Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - REGIONS FINANCIAL CORP | rf-2018prdfastexh991.htm |

| 8-K - 8-K - REGIONS FINANCIAL CORP | rf-062118dfast8xk.htm |

Exhibit 99.2

Regions Financial Corporation - Dodd-Frank Act Stress Test Annual Disclosure - June 21, 2018

Overview

Section 165(i)(2) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”) requires covered institutions with $50 billion or more in assets to conduct annual stress tests (the “Dodd-Frank stress test” or “DFAST”) using a set of macroeconomic scenarios (Supervisory Baseline, Supervisory Adverse, and Supervisory Severely Adverse) developed by the Board of Governors of the Federal Reserve System (the “Federal Reserve”).

The following disclosure of summary stress test results is required by regulations promulgated by the Federal Reserve pursuant to the Dodd-Frank Act. These results present management’s estimation of the impact of the Federal Reserve’s annual Supervisory Severely Adverse stress test scenario for 2018 (the “Supervisory Severely Adverse scenario”) on Regions Financial Corporation (“Regions” or “Company”) and Regions Bank, its wholly-owned banking subsidiary. The results reflect pro forma capital ratios, select Income Statement and Balance Sheet line items, and other related information for the Supervisory Severely Adverse scenario. This Supervisory Severely Adverse scenario, however, does not represent forecasts of anticipated economic conditions, and stress tests are not forecasts of expected losses, revenues, net income before taxes, or capital ratios. This disclosure precedes Regions' planned disclosure of its Comprehensive Capital Analysis and Review ("CCAR") results, which is expected to be disclosed on or about June 28, 2018.

As specified by the Federal Reserve regulations, stress testing is performed through a forward-looking exercise using hypothetical severely adverse macroeconomic assumptions developed and provided by the Federal Reserve. Stress tests were conducted by the Federal Reserve and results were published on June 21, 2018 from its own internal models. Conversely, the results in this disclosure were generated internally by Regions using the Federal Reserve’s prescribed macroeconomic assumptions; thus, the processes and modeling methodologies used to produce the results in this disclosure are specific to Regions. Therefore, our internal stress test results are not directly comparable to those disclosed by other bank holding companies since modeling techniques, processes, and assumptions could differ significantly across companies. These results are not intended to reflect management’s expectations about future economic conditions and should not be taken as an indication of our expected present or future financial results.

Dodd-Frank Act Stress Test Assumptions

Dodd-Frank Act stress test assumptions reflect hypothetical, severe economic conditions that are more adverse than expected by the Federal Reserve or Regions. Accordingly, the scenario is not a forecast of anticipated economic conditions, nor are the estimates forecasts of expected losses, revenues, net income before taxes, or capital ratios. Rather, the Supervisory Severely Adverse scenario is a hypothetical scenario designed by the Federal Reserve to impose specific stresses on large banks to assess the strength and resilience of financial institutions and their ability to continue to meet the credit needs of households and businesses if the severe economic and financial environments were to develop. A full description of the Supervisory Severely Adverse scenario can be found on the Federal Reserve’s website at http://www.federalreserve.gov.

The table below presents key assumptions from the Federal Reserve’s Supervisory Severely Adverse scenario, which reflects a severe recession including significant declines in Gross Domestic Product (“GDP”) and the House Price Index (“HPI”), increases in the Unemployment Rate, and short-term market interest rates near zero with long-term market interest rates remaining unchanged. For purposes of the table below, the period forecasted includes 1Q 2018 through 1Q 2020 where PQ1 represents 1Q 2018 and PQ9 represents 1Q 2020.

Q1 2018 DFAST Supervisory Severely Adverse Scenario | |||||||||

% | PQ1 | PQ2 | PQ3 | PQ4 | PQ5 | PQ6 | PQ7 | PQ8 | PQ9 |

Annual Gross Domestic Product ("GDP") | (4.7) | (8.9) | (6.8) | (4.7) | (3.6) | (1.3) | (0.2) | 2.8 | 3.5 |

Annual Consumer Price Index ("CPI") | 1.7 | 2.0 | 1.8 | 1.2 | 1.2 | 1.4 | 1.5 | 1.6 | 1.7 |

House Price Index ("HPI")(1) | (3.9) | (11.4) | (17.5) | (22.0) | (25.8) | (28.1) | (29.6) | (29.6) | (29.5) |

Unemployment Rate | 5.0 | 6.5 | 7.6 | 8.5 | 9.3 | 9.7 | 10.0 | 9.9 | 9.7 |

10 Year Treasury | 2.4 | 2.4 | 2.4 | 2.4 | 2.4 | 2.4 | 2.4 | 2.4 | 2.4 |

3 Month Treasury | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

_________

(1) | Core Logic cumulative percentage change from Q3 2017 |

1

As the specific requirements are set forth in the Federal Reserve's regulations, bank holding companies, such as Regions, must assume a standard set of capital actions over the forecast horizon to estimate the Supervisory Severely Adverse scenario. The use of a standard set of capital actions is intended to assist the public in comparing stress test results disclosed by the various institutions subject to the stress test requirements. These capital action assumptions that are required for supervisory stress test purposes may not represent the actual capital actions taken should severely adverse conditions develop. In particular, the Dodd-Frank Act capital action assumptions in the Supervisory Severely Adverse scenario for Regions are:

1) | Actual capital distributions completed in the first quarter of 2018, including: |

a. | payment of a $0.09 per share common stock dividend, and |

b. | repurchase of $235 million of common stock; |

2) | Quarterly common stock dividends of approximately $0.085 per share for each quarter from the second quarter of 2018 through the first quarter of 2020, which is equal to the average quarterly dollar amount of common stock dividends that Regions paid over the four-quarter period beginning in the second quarter of 2017 and ending in the first quarter of 2018; |

3) | Payments on any other instrument that is eligible for inclusion in the numerator of a regulatory capital ratio equal to the stated dividend, interest, or principal due on such instrument(s) during the nine quarter horizon (this includes subordinated debt and preferred stock); |

4) | No redemption or repurchase of any capital instrument that is eligible for inclusion in the numerator of a regulatory capital ratio; and |

5) | No issuances of capital securities beginning in the second quarter of 2018. |

These assumed capital actions and the disclosed summary stress test results do not reflect the specific capital actions Regions may have requested for regulatory approval as part of the Company's 2018 CCAR submission.

Description of the Types of Risks Included in the Stress Test

Regions considers all risks in its stress testing activities which are identified through a comprehensive risk identification process. These risks range from idiosyncratic risks, such as geographic footprint and industry concentrations in the credit portfolios, to broad economic, political, regulatory and compliance risks which Regions believes may impact the Company and its peers. Specifically, Regions considers the following key risks in its stress testing activities: (1) credit risk, or the risk that arises from the potential that a borrower or counterparty will fail to perform on an obligation; (2) market risk, or the risk to Regions’ financial condition resulting from adverse movements in market rates or prices, such as interest rates, foreign exchange rates or equity prices; (3) liquidity risk, or the potential that the Company will be unable to meet its obligations as they come due because of an inability to liquidate assets or obtain adequate funding (referred to as "funding liquidity risk") or the potential that it cannot easily unwind or offset specific exposures without significantly lowering market prices because of inadequate market depth or market disruptions (referred to as "market liquidity risk"); (4) operational risk, or the risk of loss resulting from inadequate or failed internal processes, people, and systems, or from external events; (5) legal risk, or the risk that arises from the potential that unenforceable contracts, lawsuits, or adverse judgments may disrupt or otherwise negatively affect the operations or financial condition of Regions; (6) compliance risk, or the risk to current or anticipated earnings or capital arising from violations of laws, rules, or regulations, or from non-conformance with prescribed practices, internal policies and procedures, or ethical standards; (7) reputational risk, or the potential that negative publicity regarding Regions' business practices, whether true or not, will cause a decline in the customer base, lead to costly litigation, or result in revenue reductions, and (8) strategic risk, or the risk to current or anticipated earnings, capital, or franchise or enterprise value arising from adverse business decisions, poor implementation of business decisions, or lack of responsiveness to changes in the banking industry and Regions’ operating environment.

Each of the risks, which are discussed in further detail below, are stressed within particular portfolios of assets where those risks are applicable. Additionally, these risks are assessed through a comprehensive risk identification process across Regions’ three Business Segments (namely, Corporate Bank, Consumer Bank, and Wealth Management), as well as general corporate functions such as Treasury. Regions, to the best of its ability, fully captures the impacts of each risk as it relates to the defined scenarios. As part of its risk management practices, Regions monitors these risks through additional stress testing activities to ensure the risks are fully understood under a wide range of potential scenarios.

2

Credit Risk

Regions’ primary credit risk arises from the possibility that borrowers may not be able to repay loans and, to a lesser extent, the failure of securities issuers, obligors, or counterparties to perform as contractually required. In monitoring credit risk, Regions’ objective is to maintain a high-quality credit portfolio that provides for stable credit costs with acceptable volatility through an economic cycle. In order to assess the risk profile of the loan portfolio, Regions considers the current U.S. economic environment and that of its primary banking markets, as well as risk factors within the loan portfolio segments and classes.

Credit risk spans all Business Segments, but is concentrated in the Corporate Bank and Consumer Bank segments. Regions specifically measures credit risk for each portfolio of assets on the balance sheet, as well as risks that arise from off-balance sheet unfunded commitments. The underlying credit quality of these assets is stressed per the methodologies discussed below under “Description of Methodologies Employed by Regions.”

Market Risk

Regions’ primary market risk is interest rate risk. This includes, uncertainty with respect to absolute and relative interest rate levels, which are impacted by both the shape and the slope of the various yield curves that affect the financial products and services that the Company offers. To quantify this risk, Regions measures the change in its net interest income and other financing income in various interest rate scenarios compared to a base case scenario. Net interest income and other financing income sensitivity is a useful short-term indicator of Regions’ interest rate risk.

In addition, Regions, like most financial institutions, is subject to changing prepayment speeds on mortgage-related assets under different interest rate environments. Prepayment risk is a significant risk to earnings and specifically to net interest income and other financing income. Prepayment risk can also impact the value of securities and the carrying value of equity. Regions’ greatest exposures to prepayment risks primarily rest in its mortgage-backed securities portfolio, the mortgage fixed-rate loan portfolio, and the residential mortgage servicing asset, all of which tend to be sensitive to interest rate movements. Regions also has prepayment risk that would be reflected in non-interest income in the form of servicing income on the residential mortgage servicing asset. Regions’ capital markets business includes derivatives, loan syndication, and foreign exchange trading activities, which exposes the Company to market risk. Further, the Company is exposed to non-trading market risk from mortgage hedging activities, which include secondary marketing of loans to government-sponsored entities and mortgage servicing rights valuation.

Liquidity Risk

Liquidity is an important factor in the financial condition of Regions and affects Regions’ ability to meet the borrowing needs and deposit withdrawal requirements of its customers. Regions considers liquidity risk in its stress testing activities through an evaluation of its funding sources and assumptions regarding how those liabilities may re-price during times of stress. Regions’ analysis includes evaluation of the liquidity risks that are present in Regions Bank, largely arising from the changes in the relative movements between loans and deposits, and at the Company, largely arising from changes in the overall earnings of its wholly-owned subsidiary, Regions Bank.

Operational and Legal Risks

Cyber security, fraud, regulatory activity, and business/system failures are some of the key operational and legal risks included in the stress testing scenarios. Operational and legal risks are estimated for the stress tests considering modeled loss results, historical analysis, and evaluations of specific operational scenarios and expectations for how those types of losses may materialize in the supervisory scenarios. For example, losses that would be considered through operational scenario analysis include information security risks such as the risk of a cyber-attack.

Compliance, Reputational, and Strategic Risks

Other risks to the Company include compliance risk, reputational risk, and strategic risk. Compliance risk represents the risk that the Company will fail to comply with the laws, regulations, supervisory guidance, regulatory expectations, and rules and standards that govern the activities of the Company, including Regions’ Code of Business Conduct and Ethics. Reputational risk relates to the risk that negative publicity regarding Regions’ business practices, whether true or not, will affect the Company’s profitability, operations, customer base, or result in costly litigation. Strategic risk is the risk to the Company due to uncertainty and actions (or inaction) related to strategic risk factors, including negative effects from business planning or decisions, environmental changes, competitive dynamics, or management of our resources and activities. These risks are

3

evaluated and incorporated into stress testing results through methods such as scenario analysis to determine possible impacts to Regions’ financial condition if these risks were to materialize.

Description of Methodologies Employed by Regions

For stress testing purposes, the methodologies described herein translate identified risks into revenue and loss projections over the nine-quarter planning horizon, which are then aggregated into net income and loss estimates over the nine-quarter stress test horizon. The projections are then used to estimate Regions’ regulatory capital and key capital ratios throughout the nine quarters in accordance with the codified guidance provided by Regions’ regulators when applicable. In addition to estimating capital accretion or depletion from net income or loss over the nine-quarter planning horizon, Regions also estimates impacts to regulatory capital based on planned capital actions or prescribed actions (as is the case with the Dodd-Frank Act Stress Test scenarios). The resulting regulatory capital ratios are then compared against management’s targeted levels, which is a key step in Regions’ internal capital adequacy assessment.

In loss estimation, Regions aims to project losses that are appropriately sensitive to macroeconomic conditions and reflect the economic assumptions that, in the Supervisory Severely Adverse scenario, are meant to produce significant loss estimates with a corresponding stress on Regions’ capital levels. Regions estimates losses at a level of granularity that promotes the ability to capture unique risk drivers across different asset types. As in financial reporting, Regions establishes its stressed Allowance for Loan and Lease Losses (“ALLL”) in compliance with U.S. generally accepted accounting principles (“GAAP”). The primary consideration in estimating the ALLL is the modeled losses in the Supervisory Severely Adverse Scenario over the nine-quarter forecast period. Quantitative analysis is employed to ensure that the modeled ALLL is appropriately established.

In the development of projections for pre-provision net revenue (“PPNR,” which consists of net interest income and other financing income on a fully tax-equivalent basis plus non-interest revenues less non-interest expenses), Regions derives granular revenue and expense estimates across the Company and aggregates enterprise-level results under each macroeconomic scenario. Most revenue and expense line items are projected through specific models or driver-based approaches that are sensitive to the underlying behaviors and risks reflected in each revenue or expense category. Regions makes several key assumptions in modeling PPNR, including a determination of market interest rate projections throughout the nine-quarter period given the other Supervisory Severely Adverse scenario assumptions provided by the Federal Reserve. Other key assumptions specific to Regions that impact PPNR are the amount of loan and deposit growth, drivers of non-interest income, pricing levels for the products and services offered to our customers, usage and utilization assumptions, and level of expenses.

The process of projecting revenues and expenses often employs projections of related asset and liability balances. Thus, the balance sheet and income statement projection processes are designed to be internally consistent with coherent reflection of macroeconomic conditions across balances, revenues, and expenses. As with PPNR, macroeconomic-dependent models are utilized to develop key balance estimates. In creating these estimates, the Company makes several assumptions in addition to those enumerated previously, such as estimating the behavior of customers in adverse conditions and predicting borrower and depositor behavior in stress environments. Key assumptions such as these are discussed and challenged through the review process for reasonableness and effectiveness.

Once a consolidated balance sheet is created, on- and off-balance sheet risk-weighted assets are estimated based upon the final balance sheet. Regions’ risk-weighted asset projection process applies risk weights directly to scenario-specific balance sheet estimates. In many cases, the granularity of the balance sheet estimate allows for codified risk weights to be applied directly to the appropriate balance. Regions’ loan balances account for approximately 65% of total assets and, therefore, are the primary driver of the change in the projection of risk-weighted assets. Loans in the Supervisory Severely Adverse scenario are projected to decline by 13.4% over the nine-quarter period. As a result of deleveraging the balance sheet in this scenario, risk-weighted assets declined by 10.0% in this scenario.

In projecting losses, revenues, and expenses, the ability to translate macroeconomic factors and key risk measurements into pro forma estimates relies upon the utilization of models across Regions. Robust model development, documentation, validation, and overall model governance practices are critical to the revenue and loss estimation process. These models and estimates rely on a sound risk measurement and management infrastructure that supports the identification, measurement, assessment, and control of all material risks arising from the Company’s exposures.

A comprehensive and active governance structure provides oversight of Regions’ stress testing activities throughout the process. The governance structure is designed to review and challenge estimation methodologies to ensure that adverse projections are appropriately stressful and reflect best estimates of potential outcomes given the assumed economic conditions.

4

Summary of Results for Regions Financial Corporation

The estimates shown below reflect the methodologies and assumptions described previously for the Supervisory Severely Adverse scenario. Based upon the information available at the time of the 2018 DFAST submission, the impact to capital as well as income related to the pending sale of Regions' Insurance Group, Inc. and related affiliates (RIG), is captured in the estimates below.

Projected Stressed Capital Ratios through Q1 2020 in the Supervisory Severely Adverse Scenario | ||||||||

Actual | Stressed Capital Ratios(1) | |||||||

Q4 2017 | Ending | Minimum | ||||||

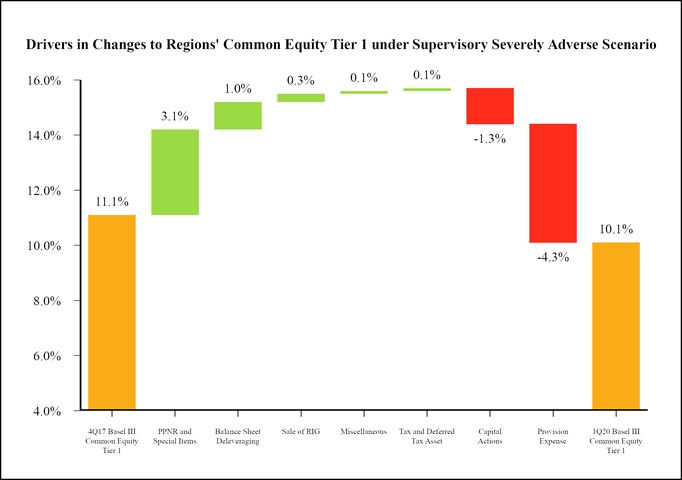

Common equity tier 1 capital ratio (%) | 11.1 | % | 10.1 | % | 10.1 | % | ||

Tier 1 risk-based capital ratio (%) | 11.9 | % | 11.1 | % | 11.0 | % | ||

Total risk-based capital ratio (%) | 13.8 | % | 13.3 | % | 13.3 | % | ||

Tier 1 leverage ratio (%) | 10.0 | % | 8.8 | % | 8.8 | % | ||

_________

(1) | The capital ratios are calculated using capital action assumptions provided within the Dodd-Frank Act stress testing rule. These projections represent hypothetical estimates that involve an economic outcome that is more adverse than expected. These estimates are not forecasts of expected losses, revenues, net income before taxes, or capital ratios. The minimum capital ratio presented is for the period Q1 2018 through Q1 2020. |

Actual Q4 2017 and Projected Q1 2020 Risk-Weighted Assets in the Supervisory Severely Adverse Scenario | |||

Actual Q4 2017 | Projected Q1 2020 | ||

Risk-weighted assets (billions of dollars) | $100.9 | $90.8 | |

Projected losses, revenue, and net income before taxes through Q1 2020 in the Supervisory Severely Adverse Scenario | |||||

Billions of Dollars | Percent of Average Assets(1) | ||||

Pre-provision net revenue(2) | $3.2 | 2.7 | % | ||

Other revenue | — | 0.0 | % | ||

less | |||||

Provisions | 4.4 | 3.7 | % | ||

Realized losses/(gains) on securities (AFS/HTM) | 0.1 | 0.1 | % | ||

Trading and counterparty losses | — | 0.0 | % | ||

Other losses/(gains) | — | 0.0 | % | ||

equals | |||||

Net income/(loss) before taxes(3) | (1.3) | (1.1 | )% | ||

Memo item | |||||

AOCI included in capital (billions of dollars)(4) | N/A | N/A | |||

_________

(1) | Average assets is the nine-quarter average of total assets. |

(2) | Pre-provision net revenue includes losses from operational-risk events and credit related expenses, which include other real estate owned (OREO) costs. |

(3) | Net income/(loss) before taxes may not appear to foot due to rounding. |

(4) | As Regions is not an advanced approaches bank holding company and opted out of including Accumulated Other Comprehensive Income ("AOCI") in regulatory capital calculations, AOCI balances are not applicable for the purposes of this disclosure. |

5

Projected loan losses by type of loan, Q1 2018 through Q1 2020 in the Supervisory Severely Adverse Scenario | |||||

Billions of Dollars | Portfolio Loss Rates (%)(1) | ||||

Loan Losses(2) | $2.9 | 3.9 | % | ||

First lien mortgages, domestic | 0.3 | 1.8 | % | ||

Junior liens and HELOCs, domestic | 0.4 | 5.9 | % | ||

Commercial and industrial(3) | 0.8 | 3.9 | % | ||

Commercial real estate, domestic(4) | 0.5 | 3.9 | % | ||

Credit cards | 0.2 | 13.3 | % | ||

Other consumer(5) | 0.5 | 10.1 | % | ||

Other loans | 0.3 | 2.2 | % | ||

_________

(1) | Average loan balances used to calculate portfolio loss rates exclude loans held for sale and loans held for investment under the fair value option, and are calculated over nine quarters. |

(2) | Total loan losses may not agree to the sum of the individual categories due to rounding. |

(3) | Commercial and industrial loans include small- and medium-enterprise loans and business cards. |

(4) | Commercial real estate loans include owner-occupied and non-owner occupied commercial real estate loans, and loans secured by farmland. |

(5) | Other consumer loans include automobile loans. |

Summary of Results for Regions Bank

The following results reflect pro forma capital ratios for Regions Bank under the Supervisory Severely Adverse scenario. These capital levels are derived using a process identical to that described in this document for the holding company. As with Regions Financial Corporation, Regions Bank’s capital ratios decline over the nine-quarter planning horizon in this theoretical severely adverse scenario as credit losses exceed PPNR generation. In its scenario planning, the holding company assumes capital actions at Regions Bank during the planning horizon that are in alignment with its internal capital adequacy assessment process. These actions, which may include dividends from or infusions into Regions Bank, as well as issuances, redemptions or repurchases of capital securities, are based on projected capital levels relative to management’s targets and limits, among other factors.

Projected stressed capital ratios through Q1 2020 in the Supervisory Severely Adverse Scenario | ||||||||

Actual | Stressed Capital Ratios(1) | |||||||

Q4 2017 | Ending | Minimum | ||||||

Common equity tier 1 capital ratio (%) | 12.5 | % | 13.3 | % | 12.4 | % | ||

Tier 1 risk-based capital ratio (%) | 12.5 | % | 13.3 | % | 12.4 | % | ||

Total risk-based capital ratio (%) | 14.0 | % | 15.1 | % | 14.1 | % | ||

Tier 1 leverage ratio (%) | 10.5 | % | 10.6 | % | 10.6 | % | ||

_________

(1) | These projections represent hypothetical estimates that involve an economic outcome that is more adverse than expected. These estimates are not forecasts of expected losses, revenues, net income before taxes, or capital ratios. The minimum capital ratio presented is for the period Q1 2018 through Q1 2020. |

Actual Q4 2017 and projected Q1 2020 risk-weighted assets in the Supervisory Severely Adverse Scenario | |||

Actual Q4 2017 | Projected Q1 2020 | ||

Risk-weighted assets (billions of dollars) | $100.5 | $90.5 | |

6

Projected losses, revenue, and net income before taxes through Q1 2020 in the Supervisory Severely Adverse Scenario | |||||

Billions of Dollars | Percent of Average Assets(1) | ||||

Pre-provision net revenue(2) | $3.9 | 3.3 | % | ||

Other revenue | — | 0.0 | % | ||

less | |||||

Provisions | 4.4 | 3.7 | % | ||

Realized losses/(gains) on securities (AFS/HTM) | 0.1 | 0.1 | % | ||

Trading and counterparty losses | — | 0.0 | % | ||

Other losses/(gains) | — | 0.0 | % | ||

equals | |||||

Net income/(loss) before taxes(3) | (0.6) | (0.5 | )% | ||

Memo item | |||||

AOCI included in capital (billions of dollars)(4) | N/A | N/A | |||

_________

(1) | Average assets is the nine-quarter average of total assets. |

(2) | Pre-provision net revenue includes losses from operational risk events and credit related expenses, which include other real estate owned (OREO) costs. |

(3) | Net income/(loss) before taxes may not appear to foot due to rounding. |

(4) | As Regions Bank is not an advanced approaches bank and opted out of including AOCI in regulatory capital calculations, AOCI balances are not applicable for the purposes of this disclosure. |

Projected Loan Losses by Type of Loan, Q1 2018 - Q1 2020 in the Supervisory Severely Adverse Scenario | |||||

Billions of Dollars | Portfolio Loss Rates (%)(1) | ||||

Loan Losses(2) | $2.9 | 3.9 | % | ||

First lien mortgages, domestic | 0.3 | 1.8 | % | ||

Junior liens and HELOCs, domestic | 0.4 | 5.9 | % | ||

Commercial and industrial(3) | 0.8 | 3.9 | % | ||

Commercial real estate, domestic(4) | 0.5 | 3.9 | % | ||

Credit cards | 0.2 | 13.3 | % | ||

Other consumer(5) | 0.5 | 10.1 | % | ||

Other loans | 0.3 | 2.2 | % | ||

_________

(1) | Average loan balances used to calculate portfolio loss rates exclude loans held for sale and loans held for investment under the fair value option, and are calculated over nine quarters. |

(2) | Total loan losses may not agree to the sum of the individual categories due to rounding. |

(3) | Commercial and industrial loans include small- and medium-enterprise loans and business cards. |

(4) | Commercial real estate loans include owner-occupied and non-owner occupied commercial real estate loans, and loans secured by farmland. |

(5) | Other consumer loans include automobile loans. |

Explanation of the Most Significant Causes for the Changes in Regulatory Capital Ratios

The Supervisory Severely Adverse scenario, as applied internally, results in meaningful projected declines in regulatory capital ratios at Regions over the nine-quarter period. The declines at Regions are primarily driven by an expectation of credit losses exceeding a weakened PPNR, which is especially stressed as a result of the significantly low short-term market interest rates present in the scenario. As detailed in the summary of results tables, this leads to a pre-tax net loss of approximately $1.3 billion over the forecast horizon for Regions. With respect to regulatory capital ratios, these losses are compounded by the Federal Reserve’s prescribed Dodd-Frank Act capital action assumption that Regions would continue to pay an average common stock dividend of approximately $0.085 per share during the relevant period, which may not align with the capital actions pursued by Regions if a similar scenario actually were to unfold. The impact of net losses and the prescribed capital

7

actions on Regions’ regulatory capital ratios is partially offset by the projected balance sheet deleveraging evident in moderately lower ending risk-weighted asset balances as well as the capital generated from the planned sale of RIG in Q3 2018. The combination of the factors described above account for the vast majority of the projected variation in regulatory capital ratios across the nine-quarter horizon in the Supervisory Severely Adverse scenario.

With respect to Regions Bank, the Supervisory Severely Adverse scenario results in a pre-tax net loss of approximately $0.6 billion over the forecast horizon. The impact of this pre-tax net loss on regulatory capital ratios is more than offset by tax benefits and projected balance sheet deleveraging, resulting in a modest increase in capital levels over the nine-quarter period.

8