Attached files

| file | filename |

|---|---|

| EX-23.4 - EX-23.4 - Alta Mesa Resources, Inc. /DE | d507450dex234.htm |

| EX-23.3 - EX-23.3 - Alta Mesa Resources, Inc. /DE | d507450dex233.htm |

| EX-23.2 - EX-23.2 - Alta Mesa Resources, Inc. /DE | d507450dex232.htm |

| EX-23.1 - EX-23.1 - Alta Mesa Resources, Inc. /DE | d507450dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on April 6, 2018

Registration No. 333-223033

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Alta Mesa Resources, Inc.

(Exact Name of Registrant as Specified in its Charter)

| Delaware |

1311 | 81-4433840 | ||

| (State or other jurisdiction of incorporation) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

15021 Katy Freeway, Suite 400

Houston, Texas 77094

(281) 530-0991

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of registrant’s principal executive offices)

Harlan H. Chappelle

Chief Executive Officer

Alta Mesa Resources, Inc.

15021 Katy Freeway, Suite 400

Houston, Texas 77094

(281) 530-0991

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

Bill Nelson

Haynes and Boone, LLP

1221 McKinney, Ste 2100

Houston, Texas 77010

(713) 547-2084

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission acting pursuant to said Section 8(a), may determine.

Table of Contents

The information contained in this prospectus is not complete and may be changed. No securities may be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated April 6, 2018

Preliminary Prospectus

ALTA MESA RESOURCES, INC.

34,500,000 Shares of Class A Common Stock Issuable upon Exercise of

Outstanding Public Warrants

341,740,095 Shares of Class A Common Stock

This prospectus relates to the issuance by Alta Mesa Resources, Inc., a Delaware corporation (the “Company,” “we,” “our” or “us”) of 34,500,000 shares of our Class A Common Stock, par value $0.0001 per share (the “Class A Common Stock”), upon the exercise of warrants (the “Public Warrants”) originally sold as part of units, consisting of one share of Class A Common Stock and one-third of one Public Warrant, in our initial public offering (our “IPO”). Each Public Warrant entitles the holder to purchase one share of Class A Common Stock at an exercise price of $11.50 per share. We will receive the proceeds from the exercise of the Public Warrants, but not from the sale of the underlying shares of Class A Common Stock.

This prospectus also relates to the resale of 341,740,095 shares of Class A Common Stock by the selling stockholders named in this prospectus or their permitted transferees. The shares of Class A Common Stock being offered by the selling stockholders consist of (i) 213,402,398 shares of Class A Common Stock that have been or may be issued by us from time to time to certain members of SRII Opco, LP, a Delaware limited partnership (“SRII Opco”), who own common units representing limited partner interests (the “SRII Opco Common Units”) in SRII Opco, upon the redemption or exchange by such members of their SRII Opco Common Units for shares of Class A Common Stock pursuant to the limited partnership agreement of SRII Opco, (ii) up to 59,871,031 shares of Class A Common Stock that may be issued to the contributors pursuant to those certain Contribution Agreements, dated August 16, 2017, described herein (the “Contribution Agreements”) if the earn-out consideration described therein is issued to the contributors thereunder (the “Earn-Out Shares”), (iii) 40,000,000 shares of Class A Common Stock to Riverstone VI SR II Holdings, L.P. (“Fund VI Holdings”) pursuant to the terms of that certain Forward Purchase Agreement, dated as of March 17, 2017 (the “Forward Purchase Agreement”), (iv) 15,133,333 shares of Class A Common Stock underlying warrants (the “Private Placements Warrants”) originally sold pursuant to that certain Private Placement Warrant Purchase Agreement, dated as of March 23, 2017 (the “Warrant Purchase Agreement”), to Silver Run Sponsor II, LLC (the “Sponsor”), and (v) 13,333,333 shares of Class A Common Stock underlying warrants (the “Forward Purchase Warrants”) originally sold to Fund VI Holdings pursuant to the terms of the Forward Purchase Agreement.

The selling stockholders may offer, sell or distribute all or a portion of their shares of Class A Common Stock publicly or through private transactions at prevailing market prices or at negotiated prices. Although we will receive the exercise price of the Private Placement Warrants and the Forward Purchase Warrants if those warrants are not exercised on a cashless basis, we will not receive any of the proceeds from the sale of the shares of Class A Common Stock owned by the selling stockholders. We will bear all costs, expenses and fees in connection with the registration of these shares of Class A Common Stock, including with regard to compliance with state securities or “blue sky” laws. The selling stockholders will bear all commissions and discounts, if any, attributable to their sale of shares of Class A Common Stock. See “Plan of Distribution” beginning on page 167 of this prospectus.

The Class A Common Stock and Public Warrants are quoted on The NASDAQ Capital Market (“NASDAQ”) under the symbols “AMR” and “AMRWW,” respectively. On April 5, 2018, the closing prices of our Class A Common Stock and Public Warrants were $7.30 and $1.50, respectively. On April 5, 2018, we had 169,371,730 shares of Class A Common Stock and 34,500,000 Public Warrants issued and outstanding.

We are an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended (the “Securities Act”), as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and are subject to reduced public company reporting requirements. This prospectus complies with the requirements that apply to an issuer that is an emerging growth company.

INVESTING IN THESE SECURITIES INVOLVES CERTAIN RISKS. SEE “RISK FACTORS” ON PAGE 10.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2018

Table of Contents

| 1 | ||||

| 10 | ||||

| 50 | ||||

| 52 | ||||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| 57 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

94 | |||

| 121 | ||||

| 129 | ||||

| 150 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

161 | |||

| 164 | ||||

| 167 | ||||

| 170 | ||||

| MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS |

180 | |||

| 184 | ||||

| 184 | ||||

| 185 | ||||

| F-1 | ||||

| A-1 | ||||

| B-1 |

You should rely only on the information contained in this prospectus, any prospectus supplement or in any free writing prospectus we may authorize to be delivered or made available to you. We have not, and the selling stockholders have not, authorized anyone to provide you with different information. We and the selling stockholders are not offering to sell, or seeking offers to buy, shares of our Class A Common Stock in jurisdictions where offers and sales are not permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our Class A Common Stock.

INDUSTRY AND MARKET DATA

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications and other published independent sources. Although we believe these third-party sources are reliable as of their respective dates, neither we nor the selling stockholders have independently verified the accuracy or completeness of this information. Some data is also based on our good faith estimates. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these publications.

TRADEMARKS AND TRADE NAMES

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks,

i

Table of Contents

service marks, trade names or products in this prospectus is not intended to, and does not imply, a relationship with us or an endorsement or sponsorship by or of us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, service marks and trade names.

ii

Table of Contents

GLOSSARY

Unless the context otherwise requires, references in this prospectus to:

| • | “20-Day VWAP” are to the per share volume-weighted average price at which the Class A Common Stock is traded over a 20 trading day period; |

| • | “Alta Mesa” are to Alta Mesa Holdings, LP, a Delaware limited partnership; |

| • | “Alta Mesa Contribution Agreement” are to the Contribution Agreement, dated as of August 16, 2017, among the Alta Mesa Contributor, High Mesa GP, the sole general partner of the Alta Mesa Contributor, Alta Mesa, Alta Mesa GP, us and, solely for certain provisions therein, the equity owners of the Alta Mesa Contributor; |

| • | “Alta Mesa Contributor” are to High Mesa Holdings, LP, a Delaware limited partnership; |

| • | “Alta Mesa GP” are to Alta Mesa Holdings GP, LLC, a Texas limited liability company and sole general partner of Alta Mesa; |

| • | “Alta Mesa Parties” are to Alta Mesa and Alta Mesa GP; |

| • | “AMR” are to Alta Mesa Resources, Inc.; |

| • | “Business Combination” are to the transactions contemplated by the Contribution Agreements; |

| • | “Charter” are to our Second Amended and Restated Certificate of Incorporation; |

| • | “Class A Common Stock” are to our Class A Common Stock, par value $0.0001 per share; |

| • | “Class B Common Stock” are to our Class B Common Stock, par value $0.0001 per share; |

| • | “Class C Common Stock” are to our Class C Common Stock, par value $0.0001 per share; |

| • | “Closing” are to the closing of the Business Combination; |

| • | “Closing Date” are to the date on which the Closing occurred, which was February 9, 2018; |

| • | “Company,” “we,” “our,” or “us” and similar terms, (i) in the context of financial information included in the body of this Prospectus, including “Selected Historical Financial Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operation,” refer to Alta Mesa prior to the Business Combination and to AMR subsequent to the Business Combination, (ii) in the context of AMR’s E&P Business, refer to Alta Mesa prior to the Business Combination and to AMR subsequent to the Business Combination, (iii) in the context of AMR’s Midstream Business, refer to Kingfisher prior to the Business Combination and to AMR subsequent to the Business Combination, and (iv) in all other contexts refers to AMR (formerly Silver Run Acquisition Corporation II) and its subsidiaries; |

| • | “Contribution Agreements” are to the Alta Mesa Contribution Agreement, the Kingfisher Contribution Agreement and the Riverstone Contribution Agreement, collectively; |

| • | “Contributors” are to the Alta Mesa Contributor, the Kingfisher Contributor and the Riverstone Contributor, collectively; |

| • | “Forward Purchase Agreement” are to the Forward Purchase Agreement, dated as of March 17, 2017, by and between us and Fund VI Holdings; |

| • | “founder shares” are to shares of our Class B Common Stock purchased by our Sponsor in a private placement prior to our IPO, which were converted into shares of Class A Common Stock on a one-for-one basis in connection with the Closing; |

| • | “Fund VI Holdings” are to Riverstone VI SR II Holdings, L.P., a Delaware limited partnership; |

| • | “High Mesa GP” are to High Mesa Holdings GP, LLC, a Texas limited liability company; |

| • | “initial business combination” are to our initial merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses; |

| • | “Initial Limited Partners” are to the Alta Mesa Contributor and the Riverstone Contributor; |

iii

Table of Contents

| • | “initial stockholders” are to holders of our founder shares prior to our IPO, including our Sponsor and our independent directors prior to the Business Combination; |

| • | “IPO” are to our initial public offering of units, which closed on March 29, 2017; |

| • | “Kingfisher” are to Kingfisher Midstream, LLC, a Delaware limited liability company; |

| • | “Kingfisher Contribution Agreement” are to the Contribution Agreement, dated as of August 16, 2017, among the Kingfisher Contributor, Kingfisher, us and, solely for certain provisions therein, the equity owners of the Kingfisher Contributor; |

| • | “Kingfisher Contributor” are to KFM Holdco, LLC, a Delaware limited liability company; |

| • | “management” or our “management team” are to our officers and directors; |

| • | “non-STACK assets” are to assets of Alta Mesa (including the Weeks Island assets) other than its oil and gas assets located in the STACK; |

| • | “Phase II assets” are to a second natural gas cryogenic processing facility, which will be located adjacent to our existing 60 MMcf/d cryogenic processing facility, with a processing capacity of 200 MMcf/d; |

| • | “Preferred Stock” are to our Series A Preferred Stock and Series B Preferred Stock; |

| • | “Private Placement Warrants” are to the warrants issued to the Sponsor in a private placement simultaneously with the closing of our IPO; |

| • | “Private Placements” are to the issuance and sale of 40,000,000 shares of Class A Common Stock and 13,133,333 private placement warrants to Fund VI Holdings pursuant to the Forward Purchase Agreement; |

| • | “public shares” are to shares of our Class A Common Stock sold as part of the units in the IPO (whether they were purchased in the IPO or thereafter in the open market); |

| • | “public stockholders” are to the holders of our public shares; |

| • | “Public Warrants” are to the warrants sold as part of the units in the IPO; |

| • | “Riverstone” are to Riverstone Investment Group LLC and its affiliates, including our Sponsor, Fund VI Holdings and the Riverstone Contributor, collectively; |

| • | “Riverstone Contribution Agreement” are to the Contribution Agreement, dated as of August 16, 2017, between the Riverstone Contributor and us; |

| • | “Riverstone Contributor” are to Riverstone VI Alta Mesa Holdings, L.P., a Delaware limited partnership; |

| • | “Series A Preferred Stock” are to our Series A Preferred Stock, par value $0.0001 per share; |

| • | “Series B Preferred Stock” are to our Series B Preferred Stock, par value $0.0001 per share; |

| • | “Sponsor” are to Silver Run Sponsor II, LLC, a Delaware limited liability company and an affiliate of Riverstone; |

| • | “SRII Opco” are to SRII Opco, LP, a Delaware limited partnership; |

| • | “SRII Opco Common Units” are to common units representing limited partner interests in SRII Opco; |

| • | “STACK” is an acronym describing both its location—Sooner Trend Anadarko Basin Canadian and Kingfisher County—and the multiple, stacked productive formations present in the area; |

| • | “Tax Receivable Agreement” are to the Tax Receivable Agreement entered into at Closing among us, SRII Opco and the Initial Limited Partners; |

iv

Table of Contents

| • | “Transactions” are to (a) the consummation of the Business Combination, (b) the completion of the Private Placements and (c) the conversion of the founder shares into shares of Class A Common Stock on a one-for-one basis in connection with the Business Combination; |

| • | “units” are to our units sold in our IPO, each of which consists of one share of Class A Common Stock and one-third of one Public Warrant; and |

| • | “voting common stock” are to our Class A Common Stock and Class C Common Stock. |

For additional defined terms commonly used in the oil and natural gas industry and used in this prospectus, please see “Glossary of Oil and Natural Gas Terms” set forth in Exhibit A.

v

Table of Contents

This summary highlights certain information appearing elsewhere in this prospectus. For a more complete understanding of this offering, you should read the entire prospectus carefully, including the risk factors and the financial statements.

Our Company

Corporate History

We were originally formed in November 2016 as a special purpose acquisition company under the name Silver Run Acquisition Corporation II for the purpose of effecting an initial business combination. On March 29, 2017, we consummated our IPO generating net proceeds of approximately $1.0 billion. Simultaneously with the closing of our IPO, we completed the private sale of 15,133,333 warrants (the “Private Placement Warrants”) to Silver Run Sponsor II, LLC (the “Sponsor”) generating gross proceeds to us of $22,700,000. A total of $1.035 billion (including approximately $36.2 million in deferred underwriting commissions to the underwriters of the IPO), which represents $1.0143 billion of the proceeds from the IPO after deducting upfront underwriting commissions of $20.7 million, and the proceeds of the sale of the private placement warrants were placed in the Trust Account (the “Trust Account”) to be used to fund an initial business combination. Until the consummation of the Business Combination, our Class A common stock, par value $0.0001 per share (the “Class A Common Stock”), warrants and units, consisting of one share of Class A Common Stock and one-third of one warrant (“units”), were traded on The NASDAQ Capital Market (“NASDAQ”) under the ticker symbols “SRUN,” “SRUNW” and “SRUNU,” respectively.

On February 9, 2018 (the “Closing Date”), we consummated the acquisition of (i) all of the limited partnership interests in Alta Mesa Holdings, LP (“Alta Mesa”), (ii) 100% of the economic interests and 90% of the voting interests in Alta Mesa Holdings GP, LLC, the sole general partner of Alta Mesa (“Alta Mesa GP”), and (iii) all of the membership interests in Kingfisher Midstream, LLC (“Kingfisher”) (such acquisition, the “Business Combination”), pursuant to:

| • | the Contribution Agreement, dated as of August 16, 2017 (the “Alta Mesa Contribution Agreement”), among High Mesa Holdings, LP (the “Alta Mesa Contributor”), High Mesa Holdings GP, LLC, the sole general partner of the Alta Mesa Contributor, Alta Mesa, Alta Mesa GP, LLC, us and the equity owners of the Alta Mesa Contributor; |

| • | the Contribution Agreement, dated as of August 16, 2017 (the “Kingfisher Contribution Agreement”), among KFM Holdco, LLC (the “Kingfisher Contributor”), Kingfisher, us and the equity owners of the Kingfisher Contributor; and |

| • | the Contribution Agreement, dated as of August 16, 2017 (the “Riverstone Contribution Agreement” and, together with the Alta Mesa Contribution Agreement and the Kingfisher Contribution Agreement, the “Contribution Agreements”), between Riverstone VI Alta Mesa Holdings, L.P. (the “Riverstone Contributor” and, together with the Alta Mesa Contributor and the Kingfisher Contributor, the “Contributors”) and us. |

At the closing of the Business Combination (the “Closing”),

| • | we issued 40,000,000 shares of Class A Common Stock and warrants to purchase 13,333,333 shares of Class A Common Stock to Riverstone VI SR II Holdings, L.P. (“Fund VI Holdings”) pursuant to the terms of that certain Forward Purchase Agreement, dated as of March 17, 2017 (the “Forward Purchase Agreement”) for cash proceeds of $400 million to us; |

1

Table of Contents

| • | we contributed $1,406 million in cash (the proceeds of the Forward Purchase Agreement and the net proceeds (after redemptions) of the Trust Account) to SRII Opco, LP, a Delaware limited partnership (“SRII Opco”), in exchange for (i) 169,371,730 of the common units (approximately 44.2%) representing limited partner interests (the “SRII Opco Common Units”) in SRII Opco issued to us and (ii) 62,966,666 warrants to purchase SRII Opco Common Units (“SRII Opco Warrants”) issued to us; |

| • | we caused SRII Opco to issue 213,402,398 SRII Opco Common Units (approximately 55.8%) to the Contributors in exchange for the ownership interests in Alta Mesa, Alta Mesa GP and Kingfisher contributed to SRII Opco by the Contributors; |

| • | we agreed to cause SRII Opco to issue up to 59,871,031 SRII Opco Common Units to the Alta Mesa Contributor and the Kingfisher Contributor if the earn-out consideration provided for in the Contribution Agreements is earned by the Alta Mesa Contributor or the Kingfisher Contributor pursuant to the terms of the Contribution Agreements; |

| • | we issued to each of the Contributors a number of shares of Class C common stock, par value $0.0001 per share (the “Class C Common Stock”), equal to the number of the SRII Opco Common Units received by such Contributor at the Closing; |

| • | SRII Opco distributed to the Kingfisher Contributor cash in the amount of approximately $814.8 million in partial payment for the ownership interests in Kingfisher contributed by the Kingfisher Contributor; and |

| • | SRII Opco entered into a voting agreement with the owners of the remaining 10% voting interests in Alta Mesa GP whereby such other owners agreed to vote their interests in Alta Mesa GP as directed by SRII Opco. |

Holders of Class C Common Stock, together with holders of Class A Common Stock, voting as a single class, have the right to vote on all matters properly submitted to a vote of the stockholders, but holders of Class C Common Stock are not entitled to any dividends or liquidating distributions from us. After a specified period of time after Closing, the Contributors will generally have the right to cause SRII Opco to redeem all or a portion of their SRII Opco Common Units in exchange for shares of our Class A Common Stock or, at SRII Opco’s option, an equivalent amount of cash. However, we may, at our option, effect a direct exchange of cash or Class A Common Stock for such SRII Opco Common Units in lieu of such a redemption by SRII Opco. Upon the future redemption or exchange of SRII Opco Common Units held by a Contributor, a corresponding number of shares of Class C Common Stock will be cancelled.

In connection with the Closing, we also issued (i) one share of Series A Preferred Stock, par value $0.0001 per share (“Series A Preferred Stock”), to each of Bayou City Energy Management, LLC (“Bayou City”), HPS Investment Partners, LLC (“HPS”), and AM Equity Holdings, LP (“AM Management”), and (ii) one share of Series B Preferred Stock, par value $0.0001 per share (“Series B Preferred Stock”), to the Riverstone Contributor. None of the holders of the Series A Preferred Stock or Series B Preferred Stock are entitled to any dividends from us related to such Preferred Stock, but such holders are entitled to preferred distributions in liquidation in the amount of $0.0001 per share of Preferred Stock, and have limited voting rights as described below. Shares of the Preferred Stock are redeemable for the par value thereof by us upon the earlier to occur of (1) the fifth anniversary of the Closing Date, (2) the optional redemption of such Preferred Stock at the election of the holder thereof or (3) upon a breach by the holder of the transfer restrictions applicable to such Preferred Stock. For so long as the Series A Preferred Stock or Series B Preferred Stock remains outstanding, as applicable, the holders thereof will be entitled to nominate and elect directors to our board of directors for a period of up to five years following the Closing based on their and their affiliates’ beneficial ownership of Class A Common Stock.

2

Table of Contents

On February 6, 2018, our stockholders voted to approve the Business Combination. In connection with that vote, the holders of shares of Class A Common Stock originally sold as part of the units issued in our IPO (such holders, the “public stockholders”), were provided with the opportunity to redeem shares of Class A Common Stock then held by them for cash equal to approximately $10.00 per share. Public holders of 3,270 shares of Class A Common Stock elected to redeem those shares and, at the Closing, $32,944 held in the Trust Account was paid to such redeeming shareholders and the remaining $1,042.7 million held in the Trust Account was disbursed to us to fund our obligations under the Contribution Agreements and to pay the underwriters’ deferred discount arising out of the IPO.

Following the Business Combination, we changed our name from “Silver Run Acquisition Corporation II” to “Alta Mesa Resources, Inc.” and continued the listing of our Class A Common Stock and Public Warrants on NASDAQ under the symbols “AMR” and “AMRWW,” respectively. Following the completion of the Business Combination, the size of our board of directors was expanded from four directors to 11, including one director appointed by Bayou City and its affiliates, one director appointed by HPS and its affiliates and two directors appointed by AM Management and its affiliates, as the holders of our Series A Preferred Stock, and three directors appointed by the Riverstone Contributor and its affiliates, as the holder of our Series B Preferred Stock. In addition, in connection with the Business Combination, we appointed the management team of Alta Mesa to hold most of our executive officer positions.

Alta Mesa is considered our accounting predecessor and hence the historical financial statements of Alta Mesa as of December 31, 2017 and 2016 and for each of the three years ended December 31, 2017 are included elsewhere in this prospectus. The (a) historical financial statements of AMR as of December 31, 2017 and 2016, and for the year ended December 31, 2017, and period from November 16, 2016 (date of inception) to December 31, 2016, (b) historical financial statements of Kingfisher as of December 31, 2017 and 2016, and for the two years ended December 31, 2017 and 2016, and (c) the unaudited pro forma balance sheet of AMR as of December 31, 2017, and income statement for the year ended December 31, 2017 are included only as Exhibits to this prospectus. Alta Mesa and Kingfisher continue to exist as separate subsidiaries of SRII Opco and those entities are separately financed, with each having debt obligations that are not obligations of the other. Consequently, references herein to Alta Mesa and to Kingfisher are to those entities and not to the Company as a whole.

Business Overview

As a result of the Business Combination, our only significant asset is our ownership of an approximate 44.2% partnership interest in SRII Opco. SRII Opco owns all of the economic interests in each of Alta Mesa and Kingfisher. Founded in 1987, Alta Mesa, the predecessor to our E&P Business, was an independent exploration and production company focused on the development and acquisition of unconventional oil and natural gas reserves in the eastern portion of the Anadarko Basin referred to as the STACK. The STACK is an acronym describing both its location—Sooner Trend Anadarko Basin Canadian and Kingfisher County—and the multiple, stacked productive formations present in the area. The STACK is a prolific hydrocarbon system with high oil and liquids-rich natural gas content, multiple horizontal target horizons, extensive production history and historically high drilling success rates. As of December 31, 2017, we have assembled a highly contiguous position of approximately 130,000 net acres largely in the up-dip, naturally-fractured oil portion of the STACK in eastern Kingfisher County, Oklahoma. Our drilling locations primarily target formations comprised of the Osage, Meramec and Oswego. We continue to acquire acreage within and adjacent to our acreage footprint with the goal of operating the drilling, completion and production operations in such locations. At present, we are operating seven horizontal drilling rigs in the STACK with plans to increase the number of rigs by the end of 2018. Following our Business Combination, our anticipated capital expenditures for 2018 of $568 million are all allocated to the STACK.

3

Table of Contents

Our Midstream Business was started by Kingfisher on January 30, 2015 for the purpose of acquiring, developing and operating midstream oil and gas assets. We primarily focus on providing crude oil gathering, gas gathering and processing and marketing to producers of natural gas, NGLs, crude oil and condensate in the STACK play. Our midstream energy asset network includes approximately 308 miles of existing low and high pressure pipelines, a 60 MMcf/d cryogenic natural gas processing plant, 10 MMcf/d in offtake processing, compression facilities, crude storage, NGL storage and purchasing and marketing capabilities.

Our goal is to build a premier development and acquisition company focused on horizontal drilling and gas gathering in the STACK.

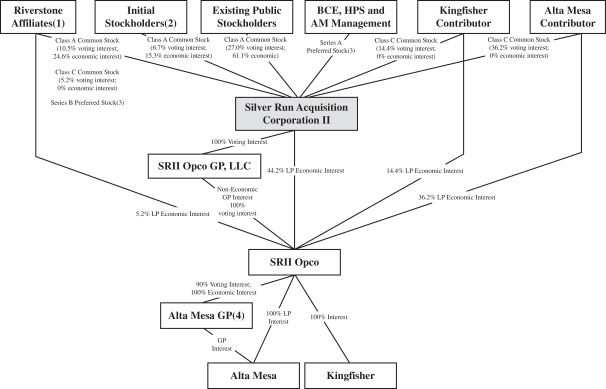

Organizational Structure

The following diagram illustrates our ownership structure immediately following the Closing.

| (1) | Includes (x) shares of Class C Common Stock, one share of Series B Preferred Stock owned by the Riverstone Contributor and a 5.2% limited partner interest in SRII Opco and (y) shares of Class A Common Stock owned by Fund VI Holdings. |

| (2) | Includes shares of Class A Common Stock issued upon conversion of the founders shares to our Sponsor and independent directors. |

| (3) | The Series A Preferred Stock and the Series B Preferred Stock will not have any voting rights (other than the right to nominate a certain number of directors for election to our board of directors as described herein) or rights with respect to dividends but are entitled to preferred distributions in liquidation in the amount of $0.0001 per share. |

| (4) | Certain existing owners of Alta Mesa, including Harlan H. Chappelle, our Chief Executive Officer and a director, Michael E. Ellis, our Chief Operating Officer, Upstream and a director, and certain affiliates of |

4

Table of Contents

| Bayou City and HPS, own an aggregate 10% voting interest in Alta Mesa GP. These existing owners are a party to a voting agreement with SRII Opco and the existing owners will agree to vote their interests in Alta Mesa GP as directed by SRII Opco. |

Additional Information

Our principal executive offices are located at 15021 Katy Freeway, Suite 400, Houston, Texas 77094, and our telephone number is (281) 530-0991. Our website is www.altamesa.net. Information on our website or any other website is not incorporated by reference into, and does not constitute a part of, this prospectus.

Our Emerging Growth Company Status

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the JOBS Act. As an emerging growth company, we may, for up to five years, take advantage of specified exemptions from reporting and other regulatory requirements that are otherwise applicable generally to public companies. These exemptions include:

| • | the presentation of only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations; |

| • | deferral of the auditor attestation requirement on the effectiveness of our system of internal control over financial reporting; |

| • | exemption from the adoption of new or revised financial accounting standards until they would apply to private companies; |

| • | exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the Company; and |

| • | reduced disclosure about executive compensation arrangements. |

We may take advantage of these provisions until we are no longer an emerging growth company, which will occur on the earliest of (i) the last day of the fiscal year following March 29, 2022, the fifth anniversary of our IPO, (ii) the last day of the fiscal year in which we have more than $1.07 billion in annual revenue, (iii) the date on which we issue more than $1.0 billion of non-convertible debt over a three-year period and (iv) the date on which we are deemed to be a “large accelerated filer,” as defined in Rule 12b-2 promulgated under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We have elected to take advantage of each of the exemptions for emerging growth companies, other than the presentation of only two years of audited financial statements and related Management’s Discussion and Analysis of Financial Conditions and Results of Operations.

Accordingly, the information that we provide you may be different than what you may receive from other public companies in which you hold equity interests.

5

Table of Contents

The Offering

We are registering (i) the issuance by us of 34,500,000 shares of Class A Common Stock underlying the Public Warrants and (ii) the resale of 341,740,095 shares of Class A Common Stock by the selling stockholders named in this prospectus, or their permitted transferees.

Issuance of Class A Common Stock Underlying the Public Warrants

| Shares of Class A Common Stock to be Issued upon Exercise of the Public Warrants |

34,500,000 shares of Class A Common Stock. |

| Shares of Class A Common Stock Outstanding Prior to Exercise of the Public Warrants(1) |

169,371,730 shares of Class A Common Stock, as of April 5, 2018. |

| Shares of Class A Common Stock to be Outstanding Assuming Exercise of the Public Warrants(1) |

203,871,730 shares of Class A Common Stock. |

| Terms of the Public Warrants |

Each Public Warrant entitles the holder to purchase one share of Class A Common Stock for $11.50 per share, at any time commencing on March 29, 2018, which is 12 months following the closing of our IPO. The Public Warrants will expire at 5:00 p.m., New York time, on February 9, 2023 (which is five years after the completion of the Business Combination) or earlier upon redemption or liquidation. |

| Use of Proceeds |

We expect to receive $396,750,000 in net proceeds assuming the exercise of all of our Public Warrants at the exercise price of $11.50 per share. We intend to use these net proceeds for general corporate purposes. |

| Trading Market and Ticker Symbol |

Our Public Warrants are listed on NASDAQ under the symbol “AMRWW.” |

Resale of Class A Common Stock by Selling Stockholders

| Shares Offered by the Selling Stockholders |

We are registering 341,740,095 shares of Class A Common Stock to be offered by the selling stockholders named herein. |

| Terms of the Offering |

The selling stockholders will determine when and how they will dispose of the shares of Class A Common Stock registered under this prospectus for resale. |

| Shares Outstanding Prior to This Offering(1)(2) |

As of April 5, 2018, 169,371,730 shares of Class A Common Stock, 213,402,398 shares of Class C Common Stock, three shares of Series A Preferred Stock and one share of Series B Preferred Stock were issued and outstanding. |

6

Table of Contents

| Shares Outstanding After This Offering(1)(2)(3) |

382,774,128 shares of Class A Common Stock, no shares of Class C Common Stock, three shares of Series A Preferred Stock and one share of Series B Preferred Stock will be issued and outstanding. |

| Terms of the Private Placement Warrants and Forward Purchase Warrants |

The Private Placement Warrants and the Forward Purchase Warrants are identical to the Public Warrants, except that for so long as they are held by the Sponsor or any of its permitted transferees, the Private Placement Warrants and the Forward Purchase Warrants: (i) may be exercised for cash or on a cashless basis, (ii) may not be transferred, assigned or sold until thirty (30) days after the completion of the Business Combination, and (iii) are not redeemable by us. |

| Use of Proceeds |

We will not receive any of the proceeds from the sale of shares of Class A Common Stock by the selling stockholders. We expect to receive $327,366,659 in net proceeds assuming the exercise of all of our Private Placement Warrants and the Forward Purchase Warrants (other than on a cashless basis) at the exercise price of $11.50 per share. We intend to use these net proceeds for general corporate purposes. |

| Trading Market and Ticker Symbol |

Our Class A Common Stock is listed on NASDAQ under the symbol “AMR.” |

| (1) | The number of shares of Class A Common Stock does not include (i) the 50,000,000 shares of Class A Common Stock available for future issuance under the Alta Mesa Resources, Inc. 2018 Long Term Incentive Plan, (ii) the 15,133,333 shares of Class A Common Stock issuable upon exercise of the Private Placement Warrants, (iii) the 13,333,333 shares of Class A Common Stock issuable upon exercise of the Forward Purchase Warrants or (iv) 59,871,031 shares of Class A Common Stock that may be issuable to the Alta Mesa Contributor and the Kingfisher Contributor pursuant to the earn-out provisions of the Contribution Agreements. |

| (2) | The number of shares of Class A Common Stock does not include the 34,500,000 shares of Class A Common Stock issuable upon exercise of the Public Warrants. |

| (3) | The number of shares of Class A Common Stock presumes the Contributors redeemed 213,402,398 SRII Opco Common Units for shares of Class A Common Stock on a one-to-one basis. Upon such redemption, an equal number of shares of Class C Common Stock were cancelled. |

For additional information concerning the offering, see “Plan of Distribution” beginning on page 167.

Risk Factors

Before investing in our securities, you should carefully read and consider the information set forth in “Risk Factors ” beginning on page 10.

7

Table of Contents

Summary Historical Reserve and Summary Historical Reserve and Operating Data

The following tables present, for the periods and as of the dates indicated, summary data with respect to Alta Mesa’s estimated net proved reserves (which includes non-STACK assets) and for its STACK assets and operating data. In connection with the Alta Mesa Contribution Agreement, Alta Mesa sold a portion of its non-STACK assets for cash on December 30, 2017 and distributed the remaining non-STACK assets to its owners (other than the Riverstone Contributor) immediately prior to Closing. Alta Mesa received $22.5 million in cash for the non-STACK assets that it sold, which proceeds were used to reduce its outstanding indebtedness, resulting in an increase in the consideration payable to the owners of Alta Mesa (other than the Riverstone Contributor) in the Business Combination. Accordingly, no reserve information with respect to non-STACK assets is presented. The operating data presented includes information operating information attributable to our predecessor’s STACK and non-STACK assets.

The reserve estimates attributable to Alta Mesa’s properties as of December 31, 2017 presented in the table below are based on a reserve report prepared by its internal engineers and audited by Ryder Scott Company, L.P. (“Ryder Scott”), its independent petroleum engineer (which we refer to as the “2017 Reserve Report”). A copy of the 2017 Reserve Report is attached to this prospectus as Exhibit B. All of these reserve estimates were prepared in accordance with the SEC’s rules regarding oil and natural gas reserve reporting that are currently in effect. The following tables also contain summary unaudited information regarding production and sales of oil, natural gas and natural gas liquids with respect to such properties.

See the sections entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business—Oil and Natural Gas Reserves” in evaluating the material presented below.

| The Company | STACK Assets | |||||||||||||||

| Oil and Natural Gas Liquids (MBbls) |

Gas (MMcf) |

Oil and Natural Gas Liquids (MBbls) |

Gas (MMcf) |

|||||||||||||

| Proved Reserves(1) |

||||||||||||||||

| Developed |

32,527 | 150,183 | 31,061 | 126,879 | ||||||||||||

| Undeveloped |

77,878 | 283,336 | 76,905 | 282,402 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Proved |

110,405 | 433,519 | 107,966 | 409,281 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Alta Mesa’s proved reserves as of December 31, 2017 were calculated using oil and natural gas price parameters established by current SEC guidelines and accounting rules based on unweighted arithmetic average prices as of the first day of each of the 12 months ended on such date. For December 31, 2017, these average prices were $51.34 per Bbl for oil and $2.98 per MMBtu for natural gas. Pricing was adjusted for basis differentials by field based on our historical realized prices. The estimated realized price for natural gas liquids using a $51.34 per Bbl benchmark and adjusted for average differentials was $26.06 per Bbl. Natural gas liquid prices vary depending on the composition of the natural gas liquids basket and current prices for various components thereof, such as butane, ethane, and propane, among others. |

8

Table of Contents

| Year Ended December 31, 2017 The Company |

Year Ended December 31, 2017 STACK Assets |

|||||||

| Net production: |

||||||||

| Oil (MBbls) |

4,167 | 3,907 | ||||||

| Natural gas (MMcf) |

18,115 | 13,973 | ||||||

| Natural gas liquids (MBbls) |

1,387 | 1,277 | ||||||

| Total (MBOE) |

8,573 | 7,513 | ||||||

| Total (MMcfe) |

51,440 | 45,077 | ||||||

| Average sales price per unit before hedging effects: |

||||||||

| Oil (per Bbl) |

$ | 49.44 | $ | 49.76 | ||||

| Natural gas (per Mcf) |

2.63 | 2.70 | ||||||

| Natural gas liquids (per Bbl) |

24.36 | 24.62 | ||||||

| Combined (per BOE) |

33.52 | 35.10 | ||||||

| Average costs per BOE: |

||||||||

| Lease and plant operating expense |

$ | 7.10 | $ | 5.32 | ||||

| Marketing and transportation expense |

3.56 | 3.92 | ||||||

| Production and ad valorem taxes |

0.84 | 0.74 | ||||||

| Workover expense |

0.69 | 0.57 | ||||||

| Average costs per Mcfe: |

||||||||

| Lease and plant operating expense |

$ | 1.18 | $ | 0.89 | ||||

| Marketing and transportation expense |

0.59 | 0.65 | ||||||

| Production and ad valorem taxes |

0.14 | 0.12 | ||||||

| Workover expense |

0.11 | 0.09 | ||||||

9

Table of Contents

Investing in our securities involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including our consolidated financial statements and related notes, before deciding whether to purchase any of our securities. Any of these risks may have a material adverse effect on our business, financial condition, results of operations and cash flows and our prospects could be harmed. In that event, the price of our securities could decline and you could lose part or all of your investment.

Risks Related to Our Securities and Capital Structure

Our only significant asset is the ownership of the general partner interest and a 44.2% limited partner interest in SRII Opco, and such ownership may not be sufficient to enable us to pay any dividends on our Class A Common Stock or satisfy our other financial obligations, including under the Tax Receivable Agreement.

We have no direct operations and no significant assets other than the ownership of the general partner interest and a 44.2% limited partner interest in SRII Opco. We will depend on SRII Opco and its subsidiaries, including Alta Mesa and Kingfisher, for distributions, loans and other payments to generate the funds necessary to meet our financial obligations or to pay any dividends with respect to our Class A Common Stock. Subject to certain restrictions, SRII Opco generally is required to (i) make pro rata distributions to its partners, including us, in an amount at least sufficient to allow us to pay our taxes and (ii) reimburse us for certain corporate and other overhead expenses. However, legal and contractual restrictions in agreements governing future indebtedness of SRII Opco and its subsidiaries, including Alta Mesa and Kingfisher, as well as the financial condition and operating requirements of Alta Mesa and Kingfisher may limit our ability to obtain cash from SRII Opco. The earnings from, or other available assets of, SRII Opco and its subsidiaries, including Alta Mesa and Kingfisher, may not be sufficient to enable us to pay any dividends on our Class A Common Stock or satisfy our other financial obligations. SRII Opco will be treated as a partnership for U.S. federal income tax purposes and, as such, will not be subject to any entity-level U.S. federal income tax. Instead, taxable income will be allocated to holders of its SRII Opco Common Units, including us. As a result, we generally will incur income taxes on our allocable share of any net taxable income of SRII Opco. Under the terms of the agreement of limited partnership of SRII Opco (the “SRII Opco LPA”), SRII Opco is obligated to make tax distributions to holders of its SRII Opco Common Units, including us, except to the extent such distributions would render SRII Opco insolvent or are otherwise prohibited by law or any of our current or future debt agreements. In addition to tax expenses, we will also incur expenses related to our operations, our interests in SRII Opco and related party agreements, including payment obligations under the Tax Receivable Agreement, and expenses and costs of being a public company, all of which could be significant. See “Certain Relationships and Related Party Transactions—Tax Receivable Agreement.” To the extent that we need funds and SRII Opco or any of its subsidiaries is restricted from making such distributions under applicable law or regulation or under the terms of their financing arrangements, or are otherwise unable to provide such funds, it could materially adversely affect our liquidity and financial condition, including our ability to pay our income taxes when due.

We may be required to take write-downs or write-offs, restructuring and impairment or other charges that could have a significant negative effect on our financial condition, results of operations and stock price, which could cause you to lose some or all of your investment.

Although we have conducted due diligence on Alta Mesa and Kingfisher, we cannot assure you that this diligence revealed all material issues that may be present in the businesses of Alta Mesa or Kingfisher, that it would be possible to uncover all material issues through a customary amount of due diligence, or that factors outside of our control will not later arise. As a result, we may be forced to later write-down or write-off assets, restructure our operations, or incur impairment or other charges that could result in losses. Even if our due diligence successfully identifies certain risks, unexpected risks may arise and previously known risks may materialize in a manner not consistent with our preliminary risk analysis. Even though these charges may be non-

10

Table of Contents

cash items and may not have an immediate impact on our liquidity, the fact that we report charges of this nature could lead to negative market perceptions about us or our securities. In addition, charges of this nature may cause us to be unable to obtain future financing on favorable terms or at all.

The unaudited pro forma condensed consolidated combined financial information included in this prospectus may not be indicative of what our actual financial position or results of operations would have been.

The unaudited pro forma condensed consolidated combined financial information for the Company following the Business Combination in this prospectus is presented for illustrative purposes only and is not necessarily indicative of what our actual financial position or results of operations would have been had the Business Combination been completed on the dates indicated. See “Unaudited Pro Forma Condensed Consolidated Combined Financial Information of the Company” in the financial statements included elsewhere in this prospectus (see “Index to Financial Statements”).

If the Business Combination’s benefits do not meet the expectations of investors, stockholders or financial analysts, the market price of our securities may decline.

If the benefits of the Business Combination do not meet the expectations of investors or securities analysts, the market price of our securities may decline. The market values of our securities may vary significantly from their prices on the date the Contribution Agreements were executed or the date of this prospectus.

In addition, fluctuations in the price of our securities could contribute to the loss of all or part of your investment. Prior to the Business Combination, trading in the shares of our Class A Common Stock had not been active. Accordingly, the valuation ascribed to Alta Mesa, Kingfisher and our Class A Common Stock in the Business Combination may not be indicative of the price that will prevail in the trading market following the Business Combination. If an active market for our securities develops and continues, the trading price of our securities could be volatile and subject to wide fluctuations in response to various factors, some of which are beyond our control. Any of the factors listed below could have a material adverse effect on your investment in our securities and our securities may trade at prices significantly below the price you paid for them. In such circumstances, the trading price of our securities may not recover and may experience a further decline.

Factors affecting the trading price of our securities may include:

| • | actual or anticipated fluctuations in our quarterly financial results or the quarterly financial results of companies perceived to be similar to us; |

| • | changes in the market’s expectations about our operating results; |

| • | success of our competitors; |

| • | our operating results failing to meet the expectation of securities analysts or investors in a particular period; |

| • | changes in financial estimates and recommendations by securities analysts concerning us or the market in general; |

| • | operating and stock price performance of other companies that investors deem comparable to us; |

| • | changes in laws and regulations affecting our business; |

| • | commencement of, or involvement in, litigation involving us; |

| • | changes in our capital structure, such as future issuances of securities or the incurrence of additional debt; |

| • | the volume of shares of our Class A Common Stock available for public sale; |

| • | any major change in our board or management; |

11

Table of Contents

| • | sales of substantial amounts of Class A Common Stock by our directors, executive officers or significant stockholders or the perception that such sales could occur; and |

| • | general economic and political conditions such as recessions, interest rates, fuel prices, international currency fluctuations and acts of war or terrorism. |

Broad market and industry factors may materially harm the market price of our securities irrespective of our operating performance. The stock market in general and NASDAQ have experienced price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of the particular companies affected. The trading prices and valuations of these stocks, and of our securities, may not be predictable. A loss of investor confidence in the market for retail stocks or the stocks of other companies which investors perceive to be similar to us could depress our stock price regardless of our business, prospects, financial conditions or results of operations. A decline in the market price of our securities also could adversely affect our ability to issue additional securities and our ability to obtain additional financing in the future.

If securities or industry analysts do not publish or cease publishing research or reports about us, our business, or our market, or if they change their recommendations regarding our securities adversely, the price and trading volume of our securities could decline.

The trading market for our securities will be influenced by the research and reports that industry or securities analysts may publish about us, our business, our market, or our competitors. Securities and industry analysts do not currently, and may never, publish research on us. If no securities or industry analysts commence coverage of us, our stock price and trading volume would likely be negatively impacted. If any of the analysts who may cover us change their recommendation regarding our securities adversely, or provide more favorable relative recommendations about our competitors, the price of our securities would likely decline. If any analyst who may cover us were to cease coverage of us or fail to regularly publish reports on us, we could lose visibility in the financial markets, which could cause our stock price or trading volume to decline.

There is no guarantee that the Public Warrants will be in the money at a time when they are exercisable, and they may expire worthless; the terms of our Public Warrants may be amended without the consent of all holders.

The exercise price for our Public Warrants is $11.50 per share. There is no guarantee that the Public Warrants will be in the money at a time when they are exercisable, and as such, the Public Warrants may expire worthless.

In addition, the warrant agreement between Continental Stock Transfer & Trust Company, as warrant agent, and us provides that the terms of the Public Warrants may be amended without the consent of any holder to cure any ambiguity or correct any defective provision, but requires the approval by the holders of at least 50% of the then outstanding Public Warrants to make any change that adversely affects the interests of the registered holders. Accordingly, we may amend the terms of the Public Warrants in a manner adverse to a holder if holders of at least 50% of the then outstanding Public Warrants approve of such amendment. Although our ability to amend the terms of the Public Warrants with the consent of at least 50% of the then outstanding Public Warrants is unlimited, examples of such amendments could be amendments to, among other things, increase the exercise price of the Public Warrants, shorten the exercise period or decrease the number of shares of our Class A Common Stock purchasable upon exercise of a Public Warrant.

We may redeem the Public Warrants prior to their exercise at a time that is disadvantageous to holders, thereby making their Public Warrants worthless.

We have the ability to redeem the outstanding Public Warrants at any time after they become exercisable and prior to their expiration at a price of $0.01 per warrant, provided that (i) the last reported sale price of our

12

Table of Contents

Class A Common Stock equals or exceeds $18.00 per share for any 20 trading days within the 30 trading-day period ending on the third business day before we send the notice of such redemption and (ii) on the date we give notice of redemption and during the entire period thereafter until the time the Public Warrants are redeemed, there is an effective registration statement under the Securities Act covering the shares of our Class A Common Stock issuable upon exercise of the Public Warrants and a current prospectus relating to them is available or we have elected to require the exercise of the Public Warrants on a cashless basis. Redemption of the outstanding Public Warrants could force holders of Public Warrants:

| • | to exercise their Public Warrants and pay the exercise price therefor at a time when it may be disadvantageous for them to do so; |

| • | to sell their Public Warrants at the then-current market price when they might otherwise wish to hold their Public Warrants; or |

| • | to accept the nominal redemption price which, at the time the outstanding Public Warrants are called for redemption, is likely to be substantially less than the market value of their Public Warrants. |

Anti-takeover provisions contained in our Charter and bylaws (the “Bylaws”), as well as provisions of Delaware law, could impair a takeover attempt.

Our Charter and Bylaws contain provisions that could have the effect of delaying or preventing changes in control or changes in our management without the consent of our board of directors. These provisions include:

| • | up to seven of our eleven directors may be appointed by the holders of the Series A Preferred Stock and Series B Preferred Stock without any vote of the holders of Class A Common Stock; |

| • | no cumulative voting in the election of directors, which limits the ability of minority stockholders to elect director candidates; |

| • | the exclusive right of our board of directors to elect a director to fill a vacancy created by the an increase in the number of directors to serve on our board of directors or the resignation, death, or removal of a director, which prevents stockholders from being able to fill vacancies on our board of directors; |

| • | the ability of our board of directors to determine whether to issue shares of our preferred stock and to determine the price and other terms of those shares, including preferences and voting rights, without stockholder approval, which could be used to significantly dilute the ownership of a hostile acquirer; |

| • | a prohibition on stockholder action by written consent, which forces stockholder action to be taken at an annual or special meeting of our stockholders; |

| • | the requirement that an annual meeting of stockholders may be called only by the chairman of the board of directors, the chief executive officer, or the board of directors, which may delay the ability of our stockholders to force consideration of a proposal or to take action, including the removal of directors; |

| • | limiting the liability of, and providing indemnification to, our directors and officers; |

| • | controlling the procedures for the conduct and scheduling of stockholder meetings; |

| • | providing that directors may be removed prior to the expiration of their terms by stockholders only for cause; and |

| • | advance notice procedures that stockholders must comply with in order to nominate candidates to our board of directors or to propose matters to be acted upon at a stockholders’ meeting, which may discourage or deter a potential acquirer from conducting a solicitation of proxies to elect the acquirer’s own slate of directors or otherwise attempting to obtain control of us. |

These provisions, alone or together, could delay hostile takeovers and changes in control of us or changes in our board of directors and management.

13

Table of Contents

As a Delaware corporation, we are also subject to provisions of Delaware law, including Section 203 of the Delaware General Corporation Law (the “DGCL”), which prevents some stockholders holding more than 15% of our outstanding voting common stock from engaging in certain business combinations without approval of the holders of substantially all of our outstanding voting common stock. Any provision of our Charter or Bylaws or Delaware law that has the effect of delaying or deterring a change in control could limit the opportunity for our stockholders to receive a premium for their securities and could also affect the price that some investors are willing to pay for our securities.

A significant portion of our total outstanding shares are restricted from immediate resale but may be sold into the market in the near future. This could cause the market price of our Class A Common Stock to drop significantly, even if our business is doing well.

Sales of a substantial number of shares of Class A Common Stock in the public market could occur at any time. These sales, or the perception in the market that the holders of a large number of shares intend to sell shares, could reduce the market price of our Class A Common Stock. The holders of our founder shares, which include our Sponsor and independent directors, and Fund VI Holdings own approximately 39% of our Class A Common Stock. Pursuant to the terms of a letter agreement entered into at the time of the IPO, the founder shares (which were converted into shares of Class A Common Stock at the Closing) may not be transferred until the earlier to occur of (i) one year after the Closing or (ii) the date on which we complete a liquidation, merger, stock exchange or other similar transaction that results in all of our public stockholders having the right to exchange their shares of Class A Common Stock for cash, securities or other property. Notwithstanding the foregoing, if the last sale price of our Class A Common Stock equals or exceeds $12.00 per share (as adjusted for stock splits, stock dividends, reorganizations, recapitalizations and other similar transactions) for any 20 trading days within any 30-trading day period commencing at least 150 days after the Closing, the shares of Class A Common Stock into which the founder shares convert will be released from these transfer restrictions.

Additionally, 90 days after Closing, the Kingfisher Contributor will have the ability to redeem or exchange up to 39,000,000 SRII Opco Common Units for shares of Class A Common Stock on a one-to-one basis. The Alta Mesa Contributor and the Riverstone Contributor will also have this redemption or exchange right with respect to all of their respective SRII Opco Common Units 180 days after Closing. If the Contributors redeem or exchange all of their SRII Opco Common Units for shares of Class A Common Stock, they will collectively own 55.8% of our Class A Common Stock.

In connection with the closing of our IPO, we entered into a registration rights agreement with our Sponsor and certain of our directors providing for registration rights to such parties. In addition, in connection with the Closing, we entered into a registration rights agreement with Fund VI Holdings and the Contributors, pursuant to which we are required to file the registration statement of which this prospectus is a part registering the shares of Class A Common Stock held by them for resale within 30 days following the Closing.

We will be required to make payments under the Tax Receivable Agreement for certain tax benefits we may claim, and the amounts of such payments could be significant.

In connection with the completion of the Business Combination, we entered into the Tax Receivable Agreement with the Alta Mesa Contributor and the Riverstone Contributor (the “Initial Limited Partners”) and SRII Opco. Pursuant to the Tax Receivable Agreement, we will be required to make cash payments to the Initial Limited Partners and their permitted transferees (together, the “TRA Holders”) equal to 85% of the amount of tax benefits, if any, that we actually realize (or are deemed to realize in certain circumstances) in periods after the Business Combination as a result of (i) certain tax basis increases resulting from the exchange of SRII Opco Common Units for Class A Common Stock (or, under certain circumstances, cash) pursuant to the redemption right or our right to effect a direct exchange of SRII Opco Common Units under the SRII Opco LPA, other than such tax basis increases allocable to assets held by Kingfisher or otherwise used in our Midstream Business, and

14

Table of Contents

(ii) interest paid or deemed to be paid by us as a result of, and additional tax basis arising from, any payments we make under the Tax Receivable Agreement. We will retain the benefit of the remaining 15% of these cash savings. The amount of the cash payments that we may be required to make under the Tax Receivable Agreement could be significant and is dependent upon significant future events and assumptions, including the timing of the exchanges of SRII Opco Common Units, the price of our Class A Common Stock at the time of each exchange, the extent to which such exchanges are taxable transactions and the amount of the exchanging TRA Holder’s tax basis in its SRII Opco Common Units at the time of the relevant exchange. The amount of such cash payments is also based on assumptions as to the amount and timing of taxable income we generate in the future, the U.S. federal income tax rate then applicable and the portion of our payments under the Tax Receivable Agreement that constitute interest or give rise to depreciable or amortizable tax basis. Moreover, payments under the Tax Receivable Agreement will be based on the tax reporting positions that we determine, which tax reporting positions are subject to challenge by taxing authorities. We will be dependent on distributions from SRII Opco to make payments under the Tax Receivable Agreement, and we cannot guarantee that such distributions will be made in sufficient amounts or at the times needed to enable us to make our required payments under the Tax Receivable Agreement, or at all. Any payments made by us to the TRA Holders under the Tax Receivable Agreement will generally reduce the amount of overall cash flow that might have otherwise been available to us. To the extent that we are unable to make timely payments under the Tax Receivable Agreement for any reason, the unpaid amounts will be deferred and will accrue interest until paid by us. Nonpayment for a specified period may constitute a breach of a material obligation under the Tax Receivable Agreement, and therefore, may accelerate payments due under the Tax Receivable Agreement. The payments under the Tax Receivable Agreement are also not conditioned upon the TRA Holders maintaining a continued ownership interest in SRII Opco or us. See “Certain Relationships and Related Party Transactions—Tax Receivable Agreement” for a discussion of the Tax Receivable Agreement and the related likely benefits to be realized by us and the TRA Holders.

We will not be reimbursed for any payments made to TRA Holders under the Tax Receivable Agreement in the event that any tax benefits are disallowed.

We will not be reimbursed for any cash payments previously made to the TRA Holders pursuant to the Tax Receivable Agreement if any tax benefits initially claimed by us are subsequently challenged by a taxing authority and are ultimately disallowed. Instead, any excess cash payments made by us to a TRA Holder will be netted against any future cash payments that we might otherwise be required to make under the terms of the Tax Receivable Agreement. However, a challenge to any tax benefits initially claimed by us may not arise for a number of years following the initial time of such payment or, even if challenged early, such excess cash payment may be greater than the amount of future cash payments that we might otherwise be required to make under the terms of the Tax Receivable Agreement and, as a result, there might not be future cash payments from which to net against. The applicable U.S. federal income tax rules are complex and factual in nature, and there can be no assurance that the Internal Revenue Service (the “IRS”) or a court will not disagree with our tax reporting positions. As a result, it is possible that we could make cash payments under the Tax Receivable Agreement that are substantially greater than our actual cash tax savings. See “Certain Relationships and Related Party Transactions — Tax Receivable Agreement” for a discussion of the Tax Receivable Agreement and the related likely benefits to be realized by us and the TRA Holders.

Certain of the TRA Holders have substantial control over us, and their interests, along with the interests of other TRA Holders, in our business may conflict with yours.

The TRA Holders may receive payments from us under the Tax Receivable Agreement upon any redemption or exchange of their SRII Opco Common Units, including the issuance of shares of our Class A Common Stock upon any such redemption or exchange. As a result, the interests of the TRA Holders may conflict with the interests of holders of our Class A Common Stock. For example, the TRA Holders may have different tax positions from us which could influence their decisions regarding whether and when to dispose of assets, whether and when to incur new or refinance existing indebtedness, especially in light of the existence of

15

Table of Contents

the Tax Receivable Agreement, and whether and when we should terminate the Tax Receivable Agreement and accelerate our obligations thereunder. In addition, the structuring of future transactions may take into consideration tax or other considerations of TRA Holders even in situations where no similar considerations are relevant to us. See “Certain Relationships and Related Party Transactions—Tax Receivable Agreement” for a discussion of the Tax Receivable Agreement and the related likely benefits to be realized by us and the TRA Holders.

In certain cases, payments under the Tax Receivable Agreement may be accelerated and/or significantly exceed the actual benefits, if any, we realize in respect of the tax attributes subject to the Tax Receivable Agreement.

The Tax Receivable Agreement provides that if we breach any of our material obligations under the Tax Receivable Agreement or if, at any time, we elect an early termination of the Tax Receivable Agreement, then the Tax Receivable Agreement will terminate and our obligations, or our successor’s obligations, to make payments under the Tax Receivable Agreement would accelerate and become immediately due and payable. The amount due and payable in those circumstances is determined based on certain assumptions, including an assumption that we would have sufficient taxable income to fully utilize all potential future tax benefits that are subject to the Tax Receivable Agreement. We may need to incur debt to finance payments under the Tax Receivable Agreement to the extent our cash resources are insufficient to meet our obligations under the Tax Receivable Agreement as a result of timing discrepancies or otherwise.

As a result of the foregoing, (i) we could be required to make cash payments to the TRA Holders that are greater than the specified percentage of the actual benefits we ultimately realize in respect of the tax benefits that are subject to the Tax Receivable Agreement, and (ii) we would be required to make a cash payment equal to the present value of the anticipated future tax benefits that are the subject of the Tax Receivable Agreement, which payment may be made significantly in advance of the actual realization, if any, of such future tax benefits. In these situations, our obligations under the Tax Receivable Agreement could have a substantial negative impact on our liquidity and could have the effect of delaying, deferring or preventing certain mergers, asset sales, other forms of business combination, or other changes of control due to the additional transaction costs a potential acquirer may attribute to satisfying such obligations. There can be no assurance that we will be able to finance our obligations under the Tax Receivable Agreement.

The recently passed comprehensive tax reform bill could adversely affect our business and financial condition.

On December 22, 2017, President Trump signed into law the final version of the tax reform bill that significantly reforms the Internal Revenue Code of 1986, as amended (the “Code”). The tax reform bill, among other things, contains significant changes to corporate taxation, including a permanent reduction of the corporate income tax rate, a partial limitation on the deductibility of business interest expense, a limitation of the deduction for net operating loss carryforwards to 80% of current year taxable income, an indefinite net operating loss carryforward, immediate deductions for certain new investments instead of deductions for depreciation expense over time, and the modification or repeal of many business deductions and credits. We continue to examine the impact this tax reform legislation may have on our business. Notwithstanding the reduction in the corporate income tax rate, the overall impact of the tax reform bill is uncertain and our business and financial condition could be adversely affected. The impact of this tax reform on holders of our Class A Common Stock is also uncertain and could be adverse.

The JOBS Act permits “emerging growth companies” like us to take advantage of certain exemptions from various reporting requirements applicable to other public companies that are not emerging growth companies.

We qualify as an “emerging growth company” as defined in the JOBS Act. As such, we take advantage of certain exemptions from various reporting requirements applicable to other public companies that are not emerging growth companies for as long as we continue to be an emerging growth company, including (i) the

16

Table of Contents

exemption from the auditor attestation requirements with respect to internal control over financial reporting under Section 404 of the Sarbanes-Oxley Act, (ii) the exemptions from say-on-pay, say-on-frequency and say-on-golden parachute voting requirements and (iii) reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements. As a result, our stockholders may not have access to certain information they deem important. We will remain an emerging growth company until the earliest of (i) the last day of the fiscal year (a) following March 29, 2022, the fifth anniversary of our IPO, (b) in which we have total annual gross revenue of at least $1.07 billion or (c) in which we are deemed to be a large accelerated filer, which means the market value of our Class A Common Stock that is held by non-affiliates exceeds $700 million as of the last business day of our prior second fiscal quarter, and (ii) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period.