Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION BY THE CHIEF EXECUTIVE OFFICER AND THE CHIEF FINANCIAL OFFICER - WPX ENERGY, INC. | exhibit32120180331.htm |

| EX-31.2 - CERTIFICATION BY THE CHIEF FINANCIAL OFFICER - WPX ENERGY, INC. | exhibit31220180331.htm |

| EX-31.1 - CERTIFICATION BY THE CHIEF EXECUTIVE OFFICER - WPX ENERGY, INC. | exhibit31120180331.htm |

| EX-12.1 - COMPUTATION OF RATIO OF EARNINGS TO FIXED CHARGES - WPX ENERGY, INC. | exhibit1220180331.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q |

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2018

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-35322

WPX Energy, Inc. |

(Exact Name of Registrant as Specified in Its Charter) |

Delaware | 45-1836028 | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) | |

3500 One Williams Center, Tulsa, Oklahoma | 74172-0172 | |

(Address of Principal Executive Offices) | (Zip Code) | |

855-979-2012

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.01 par value | New York Stock Exchange | |

6.25% Series A Mandatory Convertible Preferred Stock, $0.01 par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | þ | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Emerging growth company | ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The number of shares outstanding of the registrant’s common stock at May 2, 2018 were 399,625,264.

WPX Energy, Inc.

Index

Page | |||

Part I. | Financial Information | ||

Item 1. | Financial Statements (Unaudited) | ||

Consolidated Balance Sheets as of March 31, 2018 and December 31, 2017 | |||

Consolidated Statements of Operations for the three months ended March 31, 2018 and 2017 | |||

Consolidated Statements of Changes in Equity for the three months ended March 31, 2018 | |||

Consolidated Statements of Cash Flows for the three months ended March 31, 2018 and 2017 | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Part II. | Other Information | ||

Item 1. | |||

Item 1A. | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Item 5. | |||

Item 6. | |||

Certain matters contained in this report include forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. These forward-looking statements relate to anticipated financial performance, management’s plans and objectives for future operations, business prospects, outcome of regulatory proceedings, market conditions and other matters.

All statements, other than statements of historical facts, included in this report that address activities, events or developments that we expect, believe or anticipate will exist or may occur in the future, are forward-looking statements. Forward-looking statements can be identified by various forms of words such as “anticipates,” “believes,” “seeks,” “could,” “may,” “should,” “continues,” “estimates,” “expects,” “forecasts,” “intends,” “might,” “goals,” “objectives,” “targets,” “planned,” “potential,” “projects,” “scheduled,” “will” or other similar expressions. These forward-looking statements are based on management’s beliefs and assumptions and on information currently available to management and include, among others, statements regarding:

• | amounts and nature of future capital expenditures; |

• | expansion and growth of our business and operations; |

• | financial condition and liquidity; |

• | business strategy; |

• | estimates of proved oil and natural gas reserves; |

• | reserve potential; |

• | development drilling potential; |

• | cash flow from operations or results of operations; |

• | acquisitions or divestitures; |

• | seasonality of our business; and |

• | crude oil, natural gas and NGL prices and demand. |

2

Forward-looking statements are based on numerous assumptions, uncertainties and risks that could cause future events or results to be materially different from those stated or implied in this report. Many of the factors that will determine these results are beyond our ability to control or predict. Specific factors that could cause actual results to differ from results contemplated by the forward-looking statements include, among others, the following:

• | availability of supplies (including the uncertainties inherent in assessing, estimating, acquiring and developing future oil and natural gas reserves), market demand, volatility of prices and the availability and cost of capital; |

• | inflation, interest rates, fluctuation in foreign exchange and general economic conditions (including future disruptions and volatility in the global credit markets and the impact of these events on our customers and suppliers); |

• | the strength and financial resources of our competitors; |

• | development of alternative energy sources; |

• | the impact of operational and development hazards; |

• | costs of, changes in, or the results of laws, government regulations (including climate change regulation and/or potential additional regulation of drilling and completion of wells), environmental liabilities, litigation and rate proceedings; |

• | changes in maintenance and construction costs; |

• | changes in the current geopolitical situation; |

• | our exposure to the credit risk of our customers; |

• | risks related to strategy and financing, including restrictions stemming from our debt agreements, future changes in our credit ratings and the availability and cost of credit; |

• | risks associated with future weather conditions; |

• | acts of terrorism; |

• | other factors described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”; and |

• | additional risks described in our filings with the Securities and Exchange Commission (“SEC”). |

All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements set forth above. Given the uncertainties and risk factors that could cause our actual results to differ materially from those contained in any forward-looking statement, we caution investors not to unduly rely on our forward-looking statements. Forward-looking statements speak only as of the date they are made. We disclaim any obligation to and do not intend to update the above list or to announce publicly the result of any revisions to any of the forward-looking statements to reflect future events or developments, except to the extent required by applicable laws. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements.

In addition to causing our actual results to differ, the factors listed above and referred to below may cause our intentions to change from those statements of intention set forth in this report. Such changes in our intentions may also cause our results to differ. We may change our intentions, at any time and without notice, based upon changes in such factors, our assumptions or otherwise.

Because forward-looking statements involve risks and uncertainties, we caution that there are important factors, in addition to those listed above, that may cause actual results to differ materially from those contained in the forward-looking statements. For a detailed discussion of those factors, see Part I, Item 1A. Risk Factors in our Annual Report on Form 10-K for the year ended December 31, 2017.

3

WPX Energy, Inc.

Consolidated Balance Sheets

(Unaudited)

March 31, 2018 | December 31, 2017 | ||||||

(Millions) | |||||||

Assets | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 681 | $ | 189 | |||

Accounts receivable, net of allowance of $2 million as of March 31, 2018 and December 31, 2017 | 337 | 307 | |||||

Derivative assets | 82 | 36 | |||||

Inventories | 31 | 30 | |||||

Assets classified as held for sale (Note 2) | — | 811 | |||||

Other | 30 | 28 | |||||

Total current assets | 1,161 | 1,401 | |||||

Investments | 85 | 70 | |||||

Properties and equipment (successful efforts method of accounting) | 8,964 | 8,674 | |||||

Less—accumulated depreciation, depletion and amortization | (2,148 | ) | (1,983 | ) | |||

Properties and equipment, net | 6,816 | 6,691 | |||||

Derivative assets | 43 | 23 | |||||

Other noncurrent assets | 22 | 22 | |||||

Total assets | $ | 8,127 | $ | 8,207 | |||

Liabilities and Equity | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 522 | $ | 446 | |||

Accrued and other current liabilities | 161 | 209 | |||||

Liabilities associated with assets held for sale (Note 2) | — | 20 | |||||

Derivative liabilities | 242 | 171 | |||||

Total current liabilities | 925 | 846 | |||||

Deferred income taxes | 74 | 117 | |||||

Long-term debt, net | 2,576 | 2,575 | |||||

Derivative liabilities | 74 | 65 | |||||

Asset retirement obligations | 33 | 32 | |||||

Other noncurrent liabilities | 439 | 445 | |||||

Contingent liabilities and commitments (Note 8) | |||||||

Equity: | |||||||

Stockholders’ equity: | |||||||

Preferred stock (100 million shares authorized at $0.01 par value; 4.8 million shares outstanding at March 31, 2018 and December 31, 2017) | 232 | 232 | |||||

Common stock (2 billion shares authorized at $0.01 par value; 399.7 million and 398.3 million shares issued and outstanding at March 31, 2018 and December 31, 2017) | 4 | 4 | |||||

Additional paid-in-capital | 7,473 | 7,479 | |||||

Accumulated deficit | (3,703 | ) | (3,588 | ) | |||

Total stockholders’ equity | 4,006 | 4,127 | |||||

Total liabilities and equity | $ | 8,127 | $ | 8,207 | |||

4

WPX Energy, Inc.

Consolidated Statements of Operations

(Unaudited)

Three months ended March 31, | |||||||

2018 | 2017 | ||||||

Revenues: | (Millions, except per-share amounts) | ||||||

Product revenues: | |||||||

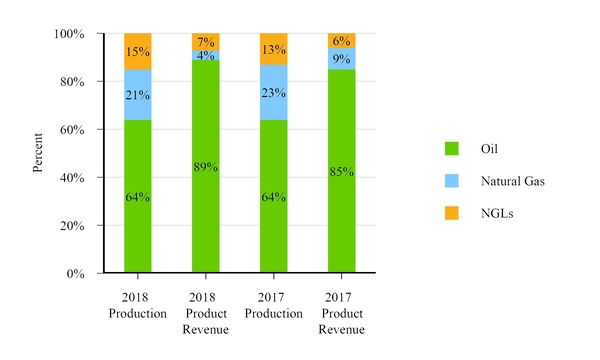

Oil sales | $ | 360 | $ | 159 | |||

Natural gas sales | 17 | 17 | |||||

Natural gas liquid sales | 30 | 11 | |||||

Total product revenues | 407 | 187 | |||||

Net gain (loss) on derivatives | (69 | ) | 203 | ||||

Commodity management | 36 | 5 | |||||

Total revenues | 374 | 395 | |||||

Costs and expenses: | |||||||

Depreciation, depletion and amortization | 161 | 113 | |||||

Lease and facility operating | 55 | 36 | |||||

Gathering, processing and transportation | 18 | 5 | |||||

Taxes other than income | 30 | 13 | |||||

Exploration (Note 4) | 19 | 36 | |||||

General and administrative (including equity-based compensation of $7 million for both periods) | 43 | 41 | |||||

Commodity management | 39 | 5 | |||||

Net (gain) loss on sales of assets (Note 4) | 1 | (31 | ) | ||||

Other—net | 2 | 4 | |||||

Total costs and expenses | 368 | 222 | |||||

Operating income | 6 | 173 | |||||

Interest expense | (46 | ) | (47 | ) | |||

Investment income and other | (1 | ) | 2 | ||||

Income (loss) from continuing operations before income taxes | (41 | ) | 128 | ||||

Provision (benefit) for income taxes | (15 | ) | 33 | ||||

Income (loss) from continuing operations | (26 | ) | 95 | ||||

Loss from discontinued operations | (89 | ) | (3 | ) | |||

Net income (loss) | (115 | ) | 92 | ||||

Less: Dividends on preferred stock | 4 | 4 | |||||

Net income (loss) available to WPX Energy, Inc. common stockholders | $ | (119 | ) | $ | 88 | ||

Amounts available to WPX Energy, Inc. common stockholders: | |||||||

Income (loss) from continuing operations | $ | (30 | ) | $ | 91 | ||

Loss from discontinued operations | (89 | ) | (3 | ) | |||

Net income (loss) | $ | (119 | ) | $ | 88 | ||

Basic earnings (loss) per common share: | |||||||

Income (loss) from continuing operations | $ | (0.07 | ) | $ | 0.24 | ||

Loss from discontinued operations | (0.23 | ) | (0.01 | ) | |||

Net income (loss) | $ | (0.30 | ) | $ | 0.23 | ||

Basic weighted-average shares | 398.6 | 386.3 | |||||

Diluted earnings (loss) per common share: | |||||||

Income (loss) from continuing operations | $ | (0.07 | ) | $ | 0.23 | ||

Loss from discontinued operations | (0.23 | ) | (0.01 | ) | |||

Net income (loss) | $ | (0.30 | ) | $ | 0.22 | ||

Diluted weighted-average shares | 398.6 | 410.4 | |||||

5

WPX Energy, Inc.

Consolidated Statements of Changes in Equity

(Unaudited)

WPX Energy, Inc., Stockholders | |||||||||||||||||||

Preferred Stock | Common Stock | Additional Paid-In- Capital | Accumulated Deficit | Total Stockholders’ Equity | |||||||||||||||

Balance at December 31, 2017 | $ | 232 | $ | 4 | $ | 7,479 | $ | (3,588 | ) | $ | 4,127 | ||||||||

Net loss | — | — | — | (115 | ) | (115 | ) | ||||||||||||

Stock-based compensation, net of tax impact | — | — | (2 | ) | — | (2 | ) | ||||||||||||

Dividends on preferred stock | — | — | (4 | ) | — | (4 | ) | ||||||||||||

Balance at March 31, 2018 | $ | 232 | $ | 4 | $ | 7,473 | $ | (3,703 | ) | $ | 4,006 | ||||||||

See accompanying notes.

6

WPX Energy, Inc.

Consolidated Statements of Cash Flows

(Unaudited)

Three months ended March 31, | |||||||

2018 | 2017 | ||||||

Operating Activities(a) | (Millions) | ||||||

Net income (loss) | $ | (115 | ) | $ | 92 | ||

Adjustments to reconcile net income (loss) to net cash provided by operating activities: | |||||||

Depreciation, depletion and amortization | 168 | 147 | |||||

Deferred income tax provision (benefit) | (43 | ) | 30 | ||||

Provision for impairment of properties and equipment (including certain exploration expenses) | 20 | 38 | |||||

Net (gain) loss on derivatives | 69 | (203 | ) | ||||

Net settlements related to derivatives | (55 | ) | (5 | ) | |||

Amortization of stock-based awards | 8 | 7 | |||||

Net (gain) loss on sales of assets including discontinued operations | 151 | (35 | ) | ||||

Cash provided (used) by operating assets and liabilities: | |||||||

Accounts receivable | (21 | ) | (14 | ) | |||

Inventories | (8 | ) | 2 | ||||

Other current assets | 6 | 2 | |||||

Accounts payable | 28 | 29 | |||||

Federal income taxes receivable | — | 12 | |||||

Accrued and other current liabilities | (48 | ) | (76 | ) | |||

Payments on liabilities accrued in prior years for retained transportation and gathering contracts related to discontinued operations | (10 | ) | (11 | ) | |||

Other, including changes in other noncurrent assets and liabilities | (5 | ) | 7 | ||||

Net cash provided by operating activities(a) | 145 | 22 | |||||

Investing Activities(a) | |||||||

Capital expenditures(b) | (321 | ) | (237 | ) | |||

Proceeds from sales of assets | 699 | 8 | |||||

Purchase of a business | — | (802 | ) | ||||

Purchase of investments | (16 | ) | — | ||||

Net cash provided by (used in) investing activities(a) | 362 | (1,031 | ) | ||||

Financing Activities | |||||||

Proceeds from common stock | 1 | 671 | |||||

Dividends paid on preferred stock | (4 | ) | (4 | ) | |||

Borrowings on credit facility | 138 | — | |||||

Payments on credit facility | (138 | ) | — | ||||

Taxes paid for shares withheld | (11 | ) | (10 | ) | |||

Net cash provided by (used in) financing activities | (14 | ) | 657 | ||||

Net increase (decrease) in cash and cash equivalents and restricted cash | 493 | (352 | ) | ||||

Cash and cash equivalents and restricted cash at beginning of period | 201 | 506 | |||||

Cash and cash equivalents and restricted cash at end of period | $ | 694 | $ | 154 | |||

__________ | |||||||

(a) Amounts reflect continuing and discontinued operations unless otherwise noted. See Note 2 of Notes to Consolidated Financial Statements for discussion of discontinued operations. | |||||||

(b) Increase to properties and equipment | $ | (349 | ) | $ | (280 | ) | |

Changes in related accounts payable and accounts receivable | 28 | 43 | |||||

Capital expenditures | $ | (321 | ) | $ | (237 | ) | |

See accompanying notes.

7

WPX Energy, Inc.

Notes to Consolidated Financial Statements

Note 1. Description of Business and Basis of Presentation

Description of Business

Operations of our company include oil, natural gas and NGL development and production primarily located in Texas, New Mexico and North Dakota. We specialize in development and production from tight-sands and shale formations in the Delaware and Williston Basins. Associated with our commodity production are sales and marketing activities, referred to as commodity management activities, that include oil and natural gas purchased from third-party working interest owners in operated wells and the management of various commodity contracts, such as transportation and related derivatives.

In March 2018, we sold our properties in the San Juan Basin’s Gallup oil play (“San Juan Gallup”) and in December 2017, we sold our natural gas-producing properties in the San Juan Basin (“San Juan Legacy”). Collectively, the San Juan Gallup and San Juan Legacy comprised our San Juan Basin operations. Subsequent to the closing of these transactions, we no longer have operations in the San Juan Basin. As a result of these divestments, the results of operations of the San Juan Basin have been reclassified as discontinued operations on the Consolidated Statements of Operations. See Note 2 for additional information on these transactions.

In addition, we have sold other operations which are reported as discontinued operations and are discussed in Note 2 of Notes to Consolidated Financial Statements.

The consolidated businesses represented herein as WPX Energy, Inc. is also referred to as “WPX,” the “Company,” “we,” “us” or “our.”

Basis of Presentation

The accompanying interim consolidated financial statements do not include all the notes included in our annual financial statements and, therefore, should be read in conjunction with the consolidated financial statements and notes thereto for the year ended December 31, 2017 in the Company’s Annual Report on Form 10-K. The accompanying interim consolidated financial statements include all normal recurring adjustments that, in the opinion of management, are necessary to present fairly our financial position at March 31, 2018, results of operations for the three months ended March 31, 2018 and 2017, changes in equity for the three months ended March 31, 2018 and cash flows for the three months ended March 31, 2018 and 2017. The Company has no elements of comprehensive income (loss) other than net income (loss).

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results could differ from those estimates.

Our continuing operations comprise a single business segment, which includes the development, production and commodity management activities of oil, natural gas and NGLs in the United States.

Discontinued Operations

See Note 2 for a discussion of discontinued operations. Unless indicated otherwise, the information in the Notes to Consolidated Financial Statements relates to continuing operations.

Recently Adopted Accounting Standards

The company adopted Accounting Standards Update (“ASU”) 2014-09, Revenue from Contracts with Customers, effective January 1, 2018 using the modified retrospective method. The core principle of the guidance in ASU 2014-09 is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The adoption of ASU 2014-09 was not material to our revenues or operating income (loss) or to our consolidated balance sheet because our performance obligations, which determine when and how revenue is recognized, are not materially changed under the new standard; thus, revenue associated with the majority of our contracts will continue to be recognized as control of products is transferred to the customer. We incorporated any new disclosure requirements into our 2017 Form 10-K. See Note 1 of our Annual Report on Form 10-K for additional discussion related to revenue accounting policies and disclosures. In addition, see Note 16 of our Form 10-K for receivables related to sales of oil, natural gas and related products and services. The composition of our receivables as of March 31, 2018 has not changed significantly as compared to December 31, 2017.

We adopted ASU 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash, effective January 1, 2018 which requires entities to show the changes in the total of cash, cash equivalents, restricted cash and restricted cash equivalents in the statement of cash flows on a retrospective basis. The requirements of this standard are reflected on our Consolidated Statement

8

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

of Cash Flows, including prior periods. Restricted cash was approximately $13 million and $12 million as of March 31, 2018 and December 31, 2017, respectively.

We adopted ASU 2017-01, Business Combinations, clarifying the definition of a business to assist entities with evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses effective January 1, 2018.

We adopted ASU 2017-09, Compensation - Stock Compensation (Topic 718), effective January 1, 2018. This ASU provides guidance about which changes to the terms or conditions of a share-based payment award require an entity to apply modification accounting in Topic 718. The adoption of this standard did not have a significant impact on our consolidated financial statements.

Accounting Standards Not Yet Adopted

In February 2016, the Financial Accounting Standards Board (“FASB”) issued ASU 2016-02, Leases, to increase transparency and comparability among organizations by recognizing right-of-use assets and lease payment liabilities on the balance sheet and disclosing key information about leasing arrangements. Under ASU 2016-02, a determination is to be made at the inception of a contract as to whether the contract is, or contains, a lease. Leases convey the right to control the use of an identified asset in exchange for consideration. Only the lease components of a contract must be accounted for in accordance with this ASU. Non-lease components, such as activities that transfer a good or service to the customer, shall be accounted for under other applicable Topics. ASU 2016-02 permits lessees to make policy elections to not recognize lease assets and liabilities for leases with terms of less than twelve months and/or to not separate lease and non-lease components and account for the non-lease components together with the lease components as a single lease component. Based on an initial review of the new guidance and the Company’s current commitments, the Company anticipates it may be required to recognize right-of-use assets and lease payment liabilities related to certain drilling rig commitments, certain equipment leases, and potentially other arrangements, the effects of which cannot be estimated at this time. We are in the process of identifying leases and have engaged a third party to assist with implementing the standard. In 2018 and 2019, we will implement appropriate changes to our business processes, systems or controls to support recognition and disclosure under the new standard. Our findings and progress toward implementation of the standard are periodically reported to management. ASU 2016-02 is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. Early adoption is permitted for any entity in any interim or annual period. The Company continues to evaluate the impact of ASU 2016-02 to the Company’s Consolidated Financial Statements or related disclosures.

In August 2017, the FASB issued ASU 2017-12, Derivatives and Hedging (Topic 815). This ASU provides guidance for various components of hedge accounting including hedge ineffectiveness, the expansion of types of permissible hedging strategies, reduced complexity in the application of the long-haul method for fair value hedges and reduced complexity in assessment of effectiveness. The amendments in this Update are effective for public entities for annual periods, and interim periods within those annual periods, beginning after December 15, 2018. Early adoption is permitted, including adoption in any interim period. The Company does not expect any significant impact on its consolidated financial statements from the adoption of this standard unless we apply hedge accounting in a future period.

Note 2. Discontinued Operations

On January 30, 2018, we signed an agreement to sell our properties in the San Juan Gallup oil play to Enduring Resources IV, LLC (“Enduring”) for $700 million (subject to closing and post-closing adjustments). The transaction closed on March 28, 2018 and we received approximately $667 million (subject to post-closing adjustments). In addition, the purchaser will assume approximately $309 million of gathering and processing commitments; however, WPX has left in place a performance guarantee with respect to these commitments. We believe that any future performance under this guarantee obligation is highly unlikely given our understanding of the buyer’s credit position, the indemnity arrangement between the Company and Enduring and the declining size of the obligations subject to the guarantee over time. Although we believe the probability of performance by WPX is low, we must determine the fair value of the guarantee that was provided. We estimated the fair value of the guarantee to be approximately $9 million based on the factors mentioned above along with projections of estimated future volume throughputs and risk adjusted discount rates, all of which are Level 3 inputs. This amount is included in our calculation of the loss on sale. We recorded a total loss on the sale of $147 million in first quarter 2018. The operations in the San Juan Gallup represented 12 percent of our total proved reserves at December 31, 2017 and 16 percent of our total production for 2017.

As previously noted, we sold our San Juan Legacy properties in December 2017. As a result of the dispositions of San Juan Gallup and San Juan Legacy properties, we no longer have operations in the San Juan Basin. Our discontinued operations consist of the previously owned properties in the San Juan Basin and accretion on certain transportation and gathering obligations retained and recognized in prior years related to the sale of Powder River properties.

9

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Summarized Results of Discontinued Operations

The following table presents the results of our discontinued operations for the periods presented.

Three months ended March 31, | |||||||

2018 | 2017 | ||||||

(Millions) | |||||||

Total revenues | $ | 76 | $ | 66 | |||

Costs and expenses: | |||||||

Depreciation, depletion and amortization | $ | 8 | $ | 34 | |||

Lease and facility operating | 7 | 12 | |||||

Gathering, processing and transportation | 12 | 16 | |||||

Taxes other than income | 6 | 6 | |||||

General and administrative | 1 | 2 | |||||

Exploration | 3 | 3 | |||||

(Gain) loss on sales of assets | — | (4 | ) | ||||

Accretion for transportation and gathering obligations retained | 2 | 2 | |||||

Other—net | 4 | 1 | |||||

Total costs and expenses | 43 | 72 | |||||

Operating income (loss) | 33 | (6 | ) | ||||

Loss on sale of assets | (149 | ) | — | ||||

Loss from discontinued operations before income taxes | (116 | ) | (6 | ) | |||

Income tax benefit | (27 | ) | (3 | ) | |||

Loss from discontinued operations | $ | (89 | ) | $ | (3 | ) | |

Assets and Liabilities in the Consolidated Balance Sheets attributable to Discontinued Operations

The following table presents assets classified as held for sale and liabilities associated with assets held for sale related to our San Juan Basin operations.

December 31, | |||

2017 | |||

(Millions) | |||

Assets classified as held for sale | |||

Inventories | $ | 14 | |

Properties and equipment, net (successful efforts method of accounting) | 797 | ||

Total assets classified as held for sale on the Consolidated Balance Sheets | $ | 811 | |

Liabilities associated with assets held for sale | |||

Current liabilities: | |||

Accounts payable | $ | 1 | |

Accrued and other current liabilities | 1 | ||

Total current liabilities | 2 | ||

Asset retirement obligations | 15 | ||

Other noncurrent liabilities | 3 | ||

Total liabilities associated with assets held for sale on the Consolidated Balance Sheets | $ | 20 | |

10

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Cash Flows Attributable to Discontinued Operations

In addition to the amounts presented below, cash outflows related to previous accruals for the Powder River Basin gathering and transportation contracts retained by WPX were $10 million and $11 million for the three months ended March 31, 2018 and 2017, respectively.

Three months Ended March 31, | |||||||

2018 | 2017 | ||||||

(Millions) | |||||||

Cash provided by operating activities(a) | $ | 46 | $ | 29 | |||

Capital expenditures within investing activities | $ | 26 | $ | 23 | |||

__________

(a) Excluding income taxes and changes in working capital items.

Note 3. Earnings (Loss) Per Common Share from Continuing Operations

The following table summarizes the calculation of earnings per share.

Three months ended March 31, | |||||||

2018 | 2017 | ||||||

(Millions, except per-share amounts) | |||||||

Income (loss) from continuing operations | $ | (26 | ) | $ | 95 | ||

Less: Dividends on preferred stock | 4 | 4 | |||||

Income (loss) from continuing operations available to WPX Energy, Inc. common stockholders for basic and diluted earnings (loss) per common share | $ | (30 | ) | $ | 91 | ||

Basic weighted-average shares | 398.6 | 386.3 | |||||

Effect of dilutive securities(a): | |||||||

Nonvested restricted stock units and awards | — | 4.1 | |||||

Stock options | — | 0.2 | |||||

Common shares issuable upon assumed conversion of 6.25% Series A mandatory convertible preferred stock | — | 19.8 | |||||

Diluted weighted-average shares | 398.6 | 410.4 | |||||

Earnings (loss) per common share from continuing operations: | |||||||

Basic | $ | (0.07 | ) | $ | 0.24 | ||

Diluted | $ | (0.07 | ) | $ | 0.23 | ||

__________

(a) The following table includes amounts that have been excluded from the computation of diluted earnings (loss) per common share as their inclusion would be antidilutive due to our loss from continuing operations attributable to WPX Energy, Inc. available to common stockholders.

Three months ended March 31, | ||

2018 | ||

(Millions) | ||

Weighted-average nonvested restricted stock units and awards | 3.1 | |

Weighted-average stock options | 0.2 | |

Common shares issuable upon assumed conversion of 6.25% Series A mandatory convertible preferred stock | 19.8 | |

11

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

The table below includes information related to stock options that were outstanding at March 31, 2018 and 2017 but have been excluded from the computation of weighted-average stock options due to the option exercise price exceeding the first quarter weighted-average market price of our common shares.

March 31, | |||||||

2018 | 2017 | ||||||

Options excluded (millions) | 1.0 | 1.6 | |||||

Weighted-average exercise price of options excluded | $ | 17.90 | $ | 17.81 | |||

Exercise price range of options excluded | $16.46 - $21.81 | $14.41 - $21.81 | |||||

First quarter weighted-average market price | $ | 14.41 | $ | 13.35 | |||

The diluted weighted-average shares excludes the effect of approximately 0.7 million and 0.6 million nonvested restricted stock units for the three months ended March 31, 2018 and 2017, respectively. These restricted stock units were antidilutive under the treasury stock method.

Note 4. Asset Sales and Exploration Expenses

Asset Sales

Net gain on sales of assets for the three months ended March 31, 2017 primarily relates to a gain from an exchange of leasehold acreage in the Permian Basin.

In conjunction with exchanges of leasehold, we estimate the fair value of the leasehold through discounted cash flow models and consideration of market data. Our estimates and assumptions include future commodity prices, projection of estimated quantities of oil and natural gas reserves, expectations for future development and operating costs and risk adjusted discount rates, all of which are Level 3 inputs.

Exploration Expenses

The following table presents a summary of exploration expenses.

Three months ended March 31, | |||||||

2018 | 2017 | ||||||

(Millions) | |||||||

Unproved leasehold property impairment, amortization and expiration | $ | 17 | $ | 35 | |||

Geologic and geophysical costs | 2 | 1 | |||||

Total exploration expenses | $ | 19 | $ | 36 | |||

Unproved leasehold property impairment, amortization and expiration in 2017 includes costs in excess of the accumulated amortization balance associated with certain leases in the Permian Basin that expired during the first quarter of 2017. These leases were renewed in second-quarter 2017.

Note 5. Inventories

The following table presents a summary of our inventories as of the dates indicated below.

March 31, 2018 | December 31, 2017 | ||||||

(Millions) | |||||||

Material, supplies and other | $ | 30 | $ | 29 | |||

Crude oil production in transit | 1 | 1 | |||||

Total inventories | $ | 31 | $ | 30 | |||

12

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Note 6. Debt and Banking Arrangements

The following table presents a summary of our debt as of the dates indicated below.

March 31, 2018 | December 31, 2017 | ||||||

(Millions) | |||||||

Credit facility agreement | $ | — | $ | — | |||

7.500% Senior Notes due 2020 | 350 | 350 | |||||

6.000% Senior Notes due 2022 | 1,100 | 1,100 | |||||

8.250% Senior Notes due 2023 | 500 | 500 | |||||

5.250% Senior Notes due 2024 | 650 | 650 | |||||

Total long-term debt | $ | 2,600 | $ | 2,600 | |||

Less: Debt issuance costs on long-term debt(a) | 24 | 25 | |||||

Total long-term debt, net(a) | $ | 2,576 | $ | 2,575 | |||

__________

(a) Debt issuance costs related to our Credit Facility are recorded in other noncurrent assets on the Consolidated Balance Sheets.

Credit Facility

As of March 31, 2018, our $1.2 billion senior secured revolving credit facility (“Credit Facility”) had a maturity date of October 28, 2019. As of March 31, 2018, we had no borrowings outstanding, $70 million of letters of credit issued under the Credit Facility and we were in compliance with our financial covenants with full access to the Credit Facility.

On April 17, 2018, the Company entered into a Second Amendment to Second Amended and Restated Credit Agreement with Wells Fargo Bank, National Association, as Administrative Agent, Lender and Swingline Lender and the other lenders party thereto (the “Credit Facility”). The Credit Facility, as amended, increases total commitments to $1.5 billion, increases the Borrowing Base to $1.8 billion, and extends the maturity date to April 17, 2023, subject to a springing maturity on October 15, 2021 if available liquidity minus outstanding 2022 notes is less than $500 million. Based on our current credit ratings, a Collateral Trigger Period applies which makes the Credit Facility subject to certain financial covenants and a Borrowing Base as described below. The Credit Facility may be used for working capital, acquisitions, capital expenditures and other general corporate purposes. The financial covenants in the Credit Facility may limit our ability to borrow money, depending on the applicable financial metrics at any given time.

Borrowing Base. During a Collateral Trigger Period, loans under the Credit Facility are subject to a Borrowing Base as calculated in accordance with the provisions of the Credit Facility. The $1.8 billion Borrowing Base will remain in effect until the next Redetermination Date as set forth in the Credit Facility and at this time, availability under the Credit Facility Agreement is limited by the total commitments of $1.5 billion. The Borrowing Base is recalculated at least every six months per the terms of the Credit Facility.

Terms and Conditions. The Credit Facility will initially be guaranteed by certain subsidiaries of the Company (excluding subsidiaries holding Midstream Assets and subsidiaries meeting other customary exclusion criteria), as Guarantors, and secured by substantially all of the Company’s and the Guarantors’ assets (including oil and gas properties), subject to customary exceptions and carve outs (which shall also exclude Midstream Assets and the equity interests of subsidiaries holding Midstream Assets). Such obligations shall terminate on the earlier of any applicable Collateral Trigger Termination Date (as described below) or the date on which all liens held by the Administrative Agent for the benefit of the secured parties are released pursuant to the terms of the Credit Facility.

The Collateral Trigger Termination Date is the first date following the date of the closing of the Credit Facility and the first date following any Collateral Trigger Date, as applicable, on which (i) the Company’s Corporate Rating is BBB- or better by S&P (without negative outlook or negative watch) or (ii) Baa3 or better by Moody’s (without negative outlook or negative watch), provided that the other of the two Corporate Ratings is at least BB+ by S&P or Ba1 by Moody’s.

Interest and Commitment Fees. Interest on borrowings under the Credit Facility is payable at rates per annum equal to, at the Company’s option: (1) a fluctuating base rate equal to the alternate base rate plus the applicable margin, or (2) a periodic fixed rate equal to LIBOR plus the applicable margin. The alternate base rate will be the highest of (i) the federal funds rate plus 0.5 percent, (ii) the Prime Rate, and (iii) one-month LIBOR plus 1.0 percent. As amended and during a Collateral Trigger Period, the applicable margin ranges from 0.25% to 1.25% per annum in the case of the alternate base rate, and from 1.25% to 2.25% per annum in the case of LIBOR. The Company is required to pay a commitment fee based on the unused portion of the commitments under the Credit Facility. As amended and during a Collateral Trigger Period, the commitment fee ranges from

13

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

0.375% to 0.500% per annum. The applicable margin and the commitment fees during a Collateral Trigger Period are determined by reference to a utilization percentage as set forth in the Credit Facility. The applicable margin and the commitment fee other than during a Collateral Trigger Period are determined by reference to the Company’s senior unsecured debt ratings.

Significant Financial Covenants.

Pursuant to the amendment, the Company is required to maintain:

• | a ratio of Net Indebtedness to Consolidated EBITDAX for the most recent ended four consecutive fiscal quarters (excluding the first three quarters of 2018 which will use an Annualized Consolidated EBITDAX) of not greater than 4.25 to 1.00 as of the last day of the most recently ended Rolling Period; and |

• | a ratio of consolidated current assets (including the unused amount of the Aggregate Commitments) of the Company and its consolidated subsidiaries to the consolidated current liabilities of the Company and its consolidated subsidiaries as of the last day of any fiscal quarter of at least 1.0 to 1.0. |

If a Collateral Trigger Termination Date occurs, other financial covenants would apply and replace those listed above.

See our Annual Report on Form 10-K for the year ended December 31, 2017 for additional information on covenants related to our Credit Facility that were unchanged under the new amendment. As of the date of this filing, we are in compliance with all terms, conditions and financial covenants of the Credit Facility, as amended.

Senior Notes

Subsequent to March 31, 2018, we commenced cash tender offers to purchase up to $500 million aggregate principal amount of our outstanding 7.500% Senior Notes due 2020, 6.000% Senior Notes due 2022 and 8.250% Senior Notes due 2023. On April 17, 2018, using $540 million of proceeds from our San Juan Gallup disposition, we redeemed $329 million aggregate principal amount of the 2020 Notes and $171 million aggregate principal amount of the 2022 Notes.

See our Annual Report on Form 10-K for the year ended December 31, 2017 for additional discussion related to our senior notes.

Note 7. Provision (Benefit) for Income Taxes

The following table presents the provision (benefit) for income taxes from continuing operations.

Three months ended March 31, | |||||||

2018 | 2017 | ||||||

(Millions) | |||||||

Current: | |||||||

Federal | $ | — | $ | — | |||

State | — | — | |||||

— | — | ||||||

Deferred: | |||||||

Federal | (9 | ) | 46 | ||||

State | (6 | ) | (13 | ) | |||

(15 | ) | 33 | |||||

Total provision (benefit) | $ | (15 | ) | $ | 33 | ||

The effective income tax rate for the three months ended March 31, 2018, differs from the new federal statutory rate of 21 percent due to the effect of an adjustment to state deferred taxes as a result of a decrease in the blended state income tax rate due to changes in state apportionment factors resulting from the divestment of our San Juan Basin assets.

The effective income tax rate for the three months ended March 31, 2017, differs from the federal statutory rate of 35 percent due to the impact of ASU 2016-09 and the effect of an adjustment to state deferred taxes as a result of a decrease in the blended state income tax rate due to changes in state apportionment factors resulting from increased presence in the Delaware Basin operations in Texas following the Panther acquisition.

Due to the uncertainty or diversity in views about the application of ASC 740 in the period of enactment of the Tax Cuts and Jobs Act (“Act”), the SEC issued Staff Accounting Bulletin (“SAB”) 118 which allowed us to provide a provisional estimate of the impacts of the Act in our earnings for December 31, 2017. Additional impacts from the enactment of the Act

14

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

will be recorded as they are identified during the one-year measurement period as provided for in SAB 118. Our estimate does not reflect the impact of potential reductions of AMT credit refunds, changes in current interpretations of performance based executive compensation deduction limitations, effects of any state tax law changes and uncertainties regarding interpretations that may arise as a result of federal tax reform. The Company will continue to analyze the effects of the Act on its financial statements and operations and record changes to our estimates as appropriate.

We have recorded valuation allowances against deferred tax assets attributable primarily to certain state net operating loss (“NOL”) carryovers as well as our federal capital loss carryover. When assessing the need for a valuation allowance, we primarily consider future reversals of existing taxable temporary differences. To a lesser extent we may also consider future taxable income exclusive of reversing temporary differences and carryovers, and tax-planning strategies that would, if necessary, be implemented to accelerate taxable amounts to utilize expiring carryovers. The ultimate amount of deferred tax assets realized could be materially different from those recorded, as influenced by future operational performance, potential changes in jurisdictional income tax laws and other circumstances surrounding the actual realization of related tax assets. Valuation allowances that we have recorded are due to our expectation that we will not have sufficient income, or income of a sufficient character, in those jurisdictions to which the associated deferred tax asset applies. We have not recorded a valuation allowance against our federal NOL carryover, but a valuation allowance could be required in future periods if the federal NOL carryover continues to increase or circumstances change.

The ability of WPX to utilize loss carryovers or minimum tax credits to reduce future federal taxable income and income tax could be subject to limitations under the Internal Revenue Code. The utilization of such carryovers may be limited upon the occurrence of certain ownership changes during any three-year period resulting in an aggregate change of more than 50 percent in beneficial ownership (an “Ownership Change”). As of March 31, 2018, we do not believe that an Ownership Change has occurred for WPX, but an Ownership Change did occur for RKI effective with the acquisition. Therefore, there is an annual limitation on the benefit that WPX can claim from RKI carryovers that arose prior to the acquisition.

Pursuant to our tax sharing agreement with Williams, we remain responsible for the tax from audit adjustments related to our business for periods prior to our spin-off from Williams on December 31, 2011. The 2011 consolidated tax filing by Williams is currently being audited by the IRS and is the only pre spin-off period for which we continue to have exposure to audit adjustments as part of Williams. In 2017, the IRS proposed an adjustment related to our business for which a payment to Williams could be required. We are currently evaluating the issue and expect to protest the adjustment within the normal appeals process of the IRS. In addition, the alternative minimum tax credit deferred tax asset that was allocated to us by Williams at the time of the spin-off could change due to audit adjustments unrelated to our business. Any such adjustment to this deferred tax asset will not be known until the IRS examination is completed, but is not expected to result in a cash settlement unless we have utilized any of the alternative minimum tax credits.

As of March 31, 2018, the Company has approximately $8 million of unrecognized tax benefits which is offset by an increase in deferred tax assets of approximately $7 million. Currently, we expect ultimate resolution of our uncertain tax position during the next 12 months.

Note 8. Contingent Liabilities and Commitments

Contingent Liabilities

Royalty litigation

In October 2011, a potential class of royalty interest owners in New Mexico and Colorado filed a complaint against us in the County of Rio Arriba, New Mexico. The complaint presently alleges failure to pay royalty on hydrocarbons including drip condensate, breach of the duty of good faith and fair dealing, fraudulent concealment, conversion, misstatement of the value of gas and affiliated sales, breach of duty to market hydrocarbons in Colorado, breach of implied duty to market, violation of the New Mexico Oil and Gas Proceeds Payment Act, and bad faith breach of contract. Plaintiffs sought monetary damages and a declaratory judgment enjoining activities relating to production, payments and future reporting. This matter was removed to the United States District Court for New Mexico where the court denied plaintiffs’ motion for class certification. In March 2017, plaintiffs appealed the denial of class certification to the Tenth Circuit and oral argument before the Tenth Circuit was held on January 17, 2018. In August 2012, a second potential class action was filed against us in the United States District Court for the District of New Mexico by mineral interest owners in New Mexico and Colorado. Plaintiffs claim breach of contract, breach of the covenant of good faith and fair dealing, breach of implied duty to market both in Colorado and New Mexico and violation of the New Mexico Oil and Gas Proceeds Payment Act, and seek declaratory judgment, accounting and injunctive relief. On August 16, 2016, the court denied plaintiffs’ motion for class certification. On September 15, 2016, plaintiffs filed their motion for reconsideration and filed a second motion for class certification, and on September 30, 2017, the Court issued its memorandum opinion and order denying the plaintiffs motion for reconsideration and their Second Motion for Class

15

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Certification. At this time, we believe that our royalty calculations have been properly determined in accordance with the appropriate contractual arrangements and applicable laws. We do not have sufficient information to calculate an estimated range of exposure related to these claims.

Other producers have been pursuing administrative appeals with a federal regulatory agency and have been in discussions with a state agency in New Mexico regarding certain deductions, comprised primarily of processing, treating and transportation costs, used in the calculation of royalties. Although we are not a party to those matters, we are monitoring them to evaluate whether their resolution might have the potential for unfavorable impact on our results of operations. Certain outstanding issues in those matters could be material to us. We received notice from the U.S. Department of Interior Office of Natural Resources Revenue (“ONRR”) in the fourth quarter of 2010, intending to clarify the guidelines for calculating federal royalties on conventional gas production applicable to many of our federal leases in New Mexico. The guidelines for New Mexico properties were revised slightly in September 2013 as a result of additional work performed by the ONRR. The revisions did not change the basic function of the original guidance. The ONRR’s guidance provides its view as to how much of a producer’s bundled fees for transportation and processing can be deducted from the royalty payment. We believe using these guidelines would not result in a material difference in determining our historical federal royalty payments for our leases in New Mexico. Similar guidelines were recently issued for certain leases in Colorado and, as in the case of the New Mexico guidelines, we do not believe that they will result in a material difference to our historical federal royalty payments. ONRR has asked producers to attempt to evaluate the deductibility of these fees directly with the midstream companies that transport and process gas.

Environmental matters

The Environmental Protection Agency (“EPA”), other federal agencies, and various state and local regulatory agencies and jurisdictions routinely promulgate and propose new rules, and issue updated guidance to existing rules. These new rules and rulemakings include, but are not limited to, new air quality standards for ground level ozone, methane, green completions, and hydraulic fracturing and water standards. We are unable to estimate the costs of asset additions or modifications necessary to comply with these new regulations due to uncertainty created by the various legal challenges to these regulations and the need for further specific regulatory guidance.

Matters related to Williams’ former power business

In connection with a Separation and Distribution Agreement between WPX and The Williams Companies, Inc. (“Williams”), Williams is obligated to indemnify and hold us harmless from any losses arising out of liabilities assumed by us for the pending litigation described below relating to the reporting of certain natural gas-related information to trade publications.

Civil suits based on allegations of manipulating published gas price indices have been brought against us and others, seeking unspecified amounts of damages. We are currently a defendant in class action litigation and other litigation originally filed in state court in Colorado, Kansas, Missouri and Wisconsin and brought on behalf of direct and indirect purchasers of natural gas in those states. These cases were transferred to the federal court in Nevada. In 2008, the court granted summary judgment in the Colorado case in favor of us and most of the other defendants based on plaintiffs’ lack of standing. On January 8, 2009, the court denied the plaintiffs’ request for reconsideration of the Colorado dismissal and entered judgment in our favor.

In the other cases, on July 18, 2011, the Nevada district court granted our joint motions for summary judgment to preclude the plaintiffs’ state law claims because the federal Natural Gas Act gives the Federal Energy Regulatory Commission exclusive jurisdiction to resolve those issues. The court also denied the plaintiffs’ class certification motion as moot. The plaintiffs appealed to the United States Court of Appeals for the Ninth Circuit. On April 10, 2013, the United States Court of Appeals for the Ninth Circuit issued its opinion in the In re: Western States Wholesale Antitrust Litigation, holding that the Natural Gas Act does not preempt the plaintiffs’ state antitrust claims and reversing the summary judgment previously entered in favor of the defendants. The U.S. Supreme Court granted Defendants’ writ of certiorari. On April 21, 2015, the U.S. Supreme Court determined that the state antitrust claims are not preempted by the federal Natural Gas Act. On March 7, 2016, the putative class plaintiffs in several of the cases filed their motions for class certification. On March 30, 2017, the court denied the motions for class certification, which decision was appealed on June 20, 2017. On May 24, 2016, in Reorganized FLI Inc. v. Williams Companies, Inc., the Court granted Defendants’ Motion for Summary Judgment in its entirety, and an agreed amended judgment was entered by the court on January 4, 2017. The parties have filed numerous motions for summary judgment, reconsideration and remand, and there are currently two appeals before the Ninth Circuit. Because of the uncertainty around pending unresolved issues, including an insufficient description of the purported classes and other related matters, we cannot reasonably estimate a range of potential exposure at this time.

16

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Other Indemnifications

Pursuant to various purchase and sale agreements relating to divested businesses and assets, including the agreements pursuant to which we divested our Piceance and San Juan Basin operations, we have indemnified certain purchasers against liabilities that they may incur with respect to the businesses and assets acquired from us. The indemnities provided to the purchasers are customary in sale transactions and are contingent upon the purchasers incurring liabilities that are not otherwise recoverable from third parties. The indemnities generally relate to breaches of representations and warranties, tax liabilities, historic litigation, personal injury, environmental matters and rights-of-way. Additionally, Federal and state laws in areas of former operations may require previous operators to perform in certain circumstances where the buyer/operator may no longer be able to perform.

The indemnity provided to the purchaser of the entity that held our Piceance Basin operations relates in substantial part to liabilities arising in connection with litigation over the appropriate calculation of royalty payments. Plaintiffs in that litigation have asserted claims regarding, among other things, the method by which we took transportation costs into account when calculating royalty payments. In 2017, we settled one of these claims.

As of March 31, 2018, we have not received a claim against any of these indemnities and thus have no basis from which to estimate any reasonably possible loss beyond any amount already accrued. Further, we do not expect any of the indemnities provided pursuant to the sales agreements to have a material impact on our future financial position. However, if a claim for indemnity is brought against us in the future, it may have a material adverse effect on our results of operations in the period in which the claim is made.

In connection with the separation from Williams, we agreed to indemnify and hold Williams harmless from any losses resulting from the operation of our business or arising out of liabilities assumed by us. Similarly, Williams has agreed to indemnify and hold us harmless from any losses resulting from the operation of its business or arising out of liabilities assumed by it.

Summary

As of March 31, 2018 and December 31, 2017, the Company had accrued approximately $11 million for loss contingencies associated with royalty litigation and other contingencies. In certain circumstances, we may be eligible for insurance recoveries, or reimbursement from others. Any such recoveries or reimbursements will be recognized only when realizable.

Management, including internal counsel, currently believes that the ultimate resolution of the foregoing matters, taken as a whole and after consideration of amounts accrued, insurance coverage, recovery from customers or other indemnification arrangements, is not expected to have a materially adverse effect upon our future liquidity or financial position; however, it could be material to our results of operations in any given year.

Commitments

See Note 2 for a discussion of commitments that will be assumed by the purchaser of our San Juan Gallup assets and a related existing performance guarantee from WPX that will remain in place.

17

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Note 9. Fair Value Measurements

The following table presents, by level within the fair value hierarchy, our assets and liabilities that are measured at fair value on a recurring basis. The carrying amounts reported in the Consolidated Balance Sheets for cash and cash equivalents and restricted cash approximate fair value due to the nature of the instrument and/or the short-term maturity of these instruments.

March 31, 2018 | December 31, 2017 | ||||||||||||||||||||||||||||||

Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||||||

(Millions) | (Millions) | ||||||||||||||||||||||||||||||

Energy derivative assets | $ | — | $ | 125 | $ | — | $ | 125 | $ | — | $ | 59 | $ | — | $ | 59 | |||||||||||||||

Energy derivative liabilities | $ | — | $ | 316 | $ | — | $ | 316 | $ | — | $ | 236 | $ | — | $ | 236 | |||||||||||||||

Total debt(a) | $ | — | $ | 2,714 | $ | — | $ | 2,714 | $ | — | $ | 2,746 | $ | — | $ | 2,746 | |||||||||||||||

__________

(a) | The carrying value of total debt, excluding capital leases and debt issuance costs, was $2,600 million as of March 31, 2018 and December 31, 2017. The fair value of our debt, which also excludes capital leases and debt issuance costs, is determined on market rates and the prices of similar securities with similar terms and credit ratings. |

Energy derivatives include commodity based exchange-traded contracts and over-the-counter (“OTC”) contracts. Exchange-traded contracts include futures, swaps and options. OTC contracts include forwards, swaps, options and swaptions. These are carried at fair value on the Consolidated Balance Sheets.

Many contracts have bid and ask prices that can be observed in the market. Our policy is to use a mid-market pricing (the mid-point price between bid and ask prices) convention to value individual positions and then adjust on a portfolio level to a point within the bid and ask range that represents our best estimate of fair value. For offsetting positions by location, the mid-market price is used to measure both the long and short positions.

The determination of fair value for our assets and liabilities also incorporates the time value of money and various credit risk factors which can include the credit standing of the counterparties involved, master netting arrangements, the impact of credit enhancements (such as cash collateral posted and letters of credit) and our nonperformance risk on our liabilities. The determination of the fair value of our liabilities does not consider noncash collateral credit enhancements.

Forward, swap, option and swaption contracts included in Level 2 are valued using an income approach including present value techniques and option pricing models. Option contracts, which hedge future sales of our production, are structured as costless collars, calls or swaptions and are financially settled. All of our financial options are valued using an industry standard Black-Scholes option pricing model. In connection with several crude oil and natural gas swaps entered into, we granted swaptions to the swap counterparties in exchange for receiving premium hedged prices on the crude oil and natural gas swaps. These swaptions grant the counterparty the option to enter into future swaps with us. Significant inputs into our Level 2 valuations include commodity prices, implied volatility and interest rates, as well as considering executed transactions or broker quotes corroborated by other market data. These broker quotes are based on observable market prices at which transactions could currently be executed. In certain instances where these inputs are not observable for all periods, relationships of observable market data and historical observations are used as a means to estimate fair value. Also categorized as Level 2 is the fair value of our debt, which is determined on market rates and the prices of similar securities with similar terms and credit ratings. Where observable inputs are available for substantially the full term of the asset or liability, the instrument is categorized in Level 2.

Our energy derivatives portfolio is largely comprised of over-the-counter products or like products and the tenure of our derivatives portfolio extends through the end of 2021. Due to the nature of the products and tenure, we are consistently able to obtain market pricing. All pricing is reviewed on a daily basis and is formally validated with broker quotes or market indications and documented on a quarterly basis.

Certain instruments trade with lower availability of pricing information. These instruments are valued with a present value technique using inputs that may not be readily observable or corroborated by other market data. These instruments are classified within Level 3 when these inputs have a significant impact on the measurement of fair value. We did not have any instruments included in Level 3 as of March 31, 2018.

Reclassifications of fair value between Level 1, Level 2 and Level 3 of the fair value hierarchy, if applicable, are made at the end of each quarter. No significant transfers occurred during the periods ended March 31, 2018 and 2017.

There have been no material changes in the fair value of our net energy derivatives and other assets classified as Level 3 in the fair value hierarchy.

18

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Note 10. Derivatives and Concentration of Credit Risk

Energy Commodity Derivatives

Risk Management Activities

We are exposed to market risk from changes in energy commodity prices within our operations. We utilize derivatives to manage exposure to the variability in expected future cash flows from forecasted sales of crude oil, natural gas and natural gas liquids attributable to commodity price risk.

We produce, buy and sell crude oil, natural gas and natural gas liquids at different locations throughout the United States. To reduce exposure to a decrease in revenues from fluctuations in commodity market prices, we enter into futures contracts, swap agreements and financial option contracts to mitigate the price risk on forecasted sales of crude oil, natural gas and natural gas liquids. We have also entered into basis swap agreements to reduce the locational price risk associated with our producing basins. Our financial option contracts are either purchased or sold options, or a combination of options that comprise a net purchased option, zero-cost collar or swaptions.

19

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Derivatives related to production

The following table sets forth the derivative notional volumes of the net long (short) positions that are economic hedges of production volumes, which are included in our commodity derivatives portfolio as of March 31, 2018.

Commodity | Period | Contract Type (a) | Location | Notional Volume (b) | Weighted Average Price (c) | ||||||||

Crude Oil | |||||||||||||

Crude Oil | Apr - Dec 2018 | Fixed Price Swaps | WTI | (57,500 | ) | $ | 52.82 | ||||||

Crude Oil | Apr - Dec 2018 | Basis Swaps | Midland-Cushing | (14,331 | ) | $ | (0.83 | ) | |||||

Crude Oil | Apr - Dec 2018 | Basis Swaps | Nymex CMA Roll | (20,000 | ) | $ | 0.03 | ||||||

Crude Oil | Apr - Dec 2018 | Fixed Price Calls | WTI | (13,000 | ) | $ | 58.89 | ||||||

Crude Oil | 2019 | Fixed Price Swaps | WTI | (34,000 | ) | $ | (52.30 | ) | |||||

Crude Oil | 2019 | Basis Swaps | Midland-Cushing | (20,000 | ) | $ | (0.93 | ) | |||||

Crude Oil | 2019 | Basis Swaps | Nymex CMA Roll | (20,000 | ) | $ | 0.11 | ||||||

Crude Oil | 2019 | Fixed Price Calls | WTI | (5,000 | ) | $ | 54.08 | ||||||

Crude Oil | 2020 | Basis Swaps | Midland-Cushing | (5,000 | ) | $ | (1.16 | ) | |||||

Natural Gas | |||||||||||||

Natural Gas | Apr - Dec 2018 | Fixed Price Swaps | Henry Hub | (130 | ) | $ | 2.99 | ||||||

Natural Gas | Apr - Dec 2018 | Basis Swaps | Permian | (48 | ) | $ | (0.31 | ) | |||||

Natural Gas | Apr - Dec 2018 | Basis Swaps | Waha | (15 | ) | $ | (0.93 | ) | |||||

Natural Gas | Apr - Dec 2018 | Basis Swaps | Houston Ship | (43 | ) | $ | (0.08 | ) | |||||

Natural Gas | Apr - Dec 2018 | Fixed Price Calls | Henry Hub | (16 | ) | $ | 4.75 | ||||||

Natural Gas | 2019 | Fixed Price Swaps | Henry Hub | (50 | ) | $ | 2.88 | ||||||

Natural Gas | 2019 | Basis Swaps | Permian | (25 | ) | $ | (0.39 | ) | |||||

Natural Gas | 2019 | Basis Swaps | Waha | (45 | ) | $ | 0.07 | ||||||

Natural Gas | 2019 | Basis Swaps | Houston Ship | (30 | ) | $ | (0.09 | ) | |||||

Natural Gas | 2020 | Basis Swaps | Waha | (20 | ) | $ | (0.57 | ) | |||||

Natural Gas | 2021 | Basis Swaps | Waha | (20 | ) | $ | (0.57 | ) | |||||

Natural Gas Liquids | |||||||||||||

Natural Gas Liquids | Apr - Dec 2018 | Fixed Price Swaps | Mont Belvieu | (3,300 | ) | $ | 0.29 | ||||||

Natural Gas Liquids | Apr - Dec 2018 | Fixed Price Swaps | Conway Propane | (900 | ) | $ | 0.79 | ||||||

Natural Gas Liquids | Apr - Dec 2018 | Fixed Price Swaps | Mont Belvieu | (3,900 | ) | $ | 0.80 | ||||||

Natural Gas Liquids | Apr - Dec 2018 | Fixed Price Swaps | Mont Belvieu Iso | (700 | ) | $ | 0.91 | ||||||

Natural Gas Liquids | Apr - Dec 2018 | Fixed Price Swaps | Mont Belvieu | (1,800 | ) | $ | 0.90 | ||||||

Natural Gas Liquids | Apr - Dec 2018 | Fixed Price Swaps | Mont Belvieu | (1,500 | ) | $ | 1.31 | ||||||

__________

(a) | Derivatives related to crude oil production are fixed price swaps settled on the business day average, basis swaps, fixed price calls and swaptions. The derivatives related to natural gas production are fixed price swaps, basis swaps, fixed price calls and swaptions. In connection with several crude oil and natural gas swaps entered into, we granted swaptions to the swap counterparties in exchange for receiving premium hedged prices on the crude oil and natural gas swaps. These swaptions grant the counterparty the option to enter into future swaps with us. Basis swaps for the Nymex CMA (Calendar Monthly Average) Roll location are pricing adjustments to the trade month versus the delivery month for contract pricing. Derivatives related to natural gas liquids production are fixed price swaps. |

(b) | Crude oil volumes are reported in Bbl/day, natural gas volumes are reported in BBtu/day and natural gas liquids volumes are reported in Bbl/day. |

(c) | The weighted average price for crude oil is reported in $/Bbl, natural gas is reported in $/MMBtu and natural gas liquids is reported in $/Gal. |

20

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Fair values and gains (losses)

Our derivatives are presented as separate line items in our Consolidated Balance Sheets as current and noncurrent derivative assets and liabilities. Derivatives are classified as current or noncurrent based on the contractual timing of expected future net cash flows of individual contracts. The expected future net cash flows for derivatives classified as current are expected to occur within the next 12 months. The fair value amounts are presented on a gross basis and do not reflect the netting of asset and liability positions permitted under the terms of our master netting arrangements. Further, the amounts below do not include cash held on deposit in margin accounts that we have received or remitted to collateralize certain derivative positions.

We enter into commodity derivative contracts that serve as economic hedges but are not designated as cash flow hedges for accounting purposes as we do not utilize this method of accounting for derivative instruments. Net gain (loss) on derivatives on the Consolidated Statements of Operations includes settlements to be paid of $55 million and $5 million for the three months ended March 31, 2018 and 2017, respectively.

The cash flow impact of our derivative activities is presented as separate line items within the operating activities on the Consolidated Statements of Cash Flows.

Offsetting of derivative assets and liabilities

The following table presents our gross and net derivative assets and liabilities.

Gross Amount Presented on Balance Sheet | Netting Adjustments (a) | Net Amount | |||||||||

March 31, 2018 | (Millions) | ||||||||||

Derivative assets with right of offset or master netting agreements | $ | 125 | $ | (92 | ) | $ | 33 | ||||

Derivative liabilities with right of offset or master netting agreements | $ | (316 | ) | $ | 92 | $ | (224 | ) | |||

December 31, 2017 | |||||||||||

Derivative assets with right of offset or master netting agreements | $ | 59 | $ | (42 | ) | $ | 17 | ||||

Derivative liabilities with right of offset or master netting agreements | $ | (236 | ) | $ | 42 | $ | (194 | ) | |||

__________

(a) | With all of our financial trading counterparties, we have agreements in place that allow for the financial right of offset for derivative assets and derivative liabilities at settlement or in the event of a default under the agreements. Additionally, we have negotiated master netting agreements with some of our counterparties. These master netting agreements allow multiple entities that have multiple underlying agreements the ability to net derivative assets and derivative liabilities at settlement or in the event of a default or a termination under one or more of the underlying contracts. |

Credit-risk-related features

Certain of our derivative contracts contain credit-risk-related provisions that would require us, under certain events, to post additional collateral in support of our net derivative liability positions. These credit-risk-related provisions require us to post collateral in the form of cash or letters of credit when our net liability positions exceed an established credit threshold. The credit thresholds are typically based on our senior unsecured debt ratings from Standard and Poor’s and/or Moody’s Investment Services. Under these contracts, a credit ratings decline would lower our credit thresholds, thus requiring us to post additional collateral. We also have contracts that contain adequate assurance provisions giving the counterparty the right to request collateral in an amount that corresponds to the outstanding net liability.

As of March 31, 2018, we had no collateral posted to derivative counterparties, to support the aggregate fair value of our net $224 million derivative liability position (reflecting master netting arrangements in place with certain counterparties), which includes a reduction of $2 million to our liability balance for our own nonperformance risk. Assuming our credit thresholds were eliminated and a call for adequate assurance under the credit risk provisions in our derivative contracts was triggered, the additional collateral that we would have been required to post at March 31, 2018 was $224 million.

Concentration of Credit Risk

Cash equivalents

Our cash equivalents are primarily invested in funds with high-quality, short-term securities and instruments that are issued or guaranteed by the U.S. government.

21

WPX Energy, Inc.

Notes to Consolidated Financial Statements — (Continued)

Accounts receivable

Accounts receivable are carried on a gross basis, with no discounting, less the allowance for doubtful accounts. We estimate the allowance for doubtful accounts based on existing economic conditions, the financial conditions of the customers and the amount and age of past due accounts. Receivables are considered past due if full payment is not received by the contractual due date. Past due accounts are generally written off against the allowance for doubtful accounts only after all collection attempts have been exhausted. A portion of our receivables are from joint interest owners of properties we operate. Thus, we may have the ability to withhold future revenue disbursements to recover any non-payment of joint interest billings.

Derivative assets and liabilities

We have a risk of loss from counterparties not performing pursuant to the terms of their contractual obligations. Counterparty performance can be influenced by changes in the economy and regulatory issues, among other factors. Risk of loss is impacted by several factors, including credit considerations and the regulatory environment in which a counterparty transacts. We attempt to minimize credit-risk exposure to derivative counterparties and brokers through formal credit policies, consideration of credit ratings from public ratings agencies, monitoring procedures, master netting agreements and collateral support under certain circumstances. Collateral support could include letters of credit, payment under margin agreements and guarantees of payment by credit worthy parties.

We also enter into master netting agreements to mitigate counterparty performance and credit risk. During 2018 and 2017, we did not incur any significant losses due to counterparty bankruptcy filings. We assess our credit exposure on a net basis to reflect master netting agreements in place with certain counterparties. We offset our credit exposure to each counterparty with amounts we owe the counterparty under derivative contracts.