Attached files

| file | filename |

|---|---|

| EX-23.3 - EX-23.3 - Carbon Black, Inc. | a2235264zex-23_3.htm |

| EX-23.1 - EX-23.1 - Carbon Black, Inc. | a2235264zex-23_1.htm |

| EX-10.14 - EX-10.14 - Carbon Black, Inc. | a2235264zex-10_14.htm |

| EX-10.13 - EX-10.13 - Carbon Black, Inc. | a2235264zex-10_13.htm |

| EX-10.12 - EX-10.12 - Carbon Black, Inc. | a2235264zex-10_12.htm |

| EX-10.11 - EX-10.11 - Carbon Black, Inc. | a2235264zex-10_11.htm |

| EX-10.5 - EX-10.5 - Carbon Black, Inc. | a2235264zex-10_5.htm |

| EX-5.1 - EX-5.1 - Carbon Black, Inc. | a2235264zex-5_1.htm |

| EX-4.1 - EX-4.1 - Carbon Black, Inc. | a2235264zex-4_1.htm |

| EX-3.4 - EX-3.4 - Carbon Black, Inc. | a2235264zex-3_4.htm |

| EX-3.2 - EX-3.2 - Carbon Black, Inc. | a2235264zex-3_2.htm |

| EX-3.1 - EX-3.1 - Carbon Black, Inc. | a2235264zex-3_1.htm |

| EX-1.1 - EX-1.1 - Carbon Black, Inc. | a2235264zex-1_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on April 23, 2018.

Registration No. 333-224196

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Carbon Black, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

7372 (Primary Standard Industrial Classification Code Number) |

55-0810166 (I.R.S. Employer Identification Number) |

1100 Winter Street

Waltham, Massachusetts 02451

(617) 393-7400

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Patrick Morley

President and Chief Executive Officer

Carbon Black, Inc.

1100 Winter Street

Waltham, Massachusetts 02451

(617) 393-7400

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||||

Kenneth J. Gordon, Esq. Jared J. Fine, Esq. Goodwin Procter LLP 100 Northern Avenue Boston, Massachusetts 02210 (617) 570-1000 |

Eric J. Pyenson, Esq. Senior Vice President and General Counsel Carbon Black, Inc. 1100 Winter Street Waltham, Massachusetts 02451 (617) 393-7400 |

Rachel Sheridan, Esq. John Chory, Esq. Latham & Watkins LLP 1000 Winter Street, Suite 3700 Waltham, Massachusetts 02451 (781) 434-6700 |

||

Approximate date of commencement of proposed sale to public:

As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o Emerging growth company ý |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ý

CALCULATION OF REGISTRATION FEE

|

||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered(1) |

Proposed Maximum Offering Price Per Share |

Proposed Maximum Aggregate Offering Price(2) |

Amount of Registration Fee(3) |

||||

|---|---|---|---|---|---|---|---|---|

Common stock, $0.001 par value per share |

9,200,000 | $17.00 | $156,400,000 | $19,472 | ||||

|

||||||||

- (1)

- Includes

shares that the underwriters have the option to purchase to cover over-allotments, if any.

- (2)

- Estimated

solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended.

- (3)

- The Registrant previously paid $12,450.00 of the total registration fee in connection with a previous filing of this Registration Statement.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued April 23, 2018

8,000,000 Shares

![]()

COMMON STOCK

Carbon Black, Inc. is offering 8,000,000 shares of its common stock. This is our initial public offering and no public market currently exists for our shares. We anticipate that the initial public offering price will be between $15.00 and $17.00 per share.

We have applied to list our common stock on The Nasdaq Global Select Market under the symbol "CBLK."

We are an "emerging growth company" as defined under the federal securities laws and, as such, have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings. Investing in our common stock involves risks. See "Risk Factors" beginning on page 18.

PRICE $ A SHARE

| |

Price to Public |

Underwriting Discounts and Commissions |

Proceeds to Company(1) |

|||

|---|---|---|---|---|---|---|

| | | | | | | |

Per share |

$ | $ | $ | |||

Total |

$ | $ | $ |

(1) We have agreed to reimburse the underwriters for certain FINRA-related expenses. See "Underwriters."

We have granted the underwriters the right to purchase up to an additional 1,200,000 shares of common stock to cover over-allotments at the initial public offering price less underwriting discounts and commissions.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on , 2018.

| MORGAN STANLEY | J.P. MORGAN | |||||

KEYBANC CAPITAL MARKETS |

WILLIAM BLAIR |

RAYMOND JAMES |

COWEN |

|||

, 2018.

TABLE OF CONTENTS

Neither we nor the underwriters have authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. Neither we nor the underwriters take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock.

For investors outside of the United States: Neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required other than in the United States. Persons who come into possession of this prospectus and any applicable free writing prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus and any such free writing prospectus applicable to that jurisdiction.

i

This summary highlights selected information that is presented in greater detail elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including the sections titled "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision. Unless the context indicates otherwise, the terms "Carbon Black," "company," "we," "us," "our" and "our company" in this prospectus refer to Carbon Black, Inc. and its consolidated subsidiaries.

CARBON BLACK, INC.

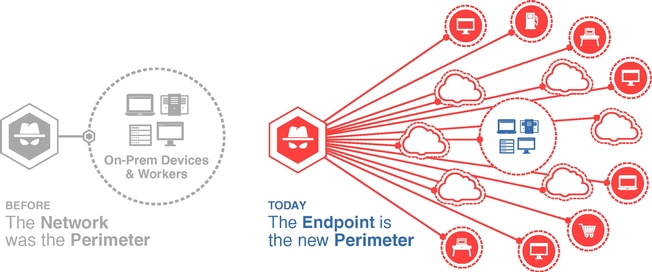

Carbon Black is a leading provider of next-generation endpoint security solutions. Our predictive security cloud platform continuously captures, records and analyzes rich, unfiltered endpoint data. We believe the depth, breadth and real-time nature of our endpoint data, combined with the strength of our analytics platform, provides customers with the most robust and data-intensive solution to address the complete endpoint security lifecycle. Our solutions enable customers to predict, prevent, detect, respond to and remediate cyber attacks before they cause a damaging incident or data breach.

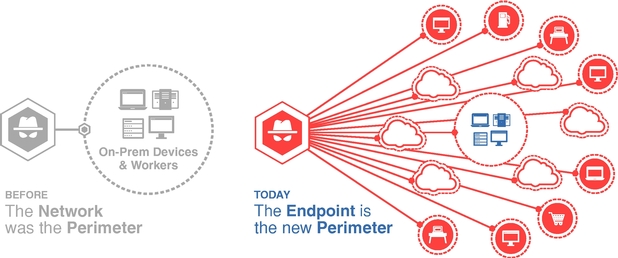

Organizations globally are re-platforming their IT by investing in cloud computing and workforce mobility, which has resulted in enterprise environments that are more open, interconnected, and vulnerable to cyber attacks. In the past, knowledge workers only had access to applications and data inside the corporate network perimeter, which were firewalled off from potential cyber threats. Today, an increasingly mobile workforce and the explosion of enterprise data and applications in the cloud have expanded the attack surface beyond the traditional network perimeter. In response, cyber attackers have adapted their attack methods and tools to directly target the endpoint. In short, the endpoint is the new perimeter.

Endpoints are the primary focus of attacks because they store valuable data that attackers seek to steal; perform critical operations that attackers seek to disrupt; and are the interface where attackers can target humans through email, social engineering and other tactics. Endpoints are the physical and virtual locations where sensitive data resides and include desktops, laptops, servers, virtual machines, cloud workloads (services running on cloud servers), fixed-function devices such as ATMs, point of sale systems, and control and data systems for power plants and other industrial assets.

1

Based on our experience and investment in next-generation solutions designed to address the full endpoint security lifecycle—predict, prevent, detect, respond to and remediate—we have developed a highly differentiated technology approach with four main pillars:

- 1.

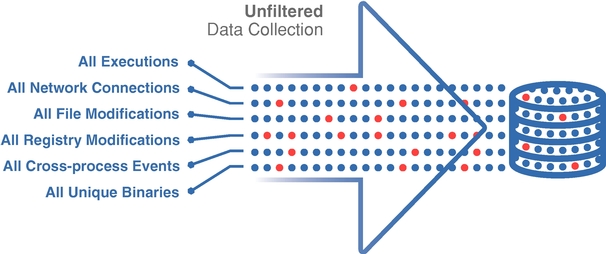

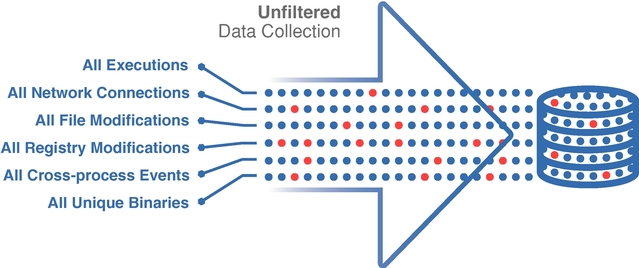

- Unfiltered data collection: Our technology uniquely collects complete, "unfiltered" endpoint data by continuously recording endpoint activity and centrally storing the collected data for advanced analytics. Other vendors take a "filtered" approach by capturing a subset of data at select points in time. Unfiltered data is more comprehensive, provides greater visibility and we believe offers more effective security capabilities.

- 2.

- Proprietary

data shaping technology: Our unfiltered data approach, which we believe is fundamental to deliver the most effective

endpoint security, required us to overcome several difficult technical challenges, which we refer to as the "edge to cloud data pipeline problem." These challenges centered on how to reliably collect

and cost effectively analyze and store massive amounts of data from edge devices (i.e., endpoints) in the cloud. To address those challenges, we have developed proprietary data shaping

technology that smooths bursts of endpoint data activity; optimizes bandwidth demands to move massive amounts of endpoint data; compresses data at a high ratio to reduce the cost of storing massive

amounts of data; and leverages a graph-like custom model for endpoint data that allows analysis of the data in multiple ways for multiple use cases. We believe our proprietary data shaping technology

creates a strong and lasting competitive advantage not just in endpoint security, but also as we seek to disrupt and consolidate adjacent security markets that leverage endpoint data.

- 3.

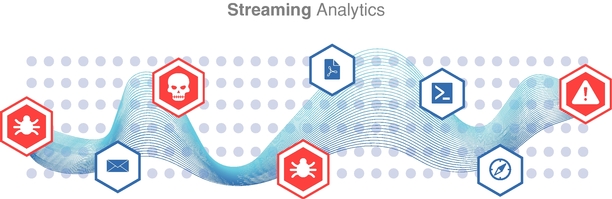

- Streaming analytics: We analyze endpoint data at massive scale leveraging event stream processing technology, which evaluates and classifies a continuously updated stream of events based on their risk level. We also employ machine learning and other advanced analytic techniques.

2

- 4.

- Extensible and open architecture: Our open architecture was designed to integrate with leading security technologies and IT products used by our customers. Moreover, endpoint data is the fuel that powers multiple security products across an organization's security stack. Our open architecture, when combined with the value of our data, positions our platform to serve as the hub of security activity in a customer's IT organization and enables deep customer relationships.

We have a strong heritage of innovative technology leadership in multiple endpoint security categories: application control, endpoint detection and response, or EDR, and next-generation antivirus, or NGAV. Our flagship solutions are technology leaders in each of these categories, and we are integrating each with our predictive cloud platform. Unlike legacy security products that install an agent and collect data specific to its domain or use case, our platform provides a single agent that continuously collects unfiltered endpoint data to address the entire endpoint security lifecycle, which today is addressed by multiple point products. We believe that we are well positioned to continue serving the $6.5 billion endpoint security market.

We focus on solutions that enable organizations to address the entire security lifecycle of an endpoint and integrate endpoint security within their cyber security architecture. We are transforming cyber security with our predictive security cloud, which positions us to address adjacent security use cases requiring endpoint data, such as IT asset management, public cloud security software and security and vulnerability management, which, according to IDC, represented markets of $1.9 billion, $5.3 billion and $5.4 billion, respectively, in 2016. This presents us with the opportunity to extend into adjacent security markets, and potentially expand our market opportunity, from $6.5 billion to $19.1 billion. While we have not yet penetrated these adjacent security markets, and there are multiple challenges associated with doing so, we believe that we can leverage the unfiltered endpoint data, proprietary data shaping technology, streaming analytics capabilities and extensible open architecture of our predictive security cloud to address adjacent security use cases and the market opportunities that they present through the development of additional product functionality.

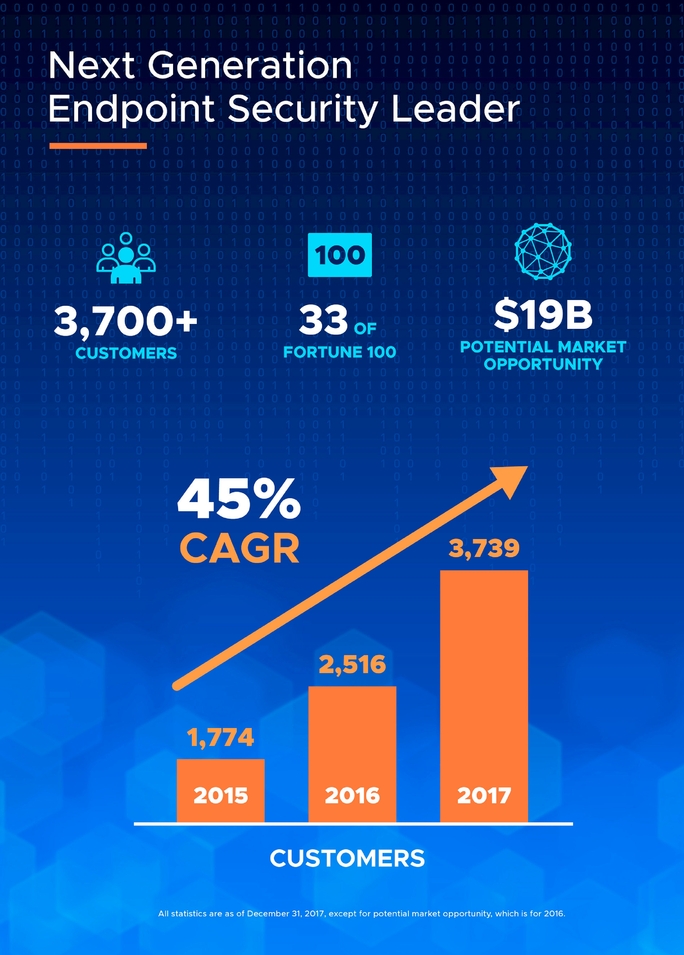

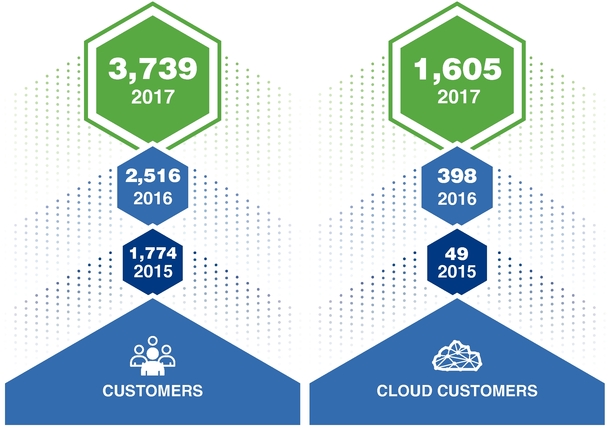

Our customers include many of the world's largest, security-focused enterprises and government agencies that are among the most heavily targeted by cyber adversaries, as well as mid-sized organizations. We serve over 3,700 customers globally across multiple industries, including 33 of the Fortune 100. Our solutions address the needs of a diverse range of customers. Over 70 security technology companies, including industry leaders such as VMware, Inc., or VMware, Splunk Inc., and the International Business Machines Corporation, or IBM, have integrated their products with Carbon Black to access our unfiltered endpoint data.

We primarily sell our products through a channel go-to-market model, which significantly extends our global market reach and ability to rapidly scale our sales efforts. Our inside sales and field sales representatives work alongside an extensive network of value-added resellers, or VARs, distributors, managed security service providers, or MSSPs, and incident response, or IR, firms. Our MSSP and IR firm channel partners both use and recommend our products to their clients. We have established significant

3

relationships with leading channel partners, including the CDW Corporation, one of the world's largest software VARs; Arrow Electronics, Inc., a major global distributor; SecureWorks, Inc., a leading MSSP; and Kroll Inc., or Kroll, a leading IR firm. In addition, we have technology and go-to-market partnerships with both IBM and VMware, enabling us to leverage their sales organizations to reach their large customer bases. In the three months ended December 31, 2017, 94% of our new and add-on business was closed in collaboration with a channel partner.

We have experienced strong revenue growth, with revenue increasing from $70.6 million in 2015 to $116.2 million in 2016 and $162.0 million in 2017, representing a 51% compound annual growth rate over the same period. We have a subscription-based revenue model that provides visibility into future revenue. Recurring revenue represented 77%, 83% and 88% of our total revenue in 2015, 2016 and 2017, respectively. Annual recurring revenue, or ARR, was $76.8 million, $124.2 million and $174.2 million as of December 31, 2015, 2016 and 2017, respectively. We define ARR as the annualized value of all active subscription contracts as of the end of the period. ARR excludes revenue from perpetual licenses and services. The portion of ARR related to our cloud-based subscription contracts was $2.5 million, $15.1 million and $46.0 million as of December 31, 2015, 2016 and 2017, respectively. The percentage of our total recurring revenue generated by sales of our cloud-based solutions was negligible in 2015, 7% in 2016 and 18% in 2017. We incurred net losses of $38.7 million in 2015, $44.6 million in 2016 and $55.8 million in 2017 as we continued to invest for growth to address the large market opportunity for our platform.

Cyber security is critical to organizations as they face an increasingly hostile threat environment with a growing number of cyber adversaries launching stealthy, sophisticated and targeted attacks. The following major trends are driving strong and growing demand for our products:

Endpoints are the new front line in the cyber war, and organizations are shifting their defenses as a result

The attack surface is expanding. Workforce mobility is increasing the number of connected devices that operate outside the traditional network perimeter, which is expanding the potential "attack surface." Moreover, enterprises are increasing their use of public clouds for a broad range of services, such as virtual machines, cloud workloads and cloud-based applications. As a result, enterprises' critical data and operations have increasingly shifted outside of their traditional network defenses, and the importance of protecting their endpoint devices has become paramount.

Endpoints are the primary target of cyber attacks. Endpoints are the primary targets of attacks because these devices store valuable data and intellectual property and are the interface where attackers can target humans through email, social engineering techniques, keylogging and other tactics.

Endpoint data is critical to an effective cyber security program. Effective security critically depends on having complete visibility into what is happening on each endpoint. Multiple categories of security products, from vulnerability assessment to patch management, require endpoint data for their core functionality.

Organizations are shifting their defenses to focus on next-generation endpoint security solutions. Because network-centric security is no longer adequate, organizations must focus on securing the endpoint. The majority of endpoint security technology in use today relies on multiple agents and uses the same ineffective, traditional signature-based antivirus software originally designed more than 20 years ago. As a result, organizations are increasingly shifting their security budgets toward next-generation endpoint security solutions.

4

With the continued success of cyber attacks, organizations are shifting from a passive prevention-only response to a holistic approach. Historically, organizations have relied on passive prevention-only technologies that sought to block attackers from penetrating the network perimeter and protect corporate endpoints and data. This limited, passive prevention-only approach has proven inadequate and the number of successful cyber attacks has continued to grow. Organizations are shifting to a holistic and active security approach that requires next-generation technologies to predict, prevent, detect, respond to and remediate today's advanced cyber attacks.

The cyber threat is large, sophisticated and growing and requires new and more advanced approaches to combat it

Cyber security is a board-level issue and a focal point for governments worldwide. The ongoing occurrence and devastating consequences of high profile cyber attacks have elevated cyber security to a top priority for executives. Additionally, due to the financial, operational and reputational risks of breaches and non-compliance with regulatory requirements, C-level security officers are now commonplace and cyber security strategy is a critical focus area for boards of directors.

The rise of ransomware has made every organization a potential target. In the past, cyber attackers tended to target entities that held commercially valuable data that could be stolen and used for financial gain. However, with the emergence and proliferation of ransomware in recent years, cyber attackers now target organizations regardless of type or size to extort money by holding computers and data hostage.

Today's attacks are stealthy, sophisticated and targeted. Today's organizations face a complex threat landscape with a broad range of well-funded cyber attackers who use techniques designed to circumvent traditional security approaches. Less skilled attackers can purchase these attacks through cybercrime marketplaces on the "Dark Web," leading to a widespread proliferation of successful, advanced attacks. Once an organization has been breached, attackers can move unseen for months or even years, exfiltrating a larger amount of data and intellectual property. The longer these invisible breaches remain undetected, the greater the costs and reputational damage they can cause.

The shortage of security talent creates a need for next-generation solutions. The continuous growth in the number and sophistication of cyber attacks and the expansion of the attack surface are driving the need for more security professionals with deeper expertise. As the number of threats multiplies, legacy solutions either miss threats or produce more alerts than security teams are able to process and investigate. The number of security professionals has not kept pace with total demand. Organizations are increasingly turning to next-generation solutions, advanced analytics and automation tools to empower their security professionals to increase their efficiency and focus on the highest value cyber security tasks, thereby reducing the need for additional security headcount.

We believe that our cloud platform addresses a significant capability gap in the enterprise endpoint security market and that our solutions will address an increasing subset of additional use cases in public cloud security software, security and vulnerability management and IT asset management. According to International Data Corporation, or IDC, the market for enterprise endpoint security software, our primary market, was $6.5 billion in 2016 and is expected to reach $8.3 billion by 2021. According to IDC, the market for security and vulnerability management was $5.4 billion in 2016 and is expected to reach $9.0 billion in 2021. According to IDC, the market for public cloud security software was $5.3 billion in 2016 and is expected to reach almost $10.0 billion in 2021. According to IDC, the market for IT asset management was $1.9 billion in 2016 and is expected to reach $2.8 billion in 2021.

5

Powered by the Cb Predictive Security Cloud, our solutions provide best-in-class security by collecting and analyzing unfiltered data from the endpoint, addressing the entire security lifecycle and enabling our customers to continuously improve their security posture.

Our customers use our products to:

- •

- Augment or replace legacy antivirus software;

- •

- Prevent malware and fileless attacks that do not use malware;

- •

- Protect against ransomware;

- •

- Hunt down threats;

- •

- Respond to and remediate security incidents;

- •

- Lock down critical systems and applications;

- •

- Protect fixed-function devices;

- •

- Secure workloads and applications in virtualized and cloud environments;

- •

- Comply with regulatory mandates; and

- •

- Enhance other security products through our unfiltered endpoint data.

Benefits of Our Platform and Solutions

Decreased risk of breach by protecting against known and unknown endpoint attacks

We believe our solutions extend beyond legacy antivirus solutions to detect and stop the widest possible array of cyber attacks, including file-based attacks such as malware and ransomware, as well as next-generation attacks, such as memory-based, PowerShell and script-based attacks. Our solutions apply a full spectrum of technologies to analyze attack patterns in the cloud using richer and more complete endpoint data than any other vendor. According to a MRG Effitas Ltd. efficacy assessment commissioned by us, Cb Defense has a 100% prevention rate against known and unknown ransomware samples. We believe the increased security efficacy from the use of our solutions results in a decreased risk of breach for our customers.

Ability to identify root cause of attacks and quickly respond to security incidents

Our next-generation detection and response capabilities enable organizations and incident responders to rapidly identify the root cause of an attack and the scope of compromise on the network. By capturing unfiltered data, the Cb Predictive Security Cloud provides full visibility into potential threats, both proactively as well as retroactively after a threat is blocked or identified, providing complete details of what happened and what was impacted.

Automated remediation and threat containment

Using the unfiltered data that is continuously collected from each endpoint where our solutions are deployed, our users can launch automated remediation and threat containment actions. These automated capabilities enable organizations to respond to attacks as they happen and minimize the impact and cost of an attack.

6

Continuous enhancement by leveraging intelligence from across the security community

Our solutions allow organizations to continuously improve their security posture, benefiting from ongoing refinement of endpoint hardening and the latest threat intelligence. Through the Cb Predictive Security Cloud, our customers anonymously share data with each other. We believe the ability to share intelligence across our users increases the security expertise of each customer in our community and reduces their need to hire additional security experts.

Seamless integration with other best-of-breed security solutions

Our next-generation endpoint security solutions are designed to integrate seamlessly with other security technologies deployed in an organization's IT environment. Our open architecture enables customers to build their own integrations with other systems across their IT environment. Our emphasis on open architecture and integration with partners at all layers of the security stack enhances an enterprise's security posture, reduces incident response times and increases overall operational efficiency. Ultimately, this ability enables customers to evolve with the dynamic threat landscape and achieve greater utility across their cyber security architecture.

Security efficacy without blocking legitimate activity

Customers require security products that are highly effective in detecting and preventing attacks, while also minimizing the number of "false positive" alerts that interrupt legitimate end-user activity. In order to achieve these dual requirements, we apply an approach that combines endpoint-based prevention models that are optimized for low false positives, with cloud-based detection algorithms that are optimized for low false negatives.

Increased security operations efficiency and less reliance on scarce security talent

Carbon Black solutions enable our customers to significantly improve the efficiency of their security operations and reduce their reliance on additional security professionals through our automated security solutions, streamlined workflow management and access to the collective expertise available in the Cb Predictive Security Cloud.

Greater ability to meet compliance requirements

Our solutions enable organizations to comply with numerous regulatory requirements for data collection, analysis, reporting, archival and retrieval, while also optimizing the overall enterprise cyber security posture.

Ability to deploy endpoint security at any scale and grow and evolve their defenses

Carbon Black products are used by customers of all sizes, from small and medium sized businesses to large global enterprises. We have designed the Cb Predictive Security Cloud to enable customers to easily grow and evolve their defenses. Customers can start by deploying whichever solutions best match their immediate needs and then extend and enhance their deployment over time.

We believe a number of competitive advantages enable us to maintain and extend our leadership position, including:

- •

- Differentiated technology and intellectual property. Our predictive security approach continuously captures unfiltered endpoint activity for real-time and retrospective analysis using our analytics technology that incorporates event stream processing, dynamic and static behavioral analysis, machine learning and reputation analysis and scoring. We believe our unfiltered approach is highly

7

- •

- Extensible next-generation security cloud

platform. The extensible architecture of our platform positions us to enhance and expand our offerings to address evolving customer

needs as the landscape of cyber threats changes over time.

- •

- Pioneers in application

control. We pioneered the zero trust model at the endpoint with Cb Protection, our application control solution, which allows software

to execute only if it is known and explicitly trusted. Building on this foundation, we have enhanced our application control offering by expanding our range of threat prevention options to create the

most effective and complete endpoint prevention solution available in the market.

- •

- Powerful ecosystem based on unfiltered endpoint data and open

platform. In the security ecosystem, endpoints yield the most valuable security data. We believe the endpoint data that we capture is

considered the "gold standard" for the industry and is preferred by leading security vendors. This strategically positions our platform as the system of record for the security industry and we are

therefore an enabler for any other offering in the security market.

- •

- High-leverage channel

model. We believe our partnerships with leading MSSPs and security-focused VARs are a unique competitive differentiator, as enterprises

increasingly engage external experts as trusted advisors to help select security solutions, integrate architectures and manage their ongoing defense posture.

- •

- Partnerships with leading incident response

firms. We have established contractual relationships with more than 100 IR firms, including many industry leaders such as Kroll and

Ernst & Young. We believe our IR partnerships are a significant competitive strength that extends our ability to build sales pipeline and acquire new customers.

- •

- Strategic partnerships with IBM and

VMware. We have established significant and promising partnerships with both IBM and VMware, two of the largest and most influential

technology companies in the world. We believe these relationships are a competitive strength that will enable us to reach the large global customer bases of these technology

leaders.

- •

- Deep security DNA. Our management and technical leadership teams are comprised of cyber security leaders who have deep expertise from leading corporations and government organizations, such as the National Security Agency, the Department of Defense and the Central Intelligence Agency.

scalable and uniquely positions us to address the needs of adjacent security markets by delivering additional products that leverage this data.

The key elements of our growth strategy include:

- •

- Drive new customer growth.

- •

- Expand the use of our solutions by our existing customer base.

- •

- Strengthen relationships with channel distributors and strategic partners.

- •

- Grow our international business.

- •

- Continue to innovate and add new offerings to our platform.

- •

- Increase sales to the U.S. federal government.

- •

- Selectively pursue acquisitions of complementary businesses, technologies and assets.

8

Selected Risks Associated with our Business

Our business is subject to a number of risks and uncertainties, including those highlighted in the section titled "Risk Factors" immediately following this prospectus summary. Some of these risks include:

- •

- We are a rapidly growing company, which makes it difficult to evaluate our future prospects.

- •

- We have not been profitable historically and may not achieve or maintain profitability in the future.

- •

- Our quarterly financial results may fluctuate for a variety of reasons.

- •

- We face intense competition in our market.

- •

- The next-generation endpoint security market is new and evolving, and may not grow as expected.

- •

- If our products fail or are perceived to fail to detect cyber attacks, our business could suffer.

- •

- We rely on channel partners to generate a significant portion of our revenue.

- •

- If we are unable to retain our customers and to sell additional products to our customers, our future revenue and operating results

will be harmed.

- •

- As a cyber security provider, we have been, and expect to continue to be, a target of cyber attacks.

- •

- Our directors, executive officers and principal stockholders will, in the aggregate, own approximately 41.8% of the outstanding shares of our common stock after this offering, which could limit your ability to influence the outcome of key transactions, including a change of control.

Recent Operating Results (Preliminary and Unaudited)

Set forth below are selected preliminary consolidated financial results for the three months ended March 31, 2017 and 2018. Our consolidated financial results for the three months ended March 31, 2018 are not yet available. The following information reflects our preliminary estimates with respect to such results based on currently available information and is subject to change. We have provided ranges, rather than specific amounts, for the preliminary results described below primarily because our financial closing procedures for the three months ended March 31, 2018 are not yet completed and, as a result, our final results upon completion of our closing procedures may differ materially from the preliminary estimates.

Our selected preliminary consolidated financial results presented below for the three months ended March 31, 2017 and 2018 reflect our adoption of Accounting Standard Codification Topic 606, Revenue from Contracts with Customers, or ASC 606, as of January 1, 2018, applied on a full retrospective basis. The anticipated impact of the adoption of ASC 606 on our accounting policies with respect to revenue recognition and capitalization and amortization of costs associated with obtaining a customer contract,

9

such as sales commissions, is described in Note 2 to our consolidated financial statements appearing at the end of this prospectus.

| |

|

Three Months Ended March 31, 2018 |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

Three Months Ended March 31, 2017 |

|||||||||

| |

Low End of Range |

High End of Range |

||||||||

| |

As Adjusted(1) | |||||||||

| |

(unaudited, in thousands) |

|||||||||

Revenue: |

||||||||||

Subscription, license and support |

$ | 33,005 | $ | 44,500 | $ | 44,800 | ||||

Services |

2,940 | 3,000 | 3,200 | |||||||

| | | | | | | | | | | |

Total revenue |

$ | 35,945 | $ | 47,500 | $ | 48,000 | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Loss from operations |

$ |

(12,491 |

) |

$ |

(18,869 |

) |

$ |

(18,369 |

) |

|

Stock-based compensation |

2,207 | 2,578 | 2,578 | |||||||

Amortization of acquired intangible assets |

391 | 391 | 391 | |||||||

Legal settlement |

— | 3,900 | 3,900 | |||||||

| | | | | | | | | | | |

Non-GAAP operating loss(2) |

$ | (9,893 | ) | $ | (12,000 | ) | $ | (11,500 | ) | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Net loss |

$ |

(12,439 |

) |

$ |

(21,600 |

) |

$ |

(21,100 |

) |

|

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

- (1)

- The impact of our adoption of ASC 606 on the preliminary consolidated financial data for the three months ended March 31, 2017 was as follows:

| |

As Previously Reported |

Adjustments for ASC 606 Adoption |

As Adjusted |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

(unaudited, in thousands) |

|||||||||

Revenue: |

||||||||||

Subscription, license and support |

$ | 33,739 | $ | (734 | ) | $ | 33,005 | |||

Services |

3,023 | (83 | ) | 2,940 | ||||||

| | | | | | | | | | | |

Total revenue |

$ | 36,762 | $ | (817 | ) | $ | 35,945 | |||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Loss from operations |

$ |

(12,612 |

) |

$ |

121 |

$ |

(12,491 |

) |

||

Stock-based compensation |

2,207 | — | 2,207 | |||||||

Amortization of acquired intangible assets |

391 | — | 391 | |||||||

| | | | | | | | | | | |

Non-GAAP operating loss |

$ | (10,014 | ) | $ | 121 | $ | (9,893 | ) | ||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Net loss |

$ |

(12,560 |

) |

$ |

121 |

$ |

(12,439 |

) |

||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

The adoption of ASC 606 on a full retrospective basis had the effect of decreasing revenue, decreasing sales commission expense, and decreasing loss from operations, non-GAAP operating loss and net loss from the amounts we previously reported for the three months ended March 31, 2017. Our adoption of ASC 606 had no effect on cash and cash equivalents used in operating, investing or financing activities previously reported in our consolidated statement of cash flows for the three months ended March 31, 2017. The impact of our adoption of ASC 606 on previously reported revenue for other periods prior to adoption of the standard on January 1, 2018 will vary based on the timing of recognition of customer arrangements, and the impact of adoption for the three months ended March 31, 2017 is not necessarily indicative of the impact of adoption that should be expected in any other period.

10

- (2)

- Non-GAAP operating loss is a financial measure not calculated in accordance with U.S. generally accepted accounting principles, or GAAP. For a definition of non-GAAP operating loss, as well as the reasons for which we believe that non-GAAP operating loss is a useful metric for investors and other users of our financial information in evaluating our operating performance, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Key Metrics—Non-GAAP operating loss." We recommend that you review the reconciliation of non-GAAP operating loss to loss from operations, the most directly comparable GAAP financial measure, provided in the table above, and that you not rely on non-GAAP operating loss or any single financial measure to evaluate our business.

In our selected preliminary consolidated financial data above, the increase in revenue from the three months ended March 31, 2017 to the three months ended March 31, 2018 is due primarily to an increase in the number of total customers as well as increased revenue from existing customers as they expanded their use of our solutions. The increases in loss from operations, non-GAAP operating loss and net loss from the three months ended March 31, 2017 to the three months ended March 31, 2018 are due primarily to the addition of personnel in connection with the expansion of our business and other related expenses to support our growth, partially offset by higher revenue. In addition, during the three months ended March 31, 2018, we accrued an expense of $3.9 million in connection with settlement of a lawsuit, as described in Note 21 to our consolidated financial statements appearing at the end of this prospectus. The increase in net loss from the three months ended March 31, 2017 to the three months ended March 31, 2018 is also due to an increase of $2.8 million in the expense associated with the change in the fair value of our warrant liabilities as a result of the quarter-over-quarter increases in the fair values of our common stock and preferred stock.

The selected preliminary consolidated financial data presented above for the three months ended March 31, 2017 and 2018 is preliminary, is not a comprehensive statement of our financial results and is subject to completion of our financial closing procedures. While we have not identified any unusual or unique events or trends that occurred during the period that might materially affect these preliminary estimates, our actual results for the three months ended March 31, 2017 and 2018 will not be available until after this offering is completed. Accordingly, these results may change, and those changes may be material. Further, our preliminary estimated results are not necessarily indicative of the results to be expected for the remainder of 2018 or any future period as a result of various factors, including, but not limited to, those discussed in the sections titled "Risk Factors" and "Special Note Regarding Forward-Looking Statements." Accordingly, you should not place undue reliance upon these preliminary estimates.

This selected preliminary consolidated financial data has been prepared by, and is the responsibility of, our management. PricewaterhouseCoopers LLP has not audited, reviewed, compiled or applied agreed-upon procedures with respect to this preliminary consolidated financial data. Accordingly, PricewaterhouseCoopers LLP does not express an opinion or any other form of assurance with respect thereto.

Corporate Information

We were incorporated in the State of Delaware in December 2002 as Bit 9, Inc. In April 2005, we changed our name to Bit9, Inc. In February 2014, Bit9, Inc. acquired Carbon Black, Inc., which we refer to as the acquired company, and in January 2016, we changed our name to Carbon Black, Inc. Our principal executive offices are located at 1100 Winter Street Waltham, Massachusetts 02451, and our telephone number is (617) 393-7400. Our website address is www.carbonblack.com. The information contained on, or that can be accessed through, our website is not a part of this prospectus. Investors should not rely on any such information in deciding whether to purchase our common stock.

This prospectus contains references to our trademarks, including "Carbon Black," "Bit9" and our logo, and to trademarks belonging to other entities. Solely for convenience, trademarks and trade names

11

referred to in this prospectus, including logos, artwork and other visual displays, may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other companies' trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our most recently completed fiscal year, we qualify as an "emerging growth company" as defined in Section 2(a) of the Securities Act of 1933, as amended, or the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable, in general, to public companies that are not emerging growth companies. These provisions include:

- •

- reduced disclosure of audited and selected financial information;

- •

- an exemption from compliance with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, as

amended, or the Sarbanes-Oxley Act, in the assessment of our internal control over financial reporting;

- •

- reduced disclosure about our executive compensation arrangements;

- •

- exemptions from the requirements to obtain a non-binding advisory vote on executive compensation or a stockholder approval of any

golden parachute arrangements; and

- •

- an exemption from compliance with the requirement of the Public Company Accounting Oversight Board regarding the communication of critical audit matters in the auditor's report on the financial statements.

We may take advantage of these exemptions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company upon the earliest to occur of: the last day of the fiscal year in which we have more than $1.07 billion in annual revenue; the date we qualify as a "large accelerated filer," with at least $700 million in market value of our common stock held by non-affiliates; the issuance, in any three-year period, by us of more than $1.0 billion in non-convertible debt securities; and the last day of the fiscal year ending after the fifth anniversary of this offering.

We are choosing to "opt out" of the provision of the JOBS Act that permits emerging growth companies to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies and, as a result, we will comply with new or revised accounting standards as required when they are adopted. This decision to opt out of the extended transition period is irrevocable.

We have elected to adopt certain of the reduced disclosure requirements available to emerging growth companies. As a result of these elections, the information that we provide in this prospectus may be different than the information you may receive from other public companies in which you hold equity interests. In addition, it is possible that some investors will find our common stock less attractive as a result of these elections, which may result in a less active trading market for our common stock and higher volatility in our stock price.

12

Common stock offered by us |

8,000,000 shares | |

Common stock to be outstanding after this offering |

65,825,141 shares |

|

Over-allotment option to purchase additional shares from us |

We have granted the underwriters an over-allotment option, exercisable for 30 days after the date of this prospectus, to purchase up to an additional 1,200,000 shares from us. |

|

Use of proceeds |

We estimate that the net proceeds from the sale of shares of our common stock in this offering will be approximately $114.1 million (or approximately $132.0 million if the underwriters' over-allotment option to purchase additional shares in this offering is exercised in full), based upon an assumed initial public offering price of $16.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. We currently intend to use a majority of the net proceeds of this offering to invest further in our sales and marketing activities to grow our customer base, to fund our research and development efforts to enhance our technology platform and product functionality, to pay general and administrative expenses and to fund our other growth strategies described elsewhere in this prospectus. We may also use a portion of the net proceeds for the acquisition of complementary businesses, technologies or other assets, although we currently have no agreements, commitments or understandings with respect to any such transaction. See "Use of Proceeds" for additional information. |

|

Risk factors |

See "Risk Factors" for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

|

Proposed Nasdaq Global Select Market symbol |

"CBLK" |

The number of shares of common stock to be outstanding after this offering is based on 57,825,141 shares of common stock outstanding as of March 31, 2018 and excludes:

- •

- 1,805,009 shares of common stock issuable upon the exercise of stock options outstanding under our Amended and Restated 2010

Series A Option Plan as of March 31, 2018, at a weighted-average exercise price of $2.85 per share;

- •

- 89,716 shares of common stock issuable upon the exercise of stock options outstanding under our Amended and Restated Equity Incentive

Plan as of March 31, 2018, at a weighted-average exercise price of $1.18 per share;

- •

- 14,869,768 shares of common stock issuable upon the exercise of stock options outstanding under our 2012 Stock Option and Grant Plan as of March 31, 2018, at a weighted-average exercise price of $5.29 per share;

13

- •

- 837,835 shares of common stock issuable upon the exercise of stock options outstanding under our Carbon Black, Inc. Amended and

Restated 2012 Equity Incentive Plan as of March 31, 2018, at a weighted-average exercise price of $0.86 per share;

- •

- 409,305 shares of common stock issuable upon the exercise of stock options outstanding under our Confer Technologies, Inc. 2013 Stock

Plan as of March 31, 2018, at a weighted-average exercise price of $2.66 per share;

- •

- 273,750 shares of common stock issuable upon the exercise of warrants outstanding as of March 31, 2018, at a weighted-average

exercise price of $4.83 per share;

- •

- 885,823 shares of common stock issuable upon the exercise of stock options approved subsequent to March 31, 2018 by our board

of directors for grant effective upon the pricing of this offering at an exercise price equal to the price to the public listed on the cover page of this prospectus;

- •

- 394,500 shares of common stock issuable from time to time after this offering upon the settlement of restricted stock units, or RSUs,

outstanding as of March 31, 2018; and

- •

- 6,270,650 shares of common stock reserved for future issuance under our 2018 Stock Option and Incentive Plan and 1,735,729 shares of common stock reserved for issuance under our 2018 Employee Stock Purchase Plan, each of which will become effective in connection with this offering and contains provisions that will automatically increase its shares reserved each year, as more fully described in "Executive Compensation—Employee Benefit Plans."

Except as otherwise indicated, the information in this prospectus assumes or gives effect to:

- •

- the filing of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws, each of which

will be in effect upon the closing of this offering;

- •

- the conversion of all outstanding shares of our preferred stock (other than our Series A preferred stock, as described below)

into an aggregate of 44,370,560 shares of common stock upon the closing of this offering;

- •

- the conversion of all outstanding shares of our Series A preferred stock into 1,560,931 shares of common stock upon the closing

of this offering;

- •

- options to purchase shares of our Series A preferred stock outstanding as of March 31, 2018 becoming options to purchase

1,805,009 shares of our common stock, at a weighted-average exercise price of $2.85 per share, upon the closing of this offering;

- •

- options to purchase shares of our Series E-1 preferred stock outstanding as of March 31, 2018 becoming options to

purchase an aggregate of 837,835 shares of our common stock, at a weighted-average exercise price of $0.86 per share, upon the closing of this offering;

- •

- warrants to purchase shares of our Series D preferred stock outstanding as of March 31, 2018 becoming warrants to

purchase an aggregate of 167,500 shares of our common stock, at a weighted-average exercise price of $5.98 per share, upon the closing of this offering;

- •

- no settlement of RSUs or exercise of options or warrants subsequent to March 31, 2018, other than the assumed full exercise on

the date of the closing of this offering of the warrant to purchase 480,848 shares of common stock held by SC US GF Holdings, Ltd., an entity affiliated with Sequoia Capital, at an exercise

price of $0.002 per share;

- •

- a 1-for-2 reverse stock split of our common stock effected on April 20, 2018; and

- •

- no exercise by the underwriters of their over-allotment option to purchase up to an additional 1,200,000 shares of our common stock in this offering.

14

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables present summary consolidated financial data for the periods indicated. You should read this information in conjunction with the sections titled "Selected Consolidated Financial Data" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes and other information included elsewhere in this prospectus. We have derived the summary consolidated statement of operations data for the years ended December 31, 2015, 2016 and 2017 and the summary consolidated balance sheet data as of December 31, 2017 from our audited consolidated financial statements appearing at the end of this prospectus. Our historical results are not necessarily indicative of the results to be expected in any future period.

| |

Year Ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2015 | 2016 | 2017 | |||||||

| |

(in thousands, except per share data) |

|||||||||

Consolidated Statement of Operations Data: |

||||||||||

Revenue: |

||||||||||

Subscription, license and support |

$ | 63,747 | $ | 104,786 | $ | 149,262 | ||||

Services |

6,847 | 11,453 | 12,752 | |||||||

| | | | | | | | | | | |

Total revenue |

70,594 | 116,239 | 162,014 | |||||||

| | | | | | | | | | | |

Cost of revenue: |

||||||||||

Subscription, license and support(1) |

4,492 | 11,296 | 24,217 | |||||||

Services(1) |

8,821 | 9,743 | 11,421 | |||||||

| | | | | | | | | | | |

Total cost of revenue |

13,313 | 21,039 | 35,638 | |||||||

| | | | | | | | | | | |

Gross profit |

57,281 | 95,200 | 126,376 | |||||||

| | | | | | | | | | | |

Operating expenses: |

||||||||||

Sales and marketing(1) |

55,432 | 80,997 | 107,190 | |||||||

Research and development(1) |

24,042 | 36,493 | 52,047 | |||||||

General and administrative(1) |

14,389 | 23,289 | 22,337 | |||||||

| | | | | | | | | | | |

Total operating expenses |

93,863 | 140,779 | 181,574 | |||||||

| | | | | | | | | | | |

Loss from operations |

(36,582 | ) | (45,579 | ) | (55,198 | ) | ||||

Interest expense, net |

(817 | ) | (518 | ) | 32 | |||||

Other income (expense), net |

(1,253 | ) | (648 | ) | (583 | ) | ||||

| | | | | | | | | | | |

Loss before income taxes |

(38,652 | ) | (46,745 | ) | (55,749 | ) | ||||

Benefit from (provision for) income taxes |

— | 2,191 | (78 | ) | ||||||

| | | | | | | | | | | |

Net loss |

(38,652 | ) | (44,554 | ) | (55,827 | ) | ||||

Accretion of preferred stock to redemption value |

(24,979 | ) | (3,569 | ) | (28,056 | ) | ||||

| | | | | | | | | | | |

Net loss attributable to common stockholders |

$ | (63,631 | ) | $ | (48,123 | ) | $ | (83,883 | ) | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Net loss per share attributable to common stockholders—basic and diluted(2) |

$ | (12.12 | ) | $ | (5.85 | ) | $ | (8.08 | ) | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Weighted-average common shares outstanding—basic and diluted(2) |

5,249 | 8,230 | 10,383 | |||||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Pro forma net loss per share attributable to common stockholders—basic and diluted (unaudited)(2) |

$ | (0.97 | ) | |||||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Pro forma weighted-average common shares outstanding—basic and diluted (unaudited)(2) |

56,535 | |||||||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

15

- (1)

- The following table summarizes the classification of stock-based compensation expense in our consolidated statements of operations:

| |

Year Ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2015 | 2016 | 2017 | |||||||

| |

(in thousands) |

|||||||||

Cost of subscription, license and support revenue |

$ | 103 | $ | 184 | $ | 403 | ||||

Cost of services revenue |

179 | 219 | 227 | |||||||

Sales and marketing expense |

1,595 | 2,501 | 3,310 | |||||||

Research and development expense |

1,585 | 2,035 | 2,506 | |||||||

General and administrative expense |

1,446 | 2,417 | 2,510 | |||||||

| | | | | | | | | | | |

Total stock-based compensation expense |

$ | 4,908 | $ | 7,356 | $ | 8,956 | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

- (2)

- See Note 18 to our consolidated financial statements appearing at the end of this prospectus for further details on the calculations of basic and diluted net loss per share attributable to common stockholders and basic and diluted pro forma net loss per share attributable to common stockholders.

| |

As of December 31, 2017 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

Actual | Pro Forma(2) | Pro Forma As Adjusted(3) | |||||||

| |

(in thousands) |

|||||||||

Consolidated Balance Sheet Data: |

||||||||||

Cash and cash equivalents |

$ | 36,073 | $ | 36,073 | $ | 152,123 | ||||

Working capital(1) |

(36,391 | ) | (36,391 | ) | 79,916 | |||||

Total assets |

260,612 | 260,612 | 374,495 | |||||||

Deferred revenue |

164,180 | 164,180 | 164,180 | |||||||

Warrant liability |

2,766 | — | — | |||||||

Redeemable convertible and convertible preferred stock |

334,714 | — | — | |||||||

Total stockholders' equity (deficit) |

(266,508 | ) | 70,972 | 185,112 | ||||||

- (1)

- We

define working capital as current assets less current liabilities.

- (2)

- The

pro forma consolidated balance sheet data give effect to:

- •

- the conversion of all outstanding shares of our preferred stock into 45,849,708 shares of common stock upon the closing of this

offering;

- •

- the assumed exercise of the outstanding warrant held by SC US GF Holdings, Ltd., an entity affiliated with Sequoia Capital, to

purchase 468,587 shares of our common stock, at an exercise price of $0.002 per share, that will become exercisable upon the closing of this offering; and

- •

- outstanding warrants to purchase shares of our preferred stock becoming warrants to purchase 167,500 shares of common stock upon the

closing of this offering.

- (3)

- The

pro forma as adjusted consolidated balance sheet data give further effect to our sale of 8,000,000 shares of our common stock in this offering at an

assumed initial public offering price of $16.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus, after deducting estimated underwriting discounts and

commissions and estimated offering expenses payable by us.

- The pro forma as adjusted information presented in the summary consolidated balance sheet data is illustrative only and will change based on the actual initial public offering price and other terms of this offering determined at pricing. A $1.00 increase (decrease) in the assumed initial public offering price

16

of $16.00 per share, which is the midpoint of the price range set forth on the cover page of this prospectus, would increase (decrease) the pro forma as adjusted amount of each of cash and cash equivalents, working capital, total assets and total stockholders' equity by $7.4 million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. An increase (decrease) of 1,000,000 shares in the number of shares of common stock offered by us, as set forth on the cover page of this prospectus, would increase (decrease) the pro forma as adjusted amount of each of cash and cash equivalents, working capital, total assets and total stockholders' equity by $14.9 million, assuming the assumed initial public offering price remains the same and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us.

17

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this prospectus, including the section titled "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes included elsewhere in this prospectus, before deciding whether to purchase shares of our common stock. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of may also become important factors that adversely affect our business. If any of the following risks actually occur, our business, financial condition, results of operations and future prospects could be adversely affected. In that event, the market price of our stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business and Industry

We are a rapidly growing company, which makes it difficult to evaluate our future prospects.

We are a rapidly growing company. Our ability to forecast our future operating results is subject to a number of uncertainties, including our ability to plan for and model future growth. We have encountered and will continue to encounter risks and uncertainties frequently experienced by growing companies in rapidly evolving industries. If our assumptions regarding these uncertainties, which we use to plan our business, are incorrect or change in reaction to changes in our markets, or if we do not address these risks successfully, our operating and financial results could differ materially from our expectations, our business could suffer and the trading price of our stock may decline.

We have not been profitable historically and may not achieve or maintain profitability in the future.

We have incurred net losses in each year since inception, including net losses of $38.7 million in 2015, $44.6 million in 2016 and $55.8 million in 2017. As of December 31, 2017, we had an accumulated deficit of $279.9 million. While we have experienced significant revenue growth in recent periods, we are not certain whether or when we will obtain a high enough volume of sales of our products to sustain or increase our growth or achieve or maintain profitability in the future. We also expect our costs to increase in future periods, which could negatively affect our future operating results if our revenue does not increase. In particular, we expect to continue to expend substantial financial and other resources on:

- •

- research and development related to our products, including investments in our research and development team;

- •

- sales and marketing, including a significant expansion of our sales organization, both domestically and internationally;

- •

- continued international expansion of our business;

- •

- expansion of our professional services organization; and

- •

- general administration expenses, including legal and accounting expenses related to being a public company.

These investments may not result in increased revenue or growth in our business. We expect to continue to devote research and development resources to our on-premise solutions; if our customers and potential customers shift their information technology, or IT, infrastructures to the cloud faster than we anticipate, we may not realize our expected return from the costs we incur. If we are unable to increase our revenue at a rate sufficient to offset the expected increase in our costs, our business, financial position and results of operations will be harmed, and we may not be able to achieve or maintain profitability over the long term. Additionally, we may encounter unforeseen operating expenses, difficulties, complications, delays and other unknown factors that may result in losses in future periods. If our revenue growth does not meet our expectations in future periods, our financial performance may be harmed, and we may not achieve or maintain profitability in the future.

18

If we are unable to sustain our revenue growth rate, we may not achieve or maintain profitability in the future.

Our revenue grew from $70.6 million in 2015 to $116.2 million in 2016 and $162.0 million in 2017, representing a 51% compound annual growth rate over the same period. Although we have experienced rapid growth historically and currently have high customer retention rates, we may not continue to grow as rapidly in the future and our customer retention rates may decline. Any success that we may experience in the future will depend in large part on our ability to, among other things:

- •

- maintain and expand our customer base;

- •

- increase revenues from existing customers through increased or broader use of our products within their organizations;

- •

- maintain and expand strategic partnerships with our channel partners;

- •

- improve the performance and capabilities of our products through research and development;

- •

- continue to develop our cloud-based solutions;

- •

- maintain the rate at which customers purchase our support services;

- •

- continue to successfully expand our business domestically and internationally;

- •

- successfully identify and consummate acquisitions of complementary businesses, technology and assets; and

- •

- successfully compete with other companies.

If we are unable to maintain consistent revenue or revenue growth, our stock price could be volatile, and it may be difficult to achieve and maintain profitability. You should not rely on our revenue for any prior quarterly or annual periods as any indication of our future revenue or revenue growth.

Our quarterly financial results, including our billings and deferred revenue, may fluctuate for a variety of reasons, including our failure to close significant sales before the end of a particular quarter.

A meaningful portion of our revenue is generated by significant sales to new customers and sales of additional products to existing customers. Purchases of our solutions often occur during the last month of each quarter, particularly in the last quarter of the year. In addition, our sales cycle can last several months from proof of concept to contract negotiation, to delivery of our solution to our customers, and this sales cycle can be even longer, less predictable and more resource-intensive for larger sales. Customers may also require additional internal approvals or seek to test our products for a longer trial period before deciding to purchase our solutions. As a result, the timing of individual sales can be difficult to predict. In some cases, sales have occurred in a quarter subsequent to those we anticipated, or have not occurred at all, which can significantly impact our quarterly financial results and make it more difficult to meet market expectations. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies—Revenue Recognition."

In addition to the sales cycle-related fluctuations noted above, our financial results, including our billings and deferred revenue, will continue to vary as a result of a number of factors, many of which are outside of our control and may be difficult to predict, including:

- •

- our ability to attract and retain new customers;

- •

- our ability to sell additional products to existing customers;

- •

- our ability to expand into adjacent and complementary markets;

- •

- changes in customer or channel partner requirements or market needs;

- •

- changes in the growth rate of the next-generation endpoint security market;

19

- •

- the timing and success of new product introductions by us or our competitors, or any other change in the competitive landscape of the

next-generation endpoint security market, including consolidation among our customers or competitors;

- •

- a disruption in, or termination of, any of our relationships with channel partners;

- •

- our ability to successfully expand our business globally;

- •

- reductions in customer retention rates;

- •

- changes in our pricing policies or those of our competitors;

- •

- general economic conditions in our markets;

- •

- future accounting pronouncements or changes in our accounting policies or practices;

- •

- the amount and timing of our operating costs, including cost of goods sold;

- •

- a change in our mix of products and services, including shifts to cloud-based products offered through a software-as-a-service model;

and

- •

- increases or decreases in our revenue and expenses caused by fluctuations in foreign currency exchange rates.

Any of the above factors, individually or in the aggregate, may result in significant fluctuations in our financial and other operating results from period to period. These fluctuations could result in our failure to meet our operating plan or the expectations of investors or analysts for any period. If we fail to meet such expectations for these or other reasons, the trading price of our common stock could fall substantially, and we could face costly lawsuits, including securities class action suits.

We recognize substantially all of our revenue ratably over the term of our agreements with customers and, as a result, downturns or upturns in sales may not be immediately reflected in our operating results.

We recognize substantially all of our revenue ratably over the terms of our agreements with customers, which generally occurs over a one- or three-year period. As a result, a substantial portion of the revenue that we report in each period will be derived from the recognition of deferred revenue relating to agreements entered into during previous periods. Consequently, a decline in new sales or renewals in any one period may not be immediately reflected in our revenue results for that period. This decline, however, will negatively affect our revenue in future periods. Accordingly, the effect of significant downturns in sales and market acceptance of our products, and potential changes in our rate of renewals may not be fully reflected in our results of operations until future periods. Our model also makes it difficult for us to rapidly increase our revenue through additional sales in any period, as revenue from new customers generally will be recognized over the term of the applicable agreement.

We also intend to increase our investment in research and development, sales and marketing and general and administrative functions and other areas to grow our business. These costs are generally expensed as incurred (with the exception of sales commissions), as compared to our revenue, substantially all of which is recognized ratably in future periods. We are likely to recognize the costs associated with these increased investments earlier than some of the anticipated benefits and the return on these investments may be lower, or may develop more slowly, than we expect, which could adversely affect our operating results.

We face intense competition in our market, especially from larger, well-established companies, and we may lack sufficient financial or other resources to maintain or improve our competitive position.

Our market is large, highly competitive, fragmented and subject to rapidly evolving technology, shifting customer needs and frequent introductions of new solutions. We expect competition to increase in the future from both established competitors and new market entrants. Our current competitors include

20

legacy antivirus solution providers, such as McAfee and Symantec Corporation, established network security providers, such as Palo Alto Networks, Inc., FireEye, Inc. and Cisco Systems, Inc., and privately held companies, such as Crowdstrike and Cylance. New startup companies, as well as established public and private companies, have entered or are currently attempting to enter the next-generation endpoint security market, some of which are or may become significant competitors in the future. Many of our existing competitors have, and some of our potential competitors could have, substantial competitive advantages such as:

- •

- greater name recognition and longer operating histories;

- •

- larger sales and marketing budgets and resources;

- •

- broader distribution and established relationships with distribution partners and customers;

- •

- greater customer support resources;

- •

- greater resources to make acquisitions;

- •

- lower labor and development costs;

- •

- larger and more mature intellectual property portfolios; and

- •

- substantially greater financial, technical and other resources.