Attached files

| file | filename |

|---|---|

| EX-31.4 - EXHIBIT 31.4 - SAFEGUARD SCIENTIFICS INC | tv492495_ex31-4.htm |

| EX-31.3 - EXHIBIT 31.3 - SAFEGUARD SCIENTIFICS INC | tv492495_ex31-3.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K/A

Amendment No. 1

(Mark One)

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ___________

Commission File Number 1-5620

Safeguard Scientifics, Inc.

(Exact name of registrant as specified in its charter)

| Pennsylvania | ||

(State or other jurisdiction of incorporation or organization) |

23-1609753 (I.R.S. Employer Identification No.) | |

170 North Radnor-Chester Road Suite 200 Radnor, PA |

19087 | |

| (Address of principal executive offices) | (Zip Code) |

(610) 293-0600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock ($.10 par value) | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer þ | Smaller reporting company ¨ |

| Non-accelerated filer ¨ | (Do not check if a smaller reporting company) | Emerging growth company ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of June 30, 2017, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $237,111,560 based on the closing sale price as reported on the New York Stock Exchange.

The number of shares outstanding of the registrant’s common stock as of April 25, 2018 was 20,560,746.

DOCUMENTS INCORPORATED BY REFERENCE

None.

SAFEGUARD SCIENTIFICS, INC.

FORM 10-K/A

December 31, 2017

TABLE OF CONTENTS

| 2 |

Safeguard Scientifics, Inc. (“Safeguard,” the “Company,” “we,” “us,” and “our”) is filing this Amendment No. 1 on Form 10-K/A for the year ended December 31, 2017 (“Amendment”) to amend our Form 10-K for the year ended December 31, 2017, filed with the Securities and Exchange Commission (the “SEC”) on March 7, 2018 (the “Original Form 10-K”). We are filing this Amendment to (i) revise one risk factor as described in Item 503(c) of Regulation S-K that is applicable to the Company; and (ii) present the information required by Part III of Form 10-K that was previously omitted from the Original Form 10-K in reliance on General Instruction G(3) to Form 10-K. The Company is hereby amending the Original Form 10-K as follows:

| · | On the cover page, to (i) delete the reference in the Original Form 10-K to the incorporation by reference of the Company’s proxy statement for its 2018 annual shareholders’ meeting and (ii) update the date as of which the number of outstanding shares of the Company’s common stock is being provided; |

| · | To present in Part I, Item 1A, the risk factor captioned “Our success is dependent on our senior management,” which has been revised; |

| · | To present the information required by Part III of Form 10-K, which information was originally expected to be incorporated by reference to our definitive proxy statement to be delivered to our shareholders in connection with our 2018 annual meeting of shareholders; and |

| · | To amend and restate Exhibits 31.3 and 31.4, in Part IV, Item 15(b), in their entirety to contain the currently dated certifications from the Company’s principal executive officer and principal financial officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. The certifications of the Company’s principal executive officer and principal financial officer are attached to this Amendment as Exhibits 31.3 and 31.4. Because no financial statements have been included in this Amendment and this Amendment does not contain or amend any disclosure with respect to Items 307 and 308 of Regulation S-K, paragraphs 3, 4 and 5 of the certifications have been omitted. The Exhibit Index has also been amended and restated in its entirety to include the certifications as exhibits. |

Except as described above, no other changes have been made to the Original Form 10-K. This Amendment does not otherwise update information in the Original Form 10-K to reflect facts or events occurring subsequent to the filing date of the Original Form 10-K. This Amendment should be read in conjunction with the Original Form 10-K and with any of our filings made with the SEC subsequent to the filing of the Original Form 10-K.

| 3 |

| Item 1A. | RISK FACTORS |

You should carefully consider the information set forth below. The following risk factors describe situations in which our business, financial condition and/or results of operations could be materially harmed, and the value of our securities may be adversely affected. You should also refer to other information included or incorporated by reference in the Original Form 10-K and this Form 10-K/A.

The intended monetization of our partner company interests and distribution of net proceeds to shareholders are subject to factors beyond our control.

In January 2018, we announced that we will not deploy any capital into new partner companies. We will instead focus on supporting, and maximizing monetization opportunities for our existing partner company interests to enable distributions of net proceeds to shareholders. However, this strategic plan may require providing significant additional capital and operational support to such existing partner companies and we may not be able to sell our partner company interests during any specific time frame or otherwise on desirable terms, if at all, and there can be no assurance as to how long this process will take or the results that this process will yield. There can be no assurance as to whether we will realize the value of escrowed proceeds, holdbacks or other contingent consideration, if any, associated with the sale of partner company interests. Additionally, there can be no assurance that we will be able to satisfy our liabilities during this process. Further, the method, timing and amount of any distributions resulting from the monetization of existing partner companies will be at the discretion of our Board of Directors and will depend on market and business conditions and our overall liabilities, capital structure and liquidity position.

The continuing costs and burdens associated with being a public company will constitute a much larger percentage of our expenses and we may in the future delist our Common Stock with the New York Stock Exchange and seek to deregister our Common Stock with the SEC.

We will remain a public company and will continue to be subject to the listing standards of the New York Stock Exchange and SEC rules and regulations, including the Dodd-Frank Wall Street Reform and Consumer Protection Act and the Sarbanes-Oxley Act of 2002. The costs and burdens of being a public company will be a significant and continually increasing portion of our expenses under our new strategy. As part of such monetization efforts, we will likely in the future, once the majority of our partner company interests have been monetized and proceeds therefrom distributed, delist our Common Stock from the New York Stock Exchange and seek to deregister our Common Stock with the SEC. However, there can be no assurance as to the timing of such transactions, or whether such transactions will be completed at all, and we will continue to face the costs and burdens of being a public company until such time as our Common Stock is delisted with the New York Stock Exchange and deregistered with the SEC.

Our principal business strategy depends upon our ability to make good decisions regarding the deployment of capital into, and subsequent disposition of, existing partner company interests and, ultimately, the performance of our partner companies, which is uncertain.

If we make poor decisions regarding the deployment of capital into, and subsequent disposition of, existing partner companies, our business strategy will not succeed. If our partner companies do not succeed, the value of our assets could be significantly reduced and require substantial impairments or write-offs and our results of operations and the price of our common stock would be adversely affected. The risks relating to our partner companies include:

| · | most of our partner companies have a history of operating losses and/or limited operating history; |

| · | the intense competition affecting the products and services our partner companies offer could adversely affect their businesses, financial condition, results of operations and prospects for growth; |

| 4 |

| · | the inability to adapt to changing marketplaces; |

| · | the inability to manage growth; |

| · | the need for additional capital to fund their operations, which we may not be able to fund or which may not be available from third parties on acceptable terms, if at all; |

| · | the inability to protect their proprietary rights and/or infringing on the proprietary rights of others; |

| · | that our partner companies could face legal liabilities from claims made against them based upon their operations, products or work; |

| · | the impact of economic downturns on their operations, results and growth prospects; |

| · | the inability to attract and retain qualified personnel; |

| · | the existence of government regulations and legal uncertainties may place financial burdens on the businesses of our partner companies; and |

| · | the inability to plan for and manage catastrophic events. |

These and other risks are discussed in detail under the caption “Risks Related to Our Partner Companies” below.

Our Credit Facility subjects us to interest rate risk.

In May 2017, we entered into a $75.0 million secured, revolving credit facility (“Credit Facility”) with HPS Investment Partners, LLC (“Lender”). Debt service costs under the Credit Facility are subject to interest rate changes. Interest rates could rise from time to time and significantly increase our cost of borrowing. If that were to occur, replacing the Credit Facility with alternative credit arrangements having a lower cost of borrowing would likely not be possible and no assurance can be given that we would be able to refinance the Credit Facility on attractive terms or at all.

Servicing the indebtedness under the Credit Facility will require a significant amount of cash and our ability to generate cash depends on many factors beyond our control.

Our ability to make payments on the indebtedness under the Credit Facility will depend on our ability to generate cash in the future. We generate cash from proceeds we receive in connection with the sales of our interests in our partner companies. Due to the nature of the mergers and acquisitions market, and the developmental cycle of companies like our partner companies, our ability to generate specific amounts of liquidity from sales of our partner company interests in any given period of time cannot be assured. Our ability to generate cash is also, to a certain extent, subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control. The risk exists that our business will be unable to generate sufficient cash flow to service our indebtedness under the Credit Facility.

Covenants in the agreements governing the Credit Facility could adversely affect our business and/or result in the operation of our business in a way other than as desired by management; our ability to comply with such covenants may be affected by events beyond our control; and a breach of any of these covenants could result in a default under the agreements governing the Credit Facility, which, if not cured or waived, could result in the acceleration of the indebtedness under the Credit Facility.

The Credit Facility contains various covenants that prohibit or limit, subject to certain exceptions, our ability to, among other things:

| 5 |

| · | Sell, transfer, lease, convey or otherwise dispose of all or any part of our business or property; |

| · | Exceed concentration limits with respect to the amount of capital deployed to any single partner company; |

| · | Exceed concentration limits with respect to the amount of capital deployed to one or more partner companies operating in the same or similar industries; |

| · | Deploy capital to partner companies operating outside of certain specified industries; |

| · | Incur or assume liens or additional debt or provide guarantees in respect of obligations of other persons; |

| · | Pay any dividends or make any distribution (in cash or in kind) or payment in respect of, or redeem, retire or purchase any capital stock; |

| · | Enter into, or permit any of our subsidiaries to enter into, any sale and leaseback transaction; |

| · | Wind-up, liquidate or dissolve, or merge, consolidate or amalgamate with any person, or permit any of our subsidiaries to do (or agree to do) so; |

| · | Enter into certain transactions with affiliates; and |

| · | Amend, modify or otherwise change any of our governing documents. |

In addition, the Credit Facility requires us to among other things, maintain (i) a liquidity threshold of at least $20 million of unrestricted cash; (ii) a tangible net worth, plus unrestricted cash, of at least 1.75x the amount then outstanding under the Credit Facility; and (iii) a minimum aggregate appraised value of the Company’s ownership interests in its partner companies, plus unrestricted cash in excess of the liquidity threshold, of at least $350 million.

The foregoing covenants could adversely affect our ability to finance our operations, engage in business activities that may be in our interest and plan for or react to market conditions or otherwise execute our business strategies.

Our ability to comply with these covenants may be affected by events beyond our control, including prevailing economic, financial and industry conditions.

Our failure to comply with any of these covenants could result in a default under the Credit Facility. If that were to occur, the Lender could choose to accelerate the maturity of the indebtedness. If the Lender were to accelerate the maturity of the indebtedness, we may not have sufficient liquidity to repay the entire balance of the outstanding borrowings and other obligations under the Credit Facility.

A significant amount of our deployed capital may be concentrated in partner companies operating in the same or similar industries, limiting the diversification of our capital deployments.

Except as may be agreed to with our debt providers, we do not have fixed guidelines for diversification of capital deployments, and our capital deployments could be concentrated in several partner companies that operate in the same or similar industries. This may cause us to be more susceptible to any single economic, regulatory or other occurrence affecting those particular industries than we would otherwise be if our partner companies operated in more diversified industries.

Our business model does not rely upon, or plan for, the receipt of operating cash flows from our partner companies. Our partner companies generally provide us with no cash flow from their operations. We rely on cash on hand, liquidity events and our ability to generate cash from capital raising activities to finance our operations.

| 6 |

We need capital to fund the capital needs of our existing partner companies. We also need cash to service and repay our outstanding debt, finance our corporate overhead and meet our existing funding commitments. As a result, we have substantial cash requirements. Our partner companies generally provide us with no cash flow from their operations. To the extent our partner companies generate any cash from operations, they generally retain the funds to develop their own businesses. As a result, we must rely on cash on hand, partner company liquidity events and new capital raising activities to meet our cash needs. If we are unable to find ways of monetizing our holdings or raising additional capital on attractive terms, we may face liquidity issues that will require us to constrain our ability to execute our business strategy and limit our ability to provide financial support to our existing partner companies.

Fluctuations in the price of the common stock of our publicly traded holdings may affect the price of our common stock.

From time to time, we may hold equity interests in companies that are publicly traded. Fluctuations in the market prices of the common stock of publicly traded holdings may affect the price of our common stock. Historically, the market prices of our publicly traded holdings have been highly volatile and subject to fluctuations unrelated or disproportionate to operating performance.

We may be unable to obtain maximum value for our holdings or to sell our holdings on a timely basis.

We hold significant positions in our partner companies. Consequently, if we were to divest all or part of our holdings in a partner company, we may have to sell our interests at a relative discount to a price which may be received by a seller of a smaller portion. For partner companies with publicly traded stock, we may be unable to sell our holdings at then-quoted market prices. The trading volume and public float in the common stock of a publicly traded partner company may be small relative to our holdings. As a result, any significant open-market divestiture by us of our holdings in such a partner company, if possible at all, would likely have a material adverse effect on the market price of its common stock and on our proceeds from such a divestiture. Additionally, we may not be able to take our partner companies public as a means of monetizing our position or creating shareholder value.

Registration and other requirements under applicable securities laws and contractual restrictions also may adversely affect our ability to dispose of our partner company holdings on a timely basis.

Our success is dependent on our senior management.

Our success is dependent on our senior management team’s ability to execute our strategy. On April 6, 2018, we publicly announced a series of management changes intended to streamline our organizational structure and reduce our operating costs. These aggressive cost-reduction initiatives are intended to better align our cost structure with the strategy we announced in January 2018. These management changes included the departure of three members of our management team, including our current President and Chief Executive Officer, our current Senior Vice President and Chief Financial Officer, and our current Senior Vice President of Investor Relations and Corporate Communications. A loss of one or more of the remaining members of our senior management team without adequate replacement could have a material adverse effect on us.

Our business strategy may not be successful if valuations in the market sectors in which our partner companies participate decline.

Our strategy involves creating value for our shareholders by helping our partner companies build value and, if appropriate, accessing the public and private capital markets. Therefore, our success is dependent on the value of our partner companies as determined by the public and private capital markets. Many factors, including reduced market interest, may cause the market value of our partner companies to decline. If valuations in the market sectors in which our partner companies participate decline, their access to the public and private capital markets on terms acceptable to them may be limited.

| 7 |

Our partner companies could make business decisions that are not in our best interests or with which we do not agree, which could impair the value of our holdings.

Although we currently own a significant, influential interest in some of our partner companies, we do not maintain a controlling interest in any of our partner companies. Acquisitions of interests in partner companies in which we share or have no control, and the dilution of our interests in or loss of control of partner companies, will involve additional risks that could cause the performance of our interests and our operating results to suffer, including:

| · | the management of a partner company having economic or business interests or objectives that are different from ours; and |

| · | the partner companies not taking our advice with respect to the financial or operating issues they may encounter. |

Our inability to control our partner companies also could prevent us from assisting them, financially or otherwise, or could prevent us from liquidating our interests in them at a time or at a price that is favorable to us. Additionally, our partner companies may not act in ways that are consistent with our business strategy. These factors could hamper our ability to maximize returns on our interests and cause us to incur losses on our interests in these partner companies.

We may have to buy, sell or retain assets when we would otherwise not wish to do so in order to avoid registration under the Investment Company Act.

The Investment Company Act of 1940 regulates companies which are engaged primarily in the business of investing, reinvesting, owning, holding or trading in securities. Under the Investment Company Act, a company may be deemed to be an investment company if it owns investment securities with a value exceeding 40% of the value of its total assets (excluding government securities and cash items) on an unconsolidated basis, unless an exemption or safe harbor applies. We refer to this test as the “40% Test.” Securities issued by companies other than consolidated partner companies are generally considered “investment securities” for purposes of the Investment Company Act, unless other circumstances exist which actively involve the company holding such interests in the management of the underlying company. We are a company that partners with growth-stage companies to build value; we are not engaged primarily in the business of investing, reinvesting or trading in securities. We are in compliance with the 40% Test. Consequently, we do not believe that we are an investment company under the Investment Company Act.

We monitor our compliance with the 40% Test and seek to conduct our business activities to comply with this test. It is not feasible for us to be regulated as an investment company because the Investment Company Act rules are inconsistent with our strategy of actively helping our partner companies in their efforts to build value. In order to continue to comply with the 40% Test, we may need to take various actions which we would otherwise not pursue. For example, we may need to retain a controlling interest in a partner company that we no longer consider strategic, we may not be able to acquire an interest in a company unless we are able to obtain a controlling ownership interest in the company, or we may be limited in the manner or timing in which we sell our interests in a partner company. Our ownership levels also may be affected if our partner companies are acquired by third parties or if our partner companies issue stock which dilutes our ownership interest. The actions we may need to take to address these issues while maintaining compliance with the 40% Test could adversely affect our ability to create and realize value at our partner companies.

Economic disruptions and downturns may have negative repercussions for us.

Events in the United States and international capital markets, debt markets and economies may negatively impact our stock price and our ability to pursue certain tactical and strategic initiatives, such as accessing additional public or private equity or debt financing for us or for our partner companies and selling our interests in partner companies on terms acceptable to us and in time frames consistent with our expectations.

| 8 |

We cannot provide assurance that material weaknesses in our internal control over financial reporting will not be identified in the future.

We cannot assure you that material weaknesses in our internal control over financial reporting will not be identified in the future. Any failure to maintain or implement required new or improved controls, or any difficulties we encounter in their implementation, could result in a material weakness, or could result in material misstatements in our Consolidated Financial Statements. These misstatements could result in a restatement of our Consolidated Financial Statements, cause us to fail to meet our reporting obligations and/or cause investors to lose confidence in our reported financial information, leading to a decline in our stock price.

Risks Related to Our Partner Companies

Most of our partner companies have a history of operating losses and/or limited operating history and may never be profitable.

Most of our partner companies have a history of operating losses and/or limited operating history, have significant historical losses and may never be profitable. Many have incurred substantial costs to develop and market their products, have incurred net losses and cannot fund their cash needs from operations. We expect that the operating expenses of certain of our partner companies will increase substantially in the foreseeable future as they continue to develop products and services, increase sales and marketing efforts, and expand operations.

Our partner companies face intense competition, which could adversely affect their business, financial condition, results of operations and prospects for growth.

There is intense competition in the technology marketplaces, and we expect competition to intensify in the future. Our business, financial condition, and results of operations will be materially adversely affected if our partner companies are not able to compete successfully. Many of the present and potential competitors may have greater financial, technical, marketing and other resources than those of our partner companies. This may place our partner companies at a disadvantage in responding to the offerings of their competitors, technological changes or changes in client requirements. Also, our partner companies may be at a competitive disadvantage because many of their competitors have greater name recognition, more extensive client bases and a broader range of product offerings. In addition, our partner companies may compete against one another.

The success or failure of many of our partner companies is dependent upon the ultimate effectiveness of newly-created technologies, medical devices, financial services, healthcare diagnostics, etc.

Our partner companies’ business strategies are often highly dependent upon the successful launch and commercialization of an innovative technology or device, including, without limitation, technologies or devices used in healthcare, financial services or digital media. Despite all of our efforts to understand the research and development underlying the innovation or creation of such technologies and devices before we deploy capital into a partner company, sometimes the performance of the technology or device does not match our expectations or those of our partner company. In those situations, it is likely that we will incur a partial or total loss of the capital which we deployed in such partner company.

Our partner companies may fail if they do not adapt to changing marketplaces.

If our partner companies fail to adapt to changes in technology and customer and supplier demands, they may not become or remain profitable. There is no assurance that the products and services of our partner companies will achieve or maintain market penetration or commercial success, or that the businesses of our partner companies will be successful.

| 9 |

The technology marketplaces are characterized by:

| · | rapidly changing technology; |

| · | evolving industry standards; |

| · | frequent introduction of new products and services; |

| · | shifting distribution channels; |

| · | evolving government regulation; |

| · | frequently changing intellectual property landscapes; and |

| · | changing customer demands. |

Our future success will depend on our partner companies’ ability to adapt to these evolving marketplaces. They may not be able to adequately or economically adapt their products and services, develop new products and services or establish and maintain effective distribution channels for their products and services. If our partner companies are unable to offer competitive products and services or maintain effective distribution channels, they will sell fewer products and services and forego potential revenue, possibly causing them to lose money. In addition, we and our partner companies may not be able to respond to the marketplace changes in an economically efficient manner, and our partner companies may become or remain unprofitable.

Our partner companies may grow rapidly and may be unable to manage their growth.

We expect some of our partner companies to grow rapidly. Rapid growth often places considerable operational, managerial and financial strain on a business. To successfully manage rapid growth, our partner companies must, among other things:

| · | improve, upgrade and expand their business infrastructures; |

| · | scale up production operations; |

| · | develop appropriate financial reporting controls; |

| · | attract and retain qualified personnel; and |

| · | maintain appropriate levels of liquidity. |

If our partner companies are unable to manage their growth successfully, their ability to respond effectively to competition and to achieve or maintain profitability will be adversely affected.

Based on our business model, some or all of our partner companies will need to raise additional capital to fund their operations at any given time. We may not be able to fund some or all of such amounts and such amounts may not be available from third parties on acceptable terms, if at all. Further, if our partner companies do raise additional capital, either debt or equity, such capital may rank senior to our interests in such companies.

We cannot be certain that our partner companies will be able to obtain additional financing on favorable terms when needed, if at all. Because our resources and our ability to raise capital are not unlimited, we may not be able to provide partner companies with sufficient capital resources to enable them to reach a cash-flow positive position or a sale of the company, even if we wish to do so. General economic disruptions and downturns may also negatively affect the ability of some of our partner companies to fund their operations from other stockholders and capital sources. We also may fail to accurately project the capital needs of partner companies. If partner companies need capital but are not able to raise capital from us or other outside sources, then they may need to cease or scale back operations. In such event, our interest in any such partner company will become less valuable. If our partner companies raise additional capital, either debt or equity, that ranks senior to the capital we have deployed, such capital may entitle its holders to receive returns of capital before the dates on which we are entitled to receive any return of our deployed capital. Also, in the event of any insolvency, liquidation, dissolution, reorganization or bankruptcy of a partner company, holders of such partner company’s instruments that rank senior to our deployed capital will typically be entitled to receive payment in full before we receive any return of our deployed capital. After returning such senior capital, such partner company may not have any remaining assets to use for returning capital to us, causing us to lose some or all of our deployed capital in such partner company.

| 10 |

Economic disruptions and downturns may negatively affect our partner companies’ plans and their results of operations.

Many of our partner companies are largely dependent upon outside sources of capital to fund their operations. Disruptions in the availability of capital from such sources will negatively affect the ability of such partner companies to pursue their business models and will force such companies to revise their growth and development plans accordingly. Any such changes will, in turn, negatively affect our ability to realize the value of our capital deployments in such partner companies.

In addition, downturns in the economy as well as possible governmental responses to such downturns and/or to specific situations in the economy could affect the business prospects of certain of our partner companies, including, but not limited to, in the following ways: weaknesses in the financial services industries; reduced business and/or consumer spending; and/or systemic changes in the ways the healthcare system operates in the United States.

Some of our partner companies may be unable to protect their proprietary rights and may infringe on the proprietary rights of others.

Our partner companies assert various forms of intellectual property protection. Intellectual property may constitute an important part of partner company assets and competitive strengths. Federal law, most typically copyright, patent, trademark and trade secret laws, generally protects intellectual property rights. Although we expect that our partner companies will take reasonable efforts to protect the rights to their intellectual property, third parties may develop similar intellectual property independently. Moreover, the complexity of international trade secret, copyright, trademark and patent law, coupled with the limited resources of our partner companies and the demands of quick delivery of products and services to market, create a risk that partner company efforts to prevent misappropriation of their technology will prove inadequate.

Some of our partner companies also license intellectual property from third parties and it is possible that they could become subject to infringement actions based upon their use of the intellectual property licensed from those third parties. Our partner companies generally obtain representations as to the origin and ownership of such licensed intellectual property. However, this may not adequately protect them. Any claims against our partner companies’ proprietary rights, with or without merit, could subject the companies to costly litigation and divert their technical and management personnel from other business concerns. If our partner companies incur costly litigation and their personnel are not effectively deployed, the expenses and losses incurred by our partner companies will increase and their profits, if any, will decrease.

Third parties have and may assert infringement or other intellectual property claims against our partner companies based on their patents or other intellectual property claims. Even though we believe our partner companies’ products do not infringe any third party’s patents, they may have to pay substantial damages, possibly including treble damages, if it is ultimately determined that they do. They may have to obtain a license to sell their products if it is determined that their products infringe on another person’s intellectual property. Our partner companies might be prohibited from selling their products before they obtain a license, which, if available at all, may require them to pay substantial royalties. Even if infringement claims against our partner companies are without merit, defending these types of lawsuits takes significant time, is expensive and may divert management attention from other business concerns.

| 11 |

Certain of our partner companies could face legal liabilities from claims made against their operations, products or work.

Because manufacture and sale of certain partner company products entail an inherent risk of product liability, certain partner companies maintain product liability insurance. Although none of our current partner companies have experienced any material losses in this regard, there can be no assurance that they will be able to maintain or acquire adequate product liability insurance in the future and any product liability claim could have a material adverse effect on a partner company’s financial stability, revenues and results of operations. In addition, many of the engagements of our partner companies involve projects that are critical to the operation of their clients’ businesses. If our partner companies fail to meet their contractual obligations, they could be subject to legal liability, which could adversely affect their business, operating results and financial condition. Partner company contracts typically include provisions designed to limit their exposure to legal claims relating to their services and products. However, these provisions may not protect our partner companies or may not be enforceable. Also, some of our partner companies depend on their relationships with their clients and their reputation for high-quality services and integrity to retain and attract clients. As a result, claims made against our partner companies’ work may damage their reputation, which in turn could impact their ability to compete for new work and negatively impact their revenue and profitability.

Our partner companies’ success depends on their ability to attract and retain qualified personnel.

Our partner companies depend upon their ability to attract and retain senior management and key personnel, including trained technical and marketing personnel. Our partner companies also will need to continue to hire additional personnel as they expand. Although our current partner companies have not been the subject of a work stoppage, any future work stoppage could have a material adverse effect on their respective operations. A shortage in the availability of the requisite qualified personnel or work stoppage would limit the ability of our partner companies to grow, to increase sales of their existing products and services, and to launch new products and services.

Government regulations and legal uncertainties may place financial burdens on the businesses of our partner companies.

Failure to comply with applicable requirements of the FDA or comparable regulation in foreign countries can result in fines, recall or seizure of products, total or partial suspension of production, withdrawal of existing product approvals or clearances, refusal to approve or clear new applications or notices and criminal prosecution. Manufacturers of pharmaceuticals and medical diagnostic devices and operators of laboratory facilities are subject to strict federal and state regulation regarding validation and the quality of manufacturing and laboratory facilities. Failure to comply with these quality regulation systems requirements could result in civil or criminal penalties or enforcement proceedings, including the recall of a product or a “cease distribution” order. The enactment of any additional laws or regulations that affect healthcare insurance policy and reimbursement (including Medicare reimbursement) could negatively affect some of our partner companies. If Medicare or private payers change the rates at which our partner companies or their customers are reimbursed by insurance providers for their products, such changes could adversely impact our partner companies.

Some of our partner companies may be subject to significant environmental, health and safety regulation.

Some of our partner companies may be subject to licensing and regulation under federal, state and local laws and regulations relating to the protection of the environment and human health and safety, including laws and regulations relating to the handling, transportation and disposal of medical specimens, infectious and hazardous waste and radioactive materials, as well as to the safety and health of manufacturing and laboratory employees. In addition, the federal Occupational Safety and Health Administration has established extensive requirements relating to workplace safety. Compliance with such regulations could increase operating costs at certain of our partner companies, and the failure to comply could negatively affect the operations and results of some of our partner companies.

| 12 |

Catastrophic events may disrupt our partner companies’ businesses.

Some of our partner companies are highly automated businesses and rely on their network infrastructure, various software applications and many internal technology systems and data networks for their customer support, development, sales and marketing and accounting and finance functions. Further, some of our partner companies provide services to their customers from data center facilities in multiple locations. Some of these data centers are operated by third parties, and the partner companies have limited control over those facilities. A disruption or failure of these systems or data centers in the event of a natural disaster, telecommunications failure, power outage, cyber-attack, war, terrorist attack or other catastrophic event could cause system interruptions, reputational harm, delays in product development, breaches of data security and loss of critical data. Such an event could also prevent the partner companies from fulfilling customer orders or maintaining certain service level requirements, particularly in respect of their SaaS offerings. While certain of our partner companies have developed certain disaster recovery plans and maintain backup systems to reduce the potentially adverse effect of such events, a catastrophic event that resulted in the destruction or disruption of any of their data centers or their critical business or information technology systems could severely affect their ability to conduct normal business operations and, as a result, their business, operating results and financial condition could be adversely affected.

We cannot provide assurance that our partner companies’ disaster recovery plans will address all of the issues they may encounter in the event of a disaster or other unanticipated issue, and their business interruption insurance may not adequately compensate them for losses that may occur from any of the foregoing. In the event that a natural disaster, terrorist attack or other catastrophic event were to destroy any part of their facilities or interrupt their operations for any extended period of time, or if harsh weather or health conditions prevent them from delivering products in a timely manner, their business, financial condition and operating results could be adversely affected.

| 13 |

| ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

| Names of Directors and other Information: |

| Stephen T. Zarrilli, age 56 | Other public directorships: Virtus Investment | |

| President and Chief Executive Officer | Partners, Inc. | |

| Director since: 2012 | Former public directorships within past five years: | |

| Safeguard Board Committees: None | Nutrisystem, Inc. |

Career Highlights:

| — | President and Chief Executive Officer (November 2012 – present); Senior Vice President and Chief Financial Officer (June 2008 – November 2012); and Acting Chief Administrative Officer and Acting Chief Financial Officer (December 2006 – June 2007), Safeguard Scientifics, Inc. |

| — | Co-founder and Managing Director, Penn Valley Group, a middle-market management advisory and private equity firm (2004 – June 2008) |

| — | Chief Financial Officer, Fiberlink Communications Corporation (2001 – 2004) |

| — | Chief Executive Officer, Concellera Software, Inc. (2000 – 2001) |

| — | Chief Executive Officer (1999 – 2000) and Chief Financial Officer (1994 – 1998), US Interactive, Inc. |

| — | Deloitte & Touche (1983 – 1994) |

Experience and Qualifications: Mr. Zarrilli has more than 30 years of experience in corporate finance and accounting, general operations and executive management; capital markets transactions; debt and equity financings; merger and acquisition transactions; and emerging ventures.

|

Julie A. Dobson, age 61 Director since: 2003 Safeguard Board Committees: Compensation (Chair), Nominating & Corporate Governance |

Other public directorships: None. Former public directorships within past five years: American Water Works Company Inc., PNM Resources, Inc. and RadioShack Corporation |

Career Highlights:

| — | Chief Operating Officer, Telecorp PCS, Inc., a wireless/mobile phone company that was acquired by AT&T Wireless, Inc. (1998 – 2002) |

| — | Various executive positions during her 18-year career with Bell Atlantic Corporation, including President, Bell Atlantic Corporation’s New York/New Jersey Metro Region mobile phone operations, Vice President of Bell Atlantic Enterprises Corporation, and President and Chief Executive Officer of Bell Atlantic Business Systems International |

Experience and Qualifications: Ms. Dobson has 22 years of corporate and entrepreneurial experience, including experience relevant to corporate finance and accounting matters; strategic planning, corporate development and operations management; capital markets transactions; and debt and equity financings. Ms. Dobson also has relevant experience growing businesses organically and through merger and acquisition transactions and experience serving on public company boards and the principal committees thereof.

| 14 |

|

Russell D. Glass, age 55 Director since: 2018 Safeguard Board Committees: Compensation |

Other public directorships: None Former public directorships within past five years: None |

Career Highlights:

| — | Founder and Managing Member of RDG Capital LLC (2005 – present) |

| — | Managing Partner of RDG Capital Fund Management, an investment advisory firm (2014 – present) |

| — | Senior Adviser at Knights Genesis Group, a private equity firm (2017 – present) |

| — | Director of Blue Bite LLC, a digital marketing technology company (2009 – present) |

| — | Director of A.G. Spanos Corporation, a national real estate developer and owner of the NFL Los Angeles Chargers (1993 – present) |

| — | Managing Member of Princeford Capital Management, an investment advisory firm (2009 – 2014) |

| — | Chief Executive Officer of Cadus Pharmaceutical Corporation (n/k/a Cadus Corporation), a biotechnology holding company (2000 – 2003), and director (1998 – 2011) |

| — | Co-Chairman and Chief Investment Officer of Ranger Partners, an investment fund management company (2002 – 2003) |

| — | President and Chief Investment Officer of Icahn Associates Corporation, a diversified investment firm and principal investment vehicle for Carl Icahn (1998 – 2002) |

| — | Partner at Relational Investors LLC, an investment fund management company (1996 – 1998) |

| — | Partner at Premier Partners Inc., an investment banking and research firm (1988 – 1996) |

| — | Analyst with Kidder, Peabody & Co., an investment banking firm (1984 – 1986) |

| — | Holds directorship at the Council for Economic Education and held other previous directorships at Automated Travel Systems, Inc., Axiom Biotechnologies, Global Discount Travel Services/Lowestfare.com, National Energy Group and Next Generation Technology Holdings, Inc. |

| — | Received A.B. in Economics from Princeton University |

| — | Received M.B.A. from Stanford Graduate School of Business |

Experience and Qualifications: Mr. Glass has experience relating to private equity, investment banking, and serving as chief executive officer of a public company. Mr. Glass has experience serving on the boards of public and private companies in a wide range of industries, including biotech, healthcare information technology, pharmacology, enterprise systems software, real estate, energy, and digital marketing.

|

Stephen Fisher, age 53 Director since: 2015 Safeguard Board Committees: Audit , Compensation |

Other public directorships: Vonage Holdings Corp., Inc. Former public directorships within past five years: None |

Career Highlights:

| — | Senior Vice President and Chief Technology Officer, eBay Inc., a leading ecommerce company (September 2014 – present) |

| — | Executive Vice President, Technology (December 2008 – September 2014) and several other executive positions (October 2004 – December 2008) during his tenure with salesforce.com, a provider of leading, worldwide customer relationship management applications and products |

| — | Various positions with AT&T Labs (1996 – 1999 and 2001 – 2004) |

| — | Founder, President and Chief Executive Officer, NotifyMe Networks (1999 – 2000) |

Experience and Qualifications: Mr. Fisher’s corporate experience includes experience relevant to strategic planning; business and product development; operations management; and growing businesses organically. In addition, he possesses deep domain expertise in the technology and communications services sectors.

| 15 |

|

Ira M. Lubert, age 67 Director since: 2018 Safeguard Board Committees: Nominating & Corporate Governance |

Other public directorships: None Former public directorships within past five years: Pennsylvania Real Estate Investment Trust |

Career Highlights:

| — | Co-Founder of and a Partner of Quaker Partners Management, L.P., which advises a series of life sciences funds (2002 – present) |

| — | Co-Founder of and a Partner of LEM Capital, L.P., which advises a series of real estate funds invested primarily in multifamily properties (2002 – present) |

| — | Co-Founder of and a Partner of LBC Credit Management, LP, which advises a series of structured finance funds (2005 – present) |

| — | Co-Founder of and a Partner of Patriot Financial Management, L.P., which advises a series of community banking funds (2007 – 2017) |

| — | Co-Founder of Versa Capital Management, LLC, specializing in distressed and special situations (2004) |

| — | Co-Founder of and a Partner of LLR Management, L.P., which focuses on lower middle market growth companies (1999 – present) |

| — | Co-Founder and Chairman of Lubert-Adler Management Company, L.P., which advises a series of real estate funds (1997 – present) |

| — | Co-Founder and Chairman of Independence Capital Partners, LLC, which provides services to certain investment advisers (1997 – present) |

| — | Managing Director and Co-Founder of TL Ventures, the subsequent Safeguard-affiliated family of early stage venture funds with over $1 billion of capital under management (1986 – 1997) |

Experience and Qualifications: Mr. Lubert has 30 years of experience relating to private equity and investment management, including life sciences funds. Mr. Lubert began his private equity career with Safeguard. Mr. Lubert was honored as Drexel University’s LeBow College of Business 60th Business Leader of the Year and was honored by Temple University for his excellence in leadership with the Musser Award.

|

George MacKenzie, age 69 Director since: 2003 Safeguard Board Committees: Audit (Chair), Compensation, Nominating & Corporate Governance |

Other public directorships: American Water Works Company Inc. (Chair) and Tractor Supply Company Former public directorships within past five years: None |

Career Highlights:

| — | Interim Chief Executive Officer, American Water Works Company Inc., a provider of water services in North America (January – April 2006) |

| — | Interim Chief Executive Officer, C&D Technologies, Inc., a technology company that markets systems for the conversion and storage of electrical power (March – July 2005) |

| — | Executive Vice President and Chief Financial Officer, P.H. Glatfelter Company, a manufacturer of specialty papers and engineered products (September 2001 – June 2002) |

| — | Vice Chairman (2000 – 2001) and Chief Financial Officer (1995 – 2001) of, and several other executive positions during his 22-year career with, Hercules, Incorporated, a global chemical specialties manufacturer |

Experience and Qualifications: Mr. MacKenzie has extensive experience in corporate finance and accounting. He has served as the chief financial officer of a publicly traded company, and he is a certified public accountant. Mr. MacKenzie also has experience in capital markets transactions; debt and equity financings; global strategic planning and operations management; merger and acquisition transactions; and risk management. In addition, he has extensive public company board experience, including service on multiple audit, compensation and nominating and corporate governance committees.

| 16 |

|

Maureen F. Morrison, age 63 Director since: October, 2017 Safeguard Board Committees: Audit |

Other public directorships: None

Former public directorships within past five years: None |

Career Highlights:

| — | Audit Partner with PriceWaterhouseCoopers LLP for 28 years, serving public and private multi-national clients in the technology and manufacturing industries. Ms. Morrison led the Atlanta, Georgia Technology Audit Practice for six years, and held other positions at the firm, prior to her retirement in 2015. |

Experience and Qualifications: During her tenure at PriceWaterhouseCoopers LLP, Ms. Morrison worked closely with clients concentrated in the technology industry dealing with acquisitions, international expansion, financing transactions, subjective technical matters and regulatory compliance. Ms. Morrison is a certified public accountant and has extensive experience in accounting, finance, mergers and acquisitions and capital markets transactions.

|

John J. Roberts, age 73 Director since: 2003 Safeguard Board Committees: Audit, Compensation, Nominating & Corporate Governance (Chair) |

Other public directorships: Armstrong World Industries, Inc., Vonage Holdings Corp., Inc. and Trustee, Pennsylvania Real Estate Investment Trust Former public directorships within past five years: None |

Career Highlights:

| — | Global Managing Partner and a Member of the Leadership Team, PricewaterhouseCoopers LLP at the time of his retirement in June 2002, completing a 35-year career with the professional services firm during which he served in a variety of client service and operating positions |

Experience and Qualifications: Mr. Roberts is a certified public accountant and has extensive experience in corporate finance and accounting; capital markets transactions; debt and equity financings; global strategic planning, corporate development and operations management; management and technology consulting; risk management; and merger and acquisition transactions. He also has extensive public and private company board service experience, including service on multiple audit committees.

| 17 |

|

Robert J. Rosenthal, PhD, age 61 Chairman of the Board (effective May 2016) Director since: 2007 Safeguard Board Committees: None* |

Other public directorships: Bruker Corporation Former public directorships within past five years: None |

*As our current Chairman of the Board, Dr. Rosenthal is an ex officio member of each of our standing committees.

Career Highlights:

| — | Chief Executive Officer and director, Taconic Biosciences, Inc., a provider of research models for pharmaceutical and biotechnology researchers (June 2014 – present) |

| — | Chairman and Chief Executive Officer, IMI Intelligent Medical Implants, AG, a medical technology company that developed an intelligent retinal implant for degenerative retinal disorders (January 2010 – December 2013) |

| — | President and Chief Executive Officer, Magellan Biosciences, Inc., a provider of clinical diagnostics and life sciences research tools (October 2005 – December 2009) |

| — | President and Chief Executive Officer, TekCel, Ltd., a provider of life sciences research tools (October 2003 – January 2007) |

| — | President and Chief Executive Officer, Boston Life Sciences, Inc., a diagnostic and therapeutic development company (July 2002 – October 2003) |

| — | President and Chief Executive Officer, Magellan Discovery Technologies, LLC, a life sciences acquisition company (January 2001 – July 2002) |

| — | Senior Vice President, Perkin Elmer Corporation and President of its instrument division (March 1999 – November 2000) |

| — | Various executive positions, Thermo Optek Corporation (September 1995 – February 1999) |

Experience and Qualifications: Dr. Rosenthal has 30 years of experience relating to companies involved in the development of diagnostics, therapeutics, medical devices and life sciences tools and technologies. His specific experience includes strategic planning and positioning; corporate, business and product development; operations management; capital markets transactions; debt and equity financings; fund-raising; merger and acquisition transactions; and corporate finance. Dr. Rosenthal also has significant public and private company board experience.

Names of Officers and Biographical Information

| Name | Age | Position | Executive Officer Since | ||

| Stephen T. Zarrilli | 56 | President, Chief Executive Officer and Director | 2008 | ||

| Jeffrey B. McGroarty | 48 | Senior Vice President and Chief Financial Officer | 2012 | ||

| Brian J. Sisko | 57 | Chief Operating Officer, Executive Vice President and Managing Director | 2007 |

Mr. Zarrilli joined Safeguard as Senior Vice President and Chief Financial Officer in June 2008 and became President and Chief Executive Officer in November 2012. Prior to joining Safeguard, Mr. Zarrilli co-founded, in 2004, the Penn Valley Group, a middle-market management advisory and private equity firm, and served as a Managing Director there until June 2008. Mr. Zarrilli also served as Acting Senior Vice President, Acting Chief Administrative Officer and Acting Chief Financial Officer of Safeguard from December 2006 to June 2007. Mr. Zarrilli also served as the Chief Financial Officer, from 2001 to 2004, of Fiberlink Communications Corporation, a provider of mobile access solutions for large enterprises; as the Chief Executive Officer, from 2000 to 2001, of Concellera Software, Inc., a developer of content management software; as the Chief Executive Officer, from 1999 to 2000, and Chief Financial Officer, from 1994 to 1998, of US Interactive, Inc. (at the time a public company), a provider of Internet strategy consulting, marketing and technology services; and, previously, with Deloitte & Touche from 1983 to 1994. Mr. Zarrilli is a director of Virtus Investment Partners, Inc. and currently serves as Chair of the Audit Committee and, until June 2015, was a director and Chairman of the Audit Committee of NutriSystem, Inc.

| 18 |

Mr. McGroarty joined Safeguard as Vice President and Corporate Controller in December 2005, subsequently became Vice President - Finance and Corporate Controller, and served as Senior Vice President - Finance from November 2012 until his promotion to Senior Vice President and Chief Financial Officer in April 2013. Prior to joining Safeguard, Mr. McGroarty served as Interim Controller of Cephalon, Inc. from October 2005 to December 2005; Vice President-Financial Planning & Analysis and previously Assistant Controller at Exide Technologies from March 2002 to September 2005; and, previously, with PricewaterhouseCoopers from 1991 to 2001.

Mr. Sisko joined Safeguard as Senior Vice President and General Counsel in August 2007 and served as Executive Vice President and Managing Director from November 2012 until his promotion to Chief Operating Officer, Executive Vice President and Managing Director in January 2014. Prior to joining Safeguard, Mr. Sisko served as Chief Legal Officer, Senior Vice President and General Counsel of Traffic.com (at the time, a public company), a former partner company of Safeguard, from February 2006 until June 2007 (following its acquisition by NAVTEQ Corporation in March 2007); Chief Operating Officer from February 2005 to January 2006 of Halo Technology Holdings, Inc., a public holding company for enterprise software businesses (Halo Technology Holdings filed for bankruptcy protection under Chapter 11 of the United States Bankruptcy Code in August 2007); ran B/T Business and Technology, an advisor and strategic management consultant to a variety of public and private companies, from January 2002 to February 2005; and was a Managing Director from April 2000 to January 2002, of Katalyst, LLC, a venture capital and consulting firm. Mr. Sisko also previously served as Senior Vice President-Corporate Development and General Counsel of National Media Corporation, at the time a New York Stock Exchange-listed multi-media marketing company with operations in 70 countries, and as a partner in the corporate finance, mergers and acquisitions practice group of the Philadelphia-based law firm, Klehr, Harrison, Harvey, Branzburg LLP.

Skills and Qualifications of Board

The following table includes the skills and qualifications of each director that led our Board to conclude that the director is qualified to serve on our Board.

| George MacKenzie |

Russell Glass |

Ira Lubert |

Maureen Morrison |

John Roberts |

Robert Rosenthal |

Stephen Zarrilli |

Julie Dobson |

Stephen Fisher | |||||||||

| Operational / Direct Management Experience | ü | ü | ü | ü | ü | ü | ü | ü | ü | ||||||||

| Capital Markets Experience | ü | ü | ü | ü | ü | ü | ü | ü | ü | ||||||||

| Private Equity / Venture Capital Industry Experience | ü | ü | ü | ü | ü | ü | ü | ü | ü | ||||||||

| Financial Expertise / Literacy | ü | ü | ü | ü | ü | ü | ü | ü | ü | ||||||||

| C-level Experience | ü | ü | ü | ü | ü | ü | ü | ü | |||||||||

| Other Public / Private Director Experience | ü | ü | ü | ü | ü | ü | ü | ü |

Audit Committee. The Audit Committee held four meetings during 2017. The Audit Committee’s responsibilities, which are described in detail in its charter, include, among other duties, the responsibility to:

| · | Assist the Board in fulfilling its responsibilities regarding general oversight of the integrity of Safeguard’s financial statements, Safeguard’s compliance with legal and regulatory requirements and the performance of Safeguard’s internal audit function; |

| · | Interact with and evaluate the performance, qualifications and independence of Safeguard’s independent registered public accounting firm; |

| · | Review and approve related party transactions; and |

| · | Prepare the report required by SEC regulations to be included in the proxy statement. |

| 19 |

The Audit Committee has the sole authority to retain, set compensation and retention terms for, terminate and oversee the relationship with Safeguard’s independent registered public accounting firm (which reports directly to the Audit Committee). The Audit Committee also oversees the activities of the internal auditor, reviews the effectiveness of the internal audit function and approves the appointment of the internal auditor. The Audit Committee has the authority to obtain advice, counsel and assistance from internal and external legal, accounting or other advisors as the Audit Committee deems necessary to carry out its duties and to receive appropriate funding from Safeguard for such advice and assistance. Although the Audit Committee has the powers and responsibilities set forth in its charter, its role is oversight, and management has primary responsibility for the financial reporting process of Safeguard.

The Board has determined that each member of the Audit Committee meets the independence requirements established by SEC regulations, the NYSE listing standards and our Corporate Governance Guidelines. The Board has determined that Ms. Morrison, Mr. Roberts and Dr. Rosenthal are “audit committee financial experts” within the meaning of the SEC regulations, and the Board has determined that each member of the Audit Committee has accounting and related financial management expertise within the meaning of the NYSE listing standards. The Board previously determined that Mr. MacKenzie, who is not standing for re-election at this year’s annual meeting, was an “audit committee financial expert” within the meaning of the SEC regulations. Mr. Roberts serves as a member of the audit committee of the board of directors of four publicly traded companies, including our Audit Committee. The Board has determined that such simultaneous service does not impair Mr. Roberts’ ability to effectively serve on our Audit Committee.

| 20 |

Code of Business Conduct and other Charters.

Safeguard’s Corporate Governance Guidelines, Code of Business Conduct and Ethics, Audit Committee Charter, Compensation Committee Charter and Nominating & Corporate Governance Committee Charter are available at www.safeguard.com/governance. The Code of Business Conduct and Ethics is applicable to all employees of Safeguard, including each of our executive and financial officers, and the members of our Board. Safeguard will post information regarding amendments to or waivers from our Code of Business Conduct and Ethics (to the extent applicable to Safeguard’s directors or executive officers) in the Corporate Governance section of our website. Our website is not part of this report. All references to our website address are intended to be inactive textual references only.

Section 16(a) Beneficial Ownership Reporting Compliance.

Section 16(a) of the Securities Exchange Act of 1934 requires our directors, executive officers and greater than 10% holders of our common stock to file with the SEC reports of ownership of our securities and changes in ownership of our securities. Based solely on our review of the copies of reports we have received and upon written representations from the reporting persons that no Form 5 reports were required to be filed by those persons, Safeguard believes there were no late filings by our directors and executive officers during 2017. There were no known holders of greater than 10% of our common stock during 2017 who failed to file the required reports.

| ITEM 11. | EXECUTIVE COMPENSATION |

Compensation Discussion and Analysis

Executive Summary

Our Compensation Committee (for purposes of this discussion, the “Committee”) is responsible for establishing our company-wide compensation philosophy and practices, for determining the compensation for our “named executive officers,” and for approving the compensation for our other senior executives, based on the recommendations of our President and Chief Executive Officer. This Compensation Discussion and Analysis describes our executive compensation program and the compensation decisions made for 2017 for our named executive officers. At December 31, 2017, there were three individuals serving as named executive officers of Safeguard:

| Stephen T. Zarrilli | President and Chief Executive Officer | |

| Jeffrey B. McGroarty | Senior Vice President and Chief Financial Officer | |

| Brian J. Sisko | Chief Operating Officer, Executive Vice President and Managing Director |

Our senior executive group is currently comprised of a total of six executives with the title of Senior Vice President or higher, including our current three named executive officers. This Compensation Discussion and Analysis (“CD&A”) also describes programs that apply to our senior executive group as a whole.

In January 2018, the Company announced that, effective immediately, the Company would cease making capital deployments into any new partner company opportunities and that it would focus its efforts on managing and financially supporting its existing partner companies to exit events, and ultimately returning the net proceeds of such efforts to its shareholders. This strategy is sometimes referred to in this CD&A as the “New Strategy.” Further, on April 6, 2018, the Company announced that the Company promoted Mr. Sisko to the position of President and Chief Executive Officer, effective as of July 1, 2018, to succeed Mr. Zarrilli. Mr. Zarrilli will act as a special advisor to the Company through September 30, 2018 and then retire. In addition, Mr. McGroarty will depart from the Company, effective June 30, 2018. David Kille, currently the Company’s Corporate Controller, will assume the role of Chief Financial Officer, effective June 1, 2018.

| 21 |

Other than as specifically noted, the discussion set forth in this CD&A concerning the Company’s compensation policies and practices, relates to periods prior to the establishment of the New Strategy and, therefore, does not necessarily reflect policies and practices that will prevail or apply under the New Strategy. Set forth below under the heading “New Strategy - Changes in Compensation Policies and Practices” is a summary regarding changes in compensation policies and practices recently adopted by the Committee in the context of the New Strategy.

2017 Business Highlights

Highlights of the year are included below because the Committee believes senior executive compensation should correlate with Safeguard’s performance.

Overall, the Committee believes that Safeguard executed well against its 2017 strategic plan.

| · | We deployed $36.8 million of additional capital to support the growth of partner companies in which we already had an interest at December 31, 2016. |

| · | Most of our partner companies performed on or ahead of plan, with year over year revenue growth in excess of 23%. |

| · | We returned an aggregate of $16.9 million to our balance sheet, consisting of $15.5 million in cash related to the sale of our interest in Nexxt, Inc., formerly Beyond.com, and $1.4 million from escrows related to prior years’ transactions. |

| · | In addition, we received a $10.5 million promissory note bearing 9.5% interest payable on or before March 1, 2020 in connection with the Beyond.com transaction. |

| · | We repurchased an aggregate of $14 million of our outstanding convertible debentures. |

| · | We entered into a $75 million debt facility with HPS Investment Partners, LLC. |

Key 2017 Compensation Decisions

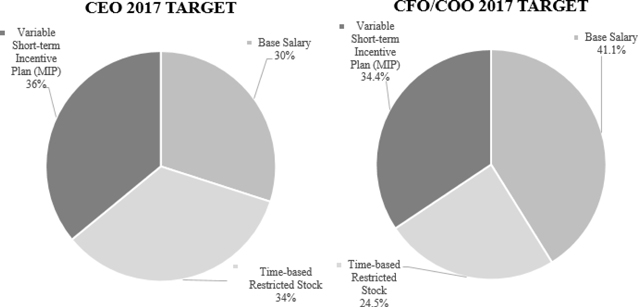

| · | The 2017 base salaries and target management incentive plan awards for Messrs. Zarrilli, McGroarty and Sisko were unchanged from their 2016 levels. |

| · | After reviewing Safeguard’s performance against the objectives set forth in the 2017 management incentive plan, the Committee approved a 90% achievement level in the partner company performance component of the corporate objectives and a 60% achievement level in overall corporate performance, resulting in a 75% payout (against targeted amounts) to our named executive officers. While the Committee believed the year included positive results in corporate operations, and in most of the partner companies, Safeguard did not meet all of our objectives, particularly in the returns provided to shareholders. |

| · | As part of the deliberations regarding long-term incentive awards made to our management team, the Committee reviewed the competitive market data provided by its consultant, the individual performance of each of our named executive officers and an assessment of the long-term compensation element relative to our peers. Based on such review and taking into consideration that no deployments were made in 2017 into new partner companies and, therefore, a pool of new partner companies to measure performance against does not exist, for the grants made in 2017, the Committee (1) chose to reduce the opportunity to earn long-term incentives by approximately 40% for each of Messrs. Zarrilli, McGroarty and Sisko as compared to the grants made in 2016 and (2) awarded such incentives solely in the form of restricted stock grants subject to time-based vesting. This compares to the value of the 2016 grants that were awarded at a ratio of 1/3 in time-based restricted stock and 2/3 in performance based stock units. |

| 22 |

Effective Corporate Governance Principles

Below is a summary of what we did and what we didn’t do relating to executive compensation during and related to 2017, and prior to our announcement of the New Strategy:

| WHAT WE DID: | |

| ü | Emphasized variable pay for performance by linking our named executive officers’ target incentive compensation to Safeguard’s financial performance and the attainment of specified metrics |

| ü | Maintained short-term and long-term incentive programs with distinct performance-based measures |

| ü | Emphasized a long-term orientation under our equity compensation program by requiring a minimum service vesting period for performance-based equity grants if the performance hurdles are achieved in the near term |

| ü | Applied double-trigger change of control vesting of equity awards made to our senior executives |

| ü | Retained an independent compensation consulting firm that provides no other services to Safeguard |

| ü | Maintained a compensation recoupment policy that will permit us to seek reimbursement of cash and incentive compensation and/or equity grants in certain instances of financial statement restatement |

| ü | Maintained meaningful stock ownership guidelines for our senior executives and Board members |

| WHAT WE DIDN’T DO: | |

| Ä | Provide golden parachute excise tax or other tax gross-ups upon a change in control |

| Ä | Provide any material perquisites |

| Ä | Permit repricing of underwater options without shareholder approval |

| Ä | Grant stock option awards or stock appreciation rights (“SARs”) below 100% of fair market value |

| Ä | Permit hedging or short-sales transactions in our stock by our senior executives, or permit the use of Safeguard stock as collateral for indebtedness by our executive officers |

| Ä | Provide a pension plan or special retirement program other than our 401(k) plan, which is available to all employees |

| Ä | Provide post-retirement health coverage |

The Committee reviews our compensation philosophy each year to ensure that its principles and objectives are aligned with our overall business strategy and aligned with the interests of our shareholders. We seek to apply a consistent philosophy across our executive group, not just among our named executive officers.

| 23 |

Compensation Philosophy and Objectives

Our overall goals in compensating our executives in 2017 were as follows:

| · | Attract, retain and motivate executives whose experience and skills could be leveraged across our partner companies to facilitate the partner companies’ growth, success and ultimate monetization; |

| · | Promote and reward the achievement of short-term and long-term corporate and individual objectives that our Board and management believe will lead to long-term growth in shareholder value; and |

| · | Encourage meaningful equity ownership and the alignment of executive and shareholder interests as an incentive to increase shareholder value. |

Our executive compensation program in 2017 was intended to:

| · | Provide a mix of fixed and variable at-risk cash compensation; |

| · | Balance rewards for short-term performance with our ultimate goal of producing long-term shareholder value; |

| · | Link variable compensation to specific, identifiable metrics that demonstrate value creation for Safeguard; and |

| · | Facilitate executive retention. |

In January 2018, Safeguard announced the New Strategy. See “New Strategy - Changes in Compensation Policies and Practices” below.

Role of the Compensation Committee in Compensation Decisions