Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Senmiao Technology Ltd | tv497207_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Senmiao Technology Ltd | tv497207_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Senmiao Technology Ltd | tv497207_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - Senmiao Technology Ltd | tv497207_ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2018

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number: 001-38426

SENMIAO TECHNOLOGY LIMITED

(Exact name of registrant as specified in its charter)

| Nevada | 35-2600898 | |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

|

16F, Shihao Square, Middle Jiannan Blvd. High-Tech Zone, Chengdu Sichuan, People's Republic of China |

610000 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number: +86 28 61554399

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class: | Name of Each Exchange on Which Registered: | |

| Common Stock, par value $0.0001 per share | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer ¨ | Smaller reporting company x |

| Emerging growth company x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of September 29, 2017, the last business day of the registrant's most recently completed second fiscal quarter, there was no established public market for the registrant’s common stock and, therefore, the registrant cannot calculate the aggregate market value of its voting and non-voting common stock held by non-affiliates as of such date. The aggregate market value of the voting and non-voting common stock held by non-affiliates computed by reference to the price at which the common stock was last sold as of June 28, 2018, was approximately $78,424,525. Common stock held by each officer and director and by each person known to the registrant who owned 10% or more of the outstanding voting and non-voting common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of June 28, 2018, there were 25,879,400 shares of common stock, par value $0.0001 per share, of the registrant issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

If the following documents are incorporated by reference, briefly describe them and identify the part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (i) any annual report to security holders; (ii) any proxy or information statement; and (iii) any prospectus filed pursuant to Rule 424(b) or (c) of the Securities Act of 1933 (the "Securities Act"). The listed documents should be clearly described for identification purposes (e.g. annual reports to security holders for fiscal year ended December 24, 1980): None

SENMIAO TECHNOLOGY LIMITED

TABLE OF CONTENTS

| 2 |

Unless otherwise stated in this Annual Report on Form 10-K ("Report"), references to:

| · | "APR" or "annual percentage rate" refers to the annual interest rate that is charged to borrowers, expressed as a single percentage number that represents the actual yearly cost of funds over the term of a loan. |

| · | "China" or the "PRC" refers to the People's Republic of China, excluding, for the purposes of this Report only, Hong Kong, Macau and Taiwan; |

| · | "Restructuring" refers to the establishment of a WFOE and the execution of a series of agreements among the Company, WFOE, Sichuan Senmiao and the equity holders of Sichuan Senmiao, pursuant to which the we have gained control of and become the primary beneficiary to Sichuan Senmiao; |

| · | "RMB" and "Renminbi" refer to the legal currency of China; |

| · | "Sichuan Senmiao" refers to Sichuan Senmiao Ronglian Technology Co., Ltd., our variable interest entity; |

| · | "Senmiao," "we," "us," "our company" and "our" refer to Senmiao Technology Limited., its subsidiary and its consolidated variable interest entity; |

| · | "Senmiao Consulting" and "WFOE" refer to Sichuan Senmiao Zecheng Business Consulting Co., Ltd., our wholly owned subsidiary in China; |

| · | "US$," "U.S. dollars," "$," and "dollars" refer to the legal currency of the United States. |

We use U.S. dollars as reporting currency in our financial statements and in this Report. Monetary assets and liabilities denominated in Renminbi are translated into U.S. dollars at the rates of exchange as of the balance sheet date, equity accounts are translated at historical exchange rates, and revenues, expenses, gains and losses are translated using the average rate for the period. In other parts of this Report, any Renminbi denominated amounts are accompanied by translations. With respect to amounts not recorded in our consolidated financial statements included elsewhere in this Report, all translations from Renminbi to U.S. dollars were made at RMB 6.5027 to US$1.00, the noon buying rate set forth in the H.10 statistical release of the Federal Reserve Board on June 22, 2018. We make no representation that the Renminbi or U.S. dollar amounts referred to in this Report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all. The PRC government restricts or prohibits the conversion of Renminbi into foreign currency and foreign currency into Renminbi for certain types of transactions.

| 3 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report, including, without limitation, statements under the heading "Management's Discussion and Analysis of Financial Condition and Results of Operations," includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements can be identified by the use of forward-looking terminology, including the words "believes," "estimates," "anticipates," "expects," "intends," "plans," "may," "will," "potential," "projects," "predicts," "continues," or "should," or, in each case, their negative or other variations or comparable terminology. There can be no assurance that actual results will not materially differ from expectations. Such statements include, but are not limited to, any statements relating to our ability to consummate any acquisition or other business combination and any other statements that are not statements of current or historical facts. These statements are based on management's current expectations, but actual results may differ materially due to various factors, including, but not limited to:

| · | our goals and strategies; |

| · | our future business development, financial condition and results of operations; |

| · | the expected growth of the credit industry, and marketplace lending in particular, in China; |

| · | our expectations regarding demand for and market acceptance of our platform's products and services; |

| · | our expectations regarding our platform's user base; |

| · | our plans to invest in our platform; |

| · | our relationships with our partners; |

| · | competition in our industry; and |

| · | relevant government policies and regulations relating to our industry. |

The forward-looking statements contained in this Report are based on our current expectations and beliefs concerning future developments and their potential effects on us. Future developments affecting us may not be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) and other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading "Risk Factors." Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws. These risks and others described under "Risk Factors" may not be exhaustive.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and developments in the industry in which we operate may differ materially from those made in or suggested by the forward-looking statements contained in this Report. In addition, even if our results or operations, financial condition and liquidity, and developments in the industry in which we operate are consistent with the forward-looking statements contained in this Report, those results or developments may not be indicative of results or developments in subsequent periods.

| 4 |

| Item 1. | Business |

Overview

We are an online lending platform in China connecting Chinese investors with individual and small-to-medium-sized enterprise ("SME") borrowers. Through our platform, we offer quick and easy access to credit to borrowers and attractive investment returns for investors. Since the acquisition of our platform in September 2016, which is more fully described below, through March 31, 2018, we have facilitated loans (including assigned loans) with an aggregate of principal of over RMB 579 million (approximately US$89 million). As of March 31, 2018, we had a total of 3,372 investors, 2,558 borrowers and two creditor partners had participated in loan transactions through our platform. We currently conduct our business operations exclusively in China, and all of our investors and borrowers are located in China.

Our online platform enables us to efficiently match borrowers with investors and execute loan transactions. We seek to address an unmet investor and borrower demand in China. While presently our borrowers mainly come from referrals from financial institutions and business partners, our investors come from a variety of channels, including internet and our mobile applications, promotion through our own business development department as well as referrals from our business partners.

As of March 31, 2018, we had an aggregate of 40,044 registered users. We interact with registered users of our platform on a regular basis. We post articles of third parties related to investment and wealth management on our platform for our registered users. Information in these materials may potentially be used by registered users on our platform for their investment decisions, including investment in loans posted on our platform. All registered users of our platform have access to loans posted on our platform and can forward the loan posting to individuals in their network. Any of these users and their connections can invest in loans posted on our website if they are willing to.

Historically, we offered two types of products: standard loans and assignment of loans, providing qualified borrowers with convenient access to affordable credit at competitive prices and creditors with a fast and cost-efficient way to assign their existing loans for more liquidity. Our investors have the option to individually select specific loans to invest in or to use our automated investing tool that identifies and selects loans on the basis of an investor targeted return and risk tolerance.

All our loans currently facilitated on our platform are unsecured, feature fixed interest rate and have terms ranging from one to 36 months. We generate revenues primarily from fees charged for facilitating loan transactions on our platform. We charge borrowers transaction fees based on the loan amounts for services provided through our platform. Our current transaction fees range from 4.14% to 6.14% of the loan amount for borrowers. The transaction fees are paid (i) upon disbursement of the proceeds for loans accruing interest on a monthly basis and (ii) upon full payment of principal and interest of loans accruing interest on a daily basis. We also charge our investors a service fee of 8.00% of their actual investment return and the service fee is paid when the investors receive their interest payment.

| 5 |

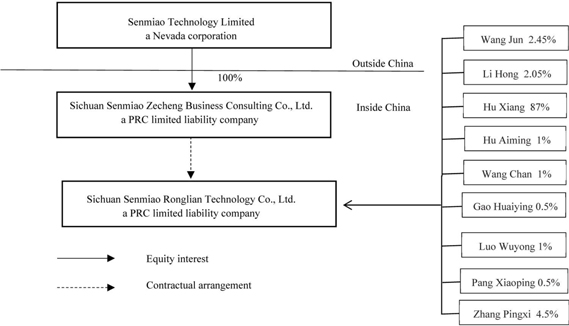

Our Corporate History and Structure

We were incorporated in the State of Nevada on June 8, 2017. We have established a wholly owned subsidiary, Sichuan Senmiao Zecheng Business Consulting Co., Ltd. ("WFOE," or "Senmiao Consulting") in China. Substantially all of our business activities are undertaken by WFOE and a variable interest entity ("VIE"), Sichuan Senmiao Ronglian Technology Co., Ltd. ("Sichuan Senmiao") in China. As of the date of this Report, the WFOE only provides services to Sichuan Senmiao, our VIE entity, pursuant to our VIE agreements. We anticipate that the WFOE will conduct a major portion of our research, development and marketing activities.

Sichuan Senmiao was established in China in June 2014. The equity interest of Sichuan Senmiao is owned by 9 individuals in the PRC (see the corporate structure diagram below for details). As of February 26, 2018, purchase price for all equity transfers has been fully paid and the transfers have been completed. We have entered into a series of contractual arrangements with Sichuan Senmiao and each of its equity holders through WFOE to obtain control and become the primary beneficiary of Sichuan Senmiao. The contractual arrangements have been in place since the establishment of WFOE (the "Restructuring").

On September 25, 2016, Sichuan Senmiao acquired a peer-to-peer platform (including website, internet content provider ("ICP") registration, operating systems, servers, management system, employees and users) (the “Aihongsen platform”) from Sichuan Chenghexin Investment and Asset Management Co., Ltd. ("Chenghexin"), who had established and operated the platform for two years prior to our acquisition (the "Acquisition"), for an initial payment of RMB 60 million (approximately US$8.9 million) with the remaining payment to be confirmed upon completion of an appraisal of the platform. On March 26, 2017, the parties signed a supplement agreement to the purchase agreement whereby they confirmed the remaining payment based on the appraisal report. We paid a total cash consideration of RMB 69,690,000 (approximately US$10.1 million) for the platform.

Prior to the Acquisition, Sichuan Senmiao was a holding company that owned a 60% equity interest in an equity investment fund management company. Sichuan Senmiao sold its 60% equity interest for a cash consideration of RMB 60 million (approximately US$8.9 million) immediately following the Acquisition, in order to focus on the online marketplace lending business.

The following diagram illustrates our corporate structure, including our subsidiary and consolidated variable interest entity as of the date of this Report:

Contractual Arrangements with Sichuan Senmiao

Due to PRC legal restrictions on foreign ownership and investment in value-added telecommunications services, and internet content provision services in particular, we currently conduct these activities through Sichuan Senmiao, which we effectively control through a series of contractual arrangements as follows:

| 6 |

| • | Equity Interest Pledge Agreement. The WFOE, Sichuan Senmiao and all of the Sichuan Senmiao equity holders ("Sichuan Senmiao Shareholders") entered into an Equity Interest Pledge Agreement, pursuant to which Sichuan Senmiao Shareholders pledged all of their equity interest in Sichuan Senmiao to WFOE in order to guarantee the performance of Sichuan Senmiao's obligations under the Exclusive Business Cooperation Agreement as described below. During the term of the pledge, WFOE is entitled to receiving any dividends declared on the pledged equity interest of Sichuan Senmiao. The Equity Interest Pledge Agreement ends when all contractual obligations under the Exclusive Business Cooperation Agreement have been fully performed. |

| • | Exclusive Business Cooperation Agreement. Pursuant to an Exclusive Business Cooperation Agreement by and among the Company, WFOE, Sichuan Senmiao and each of the Sichuan Senmiao Shareholders, WFOE will provide Sichuan Senmiao with complete technical support, business support and related consulting services during the term of the agreement. The Sichuan Senmiao Shareholders and Sichuan Senmiao have agreed not to engage any other party for the same or similar consultation services without WFOE's prior consent. Further, Sichuan Senmiao Shareholders are entitled to receive an aggregate of 20,250,000 shares of common stock of the Company under the Exclusive Business Cooperation Agreement. The term of the Exclusive Business Cooperation Agreement is ten years from September 18, 2017. The WFOE may terminate the Exclusive Business Operation Agreement at any time upon prior written notice to Sichuan Senmiao and the Sichuan Senmiao Shareholders. |

| • | Exclusive Option Agreement. Pursuant to an Exclusive Option Agreement by and among the WFOE, Sichuan Senmiao and each of the Sichuan Senmiao Shareholders, the Sichuan Senmiao Shareholders have granted WFOE an exclusive option to purchase at any time in part or in whole their equity interests in Sichuan Senmiao for a purchase price equal to the capital paid by the Senmiao Shareholders, pro-rated for purchase of less than all the equity interest. The Exclusive Option Agreement terminates in ten years from September 18, 2017 but can be renewed by WOFE at its discretion. |

| • | Powers of Attorney. Each of the Sichuan Senmiao Shareholders has entered into a power of attorney (the "Power of Attorney") pursuant to which each of the Sichuan Senmiao Shareholders has authorized the WFOE to act on his or her behalf as the exclusive agent and attorney with respect to all rights of such individual as a shareholder, including but not limited to: (a) attending shareholders' meetings; (b) exercising all the shareholder's rights, including voting, that shareholders are entitled to under PRC law and the Articles of Association of Sichuan Senmiao, including but not limited to the sale or transfer or pledge or disposition of the equity interests of Sichuan Senmiao owned by such shareholder; and (c) designating and appointing on behalf of the shareholders the legal representative, chairperson, director, supervisor, chief executive officer and other senior management members of Sichuan Senmiao. The Power of Attorney has the same term of the Exclusive Option Agreement. |

| • | Timely Report Agreement. The Company and Sichuan Senmiao entered into a timely report agreement pursuant to which Sichuan Senmiao agrees to make its officers and directors available to the Company and promptly provide all information required by the Company so that the Company can make necessary SEC and other regulatory reports in a timely fashion. |

Our Industry

Consumption in China is growing rapidly but remains underfinanced, suggesting significant growth potential for China's consumer finance market.

Consumption in China has experienced rapid growth as a result of China's economic development and rising consumption power among Chinese consumers. According to the World Bank, China's GDP increased from US$7.6 trillion in 2011 to US$10.1 trillion in 2015, while annual per capita disposable income increased from US$5,634 in 2011 to US$8,069 in 2015. Consumption has increasingly become an important driver of China's GDP growth, with the ratio of final consumption to GDP reaching 51.1% in 2015, according to the National Bureau of Statistics of China. "Final consumption" is the total expenditure of residents on the consumption of goods and services in a certain period, namely the expenditure of residents for purchases of goods and services from the domestic economic territory and abroad to meet the requirements of their daily life, and excludes the expenditure of non-residents on consumption in the economic territory of the country. While China's ratio of final consumption to GDP in 2015 was 51.1%, it was still relatively low compared to the corresponding figure for the U.S. in the same period, which was 82.5% according to the World Bank, suggesting tremendous future potential. We believe the United States, which is characterized by high levels of consumption and high consumption loan balance to GDP ratios, provides a good proxy for the way China may develop given the growth of China's economy, China's large and expanding consumer base and the Chinese government's policies to encourage consumption. As consumption in China continues to rise, we believe China's consumer finance market will develop to address unmet consumer demand.

| 7 |

China's Consumer Finance Market

Despite growing consumption levels, consumption in China is underfinanced primarily because loans from traditional financial institutions are not easily accessible. For example, to obtain a bank loan, a potential borrower needs to physically go to a bank branch. However, most bank branches offering consumption loans are located only in tier 1 and tier 2 cities such as Beijing, Shanghai and Guangzhou. In addition, the application process for a bank loan is complex and time-consuming. The perceived ineffectiveness of traditional financial institutions at serving the consumer finance market potentially suggests business opportunities for alternative credit providers. According to iResearch Consulting Group, a market research and marking company in China ("iResearch"), China's consumption loan exceeded RMB 22 trillion (approximately US$3.4 trillion) in 2016 and is expected to further grow to RMB 40.1 trillion (approximately US$6.2 trillion) by 2020. The development of new financial services and products will be one of the key growth drivers.

The consumer finance market consists of secured consumption loans such as car loans and home mortgages, and unsecured consumption loans such as credit cards and other unsecured loans from banks and consumer financing companies. China's credit balance in 2015 was RMB 93.6 trillion (approximately US$14.4 trillion), representing an increase of 14.9% from the prior year. Unsecured consumption loans are expected to exhibit relatively stronger growth. According to a report issued by iResearch, China's consumption loan balance had reached RMB 19 trillion (approximately US$2.9 trillion) by the end of 2015, and is expected to reach RMB 41.1 trillion (approximately US$6.3 trillion) by the end of 2019. Key drivers behind the expected growth in China's unsecured consumer finance market include the penetration of consumer finance into more consumption categories, the continued development of a nationwide personal credit information database, which improves the ability of lenders to evaluate potential borrower risk, and credit providers' increasing awareness of the business opportunity in the sector.

Opportunities for Marketplaces Connecting Borrowers and Investors

We believe China's rapidly growing consumption levels and relatively limited consumer finance options have created opportunities for marketplaces that connect borrowers and investors. According to iResearch, transaction values for marketplaces that focus on consumption loans, or consumer finance marketplaces, are expected to grow from RMB 436.7 billion (approximately US$522.9 billion) in 2016 to RMB 3.4 trillion (approximately US$67.2 billion) in 2019, representing a compound annual growth rate of 98.2%. The primary drivers for the growth of consumer finance marketplaces include the growing consumption market and increasing demand for consumer finance. In addition, it is also driven by consumers' need for higher borrowing limits and convenient transaction processing, and improved credit assessment capabilities made possible through the application of big data analytics.

Additional drivers for the growth of online consumer finance marketplaces include increased internet and mobile penetration among consumers, the emergence of online marketplaces and ecommerce platforms that drive consumer behavior from offline to online, as well as the ability to realize comparatively lower user acquisition costs and higher operating efficiencies.

Recent Developments in the Peer-to-Peer Lending Industry

The online lending marketplace industry in China is intensely competitive and we compete with many other peer-to-peer marketplaces. According to the China Peer-to-Peer Industry Report for 2016 (the "P2P Report") issued by Lingyi Research Center, an independent research institution, there were approximately 4,856 peer-to-peer lending marketplaces in China as of December 2016. The number of platforms increased to 5,229 as of July 2017. In light of the low barriers to entry in the peer-to-peer lending industry in China, we expect more players to enter this market and increase the level of competition.

Despite the continuous increase of the number of lending platforms, the peer-to-peer lending market in China has been subject to risky lending practices (such as over-leveraging) and platform failures. According to the P2P Report, as of December 2016, 3,201 platforms (or 65.9%) had the above referenced issues, 21 of which were located in Sichuan. Among these problematic platforms, 433 platforms (or 39.2%) closed and 395 platform (or 35.7%) suspended their operations.

| 8 |

In response to the ongoing platform failures and continuous risky lending practices, the PRC government has increased its regulation of peer-to-peer lending since 2015. The most significant regulation is the Interim Measures for the Administration of Business Activities of Online Lending Information Intermediaries (the "Interim Measures"). The Interim Measures set forth the upper limit for borrowing amounts of individuals and entities from one platform and the upper limit for aggregate borrowing amounts of each type of these borrowers from all peer-to-peer lending platforms within one year. Recent regulatory developments have facilitated operational adjustments that we expect will improve lending practices on peer-to-peer platforms in China. In order to comply with the Interim Measures, peer-to-peer lending companies are adjusting various aspects of their operations, including loans offered on their platforms and risk management programs. One of the significant trends since the Interim Measures became effective is the transition to smaller loans. The Interim Measures also require lending platforms to use banks as custodian. As a result, lending platforms are switching to bank custodians. According to Lingyi Research Center, as of December 2016, 227 platforms signed depository agreements with custodian banks.

In light of the increased regulations, the number of peer-to-peer lending platforms entering the market has been decreasing since mid-2016. According to Lingyi Research Center, approximately 38 lending platforms entered into the market in July 2016 and the number decreased to 8 in December 2016. For more information on regulations on marketplace lending, see "Business – Regulations" and "Risk Factors."

Our Platform

Our platform capitalizes on opportunities presented by a financial system that leaves many creditworthy individuals and businesses underserved or even unserved. Our online business platform allows us to efficiently match borrowers with investors. We provide borrowers with convenient access to financing at competitive rates, while we offer investors attractive returns. Our platform provides the following benefits to borrowers, creditors and investors:

Benefits to Borrowers

We believe our platform provides the following benefits to our borrowers:

| • | Easy access to credit or more liquidity. We believe borrowers are significantly underserved by the current consumer finance system in China, which provides insufficient or, in some cases, no access to funds at all. We provide borrowers with access to loans based on borrower's risk profile and credit history. The principal amount of loans facilitated on our platform generally range from RMB 10,000 (approximately US$1,538) to RMB 1,000,000 (approximately US$153,782). |

| • | Quick and convenient access. We provide borrowers with an online loan application and management platform that can be accessed anytime and anywhere through our website and mobile applications. We also provide borrowers with access to live support and easy-to-use online tools throughout the application process and for the lifetime of the loan including a 24/7 customer service hotline and web chat. |

| • | Fast credit approval. We provide borrowers with faster decisioning compared to traditional sources of consumer financing in China, which may take weeks to provide a decision on a loan application. We generally notify qualified borrowers with completed documentation of our decision within a day. |

| • | Competitive rates and payments. We offer borrowers competitive interest rates as compared with the rates charged by our competitors. During the year ended March 31, 2018, qualified borrowers paid an average interest rate of approximately 7.57% on an APR basis. |

| • | Transparent marketplace. We offer borrowers a transparent application process with foreseeable turnaround times and clear documentation requirements. All of the loans facilitated through our platform feature fixed interest rates, which together with service fees and late payment penalties, are clearly disclosed to borrowers during the application process. |

| 9 |

Benefits to Investors

We believe our platform provides the following benefits to our investors:

| • | Access to a new asset class. We provide investors seeking funding opportunities with access to an investment opportunity that is outside the traditional and limited investment channels available to investors in China. We offer investors the ability to invest as little as RMB 100 (approximately US$15.4), allowing the investors to invest in diversified portfolio of loans. |

| • | Attractive returns. We offer investors attractive potential returns, which currently range from 7.07% to 9.94% on an annualized basis after fees, which is higher than traditional investment products such as bonds, treasurer bills, and certificates of deposit. Our risk management and credit screening capabilities help to improve the reliability of returns obtained through our platform. |

| • | Easy and quick access. We offer investors 24/7 access to all available services through our website and mobile applications. We provide investors with an online tool that automatically invests a specified amount of funds committed by the investor according to investor-specified criteria, including: investment amount, method of repayment, desired rate of return and tenure. We also provide a 24/7 customer service hotline and web chat to answer any additional questions that investors may have. |

| • | Investor protection. We focus on investor protection through all stages of a transaction including but not limited to implementing strict risk management measures to assess and verify borrowers' creditworthiness and monitoring payment status. With all these efforts, we have not had any defaulted loan or delinquencies since our inception. We also strive to follow good industry practices to protect our investors. For example, we have engaged Sichuan XW Bank Co., Ltd. ("XW Bank") for fund depository functions including settlement, accounting and safeguarding online lending capital and obtained the Level III Certification of Information System Security issued by the Ministry of Public Security (the "MPS"). |

Our Strengths

We believe the following competitive strengths contribute to our success and differentiate us from our competitors:

Fast growing online lending platform in Sichuan servicing direct selling industry

Our platform was one of the early online lending platforms in Sichuan province. From the Acquisition of our platform through March 31, 2018, our platform successfully facilitated loans (including loan assignments) between 2,089 investors, 2,406 borrowers and two creditors, representing an aggregate value of approximately RMB 579 million (approximately US$89 million). We are also leveraging our relationship with Resgreen Group, a direct selling company based in Changsha, China, with over a million members, to jointly promote our products and services to their business partners and members. We are aiming to position ourselves as a leading online consumer finance platform for the direct selling industry in the PRC. We believe our scale, brand, risk management capabilities and technology platform allow us to effectively attract new participants, lower costs for our users, provide high-quality loan investment opportunities, create higher liquidity and thus reinforce our market position. As of the date of this Report, there are approximately 35 lending platforms in Sichuan province. The Company's primary competitors in Sichuan include Sichuan Jinding Wealth Information Technology Co., Ltd. ("Jinding Wealth"), Koudai Network Services Co., Ltd., Chengdu Hongxue Jinxin Business Consulting Co., Ltd. and Chengdu Zhongke E-Commerce Co., Ltd. Although some of these companies, such as Jinding Wealth, are established lending platforms with large and existing borrower and investor bases as well as substantial financial resources, compared to these lending platforms, we believe that our sophisticated custodian system and compatibility with current PRC regulations will make us more attractive to both borrowers and investors. Based on information available on the websites of our competitors as well as www.wdzj.com, an independent third party website that focuses on the P2P lending industry in China, we believe we are the first non-state owned lending platform in Sichuan that has established a custodian system with a depository bank pursuant to the requirements of applicable PRC regulations. We set up our custodian system in February of 2017 while most of our competitors were either negotiating their agreements with custodian banks or were (or remain) in the process of transitioning to the custodian system operated by their depository banks. In addition, loan transactions on our platform comply with restrictions on aggregate loan amounts for individual borrowers and entities set forth in PRC regulations while our competitors are in the process of restructuring loans on their platforms to comply with such requirement.

| 10 |

Low investment thresholds

We attract investors with a minimum investment amount of RMB 100 (approximately US$15.4), which is lower than most of the traditional investment products, thereby providing investors with the flexibility to invest as much and as frequently through our platform as desired. A low minimum investment amount also enables investors to diversify their loan portfolio.

From the Acquisition to March 31, 2018, the average investment was approximately RMB 40,612 (approximately US$6,245) and the average number of loans in an investor's loan portfolio was 7.07.

Attractive user experience

We offer a superior user experience to our platform participants. We provide borrowers and creditors with quick and convenient access to credit at affordable and competitive rates through our online platform that is accessible anytime and anywhere online and through our mobile application. For the year ended March 31, 2018, we facilitated loans to 2,369 borrowers and loan assignments to two creditors through our platform.

We offer investors easy and quick access to an alternative asset class with attractive potential returns, as well as an attractive user experience. For the year ended March 31, 2018, 1,839 investors made investments through our platform with an average investment amount of approximately RMB 45,526 (approximately US$7,001) per investor. Of these investors, 73.01% were repeat users of our platform, defined as those investors who made two or more investments through our platform during the period.

Cost efficient user acquisition

We invest in developing relationships with direct selling companies because we believe that they are well positioned to introduce our platform to a very broad potential user base due to the nature of their business. We have partnered with Resgreen Group. Since March 2017 through March 31, 2018, we acquired approximately 22,654 new users through referrals from Resgreen Group, of which approximately 471 had invested through our platform while none of them had borrowed. With the increase in the number of new users from our partnership with Resgreen Group, we are able to effectively lower our user acquisition costs as compared to traditional user acquisition channels because we have been able to precisely market our platform to a large number of potential users with relevant low marketing expenses. Pursuant to our strategic cooperation agreement with Resgreen Group, we have the right to participate in all meetings Resgreen Group organizes for its members, at which we can promote our brand and services and attract Resgreen members. Once these Resgreen members become registered users of our platform, they can potentially become borrowers and investors on our platform. We have agreed to provide Resgreen members access to our platform where they can view investment opportunities and information related to wealth management posted on our platform. Resgreen has also agreed to provide to us information regarding their members, including members' basic information as well as sales and financial data of each member within the Resgreen direct sale network. We plan to develop targeted marketing strategies towards Resgreen members by analyzing such data. We have agreed to provide Resgreen Group our analysis of their members' information. Our business relationship with Resgreen Group is strategic rather than economic by its nature. Resgreen Group is not entitled to any fees when any of its members becomes a borrower or investor on our platform.

Comprehensive risk management system

Our risk management system enables us to evaluate potential borrowers in a market where reliable credit scores and borrower databases are still at early stage of development. Our system is built upon data accumulated through our operations, publicly available governmental data, and third-party credit sources. We supplement these data with manual verification and fraud prevention processes. We consistently upgrade our risk management model with new credit data and technologies. We believe our risk management is prudent, as evidenced by the performance of various loan vintages facilitated through our platform.

Experienced management team

We have a strong management team with many years of experience in consumer finance in China. Our chief executive officer, Ms. Xin Chen, played a key role in the establishment and operation of another peer-to-peer lending platform prior to joining Sichuan Senmiao. She also has over 20 years' of accounting and finance experience based on her managerial and executive positions at various investment and real estate companies. Our management members also have significant experience in the consumer lending industry spanning multiple areas of expertise, including loan origination, risk management, product development, third party payment and collection in China.

| 11 |

Our Users

Our Borrowers

We service both individuals and SME borrowers. We acquire our borrowers mostly through referrals from financial institutions such as banks, micro-lending companies and guarantee companies due to the differences between these institutions' operation model, product offering and targeted customer and our own. These institutions refer borrowers to us if they believe that our platform and loans offered on our platform better serve the borrowers' needs for financing. For example, guaranty companies are not allowed to extend loans, so they refer borrowers to us and they may serve as guarantors in such transactions for services fees, while banks in China focus on traditional large scale standardized loan products and they do not typically serve our targeted market. The borrowers they refer to us are generally looking for short-term financings below RMB 1,000,000 (approximately US$153,782) to fund their cash flow requirement. We are not obligated to pay any fees to any of these institutions and have not paid any referral fees as of the date of this Report. We also acquire borrowers through our own marketing efforts such as event promotions, online marketing, user meetings and sales support. For the year ended March 31, 2018, we have facilitated loans to over 2,369 borrowers with an aggregate principal amount of approximately RMB 529 million (approximately US$81.4 million).

Our Creditor Partners

Prior to 2018, our platform was also accessible to creditors ("Creditor Partners") who had extended loans to borrowers outside our platform ("Outside Loans"). We provided our Creditor Partners the ability to assign their creditor's rights under the Outside Loans to obtain interim financing before loan maturities.

We would review and evaluate a Creditor Partner's financial conditions and credit profiles and make a determination if they would meet our minimum requirements for listing the Outside Loans on our platform. We would re-evaluate these partners' credit status from time to time, usually on a monthly basis. Once the Creditor Partner was approved, we would categorize the partner's credit facility into one or more of the loan products and post their loans on our platform. Investors would then have access to information regarding the original borrower, the loans being assigned, the collateral or guaranty securing the loans and other details related to the assigned loans. Our Creditor Partners were required to repurchase the Outside Loans at the end of the assignment term.

The Creditor Partners had conducted their own due diligence on the original borrower's creditworthiness for the Outside Loans when they originally made these loans. Our risk control department also would conduct its own due diligence on the creditor's rights sought to be assigned and the original borrower's credit-worthiness, applying the same standards we use to review borrowers for direct loans. As part of this process, our risk control department would review the loan contract between the Creditor Partner and the original borrower to determine whether the original borrower had agreed to the proposed assignment of creditor's rights. We would then directly contact the original borrower to ensure that they had received notice of proposed assignment from the Creditor Partner.

When our Creditor Partners assigned Outside Loans to investors on our platform, all rights of the Creditor Partners were assigned to the investors. Borrowers under the Outside Loans would remain legally obligated to pay off the assigned Outside Loans. Existing guarantors of the Outside Loan would remain legally obligated to perform their obligations under the assigned loans. Neither we nor the Creditor Partner would have any obligation to repay the assigned loan or provide a payment guarantee.

For this service, we charged our Creditor Partners service fees ranging from 0.32%-0.94% of the assigned loan principal. For the year ended March 31, 2018, the term of assignment of the loans averaged 28 days and the size of the loans assigned on our platform during this period was $36,281 on average.

Each Creditor Partner had a maximum amount of outstanding loan assignments permitted on our platform ("Total Assignment Cap") that was approved by our loan assessment committee when we approved the Creditor Partner. The Total Assignment Cap was RMB 50 million (approximately US$7.7 million) for each of our Creditor Partners prior to our discontinuation of the assigned loan products.

| 12 |

We had two Creditor Partners prior to discontinuation of our loan assignment services — one is an automobile dealer that offers short-term financing to car purchasers and the other is engaged in providing loan services.

Starting in January 2018, we no longer offer the loan assignment services to our Creditor Partners in preparation for our record-filing under the newly promulgated regulations of the marketplace lending industry. For more information on these regulations, see " Regulations — Regulations Related to the Marketplace Lending Industry." All the balance of the assigned loans was paid in full during the year ended March 31, 2018 before the date we applied for our record-filing.

Our Investors

We accept investments from individual investors of all income levels. This large and rapidly growing sector of the Chinese investors is currently underserved by traditional investment products in China. We seek to attract individual investors because members of this demographic group are a significant untapped source of capital.

For the year ended March 31, 2018, 1,839 investors made investments totaling approximately RMB 529 million (approximately US$81.4 million) through our platform. During this period, average annual investment return for investors on our platform was 7.57%. As of March 31, 2018, we had over 3,372 investors on our platform.

Cooperation with Business Partners

With an aim to facilitate our record-filing with relevant authorities under Circular 57 (defined below) and the Interim Measures, we discontinued our loan assignment services for our Creditor Partners in January 2018.

However, in order to continue to utilize our relationships with prior creditors, whom we referred to as business partners due to change of business model, we signed cooperation agreements with them pursuant to which they would refer their customers with financing needs to our platform. Pursuant to the cooperation agreements, we sent our employees to the office of our business partners and such employees would collect and review loan application materials from our business partners' customers who would like to seek financing through out platform and verify their identity, credit and financial conditions based on our standards. Our business partners would also collect, review and assess loan application materials from their customers as part of their risk management process because they will provide guaranty for the loans their customers take through our platform.

Our business partners would pay for the transaction fees on behalf of their customers when the loans transactions of their customers are concluded. Specifically, the transaction fees for loans accruing interest on a monthly basis are paid upon disbursement of loan proceeds and the transaction fees for loans accruing interest on a daily basis are paid upon full payment of principal and interest. The transaction fees charged to the borrowers referred by business partners varied based on the amount of business our business partners refer to us and the default risk of borrowers referred, ranging from 0.30% to 2.98% of the loan amounts.

Our business partners as well as their affiliates would guarantee the payment of the loans. They are parties to the loan transaction documents and would be jointly and severally liable for the payment of the loans, including principal, interest, penalties, and other fees associated with collection of the loans. In addition, to further secure the loan transaction, we sometimes would require a business partner to provide a security deposit for each referred loan transaction. The security deposit would be used to pay back the investors when the referred borrower failed to pay principal and interest in time and the business partner would need to deposit additional funds to ensure sufficient funds at required level.

Each business partner had a maximum amount of loans referred permitted on our platform ("Total Referral Credit") that was approved by our loan assessment committee when we approved the business partner. The Total Referral Credit ranged from RMB 50 million (approximately US$7.7 million) to RMB 200 million (approximately US$30.8 million).

In February 2018, Sichuan province issued local guidelines on the rectification and acceptance of internet lending information intermediaries which require the guarantors for the loans facilitated by lending platforms to be guaranty institutions or insurance companies that hold professional guaranty qualifications. Our business partners who guaranteed the loans do not hold the guarantor qualifications. To comply with the local guidelines and also as part of our preparation for our record –filing under the new marketplace lending regulations and as requested by the local finance bureau in connection with their inspection of our operations, we ceased our cooperation with business partners in March 2018 and began to focus on facilitating loan transactions solely between borrowers and investors on our platform.

| 13 |

User Acquisition

We have adopted a sales and marketing strategy aimed at enhancing our profile in the marketplace lending industry and the credit industry as a whole. Our sales and marketing efforts have included event promotions, online marketing, user meetings and sales support. In addition, in order to increase our brand recognition among potential borrowers and investors, we have participated in industry or government organized forums and summits. Our recent borrower acquisition activities have primarily comprised of developing user base through our strategic alliance with Resgreen Group as well as identifying potential borrowers through online advertisement. In connection with our online marketing efforts, we have taken search engine optimization measures to increase our search index results on third-party search engines.

Our Products and Services

Products Offered to Borrowers

We facilitate fixed-rate loans to individual and SME borrowers who are in need of capital for business operations. Currently, the loans offered on our platform have a term ranging from 1 month to 36 months and are unsecured. Historically, the loans facilitated on our platform were secured either by real property, large tangible assets such as automobiles, or guaranteed by unaffiliated third parties. As described above, we ceased to offer loans secured by guarantors who do not hold guarantor qualifications in February 2018 following the issuance of local guidelines on the rectification and acceptance of online lending information intermediaries.

Pursuant to the requirement of the Interim Measures, we do not permit individual borrowers to hold loans with aggregated outstanding principal of more than RMB 200,000 (approximately US$30,756) or SME borrowers to hold loans with aggregated outstanding principal of more than RMB 1,000,000 (approximately US$153,782). Within the maximum loan amount permitted by applicable PRC regulations and the scope of our risk management policy, we allow borrowers to hold multiple loans that are facilitated through our platform at one time.

Direct loans facilitated on our platform range in the amount of RMB 10,000 (approximately US$1,538) to RMB 200,000 (US$30,756) for individual borrowers and RMB 23,900 (approximately US$3,675) to RMB 1,000,000 (approximately US$153,782) for SMEs. Our direct loans currently outstanding include loans of three months, six months and 36 months. The annual interest rate for direct loans averaged 7.57% for the year ended March 31, 2018.

For the year ended March 31, 2018, we facilitated loans to 2,369 borrowers through our platform and the total amount of funds loaned to borrowers through our platform was approximately RMB 529 million (approximately US$81.4 million).

The APRs for the term loans on our platform currently range from 7.68% to 10.8%. We also charge borrowers transaction fees for our services ranging from 4.14% to 6.14%. The transaction fee is charged as a percentage of the loan amount and is typically paid up-front at the time of the disbursement of loan proceeds for loans accruing interest on a monthly basis and upon full payment of principal and interest of loans accruing interest on a daily basis. We recognize revenues generated from transaction fees when the loan transactions are closed and invoices for such fees are issued. The interest rate and transaction fee represent the total cost of borrowing for borrowers. A penalty fee for late payment is imposed as a percentage of the amount past due and will be paid to the investors should a default occur. All fees are clearly disclosed to the borrowers. As of the date of this Report, we have not collected any penalty for late payment because there has not been any default or delinquencies since we acquired the Aihongsen platform.

We do not allow loan rollovers, i.e., the repayment of a loan using proceeds from a new loan. If an applicant has outstanding loans below the statutory limit, (i.e. RMB 200,000 for individuals and RMB 1,000,000 for enterprises), we would allow such applicant to borrow additional amounts provided that additional guaranty/collateral is provided and such application meets all the criteria for a new loan. The proceeds of a new loan cannot be used to pay off the prior loans of the same borrower.

Services Offered to Creditor Partners

We used to provide our Creditor Partners with a platform to assign their existing loans to meet their cash flow requirements. Starting January 2018, we discontinued the offering of assigned loan products on our platform to facilitate a smooth record-filing under Circular 57 (defined below) and the Interim Measures.

| 14 |

By the time we suspended our loan assignment services, an aggregate of 1,295 loans totaling approximately RMB 230 million (approximately US$35.4 million) were assigned to investors through our platform. We also charged fixed interest rate based on the term of the assignment of the loans. The APRs for the assigned loans on our platform ranged from 6.78% to 8.64%. Including interest, our total charge for Creditor Partners generally ranged from 12% to 18% of the loan amount. The interest and transaction fee were typically paid when assignment proceeds were disbursed but we sometimes allowed payment at the time the Creditor Partner repurchased the Outside Loans. We generally recognized revenues from Creditor Partners when the assignments were consummated.

Services Offered to Investors

Through our platform, investors have the opportunity to invest in a range of loan products with attractive returns. We provide our investors with an automated investing tool with which an investor can invest a specified amount of money to borrowers or previously our Creditor Partners through our platform for a specified period of time. Once an investor commits funds to invest, the funds are automatically allocated among approved borrowers. Our automated investing tool automatically reinvests investors' funds as long as there are sufficient funds in the investor's account, enabling investors to automatically reinvest without having to continually revisit our website or mobile application. Investors using our automated investing tool are allowed to withdraw their funds before a loan is fully subscribed. During the fiscal year ended March 31, 2018, over 70% of the funds invested by investors through our platform were invested utilizing this automated investing tool.

The minimum threshold for a lending commitment made through our automated investing tool is RMB 100 (approximately US$15.4). For the year ended March 31, 2018, the average amount invested through our automated investing tool by each investor was approximately RMB 24,404 (approximately US$3,753). The rate of return offered to an investor after deducting the management fee varies with the duration of the investment term. Currently, the rate ranges from 7.23% to 9.94% for loans with a term from 90 days to 36 months.

We charge investors a service fee for using our investing platform. The service fee is equal to 8.00% of the interest that investors receive, and is paid at the time of each interest payment. There is no service fee if there's no investment made from investors. We recognize revenues for services provided to investors when such fees are paid by and invoices are issued to the investors.

Our Platform and the Transaction Process

Our platform provides a streamlined application process for borrowers and investors alike. The entire process from initial application to disbursement of funds on average takes approximately 20 days for direct loans and approximately one day for loan assignments. With respect to loan assignments, the initial review and approval of our Creditor Partners would generally take one to three months but the approval of subsequent loan assignments would generally take a day as the Creditor Partners had been pre-approved and our review would involve less documents and procedures. Our initial review and approval of our business partners would generally take a month but the approval of loans to borrowers referred by our business partners would take one to five days.

The following illustrates the entire application and funding process through our platform:

Stage 1: Application

Our borrower application process begins with the submission of a loan application by a prospective borrower. Borrowers can apply through our website or mobile applications. As part of the application process, the prospective borrower is asked to provide various personal and business details. The specific personal and business details required will depend upon the borrower's desired loan product, but typically include PRC identity card information, employer information, bank account information, credit card information and a credit Report from the PBOC. For business, they will need business registration certificate, tax certificate, financial report, bank statements and credit report from the People's Bank of China (the "PBOC"). Our borrowers are also required to designate the use of loan proceeds in their loan applications. After loan proceeds are disbursed, we will follow up with telephone calls to confirm such designated use of proceeds. However, due to the lack of detailed regulations, implementation measures and guidance on regulations concerning our industry, it is unclear what measures are required to verify the use of proceeds. We believe our current practice is sufficient in light of the type of loans facilitated and our transaction volume.

Our Creditor Partners were also required to open an account with us and send us the application materials before they could list their loans on our platform. However, once we had approved the Creditor Partners, we would not conduct additional verification on the Creditor Partners for subsequent loan assignment requests. We would only review the documents and conduct procedures in relation to each loan assignment. Nonetheless, we would re-evaluate these partners' creditability from time to time, usually on a monthly basis.

| 15 |

We sent our employees to the office of our business partners to prepare the applications of borrowers referred to us by our business partners. Our employees would review and verify the accuracy of such information and documents. In certain cases, our employees stationed at the offices of our business partners would also assist our business partners with their review and evaluation of customers for purposes of their risk management.

New investors sign up to our platform using a simple online portal in which they input their PRC identity card information and bank account information. Prior to March 2017, the funds they invested over our platform were deposited into a custody account run by established third-party online payment platforms. In March 2017, we fully migrated to a new payment system with Guangdong Huaxing Bank, which took over the investor custody accounts previously managed by the third-party payment platform. On April 8, 2018, we changed our custodian bank to XW Bank because peer-to-peer lending platforms in Sichuan province are required to have local commercial banks within the same province serve as custodians according to certain local regulations.

Stage 2: Verification and Credit Assessment

We also supplement our review of borrower's and Creditor Partner's application with data from a number of internal and external sources, including the following:

• historical credit data accumulated through our online platform;

• personal identity information maintained by an organization operated under the MPS;

• personal credit information maintained by an organization operated under the PBOC;

• online data from internet or wireless service providers, including social network information;

• third-party credit check services; and

• fraud "blacklists" and databases.

This data is then aggregated and used to verify an applicant's identity, for possible fraud detection and for assessment and determination of creditworthiness.

Stage 3: Anti-Fraud and Decisioning

In order to efficiently screen borrower applicants, we have designed an initial qualification phase to review the basic information regarding a prospective borrower that has been submitted with his application and gathered by us from available sources. After an initial check is performed, the prospective borrower's loan application either proceeds to the next phase of the application process or the prospective borrower is notified of the decision to decline the application.

As part of the initial qualification process, we also send our on-the-ground team to visit the applicant at their residence or office to verify borrower identity, credit data as well as collateral properties. If needed, we also engage appraisal firms to determine the value of collaterals. Based on initial due diligence, our business development department prepares requisite reports as well as loan requests for submission to our risk management department for further review and verification.

If a member of the credit assessment team suspects there may be fraud involved with a particular loan application or determines that additional verification is needed to complete the credit decisioning process, that team member will conduct further due diligence and verification, such as additional phone calls or onsite visits to the applicant and the applicant's employer that is identified in the application.

Following our multi-level review, the credit assessment team will either approve the loan as is, approve the loan with one or more modified sets of loan characteristics, or decline the loan application. Unqualified borrowers are notified of the decision to decline their applications for failing to meet minimum requirements. Qualified borrowers proceed directly to the approval, listing and funding stage.

| 16 |

Our Creditor Partners conducted their own due diligence investigation in the original borrower's credit-worthiness when they extended the Outside Loans. In addition, our risk management department would conduct its own due diligence on the creditor's rights sought to be assigned and the original borrower's credit-worthiness, using the same standards discussed above. As part of this process, our risk management department would review the loan agreement between the Creditor Partner and the original borrower to determine whether the original borrower had agreed to the proposed assignment of a Creditor Partner's rights. We would then directly contact the original borrower to ensure that they have received notice of proposed assignment from the Creditor Partner.

As part of their agreement with us, our business partners were required to conduct face-to-face interview and/or site visits of the applicants to verify the identity, credit data and collaterals of the borrowers they refer to us. Apart from this, our risk management department would also conduct our own review, evaluation and verification of the applicants.

Stage 4: Approval, Listing and Funding

Once a loan application is approved, we enter into a loan agreement with respect to borrowers or a loan assignment and repurchase agreement in the case of a loan assignment by a Creditor Partner. The loan agreements are between a borrower, investor(s) who fund the borrower's loan and our platform, or in the case of a loan assignment and repurchase agreement, among the Creditor Partner, the investor(s), guarantors and our platform, or in the case of a loan transaction through referral by our business partner, among the investor, borrower, the business partner and its affiliates and our platform. Upon a borrower's or Creditor Partner's acceptance of the loan documents, the loan or the Outside Loan is then listed on our platform for investors to view. Once a loan or an Outside Loan assignment is listed on our platform, investors may then subscribe to the loan or the Outside Loan using our automated or self-directed investing tools. We also make available a security agreement that enables our investors to take a security interest in the borrower's collateral or a guaranty whereby the guarantor will be jointly and severally liable for the payment of loans. Except in the case of referral through our business partners where we enter into a Finance Intermediary Service Contract with our business partners with respect to each borrower referred, we enter into such contract directly with each borrower prior to the disbursement of the loan proceeds. The contract provides for the services fees we will charge the borrower to facilitate the loan transaction on our platform as well as the rights and obligations of each party in the transaction.

Once a loan or an Outside Loan is fully subscribed, funds are then drawn from a custody account and disbursed to the borrower or the Creditor Partner.

Real estate and automobiles used to be the two types of collateral for loans facilitated and assigned through our platform. As part of our risk management program, we would first examine the value of the real estate to be used as collateral and then record the collateralization with local real estate bureau if such registration was allowed by PRC real estate laws and regulations. If such registration was not feasible under applicable PRC laws and regulations, we would require the property owner reflected in the real estate registry to guarantee the loan. Automobiles used to be collateral for loans assigned from one of our Creditor Partners and the loans with borrowers referred by our business partners. The Creditor Partner had completed the collateralization process prior to the loan assignment. When such loans were assigned to investors on our platform, these investors would have the right of the Creditor Partner with regard to the collateral.

Stage 5: Servicing and Collections

We provide payment reminder services through text messages or phone calls one week before payment dates. For loans with a term of 30 days or shorter, borrowers repay interest and principle upon maturity. For loans with a term of longer than 30 days, borrowers pay interest on a monthly basis.

We are generally not involved in the collection process after a loan is delinquent or a Creditor Partner fails to repurchase its Outside Loan. Upon any of these events, the investors may sell defaulted loans to third party asset companies. They may also initiate legal action against the borrowers in default. We only become involved in the legal action when a lender engages us to assist the lender in a legal action initiated upon a default. Since there have not been any defaulted loans on our platform as of the date of this Report, our collection process has not been tested in practice.

| 17 |

Risk Management

Traditional risk management tools and the types of consumer finance data available in developed economies, such as widely available consumer credit reporting services, are currently at an early stage of development in China. We believe our strong risk management capabilities provide us with a competitive advantage in attracting capital to our platform by providing investors with comfort that they are investing in high quality loans through a sustainable platform.

Our Loan Assessment Committee and Risk Management Division

We have a loan assessment committee, comprised of five individuals: director of operation, director of risk management, chief compliance officer, chief executive officer and independent review officer. Based on the recommendation of our operation and risk management teams, each application received through our platform is submitted to our loan assessment committee for final review and decision.

We did not submit each loan assignment to our loan assessment committee. Instead, they would assess the qualifications of our Creditor Partners and approve them along with a Total Assignment Cap and specific guidelines on the review and approval of subsequent loan assignments. Our risk management team followed these guidelines when they reviewed and approved the loan assignments. Our loan assessment committee reevaluated our Creditor Partners and adjusted the assignment cap periodically based on the performance of the Creditor Partner on existing assignments and their current and future financial conditions.

To approve a loan or a Creditor Partner or business partner, our loan assessment committee must reach a consensus and the independent review officer has the authority to veto the decision of other committee members. In the year ended March 31, 2018, approximately 99.26% of the loan applications submitted to our loan assessment committee were approved, 100% of Creditor Partners and 75% of business partners were approved.

We also have an independent risk management division, responsible for establishment and maintenance of risk management systems, evaluation and assessment of risks in operation, documentation, and completion of risk analysis reports etc.

Fraud Detection

Our fraud detection system is part of our larger risk management system. The system identifies and rejects potential borrower applications. Our system combines offline verification and the use of third-party credit services. Our offline verification activities involve members of our credit assessment team speaking with potential borrowers and their third-party references to inquire after any inconsistencies in a loan application. We also utilize government agency's open database to check their identity card numbers against known criminals and third party companies' credit information on potential borrowers. We maintain a blacklist of applicants after detecting any fraudulent borrowers.

Investor Protection

We emphasize investor protection through all stages of a transaction including but not limited to implementing strict risk management measures to assess and verify borrowers' or Creditor Partners' creditworthiness, requiring collateral or guaranties for our loans, monitoring borrowers' or Creditor Partners' payment status, and employing professional collection team to collect late payments or defaulted loans. With all these efforts, we have not had any defaulted loan since the launch of our platform.

We also strike to follow the best industry practice to protect our investors. For example, we have engaged XW Bank to provide fund depository services for our platform and assume fund depository functions including settlement, accounting and safeguarding online lending capital. In addition, we have obtained the Level III Certification of Information System Security issued by the MPS.

Depository Banks and Third-Party Payment Agents

Through March 2017, we used third-party online payment platforms to administer payments between borrowers, investors and ourselves and perform the related clearing and fund settlement actions associated with these payments. Our third-party payment agents transferred funds to and from borrowers' and investors' payment accounts as payment channels. We established checks and balances to ensure that all payments, transfers and made by the third-party payment agents were checked multiple times prior to the transmission of any funds to avoid errors.

| 18 |

In the spring of 2017, as required by law and with an aim to implement better risk management for our users, we engaged Guangdong Huaxing Bank to provide fund depository services for our platform in March 2017, pursuant to which Guangdong Huaxing Bank sets up separate accounts for borrowers and investors, and assumes fund depository functions including settlement, accounting and safeguarding online lending capital. We changed our custodian bank to XW Bank on April 8, 2018 because peer-to-peer lending platforms in Sichuan Province are required to have local commercial banks within the same province serve as custodians according to certain local regulations. We are one of the first few online lending platforms in Sichuan Province that have been accepted into the bank payment system.

Third-party payment agent operates as the payment channels and only transfer funds to and from fund depository accounts. Applicable Chinese regulations require us to centralize our depository business to one commercial bank, and sign or amend implementation agreements to the extent necessary. As a result, we ceased our business relationships with third party payment agents and engaged Guangdong Huaxing Bank, which was replaced by XW Bank as our sole custodian service provider. Other than XW Bank, none of our current service providers is critical to our business operations. If we discontinue our business relationship with XW Bank, we do not anticipate any material challenges finding another bank as our alternative custodian service provider.

Our Technology

We believe our technology platform is a competitive advantage and an important reason that borrowers and investors utilize our platform. Key features of our technology platform include:

| • | Mobile applications. We have developed different user-friendly mobile applications for borrowers and investors, which enable borrowers, Creditor Partners and investors to access our platform at any time or location. We launched our first mobile application in February 2017, and approximately 94.26% of investments were facilitated through our mobile application during the year ended March 31, 2018. |

| • | Fraud detection. We use a combination of current and historical data obtained during the application process, third-party data and sophisticated analytical tools to help determine an application's fraud risk. High risk applications are subject to further investigation. In case where fraud is confirmed, the application is cancelled, and we identify and flag characteristics of the loan to help refine our fraud detection efforts. |

| • | Scalable platform. Our platform is built on a distributed, load-balanced computing infrastructure, which is both highly scalable and reliable. The infrastructure can be expanded easily as data storage requirements and user visits increase. We utilize a unified platform, which administrates all systems and servers and can reconfigure or redeploy systems or servers automatically whenever needed. |

| • | Data security. Our network is configured with multiple layers of security to isolate our databases from unauthorized access and we use sophisticated security protocols for communication among applications. To prevent unauthorized access to our system we utilize a system of firewalls and also maintain a perimeter network, or a demilitarized zone, to separate our external-facing services from our internal systems. Our entire website and public and private application programming interfaces use the Secure Sockets Layer networking protocol. |

| • | Stability. Our systems infrastructure is hosted in cloud based data centers in Hangzhou and Shenzhen. We have multiple layers of redundancy to ensure the reliability of our network. We also have a working data redundancy model with comprehensive backups of our databases and our development environment conducted every day. |

Product Development