Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - I-ON Digital Corp. | ex31_1.htm |

| EX-32.1 - EXHIBIT 32.1 - I-ON Digital Corp. | ex32_1.htm |

| EX-21.1 - EXHIBIT 21.1 - I-ON Digital Corp. | ex21_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______________to ______________

Commission File Number 000-549995

|

I-ON COMMUNICATIONS CORP.

|

(Exact name of registrant as specified in its charter)

(formerly known as Evans Brewing Company Inc.)

|

Delaware

|

46-3031328

|

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

(I.R.S. Employer Identification Number)

|

|

15, Tehran-ro 10-gil, Gangam-gu, Seoul, Korea

|

|

06234

|

|

(Address of Principal Executive Offices)

|

|

(Zip Code)

|

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

|

Name of each exchange on which registered

|

|

|

|

|

|

Common Stock, par value $0.001 per share

|

|

OTC Markets LLC

|

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirement for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

|

Non-accelerated filer ☐

|

Smaller reporting company ☒

|

|

(Do not check if a smaller reporting company)

|

Emerging growth company ☐

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

As of June 30, 2017 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the common stock held by non-affiliates of the registrant was approximately $1.15 million based on the closing sales price of $2.05 on the OTC Markets. All executive officers and directors of the registrant have been deemed, solely for the purpose of the foregoing calculation, to be “affiliates” of the registrant.

As of June 8, 2018, there were approximately 34,930,339 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

None.

|

PART I

|

|

Page

|

|

|

|

|

|

Item 1.

|

2 | |

|

Item 1A

|

12 | |

|

Item 1B

|

20 | |

|

Item 2.

|

20 | |

|

Item 3.

|

20 | |

|

Item 4.

|

20 | |

|

|

|

|

|

PART II

|

|

|

|

|

|

|

|

Item 5.

|

21 | |

|

Item 6.

|

25 | |

|

Item 7.

|

25 | |

|

Item 7A

|

29 | |

|

Item 8.

|

29 | |

|

Item 9.

|

29 | |

|

Item 9A

|

29 | |

|

Item 9B.

|

29 | |

|

|

|

|

|

PART III

|

|

|

|

|

|

|

|

Item 10.

|

30 | |

|

Item 11.

|

30 | |

|

Item 12.

|

31 | |

|

Item 13.

|

32 | |

|

Item 14.

|

33 | |

|

|

|

|

|

PART IV

|

|

|

|

|

|

|

|

Item 15.

|

35 | |

|

|

|

|

| 36 | ||

PART I

|

|

SPECIAL NOTE ON FORWARD-LOOKING STATEMENTS

The information in this report contains forward-looking statements. All statements other than statements of historical fact made in this report are forward looking. In particular, the statements herein regarding industry prospects and future results of operations or financial position are forward-looking statements. These forward-looking statements can be identified by the use of words such as “believes,” “estimates,” “intends”, “plans”, “could,” “possibly,” “probably,” anticipates,” “projects,” “expects,” “may,” “will,” or “should,” “designed to,” “designed for,” or other variations or similar words or language. No assurances can be given that the future results anticipated by the forward-looking statements will be achieved. Forward-looking statements reflect management’s current expectations and are inherently uncertain. Our actual results may differ significantly from management’s expectations.

Although these forward-looking statements reflect the good faith judgment of our management, such statements can only be based upon facts and factors currently known to us. Forward-looking statements are inherently subject to risks and uncertainties, many of which are beyond our control. As a result, our actual results could differ materially from those anticipated in these forward-looking statements as a result of various factors, including those set forth below under the caption “Risk Factors.” For these statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. You should not unduly rely on these forward-looking statements, which speak only as of the date on which they were made. They give our expectations regarding the future but are not guarantees. We undertake no obligation to update publicly or revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by law.

|

|

Organization and Corporate History

I-ON Communications, Corp. (formerly known as Evans Brewing Company, Inc.) was incorporated under the laws of the State of Delaware on June 18, 2013 as ALPINE 3 Inc. Alpine 3 Inc. was set up to serve as a vehicle to effect an asset acquisition, merger, exchange of capital stock or other business combination with a domestic or foreign business. ALPINE 3 did not undertake any effort to cause a market to develop in its securities, either debt or equity, before it successfully concluded a business combination. On April 4, 2014, The Michael J. Rapport Trust (the “Trust”) purchased 10,000,000 shares of common stock which was all of the outstanding shares of Alpine 3, Inc., and subsequently changed the name to Evans Brewing Company Inc. (“EBC”) on May 29, 2014. On October 9, 2014 the Trust agreed to the cancellation of 9,600,000 of the shares of common stock that it had acquired and retained 400,000 shares of common stock.

On October 15, 2014, Bayhawk and EBC entered into an Asset Purchase and Share Exchange Agreement (the “Agreement”), subject to receiving approval of the independent Bayhawk shareholders who voted on the transaction. On September 17, 2015, the independent Bayhawk shareholders approved the agreement by a vote of 251,212 shares for and 1,600 shares against. As such, Bayhawk sold to EBC, and EBC purchased from Bayhawk, assets of Bayhawk, including but not limited to: (A) all assets, including personal property, intellectual property, inventory, contracts, websites, documents, and all other assets however delineated relating to the Bayhawk Ales label (as defined in the Agreement and discussed in more detail below); and (B) all assets, including personal property, intellectual property, inventory, contracts, websites, documents, and all other assets however delineated relating to the Evans Brands (as defined in the Agreement and discussed in more detail below) (collectively, the “Transferred Assets”). Bayhawk retained ownership of 100% of the stock in Evans Brewing Co. (CA) (“Evans Brewing California”) which has the brewers license at City Brewery in Lacrosse, WI (where the non-craft brands will be brewed, with the balance of the craft brands being brewed in Irvine, California). Based on the affirmative vote by the independent Bayhawk shareholders to approve the Asset Purchase transaction, EBC proceeded with the share exchange and tender offer to the Bayhawk shareholders, pursuant to which EBC offered to exchange shares of EBC common stock for shares of Bayhawk common stock, on a one-for-one basis (the “Exchange Offer”). Bayhawk shareholders had until December 2, 2015, to tender their Bayhawk shares in the share exchange. Bayhawk shareholders also had until December 2, 2015, to rescind the exchange of shares. There was no minimum number of shares of Bayhawk common stock that must be tendered for the Exchange Offer to close. At the close of the share exchange on December 2, 2015, Premier Stock Transfer accepted on behalf of EBC 4,033,863 Bayhawk shares and issued 4,033,863 shares of EBC common stock upon the terms and subject to the conditions set forth in the Asset Purchase and Share Exchange Agreement by and between EBC and Bayhawk, dated October 15, 2014, as amended (the “Asset Purchase Agreement”). EBC filed a copy of the Asset Purchase Agreement as an annex to a combination registration statement and proxy statement on Form S-4. The Bayhawk shares were validly tendered pursuant to the Exchange Offer and not withdrawn. The asset purchase and share exchange will be treated as business combination as both companies are controlled by the same management.

On January 25, 2018, Evans Brewing Company, Inc. consummated an Agreement of Merger and Plan of Reorganization (the “Merger Agreement”), with I-ON Communications Co., Ltd., a company organized under the laws of the Republic of Korea (South Korea) (“I-ON”) and I-ON Acquisition Corp., a wholly-owned subsidiary of the Company (“Acquisition”). Pursuant to the terms of the Merger Agreement, Acquisition merged with and into I-ON in a statutory reverse triangular merger (the “Merger”) with I-ON surviving as a wholly-owned subsidiary of the Registrant. As consideration for the Merger, the Registrant agreed to issue the shareholders of I-ON (the “I-ON Holders”) an aggregate of 26,000,000 shares of our common stock, par value $0.001 per share (the “Common Stock”) in accordance with their pro rata ownership of I-ON capital stock. Following the Merger, the Registrant adopted the business plan of I-ON in information technology consultancy and software development. On December 14, 2017, in connection with the Merger, the Registrant’s Board of Directors approved an amendment to its Certificate of Incorporation (the “Amendment”) to change its name to I-ON Communications Corp.

At the effective time of the Merger, our board of directors and officers were reconstituted by the appointment of Jae Cheol James Oh as Chairman, Chief Executive Officer, and Chief Financial Officer, Hong Rae Kim as Executive Director and Jae Ho Cho as Director. Michael Rapport resigned as President, Chief Executive Officer, and Chairman in connection with the Transaction and Evan Rapport resigned as Vice President and Director, Kenneth Wiedrich resigned as Chief Financial Officer and Director and Kyle Leingang resigned as Secretary. Roy Robertson, Mark Lamb, Joe Ryan, and Kevin Hammons resigned as members of the Board of Directors and their respective committees.

Evans Brewing Company

As of the period covered by this report, I-ON Communications Corp., formerly known as Evans Brewing Company Inc. (“EBC”) was a craft brewery based on Orange County, California that produces and sells premium craft beers, including a variety of ales and lagers. EBC’s beers are currently produced in its 17-barrel brewery in Irvine, California, the oldest continuously operating brewing facility in Orange County and one of the oldest in all of Southern California. This facility has been producing craft beers since January 1995. The brewery is located in a leased building in the McCormick & Schmick’s Seafood Restaurant.

EBC products include four beers that are packaged year-round (Pollen Nation Honey Blonde Ale, The KrHOPen India Pale Ale, Oaklore Brown Ale, and ChocōLatté Chocolate Porter), various draft-only offerings (which include The Joaquin Dead Mexican Red Ale, OC Pale Ale, Son of a Beach Blonde Ale), and seasonal beers (which include Approachable Bastard Session IPA, Stout at the Devil Russian Imperial Stout, crHOP Dust Hefeweizen, and Oktoberfest). EBC’s labels for its year round packaging were approved in 2016 and the beers are currently being sold with these labels. EBC has the exclusive rights to make, manufacture, produce, market, sell, and distribute original beers, lagers, and ales known as Evans Lager Original, Evans Lager Black, Evans Lager Light, Bad Kat Ice, and Dead Presidents. EBC also owns the assets of Pig’s Eye Brewing Company, LLC, (the “EBC Malt Assets”) including the intellectual property and trademarks relating to original beers, lagers, and ales, including Milwaukee Select and Pig’s Eye (the “EBC Malt Brands”). EBC’s products are distributed to restaurants and other retail outlets in nine states. EBC also produces and packages kegged beer on a private label basis for restaurants and other customers, with the names for such products determined collaboratively with such customer and each product co-branded with the phrase “by Evans Brewing Company”.

In addition to manufacturing and selling the products above, EBC also produces and packages beers for other craft breweries in Southern California on a contract-basis. Further, in addition to beer production and sales generally, EBC also produces and offers for sale certain “Evans Brewing Company” branded merchandise including apparel, glassware and other beer accessories.

On September 29, 2016, Evans Brewing Company, Inc., closed the acquisition of a restaurant business located in the downtown SOCO District of Fullerton, California, through the acquisition of all the outstanding stock of EBC Public House, Inc., which the Company now operates as its first branded restaurant and taproom under the trade name “The Public House by Evans Brewing Company”. The Public House features the Company’s beers – as well as beers from other selected local Orange County, California breweries, -- food and, potentially, occasional entertainment.

In connection with such closing, the Company acquired 100% of the outstanding shares of EBC Public House from Mr. Rapport and issued 1,000,000 shares of the Company’s Series A Preferred Stock to Mr. Rapport. The asset purchase and share exchange have been treated as business combination as both companies are controlled by the same management.

Background

EBC and Bayhawk filed a registration statement on Form S-4 with the U.S. Securities and Exchange Commission (the “Registration Statement”), which went effective on August 10, 2015. The Registration Statement included a proxy statement seeking the votes of the Bayhawk shareholders on the Asset Purchase Transaction by written consent. On September 17, 2015, the voting period closed, and EBC announced that approximately 99% of the shares that were voted had voted in favor of the Asset Purchase Transaction.

In connection with the Asset Purchase Transaction, EBC and Bayhawk entered into a General Assignment and Bill of Sale agreement (the “Bill of Sale”) which outlined the specific assets purchased, as well as an Assignment and Assumption of Liabilities agreement (the “Assumption Agreement) which outlined the specific liabilities of Bayhawk assumed by EBC.

In connection with the closing of the Asset Purchase Transaction and the entry into the Bill of Sale and the Assumption Agreement, EBC acquired the assets (other than the ownership of Evans Brewing California), the liabilities, and the operations of Bayhawk. As such, on December 10, 2015, in connection with this acquisition, EBC ceased to be a shell company as defined in Rule 12b-2, in that it had assets consisting of more than cash and cash equivalents, and has a business plan and operations.

Bayhawk Ales

Bayhawk Ales, Inc. (formerly Orange County Brewing Company) (“Bayhawk”) was formed in February 1994 for the purpose of developing and operating one or more breweries in California for the production of high quality, hand-crafted ales for sale in bottle and draft. The Company built a 17-barrel showcase brewery (the "Southern California Brewery") in a leased building in the McCormick & Schmick’s Seafood Restaurant in Irvine, California. The Southern California Brewery, located in the central business district of Irvine near John Wayne International Airport, began brewing beer in January 1995. Irvine is south of Los Angeles and is adjacent to Newport Beach. It is a suburban city of the greater Los Angeles metropolitan area and the location of numerous businesses. At the time of the construction of the Southern California Brewery, the Los Angeles metropolitan area was the largest single market for beer in the United States. The products produced by Bayhawk are 90% private labeled. The business has only recently in the last few years become profitable.

Evans Brewing Company, Inc. (Formerly ALPINE 3, Inc.) was incorporated in Delaware in June 18th, 2013 with a fiscal year ending on December 31st.

Evans Brewing Company, Inc., acquired a restaurant business located in the downtown SOCO District of Fullerton, California, through the acquisition of all the outstanding stock of EBC Public House, Inc., which the Company now operates as its first branded restaurant and taproom under the trade name “The Public House by Evans Brewing Company”. The restaurant was acquired from Michael J Rapport and it features the Company’s beers, as well as beers from other selected local Orange County, California breweries, food and occasional entertainment. The Restaurant is the first in a chain of restaurants to be added by the Company.

PRINCIPAL PRODUCTS

EBC products include four packaged year-round beers: Pollen Nation Honey Blonde Ale, The KrHOPen India Pale Ale, Oaklore Brown Ale, and ChocōLatté Chocolate Porter; draft-only offerings include The Joaquin Dead Mexican Red Ale, OC Pale Ale, Son of a Beach Blonde Ale; and seasonals include Approachable Bastard Session IPA, Stout at the Devil Russian Imperial Stout, crHOP Dust Hefeweizen, and Oktoberfest.

EBC also produces malt liquor at a third party site in Lacrosse, Wisconsin. By way of background, in August 2013, Evans Brewing California had acquired from City Brewing Company, LLC (“City Brewing”) the assets of Pig’s Eye Brewing Company, LLC, (the “Pig’s Eye Assets”) including the intellectual property and trademarks relating to original beers, lagers, and ales, including Milwaukee Select and Pig’s Eye (the “Pig’s Eye Brands”). Additionally, Evans Brewing California had the exclusive rights to make, manufacture, produce, market, sell, and distribute original beers, lagers, and ales known as Evans Lager Original, Evans Lager Black, Evans Lager Light, Bad Kat Ice, and Dead Presidents.

I-ON Communications

Following the Merger, as described more fully herein, the Company adopted the business plan of I-ON. I-ON was founded by Jae Cheol James Oh, who currently serves as CEO. The Company’s roots are in IT consultancy and software development. I-ON services South Korea’s Enterprise Content Management system’s market and specializes in advancing market-leading internet software applications to capitalize on rapidly growing market sectors.

After being awarded its first of 6 patents in 2003, I-ON has since evolved into an industry-leading and recognized software developer and provider of enterprise-class unstructured data management and digital marketing software and solutions. I-ON services over 1,000 blue-chip and middle-market clients across virtually all verticals in both private and public sectors. The Company has meaningfully expanded its reach over the past decade and now currently licenses and sells its products and services directly to clients in South Korea and Japan, as well as in Singapore, Malaysia, Indonesia, Thailand, Vietnam, and the U.S. through value-added resellers and partnerships.

I-ON’s portfolio of software and solutions serves the digital marketing and technology needs of organizations, enabling clients to create, measure, and optimizes digital experiences for their audiences across marketing channels and devices. We believe these solutions help clients reduce the cost of content management and delivery and increase the return on their investments in digital communication.

I-ON currently holds 6 international patents for both products and methodologies (with 3 more pending) built into the 11 product offerings the Company currently has at market. These encompass enterprise web content management systems (CMS), web experience and service delivery software, digital marketing, smart mobility and analytics tools, and, more recently, energy management solutions and sports and IT convergence services. The Company has designed and developed industry-leading technologies that are compliant with global standards including GS (Good Software) and NET (New Excellent Technology). I-ON also holds numerous domestic and global industry awards, earning high rankings and recognition from the likes of Gartner (Magic Quadrant 2014) and Red Herring (2014 Asia Top 100 Winner), among many others.

In addition to South Korea, Japan has particularly helped fuel I-ON’s growth over the past 10 years owing to the success of an exclusive licensing deal with Ashisuto, a large Japan-based technology services firm that employs approximately 800 technical, engineering and marketing staff across 9 office locations. Ashisuto, which has provided technology services to Japan’s enterprises and government entities since 1973, currently white labels and sells I-ON’s core CMS offering ICS6 to over 610 clients as NOREN 6.

As a result of global enterprise digital marketing and I-ON’s 18-year track record in South Korea, Japan and now, Southeast Asia, the Company’s objective is to continue to gain market share in these markets. I-ON will continue to closely engage and consult with existing and prospective clients as their subject matter expert across multiple touchpoints in the digital marketing and technology ecosystem, helping Chief Marketing Officers (CMO) and Chief Information Officers (CIO) drive critical change and growth for their organizations.

I-ON has invested and continues to spend over 15% of total annual revenue on research and development. The Company has grown its total number of employees to approximately 150 as of June 30, 2017, 90% of whom are considered full-time. Research and development is comprised of roughly 100 junior, mid to senior level engineers and developers, most of whom are based at the Company’ headquarters located at 15 Teheran-ro 10-gil, Gangnam-gu, Seoul, South Korea, 06234.

PRODUCTS AND SERVICES

I-ON’s product line is comprised of:

|

Enterprise Web Content Management :

|

Service Delivery Platform (PaaS):

|

|

I-ON Content Server - ICS Gen 6 & 7

|

I-ON Content Application Framework Engine - ICAFE

|

|

I-ON Deploy Server - IDS

|

- broadcasting CSDP

|

|

I-ON Digital Asset Management System - IDAS

|

- mobile content

|

|

I-ON Web Analytics Server

|

- digital content SDP

|

|

I-ON Content Ecosystem - ICE

|

|

|

Software as a Service (SaaS) :

|

Energy Management Solutions :

|

|

Distributed Repository Service - GAIA

|

Load Aggregator’s Management System - LAMS

|

|

iDrive - E-Document Management System

|

- Demand Resource Management

|

|

e.Form - mobile contract platform

|

- Advanced Metering Infrastructure

|

|

Assist9 - mobile ERPdashboard

|

|

|

TAMM - pro-sports marketing & analytics

|

Sports & IT Convergence Service

VoiceBall – Amateur League Umpire & Data Service

Following is a summary description of I-ON’s products:

ICS6 (I-ON Content Server) – ICS6 is I-ON’s generation 6 web content management system that helps reduce burdens of complex website management by organizing vast amounts of ever-increasing digital content and big data into physical directory and logical site structure. ICS6 is one of South Korea’s first-to-market cloud-based CMS platforms and a market share leader in both Korea & Japan.

IDS (I-ON Deploy Server) – IDS, in conjunction with ICS6, securely, conveniently and automatically deploys files and content between servers when distribution inefficiencies and services issues arise.

IDAS (I-ON Digital Asset Management System) – IDAS, in conjunction with ICS6, ensures a virtuous cycle of an organization’s digital assets through an integrated framework that collects, manages, deploys and distributes content. It also provides ample storage and categorization functionalities necessary to address high multi-media content demand including high-resolution video. The software supports digital archiving, scalability and changes in physical environment.

e.Form – e.Form is a one-stop mobile contract solution for smartphones and tablets that digitizes and expedites document creation and execution processes for organizations. The platform supports over 200 application programming interfaces (APIs).

iDrive – iDrive is a SaaS-based EDMS (e-document management system) which centralizes all categories of e-documents within an organization, iDrive is geared for streamlining and managing the e-document lifecycle from creation, approval, archiving to destruction.

iCAFE (I-ON Content Application Framework Engine) – iCAFE is a content delivery platform optimized for N-Screen environments, offering a robust wire-wireless service delivery platform for broadcasting, imaging & mobile content

GAIA – GAIA is a back-end unstructured data repository platform that manages a cloud-based ecosystem that enterprises or individuals can use to build and share mobile applications.

LAMS (Load Aggregator’s Management System) - LAMS is one of South Korea’s first Open ADR 2.0-based demand response management solutions designed to manage and reduce electricity consumption and peak demand through demand response program participation.

ICE (I-ON Content Ecosystem) - ICE is a platform that manages the digital content management lifecycle beginning from creation, registration, distribution, deletion, billing to analytics. ICE is geared for SOs seeking ways to enhance business to business to consumer (B2B2C) value.

TAMM (Ticket Admission Marketing Management) - TAMM is a mobile B2B2C platform that integrates and manages the professional sports event experience from marketing and promotion and ticket purchases and reservations to the delivery of a mobile analytics dashboard for followers. Event organizers/sponsors have included, among others, the LPGA Hana Bank Championship and SK Telecom Open. I-ON acquired the core TAMM developers and intellectual property from South Korea-based MoceanPeople in March 2016.

Assist9 – Assist9 is a mobile all-in-one work flow process and data management dashboard geared towards small and medium-sized businesses and startups. Core functions revolve around ERP, PMS, SFA, HR, and e-approval – with up to fifteen others- and are designed to improve operational efficiencies and provide CEOs with greater analytical insight into their businesses.

ADDRESSABLE MARKETS

South Korea, Japan and Southeast Asia

Econsultancy and Adobe reported in recent studies that less than 15% of CMO respondents identified as working for digital-first organizations, despite a study by Forrester Research that indicated 51% of B2B enterprises were ratcheting up digital marketing initiatives in 2017 and 2018. A key driver of I-ON’s ability to tap further into existing and future addressable markets, the Company believes, will depend on how quickly mid to large enterprises can adopt a digital-first mindset through continued client engagement.

According to many industry researchers, such as Forrester and Gartner, the combined enterprise digital marketing and CMS sector in South Korea and Japan is expected to generate a high single digit compounded annual growth rate to over $800 million by 2020.

Given its market share-leading in both South Korea and Japan, I-ON remains uniquely positioned to serve as a localized partner and to address the evolving marketing needs of mid to large enterprises. CMOs continue to seek new and innovative ways to analyze, improve return on investment (ROI) and justify the value of increased digital marketing spending.

According to numerous industry sources, including Forbes, South Korea has emerged as one of Asia’s fastest growing technology startup hubs, attracting increasing investment from domestic funds and foreign investment.

Today, South Korea remains the eleventh largest economy in the world and, with 51 million people, the twenty-eighth largest population in the world, while boasting the world’s highest broadband penetration at 97%. South Korea was recently highlighted in Bloomberg’s list of most innovative countries, owing to the country’s research and development intensity, as well as productivity and educational standards. Home to Samsung, Hyundai and over 10 other Fortune 500 companies, South Korea, for the past several decades, has also been on a path pivoting from big industry and manufacturing to transformative technology, thanks to government and private/public partnership initiatives. Favorable policy initiatives have recently led to larger budget allocation towards science and technology, matching funds with international investors, establishing international entrepreneurship programs at universities, opening up many of the country’s research institutes, and providing safety nets for technologists and scientists that take capital risk.

Similarly, Japan remains the third largest economy and second largest developed economy in the world, the third largest automobile manufacturing, and the largest electronics goods industry in the world. Despite being home to over 50 Fortune 500 companies, and facing growing competition from China and South Korea, manufacturing and investment in Japan have also pivoted toward software development, high-technology, and precision goods sectors, such as robotics and optical instruments.

Asia-Pacific and Global

Across not only South Korea and Japan, but the entire Asia-Pacific region, businesses and consumers today increasingly demand personalized content and experiences in their online interactions, across multiple digital channels and devices. This is accelerating growth in the CMS and digital marketing arenas as well demand from marketers seeking solutions that optimize customers’ experiences, demonstrate the success of their programs with objective metrics, and deliver the greatest return on their marketing spend.

According to Gartner, the enterprise CMS market across the Asia-Pacific region, which includes China, South Korea, Hong Kong, Japan, Indonesia, Malaysia, Singapore and Vietnam – exceeded $700 million in 2016, up significantly from $500 million in 2014 and is projected to exceed $900 million by 2019, reflecting a compounded annual growth rate of at least 12%. Malaysia, Indonesia and Singapore collectively generated $180 million in enterprise CMS revenue last year and Gartner projects a 16% annual growth rate into 2020.

In North America, aggregate digital marketing spend, which includes CMS for both products and professional services by both mid and large-sized enterprises, exceeded $135 billion in 2016 from approximately $95 billion in 2014, and according to forecasts from both IDC and Statista, is projected to grow 18% annually to over $225 billion by 2019.

Globally, sources such as the CMO Council and Gartner estimate the current web and mobile digital marketing industry size at $450 billion, while forecasting a high single digit 5 year compounded annual growth rate to over $600 billion by 2019.

Between North America, Western Europe and developed economies within the Asia-Pac, the CMO Council currently foresees enterprise CMS implementation, content creation and optimization as representing over 50% of digital marketing spend, while mobile advertising, search engine and social media advertising contribute about 20%, 15% and 15%, respectively.

MARKETING AND GROWTH STRATEGY

Push Defining Value Proposition

I-ON believes it remains uniquely positioned to address the evolving marketing needs of medium to large enterprises.

Given the growth across the global enterprise digital marketing spectrum and I-ON’s 18-year track record serving a marquee clientele in South Korea, Japan, and parts of Southeast Asia, I-ON’s objective is to continue to aggressively gain market share by closely engaging with existing and prospective clients and while driving sales for both its core CMS offering and complementary solutions that enable organizations to transform traditional marketing initiatives into analytics and data-driven strategies vital to delivering measurable results.

I-ON believes that its software products and solutions will continue to be a primary revenue source for the Company over time and that its growing portfolio of products may generate profitable demand for associated maintenance, support, implementation, consulting, and training services that the Company, and a channel of licensees and value-added resellers (VARs), can provide.

Near-term, I-ON intends to do the following to drive organic growth:

| § |

Continue to leverage knowledge and experience into new or enhanced solutions and products

|

| § |

Continue to deploy secure pilot environments for prospective customers to evaluate and envision additional uses for customized application development

|

| § |

Continue to procure contracts directly, via strategic partnerships and increasing sales personnel

|

| § |

Recruit seasoned executives as well as younger talent to utilize unique training model that addresses resource shortages

|

| § |

Incubate and build-out focused profitable technology practices

|

| § |

Continue to participate in multi-lateral joint R&D projects in concert with 28 partners from 7 different countries

|

South East Asia Market Penetration

According to Gartner, Malaysia, Indonesia and Singapore generated $180 million in enterprise CMS revenue last year and project a 16% annual growth rate by 2020. As a result, I-ON intends to continue to build off of its initial successes in the Southeast Asia region, which include, among other projects, the following: implementation of a fully integrated mobile/online trading solution for Malaysia’s MNC Securities; a CMS implementation for a leading USA cable manufacturer, Commscope- supporting 13 languages to meet global standards; the implementation of a CMS solution based on CSDP (Convergence Service Delivery Platform) for Indonesia’s BOLEH Mobile; and an integration of CMS platforms for the Malaysia Ministry of Works.

Acquisition Strategy

I-ON will attempt to continue to leverage its ongoing success in CMS and its international partnerships to move upstream, cross-sell, and serve clients more directly as either their digital strategist of choice and/or by acquiring businesses with (i) a revenue producing platform with existing enterprise clients, (ii) subject matter expertise and or (iii) rights to intellectual property in at least one of the following digital marketing-related disciplines: predictive analytics, smart mobility, marketing automation, search engine optimization (SEO), enterprise resource planning (ERP), workflow automation, and eCommerce. I-ON has already identified multiple compelling acquisition opportunities within these domains, both in South Korea and Japan. However, there can be no assurance that I-ON will be able to acquire one or more of these businesses or that it will be able to do so on terms that are favorable to I-ON.

Notably, I-On believes that overall macro conditions that drive consolidation and acquisitions also remain ideal for I-ON including the historical low interest rate, a large, evolving and fragmented technology services and solutions market across South Korea and developed East Asia, and the relatively low organic growth opportunities that ordinarily may not exist for smaller businesses. These pre-existing conditions could enable I-ON to identify and purchase compelling assets inexpensively.

Expand Product Offering and Geographic Coverage over the long-term

Over the next 5 years, I-ON’s growth strategy is to significantly expand its client base in South Korea, Japan, and Southeast Asia, while also expanding into new geographic areas, such as the U.S. and Europe to provide clients with global coverage and around the clock services that CMS and digital marketing requires. I-ON’s continued business model is to allow its work and unique technical skills to attract new clients as well as win repeat projects with past and current clients. At the same time, ION intends to expand its core offerings and increase brand awareness with new service capabilities and software products that produce significant value for clients.

PATENTS AND TRADEMARKS

Patents:

| § |

Integrated certification system using electronic contract #10-1132672

|

| § |

Website construction and management methodology #0457428

|

| § |

Website integrated management system and management methodology #10-0764690

|

| § |

Internet Reaction application reaction survey methodology and systems #0366708

|

| § |

Modification and restoration methodology on comment utilizing digital items #10-0634047

|

| § |

Power Quantity Reduction Compensation System management method #10-1046943

|

| § |

I-ON currently has 3 additional patents pending

|

Certifications:

| § |

I-ON e.Form Server Green Technology Certificate #GT-12-00040

|

| § |

I-ON Content Server v6.1 Certificate of Software Quality – GS (Good Software) #14-0017

|

| § |

DRMS OpenADR 2.0a/b Certificate of System Conformance

|

| § |

Certificate for Company Research Institute #20022427

|

AWARDS AND INDUSTRY RECOGNITION HISTORY

| § |

Selected to participate in ‘IP-Star Company development’ project by Seoul Business Agency (2013)

|

| § |

Designated as Best Small and Medium Company Workplace by Small and Medium Business Corporation (2012-2014)

|

| § |

Designated as Global Small Giant Company by Small and Medium Business Administration (2012-2014)

|

| § |

Grand prize at New Software Solution in General Software section by Ministry of Knowledge Economy (2012)

|

| § |

Designated as top Promising Future-Leading Company by Money Today (Economic newspaper 2012)

|

| § |

Certified ‘Promising Export Firm’ by Small and Medium Business Administration (2011-2013)

|

| § |

KOSA (Korea Software Industry Association)

|

| § |

Best prize at 11th Korean Software Companies’ Competitiveness Award - Mobile SW section (2012)

|

| § |

Best prize at 10th Korean Software Companies’ Competitiveness Award– KMS/EMC/BMP section (2011)

|

| § |

Best prize at SoftBank Mobile Solution Contest in Japan (2011)

|

| § |

Citation of Prime Minister awarded on the SW Industrial Day (2011)

|

| § |

Tower of million USD exports award (2007)

|

| § |

Grand prize in Internet Service Section (oneul.com) (2012)

|

| § |

Winner of Brand Service Section (Lotte Duty Free) (2012)

|

| § |

Grand prize in Business Improvement section (e.Form) (2012)

|

| § |

Grand Prize in Information Management (Real-time Power demand resources Operation System) (2012)

|

| § |

Grand Prize in Location Based System (LBS) (Lucky Bird) (2012)

|

| § |

Grand Prize in Product brand (Catch Chevrolet) (2011)

|

| § |

Grand Prize eBook (Kyowon Aesop) (2011)

|

CUSTOMERS

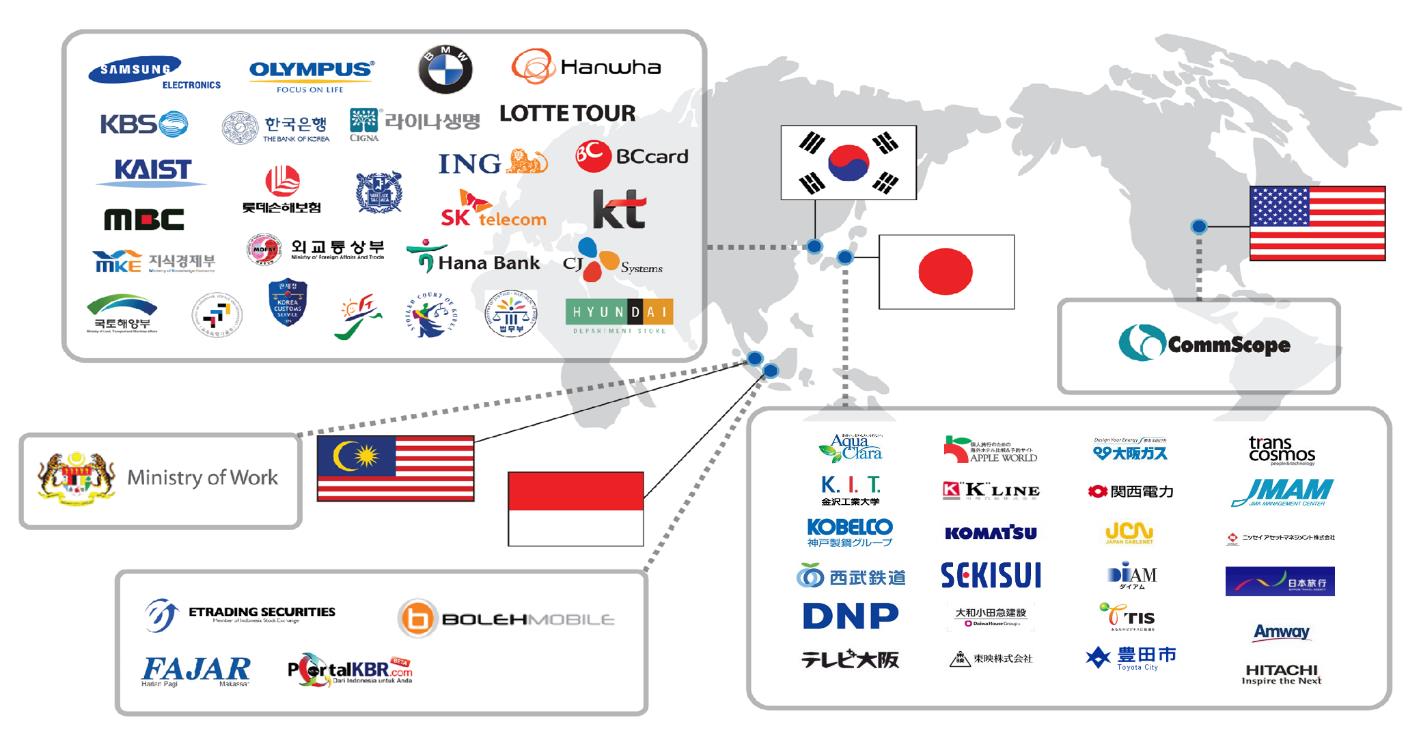

Because organizations in virtually every sector of the economy perform or need the functions I-ON supports, the Company has successfully deployed its software solutions to over 1,000 blue-chip and middle-market enterprises across virtually all industries and verticals in both the private and public sectors. Such industries include but are not limited to financial services, banking, informational technology services, telecommunications, internet, automotive, healthcare, publishing, media, education, energy, logistics, retail, consumer and business services, as well as government institutions. Over 400 enterprise clients in South Korea, 500 in Japan, and 100 across Southeast Asia and globally currently utilize I-ON products, solutions and professional services capabilities.

Given its current foothold, I-ON believes it remains uniquely positioned to address the evolving marketing needs of medium to large enterprises as CMOs continue to lack the wherewithal to analyze, improve ROI, and justify the value of increased digital marketing spend. I-ON’s diversified product suite, introduction of new products, tools and data sources, combined with media consumption devices such as mobile and tablets have created an environment that’s been uncharted by numerous enterprise marketers and their CMOs, particularly in South Korea, Japan, Southeast Asia and China.

Below is a sample of I-ON’s clientele based on region.

Entry into new markets combined with relevant new product introductions has also enabled I-ON to diversify its client mix, thereby minimizing client concentration risk as reflected by the decline in top 10 client contribution since 2013.

Below highlights I-ON’s top 10 clients as percentage of total revenue (Fiscal Years 2013-2016):

|

2013

|

2014

|

2015

|

2016

|

|||||||||||||||||||

|

KT Corporation

|

23.2

|

%

|

Public Procurement

|

23.9

|

%

|

KT Corporation

|

8.0

|

%

|

JoongAng Ilbo

|

7.0

|

%

|

|||||||||||

|

Lotte.com

|

7.0

|

%

|

KT Corporation

|

10.8

|

%

|

KCA

|

7.7

|

%

|

K.K I-ON

|

5.0

|

%

|

|||||||||||

|

KBS Media

|

6.0

|

%

|

Hyundai AutoEver

|

5.6

|

%

|

K.K. I-ON

|

6.6

|

%

|

Samsung Electro

|

5.0

|

%

|

|||||||||||

|

K.K. I-ON

|

5.9

|

%

|

K.K. I-ON

|

4.8

|

%

|

KT DS

|

6.3

|

%

|

GlobalTelecom

|

4.0

|

%

|

|||||||||||

|

PIXDINE

|

5.5

|

%

|

K.K. Ashisuto

|

3.9

|

%

|

Samsung Card

|

5.3

|

%

|

Hyunday Auto

|

4.0

|

%

|

|||||||||||

|

LG CNS

|

5.1

|

%

|

LG CNS

|

3.6

|

%

|

K.K. Ashisuto

|

3.7

|

%

|

Kolonbenit

|

4.0

|

%

|

|||||||||||

|

SD Solution

|

5.0

|

%

|

Hyundai ESG

|

3.5

|

%

|

Hyundai ESG

|

3.6

|

%

|

KEPCO

|

3.0

|

%

|

|||||||||||

|

K.K. Ashisuto

|

4.6

|

%

|

The financial news

|

3.2

|

%

|

KyoWon

|

3.6

|

%

|

Ssangyong

|

3.0

|

%

|

|||||||||||

|

KTH Co., Ltd.

|

4.3

|

%

|

REVOLUTION

|

2.8

|

%

|

MBC

|

3.6

|

%

|

K.K. Ashisuto

|

3.0

|

%

|

|||||||||||

|

SquarenetTM

|

4.1

|

%

|

KOBACO

|

2.7

|

%

|

Accenture

|

3.2

|

%

|

Korea Comm.

|

3.0

|

%

|

|||||||||||

|

Top 10 Customers

|

70.9

|

%

|

64.9

|

%

|

51.7

|

%

|

41.0

|

%

|

||||||||||||||

MARKETING, SALES AND DISTRIBUTION

I-ON relies both on inside and outside sales efforts as well as value-added resellers based in specific geographies to drive a bulk of their business development efforts. The Company has over 100 partners, formal and informal, across 28 countries that provides client leads The Company also relies on client references and its track record and regularly attends reputable industry and technology conferences internationally.

COMPETITION

The market for I-ON’s products and solutions, primarily in South Korea, Japan and Southeast Asia is competitive but not considerably fragmented. We compete primarily with systems consulting firms, boutique consulting firms, that maintain specialized skills or products or are geographically focused, and clients’ own IT firms. Many of the firms we compete with have longer operating histories and are more developed than we are. The principal competitive factors in these addressable markets include the ability to solve problems; the ability to deliver creative concepts and solutions; expertise and talent with advanced technologies; availability of resources; the quality and speed of solutions; a deep understanding of user experiences; and the price of solutions. I-ON competes favorably when considering these factors and believes that its ability to deliver business innovation and outstanding value to its clients on time and on budget, along with its successful track record, distinguishes them from competitors.

Interoperability has emerged as a key differentiator in I-ON’s addressable markets, as CMS is now seldom viewed as a stand-alone system for an enterprise’s website. Large enterprises and to a growing extent small and middle market companies, particularly those with complex distribution and supply chain issues, not only require a portal for their intranet for external needs, but expect CMS platforms to allow for a real-time connection between the business, people, behavior and things that allow all to communicate, transact and even negotiate with each other. Thus, in order to be better served and remain competitive in their own circles, clients are increasingly looking to ION to consult with and integrate disparate and increasingly complex systems.

I-ON has differentiated itself and garnered market share over the years through competitive and flexible pricing strategies, leveraging its domestic first-mover advantage and proven time-tested licensing model, and by the continuous introduction of next generation and complementary product lines geared towards addressing growing market trends and client needs.

I-ON also has a localized and cultural advantage, whereas global competitors such as Adobe’s marketing cloud product (AEM), Oracle’s marketing cloud product and IBM platform generally lack local knowledge of domain expertise and complexities, middle-market cachet and competitive pricing suited for regional enterprises. On the other hand, opensource models such as Wordpress, Drupal and Xpress Engine are more suitable for the SME and startup markets outside of the Asia-pacific region, provide often vague and less complex offerings unsuitable for mid to large enterprises and lack vendor relationships and responsibilities.

RESEARCH AND DEVELOPMENT

Because the verticals in which I-ON competes are characterized by rapid technological change, the Company’s ability to compete successfully depends upon maintaining and enhancing expertise in its core business segments and product lines. As a result, I-ON has reinvested and continues to spend over 15% of annual revenue on research and development alone. The Company currently employs over 100 junior, mid to senior level engineers and developers, most of whom are based at the Company’s headquarters in Seoul. In order enable its employees to provide expert, timely, competitive services to the marketplace, I-ON also provides ongoing training and sponsors advanced university education to enhance employee skills and knowledge of all current and future product offerings.

MANAGEMENT AND EMPLOYEES

As of the date of this Report, I-ON has 150 full time and 10 part time employees. We believe we enjoy good employee relations. None of our employees are members of any labor union, and we are not a party to any collective bargaining agreement.

PROPERTIES

The Company does not own any physical location. I-ON currently leases its corporate headquarters and other offices in Seoul, South Korea which expires on December 31, 2020. I-ON’s lease for its Tokyo, Japan office expires on September 30, 2019. We believe that our current offices are sufficient in size for current and future operations.

POTENTIAL FUTURE PROJECTS AND CONFLICTS OF INTEREST

Members of the Company’s management may serve in the future as an officer, director or investor in other entities. Neither the Company nor any of its shareholders would have any interest in these other companies’ projects. Management believes that it has sufficient resources to fully discharge its responsibilities for all current and future projects.

GOVERNMENT REGULATION

We believe we are in compliance with applicable federal, state and other regulations and that we have compliance programs in place to ensure compliance going forward. There are no regulatory notifications or actions pending.

LEGAL MATTERS

None.

RELATED PARTY TRANSACTIONS

On July 21, 2014, Michael J. Rapport, the Company’s former Chief Executive Officer, sole director, and controlling shareholder, advanced the Company a $100,000 long term unsecured loan with a 1.5% interest rate per annum, due no later than July 21, 2017. The loan is convertible into common shares of the Company at any time after the second year’s anniversary at a price based upon either: a) The price of its most recent private placement offering, closest to the time of conversion; or b) if the Company’s common stock is then publicly-traded, the bid price of its common stock on the closing day of the conversion. For the period ended December 31, 2017, the Company accrued $1,500 of interest on this note. For the year ended December 31, 2016, the Company accrued $1,504 on this same note. The accrued amount is included in accounts payable and accrued liabilities on the balance sheet. Mr. Rapport has extended the due date of the note to December 31, 2017.

Michael J. Rapport also advanced the Company $10,000 on April 21, 2014; $8,000 on June 13, 2014; $20,000 on June 2, 2015; $30,000 on July 2, 2015; and $40,000 on August 25, 2015, for a total amount advanced of $108,000. All of these payments are secured by 8% interest bearing notes that are due on April 21, 2015, June 13, 2015, June 2, 2016, July 2, 2016, and August 25, 2016, respectively. As of June 30, 2016, four of the five notes totaling $108,000 were past due. On July 30, 2016, Michael J. Rapport exchanged the 5 notes, 4 of which were past due, for a single note. The 5 notes total $108,000 and are replaced by a single note for $118,603, which includes the original principal of $108,000 plus $10,603 of accrued interest. The new note has a term of one year and will bear interest at per annum rate of 6% instead of the 8% per annum rate on the old notes. For the year ended December 31, 2017, the Company accrued $7,116 of interest for this note. For the year ended December 31, 2016, the Company had an accrued balance of $3,002 interest for the notes due Mr. Rapport. Mr. Rapport has extended the note to December 31,2017

Michael J. Rapport paid for a new piece of equipment for the brewery on June 15, 2016, in the amount of $17,496. A separate 8% interest bearing note was drawn up for this amount. For the year ended December 31, 2017, the Company accrued interest on this note in the amount of $1.400. The Company accrued interest in the amount of $763 has been recorded as of the year ended December 31, 2016. Mr. Rapport has extended the note to December 31,2017

On July 27, 2016, Mr. Rapport’s loaned the Company $250,000. The note is unsecured, has a term of one year and bears interest at the rate of 4% per annum. For the year ended December 31, 2017 the Company accrued interest in the amount of $10,000. For the year ended December 31, 2016, the Company accrued $4,301 of interest for this note. Mr. Rapport has extended the due date of this note to December 31, 2017, as well.

On October 1, 2016, Mr. Rapport executed a note in the amount of $400,000 with EBC Public House. The note is unsecured and has a one-year term and bears interest at the rate of 3% per annum. The note is an installment note to provide working capital as needed for EBC Public House for the Fullerton Restaurant. On October 6, 2017, Mr. Rapport executed a one-year installment note for an additional $100,000 bearing interest at 3% per annum, bringing the total of the installment notes to $500,000. During the year ended December 31, 2017, EBC Public House drew done these notes by $354,980 bringing the total amount drawn on the note to $473,078. The accrued interest for the year ended December 31, 2017, is $6,757. During the year ended December 31, 2016, EBC Public House had 5 different draws against the note for a total of $118,098 and recorded $709 in accrued interest. The balance of the note as of December 31, 2017, is $473,078 and the total amount of accrued interest on the note is $7,467.

On March 2, 2017 Mr. Rapport’s loaned the Company $20,000. The note is unsecured, has a term of one year and bears interest at the rate of 6% per annum. For the year ended December 31, 2017, the Company accrued $999 of interest for this note.

On March 6, 2017, Mr. Rapport’s loaned the Company $120,000. The note is unsecured, has a term of one year and bears interest at the rate of 6% per annum. For the year ended December 31, 2017, the Company accrued $5,918 of interest for this note.

On April 1, 2017, Mr. Rapport executed a note in the amount of $85,000 with EBC Public House for the advance of funds to purchase a Food Truck with the EBC Public House brand on it. The note has a three-year term and will be secured by the truck and bear interest at the rate of 3% per annum. As of the year ended December 31, 2017, EBC Public House accrued interest on the note in the amount of $1,958.

On April 1, 2017, Mr. Rapport advance EBC Public House $1,617 to purchase equipment for the Food Truck. The note is unsecured and has a one-year term and bears interest at the rate of 3% per annum. As of the year ended December 31, 2017, EBC Public House accrued interest on the note in the amount of $37.

On June 26, 2017, Mr. Rapport executed a note in the amount of $250,000 with EBC Public House. The note is unsecured and has a one-year term and bears interest at the rate of 3% per annum. The note is an installment note to provide working capital as needed for EBC Public House - Huntington Beach Restaurant. On August 11, 2017, Mr. Rapport executed an additional note in the amount of $300,000 with EBC Public House. The note is unsecured and has a one-year term and bears interest at the rate of 3% per annum. The note is also an installment note to provide working capital as needed for EBC Public House- Huntington Beach Restaurant. On October 13, 2017, Mr. Rapport executed a new one-year installment note for an additional $400,000t bearing interest at the rate of 3% per annum bringing the total amount of the three notes to $950,000. During the year ended December 31. 2017, EBC Public House drew done these notes in the amount of $909,156. The accrued interest on this notes for the year ended December 31, 2017, is $10,677.

On August 2, 2017, Mr. Rapport’s loaned the Company $25,000. The note is unsecured, has a term of one year and bears interest at the rate of 6% per annum. For the year ended December 31, 2017, the Company accrued $621 of interest for this note.

On August 24, 2017, Mr. Rapport’s loaned the Company $40,963. The note is unsecured, has a term of one year and bears interest at the rate of 6% per annum. For the year ended December 31, 2017, the Company accrued $869 of interest for this note.

On August 31, 2017, Mr. Rapport’s loaned the Company $25,000. The note is unsecured, has a term of one year and bears interest at the rate of 6% per annum. For the year ended December 31, 2017, the Company accrued $501 of interest for this note.

On September 11, 2017, Mr. Rapport’s loaned the Company $13,000. The note is unsecured, has a term of one year and bears interest at the rate of 6% per annum. For the year ended December 31, 2017, the Company accrued $237 of interest for this note

On November 5, 2017, Mr. Rapport’s loaned the Company $24,000. The note is unsecured, has a term of one year and bears interest at the rate of 6% per annum. For the year ended December 31, 2017, the Company accrued $221 of interest for this note

Accrued Interest

For the year ended December 31, 2017, the Company accrued interest of $48,724 on the notes due to Mr. Rapport. For the year ended December 31, 2016, the Company accrued interest of $12,450 pertaining to all the notes due to Mr. Rapport.

Available Information

We will make available free of charge any of our filings as soon as reasonably practicable after we electronically file these materials with, or otherwise furnish them to, the Securities and Exchange Commission (“SEC”). We are not including the information contained in our website as part of, or incorporating it by reference into, this report on Form 10-K.

The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, D.C. 20002. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov.

Within our website’s “Investor” section, “SEC Filings” tab, all of our filings with the Commission and all amendments to these reports are available as soon as reasonably practicable after filing.

Website

Our website address is

Our Information

Our principal executive offices are located at 15, Tehran-ro 10-gil, Gangam-gu, Seoul, Korea 06234 and our telephone number is 82-2-3430-1200 . We can be contacted by email at intlbiz@i-on.net.

Our business, financial condition, operating results and prospects are subject to the following risks. Additional risks and uncertainties not presently foreseeable to us may also impair our business operations. If any of the following risks actually occurs, our business, financial condition or operating results could be materially adversely affected. In such case, the trading price of our common stock could decline, and our stockholders may lose all or part of their investment in the shares of our common stock.

This Form 10-K contains forward-looking statements that involve risks and uncertainties. These forward-looking statements can be identified by the use of words such as “believes,” “estimates,” “intends”, “plans”, “could,” “possibly,” “probably,” anticipates,” “projects,” “expects,” “may,” “will,” or “should,” “designed to,” “designed for,” or other variations or similar words or language. Actual results could differ materially from those discussed in the forward-looking statements as a result of certain factors, including those set forth below and elsewhere in this Form 10-K.

Risks Specific to Our Business

Our proprietary software or service delivery may not operate properly, which could damage our reputation, give rise to claims against us, or divert application of our resources from other purposes, any of which could harm our business and operating results.

We may encounter human or technical obstacles that prevent our proprietary applications from operating properly. If our applications do not function reliably or fail to achieve customer expectations in terms of performance, customers could assert liability claims against us or attempt to cancel their contracts with us. This could damage our reputation and impair our ability to attract or maintain customers. We provide a limited warranty, have not paid warranty claims in the past, and do not have a reserve for warranty claims.

Moreover, information services as complex as those we offer have in the past contained, and may in the future develop or contain, undetected defects or errors. We cannot assure you that material performance problems or defects in our products or services will not arise in the future. Errors may result from receipt, entry, or interpretation of customer information or from interface of our services with legacy systems and data that we did not develop and the function of which is outside of our control. Despite testing, defects or errors may arise in our existing or new software or service processes. These defects and errors and any failure by us to identify and address them could result in loss of revenue or market share, liability to customers or others, failure to achieve market acceptance or expansion, diversion of development resources, injury to our reputation, and increased service and maintenance costs. Defects or errors in our software might discourage existing or potential customers from purchasing our products and services. Correction of defects or errors could prove to be impossible or impracticable. The costs incurred in correcting any defects or errors or in responding to resulting claims or liability may be substantial and could adversely affect our operating results.

If our security measures are breached or fail and unauthorized access is obtained to a customer’s data, our service may be perceived as insecure, the attractiveness of our services to current or potential customers may be reduced, and we may incur significant liabilities.

Our services involve the web-based storage and transmission of customers’ proprietary information. We rely on proprietary and commercially available systems, software, tools and monitoring, as well as other processes, to provide security for processing, transmission and storage of such information. Because of the sensitivity of this information and due to requirements under applicable laws and regulations, the effectiveness of our security efforts is very important. If our security measures are breached or fail as a result of third-party action, acts of terror, social unrest, employee error, malfeasance or for any other reasons, someone may be able to obtain unauthorized access to customer data. Improper activities by third-parties, advances in computer and software capabilities and encryption technology, new tools and discoveries and other events or developments may facilitate or result in a compromise or breach of our security systems. Our security measures may not be effective in preventing unauthorized access to the customer data stored on our servers. If a breach of our security occurs, we could face damages for contract breach, penalties for violation of applicable laws or regulations, possible lawsuits by individuals affected by the breach and significant remediation costs and efforts to prevent future occurrences. In addition, whether there is an actual or a perceived breach of our security, the market perception of the effectiveness of our security measures could be harmed and we could lose current or potential customers.

Disruptions in Internet or telecommunication service or damage to our data centers could adversely affect our business by reducing our customers’ confidence in the reliability of our services and products.

Our information technologies and systems are vulnerable to damage or interruption from various causes, including acts of God and other natural disasters, war and acts of terrorism and power losses, computer systems failures, internet and telecommunications or data network failures, operator error, losses of and corruption of data and similar events. Data regarding our business and our customers’ insurance claims and encounters resides on computer hardware located domestically and abroad. Although we conduct business continuity planning to protect against fires, floods, other natural disasters and general business interruptions to mitigate the adverse effects of a disruption, relocation or change in operating environment at our data centers, the situations we plan for and the amount of insurance coverage we maintain may not be adequate in any particular case. In addition, the occurrence of any of these events could result in interruptions, delays or cessations in service to our customers. Any of these events could impair or prohibit our ability to provide our services, reduce the attractiveness of our services to current or potential customers and adversely impact our financial condition and results of operations.

In addition, despite the implementation of security measures, our infrastructure, data centers, or systems that we interface with or utilize, including the internet and related systems, may be vulnerable to physical break-ins, hackers, improper employee or contractor access, computer viruses, programming errors, denial-of-service attacks or other attacks by third-parties seeking to disrupt operations or misappropriate information or similar physical or electronic breaches of security. Any of these can cause system failure, including network, software or hardware failure, which can result in service disruptions. As a result, we may be required to expend significant capital and other resources to protect against security breaches and hackers or to alleviate problems caused by such breaches.

We depend on key information systems and third party service providers.

We depend on key information systems to accurately and efficiently transact our business. These systems and services are vulnerable to interruptions or other failures resulting from, among other things, natural disasters, terrorist attacks, software, equipment or telecommunications failures, processing errors, computer viruses, other security issues or supplier defaults. Security, backup and disaster recovery measures may not be adequate or implemented properly to avoid such disruptions or failures. Any disruption or failure of these systems or services could cause substantial errors, processing inefficiencies, security breaches, inability to use the systems or process transactions, loss of customers or other business disruptions, all of which could negatively affect our business and financial performance.

As cybersecurity attacks continue to evolve and increase, our information systems could also be penetrated or compromised by internal and external parties’ intent on extracting confidential information, disrupting business processes or corrupting information. These risks could arise from external parties or from acts or omissions of internal or service provider personnel. Such unauthorized access could disrupt our business and could result in the loss of assets, litigation, remediation costs, damage to our reputation and failure to retain or attract customers following such an event, which could adversely affect our business.

We may be unable to adequately establish, protect or enforce our intellectual property rights.

Our success depends in part upon our ability to establish, protect and enforce our intellectual property and other proprietary rights. If we fail to establish, protect or enforce our intellectual property rights, we may lose an important advantage in the market in which we compete. We rely on a combination of trademark, copyright and trade secret law and contractual obligations to protect our key intellectual property rights, all of which provide only limited protection. Our intellectual property rights may not be sufficient to help us maintain our position in the market and our competitive advantages.

We hold several patents and also rely on trade secrets to protect certain of our proprietary technology. However, trade secrets may not be protectable if not properly kept confidential. We strive to enter into non-disclosure agreements with our employees, customers, contractors and business partners to limit access to and disclosure of our proprietary information. However, the steps we have taken may not be sufficient to prevent unauthorized use of our technology, and adequate remedies may not be available in the event of unauthorized use or disclosure of our trade secrets and proprietary technology. Moreover, others may reverse engineer or independently develop technologies that are competitive to ours or infringe our intellectual property.

Accordingly, despite our efforts, we may be unable to prevent third-parties from using our intellectual property for their competitive advantage. Any such use could have a material adverse effect on our business, results of operations and financial condition. Monitoring unauthorized uses of and enforcing our intellectual property rights can be difficult and costly. Legal intellectual property actions are inherently uncertain and may not be successful, and may require a substantial amount of resources and divert our management’s attention.

Claims by others that we infringe their intellectual property could force us to incur significant costs or revise the way we conduct our business.

Our competitors protect their proprietary rights by means of patents, trade secrets, copyrights, trademarks and other intellectual property. We have not conducted an independent review of patents and other intellectual property issued to third-parties, who may have patents or patent applications relating to our proprietary technology. We may receive letters from third parties alleging, or inquiring about, possible infringement, misappropriation or violation of their intellectual property rights. Any party asserting that we infringe, misappropriate or violate proprietary rights may force us to defend ourselves, and potentially our customers, against the alleged claim. These claims and any resulting lawsuit, if successful, could subject us to significant liability for damages and/or invalidation of our proprietary rights or interruption or cessation of our operations. Any such claims or lawsuit could:

| ● |

be time-consuming and expensive to defend, whether meritorious or not;

|

| ● |

require us to stop providing products or services that use the technology that allegedly infringes the other party’s intellectual property;

|

| ● |

divert the attention of our technical and managerial resources;

|

| ● |

require us to enter into royalty or licensing agreements with third-parties, which may not be available on terms that we deem acceptable;

|

| ● |

prevent us from operating all or a portion of our business or force us to redesign our products, services or technology platforms, which could be difficult and expensive and may make the performance or value of our product or service offerings less attractive;

|

| ● |

subject us to significant liability for damages or result in significant settlement payments; or

|

| ● |

require us to indemnify our customers.

|

Furthermore, during the course of litigation, confidential information may be disclosed in the form of documents or testimony in connection with discovery requests, depositions or trial testimony. Disclosure of our confidential information and our involvement in intellectual property litigation could materially adversely affect our business. Some of our competitors may be able to sustain the costs of intellectual property litigation more effectively than we can because they have substantially greater resources. In addition, any litigation could significantly harm our relationships with current and prospective customers. Any of the foregoing could disrupt our business and have a material adverse effect on our business, operating results and financial condition.

The continued success of our business model is heavily dependent upon our offshore operations, and any disruption to those operations will adversely affect us.

The majority of our operations, including the development and maintenance of our Web-based platform and our customer support services, are performed by our highly educated workforce of approximately 120 employees in South Korea which may experience unrest due to the threats posed by North Korea. The performance of our operations in South Korea, and our ability to maintain our offshore offices, is an essential element of our business model, as South Korea is a tech hub for Enterprise CMS/Digital marketing as well as all of our senior leadership are located in South Korea. Our competitive advantage will be greatly diminished and may disappear altogether if our operations in South Korea are negatively impacted.

Our offshore operations expose us to additional business and financial risks which could adversely affect us and subject us to civil and criminal liability.

The risks and challenges associated with our operations outside the United States include laws and business practices favoring local competitors; compliance with multiple, conflicting and changing governmental laws and regulations, including employment and tax laws and regulations; and fluctuations in foreign currency exchange rates. Foreign operations subject us to numerous stringent U.S. and foreign laws, including the Foreign Corrupt Practices Act, or FCPA, and comparable foreign laws and regulations that prohibit improper payments or offers of payments to foreign governments and their officials and political parties by U.S. and other business entities for the purpose of obtaining or retaining business. Safeguards we implement to discourage these practices may prove to be less than effective and violations of the FCPA and other laws may result in severe criminal or civil sanctions, or other liabilities or proceedings against us, including class action lawsuits and enforcement actions from the SEC, Department of Justice and overseas regulators.

Future product development is dependent upon access to and reliability of third party software products and open source software.

Certain of our software products contain components developed and maintained by third party software vendors. We expect that we may have to incorporate software from third party vendors in our future products. We also incorporate open source software in certain of our software products. We may not be able to replace the functionality provided by the third party or open source software currently offered with our products if that software becomes obsolete, defective, non-compliant with third party patent restrictions or incompatible with future versions of our products or is not adequately maintained or updated, or if our relationship with the third party vendor terminates. In addition, we must carefully monitor and manage our use of, and compliance with the licensing requirements of, open source software. Any significant interruption in the availability of these third party software products on commercially acceptable terms, defects in these products, non-compliance with third party patent restrictions or our inability to comply with the licensing terms of either third party commercial software or open source software could delay development of future products or enhancement of future products and could have a material adverse effect on our business, financial condition, operating results and cash flows.

Future product development is dependent on adequate research and development resources.