Attached files

| file | filename |

|---|---|

| 8-K - 8-K - ESSEX PROPERTY TRUST, INC. | form8k.htm |

Exhibit 99.1

INVESTOR PRESENTATIONMAY/JUNE 2018

ABOUT ESSEX EXECUTIVE SUMMARYWEST COAST FUNDAMENTALSINVESTMENT OVERVIEW AND CAPITAL STRUCTUREFINANCIAL PERFORMANCE AND 2018 GUIDANCEAPPENDIXPROVEN TRACK RECORD ESSEX PORTFOLIODEFINITIONS & RECONCILIATIONS PAGE(S)23 4 – 17 18 – 2526 – 3031 32 – 3435 – 3839 – 48 TABLE OF CONTENTS *

(1) Represents percent of pro rata NOI as of 3/31/18.(2) Oakland includes Alameda and Contra Costa Counties.(3) As of 3/31/18. * San Francisco MD 8%Oakland(2) 13%Santa Clara 19% Ventura 4%Los Angeles 19%Orange County 11%San Diego 8% SOUTHERN CA43% of NOI(1) NORTHERN CA40% of NOI(1) Washington & California combined represent the 5th highest GDP in the world SEATTLE17% of NOI(1) ESSEX IS THE ONLY PUBLIC MULTIFAMILY REIT DEDICATED EXCLUSIVELY TO THE WEST COAST, WITH A PRIMARY FOCUS IN 8 MAJOR METROS: ESSEX AT A GLANCE

EXECUTIVE SUMMARY * ESSEX’S WEST COAST MARKETS ARE EXPECTED TO LEAD THE NATION IN RENT GROWTH OVER THE NEXT SEVERAL YEARS DUE TO FAVORABLE SUPPLY AND DEMAND DYNAMICS KEY HIGHLIGHTS The embedded housing shortage of 7.3 million units remains a key issue – California represents roughly half of the nation’s underproduction of housing from 2000-2015 (p. 6)Pockets of new multifamily supply continue to periodically disrupt pricing power in certain urban submarkets; however, we believe the construction pipeline has peaked in our markets and multifamily supply will slowly taper off over the next several years (p. 8)Nearly 40% of the current under-construction pipeline is in downtown CBD markets, where only 10% of Essex’s same-property apartment homes are locatedWealth creation on the West Coast continues to lead the nation (pp. 9-10)Demand drivers on the West Coast remain strong, demonstrated by favorable job growth that has led to ultra-low unemployment rates across our markets, averaging 3.1% (p. 11)Solid job growth has been favorably impacted by migration trends and the ability of local employers to source and retain skilled workers (pp. 12-13)As the skilled labor shortage intensifies, wage growth continues to improve, helping alleviate affordability pressures (pp. 14-15)The technology markets remain robust – California and Washington had ~20,000 technology company job openings in April 2018, compared to ~16,000 at the beginning of 2018Essex’s West Coast markets are expected to generate 3.0% rent growth in 2018, which is above the U.S. at 2.5%(1) and major East Coast metros (pp. 30 & 17) Source: Axiometrics (1) Includes Axiometrics’ top 120 MSA’s.

Gas Company LoftsLos Angeles, CA(Renovation included the addition of rooftop amenity with pool) Agora at South MainWalnut Creek, CA(2016 Development) WEST COAST FUNDAMENTALS EmmeEmeryville, CA

WHY WEST COAST MARKETS? * LONG-TERM FAVORABLE SUPPLY/DEMAND DYNAMICS

* CALIFORNIA’S CHRONIC HOUSING SHORTAGE Source: Up for Growth National Coalition - Housing Underproduction in the U.S., April 2018 IN THE U.S., 23 STATES HAVE PRODUCED ~7.3 MILLION TOO FEW HOUSING UNITS FROM 2000-2015CALIFORNIA REPRESENTS NEARLY 50% OF THE HOUSING SHORTFALL AT ~3.4 MILLION UNITS

Sources: Census, Essex, and Rosen LIMITED SUPPLY IN ESSEX MARKETS ESSEX CA SUPPLY AS A PERCENT OF STOCK HAS HISTORICALLY REMAINED BELOW 1% RELATIVE TO THE NATION, ESSEX’S CA MARKETS HAVE LESS HOUSING SUPPLY WITH BETTER JOB GROWTH *

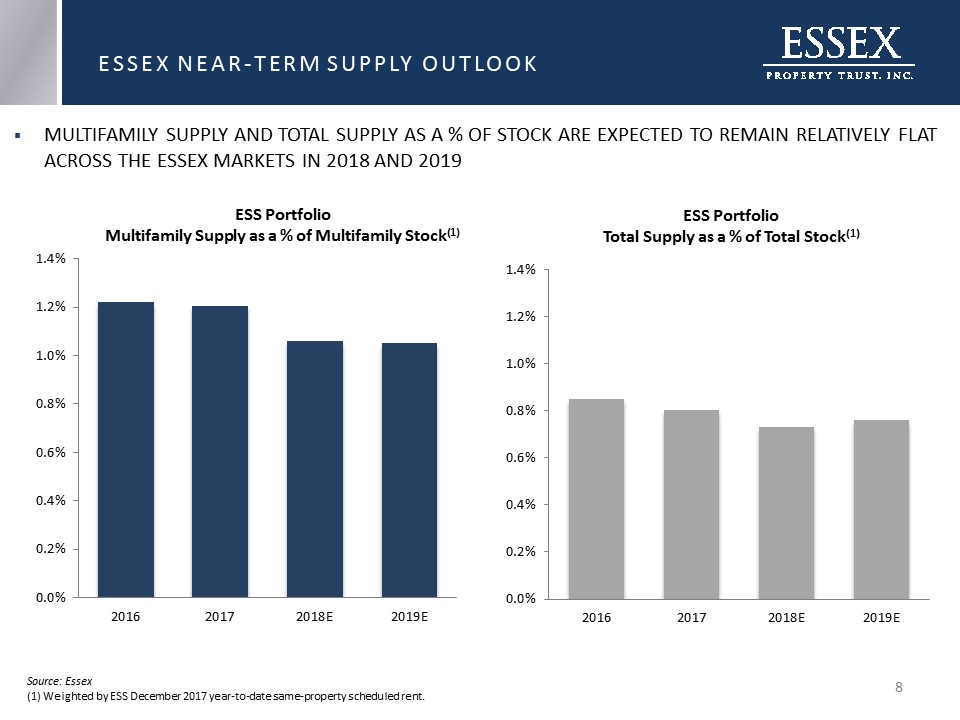

MULTIFAMILY SUPPLY AND TOTAL SUPPLY AS A % OF STOCK ARE EXPECTED TO REMAIN RELATIVELY FLAT ACROSS THE ESSEX MARKETS IN 2018 AND 2019 Source: Essex(1) Weighted by ESS December 2017 year-to-date same-property scheduled rent. ESSEX NEAR-TERM SUPPLY OUTLOOK *

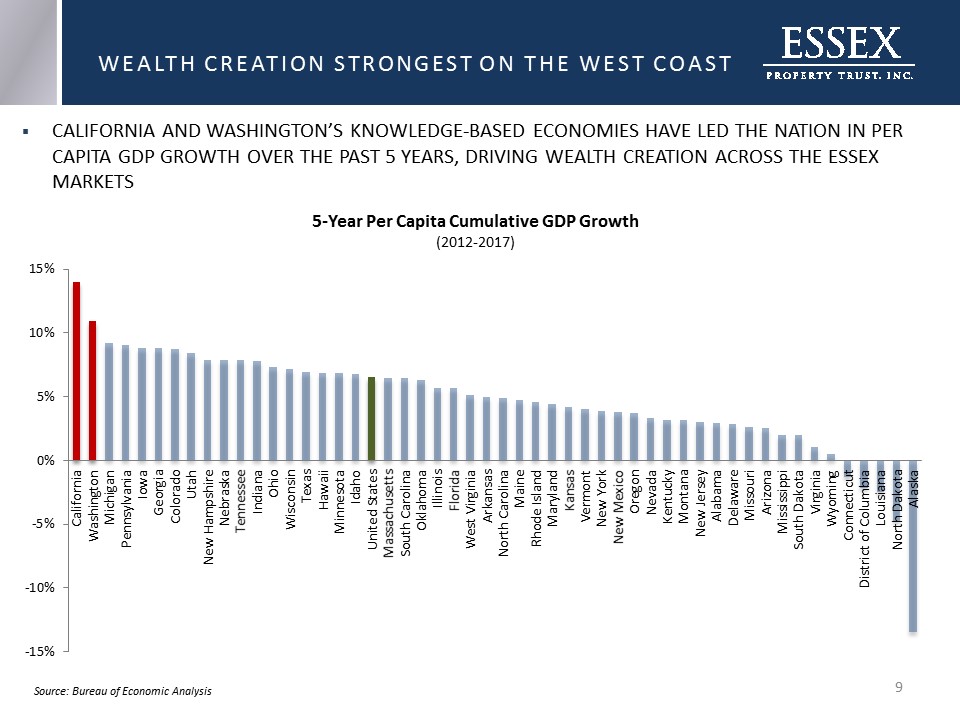

* WEALTH CREATION STRONGEST ON THE WEST COAST CALIFORNIA AND WASHINGTON’S KNOWLEDGE-BASED ECONOMIES HAVE LED THE NATION IN PER CAPITA GDP GROWTH OVER THE PAST 5 YEARS, DRIVING WEALTH CREATION ACROSS THE ESSEX MARKETS Source: Bureau of Economic Analysis

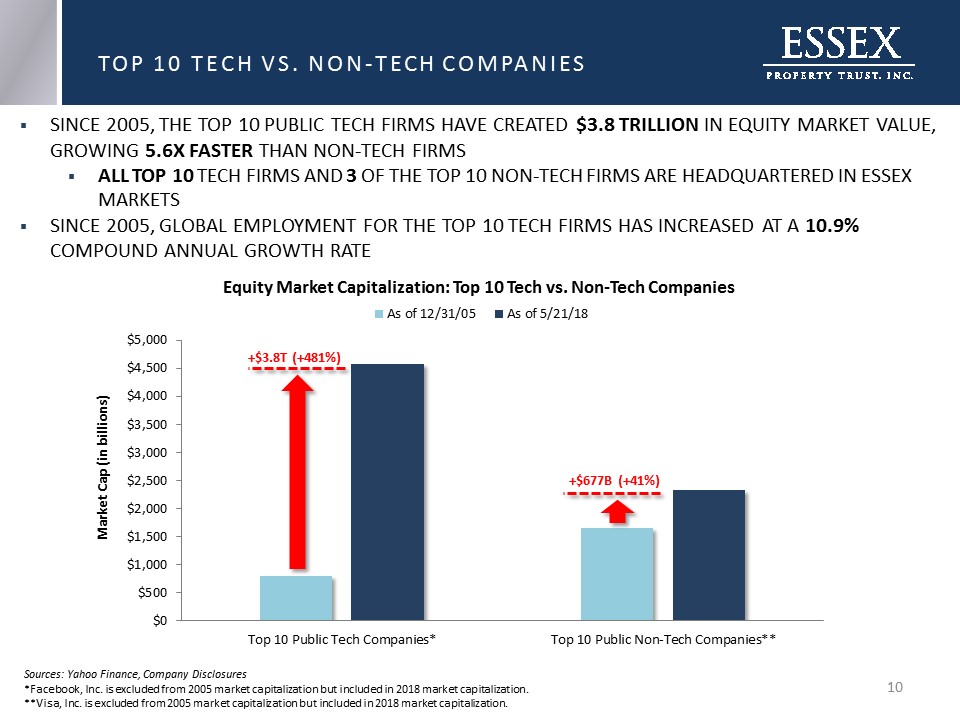

* TOP 10 TECH VS. NON-TECH COMPANIES SINCE 2005, THE TOP 10 PUBLIC TECH FIRMS HAVE CREATED $3.8 TRILLION IN EQUITY MARKET VALUE, GROWING 5.6X FASTER THAN NON-TECH FIRMSALL TOP 10 TECH FIRMS AND 3 OF THE TOP 10 NON-TECH FIRMS ARE HEADQUARTERED IN ESSEX MARKETSSINCE 2005, GLOBAL EMPLOYMENT FOR THE TOP 10 TECH FIRMS HAS INCREASED AT A 10.9% COMPOUND ANNUAL GROWTH RATE +$3.8T (+481%) +$677B (+41%) Sources: Yahoo Finance, Company Disclosures*Facebook, Inc. is excluded from 2005 market capitalization but included in 2018 market capitalization.**Visa, Inc. is excluded from 2005 market capitalization but included in 2018 market capitalization.

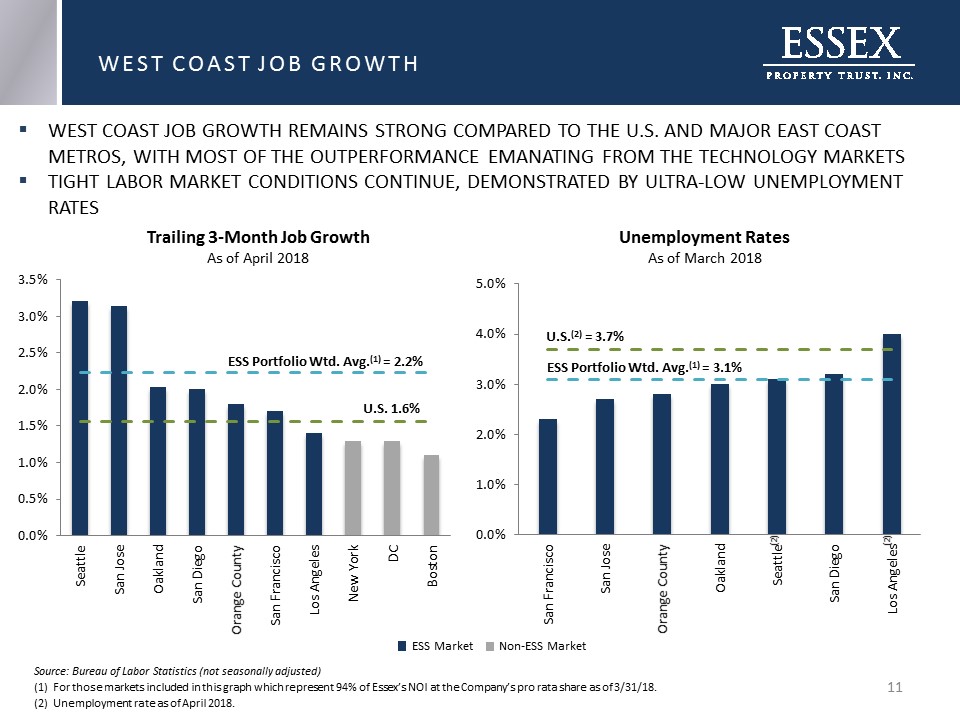

WEST COAST JOB GROWTH WEST COAST JOB GROWTH REMAINS STRONG COMPARED TO THE U.S. AND MAJOR EAST COAST METROS, WITH MOST OF THE OUTPERFORMANCE EMANATING FROM THE TECHNOLOGY MARKETSTIGHT LABOR MARKET CONDITIONS CONTINUE, DEMONSTRATED BY ULTRA-LOW UNEMPLOYMENT RATES Source: Bureau of Labor Statistics (not seasonally adjusted)(1) For those markets included in this graph which represent 94% of Essex’s NOI at the Company’s pro rata share as of 3/31/18.(2) Unemployment rate as of April 2018. * (2) U.S.(2) = 3.7% ESS Portfolio Wtd. Avg.(1) = 2.2% ESS Market Non-ESS Market U.S. 1.6% (2)

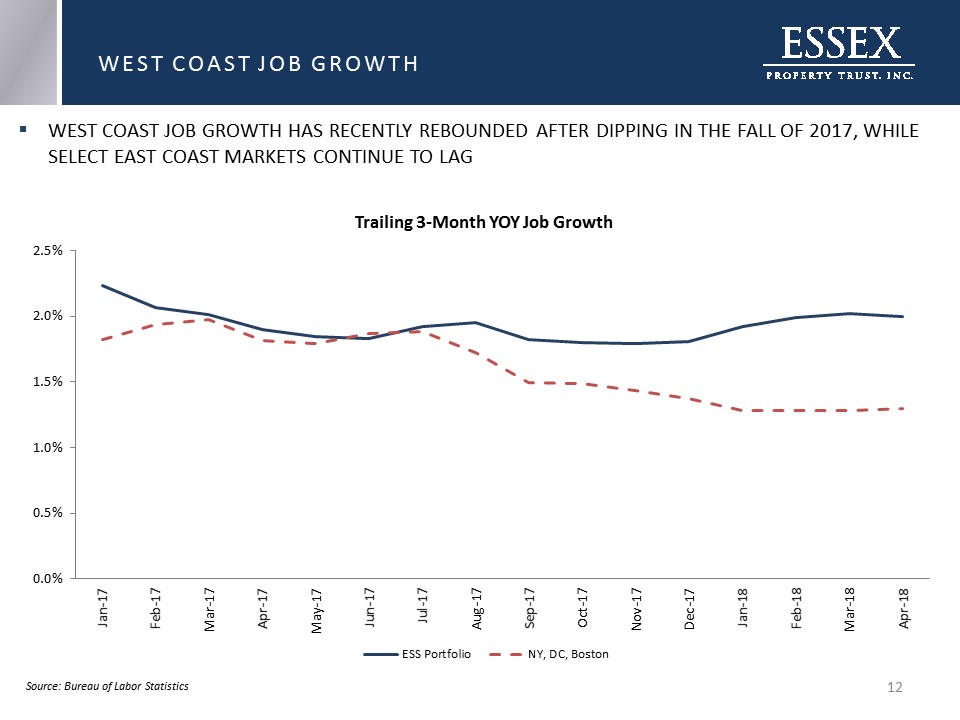

WEST COAST JOB GROWTH WEST COAST JOB GROWTH HAS RECENTLY REBOUNDED AFTER DIPPING IN THE FALL OF 2017, WHILE SELECT EAST COAST MARKETS CONTINUE TO LAG Source: Bureau of Labor Statistics *

* RECENT MIGRATION TRENDS REFLECT THE INFLUX OF WORKERS TO ESSEX’S WEST COAST MARKETS, PRIMARILY FROM MAJOR EAST COAST METROS LINKEDIN WORKER MIGRATION TRENDS Note: LinkedIn defines migration as a member changing their location on their LinkedIn profile. The maps reflect the cities the most LinkedIn members moved to and from in the past 12 months. For every 10,000 LinkedIn members in the San Francisco Bay Area, 6 moved to the city in the last 12 months from New York City.Source: LinkedIn Workforce Report, April 2018

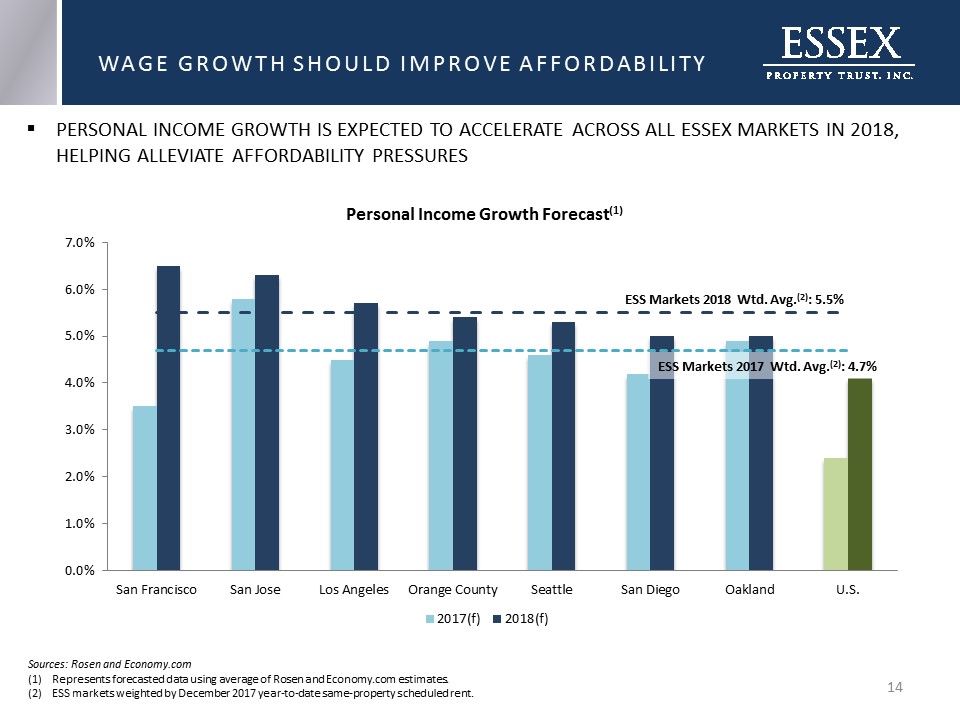

* PERSONAL INCOME GROWTH IS EXPECTED TO ACCELERATE ACROSS ALL ESSEX MARKETS IN 2018, HELPING ALLEVIATE AFFORDABILITY PRESSURES WAGE GROWTH SHOULD IMPROVE AFFORDABILITY Sources: Rosen and Economy.comRepresents forecasted data using average of Rosen and Economy.com estimates.ESS markets weighted by December 2017 year-to-date same-property scheduled rent. ESS Markets 2018 Wtd. Avg.(2): 5.5%

* Sources: Axiometrics, Rosen and Bureau of Economic Analysis WE EXPECT PERSONAL INCOMES TO GROW FASTER THAN RENTS FOR THE 3RD CONSECUTIVE YEAR IN 2018, WHICH IS HELPING ALLEVIATE AFFORDABILITY PRESSURES IN ESSEX MARKETS PERSONAL INCOME GROWTH VS. RENT GROWTH

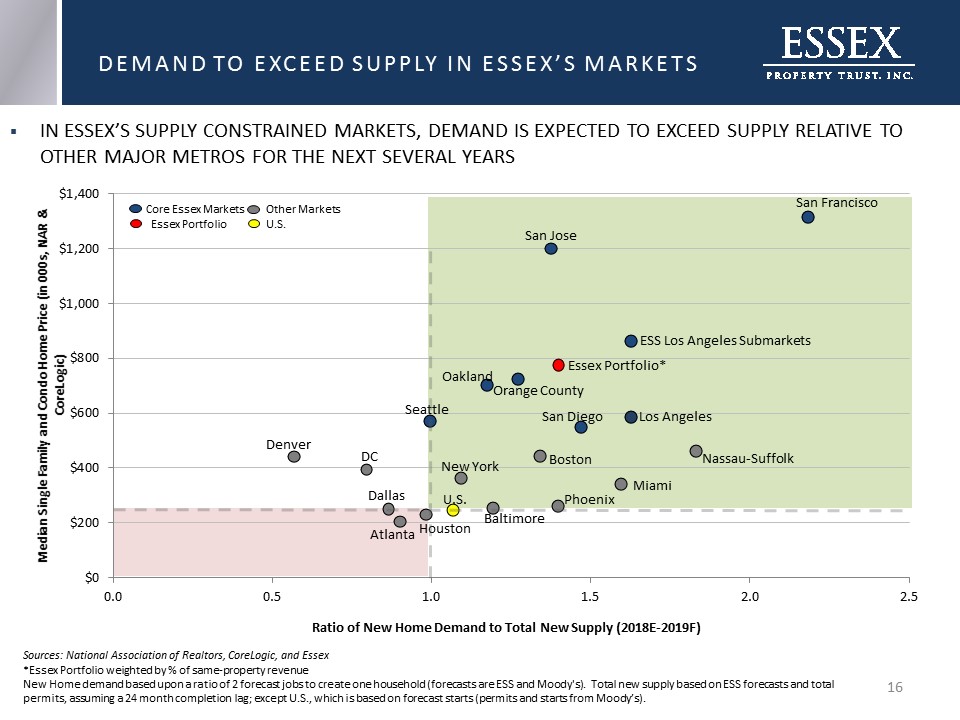

* DEMAND TO EXCEED SUPPLY IN ESSEX’S MARKETS IN ESSEX’S SUPPLY CONSTRAINED MARKETS, DEMAND IS EXPECTED TO EXCEED SUPPLY RELATIVE TO OTHER MAJOR METROS FOR THE NEXT SEVERAL YEARS Sources: National Association of Realtors, CoreLogic, and Essex*Essex Portfolio weighted by % of same-property revenueNew Home demand based upon a ratio of 2 forecast jobs to create one household (forecasts are ESS and Moody's). Total new supply based on ESS forecasts and total permits, assuming a 24 month completion lag; except U.S., which is based on forecast starts (permits and starts from Moody’s).

RENT GROWTH OUTLOOK - AXIO FORECAST WEST COAST MARKETS ARE PROJECTED TO BE THE TOP PERFORMING MARKETS THROUGH 2019ROUGHLY 88% OF ESSEX’S TOTAL NOI IS IN THE TOP PROJECTED MSA’S Axiometrics Top Projected Rent Growth Markets * Source: Axiometrics. Ranking of the top 40 largest major metros in the U.S. Weighted by % of ESS Total NOI as of first quarter 2018. Orange County (2.8%) ranks 25th.Includes Axiometrics’ top 120 MSA’s. Rank MSA Name Axio 2018 Market Rent Growth Axio 2019 Market Rent Growth '18-'19 CAGR Rent Growth % of ESS Total NOI 1 San Jose, CA 4.2% 4.9% 4.5% 19.1% 2 San Francisco, CA 3.6% 4.9% 4.3% 8.4% 3 Boston, MA 3.1% 4.6% 3.8% 4 San Diego, CA 4.4% 3.1% 3.8% 8.4% 5 Fort Lauderdale, FL 3.4% 4.0% 3.7% 6 Phoenix, AZ 4.0% 3.4% 3.7% 7 Ventura, CA 3.5% 3.8% 3.7% 4.6% 8 Denver, CO 2.7% 4.6% 3.7% 9 Houston, TX 2.6% 4.6% 3.6% 10 Oakland, CA 3.2% 4.0% 3.6% 12.4% 11 Orlando, FL 4.2% 2.9% 3.5% 12 Seattle, WA 3.1% 3.9% 3.5% 16.7% 13 Los Angeles, CA 2.5% 4.5% 3.5% 18.8% 14 Charlotte, NC 2.9% 4.0% 3.4% 15 Las Vegas, NV 2.9% 3.4% 3.2% ESS Weighted Average(1) 3.3% 4.2% 3.7% 88.4% U.S. Average Growth(2) 2.5% 3.2% 2.8%

Palm ValleySan Jose, CA MB360San Francisco, CA(2014 Development) INVESTMENT OVERVIEW AND CAPITAL STRUCTURE Station Park GreenSan Mateo, CA(2018 Development)

CORE COMPETENCIES TO CREATE VALUE * The GallowayPleasanton, CA CONDO OPTIONALITY:Potential value creation through 8,600 condo convertible apartment homes in the Essex Portfolio DEVELOPMENT:Develop high-quality tenant-desired apartment homes near transportation nodes ACQUISITIONS:Improve the NAV/share, cash flow/share and growth prospects of the Company REDEVELOPMENTFocused on rent justified improvements to maximize NOI and value CO-INVESTMENT PLATFORM:Facilitates growth via private capital and provides attractive risk adjusted returns PREFERRED EQUITY/SUBORDINATED DEBT: Opportunistically invest in high-quality development and stabilized assets in our existing markets

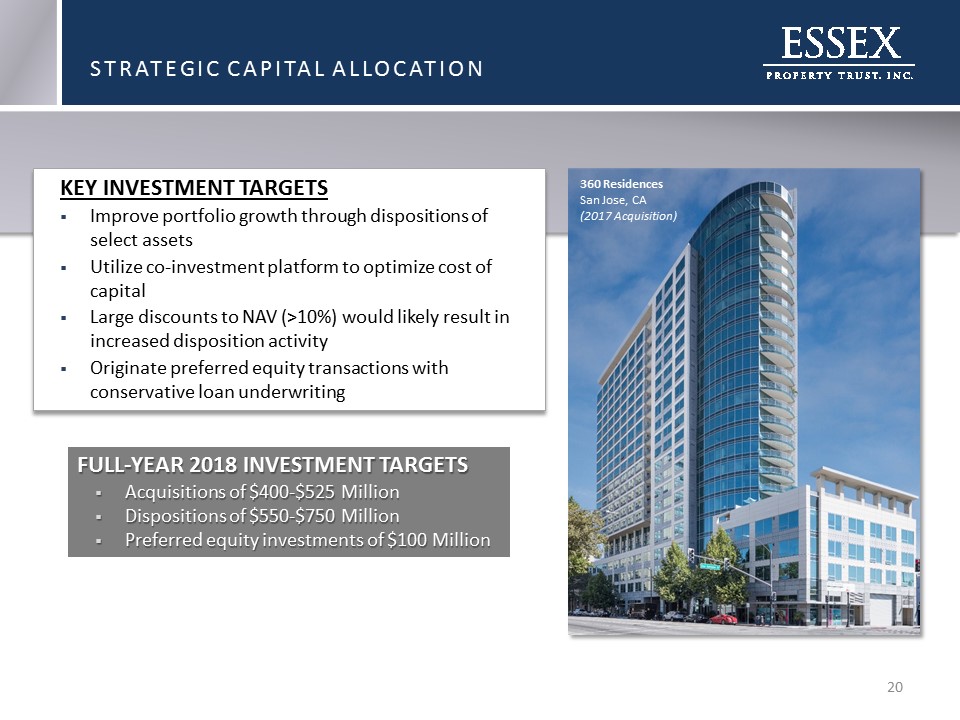

STRATEGIC CAPITAL ALLOCATION * 360 ResidencesSan Jose, CA(2017 Acquisition) KEY INVESTMENT TARGETSImprove portfolio growth through dispositions of select assetsUtilize co-investment platform to optimize cost of capital Large discounts to NAV (>10%) would likely result in increased disposition activityOriginate preferred equity transactions with conservative loan underwriting FULL-YEAR 2018 INVESTMENT TARGETSAcquisitions of $400-$525 MillionDispositions of $550-$750 MillionPreferred equity investments of $100 Million

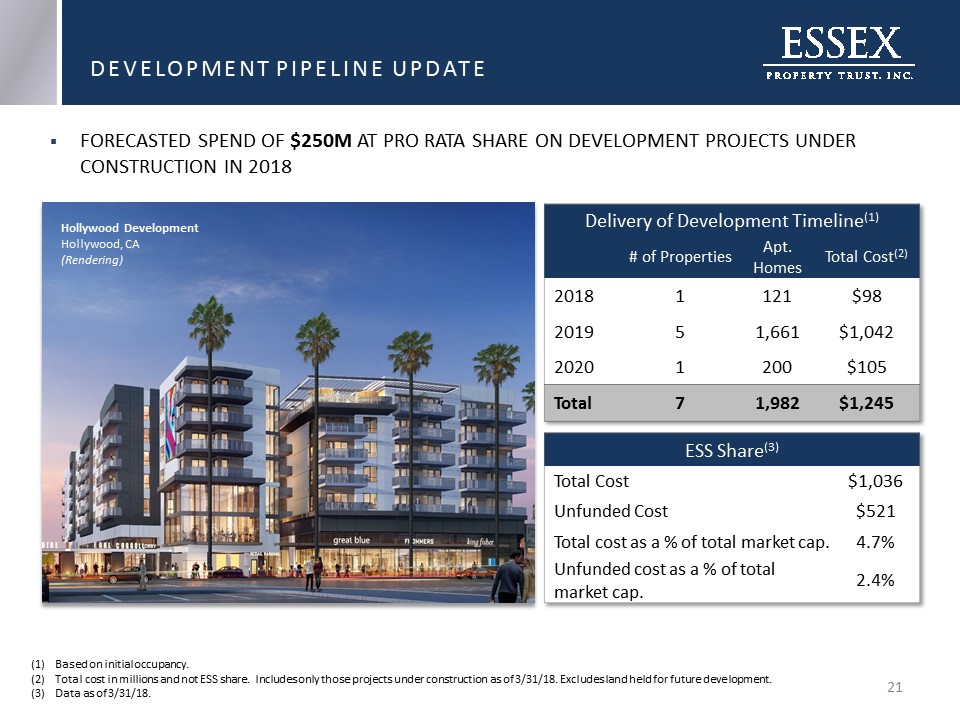

Based on initial occupancy.Total cost in millions and not ESS share. Includes only those projects under construction as of 3/31/18. Excludes land held for future development.Data as of 3/31/18. FORECASTED SPEND OF $250M AT PRO RATA SHARE ON DEVELOPMENT PROJECTS UNDER CONSTRUCTION IN 2018 DEVELOPMENT PIPELINE UPDATE * GallowayPleasanton, CA(2016 Development) Hollywood DevelopmentHollywood, CA(Rendering)

DISCIPLINED CAPITAL ALLOCATION PROCESS * DEALS MUST BE ACCRETIVE TO 3 METRICS:

$22.2 Billion Total Capitalization Data as of 3/31/18(1) Consolidated portfolio only. CAPITAL STRUCTURE & LIQUIDITY PROFILE Debt Composition(1) * STRONG BALANCE SHEET WITH AMPLE LIQUIDITY AND FINANCIAL FLEXIBILITY

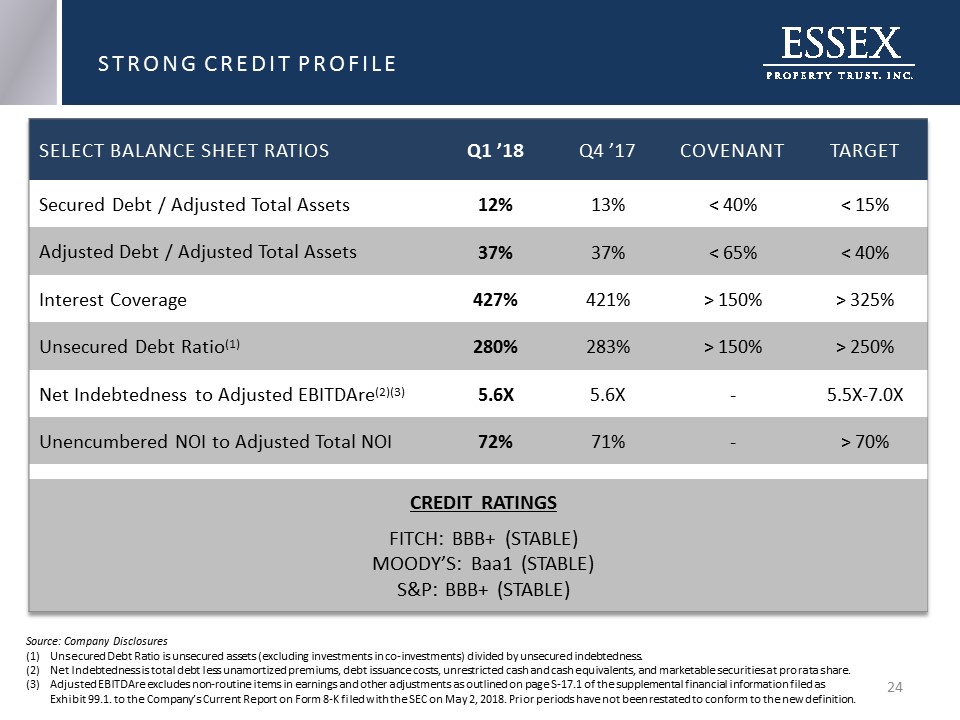

STRONG CREDIT PROFILE * Source: Company DisclosuresUnsecured Debt Ratio is unsecured assets (excluding investments in co-investments) divided by unsecured indebtedness.Net Indebtedness is total debt less unamortized premiums, debt issuance costs, unrestricted cash and cash equivalents, and marketable securities at pro rata share.Adjusted EBITDAre excludes non-routine items in earnings and other adjustments as outlined on page S-17.1 of the supplemental financial information filed as Exhibit 99.1. to the Company’s Current Report on Form 8-K filed with the SEC on May 2, 2018. Prior periods have not been restated to conform to the new definition.

WELL LADDERED DEBT MATURITY SCHEDULE % of Total Debt Maturing/Year 2.2% 11.0% 12.2% 9.5% 12.1% 10.5% 7.0% 9.0% 8.8% 8.8% 0.1% 8.8% Debt Maturity Schedule(1) (1) Data as of 3/31/2018. Excludes lines of credit. Weighted Average Interest Rate 5.5% 4.1% 4.8% 4.3% 3.1% 3.6% 4.0% 3.6% 3.4% 3.4% 3.0% 3.7% Weighted Average Interest Rate: 3.9% *

Gas Company LoftsLos Angeles, CA(Renovation included the addition of rooftop amenity with pool) Agora at South MainWalnut Creek, CA(2016 Development) FINANCIAL PERFORMANCE AND 2018 GUIDANCE EmmeEmeryville, CA 8th & RepublicanSeattle, WA(2017 Acquisition)

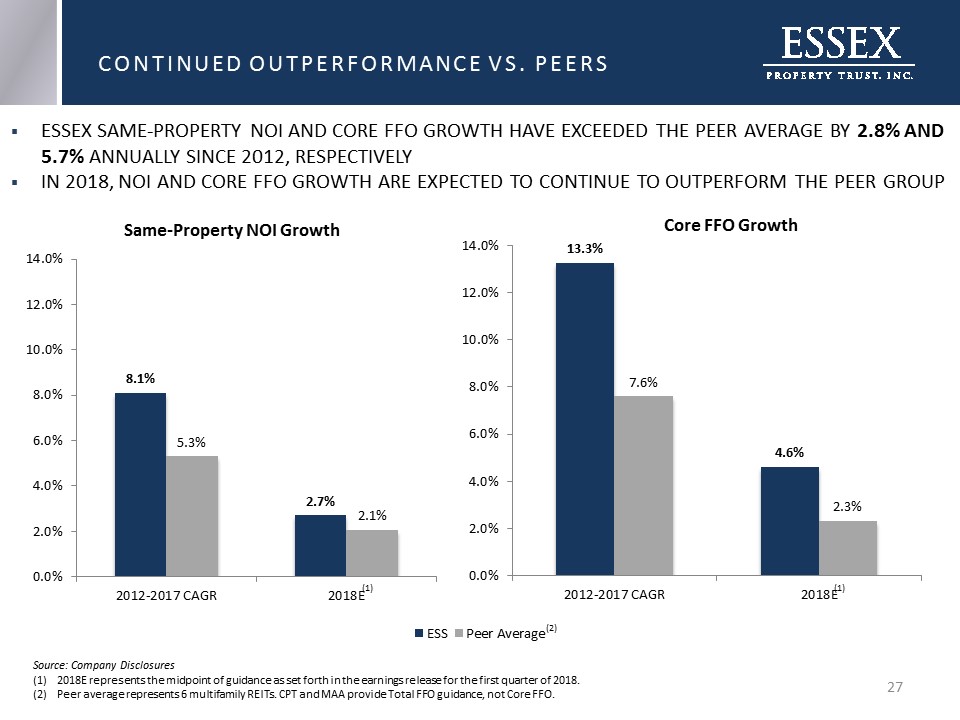

Source: Company Disclosures 2018E represents the midpoint of guidance as set forth in the earnings release for the first quarter of 2018. Peer average represents 6 multifamily REITs. CPT and MAA provide Total FFO guidance, not Core FFO. CONTINUED OUTPERFORMANCE VS. PEERS ESSEX SAME-PROPERTY NOI AND CORE FFO GROWTH HAVE EXCEEDED THE PEER AVERAGE BY 2.8% AND 5.7% ANNUALLY SINCE 2012, RESPECTIVELYIN 2018, NOI AND CORE FFO GROWTH ARE EXPECTED TO CONTINUE TO OUTPERFORM THE PEER GROUP * (2) (1) (1)

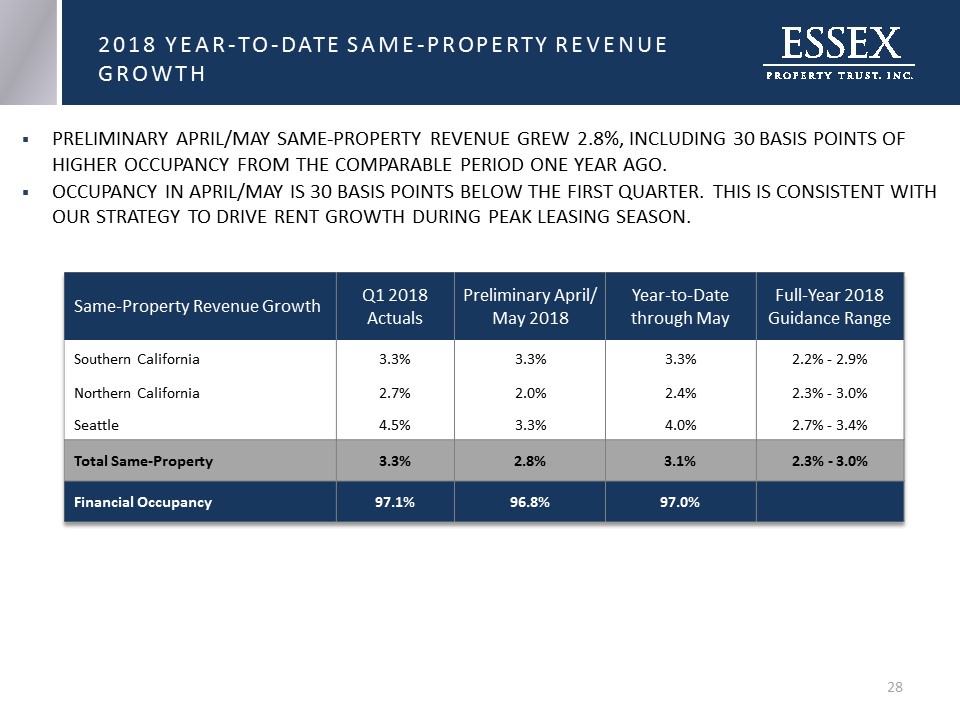

PRELIMINARY APRIL/MAY SAME-PROPERTY REVENUE GREW 2.8%, INCLUDING 30 BASIS POINTS OF HIGHER OCCUPANCY FROM THE COMPARABLE PERIOD ONE YEAR AGO.OCCUPANCY IN APRIL/MAY IS 30 BASIS POINTS BELOW THE FIRST QUARTER. THIS IS CONSISTENT WITH OUR STRATEGY TO DRIVE RENT GROWTH DURING PEAK LEASING SEASON. * 2018 YEAR-TO-DATE SAME-PROPERTY REVENUE GROWTH

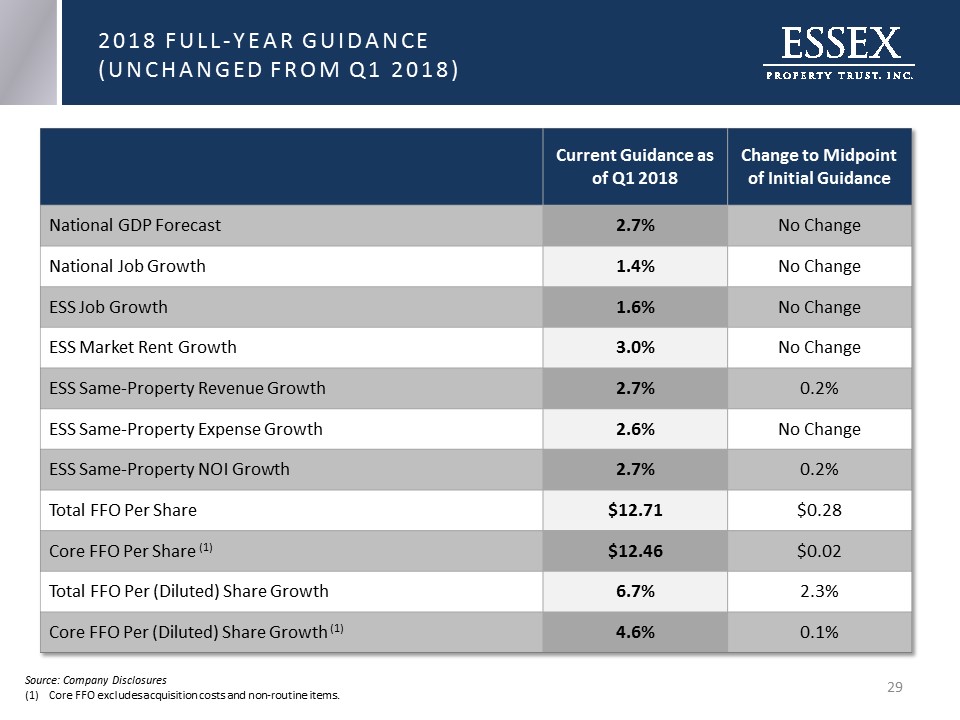

Source: Company DisclosuresCore FFO excludes acquisition costs and non-routine items. * 2018 FULL-YEAR GUIDANCE (UNCHANGED FROM Q1 2018)

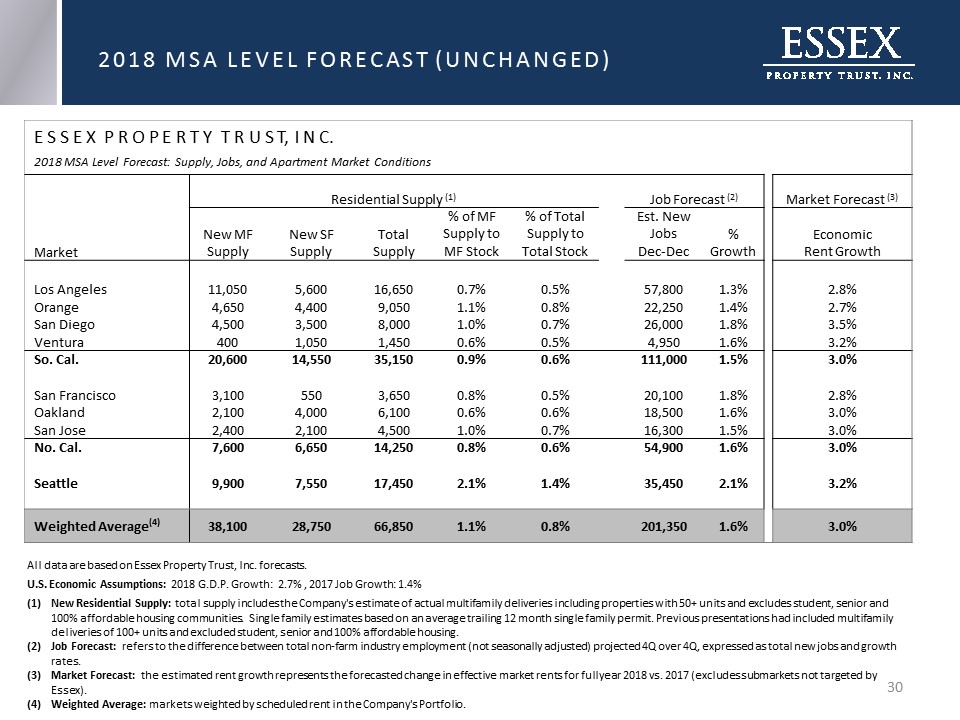

E S S E X P R O P E R T Y T R U S T, I N C. 2018 MSA Level Forecast: Supply, Jobs, and Apartment Market Conditions Residential Supply (1) Job Forecast (2) Market Forecast (3) Market New MF Supply New SF Supply Total Supply % of MF Supply to MF Stock % of Total Supply to Total Stock Est. New Jobs Dec-Dec % Growth Economic Rent Growth Los Angeles 11,050 5,600 16,650 0.7% 0.5% 57,800 1.3% 2.8% Orange 4,650 4,400 9,050 1.1% 0.8% 22,250 1.4% 2.7% San Diego 4,500 3,500 8,000 1.0% 0.7% 26,000 1.8% 3.5% Ventura 400 1,050 1,450 0.6% 0.5% 4,950 1.6% 3.2% So. Cal. 20,600 14,550 35,150 0.9% 0.6% 111,000 1.5% 3.0% San Francisco 3,100 550 3,650 0.8% 0.5% 20,100 1.8% 2.8% Oakland 2,100 4,000 6,100 0.6% 0.6% 18,500 1.6% 3.0% San Jose 2,400 2,100 4,500 1.0% 0.7% 16,300 1.5% 3.0% No. Cal. 7,600 6,650 14,250 0.8% 0.6% 54,900 1.6% 3.0% Seattle 9,900 7,550 17,450 2.1% 1.4% 35,450 2.1% 3.2% Weighted Average(4) 38,100 28,750 66,850 1.1% 0.8% 201,350 1.6% 3.0% All data are based on Essex Property Trust, Inc. forecasts.U.S. Economic Assumptions: 2018 G.D.P. Growth: 2.7% , 2017 Job Growth: 1.4%New Residential Supply: total supply includes the Company's estimate of actual multifamily deliveries including properties with 50+ units and excludes student, senior and 100% affordable housing communities. Single family estimates based on an average trailing 12 month single family permit. Previous presentations had included multifamily deliveries of 100+ units and excluded student, senior and 100% affordable housing.Job Forecast: refers to the difference between total non-farm industry employment (not seasonally adjusted) projected 4Q over 4Q, expressed as total new jobs and growth rates.Market Forecast: the estimated rent growth represents the forecasted change in effective market rents for full year 2018 vs. 2017 (excludes submarkets not targeted by Essex).Weighted Average: markets weighted by scheduled rent in the Company's Portfolio. 2018 MSA LEVEL FORECAST (UNCHANGED) *

Gas Company LoftsLos Angeles, CA(Renovation included the addition of rooftop amenity with pool) Agora at South MainWalnut Creek, CA(2016 Development) WEST COAST FUNDAMENTALS EmmeEmeryville, CA Pinnacle at MacArthur PlaceSanta Ana, CA APPENDIX

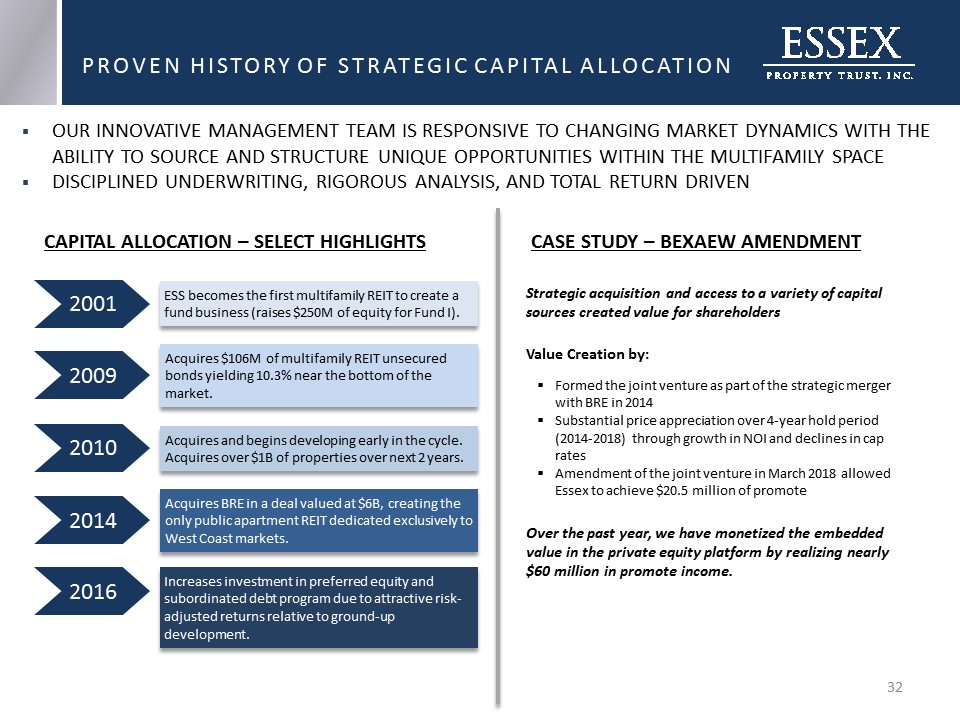

Acquires BRE in a deal valued at $6B, creating the only public apartment REIT dedicated exclusively to West Coast markets. Increases investment in preferred equity and subordinated debt program due to attractive risk-adjusted returns relative to ground-up development. Acquires and begins developing early in the cycle. Acquires over $1B of properties over next 2 years. ESS becomes the first multifamily REIT to create a fund business (raises $250M of equity for Fund I). Acquires $106M of multifamily REIT unsecured bonds yielding 10.3% near the bottom of the market. PROVEN HISTORY OF STRATEGIC CAPITAL ALLOCATION * OUR INNOVATIVE MANAGEMENT TEAM IS RESPONSIVE TO CHANGING MARKET DYNAMICS WITH THE ABILITY TO SOURCE AND STRUCTURE UNIQUE OPPORTUNITIES WITHIN THE MULTIFAMILY SPACEDISCIPLINED UNDERWRITING, RIGOROUS ANALYSIS, AND TOTAL RETURN DRIVEN 2016 2014 2010 2009 2001 CAPITAL ALLOCATION – SELECT HIGHLIGHTS CASE STUDY – BEXAEW AMENDMENT Strategic acquisition and access to a variety of capital sources created value for shareholders Value Creation by:Formed the joint venture as part of the strategic merger with BRE in 2014Substantial price appreciation over 4-year hold period (2014-2018) through growth in NOI and declines in cap ratesAmendment of the joint venture in March 2018 allowed Essex to achieve $20.5 million of promote Over the past year, we have monetized the embedded value in the private equity platform by realizing nearly $60 million in promote income.

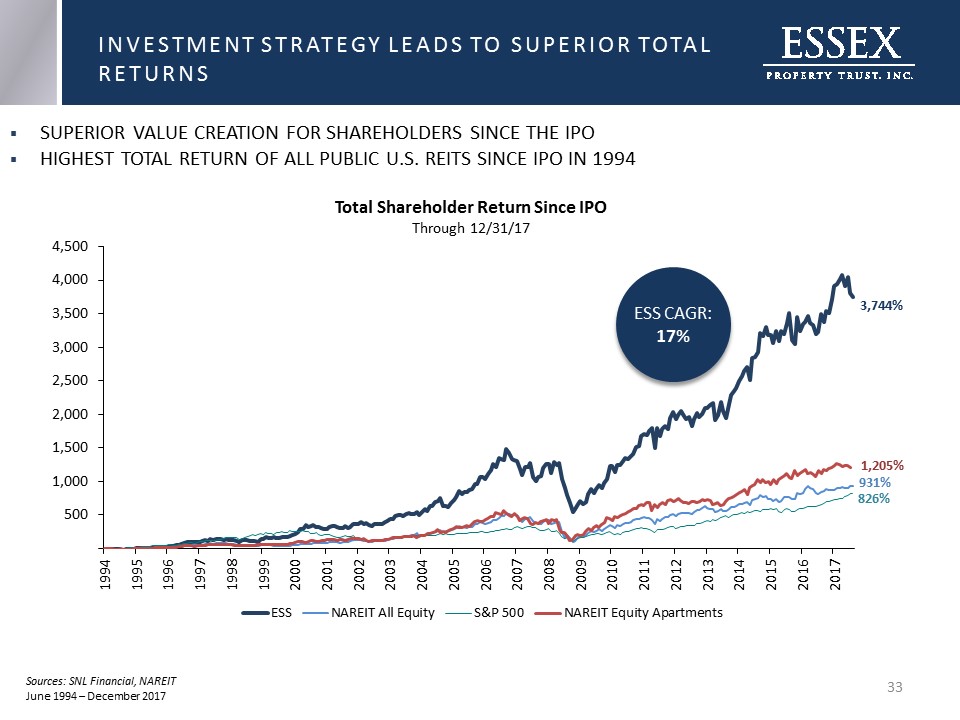

INVESTMENT STRATEGY LEADS TO SUPERIOR TOTAL RETURNS SUPERIOR VALUE CREATION FOR SHAREHOLDERS SINCE THE IPOHIGHEST TOTAL RETURN OF ALL PUBLIC U.S. REITS SINCE IPO IN 1994 Sources: SNL Financial, NAREITJune 1994 – December 2017 * ESS CAGR: 17% 3,744% 1,205% 931% 826%

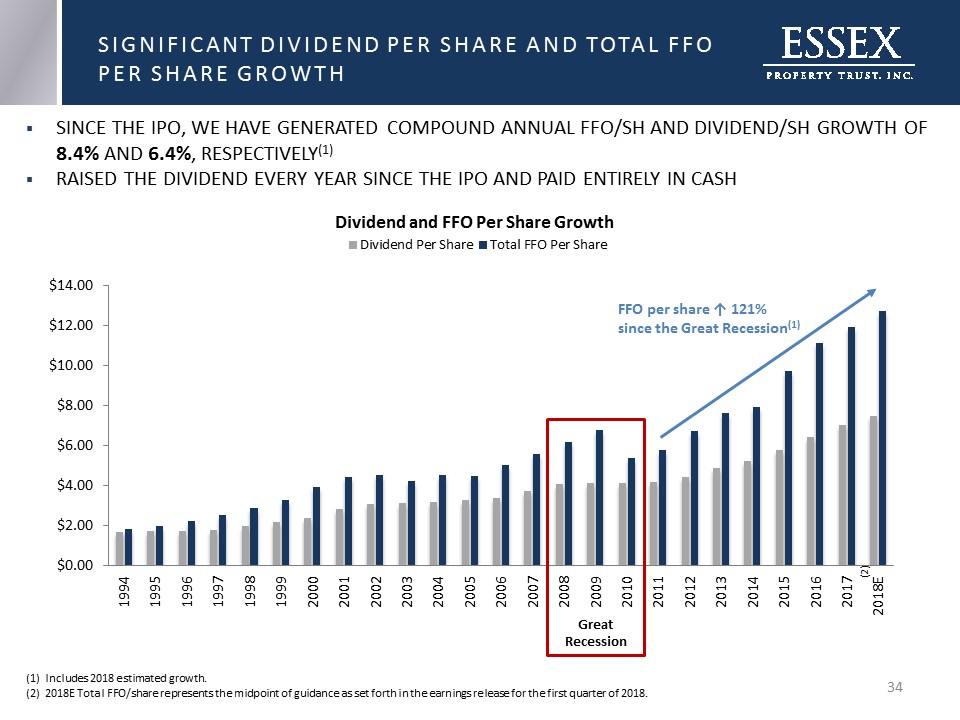

* SINCE THE IPO, WE HAVE GENERATED COMPOUND ANNUAL FFO/SH AND DIVIDEND/SH GROWTH OF 8.4% AND 6.4%, RESPECTIVELY(1)RAISED THE DIVIDEND EVERY YEAR SINCE THE IPO AND PAID ENTIRELY IN CASH SIGNIFICANT DIVIDEND PER SHARE AND TOTAL FFO PER SHARE GROWTH (1) Includes 2018 estimated growth.(2) 2018E Total FFO/share represents the midpoint of guidance as set forth in the earnings release for the first quarter of 2018. (2) Great Recession FFO per share ↑ 121% since the Great Recession(1)

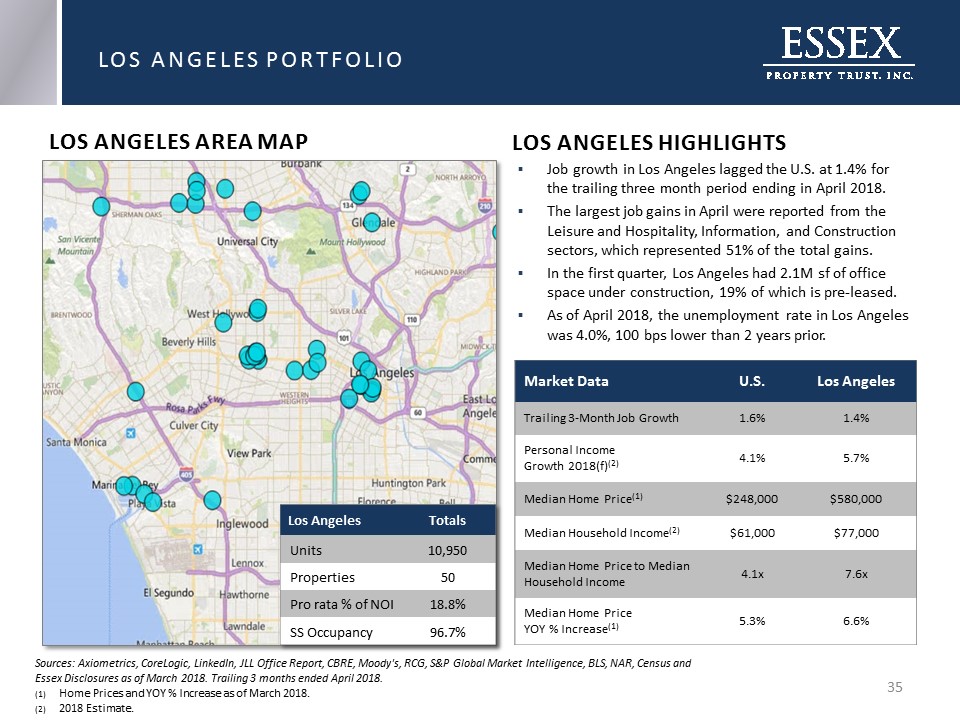

Sources: Axiometrics, CoreLogic, LinkedIn, JLL Office Report, CBRE, Moody's, RCG, S&P Global Market Intelligence, BLS, NAR, Census and Essex Disclosures as of March 2018. Trailing 3 months ended April 2018.Home Prices and YOY % Increase as of March 2018.2018 Estimate. LOS ANGELES PORTFOLIO LOS ANGELES HIGHLIGHTS Job growth in Los Angeles lagged the U.S. at 1.4% for the trailing three month period ending in April 2018.The largest job gains in April were reported from the Leisure and Hospitality, Information, and Construction sectors, which represented 51% of the total gains. In the first quarter, Los Angeles had 2.1M sf of office space under construction, 19% of which is pre-leased.As of April 2018, the unemployment rate in Los Angeles was 4.0%, 100 bps lower than 2 years prior. Market Data U.S. Los Angeles Trailing 3-Month Job Growth 1.6% 1.4% Personal Income Growth 2018(f)(2) 4.1% 5.7% Median Home Price(1) $248,000 $580,000 Median Household Income(2) $61,000 $77,000 Median Home Price to Median Household Income 4.1x 7.6x Median Home Price YOY % Increase(1) 5.3% 6.6% LOS ANGELES AREA MAP *

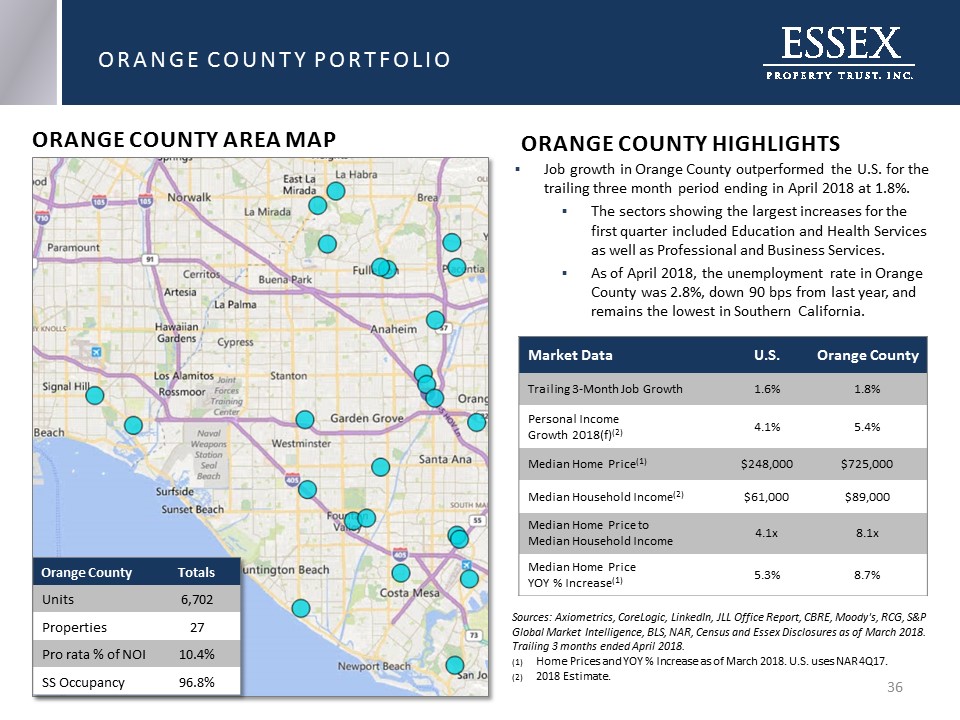

Sources: Axiometrics, CoreLogic, LinkedIn, JLL Office Report, CBRE, Moody's, RCG, S&P Global Market Intelligence, BLS, NAR, Census and Essex Disclosures as of March 2018. Trailing 3 months ended April 2018.Home Prices and YOY % Increase as of March 2018. U.S. uses NAR 4Q17.2018 Estimate. ORANGE COUNTY PORTFOLIO ORANGE COUNTY HIGHLIGHTS Job growth in Orange County outperformed the U.S. for the trailing three month period ending in April 2018 at 1.8%.The sectors showing the largest increases for the first quarter included Education and Health Services as well as Professional and Business Services.As of April 2018, the unemployment rate in Orange County was 2.8%, down 90 bps from last year, and remains the lowest in Southern California. Market Data U.S. Orange County Trailing 3-Month Job Growth 1.6% 1.8% Personal Income Growth 2018(f)(2) 4.1% 5.4% Median Home Price(1) $248,000 $725,000 Median Household Income(2) $61,000 $89,000 Median Home Price to Median Household Income 4.1x 8.1x Median Home Price YOY % Increase(1) 5.3% 8.7% ORANGE COUNTY AREA MAP *

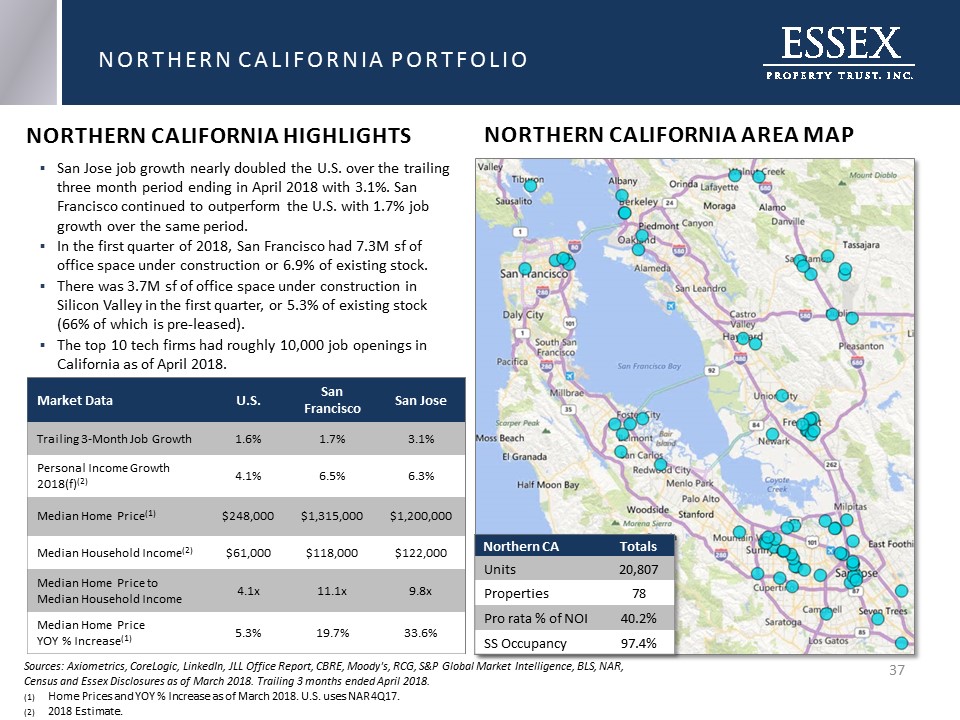

San Jose job growth nearly doubled the U.S. over the trailing three month period ending in April 2018 with 3.1%. San Francisco continued to outperform the U.S. with 1.7% job growth over the same period.In the first quarter of 2018, San Francisco had 7.3M sf of office space under construction or 6.9% of existing stock. There was 3.7M sf of office space under construction in Silicon Valley in the first quarter, or 5.3% of existing stock (66% of which is pre-leased).The top 10 tech firms had roughly 10,000 job openings in California as of April 2018. Sources: Axiometrics, CoreLogic, LinkedIn, JLL Office Report, CBRE, Moody's, RCG, S&P Global Market Intelligence, BLS, NAR, Census and Essex Disclosures as of March 2018. Trailing 3 months ended April 2018.Home Prices and YOY % Increase as of March 2018. U.S. uses NAR 4Q17.2018 Estimate. NORTHERN CALIFORNIA HIGHLIGHTS Market Data U.S. San Francisco San Jose Trailing 3-Month Job Growth 1.6% 1.7% 3.1% Personal Income Growth 2018(f)(2) 4.1% 6.5% 6.3% Median Home Price(1) $248,000 $1,315,000 $1,200,000 Median Household Income(2) $61,000 $118,000 $122,000 Median Home Price toMedian Household Income 4.1x 11.1x 9.8x Median Home Price YOY % Increase(1) 5.3% 19.7% 33.6% NORTHERN CALIFORNIA PORTFOLIO NORTHERN CALIFORNIA AREA MAP *

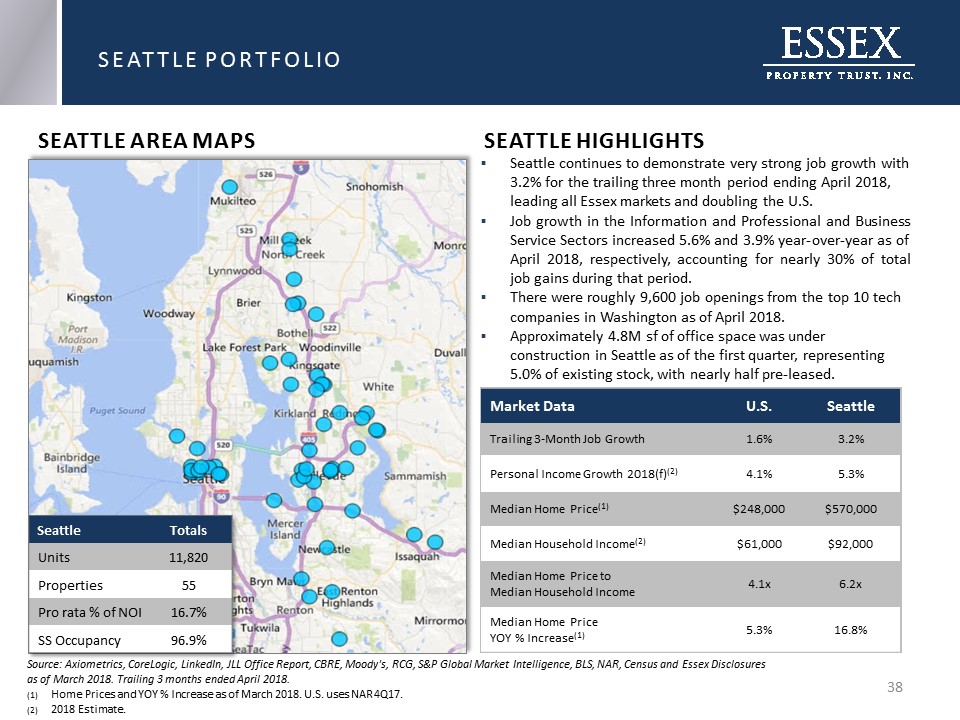

Source: Axiometrics, CoreLogic, LinkedIn, JLL Office Report, CBRE, Moody's, RCG, S&P Global Market Intelligence, BLS, NAR, Census and Essex Disclosures as of March 2018. Trailing 3 months ended April 2018.Home Prices and YOY % Increase as of March 2018. U.S. uses NAR 4Q17.2018 Estimate. SEATTLE HIGHLIGHTS SEATTLE PORTFOLIO Market Data U.S. Seattle Trailing 3-Month Job Growth 1.6% 3.2% Personal Income Growth 2018(f)(2) 4.1% 5.3% Median Home Price(1) $248,000 $570,000 Median Household Income(2) $61,000 $92,000 Median Home Price to Median Household Income 4.1x 6.2x Median Home Price YOY % Increase(1) 5.3% 16.8% Seattle continues to demonstrate very strong job growth with 3.2% for the trailing three month period ending April 2018, leading all Essex markets and doubling the U.S. Job growth in the Information and Professional and Business Service Sectors increased 5.6% and 3.9% year-over-year as of April 2018, respectively, accounting for nearly 30% of total job gains during that period. There were roughly 9,600 job openings from the top 10 tech companies in Washington as of April 2018.Approximately 4.8M sf of office space was under construction in Seattle as of the first quarter, representing 5.0% of existing stock, with nearly half pre-leased. SEATTLE AREA MAPS *

DEFINITIONS & RECONCILIATIONS

* DISCLAIMERS SAFE HARBOR STATEMENT UNDER THE PRIVATE LITIGATION REFORM ACT OF 1995This presentation includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward looking statements are statements which are not historical facts, including statements regarding the Company's expectations, estimates, assumptions, hopes, intentions, beliefs and strategies regarding the future. Words such as “expects,” “assumes,” “anticipates,” “may,” “will,” “intends,” “plans,” “believes,” “seeks,” “estimates,” and variations of such words and similar expressions are intended to identify such forward looking statements. Such forward-looking statements include, among other things, statements regarding the Company’s financial guidance for the full-year 2018, its intent, beliefs or expectations with respect to the timing of completion of current development and redevelopment projects and the stabilization of such projects, the timing of lease-up and occupancy of its apartment communities, the anticipated operating performance of its apartment communities, the total projected costs of development and redevelopment projects, co-investment activities, qualification as a REIT under the Internal Revenue Code, the real estate markets in the geographies in which the Company’s properties are located and in the United States in general, the adequacy of future cash flows to meet anticipated cash needs, its financing activities and the use of proceeds from such activities, the availability of debt and equity financing, general economic conditions including the potential impacts from the economic conditions, trends affecting the Company’s financial condition or results of operations, changes to U.S. tax laws and regulations in general or specifically related to REITs or real estate, changes to laws and regulations in jurisdictions in which communities the Company owns are located, and other information that is not historical information.While the Company’s management believes the assumptions underlying its forward-looking statements are reasonable, such forward-looking statements involve known and unknown risks, uncertainties and other factors, many of which are beyond the Company’s control, which could cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. The Company cannot assure the future results or outcome of the matters described in these statements; rather, these statements merely reflect the Company’s current expectations of the approximate outcomes of the matters discussed. Factors that might cause the Company’s actual results, performance or achievements to differ materially from those expressed or implied by these forward-looking statements include, but are not limited to, the following: the Company may fail to achieve its business objectives; the actual completion of development and redevelopment projects may be subject to delays; the stabilization dates of such projects may be delayed; the Company may abandon or defer development projects for a number of reasons, including changes in local market conditions which make development less desirable, increases in costs of development, increases in the cost of capital or lack of capital availability, resulting in losses; the total projected costs of current development and redevelopment projects may exceed expectations; such development and redevelopment projects may not be completed; development and redevelopment projects and acquisitions may fail to meet expectations; estimates of future income from an acquired property may prove to be inaccurate; occupancy rates and rental demand may be adversely affected by competition and local economic and market conditions; there may be increased interest rates and operating costs; the Company may be unsuccessful in the management of its relationships with its co-investment partners; future cash flows may be inadequate to meet operating requirements and/or may be insufficient to provide for dividend payments in accordance with REIT requirements; there may be a downturn in general economic conditions, the real estate industry, and the markets in which the Company’s communities are located; changes in laws or regulations; the terms of any refinancing may not be as favorable as the terms of existing indebtedness; and those risks, special considerations, and other factors referred to in the Company’s quarterly reports on Form 10-Q, in the Company’s annual report on Form 10-K for the year ended December 31, 2017, and in the Company’s other filings with the Securities and Exchange Commission. All forward-looking statements are made as of the date hereof, the Company assumes no obligation to update or supplement this information for any reason, and therefore, they may not represent the Company’s estimates and assumptions after the date of this presentation.REGULATION G DISCLAIMERThis presentation contains certain non-GAAP financial measures within the meaning of Regulation G of the Securities Exchange Act of 1934. The Company’s definitions and calculations of such measures may differ from those used by other companies and, therefore, may not be comparable. The Company’s definitions of these terms and, if applicable, the reasons for their use and reconciliations to the most directly comparable GAAP measures are included in the Appendix.

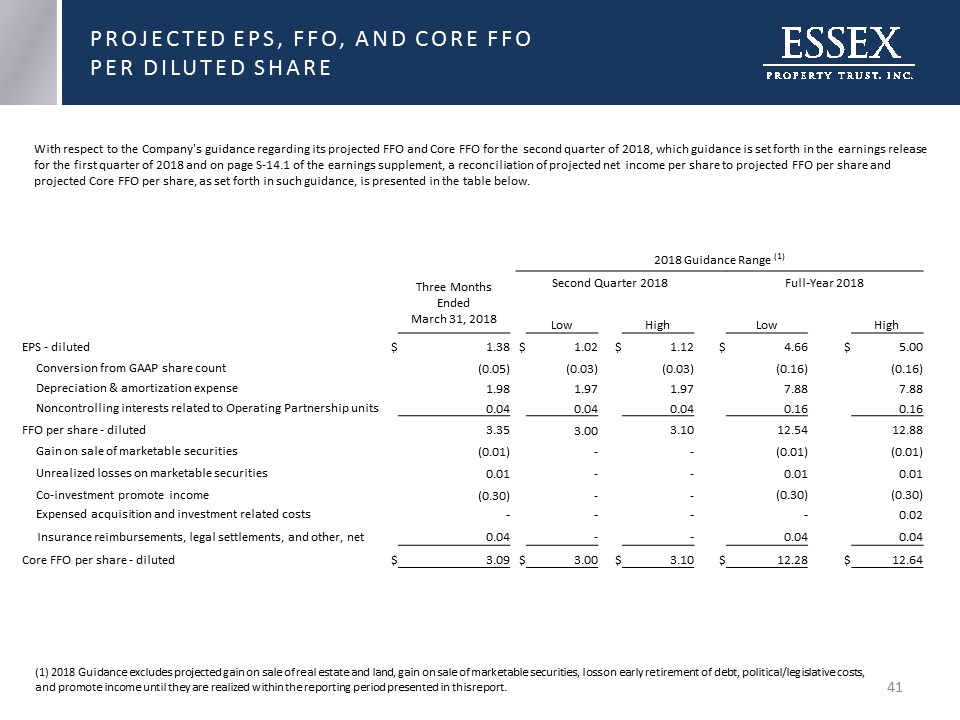

* With respect to the Company's guidance regarding its projected FFO and Core FFO for the second quarter of 2018, which guidance is set forth in the earnings release for the first quarter of 2018 and on page S-14.1 of the earnings supplement, a reconciliation of projected net income per share to projected FFO per share and projected Core FFO per share, as set forth in such guidance, is presented in the table below. 2018 Guidance Range (1) Three Months Ended March 31, 2018 Second Quarter 2018 Full-Year 2018 Low High Low High EPS - diluted $ 1.38 $ 1.02 $ 1.12 $ 4.66 $ 5.00 Conversion from GAAP share count (0.05) (0.03) (0.03) (0.16) (0.16) Depreciation & amortization expense 1.98 1.97 1.97 7.88 7.88 Noncontrolling interests related to Operating Partnership units 0.04 0.04 0.04 0.16 0.16 FFO per share - diluted 3.35 3.00 3.10 12.54 12.88 Gain on sale of marketable securities (0.01) - - (0.01) (0.01) Unrealized losses on marketable securities 0.01 - - 0.01 0.01 Co-investment promote income (0.30) - - (0.30) (0.30) Expensed acquisition and investment related costs - - - - 0.02 Insurance reimbursements, legal settlements, and other, net 0.04 - - 0.04 0.04 Core FFO per share - diluted $ 3.09 $ 3.00 $ 3.10 $ 12.28 $ 12.64 (1) 2018 Guidance excludes projected gain on sale of real estate and land, gain on sale of marketable securities, loss on early retirement of debt, political/legislative costs, and promote income until they are realized within the reporting period presented in this report. PROJECTED EPS, FFO, AND CORE FFOPER DILUTED SHARE

* RECONCILIATIONS OF NON-GAAP FINANCIALMEASURES AND OTHER TERMS ADJUSTED EBITDAre RECONCILIATION The National Association of Real Estate Investment Trusts ("NAREIT”) defines earnings before interest, taxes, depreciation and amortization for real estate ("EBITDAre") (September 2017 White Paper) as net income (computed in accordance with U.S. generally accepted accounting principles ("U.S. GAAP")) before interest expense, income taxes, depreciation and amortization expense, and further adjusted for gains and losses from sales of depreciated operating properties, impairment write-downs of depreciated operating properties, impairment write-downs of investments in unconsolidated entities caused by a decrease in value of depreciated operating properties within the joint venture and adjustments to reflect the Company’s share of EBITDAre of investments in unconsolidated entities. The Company believes that EBITDAre is useful to investors, creditors and rating agencies as a supplemental measure of the Company’s ability to incur and service debt because it is a recognized measure of performance by the real estate industry, and by excluding gains or losses related to sales or impairment of depreciated operating properties, EBITDAre can help compare the Company’s credit strength between periods or as compared to different companies. Adjusted EBITDAre represents EBITDAre further adjusted for non-comparable items and is a component of the credit ratio, "Net Indebtedness Divided by Adjusted EBITDAre," presented on page S-6 of the earnings supplement for the first quarter of 2018, in the section titled "Selected Credit Ratios," and it is not intended to be a measure of free cash flow for our management’s discretionary use, as it does not consider certain cash requirements such as income tax payments, debt service requirements, capital expenditures and other fixed charges. Adjusted EBITDAre is an important metric in evaluating the credit strength of the Company and its ability to service its debt obligations. The Company believes that Adjusted EBITDAre is useful to investors, creditors and rating agencies because it allows investors to compare the Company’s credit strength to prior reporting periods and to other companies without the effect of items that by their nature are not comparable from period to period and tend to obscure the Company’s actual credit quality. EBITDAre and Adjusted EBITDAre are not recognized measurements under U.S. GAAP. Because not all companies use identical calculations, our presentation of EBITDAre and Adjusted EBITDAre may not be comparable to similarly titled measures of other companies.

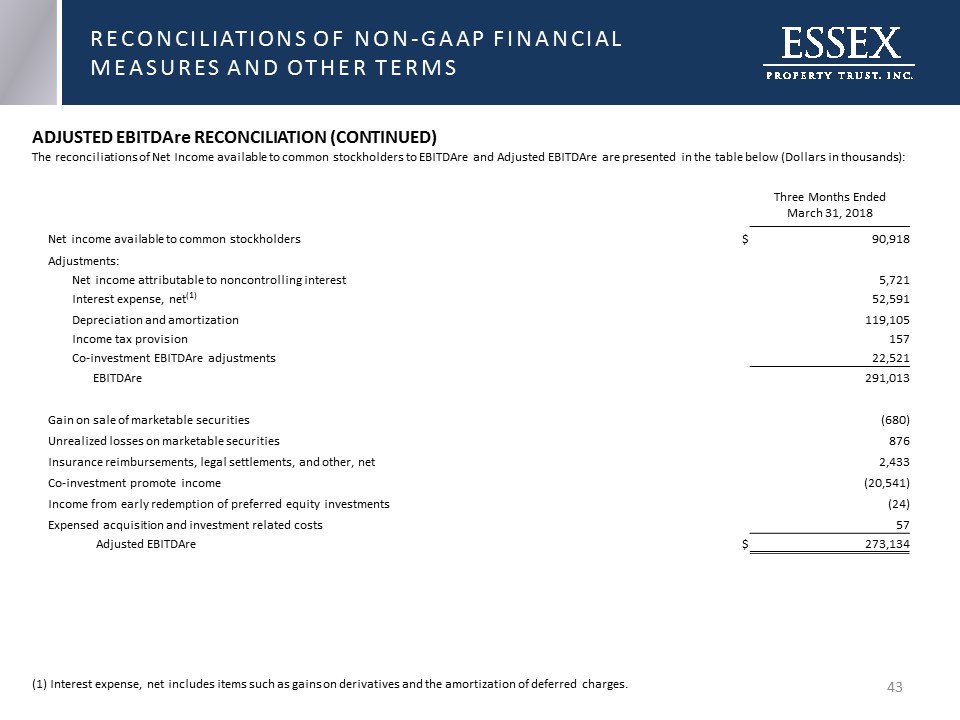

* RECONCILIATIONS OF NON-GAAP FINANCIALMEASURES AND OTHER TERMS ADJUSTED EBITDAre RECONCILIATION (CONTINUED)The reconciliations of Net Income available to common stockholders to EBITDAre and Adjusted EBITDAre are presented in the table below (Dollars in thousands): (1) Interest expense, net includes items such as gains on derivatives and the amortization of deferred charges. Three Months EndedMarch 31, 2018 Net income available to common stockholders $ 90,918 Adjustments: Net income attributable to noncontrolling interest 5,721 Interest expense, net(1) 52,591 Depreciation and amortization 119,105 Income tax provision 157 Co-investment EBITDAre adjustments 22,521 EBITDAre 291,013 Gain on sale of marketable securities (680) Unrealized losses on marketable securities 876 Insurance reimbursements, legal settlements, and other, net 2,433 Co-investment promote income (20,541) Income from early redemption of preferred equity investments (24) Expensed acquisition and investment related costs 57 Adjusted EBITDAre $ 273,134

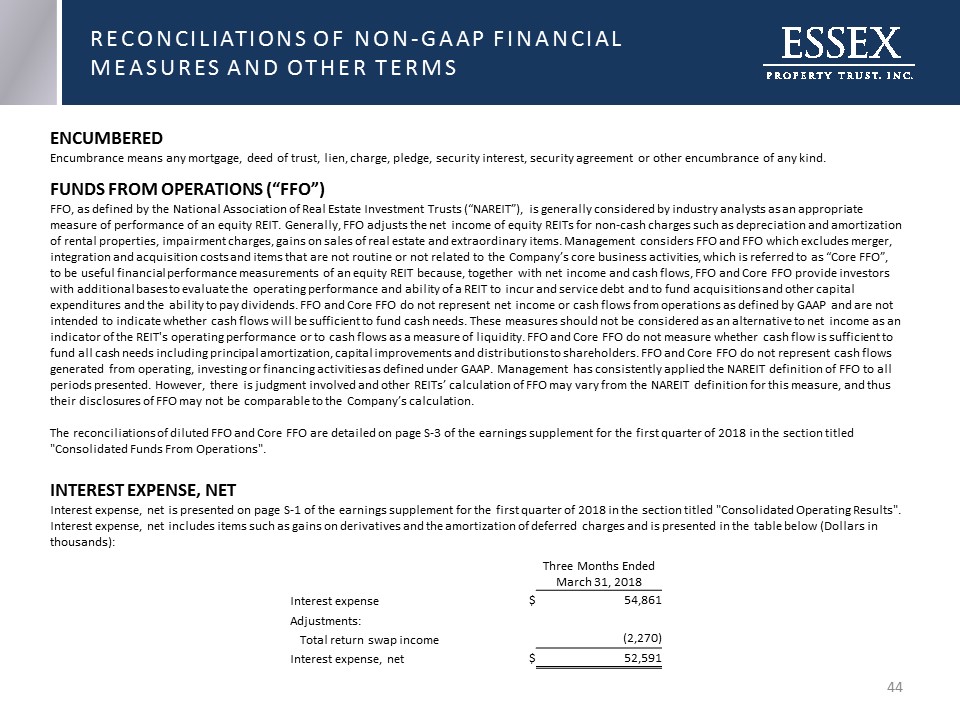

* RECONCILIATIONS OF NON-GAAP FINANCIALMEASURES AND OTHER TERMS FUNDS FROM OPERATIONS (“FFO”) FFO, as defined by the National Association of Real Estate Investment Trusts (“NAREIT”), is generally considered by industry analysts as an appropriate measure of performance of an equity REIT. Generally, FFO adjusts the net income of equity REITs for non-cash charges such as depreciation and amortization of rental properties, impairment charges, gains on sales of real estate and extraordinary items. Management considers FFO and FFO which excludes merger, integration and acquisition costs and items that are not routine or not related to the Company’s core business activities, which is referred to as “Core FFO”, to be useful financial performance measurements of an equity REIT because, together with net income and cash flows, FFO and Core FFO provide investors with additional bases to evaluate the operating performance and ability of a REIT to incur and service debt and to fund acquisitions and other capital expenditures and the ability to pay dividends. FFO and Core FFO do not represent net income or cash flows from operations as defined by GAAP and are not intended to indicate whether cash flows will be sufficient to fund cash needs. These measures should not be considered as an alternative to net income as an indicator of the REIT's operating performance or to cash flows as a measure of liquidity. FFO and Core FFO do not measure whether cash flow is sufficient to fund all cash needs including principal amortization, capital improvements and distributions to shareholders. FFO and Core FFO do not represent cash flows generated from operating, investing or financing activities as defined under GAAP. Management has consistently applied the NAREIT definition of FFO to all periods presented. However, there is judgment involved and other REITs’ calculation of FFO may vary from the NAREIT definition for this measure, and thus their disclosures of FFO may not be comparable to the Company’s calculation. The reconciliations of diluted FFO and Core FFO are detailed on page S-3 of the earnings supplement for the first quarter of 2018 in the section titled "Consolidated Funds From Operations".INTEREST EXPENSE, NETInterest expense, net is presented on page S-1 of the earnings supplement for the first quarter of 2018 in the section titled "Consolidated Operating Results". Interest expense, net includes items such as gains on derivatives and the amortization of deferred charges and is presented in the table below (Dollars in thousands): Three Months EndedMarch 31, 2018 Interest expense $ 54,861 Adjustments: Total return swap income (2,270) Interest expense, net $ 52,591 ENCUMBEREDEncumbrance means any mortgage, deed of trust, lien, charge, pledge, security interest, security agreement or other encumbrance of any kind.

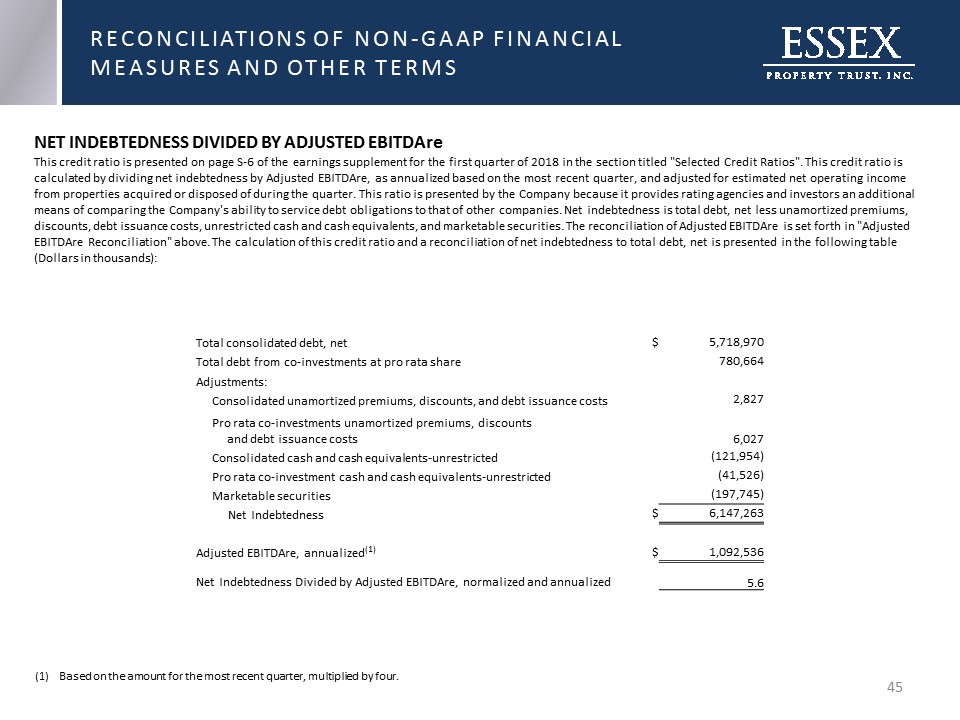

* RECONCILIATIONS OF NON-GAAP FINANCIALMEASURES AND OTHER TERMS Total consolidated debt, net $ 5,718,970 Total debt from co-investments at pro rata share 780,664 Adjustments: Consolidated unamortized premiums, discounts, and debt issuance costs 2,827 Pro rata co-investments unamortized premiums, discounts and debt issuance costs 6,027 Consolidated cash and cash equivalents-unrestricted (121,954) Pro rata co-investment cash and cash equivalents-unrestricted (41,526) Marketable securities (197,745) Net Indebtedness $ 6,147,263 Adjusted EBITDAre, annualized(1) $ 1,092,536 Net Indebtedness Divided by Adjusted EBITDAre, normalized and annualized 5.6 NET INDEBTEDNESS DIVIDED BY ADJUSTED EBITDAreThis credit ratio is presented on page S-6 of the earnings supplement for the first quarter of 2018 in the section titled "Selected Credit Ratios". This credit ratio is calculated by dividing net indebtedness by Adjusted EBITDAre, as annualized based on the most recent quarter, and adjusted for estimated net operating income from properties acquired or disposed of during the quarter. This ratio is presented by the Company because it provides rating agencies and investors an additional means of comparing the Company's ability to service debt obligations to that of other companies. Net indebtedness is total debt, net less unamortized premiums, discounts, debt issuance costs, unrestricted cash and cash equivalents, and marketable securities. The reconciliation of Adjusted EBITDAre is set forth in "Adjusted EBITDAre Reconciliation" above. The calculation of this credit ratio and a reconciliation of net indebtedness to total debt, net is presented in the following table (Dollars in thousands): Based on the amount for the most recent quarter, multiplied by four.

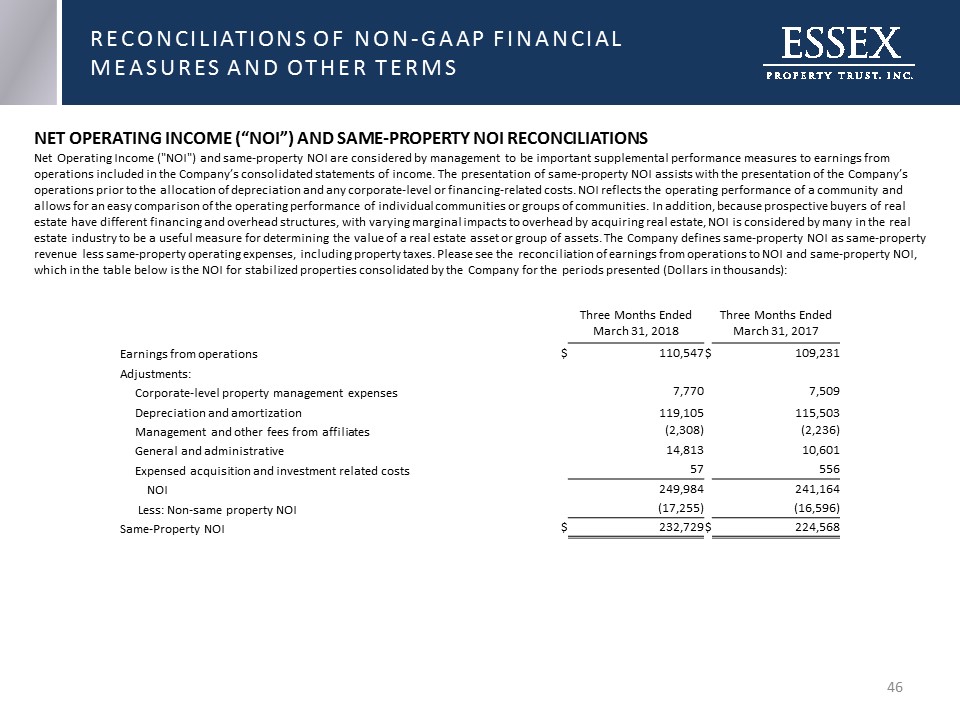

* NET OPERATING INCOME (“NOI”) AND SAME-PROPERTY NOI RECONCILIATIONSNet Operating Income ("NOI") and same-property NOI are considered by management to be important supplemental performance measures to earnings from operations included in the Company’s consolidated statements of income. The presentation of same-property NOI assists with the presentation of the Company’s operations prior to the allocation of depreciation and any corporate-level or financing-related costs. NOI reflects the operating performance of a community and allows for an easy comparison of the operating performance of individual communities or groups of communities. In addition, because prospective buyers of real estate have different financing and overhead structures, with varying marginal impacts to overhead by acquiring real estate, NOI is considered by many in the real estate industry to be a useful measure for determining the value of a real estate asset or group of assets. The Company defines same-property NOI as same-property revenue less same-property operating expenses, including property taxes. Please see the reconciliation of earnings from operations to NOI and same-property NOI, which in the table below is the NOI for stabilized properties consolidated by the Company for the periods presented (Dollars in thousands): RECONCILIATIONS OF NON-GAAP FINANCIALMEASURES AND OTHER TERMS Three Months EndedMarch 31, 2018 Three Months EndedMarch 31, 2017 Earnings from operations $ 110,547 $ 109,231 Adjustments: Corporate-level property management expenses 7,770 7,509 Depreciation and amortization 119,105 115,503 Management and other fees from affiliates (2,308) (2,236) General and administrative 14,813 10,601 Expensed acquisition and investment related costs 57 556 NOI 249,984 241,164 Less: Non-same property NOI (17,255) (16,596) Same-Property NOI $ 232,729 $ 224,568

* PUBLIC BOND COVENANTSPublic Bond Covenants refers to certain covenants set forth in instruments governing the Company's unsecured indebtedness. These instruments require the Company to meet specified financial covenants, including covenants relating to net worth, fixed charge coverage, debt service coverage, the amounts of total indebtedness and secured indebtedness, leverage and certain investment limitations. These covenants may restrict the Company's ability to expand or fully pursue its business strategies. The Company's ability to comply with these covenants may be affected by changes in the Company's operating and financial performance, changes in general business and economic conditions, adverse regulatory developments or other events adversely impacting it. The breach of any of these covenants could result in a default under the Company's indebtedness, which could cause those and other obligations to become due and payable. If any of the Company's indebtedness is accelerated, it may not be able to repay it. For risks related to failure to comply with these covenants, see "Item 1A: Risk Factors - Risks Related to Our Indebtedness and Financing" in the Company's annual report on Form 10-K and other reports filed by the Company with the SEC.The ratios set forth on page S-6 of the earnings supplement for the first quarter of 2018 in the section titled "Public Bond Covenants" are provided only to show the Company's compliance with certain specified covenants that are contained in indentures related to the Company's issuance of Senior Notes, which indentures are filed by the Company with the SEC. See, for example, the Indenture dated March 8, 2018, filed by the Company as Exhibit 4.1 to the Company's Form 8-K, filed on March 8, 2018. These ratios should not be used for any other purpose, including without limitation to evaluate the Company's financial condition or results of operations, nor do they indicate the Company's covenant compliance as of any other date or for any other period. The capitalized terms in the disclosure are defined in the indentures filed by the Company with the SEC and may differ materially from similar terms used by other companies that present information about their covenant compliance.SECURED DEBTSecured Debt means debt of the Company or any of its subsidiaries which is secured by an encumbrance on any property or assets of the Company or any of its subsidiaries. The Company’s total amount of Secured Debt is set forth on page S-5 of the earnings supplement for the first quarter of 2018. RECONCILIATIONS OF NON-GAAP FINANCIALMEASURES AND OTHER TERMS

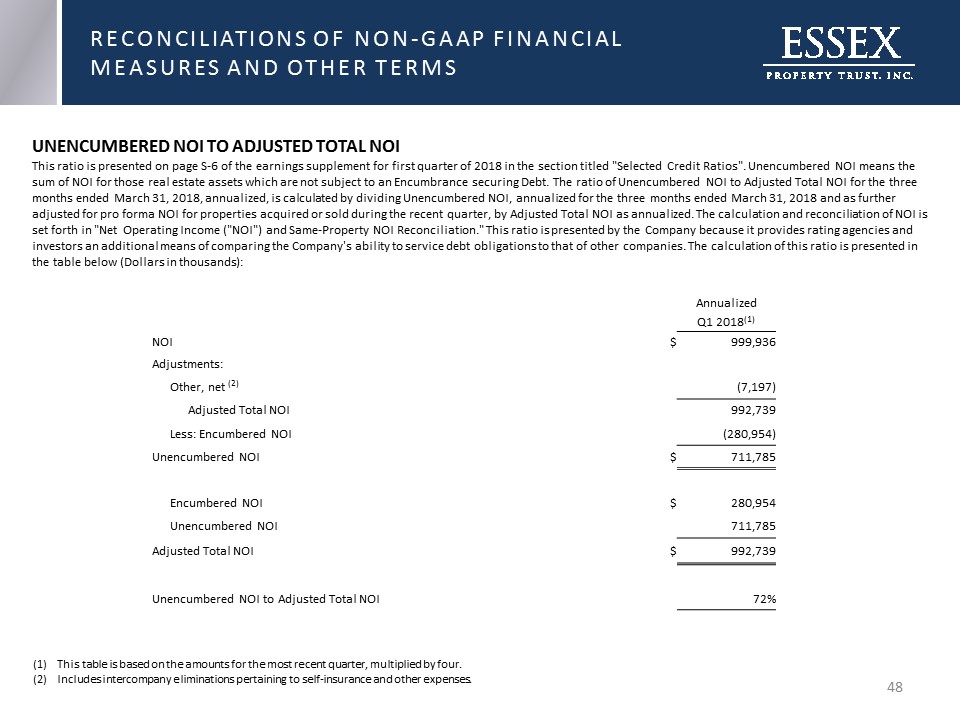

* RECONCILIATIONS OF NON-GAAP FINANCIALMEASURES AND OTHER TERMS UNENCUMBERED NOI TO ADJUSTED TOTAL NOIThis ratio is presented on page S-6 of the earnings supplement for first quarter of 2018 in the section titled "Selected Credit Ratios". Unencumbered NOI means the sum of NOI for those real estate assets which are not subject to an Encumbrance securing Debt. The ratio of Unencumbered NOI to Adjusted Total NOI for the three months ended March 31, 2018, annualized, is calculated by dividing Unencumbered NOI, annualized for the three months ended March 31, 2018 and as further adjusted for pro forma NOI for properties acquired or sold during the recent quarter, by Adjusted Total NOI as annualized. The calculation and reconciliation of NOI is set forth in "Net Operating Income ("NOI") and Same-Property NOI Reconciliation." This ratio is presented by the Company because it provides rating agencies and investors an additional means of comparing the Company's ability to service debt obligations to that of other companies. The calculation of this ratio is presented in the table below (Dollars in thousands): Annualized Q1 2018(1) NOI $ 999,936 Adjustments: Other, net (2) (7,197) Adjusted Total NOI 992,739 Less: Encumbered NOI (280,954) Unencumbered NOI $ 711,785 Encumbered NOI $ 280,954 Unencumbered NOI 711,785 Adjusted Total NOI $ 992,739 Unencumbered NOI to Adjusted Total NOI 72% This table is based on the amounts for the most recent quarter, multiplied by four.Includes intercompany eliminations pertaining to self-insurance and other expenses.

NOTES