Attached files

| file | filename |

|---|---|

| EX-32 - EX-32 - READING INTERNATIONAL INC | rdi-20180331xex32.htm |

| EX-31.2 - EX-31.2 - READING INTERNATIONAL INC | rdi-20180331xex31_2.htm |

| EX-31.1 - EX-31.1 - READING INTERNATIONAL INC | rdi-20180331xex31_1.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________

FORM 10-Q

(Mark One)

|

|

|

|

☑ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended: March 31, 2018

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission file number 1-8625

READING INTERNATIONAL, INC.

(Exact name of Registrant as specified in its charter)

|

NEVADA (State or other jurisdiction of incorporation or organization) |

95-3885184 (IRS Employer Identification No.) |

|

5995 Sepulveda Boulevard, Suite 300 Culver City, CA (Address of principal executive offices) |

90230 (Zip Code) |

Registrant’s telephone number, including area code: (213) 235-2240

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding twelve months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

(Check one): Large accelerated filer ☐ Accelerated filer ☑ Non-accelerated filer ☐ Smaller reporting company ☐

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. As of May 10, 2018, there were 21,296,438 shares of Class A Nonvoting Common Stock, $0.01 par value per share and 1,680,590 shares of Class B Voting Common Stock, $0.01 par value per share outstanding.

1

READING INTERNATIONAL, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

|

|

Page |

|

3 |

|

|

3 |

|

|

3 |

|

|

4 |

|

|

Consolidated Statements of Comprehensive Income (Unaudited) |

5 |

|

6 |

|

|

7 |

|

|

Item 2 – Management’s Discussion and Analysis of Financial Condition and Results of Operations |

28 |

|

Item 3 – Quantitative and Qualitative Disclosure about Market Risk |

44 |

|

45 |

|

|

46 |

|

|

46 |

|

|

46 |

|

|

Item 2 - Unregistered Sales of Equity Securities and Use of Proceeds |

46 |

|

46 |

|

| 47 | |

| 47 | |

|

48 |

|

|

Certifications |

|

2

PART 1 – FINANCIAL INFORMATION

READING INTERNATIONAL, INC.

CONSOLIDATED BALANCE SHEETS

(Unaudited; U.S. dollars in thousands, except share information)

|

|

||||

|

|

||||

|

|

March 31, |

December 31, |

||

|

|

2018 |

2017 |

||

|

ASSETS |

(unaudited) |

|||

|

Current Assets: |

||||

|

Cash and cash equivalents |

$ |

8,668 |

$ |

13,668 |

|

Receivables |

8,922 | 13,050 | ||

|

Inventory |

1,342 | 1,432 | ||

|

Prepaid and other current assets |

6,713 | 5,325 | ||

|

Total current assets |

25,645 | 33,475 | ||

|

Operating property, net |

269,578 | 264,724 | ||

|

Investment and development property, net |

66,944 | 61,254 | ||

|

Investment in unconsolidated joint ventures |

5,283 | 5,304 | ||

|

Goodwill |

20,383 | 20,276 | ||

|

Intangible assets, net |

8,227 | 8,542 | ||

|

Deferred tax asset, net |

24,834 | 24,908 | ||

|

Other assets |

5,661 | 4,543 | ||

|

Total assets |

$ |

426,555 |

$ |

423,026 |

|

LIABILITIES AND STOCKHOLDERS' EQUITY |

||||

|

Current Liabilities: |

||||

|

Accounts payable and accrued liabilities |

$ |

27,101 |

$ |

34,359 |

|

Film rent payable |

7,708 | 13,511 | ||

|

Debt – current portion |

10,544 | 8,109 | ||

|

Taxes payable – current |

3,031 | 2,938 | ||

|

Deferred current revenue |

8,276 | 9,850 | ||

|

Other current liabilities |

9,515 | 11,679 | ||

|

Total current liabilities |

66,175 | 80,446 | ||

|

Debt – long-term portion |

108,322 | 94,862 | ||

|

Subordinated debt, net |

27,564 | 27,554 | ||

|

Noncurrent tax liabilities |

12,186 | 12,274 | ||

|

Other liabilities |

28,553 | 26,649 | ||

|

Total liabilities |

242,800 | 241,785 | ||

|

Commitments and contingencies (Note 13) |

||||

|

Stockholders’ equity: |

||||

|

Class A non-voting common stock, par value $0.01, 100,000,000 shares authorized, |

||||

|

33,082,295 issued and 21,295,031 outstanding at March 31, 2018, and |

|

232 |

|

231 |

|

Class B voting common stock, par value $0.01, 20,000,000 shares authorized and |

||||

|

1,680,590 issued and outstanding at March 31, 2018 and December 31, 2017 |

17 | 17 | ||

|

Nonvoting preferred stock, par value $0.01, 12,000 shares authorized and no issued |

||||

|

or outstanding shares at March 31, 2018 and December 31, 2017 |

-- |

-- |

||

|

Additional paid-in capital |

146,236 | 145,898 | ||

|

Retained earnings |

35,920 | 32,679 | ||

|

Treasury shares |

(23,223) | (22,906) | ||

|

Accumulated other comprehensive income |

20,241 | 20,991 | ||

|

Total Reading International, Inc. stockholders’ equity |

179,423 | 176,910 | ||

|

Noncontrolling interests |

4,332 | 4,331 | ||

|

Total stockholders’ equity |

183,755 | 181,241 | ||

|

Total liabilities and stockholders’ equity |

$ |

426,555 |

$ |

423,026 |

See accompanying Notes to the Unaudited Consolidated Financial Statements.

3

CONSOLIDATED STATEMENTS OF INCOME

(Unaudited; U.S. dollars in thousands, except per share data)

|

|

||||

|

|

Three Months Ended |

|||

|

|

March 31, |

March 31, |

||

|

|

2018 |

2017(1) |

||

|

Revenue |

|

|

|

|

|

Cinema |

$ |

72,255 |

$ |

66,560 |

|

Real estate |

|

3,567 |

|

2,894 |

|

Total revenue |

|

75,822 |

|

69,454 |

|

Costs and expenses |

|

|

|

|

|

Cinema |

|

(54,948) |

|

(51,782) |

|

Real estate |

|

(2,384) |

|

(2,036) |

|

Depreciation and amortization |

|

(5,250) |

|

(3,934) |

|

General and administrative |

|

(7,597) |

|

(6,174) |

|

Total costs and expenses |

|

(70,179) |

|

(63,926) |

|

Operating income |

|

5,643 |

|

5,528 |

|

Interest expense, net |

|

(1,594) |

|

(1,860) |

|

Other income (expense) |

|

(82) |

|

821 |

|

Income before income tax expense and equity earnings of unconsolidated joint ventures |

|

3,967 |

|

4,489 |

|

Equity earnings of unconsolidated joint ventures |

|

257 |

|

255 |

|

Income before income taxes |

|

4,224 |

|

4,744 |

|

Income tax expense |

|

(1,155) |

|

(1,703) |

|

Net income |

$ |

3,069 |

$ |

3,041 |

|

Less: net income (loss) attributable to noncontrolling interests |

|

22 |

|

12 |

|

Net income attributable to Reading International, Inc. common shareholders |

$ |

3,047 |

$ |

3,029 |

|

Basic earnings per share attributable to Reading International, Inc. shareholders |

$ |

0.13 |

$ |

0.13 |

|

Diluted earnings per share attributable to Reading International, Inc. shareholders |

$ |

0.13 |

$ |

0.13 |

|

Weighted average number of shares outstanding–basic |

|

22,967,237 |

|

23,168,351 |

|

Weighted average number of shares outstanding–diluted |

|

23,132,989 |

|

23,465,176 |

See accompanying Notes to the Unaudited Consolidated Financial Statements.

(1) Certain prior year balances have been reclassified to conform to the 2018 presentation (see Note 2 – Summary of Significant Accounting Policies – Reclassifications).

4

READING INTERNATIONAL, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited; U.S. dollars in thousands)

|

|

|||||

|

|

Three Months Ended |

||||

|

|

March 31, |

March 31, |

|||

|

|

2018 |

2017(1) |

|||

|

Net income |

$ |

3,069 |

$ |

3,041 | |

|

Foreign currency translation (loss) gain |

(803) | 5,826 | |||

|

Other |

50 | 48 | |||

|

Comprehensive income |

2,316 | 8,915 | |||

|

Less: net income attributable to noncontrolling interests |

22 | 12 | |||

|

Less: comprehensive (loss) income attributable to noncontrolling interests |

(3) | 13 | |||

|

Comprehensive income attributable to Reading International, Inc. |

$ |

2,297 |

$ |

8,890 | |

See accompanying Notes to the Unaudited Consolidated Financial Statements.

(1) Certain prior year balances have been reclassified to conform to the 2018 presentation (see Note 2 – Summary of Significant Accounting Policies – Reclassifications).

5

READING INTERNATIONAL, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited; U.S. dollars in thousands)

|

|

|||||

|

|

Three Months Ended |

||||

|

|

March 31, |

March 31, |

|||

|

|

2018 |

2017 |

|||

|

Operating Activities |

|||||

|

Net income |

$ |

3,069 |

$ |

3,041 | |

|

Adjustments to reconcile net income to net cash provided by operating activities: |

|||||

|

Equity earnings of unconsolidated joint ventures |

(257) | (255) | |||

|

Distributions of earnings from unconsolidated joint ventures |

236 | 220 | |||

|

Gain recognized on foreign currency transactions |

-- |

(825) | |||

|

Change in net deferred tax assets |

157 | 577 | |||

|

Depreciation and amortization |

5,250 | 3,934 | |||

|

Other amortization |

224 | 532 | |||

|

Stock based compensation expense |

379 | 166 | |||

|

Net changes in operating assets and liabilities: |

|||||

|

Receivables |

3,205 | 2,215 | |||

|

Prepaid and other assets |

(2,259) | (1,504) | |||

|

Payments for accrued pension |

(2,404) |

-- |

|||

|

Accounts payable and accrued expenses |

1,997 | (5,426) | |||

|

Film rent payable |

(5,790) | (1,710) | |||

|

Taxes payable |

150 | 44 | |||

|

Deferred revenue and other liabilities |

(1,505) | (698) | |||

|

Net cash provided by operating activities |

2,452 | 311 | |||

|

Investing Activities |

|||||

|

Demolition costs of operating property |

-- |

(2,458) | |||

|

Purchases of and additions to operating and investment properties |

(23,231) | (8,478) | |||

|

Change in restricted cash |

(260) | 12 | |||

|

Net cash used in investing activities |

(23,491) | (10,924) | |||

|

Financing Activities |

|||||

|

Repayment of long-term borrowings |

(9,707) | (12,875) | |||

|

Proceeds from borrowings |

25,998 | 16,119 | |||

|

Repurchase of Class A Nonvoting Common Stock |

(317) | (671) | |||

|

Proceeds from the exercise of stock options |

203 | 3 | |||

|

Noncontrolling interest contributions |

27 | 41 | |||

|

Noncontrolling interest distributions |

(43) | (77) | |||

|

Net cash provided by financing activities |

16,161 | 2,540 | |||

|

Effect of exchange rate changes on cash and cash equivalents |

(122) | 87 | |||

|

Net decrease in cash and cash equivalents |

(5,000) | (7,986) | |||

|

Cash and cash equivalents at January 1 |

13,668 | 19,017 | |||

|

Cash and cash equivalents at March 31 |

$ |

8,668 |

$ |

11,031 | |

|

Supplemental Disclosures |

|||||

|

Interest paid |

$ |

2,121 |

$ |

1,658 | |

|

Income taxes paid |

808 | 1,408 | |||

|

Non-Cash Transactions |

|||||

|

Additions to operating and investing properties through accrued expenses |

4,530 |

-- |

|||

See accompanying Notes to the Unaudited Consolidated Financial Statements.

6

READING INTERNATIONAL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

Note 1 – Description of Business and Segment Reporting

The Company

Reading International, Inc., a Nevada corporation (“RDI” and collectively with our consolidated subsidiaries and corporate predecessors, the “Company,” “Reading” and “we,” “us,” or “our”), was incorporated in 1999. Our businesses consist primarily of:

|

· |

the development, lease or ownership, and operation of multiplex cinemas in the United States, Australia, and New Zealand; and, |

|

· |

the development, ownership, and operation of retail and commercial real estate in Australia, New Zealand, and the United States. |

Business Segments

Reported below are the operating segments of the Company for which separate financial information is available and evaluated regularly by the Chief Executive Officer, the chief operating decision-maker of the Company. As part of our real estate activities, we hold undeveloped land in urban and suburban centers in New Zealand and the United States.

The table below summarizes the results of operations for each of our business segments for the quarter ended March 31, 2018 and 2017, respectively. Operating expense includes costs associated with the day-to-day operations of the cinemas and the management of rental properties, including our live theater assets.

|

|

Three Months Ended |

|||||

|

(Dollars in thousands) |

|

March 31, 2018 |

|

March 31, 2017 |

||

|

Revenue: |

||||||

|

Cinema exhibition |

$ |

72,255 |

$ |

66,560 | ||

|

Real estate |

5,958 | 4,497 | ||||

|

Inter-segment elimination |

(2,391) | (1,603) | ||||

|

|

$ |

75,822 |

$ |

69,454 | ||

|

Segment operating income: |

||||||

|

Cinema exhibition |

$ |

10,285 |

$ |

9,093 | ||

|

Real estate |

1,631 | 1,294 | ||||

|

|

$ |

11,916 |

$ |

10,387 | ||

A reconciliation of segment operating income to income before income taxes is as follows:

|

|

Three Months Ended |

|||||

|

(Dollars in thousands) |

March 31, 2018 |

March 31, 2017 |

||||

|

Segment operating income |

$ |

11,916 |

$ |

10,387 | ||

|

Unallocated corporate expense |

||||||

|

Depreciation and amortization expense |

(117) | (106) | ||||

|

General and administrative expense |

(6,156) | (4,753) | ||||

|

Interest expense, net |

(1,594) | (1,860) | ||||

|

Equity earnings of unconsolidated joint ventures |

257 | 255 | ||||

|

Other income (expense) |

(82) | 821 | ||||

|

Income before income tax expense |

$ |

4,224 |

$ |

4,744 | ||

Note 2 – Summary of Significant Accounting Policies

Basis of Consolidation

The accompanying consolidated financial statements include the accounts of the Company’s wholly-owned subsidiaries as well as majority-owned subsidiaries that the Company controls, and should be read in conjunction with the Company’s Annual Report on Form 10-K as of and for the year-ended December 31, 2017 (“2017 Form 10-K”). All significant intercompany balances and transactions have been eliminated on consolidation. These consolidated financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim reporting with the instructions for Form 10-Q and Rule 10-01 of Regulation S-X of the Securities and Exchange Commission (“SEC”). As such, they do not include all information and footnotes required by U.S. GAAP for complete financial statements. We believe that we have included all normal and recurring adjustments necessary for a fair presentation of the results for the interim period. Operating results for the quarter ended March 31, 2018 are not necessarily indicative of the results that may be expected for the year ending December 31, 2018.

7

Use of Estimates

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and footnotes thereto. Significant estimates include (i) projections we make regarding the recoverability and impairment of our assets (including goodwill and intangibles), (ii) valuations of our derivative instruments, (iii) recoverability of our deferred tax assets, (iv) estimation of breakage and redemption experience rates, which drive how we recognize breakage on our gift card and gift certificates, and revenue from our customer loyalty program, and (v) allocation of insurance proceeds to various recoverable components. Actual results may differ from those estimates.

Reclassifications

Certain reclassifications have been made in the March 31, 2017 comparative information in our consolidated financial statements and accompanying notes to conform to the 2018 presentation. These reclassifications relate to the following immaterial balances:

|

(i) |

net-off of interest income against interest expense in our consolidated statements of income; and, |

|

(ii) |

combination of certain components in our consolidated statements of comprehensive income into one line, “Others”. |

Recently Adopted and Issued Accounting Pronouncements

Adopted:

ASU 2014-09 Revenue from Contracts with Customers: On 1 January 2018, we adopted the new accounting standard ASC 606 Revenue from Contracts with Customers using the modified retrospective method. We recognized the cumulative effect of initially applying the new revenue standard as an adjustment to the opening balance of retained earnings. The comparative information has not been restated and continues to be reported under the accounting standards in effect for those periods. We expect the impact of the adoption of the new standard to be immaterial to our net income and cash flows from operations on an ongoing basis.

Our cinema and food and beverage revenue continues to be recognized upon sale and completion of the provision of the movie or performance, or delivery of food and beverage items. Where necessary, revenue is deferred until these obligations are discharged. Property rentals continue to be recognized on a straight line basis, and live theatre license fees continue to be based on a percentage of weekly ticket sales. Under the new standard, rewards owed to and points accrued by Members of our customer loyalty programs are held as deferred revenue. Revenue from unredeemed gift cards and certificates (known as “breakage” in our industry) is recognized in proportion to the pattern of rights exercised by the customer, when the Company expects that it is probable that a significant revenue reversal would not occur for any estimated breakage amounts.

The cumulative effect of the changes made to our consolidated January 1, 2018 balance sheet for the adoption of ASU 2014-09 Revenue from Contracts with Customers were as follows:

|

|

|

|

|

|

|

|

|

(Dollars in thousands) |

|

Balance at December 31, 2017 |

|

Adjustments due to ASU 2014-09 |

|

Balance at January 1, 2018 |

|

Assets |

|

|

|

|

|

|

|

Deferred income taxes |

|

24,908 |

|

(161) |

|

24,747 |

|

Liabilities |

|

|

|

|

|

|

|

Deferred current revenue |

|

9,850 |

|

(354) |

|

9,496 |

|

Stockholders' Equity |

|

|

|

|

|

|

|

Retained earnings |

|

32,679 |

|

194 |

|

32,873 |

8

In accordance with the new revenue standard requirements, the disclosure of the impact of adoption on our consolidated income statement and balance sheet was as follows:

|

|

|

|

|

|

|

|

|

(Dollars in thousands) |

|

As Reported, March 31, 2018 |

|

Balances Without Adoption of ASC 606 |

|

Effect of change Higher / (Lower) |

|

Revenues |

|

|

|

|

|

|

|

Cinema |

|

72,255 |

|

71,995 |

|

260 |

|

Income tax expense |

|

(1,155) |

|

(1,084) |

|

(71) |

|

Net income |

|

3,047 |

|

2,858 |

|

189 |

|

|

|

|

|

|

|

|

|

(Dollars in thousands) |

|

As Reported |

|

Balances Without Adoption of ASC 606 |

|

Effect of change Higher / (Lower) |

|

Assets |

|

|

|

|

|

|

|

Deferred income taxes |

|

24,834 |

|

24,905 |

|

(71) |

|

Liabilities |

|

|

|

|

|

|

|

Deferred current revenue |

|

8,276 |

|

8,536 |

|

(260) |

|

Stockholders' Equity |

|

|

|

|

|

|

|

Retained earnings |

|

35,920 |

|

35,731 |

|

189 |

Refer to Note 1: - Description of the Business and Segment Reporting for a disaggregation of our revenue sources.

Cinema Segment

Sales of cinema tickets and food and beverage (“F&B”) revenue: recognized when sold and collected, either in cash or by credit card at our theatre locations and through our online selling channels. Sales of bulk or advanced tickets are deferred and recognized as revenue when the related screening for that ticket is shown.

Gift Card/Certificate Programs: We run gift card and gift certificate programs in all three countries. Revenue from these programs is deferred and recognized when redeemed. From January 1, 2018, we recognize revenue on unredeemed cards and certificates using the proportional method, whereby breakage revenue is recognized in proportion to the pattern of rights exercised by the customer when the Company expects that it is probable that a significant revenue reversal would not occur for any estimated breakage amounts. This is based on a breakage ‘experience rate’, which is determined by historical redemption data.

Loyalty revenue: We run a customer loyalty program in every country. From January 1, 2018, a component of revenue from Members of our Loyalty Programs relating to the earning of loyalty rewards is deferred until such a time as Members redeem rewards, or until we believe the likelihood of redemption by the Member is remote. Deferral is based on the progress made toward the next reward, the fair value of that reward, and the likelihood of redemption, determined by historical redemption data.

Advertising revenue: recognized based on contractual arrangements or relevant admissions information, as appropriate.

Real Estate

Live Theatre License Fees: We lease theatre space to third party production companies. Revenue is recognized in accordance with the license agreement, and is recorded on a weekly basis after the performance of a show has occurred.

Property Rentals: we contractually retain substantially all of the risks and benefits of ownership of our real estate properties and therefore, we account for our tenant leases as operating leases. Accordingly, rental revenue is recognized on a straight-line basis over the lease term.

On January 1, 2018, the Company adopted ASU 2016-18, Statement of Cash Flows, Topic 230: Restricted Cash, a consensus of the FASB Emerging Issues Task Force. This new guidance requires that amounts generally described as restricted cash and cash equivalents should be combined with unrestricted cash and cash equivalents when reconciling the beginning and end of period balances on the statement of cash flows. This guidance has no material effect on our consolidated statement of cash flows.

On January 1, 2018, the Company adopted ASU 2016-15, Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments). The amendments covered in this ASU are improvements to current GAAP, as such amendments will provide guidance with respect to eight (8) specific cash flow classification issues, thereby reducing the current and potential future diversity in practice. Adoption of this guidance has no material effect on our consolidated statement of cash flows.

9

On January 1, 2018, the Company adopted ASU 2017-07, Compensation—Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost. The amendments in this Update (i) require that an employer disaggregate the service cost component from the other components of net benefit cost, and (ii) provide explicit guidance on how to present the service cost component and the other components of net benefit cost in the income statement and (iii) allow only the service cost component of net benefit cost to be eligible for capitalization. The new guidance has no material impact on our consolidated financial statements.

Also, on January 1, 2018, the Company adopted ASU 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business. This ASU provides that when substantially all of the fair value of the gross assets acquired (or disposed of) is concentrated in a single identifiable asset or a group of similar identifiable assets, the asset is not a “business”, thus reducing the number of transactions that need further evaluation for business combination. The new guidance has no material impact on our current consolidated financial statements, and we do not expect the ASU 2017-01 to be applicable to our consolidated financial statements in the near term unless we enter into a definitive business acquisition transaction.

On January 1, 2017, the Company adopted ASU 2016-09, Compensation—Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting. This new guidance, which became effective for fiscal years beginning after December 15, 2016, provides for the simplification of several aspects of the accounting for share-based payment transactions, including (i) accounting for tax benefits in excess of compensation cost and tax deficiencies, (ii) accounting for forfeitures, and (iii) classification on the statement of cash flows. The only significant impact of the adoption of this new guidance to us is the immediate recognition of excess tax benefits (or “windfalls”) and tax deficiencies (or “shortfalls”) in the consolidated statement of income. Previously, (i) tax windfalls were recorded in additional paid-in capital (“APIC”) in the consolidated statement of stockholders’ equity and (ii) tax shortfalls were recorded in APIC to the extent of previous windfalls and then to the consolidated statement of income.

Issued:

|

v |

ASUs Effective 2019 and Beyond |

|

· |

New Lease Accounting Model (ASU 2016-02, Leases: Topic 842) |

This new guidance, which becomes effective for us by January 1, 2019, establishes a right-of-use ("ROU") model that requires a lessee to record a ROU asset and a lease liability on the balance sheet for all leases with terms longer than 12 months. Leases will be classified as either finance or operating, with classification affecting the pattern of expense recognition in the income statement. A modified retrospective transition approach is required for lessees with capital and operating leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements, with certain practical expedients available. While we are still evaluating the impact of our pending adoption of this new standard on our consolidated financial statements, we expect that upon adoption we will recognize ROU assets and lease liabilities and that the amounts could be material since a majority of our operating cinemas are leased. We have developed an implementation plan. Significant implementation matters that we are addressing include (i) assessment of lease population, (ii) determination of appropriate discount rate to use and (ii) assessment of renewal options to include in the initial lease term. While the Company is continuing to assess the effect of adoption, the Company currently believes the most significant changes relate to the recognition of new ROU assets and lease liabilities on its balance sheet for cinemas currently subject to operating leases.

|

· |

Goodwill Impairment Simplification (ASU 2017-04, Intangibles – Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment) |

Issued by FASB in January 2017, this new guidance removes the second step of the two-step impairment test for measuring goodwill and is to be applied on a prospective basis only. The new guidance is effective for the Company on January 1, 2020, including interim periods within the year of adoption. Early adoption is permitted for interim or annual goodwill impairment tests performed on testing dates after January 1, 2017. We do not anticipate the adoption of ASU 2017-04 to have a material impact on our consolidated financial statements.

Note 3 – Operations in Foreign Currency

We have significant assets in Australia and New Zealand. Historically, we have conducted our Australian and New Zealand operations (collectively “foreign operations”) on a self-funding basis where we use cash flows generated by our foreign operations to pay for the expense of foreign operations. Our Australian and New Zealand assets and liabilities are translated from their functional currencies of Australian dollar (“AU$”) and New Zealand dollar (“NZ$”), respectively, to the U.S. dollar based on the exchange rate as of March 31, 2018. The carrying value of the assets and liabilities of our foreign operations fluctuates as a result of changes in the exchange rates between the functional currencies of the foreign operations and the U.S. dollar. The translation adjustments are accumulated in the Accumulated Other Comprehensive Income in the Consolidated Balance Sheets.

10

Likewise, historically, our overall operating strategy has been to conduct business mostly on a self-funding basis (except for funds used to pay an appropriate share of our U.S. corporate overhead). As such, we have not historically used derivative financial instruments to hedge against the risk of foreign currency exposure. However, in certain circumstances, we may decide to move funds between jurisdictions where circumstances encouraged us to do so from an overall economic standpoint. Going forward, particularly in light of recent tax law changes, we intend to take a more global view of our financial resources, and to be more flexible in making use of resources from one jurisdiction in other jurisdictions.

As of December 31, 2016, we determined certain historically long-term intercompany loans from the U.S. Parent Company to our Australian subsidiary should be considered short-term. Subsequently, on September 1, 2017, we determined that the remaining AU$21.1 million in such long-term intercompany loans should be considered as short-term as well. This loan was paid in full on December 21, 2017. As a result of the above, we recognized foreign exchange gain on these intercompany advances based on the relative strengthening of the Australian dollar to the U.S. dollar in the amounts of $0 and $825,000 for the three months ended March 31, 2018 and March 2017 respectively in our Consolidated Statements of Income.

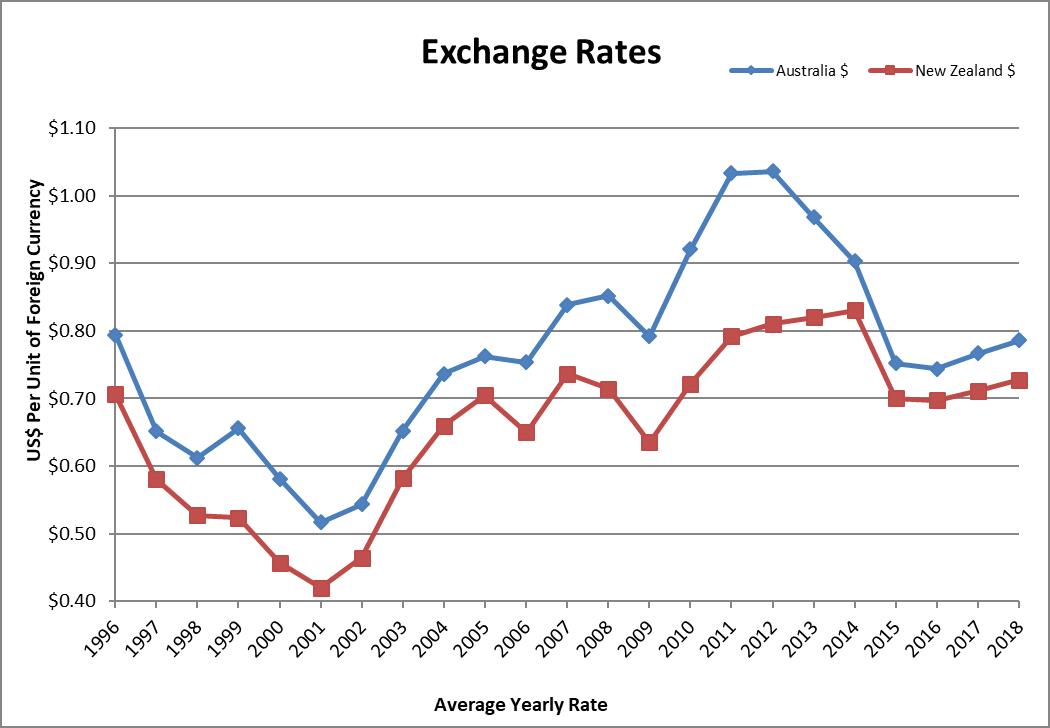

Presented in the table below are the currency exchange rates for Australia and New Zealand:

|

|

Foreign Currency / USD |

|||||

|

|

As of and for the quarter ended |

|

As of and for the twelve months ended |

|

As of and for the quarter ended |

|

|

|

March 31, 2018 |

December 31, 2017 |

March 31, 2017 |

|||

|

Spot Rate |

||||||

|

Australian Dollar |

0.7690 |

0.7815 |

0.7638 |

|||

|

New Zealand Dollar |

0.7239 |

0.7100 |

0.7001 |

|||

|

Average Rate |

||||||

|

Australian Dollar |

0.7861 |

0.7670 |

0.7584 |

|||

|

New Zealand Dollar |

0.7275 |

0.7111 |

0.7122 |

|||

Note 4 – Earnings Per Share

Basic earnings per share (“EPS”) is calculated by dividing the net income attributable to the Company’s common stockholders by the weighted average number of common shares outstanding during the period. Diluted EPS is calculated by dividing the net income attributable to the Company’s common stockholders by the weighted average number of common and common equivalent shares outstanding during the period and are calculated using the treasury stock method for equity-based compensation awards.

The following table sets forth the computation of basic and diluted EPS and a reconciliation of the weighted average number of common and common equivalent shares outstanding:

|

|

Three Months Ended |

|||||

|

(Dollars in thousands, except share data) |

March 31, 2018 |

March 31, 2017 |

||||

|

Numerator: |

||||||

|

Net income attributable to RDI common stockholders |

$ |

3,047 |

$ |

3,029 | ||

|

Denominator: |

||||||

|

Weighted average number of common stock – basic |

22,967,237 | 23,168,351 | ||||

|

Weighted average dilutive impact of awards |

165,752 | 296,825 | ||||

|

Weighted average number of common stock – diluted |

23,132,989 | 23,465,176 | ||||

|

Basic EPS attributable to RDI common stockholders |

$ |

0.13 |

$ |

0.13 | ||

|

Diluted EPS attributable to RDI common stockholders |

$ |

0.13 |

$ |

0.13 | ||

|

Awards excluded from diluted EPS |

-- |

-- |

||||

Our weighted average number of common stock - basic decreased primarily as a result of our repurchase of 386,462 shares of Class A Common Stock during the 12 months ended March 31, 2018, pursuant to our current stock repurchase program offset by the issuance of shares due to the exercise of share options and vesting of restricted stock units.

11

Note 5 – Property and Equipment

Operating Property, net

As of March 31, 2018 and December 31, 2017, property associated with our operating activities is summarized as follows:

|

|

March 31, |

December 31, |

||||

|

(Dollars in thousands) |

2018 |

2017 |

||||

|

Land |

$ |

76,125 |

$ |

76,457 | ||

|

Building and improvements |

152,350 | 153,232 | ||||

|

Leasehold improvements |

48,469 | 48,481 | ||||

|

Fixtures and equipment |

152,116 | 145,033 | ||||

|

Construction-in-progress |

29,477 | 26,000 | ||||

|

Total cost |

458,537 | 449,203 | ||||

|

Less: accumulated depreciation |

(188,959) | (184,479) | ||||

|

Operating property, net |

$ |

269,578 |

$ |

264,724 | ||

Depreciation expense for operating property was $4.7 million for the quarter ended March 31, 2018 and $3.5 million for the quarter ended March 31, 2017.

Investment and Development Property, net

As of March 31, 2018 and December 31, 2017, our investment and development property is summarized below:

|

|

March 31, |

December 31, |

||||

|

(Dollars in thousands) |

2018 |

2017 |

||||

|

Land |

$ |

25,283 |

$ |

25,025 | ||

|

Building |

1,900 | 1,900 | ||||

|

Construction-in-progress (including capitalized interest) |

39,761 | 34,329 | ||||

|

Investment and development property |

$ |

66,944 |

$ |

61,254 | ||

Construction-in-Progress – Operating and Investing Properties

Construction-in-Progress balances are included in both our operating and development properties. The balances of our major projects along with the movements for the three months ended March 31, 2018 are shown below:

|

(Dollars in thousands) |

Balance, December 31, 2017 |

Additions during the period(1) |

Completed during the period |

Foreign currency translation |

Balance, March 31, 2018 |

|||||

|

Union Square development |

$ |

29,223 |

$ |

5,486 |

$ |

-- |

$ |

-- |

$ |

34,709 |

|

Newmarket Property development |

370 | 756 | (636) | (8) | 482 | |||||

|

Courtenay Central development |

4,676 |

- |

-- |

91 | 4,767 | |||||

|

Cinema developments and improvements |

19,015 | 5,123 | (2,879) | 54 | 21,313 | |||||

|

Other real estate projects |

7,045 | 1,020 |

-- |

(98) | 7,967 | |||||

|

Total |

$ |

60,329 |

$ |

12,385 |

$ |

(3,515) |

$ |

39 |

$ |

69,238 |

(1) Includes capitalized interest of $335,000 for the quarter ended March 31, 2018.

Real Estate Transactions

Sale of Landholding in Burwood, Australia

On December 14, 2017, we received $28.1 million (AU$36.6 million) representing the final payment with respect to the $50.6 million (AU$64.9 million) sale price of our property in Burwood, Victoria, Australia. Previously, partial payments of $16.6 million (AU$21.8 million) and $5.9 million (AU$6.5 million) were received on June 19, 2017 and May 23, 2014.

12

Note 6 – Investments in Unconsolidated Joint Ventures

Our investments in unconsolidated joint ventures are accounted for under the equity method of accounting.

The table below summarizes our active investment holdings in two (2) unconsolidated joint ventures as of March 31, 2018 and December 31, 2017:

|

|

March 31, |

December 31, |

||||||

|

(Dollars in thousands) |

Interest |

2018 |

2017 |

|||||

|

Rialto Cinemas |

50.0% |

$ |

1,279 |

$ |

1,186 | |||

|

Mt. Gravatt |

33.3% |

4,004 | 4,118 | |||||

|

Total investments |

$ |

5,283 |

$ |

5,304 | ||||

For the quarter ended March 31, 2018 and 2017, the recognized share of equity earnings from our investments in unconsolidated joint ventures are as follows:

|

|

Quarter Ended |

|||||||

|

|

March 31, |

March 31, |

||||||

|

(Dollars in thousands) |

2018 |

2017 |

||||||

|

Rialto Cinemas |

$ |

70 |

$ |

39 | ||||

|

Mt. Gravatt |

187 | 216 | ||||||

|

Total equity earnings |

$ |

257 |

$ |

255 | ||||

Note 7 – Goodwill and Intangible Assets

The table below summarizes goodwill by business segment as of March 31, 2018 and December 31, 2017.

|

(Dollars in thousands) |

Cinema |

Real Estate |

Total |

||||||

|

Balance at December 31, 2017 |

$ |

15,052 |

$ |

5,224 |

$ |

20,276 | |||

|

Foreign currency translation adjustment |

107 |

-- |

107 | ||||||

|

Balance at March 31, 2018 |

$ |

15,159 |

$ |

5,224 |

$ |

20,383 | |||

The Company is required to test goodwill and other intangible assets for impairment on an annual basis and, if current events or circumstances require, on an interim basis. Our next annual evaluation of goodwill and other intangible assets is scheduled during the fourth quarter of 2018. To test the impairment of goodwill, the Company compares the fair value of each reporting unit to its carrying amount, including the goodwill, to determine if there is potential goodwill impairment. A reporting unit is generally one level below the operating segment. As of March 31, 2018, we were not aware of any events indicating potential impairment of goodwill had occurred.

The tables below summarize intangible assets other than goodwill as of March 31, 2018 and December 31, 2017, respectively.

|

|

As of March 31, 2018 |

|||||||||||

|

(Dollars in thousands) |

Beneficial Leases |

Trade Name |

Other Intangible Assets |

Total |

||||||||

|

Gross carrying amount |

$ |

28,836 |

$ |

7,255 |

$ |

1,139 |

$ |

37,230 | ||||

|

Less: Accumulated amortization |

(23,511) | (5,004) | (488) | (29,003) | ||||||||

|

Net intangible assets other than goodwill |

$ |

5,325 |

$ |

2,251 |

$ |

651 |

$ |

8,227 | ||||

|

|

As of December 31, 2017 |

|||||||||||

|

(Dollars in thousands) |

Beneficial Leases |

Trade Name |

Other Intangible Assets |

Total |

||||||||

|

Gross carrying amount |

$ |

28,860 |

$ |

7,254 |

$ |

1,139 |

$ |

37,253 | ||||

|

Less: Accumulated amortization |

(23,292) | (4,936) | (483) | (28,711) | ||||||||

|

Net intangible assets other than goodwill |

$ |

5,568 |

$ |

2,318 |

$ |

656 |

$ |

8,542 | ||||

13

Beneficial leases are amortized over the life of the lease up to 30 years, trade names are amortized based on the accelerated amortization method over its estimated useful life of 45 years, and other intangible assets are amortized over their estimated useful lives of up to 30 years (except for transferrable liquor licenses, which are indefinite-lived assets). The table below summarizes the amortization expense of intangible assets for the quarter ended March 31, 2018.

|

|

Quarter Ended |

|||||

|

|

March 31, |

March 31, |

||||

|

(Dollars in thousands) |

2018 |

2017 |

||||

|

Beneficial lease amortization |

$ |

207 |

$ |

304 | ||

|

Other amortization |

93 | 102 | ||||

|

Total intangible assets amortization |

$ |

300 |

$ |

406 | ||

Note 8 – Prepaid and Other Assets

Prepaid and other assets are summarized as follows:

|

|

March 31, |

December 31, |

||||

|

(Dollars in thousands) |

2018 |

2017 |

||||

|

Prepaid and other current assets |

||||||

|

Prepaid expenses |

$ |

2,486 |

$ |

1,625 | ||

|

Prepaid rent |

1,101 | 1,055 | ||||

|

Prepaid taxes |

633 | 653 | ||||

|

Income taxes receivable |

2,187 | 1,686 | ||||

|

Deposits |

243 | 243 | ||||

|

Investment in marketable securities |

46 | 46 | ||||

|

Restricted cash |

17 | 17 | ||||

|

Total prepaid and other current assets |

$ |

6,713 |

$ |

5,325 | ||

|

Other non-current assets |

||||||

|

Straight-line rent |

3,421 | 2,564 | ||||

|

Other non-cinema and non-rental real estate assets |

1,134 | 1,134 | ||||

|

Investment in Reading International Trust I |

838 | 838 | ||||

|

Long-term deposits |

8 | 7 | ||||

|

Long-term restricted cash |

260 |

-- |

||||

|

Total other non-current assets |

$ |

5,661 |

$ |

4,543 | ||

Note 9 – Income Taxes

On December 22, 2017, the U.S. Tax Cuts and Jobs Act of 2017 (the “Tax Act”) was signed into law. The Tax Act significantly changed the U.S. corporate income tax law by lowering the statutory corporate tax rate from 35% to 21%, imposing a one-time mandatory repatriation tax on earnings of foreign subsidiaries, and changing how foreign earnings are subject to U.S. tax. Due to the timing of the enactment and the complexity involved in applying the provisions of the Tax Act, we made reasonable estimates of the effects and recorded provisional amounts in our financial statements as of December 31, 2017, pursuant to the guidance of the U.S. Securities and Exchange Commission Staff Accounting Bulletin No. 118. We recorded income tax expense in 2017 for the impact of the Tax Act of approximately $13.0 million. This 2017 net amount is primarily comprised of $8.3 million from re-measurement of federal net deferred tax assets resulting from the reduction in the U.S. statutory corporate tax rate and a provisional amount of $4.7 million from the one-time mandatory repatriation tax on deferred earnings of our foreign subsidiaries. As we complete our analysis of the Tax Act, collect and prepare necessary data, and interpret any additional guidance issued by the U.S. Treasury Department and the IRS, we may make adjustments to the provisional amount. Those adjustments may materially impact our provision for income taxes in the period in which the adjustments are made. The accounting for the tax effects of the Tax Act will be completed in 2018.

The interim provision for income taxes is different from the amount determined by applying the U.S. federal statutory rate to consolidated income before taxes. The differences are attributable to foreign tax rate differential, unrecognized tax benefits, and foreign tax credit. Our effective tax rate was 27.3% and 35.9% for the three months ended March 31, 2018 and 2017, respectively. The change between 2018 and 2017 is primarily related to the reduction of U.S. statutory corporate tax rate as the result of the Tax Act, foreign tax credit, partially offset by a change in the foreign tax rate differential.

14

Note 10 – Debt

The Company’s borrowings at March 31, 2018 and December 31, 2017, net of deferred financing costs and including the impact of interest rate derivatives on effective interest rates, are summarized below:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of March 31, 2018 |

|||||||||||||

|

(Dollars in thousands) |

|

Maturity Date |

|

Contractual Facility |

|

Balance, Gross |

|

Balance, Net(3) |

|

Stated Interest Rate |

|

Effective Interest Rate (1) |

||||

|

Denominated in USD |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trust Preferred Securities (USA) |

|

April 30, 2027 |

|

$ |

27,913 |

|

$ |

27,913 |

|

$ |

27,564 |

|

5.77% |

|

5.77% |

|

|

Bank of America Credit Facility (USA) |

|

November 28, 2019 |

|

|

55,000 |

|

|

31,000 |

|

|

31,000 |

|

4.88% |

|

4.88% |

|

|

Bank of America Line of Credit (USA) |

|

October 31, 2019 |

|

|

5,000 |

|

|

-- |

|

|

-- |

|

4.84% |

|

4.84% |

|

|

Bank of America digital projector loan (USA) |

|

December 28, 2019 |

|

|

4,031 |

|

|

4,031 |

|

|

4,031 |

|

5.00% |

|

5.00% |

|

|

Cinema 1, 2, 3 Term Loan (USA)(4) |

|

August 31, 2019 |

|

|

19,396 |

|

|

19,396 |

|

|

19,037 |

|

3.25% |

|

3.25% |

|

|

Minetta & Orpheum Theatres Loan (USA)(4) |

|

June 1, 2018 |

|

|

7,500 |

|

|

7,500 |

|

|

7,488 |

|

4.44% |

|

4.44% |

|

|

U.S. Corporate Office Term Loan (USA)(4) |

|

January 1, 2027 |

|

|

9,665 |

|

|

9,665 |

|

|

9,531 |

|

4.64% / 4.44% |

|

4.61% |

|

|

Union Square Construction Financing (USA)(4) |

|

December 29, 2019 |

|

|

57,500 |

|

|

9,155 |

|

|

6,326 |

|

6.06% / 11.88% |

|

6.79% |

|

Denominated in foreign currency ("FC") (2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAB Corporate Term Loan (AU) |

|

June 28, 2019 |

|

|

51,139 |

|

|

41,525 |

|

|

41,453 |

|

3.78% |

|

3.78% |

|

|

Westpac Bank Corporate (general/non-construction) Credit Facility (NZ) |

|

December 31, 2019 |

|

|

25,337 |

|

|

-- |

|

|

- |

|

3.70% |

|

3.70% |

|

|

Westpac Bank Corporate (construction) Credit Facility (NZ) |

|

December 31, 2018 |

|

|

13,030 |

|

|

-- |

|

|

-- |

|

3.70% |

|

3.70% |

|

|

|

$ |

275,511 |

|

|

150,185 |

|

|

146,430 |

|

|

|

|

|||

(1) Both interest rate derivatives associated with the Trust Preferred Securities and Bank of America Credit Facility expired in October 2017 so the effective interest rate no longer applies as of December 31, 2017

(2) The contractual facilities and outstanding balances of the FC-denominated borrowings were translated into U.S. dollars based on the applicable exchange rates as of March 31, 2018.

(3) Net of deferred financing costs amounting to $3.8 million.

(4) The loan for our Minetta & Orpheum Theatres was obtained from Santander Bank. The term loan for our Cinema 1,2,3 Theatre was refinanced during the third quarter of 2016 with Valley National Bank. The term loan, which is collateralized by our new U.S Corporate Headquarters office building, was obtained with Citizens Asset Finance, Inc. In December 2016, we completed the negotiation of the construction financing for our Union Square redevelopment project, $8.0 million of which was advanced from the total construction loan limit of $57.5 million on December 29, 2016. As of March 31, 2018 an additional $1.2 million had been advanced.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of December 31, 2017 |

|||||||||||||

|

(Dollars in thousands) |

|

Maturity Date |

|

Contractual Facility |

|

Balance, Gross |

|

Balance, Net(3) |

|

Stated Interest Rate |

|

Effective Interest Rate (1) |

||||

|

Denominated in USD |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trust Preferred Securities (USA) |

|

April 30, 2027 |

|

$ |

27,913 |

|

$ |

27,913 |

|

$ |

27,554 |

|

5.38% |

|

5.38% |

|

|

Bank of America Credit Facility (USA) |

|

November 28, 2019 |

|

|

55,000 |

|

|

31,000 |

|

|

31,000 |

|

4.57% |

|

4.57% |

|

|

Bank of America Line of Credit (USA) |

|

October 31, 2019 |

|

|

5,000 |

|

|

-- |

|

|

-- |

|

4.57% |

|

4.57% |

|

|

Cinema 1, 2, 3 Term Loan (USA) |

|

September 1, 2019 |

|

|

19,500 |

|

|

19,500 |

|

|

19,105 |

|

3.25% |

|

3.25% |

|

|

Minetta & Orpheum Theatres Loan (USA) |

|

June 1, 2018 |

|

|

7,500 |

|

|

7,500 |

|

|

7,470 |

|

4.13% |

|

4.13% |

|

|

U.S. Corporate Office Term Loan (USA)(4) |

|

January 1, 2027 |

|

|

9,719 |

|

|

9,719 |

|

|

9,582 |

|

4.64% / 4.44% |

|

4.61% |

|

|

Union Square Construction Financing (USA) |

|

December 29, 2019 |

|

|

57,500 |

|

|

8,000 |

|

|

5,033 |

|

5.81% |

|

5.81% |

|

Denominated in FC (2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAB Corporate Loan Facility (AU) |

|

June 30, 2019 |

|

|

51,970 |

|

|

30,869 |

|

|

30,781 |

|

3.66% |

|

3.66% |

|

|

Westpac Bank Corporate (general/non-construction) Credit Facility (NZ) |

|

December 31, 2019 |

|

|

24,850 |

|

|

-- |

|

|

-- |

|

3.70% |

|

3.70% |

|

|

Westpac Bank Corporate (construction) Credit Facility (NZ) |

|

December 31, 2018 |

|

|

12,780 |

|

|

-- |

|

|

-- |

|

3.70% |

|

3.70% |

|

|

|

|

|

|

$ |

271,732 |

|

$ |

134,501 |

|

$ |

130,525 |

|

|

|

|

(1) Both interest rate derivatives associated with the Trust Preferred Securities and Bank of America Credit Facility expired in October 2017 so the effective interest rate no longer applies as of December 31, 2017.

(2) The contractual facilities and outstanding balances of the FC-denominated borrowings were translated into U.S. dollars based on the applicable exchange rates as of December 31, 2016.

(3) Net of deferred financing costs amounting to $4.0 million.

(4) The loan for our Minetta & Orpheum Theatres was obtained from Santander Bank. The term loan for our Cinema 1,2,3 Theatre was refinanced during the third quarter of 2016 with Valley National Bank. The term loan, which is collateralized by our new U.S Corporate Headquarters office building, was obtained with Citizens Asset Finance, Inc.. In December 2016, we completed the negotiation of the construction financing for our Union Square redevelopment project, $8.0 million of which was advanced from the total construction loan limit of $57.5 million on December 29, 2016. As of December 31, 2017 no further advances had been made under this financing agreement.

Our loan arrangements are presented, net of the deferred financing costs, on the face of our consolidated balance sheet as follows:

|

|

Dollars in thousands |

|||||

|

Balance Sheet Caption |

March 31, 2018 |

December 31, 2017 |

||||

|

Debt - current portion |

$ |

10,544 |

$ |

8,109 | ||

|

Debt - long-term portion |

108,322 | 94,862 | ||||

|

Subordinated debt |

27,564 | 27,554 | ||||

|

Total borrowings |

$ |

146,430 |

$ |

130,525 | ||

15

Union Square Construction Financing

On December 29, 2016, we closed on our new construction finance facilities totaling $57.5 million to fund the non-equity portion of the anticipated construction costs of the redevelopment of our property at 44 Union Square in New York City. The combined facilities consist of $50 million in aggregate loans (comprised of three loan tranches) from Bank of the Ozarks and a $7.5 million mezzanine loan from Tammany Mezz Investor, LLC, an affiliate of Fisher Brothers. At December 29, 2016, Bank of the Ozarks advanced $8.0 million to repay the then existing $8.0 million loan with East West Bank. As of March 31, 2018, an additional $1.2 million had been advanced under the mezzanine loan facility.

Presented in the table below is the breakdown of the Union Square construction financing as of March 31, 2018:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Dollars in thousands) |

|

|

|

|

Facility Limits and Advances |

|

|

|

|

|||||||

|

Financing Component |

|

Lender |

|

Facility Limit |

|

Advanced-to- Date |

|

Remaining Facility |

|

Interest Rate(1) |

|

Maturity Date(2) |

||||

|

Mezzanine loan |

|

Tammany Mezz Investor LLC |

|

$ |

7,500 |

|

$ |

1,155 |

|

$ |

6,345 |

|

Greater of (i) 10.50% and (ii) Adjusted LIBOR + 10% |

|

December 29, 2019 |

|

|

Senior loan, including building and project loan |

|

Bank of the Ozarks |

|

|

50,000 |

|

|

8,000 |

|

|

42,000 |

|

Greater of (i) 4.75% and (ii) Adjusted LIBOR + 4.25% |

|

December 29, 2019 |

|

|

Total Union Square Financing |

|

|

|

$ |

57,500 |

|

$ |

9,155 |

|

$ |

48,345 |

|

|

|

|

|

(1) Not to exceed the New York State maximum lawful borrowing rate, which typically is 16%.

(2) Allowable for up to two (2) extension request options, one (1) year for each extension request.

Cinema 1,2,3 Term Loan

On August 31, 2016, Sutton Hill Properties LLC (“SHP”), a 75% subsidiary of RDI, refinanced its $15.0 million Santander Bank term loan with a different lender, Valley National Bank. This new $20.0 million loan is collateralized by our Cinema 1,2,3 property and bears an interest rate of 3.25% per annum, with principal instalments and accruing interest paid monthly. The new loan matures on September 1, 2019, with a one-time option to extend the maturity date for another year.

Bank of America Credit Facility

On March 3, 2016, we amended our $55.0 million credit facility with Bank of America to permit real property acquisition loans. This amendment provides that the consolidated leverage ratio be reduced by 0.25% from the established levels in the credit facility during the period of such borrowing, with a repayment term based on the earlier of the eighteen months from the date of such borrowing or the maturity date of the credit agreement. Such modification was not considered substantial in accordance with U.S. GAAP.

Bank of America Line of Credit

In October 2016, the term of this line of credit was extended to October 31, 2019. Such modification was not considered to be substantial under US GAAP.

Westpac Bank Corporate Credit Facility

On December 15, 2017, we extended the maturity of the 1st tranche (general/non-construction credit line) of our Westpac Corporate Credit Facility to December 31, 2019. Prior to this on April 26, 2017, we extended the maturity of our entire Westpac Corporate Credit Facility, $38.4 million (NZ$53.0 million) to December 31, 2018, from March 31, 2018. We are currently working on a longer-term renewal of our Westpac Corporate Credit Facility which will replace the existing facility.

U.S. Corporate Office Term Loan

On December 13, 2016, we obtained a ten-year $8.4 million mortgage loan on our new Los Angeles Corporate Headquarters at a fixed annual interest rate of 4.64%. This loan provided for a second loan upon completion of certain improvements. On June 26, 2017, we obtained a further $1.5 million under this provision at a fixed annual interest rate of 4.44%.

Bank of America Digital Projector Loan

On February 5, 2018, we purchased our U.S. cinema projectors, which had previously been held on operating leases, using a $4.6 million loan from Bank of America. This loan carries an interest rate of 5%.

16

Note 11 – Other Liabilities

Other liabilities are summarized as follows:

|

(Dollars in thousands) |

March 31, 2018 |

December 31, 2017 |

||||

|

Current liabilities |

||||||

|

Lease liability |

$ |

5,900 |

$ |

5,900 | ||

|

Liability for demolition costs |

2,836 | 2,781 | ||||

|

Accrued pension |

684 | 2,907 | ||||

|

Security deposit payable |

76 | 91 | ||||

|

Other |

19 |

-- |

||||

|

Other current liabilities |

$ |

9,515 |

$ |

11,679 | ||

|

Other liabilities |

||||||

|

Straight-line rent liability |

$ |

15,529 |

$ |

13,444 | ||

|

Lease make-good provision |

5,687 | 5,648 | ||||

|

Accrued pension |

5,047 | 5,228 | ||||

|

Environmental reserve |

1,656 | 1,656 | ||||

|

Deferred revenue - real estate |

16 | 18 | ||||

|

Acquired leases |

163 | 186 | ||||

|

Other |

455 | 469 | ||||

|

Other liabilities |

$ |

28,553 |

$ |

26,649 | ||

On August 29, 2014, the Supplemental Executive Retirement Plan (“SERP”) that has been effective since March 1, 2007, was ended and replaced in accordance with the terms of a pension annuity. As a result of the termination of the SERP program, the accrued pension liability of $7.6 million was reversed and replaced with this pension annuity liability of $7.5 million. The valuation of the liability is based on the present value of $10.2 million discounted at a rate of 4.25% over a 15- year term, resulting in a monthly payment of $57,000. The discount rate of 4.25% has been applied since 2014 to determine the net periodic benefit cost and plan benefit obligation and is expected to be used in future years. The discounted value of $2.7 million (which is the difference between the estimated payout of $10.2 million and the present value of $7.5 million) as of August 29, 2014 will be amortized and expensed based on the 15-year term. In addition, the accumulated actuarial loss of $3.1 million recorded, as part of other comprehensive income will also be amortized based on the 15-year term.

In February 2018 we made a payment of $2.4 million relating to the annuity representing payments for the 42 months outstanding at the time. Monthly ongoing payments of $57,000 are now being made.

As a result of the above, included in our current and non-current liabilities are accrued pension costs of $5.7 million at March 31, 2018. The benefits of our pension plans are fully vested and therefore no service costs were recognized for the quarter ended March 31, 2018 and 2017. Our pension plans are unfunded.

During the quarter ended March 31, 2018, the interest cost was $45,000 and actuarial loss was $52,000. During the quarter ended March 31, 2017, the interest cost was $45,000, and actuarial loss was $52,000.

Note 12 – Accumulated Other Comprehensive Income

The following table summarizes the changes in each component of accumulated other comprehensive income attributable to RDI:

|

(Dollars in thousands) |

Foreign Currency Items |

|

Unrealized Gain (Losses) on Available-for-Sale Investments |

|

Accrued Pension Service Costs |

|

Total |

||||

|

Balance at January 1, 2018 |

$ |

23,575 |

$ |

8 |

$ |

(2,592) |

$ |

20,991 | |||

|

Net current-period other comprehensive (loss) income |

(800) | (2) | 52 | (750) | |||||||

|

Balance at March 31, 2018 |

$ |

22,775 |

$ |

6 |

$ |

(2,540) |

$ |

20,241 | |||

17

Note 13 – Commitments and Contingencies

Litigation General

We are currently involved in certain legal proceedings and, as required, have accrued estimates of probable and estimable losses for the resolution of these claims, including legal costs.

|

· |

Where we are the plaintiffs, we accrue legal fees as incurred on an on-going basis and make no provision for any potential settlement amounts until received. In Australia, the prevailing party is usually entitled to recover its attorneys’ fees, which recoveries typically work out to be approximately 60% of the amounts actually spent where first-class legal counsel is engaged at customary rates. Where we are a plaintiff, we have likewise made no provision for the liability for the defendant’s attorneys' fees in the event we are determined not to be the prevailing party. |

|

· |

Where we are the defendants, we accrue for probable damages that insurance may not cover as they become known and can be reasonably estimated. In our opinion, any claims and litigation in which we are currently involved are not reasonably likely to have a material adverse effect on our business, results of operations, financial position, or liquidity. It is possible, however, that future results of the operations for any particular quarterly or annual period could be materially affected by the ultimate outcome of the legal proceedings. From time-to-time, we are involved with claims and lawsuits arising in the ordinary course of our business that may include contractual obligations, insurance claims, tax claims, employment matters, and anti-trust issues, among other matters. |

All of these matters require significant judgments based on the facts known to us. These judgments are inherently uncertain and can change significantly when additional facts become known. We provide accruals for matters that have probable likelihood of occurrence and can be properly estimated as to their expected negative outcome. We do not record expected gains until the proceeds are received by us. However, we typically make no accruals for potential costs of defense, as such amounts are inherently uncertain and dependent upon the scope, extent and aggressiveness of the activities of the applicable plaintiff.

Environmental and Asbestos Claims on Reading Legacy Operations

Certain of our subsidiaries were historically involved in railroad operations, coal mining, and manufacturing. Also, certain of these subsidiaries appear in the chain-of-title of properties that may suffer from pollution. Accordingly, certain of these subsidiaries have, from time-to-time, been named in and may in the future be named in various actions brought under applicable environmental laws. Also, we are in the real estate development business and may encounter from time-to-time unanticipated environmental conditions at properties that we have acquired for development. These environmental conditions can increase the cost of such projects and adversely affect the value and potential for profit of such projects. We do not currently believe that our exposure under applicable environmental laws is material in amount.

From time-to-time, there are claims brought against us relating to the exposure of former employees of our railroad operations to asbestos and coal dust. These are generally covered by an insurance settlement reached in September 1990 with our insurance providers. However, this insurance settlement does not cover litigation by people who were not our employees and who may claim second-hand exposure to asbestos, coal dust and/or other chemicals or elements now recognized as potentially causing cancer in humans. Our known exposure to these types of claims, asserted or probable of being asserted, is not material.

Cotter Jr. Related Litigation Matters

The following table provides a list of legal matters and current status relating to James J. Cotter, Jr’s (“Cotter, Jr.”) employment termination, Mr. Cotter, Jr.’s subsequent derivative action brought against the Company and our Directors alleging, among other things, that such termination violated the fiduciary duties of such Directors, and Mr. Cotter, Jr.’s efforts to cause a change of control of the Company, with detailed discussions following:

18

|

|

|

|

|

|

|

|

|

|

|

|

|

Description |

Plaintiff/ Claimant |

Filed with |

Current Status |

|

|

James J. Cotter, Jr. Legal Cases |

|

|||

|

Cotter, Jr. Derivative Litigation against all Directors on matters other than the handling by the Directors of the Patton Vision Unsolicited Indication of Interest |

Cotter, Jr. |

Nevada District Court |

Claims against Directors Judy Codding, William Gould, Edward L. Kane, Douglas McEachern and Michael Wrotniak were dismissed on December 29, 2017; court trial for the remaining claim was postponed at Cotter, Jr.’s request. The Court put the trial on a trial stack with the trial set to begin on July 9, 2018. It is anticipated that various summary judgment motions being brought by the Company and the Defendant Directors will be heard before the case is tried. |

|

|

Cotter, Jr. Derivative Litigation against all Directors re handling by the Directors of unsolicited indication of interest by Patton Vision, LLC. |

Cotter, Jr. |

Nevada District Court |

Dismissed as to all Directors on December 29, 2017. |

|

|

Direct Case against the Company seeking reimbursement and advancement of attorney’s fees incurred with respect to the Employment Arbitration |

Cotter, Jr. |

Nevada District Court |

Summary judgment entered in favor of the Company on October 3, 2016. |

|

|

Employment Arbitration |

RDI |

American Arbitration Association |

While RDI is the named claimant, the matter relates to Mr. Cotter, Jr’s claims for compensation related to his termination. In Discovery Phase: hearing anticipated in October, 2018. |

|

|

T2 Partners Derivative Complaint |

T2 Partners Management |

Nevada District Court |

Settled on October 6, 2016, without the payment of any monetary consideration or any reimbursement of attorney’s fees. |

|

James J. Cotter, Jr., Litigation Matters.

The James J. Cotter, Jr. Derivative Litigation: On June 12, 2015, the Board of Directors terminated James J. Cotter, Jr. as the President and Chief Executive Officer of our Company. That same day, Mr. Cotter, Jr. filed a lawsuit, styled as both an individual and a derivative action, and titled “James J. Cotter, Jr., individually and derivatively on behalf of Reading International, Inc. vs. Margaret Cotter, et al.” Case No,: A-15-719860-V, Dept. XI, against our Company and each of our then sitting Directors (Ellen Cotter, Margaret Cotter, Guy Adams, William Gould, Edward Kane, Douglas McEachern, and Tim Storey) in the Eighth Judicial District Court of the State of Nevada for Clark County (the “Nevada District Court”). Since that date, our Company has been engaged in ongoing litigation with Mr. Cotter, Jr. with respect to his claims against our Directors. Mr. Cotter, Jr. has over this period of time twice amended his complaint, removing his individual claims and withdrawing his claims against Tim Storey (but reserving the right to reinstitute such claims), adding claims relating to actions taken by our Board since the filing of his original complaint, and adding as defendants two of our directors who were not on our Board at the time of his termination: Judy Codding and Michael Wrotniak. Mr. Cotter, Jr.’s lawsuit, as amended from time to time, is referred to herein as the “Cotter Jr. Derivative Action” and his complaint, as amended from time to time, is referred to herein as the “Cotter Jr. Derivative Complaint.” The defendant directors named in the Cotter Jr. Derivative Complaint, from time to time, are referred to herein as the “Defendant Directors.”