Attached files

| file | filename |

|---|---|

| EX-32.2 - JAKROO INC. | ex32-2.htm |

| EX-32.1 - JAKROO INC. | ex32-1.htm |

| EX-31.2 - JAKROO INC. | ex31-2.htm |

| EX-31.1 - JAKROO INC. | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _____________ to _____________

Commission file number 333-217412

Jakroo Inc.

(Exact name of registrant as specified in its charter)

| Nevada | 81-1565811 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

5906 Stoneridge Mall Road Pleasanton, CA |

94588 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (800)485-7067

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Name of exchange on which registered | |

| None | n/a |

Securities registered pursuant to Section 12(g) of the Act: Common stock, par value $.001

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes [ ] No [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, a smaller reporting company or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | [ ] | Accelerated filer | [ ] | |

| Non-accelerated filer | [ ] | (Do not check if a smaller reporting company) | Smaller reporting company | [X] |

| Emerging growth company | [X] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

As of March 30, 2018, there were 31,288,650 shares of company common stock issued and outstanding.

Jakroo Inc.

Annual Report on Form 10-K

For the fiscal year ended December 31, 2017

TABLE OF CONTENTS

Unless we have indicated otherwise, or the context otherwise requires, references in this Report to the “Company,” “we,” “us” and “our” or similar terms refer to Jakroo Inc., a Nevada corporation.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report and the documents we have filed with the SEC that are incorporated by reference herein contain forward-looking statements, within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), that involve significant risks and uncertainties. Any statements contained, or incorporated by reference, in this Report that are not statements of historical fact may be forward-looking statements. When we use the words “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “will” and other similar terms and phrases, including references to assumptions, we are identifying forward-looking statements. Forward-looking statements involve risks and uncertainties which may cause our actual results, performance or achievements to be materially different from those expressed or implied by those forward-looking statements.

A variety of factors, some of which are outside our control, may cause our operating results to fluctuate significantly. They include:

| ● | our ability to establish our business model and generate revenue and profit; | |

| ● | our ability to expand our business model beyond engaging in activities on behalf of related parties; | |

| ● | our ability to manage or expand operations and to fill customers’ orders on time; | |

| ● | our ability to maintain adequate control of our expenses and internal accounting processes generally as we seek to grow; | |

| ● | our ability to establish or protect our intellectual property; | |

| ● | the impact of significant government regulation in China; | |

| ● | our ability to implement marketing and sales strategies and adapt and modify them as needed; and | |

| ● | our implementation of required financial, accounting and disclosure controls and procedures and related corporate governance policies. |

The foregoing does not represent an exhaustive list of risks that may impact upon the forward-looking statements used herein or in the documents incorporated by reference herein. Please see “Risk Factors” for additional risks which could adversely impact our business and financial performance and related forward-looking statements.

Moreover, new risks regularly emerge, and it is not possible for our management to predict all risks, nor can we assess the impact of all risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ from those contained in any forward-looking statements. All forward-looking statements included in this report are based on information available to us on the date hereof. Except to the extent required by applicable laws or rules, we undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained throughout this Report and the documents we have filed with the SEC.

We specialize in the design, manufacture and direct sale of customized technical endurance apparel for the cycling, triathlon, running and Nordic skiing markets across Asia, Europe and North America. Our made-to-order, just-in-time (known as JIT) manufacturing process and vertical integration of design, sales and distribution minimizes risk, provides autonomous control of quality across all stages of our vertically integrated supply chain and maximizes value to our customers.

In 1996, Weidong “Wayne” Du, our Chief Executive Officer conceived of the idea of manufacturing sublimated sportswear while working as an agent serving European customers for a Chinese trading company. Sublimation is a computerized printing process that uses heat to transfer dye onto the fabric. In 2003, Mr. Du founded Rider Sportsfashion Ltd in Beijing, China to handle original equipment manufacturing (or OEM) of sublimated cycling apparel. In 2006, the Jakroo® brand was launched and focused on the manufacture and sale of cycling apparel products within the domestic Chinese market.

In 2010, we shifted our strategy toward customization, at which time we formed Rider Sportsfashion LLC and began marketing our products in the U.S. through our home base in Pleasanton, California. In 2014, we established Jakroo Canada Inc., based in Vancouver, British Columbia, to oversee marketing, sales and distribution in the Canadian market. Soon thereafter, in 2015, we established Jakroo GmbH, based in Dornbirn, Austria, to manage marketing, sales and distribution in the European market. Within the U.S. and Canadian markets, the brand is considered to be among the top custom cycling wear brands along with Champion System, Hincapie, Voler, Pactimo and Louis Garneau. While the competitive landscape across Europe varies greatly by region, we consider brands such as Castelli, Bio Racer, Santini, Owayo and Cuore to be our primary competitors. The Jakroo® brand is among the top three selling cycling apparel brands on China’s largest e-commerce platforms, TMALL. Among cycling enthusiasts, Jakroo ranks among the most popular cycling apparel brands in the Chinese market alongside the likes of Santic, Sobike and CCN, all of which are Chinese domestic brands.

Our global business is currently comprised of three core business units: (1) inline retail, which consists of products produced and sold as part of a collection; (2) OEM contract manufacturing; and (3) custom retail. We will continue to maintain the current business ‘mix’ of business, although we expect our OEM business, which currently represents 8% of sales, to account for a lower percentage of our total business at some point in the foreseeable future. We expect inline retail to remain stable around 18% and custom retail is expected to expand slightly higher from its current 74% share.

We have two primary sales channels for our inline and custom retail businesses: (1) direct to consumer sales through our website, which represents 84% of total revenues and (2) wholesale, defined as sales to retail shops, promotional distributors and event organizers, which represents, 16% of total revenues for these two channels. Both channels are sold exclusively online through our e-commerce websites or, in the case of China, through large online retailers such as TMALL. Over 98% of our business from these channels is executed with payments made to us online in advance of production and shipment of goods.

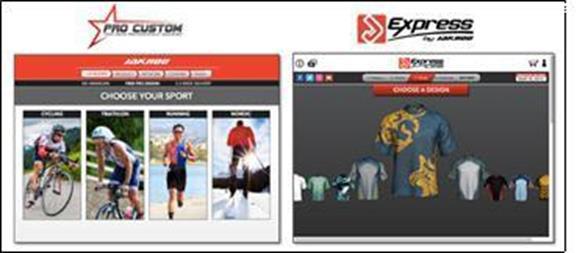

Our value proposition is based on fast delivery, no minimum purchase requirements and free design. We currently offer a two week turnaround time and offer customers two pathways for design: (1) Do it yourself (or DIY), through the exclusive Jakroo Express™ design application and; (2) Jakroo Pro Custom, a free professional design service offered through the Jakroo website. We believe that the combination of these novel offerings provides us with a distinct competitive advantage.

| 1 |

Market Overview & Opportunity

Overview

A 2014 survey by Paris based NPD Group estimated the cycling apparel market to be valued at $2.2 billion Euro (US$2.5 billion) in 2014 and estimates the broader active wear market will continue to experience growth and reach $178 billion by 2019.1

According to the Sports & Fitness Industry Association (SFIA), participation in running, cycling and hiking in 2015 reached 140 million people worldwide.2 Participation in cycling as a pastime in the U.S. was estimated at 67 million in 2014, as noted by the online statistics site, Statista.3 This indicates a large potential market for cycling gear. With the inclusion of running and triathlon, we expect to see continued growth in the endurance sports participation, particularly in the youth and women’s segments. According to USA Triathlon, female participation in triathlons has grown from 27% of all participants in 2000 to more than 37% in 2014.

In China, the concept of cycling as a component of a healthy lifestyle has increased as a growing middle class has begun participating in cycling for recreation. In 2014, Ji Cheng, nicknamed the “breakaway killer” for his skill in controlling the speed of the peloton (i.e., the main group of riders in a cycling road race), was the first Chinese cyclist in the history of the Tour de France.

A recent survey entitled “Millennial Consumer Trends” by Elite Daily of more than 1,300 millennials (those born between 1980-1996) reports that more than 42% of those surveyed are deeply interested in helping companies develop future products and services, and 62% of millennials say that if a brand engages with them on social networks, they are more likely to become a loyal customer.4

We believe that these trends, coupled with the rapidly growing direct-to-consumer e-commerce and product personalization markets, will create significant opportunities for companies like Jakroo that are equipped with the information and manufacturing architecture to support the new era of “social” commerce.

Customization is the Future

While gathering data to quantify the potential market size for a new product or service can be challenging, a 2013 report by Forbes magazine cites a Bain survey of more than 1,000 online shoppers among whom, although only 10% had tried online customization options, 25-30% expressed interest in doing so. While it is difficult to quantify the potential of customization, if 25% of sales from the $2.5 billion cycling apparel market were customized, that would equate to $625 million per year.5

Customization will also create distinct advantages for companies to differentiate their products from their competitors at a time when the Internet is making it easier for customers to easily compare prices and products with standard features or options.

Within the wholesale markets, the ability to extend customization to a re-seller can provide a competitive advantage through the offering of novel versions of a company’s products, thus allowing the retailer to minimize high capital investments in inventory and avoid deep discounting which can arise as a result of overstocking on a particular item or from price wars among competitors of similar products.

1 “2014 Global Cycling Market Valued at € 35.7 Billion,” Bike Europe, 8 Dec 2015, http://www.bike-eu.com/sales-trends/nieuws/2015/12/2014-global-cycling-market-valued-at-e-35-7-billion-10125262.

2 SFIA survey.

3 “Number of Cyclists/Bike Riders Report,” Statista 2016. http://www.statista.com/statistics/227415/number-of-cyclists-and-bike-riders-usa/

4 “Millennial Consumer Trends,” Elite Daily Survey 2015.

5 “Having It Their Way: The Big Opportunity in Personalized Products,” Forbes, Nov. 5, 2013.

| 2 |

Developments in the fields of 3D fashion design, DIY design applications and apparel centric wearables will expedite the acceptance and growth of personalization, creating new value and new market opportunities. Personalization now extends beyond ascetic design and is quickly becoming an integral part of the customers sizing and fit options during purchase. We anticipate that existing companies that fail to reengineer their offerings will suffer either a significant competitive disadvantage or be forced to exit the market altogether. We believe that our highly customized information architecture, vertical integration and JIT manufacturing infrastructure will position Jakroo to assume a leadership position within our target markets.

The Evolution of E-commerce

According to a report by Statista, the number of online shoppers in the U.S. is projected to reach 230 million by 2021. This represents a 20% increase from the 191 million recorded in 2013.6 Net sales for Amazon alone reached $177 billion for the 2017. E-commerce sales in China are projected to exceed $400 billion by the end of 2016. Market research firm eMarketer projects e-commerce sales will eclipse $3.5 trillion within the next five years. The web is projected to account for 7.3% of global retail sales this year and grow to 12.4% by 2019, according to eMarketer.7 As more than 95% of our sales are derived through e-commerce, we will continue to invest heavily in digital advertising to direct online shoppers to our customized design center and online shops. This investment includes upgrading our existing e-commerce architecture and adding new features to improve the overall user experience and enhance brand loyalty.

Companies such as Facebook and Twitter are making significant investments in social commerce as community and social engagement play a larger role in consumer purchasing decisions. Additionally, the gap between search and purchase domains is quickly fading. In a 2015 Surveta survey of 2,000 consumers, 44% of respondents stated they go direct to Amazon to start their product searches compared to 34% who start on a Search engine such as Google, Bing or Yahoo.8 Jakroo’s business is poised to leverage this trend through its direct to consumer sales channel across the Jakroo group of e-commerce shopping sites as well as its sales through sites such as TMALL. In fact, since 2016, we have been leveraging these trends through investing in digital advertising on the Facebook platform. In 2018, we will begin selling our inline retail products on the Amazon platform in an effort to expand revenues and build brand awareness. While the immediate benefit will from using the Amazon platform will be the revenues earned from those sales, we expect to achieve additional benefits as this provides us with an additional means through of introducing customers to our custom order business through interaction with us and ongoing marketing campaigns.

Competitive Strengths

We believe that the following key competitive strengths differentiate us from our competitors and are critical to our continuing success:

Lean Manufacturing & Vertical Integration

We own and operate all facets of our design, manufacturing and sales process. This vertical integration allows us complete control over our quality assurance of products and services, user experience and brand. Unlike many of our competitors who rely on contract manufacturing, direct ownership of the manufacturing facility allows us to tightly control production timelines, quality control and delivery.

6 “Number of digital shoppers in the United States from 2016 to 2021,” Statista. 2016.

https://www.statista.com/statistics/183755/number-of-us-internet-shoppers-since-2009/

7 “Global e-commerce sales set to grow 25% in 2015” Matt Lindner, Internet Retailer July 2015.

https://www.internetretailer.com/2015/07/29/global-e-commerce-set-grow-25-2015

8 “Amazon Commands Nearly Half Of Consumers' First Product Search, BloomReach Study Finds”. 2015. Forbes“ http://www.forbes.com/sites/fionabriggs/2015/10/06/amazon-commands-nearly-half-of-consumers-first-product-search-bloomreach-study-finds/#a3ef0627b779

| 3 |

Our production facility, which had been located in the Tongzhou District of Beijing and was recently relocated to a newly built facility on the border of Beijing and Hebei Province, has been producing technical endurance apparel for more than 13 years. This extensive experience has allowed us to develop specially engineered processes that have been optimized to produce and deliver a high capacity of small quantity orders ranging from 1 piece to 25 pieces, on average, within 14 days, which is a substantially quicker turnaround than our competitors based on delivery times posted on their websites.

In 2017, 80% of our production lot quantities were less than 9 pieces. Moreover, 66% of our production lot quantities were less than 5 pieces. Additionally, 88% of orders were delivered to customers in less than three weeks and 31% were delivered to customers in less than two weeks.

While consistently delivering the value proposition of either short delivery times or low minimum orders can pose logistical challenges, Jakroo has mastered both through developing a specialized work process and complex manufacturing system. More importantly, Jakroo has developed the ability to scale those processes without degradation of quality or compromising timelines. We believe this combination is novel to Jakroo in the technical endurance sports apparel industry and allows us a significant competitive advantage.

Integrated Information Systems

Our core information system is built on a robust, cloud-based consolidated financial platform and ecommerce module. This allows us to easily deploy and manage localized subsidiary companies and e-commerce platforms across our online properties while effectively addressing local tax compliance requirements, language and currency. We’ve made significant investments in customization of the platform to meet our particular requirements and create a compelling proprietary service for our customers.

We’ve developed a proprietary, comprehensive design architecture using 3D modeling and, in partnership with external vendors, developed Express by Jakroo, the industry’s most advanced self-design platform that provides a rich user experience for the customer and utilizes back-end efficiencies by our production team.

In the spring of 2016, we implemented our make-to-order production module in order to further streamline the item configuration process and achieve greater efficiencies with raw material asset management, production scheduling and cost accounting.

With this system in place, we are able to capture and track all customer activity from the initial inbound lead through to product design and the final delivery of purchased products. This end-to-end visibility allows us to quickly troubleshoot activity and scale our business.

Global presence

The current competitive landscape within the endurance sports apparel market varies significantly based on region. Many of the incumbent brands in the U.S. have minimal or no presence in the primary European or Asian markets. On the other hand, a handful of European brands have, through years of investment, gained market awareness across North America and Asia. Very few Chinese domestic brands, however, have any reasonable brand awareness in either Europe or North America. We are working to change that.

| 4 |

In addition to our operating headquarters in Pleasanton, California, we have fully functional operating subsidiaries in Beijing, China, Vancouver, British Columbia and Dornbirn, Austria that provide sales, marketing and customer service support to our regional markets. This allows us to provide superior localized support to our regional customers while building brand loyalty therein.

With our current established presence in each of the core markets and our proven business model, we believe we are positioned to take a leadership position in the endurance sports apparel market. Our plan is to continue to establish and grow subsidiary offices and joint venture operations in key regions around the globe as part of our commitment to building trust, premium customer service and brand loyalty.

Significant Design & Shopping Experience

With the use of proprietary and highly customized customer relationship management and design applications, we are able to offer our customers two options for their design experience. Our proprietary Express by Jakroo DIY application was built to specification using state of the art technology and proprietary know-how to allow customers to design on a 99% true to size 3D model and easily purchase anytime. Unlike similar services offered by our competitors, which provide conceptual mock ups and require significant back-end interaction with designers and sales persons to process the order, designs created using Express by Jakroo are transferred directly to the production floor with minimal human interaction and enter the production process upon the customer’s placement of the order.

Customers who elect to use our Pro Custom service will enjoy the benefits of having a trained professional designer create their design according to specification. The customer is able to participate in the design editing process through an interactive online review/approval system. Unlike many of our competitors, who typically charge a design set-up fee and require several days to prepare the artwork, we offer this service free of charge and provide the designs within 48 hours of design request.

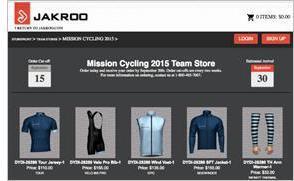

Since 2013, we have created more than 150,000 unique products and published more than 11,000 online custom storefronts on the Jakroo e-commerce platform. These semi-private webpages, hosting the customer’s customized products, allow the customer to order at their convenience 24/7 and share their store with friends, family and team members. We believe we are presently on track to create an additional 4,000 customer storefronts in 2018. Our custom e-commerce platform has been engineered to facilitate the particular requirements of each customer, including flexible ordering dates, order windows, individual shipping and sharing of stores and products.

| 5 |

Through our online account center, customers can review pending design approvals, track the status of all of their designs as they progress through the design process, as well as submit new design requests.

Based on more than 5,400 individual customer reviews which we solicited through direct feedback requests since 2013, over 92% of respondents rated their overall experience with Jakroo as positive and more than 96% of respondents indicated they were either very satisfied or “blown away” by the quality of our products.

By addressing the ongoing challenges faced by our traditional retailing competitors with forecasting and carrying inventory, we provide a competitive offering by maintaining a full service ‘hands-free’ custom online storefront option. This allows retailers who use our system to offer a broad selection of highly customizable products to their customers without having to purchase or carry the inventory in advance. Orders are made-to-order and shipped directly to the customer from our production facility in Beijing. The combination of made-to-order, JIT and custom commerce provides retailers the ability to better differentiate their offerings in a highly competitive marketplace.

Our Growth Strategy

Customer Acquisition

We acquire the majority of our direct customers online through Search Engine Marketing (SEM) and display marketing campaigns on Google, Bing and social websites such as Facebook and Twitter. In China, comprehensive platforms such as WeChat, QQ and Weibo play an important role in our customer acquisition, engagement and social commerce strategies. We will continue to invest in advertising and marketing to strengthen brand awareness in key markets.

Globally, sponsorship of organized race events and charity rides also plays a key role for customer acquisition, along with sponsorship of influential cycling teams and athletes to establish brand credibility. We currently sponsor several large profile Gran Fondo cycling events and Triathlon events across Canada, California and Austria. During 2013 and 2014, we sponsored the UCI Tour of Beijing and Tour of Hainan, both of these were high profile cycling events in China with international athlete participation and media exposure. Sponsorships for 2016 include the Trans Vorarlberg Triathlon in Bregenz, Austria, the Oakland Gran Fondo in Oakland California, and the EPIC Tour, Canada’s largest Fondo event with over 3000 participants. As of January 2017, we have been the exclusive race apparel sponsor of the UnitedHeathcare Pro Cycling Team, a U.S. based pro-continental team with global recognition among the competitive cycling community.

Vertical and Lateral Expansion

In the near-term, we will continue our focus on the endurance sports apparel market. We define this market as products used for cycling, triathlon, running and Nordic skiing. We aim to strengthen our brand and gain share within these core markets through: (1) investing in new product development and technologies geared toward improving the customer experience and reducing delivery times; (2) expanding geographically through establishing subsidiary companies and/or partnerships in key regions across the globe; and (3) making deeper investments in marketing partnerships and advertising.

| 6 |

We have experienced profitable operational growth since 2011 and we plan to continue our international expansion across Europe and the Asia-Pacific regions. Additional opportunities for growth will focus on lateral expansion into related product or sport categories that can benefit from customization. Examples of such categories include high school and collegiate level volleyball, soccer and wrestling teams.

In 2017, 89% of Jakroo’s sales within the North American and European markets came from the Cycling product category, 6% from Triathlon and the remainder were shared between Running and Nordic. 78% of total revenues were generated through our direct-to-consumer channel and 22% through resellers. In 2016, 87% of Jakroo’s sales within the North American market came from the Cycling product category, 6% from Triathlon and the remainder were shared between Running and Nordic. We’ve acquired more than 40,000 paying customers since 2013 and have acquired more than 9,000 new customers each year during 2016 and 2017. We will continue to invest in technologies aimed at improving the end-user customer experience and monetizing new leads through expediting the design-to-sale process.

Currently, approximately 78% of total domestic revenues in China come from our Inline retail product collection while the remaining 22% arise from the Custom product category. We plan to continue to drive growth within the custom product channel through investments in marketing and front-end systems. We will transition our make-to-stock production into micro-production lots (quantities of less than 50 pieces) to improve inventory turnover and net margins.

Our Wholesale channel, defined as retail shops and promotional goods distributors, represents 22% of total revenues across North America. For the period from January 2016 to December 2017, we had more than 650 paying customers with the median order value of $1,300 and average order value of $3,700. We will continue to invest in service offerings and technology platforms that provide competitive advantages for retailers.

We expect to launch a new state of the art Design and E-commerce center in the third quarter of 2018 which will employ some of the latest technologies emerging from the 3D parametric design and machine learning fields.

Increased Margins and Return on Invested Capital

Our made-to-order, JIT business model mitigates the need to carry inventory, thus freeing up capital to be used for investments in future expansion. Customers pay for goods in advance of production, which allows receivables to be as low as 0.1% of total revenue. North America continues to be our fastest growing market as we continue to establish the Jakroo brand across the East Coast. Looking forward, however, we expect our newly founded European operations to generate a significant portion of global sales over the next three years.

| 7 |

Revenues and profitability were impacted in 2015 as a result of one-time costs associated with auditing, corporate restructuring, investments in information technology infrastructure and the establishment of our European operations. Losses in 2017 were the result of one-time costs associated with the relocation and purchase of our new office in Pleasanton, California and amortization costs related to our stock-based compensation plan.

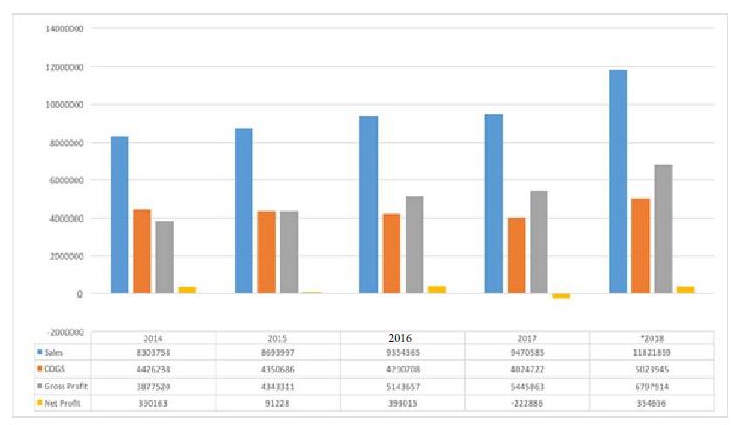

With continually improved design applications and deployment of our advanced Production Module, we expect to be able to reduce raw material waste and increase front-end efficiencies associated with customer service resulting in greater operating margins. Readers should note that audited results are shown for 2014, 2015, 2016 and 2017, and the values for 2018 are projections (see “Cautionary Note on Forward-Looking Statements”).

Overview of Our Company

Our Core Values

Our respect for our employees and community, and our emphasis on continuous improvement and social responsibility, are all borne from our core values of community, teamwork, integrity and innovation. We believe our employees are our greatest asset to help us build lasting value for all of Jakroo’s stockholders, including our customers.

Compliance and Sustainability

We maintain an ongoing commitment to the environment and our products are OEKO-TEX® certified. OEKO-TEX® Standard 100 is an independent test and certification system for all types of textiles tested for harmful substances – from threads and fabrics to the ready-to-use items that are available for purchase in stores.

In our commitment to ensuring safe and healthy working conditions for our employees and community at large, our production facility in China was fully audited and certified by a globally recognized environmental compliance auditor in September of 2015 through the Business Social Compliance Initiative (BSCI) that audits and certifies working conditions and environmental performance in a company’s global supply chains. Proposition 65 compliance is ongoing for the materials and fabrics used in products sold in California.

Experienced Management Team

The senior management team at Jakroo and its subsidiaries is comprised of individuals with extensive backgrounds in the sports apparel and manufacturing industries. Our senior operations team also has extensive experience in brand management and market development within the sports apparel industry. Jakroo’s management team is described in more detail beginning on page 54 in the Management section below.

| 8 |

Employees

As of the date of this report, we employed approximately 182 employees as follows:

| ● | Rider Sportsfashion LLC: 17 full time employees, 1 part-time employee, 2 independent contractors | |

| ● | Jakroo Canada Inc.: 5 full time employees | |

| ● | Jakroo GmbH: 2 full-time employees | |

| ● | Rider Sportsfashion Ltd: 28 full-time employees | |

| ● | Rider Sportsfashion (Langfang) Ltd: 130 full-time employees |

We consider our relationships with our employees to be good. None of our employees is covered by collective bargaining agreements.

Proprietary Rights

Each of the “J” logo and “Jakroo” mark has been registered as a service mark or trademark within the United States Patent and Trademark Office. In addition, we have obtained trademarks in Benelux, Canada, Mainland China, Denmark, Finland, Hong Kong, Taiwan, Malaysia, France, Thailand, Japan, Germany, Korea, Norway, Sweden, Spain, Switzerland and the United Kingdom. Additional registrations of our trademarks in secondary product categories have been registered or are in process of being registered within the respective Trademark offices in the primary countries in which we do business.

| 9 |

RISK FACTORS

An investment in our common stock is highly speculative and involves a high degree of risk. You should carefully consider the following risk factors in evaluating our business before investing. No purchase of our common stock should be made by any person who is not in a position to lose the entire amount of his or her investment. The order of the following risk factors is presented arbitrarily. You should not conclude the significance of a risk factor based on the order of presentation. Our business and operations could be seriously harmed as a result of any of these risks.

Risks Related to Our Business

We are an early stage company with a limited operating history as a manufacturer and seller of sporting apparel products. Our limited operating history may not provide an adequate basis to judge our future prospects and results of operations.

We have a limited operating history. Our first operating subsidiary, Rider Sports Fashion Limited (“Rider Beijing”) was established in Beijing in March 2003 to engage in cycling apparel development, production and sales. In 2007, we established our manufacturing subsidiary, which currently manufactures all of our products. As part of our international expansion and in response to international customer demands, we established our U.S. subsidiary in 2008 and our subsidiaries in Canada and Austria in 2014 and 2015, respectively. Despite our continuous growth, we have limited experience and operating history in the sporting apparel industry. Our limited history may not provide a meaningful basis for investors to evaluate our business, financial performance and prospects.

Any disruption of our supply chain could have an adverse impact on our net sales and profitability.

We rely on third party suppliers for fabrics, accessories and printing paper and machines that are essential to our product manufacturing. We cannot predict when, or the extent to which, we will experience a disruption in our supply chain. Any such disruption could negatively impact our ability to market and sell our products and serve our customers, which could adversely impact our net sales and profitability.

Based on our past business practice, we place purchase orders or enter into short term agreements with our raw material suppliers. Without long term supply agreements, any of our current suppliers may discontinue selling to us at any time. Changes in the commercial practices or financial condition of any of our key suppliers could also negatively impact our results. If we lose one or more key suppliers and are unable to promptly find alternative suppliers who are willing and able to provide equally appealing raw materials or manufacturing machines at comparable prices, we may not be able to deliver quality products that satisfy the requirements of our customers.

We also are subject to risks, such as the price and availability of raw materials and fabrics, labor disputes, union organizing activity, strikes, inclement weather, natural disasters, war and terrorism and adverse general, economic and political conditions that might limit our suppliers’ ability to provide us with quality merchandise on a timely and cost-efficient basis. We may not be able to develop relationships with new suppliers, and materials from alternative sources, if any, may be of a lesser quality and more expensive than those we currently purchase. Any delay or failure in offering products to our customers could have a material adverse impact on our net sales and profitability.

Our operating results can be adversely affected by changes in the cost or availability of raw materials.

Pricing and availability of raw materials for use in our businesses can be volatile due to numerous factors beyond our control, including general, domestic and international economic conditions, labor costs, production levels, competition, consumer demand, import duties and tariffs and currency exchange rates. This volatility can significantly affect the availability and cost of raw materials for us, and may therefore have a material adverse effect on our business, results of operations and financial condition.

| 10 |

During periods of rising prices of raw materials, there can be no assurance that we will be able to pass any portion of such increases on to customers. Conversely, when raw material prices decline, customer demands for lower prices could result in lower sales prices and, to the extent we have existing inventory, lower margins. We currently do not hedge against our exposure to changing raw material prices. As a result, fluctuations in raw material prices could have a material adverse effect on our business, results of operations and financial condition.

Supply shortages or changes in availability for any particular type of raw material can delay production or cause increases in the cost of manufacturing our products. We may be negatively affected by changes in availability and pricing of raw materials, which could negatively impact our results of operations.

Our sales may fluctuate and historical sales revenue may not be a meaningful indicator of future performance.

Our product sales may vary from quarter to quarter and year to year, and an unanticipated decline in net sales may cause the price of our common stock to fluctuate significantly. A number of factors have historically affected, and will continue to affect, our sales revenue, including:

| ● | consumer preferences, buying trends and overall economic trends; | |

| ● | our ability to identify and respond effectively to local and regional trends and customer preferences; | |

| ● | our ability to provide quality customer service that will increase our conversion of shoppers into paying customers; | |

| ● | competition in any of the regional markets we operate; | |

| ● | changes in our product mix; and | |

| ● | changes in pricing. |

Our online retail custom order and inline retail segments are affected by general economic conditions in our markets and ongoing economic and financial uncertainties may cause a decline in consumer spending that may adversely affect our business, operations, liquidity, financial results and stock price.

Our custom order and internet retail segments are the core of our business, contributing to more than 92% of our sales revenue in fiscal year 2017. Both segments are retail-based and depend on consumer discretionary spending. As a result, we may be adversely affected if our customers reduce, delay or forego their purchases of our products as a result of continued job losses, bankruptcies, higher consumer debt and interest rates, higher energy and fuel costs, reduced access to credit, falling home prices, lower consumer confidence, uncertainty or changes in tax policies and tax rates and uncertainty due to national or international security concerns. Decreases in sales or online customer traffic will negatively affect our financial performance, and a prolonged period of depressed consumer spending could have a material adverse effect on our business. Promotional activities and decreased demand for consumer products could affect profitability and margins. In addition, adverse economic conditions may result in an increase in our operating expenses due to, among other things, higher costs of labor, energy, equipment and facilities. Any of the foregoing factors could have a material adverse effect on our business, results of operations and financial condition and could adversely affect our stock price.

Our results of operations could be materially harmed if we are unable to accurately forecast demand for our products.

We often place orders for raw materials with our suppliers before our customers’ orders are firm. Therefore, if we fail to accurately forecast customer demand, we may experience excess inventory levels or a shortage of product to deliver to our customers. Factors that could affect our ability to accurately forecast demand for our products include:

| ● | an increase or decrease in consumer demand for our products or for products of our competitors; |

| 11 |

| ● | our failure to accurately predict customer acceptance of new products; | |

| ● | new product introductions by competitors; | |

| ● | unanticipated changes in general market conditions or other factors, which may result in cancellations of orders or a reduction or increase in the rate of reorders placed by retailers; | |

| ● | weak economic conditions or consumer confidence, which could reduce demand for discretionary items such as our products; and | |

| ● | terrorism or acts of war, or the threat of terrorism or acts of war, which could adversely affect consumer confidence and spending or interrupt production and distribution of product and raw materials. |

Inventory levels in excess of customer demand may result in inventory write-downs and the sale of excess inventory at discounted prices, which could have an adverse effect on our business, results of operations, and financial condition. On the other hand, if we underestimate demand for our products, our manufacturing facilities may not be able to produce products to meet customer requirements, and this could result in delays in the shipment of products and lost revenues, as well as damage to our reputation and customer relationships. There can be no assurance that we will be able to successfully manage inventory levels to exactly meet future order and reorder requirements.

Expanding our brand into new territories may be difficult and expensive, and if we are unable to successfully expand into these territories as expected, our brand may be adversely affected, and we may not achieve our planned sales growth.

Our growth strategy includes continuous expansion of our brand into new territories in North America, Europe and Asia. Products that we introduce into these new markets may not be successful with the consumers we target. Our brand may also fall out of favor with our current customer base as we expand our products into new markets. In addition, if we are unable to anticipate, identify or react appropriately to evolving consumer preferences, our sporting apparel sales may not grow as fast as we plan or may decline and our brand image may suffer.

Achieving market acceptance for new products will likely require us to exert substantial product development and marketing efforts, which could result in a material increase in selling, general and administrative expenses, both in absolute dollars and as a percentage of revenue. There can be no assurance that we will have the resources necessary to undertake these efforts or that these efforts will sufficiently increase our sporting apparel sales. Material increases in our selling and general and administrative expenses could adversely impact our results of operations.

Changes in the retail industry and markets for consumer products affecting our customers or retail practices could negatively impact existing customer relationships and our results of operations.

While the majority of our products are sold directly to consumers, a portion of our products are sold to resellers and distribution agents. A significant deterioration in the financial condition of these wholesale customers could have a material adverse effect on our sales and profitability. As a result, we periodically monitor and evaluate the credit status of these wholesale customers and attempt to adjust sales terms as appropriate. Despite these efforts, a bankruptcy filing by a key customer could have a material adverse effect on our business, results of operations, and financial condition. We do not monitor the credit status of our retail customers or direct customer database.

Failure to maintain our reputation and brand image could negatively impact our business.

Our brand has received a certain level of recognition in China, North America and Europe. Our success depends on our ability to maintain and enhance our brand image and reputation. We could be adversely affected if our brand is tarnished or receives negative publicity. In addition, adverse publicity about regulatory or legal action against us could damage our reputation and brand image, undermine consumer confidence in us, and reduce long-term demand for our products, even if the regulatory or legal action is unfounded or not material to our operations.

| 12 |

In addition, our success in maintaining, extending and expanding our brand image depends on our ability to adapt to a rapidly changing media and internet environment, including our reliance on online advertising. Negative posts or comments about us on social networking websites could seriously damage our reputation and brand image. If we do not maintain, extend and expand our brand image, our product sales, financial condition or results of operations could be materially and adversely affected.

Our core information technology platform is operated by a third party and any failure in maintenance or security of this platform could have adverse consequences on our business.

Our core information technology platform runs on Oracle’s NetSuite ERP platform. This includes, all customer management (CRM), manufacturing and resource planning (ERP) and e-commerce processes. All application data, and servers and functionality are outside of our direct ownership and control. As a global service provider, Oracle is fully responsible for the maintenance and security of their platform. Additionally, all related customer payment processing is managed by PCI compliant third party processors and payment gateways such as Merchante Solutions, Cybersource, Altapay and Alipay. As such, we do not store any customer data on our computer systems. Should any of those systems become compromised, our business would be adversely affected until remedied.

Failure to adequately protect or enforce our intellectual property rights could adversely affect our business.

We utilize trademarks on nearly all of our products and believe that having distinctive marks that are readily identifiable is an important factor in creating a market for our goods, in identifying us and in distinguishing our goods from the goods of others. We consider our “Jakroo®” series trademarks to be among our most valuable assets, and we have registered these trademarks in 19 countries and jurisdictions.

We believe that our trademarks, copyrights and other intellectual property rights are important to our brand, our success and our competitive position. In the future, we may encounter counterfeit reproductions of our products or that otherwise infringe on our intellectual property rights. If we are unsuccessful in challenging a party’s products on the basis of trademark or other intellectual property infringement, continued sales of these products could adversely affect our sales and our brand and result in the shift of consumer preference away from our products.

The actions we take to establish and protect trademarks and other intellectual property rights may not be adequate to prevent imitation of our products by others or to prevent others from seeking to block sales of our products as violations of proprietary rights.

In addition, the laws of certain foreign countries may not protect or allow enforcement of intellectual property rights to the same extent as the laws of the United States. We may face significant expenses and liabilities in connection with the protection of our intellectual property rights outside the United States, and if we are unable to successfully protect our rights or resolve intellectual property conflicts with others, our business or financial condition may be adversely affected.

Third parties may claim that we are infringing their intellectual property rights, and these claims may be costly to defend, may require us to pay licensing fees, damages, or other amounts, and may prevent, or otherwise impose limitations on the manufacture, distribution or sale of our products.

From time to time, third parties may claim that we are infringing on their intellectual property rights, and we may be found to infringe those intellectual property rights. While we do not believe that any of our products infringe the valid intellectual property rights of third parties, we may be unaware of the intellectual property rights of others that may cover some of our current or planned new products. If we are forced to defend against third party claims, whether or not the claims are resolved in our favor, we could encounter expensive and time consuming litigation which could divert our management and key personnel from business operations. If we are found to be infringing on the intellectual property rights of others, we may be required to pay damages or ongoing royalty payments, or comply with other unfavorable terms. Additionally, if we are found to be infringing on the intellectual property rights of others, we may not be able to obtain license agreements on terms acceptable to us, and this may prevent us from manufacturing, marketing or selling our products. Thus, these third party claims may significantly reduce the sales of our products or increase our cost of goods sold. Any reductions in sales or cost increases could be significant, and could have a material and adverse effect on our business.

| 13 |

Our products are used for inherently risky sports activities and could give rise to product liability or product warranty claims and other loss contingencies, which could affect our earnings and financial condition.

Many of our products are used in applications and situations that involve certain levels of risk of personal injury. As a result, we may be exposed to product liability claims by the nature of the products we produce. Exposure occurs if one of our products is alleged to have resulted in bodily injury or other adverse effects. Any such product liability claim may include allegations of defects in manufacturing, defects in design, a failure to warn of dangers inherent in the product or activities associated with the product, negligence, strict liability, and a breach of warranties. Although we maintain product liability insurance in amounts that we believe are reasonable, there can be no assurance that we will be able to maintain such insurance on acceptable terms, if at all, in the future or that product liability claims will not exceed the amount of insurance coverage. Additionally, we do not maintain product recall insurance. As a result, product recalls or product liability claims could have a material adverse effect on our business, results of operations and financial condition.

As a manufacturer and distributor of consumer products, we are subject to the Consumer Products Safety Act, which empowers the Consumer Products Safety Commission to exclude from the market products that are found to be unsafe or hazardous. Under certain circumstances, the Consumer Products Safety Commission could require us to repurchase or recall one or more of our products. Additionally, laws regulating certain consumer products exist in some cities and states, as well as in other countries in which we sell our products, and more restrictive laws and regulations may be adopted in any of these jurisdictions in the future. Any repurchase or recall of our products could be costly to us and could damage our reputation. If we were required to remove, or we voluntarily removed, our products from the market, our reputation could be tarnished and we might have large quantities of finished products that we could not sell.

We spend substantial resources ensuring compliance with governmental and other applicable standards. However, compliance with these standards does not necessarily prevent individual or class action lawsuits, which can entail significant cost and risk. We do not maintain insurance against many types of claims involving alleged defects in our products that do not involve personal injury or property damage. As a result, these types of claims could have a material adverse effect on our business, results of operations and financial condition.

Our success is dependent on retaining key personnel who would be difficult to replace.

Our success depends largely on the continued services of our key management members. In particular, our success depends on the continued efforts of Mr. Weidong Du, our Chief Executive Officer, President and Director, and Ms. Wei Tan, our Chief Financial Officer and Treasurer, who is also the wife of Mr. Du. Mr. Du and Ms. Tan have been instrumental in developing our business model and are crucial to our business development. There can be no assurance that Mr. Du and Ms. Tan will continue in their present capacities for any particular period of time. The loss of the services of Mr. Du and Ms. Tan could materially and adversely affect our business development. Derek Wiseman, our Chief Operating Officer, also plays a significant role in our business operations, particularly expansion of our customer base in North America and Europe. In addition, we rely on officers and directors of our operating subsidiaries such as Mr. Guichun Liu, Ms. Wen Li, and Mr. Hao Wang, for key aspects of our operations, including sales, product design, manufacturing and quality control. The loss of these key employees would negatively affect our ability to manufacture quality sporting apparel, maintain existing customers, capture new market share and generate sales revenue.

The legal requirements associated with being a public company, including those contained in and issued under the Sarbanes-Oxley Act, may make it difficult for us to retain or attract qualified officers and directors, which could adversely affect the management of our business and our ability to obtain listing of our common stock.

We may be unable to attract and retain qualified officers and directors necessary to provide for our effective management because of the rules and regulations that govern publicly listed companies, including, but not limited to, certifications by principal executive officers. Currently, our officers do not have extensive experience in operating a U.S. public company. Moreover, the actual and perceived personal risks associated with compliance with the Sarbanes-Oxley Act and other public company requirements may deter qualified individuals from accepting roles as directors and executive officers. At present, we do not maintain an independent board of directors. Further, the requirements for board or committee membership, particularly with respect to an individual’s independence and level of experience in finance and accounting matters, may make it difficult to attract and retain qualified board members going forward. If we are unable to attract and retain qualified officers and directors, the management of our business and our ability to obtain or retain the listing of our common stock on any stock exchange (assuming we are able to obtain such listing) could be adversely affected.

| 14 |

If we fail to establish and maintain an effective system of internal controls, we may not be able to report our financial results accurately or prevent fraud. Any inability to report and file our financial results accurately and timely could harm our business and adversely impact the trading price of our common stock.

We are required to establish and maintain internal controls over financial reporting, disclosure controls and to comply with other requirements of the Sarbanes-Oxley Act and the rules promulgated by the U.S. Securities and Exchange Commission (or the SEC) thereunder. Our senior management, which currently consists of Mr. Weidong Du, Ms. Wei Tan and Mr. Derek Wiseman, cannot guarantee that our internal controls and disclosure procedures will prevent all possible errors or all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. In addition, the design of a control system must reflect the fact that there are resource constraints and the benefit of controls must be relative to their costs. Because of the inherent limitations in all control systems, no system of controls can provide absolute assurance that all control issues and instances of fraud, if any, within our company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty and that breakdowns can occur because of simple error or mistake. Further, controls can be circumvented by individual acts of some persons, by collusion of two or more persons, or by management’s override of the controls. The design of any system of controls is also based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Over time, a control may become inadequate because of changes in conditions or the degree of compliance with policies or procedures may deteriorate. Because of inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and may not be detected.

Our compliance with complicated U.S. regulations concerning corporate governance and public disclosure will result in additional expenses. Moreover, our ability to comply with all applicable laws, rules and regulations is uncertain given our management’s relative inexperience with operating U.S. public companies.

As a public company, we will be faced with expensive, complicated and evolving disclosure, governance and compliance laws, regulations and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act and the Dodd–Frank Wall Street Reform and Consumer Protection Act. New or changing laws, regulations and standards are subject to varying interpretations in many cases due to their lack of specificity, and, as a result, their application in practice may evolve over time as new guidance is provided by regulatory and governing bodies, which could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure and governance practices. As a result, our efforts to comply with evolving laws, regulations and standards of a U.S. public company are likely to continue to result in increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities.

Moreover, our officers and directors do not have extensive experience in operating a U.S. public company, which makes our ability to comply with applicable laws, rules and regulations uncertain. Our failure to comply with all laws, rules and regulations applicable to U.S. public companies could subject us or our management to regulatory scrutiny or sanction, which could harm our reputation and stock price.

| 15 |

As an “emerging growth company” under applicable law, we will be subject to lessened disclosure requirements, which could leave our shareholders without information or rights available to shareholders of more mature companies.

For as long as we remain an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (which we refer to herein as the JOBS Act), we have elected to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to:

| ● | not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act; | |

| ● | taking advantage of an extension of time to comply with new or revised financial accounting standards; | |

| ● | reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements; and | |

| ● | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. |

We expect to take advantage of these reporting exemptions until we are no longer an “emerging growth company.” Because of these lessened regulatory requirements, our shareholders would be left without information or rights available to shareholders of more mature companies.

Because we have elected to use the extended transition period for complying with new or revised accounting standards for an “emerging growth company,” our financial statements may not be comparable to companies that comply with public company effective dates.

We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act. This election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates. Consequently, our financial statements may not be comparable to companies that comply with public company effective dates. As such, investors may have difficulty evaluating or comparing our business, performance or prospects in comparison to other public companies, which may have a negative impact on the value and liquidity of shares of our common stock.

Risks Related to Our Industry

Intense competition in the sporting goods industry could limit our growth and reduce our profitability.

The sporting goods manufacturing and retail market in general is highly fragmented and intensely competitive. In each of the three geographic areas in which we operate, we compete directly with a number of brand name cycling apparel manufacturers, some of whom are top ranking brands in their respective geographic markets. In particular, we primarily compete with domestic Chinese brands in the China market, including Champion System, Santic, Sobike and CCN, and we compete with top cycling apparel brands in the North America and European markets. Some of our competitors have a large base of direct consumer and reseller accounts, greater financial resources and mature commercial infrastructures. In addition, if our competitors reduce their prices, it may be difficult for us to reach our net sales goals without reducing our prices. As a result of this competitive environment, we may also need to spend more on advertising and promotion than we anticipate. If we are unable to compete effectively, our operating results will suffer.

| 16 |

Seasonal fluctuations in the sales of sporting goods could cause our annual operating results to suffer significantly.

We experience seasonal fluctuations in our net sales and operating results. Summer and fall are the peak selling season of our products during which time we generate more sales revenue. If we miscalculate the demand for our products generally or for our product mix during the peak season, our net sales could decline, resulting in excess inventory, which could harm our financial performance. Because a substantial portion of our operating income is derived from our net sales during the peak season, a shortfall in expected net sales during that time could cause our annual operating results to suffer significantly.

If we fail to anticipate changes in consumer preferences, we may experience lower net sales, higher inventory markdowns and lower margins.

Our products must appeal to a broad range of consumers whose preferences can only be predicted to a certain degree. These preferences are also subject to change. Our success depends upon our ability to anticipate and respond in a timely manner to trends in sporting apparel and accessories in general and cycling apparel in particular. If we fail to identify and respond to these changes, our net sales may decline.

Risks Associated with Our International Operations

Our operations in international markets, and earnings in those markets, may be affected by legal, regulatory, political and economic risks.

Our operations in international markets, and earnings in those markets, may be affected by legal, regulatory, political and economic risks. Our ability to maintain the current level of operations in our existing international markets and to capitalize on growth in existing and new international markets is subject to risks associated with international operations. These include the burdens of complying with a variety of foreign laws and regulations, unexpected changes in regulatory requirements, new tariffs or other barriers to some international markets.

We cannot predict whether quotas, duties, taxes, exchange controls or other restrictions will be imposed by the United States, China, the European Union or other countries upon the import or export of our products in the future, or what effect any of these actions would have on our business, financial condition or results of operations. We cannot predict whether there might be changes in our ability to repatriate earnings or capital from international jurisdictions. Changes in regulatory and geopolitical policies and other factors may adversely affect our business or may require us to modify our current business practices.

Approximately 72% of our sales for the year ended December 31, 2017 were earned in international markets. We are exposed to risks of changes in U.S. policy for companies having business operations outside the United States, which could have a material adverse effect on our business, results of operations and financial condition.

We use foreign suppliers for a significant portion of our raw materials and our manufacturing facility is located in China, which poses risks to our business operations.

Our products are manufactured at our facility in China. Any of the following could materially and adversely affect our ability to produce or deliver our products and, as a result, have a material adverse effect on our business, financial condition and results of operations:

| ● | political or labor instability in countries where our facilities, contractors, and suppliers are located; | |

| ● | political or military conflict, which could cause a delay in the transportation of raw materials and products to us and an increase in transportation costs; | |

| ● | heightened terrorism security concerns, which could subject imported or exported goods to additional, more frequent or more lengthy inspections, leading to delays in deliveries or impoundment of goods for extended periods or could result in decreased scrutiny by customs officials for counterfeit goods, leading to lost sales, increased costs for our anti-counterfeiting measures and damage to the reputation of our brands; |

| 17 |

| ● | imposition of regulations and quotas relating to imports and our ability to adjust timely to changes in trade regulations, which, among other things, could limit our ability to produce products in cost-effective countries that have the labor and expertise needed; | |

| ● | imposition of duties, taxes and other charges on imports; and | |

| ● | imposition or the repeal of laws that affect intellectual property rights. |

Our business is subject to foreign, national, state and local laws and regulations for environmental, employment, safety and other matters. The costs of compliance with, or the violation of, such laws and regulations by us could have an adverse effect on our business, results of operations and financial condition.

Numerous governmental agencies in the United States and in other countries in which we have operations, enforce comprehensive national, state, and local laws and regulations on a wide range of environmental, employment, health, safety and other matters. We could be adversely affected by costs of compliance or violations of those laws and regulations. In addition, the costs of raw materials purchased by us from our suppliers could increase due to the costs of compliance by those entities. Further, violations of such laws and regulations could affect the availability of inventory, thereby affecting our net sales.

Changes in foreign, cultural, political, and financial market conditions could impair our international operations and financial performance.

The economies of foreign countries important to our operations, including countries in Asia and Europe, could suffer slower economic growth or economic, social and/or political instability or hyperinflation in the future. International operations, including manufacturing and sales (and the international operations of our customers), are subject to inherent risks which could adversely affect us, including, among other things:

| ● | protectionist policies restricting or impairing the manufacturing, sales or import and export of our products; | |

| ● | new restrictions on access to markets; | |

| ● | lack of developed infrastructure; | |

| ● | inflation or recession; | |

| ● | devaluations or fluctuations in the value of currencies; | |

| ● | changes in and the burdens and costs of compliance with a variety of foreign laws and regulations, including tax laws, accounting standards, environmental laws and occupational health and safety laws; | |

| ● | social, political or economic instability; | |

| ● | acts of war and terrorism; | |

| ● | natural disasters or other crises; | |

| ● | reduced protection of intellectual property rights in some countries; | |

| ● | increases in duties and taxation; and | |

| ● | restrictions on transfer of funds and/or exchange of currencies; expropriation of assets; and other adverse changes in policies, including monetary, tax and/or lending policies, relating to foreign investment or foreign trade by our host countries. |

| 18 |

Should any of these risks occur, our ability to sell our products or repatriate profits could be impaired and we could experience a loss of sales and profitability from our international operations, which could have a material adverse impact on our business and financial conditions.

Risks Associated With Doing Business in China

Changes in the political and economic policies of the PRC government may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies.

Most of our operations are conducted in the PRC and a significant percentage of our revenue is sourced from the PRC. Accordingly, our financial condition and results of operations are affected to a significant extent by economic, political and legal developments in the PRC.

The PRC economy differs from the economies of most developed countries in many respects, including the extent of government involvement, level of development, growth rate, control of foreign exchange and allocation of resources. Although the PRC government has implemented measures emphasizing the utilization of market forces for economic reform, the reduction of state ownership of productive assets, and the establishment of improved corporate governance in business enterprises, a substantial portion of productive assets in China is still owned by the government. In addition, the PRC government continues to play a significant role in regulating industry development by imposing industrial policies. The PRC government also exercises significant control over China’s economic growth by allocating resources, controlling payment of foreign currency-denominated obligations, setting monetary policy, regulating financial services and institutions and providing preferential treatment to particular industries or companies.

While the PRC economy has experienced significant growth in the past three decades, growth has been uneven, both geographically and among various sectors of the economy. The PRC government has implemented various measures to encourage economic growth and guide the allocation of resources. Some of these measures may benefit the overall PRC economy, but may also have a negative effect on us. Our financial condition and results of operation could be materially and adversely affected by government control over capital investments or changes in tax regulations that are applicable to us. In addition, the PRC government has implemented in the past certain measures, including interest rate increases, to control the pace of economic growth. These measures may cause decreased economic activity, which in turn could lead to a reduction in demand for our services and consequently have a material adverse effect on our businesses, financial condition and results of operations.

If relations between the United States and China worsen, investors may be unwilling to hold or buy our stock and our stock price may decrease.

At various times during recent years, the U.S and China have had significant disagreements over political and economic issues. Controversies may arise in the future between these two countries that may affect our economic outlook both in the U.S and in China. Any political or trade controversies between the U.S and China, whether or not directly related to our business, could reduce the price of our common stock.

Future inflation in China may inhibit the profitability of our business in China.

In recent years, the Chinese economy has experienced periods of rapid expansion and high rates of inflation. Rapid economic growth can lead to growth in the money supply and rising inflation. If prices for our services and products rise at a rate that is insufficient to compensate for the rise in the costs of supplies, it may have an adverse effect on profitability. These factors have led to the adoption by the Chinese government, from time to time, of various corrective measures designed to restrict the availability of credit or regulate growth and contain inflation. High inflation may in the future cause the Chinese government to impose controls on credit and/or prices, or to take other action, which could inhibit economic activity in China and thereby harm the market for our services and products.

| 19 |

The fluctuation of the Renminbi may have a material adverse effect on your investment.