conversion is calculated as adjusted free cash flow divided by net earnings from continuing operations. Targets: Minimum free cash flow of $250 Million (unchanged) Average free cash flow conversion of at least 110% (previously >125%) – Change due to expectations for higher than expected net income due to reduced corporate tax rate

10 | July 26, 2018 | © 2018 Curtiss-Wright Positioned to Deliver Strong 2018 Results Synchronized sales growth, up 8 - 9% – Up 5 - 6% organic, increases in all end markets Continued operating margin expansion – Driven by improving sales outlook and benefit of ongoing margin improvement initiatives – Adjusted operating margin of 15.2% - 15.4%, up 50 - 70 bps Strong growth in adjusted diluted EPS, up 21 - 24% Adjusted free cash flow remains solid, driven by efficient working capital management Committed to a balanced capital allocation strategy Notes: 1) Any references to organic growth exclude the effects of foreign currency translation, acquisitions and divestitures, unless otherwise noted. 2) Adjusted operating income, operating margin and diluted EPS exclude first year purchase accounting costs, specifically one-time inventory step-up, backlog amortization and transaction costs, for current and prior year acquisitions. 3) Adjusted Free Cash Flow is defined as cash flow from operations less capital expenditures, and excludes a voluntary contribution to the Company’s corporate defined benefit pension plan of $50 million in 2018. Any

11 | July 26, 2018 | © 2018 Curtiss-Wright Appendix Non-GAAP Financial Results The company reports its financial performance in accordance with accounting principles generally accepted in the United States of America ("GAAP"). This press release refers to "Adjusted" amounts, which are Non-GAAP financial measures described below. We utilize a number of different financial measures in analyzing and assessing the overall performance of our business, and in making operating decisions, forecasting and planning for future periods. We consider the use of the non-GAAP measures to be helpful in assessing the performance of the ongoing operation of our business. We believe that disclosing non-GAAP financial measures provides useful supplemental data that, while not a substitute for financial measures prepared in accordance with GAAP, allows for greater transparency in the review of our financial and operational performance. Beginning with the second quarter of 2018, coinciding with the initial reporting of the DRG acquisition, the Company has elected to also present its financials and guidance on an Adjusted, non-GAAP basis for operating income, operating margin, net earnings and diluted earnings per share to exclude first year purchase accounting costs associated with its acquisitions, specifically one-time inventory step-up, backlog amortization and transaction costs for current and prior year acquisitions. Management believes that this approach will provide improved transparency to the investment community in order to measure Curtiss-Wright’s core operating and financial performance, provide quarter-over-quarter comparisons excluding one-time items and show better comparisons among company peers. Reconciliations of non-GAAP to GAAP amounts are furnished with this presentation. All per share amounts are reported on a diluted basis. The following definitions are provided: Adjusted Operating Income, Operating Margin, Net Income and Diluted EPS These Adjusted financials are defined as Reported Operating Income, Operating Margin, Net Income and Diluted EPS under GAAP excluding the impact of first year purchase accounting costs associated with acquisitions for current and prior year periods, specifically one-time inventory step-up, backlog amortization and transaction costs.

12 | July 26, 2018 | © 2018 Curtiss-Wright ($ Millions) Naval Aerospace Industrial Vehicles Ground Industrial Controls Other Industrial Valves Surface Tech Services Total CW End Markets $2,445 - 2,485 UP 8 - 9% Non-Nuclear 41% 59% Defense Markets Commercial Aerospace Aircraft Equipment Surface Tech Services Power Generation Commercial Markets Aftermarket Nuclear New Build / AP1000 General Industrial 20% 16% 4% 1% 17% 70% 30% 20% 17% 61% 28% 11% 25% 33% 27% 20% 2018E End Market Sales Waterfall (Guidance as of July 25, 2018) Guidance: Defense Markets up 13-15% (up 6-8% organic) Comm’l Markets up 3-5% Industrial Controls: Medical Mobility, Industrial Automation equipment, Sensors and Controls Industrial Vehicles: “Own the Cab” strategy 49% On-highway, 51% Off-Highway Industrial Valves: 65% O&G, 35% Chem/Petro; 75% MRO, 25% projects Non-Nuclear: Surface Technologies services (peening, coatings); Fossil power gen equipment Note: Percentages in chart relate to Full-Year 2018 sales

13 | July 26, 2018 | © 2018 Curtiss-Wright Non-GAAP Reconciliation – Organic Results Organic Revenue and Organic Operating Income The Corporation discloses organic revenue and organic operating income because the Corporation believes it provides investors with insight as to the Company’s ongoing business performance. Organic revenue and organic operating income are defined as revenue and operating income excluding the impact of foreign currency fluctuations and contributions from acquisitions made during the last twelve months. Note: Amounts may not add due to rounding Sales Operating income Sales Operating income Sales Operating income Sales Operating income Organic 5% 16% 15% 86% (7%) (3%) 4% 32% Acquisitions 0% 0% 0% 0% 15% (17%) 4% (5%) Foreign Currency 2% 3% 1% (3%) 0% 0% 1% 1% Total 7% 19% 16% 83% 8% (20%) 9% 28% Sales Operating income Sales Operating income Sales Operating income Sales Operating income Organic 5% 21% 9% 86% (3%) (2%) 4% 34% Acquisitions 0% 0% 0% 0% 8% (10%) 2% (3%) Foreign Currency 2% 2% 1% (5%) 0% 0% 1% (0%) Total 7% 23% 10% 81% 5% (12%) 7% 30% Three Months Ended 2018 vs 2017 Commercial/Industrial Defense Power Total Curtiss-Wright June 30 Six Months Ended 2018 vs 2017 Commercial/Industrial Defense Power Total Curtiss-Wright June

14 | July 26, 2018 | © 2018 Curtiss-Wright Non-GAAP Reconciliations – 2Q 2018 Results (In millions, except EPS) 2Q-2018 2Q-2017 Change Sales $ 620.3 $ 567.7 9% Reported operating income (GAAP) $ 102.1 $ 79.7 28% Adjustments (1) 7.0 5.2 - Adjusted operating income (Non-GAAP) $ 109.1 $ 85.0 28% Adjusted operating margin (Non-GAAP) 17.6% 15.0% 260 bps Reported net earnings (GAAP) $ 74.8 $ 50.7 48% Adjustments (1) 7.0 5.2 - Tax impact on Adjustments (1) (1.6) (1.6) - Adjusted net earnings (Non-GAAP) $ 80.2 $ 54.3 48% Reported diluted EPS (GAAP) $1.68 $1.13 48% Adjustments (1) $0.16 $0.12 - Tax impact on Adjustments (1) ($0.04) ($0.04) - Adjusted diluted EPS (Non-GAAP) $1.80 $1.21 49% (1) Includes one-time Inventory Step-up, Backlog Amortization and Transaction costs for current and prior year acquisitions.

Non-GAAP Reconciliation – 2018 Guidance 15 | July 26, 2018 | © 2018 Curtiss-Wright CURTISS-WRIGHT CORPORATION 2018 Guidance (1) (2) As of July 25, 2018 ($’s in millions, except per share data) Adjusted (Non-GAAP) 2018 Prior Reported Guidance (GAAP) 2018 Reported Guidance (GAAP) 2018 Current Adjusted Guidance (Non-GAAP) Sales: Commercial/Industrial Defense Power Total sales Operating income: Commercial/Industrial Defense Power Total segments Corporate and other Total operating income Interest expense Other income, net Earnings before income taxes Provision for income taxes Net earnings Diluted earnings per share Diluted shares outstanding Effective tax rate Operating margins: Commercial/Industrial Defense Power Total operating margin 1405% 21.4% 14.7% 14.8% 21.6% 12.2% 14.2% 15.0% 21.5% 12.4% 14.4% +30 bps +20 bps +70 bps +40 bps 15.1% 12.9% 14.6% 15.2% 21.7% 13.1% 14.8% 60 to 70 bps 10 to 30 bps (160 to 180 bps) (10) to 10 bps - +220 bps +60 bps 15.2% 15.3% 15.4% 40 to 60 bps 50 to 70 bps $ 1,163 555 553 2,271 1,193 565 657 2,415 1,213 575 667 2,455 168 119 81 368 (34) 335 (41) 16 309 (88) 222 4.96 44.8 28.3% 177 121 80 378 (34) 343 (36) 14 322 (77) 245 (37) 14 331 (79) 5347 5362 44.7 24.0% 182 124 83 389 (35) 353 (37) 14 331 (79) 251 6 to 8% 6 to 9% 14 to 17% 20 10 – 30 6 3 4 13 – 1 – (4) 12 0.28 4436 5.75 44.6 5.90 8 to 9% 7 to 10% 16 to 19% 11 to 14% 21 to 24% Note: Full year amounts may not add due to rounding (1) Full-year 2017 and 2018 effective tax rate guidance includes the impacts of the Tax Cuts and Jobs Act. (2) Reconciliations of 2017 Reported (GAAP) results to Adjusted (non-GAAP) results are furnished within this release. (3) Adjustments include one-time inventory step-up, backlog amortization and transaction costs for current and prior year acquisitions.

Non-GAAP Reconciliation – 2017 Results 16 | July 26, 2018 | © 2018 Curtiss-Wright CURTISS-WRIGHT CORPORATION 2018 Guidance (1) (2) As of July 25, 2018 ($’s in millions, except per share data) Adjusted (Non-GAAP) 2018 Prior Reported Guidance (GAAP) 2018 Reported Guidance (GAAP) 2018 Current Adjusted Guidance (Non-GAAP) Sales: Commercial/Industrial Defense Power Total sales Operating income: Commercial/Industrial Defense Power Total segments Corporate and other Total operating income Interest expense Other income, net Earnings before income taxes Provision for income taxes Net earnings Diluted earnings per share Diluted shares outstanding Effective tax rate Operating margins: Commercial/Industrial Defense Power Total operating margin 1405% 21.4% 14.7% 14.8% 21.6% 12.2% 14.2% 15.0% 21.5% 12.4% 14.4% +30 bps +20 bps +70 bps +40 bps 15.1% 12.9% 14.6% 15.2% 21.7% 13.1% 14.8% 60 to 70 bps 10 to 30 bps (160 to 180 bps) (10) to 10 bps - +220 bps +60 bps 15.2% 15.3% 15.4% 40 to 60 bps 50 to 70 bps $ 1,163 555 553 2,271 1,193 565 657 2,415 1,213 575 667 2,455 168 119 81 368 (34) 335 (41) 16 309 (88) 222 4.96 44.8 28.3% 177 121 80 378 (34) 343 (36) 14 322 (77) 245 (37) 14 331 (79) 5347 5362 44.7 24.0% 182 124 83 389 (35) 353 (37) 14 331 (79) 251 6 to 8% 6 to 9% 14 to 17% 20 10 – 30 6 3 4 13 – 1 – (4) 12 0.28 4436 5.75 44.6 5.90 8 to 9% 7 to 10% 16 to 19% 11 to 14% 21 to 24 Note: Full year amounts may not add due to rounding (1) Reported 2017 results reflect the restrospective impact from the adoption of ASU 2017-07 "Improving the Presnetation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost," which results in reclassification of the non-service components of Pension expense from Operating Income to Other Income/Expense effective for fiscal years beginning after December 15, 2017. This accounting change lowers operating income by $14.6 million and lowers operating margin by 70 basis points for the full-year 2017 period. This change is neutral to earnings pre share. (2) Adjusted operating income, operating margin and diluted EPS exclude first year purchase accounting costs, specifically one-time inventory step-up, backlog amortization and transactions costs, associated with the acquisition of TTC in 2017 (Defense segment). First year purchase accounting costs in the third and fourth quarters of 2017 are not material.