Attached files

| file | filename |

|---|---|

| EX-31.2 - EX 31.2 - SUPERVALU INC | f18form10-kaex312.htm |

| EX-31.1 - EX 31.1 - SUPERVALU INC | f18form10-kaex311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

(Mark One)

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 24, 2018

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number: 1-5418

SUPERVALU INC.

(Exact name of registrant as specified in its charter)

DELAWARE | 41-0617000 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

11840 VALLEY VIEW ROAD EDEN PRAIRIE, MINNESOTA | 55344 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (952) 828-4000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, par value $0.01 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | Emerging growth company ¨ | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value of the voting and non-voting stock held by non-affiliates of the registrant as of September 8, 2017 was approximately $750,406,810 (based upon the closing price of registrant’s Common Stock on the New York Stock Exchange).

As of April 20, 2018, there were 38,405,453 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

EXPLANATORY NOTE

SUPERVALU INC. (“Supervalu”) is filing this Amendment No. 1 to Annual Report on Form 10-K (this “Amendment”) to amend the Annual Report on Form 10-K for the fiscal year ended February 24, 2018 (File Number 001-05418) (the “Form 10-K”) as filed by Supervalu with the U.S. Securities and Exchange Commission (the “SEC”) on April 24, 2018. This Amendment is being filed solely to provide the information required by Part III of Form 10-K. In connection with the filing of this Amendment and pursuant to the rules of the SEC, we are including with this Amendment certain currently dated certifications of Supervalu’s principal executive officer and principal financial officer.

This Amendment does not modify or update the other disclosures presented in the Form 10-K. Except as expressly provided herein, this Amendment does not reflect events occurring after the filing of the original Form 10-K (i.e., those events occurring after April 24, 2018) or modify or update those disclosures that may be affected by subsequent events. Accordingly, this Amendment should be read in conjunction with the Form 10-K and Supervalu’s other filings with the SEC.

2

SUPERVALU INC.

Annual Report on Form 10-K/A (Amendment No. 1)

TABLE OF CONTENTS

Item | Page | |

10. | ||

11. | ||

12. | ||

13. | ||

14. | ||

15. | ||

2

BASIS OF PRESENTATION

Unless otherwise indicated, all references to “Supervalu,” “we,” “us,” “our,” “ourselves” and the “Company” relate to SUPERVALU INC. and its wholly and majority-owned subsidiaries unless the context indicates otherwise.

PART III

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

The following sets forth information concerning members of the the Board of Directors:

| Donald R. Chappel, Chairman Director Since: 2010 Independent Age: 66 • Supervalu Committees: Corporate Governance and Nominating Committee• Retired Senior Vice President and Chief Financial Officer of The Williams Companies, Inc.• Former director of the general partner of Williams PartnersMr. Chappel is the retired Senior Vice President and Chief Financial Officer of The Williams Companies, Inc., a position he held from April 2003 until his retirement in November 2017. Williams is one of the leading energy infrastructure companies in North America. Williams owns an approximate 74% interest in Williams Partners L.P. (“Williams Partners”), including all of the general partnership interest. Williams Partners is a large-cap master limited partnership (“MLP”) with operations across the natural gas value chain from gathering, processing and interstate transportation of natural gas and natural gas liquids to petchem production of ethylene, propylene and other olefins. Williams Partners was formerly known as Access Midstream Partners, L.P. and in February 2015 merged with another energy infrastructure MLP controlled by Williams also known as Williams Partners L.P. (“Pre-Merger Williams Partners”). Access Midstream Partners was the surviving entity in the merger and changed its name to Williams Partners L.P. Mr. Chappel served as a director of the general partner of Williams Partners from 2012, and as its Chief Financial Officer from December 31, 2014, until his retirement in November 2017. Mr. Chappel served as Chief Financial Officer and a director of the general partner of Pre-Merger Williams Partners from 2005 until its merger in 2015. Mr. Chappel was Chief Financial Officer, from 2007, and a director, from 2008, of the general partner of Williams Pipeline Partners L.P., until its merger with Pre-Merger Williams Partners in 2010. Williams Pipeline Partners L.P. was an energy pipeline MLP formed and controlled by Williams. Prior to joining Williams, Mr. Chappel held various financial, administrative and operational leadership positions. Mr. Chappel is included in Institutional Investor magazine’s Best CFOs listing for 2006 to 2008 and 2010 to 2014. Among his many qualifications, Mr. Chappel brings significant experience in finance and accounting as a senior finance executive of several large public companies. Mr. Chappel serves as a director of two non-profit organizations, The Children’s Hospital Foundation at St. Francis and Family & Children’s Services of Oklahoma. |

3

| Irwin S. Cohen Director Since: 2003 Independent Age: 77 • Supervalu Committees: Audit Committee (Chair) • Retired Partner of Deloitte & Touche LLP• Founder of Deloitte’s Consumer Products, Retail and Services Practice and former Global Managing Partner• Director of Stein Mart, Inc., Chair of Audit Committee Mr. Cohen is a Retired Partner of Deloitte & Touche LLP, a professional services firm providing audit, tax, financial advisory and consulting services. Mr. Cohen, who joined Deloitte in 1962 and became a partner in 1972, served as the Global Managing Partner of the Consumer Products, Retail and Services Practice of Deloitte from 1997 to 2003. Mr. Cohen also founded and led Deloitte’s Consumer Products, Retail and Services Practice as it grew to serve over 100 countries in Europe, Asia Pacific and the Americas. Mr. Cohen brings considerable experience in retail and accounting as a result of his experience with Deloitte. Mr. Cohen is also a director and chair of the Audit Committee of Stein Mart, Inc., a discount fashion retailer with sales in excess of $1 billion. In addition, he currently serves or has served on the boards of several private and non-profit companies. |

| Philip L. Francis Director since: 2006 Independent Age: 71 • Supervalu Committees: Leadership Development and Compensation Committee (Chair)• Former President and Chief Executive Officer of Shaw’s Supermarkets, Inc. and Cardinal Foods• Retired Executive Chairman of PetSmart, Inc.• Director of At Home Group, Inc.• Former director of CareFusionMr. Francis retired in 2012 from PetSmart, Inc. after serving ten years as Chief Executive Officer and two years as the Executive Chairman. PetSmart is a specialty retailer of services and solutions for pets. Prior to joining PetSmart, Mr. Francis was the President and Chief Executive Officer of Shaw’s Supermarkets, Inc. and Cardinal Foods. His formal education includes a Bachelor of Science degree from the University of Illinois in Agricultural Science and an MBA in Marketing and Management from Indiana University. Among his many qualifications, Mr. Francis brings significant retail industry experience, as well as experience in business strategy as a senior executive of a large public company. Mr. Francis is a director of At Home Group, Inc., a retail chain specializing in home décor products. He previously served as a director of PetSmart, Inc. from 1989 to 2012, and as a director of CareFusion from 2009 until it was sold in March 2015. He is active with several non-profit or service organizations that include Teach for America, Greater Phoenix Leadership (past chairman), Federal Reserve Board-Western Region Advisory Council, and TGEN-Translational Genomics Research Institute. He is a past campaign chair and board chair of Valley of the Sun United Way and is active in UMOM (homeless) and ASU Idea Enterprise. |

4

| Mark Gross Director Since: 2016 President and Chief Executive Officer Age: 55 • President and Chief Executive Officer of Supervalu • Founder and former President of Surry Investment Advisors LLC• Former Co-President, Chief Financial Officer and General Counsel of C&S Wholesale Grocers and President of its retail grocery affiliateMr. Gross has served as the President and Chief Executive Officer of the Company since February 5, 2016. Prior to joining the Company, Mr. Gross had served since 2006 as President of Surry Investment Advisors LLC, an advisory firm that Mr. Gross founded to provide services to grocery distributors and retailers with respect to strategic and operational matters. In this role, Mr. Gross assisted grocery clients on several multi-billion dollar acquisitions and divestitures and consulted with private equity firms with respect to investments in food retail, distribution and consumer packaged goods sectors. From 1997 to 2006, Mr. Gross worked at C&S Wholesale Grocers, most significantly serving as Co-President of C&S from 2005 to 2006. Additionally, during his tenure with C&S, Mr. Gross served as Chief Financial Officer and General Counsel of C&S, and President of its retail grocery affiliate. Among his many qualifications, Mr. Gross brings a wealth of grocery wholesale and retail industry experience, including significant experience in business strategy and operations as a senior executive of a large grocery wholesale company and as an advisor to several grocery companies and investors. Mr. Gross graduated cum laude from the University of Pennsylvania Law School and holds a BA from Dartmouth College where he graduated with highest honors in his major. |

| Eric G. Johnson Director Since: 2013 Independent Age: 67 • Supervalu Committees: Corporate Governance and Nominating Committee (Chair)• President and Chief Executive Officer of Baldwin Richardson Foods Company• Former Chief Executive Officer of Johnson Products Company• Director of Lincoln National Corporation, Chairman of Finance Committee Mr. Johnson is the President and Chief Executive Officer of Baldwin Richardson Foods Company (“Baldwin Richardson”), one of the largest African-American-owned businesses in the food industry, a position he has held since 1997. Baldwin Richardson is a major producer of products and ingredients for McDonald’s, Kellogg, General Mills and Frito Lay. Baldwin Richardson also has retail brands and foodservice products that it distributes nationally. Mr. Johnson purchased Baldwin Ice Cream Co. in 1992, and, in 1997, he completed the acquisition of Richardson Foods from Quaker Oats Company to form Baldwin Richardson. From 1989 to 1991, Mr. Johnson served as Chief Executive Officer of Johnson Products Company. Among his many qualifications, Mr. Johnson brings considerable food industry and business experience from the perspective of a manufacturer and supplier of food products to the retail and foodservice markets. Mr. Johnson serves as a member of the Board of Directors for Lincoln National Corporation and is chairman of its Finance Committee. He also sits on the Board of Trustees for Babson College and serves on the Board of the Urban League of Rochester. Mr. Johnson is a graduate of Babson College. |

5

| Mathew M. Pendo Director Since: 2014 Independent Age: 54 • Supervalu Committees: Corporate Governance and Nominating Committee • Managing Director of Oaktree Capital• Former Managing Director at Sandler O’Neill Partners• Former Director of Ally Financial Inc.Mr. Pendo serves as Managing Director of Oaktree Capital, an investment firm that specializes in less efficient markets and alternative investments, and has held that position since June 2015. Prior to joining Oaktree, from September 2013 until June 2015, Mr. Pendo served as a Managing Director at Sandler O’Neill Partners, an investment banking boutique focused on the financial services industry. Prior to joining Sandler O’Neill Partners, Mr. Pendo served as the Chief Investment Officer for the Troubled Asset Relief Program (“TARP”) at the U.S. Department of the Treasury from November 2010 until March 2013. He previously served as Managing Director Investment Banking for Barclays Capital from 2003 until October 2010, where he served as Co-Head of the Industrials Group and the U.S. Investment Banking Group. Among his many qualifications, Mr. Pendo brings substantial financial and investment banking experience to the Board. Mr. Pendo previously served as a director of Ally Financial Inc., a bank holding company focused on the auto finance and online banking industries, from 2013 to 2015. Mr. Pendo holds a Bachelor of Arts degree in Economics from Princeton University and received a Distinguished Service Award from the U.S. Department of Treasury for his work overseeing TARP’s investment activities. |

6

| Francesca Ruiz de Luzuriaga Director Since: 2015 Independent Age: 64 • Supervalu Committees: Audit Committee• Former Chief Operating Officer of Mattel Interactive, a business unit of Mattel, Inc.• Former Executive Vice President, Worldwide Business Planning and Resources, and former Chief Financial Officer of Mattel, Inc. • Director of Office Depot, Inc., member of Compensation and Governance Committees • Former Director of Providian Financial Corporation and OfficeMax IncorporatedMs. Luzuriaga has been an independent business development consultant since 2000. Previously, she was the Chief Operating Officer of Mattel Interactive, a business unit of Mattel, Inc., one of the major toy manufacturers in the world, from 1999 to 2000. Prior to holding this position, she served Mattel as its Executive Vice President, Worldwide Business Planning and Resources, from 1997 to 1999, and as its Chief Financial Officer from 1995 to 1997. Among her many qualifications, Ms. Luzuriaga brings substantial prior leadership experience in the operations and strategy side of businesses, both in the United States and internationally, as well as financial expertise and experience in corporate finance. Ms. Luzuriaga is a director and serves on the Compensation and Governance Committees for Office Depot, Inc. Previously, she was a director of OfficeMax Incorporated from 1998 to November 2013. She has been a director since January 2012, and chair of the Board since January 2017, of SCAN Health Plan, a not-for-profit Medicare Advantage health plan, as well as a director of its Foundation since January 2017. From 2002 until 2005, she was also a director of Providian Financial Corporation. |

| Frank A. Savage Director Since: 2014 Independent Age: 70 • Supervalu Committees: Leadership Development and Compensation Committee• Senior Advisor to Lazard Ltd.• Former Vice Chairman of U.S. Investment Banking at Lazard Ltd., and current Senior Advisor • Former Co-Head of Lazard’s Restructuring Group and member of Lazard’s Deputy Chairman Committee• Director of Rite Aid CorporationMr. Savage has been a senior advisor to investment banking firm Lazard Ltd. (“Lazard”) since January 2014 and served as Vice Chairman of U.S. Investment Banking at Lazard from 2009 to December 2013. He was the Co-Head of Lazard’s Restructuring Group from June 1999 to December 2013 and also served on Lazard’s Deputy Chairman Committee from 2006 to December 2013. Prior to joining Lazard, Mr. Savage served as Co-Head of the Restructuring Practice at investment banking firm BT Alex. Brown Inc. and before that was the Head of the Restructuring Group at investment bank UBS AG. Mr. Savage holds a degree from the University of Pennsylvania’s Wharton School of Business. Among his many qualifications, Mr. Savage brings extensive financial, restructuring and investment banking experience to the Board. Mr. Savage has served as a director of Rite Aid Corporation since June 2015. |

7

| Mary A. Winston Director Since: 2016 Independent Age: 56 • Supervalu Committees: Leadership Development and Compensation Committee; Audit Committee• Former Executive Vice President and Chief Financial Officer of Family Dollar Stores, Inc.• Founder and President of WinsCo Enterprises, Inc.• Former Senior Vice President and Chief Financial Officer for Giant Eagle, Inc.• Director of Dover Corporation, Member of Finance and Compensation Committees, Former Chair of Audit Committee• Director of Domtar Corporation, Member of Audit and Finance Committees• Director of Acuity BrandsMs. Winston is the founder and President of WinsCo Enterprises, Inc., a consulting firm providing financial and board governance advisory services, and has held that position since 2016. Ms. Winston previously served from 2012 until August 2015 as Executive Vice President - Chief Financial Officer of Family Dollar Stores, Inc., a discount retailer with more than 8,300 stores and nearly $11 billion in revenues prior to its acquisition by Dollar Tree in July 2015. Before joining Family Dollar, from 2008 to 2012, Ms. Winston served as Senior Vice President and Chief Financial Officer for Giant Eagle, Inc., a regional grocery and fuel retailer. Ms. Winston was Founder and President of WinsCo Financial, LLC, a financial solutions consulting firm, from 2007 to 2008 and served as Executive Vice President and Chief Financial Officer of Scholastic Corporation, a children’s publishing and media company, from 2004 to 2007. Among her many qualifications, Ms. Winston brings corporate executive leadership experience as well as extensive financial management and leadership. Ms. Winston has served as a director of Dover Corporation, a diversified industrial manufacturing company, since 2005, where she served as chair of its Audit Committee from 2008 to 2018 and now serves on its Finance and Compensation Committees. She has served as a director and member of the Audit and Finance Committees of Domtar Corporation, a paper, pulp and consumer personal care products manufacturer, since 2015, and as a director of Acuity Brands, Inc., a provider of indoor and outdoor lighting and energy management solutions, since April 2017. Ms. Winston previously served as a director of Plexus Corporation, an electronic manufacturing services company, from 2008 to February 2016. Ms. Winston is also Board chair and President of the Carolinas chapter of the National Association of Corporate Directors. |

8

The following table provides certain information concerning the executive officers of Supervalu as of April 24, 2018.

Name | Age | Present Position | Calendar Year Elected to Present Position | Other Positions Recently Held with Supervalu | ||||

Mark Gross(1) | 55 | President and Chief Executive Officer | 2016 | |||||

Rob N. Woseth(2) | 47 | Executive Vice President and Chief Financial Officer | 2018 | Executive Vice President, Chief Strategy Officer, 2013-2018; and Interim Chief Financial Officer, 2017-2018 | ||||

Randy G. Burdick(3) | 60 | Executive Vice President, Chief Information Officer | 2013 | |||||

Anne M. Dament(4) | 51 | Executive Vice President, Retail, Marketing and Private Brands | 2017 | Senior Vice President, Retail, Merchandising and Marketing, January 2017-October 2017 | ||||

Stuart D. McFarland(5) | 40 | Senior Vice President, General Counsel and Corporate Secretary | 2017 | Vice President, Associate General Counsel and Assistant Corporate Secretary, 2014-2017; Director and Associate General Counsel, 2013-2014, Senior Attorney, 2012-2013; and Attorney 2010-2012 | ||||

Michael C. Stigers(6) | 59 | Executive Vice President, Wholesale | 2015 | President of Cub Foods, 2014-2015; President, Northern and Western Region of Wholesale, 2013-2014; President of Shaw’s, 2011-2013 | ||||

James W. Weidenheimer(7) | 59 | Executive Vice President, Corporate Development and Chief Innovation Officer | 2016 | |||||

(1) | Mark Gross was appointed President and Chief Executive Officer in February 2016. Prior to joining Supervalu, from 2006 to 2016 Mr. Gross served as President of Surry Investment Advisors LLC, an advisory firm that he founded to provide consulting services to grocery distributors and retailers with respect to strategic and operational matters. From 1997 to 2006, Mr. Gross held various positions at C&S Wholesale Grocers, Inc., a wholesale grocery distributor (“C&S”), including serving as Co-President of C&S’s overall operations from 2005 to 2006. Additionally, during his tenure with C&S, Mr. Gross served as Chief Financial Officer, General Counsel, and President of its affiliated retail grocery operations. |

(2) | Rob N. Woseth was appointed Executive Vice President and Chief Financial Officer in February 2018. He served as Executive Vice President, Chief Strategy Officer from March 2013 to February 2018 and as Interim Chief Financial Officer from July 2017 to February 2018. Prior to joining Supervalu, Mr. Woseth served as Vice President Business Development and Strategy at Albertson’s LLC, a grocery company, from 2006 to 2013. |

(3) | Randy G. Burdick was appointed Executive Vice President, Chief Information Officer in March 2013. Prior to joining Supervalu, Mr. Burdick served as Executive Vice President and Chief Information Officer at OfficeMax, an office supplies retailer, from 2005-2013. |

(4) | Anne M. Dament was appointed Executive Vice President, Retail, Marketing and Private Brands, in November 2017. She served as Senior Vice President, Retail, Merchandising and Marketing from January 2017 to November 2017. Prior to joining Supervalu, Ms. Dament served as Senior Vice President, Merchandising at Target Corporation, a general merchandise retailer, from April 2015 to November 2016. Ms. Dament previously served as Vice President, Merchandising Solutions, from January 2009 to September 2012 and as Vice President, Services from September 2012 to April 2015 at PetSmart, Inc., a specialty retailer of services and solutions for pets. |

(5) | Stuart D. McFarland was appointed Senior Vice President, General Counsel and Corporate Secretary in November 2017. He served as Vice President, Associate General Counsel and Assistant Corporate Secretary from July 2014 to November 2017, Director and Associate General Counsel from August 2013 to July 2014, Senior Attorney from October 2012 to August 2013, and Attorney from August 2010 to October 2012. Prior to joining Supervalu, Mr. McFarland was an associate at the law firm of Gibson, Dunn & Crutcher LLP in Los Angeles. |

(6) | Michael C. Stigers was appointed Executive Vice President, Wholesale in December 2015. He served as President of Cub Foods from December 2014 to December 2015, President, Northern and Western Region of Wholesale, from 2013 to 2014, and President of Shaw’s, a retail banner that we formerly owned, from 2011 to 2013. Prior to joining Supervalu, Mr. Stigers served as President of PW Supermarkets, Inc., an operator of retail grocery supermarkets, from 2006 to 2010 and as Chief Executive Officer in 2010. In April 2011, creditors filed a petition for involuntary bankruptcy against PW Supermarkets in U.S. Bankruptcy Court, Northern District of California to force PW Supermarkets into a Chapter 7 liquidation. The bankruptcy case was transferred to the Oakland Division in October 2014 and remains pending in that court. |

(7) | James W. Weidenheimer was appointed Executive Vice President, Corporate Development and Chief Innovation Officer in April 2016. Prior to joining Supervalu, Mr. Weidenheimer served as Senior Vice President of Corporate Development for C&S from 2008 to 2016, where Mr. Weidenheimer oversaw significant M&A activity and led the development of procurement and distribution outsourcing plans. From 1998 to 2008, Mr. Weidenheimer had operating responsibility for finance, treasury, procurement, facilities, internal audit, quality assurance and inventory control at C&S. |

9

Directors are elected for a term of one year and until their successors are elected and qualified. The term of office of each executive officer is from one annual meeting of the Board of Directors until the next annual meeting of the Board of Directors or until a successor is elected. There are no family relationships between or among any of our directors and executive officers.

Audit Committee

The Board maintained a standing Audit Committee during fiscal 2018. The following directors served on the Audit Committee in fiscal 2018: Irwin S. Cohen (Chair), Francesca Ruiz de Luzuriaga and Mary A. Winston. The Board determined that all such members of the Audit Committee were financially literate under the NYSE listing standards and that each member qualified as an “audit committee financial expert” under the NYSE listing standards and the rules of the SEC.

The primary responsibilities of the Audit Committee are to assist the Board of Directors in:

• | its oversight of our accounting and financial reporting principles and policies, and our internal controls and procedures; |

• | its review and oversight of our financial statements and the independent registered public accounting firm; |

• | selecting, appointing, compensating, evaluating and, where deemed appropriate, replacing the independent registered public accounting firm, which reports directly to the Audit Committee; |

• | evaluating the independence of the independent registered public accounting firm; |

• | its oversight of our major financial risk exposures and assessment of the steps that we have taken to assess and manage such exposures; and |

• | its oversight of our compliance with legal and regulatory requirements. |

In addition, the Audit Committee has the responsibility to:

• | review the scope of the annual audit plan and organizational structure of the internal auditors, and the results of the internal auditor’s activities; |

• | regularly meet separately with the senior internal audit executive, who reports functionally to the Audit Committee and administratively to our Chief Financial Officer, and the independent registered public accounting firm; |

• | review reports by the independent registered public accounting firm describing and assessing our internal controls and discuss the adequacy and effectiveness of our internal controls and any specified audit procedures taken in light of any material weakness or significant deficiencies identified by us or the independent registered public accounting firm; and |

• | establish procedures concerning the receipt, retention and treatment of complaints regarding financial reporting, accounting, internal accounting controls or auditing and federal securities law matters. |

Code of Ethics

We have adopted a code of ethics called the Code of Business Conduct that applies to our principal executive officer, principal financial officer, principal accounting officer and controller, or persons performing similar functions and all other employees, and a Code of Business Conduct and Ethics that applies to our directors. The Codes are posted on our website at www.supervalu.com. We intend to satisfy the disclosure requirement under Item 5.05 of Form 8-K regarding an amendment to, or waiver from, a provision of the code of ethics that applies to Supervalu’s principal executive officer, principal financial officer, principal accounting officer and controller, or persons performing similar functions, by posting such information on our website at the address specified above.

Our Governance Principles and charters for each Committee of our Board of Directors are also available on our website. The Codes, Governance Principles and charters are also available in print to any stockholder who submits a request to: Corporate Secretary, SUPERVALU INC., P.O. Box 990, Minneapolis, Minnesota 55440.

Information on our website is not deemed to be incorporated by reference into this Amendment.

Section 16(a) Beneficial Ownership Reporting Compliance

The rules of the SEC require our directors, executive officers and holders of more than 10% of our common stock to file reports of stock ownership and changes in ownership with the SEC. Based solely on a review of the Section 16 reports filed by our directors and executive officers and written representations of our directors and executive officers, we believe that our directors and executive officers complied with all Section 16(a) filing requirements for fiscal year 2018.

10

ITEM 11. EXECUTIVE COMPENSATION

COMPENSATION DISCUSSION AND ANALYSIS

This Compensation Discussion and Analysis (“CD&A”) provides an overview of our fiscal 2018 business transformation and highlights, a detailed explanation of our executive compensation philosophy and programs and decisions made with respect to compensation for the Named Executive Officers (“NEOs”) below. Our fiscal 2018 included 52 weeks, starting on February 26, 2017 and ending on February 24, 2018. Compensation provided to our NEOs is also outlined in the Summary Compensation Table on page 27 of this Amendment and other compensation-related tables that follow in this Amendment.

Named Executive Officers | Title(s) Held During Fiscal 2018 | Dates From Start of Fiscal 2018 |

Mark Gross | -President and Chief Executive Officer | February 26, 2017 to present |

Rob N. Woseth(1) | -Executive Vice President, Chief Strategy Officer -Interim Chief Financial Officer | February 26, 2017 to February 24, 2018 July 6, 2017 to February 24, 2018 |

James W. Weidenheimer | -Executive Vice President, Corporate Development and Chief Innovation Officer | February 26, 2017 to present |

Michael C. Stigers | -Executive Vice President, Wholesale | February 26, 2017 to present |

Randy G. Burdick | -Executive Vice President, Chief Information Officer | February 26, 2017 to present |

Bruce H. Besanko | -Former Executive Vice President, Chief Operating Officer and Chief Financial Officer | February 26, 2017 to July 5, 2017 |

(1) Mr. Woseth was promoted to the position of Executive Vice President and Chief Financial Officer effective the first day of fiscal 2019, February 25, 2018.

Summary: Our compensation is tied closely to our strategy

We are leveraging our position as the largest public grocery wholesaler in the United States to transform our business and build upon our core competencies to become the wholesale supplier of choice to grocery retailers and to benefit from the rapidly changing food sector.

The individual elements and overall philosophy of our executive compensation plans are designed to support our transformation, as well as maintain and grow our existing core business. Accordingly, our plans include elements that align NEO compensation to:

• | absolute and relative shareholder return; |

• | achievement of annual operational and financial goals that reflect growing our top-line sales while delivering Adjusted EBITDA; |

• | achievement of our business transformation goals that support long-term returns; and |

• | rewarding and shaping our executives’ leadership strengths and contributions. |

This close alignment between our executive compensation and our strategy and long-term stockholder interests continues our philosophy from fiscal 2017. We received 98.1% approval from our voting stockholders for our 2017 advisory “say-on-pay” referendum.

We open this CD&A with a short summary of who we are and what our key strategic initiatives were over the last year. We believe you will see in this CD&A the strong tie between these initiatives and our executive compensation programs in fiscal 2018.

Who We Are

We are the largest public company grocery wholesaler in the United States. We operate a network of 28 distribution centers covering approximately 21 million square feet from which we deliver a broad assortment of products to retailers, including independent retailers operating diverse formats, regional and national chains, our corporate-owned retail stores and military commissaries. We enable our customers to better serve their consumers by leveraging scale efficiencies in procurement, logistics and merchandising; supplying a broad assortment of products, including an industry-leading portfolio of private, ethnic and specialty brands; and offering a suite of professional services. Our business is classified into two reportable segments: Wholesale and Retail.

During fiscal 2018, we expanded our Wholesale capabilities and distribution network through the acquisitions of Unified Grocers, Inc. (“Unified”) and Associated Grocers of Florida, Inc. (“AG Florida”), as well as new distribution centers in Harrisburg, Pennsylvania and Joliet, Illinois. We serve customers in nearly all U.S. states, as well as internationally, including in the Caribbean, Central and South America and Asia.

11

We also operate three retail banners (in continuing operations) with strong local and regional recognition: Cub Foods, Shoppers Food & Pharmacy and Hornbacher’s. The retail banners extend our Wholesale value proposition and offer consumers an assortment of products and services at competitive prices through a network of well-maintained stores.

Strategic Transformation and Initiatives

We began a strategic transformation in 2016 to become the wholesale supplier of choice for grocery retailers across the United States, all in furtherance of our goal to deliver long-term value to our stockholders. To further align our executive compensation with the priority of transforming our business, we introduced a business transformation metric in our annual incentive plan this year (see “Total Direct Compensation for our Executive Officers — Annual Incentive Plan — Annual incentive metrics — Business Transformation Metric”). The Wholesale and Retail leadership team that we appointed in the last two years to lead and manage the continued execution of our four strategic pillars continue to drive our transformation to grow our core Wholesale business, optimize our asset base, de-lever our balance sheet and take advantage of strategic and opportunistic mergers and acquisitions.

Grow our Core Wholesale Business

• | We have added more than $5 billion in run-rate sales to grow our core Wholesale business to nearly $13 billion, when annualizing the sales from Unified and AG Florida. These acquisitions, plus the addition of significant new Wholesale customers, such as The Fresh Market, drove our growth in fiscal 2018. |

• | We made strategic capital investments of approximately $135 million in fiscal 2018 toward the purchase and improvement of distribution warehouses, including Harrisburg, Pennsylvania and Joliet, Illinois, to support the growth of our Wholesale business, including our Market Centre division that supplies specialty and ethnic foods and non-food products, to solidify our East Coast distribution and to enable further growth in certain key markets. |

Optimize our Asset Base

• | We sold a majority of our Farm Fresh retail stores and pharmacy assets for a total of $53 million in March 2018. |

• | We announced that we are pursuing the sale of our corporately owned and operated retail operations of Shop ‘n Save (based in St. Louis) and Shop ‘n Save East (with stores in West Virginia, Maryland, Pennsylvania and Virginia) in April 2018. These operations along with Farm Fresh are now reported in discontinued operations. |

• | We sold our minority interest in an entity that operates multiple franchised Cub Foods stores in the Minneapolis - St. Paul, Minnesota market in February 2018. |

De-lever the Balance Sheet

• | The sale of Save-A-Lot for $1.3 billion in late fiscal 2017 significantly reduced our debt and improved our balance sheet, eliminating high levels of capital expenditures for retail operations and increasing our flexibility and resources to execute our wholesale growth strategy in fiscal 2018. |

• | We announced a sale leaseback transaction in April 2018 for eight of our distribution centers, with expected gross proceeds of approximately $483 million before costs and taxes, the net proceeds of which will be used to further reduce outstanding debt and improve our balance sheet. We closed on seven of the eight properties in May 2018 and expect to close on the remaining property by October 2018, as originally intended. |

Strategic and Opportunistic Mergers and Acquisitions

• | We expanded our Wholesale business and distribution network on the West Coast through the acquisition of Unified on June 23, 2017, a business that had $3.7 billion of annual net sales, including Market Centre. |

• | We expanded our Wholesale business and distribution network in Florida through the acquisition of AG Florida on December 8, 2017, a business that had $0.6 billion in annual net sales, including international customers and specialty and ethnic foods to local wholesale customers. |

• | We have increased our expected run-rate cost synergies of approximately $95 million to be achieved by the end of the third year following the respective closings of the Unified and AG Florida transactions, of which we realized approximately $23 million in fiscal 2018. |

• | We expect the food wholesale industry consolidation to continue and believe our strategy enables us to build upon the recent acquisitions of Unified and AG Florida to further grow and expand our capabilities through merger and acquisition opportunities. |

We believe we had significant success rapidly and strategically transforming our business in fiscal 2018 as described above. Fiscal 2018 results were above expectations and, as intended with our pay-for-performance philosophy, that

12

performance translated into higher incentive payouts to our NEOs, as discussed further below, including a maximum payout under our Business Transformation metric.

Business Strategies and Initiatives

While we have been strategically transforming our business, we also continued to execute on our Wholesale and Retail business strategies in fiscal 2018. In Wholesale, we continued to execute on our three-pronged strategy of:

• | retaining existing customers by anticipating, listening to and meeting our customer needs and differentiating ourselves through our service levels, pricing, product offerings and professional services; |

• | growing our business with existing customers by marketing our fresh product offerings, such as produce, our ethnic and specialty capabilities and our professional service offerings to help our customers compete and grow their businesses, including retail store support, advertising, couponing, e-commerce, network and data hosting solutions, training and certifications classes and administrative back-office solutions; and |

• | affiliating new customers, including traditional and non-traditional formats, and aggressively pursuing external growth and market opportunities. We are also expanding the Market Centre product offerings into our supply chain and continuing to optimize our product offerings to anticipate and meet our customers’ needs. |

In Retail, we executed on a strategy to drive profitable retail sales through competitive pricing, strong, event-based promotions, and enhancing merchandising displays and product offerings such as Quick & Easy meal solutions, including meal kits and grab ‘n go options. We also made targeted and innovative capital investments in our continuing operations banners for new stores, relocations and store remodels.

“Say-on-Pay,” Frequency of Votes on Executive Compensation and Stockholder Outreach

We believe that open dialogue with our stockholders and incorporating their feedback in our compensation decisions is important. One form of feedback from our stockholders is our annual advisory vote to approve the compensation paid to our NEOs, commonly referred to as “say-on-pay.” The Board and the Leadership Development and Compensation Committee of the Board (the “Committee”) reviews and considers the say-on-pay voting results when evaluating our executive compensation programs. At the 2017 Annual Meeting of Stockholders, our stockholders voted to approve, on an advisory basis, the compensation of our NEOs with 98.1% of the voted shares voting “For” the proposal, a slight increase from our prior year’s results. The Board and the Committee viewed this result as a continued strong expression of support by our stockholders for our executive compensation programs.

At the 2017 Annual Meeting of Stockholders, we provided our stockholders with an advisory vote on the frequency of conducting an advisory vote on the compensation of our NEOs. Our stockholders could vote on their preferred voting frequency by choosing the option of one year, two years or three years, or they could abstain from voting. A substantial majority, 77.5%, of votes were to continue an annual advisory vote to approve the compensation paid to our NEOs. While this vote was advisory and not binding on the Board of Directors or the Company, the Board determined to continue the annual advisory vote. This “say-on-pay” frequency vote will be held again in six years.

In addition to regular communication with our stockholders about our business results, we welcome feedback from our stockholders on our executive compensation programs and corporate governance.

13

Executive Compensation Policies and Practices

Our executive compensation program is designed to provide appropriate performance incentives for our executive officers, while avoiding compensation practices that do not promote the interests of our stockholders.

Executive Compensation Governance: What We Do | |||

ü | Maintain a strong alignment between executive compensation and performance. | ü | Require our NEOs to adhere to restrictive covenants upon separation from Supervalu, including non-compete, non-solicitation and non-disclosure obligations. |

ü | Directly link a significant portion of our executives’ incentive opportunities to stock price performance. | ü | Conduct an annual Peer Group review and competitive benchmarking to align executive compensation to market. |

ü | Align executive incentives with both absolute measures of financial and stock price performance, and relative stock price performance. | ü | Review the Committee charter annually to incorporate any new best practices or other changes deemed necessary. |

ü | Maintain stock ownership and retention guidelines. | ü | Limit the amount and number of executive perquisites. |

ü | Maintain a recoupment (or clawback) policy. | ü | Use an independent compensation consultant retained by the Committee. |

Executive Compensation Governance: What We Don’t Do | |||

x | Provide single-trigger change-of-control benefits for any employees. | x | Utilize incentives that motivate excessive risk-taking. |

x | Permit payment of dividends on unearned performance share units. | x | Allow adjustments for option exercise prices (re-pricing) without stockholder approval, except to adjust for stock splits or similar transactions. |

x | Provide for tax gross-ups, whether associated with potential change-of-control golden parachute excise taxes or otherwise. | x | Allow directors or executive officers to pledge, engage in short sales, hedge or trade put and call options with respect to our securities. |

Compensation Philosophy & Pay-for-Performance

Our executive compensation programs are designed to:

• | align our executives’ interests with those of our stockholders by delivering a greater percentage of variable pay as executives reach more senior levels in the organization; |

• | reward strong financial performance, effective strategic leadership and the creation of long-term value for our stockholders; |

• | attract, motivate and retain leaders who help us achieve our objectives; |

• | enhance alignment with our stockholders’ interests and executive retention with the use of multi-year vesting and stock ownership guidelines for our executives; |

• | maintain an emphasis on consistent and sustainable top-line and bottom-line growth, while discouraging excessive risk-taking; and |

• | provide competitive total direct compensation for our executives. |

We believe that our compensation policies and practices are effective in achieving pay-for-performance balance. In keeping with our pay-for-performance philosophy, our fiscal 2018 annual incentive program was tied to the objective performance criteria of Consolidated Sales and Consolidated Adjusted EBITDA, with achievement of a minimum Consolidated Adjusted EBITDA threshold required for any payout on these metrics, plus a performance criterion based on business transformation initiatives. In addition, we make a significant portion of our NEOs’ compensation dependent on the performance of our common stock. As a result, the value of our long-term incentive awards for fiscal 2018 was closely tied to our long-term stock price performance, including our absolute total stockholder return (“TSR”) and our TSR relative to our Peer Group (described below), which we refer to as “Relative TSR.” Both forms of compensation are discussed in more detail later in this CD&A.

Assessing the Competitive Market

We assess our executives’ total target compensation opportunities with reference to the median of the competitive market. In assessing competitiveness, the Committee reviews compensation information from our Peer Group, as well as compensation information available from third-party surveys. This information is used to inform the Committee of competitive pay practices, including the relative mix among elements of compensation. This information is also used to determine, as a point of reference

14

for each NEO, a midpoint (or median) within the competitive compensation range, for base salary, annual incentive, long-term equity incentive and the total of these elements.

The Committee also recognizes that comparative pay assessments have inherent limitations, due to the lack of precise comparability of executive positions between companies, as well as the companies themselves. As a result, the competitive medians are used only as a guide and are not the sole determinative factor for making NEO compensation decisions. In exercising its judgment, the Committee looks beyond the competitive market data and considers individual job responsibilities, individual performance, experience, compensation history, internal comparisons, compensation at former employers (in the case of new hires) and our performance.

The third-party compensation surveys used by the Committee provide data on similarly-sized organizations based on revenue and industry. In fiscal 2018, the Committee referenced comparable positions from our Peer Group, as well as Willis Towers Watson’s Food Industry and General Industry surveys. Both surveys were size-adjusted in determining market median pay for our NEOs.

Peer Group

In April 2017, Exequity LLP (“Exequity”) assisted the Committee in reviewing and updating our Peer Group for fiscal 2018 so that it aligned with our industry (wholesale distribution company with regional retail grocery segments), revenue base (approximately $13 billion in annual revenue at that time) and employee base (approximately 31,000 employees at that time). Based upon the Committee’s assessment of operational comparability, the competitive landscape and our focus on our core Wholesale business, the changes made to our Peer Group for fiscal 2018 were to add Performance Food Group Company, United Natural Foods, Inc., US Foods Holding Corp., Big Lots, Inc., Dollar General Corporation and Dollar Tree Inc., and remove Publix Super Markets, Inc., Toys “R” Us, Inc. and Whole Foods Markets, Inc. The Committee believes that this group of companies represents a highly appropriate mix of size-relevant distributors (both food-oriented and more broadly) available for benchmarking pay for our NEOs for fiscal 2018.

Our fiscal 2018 Peer Group consisted of 15 companies that have median revenues of approximately $13 billion.

Fiscal 2018 Peer Companies | |

Big Lots, Inc. | SYNNEX Corporation |

Core-Mark Holding Company, Inc. | Sysco Corporation |

Dollar General Corporation | Tech Data Corporation |

Dollar Tree, Inc. | United Natural Foods, Inc. |

Office Depot, Inc. | US Foods Holding Corp. |

Performance Food Group Company | WESCO International Inc. |

SpartanNash Company | W. W. Grainger, Inc. |

Staples, Inc. | |

15

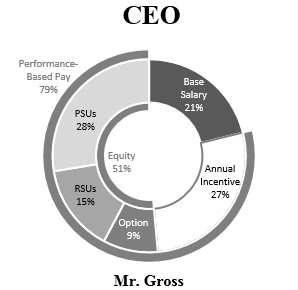

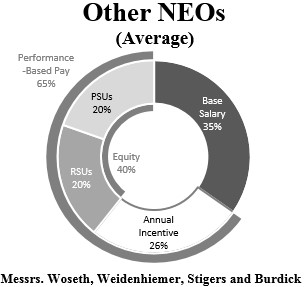

Fiscal 2018 Named Executive Officer Pay Mix

Our executive compensation program directly links a substantial portion of our executives’ compensation to our performance through our annual bonus and long-term incentive plans. Total direct compensation includes base salary, target annual incentive compensation and the grant value of long-term incentive compensation. The mix of targeted total direct compensation elements for our Chief Executive Officer (“CEO”) and our other continuing NEOs is below, with each element of compensation described as a percentage of targeted total direct compensation.

Our compensation programs are structured to align the interests of our executive officers with the interests of our stockholders. Seventy-nine percent (79%) of Mr. Gross’s targeted total direct compensation is tied to Company performance and stock price. On average, 65% of the targeted total direct compensation for our other continuing NEOs is tied to Company performance and stock price. These percentages reflect our commitment to aligning the interests of our executives with those of our stockholders by delivering progressively higher amounts of at-risk pay to our CEO and other NEOs.

Compensation Oversight and the Role of Executive Officers

Our annual review of executive compensation occurs at the April meeting of the Committee and the Board. As delegated by the Board, compensation for our NEOs is reviewed and approved by the Committee and, with respect to the CEO, ratified by the independent members of the Board. As part of that review, the Committee takes into consideration competitive market analyses, annual performance evaluations and the recommendations of our Chief Human Resources Officer (which for fiscal 2018 was an Interim Chief Human Resources Officer), the Committee’s independent compensation consultant(s) and, other than with respect to the CEO’s pay, the CEO. The Committee annually reviews the relationship of target compensation levels for each NEO relative to the median pay levels of executives at companies in our Peer Group for base salary, annual incentives and long-term incentive compensation and relative to the compensation target for the CEO. The Committee also annually reviews internal equity relationships for comparable positions across the Company. With respect to the compensation of our CEO, the CEO does not participate in any such approval or ratification.

Significant Compensation Decisions

Fiscal 2018

• | Annual Incentive Plan: We revised the structure of our annual incentive plan for fiscal 2018. For fiscal 2018, all executive officers participated under the same annual incentive plan rather than having different metrics and payouts for our business segment leaders. The plan contained three metrics: Consolidated Adjusted EBITDA, Consolidated Sales and our Business Transformation metric. Consistent with practices among our Peer Group, we also set the performance threshold for our Consolidated Adjusted EBITDA qualifier to 85% of target. We believe this threshold aligned with our peers and took into account the highly competitive grocery environment. The qualifier applied to payouts on the Consolidated Adjusted EBITDA and Consolidated Sales metrics. Our fiscal 2018 annual incentive plan structure reflects our desire to simplify the compensation programs for our executive officers. |

• | Long-Term Incentive Plan: We continued the use of performance share units (“PSUs”) in fiscal 2018. The Committee felt that our long-term incentives (“LTI”) for fiscal 2018 should even more closely align with stock price improvements given our ongoing strategic transformation. As a result, the PSU awards granted for fiscal 2018 were tied to relative and absolute TSR growth metrics. In addition to the PSUs, our LTI plan for fiscal 2018 included restricted stock unit (“RSU”) grants similar to fiscal 2017. |

16

At the time of the fiscal 2018 LTI grants in April 2017, the Committee believed that we had made strong progress and built momentum towards achieving our strategic vision. Additionally, our NEOs continued to engage in several key initiatives intended to continue to execute on our vision and transform the business for the benefit of our stockholders. As a result, the Committee increased the value of PSUs granted to our NEOs in fiscal 2018. The incremental amounts of the PSU awards varied by NEO, as detailed in the “Annual Incentive Plan Targets and Payouts for our NEOs” table below, and was determined based on a variety of factors, including then-current incentive compensation, scope of responsibilities and role in driving our strategic transformation.

Pursuant to his employment agreement, Mr. Gross received a $500,000 grant of stock options for fiscal 2018. Additionally, Mr. Gross received a PSU award (target value of $1,500,000) and a time-based RSU award ($800,000) to retain Mr. Gross and to further incentivize his progress towards our business transformation, which grants were incremental to the fiscal 2018 LTI target grant value initially established for Mr. Gross. Similarly, each of Messrs. Stigers and Weidenheimer received a RSU award ($100,000) that was incremental to the fiscal 2018 LTI target grant value established for each of them, in consideration of each of their contributions and responsibilities in driving new affiliations for our Wholesale business.

• | CEO & NEO Pay Changes: In April 2017, the Committee approved, and the independent members of our Board ratified, increases to Mr. Gross’s base salary (from $1,000,000 to $1,150,000 effective April 23, 2017) and target bonus opportunity percentage (from 100% to 130% of base salary; retroactive to the beginning of fiscal 2018). These increases were provided in recognition of Mr. Gross’s performance in his first year as President and Chief Executive Officer and to more closely align his total direct compensation with the median CEO compensation of the Peer Group and the general industry. The Committee also approved base pay increases for Messrs. Woseth and Stigers as detailed under “Total Direct Compensation for our Executive Officers — Base Salaries” below, while reducing the target LTI award value for Mr. Woseth by $40,000. The Committee also approved increasing the target LTI award value for Mr. Burdick by $50,000. These pay changes were made in recognition of each executives’ contributions to our business and strategic transformation and to better align their total direct compensation with the market. |

Named Executive Officers no longer with the Company

• | Bruce H. Besanko: In connection with Mr. Besanko voluntarily leaving the Company in July 2017, he was not eligible for an annual bonus payout and forfeited any unvested equity awards that were outstanding. |

Fiscal 2019

• | NEO Pay Changes: Effective February 25, 2018, Mr. Woseth was named Executive Vice President and Chief Financial Officer. In connection with this election, the Committee approved the following changes to Mr. Woseth’s compensation: (i) Mr. Woseth’s annual base salary was increased from $500,000 to $550,000 effective with the first pay period following the date of his appointment; and (ii) Mr. Woseth’s target LTI grant value for fiscal 2019 increased to $675,000. Mr. Woseth’s target annual incentive for fiscal 2019 remained 75% of his base salary, but will be calculated based on his increased base salary of $550,000. In March 2018, the Committee approved an increase to Mr. Stigers’ base salary (from $525,000 to $575,000 effective June 4, 2018). The increase was provided in recognition of his performance and to more closely align his total direct compensation with the market median compensation for similarly situated executives in our Peer Group. |

• | Annual Incentive Plan: The annual incentive plan for fiscal 2019 is very similar to that of fiscal 2018 and continues to utilize the three metrics of Consolidated Adjusted EBITDA, Consolidated Sales and Business Transformation. For fiscal 2019, we continue to apply a Consolidated Adjusted EBITDA qualifier as a performance threshold for any payout on the Consolidated Adjusted EBITDA and Consolidated Sales metrics, which qualifier was increased to 88% of target for fiscal 2019. |

• | Long-Term Incentive Plan: To further align our executive compensation with stockholders, all equity awards to our NEOs under our LTI plan for fiscal 2019 are in the form of PSUs. Approximately half of each NEO’s PSU award will be earned based on the achievement of three strategic metrics and the remaining portion of each NEO’s PSU award will be earned based on the achievement of certain Supervalu stock price performance levels. The grant value for each NEO’s PSU award in fiscal 2019 was increased in acknowledgement of the demand that has been and will continue to be placed on each NEO to achieve our fiscal 2019 goals and continue our transformation. The Committee believes these PSU awards further focus our executive team on driving stock performance and delivering long-term value to our stockholders. |

• | Peer Group: For fiscal 2019, we adjusted our Peer Group to (1) place a heavier emphasis on distribution; (2) take into account that our recent acquisitions have resulted in our revenue exceeding the median of the fiscal 2018 Peer Group; and (3) increase the number of peer companies to 18. |

17

Total Direct Compensation for our Executive Officers

The fundamental elements of our fiscal 2018 executive compensation program and the key characteristics and objective(s) of each element are presented in the following sections.

Base Salaries

We pay our NEOs and other executives an annual base salary that is intended to provide executives with a competitive fixed component of pay to support retention and recruitment of executive talent. Base salary levels for our NEOs are based on individual performance and experience, job responsibility and internal equity, and also take into consideration the competitive market median. We do not guarantee salary adjustments on an annual basis. During April of each year, the Committee considers adjustments to base salary as a part of our overall compensation assessment for our executives. For fiscal 2018, the Committee determined that base salaries for Messrs. Gross, Woseth and Stigers would be increased as detailed below to better align pay internally and with market median levels. The effective date of these increases was April 23, 2017 for the CEO and June 4, 2017 for the other NEOs.

Base Salary Changes for our Continuing NEOs

NEO | Fiscal 2017 Base Salary(1) | Fiscal 2018 Base Salary(1) | % Change |

Mark Gross | $1,000,000 | $1,150,000 | 15.0% |

Rob N. Woseth | $420,000 | $500,000 | 19.0% |

James W. Weidenheimer | $575,000 | $575,000 | 0.0% |

Michael C. Stigers | $475,000 | $525,000 | 10.5% |

Randy G. Burdick | $550,000 | $550,000 | 0.0% |

(1) Represents end of fiscal year base salary amounts. | |||

Annual Incentive Plan

We provide our executives with annual incentive compensation through plans that are designed to align a significant portion of their total cash compensation with the financial and strategic performance of the Company. Each executive is assigned a target amount of annual incentive compensation as part of his or her total cash compensation, but the amount of annual incentive compensation paid depends on the performance of the Company.

Annual incentive targets. Target amounts of annual incentive compensation for our NEOs were determined based on job responsibilities, internal parity, alignment with Peer Group pay levels and input from the Committee’s independent compensation consultant. The Committee established annual minimum, target and maximum bonus opportunities expressed as a percentage of base salary for each NEO in fiscal 2018, which were then ratified by the independent members of the Board for the CEO. The Committee’s objectives were to set targets such that total cash compensation (base salary and annual incentive at target) was generally aligned with the Peer Group median for each role, with a substantial portion of compensation linked to Company performance. Individuals with greater job responsibilities or scope generally had a greater proportion of their total cash compensation tied to Company performance through the annual incentive plan.

Annual incentive metrics. Performance metrics for our fiscal 2018 annual incentive plan for NEOs were Consolidated Adjusted EBITDA, Consolidated Sales and a new Business Transformation (“BT”) metric. In fiscal 2018, all NEOs participated in the same annual incentive plan to align focus, resources and efforts across our functional teams.

Consolidated Adjusted EBITDA Metric. Our Consolidated Adjusted EBITDA metric creates a focus on delivering strong bottom-line performance while reinforcing the importance of balancing growth and profitability. Consolidated Adjusted EBITDA is a qualifier metric for our 2018 annual incentive plan, such that no payouts under the plan for the Consolidated Sales or the Consolidated Adjusted EBITDA metrics occur unless the minimum Adjusted EBITDA performance threshold of eighty five percent (85%) of strike zone performance target is met (regardless of the results underlying the sales metric). We utilized a range, or “strike zone,” for our performance target in fiscal 2018 due to the stretch nature of the target and our expected variability in performance as we transform our business in a competitive industry. The dollar amounts of the strike zone target performance are provided below under “— Annual incentive performance.”

Adjusted EBITDA is a non-GAAP measure (as defined below). We use Adjusted EBITDA to analyze underlying core business trends, to understand operating performance and for compensation purposes. We believe Adjusted EBITDA performance provides our management and investors with useful supplemental information, such as additional understanding of the underlying factors and trends affecting our core business. See “Supplemental Non-GAAP Financial Information Used In Compensation Performance Metrics” below for additional detail on this non-GAAP measure.

18

Consolidated Sales Metric. Our Consolidated Sales metric consists of the combined net sales of our Wholesale and Retail businesses in fiscal 2018. This metric emphasizes driving top-line growth across our Company, including maintaining customers, affiliating new customers and continuing our strategic efforts around business growth.

Business Transformation Metric. The BT metric was added for the fiscal 2018 annual incentive plan to further align our executive compensation with our focus and priority on transforming our business and becoming the wholesale supplier of choice for grocery retailers across the United States. The BT metric provides for payouts independent of the Consolidated Adjusted EBITDA qualifier. Performance under the BT metric can include accomplishing or making significant progress towards:

• | evolving Supervalu to the business of the future including through thoughtful acquisitions or divestitures; |

• | driving top-line growth through notable new customer affiliations, expansion of new businesses or products or meaningful expansion with current customers; and |

• | simplifying our business and efficiently using capital and reducing overhead expense. |

Metrics for all executives are tracked regularly, are well understood and our executives can deliver against these metrics by taking actions to improve operating performance.

Annual Incentive Plan Metrics, Weightings and Payout Levels for our NEOs

Metric | Metric Weight | Threshold Payout | Target Payout | Maximum Payout |

Consolidated Adjusted EBITDA* | 50% | 35% | 100% | 200% |

Consolidated Sales | 30% | 25% | 100% | 200% |

Business Transformation | 20% | 0% | 100% | 200% |

*Note: Metric represents a plan qualifier for NEOs. If the plan qualifier threshold is not met, no payments are made under the plan for the Consolidated Adjusted EBITDA metric or the Consolidated Sales metric.

The threshold and maximum level of performance for Consolidated Adjusted EBITDA was widened from 95% – 105% of target in fiscal 2017 to 85% – 115% of target for fiscal 2018 to better align with market and peers and to recognize the highly competitive grocery environment. The threshold and maximum level of performance for Consolidated Sales was 90% – 110% of target for fiscal 2018.

Annual incentive performance. The amount paid to an NEO under the annual incentive plan for fiscal 2018 may range from 0% to 200% of the NEO’s prorated target amount for that year. The fiscal 2018 targets that the Committee established for the performance metrics were intended to encourage our executives to meet or exceed operational goals. At the time the performance targets were set, the target goals were characterized as stretch goals, meaning that depending on our ability to grow sales and Adjusted EBITDA while controlling our costs, this level of performance was uncertain, but could reasonably be achieved. The following table illustrates the target and actual performance attained during fiscal 2018:

Annual Incentive Plan Metric Performance for our NEOs

Metric Weight | Threshold | Target | Maximum | Results | Metric Performance | Weighted Payout | |

Metric | (dollars in millions) | ||||||

Consolidated Adjusted EBITDA | 50% | $383 | $450 - $474 | $545 | $442 | 93% | 46% |

Consolidated Sales | 30% | $11,852 | $13,169 | $14,486 | $13,055 | 94% | 28% |

Business Transformation (BT) | 20% | See Performance below | 200% | 40% | |||

Total | 100% | 114% | |||||

The Committee reviewed our performance under the BT metric against its design to incentivize transformational growth that will strengthen the Company and benefit our stockholders over the long-term. The Committee approved a 200% payout on the BT metric based on significant accomplishments achieved in fiscal 2018. As detailed above under “— Strategic Transformation and Initiatives,” we continued to significantly transform our business in fiscal 2018 including:

• | completing the acquisitions of Unified and AG Florida. These transactions added $4.3 billion of annual net sales. We have also made significant progress in integrating these companies and realizing the expected synergies, including increasing the targeted synergies from $76 million to $96 million to be achieved by the end of the third year following the respective closings; |

19

• | aligning our distribution network, with the completed acquisitions of distribution centers in Harrisburg, Pennsylvania and Joliet, Illinois, in addition to the facilities owned and operated by Unified and AG Florida. Among other benefits, our network alignment will help expand Market Centre across the United States; |

• | progressing significantly toward the sale of Farm Fresh and pursuit of the sales of Shop ‘n Save and Shop ‘n Save East; and |

• | retaining our Wholesale customer base. |

Annual Incentive Plan Targets and Payouts for our NEOs

NEO | Base Salary (fiscal 2018 year-end) | Incentive Target as % of Base Salary | Incentive Target in Dollars | Payout Percentage | Payment Earned |

Mark Gross(1) | $1,150,000 | 127% | $1,465,000 | 114% | $1,676,854 |

Rob N. Woseth(2) | $500,000 | 72% | $358,846 | 114% | $410,739 |

James W. Weidenheimer | $575,000 | 75% | $431,250 | 114% | $493,613 |

Michael C. Stigers(3) | $525,000 | 73% | $383,653 | 114% | $439,135 |

Randy G. Burdick | $550,000 | 75% | $412,500 | 114% | $472,152 |

Bruce H. Besanko(4) | $268,269 | 100% | $268,269 | 0% | $0 |

(1) | Mr. Gross’s base salary increased from $1,000,000 to $1,150,000 effective April 23, 2017 and his incentive target adjusted from 100% to 130%, with his bonus target adjustment retroactive to the beginning of the fiscal year. |

(2) | Mr. Woseth’s base salary increased from $420,000 to $500,000 effective June 4, 2017 and his incentive target remained at 75%. |

(3) | Ms. Stigers’s base salary increased from $475,000 to $525,000 effective June 4, 2017 and his incentive target remained at 75%. |

(4) | Mr. Besanko left the Company on July 5, 2017 and his base salary has been adjusted to reflect this departure before the end of fiscal 2018. He did not receive a payout associated with his annual incentive plan for fiscal 2018. |

Annual incentive plan metric adjustments. In April of each year, following preparation of our consolidated financial statements, the Committee reviews our performance and determines the extent to which performance goals under the annual incentive plan are met. In making its determination, the Committee may make discretionary adjustments to our originally established targets or to our results such that our performance results may differ from the numbers reported in our financial statements. In applying these discretionary adjustments, the Committee may exclude all or a portion of both the positive or negative effect of external events that are outside the control of our executives, such as natural disasters, litigation or changes in accounting or taxation standards.

For fiscal 2018, the Committee did not make any adjustments to the targets set under the fiscal 2018 annual incentive plan but did approve two discretionary adjustments to results, which the independent members of the Board ratified with respect to the CEO’s annual incentive payout. The two discretionary adjustments affected both the Consolidated Adjusted EBITDA and Consolidated Sales results as outlined in the table below. The results were objectively calculated based on our original plan for these metrics and then adjusted to: (1) remove the Consolidated Sales and Consolidated Adjusted EBITDA from Unified and AG Florida, which were acquired during the year and not considered when adopting the fiscal 2018 bonus targets; and (2) include the results of operations from our retail stores that were classified in the fourth quarter of fiscal 2018 as assets held for sale and reported in our consolidated financial statements within discontinued operations (Farm Fresh, Shop ‘n Save (based in St. Louis) and Shop ‘n Save East (with stores in West Virginia, Maryland, Pennsylvania and Virginia)).

Adjustments to Results under Fiscal 2018 Annual Incentive Plan

(dollars in millions) | Consolidated Adjusted EBITDA | Consolidated Sales |

Reported Results | $436 | $14,157 |

Discontinued Operations Adjustment | $42 | $1,522 |

Unified Acquisition Adjustment | $(31) | $(2,492) |

AG Florida Acquisition Adjustment | $(5) | $(132) |

Bonus Performance Results | $442 | $13,055 |

20

Long-Term Incentives and Other Stock-Based Awards

We provide long-term incentive compensation opportunities to reinforce the link between the interests of our executives and stockholders. The awards are intended to motivate our executives to improve financial performance over multiple years, to reward our executives for achieving long-term objectives and to drive retention. The awards are also an important component in making our compensation program competitive with the market, yet represent a variable, at-risk pay component that meets the objectives of our compensation philosophy.

We currently grant all LTI and other stock-based awards under our amended and restated SUPERVALU INC. 2012 Stock Plan (the “2012 Stock Plan”) that was approved by our stockholders at our 2016 Annual Meeting of Stockholders. In April of each year, the Committee reviews and approves annual grants of stock-based awards to equity-eligible employees. LTI amounts for our NEOs are informed by internal equity considerations, as well as survey and Peer Group data. For fiscal 2018, the Committee approved our annual LTI compensation in the form of PSUs and RSUs, as well as stock options for our CEO pursuant to his employment agreement, as follows:

50% of initial annual LTI target value in the form of PSUs. We continually review our LTI program to align our executives with our long-term stockholders’ interests and strategic objectives. As part of this review and after considering recent LTI compensation data from companies inside and outside our Peer Group, we continued to utilize PSUs in our LTI program for fiscal 2018. In fiscal 2018, PSUs represented 50% of the initial annual target value for LTI. In addition, for fiscal 2018 the Committee considered the importance of retaining our NEOs as we continued to engage in several key initiatives to transform our business for the benefit of our stockholders, against the retentive value of outstanding awards.

As a result of that review, the Committee increased the target value of PSUs to our NEOs in fiscal 2018. The incremental amount of the PSU awards varied by NEO and was determined based on a variety of factors, including current incentive compensation, scope of responsibilities and role in driving our strategic transformation. Any payouts for the PSUs granted in fiscal 2018 are formulaically determined as discussed below and cliff vest after three years if the Company achieves the pre-determined performance thresholds. An NEO may forfeit all or a portion of the PSUs if he or she does not remain employed by the Company throughout the three-year performance period.

50% of initial annual LTI target value in the form of time-vesting RSUs. RSUs reward and retain NEOs by offering the opportunity to receive Supervalu common stock if they remain employed through the vesting period. RSUs vest 34% on the first anniversary of the grant date and 33% on the second and third anniversaries of the grant date. As part of the review discussed above, the Committee increased the RSU value for Messrs. Weidenheimer and Stigers in recognition of their contributions to our performance, as well as their responsibilities in continuing to transform our business and drive new Wholesale affiliations.

The table below summarizes the grant date value of our long-term incentive awards for fiscal 2018. These awards reflect a blend of considerations, including market value for the NEO’s role, the need for strong incentives that facilitate improved performance, enduring retention, as well as internal equity. Importantly, these grant date values are opportunities not realized values. The ultimate amount realized from these awards may vary substantially as driven by performance against specific financial and total shareholder return goals, as well as the long-term performance of our stock. The realizable value of these awards are directly aligned with shareholder value.

Long-Term Incentive Grants for our NEOs

NEO | Performance Share Units | Restricted Stock Units | Non-Qualified Stock Options | Total Fiscal 2018 LTI Target Value | PSUs | RSUs | Stock Options | |||||||||

(in shares) | ||||||||||||||||

Mark Gross | $ | 1,500,000 | $ | 800,000 | $ | 500,000 | $ | 2,800,000 | 51,387 | 27,407 | 35,903 | |||||

Rob N. Woseth | $ | 452,500 | $ | 317,500 | $ | — | $ | 770,000 | 15,502 | 10,877 | — | |||||

James W. Weidenheimer | $ | 442,500 | $ | 412,500 | $ | — | $ | 855,000 | 15,160 | 14,132 | — | |||||

Michael C. Stigers | $ | 442,500 | $ | 412,500 | $ | — | $ | 855,000 | 15,160 | 14,132 | — | |||||

Randy G. Burdick | $ | 375,000 | $ | 275,000 | $ | — | $ | 650,000 | 12,847 | 9,421 | — | |||||