Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - AAR CORP | a2236183zex-32_2.htm |

| EX-32.1 - EX-32.1 - AAR CORP | a2236183zex-32_1.htm |

| EX-31.2 - EX-31.2 - AAR CORP | a2236183zex-31_2.htm |

| EX-31.1 - EX-31.1 - AAR CORP | a2236183zex-31_1.htm |

| EX-23.1 - EX-23.1 - AAR CORP | a2236183zex-23_1.htm |

| EX-21.1 - EX-21.1 - AAR CORP | a2236183zex-21_1.htm |

| EX-10.9 - EX-10.9 - AAR CORP | a2236183zex-10_9.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| ý | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

For the fiscal year ended May 31, 2018 or |

||

o |

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

For the transition period from to

Commission file number 1-6263

AAR CORP.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

36-2334820 (I.R.S. Employer Identification No.) |

One AAR Place, 1100 N. Wood Dale Road, Wood Dale, Illinois 60191

(Address of principal executive offices, including zip code)

Registrant's telephone number, including area code: (630) 227-2000

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

| Common Stock, $1.00 par value | New York Stock Exchange Chicago Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.(Check one):

| Large accelerated filer ý | Accelerated filer o | Non-Accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period prior to complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the registrant's voting stock held by nonaffiliates was approximately $1,344 million (based upon the closing price of the Common Stock at November 30, 2017 as reported on the New York Stock Exchange).

On June 29, 2018, there were 34,740,330 shares of Common Stock outstanding.

Documents Incorporated by Reference

Portions of the Company's proxy statement for the Company's 2018 Annual Meeting of Stockholders, to be held October 10, 2018, are incorporated by reference in Part III of this report.

1

General

AAR CORP. and its subsidiaries are referred to herein collectively as "AAR," "Company," "we," "us," and "our" unless the context indicates otherwise. AAR was founded in 1951, organized in 1955 and reincorporated in Delaware in 1966. We are a diversified provider of products and services to the worldwide aviation and government and defense markets.

Beginning in fiscal 2015, we implemented a comprehensive strategic plan to narrow our strategy to focus on our best-in-class aviation and expeditionary services through our two business segments: Aviation Services and Expeditionary Services. We sold our Telair Cargo Group for cash of $714 million, resulting in pre-tax gains of $198.6 million in the fourth quarter of fiscal 2015 (and $27.7 million in the first quarter of fiscal 2016 from the receipt of contingent consideration). We used the proceeds from the sale in fiscal 2015 to reduce our total debt and return capital to shareholders through common stock repurchases and dividends.

Through execution of our strategic plan over the last three years, we have succeeded in expanding customer relationships and securing new flight hour component inventory management and repair programs work with multiple international commercial customers and government customers. We also invested in our rotable assets to support these programs and continued our focus on expanding our business development resources. These investments in our supply chain activities have allowed us to increase market share, expand our customer base, and enlarge our geographic footprint.

In fiscal 2018, we began the ramp-up for the 15-year, U.S. Air Force Landing Gear Performance-Based Logistics One program. Under the program, we are providing total supply chain management including purchasing, distribution and inventory control to support all landing gear components for the U.S. Air Force's fleet of C-130, KC-135 and E-3 aircraft.

In fiscal 2018, we also began providing services to the U.S. Department of State ("DoS") under the INL/A Worldwide Aviation Support Services ("WASS") contract. This contract leverages our capabilities in aviation services, including flight operations, supply chain logistics, and other services. We are the prime contractor on this 10-year performance-based contract to globally operate and maintain the DoS fleet of fixed and rotary-wing aircraft. We successfully completed the transition and phase-in of the WASS program in June 2018. We have full operational capability at all contract sites, which include Afghanistan, Iraq, Panama, Peru, and Patrick Air Force Base as well as support locations in Brevard County, Florida.

Our long-term strategy continues to emphasize the return of capital to shareholders. Over the past three years, we have returned $82.6 million to shareholders through common stock repurchases of $51.7 million and dividends of $30.9 million.

We remain in a strong financial position to further execute on our strategy in fiscal 2019. Both our commercial and government businesses are executing on our many contract wins and will continue to deliver growth in fiscal 2019. Our cash on hand plus unused capacities on our Revolving Credit Facility and accounts receivable financing program was $473 million at May 31, 2018. We expect to invest opportunistically in expanding our comprehensive suite of services to the global commercial aviation and government and defense markets. We continue to have the flexibility in our balance sheet allowing us to invest in our growth. As we generate positive cash flow, we will continue our strategy of returning capital to our shareholders without hampering our future operating flexibility.

2

Business Segments

Aviation Services

The Aviation Services segment provides aftermarket support and services for the commercial aviation and government and defense markets and accounted for 93% of our sales in fiscal 2018, 2017, and 2016. In this segment, we also provide inventory management and distribution services, maintenance, repair and overhaul ("MRO"), and engineering services. Business activities in this segment are primarily conducted through AAR Supply Chain, Inc.; AAR Government Services, Inc.; AAR Aircraft & Engine Sales & Leasing, Inc.; AAR Aircraft Services, Inc.; AAR Allen Services, Inc.; AAR Landing Gear LLC; and AAR International, Inc.

We sell and lease a wide variety of new, overhauled and repaired engine and airframe parts and components and aircraft to our commercial aviation and government/defense customers.

We provide customized flight hour component inventory and repair programs, warranty claim management, and outsourcing programs for engine and airframe parts and components in support of our airline and government customers' maintenance activities. The types of services provided under these programs include material planning, sourcing, logistics, information and program management, and parts and component repair and overhaul. We are also an authorized distributor for more than 70 product lines across over 25 leading aviation product manufacturers.

We also provide customized performance-based supply chain logistics programs in support of the U.S. Department of Defense ("DoD") and foreign governments. The types of services provided under these programs include material planning, sourcing, logistics, information and program management, airframe maintenance and maintenance planning, and component repair and overhaul.

We provide major airframe inspection, maintenance, repair and overhaul, painting services, line maintenance, airframe modifications, structural repairs, avionic service and installation, exterior and interior refurbishment, and engineering services and support for many types of commercial and military aircraft. We also repair and overhaul various components, landing gears, wheels, and brakes for commercial and military aircraft.

We operate seven airframe maintenance facilities and one landing gear overhaul facility. Our landing gear overhaul facility is in Miami, Florida, where we repair and overhaul landing gear, wheels, brakes, and actuators for different types of commercial and military aircraft. Our U.S. airframe maintenance facilities are in Indianapolis, Indiana; Oklahoma City, Oklahoma; Duluth, Minnesota; Miami, Florida; and Rockford, Illinois and our Canadian airframe maintenance facilities are in Trois Rivieres, Quebec and Windsor, Ontario. In addition, we also announced a joint venture with Indamer Aviation which will develop and operate an airframe maintenance facility in India. The facility is currently under construction and is expected to begin operations in fiscal 2019.

The majority of our product sales are made pursuant to standard commercial purchase orders. Government sales are generally made under standard types of government contracts which can include firm fixed-price contracts, cost plus fixed fee contracts, and time-and-materials contracts. Some of our contracts call for the performance of specified services or the delivery of specified products under indefinite delivery/indefinite quantity ("ID/IQ") arrangements. Certain inventory supply and management and performance-based logistics program agreements reflect negotiated terms and conditions.

To support activities within the Aviation Services segment, we acquire aviation parts and components from domestic and foreign airlines, independent aviation service companies, aircraft leasing companies, and original equipment manufacturers ("OEM"s). We have ongoing arrangements with OEMs that provide us access to parts, repair manuals, and service bulletins in support of parts manufactured by them. Although the terms of each arrangement vary, they typically are made on standard OEM terms as to

3

duration, price, and delivery. From time to time, we purchase engines for disassembly into individual parts and components. These engines may be leased to airlines on a short-term basis prior to disassembly.

Expeditionary Services

The Expeditionary Services segment consists of businesses that primarily provide products and services supporting the movement of equipment and personnel by the U.S. and foreign governments and non-governmental organizations. The Expeditionary Services segment accounted for 7% of our sales in fiscal 2018, 2017, and 2016. Business activities in this segment are primarily conducted through AAR Airlift Group, Inc.; AAR Manufacturing, Inc. and Brown International Corporation.

We provide fleet management and operations of customer-owned aircraft for the DoS under the INL/A WASS contract. We are the prime contractor on this ten-year performance-based contract to globally operate and maintain the DoS fleet of fixed- and rotary-wing aircraft.

We also design, manufacture, and repair transportation pallets and a wide variety of containers and shelters used in support of military and humanitarian tactical deployment activities. The containers and shelters are used in numerous mission requirements, including armories, supply and parts storage, refrigeration systems, tactical operation centers, briefing rooms, laundry and kitchen facilities, water treatment, and sleeping quarters. Shelters include both stationary and vehicle-mounted applications.

We also provide engineering, design, and system integration services for specialized command and control systems and design and manufacture advanced composite materials for commercial, business and military aircraft.

Sales in this segment are generally made to customers pursuant to standard commercial purchase orders and contracts. Government sales are generally made under standard types of government contracts which can include firm fixed-price contracts, cost plus fixed fee contracts, and time-and-materials contracts. Some of our contracts call for the performance of specified services or the delivery of specified products under ID/IQ arrangements, however, the majority of our products and services are procured via definite contracts.

Raw Materials

Although we generated 60% of our fiscal 2018 sales from the sale of products, our businesses are generally engaged in limited manufacturing activities and have minimal exposure to fluctuations in both the availability and pricing of raw materials. We purchase raw materials for our manufacturing operations, including steel, aluminum, extrusions, balsa, and other necessary supplies from several vendors. Where necessary, we have been able to obtain raw materials and other inventory items from numerous sources for each segment at competitive prices, terms, and conditions, and we expect to be able to continue to do so.

Terms of Sale

We generally sell our products and services under standard 30-day payment terms. On occasion, certain customers, principally foreign customers, will negotiate extended payment terms of 60-90 days. Except for customary warranty provisions, customers neither have the right to return products nor do they have the right to extended financing. Our government contracts may extend several years and include one or more base years and one or more option years. The government generally has the right not to exercise options to extend or expand our contracts and may otherwise terminate, cancel, or modify some contracts at its convenience.

Customers

The principal customers for our products and services in the Aviation Services segment are domestic and foreign commercial airlines, domestic and foreign freight airlines, regional and commuter airlines,

4

business and general aviation operators, OEMs, aircraft leasing companies, aftermarket aviation support companies, the DoD and its contractors, and foreign military organizations or governments. In the Expeditionary Services segment, our principal customers include the DoS, DoD and its contractors, foreign military organizations or governments, defense organizations, and OEMs.

Sales of aviation products and services to our commercial airline customers are generally affected by such factors as the number, type and average age of aircraft in service, the levels of aircraft utilization (e.g., frequency of schedules), the number of airline operators, the general economy, and the level of sales of new and used aircraft. Sales to the DoD and other government agencies are subject to a number of factors, including the level of troop deployment worldwide, government funding, competitive bidding, and requirements generated by worldwide geopolitical events.

We primarily market and sell products and services through our own employees. In certain markets outside of the United States, we rely on foreign sales representatives to assist in the sale of our products and services.

Sales to Government and Defense Customers

Sales to global government and defense customers (including sales to branches, agencies, and departments of the U.S. government) were $428.8 million (24.5% of consolidated sales), $438.7 million (27.6% of consolidated sales) and $489.4 million (32.1% of consolidated sales) in fiscal 2018, 2017 and 2016, respectively. Sales to branches, agencies, and departments of the U.S. government and their contractors were $304.3 million (17.4% of consolidated sales), $321.5 million (20.2% of consolidated sales), and $366.1 million (24.0% of consolidated sales) in fiscal 2018, 2017, and 2016, respectively.

Sales to government and defense customers are reported in each of our reportable segments (See Note 13 of Notes to Consolidated Financial Statements). Since such sales are subject to competitive bidding and government funding, no assurance can be given that such sales will continue at levels previously experienced. The majority of our U.S. government sales are for products and services supporting the DoD logistics and mobility strategy. Thus, our government contracts have changed, and may continue to change, with fluctuations in defense and other governmental agency spending. Our government contracts are also subject to termination by the customer; in the event of such a termination, we are entitled to recover all allowable costs incurred by us through the date of termination.

Government Regulation and Certificates

The Federal Aviation Administration ("FAA") regulates the manufacture, repair, and operation of all aircraft and aircraft parts operated in the United States. Similar rules and regulatory authorities exist in other countries. The inspection, maintenance and repair procedures for the various types of aircraft and equipment are prescribed by these regulatory authorities and can be performed only by certified repair facilities utilizing certified technicians. The FAA requires that various maintenance routines be performed on aircraft engines, certain engine parts, and airframes at regular intervals based on take off and landing cycles or flight time. Our businesses which sell defense products and services directly to the U.S. government or through its contractors can be subject to various laws and regulations governing pricing and other factors.

We have 13 FAA certificated repair stations in the United States, Canada, and Europe. Of the 13 certificated FAA repair stations, seven are also European Aviation Safety Agency ("EASA") and four are also Transport Canada Civil Aviation ("TCCA") certificated repair stations. Such certificates, which are ongoing in duration, are required for us to perform authorized maintenance, repair and overhaul services for our customers and are subject to revocation by the government for non-compliance with applicable regulations. Of the 13 FAA certificated repair stations, 12 are in the Aviation Services segment and one is held by our Contractor-Owned, Contractor-Operated business ("COCO") which is classified as a discontinued operation as the COCO business is currently held for sale. The EASA and TCCA certificated

5

repair stations are in the Aviation Services segment. We also hold a FAR Part 135 certificate to operate aircraft for our expeditionary airlift services business. We are also Commercial Airlift Review Board certified with the DoD. We believe that we possess all licenses and certifications that are material to the conduct of our business.

Competition

Competition in each of our markets is based on quality, ability to provide a broad range of products and services, speed of delivery, and price. Competitors in our Aviation Services segment include OEMs, the service divisions of large commercial airlines, and other independent suppliers of parts, repair, and overhaul services to the commercial and defense markets. Our Expeditionary Services segment competes with domestic and foreign contracting companies and a number of divisions of large corporations and other large and small companies. Although certain of our competitors have substantially greater financial and other resources than we do, we believe that we have maintained a satisfactory competitive position through our responsiveness to customer needs, our attention to quality, and our unique combination of market expertise and technical and financial capabilities.

Backlog

Backlog represents the amount of revenue that we expect to derive from unshipped orders or signed contracts. At May 31, 2018, backlog was approximately $1,053 million compared to $519 million at May 31, 2017 which reflects the significant new commercial and government contract awards received over the last twelve months. Approximately $510 million of our May 31, 2018 backlog is expected to be filled in fiscal 2019.

Employees

At May 31, 2018, we employed approximately 5,000 employees worldwide, of which approximately 155 employees are subject to a collective bargaining agreement. We also retain approximately 775 contract workers, the majority of whom are located at our airframe maintenance facilities.

Available Information

For additional information concerning our business segments, see Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Business Segment Information" in Note 13 of Notes to Consolidated Financial Statements under Item 8, "Financial Statements and Supplementary Data."

Our internet address is www.aarcorp.com. We make available free of charge through our web site our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the Securities and Exchange Commission. Information contained on our web site is not a part of this report.

6

The following is a description of the principal risks inherent in our business.

We are affected by factors that adversely impact the commercial aviation industry.

As a provider of products and services to the commercial aviation industry, we are greatly affected by overall economic conditions of that industry. The commercial aviation industry is historically cyclical and has been negatively affected in the past by geopolitical events, high fuel and oil prices, lack of capital, and weak economic conditions. As a result of these and other events, from time to time certain of our customers have filed for bankruptcy protection or ceased operation. The impact of instability in the global financial markets may lead airlines to reduce domestic or international capacity. In addition, certain of our airline customers have in the past been impacted by tight credit markets, which limited their ability to buy parts, services, engines, and aircraft.

A reduction in the operating fleet of aircraft both in the U.S. and abroad will result in reduced demand for parts support and maintenance activities for the type of aircraft affected. Further, tight credit conditions negatively impact the amount of liquidity available to buy parts, services, engines, and aircraft. A deteriorating airline environment may also result in additional airline bankruptcies, and in such circumstances we may not be able to fully collect outstanding accounts receivable. Reduced demand from customers caused by weak economic conditions, including tight credit conditions and customer bankruptcies, may adversely impact our financial condition or results of operations.

Our business, financial condition, results of operations, and growth rates may be adversely affected by these and other events that impact the aviation industry, including the following:

- •

- deterioration in the financial condition of our existing and potential customers;

- •

- reductions in the need for, or the deferral of, aircraft maintenance and repair services and spare parts support;

- •

- retirement of older generation aircraft, resulting in lower prices for spare parts and services for those aircraft;

- •

- reductions in demand for used aircraft and engines;

- •

- increased in-house maintenance by airlines;

- •

- lack of parts in the marketplace;

- •

- acts of terrorism;

- •

- future outbreaks of infectious diseases; and

- •

- acts of God.

Our U.S. government contracts may not continue at present sales levels, which may have a material adverse effect on our financial condition and results of operations.

Our sales to branches, agencies and departments of the U.S. government and their contractors were $304.3 million (17.4% of consolidated sales) in fiscal 2018 (See Note 13 of Notes to Consolidated Financial Statements). The majority of our U.S. government sales is for products and services supporting DoD logistics and mobility strategy and is, therefore, subject to changes in defense and other governmental agency funding and spending. Our contracts with the U.S. government and their contractors are typically agreements to provide products and services at a fixed price and have a term of one year or less, frequently subject to extension for one or more additional periods of one year at the option of the government customer. Sales to agencies of the U.S. government and their contractors are subject to a number of

7

factors, including the level of troop deployment worldwide, competitive bidding, U.S. government funding, requirements generated by world events, and budgetary constraints.

U.S. government programs are subject to annual congressional budget authorization and appropriation processes. In recent years, U.S. government appropriations have been affected by larger U.S. government budgetary issues and related legislation, including the statutory limit on the amount of permissible federal debt (the "debt ceiling"). These issues could negatively affect the timely collection of our U.S. government invoices.

Future congressional appropriation and authorization of defense spending and the application of sequestration remain marked by significant debate and an uncertain schedule. The federal debt limit continues to be actively debated as plans for long-term national fiscal policy are discussed. The outcome of these debates could have a significant impact on defense spending broadly and programs we support in particular.

If there are funding delays and constraints, we may be required to continue to perform for some period of time on certain of our U.S. government contracts even if the U.S. government is unable to make timely payments. Future budget cuts, including cuts mandated by sequestration, or future procurement decisions could result in reductions, cancellations, and/or delays of existing contracts or programs which could adversely affect our results of operations and financial condition.

We face risks of cost overruns and losses on fixed-price contracts.

We sell certain of our products and services to our commercial, government, and defense customers under firm contracts providing for fixed unit prices, regardless of costs incurred by us. The cost of producing products or providing services may be adversely affected by increases in the cost of labor, materials, fuel, overhead, and other unknown variants, including manufacturing and other operational inefficiencies and differences between assumptions used by us to price a contract and actual results. Increased costs may result in cost overruns and losses on such contracts, which could adversely affect our results of operations and financial condition.

Success at our airframe maintenance facilities is dependent upon continued outsourcing by the airlines.

We currently perform airframe maintenance, repair and overhaul activities at seven leased locations. Revenues at these facilities fluctuate based on demand for maintenance which, in turn, is driven by the number of aircraft operating and the extent of outsourcing of maintenance activities by airlines. In addition, certain airlines operate certain new fleet types and/or newer generation aircraft and we may not have contractual arrangements to service these aircraft nor technicians trained and certified to perform the required airframe maintenance, repair and overhaul activities. If either the number of aircraft operating or the level of outsourcing of maintenance activities declines, we may not be able to execute our operational and financial plans at our maintenance, repair and overhaul facilities, which could adversely affect our results of operations and financial condition.

We operate in highly competitive markets, and competitive pressures may adversely affect us.

The markets for our products and services to our commercial, government, and defense customers are highly competitive, and we face competition from a number of sources, both domestic and international. Our competitors include aircraft manufacturers, aircraft component and parts manufacturers, airline and aircraft service companies, other companies providing maintenance, repair and overhaul services, other aircraft spare parts distributors and redistributors, and other expeditionary airlift service providers. Some of our competitors have substantially greater financial and other resources than we have and others may price their products and services below our selling prices. These competitive markets also create pressure on our ability to hire and retain qualified technicians and other skilled labor needs. We believe that our

8

ability to compete depends on superior customer service and support, on-time delivery, sufficient inventory availability, competitive pricing and effective quality assurance programs.

Our government customers, including the DoD, may turn to commercial contractors, rather than traditional defense contractors, for certain work, or may utilize small business contractors or determine to source work internally rather than use us. We are also impacted by bid protests from unsuccessful bidders on new program awards. Bid protests could result in significant expense for us, contract modifications, or the award decision being overturned and loss of the contract award. Even where a bid protest does not result in the loss of an award, the resolution can extend the time until the contract activity can begin, and delay earnings. These competitive pressures, with potential impacts on both our commercial and government business, could adversely affect our results of operations and financial condition.

We are subject to significant government regulation and may need to incur significant expenses to comply with new or more stringent governmental regulation.

The aviation industry is highly regulated by the FAA in the United States and equivalent regulatory agencies in other countries. Before we sell any of our products that are to be installed in an aircraft, such as engines, engine parts and components, and airframe and accessory parts and components, they must meet certain standards of airworthiness established by the FAA or the equivalent regulatory agencies in certain other countries. We operate repair stations that are licensed by the FAA and the equivalent regulatory agencies in certain other countries, and hold certificates to operate aircraft. Specific regulations vary from country to country, although regulatory requirements in other countries are generally satisfied by compliance with FAA requirements. New and more stringent governmental regulations may be adopted in the future that, if enacted, may have an adverse impact on us.

If any of our material licenses, certificates, authorizations, or approvals were revoked or suspended by the FAA or equivalent regulatory agencies in other countries, our results of operations and financial condition may be adversely affected.

If we fail to comply with government procurement laws and regulations, we could lose business and be liable for various penalties or sanctions.

We must comply with laws and regulations relating to the formation, administration, and performance of U.S. government contracts. These laws and regulations include the Federal Acquisition Regulations, Defense Federal Acquisition Regulations, the Truth in Negotiations Act, Cost Accounting Standards, and laws, regulations, and orders restricting the use and dissemination of classified information under the U.S. export control laws and the export of certain products and technical information and safeguarding of contractor information systems. Certain government contracts provide audit rights by government agencies, including with respect to performance, costs, business systems, internal controls and compliance with applicable laws and regulations. In complying with these laws and regulations, we may incur significant costs, and non-compliance may result in the imposition of fines and penalties, including contractual damages. If we fail to comply with these laws and regulations or if a government audit, review, or investigation uncovers improper or illegal activities, we may be subject to civil penalties, criminal penalties, or administrative sanctions, including suspension or debarment from contracting with the U.S. government. Our reputation could suffer harm if allegations of impropriety were made or found against us, which could adversely affect our operating performance and may result in additional expenses and possible loss of revenue.

9

We are exposed to risks associated with operating internationally.

We conduct our business in a number of foreign countries, some of which are politically unstable or subject to military or civil conflicts. Consequently, we are subject to a variety of risks that are specific to international operations, including the following:

- •

- military conflicts, civil strife, and political risks;

- •

- export regulations that could erode profit margins or restrict exports;

- •

- compliance with the U.S. Foreign Corrupt Practices Act, United Kingdom ("UK") Anti-bribery Act, and other anti-bribery and anti-corruption

laws;

- •

- the burden and cost of compliance with foreign laws, treaties, and technical standards and changes in those regulations;

- •

- contract award and funding delays;

- •

- potential restrictions on transfers of funds;

- •

- import and export duties and value added taxes;

- •

- foreign exchange risk;

- •

- transportation delays and interruptions;

- •

- uncertainties arising from foreign local business practices and cultural considerations; and

- •

- changes in U.S. policies on trade relations and trade policy, including implementation of or changes in trade sanctions, tariffs, and embargoes.

In addition, the UK held a referendum in 2016 in which voters approved an exit from the European Union ("EU"). On March 29, 2017, the UK government commenced the exit process under Article 50 of the Treaty of the EU by notifying the European Council of the UK's intention to leave the EU. This notification started a two-year time period for the UK and the remaining EU countries to negotiate a withdrawal agreement. The final terms of the UK's potential exit from the EU have yet to be determined and it is possible there will be greater restrictions on imports and exports between the UK and EU countries along with increased regulatory complexities.

While we have adopted and will continue to adopt measures to reduce the potential impact of losses resulting from the risks of doing business internationally, such measures may not be adequate, and the regions in which we operate might not continue to be stable enough to allow us to operate profitably or at all.

Acquisitions expose us to risks, including the risk that we may be unable to effectively integrate acquired businesses.

We have completed multiple acquisitions over the past few years and we have discussions with third parties regarding acquisitions on a regular basis. Acquisitions involve risks, including difficulties in integrating the operations and personnel, the effects of amortization of any acquired intangible assets and the potential impairment of goodwill, and the potential loss of key employees of the acquired business. In addition, acquisitions often require substantial management resources and have the potential to divert our attention from our existing business. For any businesses we may acquire in the future, we may not be able to execute our operational, financial, or integration plans for the acquired businesses, which could adversely affect our results of operations and financial condition.

10

Market values for our aviation products fluctuate and we may be unable to recover our costs incurred on engines, rotable components and other aircraft parts.

We make a number of assumptions when determining the recoverability of rotable components, engines, and other assets which are on lease, available for lease, or supporting our long-term programs. These assumptions include historical sales trends, current and expected usage trends, replacement values, current and expected lease rates, residual values, future demand, and future cash flows. Reductions in demand for these assets or declining market values, as well as differences between actual results and the assumptions utilized by us when determining the recoverability of our aircraft, engines, and other assets could result in impairment charges in future periods, which would adversely affect our results of operations and financial condition.

We may need to reduce the carrying value of our assets.

We own and distribute a significant amount of engines, aircraft parts and components, and manufacturing facilities and related equipment. The removal of aircraft from service or recurring losses in certain operations could require us to evaluate the recoverability of the carrying value of those assets and record an impairment charge through earnings to reduce the carrying value. During the second quarter of fiscal 2018, we recognized impairment charges of $54.2 million related to assets included in our COCO business which is classified as a discontinued operation. In addition, if aircraft or engines for which we offer replacement parts or supply repair and overhaul services are retired and there are fewer aircraft that require these parts or services, our revenues may decline.

We make a number of assumptions when determining the recoverability of our assets including historical sales trends, current and expected usage trends, replacement values, current and expected lease rates, residual values, future demand, and future cash flows. Differences between actual results and the assumptions utilized by us when determining the recoverability of our assets could result in impairment charges in future periods, which would adversely affect our results of operations and financial condition.

We have recorded goodwill and other intangible assets related to acquisitions. If we are unable to achieve the projected levels of operating results, it may be necessary to record an impairment charge to reduce the carrying value of goodwill and related intangible assets. During the third quarter of fiscal 2018, we recognized a goodwill impairment charge of $9.8 million related to our COCO business. Similarly, if we were to lose a key customer or one of our airframe maintenance or landing gear facilities were to lose its authority to operate, we might be required to record an impairment charge.

We are dependent upon continued availability of financing to manage our business and to execute our business strategy, and additional financing may not be available on terms acceptable to us.

Our ability to manage our business and to execute our business strategy is dependent, in part, on the continued availability of debt and equity capital. Access to the debt and equity capital markets may be limited by various factors, including the condition of overall credit markets, general economic factors, state of the aviation industry, our financial performance, and credit ratings. Debt and equity capital may not continue to be available to us on favorable terms, or at all. Our inability to obtain financing on favorable terms could adversely affect our results of operations and financial condition.

Our existing debt includes restrictive and financial covenants.

Certain financing arrangements, including our Revolving Credit Facility and our accounts receivable financing program, require us to comply with various restrictive covenants and some contain financial covenants that require us to comply with specified financial ratios and tests. Our failure to meet these covenants could result in default under these loan and debt agreements and may result in a cross-default under other debt agreements. In the event of a default and our inability to obtain a waiver of the default, all amounts outstanding under our debt agreements could be declared immediately due and payable. Our

11

failure to comply with these covenants could adversely affect our results of operations and financial condition.

Our industry is susceptible to product and other liability claims, and claims not adequately covered by insurance may adversely affect our financial condition.

Our business exposes us to possible claims for property damage and bodily injury or death which may result if an engine, engine part or component, airframe part or accessory, or any other aviation product which we have sold, manufactured, or repaired fails, or if an aircraft we operated, serviced, or in which our products are installed, crashes. We carry substantial liability insurance in amounts that we believe are adequate for our risk exposure and commensurate with industry norms. However, claims may arise in the future, and our insurance coverage may not be adequate to protect us in all circumstances. Additionally, we might not be able to maintain adequate insurance coverage in the future at an acceptable cost. Any liability claim not covered by adequate insurance could adversely affect our results of operations and financial condition.

Our business could be negatively affected by cyber or other security threats or other disruptions.

Our businesses depend heavily on information technology and computerized systems to communicate and operate effectively. The Company's systems and technologies, or those of third parties on which we rely, could fail or become unreliable due to equipment failures, software viruses, cyber threats, ransomware attacks, terrorist acts, natural disasters, power failures or other causes. These threats arise in some cases as a result of our role as a defense contractor.

Cyber security threats are evolving and include, but are not limited to, malicious software, attempts to gain unauthorized access to our sensitive information, ransomware attacks, including our customers, suppliers, subcontractors, and joint venture partners, and other electronic security breaches that could lead to disruptions in mission critical systems, unauthorized release of confidential or otherwise protected information, and corruption of data.

The procedures and controls we utilize to monitor and mitigate these threats may not be sufficient to prevent security threats from materializing. If any of these events were to materialize, the costs related to cyber or other security threats or disruptions may not be fully insured or indemnified and could have a material adverse effect on our reputation, operating results, and financial condition.

Moreover, expenditures incurred in implementing and maintaining cyber security and other procedures and controls could adversely affect our results of operations and financial condition.

We must comply with extensive environmental requirements, and any exposure to environmental liabilities may adversely affect us.

Federal, state, and local requirements relating to the discharge and emission of substances into the environment, the disposal of hazardous wastes, the remediation and abatement of contaminants, and other activities affecting the environment have had and may continue to have an impact on our operations. Management cannot assess the possible effect of compliance with future environmental requirements or of future environmental claims for which we may not have adequate indemnification or insurance coverage. If we were required to pay the expenses related to any future environmental claims for which neither indemnification nor insurance coverage were available, these expenses could have an adverse impact on our results of operations and financial condition.

Future environmental regulatory developments in the United States and abroad concerning environmental issues, such as climate change, could adversely affect our operations and increase operating costs and, through their impact on our customers, reduce demand for our products and services. Actions may be taken in the future by the U.S. government, state governments within the United States, foreign

12

governments, the International Civil Aviation Organization, or by signatory countries through a new global climate change treaty to regulate the emission of greenhouse gases by the aviation industry. The precise nature of any such requirements and their applicability to us and our customers are difficult to predict, but the impact to us and the aviation industry would likely be adverse and could be significant, including the potential for increased fuel costs, carbon taxes or fees, or a requirement to purchase carbon credits.

We may need to make significant capital expenditures to keep pace with technological developments in our industry.

The industries in which we participate are constantly undergoing development and change, and it is likely that new products, equipment, and methods of repair and overhaul services will be introduced in the future. We may need to make significant expenditures to purchase new equipment and to train our employees to keep pace with any new technological developments. These expenditures could adversely affect our results of operations and financial condition.

Our operations would be adversely affected by a shortage of skilled personnel or work stoppages.

We are dependent on an educated and highly skilled workforce because of the complex nature of many of our products and services. Furthermore, we have a collective bargaining agreement covering approximately 155 employees. Our ability to operate successfully and meet our customers' demands could be jeopardized if we are unable to attract and retain a sufficient number of skilled personnel, including qualified licensed mechanics, to conduct our business, or if we experience a significant or prolonged work stoppage. These and similar events may adversely affect our results of operations and financial condition.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not Applicable.

In the Aviation Services segment, we conduct parts supply activities from our headquarters in Wood Dale, Illinois, which we own. In addition to warehouse space, this facility includes executive, sales and administrative offices. Our principal maintenance, repair, overhaul, engineering and other service activities for this segment are conducted at U.S. facilities leased by us in Indianapolis, Indiana; Oklahoma City, Oklahoma; Miami, Florida; Duluth, Minnesota; and Rockford, Illinois and at Canadian facilities leased by us in Trois Rivieres, Quebec and Windsor, Ontario.

We also lease facilities in Garden City, New York; Jacksonville, Florida; Brussels, Belgium; Singapore, Republic of Singapore; London, England; and Crawley, England, and own a building near Schiphol International Airport in the Netherlands to support activities in the Aviation Services segment.

Our principal activities in the Expeditionary Services segment are conducted at facilities we lease in Melbourne, Florida; Huntsville, Alabama; and Sacramento, California and own in Cadillac, Michigan; Clearwater, Florida; and Goldsboro, North Carolina.

We also operate sales offices which support all our activities and are leased in London, England; Crawley, England; Paris, France; Rio de Janeiro, Brazil; Shanghai, China; Singapore, Republic of Singapore; and Abu Dhabi, UAE.

We believe that our owned and leased facilities are suitable and adequate for our operational requirements.

13

DynCorp International LLC v. AAR Airlift Group, Inc.

On September 5, 2015, DynCorp International LLC ("DynCorp") filed a complaint in the United States District Court for the Middle District of Florida, Orlando Division (the "District Court"), accusing AAR Airlift Group, Inc. ("Airlift"), a wholly-owned subsidiary of AAR CORP., of misappropriation of DynCorp information, including trade secrets, and other related allegations, in connection with the submission of proposals in response to the solicitation issued by the U.S. Department of State ("DoS") Bureau of International Narcotics and Law Enforcement Affairs, Office of Aviation in support of the Worldwide Aviation Support Services program ("WASS").

On October 19, 2015, DynCorp filed an amended complaint with the District Court. On January 14, 2016, the District Court granted Airlift's motion to dismiss DynCorp's amended complaint. On February 2, 2016, DynCorp appealed the District Court's order to the United States Court of Appeals for the Eleventh Circuit (the "Eleventh Circuit").

On November 21, 2016, the Eleventh Circuit reversed in part the District Court's dismissal of the amended complaint and remanded the case to the District Court for further proceedings.

On January 31, 2018, Airlift and DynCorp filed a joint notice of settlement, advising the District Court that they had reached an agreement in principle to resolve DynCorp's lawsuit and that they expected to file a stipulation of dismissal with prejudice within 14 days.

On February 1, 2018, the District Court entered an order dismissing the DynCorp lawsuit without prejudice, subject to the right of any party within 60 days to move the court for the purpose of entering a stipulated form of a final order or judgment or, on good cause shown, to reopen the case for further proceedings.

On June 20, 2018, the parties entered into a confidential settlement agreement to dismiss the lawsuit with prejudice without the payment of any money by either party. On June 26, 2018, the District Court entered an order dismissing the lawsuit with prejudice.

Appeals Proceeding Relating to the INL/A WASS Contract Award

On September 1, 2016, the DoS awarded the WASS contract to Airlift. On December 20, 2016, the U.S. Government Accountability Office ("GAO") denied a protest filed by DynCorp and confirmed the award of the WASS contract to Airlift.

On December 28, 2016, DynCorp filed a further protest with the U.S. Court of Federal Claims ("COFC"). On October 31, 2017, the COFC denied DynCorp's protest. On November 20, 2017, DynCorp filed an emergency motion for interim relief pending appeal with the COFC. On December 13, 2017, the COFC issued an order denying DynCorp's motion.

On November 14, 2017, DynCorp filed notice of appeal of the denial by the COFC of its protest to the U.S. Court of Appeals for the Federal Circuit (the "Court of Appeals"). On December 15, 2017, DynCorp filed a motion for injunction pending appeal with the Court of Appeals. On January 17, 2018, the Court of Appeals denied DynCorp's motion for injunction. The appeal on the merits before the Court of Appeals has been fully briefed by the parties, with no scheduled date for a decision.

Department of Justice Investigation

The U.S. Department of Justice ("DoJ"), acting through the U.S. Attorney's Office for the Southern District of Illinois, is conducting an investigation of Airlift under the federal civil False Claims Act ("FCA"). The investigation relates to Airlift's performance of several contracts awarded by the U.S. Transportation Command concerning the operations and maintenance of rotary-wing and fixed-wing

14

aircraft in Afghanistan and Africa, as well as several U.S. Navy contracts. In June 2018, the DoJ informed Airlift that part of the investigation was precipitated by a lawsuit filed under the qui tam provisions of the FCA by a former employee of Airlift. That lawsuit remains under seal. Airlift is cooperating with the DoJ investigation.

ITEM 4. MINE SAFETY DISCLOSURES

Not Applicable.

Supplemental Item:

EXECUTIVE OFFICERS OF THE REGISTRANT

Information concerning each of our executive officers is set forth below:

Name

|

Age | Present Position with the Company

|

||

|---|---|---|---|---|

| John M. Holmes | 41 | Chief Executive Officer and President, Director | ||

| Michael D. Milligan | 55 | Vice President and Chief Financial Officer | ||

| Robert J. Regan | 60 | Vice President, General Counsel and Secretary | ||

| Eric S. Pachapa | 45 | Vice President, Controller and Chief Accounting Officer |

Mr. Holmes is Chief Executive Officer and President, having served in that capacity since June 2018. From June 2017 to May 2018, Mr. Holmes served as President and Chief Operating Officer. From February 2015 to June 2017, Mr. Holmes served as Chief Operating Officer—Aviation Services. Prior to that, Mr. Holmes served as Group Vice President, Aviation Services—Inventory Management and Distribution from 2012 to 2015, General Manager and Division President of our Allen Asset Management business from 2003 to 2012, and in various other positions since joining the Company in September 2001. Mr. Holmes has been a director of the Company since 2017.

Mr. Milligan is Vice President and Chief Financial Officer, having served in that capacity since September 2017. Prior to joining AAR, he was Senior Vice President and Chief Financial Officer of NES Rentals Holdings, Inc. since 2005. Mr. Milligan was previously Executive Vice President and Chief Financial Officer of Telenisus Corporation from 1999 to 2001 and, prior thereto, was a partner with Pricewaterhouse Coopers LLP.

Mr. Regan is Vice President, General Counsel and Secretary, having served in that capacity since June 2009. From 2008 to June 2009, Mr. Regan served as Vice President and General Counsel and, prior to that, Associate General Counsel since joining AAR in February 2008. Prior to joining AAR, he was a partner at the law firm of Schiff Hardin LLP since 1989.

Mr. Pachapa is Vice President, Controller and Chief Accounting Officer, having served in that capacity since July 2016. Mr. Pachapa previously served as Controller since October 2015 and Senior Director of Accounting and Reporting since April 2014. Prior to joining the Company, he was with Glanbia plc from 2011 to 2014, and with Ernst & Young LLP from 1996 to 2011.

Each executive officer is elected annually by the Board of Directors. Executive officers continue to hold office until their successors are duly elected or until their death, resignation, termination or reassignment.

15

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is traded on the New York Stock Exchange and the Chicago Stock Exchange under the symbol "AIR." On June 29, 2018, there were approximately 900 holders of common stock, including participants in security position listings.

The following table shows the range of prices for our common stock and the amount of dividends declared per share during each quarter of our last two fiscal years:

| |

First Quarter |

Second Quarter |

Third Quarter |

Fourth Quarter |

Full Year | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Market price |

||||||||||||||||

High |

$ | 37.64 | $ | 41.58 | $ | 43.95 | $ | 47.70 | $ | 47.70 | ||||||

Low |

34.00 | 34.54 | 37.39 | 41.41 | 34.00 | |||||||||||

Dividends declared |

0.075 | 0.075 | 0.075 | 0.075 | 0.30 | |||||||||||

| |

First Quarter |

Second Quarter |

Third Quarter |

Fourth Quarter |

Full Year | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Market price |

||||||||||||||||

High |

$ | 25.04 | $ | 38.67 | $ | 38.31 | $ | 36.01 | $ | 38.67 | ||||||

Low |

22.06 | 26.21 | 31.49 | 32.74 | 22.06 | |||||||||||

Dividends declared |

0.075 | 0.075 | 0.075 | 0.075 | 0.30 | |||||||||||

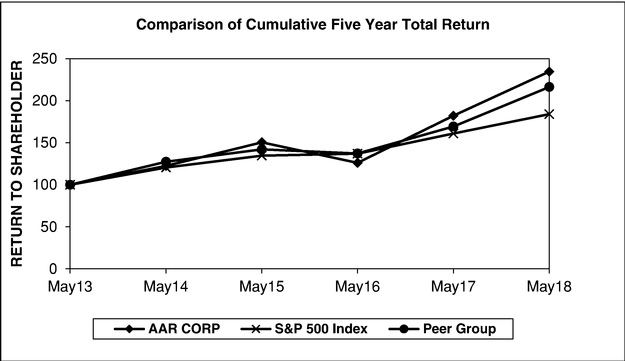

Stockholder Return Performance Graph

The following graph compares the total return on a cumulative basis of $100 invested, and reinvestment of dividends in our common stock on May 31, 2013 to the Standard and Poor's ("S&P") 500 Index and the Proxy Peer Group.

16

The S&P 500 Index is comprised of domestic industry leaders in four major sectors: Industrial, Financial, Utility, and Transportation, and serves as a broad indicator of the performance of the U.S. equity market. The Company's Fiscal 2018 Proxy Peer Group companies are listed as follows:

| Aerojet Rocketdyne Holdings, Inc. | KLX Inc. | |

| Barnes Group Inc. | Moog Inc. | |

| CACI International Inc | Rockwell Collins, Inc. | |

| Crane Co. | Science Applications International Corporation | |

| Cubic Corporation | Teledyne Technologies Incorporated | |

| Curtiss-Wright Corporation | TransDigm Group Incorporated | |

| Esterline Technologies Corporation | Triumph Group, Inc. | |

| Heico Corporation | Wesco International, Inc. | |

| Hexcel Corporation | Woodward, Inc. | |

| Kaman Corporation |

The Company annually revisits the composition of the peer group to ensure that the Company's performance is measured against those of comparably-sized and situated companies. The mix of the Company's commercial and defense businesses presents a challenge in constructing a peer group, given that many defense contractors have substantially greater resources than the Company. No changes were made to the composition of the peer group for fiscal 2018.

Issuer Purchases of Equity Securities

We did not purchase any shares of our common stock during the quarter ended May 31, 2018. Our Board of Directors authorized a stock repurchase program on July 10, 2017 providing for the repurchase of up to $250 million of our common stock with no expiration date. The remaining number of shares available for repurchase under that authorization is $237 million.

17

ITEM 6. SELECTED FINANCIAL DATA

(In millions, except per share amounts)

| |

For the Year Ended May 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||

RESULTS OF OPERATIONS1 |

||||||||||||||||

Sales |

$ | 1,748.3 | $ | 1,590.8 | $ | 1,525.4 | $ | 1,448.0 | $ | 1,415.5 | ||||||

Gross profit2 |

294.6 | 263.4 | 233.1 | 152.8 | 204.3 | |||||||||||

Operating income (loss)2 |

86.0 | 82.3 | 75.5 | (31.2 | ) | 53.8 | ||||||||||

Loss on extinguishment of debt3 |

— | — | (0.4 | ) | (44.9 | ) | — | |||||||||

Interest expense |

8.0 | 5.3 | 6.4 | 27.2 | 29.4 | |||||||||||

Income (Loss) from continuing operations |

73.7 | 52.0 | 45.5 | (67.4 | ) | 19.7 | ||||||||||

Income (Loss) from discontinued operations4 |

(58.1 | ) | 4.5 | 2.2 | 77.6 | 53.2 | ||||||||||

Net income |

15.6 | 56.5 | 47.7 | 10.2 | 72.9 | |||||||||||

Share data: |

||||||||||||||||

Earnings per share—basic: |

||||||||||||||||

Earnings (Loss) from continuing operations |

$ | 2.14 | $ | 1.53 | $ | 1.30 | $ | (1.73 | ) | $ | 0.50 | |||||

Earnings (Loss) from discontinued operations |

(1.70 | ) | 0.13 | 0.07 | 1.99 | 1.35 | ||||||||||

| | | | | | | | | | | | | | | | | |

Earnings per share—basic |

$ | 0.44 | $ | 1.66 | $ | 1.37 | $ | 0.26 | $ | 1.85 | ||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Earnings per share—diluted: |

||||||||||||||||

Earnings (Loss) from continuing operations |

$ | 2.11 | $ | 1.51 | $ | 1.30 | $ | (1.73 | ) | $ | 0.49 | |||||

Earnings (Loss) from discontinued operations |

(1.70 | ) | 0.13 | 0.07 | 1.97 | 1.34 | ||||||||||

| | | | | | | | | | | | | | | | | |

Earnings per share—diluted |

$ | 0.41 | $ | 1.64 | $ | 1.37 | $ | 0.24 | $ | 1.83 | ||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Cash dividends declared per share |

$ | 0.30 | $ | 0.30 | $ | 0.30 | $ | 0.30 | $ | 0.30 | ||||||

Weighted average common shares outstanding—basic |

34.2 | 33.9 | 34.4 | 39.1 | 38.6 | |||||||||||

Weighted average common shares outstanding—diluted |

34.6 | 34.3 | 34.6 | 39.4 | 39.1 | |||||||||||

| |

May 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||

FINANCIAL POSITION1 |

||||||||||||||||

Total cash and cash equivalents |

$ | 31.1 | $ | 10.3 | $ | 31.2 | $ | 54.7 | $ | 89.2 | ||||||

Working capital |

609.4 | 553.4 | 540.3 | 456.9 | 645.4 | |||||||||||

Total assets |

1,524.7 | 1,504.1 | 1,456.0 | 1,454.1 | 2,159.8 | |||||||||||

Total debt3 |

178.9 | 156.2 | 145.3 | 154.0 | 634.0 | |||||||||||

Equity5 |

936.3 | 914.2 | 865.8 | 845.1 | 1,000.7 | |||||||||||

Number of shares outstanding at end of year5 |

34.7 |

34.4 |

34.5 |

35.4 |

39.6 |

|||||||||||

Book value per share of common stock |

$ | 26.98 | $ | 26.58 | $ | 25.10 | $ | 23.87 | $ | 25.27 | ||||||

Notes:

- 1

- During

the third quarter of fiscal 2018, we decided to pursue the sale of our Contractor-Owned, Contractor-Operated ("COCO") business previously included

in our Expeditionary Services segment. The Results of Operations and Financial Position data has been recast to reflect the classification of our COCO business as a discontinued operation for all

periods presented.

- 2

- In fiscal 2015, we recognized $61.5 million in impairment charges and other losses related to product lines and inventories identified as underperforming or not part of our strategy going forward. These actions included aircraft in our aircraft lease portfolio and inventory in our supply chain and MRO

18

operations. We also recognized impairment charges of $25.6 million related to our composite manufacturing operations.

- 3

- In

fiscal 2015, we redeemed our $325 million 7.25% Senior Notes due 2022 for $370.6 million. We recognized a loss on extinguishment of debt

of $44.9 million comprised of a make-whole premium of $45.6 million and unamortized deferred financing costs of $6.2 million, partially offset by an unamortized net premium of

$6.9 million.

- 4

- In fiscal 2015, we sold our Telair Cargo Group for $725 million resulting in a $198.6 million pre-tax gain. We also recognized impairment charges of $31.9 million in fiscal 2015 to reduce the carrying value of our metal machining business's net assets to their expected value at the time of sale.

In fiscal 2016, we received contingent consideration from the sale of Telair Cargo Group and recognized a pre-tax gain of $27.7 million.

In fiscal 2018, we recognized asset impairment charges of $64.0 million related to our COCO business.

- 5

- On May 29, 2015, we repurchased 4,185,960 shares of our common stock at a price of $31.90 per share pursuant to a tender offer utilizing $133.5 million cash on hand. Fees and expenses of $1.2 million were incurred related to the tender offer and were recorded in treasury stock.

19

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

(Dollars in millions)

Forward-Looking Statements

Management's Discussion and Analysis of Financial Condition and Results of Operations contain certain statements relating to future results, which are forward-looking statements as that term is defined in the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on the beliefs of management, as well as assumptions and estimates based on information available to us as of the dates such assumptions and estimates are made, and are subject to certain risks and uncertainties that could cause actual results to differ materially from those anticipated, depending on a variety of factors, including those factors discussed under Item 1A, "Risk Factors." Should one or more of those risks or uncertainties materialize adversely, or should underlying assumptions or estimates prove incorrect, actual results may vary materially from those described. Those events and uncertainties are difficult or impossible to predict accurately and many are beyond our control. We assume no obligation to update any forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

General Overview

We report our activities in two business segments: Aviation Services comprised of supply chain and maintenance, repair and overhaul ("MRO") activities and Expeditionary Services comprised of airlift and mobility activities.

The Aviation Services segment consists of aftermarket support and services businesses that provide spares and maintenance support for aircraft operated by our commercial and government/defense customers. Sales in the Aviation Services segment are derived from the sale and lease of a wide variety of new, overhauled and repaired engine and airframe parts and components and aircraft to the commercial aviation and government and defense markets. We provide customized inventory supply chain management, performance based logistics programs, aircraft component repair management services, and aircraft modifications. The segment also includes MRO of aircraft, landing gear and components. Cost of sales consists principally of the cost of product, direct labor, and overhead.

The Expeditionary Services segment consists of businesses that provide products and services supporting the movement of equipment and personnel by the U.S. and foreign governments and other non-governmental organizations. Sales in the Expeditionary Services segment are derived from fleet management and operations of customer-owned aircraft and the design and manufacture of pallets, shelters, and containers used to support the U.S. military's requirements for a mobile and agile force. We also design and manufacture advanced composite materials for commercial, business and military aircraft. Cost of sales consists principally of the cost of material to manufacture products, direct labor and overhead.

Our chief operating decision making officer (Chief Executive Officer) evaluates performance based on the reportable segments and utilizes gross profit as a primary profitability measure. Gross profit is calculated by subtracting cost of sales from sales. The assets and certain expenses related to corporate activities are not allocated to the segments. Our reportable segments are aligned principally around differences in products and services.

Beginning in fiscal 2015, we implemented a comprehensive strategic plan to narrow our strategy to focus on our best-in-class aviation and expeditionary services through our two business segments: Aviation Services and Expeditionary Services. We sold our Telair Cargo Group for cash of $714 million, resulting in pre-tax gains of $198.6 million in the fourth quarter of fiscal 2015 (and $27.7 million in the first quarter of fiscal 2016 from the receipt of contingent consideration). We used the proceeds from the sale in fiscal 2015

20

to reduce our total debt and return capital to shareholders through common stock repurchases and dividends.

Through execution of our strategic plan over the last three years, we have succeeded in expanding customer relationships and securing new flight hour component inventory management and repair programs work with multiple international commercial customers and government customers. We also invested in our rotable assets to support these programs and continued our focus on expanding our business development resources. These investments in our supply chain activities have allowed us to increase market share, expand our customer base, and enlarge our geographic footprint.

In fiscal 2018, we began the ramp-up for the 15-year, U.S. Air Force Landing Gear Performance-Based Logistics One program. Under the program, we are providing total supply chain management including purchasing, distribution and inventory control to support all landing gear components for the U.S. Air Force's fleet of C-130, KC-135 and E-3 aircraft.

In fiscal 2018, we also began providing services to the U.S. Department of State ("DoS") under the INL/A Worldwide Aviation Support Services ("WASS") contract. This contract leverages our capabilities in aviation services, including flight operations, supply chain logistics, and other services. We are the prime contractor on this 10-year performance-based contract to globally operate and maintain the DoS fleet of fixed and rotary-wing aircraft. We successfully completed the transition and phase-in of the WASS program in June 2018. We have full operational capability at all contract sites, which include Afghanistan, Iraq, Panama, Peru, and Patrick Air Force Base as well as support locations in Brevard County, Florida.

Our long-term strategy continues to emphasize the return of capital to shareholders. Over the past three years, we have returned $82.6 million to shareholders through common stock repurchases of $51.7 million and dividends of $30.9 million.

Business Trends and Outlook for Fiscal 2019

Consolidated sales for fiscal 2018 increased $157.5 million or 9.9% compared to the prior year primarily due to an increase in sales of $133.5 million or 9.0% in our Aviation Services segment. This increase was driven by strong growth in our aviation supply chain activities including our recent contract awards for component inventory management and repair programs for commercial and government customers. This growth was partially offset by the impact from the wind-down of our KC-10 program. Our principal services under the KC-10 program were completed in January 2017 with the wind-down completed in fiscal 2018. Sales for the KC-10 program during fiscal 2017 were $110.6 million compared to $29.1 million in fiscal 2018. Sales in the Expeditionary Services segment increased $24.0 million or 22.8% over the prior year primarily due to the start of our services on the WASS program on November 1, 2017.

For fiscal 2019, we expect to see continued strength in our Aviation Services segment given its leadership positions in value-added services to both commercial and government and defense customers. Long-term aftermarket growth trends are favorable and our comprehensive suite of integrated services will continue to drive growth across our diverse base of customers.

We remain in a strong financial position to further execute on our strategy in fiscal 2019. Both our commercial and government businesses are executing on our many contract wins and will continue to deliver growth in fiscal 2019. Our cash on hand plus unused capacities on our Revolving Credit Facility and accounts receivable financing program was $473 million at May 31, 2018. We expect to invest opportunistically in expanding our comprehensive suite of services to the global commercial aviation and government and defense markets. We continue to have the flexibility in our balance sheet to invest in our growth. As we generate positive cash flow, we will continue our strategy of returning capital to our shareholders without hampering our future operating flexibility and our growth plans.

21

For fiscal 2019, we expect the Company's consolidated sales in the range of $2.1 to $2.2 billion. Diluted earnings per share from continuing operations for fiscal 2019 is expected to be in the range of $2.50 to $2.80.

Results of Operations—Fiscal 2018 Compared with Fiscal 2017

Sales and gross profit for our two business segments for the two years ended May 31, 2018 and 2017 were as follows:

| |

For the Year Ended May 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2018 | 2017 | % Change | |||||||

Sales: |

||||||||||

Aviation Services |

||||||||||

Commercial |

$ | 1,281.9 | $ | 1,114.9 | 15.0 | % | ||||

Government and Defense |

337.0 | 370.5 | (9.0 | )% | ||||||

| | | | | | | | | | | |

|

$ | 1,618.9 | $ | 1,485.4 | 9.0 | % | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Expeditionary Services |

||||||||||

Commercial |

$ | 37.5 | $ | 37.1 | 1.1 | % | ||||

Government and Defense |

91.9 | 68.3 | 34.6 | % | ||||||

| | | | | | | | | | | |

|

$ | 129.4 | $ | 105.4 | 22.8 | % | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| |

For the Year Ended May 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2018 | 2017 | % Change | |||||||

Gross Profit: |

||||||||||

Aviation Services |

||||||||||

Commercial |

$ | 203.8 | $ | 183.1 | 11.3 | % | ||||

Government and Defense |

68.1 | 62.9 | 8.3 | % | ||||||

| | | | | | | | | | | |

|

$ | 271.9 | $ | 246.0 | 10.5 | % | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Expeditionary Services |

||||||||||

Commercial |

$ | 8.3 | $ | 8.2 | 1.2 | % | ||||

Government and Defense |

14.4 | 9.2 | 56.5 | % | ||||||

| | | | | | | | | | | |

|

$ | 22.7 | $ | 17.4 | 30.5 | % | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Aviation Services Segment

Sales in the Aviation Services segment increased $133.5 million or 9.0% over the prior year due to a $167.0 million or 15.0% increase in sales to commercial customers. The increase in sales to commercial customers was primarily attributable to higher volumes in aviation supply chain activities driven by new contract awards.

During fiscal 2018, sales in this segment to government and defense customers decreased $33.5 million or 9.0% from the prior year. The decrease was primarily due to the wind-down of our KC-10 program.

Changes in estimates and assumptions related to our programs accounted for using the percentage-of-completion method are recorded using the cumulative catch-up method of accounting. In fiscal 2018, we recognized favorable and unfavorable cumulative catch-up adjustments of $11.6 million and $8.0 million, respectively, compared to favorable and unfavorable cumulative catch-up adjustments of $9.2 million and $0.7 million, respectively, in fiscal 2017. When considering these adjustments on a net

22

basis, we recognized favorable cumulative catch-up adjustments of $3.6 million and $8.5 million for fiscal 2018 and 2017, respectively. These adjustments primarily relate to our long-term, power-by-the-hour programs where we provide component inventory management and repair services.

Cost of sales in Aviation Services increased $107.6 million or 8.7% over the prior year which was in line with the sales increase discussed above. Gross profit in the Aviation Services segment increased $25.9 million or 10.5% over the prior year. Gross profit on sales to commercial customers increased $20.7 million or 11.3% over the prior year primarily driven by the higher volumes in aviation supply chain activities. The gross profit margin on sales to commercial customers was 15.9% compared to 16.4% in the prior year and was largely attributable to labor challenges at our airframe maintenance hangars.

Gross profit in this segment on sales to government and defense customers increased $5.2 million or 8.3% from the prior year primarily driven by improved profitability on new contract awards. The gross profit margin increased from 17.0% to 20.2% primarily due to these new contract awards.

Expeditionary Services Segment

Sales in the Expeditionary Services segment increased $24.0 million or 22.8% over the prior year primarily due to the start of our services on the WASS program on November 1, 2017. Gross profit in the Expeditionary Services segment increased $5.3 million over the prior year due to the addition of the WASS program in fiscal 2018.

Selling, General and Administrative Expenses

Selling, general and administrative expenses increased $27.5 million in fiscal 2018 or 15.2% from the prior year primarily attributable to supporting our sales growth, including increased personnel-related costs and business development activities.

Interest Expense