Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION - 1847 Holdings LLC | efsh_ex321.htm |

| EX-31.1 - CERTIFICATION - 1847 Holdings LLC | efsh_ex311.htm |

| EX-21.1 - LIST OF SUBSIDIARIES - 1847 Holdings LLC | efsh_ex211.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2017

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to _____________

Commission File No. 333-193821

|

1847 HOLDINGS LLC |

|

(Exact name of registrant as specified in its charter) |

|

Delaware |

|

38-3922937 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

590 Madison Avenue, 21st Floor, New York, NY 10022

(Address of principal executive offices)

(212) 521-4052

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes x No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large Accelerated Filer |

¨ |

|

Accelerated Filer |

¨ |

|

Non-Accelerated Filer |

¨ |

(Do not check if a smaller reporting company) |

Smaller reporting company |

x |

|

|

|

|

Emerging growth company |

x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of common shares held by non-affiliates of the registrant on June 30, 2017 was $0 based on a $0 average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

There were a total of 623,125 shares of the registrant’s common stock outstanding as of April 16, 2018.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Annual Report on Form 10-K

Year Ended December 31, 2017

TABLE OF CONTENTS

| 2 |

| Table of Contents |

INTRODUCTORY NOTE

Use of Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to:

|

|

· | “1847 Holdings,” “we,” “our” and “our company” refer to 1847 Holdings LLC, a Delaware limited liability company, and its consolidated subsidiaries; |

|

|

|

|

|

|

· | “1847 Neese” refer to our majority-owned subsidiary 1847 Neese Inc., a Delaware corporation; |

|

|

|

|

|

|

· | “1847 Fitness” refer to our wholly-owned subsidiary 1847 Fitness, Inc., a Delaware corporation; |

|

|

|

|

|

|

· | “Neese” refer to 1847 Neese’s wholly-owned subsidiary Neese, Inc., an Iowa corporation; |

|

|

|

|

|

|

· | “Fitness CF” refer, collectively, to (i) Central Florida Health Clubs, LLC d/b/a Fitness CF Orlando, a Florida limited liability company; (ii) CLFL, LLC d/b/a Fitness CF Clermont, a Florida limited liability company; (iii) MTDR LLC d/b/a Fitness CF Mt. Dora, a Florida limited liability company; and (iv) SCFL, LLC d/b/a Fitness CF St. Cloud, a Florida limited liability company; |

|

|

|

|

|

|

· | “our manager” refer to 1847 Partners LLC, a Delaware limited liability company; |

|

|

|

|

|

|

· | “our shareholders” refer to holders of our common shares; |

|

|

|

|

|

|

· | “small businesses” refer to businesses that have an enterprise value of less than $50 million; |

|

|

|

|

|

|

· | “public offering” refer to our planned underwritten public offering as described in the registration statement; |

|

|

|

|

|

|

· | “registration statement” refer to our registration statement on Form S-1 filed with the SEC on October 6, 2017, as amended; |

|

|

|

|

|

|

· | “SEC” refer to the Securities and Exchange Commission; |

|

|

|

|

|

|

· | “Securities Act” refer to the Securities Act of 1933, as amended; and |

|

|

|

|

|

|

· | “Exchange Act” refer to the Securities Exchange Act of 1934, as amended. |

Special Note Regarding Forward Looking Statements

Certain information contained in this report includes forward-looking statements. The statements herein which are not historical reflect our current expectations and projections about our company’s future results, performance, liquidity, financial condition, prospects and opportunities and are based upon information currently available to our company and our management and our interpretation of what is believed to be significant factors affecting the businesses, including many assumptions regarding future events. The following factors, among others, may affect our forward-looking statements:

|

|

· | our ability to integrate Neese’s land application business; |

|

|

|

|

|

|

· | our ability to successfully identify and acquire additional businesses, and to operate such businesses that we may acquire in the future and to effectively integrate and improve such businesses; |

|

|

|

|

|

|

· | our organizational structure, which may limit our ability to meet our dividend and distribution policy; |

|

|

|

|

|

|

· | our ability to service and comply with the terms of indebtedness that we expect to incur in the future; |

| 3 |

| Table of Contents |

|

|

· | our cash flow available for distribution and our ability to make monthly distributions in the future to our shareholders; |

|

|

|

|

|

|

· | our ability to pay the management fee, profit allocation and put price to our manager when due; |

|

|

|

|

|

|

· | labor disputes, strikes or other employee disputes or grievances; |

|

|

|

|

|

|

· | our ability to implement our acquisition and management strategies; |

|

|

|

|

|

|

· | the regulatory environment in which our businesses may operate under; |

|

|

|

|

|

|

· | trends in the industries in which our businesses may operate; |

|

|

|

|

|

|

· | operational costs and expenses, including, energy and labor costs; |

|

|

|

|

|

|

· | the competitive environment in which our businesses will operate; |

|

|

|

|

|

|

· | changes in general economic or business conditions or economic or demographic trends in the United States including changes in interest rates and inflation; |

|

|

|

|

|

|

· | our and our manager’s ability to retain or replace qualified employees of our future businesses and our manager; |

|

|

|

|

|

|

· | casualties, condemnation or catastrophic failures with respect to any of our future business’ facilities; |

|

|

|

|

|

|

· | costs and effects of legal and administrative proceedings, settlements, investigations and claims; and |

|

|

|

|

|

|

· | extraordinary or force majeure events affecting the business or operations of our future businesses. |

Forward-looking statements, which involve assumptions and describe our future plans, strategies, and expectations, are generally identifiable by use of the words “may,” “should,” “expect,” “anticipate,” “estimate,” “believe,” “intend,” or “project” or the negative of these words or other variations on these words or comparable terminology. Actual results, performance, liquidity, financial condition, prospects and opportunities could differ materially from those expressed in, or implied by, these forward-looking statements as a result of various risks, uncertainties and other factors. These statements may be found under “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Item 1. Business,” as well as in this report generally. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, the risks outlined under “Item 1A. Risk Factors” and matters described in this report generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this report will in fact occur.

Potential investors should not place undue reliance on any forward-looking statements. Except as expressly required by the federal securities laws, there is no undertaking to publicly update or revise any forward-looking statements, whether as a result of new information, future events, changed circumstances or any other reason.

The specific discussions herein about our company include financial projections and future estimates and expectations about our business. The projections, estimates and expectations are presented in this report only as a guide about future possibilities and do not represent actual amounts or assured events. All the projections and estimates are based exclusively on our management’s own assessment of our business, the industry in which we work and the economy at large and other operational factors, including capital resources and liquidity, financial condition, fulfillment of contracts and opportunities. The actual results may differ significantly from the projections.

Potential investors should not make an investment decision based solely on our projections, estimates or expectations.

Stock Splits

On June 9, 2017, we completed a 1-for-25 reverse stock split of our outstanding common shares. As a result of this stock split, our issued and outstanding common shares decreased from 77,887,500 to 3,115,500 shares. On January 22, 2018, we completed a 1-for-5 reverse stock split of our outstanding common shares. As a result of this stock split, our issued and outstanding common shares decreased from 3,115,500 to shares 623,125 shares. Accordingly, all share and per share information contained in this report has been restated to retroactively show the effect of these stock splits.

| 4 |

| Table of Contents |

OVERVIEW OF OUR BUSINESS

We are an acquisition holding company focused on acquiring and managing a group of small businesses in a variety of different industries headquartered in North America. Through our subsidiaries, we currently provide products and services to the agriculture, construction, lawn and garden industries, which we refer to as our land application business. We have also entered into an agreement for the acquisition of four Florida health clubs and have plans to acquire additional small businesses in a variety of different industries. Through our structure, we plan to offer investors an opportunity to participate in the ownership and growth of a portfolio of businesses that traditionally have been owned and managed by private equity firms, private individuals or families, financial institutions or large conglomerates. We believe that our management and acquisition strategies will allow us to achieve our goals to begin making and growing regular monthly distributions to our shareholders and increasing shareholder value over time.

We seek to acquire controlling interests in small businesses that we believe operate in industries with long-term macroeconomic growth opportunities, and that have positive and stable earnings and cash flows, face minimal threats of technological or competitive obsolescence and have strong management teams largely in place. We believe that private company operators and corporate parents looking to sell their businesses will consider us to be an attractive purchaser of their businesses. Like we did when we acquired our land application business, we intend to make these future businesses our majority-owned subsidiaries and intend to actively manage and grow such businesses. We expect to improve our businesses over the long term through organic growth opportunities, add-on acquisitions and operational improvements.

Market Opportunity

We seek to acquire and manage small businesses, which we characterize as those that have an enterprise value of less than $50 million. We believe that the merger and acquisition market for small businesses is highly fragmented and provides significant opportunities to purchase businesses at attractive prices. For example, according to GF Data, platform acquisitions with enterprise values greater than $50.0 million commanded valuation premiums 30% higher than platform acquisitions with enterprise values less than $50.0 million (8.2x trailing twelve month adjusted EBITDA versus 6.3x trailing twelve month adjusted EBITDA, respectively).

We believe that the following factors contribute to lower acquisition multiples for small businesses:

·

there are typically fewer potential acquirers for these businesses;

·

third-party financing generally is less available for these acquisitions;

·

sellers of these businesses may consider non-economic factors, such as continuing board membership or the effect of the sale on their employees; and

·

these businesses are generally less frequently sold pursuant to an auction process.

We believe that our management team’s strong relationships with business brokers, investment and commercial bankers, accountants, attorneys and other potential sources of acquisition opportunities offers us substantial opportunities to purchase small businesses. See “—Our Manager—Key Personnel of our Manager” for more information about our management team.

We also believe that significant opportunities exist to improve the performance of the businesses upon their acquisition. In the past, our manager has acquired businesses that are often formerly owned by seasoned entrepreneurs or large corporate parents. In these cases, our manager has frequently found that there have been opportunities to further build upon the management teams of acquired businesses. In addition, our manager has frequently found that financial reporting and management information systems of acquired businesses may be improved, both of which can lead to substantial improvements in earnings and cash flow. Finally, because these businesses tend to be too small to have their own corporate development efforts, we believe opportunities exist to assist these businesses in meaningful ways as they pursue organic or external growth strategies that were often not pursued by their previous owners.

| 5 |

| Table of Contents |

Our Strategy

Our long-term goals are to begin making and growing monthly distributions to our shareholders and to increase shareholder value over the long-term. We acquired Neese primarily so that we can achieve a base of cash flow to build our company and begin making and growing monthly distributions. We believe this acquisition will help us achieve our long-term goals.

We plan to continue focusing on acquiring other businesses. Therefore, we intend to continue to identify, perform due diligence on, negotiate and consummate platform acquisitions of small businesses in attractive industry sectors.

Unlike buyers of small businesses that rely on significant leverage to consummate acquisitions (as demonstrated by the data below), we plan to limit the use of third party (i.e., external) acquisition leverage so that our debt will not exceed the market value of the assets we acquire and so that our debt to EBITDA ratio will not exceed 1.25x to 1 for our operating subsidiaries. We believe that limiting leverage in this manner will avoid the imposition on stringent lender controls on our operations that would otherwise potentially hamper the growth of our operating subsidiaries and otherwise harm our business even during times when we have positive operating cash flows. Additionally, in our experience, leverage rarely leads to “break-out” returns and often creates negative return outcomes that are not correlated with the profitability of the business.

Source: GF Data M&A Report (August 2017)

Source: GF Data Leverage Report (August 2017)

In addition to acquiring businesses, we expect to sell businesses that we own from time to time when attractive opportunities arise. Upon the sale of a business, we may use the resulting proceeds to retire debt or retain proceeds for future acquisitions or general purposes. Generally, we do not expect to make special distributions at the time of a sale of one of our businesses; instead, we expect that we will seek to gradually increase monthly shareholder distributions over time.

| 6 |

| Table of Contents |

Management Strategy

Our management strategy involves the identification, performance of due diligence, negotiation and consummation of acquisitions. After acquiring businesses, we will attempt to grow the businesses both organically and through add-on or bolt-on acquisitions. Add-on or bolt-on acquisitions are acquisitions by a company of other companies in the same industry. Following the acquisition of companies, we will seek to grow the earnings and cash flow of acquired companies and, in turn, begin making and growing regular monthly distributions to our shareholders and to increase shareholder value over time. We believe we can increase the cash flows of our businesses by applying our intellectual capital to improve and grow our future businesses.

We will seek to acquire and manage small businesses, which we characterize as those that have an enterprise value of less than $50 million. We believe that the merger and acquisition market for small businesses is highly fragmented and provides opportunities to purchase businesses at attractive prices. We believe we will be able to acquire small businesses for multiples ranging from three to six times EBITDA. We also believe, and our manager has historically found, that significant opportunities exist to improve the performance of these businesses upon their acquisition.

In general, our manager will oversee and support the management team of our future platform businesses by, among other things:

·

recruiting and retaining managers to operate our future businesses by using structured incentive compensation programs, including minority equity ownership, tailored to each business;

·

regularly monitoring financial and operational performance, instilling consistent financial discipline, and supporting management in the development and implementation of information systems;

·

assisting the management teams of our future businesses in their analysis and pursuit of prudent organic growth strategies

·

identifying and working with future business management teams to execute on attractive external growth and acquisition opportunities;

·

identifying and executing operational improvements and integration opportunities that will lead to lower operating costs and operational optimization;

·

providing the management teams of our future businesses the opportunity to leverage our experience and expertise to develop and implement business and operational strategies; and

·

forming strong subsidiary level boards of directors to supplement management teams in their development and implementation of strategic goals and objectives.

We also believe that our long-term perspective provides us with certain additional advantages, including the ability to:

|

|

· | recruit and develop management teams for our future businesses that are familiar with the industries in which our future businesses operate; |

|

|

|

|

|

|

· | focus on developing and implementing business and operational strategies to build and sustain shareholder value over the long term; |

|

|

|

|

|

|

· | create sector-specific businesses enabling us to take advantage of vertical and horizontal acquisition opportunities within a given sector; |

|

|

|

|

|

|

· | achieve exposure in certain industries in order to create opportunities for future acquisitions; and |

|

|

|

|

|

|

· | develop and maintain long-term collaborative relationships with customers and suppliers. |

We intend to continually increase our intellectual capital as we operate our businesses and acquire new businesses and as our manager identifies and recruits qualified operating partners and managers for our businesses.

| 7 |

| Table of Contents |

Acquisition Strategy

Our acquisition strategies involve the acquisition of small businesses in various industries that we expect will produce positive and stable earnings and cash flow, as well as achieve attractive returns on our invested capital. In this respect, we expect to make acquisitions in industries wherein we believe an acquisition presents an attractive opportunity from the perspective of both (i) return on assets or equity and (ii) an easily identifiable path for growing the acquired businesses. We believe that attractive opportunities will increasingly present themselves as private sector owners seek to monetize their interests in longstanding and privately-held businesses and large corporate parents seek to dispose of their “non-core” operations.

We believe that the greatest opportunities for generating consistently positive annual returns and, ultimately, residual returns on capital invested in acquisitions will result from targeting capital light businesses operating in niche geographical markets with a clearly identifiable competitive advantage within the following industries: business services, consumer services, consumer products, consumable industrial products, industrial services, niche light manufacturing, distribution, alternative/specialty finance and in select cases, specialty retail. While we believe that the professional experience of our management team within the industries identified above will offer the greatest number of acquisition opportunities, we will not eschew opportunities if a business enjoys an inarguable moat around its products and services in an industry which our management team may have less familiarity.

From a financial perspective, we expect to make acquisitions of small businesses that are stable, have minimal bad debt, and strong accounts receivable. In addition, we expect to acquire companies that have been able to generate positive pro forma cash available for distribution for a minimum of three years prior to acquisition.

We expect to benefit from our manager’s ability to identify diverse acquisition opportunities in a variety of industries. In addition, we intend to rely upon our management teams’ experience and expertise in researching and valuing prospective target businesses, as well as negotiating the ultimate acquisition of such target businesses. In particular, because there may be a lack of information available about these target businesses, which may make it more difficult to understand or appropriately value such target businesses, we expect our manager will:

·

engage in a substantial level of internal and third-party due diligence;

·

critically evaluate the management team;

·

identify and assess any financial and operational strengths and weaknesses of any target business;

·

analyze comparable businesses to assess financial and operational performances relative to industry competitors;

·

actively research and evaluate information on the relevant industry; and

·

thoroughly negotiate appropriate terms and conditions of any acquisition.

We expect the process of acquiring new businesses to be time-consuming and complex. Our manager has historically taken from 2 to 24 months to perform due diligence on, negotiate and close acquisitions. Although we expect our manager to be at various stages of evaluating several transactions at any given time, there may be significant periods of time during which it does not recommend any new acquisitions to us.

Upon an acquisition of a new business, we intend to rely on our manager’s experience and expertise to work efficiently and effectively with the management of the new business to jointly develop and execute a business plan.

While we will primarily seek to acquire controlling interests in a business, we may also acquire non-control or minority equity positions in businesses where we believe it is consistent with our long-term strategy.

| 8 |

| Table of Contents |

As discussed in more detail below, we intend to raise capital for additional acquisitions primarily through debt financing, primarily at our operating company level, additional equity offerings by our company, the sale of all or a part of our businesses or by undertaking a combination of any of the above.

In addition to acquiring businesses, we expect to sell businesses that we own from time to time when attractive opportunities arise. Our decision to sell a business will be based on our belief that the sale will provide our shareholders with a more favorable return on the investment than continued ownership, and will be consistent with the disposition criteria to be established by our company’s board of directors from time to time. Upon the sale of a business, we may use the resulting proceeds to retire debt or retain proceeds for future acquisitions or general purposes. Generally, we do not expect to make special distributions at the time of a sale of one of our businesses; instead, we expect that we will seek to gradually increase monthly shareholder distributions over time.

There are several risks associated with our acquisition strategy, including the following risks, which are described more fully in “Item 1A. Risk Factors—Risks Related to Our Business and Structure”:

·

we may not be able to successfully fund future acquisitions of new businesses due to the unavailability of debt or equity financing on acceptable terms, which could impede the implementation of our acquisition strategy;

·

we may experience difficulty as we evaluate, acquire and integrate Neese and future businesses that we may acquire, which could result in drains on our resources, including the attention of our management, and disruptions of our on-going business;

·

we face competition for businesses that fit our acquisition strategy and, therefore, we may have to acquire targets at sub-optimal prices or, alternatively, forego certain acquisition opportunities; and

·

we may change our management and acquisition strategies without the consent of our shareholders, which may result in a determination by us to pursue riskier business activities.

Strategic Advantages

Based on the experience of our manager and its ability to identify and negotiate acquisitions, we expect to be strongly positioned to acquire additional businesses. Our manager has strong relationships with business brokers, investment and commercial bankers, accountants, attorneys and other potential sources of acquisition opportunities. In negotiating these acquisitions, we believe our manager will be able to successfully navigate complex situations surrounding acquisitions, including corporate spin-offs, transitions of family-owned businesses, management buy-outs and reorganizations.

We expect that the flexibility, creativity, experience and expertise of our manager in structuring transactions will provide us with strategic advantages by allowing us to consider non-traditional and complex transactions tailored to fit a specific acquisition target.

Our manager also has a large network of deal intermediaries who we expect to expose us to potential acquisitions. Through this network, we expect to have a substantial pipeline of potential acquisition targets. Our manager also has a well-established network of contacts, including professional managers, attorneys, accountants and other third-party consultants and advisors, who may be available to assist us in the performance of due diligence and the negotiation of acquisitions, as well as the management and operation of our businesses once acquired.

Valuation and Due Diligence

When evaluating businesses or assets for acquisition, we will perform a rigorous due diligence and financial evaluation process. In doing so, we will seek to evaluate the operations of the target business as well as the outlook for the industry in which the target business operates. While valuation of a business is, by definition, a subjective process, we will be defining valuations under a variety of analyses, including:

·

discounted cash flow analyses;

·

evaluation of trading values of comparable companies;

| 9 |

| Table of Contents |

·

expected value matrices;

·

assessment of competitor, supplier and customer environments; and

·

examination of recent/precedent transactions.

One outcome of this process is an effort to project the expected cash flows from the target business as accurately as possible. A further outcome is an understanding of the types and levels of risk associated with those projections. While future performance and projections are always uncertain, we believe that our detailed due diligence review process allows us to more accurately estimate future cash flows and more effectively evaluate the prospects for operating the business in the future. To assist us in identifying material risks and validating key assumptions in our financial and operational analysis, in addition to our own analysis, we intend to engage third-party experts to review key risk areas, including legal, tax, regulatory, accounting, insurance and environmental. We may also engage technical, operational or industry consultants, as necessary.

A further critical component of the evaluation of potential target businesses will be the assessment of the capability of the existing management team, including recent performance, expertise, experience, culture and incentives to perform. Where necessary, and consistent with our management strategy, we will actively seek to augment, supplement or replace existing members of management who we believe are not likely to execute the business plan for the target business. Similarly, we will analyze and evaluate the financial and operational information systems of target businesses and, where necessary, we will actively seek to enhance and improve those existing systems that are deemed to be inadequate or insufficient to support our business plan for the target business.

Financing

We will finance future acquisitions primarily through additional equity and debt financings. We believe that having the ability to finance most, if not all, acquisitions with the general capital resources raised by our company, rather than financing relating to the acquisition of individual businesses, provides us with an advantage in acquiring attractive businesses by minimizing delay and closing conditions that are often related to acquisition-specific financings. In this respect, we believe that, at some point in the future, we may need to pursue additional debt or equity financings, or offer equity in our company or target businesses to the sellers of such target businesses, in order to fund acquisitions.

Our Competitive Advantages

We believe that our manager’s collective investment experience and approach to executing our investment strategy provide our company with several competitive advantages. These competitive advantages, certain of which are discussed below, have enabled our management to generate very attractive risk- adjusted returns for investors in their predecessor firms.

Robust Network. Through their activities with their predecessor firms and their comprehensive marketing capabilities, we believe that the management team of our manager has established a “top of mind” position among investment bankers and business brokers targeting small businesses. By employing an institutionalized, multi-platform marketing strategy, we believe our manager has established a robust national network of personal relationships with intermediaries, seasoned operating executives, entrepreneurs and managers, thereby firmly establishing our company’s presence and credibility in the small business market. In contrast to many other buyers of and investors in small businesses, we believe that we can buy businesses at value-oriented multiples and through our asset management activities with a group of professional, experienced and talented operating partners, create appreciable value. We believe our experience, track record and consistent execution of our marketing and investment activities will allow us to maintain a leadership position as the preferred partner for today’s small business market.

Disciplined Deal Sourcing. We employ an institutionalized, multi-platform approach to sourcing new acquisition opportunities. Our deal sourcing efforts include leveraging relationships with more than 3,000 qualified deal sources through regular calling, mail and e-mail campaigns, assignment of regional marketing responsibilities, in-person visits and high-profile sponsorship of important conferences and industry events. We supplement these activities by retaining selected intermediary firms to conduct targeted searches for opportunities in specific categories on an opportunistic basis. As a result of the significant time and effort spent on these activities, we believe we established close relationships and unique “top of mind” awareness with many of the most productive intermediary sources for small business acquisition opportunities in the United States. While reinforcing our market leadership, this capability enables us to generate a large number of attractive acquisition opportunities.

| 10 |

| Table of Contents |

Differentiated Acquisition Capabilities in the Small Business Market. We deploy a differentiated approach to acquiring businesses in the small business market. Our management concentrates their efforts on mature companies with sustainable value propositions, which can be supported by our resources and institutional expertise. Our evaluation of acquisition opportunities typically involves significant input from a seasoned operating partner with relevant experience, which we believe enhances both our diligence and ongoing monitoring capabilities. In addition, we approach every acquisition opportunity with creative structures, which we believe enables us to engineer mutually attractive scenarios for sellers, whereas competing buyers may be limited by their rigid structural requirements. We believe our commitment to conservative capital structures and valuation will enhance each acquired operating subsidiary’s ability to deliver consistent levels of cash available for distribution, while additionally supporting reinvestment for growth.

Value Proposition for Business Owners. We employ a creative, flexible approach by tailoring each acquisition structure to meet the specific liquidity needs and certain qualitative objectives of the target’s owners and management team. In addition to serving as an exit pathway for sellers, we seek to align our interests with the sellers by enabling them to retain and/or earn (through incentive compensation) a substantial economic interest in their businesses following the acquisition and by typically allowing the incumbent management team to retain operating control of the acquired operating subsidiary on a day-to-day basis. We believe that our company is an appealing buyer for small business owners and managers due to our track record of capitalizing portfolio companies conservatively, enhancing the company’s ability to execute on its strategic initiatives and adding equity value. As a result, we believe business owners and managers will find in our company to be a dynamic, value-added buyer that brings considerable resources to achieve their strategic, capital and operating needs, resulting in substantial value creation for the operating subsidiary.

Operating Partner. Our manager has consistently worked with a strong network of seasoned operating partners - former entrepreneurs and executives with extensive experience building, managing and optimizing successful small businesses across a range of industries. We believe that our operating partner model will enable our company to make a significant improvement in the operating subsidiary, as compared to other buyers, such as traditional private equity firms, which rely principally upon investment professionals to make acquisition/investment and monitoring decisions regarding not only the business, financial and legal due diligence aspects of a business but also the more operational aspects including industry dynamics, management strength and strategic growth initiatives. We typically engage an operating partner soon after identifying a target business for acquisition, enhancing our acquisition judgment and building the acquisition team’s relationship with the subsidiary’s management team. Operating partners usually serve as a member of the board of directors of an operating subsidiary and spend two to four days per month working with the subsidiary’s management team. We leverage the operating partner’s extensive experience to build the management team, improve operations and assist with strategic growth initiatives, resulting in value creation.

Small Business Market Experience. We believe the history and experience of our manager’s partnering with companies in the small business market allows us to identify highly attractive acquisition opportunities and add significant value to our operating subsidiaries. Our manager’s investment experience in the small business market prior to forming our company has further contributed to our institutional expertise in the acquisition, strategic and operational decisions critical to the long-term success of small businesses. Since 2000, the management team of our manager has collectively been presented with several thousand investment opportunities and actively worked with more than 30 small businesses on all facets of their strategy, development and operations, which we have successfully translated into unique, institutionalized capabilities directed towards creating value in small businesses.

Intellectual Property

Our manager owns certain intellectual property relating to the term “1847.” Our manager has granted our company a license to use the term “1847” in its business.

Employees

As of the date of this report, the only full-time employee at the holding company, 1847 Holdings LLC, is Ellery W. Roberts, our Chairman, Chief Executive Officer, President and Chief Financial Officer.

| 11 |

| Table of Contents |

OUR CORPORATE STRUCTURE AND HISTORY

Our company is a Delaware limited liability company that was formed on January 22, 2013. Your rights as a holder of common shares, and the fiduciary duties of our board of directors and executive officers, and any limitations relating thereto, are set forth in the operating agreement governing our company and may differ from those applying to a Delaware corporation. However, subject to certain exceptions, the documents governing our company specify that the duties of our directors and officers will be generally consistent with the duties of directors and officers of a Delaware corporation.

Our company will be classified as a partnership for U.S. federal income tax purposes. Under the partnership income tax provisions, our company will not incur any U.S. federal income tax liability; rather, each of our shareholders will be required to take into account his or her allocable share of company income, gain, loss, and deduction. As a holder of common shares, you may not receive cash distributions sufficient in amount to cover taxes in respect of your allocable share of our company’s net taxable income. Our company will file a partnership return with the IRS and will issue tax information, including a Schedule K-1, to you that describes your allocable share of our company’s income, gain, loss, deduction, and other items. The U.S. federal income tax rules that apply to partnerships are complex, and complying with the reporting requirements may require significant time and expense. See “Material U.S. Federal Income Tax Considerations” included in the registration statement for more information.

Our company has two classes of limited liability company interests - the common shares and the allocation shares, all of which have been and will continue to be held by our manager. See “Description of Securities” included in the registration statement for more information about the common shares and the allocation shares.

On September 15, 2013, our subsidiary, 1847 Management Services Inc., a Delaware corporation, or 1847 Management, acquired a 50% interest in each of PPI Management Group, LLC, or PPI Management, and Christals Management LLC, or Christals Management, from our Chief Executive Officer and controlling shareholder, Ellery W. Roberts. Each of PPI Management and Christals Management were management consulting and advisory firms. On October 3, 2017, our board decided to discontinue our management consulting operations in order to devote more time and resources to Neese and our proposed acquisition of Fitness CF.

On March 3, 2017, our wholly-owned subsidiary 1847 Neese acquired all of the issued and outstanding capital stock of Neese for an aggregate purchase price of $6,655,000, consisting of: (i) $2,225,000 in cash (subject to certain adjustments); (ii) 450 shares of the common stock of 1847 Neese, valued by the parties at $1,530,000, constituting 45% of its capital stock; (iii) the issuance of a vesting promissory note in the principal amount of $1,875,000 (which was determined to have a fair value of $395,634) due June 30, 2020; and (iv) the issuance of a short-term promissory note in the principal amount of $1,025,000 due March 3, 2018. Neese was formed in January 1993.

On July 6, 2017, we formed 1847 Fitness as a wholly-owned subsidiary for the purpose of entering into the purchase agreement with Fitness CF.

| 12 |

| Table of Contents |

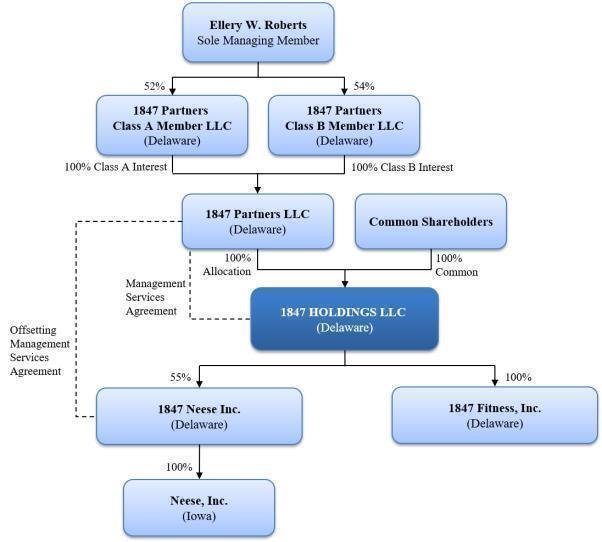

The following chart depicts our current organizational structure.

See “—Our Manager” for more details regarding the ownership of our manager.

OUR MANAGER

Overview of Our Manager

Our manager, 1847 Partners LLC, is a Delaware limited liability company. It has two classes of limited liability interests known as Class A interests and Class B interests. The Class A interests, which give the holder the right to the profit allocation received by our manager as a result of holding our allocation shares, are owned in their entirety by 1847 Partners Class A Member LLC; and the Class B interests, which give the holder the right to all other profits or losses of our manager, including the management fee payable to our manager by us, are owned in their entirety by 1847 Partners Class B Member LLC. 1847 Partners Class A Member LLC is owned 52% by Ellery W. Roberts, our Chief Executive Officer, and 38% by 1847 Founders Capital LLC, which is owned by Edward J. Tobin. 1847 Partners Class B Member LLC is owned 54% by Ellery W. Roberts and 36% by 1847 Founders Capital LLC. Mr. Roberts is also the sole manager of both entities. In the future, Mr. Roberts may cause 1847 Partners Class A Member LLC or 1847 Partners Class B Member LLC to issue units to employees of the manager to incentivize those employees by providing them with the ability to participate in our manager’s incentive allocation and management fee.

| 13 |

| Table of Contents |

Key Personnel of Our Manager

The key personnel of our manager are Ellery W. Roberts, our Chief Executive Officer, and Edward J. Tobin. Please see “Item 10. Directors, Executive Officers and Corporate Governance” for a description of the business experience of these individuals. Each of these individuals will be compensated entirely by our manager from the management fees it receives. As employees of our manager, these individuals devote a substantial majority of their time to the affairs of our company.

Collectively, the management team of our manager has more than 60 years of combined experience in acquiring and managing small businesses and has overseen the acquisitions and financing of over 50 businesses.

Acquisition and Disposition Opportunities

Our manager has exclusive responsibility for reviewing and making recommendations to our board of directors with respect to acquisition and disposition opportunities. If our manager does not originate an opportunity, our board of directors will seek a recommendation from our manager prior to making a decision concerning such opportunity. In the case of any acquisition or disposition opportunity that involves an affiliate of our manager or us, our nominating and corporate governance committee, or, if we do not have such a committee, the independent members of our board of directors, will be required to authorize and approve such transaction.

Our manager will review each acquisition or disposition opportunity presented to our manager to determine if such opportunity satisfies the acquisition and disposition criteria established by our board of directors. The acquisition and disposition criteria provide that our manager will review each acquisition opportunity presented to it to determine if such opportunity satisfies our company’s acquisition and disposition criteria, and if it is determined, in our manager’s sole discretion, that an opportunity satisfies the criteria, our manager will refer the opportunity to our board of directors for its authorization and approval prior to the consummation of any such opportunity.

Our investment criteria include the following:

|

|

· | Revenue of at least $5.0 million |

|

|

|

|

|

|

· | Current year EBITDA/Pre-tax Income of at least $1.5 million with a history of positive cash flow |

|

|

|

|

|

|

· | Clearly identifiable “blueprint” for growth with the potential for break-out returns |

|

|

|

|

|

|

· | Well-positioned companies within our core industry categories (consumer-driven, business-to-business, light manufacturing and specialty finance) with strong returns on capital |

|

|

|

|

|

|

· | Opportunities wherein building management team, infrastructure and access to capital are the primary drivers of creating value |

|

|

|

|

|

|

· | Headquartered in North America |

We believe we will be able to acquire small businesses for multiples ranging from three to six times EBITDA. With respect to investment opportunities that do not fall within the criteria set forth above our manager must first present such opportunities to our board of directors. Our board of directors and our manager will review these criteria from time to time and our board of directors may make changes and modifications to such criteria as our company makes additional acquisitions and dispositions.

If an acquisition opportunity is referred to our board of directors by our manager and our board of directors determines not to timely pursue such opportunity in whole or in part, any part of such opportunity that our company does not promptly pursue may be pursued by our manager or may be referred by our manager to any person, including affiliates of our manager. In this case, our manager is likely to devote a portion of its time to the oversight of this opportunity, including the management of a business that we do not own.

If there is a disposition, our manager must use its commercially reasonable efforts to manage a process through which the value of such disposition can be maximized, taking into consideration non-financial factors such as those relating to competition, strategic partnerships, potential favorable or adverse effects on us, our businesses, or our investments or any similar factors that may reasonably perceived as having a short- or long-term impact on our business, results of operations and financial condition.

| 14 |

| Table of Contents |

Management Services Agreement

The management services agreement sets forth the services to be performed by our manager. Our manager will perform such services subject to the oversight and supervision of our board of directors.

In general, our manager will perform those services for our company that would be typically performed by the executive officers of a company. Specifically, our manager will perform the following services, which we refer to as the management services, pursuant to the management services agreement:

·

manage the day-to-day business and operations of our company, including our liquidity and capital resources and compliance with applicable law;

·

identify, evaluate, manage, perform due diligence on, negotiate and oversee acquisitions of target businesses and any other investments;

·

evaluate and oversee the financial and operational performance of our businesses, including monitoring the business and operations of such businesses, and the financial performance of any other investments that we make;

·

provide, on our behalf, managerial assistance to our businesses;

·

evaluate, manage, negotiate and oversee dispositions of all or any part of any of our property, assets or investments, including disposition of all or any part of our businesses;

·

provide or second, as necessary, employees of our manager to serve as executive officers or other employees of our company or as members of our board of directors; and

·

perform any other services that would be customarily performed by executive officers and employees of a publicly listed or quoted company.

Our company and our manager have the right at any time during the term of the management services agreement to change the services provided by our manager. In performing management services, our manager will have all necessary power and authority to perform, or cause to be performed, such services on behalf of our company, and, in this respect, our manager will be the only provider of management services to our company. Nonetheless, our manager will be required to obtain authorization and approval of our board of directors in all circumstances where executive officers of a corporation typically would be required to obtain authorization and approval of a corporation’s board of directors, including, for example, with respect to the consummation of an acquisition of a target business, the issuance of securities or the entry into credit arrangements.

While our Chief Executive Officer, Mr. Ellery W. Roberts, intends to devote substantially all of his time to the affairs of our company, neither Mr. Roberts, nor our manager, is expressly prohibited from investing in or managing other entities. In this regard, the management services agreement will not require our manager and its affiliates to provide management services to our company exclusively.

Secondment of Our Executive Officers

In accordance with the terms of the management services agreement, our manager may second to our company our executive officers, which means that these individuals will be assigned by our manager to work for us during the term of the management services agreement. Our board of directors has appointed Mr. Roberts as an executive officer of our company. Although Mr. Roberts is an employee of our manager, he will report directly, and be subject, to our board of directors. In this respect, our board of directors may, after due consultation with our manager, at any time request that our manager replace any individual seconded to our company and our manager will, as promptly as practicable, replace any such individual; however, our Chief Executive Officer, Mr. Roberts, controls our manager, which may make it difficult for our board of directors to completely sever ties with Mr. Roberts. Our manager and our board of directors may agree from time to time that our manager will second to our company one or more additional individuals to serve on behalf of our company, upon such terms as our manager and our board of directors may mutually agree.

| 15 |

| Table of Contents |

Indemnification by our Company

Our company has agreed to indemnify and hold harmless our manager and its employees and representatives, including any individuals seconded to our company, from and against all losses, claims and liabilities incurred by our manager in connection with, relating to or arising out of the performance of any management services. However, our company will not be obligated to indemnify or hold harmless our manager for any losses, claims and liabilities incurred by our manager in connection with, relating to or arising out of (i) a breach by our manager or its employees or its representatives of the management services agreement, (ii) the gross negligence, willful misconduct, bad faith or reckless disregard of our manager or its employees or representatives in the performance of any of its obligations under the management services agreement, or (iii) fraudulent or dishonest acts of our manager or its employees or representatives with respect to our company or any of its businesses.

We expect that our directors and officers insurance policy for our directors and officers will be expanded, or supplemental insurance will be obtained, to cover this indemnification obligation.

Termination of Management Services Agreement

Our board of directors may terminate the management services agreement and our manager’s appointment if, at any time:

·

a majority of our board of directors vote to terminate the management services agreement, and the holders of at least a majority of the outstanding shares (other than shares beneficially owned by our manager) then entitled to vote also vote to terminate the management services agreement;

·

neither Mr. Roberts nor his designated successor controls our manager, which change of control occurs without the prior written consent of our board of directors;

·

there is a finding by a court of competent jurisdiction in a final, non-appealable order that (i) our manager materially breached the terms of the management services agreement and such breach continued unremedied for 60 days after our manager receives written notice from our company setting forth the terms of such breach, or (ii) our manager (x) acted with gross negligence, willful misconduct, bad faith or reckless disregard in performing its duties and obligations under the management services agreement, or (y) engaged in fraudulent or dishonest acts in connection with the business or operations of our company;

·

our manager has been convicted of a felony under federal or state law, our board of directors finds that our manager is demonstrably and materially incapable of performing its duties and obligations under the management services agreement, and the holders of at least 66 2/3% of the then outstanding shares, other than shares beneficially owned by our manager, vote to terminate the management services agreement; or

·

there is a finding by a court of competent jurisdiction that our manager has (i) engaged in fraudulent or dishonest acts in connection with the business or operations of our company or (ii) acted with gross negligence, willful misconduct, bad faith or reckless disregard in performing its duties and obligations under the management services agreement, and the holders of at least 66 2/3% of the then outstanding shares (other than shares beneficially owned by our manager) vote to terminate the management services agreement.

In addition, our manager may resign and terminate the management services agreement at any time upon 120 days prior written notice to our company, and this right is not contingent upon the finding of a replacement manager. However, if our manager resigns, until the date on which the resignation becomes effective, it will, upon request of our board of directors, use reasonable efforts to assist our board of directors to find a replacement manager at no cost and expense to our company.

Upon the termination of the management services agreement, seconded officers, employees, representatives and delegates of our manager and its affiliates who are performing the services that are the subject of the management services agreement will resign their respective position with our company and cease to work at the date of such termination or at any other time as determined by our manager. Any director appointed by our manager may continue serving on our board of directors subject to the terms of the operating agreement.

If we terminate the management services agreement, our company and its businesses have agreed to cease using the term “1847”, including any trademarks based on the name of our company that may be licensed to them by our manager, under the licensing provisions of the management services agreement, entirely in their businesses and operations within 180 days of such termination. Such licensing provisions of the management services agreement would require our company and its businesses to change their names to remove any reference to the term “1847” or any reference to trademarks licensed to them by our manager. In this respect, our right to use the term “1847” and related intellectual property is subject to licensing provisions between our manager, on the one hand, and our company and our businesses, on the other hand.

| 16 |

| Table of Contents |

Except with respect to the termination fee payable to our manager due to a termination of the management services agreement based solely on a vote of our board of directors and our shareholders, no other termination fee is payable upon termination of the management services agreement for any other reason. See “Our Manager—Our Manager as a Service Provider—Termination Fee” for more information about the termination fee payable upon termination of the management services agreement.

While termination of the management services agreement will not affect any terms and conditions, including those relating to any payment obligations, that exist under any offsetting management services agreements or transaction services agreements, such agreements will be terminable by future businesses that we acquire upon 60 days prior written notice and there will be no termination or other similar fees due upon such termination. Notwithstanding termination of the management services agreement, our manager will maintain its rights with respect to the allocation shares it then owns, including its rights under the supplemental put provision of our operating agreement. See “—Our Manager—Our Manager as an Equity Holder—Supplemental Put Provision” for more information on our manager’s put right with respect to the allocation shares.

Our Relationship with Our Manager, Manager Fees and Manager Profit Allocation

Our relationship with our manager is based on our manager having two distinct roles: first, as a service provider to us and, second, as an equity holder of the allocation shares.

As a service provider, our manager performs a variety of services for us, which entitles it to receive a management fee. As holder of our company’s allocation shares, our manager has the right to a preferred distribution in the form of a profit allocation upon the occurrence of certain events. Our manager paid $1,000 for the allocation shares. In addition, our manager will have the right to cause our company to purchase the allocation shares then owned by our manager upon termination of the management services agreement.

These relationships with our manager are governed principally by the following agreements:

·

the management services agreements relating to the services our manager will perform for us and our businesses; and

·

our company’s operating agreement relating to our manager’s rights with respect to the allocation shares it owns and which contains the supplemental put provision relating to our manager’s right to cause our company to purchase the allocation shares it owns.

We also expect that our manager will enter into offsetting management services agreements and transaction services agreements with our businesses directly. These agreements, and some of the material terms relating thereto, are discussed in more detail below. The management fee, profit allocation and put price under the supplemental put provision will be payment obligations of our company and, as a result, will be paid, along with other company obligations, prior to the payment of monthly distributions to shareholders.

The following table provides a simplified description of the fees and profit allocation rights held by our manager. Further detail is provided in the following subsections.

| 17 |

| Table of Contents |

|

Description |

|

Fee Calculation |

|

Payment Term |

|

|

|

|

|

|

|

Management Fees |

||||

|

| ||||

|

Determined by Management Services Agreement |

|

0.5% of adjusted net assets (2.0% annually) |

|

Quarterly |

|

|

| |||

|

Determined by Offsetting Management Services Agreement |

|

Payment of fees by our subsidiary businesses that result in a dollar for dollar reduction of manager fees paid by us to our manager such that our manager cannot receive duplicate fees from both us and our subsidiary |

|

Quarterly |

|

|

| |||

|

Termination Fee – Determined by Management Services Agreement |

|

Accumulated management fee paid in the preceding 4 fiscal quarters multiplied by 2. Paid only upon termination by our board and a majority in interest of our shareholders |

||

|

| ||||

|

Determined by Management Services Agreement |

|

Reimbursement of manager’s costs and expenses in providing services to us, but not including: (1) costs of overhead; (2) due diligence and other costs for potential acquisitions our board of directors does not approve pursuing or that are required by acquisition target to be reimbursed under a Transaction Services Agreement; and (3) certain seconded officers and employees |

|

Ongoing |

|

| ||||

|

Transaction Services Fees |

||||

|

| ||||

|

Acquisition services of target businesses or disposition of subsidiaries – fees determined by Transaction Services Agreements |

|

2.0% of aggregate purchase price up to $50 million; plus 1.5% of aggregate purchase price in excess of $50 million and up to and equal to $100 million; plus 1.0% of aggregate purchase price in excess of $100 million |

|

Per Transaction |

|

|

| |||

|

Manager Profit Allocation determined by our operating agreement |

|

20% of certain profits and gains on a sale of subsidiary after clearance of the 8% annual hurdle rate 8% hurdle rate determined for any subsidiary by multiplying the subsidiary’s average quarterly share of our assets by an 8% annualized rate |

|

Sale of a material amount of capital stock or assets of one of our businesses or subsidiaries.

Holding event: at the option of our manager, for the 30 day period following the 5th anniversary of an acquired business (but only based on historical profits of the business) |

Our Manager as a Service Provider

Management Fee

Our company will pay our manager a quarterly management fee equal to 0.5% (2.0% annualized) of its adjusted net assets, as discussed in more detail below.

Subject to any adjustments discussed below, for performing management services under the management services agreement during any fiscal quarter, our company will pay our manager a management fee with respect to such fiscal quarter. The management fee to be paid with respect to any fiscal quarter will be calculated as of the last day of such fiscal quarter, which we refer to as the calculation date. The management fee will be calculated by an administrator, which will be our manager so long as the management services agreement is in effect. The amount of any management fee payable by our company as of any calculation date with respect to any fiscal quarter will be (i) reduced by the aggregate amount of any offsetting management fees, if any, received by our manager from any of our businesses with respect to such fiscal quarter, (ii) reduced (or increased) by the amount of any over-paid (or under-paid) management fees received by (or owed to) our manager as of such calculation date, and (iii) increased by the amount of any outstanding accrued and unpaid management fees.

As an obligation of our company, the management fee will be paid prior to the payment of monthly distributions to our shareholders. If we do not have sufficient liquid assets to pay the management fee when due, we may be required to liquidate assets or incur debt in order to pay the management fee.

| 18 |

| Table of Contents |

Offsetting Management Services Agreements

Pursuant to the management services agreement, we have agreed that our manager may, at any time, enter into offsetting management services agreements with our businesses pursuant to which our manager may perform services that may or may not be similar to management services. Any fees to be paid by one of our businesses pursuant to such agreements are referred to as offsetting management fees and will offset, on a dollar-for-dollar basis, the management fee otherwise due and payable by our company under the management services agreement with respect to a fiscal quarter. The management services agreement provides that the aggregate amount of offsetting management fees to be paid to our manager with respect to any fiscal quarter shall not exceed the management fee to be paid to our manager with respect to such fiscal quarter.

Our manager entered into offsetting management services agreements with 1847 Neese and 1847 Fitness and may enter into offsetting management services agreements with our future subsidiaries, which agreements would be in the form prescribed by our management services agreement.

The services that our manager will provide to future subsidiaries under the offsetting management services agreements will include: conducting general and administrative supervision and oversight of the subsidiary’s day-to-day business and operations, including, but not limited to, recruiting and hiring of personnel, administration of personnel and personnel benefits, development of administrative policies and procedures, establishment and management of banking services, managing and arranging for the maintaining of liability insurance, arranging for equipment rental, maintenance of all necessary permits and licenses, acquisition of any additional licenses and permits that become necessary, participation in risk management policies and procedures; and overseeing and consulting with respect to the company’s business and operational strategies, the implementation of such strategies and the evaluation of such strategies, including, but not limited to, strategies with respect to capital expenditure and expansion programs, acquisitions or dispositions and product or service lines. If our manager and the subsidiary do not enter into an offsetting management services agreement, our manager will provide these services for our subsidiaries under our management services agreement.

The offsetting management fee paid to our manager for providing management services to a future subsidiary will vary.

On March 3, 2017, in connection with the acquisition of Neese, 1847 Neese entered into an offsetting management services agreement with our manager. Pursuant to the offsetting management services agreement, 1847 Neese appointed the manager to provide certain services to it for a quarterly management fee equal to $62,500 per quarter; provided, however, that (i) pro rated payments shall be made in the first quarter and the last quarter of the term, (ii) if the aggregate amount of management fees paid or to be paid by 1847 Neese, together with all other management fees paid or to be paid by all other subsidiaries of the company to the manager, in each case, with respect to any fiscal year exceeds, or is expected to exceed, 9.5% of the company’s gross income with respect to such fiscal year, then the management fee to be paid by 1847 Neese for any remaining fiscal quarters in such fiscal year shall be reduced, on a pro rata basis determined by reference to the management fees to be paid to the manager by all of the subsidiaries of the company, until the aggregate amount of the management fee paid or to be paid by 1847 Neese, together with all other management fees paid or to be paid by all other subsidiaries of the company to the manager, in each case, with respect to such fiscal year, does not exceed 9.5% of the company’s gross income with respect to such fiscal year, and (iii) if the aggregate amount the management fee paid or to be paid by 1847 Neese, together with all other management fees paid or to be paid by all other subsidiaries of the company to the manager, in each case, with respect to any fiscal quarter exceeds, or is expected to exceed, the aggregate amount of the management fee (before any adjustment thereto) calculated and payable under the management services agreement, which we refer to as the parent management fee, with respect to such fiscal quarter, then the management fee to be paid by 1847 Neese for such fiscal quarter shall be reduced, on a pro rata basis, until the aggregate amount of the management fee paid or to be paid by 1847 Neese, together with all other management fees paid or to be paid by all other subsidiaries of the company to the manager, in each case, with respect to such fiscal quarter, does not exceed the parent management fee calculated and payable with respect to such fiscal quarter.

1847 Neese shall also reimburse the manager for all costs and expenses of 1847 Neese which are specifically approved by the board of directors of 1847 Neese, including all out-of-pocket costs and expenses, which are actually incurred by the manager or its affiliates on behalf of 1847 Neese in connection with performing services under the offsetting management services agreement.

The services provided by the manager include: conducting general and administrative supervision and oversight of 1847 Neese’s day-to-day business and operations, including, but not limited to, recruiting and hiring of personnel, administration of personnel and personnel benefits, development of administrative policies and procedures, establishment and management of banking services, managing and arranging for the maintaining of liability insurance, arranging for equipment rental, maintenance of all necessary permits and licenses, acquisition of any additional licenses and permits that become necessary, participation in risk management policies and procedures; and overseeing and consulting with respect to 1847 Neese’s business and operational strategies, the implementation of such strategies and the evaluation of such strategies, including, but not limited to, strategies with respect to capital expenditure and expansion programs, acquisitions or dispositions and product or service lines.

| 19 |

| Table of Contents |

We expect that 1847 Fitness will enter into a similar offsetting management services agreement with our manager upon closing of the acquisition of Fitness CF. We expect that the quarterly management fee will be equal to $75,000.

Example of Calculation of Management Fee with Adjustment for Offsetting Management Fees

In order to better understand how the management fee is calculated, we are providing the following example:

|

Quarterly management fee: |

|

(in thousands) |

| ||||

| 1 |

|

|

Consolidated total assets |

|

$ | 100,000 |

|

| 2 |

|

|

Consolidated accumulation amortization of intangibles |

|

|

5,000 |

|

| 3 |

|

|

Total cash and cash equivalents |

|

|

5,000 |

|

| 4 |

|

|

Adjusted total liabilities |

|

|

(10,000 | ) |

| 5 |

|

|

Adjusted net assets (Line 1 + Line 2 – Line 3 – Line 4) |

|

|

90,000 |

|

| 6 |

|

|

Multiplied by quarterly rate |

|

|

0.5 | % |

| 7 |

|

|

Quarterly management fee |

|

$ | 450 |

|

|

|

|

|

|

|

|

|

|

|

Offsetting management fees: |

| ||||||

| 8 |

|

|

Acquired company A offsetting management fees |

|

$ | (100 | ) |

| 9 |

|

|

Acquired company B offsetting management fees |

|

|

(100 | ) |

| 10 |

|

|

Acquired company C offsetting management fees |

|

|

(100 | ) |

| 11 |

|

|

Acquired company D offsetting management fees |

|

|

(100 | ) |

| 12 |

|

|

Total offsetting management fees (Line 8 + Line 9 – Line 10 – Line 11) |

|

|

(400 | ) |

| 13 |

|

|

Quarterly management fee payable by Company (Line 7 + Line 12) |

|

$ | 50 |

|

The foregoing example provides hypothetical information only and does not intend to reflect actual or expected management fee amounts.

For purposes of the calculation of the management fee:

|

|

· | “Adjusted net assets” will be equal to, with respect to our company as of any calculation date, the sum of (i) consolidated total assets (as determined in accordance with U.S. generally accepted accounting principles, or GAAP) of our company as of such calculation date, plus (ii) the absolute amount of consolidated accumulated amortization of intangibles (as determined in accordance with GAAP) for our company as of such calculation date, minus (iii) total cash and cash equivalents, minus (iv) the absolute amount of adjusted total liabilities of our company as of such calculation date. |

|

|

|

|

|

|

· | “Adjusted total liabilities” will be equal to, with respect to our company as of any calculation date, our company’s consolidated total liabilities (as determined in accordance with GAAP) as of such calculation date after excluding the effect of any outstanding third party indebtedness of our company. |

|

|

|

|

|

|

· | “Quarterly management fee” will be equal to, as of any calculation date, the product of (i) 0.5%, multiplied by (ii) our company’s adjusted net assets as of such calculation date; provided, however, that with respect to any fiscal quarter in which the management services agreement is terminated, our company will pay our manager a management fee with respect to such fiscal quarter equal to the product of (i)(x) 0.5%, multiplied by (y) our company’s adjusted net assets as of such calculation date, multiplied by (ii) a fraction, the numerator of which is the number of days from and including the first day of such fiscal quarter to but excluding the date upon which the management services agreement is terminated and the denominator of which is the number of days in such fiscal quarter. |

|

|

|

|

|

|

· | “Total offsetting management fees” will be equal to, as of any calculation date, fees paid to our manager by the businesses that we acquire in the future under separate offsetting management services agreements. |

| 20 |

| Table of Contents |

Transaction Services Agreements