Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - Charah Solutions, Inc. | d496329dex232.htm |

| EX-23.1 - EX-23.1 - Charah Solutions, Inc. | d496329dex231.htm |

| EX-10.13 - EX-10.13 - Charah Solutions, Inc. | d496329dex1013.htm |

| EX-10.12 - EX-10.12 - Charah Solutions, Inc. | d496329dex1012.htm |

| EX-10.11 - EX-10.11 - Charah Solutions, Inc. | d496329dex1011.htm |

| EX-5.1 - EX-5.1 - Charah Solutions, Inc. | d496329dex51.htm |

Table of Contents

As filed with the Securities and Exchange Commission on June 4, 2018

No. 333-225051

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Charah Solutions, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 4953 | 82-4228671 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

12601 Plantside Dr.

Louisville, KY 40299

(502) 245-1353

(Address, including zip code and telephone number, including area code, of registrant’s principal executive offices)

Charles Price

President and Chief Executive Officer

12601 Plantside Dr.

Louisville, KY 40299

(502) 245-1353

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies to:

| Julian J. Seiguer Michael W. Rigdon Kirkland & Ellis LLP 609 Main Street Houston, Texas 77002 (713) 836-3600 |

Richard D. Truesdell, Jr. Shane Tintle Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Regustered(1) |

Proposed Maximum Offering Price Per Share(2) |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) | ||||

| Common stock, par value $0.01 per share |

8,455,882 | $18.00 | $152,205,876 | $18,949.63 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated pursuant to Rule 457(a) under the Securities Act of 1933, as amended. Includes 1,102,941 shares of common stock issuable upon exercise of the underwriters’ option to purchase additional shares of common stock. |

| (2) | Estimated solely for the purpose of calculating the registration fee. |

| (3) | The Registrant previously paid $12,450 of the total registration fee in connection with a previous filing of this Registration Statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS

Subject to Completion, dated June 4, 2018

7,352,941 Shares

Charah Solutions, Inc.

COMMON STOCK

Charah Solutions, Inc. is offering 5,294,117 shares of our common stock and the selling stockholders are offering 2,058,824 shares of our common stock. This is our initial public offering and no public market currently exists for our shares. We anticipate that the initial public offering price will be between $16.00 and $18.00 per share.

We have been approved, subject to official notice of issuance, to list the common stock on the New York Stock Exchange under the symbol “CHRA.”

We are an “emerging growth company” as defined under the federal securities laws and, as such, have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 16.

PRICE $ A SHARE

| Price to Public |

Underwriting Discounts and Commissions |

Proceeds to Company(1) |

Proceeds to Selling Stockholders |

|||||||||||||

| Per share |

$ | $ | $ | $ | ||||||||||||

| Total |

$ | $ | $ | $ | ||||||||||||

| (1) | We have agreed to reimburse the underwriters for certain FINRA-related expenses. See “Underwriting” for additional information regarding the underwriters’ compensation. |

The selling stockholders have granted the underwriters the right to purchase up to an additional 1,102,941 shares of common stock to cover over-allotments at the initial public offering price less the underwriting discount.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock on or about , 2018.

Joint Book-Running Managers

| MORGAN STANLEY | BofA MERRILL LYNCH | |||

| STIFEL | ||||

Co-Managers

MACQUARIE CAPITAL FIRST ANALYSIS SECURITIES CORP. HOULIHAN LOKEY

, 2018.

Table of Contents

Neither we, the selling stockholders, nor the underwriters have authorized anyone to provide you with information different from that contained in this prospectus and any free writing prospectus we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We, the selling stockholders and the underwriters are offering to sell shares of common stock and seeking offers to buy shares of common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of any sale of the common stock. Our business, liquidity position, financial condition, prospects or results of operations may have changed since the date of this prospectus.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.”

Dealer Prospectus Delivery Obligation

Until , 2018 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

i

Table of Contents

| • | “Allied Management Holdings” refers to Allied Management Holdings, LLC, a Delaware limited liability company, through which certain of our officers and employees prior to our corporate reorganization own equity interests in Allied Power Holdings. |

| • | “Allied Power Holdings” refers to Allied Power Holdings, LLC, a Delaware limited liability company, an entity indirectly owned by BCP, CEP Holdings and the Management Members. |

| • | “BCP” refers, collectively, to (i) affiliates (including Charah Holdings and the BCP Energy Services Funds) of and (ii) investment funds affiliated with or managed by, in each case, Bernhard Capital Partners Management, LP. |

| • | “BCP Energy Services Funds” refers to BCP Energy Services Fund, LP, a Delaware limited partnership owned by BCP and certain related affiliates and BCP Energy Services Fund-A, LP, a Delaware limited partnership owned by BCP and certain related affiliates. |

| • | “CCR” means coal combustion residuals, a byproduct of coal-fired power production, also commonly referred to as coal ash. |

| • | “CEP Holdings” means CEP Holdings, Inc., a Delaware corporation owned by Charles Price and certain affiliates. |

| • | “Charah Holdings” refers to Charah Holdings LP, a Delaware limited partnership owned by BCP and certain related affiliates. |

| • | “Charah Management” refers to Charah Management LLC, a Delaware limited liability company, an entity indirectly owned by BCP, CEP Holdings and the Management Members. |

| • | “Charah Management Holdings” refers to Charah Management Holdings LLC, a Delaware limited liability company, through which certain of our officers and employees prior to our corporate reorganization own equity interests in Charah Management. |

| • | “Company,” “we,” “us” or “our” relate, prior to the corporate reorganization described in this prospectus (unless otherwise disclosed), to Charah, LLC and Allied Power Management, LLC, on a combined basis and together with their consolidated subsidiaries (as combined, our “Predecessors,” and each, a “Predecessor Company”) and following the corporate reorganization described in this prospectus, to Charah Solutions, Inc. (“Charah Solutions”) and its consolidated subsidiaries. |

| • | “Credit Facility” means the ABL Credit Facility, dated October 25, 2017, by and among Charah, LLC, Allied Power Management, LLC and Allied Power Services, LLC, as borrowers, Charah Sole Member LLC and Allied Power Sole Member, LLC, as guarantors, the lenders party thereto from time to time, and Regions Bank, as administrative agent, collateral agent, swingline lender and letter of credit issuer. |

| • | “Existing Owners” refers, collectively, to BCP, CEP Holdings and the Management Members. |

| • | “Management Members” refers, collectively, to our current officers and employees, other than Charles E. Price, whose equity ownership is held through CEP Holdings, who own equity interests in Charah Management and Allied Power Holdings, including through Charah Management Holdings and Allied Management Holdings. |

| • | “Term Loan” means the Term Loan Credit Facility, dated October 25, 2017, by and among Charah, LLC and Allied Power Management, LLC, as borrowers, Charah Sole Member LLC and Allied Power Sole Member, LLC, as guarantors, the lenders party thereto from time to time, and Credit Suisse AG, Cayman Islands Branch, as administrative agent and collateral agent. |

ii

Table of Contents

Presentation of Financial and Operating Data

Unless otherwise indicated, the historical financial and operating information presented in this prospectus for the year ended and as of December 31, 2016 is that of Charah, LLC, and as of March 31, 2018 and for the three months ended March 31, 2018 and 2017 and for the year ended and as of December 31, 2017 is that of Charah, LLC and Allied Power Management, LLC on a combined basis. We present certain operational data in this prospectus that includes the operations of Allied Power Management, LLC, an entity that has been under common control with Charah, LLC since May 2017, the date of formation of Allied Power Management, LLC. Our historical financial and operating information as of and for the year ended December 31, 2017 may not be comparable to the historical financial and operating information as of and for the year ended December 31, 2016.

Certain amounts and percentages included in this prospectus have been rounded. Accordingly, in certain instances, the sum of the numbers in a column of a table may not exactly equal the total figure for that column.

Industry and Market Data

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications and other published sources, including data from the U.S. Energy Information Administration and the U.S. Environmental Protection Agency. Some data are also based on our good faith estimates. Although we believe these third-party sources are reliable as of their respective dates, neither we, the selling stockholders nor the underwriters have independently verified the accuracy or completeness of this information. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these publications.

Trademarks and Trade Names

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks, trade names or products in this prospectus is not intended to, and does not imply a relationship with, or endorsement or sponsorship by us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but the omission of such references is not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable owner of these trademarks, service marks and trade names.

iii

Table of Contents

This summary contains basic information about us and the offering. Because it is a summary, it does not contain all the information that you should consider before investing in our common stock. You should read and carefully consider this entire prospectus before making an investment decision, especially the information presented under the headings “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical combined financial statements and the related notes thereto appearing elsewhere in this prospectus.

Except as otherwise indicated, (i) references to “selling stockholders” refer to those persons identified as selling stockholders in “Principal and Selling Stockholders”, (ii) all information contained in this prospectus assumes or reflects no exercise of the underwriters’ option to purchase additional shares of common stock and (a) excludes shares of common stock reserved for issuance under our omnibus incentive plan and (b) excludes 223,994 shares of common stock that will be granted to certain of our employees (based on the midpoint of the price range set forth on the cover page of this prospectus) under our omnibus incentive plan in connection with the closing of this offering and (iii) the number of shares held by the Existing Owners prior to this offering and the total number of shares of common stock outstanding after the completion of this offering assumes that the Management Members receive 1,335,306 shares of common stock (based on the midpoint of the price range set forth on the cover page of this prospectus) with respect to the Management Reorganization Consideration (as defined herein).

Company Overview

We are a leading provider of mission-critical environmental and maintenance services to the power generation industry. We provide on-site, essential services that enable our clients to continue operations and provide necessary electric power to communities nationwide. In 2017, we performed work at 51 coal-fired and nuclear power generation sites nationwide. We are the only service provider offering a suite of coal ash management and recycling, environmental remediation and outage maintenance services. We also design and implement solutions for complex environmental projects (such as ash pond closures) and facilitate coal ash recycling through byproduct sales and other beneficial use services. We believe we are a partner-of-choice for the power generation industry due to our industry-leading quality, safety and compliance record, all of which are key criteria for our customers.

Since our founding, we have continuously anticipated our customers’ evolving environmental needs, increasing the number of services we provide and our embedded presence at their power generation facilities. Compared to service providers with more limited scope, our multi-service platform allows customers to gain efficiencies from sourcing multiple required offerings from a single, trusted partner.

We provide our services through two segments:

Environmental Solutions. Our Environmental Solutions segment includes Remediation and Compliance Services, as well as Byproduct Sales. Remediation and Compliance Services is associated with our customers’ need for multiyear environmental improvement and sustainability initiatives, whether driven by proactive engagement by power generation customers, by regulatory requirements or by consumer expectations and standards. Byproduct Sales supports both our power generation customers’ desire to profitably recycle recurring volumes of coal combustion residuals (“CCRs”) and our ultimate end customers’ need for high-quality, cost-effective raw material substitutes.

Maintenance and Technical Services. Our Maintenance and Technical Services segment includes Fossil Services and Nuclear Services. Fossil Services is the recurring and mission-critical management of coal ash for coal-fired power generation facilities. Nuclear Services, which we market under the Allied Power brand name, includes routine maintenance, outage services, facility maintenance and staffing solutions for nuclear power generation facilities.

1

Table of Contents

As a result of these unique offerings, the embedded nature of our on-site presence and our track record of successful execution, we have built long-term relationships with leading U.S. utilities and independent power producers, including Duke Energy, Exelon Corporation, Dominion Energy, Inc., Dynegy Inc. and PPL Corporation, among others. In some cases, these relationships have spanned over 20 years. The national scale of our operational footprint is also a key differentiator, as many competitors are localized, focusing on a single geographic area (sometimes isolated to a single plant). We operate in 22 states, resulting in an overall footprint and density in key markets that we believe is difficult to replicate. Our national reach enables us to successfully pursue new business within our existing customer base and attract new customers while providing consistent quality, safety and compliance standards.

Our services platform is led by a senior executive team averaging over 30 years of industry experience and supported by a highly skilled labor force. The nature of our work requires employees, particularly our nuclear end market-related labor force, to have specialized skills, training and certifications in order for them to be allowed on-site at our customers’ facilities. Collectively, our focus on human capital management allows us to maintain and develop a labor force of highly qualified, well-trained personnel capable of handling our customers’ needs.

For the fiscal year ended December 31, 2017, we generated revenue, net income (loss) and Adjusted EBITDA of $430.4 million, $12.8 million and $76.0 million, respectively ($421.2 million, $18.3 million and $76.4 million, respectively, for the period from January 13, 2017 through December 31, 2017 and $9.1 million, $(5.5) million and $(0.4) million, respectively, for the period from January 1, 2017 through January 12, 2017). For the three months ended March 31, 2018, we generated revenue, net income and Adjusted EBITDA of $155.5 million, $1.2 million and $17.4 million, respectively. For more information on Adjusted EBITDA, including a reconciliation to the most directly comparable accounting principles generally accepted in the United States of America (“GAAP”) financial measure, see “—Summary Historical Combined Financial Data.”

Market Opportunity

According to the U.S. Energy Information Administration, as of 2016, there were over 500 large-scale facilities in the U.S. with generation capabilities of at least 250 megawatts, including over 200 coal-fired plants and over 60 nuclear plants (representing 99 nuclear reactors). To maintain continuous operations, these complex facilities have specialized and recurring environmental and maintenance service needs throughout their lifecycles. These service needs are particularly significant for coal-fired and nuclear power plants, given increasing environmental demands, the aging nature of the installed base, and the characteristics of the feedstock required to power such facilities. Due to the breadth and nature of these needs, power plant operators typically do not possess these capabilities internally and instead outsource these mission-critical and often regulatory-driven requirements to a fragmented set of service providers. The continuous need for these specialized services is supported by a number of significant dynamics:

Coal and Nuclear Power Generation Will Remain Indispensable Energy Sources. According to the U.S. Energy Information Administration, as of September 2017, coal and nuclear power generation combined are expected to remain indispensable energy sources for decades, providing at least 1.6 trillion kilowatt hours of energy production annually through 2040. As of September 2017, coal and nuclear power generation combined accounted for approximately 50% of domestic U.S. energy generation and is expected to contribute a similar percentage annually for at least the next five years.

Coal-Fired Power Plants Have Significant and Recurring Environmental Management Needs Associated with Their Waste Byproducts. Coal-fired power plants consistently generate various waste byproducts throughout the power generation process. The primary type of these waste byproducts are CCRs, commonly known as coal ash. According to the American Coal Ash Association, more than 107 million tons of coal ash were generated in

2

Table of Contents

2016, and according to the U.S. Environmental Protection Agency (“EPA”), in 2015, coal ash was one of the largest types of waste in the U.S. Coal ash management is mission-critical to the daily operations of power plants, as they generally only have on-site storage capacity for three to four days of CCR waste accumulation.

Large Installed Base of Legacy Coal Ash Disposal Ponds That Require Remediation. According to the American Coal Ash Association, as of 2016, approximately 44% of coal ash generated was disposed of. According to the EPA, approximately 80% of coal ash that was disposed of in 2012 was disposed of on-site in ash ponds or landfills. As of 2016, the American Coal Ash Association estimated that more than 1.5 billion tons of coal ash existed in ash ponds and landfills around the country. The EPA also estimates that, as of 2012, there were over 1,100 active and inactive on-site ash ponds and landfills requiring remediation or closure. These sites are typically large and will require significant capital from their owners as well as specialized environmental expertise to monitor on an ongoing basis, remediate, relocate the waste or completely close in an environmentally sustainable way.

Recycling Waste Byproducts Is a Critical Component of the Coal Ash Value Chain. In 2016, approximately 56% of coal ash was recycled to produce positive environmental, economic and performance benefits such as reduced use of other natural resources, lower greenhouse gas emissions, and improved strength and durability of materials. The leading recycled use of coal ash is as a direct and more economic substitute for cement during the production of concrete (approximately 15 million tons of CCRs annually, as of 2016, according to the American Coal Ash Association).

Routine Nuclear Reactor Maintenance Is Non-Discretionary, Specialized, and Predictable. Given the scale, complexity, and near-constant operational demands on power plants, routine maintenance is critical to the ongoing functionality of each facility. Since it is costly to take nuclear plants offline, plant outages are planned, contracted, and announced far in advance and involve the completion of numerous maintenance services while offline (including inspections, repairs, maintenance, equipment replacement, facility modification, new construction and certifications). We estimate, based on our management’s experience and discussions with customers, our total addressable market for these services (including outsourced maintenance and capital needs) to be in excess of $5 billion annually. We believe this spend will increase over time as the nuclear reactor fleet continues to age and additional maintenance is required.

Power Plant Operators Are Increasingly Focused on Environmental Stewardship and Regulatory Compliance. Power plant operators face increasing pressure from advocacy groups and their communities to manage the environmental risks associated with their operations and, therefore, the industry is increasingly focused on environmental stewardship. Due to the considerable potential consequences associated with environmental liabilities, spending on environmental liability management has increased over time and is expected to increase in the future.

The Power Generation Industry Is Increasingly Requiring Larger Scale Environmental and Maintenance Service Providers. The mounting burden of environmental compliance, consistent need to maintain aging facilities and the focus on continuous and safe plant operations has the power generation industry (coal-fired and nuclear utilities in particular) increasingly seeking larger scale outsourced service providers as partners that can provide a range of services on their behalf. To date, most prospective service providers either have narrow service offerings or a highly localized geographic focus (sometimes limited to a single plant). Therefore, the market opportunity is substantial for specialized environmental and maintenance platforms that can offer a track record of quality service, exceptional safety, exacting environmental standards and a reliable labor force.

3

Table of Contents

Our Strengths

We believe our platform has become a leader in environmental and maintenance services to the power generation industry. Our strengths that support our leading position include:

Industry Leading Quality, Safety and Compliance

We believe we are a partner-of-choice for customers due to our reputation as a leader in quality, safety and compliance. Utilities and independent power producers are generally risk-averse and focus on strong environmental and safety considerations as key factors for awarding on-site service provider contracts. We believe our reputation for and dedication to quality, industry-leading safety record and adherence to environmental compliance standards provides a distinctive competitive advantage and differentiates us from many of our competitors. These attributes are key contributors to our leading market share positions.

Broad Platform of Mission-Critical Environmental and Maintenance Services

Our broad platform of essential environmental and maintenance services has enabled us to become a leading service provider to our power generation customers. We are the only service provider offering a suite of CCR management and recycling, environmental remediation, and outage maintenance services. Compared to service providers with more limited scope, our platform allows our customers to gain efficiencies and reduce the number of vendors on their sites by sourcing multiple required offerings from a single, trusted partner. This service offering is supported by the national scale of our operational footprint. This is a key differentiator, as many of our competitors are localized, focusing on a single geographic area (sometimes isolated to a single plant). We operate in 22 states across the country, resulting in an overall footprint and density in key markets that we believe is difficult to replicate. Our national reach enables us to successfully pursue new business within our existing customer base and attract new customers while providing consistent quality, safety and compliance standards.

Long-Term Partnerships with Leading Power Generators

Our customers are some of the largest power generation companies in the U.S., including Exelon Corporation, Duke Energy Corporation, and Dominion Energy, Inc. Given the essential nature of our services, our on-site personnel become integrated into the daily procedures of each facility, seamlessly working with utility employees to provide uninterrupted operations. This co-location and integration into the daily operations results in direct relationships with key decision makers at every level within our customers’ organizations. This embedded partnership deepens customer connectivity and drives long-term relationships which are critical for the renewal of existing contracts, winning incremental business from existing customers at new sites, and adding new customers. For example, over the last five years we have achieved an approximately 90% renewal rate for contracts in our Fossil Services offerings up for renewal.

Innovative Solutions to Our Customers’ Environmental Challenges

Our customers regularly face complex, large-scale environmental challenges that require bespoke, technical solutions. We believe we have a proactive and differentiated approach to solving these challenges. Our internal technical and engineering experts have developed deep domain knowledge and capabilities in environmental remediation and beneficial use as a result of our long-term and significant experience in the sector. We believe this credibility, combined with an entrepreneurial mindset, enables us to source market opportunities not readily available to our competitors.

Favorable Contract Dynamics Drive Predictable Financial Model

The contracted nature of our business and depth of our customer relationships provides significant visibility into both revenues and earnings, reflecting the predictable operations of our customers. Our platform of services

4

Table of Contents

is contracted for terms generally ranging from 18 months to five years, thereby reducing financial volatility. In excess of 90% of our services work is structured as time and materials, cost reimbursable or unit price contracts, which significantly reduces the risk of loss on contracts and provides gross margin visibility. At the beginning of 2017, 67% of our budgeted revenue for the year was already contracted, not including our Nuclear Services offerings that commenced operations in June 2017, which had 100% of its budgeted revenues contracted. The vast majority of our customers have investment-grade credit ratings and we have never experienced a payment issue with a client. In addition, because our capital expenditures are tied to specific, known contracts and are typically financed, we also have attractive and predictable free cash flow generation.

Entrepreneurial Management Team Supported by Highly Skilled Labor Force

We are led by an experienced management team with an entrepreneurial mindset and keen focus on safety and customer service. Our senior executive team consists of industry veterans averaging over 30 years of industry experience, helping us provide high-quality operational execution and solidify long-term customer relationships. Our ability to hire, develop and retain a highly skilled labor force with specialized skills, training and certifications is a key differentiator in the sector. For example, within our Nuclear Services offering, we have the proven ability to quickly ramp up to in excess of 5,000 employees to align with our customers’ outage schedules and service their planned maintenance needs. Our entrepreneurial mindset drives us to constantly search for new ways to maximize relevance to customers and develop innovative solutions. Our customers have unique certification and training requirements for the service providers they allow on-site.

Our Growth Strategy

Our growth strategy includes the following key initiatives:

Expand Market Share by Capitalizing on the Significant Environmental and Maintenance Needs of Power Generation Customers.

We believe we have a strong growth opportunity in the near-term, as U.S. coal-fired power generation facilities continue to remediate and close ash ponds and landfills. These projects are triggered as coal power plant operators preemptively manage environmental liabilities, comply with regulatory requirements (at the local, state, and federal levels) and work to meet consumer standards for environmental sustainability. We estimate a $3 billion pipeline of near-term remediation and closure projects in the next three years. Additionally, we believe the market for mission-critical maintenance services in the nuclear power generation market is large and growing. We estimate that the annual pipeline of near-term addressable projects for our nuclear-related business is $2.2 billion, comprised of $1.5 billion in capital projects and $700 million in Nuclear Services. We expect this market opportunity to grow over time as the nuclear reactor fleet continues to age and additional maintenance is required.

Continue to Grow On-Site Services Revenue by Expanding Environmental and Maintenance Offerings.

We believe our broad platform of environmental and maintenance services is a competitive differentiator and therefore continuing to enhance the breadth of services offered to our existing customers is a key growth opportunity. We believe opportunities exist across our platform in waste byproduct management, recycling, environmental remediation and maintenance services. We believe our customers will continue to find value in a full-service platform and source incremental services from us as an existing, on-site, trusted partner.

Leverage New and Existing Customer Relationships to Maximize Fleet-Wide Opportunities.

Given the breadth of our service offering, the trend among our customers to consolidate service providers, and our access to our customers’ senior decision makers, we believe we are well-positioned to grow our market share with current customers by providing our existing services to other coal-fired and nuclear power plants within their fleets.

5

Table of Contents

Invest in Innovative Technologies, Processes, and Solutions.

We believe investments in new technology and processes present opportunities to provide higher-margin offerings, improve the environment, and enhance relevance to our customers. For example, our recently announced acquisition of SCB International Materials, Inc. (“SCB”) provided two new technologies for incremental beneficiation of coal ash and other industrial byproducts. We hope that these innovative technologies will allow us to optimize our traditional fly ash sales & distribution, enter new markets for our products, and provide cleaner, environmentally friendly solutions to our customers. We intend to continue to invest in additional technologies and other process that expand our portfolio of solutions and further establish us as an innovator in our industry.

Enhance Our Platform via Disciplined Acquisitions.

We believe we can continue a focused acquisition strategy to add adjacent capabilities and services and enhance stockholder value. We intend to focus on environmental and industrial services, processes and technologies that support our existing capabilities and customer needs. We believe our national scale and market leadership make us a natural consolidator, particularly in our highly fragmented industry.

Our Equity Sponsor

BCP is a private equity firm investing in middle market services businesses across North American energy, industrial and infrastructure complexes with approximately $1.5 billion of assets under management. BCP seeks opportunities to apply its operations-based knowledge and relationships to positively influence the trajectory of its investments. Specifically, BCP leverages its network of world-class managers, expands services businesses across additional verticals to diversify and accelerate growth, and provides flexible buildup and growth capital.

In January 2017, BCP paid $104.1 million in exchange for a 76% equity interest in Charah, LLC. Following the completion of this offering, BCP and its affiliates will hold approximately 51.4% of our common stock. While we initially expect to be a controlled company under NYSE rules immediately after consummation of the offering, we do not intend to avail ourselves of the exemptions from the NYSE’s or Securities and Exchange Commission’s (“SEC”) corporate governance standards that may be available to a controlled company.

Corporate Reorganization

Charah Solutions was formed as a Delaware corporation in January 2018. Following this offering and the corporate reorganization described below, we will be a holding company and our only material assets will consist of membership interests in Charah Management and Allied Power Holdings. Through our ownership of Charah Management and Allied Power Holdings, we will own the outstanding equity interests in Charah, LLC and Allied Power Management, LLC, the subsidiaries through which we will operate our businesses.

Pursuant to the terms of certain reorganization transactions that will be completed immediately prior to the closing of this offering, (a) (i) Charah Holdings will contribute all of its interests in Charah Management and Allied Power Holdings to us in exchange for 17,514,745 shares of common stock, (ii) CEP Holdings will contribute all of its interests in Charah Management and Allied Power Holdings to us in exchange for 4,605,465 shares of common stock, (iii) Charah Management Holdings will contribute all of its interests in Charah Management and Allied Power Holdings to us in exchange for 907,113 shares of common stock and (iv) Allied Management Holdings will contribute all of its interests in Charah Management and Allied Power Holdings to us in exchange for 409,075 shares of common stock, (b) each of Charah Management Holdings and Allied Management Holdings will distribute the shares of common stock received by them pursuant to clause (a) to their respective members in accordance with the respective terms of their limited liability company agreements and (c) Charah Holdings will distribute a portion of the shares of common stock it received in clause (a) above to certain direct and indirect blocker entities which will ultimately merge into us, with us surviving, and the BCP Energy Services Funds will receive 14,020,861 shares of our common stock as consideration in the mergers.

6

Table of Contents

In addition, in exchange for the contribution of their profits interests in Charah Management Holdings and Allied Management Holdings to us, we will issue to the Management Members 1,335,306 shares of common stock (based on the midpoint of the price range set forth on the cover page of this prospectus) at the closing of this offering, of which 1,001,476 will be subject to time based vesting conditions, as well as performance vesting conditions that include metrics based off specified EBITDA targets and achievement of certain safety metrics (the “Management Reorganization Consideration”). The number of shares of common stock to be received by the Management Members with respect to the Management Reorganization Consideration will be calculated using an implied valuation of the Management Members historical profits interests based on the initial public offering price of the common stock offered hereby. See “Corporate Reorganization—Existing Owners’ Ownership.”

After giving effect to these transactions and the offering contemplated by this prospectus and assuming the underwriters’ option to purchase additional shares is not exercised:

| • | the Existing Owners will, collectively, own 22,712,880 shares of common stock, representing 75.5% of our capital stock (of which, (i) BCP will, directly or indirectly, own approximately 51.4% of the total issued and outstanding common stock, (ii) CEP Holdings will own approximately 15.3% of the total issued and outstanding common stock, and (iii) the Management Members, collectively, will own approximately 8.8% of the total issued and outstanding common stock, including the shares of common stock received with respect to the Management Reorganization Consideration. |

If the underwriters’ option to purchase additional shares is exercised in full:

| • | the Existing Owners will, collectively, own 21,609,939 shares of the common stock, representing 71.9% of our common stock (of which, (i) BCP will own, directly or indirectly, approximately 47.7% of the total issued and outstanding common stock, (ii) CEP Holdings will own approximately 15.3% of the total issued and outstanding common stock, and (iii) the Management Members, collectively, will own approximately 8.8% of the total issued and outstanding common stock, including the shares of common stock received with respect to the Management Reorganization Consideration. |

The number of shares to be received by our Existing Owners, and the ownership percentages above, assume an initial public offering price of $17.00 per share of common stock, the midpoint of the price range set forth on the cover page of this prospectus. Any increase or decrease (as applicable) of the assumed initial public offering price will result in an increase or decrease, respectively, in the number of shares of common stock to be received by the Management Members with respect to the Management Reorganization Consideration and the total number of shares of common stock that are outstanding after completion of this offering. See “Corporate Reorganization—Existing Owners’ Ownership.”

7

Table of Contents

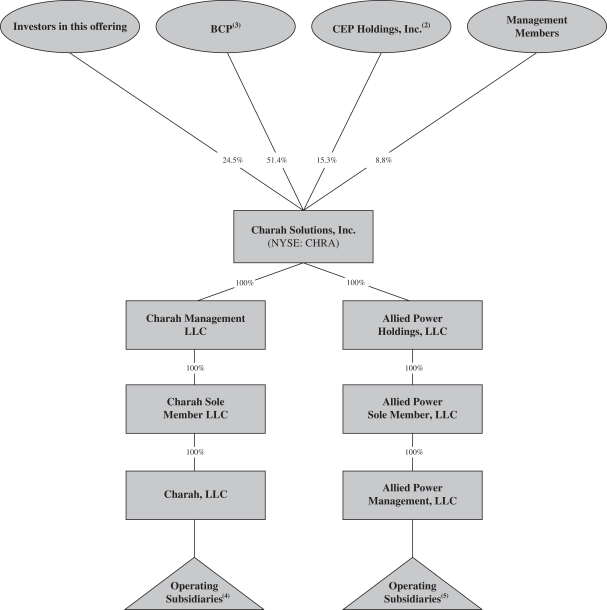

The following diagrams indicate our simplified ownership structure immediately following this offering and the transactions related thereto (assuming that the underwriters’ option to purchase additional shares is not exercised):

Simplified Ownership Structure After Giving Effect to this Offering(1)

| (1) | See “Corporate Reorganization—Existing Owners’ Ownership.” |

| (2) | CEP Holdings, Inc. is owned by Charles Price and certain affiliated entities. |

| (3) | BCP’s ownership is held through Charah Holdings and the BCP Energy Services Funds. |

| (4) | Includes (i) our operating subsidiaries, Ash Management Services, LLC and Green Meadow, LLC, (ii) our 50% interest in our equity method investment and (iii) our 67% interest in Ash Venture LLC. |

| (5) | Includes our operating subsidiaries, Allied Power Services, LLC, Allied Plant Services, LLC and Allied Power Resources, LLC. |

8

Table of Contents

Risk Factors

Investing in our common stock involves risks. You should read carefully the section of this prospectus entitled “Risk Factors” for an explanation of these risks before investing in our common stock.

Emerging Growth Company Status

We are an “emerging growth company” within the meaning of the Jumpstart Our Business Startups Act (the “JOBS Act”). For as long as we are an emerging growth company, we will not be required to comply with certain requirements that are applicable to other public companies that are not “emerging growth companies” within the meaning of the JOBS Act, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley”) and the reduced disclosure obligations regarding executive compensation in our periodic reports. In addition, Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”), for complying with new or revised accounting standards. We intend to take advantage of all of the reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards under Section 107 of the JOBS Act until we are no longer an emerging growth company. Our election to use the phase-in periods permitted by this election may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the longer phase-in periods under Section 107 of the JOBS Act and who will comply with new or revised financial accounting standards. If we were to subsequently elect instead to comply with these public company effective dates, such election would be irrevocable pursuant to Section 107 of the JOBS Act. Please see “Risk Factors—Taking advantage of the reduced disclosure requirements applicable to ‘emerging growth companies’ may make our common stock less attractive to investors.”

Our Offices

Our principal executive offices are located at 12601 Plantside Dr., Louisville, Kentucky 40299, and our telephone number at that address is (502) 245-1353. Our website address is www.charah.com. Information contained on our website, or that can be accessed from it, does not constitute part of this prospectus.

9

Table of Contents

The Offering

| Common stock offered by us |

5,294,117 shares. |

| Common stock offered by the selling stockholders |

2,058,824 shares (3,161,765 shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Total common stock offered |

7,352,941 shares (8,455,882 shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Common stock to be outstanding immediately after completion of this offering |

30,065,821 shares. |

| Common stock owned by the selling stockholders immediately after completion of this offering |

15,455,921 shares (14,352,980 shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Option to purchase additional shares |

The selling stockholders have granted the underwriters a 30-day option to purchase an aggregate of 1,102,941 additional shares of our common stock to the extent the underwriters sell more than 7,352,941 shares of common stock in this offering. |

| Use of proceeds |

We expect to receive approximately $76.0 million of net proceeds from the sale of common stock, after deducting underwriting discounts and estimated offering expenses payable by us (assuming the midpoint of the price range set forth on the cover page of this prospectus). |

| We intend to use approximately $45.3 million of the net proceeds to repay borrowings outstanding under the Term Loan and the remaining net proceeds for general corporate purposes. We have not yet made final decisions with respect to our use of the remaining proceeds for general corporate purposes, though we may use such proceeds to fund our 2018 capital program, identify and develop new services offerings or pursue acquisitions. We cannot currently allocate specific percentages of the net proceeds that we may use for such purposes. Until we use our net proceeds of the offering, we intend to invest the funds in United States government securities and other short-term, investment-grade, interest-bearing instruments or high-grade corporate notes. See “Use of Proceeds.” |

| We will not receive any proceeds from the sale of shares by the selling stockholders. |

10

Table of Contents

| Dividend policy |

The declaration and payment of any future dividends to our stockholders will be at the sole discretion of our board of directors. We do not intend to pay cash dividends in the foreseeable future. See “Dividend Policy.” |

| Registration Rights Agreement |

In connection with the closing of this offering we will enter into a Registration Rights Agreement with certain of the Existing Owners. See “Certain Relationships and Related Party Transactions—Registration Rights Agreement.” |

| Directed Share Program |

The underwriters have reserved up to 5% of the shares of common stock being offered by this prospectus (excluding the shares of common stock that may be issued upon the underwriters’ exercise of their option to purchase additional common stock) for sale to our directors, officers, employees, business associates and related persons of the Company. The number of shares of common stock available for sale to the general public will be reduced to the extent these individuals purchase such reserved shares. Any reserved shares that are not so purchased will be offered by the underwriters to the general public on the same basis as the other shares offered by this prospectus. See “Underwriting—Directed Share Program.” |

| Listing symbol |

We have been approved, subject to official notice of issuance, to list our common stock on the NYSE under the symbol “CHRA.” |

| Risk factors |

You should carefully read and consider the information set forth under the heading “Risk Factors” and all other information set forth in this prospectus before deciding to invest in our common stock. |

The number of shares of common stock to be outstanding immediately after completion of this offering reflects the issuance of 1,335,306 shares of common stock to be issued to the Management Members (1,001,476 of which will be subject to time based vesting conditions and performance vesting conditions) with respect to the Management Reorganization Consideration (which number of shares is based on the midpoint of the price range set forth on the cover page of this prospectus). See “Corporate Reorganization—Existing Owners’ Ownership.” A $1.00 increase (decrease) in the assumed initial public offering price would result in an increase (decrease) in the number of shares of common stock to be received by the Management Members with respect to the Management Reorganization Consideration of 15,911 (17,904) shares of common stock and a corresponding increase (decrease) in the total number of shares of common stock outstanding at the consummation of this offering.

Additionally, the information above does not give effect to the grant of an aggregate of 223,994 shares of common stock (based on the midpoint of the price range set forth on the cover page of this prospectus) that our board of directors has agreed to make to certain of our employees (of which 175,869 shares are restricted stock subject to vesting conditions) in connection with the completion of this offering.

11

Table of Contents

Summary Historical Combined Financial Data

Charah Solutions was formed in January 2018 and does not have historical financial results. The following table shows summary historical combined financial information of our Predecessor for the periods and as of the dates indicated. The summary historical combined financial information at December 31, 2017 and 2016, and for the years then ended, was derived from the historical audited combined financial statements of our Predecessor included elsewhere in this prospectus. The summary historical financial information at March 31, 2018 and for the three months ended March 31, 2018 and 2017 was derived from the unaudited condensed combined interim financial statements included elsewhere in this prospectus. The successor columns below represent the combined financial information of Charah, LLC and Allied Power Management, LLC for the period from January 13, 2017 through December 31, 2017 and January 1, 2018 through March 31, 2018, and the predecessor columns below represent the financial information of Charah, LLC for the year ended December 31, 2016 and the period from January 1, 2017 through January 12, 2017. The predecessor and successor columns together represent our accounting Predecessor for purposes of this registration statement. The following table should be read together with “Use of Proceeds,” “Selected Historical Combined Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Corporate Reorganization” and the financial statements and related notes included elsewhere in this prospectus.

| Successor(1) | Predecessor(2) | Successor(1) | Predecessor(2) | |||||||||||||||||||||

| Three Months Ended March 31, 2018 |

Period from January 13, 2017 through March 31, 2017 |

Period from January 1, 2017 through January 12, 2017 |

Period from January 13, 2017 through December 31, 2017 |

Period from January 1, 2017 through January 12, 2017 |

Year Ended December 31, 2016 |

|||||||||||||||||||

| (in thousands, except per share data) |

||||||||||||||||||||||||

| Statement of Income: |

||||||||||||||||||||||||

| Revenue: |

||||||||||||||||||||||||

| Environmental Solutions |

$ | 47,785 | $ | 47,856 | $ | 7,451 | $ | 232,581 | $ | 7,451 | $ | 218,051 | ||||||||||||

| Maintenance and Technical Services |

107,744 | 11,109 | 1,679 | 188,658 | 1,679 | 47,017 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total revenue |

155,529 | 58,965 | 9,130 | 421,239 | 9,130 | 265,068 | ||||||||||||||||||

| Cost of sales |

136,430 | 43,235 | 7,301 | 338,908 | 7,301 | 203,228 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Gross profit: |

||||||||||||||||||||||||

| Environmental Solutions |

12,469 | 13,036 | 1,412 | 64,433 | 1,412 | 51,282 | ||||||||||||||||||

| Maintenance and Technical Services |

6,630 | 2,694 | 417 | 17,898 | 417 | 10,558 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total gross profit |

19,099 | 15,730 | 1,829 | 82,331 | 1,829 | 61,840 | ||||||||||||||||||

| General and administrative expenses |

14,382 | 6,516 | 3,170 | 48,495 | 3,170 | 35,170 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income (loss) |

4,717 | 9,214 | (1,341 | ) | 33,836 | (1,341 | ) | 26,670 | ||||||||||||||||

| Interest expense |

(4,131 | ) | (1,055 | ) | (4,181 | ) | (14,146 | ) | (4,181 | ) | (6,244 | ) | ||||||||||||

| Income from equity method investment |

587 | 206 | 48 | 816 | 48 | 2,703 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) |

1,173 | 8,365 | (5,474 | ) | 20,506 | (5,474 | ) | 23,129 | ||||||||||||||||

| Less income attributable to non-controlling interest(3) |

(367 | ) | (270 | ) | (54 | ) | (2,190 | ) | (54 | ) | (2,198 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) attributable to Charah, LLC and Allied Power Management, LLC |

$ | 806 | $ | 8,095 | $ | (5,528 | ) | $ | 18,316 | $ | (5,528 | ) | $ | 20,931 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Pro Forma Per Share Data(4): |

||||||||||||||||||||||||

| Pro forma provision for income taxes |

$ | 202 | $ | 6,960 | (2,101) | |||||||||||||||||||

| Pro forma net income after income taxes |

$ | 604 | $ | 11,356 | (3,427) | |||||||||||||||||||

| Basic and diluted |

$ | 0.02 | $ | 0.38 | (0.11) | |||||||||||||||||||

| Pro forma weighted average shares outstanding |

||||||||||||||||||||||||

| Basic and diluted |

30,065,821 | 30,065,821 | 30,065,821 | |||||||||||||||||||||

12

Table of Contents

| Successor(1) | Predecessor(2) | Successor(1) | Predecessor(2) | |||||||||||||||||||||

| Three Months Ended March 31, 2018 |

Period from January 13, 2017 through March 31, 2017 |

Period from January 1, 2017 through January 12, 2017 |

Period from January 13, 2017 through December 31, 2017 |

Period from January 1, 2017 through January 12, 2017 |

Year Ended December 31, 2016 |

|||||||||||||||||||

| (in thousands, except per share data) |

||||||||||||||||||||||||

| Statements of Cash Flows Data: |

||||||||||||||||||||||||

| Cash flows provided by (used in) operating activities |

$ | 4,225 | $ | 1,983 | $ | (4,418 | ) | $ | 57,792 | $ | (4,418 | ) | $ | 8,351 | ||||||||||

| Cash flows provided by (used in) investing activities |

$ | (22,876 | ) | $ | (2,734 | ) | $ | — | $ | (7,270 | ) | — | $ | (15,885 | ) | |||||||||

| Cash flows provided by (used in) financing activities |

$ | (4,330 | ) | $ | 3,902 | $ | 4,463 | $ | (19,304 | ) | $ | 4,463 | $ | 7,298 | ||||||||||

| Other Financial Data: |

||||||||||||||||||||||||

| Adjusted EBITDA(5) |

$ | 17,364 | $ | 15,427 | $ | (422 | ) | $ | 76,430 | $ | (422 | ) | $ | 58,965 | ||||||||||

| Adjusted EBITDA margin(5) |

11.2 | % | $ | 26.2 | % | (4.6 | )% | 18.1 | % | (4.6 | )% | 22.7 | % | |||||||||||

| Balance Sheet Data (as of the end of the periods indicated): |

||||||||||||||||||||||||

| Total assets |

$ | 416,918 | $ | 377,651 | $ | 188,834 | ||||||||||||||||||

| Long-term debt |

$ | 233,438 | $ | 227,698 | $ | 113,182 | ||||||||||||||||||

| Total liabilities |

$ | 367,699 | $ | 329,332 | $ | 167,488 | ||||||||||||||||||

| Total members’ equity (including non-controlling interest) |

$ | 49,219 | $ | 48,319 | $ | 21,346 | ||||||||||||||||||

| (1) | The successor columns represent the combined financial information of Charah, LLC and Allied Power Management, LLC for the periods from January 13, 2017 through March 31, 2017, January 13, 2017 through December 31, 2017 and January 1, 2018 through March 31, 2018, as applicable, as reflected in our financial statements included elsewhere in this prospectus. The predecessor and successor columns together represent our accounting Predecessor for purposes of this registration statement. |

| (2) | The predecessor columns represent the financial information of Charah, LLC for the year ended December 31, 2016 and the period from January 1, 2017 through January 12, 2017 as reflected in our audited financial statements included elsewhere in this prospectus. The predecessor and successor columns together represent our accounting Predecessor for purposes of this registration statement. |

| (3) | Relates to one of our joint ventures. |

| (4) | Pro forma net income (loss), net income (loss) per share and weighted average shares outstanding reflect the estimated number of shares of common stock we expect to have outstanding upon the completion of our corporate reorganization described under “ —Corporate Reorganization.” Our Predecessor was not subject to U.S. federal income tax at an entity level. As a result, the combined net income in our historical financial statements does not reflect the tax expense we would have incurred if we were subject to U.S. federal income tax at an entity level during such periods. |

| (5) | Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP financial measures. For a definition of Adjusted EBITDA and Adjusted EBITDA margin, as well as a reconciliation to our most directly comparable financial measures calculated and presented in accordance with GAAP, please read “—Non-GAAP Financial Measures” immediately below. |

Non-GAAP Financial Measures

Adjusted EBITDA and Adjusted EBITDA margin are not financial measures determined in accordance with GAAP. We define Adjusted EBITDA as net income before interest expense, depreciation and amortization, equity-based compensation and income taxes, elimination of certain legacy expenses, amounts from a non-acquired business line, and transaction related expenses and other items. Adjusted EBITDA margin represents

13

Table of Contents

the ratio of Adjusted EBITDA to total revenues (which for the year ended December 31, 2016 were less revenues ($5,045) of a non-acquired business line).

We believe Adjusted EBITDA and Adjusted EBITDA margin are useful performance measures because they allow for an effective evaluation of our operating performance when compared to our peers, without regard to our financing methods or capital structure. We exclude the items listed above from net income in arriving at Adjusted EBITDA because these amounts are either non-recurring or can vary substantially within our industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. Adjusted EBITDA should not be considered as an alternative to, or more meaningful than, net income determined in accordance with GAAP. Certain items excluded from Adjusted EBITDA are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as the historic costs of depreciable assets, none of which are reflected in Adjusted EBITDA. Our presentation of Adjusted EBITDA should not be construed as an indication that our results will be unaffected by the items excluded from Adjusted EBITDA. Our computations of Adjusted EBITDA may not be identical to other similarly titled measures of other companies. We use Adjusted EBITDA margin to measure the success for our business in managing our cost base and improving profitability. The following tables present reconciliations of Adjusted EBITDA to net income, our most directly comparable financial measure calculated and presented in accordance with GAAP, along with our Adjusted EBITDA margin. The successor columns below represent the combined financial information of Charah, LLC and Allied Power Management, LLC for the periods from January 13, 2017 through December 31, 2017 and January 13, 2017 through March 31, 2017, as well as the three months ended March 31, 2018, and the predecessor columns below represent the financial information of Charah, LLC for the year ended December 31, 2016 and the period from January 1, 2017 through January 12, 2017, each as reflected in our unaudited and audited financial statements, as applicable, included elsewhere in this prospectus. The predecessor and successor columns together represent our accounting Predecessor for purposes of this registration statement.

| Successor(1) | Predecessor(2) | Successor(1) | Predecessor(2) | |||||||||||||||||||||

| Three Months Ended March 31, 2018 |

Period from January 13, 2017 through March 31, 2017 |

Period from January 1, 2017 through January 12, 2017 |

Period from January 13, 2017 through December 31, 2017 |

Period from January 1, 2017 through January 12, 2017 |

Year Ended December 31, 2016 |

|||||||||||||||||||

| (in thousands) |

||||||||||||||||||||||||

| Net income (loss) attributable to Charah, LLC and Allied Power Management, LLC |

$ | 806 | $ | 8,095 | $ | (5,528 | ) | $ | 18,316 | $ | (5,528 | ) | $ | 20,931 | ||||||||||

| Interest expense |

4,131 | 1,055 | 4,181 | 14,146 | 4,181 | 6,244 | ||||||||||||||||||

| Depreciation and amortization |

8,431 | 6,157 | 763 | 25,719 | 763 | 15,601 | ||||||||||||||||||

| Elimination of certain non-recurring and non-operating legal costs(3) |

2,680 | — | — | 8,650 | — | — | ||||||||||||||||||

| Elimination of certain non-recurring startup costs(4) |

793 | — | — | 6,167 | — | — | ||||||||||||||||||

| Equity-based compensation |

110 | 56 | — | 2,429 | — | 7,352 | ||||||||||||||||||

| Elimination of legacy expenses |

— | — | — | — | — | 3,910 | (5) | |||||||||||||||||

| Non-acquired business line |

— | — | — | — | — | 3,768 | (6) | |||||||||||||||||

| Transaction related expenses and other items(7) |

413 | 64 | 162 | 1,003 | 162 | 1,159 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 17,364 | $ | 15,427 | $ | (422 | ) | $ | 76,430 | $ | (422 | ) | $ | 58,965 | ||||||||||

| Adjusted EBITDA margin(8) |

11.2 | % | 26.2 | % | (4.6 | )% | 18.1 | % | (4.6 | )% | 22.7 | % | ||||||||||||

| (1) | The successor columns represent the combined financial information of Charah, LLC and Allied Power Management, LLC for the periods from January 13, 2017 through March 31, 2017 January 13, 2017 through December 31, 2017 and January 1, 2018 through March 31, 2018, as applicable, as reflected in our financial |

14

Table of Contents

| statements included elsewhere in this prospectus. The predecessor and successor columns together represent our accounting Predecessor for purposes of this registration statement. |

| (2) | The predecessor columns represent the financial information of Charah, LLC for the year ended December 31, 2016 and the period from January 1, 2017 through January 12, 2017 as reflected in our audited financial statements included elsewhere in this prospectus. The predecessor and successor columns together represent our accounting Predecessor for purposes of this registration statement. |

| (3) | For the three months ended March 31, 2018, represents non-recurring legal expenses associated with the lawsuit filed by APTIM Corp. against Allied Power Management, LLC in July 2017, and for the year ended December 31, 2017, represents non-operating and non-recurring legal expenses associated with the legal entity formation of Allied Power Management, LLC as well as legal expenses associated with the lawsuit filed by APTIM Corp. against Allied Power Management, LLC in July 2017. As a result, these costs will be non-recurring following the resolution of the APTIM litigation and are not representative of legal costs that we will incur from time to time in the ordinary course of our business. |

| (4) | Represents non-recurring start-up costs associated with the startup of Allied Power Management, LLC and our Nuclear Services offerings, including the setup of financial operations systems and modules, pre-contract expenses to obtain initial contracts and the hiring of operational staff. Because these costs are associated with the initial setup of the Allied business to initiate the operations involved in our Nuclear Services offerings, these costs are non-recurring in the normal course of our business. |

| (5) | Primary components include a change in charitable giving and other business expense policies associated with the BCP investment. |

| (6) | Non-acquired business line item adjusts for a legacy operation of Charah, LLC that was transferred to a stockholder of CEP Holdings in January 2017 prior to the BCP investment. |

| (7) | Transaction related expenses and other items include certain transaction expenses incurred in connection with the BCP investment and SCB acquisition, as well as certain financing transaction expenses. |

| (8) | Adjusted EBITDA margin is a non-GAAP measure that represents the ratio of Adjusted EBITDA to total revenues (which for the year ended December 31, 2016 were less revenues ($5,045) of a non-acquired business line). We use Adjusted EBITDA margin to measure the success of our businesses in managing our cost base and improving profitability. |

15

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with the risks and uncertainties described elsewhere in this prospectus, including our historical combined financial statements and the related notes contained elsewhere in this prospectus, before you decide to purchase shares of our common stock. If any of the following risks or uncertainties actually occurs, our business, financial condition, results of operations, cash flow and prospects could be materially and adversely affected. As a result, the price of our common stock could decline and you could lose all or part of your investment in our common stock.

Risks Related to Our Business

A decline in the production of CCRs by our coal-fired utility industry customers due to environmental regulations or otherwise could negatively impact our profitability and hinder our growth.

Many of our services are dependent upon the production of CCRs by our coal-fired utility customers. The coal-fired utility industry is facing a number of new and pending initiatives by regulatory authorities seeking to address air and water pollution, greenhouse gas emissions and management and disposal of CCRs. In recent years, federal and state environmental regulation has imposed more stringent requirements regarding emission of air pollutants and other toxic chemicals, reduction of greenhouse gas emissions and water quality impacts from coal operations. Adoption of more stringent regulations governing coal combustion, water discharges or air emissions may decrease the amount of CCRs produced by our customers and, as a result, the demand for our services. Faced with the prospect of more stringent regulations, litigation by environmental groups and the relatively low cost of natural gas, an increasing number of utilities are reducing their portfolio of coal-fired power plants. This reduction could increase if the Clean Power Plan, which urges states to substitute electricity generation from higher-emitting coal plants to low-emitting coal and natural gas plants and zero-emitting renewable sources, is upheld in court and retained by the EPA. See “Business—Regulation.”

Increasing requirements generally will increase the cost of doing business and may make coal burning less attractive for utilities. In recent years, multiple companies have announced plans to close coal-fired power plant units or plants, or dropped plans to open new plants, citing the cost of compliance with pending or new environmental regulations and the relatively low cost of natural gas. A reduction in the use of coal as fuel would cause a decline in the production and availability of CCRs, which would adversely affect our Fossil Services and Byproduct Sales offerings and result in reduced revenues. The outcome of these developments cannot be predicted but could have a material adverse effect on our business, results of operation, financial condition and cash flows.

Unsatisfactory service and safety performance may negatively affect our customer relationships and, to the extent we fail to retain existing customers or attract new customers, adversely impact our revenues.

Our ability to retain existing customers and attract new business is dependent on many factors, including our ability to demonstrate that we can reliably and safely operate our business in a manner that is consistent with our customers’ standards of service as well as applicable laws, rules and permits, which legal requirements are subject to change. Existing and potential customers consider the safety and service record of their third-party service providers to be of high importance in their decision to engage such providers. The power generation industry generally emphasizes safety and service over the lowest cost service provider due to economic and reputational risk associated with operations at their facilities. If one or more accidents were to occur while we are providing services to our customers, or if we were unable to maintain the level of safety and service our customers require, the affected customer may seek to terminate or cancel our services and may be less likely to continue to use our services, which could cause us to lose substantial revenues. Furthermore, our ability to attract new customers may be impaired if they view our safety record or service as unacceptable. In addition, it is possible that we will experience multiple or particularly severe accidents in the future, causing our safety record to deteriorate. This may be more likely as we continue to grow, if we experience high employee turnover or a labor shortage or hire inexperienced personnel to support our staffing needs.

16

Table of Contents

A substantial portion of our Maintenance and Technical Services segment consists of the provision of Nuclear Services offerings to nuclear power plants. To the extent there is a decrease in these plants, either due to reduced investment, increased regulation or otherwise, demand for our Nuclear Services offerings could decrease.

U.S. nuclear capacity and electricity generation are expected to decline due to continuing low natural gas prices and the rapid expansion of low-cost renewable energy and new technologies in the U.S., displacing more traditional sources of power, including nuclear power. Public support for nuclear power has also softened because of concerns about safety and environmental issues and new construction costs.

Very few new nuclear reactors are under construction in the U.S., and several nuclear reactors are undergoing decommissioning. In addition, changes in state and federal government subsidies and increased regulation could also negatively impact the nuclear power industry. For instance, the U.S. Nuclear Regulatory Commission has broad authority under federal law to impose safety-related and other licensing requirements for the operation of nuclear generation facilities, and events at nuclear facilities or other events impacting the industry generally could lead to additional requirements and regulations on all nuclear generation facilities and could negatively impact new construction of or continued generation from nuclear power facilities. A lower number of nuclear power facilities in operation and decrease in related maintenance and construction budgets would have a material adverse effect on our business, results of operation, financial condition and cash flows.

Loss of a large customer may adversely affect our revenue and operating results.

During 2017 and 2016, Duke Energy Corporation (“Duke Energy”) accounted for 49% and 68% of our revenues, respectively, through our provision of services at over 10 of their power plants. In 2017, Exelon Corporation (“Exelon”) accounted for 32% of our revenues, through our provision of services at 14 of their sites, representing 23 nuclear reactors. It is likely that we will continue to derive a significant portion of our revenue from a relatively small number of customers in the future. If a major customer fails to pay us, revenue would be impacted and our operating results and financial condition could be materially harmed. Additionally, if we were to lose any material customer, such loss would have a material adverse effect on our business.

We and our customers operate in industries subject to significant environmental regulation, and compliance with changes in, or liabilities under, such regulations could add significantly to the costs of conducting business.