Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - LAUREATE EDUCATION, INC. | exhibit32toform10-qq12018.htm |

| EX-31.2 - EXHIBIT 31.2 - LAUREATE EDUCATION, INC. | exhibit312toform10-qq120181.htm |

| EX-31.1 - EXHIBIT 31.1 - LAUREATE EDUCATION, INC. | exhibit311toform10-qq120181.htm |

| EX-21.1 - EXHIBIT 21.1 - LAUREATE EDUCATION, INC. | exhibit211subsidiarieslist.htm |

| EX-10.71 - EXHIBIT 10.71 - LAUREATE EDUCATION, INC. | exhibit1071charhonperforma.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended March 31, 2018

OR

o Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from __________ to __________.

Commission File Number: 001-38002

Laureate Education, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 52-1492296 | |

(State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization) | Identification No.) | |

650 S. Exeter Street, Baltimore, Maryland | 21202 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (410) 843-6100

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o Non-accelerated filer x (Do not check if a smaller reporting company)

Smaller reporting company o Emerging Growth Company o

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

Class | Outstanding at March 31, 2018 | |

Class A common stock, par value $0.004 per share | 55,255,800 shares | |

Class B common stock, par value $0.004 per share | 132,442,619 shares | |

INDEX | |||

PART I. - FINANCIAL INFORMATION | Page No. | ||

Item 1. | Financial Statements (Unaudited) | ||

Consolidated Statements of Operations - Three months ended March 31, 2018 and March 31, 2017 | |||

Consolidated Statements of Comprehensive Income - Three months ended March 31, 2018 and March 31, 2017 | |||

Consolidated Balance Sheets - March 31, 2018 and December 31, 2017 | |||

Consolidated Statements of Cash Flows - Three months ended March 31, 2018 and March 31, 2017 | |||

Notes to Consolidated Financial Statements | |||

Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | ||

Item 4. | Controls and Procedures | ||

PART II. - OTHER INFORMATION | |||

Item 1. | Legal Proceedings | ||

Item 1A. | Risk Factors | ||

Item 6. | Exhibits | ||

SIGNATURES | |||

1

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Statements of Operations

IN THOUSANDS, except per share amounts

For the three months ended March 31, | 2018 | 2017 | |||||

(Unaudited) | (Unaudited) | ||||||

Revenues | $ | 885,288 | $ | 855,933 | |||

Costs and expenses: | |||||||

Direct costs | 865,446 | 853,232 | |||||

General and administrative expenses | 47,301 | 65,567 | |||||

Operating loss | (27,459 | ) | (62,866 | ) | |||

Interest income | 6,129 | 4,694 | |||||

Interest expense | (69,465 | ) | (102,633 | ) | |||

Loss on debt extinguishment | (7,481 | ) | (1,515 | ) | |||

(Loss) gain on derivatives | (19,340 | ) | 12,147 | ||||

Other income, net | 2,406 | 436 | |||||

Foreign currency exchange (loss) gain, net | (8,754 | ) | 2,290 | ||||

Gain on sales of subsidiaries, net | 298,041 | — | |||||

Income (loss) from continuing operations before income taxes | 174,077 | (147,447 | ) | ||||

Income tax (expense) benefit | (2,532 | ) | 27,094 | ||||

Net income (loss) | 171,545 | (120,353 | ) | ||||

Net income attributable to noncontrolling interests | (2,666 | ) | (2,454 | ) | |||

Net income (loss) attributable to Laureate Education, Inc. | $ | 168,879 | $ | (122,807 | ) | ||

Accretion of Series A convertible redeemable preferred stock and other redeemable noncontrolling interests and equity | (57,403 | ) | (38,876 | ) | |||

Net income (loss) available to common stockholders | $ | 111,476 | $ | (161,683 | ) | ||

Basic and diluted earnings (loss) per share: | |||||||

Basic earnings (loss) per share | $ | 0.59 | $ | (1.05 | ) | ||

Diluted earnings (loss) per share | $ | 0.59 | $ | (1.05 | ) | ||

The accompanying notes are an integral part of these consolidated financial statements.

2

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Statements of Comprehensive Income

IN THOUSANDS

For the three months ended March 31, | 2018 | 2017 | |||||

(Unaudited) | (Unaudited) | ||||||

Net income (loss) | $ | 171,545 | $ | (120,353 | ) | ||

Other comprehensive income: | |||||||

Foreign currency translation adjustment, net of tax of $0 for both periods | 83,369 | 103,396 | |||||

Unrealized gain on derivative instruments, net of tax of $0 for both periods | 2,210 | 2,592 | |||||

Minimum pension liability adjustment, net of tax of $0 | 376 | — | |||||

Total other comprehensive income | 85,955 | 105,988 | |||||

Comprehensive income (loss) | 257,500 | (14,365 | ) | ||||

Net comprehensive income attributable to noncontrolling interests | (2,387 | ) | (2,786 | ) | |||

Comprehensive income (loss) attributable to Laureate Education, Inc. | $ | 255,113 | $ | (17,151 | ) | ||

The accompanying notes are an integral part of these consolidated financial statements.

3

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Balance Sheets

IN THOUSANDS, except per share amounts

March 31, 2018 | December 31, 2017 | ||||||

Assets | (Unaudited) | ||||||

Current assets: | |||||||

Cash and cash equivalents (includes VIE amounts of $199,609 and $231,940, see Note 2) | $ | 479,011 | $ | 468,733 | |||

Restricted cash | 184,989 | 224,934 | |||||

Receivables: | |||||||

Accounts and notes receivable | 786,145 | 535,176 | |||||

Other receivables | 21,474 | 21,551 | |||||

Allowance for doubtful accounts | (196,159 | ) | (198,802 | ) | |||

Receivables, net | 611,460 | 357,925 | |||||

Income tax receivable | 25,150 | 41,178 | |||||

Prepaid expenses and other current assets | 134,615 | 93,461 | |||||

Current assets held for sale | 57,990 | 102,623 | |||||

Total current assets (includes VIE amounts of $537,880 and $407,315, see Note 2) | 1,493,215 | 1,288,854 | |||||

Notes receivable, net | 9,448 | 4,116 | |||||

Property and equipment: | |||||||

Land | 402,781 | 397,153 | |||||

Buildings | 995,922 | 1,026,656 | |||||

Furniture, equipment and software | 1,238,810 | 1,188,211 | |||||

Leasehold improvements | 440,121 | 423,658 | |||||

Construction in-progress | 75,392 | 84,520 | |||||

Accumulated depreciation and amortization | (1,257,674 | ) | (1,185,294 | ) | |||

Property and equipment, net | 1,895,352 | 1,934,904 | |||||

Land use rights, net | 2,735 | 2,713 | |||||

Goodwill | 1,942,335 | 1,954,666 | |||||

Other intangible assets: | |||||||

Tradenames | 1,280,617 | 1,295,614 | |||||

Other intangible assets, net | 34,095 | 35,927 | |||||

Deferred costs, net | 67,061 | 64,128 | |||||

Deferred income taxes | 177,601 | 156,006 | |||||

Derivative instruments | 41,341 | 48,186 | |||||

Other assets | 261,727 | 214,218 | |||||

Long-term assets held for sale | 311,231 | 392,391 | |||||

Total assets (includes VIE amounts of $1,375,479 and $1,419,579, see Note 2) | $ | 7,516,758 | $ | 7,391,723 | |||

The accompanying notes are an integral part of these consolidated financial statements.

4

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Balance Sheets (continued)

IN THOUSANDS, except per share amounts

March 31, 2018 | December 31, 2017 | ||||||

Liabilities and stockholders' equity | (Unaudited) | ||||||

Current liabilities: | |||||||

Accounts payable | $ | 82,825 | $ | 79,568 | |||

Accrued expenses | 310,362 | 291,216 | |||||

Accrued compensation and benefits | 191,755 | 247,575 | |||||

Deferred revenue and student deposits | 675,455 | 312,422 | |||||

Current portion of long-term debt | 131,738 | 154,234 | |||||

Current portion of due to shareholders of acquired companies | 35,431 | 40,140 | |||||

Income taxes payable | 18,636 | 29,857 | |||||

Derivative instruments | 123 | 4,458 | |||||

Other current liabilities | 42,101 | 38,560 | |||||

Current liabilities held for sale | 103,340 | 176,719 | |||||

Total current liabilities (includes VIE amounts of $425,234 and $341,147, see Note 2) | 1,591,766 | 1,374,749 | |||||

Long-term debt, less current portion | 2,852,334 | 3,207,064 | |||||

Due to shareholders of acquired companies, less current portion | 39,512 | 39,429 | |||||

Deferred compensation | 14,594 | 14,470 | |||||

Income taxes payable | 81,321 | 112,576 | |||||

Deferred income taxes | 293,957 | 278,215 | |||||

Derivative instruments | 14,772 | 9,390 | |||||

Other long-term liabilities | 312,001 | 260,144 | |||||

Long-term liabilities held for sale | 86,853 | 94,407 | |||||

Total liabilities (includes VIE amounts of $496,419 and $449,561, see Note 2) | 5,287,110 | 5,390,444 | |||||

Series A convertible redeemable preferred stock, par value $0.001 per share – 512 shares authorized, 401 shares issued and outstanding as of March 31, 2018 and December 31, 2017, respectively | 447,881 | 400,276 | |||||

Redeemable noncontrolling interests and equity | 14,294 | 13,721 | |||||

Stockholders' equity: | |||||||

Preferred stock, par value $0.001 per share – 49,488 shares authorized, no shares issued and outstanding as of March 31, 2018 and December 31, 2017 | — | — | |||||

Class A common stock, par value $0.004 per share – 700,000 shares authorized, 55,256 shares issued and outstanding as of March 31, 2018 and 55,052 shares issued and outstanding as of December 31, 2017 | 221 | 220 | |||||

Class B common stock, par value $0.004 per share – 175,000 shares authorized, 132,443 shares issued and outstanding as of March 31, 2018 and December 31, 2017 | 530 | 530 | |||||

Additional paid-in capital | 3,383,778 | 3,446,206 | |||||

Accumulated deficit | (772,283 | ) | (946,236 | ) | |||

Accumulated other comprehensive loss | (839,322 | ) | (925,556 | ) | |||

Total Laureate Education, Inc. stockholders' equity | 1,772,924 | 1,575,164 | |||||

Noncontrolling interests | (5,451 | ) | 12,118 | ||||

Total stockholders' equity | 1,767,473 | 1,587,282 | |||||

Total liabilities and stockholders' equity | $ | 7,516,758 | $ | 7,391,723 | |||

The accompanying notes are an integral part of these consolidated financial statements.

5

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Statements of Cash Flows

IN THOUSANDS

For the three months ended March 31, | 2018 | 2017 | |||||

Cash flows from operating activities | (unaudited) | (unaudited) | |||||

Net income (loss) | $ | 171,545 | $ | (120,353 | ) | ||

Adjustments to reconcile net income (loss) to net cash used in operating activities: | |||||||

Depreciation and amortization | 67,762 | 64,514 | |||||

(Gain) loss on sales of subsidiaries and disposal of property and equipment, net | (297,479 | ) | 345 | ||||

Loss (gain) on derivative instruments | 19,132 | (12,267 | ) | ||||

Loss on debt extinguishment | 7,481 | 467 | |||||

Non-cash interest expense | 4,645 | 12,233 | |||||

Non-cash share-based compensation expense | (3,756 | ) | 22,388 | ||||

Bad debt expense | 22,153 | 16,502 | |||||

Deferred income taxes | (26,560 | ) | (15,882 | ) | |||

Unrealized foreign currency exchange loss | 1,082 | 1,079 | |||||

Non-cash loss from non-income tax contingencies | 2,121 | 4,037 | |||||

Other, net | (315 | ) | 1,919 | ||||

Changes in operating assets and liabilities: | |||||||

Receivables | (268,434 | ) | (267,480 | ) | |||

Prepaid expenses and other assets | (20,158 | ) | (43,773 | ) | |||

Accounts payable and accrued expenses | (61,087 | ) | (51,855 | ) | |||

Income tax receivable/payable, net | (14,810 | ) | (8,907 | ) | |||

Deferred revenue and other liabilities | 389,602 | 360,635 | |||||

Net cash used in operating activities | (7,076 | ) | (36,398 | ) | |||

Cash flows from investing activities | |||||||

Purchase of property and equipment | (44,245 | ) | (37,147 | ) | |||

Expenditures for deferred costs | (3,365 | ) | (3,476 | ) | |||

Receipts from sales of subsidiaries and property and equipment, net of cash sold | 359,510 | 126 | |||||

Settlement of derivatives related to sale of subsidiaries | (9,960 | ) | — | ||||

Property insurance recoveries | — | 370 | |||||

Payments from (to) related parties and affiliates | 750 | (347 | ) | ||||

Net cash provided by (used in) investing activities | 302,690 | (40,474 | ) | ||||

Cash flows from financing activities | |||||||

Proceeds from issuance of long-term debt, net of original issue discount | 188,563 | 6,790 | |||||

Payments on long-term debt | (541,812 | ) | (50,335 | ) | |||

Payments of deferred purchase price for acquisitions | (5,534 | ) | (5,315 | ) | |||

Payments to purchase noncontrolling interests | (127 | ) | — | ||||

Proceeds from issuance of convertible redeemable preferred stock, net of issuance costs | — | 55,290 | |||||

Payment of dividends on Series A Preferred Stock | (9,719 | ) | — | ||||

Proceeds from initial public offering, net of issuance costs | — | 456,888 | |||||

Withholding of shares to satisfy tax withholding for vested stock awards | (803 | ) | — | ||||

Payments of debt issuance costs | (148 | ) | (600 | ) | |||

Noncontrolling interest holder's loan to subsidiaries | — | 943 | |||||

Distributions from noncontrolling interest holders | 581 | 454 | |||||

Net cash (used in) provided by financing activities | (368,999 | ) | 464,115 | ||||

Effects of exchange rate changes on Cash and cash equivalents and Restricted cash | 20,133 | 10,618 | |||||

Change in cash included in current assets held for sale | 23,585 | — | |||||

Net change in Cash and cash equivalents and Restricted cash | (29,667 | ) | 397,861 | ||||

Cash and cash equivalents and Restricted cash at beginning of period | 693,667 | 654,284 | |||||

Cash and cash equivalents and Restricted cash at end of period | $ | 664,000 | $ | 1,052,145 | |||

The accompanying notes are an integral part of these consolidated financial statements.

6

Laureate Education, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

(Dollars and shares in thousands)

Note 1. Description of Business

Laureate Education, Inc. and subsidiaries (hereinafter Laureate, we, us, our, or the Company) provide higher education programs and services to students through an international network of licensed universities and higher education institutions (institutions). Laureate's programs are provided through institutions that are campus-based and internet-based, or through electronically distributed educational programs (online). On October 1, 2015, we redomiciled in Delaware as a public benefit corporation as a demonstration of our long-term commitment to our mission to benefit our students and society.

The Company's shares are listed on the Nasdaq Global Select Market under the symbol ‘‘LAUR’’. In its initial public offering (IPO) on February 6, 2017, the Company sold 35,000 shares of its Class A common stock in the IPO at a price of $14.00 per share, resulting in net proceeds to the Company during the first quarter of 2017, after deducting underwriting discounts and commissions and offering expenses payable by us, of $456,888.

As previously disclosed in our Annual Report on Form 10-K for the fiscal year ended December 31, 2017, (the 2017 Form 10-K) effective August 1, 2017, we changed our operating segments in order to realign our segments according to how our chief operating decision maker allocates resources and assesses performance. The segment changes resulted in Laureate increasing its number of operating segments from three to six, and is consistent with our goal of flattening our organizational structure to improve decision speed and operating effectiveness. As required, the segment information presented for comparative purposes for the three months ended March 31, 2017 has been revised to reflect this change.

The accompanying unaudited Consolidated Financial Statements have been prepared in accordance with accounting principles generally accepted in the United States (GAAP) for interim financial information and with the instructions to Form 10-Q. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In our opinion, these financial statements include all adjustments considered necessary to present a fair statement of our consolidated results of operations, financial position and cash flows. Operating results for any interim period are not necessarily indicative of the results that may be expected for the full year. These unaudited Consolidated Financial Statements should be read in conjunction with Laureate's audited Consolidated Financial Statements included in our 2017 Form 10-K.

7

Note 2. Significant Accounting Policies

The Variable Interest Entity (VIE) Arrangements

Laureate consolidates in its financial statements certain internationally based educational organizations that do not have shares or other equity ownership interests. Although these educational organizations may be considered not-for-profit entities in their home countries and they are operated in compliance with their respective not-for-profit legal regimes, we believe they do not meet the definition of a not-for-profit entity under GAAP, and therefore we treat them as "for-profit" entities for accounting purposes. These entities generally cannot declare dividends or distribute their net assets to the entities that control them.

Under ASC 810-10, "Consolidation," we have determined that these institutions are VIEs and that Laureate is the primary beneficiary of these VIEs because we have, as further described herein: (1) the power to direct the activities of the VIEs that most significantly affect their educational and economic performance and (2) the right to receive economic benefits from contractual and other arrangements with the VIEs that could potentially be significant to the VIEs. We account for the acquisition of the right to control a VIE in accordance with ASC 805, "Business Combinations."

As discussed further in Note 5, Dispositions, the number of our VIE institutions was reduced by one in January 2018 following the sale of LEI Lie Ying Limited (LEILY).

The VIEs in Brazil and Mexico comprise several not-for-profit foundations that have insignificant revenues and operating expenses. Selected Consolidated Statements of Operations information for VIEs was as follows, net of the charges related to the above-described contractual arrangements:

For the three months ended March 31, | 2018 | 2017 | |||||

Selected Statements of Operations information: | |||||||

Revenues, by segment: | |||||||

Brazil | $ | — | $ | — | |||

Mexico | — | — | |||||

Andean & Iberian | 55,036 | 48,311 | |||||

Central America & U.S. Campuses | 15,140 | 15,375 | |||||

EMEAA | 61,196 | 66,213 | |||||

Revenues | 131,372 | 129,899 | |||||

Depreciation and amortization | 11,023 | 12,823 | |||||

Operating (loss) income, by segment: | |||||||

Brazil | (18 | ) | (21 | ) | |||

Mexico | (157 | ) | (191 | ) | |||

Andean & Iberian | (39,262 | ) | (41,923 | ) | |||

Central America & U.S. Campuses | (305 | ) | 1,055 | ||||

EMEAA | 12,771 | 11,887 | |||||

Operating loss | (26,971 | ) | (29,193 | ) | |||

Net loss | (22,468 | ) | (20,112 | ) | |||

Net loss attributable to Laureate Education, Inc. | (22,728 | ) | (20,936 | ) | |||

8

The following table reconciles the Net income (loss) attributable to Laureate Education, Inc. as presented in the table above, to the amounts in our Consolidated Statements of Operations:

For the three months ended March 31, | 2018 | 2017 | |||||

Net income (loss) attributable to Laureate Education, Inc.: | |||||||

Variable interest entities | $ | (22,728 | ) | $ | (20,936 | ) | |

Other operations | (30,590 | ) | 30,707 | ||||

Corporate and eliminations | 222,197 | (132,578 | ) | ||||

Net income (loss) attributable to Laureate Education, Inc. | $ | 168,879 | $ | (122,807 | ) | ||

The following table presents selected assets and liabilities of the consolidated VIEs. Except for Goodwill, the assets in the table below include the assets that can be used only to settle the obligations for the VIEs. The liabilities in the table are liabilities for which the creditors of the VIEs do not have recourse to the general credit of Laureate.

Selected Consolidated Balance Sheet amounts for these VIEs were as follows:

March 31, 2018 | December 31, 2017 | ||||||||||||||

VIE | Consolidated | VIE | Consolidated | ||||||||||||

Balance Sheets data: | |||||||||||||||

Cash and cash equivalents | $ | 199,609 | $ | 479,011 | $ | 231,940 | $ | 468,733 | |||||||

Current assets held for sale | — | 57,990 | 22,246 | 102,623 | |||||||||||

Other current assets | 338,271 | 956,214 | 153,129 | 717,498 | |||||||||||

Total current assets | 537,880 | 1,493,215 | 407,315 | 1,288,854 | |||||||||||

Goodwill | 198,683 | 1,942,335 | 192,230 | 1,954,666 | |||||||||||

Tradenames | 96,949 | 1,280,617 | 110,577 | 1,295,614 | |||||||||||

Other intangible assets, net | — | 34,095 | — | 35,927 | |||||||||||

Long-term assets held for sale | — | 311,231 | 185,139 | 392,391 | |||||||||||

Other long-term assets | 541,967 | 2,455,265 | 524,318 | 2,424,271 | |||||||||||

Total assets | 1,375,479 | 7,516,758 | 1,419,579 | 7,391,723 | |||||||||||

Current liabilities held for sale | — | 103,340 | 64,895 | 176,719 | |||||||||||

Other current liabilities | 425,234 | 1,488,426 | 276,252 | 1,198,030 | |||||||||||

Long-term liabilities held for sale | — | 86,853 | 41,732 | 94,407 | |||||||||||

Long-term debt and other long-term liabilities | 71,185 | 3,608,491 | 66,682 | 3,921,288 | |||||||||||

Total liabilities | 496,419 | 5,287,110 | 449,561 | 5,390,444 | |||||||||||

Total stockholders' equity | 879,060 | 1,767,473 | 970,018 | 1,587,282 | |||||||||||

Total stockholders' equity attributable to Laureate Education, Inc. | 878,689 | 1,772,924 | 948,966 | 1,575,164 | |||||||||||

On January 24, 2018, a new Higher Education Law (the New Law) was passed by the Chilean Congress. On March 27, 2018, the Constitutional Court declared unconstitutional Article 63 of the New Law, which would have prohibited for-profit organizations such as Laureate from controlling the boards of universities in Chile. As the Constitutional Court did not release its opinion until April 26, 2018, signature and enactment of the New Law is expected to occur in the second quarter of 2018. Among other things left intact by the Constitutional Court, the New Law prohibits conflicts of interests and related party transactions with certain exceptions, including the provision of services that are educational in nature or essential for the university's purposes. The New Law provides for a transition period. The incoming Chilean presidential administration, which took office on March 11, 2018, has the responsibility to implement the new legislative mandates and compliance processes.

The Company is currently reviewing the impact the New Law will have on its Chilean operations, including the extent to which it will affect existing contractual relationships that the Company maintains with the Chilean non-profit universities. As the New Law no longer contains provisions that prohibit Laureate from controlling the boards of the Chilean non-profit universities, but still requires the promulgation of new regulations and procedures that will be applicable to any commercial relationship that the

9

Company has with the Chilean non-profit universities, the Company has determined that it will continue to consolidate the three Chilean non-profit universities, which are accounted for as variable interest entities, and its Chilean real estate subsidiary.

While we believe that all of our institutions in Chile are operating in full compliance with Chilean law, we cannot predict the extent or outcome of any educational reforms that may be implemented in Chile. The Company does not believe the New Law will change its relationship with its two tech/voc institutions in Chile that are for-profit entities. However, it is possible that the Chilean government will adopt additional laws that affect for-profit tech/voc institutions and their relationships with their owners. Depending upon how these reforms are defined and implemented, there could be a material adverse effect on our financial condition and results of operations.

Allowance for Doubtful Accounts

Receivables are deemed to be uncollectible when they have been outstanding for two years, or earlier when collection efforts have ceased, at which time they are written off. Prior to that, Laureate records an allowance for doubtful accounts to reduce our receivables to their net realizable value. Our allowance estimation methodology is based on the age of the receivables, the status of past-due amounts, historical collection trends, current economic conditions and student enrollment status. In the event that current collection trends differ from historical trends, an adjustment is made to the allowance account and bad debt expense.

The reconciliations of the beginning and ending balances of the Allowance for doubtful accounts were as follows:

For the three months ended March 31, | 2018 | 2017 | |||||

Balance at beginning of period | $ | 204,252 | $ | 196,270 | |||

Additions: charges to bad debt expense | 22,153 | 16,502 | |||||

Additions: charges to other accounts (a) | — | 503 | |||||

Deductions (b) | (24,883 | ) | (17,571 | ) | |||

Balance at end of period | $ | 201,522 | $ | 195,704 | |||

(a) Charges to other accounts includes reclassifications.

(b) Deductions includes accounts receivable written off against the allowance (net of recoveries), reclassifications, and foreign

currency translation. The beginning and ending balances of the Allowance for doubtful accounts include the current

portion, as shown on the face of Consolidated Balance Sheets, in addition to the noncurrent portion that is included in

Notes receivable, net on the Consolidated Balance Sheets.

10

Recently Adopted Accounting Standards

Accounting Standards Update (ASU) No. 2014-09, (ASU 2014-09), Revenue from Contracts with Customers (Topic 606)

On May 28, 2014, the Financial Accounting Standards Board (FASB) issued ASU 2014-09, which, along with amendments issued in 2015 and 2016, supersedes the revenue recognition requirements in Accounting Standards Codification (ASC) 605, ‘‘Revenue Recognition’’ and most industry-specific guidance. The core principle of ASU 2014-09 is that a company will recognize revenue when it transfers promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. We adopted Topic 606 as of January 1, 2018 using the modified retrospective transition method and elected to apply the standard only to contracts that are not completed as of that date. We recorded a net increase to opening retained earnings of approximately $1,400 as of January 1, 2018 due to the cumulative impact of adopting Topic 606, with the impact primarily related to the deferral of costs to obtain a contract which were previously expensed as incurred. The impact to revenues as a result of applying Topic 606 was an increase of $6,633 for the three months ended March 31, 2018.

In accordance with the requirements under Topic 606, the disclosure of the impact of adoption on our Consolidated Statement of Operations and Consolidated Balance Sheet was as follows:

For the period ended March 31, 2018 | |||||||||

As Reported | Balances Without Adoption of ASC 606 | Effect of Change Higher/(Lower) | |||||||

Statement of Operations data: | |||||||||

Revenues | $ | 885,288 | $ | 878,655 | $ | 6,633 | |||

Costs and Expenses: | |||||||||

Direct costs | 865,446 | 868,561 | (3,115 | ) | |||||

Income tax expense | (2,532 | ) | (2,502 | ) | 30 | ||||

Net income | 171,545 | 161,827 | 9,718 | ||||||

As of March 31, 2018 | ||||||

As Reported | Balances Without Adoption of ASC 606 | Effect of Change Higher/(Lower) | ||||

Balance Sheet data: | ||||||

Assets: | ||||||

Deferred costs, net | 67,061 | 62,528 | 4,533 | |||

Liabilities: | ||||||

Deferred revenue and student deposits | 675,455 | 682,088 | (6,633 | ) | ||

Deferred income taxes | 293,957 | 293,927 | 30 | |||

Equity: | ||||||

Accumulated deficit | (772,283 | ) | (783,419 | ) | 11,136 | |

11

ASU No. 2016-15 (ASU 2016-15), Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments

In August 2016, the FASB issued ASU 2016-15 in order to address the diversity in practice in how certain cash receipts and cash payments are presented and classified in the statement of cash flows under Topic 230, Statement of Cash Flows, and other Topics. This standard addresses the following eight specific cash flow issues: debt prepayment or debt extinguishment costs; settlement of zero-coupon debt instruments or other debt instruments with coupon interest rates that are insignificant in relation to the effective interest rate of the borrowing; contingent consideration payments made after a business combination; proceeds from the settlement of insurance claims; proceeds from the settlement of corporate-owned life insurance policies (COLIs) (including bank-owned life insurance policies (BOLIs)); distributions received from equity method investees; beneficial interests in securitization transactions; and separately identifiable cash flows and application of the predominance principle. The amendments in this update apply to all entities, including both business entities and not-for-profit entities that are required to present a statement of cash flows under Topic 230. The Company adopted this standard beginning January 1, 2018, and it did not have a material effect on our Consolidated Financial Statements for the periods presented.

ASU No. 2016-16 (ASU 2016-16), Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory

In October 2016, the FASB issued ASU 2016-16 in order to improve the accounting for income tax consequences for intra-entity transfers of assets other than inventory. Prior to adopting this ASU, the recognition of current and deferred income taxes for an intra-entity transfer was prohibited until the asset was sold to a third party. The amendments in this ASU state that an entity should recognize income tax consequences of an intra-entity transfer when the transfer occurs. This aligns the recognition of income tax consequences for intra-entity transfers of assets with International Financing Reporting Standards (IFRS). Laureate adopted ASU 2016-16 effective January 1, 2018 and recorded a cumulative-effect adjustment to retained earnings of approximately $3,700.

ASU No. 2016-18 (ASU 2016-18), Statement of Cash Flows (Topic 230): Restricted Cash

In November 2016, the FASB issued ASU 2016-18 in order to address the diversity that exists in the classification and presentation of changes in restricted cash on the statement of cash flows under Topic 230, Statement of Cash Flows. The amendments in this ASU require that a statement of cash flows explain the change during the period in the total of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents. Therefore, amounts generally described as restricted cash and restricted cash equivalents should be included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the statement of cash flows. The amendments in this ASU apply to all entities that have restricted cash or restricted cash equivalents and are required to present a statement of cash flows under Topic 230. This ASU was adopted by Laureate beginning January 1, 2018 and resulted in a change in presentation within the Consolidated Statements of Cash Flows. As required, Laureate retrospectively applied the guidance to the prior period presented, which resulted in an increase of $3,432 and $1,114 in operating and investing cash flows, respectively, on the Consolidated Statement of Cash Flows for the three months ended March 31, 2017. As required by the ASU, we have provided a reconciliation from cash and cash equivalents as presented on our Consolidated Balance Sheets to cash, cash equivalents, and restricted cash as reported on our Consolidated Statements of Cash Flows. See Note 20, Supplemental Cash Flow Information, for this reconciliation, as well as a discussion of the nature of our restricted cash balances.

ASU No. 2017-07 (ASU 2017-07), Compensation - Retirement Benefits (Topic 715)

In March 2017, the FASB issued ASU 2017-07 in order to improve the presentation of net periodic pension cost and net periodic post retirement benefit cost. Prior to adoption of this ASU, these costs comprised several components that reflected different aspects of an employer's financial arrangements as well as the cost of benefits provided to employees, and were aggregated for reporting purposes. Under the amendments in this ASU, the service cost component of net periodic benefit cost is disaggregated and reported in the same line item(s) as other compensation costs arising from services rendered during the period, and the remaining components are presented on the income statement separately from the service cost component and outside a subtotal of income from operations, if presented. Laureate adopted ASU 2017-07 on January 1, 2018. Since the effect of ASU 2017-07 on prior periods presented was insignificant, we did not revise the Consolidated Statement of Operations for the three months ended March 31, 2017. For the three months ended March 31, 2018, the service cost component is included in Direct costs on our Consolidated Statement of Operations and the other components of net periodic benefit cost/(income), which totaled $237 for the three months ended March 31, 2018, are included in Other income, net on our Consolidated Statement of Operations.

12

Recently Issued Accounting Standards Not Yet Adopted

ASU No. 2016-02 (ASU 2016-02), Leases (Topic 842)

On February 25, 2016, the FASB issued ASU 2016-02. Lessees will need to recognize on their balance sheet a right-of-use asset and a lease liability for virtually all of their leases (other than leases that meet the definition of a short-term lease). The liability will be equal to the present value of the lease payments. The asset will be based on the liability, subject to adjustment, such as for initial direct costs and uneven rent payments. For income statement purposes, the FASB retained a dual model, requiring leases to be classified as either operating or finance. Operating leases will result in straight-line expense (similar to current operating leases) while finance leases will result in a front-loaded expense pattern (similar to current capital leases). Classification will be based on criteria that are largely similar to those applied in current lease accounting, but without explicit bright lines. The standard is effective for Laureate beginning January 1, 2019. The new standard must be adopted using a modified retrospective transition and provides for certain practical expedients. Transition will require application of the new guidance at the beginning of the earliest comparative period presented. We have completed our diagnostic assessment and have established a cross-functional implementation team which is in the process of identifying changes to our accounting policies, business processes, systems and internal controls in preparation for the implementation. We anticipate that ASU 2016-02 will have a material impact on our Consolidated Balance Sheets, as we will record significant asset and liability balances in connection with our leased properties. We are still evaluating the impact to our Consolidated Statements of Operations. We do not currently plan to early adopt this ASU.

Note 3. Revenue

Revenue Recognition

Laureate's revenues primarily consist of tuition and educational service revenues. We also generate other revenues from student fees, dormitory/residency fees and other education-related activities. These other revenues are less material to our overall financial results and have a tendency to trend with tuition revenues. Revenues are recognized when control of the promised goods or services is transferred to our customers, in an amount that reflects the consideration we expect to be entitled to in exchange for those goods or services. These revenues are recognized net of scholarships and other discounts, refunds, waivers and the fair value of any guarantees made by Laureate related to student financing programs. Laureate's institutions have various billing and academic cycles.

We determine revenue recognition through the five-step model prescribed by Topic 606 as follows:

•Identification of the contract, or contracts, with a customer;

•Identification of the performance obligations in the contract;

•Determination of the transaction price;

•Allocation of the transaction price to the performance obligations in the contract; and

•Recognition of revenue when, or as, we satisfy a performance obligation.

We assess collectibility on a portfolio basis prior to recording revenue. Generally, students cannot re-enroll for the next academic session without satisfactory resolution of any past-due amounts. If a student withdraws from an institution, Laureate's obligation to issue a refund depends on the refund policy at that institution and the timing of the student's withdrawal. Generally, our refund obligations are reduced over the course of the academic term. We record refunds as a reduction of deferred revenue as applicable.

13

The following table shows the components of Revenues by segment and as a percentage of total net revenue for the period ended March 31, 2018:

Brazil | Mexico | Andean & Iberian | Central America & U.S. Campuses | EMEAA | Online & Partnerships | Corporate(1) | Total | |||||||||||||||||||

Tuition and educational services | $ | 202,103 | $ | 166,310 | $ | 208,769 | $ | 76,057 | $ | 171,058 | $ | 181,245 | $ | — | $ | 1,005,542 | 114 | % | ||||||||

Other | 2,859 | 25,279 | 23,913 | 13,456 | 12,916 | 14,182 | (3,725 | ) | 88,880 | 10 | % | |||||||||||||||

Gross revenue | 204,962 | 191,589 | 232,682 | 89,513 | 183,974 | 195,427 | (3,725 | ) | 1,094,422 | 124 | % | |||||||||||||||

Less: Discounts / waivers / scholarships | (82,170 | ) | (35,690 | ) | (16,452 | ) | (10,486 | ) | (36,940 | ) | (27,396 | ) | — | (209,134 | ) | (24 | )% | |||||||||

Total | $ | 122,792 | $ | 155,899 | $ | 216,230 | $ | 79,027 | $ | 147,034 | $ | 168,031 | $ | (3,725 | ) | $ | 885,288 | 100 | % | |||||||

(1) Includes the elimination of intersegment revenues.

Performance Obligations

A performance obligation is a promise in a contract to transfer a distinct good or service to the customer and is the unit of accounting in ASC Topic 606. A contract’s transaction price is allocated to each performance obligation identified in the arrangement based on the relative standalone selling price of each distinct good or service in the contract and recognized as revenue when, or as, the performance obligation is satisfied. The primary method used to estimate standalone selling price is the adjusted market assessment approach, under which we evaluate the market and estimate the price that a customer would be willing to pay for the goods and services we provide.

Our performance obligations are primarily satisfied over time during the course of an academic semester or academic year. Laureate's transaction price is determined based on gross price, net of scholarships and other discounts, refunds, waivers and the fair value of any guarantees made by Laureate related to student financing programs. The majority of our revenue is derived from tuition and educational services agreements with students, and thus, is recognized over time on a weekly straight-line basis over each academic session. We view the knowledge gained by the student as the benefit which the student receives during the academic sessions. We use the output method to recognize tuition and educational services revenue as this method faithfully depicts our performance toward complete satisfaction of the performance obligation. Dormitory/residency revenues, which are included in the Other line item in the table above, are recognized over time throughout the occupancy period using the output method based on the proportional period of time elapsed which faithfully depicts our performance toward complete satisfaction of the performance obligation.

We have elected the optional exemption to not disclose amounts where the performance obligation is part of a contract that has an original expected duration of one year or less. We expect to recognize substantially all revenue on these remaining performance obligations over the next 12 months.

Contract Balances

The timing of billings, cash collections and revenue recognition results in accounts receivable (contract assets) and deferred revenue and student deposits (contract liabilities) on the Consolidated Balance Sheets. We have various billing and academic cycles and recognize student receivables when an academic session begins, although students generally enroll in courses prior to the start of the academic session. Receivables are recognized only to the extent that it is probable that we will collect substantially all of the consideration to which we are entitled in exchange for the goods and services that will be transferred to the student. We receive advance payments or deposits from our students before revenue is recognized, which are recorded as contract liabilities in deferred revenue and student deposits. Payment terms vary by university with some universities requiring payment in advance of the academic session and other universities allowing students to pay in installments over the term of the academic session.

All of our contract assets are considered accounts receivable and are included within the Accounts and notes receivable balance in the accompanying Consolidated Balance Sheets. Total accounts receivable from our contracts with students were $786,145 and $535,176 as of March 31, 2018 and December 31, 2017, respectively. In addition, as of March 31, 2018 and December 31, 2017, accounts receivable that were classified as assets held for sale were $15,434 and $34,744, respectively. The increase in the contract assets balance for the period ended March 31, 2018 is primarily driven by our enrollment cycle. The first calendar quarter generally coincides with the primary intake for some of our larger institutions. All contract asset amounts are classified as current.

14

Contract liabilities in the amount of $675,455 and $312,422 were included within the Deferred revenue and student deposits balance in the current liabilities section of the accompanying Consolidated Balance Sheets as of March 31, 2018 and December 31, 2017, respectively. In addition, as of March 31, 2018 and December 31, 2017, contract liabilities that were classified as liabilities held for sale were $46,335 and $94,951, respectively. The increase in the contract liability balance during the period ended March 31, 2018 is the result of semester billings and cash payments received in advance of satisfying performance obligations, offset by revenue recognized during that period. Revenue recognized for the three-month period ended March 31, 2018 that was included in the contract liability balance at the beginning of the year was approximately $217,000.

Costs to Obtain a Contract

Certain commissions and bonuses earned by third party agents and our employees are considered incremental and recoverable costs of obtaining a contract with a customer. These costs are deferred and then amortized over the period of benefit which ranges from two to four years. We determined the expected period of benefit, by university, as the expected student enrollment period. As of March 31, 2018 and December 31, 2017, the asset balances were $5,179 and $0, respectively, and the accumulated amortization balances were $646 and $0, respectively, both of which are included in Deferred costs, net, in the accompanying Consolidated Balance Sheets. The associated operating cost of $646 was recorded in Direct costs in the accompanying Consolidated Statement of Operations for the three months ended March 31, 2018. We also pay certain commissions and bonuses where the period of benefit is one year or less. We have elected the practical expedient available in ASC 340-40 whereby any incremental costs of obtaining a contract are recognized as an expense when incurred if the amortization period of the asset that would have been recognized is one year or less.

Practical Expedients and Optional Exemptions

We elected to adopt this standard using the modified retrospective approach with the cumulative effect of adoption recognized at the initial date of application. We have elected to apply the standard only to contracts that are not completed at the initial date of application.

As noted above, we recognize the incremental costs of obtaining a contract with a student as an expense when incurred in instances where the amortization period of the asset that we would have recognized is one year or less.

We have made an accounting policy election to exclude from the measurement of the transaction price all taxes assessed by governmental authorities that are both imposed on and concurrent with specific revenue-producing transactions and collected by the entity from our customers (e.g., sales, use, value added, some excise taxes).

Note 4. Assets Held for Sale

The Company has identified certain subsidiaries that may not reach a scale that will be meaningful for Laureate, or that represented a strategic sale opportunity, and has undertaken a process to sell these entities. As described in Note 5, Dispositions, several of these sale transactions closed during the first quarter of 2018. Several other sale transactions closed during the second quarter of 2018, as described in Note 21, Subsequent Events.

As of March 31, 2018, the subsidiaries in our EMEAA and Central America & U.S. Campuses segments that were classified as held for sale at December 31, 2017 in our 2017 Form 10-K and were not sold during the first quarter of 2018 continued to meet the criteria for classification as held for sale under ASC 360-10-45-9, "Long-Lived Assets Classified as Held for Sale." In addition, as described further below, during the first quarter of 2018, St. Augustine, a subsidiary in our Central America & U.S. Campuses segment that was not previously classified as held for sale, met the criteria for classification as held for sale. Accordingly, as of March 31, 2018, the assets and liabilities of these disposal groups were classified as held for sale and recorded at the lower of their carrying values or their estimated 'fair values less costs to sell.'

The amounts classified as held-for-sale assets and liabilities are subject to finalization. The carrying amounts of the major classes of long-lived assets and liabilities that were classified as held for sale as of March 31, 2018 are presented in the following tables:

Property and equipment, net | $ | 195,770 | |

Goodwill | 68,459 | ||

Tradenames | 32,312 | ||

Other long-term assets | 14,690 | ||

Long-term assets held for sale | $ | 311,231 | |

15

Deferred revenue and student deposits | $ | 46,335 | |

Long-term debt, including current portion | 78,289 | ||

Other liabilities | 65,569 | ||

Total liabilities held for sale | $ | 190,193 | |

In the aggregate, revenues of the disposal groups represented approximately $65,000 and $57,000 of Laureate's total revenues during the three months ended March 31, 2018 and 2017, respectively.

University of St. Augustine for Health Sciences, LLC (St. Augustine)

On April 24, 2018, the Company and Exeter Street Holdings, LLC (the Seller) and St. Augustine, both of which are wholly owned subsidiaries of the Company, entered into a Membership Interest Purchase Agreement (the Purchase Agreement) with University of St. Augustine Acquisition Corp. (the Purchaser), an affiliate of Altas Partners LP. Pursuant to the Purchase Agreement, the Purchaser will purchase from the Seller all of the issued and outstanding membership interests of St. Augustine. As of March 31, 2018, St. Augustine has been classified as held for sale on our Consolidated Balance Sheet.

The transaction value under the Purchase Agreement is $400,000, subject to customary closing adjustments, and the parties expect that the transaction will close in late 2018, subject to required regulatory approvals, including approvals by the U.S. Department of Education and the WASC Senior College and University Commission, and customary closing conditions. For the fiscal year ended December 31, 2017, St. Augustine had $89,600 in revenue, $30,500 in operating income and $4,100 in depreciation and amortization, and as of March 31, 2018 had approximately 3,200 students.

Note 5. Dispositions

Sale of Cyprus and Italy Operations

As previously disclosed in our 2017 Form 10-K, on January 11, 2018, we completed the sale of European University-Cyprus Ltd (EUC) and Laureate Italy S.r.L. (Laureate Italy). Upon closing, we received gross proceeds of approximately 232,000 Euros (EUR) (approximately US $275,500, or approximately US $248,400 on the date of receipt net of cash sold), and recognized a total gain on sale for the three months ended March 31, 2018 of approximately $218,000, which includes the working capital settlement between the Company and the buyer that was completed during the second quarter of 2018. The Company used the proceeds from this transaction, along with borrowings on our revolving credit facility that were subsequently repaid with the China sale proceeds discussed below, to repay $350,000 of principal balance on our syndicated term loan that matures in April 2024 (the 2024 Term Loan), as discussed in Note 9, Debt.

Sale of China Operations

As previously disclosed in our 2017 Form 10-K, on January 25, 2018, we completed the sale of LEILY. At closing, the Company received initial gross proceeds totaling approximately $128,800 (approximately $110,800 net of cash sold), net of banker transaction fees and certain taxes and duties totaling approximately $16,000. Six months after the closing date, the buyer is required to pay to the Company the Hong Kong Dollar (HKD) equivalent of Chinese Renminbi (RMB) 120,000 (the First Holdback Payment, approximately US $19,100 at March 31, 2018). Twelve months after the closing date, the buyer is required to pay to the Company the HKD equivalent of RMB 60,000 (the Second Holdback Payment, approximately US $9,600 at March 31, 2018). Both the First Holdback Payment and the Second Holdback Payment are subject to deduction of any indemnifiable losses payable by the Company to the buyer pursuant to the sale purchase agreement. The remainder of the transaction value was paid into an escrow account and will be distributed to the Company pursuant to the terms and conditions of the escrow agreement.

In addition to the initial proceeds received, as of March 31, 2018, the Company has recorded a current receivable of approximately $28,700 for the First Holdback Payment and the Second Holdback Payment, as well as a long-term receivable of approximately $25,900 for the portion of the escrowed amount that the Company expects to receive. In addition, the Company has recorded a liability of approximately $16,500 related to loss contingencies for which we have indemnified the buyer. The Company recognized a gain on the sale of LEILY for the three months ended March 31, 2018 of approximately $80,000.

16

Note 6. Due to Shareholders of Acquired Companies

The amounts due to shareholders of acquired companies generally arise in connection with Laureate’s acquisition of a majority or all of the ownership interest of these companies. Promissory notes payable to the sellers of acquired companies, referred to as “seller notes,” are commonly used as a means of payment for business acquisitions. Seller note payments are classified as Payments of deferred purchase price for acquisitions within financing activities in our Consolidated Statements of Cash Flows. The amounts due to shareholders of acquired companies, currencies, and interest rates applied were as follows:

March 31, 2018 | December 31, 2017 | Nominal Currency | Interest Rate % | |||||

Universidade Anhembi Morumbi (UAM Brazil) | $ | 45,955 | $ | 45,206 | BRL | CDI + 2% | ||

University of St. Augustine for Health Sciences, LLC (St. Augustine) | 11,550 | 11,550 | USD | 7% | ||||

Monash South Africa (MSA) | 9,626 | 9,571 | AUD | n/a | ||||

Universidad Tecnologica Centroamericana (UNITEC Honduras) | 3,447 | 3,813 | HNL | IIBC | ||||

Faculdade Porto-Alegrense (FAPA) | 3,123 | 3,084 | BRL | IGP-M | ||||

IADE Group | 1,242 | 2,374 | EUR | 3% | ||||

CH Holding Netherlands B.V. (CH Holding) | — | 3,971 | USD | n/a | ||||

Total due to shareholders of acquired companies | 74,943 | 79,569 | ||||||

Less: Current portion of due to shareholders of acquired companies | 35,431 | 40,140 | ||||||

Due to shareholders of acquired companies, less current portion | $ | 39,512 | $ | 39,429 | ||||

AUD: Australian Dollar | CDI: Certificados de Depósitos Interbancários (Brazil) | |

BRL: Brazilian Real | IIBC: Índice de Inflación del Banco Central (Honduras) | |

EUR: European Euro | IGP-M: General Index of Market Prices (Brazil) | |

HNL: Honduran Lempira | ||

USD: United States Dollar | ||

Note 7. Business and Geographic Segment Information

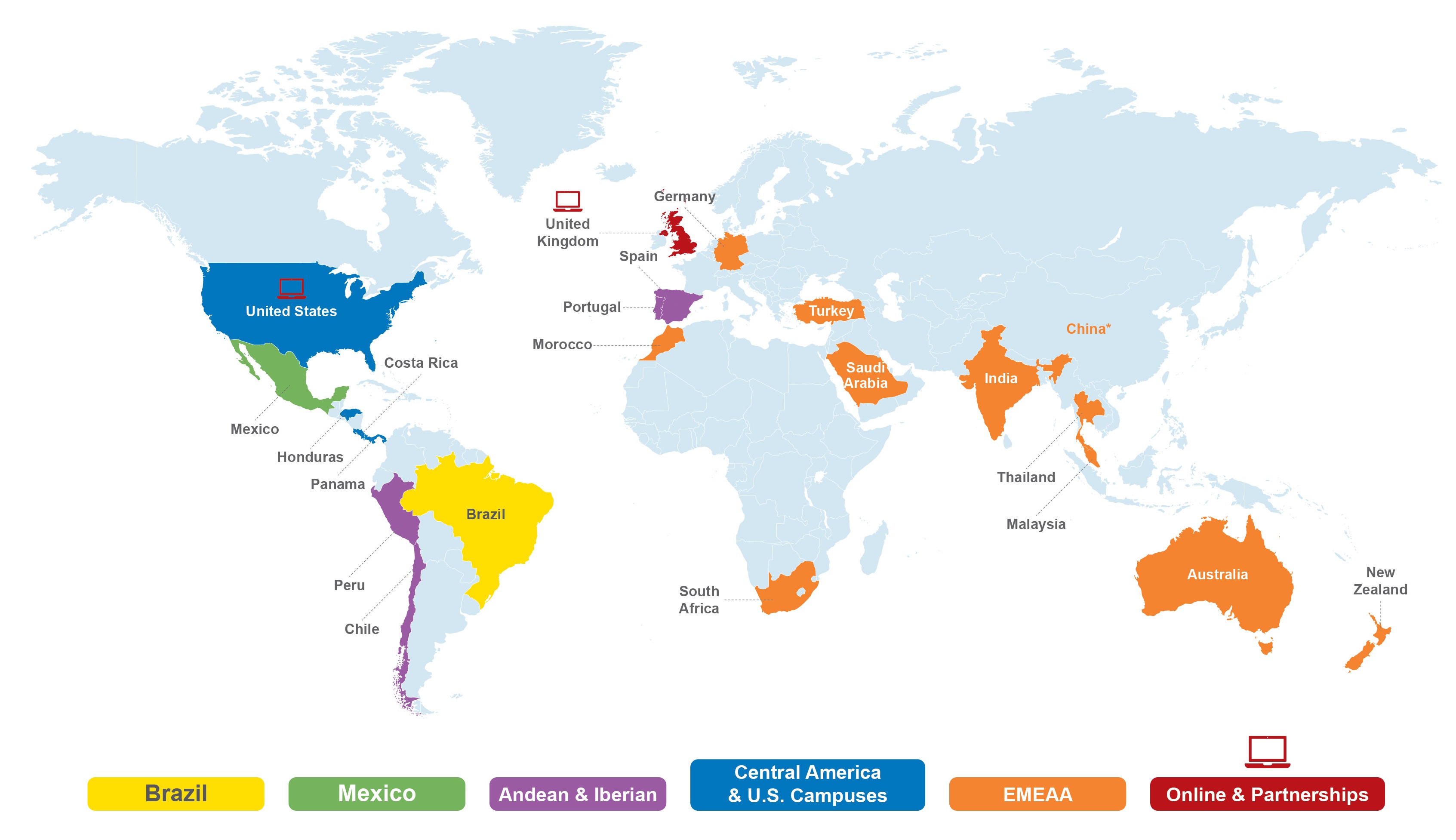

Laureate’s educational services are offered through six operating segments: Brazil, Mexico, Andean & Iberian, Central America & U.S. Campuses, EMEAA and Online & Partnerships. Laureate determines its operating segments based on information utilized by the chief operating decision maker to allocate resources and assess performance. As previously disclosed in our 2017 Form 10-K, effective August 1, 2017, we changed our operating segments in order to realign our segments according to how our chief operating decision maker allocates resources and assesses performance. As required, the segment information presented for comparative purposes for the three months ended March 31, 2017 has been revised to reflect this change.

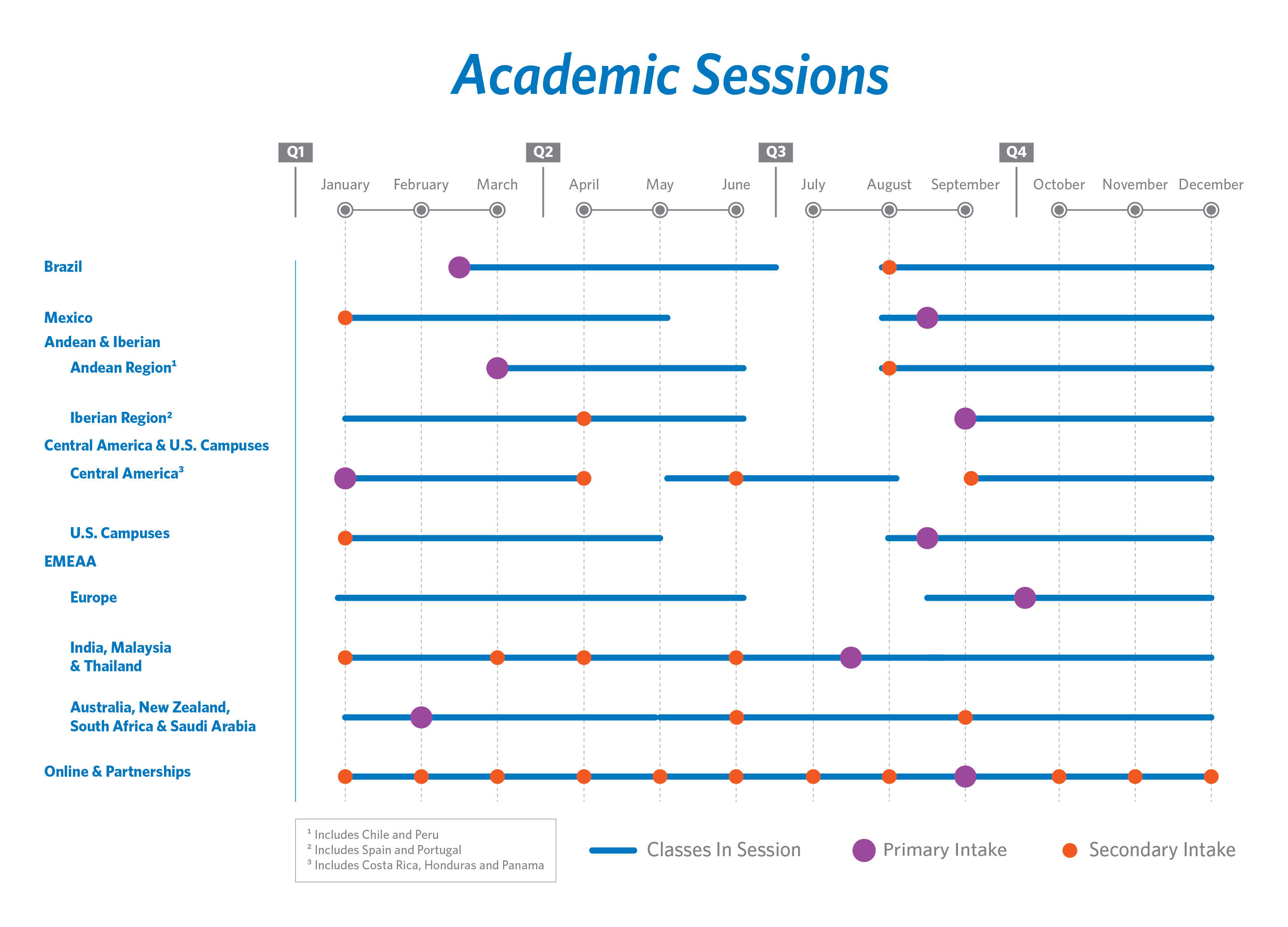

Our campus-based segments generate revenues by providing an education that emphasizes professional-oriented fields of study with undergraduate and graduate degrees in a wide range of disciplines. Our educational offerings are increasingly utilizing online and hybrid (a combination of online and in-classroom) courses and programs to deliver their curriculum. Many of our largest campus-based operations are in developing markets which are experiencing a growing demand for higher education based on favorable demographics and increasing secondary completion rates, driving increases in participation rates and resulting in continued growth in the number of higher education students. Traditional higher education students (defined as 18-24 year olds) have historically been served by public universities, which have limited capacity and are often underfunded, resulting in an inability to meet the growing student demand and employer requirements. This supply and demand imbalance has created a market opportunity for private sector participants. Most students finance their own education. However, there are some government-sponsored student financing programs which are discussed below. These campus-based segments include Brazil, Mexico, Andean & Iberian, Central America & U.S. Campuses and EMEAA. Specifics related to each of these campus-based segments and our Online & Partnerships segment are discussed below:

In Brazil, approximately 75% of post-secondary students are enrolled in private higher education institutions. While the federal government defines the national curricular guidelines, institutions are licensed to operate by city. Laureate owns 13 institutions in eight states throughout Brazil, with a particularly strong presence in the competitive São Paulo market. Many students finance their own education while others rely on the government-sponsored programs such as Prouni and FIES.

17

Public universities in Mexico enroll approximately two thirds of students attending post-secondary education. However, many public institutions are faced with capacity constraints or the quality of the education is considered low. Laureate owns two institutions and is present throughout the country with a footprint of over 40 campuses. Each institution in Mexico has a national license. Students in our Mexican institutions typically finance their own education.

The Andean & Iberian segment includes institutions in Chile, Peru, Portugal and Spain. In Chile, private universities enroll approximately 80% of post-secondary students. In Peru, the public sector plays a significant role but private universities are increasingly providing the capacity to meet growing demand. In Spain and Portugal, the high demand for post-secondary education places capacity constraints on the public sector, pushing students to turn to the private sector for high-quality education. Chile has government-sponsored student financing programs, while in the other countries students generally finance their own education.

The Central America & U.S. Campuses segment includes institutions in Costa Rica, Honduras, Panama and the United States. Students in Central America typically finance their own education while students in the United States finance their education in a variety of ways, including Title IV programs.

As of March 31, 2018, the EMEAA segment included institutions in the European countries of Germany and Turkey, as well as locations in the Middle East, Africa and Asia Pacific consisting of campus-based institutions with operations in Australia, India, Malaysia, Morocco, New Zealand, South Africa and Thailand. Additionally, EMEAA manages nine licensed institutions in the Kingdom of Saudi Arabia and manages one additional institution in China through a joint venture arrangement. As discussed in Note 21, Subsequent Events, we completed the sales of our German and Moroccan operations in April 2018.

The Online & Partnerships segment includes fully online institutions operating globally that offer professionally oriented degree programs in the United States through Walden University, a U.S.-based accredited institution, and through the University of Liverpool and the University of Roehampton in the United Kingdom. These online institutions primarily serve working adults with undergraduate and graduate degree program offerings. Students in the United States finance their education in a variety of ways, including Title IV programs.

Intersegment transactions are accounted for in a similar manner as third-party transactions and are eliminated in consolidation. The Corporate amounts presented in the following tables includes corporate charges that were not allocated to our reportable segments and adjustments to eliminate intersegment items.

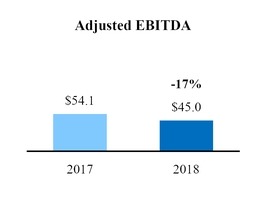

We evaluate segment performance based on Adjusted EBITDA, which is a non-GAAP performance measure defined as Income (loss) from continuing operations before income taxes and equity in net income of affiliates, adding back the following items: Gain on sales of subsidiaries, net, Foreign currency exchange (loss) gain, net, Other income, net, (Loss) gain on derivatives, Loss on debt extinguishment, Interest expense, Interest income, Depreciation and amortization expense, Loss on impairment of assets, Share-based compensation expense and expenses related to our Excellence-in-Process (EiP) initiative. EiP is an enterprise-wide initiative to optimize and standardize Laureate’s processes, creating vertical integration of procurement, information technology, finance, accounting and human resources. It includes the establishment of regional shared services organizations (SSOs) around the world, as well as improvements to the Company's system of internal controls over financial reporting. We have also expanded the EiP initiative into other back- and mid-office areas, as well as certain student-facing activities.

When we review Adjusted EBITDA on a segment basis, we exclude intercompany revenues and expenses, related to network fees and royalties between our segments, which eliminate in consolidation. We use total assets as the measure of assets for reportable segments.

18

The following tables provide financial information for our reportable segments, including a reconciliation of Adjusted EBITDA to Income (loss) from continuing operations before income taxes, as reported in the Consolidated Statements of Operations:

For the three months ended March 31, | 2018 | 2017 | |||||

Revenues | |||||||

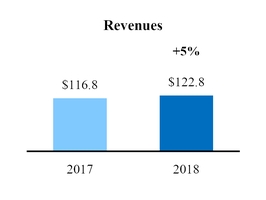

Brazil | $ | 122,792 | $ | 116,833 | |||

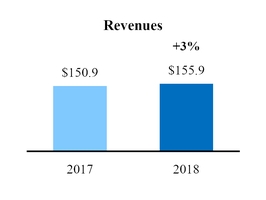

Mexico | 155,899 | 150,859 | |||||

Andean & Iberian | 216,230 | 181,151 | |||||

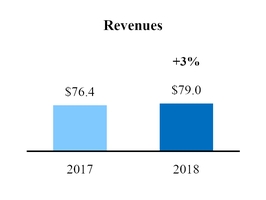

Central America & U.S. Campuses | 79,027 | 76,371 | |||||

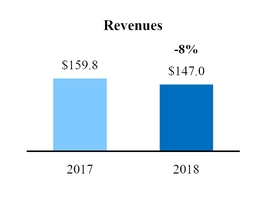

EMEAA | 147,034 | 159,833 | |||||

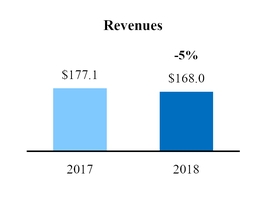

Online & Partnerships | 168,031 | 177,066 | |||||

Corporate | (3,725 | ) | (6,180 | ) | |||

Revenues | $ | 885,288 | $ | 855,933 | |||

Adjusted EBITDA of reportable segments | |||||||

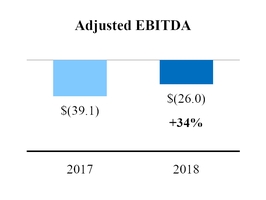

Brazil | $ | (26,016 | ) | $ | (39,125 | ) | |

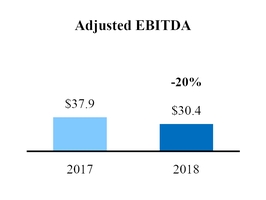

Mexico | 30,443 | 37,874 | |||||

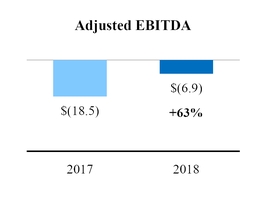

Andean & Iberian | (6,894 | ) | (18,469 | ) | |||

Central America & U.S. Campuses | 17,637 | 17,094 | |||||

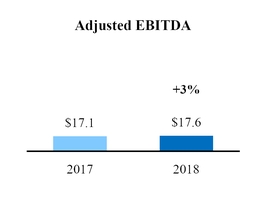

EMEAA | 23,278 | 29,796 | |||||

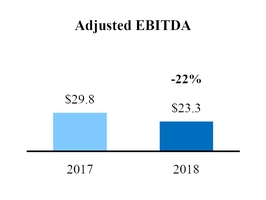

Online & Partnerships | 44,974 | 54,095 | |||||

Total Adjusted EBITDA of reportable segments | 83,422 | 81,265 | |||||

Reconciling items: | |||||||

Corporate | (35,934 | ) | (32,666 | ) | |||

Depreciation and amortization expense | (67,762 | ) | (64,514 | ) | |||

Loss on impairment of assets | — | — | |||||

Share-based compensation expense | 3,756 | (22,388 | ) | ||||

EiP expenses | (10,941 | ) | (24,563 | ) | |||

Operating loss | (27,459 | ) | (62,866 | ) | |||

Interest income | 6,129 | 4,694 | |||||

Interest expense | (69,465 | ) | (102,633 | ) | |||

Loss on debt extinguishment | (7,481 | ) | (1,515 | ) | |||

(Loss) gain on derivatives | (19,340 | ) | 12,147 | ||||

Other income, net | 2,406 | 436 | |||||

Foreign currency exchange (loss) gain, net | (8,754 | ) | 2,290 | ||||

Gain on sales of subsidiaries, net | 298,041 | — | |||||

Income (loss) from continuing operations before income taxes | $ | 174,077 | $ | (147,447 | ) | ||

March 31, 2018 | December 31, 2017 | |||||

Assets | ||||||

Brazil | $ | 1,270,981 | $ | 1,256,364 | ||

Mexico | 1,045,381 | 969,400 | ||||

Andean & Iberian | 2,318,081 | 2,117,317 | ||||

Central America & U.S. Campuses | 366,058 | 376,070 | ||||

EMEAA | 870,789 | 1,022,569 | ||||

Online & Partnerships | 1,280,811 | 1,294,147 | ||||

Corporate | 364,657 | 355,856 | ||||

Total assets | $ | 7,516,758 | $ | 7,391,723 | ||

19

Note 8. Goodwill

The change in the net carrying amount of Goodwill from December 31, 2017 through March 31, 2018 was composed of the following items:

Brazil | Mexico | Andean & Iberian | Central America & U.S. Campuses | EMEAA | Online & Partnerships | Total | |||||||||||||||

Goodwill | $ | 493,373 | $ | 503,373 | $ | 321,762 | $ | 154,759 | $ | 117,413 | $ | 460,740 | $ | 2,051,420 | |||||||

Accumulated impairment loss | — | — | — | (96,754 | ) | — | — | (96,754 | ) | ||||||||||||

Balance at December 31, 2017 | 493,373 | 503,373 | 321,762 | 58,005 | 117,413 | 460,740 | 1,954,666 | ||||||||||||||

Acquisitions | — | — | — | — | — | — | — | ||||||||||||||

Dispositions | — | — | — | — | — | — | — | ||||||||||||||

Reclassification to Long-term assets held for sale | — | — | — | (58,005 | ) | — | — | (58,005 | ) | ||||||||||||

Impairments | — | — | — | — | — | — | — | ||||||||||||||

Currency translation adjustments | (699 | ) | 38,756 | 8,121 | — | (504 | ) | — | 45,674 | ||||||||||||

Adjustments to prior acquisitions | — | — | — | — | — | — | — | ||||||||||||||

Balance at March 31, 2018 | $ | 492,674 | $ | 542,129 | $ | 329,883 | $ | — | $ | 116,909 | $ | 460,740 | $ | 1,942,335 | |||||||

Note 9. Debt

Outstanding long-term debt was as follows:

March 31, 2018 | December 31, 2017 | ||||||

Senior long-term debt: | |||||||

Senior Secured Credit Facility (stated maturity dates April 2022 and April 2024), net of discount | $ | 1,292,452 | $ | 1,625,344 | |||

Senior Notes (stated maturity dates May 2025) | 800,000 | 800,000 | |||||

Total senior long-term debt | 2,092,452 | 2,425,344 | |||||

Other debt: | |||||||

Lines of credit | 60,915 | 55,799 | |||||

Notes payable and other debt | 758,416 | 753,439 | |||||

Total senior and other debt | 2,911,783 | 3,234,582 | |||||

Capital lease obligations and sale-leaseback financings | 172,684 | 234,356 | |||||

Total long-term debt | 3,084,467 | 3,468,938 | |||||

Less: total unamortized deferred financing costs | 100,395 | 107,640 | |||||

Less: current portion of long-term debt | 131,738 | 154,234 | |||||

Long-term debt, less current portion | $ | 2,852,334 | $ | 3,207,064 | |||

$78,289 of long-term debt, including the current portion, is included in the held-for-sale liabilities recorded on the Consolidated Balance Sheet as of March 31, 2018. For further description of the held-for-sale amounts, see Note 4, Assets Held for Sale.

20

Estimated Fair Value of Debt

The estimated fair value of our debt was determined using observable market prices, as the majority of our securities, including the Senior Secured Credit Facility and the Senior Notes due 2025, are traded in a brokered market. The fair value of our remaining debt instruments approximates carrying value based on their terms. As of March 31, 2018 and December 31, 2017, our long-term debt was classified as Level 2 within the fair value hierarchy, based on the frequency and volume of trading in the brokered market. The estimated fair value of our debt was as follows:

March 31, 2018 | December 31, 2017 | ||||||||||||||

Carrying amount | Estimated fair value | Carrying amount | Estimated fair value | ||||||||||||

Total senior and other debt | $ | 2,911,783 | $ | 2,974,383 | $ | 3,234,582 | $ | 3,293,258 | |||||||

Amendment to Senior Secured Credit Facility - 2024 Term Loan

On February 1, 2018, we amended our Senior Secured Credit Facility to reduce the interest rate on our 2024 Term Loan. In connection with this transaction, we also prepaid $350,000 of the principal balance of the 2024 Term Loan in addition to $1,239 of accrued interest using the proceeds from the sale of our Cyprus and Italy operations, along with borrowings on our revolving credit facility that were subsequently repaid with the China sale proceeds. As a result of the $350,000 prepayment, there will be no further quarterly principal payments required and the remaining balance will be due at maturity.

Pursuant to this amendment, the interest rate margins applicable to the 2024 Term Loan were amended to 3.50% for LIBOR term loans and 2.50% for ABR term loans and such interest rate margins will no longer be based upon the Company’s consolidated total debt to consolidated EBITDA ratio. The amendment effectively reduces the current interest rate margins applicable to the outstanding term loans, which prior to the amendment was based on the Company’s consolidated total debt to consolidated EBITDA ratio, by 100 basis points, from 4.50% to 3.50% for LIBOR term loans, and 3.50% to 2.50% for ABR term loans. The amended credit agreement also provides for a prepayment premium with respect to the outstanding term loans. The prepayment premium equals one percent (1%) of the amount of the term loans that are subject to certain repricing transactions occurring on or prior to August 1, 2018.

Certain Covenants

As of March 31, 2018, our senior long-term debt contained certain negative covenants including, among others: (1) limitations on additional indebtedness; (2) limitations on dividends; (3) limitations on asset sales, including the sale of ownership interests in subsidiaries and sale-leaseback transactions; and (4) limitations on liens, guarantees, loans or investments. The Second Amended and Restated Credit Agreement provides, solely with respect to the Revolving Credit Facility, that the Company shall not permit its Consolidated Senior Secured Debt to Consolidated EBITDA ratio, as defined in the Second Amended and Restated Credit Agreement, to exceed 4.50x as of the last day of each quarter ending June 30, 2017 through September 30, 2017, 3.75x as of the last day of each quarter ending December 31, 2017 through March 31, 2018, and 3.50x as of the last day of each quarter ending June 30, 2018 and thereafter. However, the agreement also provides that if (i) the Company’s Consolidated Total Debt to Consolidated EBITDA ratio, as defined in the Second Amended and Restated Credit Agreement, is not greater than 4.75x as of such date and (ii) less than 25% of the Revolving Credit Facility is utilized as of that date, then such financial covenant shall not apply. As of March 31, 2018, these conditions were satisfied and, therefore, we were not subject to the leverage ratio covenant. In addition, notes payable at some of our locations contain financial maintenance covenants.

Note 10. Commitments and Contingencies

Noncontrolling Interest Holder Put Arrangements and Company Call Arrangements

The following section provides a summary table and description of the various noncontrolling interest holder put arrangements that Laureate had outstanding as of March 31, 2018. Laureate has elected to accrete changes in the arrangements’ redemption values over the period from the date of issuance to the earliest redemption date. The redeemable noncontrolling interests are recorded at the greater of the accreted redemption value or the traditional noncontrolling interest. Until the first exercise date, the put instruments’ reported values may be lower than the final amounts that will be required to settle the minority put arrangements. As of March 31, 2018, the carrying value of all noncontrolling interest holder put arrangements was $12,015, which includes accreted incremental value of $12,899 in excess of traditional noncontrolling interests.

21

If the minority put arrangements were all exercised at March 31, 2018, Laureate would be obligated to pay the noncontrolling interest holders an estimated amount of $12,015, as summarized in the following table:

Nominal Currency | First Exercisable Date | Estimated Value as of March 31, 2018 redeemable within 12-months: | Reported Value | ||||||

Noncontrolling interest holder put arrangements | |||||||||

INTI Education Holdings Sdn Bhd (Inti Holdings) - 10.10% | MYR | Current | $ | 9,979 | $ | 9,979 | |||

Pearl Retail Solutions Private Limited (Pearl) - 10% | INR | Current | 1,972 | 1,972 | |||||

Stamford International University (STIU) - Puttable preferred stock of TEDCO | THB | Current | 64 | 64 | |||||

Total noncontrolling interest holder put arrangements | 12,015 | 12,015 | |||||||

Puttable common stock - not currently redeemable | USD | * | — | 2,279 | |||||

Total redeemable noncontrolling interests and equity | $ | 12,015 | $ | 14,294 | |||||

* Contingently redeemable

MYR: Malaysian Ringgit

INR: Indian Rupee

THB: Thai Baht

Laureate’s noncontrolling interest put arrangements are specified in agreements with each noncontrolling interest holder. The terms of these agreements determine the measurement of the redemption value of the put options based on a non-GAAP measure of earnings before interest, taxes, depreciation and amortization (EBITDA, or recurring EBITDA), the definition of which varies for each particular contract.

Commitments and contingencies are generally denominated in foreign currencies.

Series A Convertible Redeemable Preferred Stock

As disclosed in our 2017 Form 10-K, in December 2016 and January 2017, the Company issued an aggregate of 400 shares of convertible redeemable preferred stock (the Series A Preferred Stock) for total gross proceeds of $400,000. The Series A Preferred Stock included a Beneficial Conversion Feature (BCF) that was contingent on a qualified IPO (as defined in the Certificate of Designations governing the terms of the Series A Preferred Stock), which was consummated on February 6, 2017. Accordingly, during the first quarter of 2017, the Company recorded the BCF at its estimated fair value as a reduction of the carrying value of the Series A Preferred Stock and an increase to Additional Paid-In Capital. The accretion of this BCF reduced net income available to common stockholders in the calculation of earnings per share, as shown in Note 16, Earnings (Loss) Per Share. The total BCF of $265,368 was accreted using a constant yield approach over a one-year period. For the three months ended March 31, 2018, we recorded total accretion on the Series A Preferred Stock of $57,324, and paid cash dividends on the Series A Preferred Stock of $9,719. As of March 31, 2018 and December 31, 2017 the Series A Preferred Stock had a carrying value of $447,881 and $400,276, respectively.

The Company and each holder of shares of the Company’s Series A Preferred Stock could elect to convert all of the shares of Series A Preferred Stock into shares of Class A Common Stock one day following the first anniversary of the closing of the Company’s initial public offering, which occurred on February 6, 2017. However, the Company was not permitted to convert any shares of Series A Preferred Stock until there was an effective registration statement available to permit the holders of Series A Preferred Stock to sell the underlying shares of Class A Common Stock. As discussed in Note 21, Subsequent Events, on April 23, 2018, immediately after the Company’s shelf registration statement on Form S-3 became effective, all of the issued and outstanding shares of the Series A Preferred Stock were converted into 36,143 shares of the Company’s Class A common stock, par value $0.004 per share.

Other Loss Contingencies

Laureate is subject to legal actions arising in the ordinary course of its business. In management's opinion, we have adequate legal defenses, insurance coverage and/or accrued liabilities with respect to the eventuality of such actions. We do not believe that any settlement would have a material impact on our Consolidated Financial Statements. Refer to Note 18, Legal and Regulatory Matters, for a discussion of certain matters.

22

Contingent Liabilities for Taxes