Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - Gadsden Properties, Inc. | s109492_ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Gadsden Properties, Inc. | s109492_ex32-1.htm |

| EX-23.1 - EXHIBIT 23.1 - Gadsden Properties, Inc. | s109492_ex23-1.htm |

| EX-31.1 - EXHIBIT 31.1 - Gadsden Properties, Inc. | s109492_ex31-1.htm |

| EX-21.1 - EXHIBIT 21.1 - Gadsden Properties, Inc. | s109492_ex21-1.htm |

| EX-14.1 - EXHIBIT 14.1 - Gadsden Properties, Inc. | s109492_ex14-1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______________ to _____________

Commission file number: 000-11635

FC GLOBAL REALTY INCORPORATED

(Exact name of registrant as specified in its charter)

| Nevada | 59-2058100 | ||||

| (State or Other Jurisdiction | (I.R.S. Employer | ||||

| of incorporation or Organization) | Identification No.) | ||||

40 Ramland Road South, Suite 200 Orangeburg, NY 10962

(Address of principal executive offices, including zip code)

(215) 619-3600

(Issuer’s telephone number, including area code)

Securities registered under Section 12(b) of the Exchange Act:

| Name of each exchange | |||||

| Title of each class | on which registered | ||||

| Common Stock | Nasdaq Capital Market, TASE | ||||

Securities registered under Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes☐ No ☒

Indicate by check mark whether the registrant: (i) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (ii) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ☐ | Accelerated Filer ☐ |

| Non-Accelerated Filer ☐ (Do not check if a smaller reporting company) | Smaller reporting company ☒ Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ☐ No ☒

As of June 30, 2017 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the shares of the registrant’s common stock held by non-affiliates (based upon the closing sale price of such shares as reported on The Nasdaq Capital Market) was approximately $4.9 million. Shares of the registrant’s common stock held by each executive officer and director and by each person who owns 10% or more of the outstanding common stock have been excluded from the calculation in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 30, 2018, the number of shares outstanding of our common stock was 11,868,619.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Table of Contents

| i |

INTRODUCTORY NOTE

Use of Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to “we,” “our” and “our company” refer to FC Global Realty Incorporated (Formerly: PhotoMedex, Inc.), a Nevada corporation, and its consolidated subsidiaries.

Special Note Regarding Forward Looking Statements

This report and the other materials we have filed or will file with the U.S. Securities and Exchange Commission, or the SEC, contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements, other than statements of historical fact, are statements that could be deemed forward-looking statements, including, but not limited to, statements regarding our business strategy, expectations and plans regarding our future operations and our future financial position. When used in this report or in the other materials we have filed or will file with the SEC, the words “believe,” “may,” “will,” “potentially,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “indicate,” “seek,” “project,” “plan,” “could,” “should” or “would” and similar expressions are intended to identify forward-looking statements. Among the factors that could cause or contribute to material differences between our actual results and those indicated from the forward-looking statements are risks and uncertainties inherent in our business, including, but not limited to:

| ● | our ability to successfully integrate the acquired real estate business; |

| ● | our ability to retain key employees; |

| ● | demand fluctuations in the real estate industry; |

| ● | adverse changes in economic conditions in markets where our real estate investments may be made; |

| ● | possible decreases in the market value of our future real estate investments; |

| ● | our ability to obtain adequate financing to fund our future property acquisitions and project developments; |

| ● | the possibility that we may not recover our advance costs in each real estate development project; |

| ● | our reliance on subcontractors to construct each property, and on building supply companies to provide components for each property’s construction; |

| ● | competition in the real estate industry; |

| ● | the possibility that legal challenges or governmental regulations may delay the start or completion of construction on our projected real estate ventures, increase our expenses, or limit our construction activities; |

| ● | the potential for increased costs or shortages of labor or components, or other circumstances beyond our control; |

| ● | our ability to continue as a going-concern; |

| ● | our ability to raise capital when needed; |

| ● | economic, political or other developments in foreign countries in which we do business; |

| ● | the international nature of our business; and |

| ● | results of existing or future litigation. |

Additional factors that could cause or contribute to such differences include, but are not limited to, those discussed in this report, and in particular, the risks discussed under Item 1A. “Risk Factors” and those discussed in other documents we file with the SEC. Except as required by law, we do not intend to update these forward-looking statements publicly or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. Accordingly, readers are cautioned not to place undue reliance on such forward-looking statements.

Stock Split

On September 7, 2016, we completed a 1-for-5 reverse stock split of our outstanding common stock. Accordingly, all share and per share information contained in this report has been restated to retroactively show the effect of that stock split.

| ii |

| ITEM 1. | BUSINESS. |

Our Company

Our company, founded in 1980, is transitioning from its former business as a skin health company to a company focused on real estate development and asset management, concentrating primarily on investments in high quality income producing assets, hotel and resort developments, residential developments and other opportunistic commercial properties.

Until the recent sale of our consumer products division, we were a global skin health company providing integrated disease management and aesthetic solutions to dermatologists, professional aestheticians and consumers. Starting in 2014, we began to sell off certain business units and product lines and on January 23, 2017, we sold the last remaining major product line. Following this transaction, we had only minimal operations and assets remaining, of immaterial value to our company. We are in the process of liquidating the remaining legacy inventory and assets of this business line, after which time we will no longer operate within the skin health business.

Following the Contribution Transaction described below, our focus is to build our company into a leading real estate, asset management and development company concentrating primarily on investments in high yield income producing assets and other opportunistic commercial properties via direct property ownership and asset management. Our objective is to generate long term net asset value growth while adhering to institutional best practices and a deep research process for all investments.

For income producing properties, we intend to acquire assets that provide recurring income with the potential for income growth over the long-term. We believe there can be an attractive risk/reward profile to such properties based on the location and the underlying creditworthiness of the tenants. We intend to use such income generation to fund additional acquisitions and development opportunities and general corporate purposes. In addition, we intend to invest in land assets that can be developed into income generating properties or properties for sale. We believe that our size and scale provide an opportunity to take advantage of smaller-tier assets that most traditional investors do not focus on due to size limitations, thus creating unique investment opportunities. In particular, we intend to target assets in secondary and tertiary markets that require minimal capital expenditures but generate initial unlevered cash flow yields that are higher than those in primary markets.

A second component of our investment strategy will revolve around sourcing asset management opportunities for which we would operate as an asset manager of real estate properties. We are not structured as a Real Estate Investment Trust “REIT”, thus we have the ability to retain earnings and to operate in real estate asset management, development and peripheral real estate activities, items that may be limited by REIT requirements. We will look to utilize our existing infrastructure to provide economies of scale to owners of real estate assets as we grow our portfolio over time.

Recent Developments

Contribution Transaction

On March 31, 2017, we entered into an Interest Contribution Agreement with First Capital Real Estate Operating Partnership, L.P., or the Contributor, First Capital Real Estate Trust Incorporated, or the Contributor Parent (the Contributor and the Contributor Parent are sometimes referred to in this report as the Contributor Parties), and FC Global Realty Operating Partnership, LLC, our wholly-owned subsidiary, or the Acquiror. The parties entered into amendments to the Interest Contribution Agreement on August 3, 2017, October 11, 2017 and December 22, 2017. Pursuant to the Interest Contribution Agreement, as amended (which we collectively refer to as the Contribution Agreement), the Contributor contributed certain real estate assets to the Acquiror. In exchange, the Contributor received shares of our common stock and newly designated Series A Convertible Preferred Stock as described below. We refer to this transaction as the Contribution Transaction.

On May 17, 2017 (referred to in this report as the Closing Date), the Contributor transferred $10 million of assets to the Acquiror, consisting of the following:

| ● | three vacant land sites intended for development as gas stations located in northern California, |

3

| ● | a 75% interest in a limited liability company that owns a vacant land site intended for development as a gas station, located in northern California; and |

| ● | a 100% interest in a limited liability company, which we refer to as the Avalon Interest, which owns a 17.9133% interest in a limited liability company called Avalon Jubilee LLC that owns property located in Los Lunas, New Mexico being developed as a single family residential development. As described below, the Contributor Parent agreed to transfer the Avalon Interest within 30 days following the Closing Date. |

Pursuant to the terms and conditions of an Agreement to Waive Closing Deliverables, dated as of May 17, 2017, the Contributor agreed to deliver the Avalon Interest to the Acquiror, in up to two installments, on or before the thirtieth (30th) calendar day following the Closing Date. The transfer of both installments of the Avalon Interest was completed on June 26, 2017. Notwithstanding that the Contributor did not complete the transfer of the Avalon Interest to the Acquiror on the Closing Date, the parties agreed that the Acquiror would be entitled to all economic benefits of ownership of the Avalon Interest from and after the date of the Closing Date.

On January 12, 2018, we received a copy of a complaint, dated November 17, 2017, that was filed by Alpha Alpha, LLC in the Thirteenth Judicial District Court in the County of Valencia in the State of New Mexico against Avalon Jubilee, LLC, the holding company that owns the property in Los Lunas, New Mexico, HiTex, LLC, MCBB, LLC, Land Strategies, LLC, Ronald R. Cobb and John Does 1 – 5. The suit asks the court to, among other things, determine whether there have been unauthorized transfers of interest in Avalon Jubilee LLC; and declare who are the holders of interests in Avalon Jubilee LLC. Although the complaint does not name our company or any of its subsidiaries or specifically question our interest in Avalon Jubilee LLC, it raises questions about whether the transfers of interest leading to our acquisition of our interest in Avalon Jubilee LLC were properly made in accordance with the Avalon Jubilee operating agreement. We have begun an internal investigation into this matter and will disclose the results of that investigation once it has been completed. Although neither our company nor any of its subsidiaries is a party to litigation regarding this matter, we recognized an impairment expense of $862 thousand to account for our estimate of the impact that such litigation may have on the operations and fair value of the underlying asset.

The proposed gas station sites are located in Atwater and Merced, California and had an agreed upon value of $2.6 million. We intend to explore our options for the development of these properties. We may (i) lease a property to a developer who will handle all further development of the property, with our company receiving monthly lease payments from the developer; (ii) engage a contractor to develop a property to a certain level, then lease it to a developer which will handle the final development and leasing of the property, with our company receiving monthly payments from the developer; or (iii) engage a contractor to completely develop a property, then lease it directly to a tenant who will remit monthly lease payments back to us. The option or options selected for these properties will depend upon the types of tenants interested in operating gas stations and/or related ventures on those properties, as well as our capitalization and available financial resources. In these arrangements, the construction and/or management of the properties are or will be handled by third-party firms which specialize in such work. Therefore, we anticipate that we will not need to hire significant additional personnel to develop, maintain and manage these properties. As for funding for any costs associated with these properties’ development, although we cannot provide any assurance that we will be able to obtain funding, we will seek funding from one or more of the following potential sources funding from third-party investors, funding as a result of loans secured by the properties, or joint-funding arrangements with developers and/or managers of these properties.

The residential development in New Mexico consists of approximately 250, non-contiguous, single family residential lots and a 10,000 square foot club house. The agreed upon value of this property was approximately $7.4 million. This property already has a management and construction arrangement in place. We are the minority holder in that property, holding a 17.9% interest.

In exchange for these assets, we issued to the Contributor 879,234 shares of our common stock, which represented approximately 19.9% of our issued and outstanding common stock immediately prior to the Closing Date, at a per share value of $2.5183, or $2.2 million in the aggregate. We issued the remaining $7.8 million of the approximately $10 million consideration to the Contributor in the form of 123,668 shares of our newly designated non-voting Series A Convertible Preferred Stock. Each share of the Series A Convertible Preferred Stock is convertible into 25 shares of our common stock, subject to the satisfaction of certain conditions, including stockholder approval of such conversion.

4

The number of shares of common stock issued to the Contributor and to be issued upon conversion of the Series A Convertible Preferred Stock was determined by dividing the $10 million value of the assets by $2.5183, a specified price per share value which represents a 7.5% premium above the volume-weighted average price of all on-exchange transactions in our common stock executed on The Nasdaq Capital Market, during the forty-three (43) trading days prior to the trading day immediately prior to the public announcement of the transaction by our company and the Contributor Parent on March 31, 2017, as reported by Bloomberg L.P. We believe that the trading price of our common stock at the time of the Contribution Transaction represented the value of our prior medical device business and not our new real estate development business. The value of the contributed assets was arrived at by the mutual agreement of the parties after analyzing each of the assets in comparison to historical sales of similar land parcels. We also assumed the obligations of the Contributor and its affiliates under certain agreements covering the delivered assets, including an Operating Agreement of Central Valley Gas Station Development, LLC, a Delaware limited liability company, dated January 28, 2013, and all amendments thereto; the Operating Agreement of Avalon Jubilee, LLC, a New Mexico limited liability company, dated as of May 16, 2012, and all amendments thereto; a Development Services Agreement, dated September 15, 2015, by and between UR-FC Contributed Assets, LLC, a Delaware limited liability company, as owner, and Land Strategies, LLC, a Nevada limited liability company, as developer, with respect to real property owned by Avalon Jubilee, LLC; and a Construction Contract dated, November 19, 2014, between Central Valley Gas Stations Development, LLC, as owner, and First Capital Builders, LLC, as contractor, with respect to the project known commonly as Green Sands and Buhach Rd., Atwater, CA. The Acquiror expects to enter into amended operating agreements with respect to some or all of these entities. As of the filing of this report, the agreements have not been amended.

Additionally, we assumed those ancillary agreements, commitments and obligations with respect to the delivered assets specified in that certain Assignment and Assumption Agreement, dated as of May 17, 2017.

Under the Contribution Agreement, on the Closing Date our Board was required to consist of seven (7) persons of whom three (3) would be designated by our company, three (3) would be designated by the Contributor Parent, and one (1) nonaffiliated director would be selected by the other six (6) directors; provided, however, that at least four (4) of the members of the Board as so designated would be independent directors. In accordance with the foregoing, on the Closing Date, Lewis C. Pell, Dr. Yoav Ben-Dror and Stephen P. Connelly resigned from our Board, Dr. Dolev Rafaeli, Dennis M. McGrath and Michael R. Stewart were designated by our company, and Suneet Singal, Richard J. Leider and Dr. Bob Froehlich were designated by the Contributor Parent to serve as members of the Board. The seventh director, Darrel C. Menthe, was designated and appointed to the Board by the other directors. On March 4, 2018, Suneet Singal resigned from the Company’s Board of Directors and on the following day, March 5, 2018, Darrel Menthe also resigned from the Company’s Board of Directors. Their resignations were not in connection with any known disagreement with the Company on any matter. Under the provisions of the Stock Purchase Agreement dated December 22, 2017, as reported in the Company’s Current Report on Form 8-K, filed with the Securities and Exchange Commission on December 29, 2017, Opportunity Fund I-SS, LLC, or “Opportunity Fund” has notified the Company that it may exercise its right to appoint two replacement directors to the Company’s Board of Directors, but it has not yet done so. The two directorships resulting from such resignations currently remain vacant. See “Private Placement” below.

Additionally, the following officer changes became effective as of the Closing Date:

| ● | Dr. Dolev Rafaeli, Dennis McGrath, and Dr. Yoav Ben-Dror resigned from their positions as officers of our company and its subsidiaries and we acknowledged and agreed that such resignations constituted valid terminations of their respective employment agreements for “Good Reason” (as that term is defined in their respective employment agreements) and the Board consented to the waiver of the notice requirements and cure periods as described in their respective resignation letters and confirmed that each of Messrs. Rafaeli and McGrath are entitled to all of the compensation described in Section 7(c) of their respective employment agreements for the remainder of the term of such employment agreements; |

| ● | Suneet Singal was appointed as Chief Executive Officer of our company and Stephen Johnson was appointed the Chief Financial Officer of our company (both of Messrs. Singal and Johnson have since resigned as officers of our company); and |

| ● | Dr. Ben-Dror resigned as managing director of our foreign subsidiaries, including Radiancy (Israel) Limited and Photo Therapeutics Limited in the United Kingdom, and agreed to enter into a non-compete agreement with our company and support the transition of his respective Board duties in lieu of his agreement for lock-up of his shares, and he will be entitled to all his compensation through a term that matches the term of Messrs. Rafaeli and McGrath. |

Closing of the Contribution Transaction was subject to customary closing conditions and certain other specific conditions, including the following: (i) the entry into a registration rights agreement requiring us to register for resale the shares being issued in connection with the Contribution Transaction; (ii) the entry into a lock up agreement that restricts the transfer of our shares that are held by certain of our affiliates and certain affiliates of the Contributor Parent; (iii) the restructuring of our Board as described above; (iv) the resignation of certain of our officers as described above; and (v) the entry into an employment agreement with Mr. Suneet Singal, who became our new Chief Executive Officer at the closing.

The Contribution Agreement contemplated that additional contributions would be made prior to December 31, 2017; however, the Contributor failed to satisfy the conditions precedent to those additional contributions before the December 31, 2017 deadline such that only the closing described above was completed.

5

We elected to early adopt ASU 2017-01, Business Combinations (Topic 805) Clarifying the Definition of a Business. Accordingly, the determination of whether the transaction represents a business combination was evaluated by applying ASU 2017-01 guidance. We have determined that the group of assets assumed do not include (and also, none of them on a stand-alone basis) include, an input and a substantive process that together significantly contribute to the ability to create output and thus it was determined that the contribution represents an acquisition of assets rather than a business combination. Accordingly, the total sum of the fair value of consideration given (i.e. the fair value of the equity interests issued) together with the transaction costs, was allocated to the individual assets acquired and liabilities assumed based on their relative fair values at the date of acquisition. Such allocation did not give rise to goodwill.

The terms of the Series A Convertible Preferred Stock are governed by a certificate of designation, or the Series A Certificate of Designation, filed by us with the Nevada Secretary of State on May 15, 2017. Pursuant to the Series A Certificate of Designation, we designated 3,000,000 shares of our preferred stock as Series A Convertible Preferred Stock. Following is a summary of the material terms of the Series A Convertible Preferred Stock:

| ● | Dividends. Except for stock dividends or distributions for which adjustments are made, holders of Series A Convertible Preferred Stock shall be entitled to receive dividends on shares of Series A Convertible Preferred Stock equal (on an as-if-converted-to-common-stock basis) to and in the same form as dividends actually paid on shares of the common stock when, as and if such dividends are paid on shares of the common stock. No other dividends shall be paid on shares of Series A Convertible Preferred Stock. |

| ● | Liquidation. Upon any liquidation, dissolution or winding-up of our company, whether voluntary or involuntary, the holders of Series A Convertible Preferred Stock shall be entitled to receive out of the assets, whether capital or surplus, of our company the same amount that a holder of common stock would receive if the Series A Convertible Preferred Stock were fully converted (disregarding for such purposes any conversion limitations) to common stock immediately prior to such liquidation, which amount shall be paid pari passu with all holders of common stock. We must mail written notice of any such liquidation to each holder not less than 45 days prior to the payment date stated therein. |

| ● | Voting Rights. Except as otherwise provided in the Series A Certificate of Designation or as otherwise required by law, the Series A Convertible Preferred Stock shall have no voting rights. However, as long as any shares of Series A Convertible Preferred Stock are outstanding, we shall not, without the affirmative vote of the holders of a majority of the then outstanding shares of the Series A Convertible Preferred Stock, (a) alter or change adversely the powers, preferences or rights given to the Series A Convertible Preferred Stock or alter or amend the Series A Certificate of Designation, (b) amend our articles of incorporation or other charter documents in any manner that adversely affects any rights of the holders, (c) increase the number of authorized shares of Series A Convertible Preferred Stock, or (d) enter into any agreement with respect to any of the foregoing. |

| ● | Conversion. Each share of Series A Convertible Preferred Stock shall be convertible, at any time and from time to time from at the option of the holder thereof, into that number of shares of common stock determined by dividing $62.9575 by the Conversion Price. The Conversion Price for the Series A Convertible Preferred Stock is equal to $2.5183, subject to adjustment as described in the Series A Certificate of Designation. |

Payout Notes and Stock Grant Agreement

Under the Contribution Agreement, amounts due to Dr. Dolev Rafaeli and Dennis M. McGrath under their employment agreements, as well as amounts due to Dr. Yoav Ben-Dror for his services as a board member and officer of our foreign subsidiaries, were converted to convertible secured notes in the principal amounts of approximately $3.1 million, $0.98 million and $1.5 million, respectively, following approval from our stockholders on October 12, 2017 (which we refer to as the Payout Notes). The Payout Notes were due on October 12, 2018, carried a ten percent (10%) interest rate, payable monthly in arrears commencing on December 1, 2017, and were secured by a security interest in all of our assets pursuant to a security agreement that we entered into with the holders of the Payout Notes on October 12, 2017. The Payout Notes were convertible into shares of our common stock and we agreed to register the shares underlying the Payout Notes within thirty (30) days of issuance with best efforts to cause the registration statement covering such shares to become effective within one-hundred twenty (120) days of issuance. On November 14, 2017, we filed a registration statement on Form S-3 (which we refer to as the First Registration Statement) to register all shares that may be issued upon conversion of the Payout Notes, which was subsequently amended to include the Payout Shares issued under the Stock Grant Agreement described below.

6

On December 22, 2017, we entered into a stock grant agreement, or the Stock Grant Agreement, with Dr. Dolev Rafaeli, Dennis M. McGrath and Dr. Yoav Ben-Dror (collectively referred to herein as the Note Holders) to (i) cause the early conversion of the Payout Notes into an aggregate of 5,628,291 shares of our common stock (which we refer to as the Payout Shares), (ii) effectuate the release of all security interests associated with the Payout Notes, (iii) provide for the issuance of an aggregate of 1,857,336 additional shares of common stock to the Note Holders as consideration for the various agreements of the Note Holders contained in the Stock Grant Agreement (which we refer to as the Additional Shares), (iv) provide for certain cash payments to the Note Holders in amounts equal to the interest payments that would have been made to the Note Holders absent the conversion of the Payout Notes, (v) obtain the agreement of the Note Holders to provide certain support services to our company, and (vi) obtain the conditional resignation of certain of the Note Holders from our Board of Directors. Accordingly, the Payout Notes were paid in full.

Pursuant to the Stock Grant Agreement, we agreed to make twelve (12) monthly payments on the first of each month commencing on January 1, 2018 in the amounts of approximately $21, $7, and $10 thousand, respectively, to Messrs. Rafaeli, McGrath, and Ben-Dror, respectively (which we refer to as the Cash Payments). The Cash Payments are consideration for certain consulting services to be provided by the Note Holders specified in the Stock Grant Agreement.

As promptly as possible following entry into the Stock Grant Agreement, we are required to file a proxy statement and hold a special meeting of our stockholders to authorize and approve the issuance of the Additional Shares. We are required to issue the Additional Shares promptly, but in any event within ten (10) days after we obtain stockholder approval of such issuance. As of the date of this report, we have not yet filed such proxy statement.

In furtherance of obtaining such stockholder approval, on December 22, 2017, the Contributor, the Note Holders and certain other significant stockholders of our company, including OFI (as defined under “Private Placement” below), entered into a shareholder voting support and confidentiality agreement, or the Note Holder Voting Agreement, pursuant to which such stockholders agreed to vote their shares in favor of the transactions contemplated by the Stock Grant Agreement, including the issuance to the Note Holders or their designees of common stock equal to 20% or more of the common stock or 20% or more of the voting power outstanding before the issuance (which we refer to as the Note Holder 20% Proposal), and also agreed to certain transfer restrictions on the securities of our company owned by them. Under the Note Holder Voting Agreement, such stockholders may not transfer or otherwise dispose of any equity securities of our company until the earlier of: (i) the first business day following approval of the Note Holder 20% Proposal by our stockholders, (ii) the mutual written consent of the parties to the Note Holder Voting Agreement, or (iii) December 31, 2018. Such transfer restrictions do not apply to (y) the exercise of any option, warrant or other securities convertible or exchangeable for securities of our company or (z) to any transfer by the Contributor or the Contributor Parent, in each case, to any holder of a security issued by it. The Note Holder Voting Agreement also includes a power of attorney pursuant to which each stockholder designated and appointed our company and its duly authorized officers and agents as its agents and attorney in fact to act on the stockholder’s behalf to execute any proxy relating to any meeting of our stockholders for the purposes set forth in the Note Holder Voting Agreement.

On December 22, 2017, in connection with the Stock Grant Agreement, we entered into a registration rights agreement, or the Note Holder Registration Rights Agreement, with the Note Holders, pursuant to which we agreed to register the Additional Shares under the Securities Act. We agreed to file a registration statement covering the resale of the Additional Shares within 30 days of the Stock Grant Agreement and cause such registration statement to be declared effective under the Securities Act as soon as possible but, in any event, no later than 120 days following the filing date if such registration statement is filed on Form S-3 or 150 days if such registration statement is filed on Form S-1. If such registration statement is not filed or declared effective by the SEC on or prior to such dates, or if after such registration statement is declared effective, without regard for the reason thereunder or efforts therefor, such registration statement ceases for any reason to be effective for more than an aggregate of 30 trading days during any 12-month period, which need not be consecutive, then in addition to any other rights the Note Holders may have under the Note Holder Registration Rights Agreement or under applicable law, we are required to pay to each Note Holder an amount in cash, as partial liquidated damages and not as a penalty, equal to 1.0% of the product obtained by multiplying (x) $1.00 by (y) the number of shares of common stock held by the Note Holder included in the registration statement (such product referred to as the Note Holder Investment Amount); provided that, in no event will we be liable for liquidated damages in excess of 1.0% of the Note Holder Investment Amount in any single month and that the maximum aggregate liquidated damages payable to the Note Holders under the Note Holder Registration Rights Agreement shall be ten percent (10%) of the Note Holder Investment Amount. The registration rights provision contained in the Payout Notes was incorporated by reference into the Note Holder Registration Rights Agreement, except that the Note Holders waived the breach by our company for failure to timely file the First Registration Statement and agreed that they are not entitled to liquidated damages as a result of such failure. Under the Note Holder Registration Rights Agreement, the Note Holders are entitled to liquidated damages if the First Registration Statement is not declared effective within 120 days following the date of the Payout Notes, but the Note Holders subsequently agreed to waive their rights to such liquidated damages until April 20, 2018. On January 23, 2018, we filed a registration statement on Form S-3 for the Additional Shares. The Note Holders waived their rights to liquidated damages in connection with the late filing of such registration statement and in connection with the effectiveness deadline for such registration statement until April 20, 2018.

7

Pursuant to the Stock Grant Agreement, Dr. Dolev Rafaeli and Dennis M. McGrath agreed to resign from our Board of Directors effective upon the last to occur of (i) receipt of all of the Payout Shares and all of the Additional Shares, (ii) receipt of all of the Cash Payments (either in accordance with the schedule provided in the Stock Grant Agreement or, at our option, in one lump sum on an accelerated basis), and (ii) the date that the Payout Shares and the Additional Shares have been registered for re-sale in accordance with the Note Holder Registration Rights Agreement.

Private Placement

On December 22, 2017, we entered into a securities purchase agreement, or the Purchase Agreement, with Opportunity Fund I-SS, LLC, a Delaware limited liability company, or OFI, under which OFI may invest up to $15 million in our company in a series of closings, in exchange for which OFI will receive shares of our newly designated Series B Preferred Stock at a purchase price of $1.00 per share.

On December 22, 2017, we completed the first closing under the Purchase Agreement, pursuant to which OFI provided $1.5 million to us in exchange for 1,500,000 shares of Series B Preferred Stock. On January 24, 2018, we completed a second closing under the Purchase Agreement, pursuant to which OFI provided approximately $2.2 million to us in exchange for 2,225,000 shares of Series B Preferred Stock. Under the Purchase Agreement, OFI may, but is not obligated to, make additional investments in one or more subsequent closings until an aggregate amount of $15 million has been invested or the Purchase Agreement has been terminated in accordance with its terms.

Under the Purchase Agreement, the proceeds from the first closing were to be used for working capital and general corporate purposes, the proceeds from the second closing were to be used to perform due diligence and invest in Income Generating Properties (as defined in the Purchase Agreement) that have been approved by our company’s Board of Directors, and proceeds from subsequent closings were to be used to invest in Income Generating Properties (as defined in the Purchase Agreement) that have been approved by our Board of Directors or as otherwise agreed to between us and OFI in writing prior to such subsequent closings. On March 16, 2018, we and OFI entered into a letter agreement, pursuant to which OFI agreed that we may use all proceeds for the purposes and uses described in a budget agreed to between us and OFI at the time the letter agreement was signed. In connection with such letter agreement, we agreed to provide OFI, on a quarterly basis, on or prior to 15 days after the end of each quarter, a report that describes, in reasonable detail, the actual expenses incurred, and payments made during such period compared to the expenses and payments specified in the budget for such period, certified by our Chief Financial Officer.

The terms of the Series B Preferred Stock are governed by a certificate of designation, or the Series B Certificate of Designation, filed by the Company with the Nevada Secretary of State on December 22, 2017. Pursuant to the Series B Certificate of Designation, we designated 15,000,000 shares of our preferred stock as Series B Preferred Stock. Following is a summary of the material terms of the Series B Preferred Stock:

| ● | Dividends. Holders of shares of Series B Preferred Stock shall receive cumulative dividends, pro rata among such holders, prior to and in preference to any dividend on our outstanding common stock at the per annum rate of 8% of the Series B Original Issue Price (as defined below). Dividends on each share of Series B Preferred Stock will accrue daily and be cumulative from December 22, 2017 (which we refer to as the Series B Original Issue Date) and shall be payable upon the occurrence of any voluntary or involuntary liquidation, dissolution or winding up of the Company (which we refer to as a Liquidation Event), a conversion or a redemption. The “Series B Original Issue Price” shall mean $1.00 per share, subject to appropriate adjustment in the event of any stock dividend, stock split, combination or other similar recapitalization with respect to the Series B Preferred Stock. Holders shall also be entitled to receive dividends on shares of Series B Preferred Stock equal (on an as-if-converted-to-common-stock basis regardless of whether the Series B Preferred Stock is then convertible or otherwise subject to conversion limitations) to and in the same form as dividends actually paid on shares of our common stock when, as and if such dividends are paid on shares of the common stock. |

8

| ● | Liquidation. In the event of (i) a Liquidation Event or (ii) a merger or consolidation (other than one in which our stockholders own a majority by voting power of the outstanding shares of the surviving or acquiring corporation) or a sale, lease, transfer, exclusive license or other disposition of all or substantially all of our assets (we refer to any such event as a Deemed Liquidation Event), the holders of shares of Series B Preferred Stock then outstanding shall be entitled to be paid out of our assets available for distribution to stockholders before any payment shall be made to the holders of our common stock, Series A Convertible Preferred Stock or any other class of securities authorized that is specifically designated as junior to the Series B Preferred Stock (referred to herein as Junior Securities) by reason of their ownership thereof, but pari passu with the holders of shares of any class of securities authorized that is specifically designated as pari passu with the Series B Preferred Stock (referred to herein as the Parity Securities) on a pro rata basis, an amount per share equal to the Series B Original Issue Price, plus any accrued dividends thereon. If upon any such Liquidation Event or Deemed Liquidation Event, our assets available for distribution to stockholders shall be insufficient to pay the holders of shares of Series B Preferred Stock the full amount to which they shall be entitled and the holders of Parity Securities the full amount to which they shall be entitled, the holders of shares of Series B Preferred Stock and the holders of shares of Parity Securities shall share ratably in any distribution of the assets available for distribution in proportion to the respective amounts which would otherwise be payable in respect of the shares held by them upon such distribution if all amounts payable on or with respect to such shares were paid in full. Upon a Liquidation Event or a Deemed Liquidation Event, in the event that following the payment of such liquidation preference we shall have additional cash and other assets available for distribution to stockholders, then the holders of shares of Series B Preferred Stock shall participate pari passu with the holders of shares of Parity Securities and Junior Securities based on the then current conversion rate (disregarding for such purposes any conversion limitations) with respect to all remaining distributions, dividends or other payments of cash, shares or other assets and property of our company, if any. |

| ● | Voting Rights. On any matter presented to our stockholders for their action or consideration, each holder of Series B Preferred Stock shall be entitled to cast the number of votes equal to the number of whole shares of common stock into which the shares of Series B Preferred Stock held by such holder are convertible as of the record date for determining stockholders entitled to vote on such matter (subject to the conversion limitations described below). Except as provided by law or by the other provisions of the Series B Certificate of Designation, the holders shall vote together with the holders of shares of common stock as a single class. However, as long as any shares of Series B Preferred Stock are outstanding, we shall not, without the affirmative vote of the holders of a majority of the outstanding shares of Series B Preferred Stock, or the Requisite Holders, (i) issue any class of equity securities that is senior in rights to the Series B Preferred Stock, (ii) issue any Parity Securities, (iii) alter or change adversely the powers, preferences or rights given to the Series B Preferred Stock or alter or amend the Series B Certificate of Designation, (iv) amend our articles of incorporation or other charter documents in any manner that adversely affects any rights of the holders of Series B Preferred Stock, (v) except pursuant to the redemption provisions of Parity Securities, redeem any shares of our preferred stock or common stock (other than pursuant to employee or consultant agreements giving us the right to repurchase shares at the original cost thereof upon the termination of services and provided that such repurchase is approved by our Board of Directors), or (vi) enter into any agreement with respect to any of the foregoing. |

| ● | Conversion. Each share of Series B Preferred Stock plus accrued, but unpaid, dividends thereon, or the Aggregate Preference Amount, shall be convertible, at any time and from time to time at the option of the holder thereof, into that number of shares of common stock determined by a formula (computed on the date of conversion), (i) the numerator of which is equal to the Aggregate Preference Amount and (ii) the denominator of which is equal to the quotient of the Conversion Price divided by $1.33. The “Conversion Price” for the Series B Preferred Stock shall initially be equal to $0.8684, subject to adjustment as described in the Series B Certificate of Designation. In addition, upon the earlier to occur of: (i) a Deemed Liquidation Event or (ii) if there has not been a breach or default by us under the Purchase Agreement that has occurred and is continuing, May 31, 2018, each share of Series B Preferred Stock plus accrued, but unpaid, dividends thereon shall be automatically converted into that number of shares of common stock determined by dividing $1.33 by the Conversion Price. Notwithstanding the forgoing, if we have not obtained approval from our stockholders with respect to the issuance of shares upon conversion in excess of 19.99% of the issued and outstanding common stock on the applicable conversion date (which we refer to as the Stockholder Approval), then we may not issue, upon conversion of the Series B Preferred Stock, a number of shares of common stock which, when aggregated with any shares of common stock issued on or after the Series B Original Issue Date and prior to such conversion date, would exceed 19.99% of the issued and outstanding shares of common stock (subject to adjustment for forward and reverse stock splits, recapitalizations and the like) (we refer to such number of shares as the Issuable Maximum). Each holder shall be entitled to a portion of the Issuable Maximum equal to the quotient obtained by dividing (i) the Series B Original Issue Price of such holder’s Series B Preferred Stock by (ii) the aggregate Series B Original Issue Price of all Series B Preferred Stock issued to all holders. |

9

| ● | Redemption. If (i) there is a breach by us of any of our representations and warranties contained in Sections 3.1(a) (Subsidiaries), 3.1(b) (Organization and Qualification), 3.1(c) (Authorization; Enforcement), 3.1(d) (No Conflicts), 3.1(f) (Issuance of the Shares), 3.1(g) (Capitalization), or 3.1(n) (Taxes) of the Purchase Agreement that has not been cured within 30 days after the date of such breach or (ii) Stockholder Approval has not been obtained by March 31, 2018 (each event being referred to herein as a Redemption Event), then each holder of Series B Preferred Stock may, at its option, require us to redeem any or all of the shares of Series B Preferred Stock held by such holder at a price per share equal to $1.33, plus accrued, but unpaid, dividends through and including the date of such redemption. We must provide a notice, or an Event Notice, to each holder of the occurrence of a Redemption Event of the kind described in (i) above (referred to herein as a Breach Event) as soon as practicable after becoming aware of such Breach Event, but in any event, not later than fifteen (15) days after such Breach Event and such notice shall provide a reasonable description of such Breach Event. A holder must send written notice of redemption, or a Redemption Notice, to us within ninety (90) days after (i) we provide such holder an Event Notice with respect to a Breach Event or (ii) the occurrence of a Redemption Event of the kind described in (ii) above. For the avoidance of doubt, if we do not timely provide an Event Notice, the holder shall nevertheless have the right to deliver a Redemption Notice in connection with any Redemption Event. If a holder fails to send a Redemption Notice on or prior to the 90th day after the occurrence of any Redemption Event, then such holder will lose such holder’s right to redemption with respect to the particular Redemption Event, but not any other Redemption Event. We did not obtain Stockholder Approval prior to March 31, 2018. |

The Purchase Agreement is subject to the usual pre- and post-closing representations, warranties and covenants. In addition, we agreed that, so long as the shares of Series B Preferred Stock purchased by OFI are outstanding, our debt (as defined by U.S. generally accepted accounting principles, or GAAP) shall not exceed 45% of our fixed assets without the prior written consent of the Requisite Holders. Subject to stockholder approval, we also agreed to amend the certificate of designation for our Series A Convertible Preferred Stock to change the conversion price from $2.5183 to $1.12024021352 such that each share of Series A Convertible Preferred Stock will be initially convertible into 56.20 shares of common stock instead of 25 shares of common stock. In addition, we agreed that at any time prior to the termination of the OFI Voting Agreement (as defined below), we shall cause any person who acquires any securities from us or any of our affiliates that, together with all securities held by such acquirer and its affiliates, will own, directly or indirectly, five percent (5%) or more of our outstanding common stock (after giving effect to the right of any such person to convert or exchange securities), to become a party to the OFI Voting Agreement by causing such person, as a condition to the delivery of such securities, to sign a counterpart signature page thereto that joins such person to the OFI Voting Agreement.

We also agreed to nominate two (2) directors to our Board of Directors upon request of OFI. In furtherance thereof, on December 22, 2017, Messrs. Suneet Singal and Darrel C. Menthe delivered resignation letters to our Board of Directors pursuant to which they resigned from the Board of Directors effective automatically on the third (3rd) day following written request to do so from OFI. Notwithstanding the fact that OFI has not yet requested Messrs. Singal and Menthe to resign from our Board of Directors, Messrs. Singal and Menthe did resign on March 3, 2018. Their resignations were not in connection with any known disagreement with the Company.

As promptly as possible following the first closing, we are also required to file a proxy statement and hold a special meeting of our stockholders to authorize and approve the issuance of shares of common stock upon conversion of the Series B Preferred Stock and the amendment to the certificate of designation for our Series A Convertible Preferred Stock described above. As of the date of this report, we have not yet filed such proxy statement.

In furtherance of obtaining such stockholder approval, on December 22, 2017, OFI entered into a shareholder voting support and confidentiality agreement, or the OFI Voting Agreement, with the Contributor and certain other significant stockholders of our company, including the Note Holders, pursuant to which the such stockholders agreed to vote their shares in favor of the transactions contemplated by the Purchase Agreement, including the issuance to OFI or its designees of common stock upon conversion of its Series B Preferred Stock equal to 20% or more of the common stock or 20% or more of the voting power outstanding before the issuance (which we refer to as the OFI 20% Proposal), and also agreed to certain transfer restrictions on the securities of our company owned by them. Under the OFI Voting Agreement, such stockholders may not transfer or otherwise dispose of any equity securities of our company until the earlier of: (i) the date of termination of the Purchase Agreement in accordance with its terms; (ii) the later of (a) the date that this registration statement becomes effective or (b) the first business day following approval of the OFI 20% Proposal by our stockholders, (iii) the mutual written consent of the parties to the OFI Voting Agreement, or (iv) December 31, 2018. Such transfer restrictions do not apply to the exercise of any option, warrant or other securities convertible or exchangeable for securities of our company, or following stockholder approval of the OFI 20% Proposal, to the following transfers: (i) if the stockholder is a corporation, partnership, limited liability company or other entity, any transfer to an affiliate if such transfer is not for value; or (ii) if the stockholder is an individual, transfers, (a) for nominal consideration or as a gift to any member of such stockholder’s immediate family (defined as the spouse, parents, lineal descendants, the spouse of any lineal descendant, and brothers and sisters) or a trust for the benefit of such stockholder or any member of such stockholder’s immediate family, (b) in connection with estate or tax planning, (c) to non-profit organizations qualified as charitable organizations under Section 501(c)(3) of the Internal Revenue Code of 1986, as amended, or (d) upon the death of such stockholder pursuant to a will or other instrument taking effect upon the death of such stockholder, or pursuant to the applicable laws of descent and distribution to such stockholder’s estate, heirs or distributes. The restrictions also do not apply to any transfer by the Contributor or the Contributor Parent, in each case, to any holder of a security issued by it. The OFI Voting Agreement also includes a power of attorney pursuant to which each stockholder designated and appointed our company and its duly authorized officers and agents as its agents and attorney in fact to act on the stockholder’s behalf to execute any proxy relating to any meeting of our stockholders for the purposes set forth in the OFI Voting Agreement.

10

As a condition to the first closing, we entered into a registration rights agreement, or the OFI Registration Rights Agreement, with OFI, pursuant to which we agreed to register all shares of common stock that may be issued upon conversion of the Series B Preferred Stock, or the Registrable Securities, under the Securities Act. We agreed to file a registration statement covering the resale of such Registrable Securities within 30 days of the first closing and cause such registration statement to be declared effective under the Securities Act as soon as possible but, in any event, no later than 120 days following the filing date if such registration statement is filed on Form S-3 or 150 days if such registration statement is filed on Form S-1. If such registration statement is not filed or declared effective by the SEC on or prior to such dates, or if after such registration statement is declared effective, without regard for the reason thereunder or efforts therefor, such registration statement ceases for any reason to be effective for more than an aggregate of 30 trading days during any 12-month period, which need not be consecutive, then in addition to any other rights the holders of Series B Preferred Stock may have under the OFI Registration Rights Agreement or under applicable law, we shall pay to each holder an amount in cash, as partial liquidated damages and not as a penalty, equal to 1.0% of the product obtained by multiplying (x) the Series B Original Issue Price by (y) the number of shares of Registrable Securities held by the holder (such product referred to herein as the Investment Amount); provided that, in no event will we be liable for liquidated damages in excess of 1.0% of the Investment Amount in any single month and that the maximum aggregate liquidated damages payable to the holders under the OFI Registration Rights Agreement shall be ten percent (10%) of the Investment Amount. On January 23, 2018, we filed a registration statement on Form S-3 to register the shares issued to OFI in the first closing. OFI waived its right to liquidated damages in connection with the late filing of such registration statement.

Under the Purchase Agreement, we also agreed to indemnify and hold OFI and its successors and permitted assignees (collectively referred to herein as the Investor Indemnified Parties) harmless from, any and all Damages (as defined below) incurred or suffered by such Investor Indemnified Party arising out of any inaccuracy or other breach of any representation or warranty of our company in any of the Transaction Documents (as defined in the Purchase Agreement) or any breach of covenant or agreement made by us in any of the Transaction Documents. “Damages” means the amount of (i) the sum of the aggregate amount of all damages, losses, liabilities and expenses (including reasonable expenses of investigation and reasonable attorneys’ fees and expenses) in connection with any action, suit or proceeding whether involving a third party claim or a claim solely between the parties, but excluding any incidental, indirect or consequential damages, losses, liabilities or expenses; (ii) multiplied by the Indemnity Gross Up Factor. The “Indemnity Gross Up Factor” is equal to X divided by Y, where X is equal to 1 and Y is equal to 1 minus a fraction, the numerator of which is equal to the number of shares of common stock held by OFI, determined and on a fully diluted basis assuming the full conversion of shares of Series B Preferred Stock that OFI is then entitled to convert; and the denominator of which is the number of shares of common stock determined on a fully diluted basis. Notwithstanding the foregoing, no Investor Indemnified Party shall be entitled to indemnification unless and until the aggregate Damages incurred in respect of all claims collectively exceeds $50,000 whereupon Investor Indemnified Parties shall only be entitled to indemnification for all such Damages in excess of such $50,000 threshold.

The Purchase Agreement may be terminated by the written agreement of us and OFI, or by us or OFI if the final closing does not take place prior to December 31, 2018.

Our Prior Business Operations

Under its previous name, PhotoMedex, Inc., our company was, until the recent sale of the last significant business unit (its consumer products division which was sold to ICTV Brands, Inc., or ICTV, on January 23, 2017; see Note 2, Discontinued Operations, to our consolidated financial statements), as described below and in other sections of this report, a Global Skin Health company providing integrated disease management and aesthetic solutions to dermatologists, professional aestheticians and consumers. We provided proprietary products and services that addressed skin diseases and conditions including psoriasis, acne, actinic keratosis (a precursor to certain types of skin cancer), photo damage and unwanted hair.

11

Before we commenced our current real estate business, we organized our business into three operating segments based upon our management structure, products and services offered, markets served and types of customers, as follows: The Consumer segment (sold to ICTV on January 23, 2017) derived its revenues from the design, development, manufacturing and selling of long-term hair reduction and acne consumer products. The Physician Recurring segment derived its revenues from the XTRAC (sold to MELA Sciences on June 22, 2015) procedures performed by dermatologists, the sales of skincare products (sold to Pharma Cosmetics on September 15, 2016), the sales of surgical disposables and accessories to hospitals and surgery centers (sold to Dalian JiKang Medical Systems September 1, 2015) and on the repair, maintenance and replacement parts on various products. The Professional segment generated revenues from the sale of equipment, such as lasers, medical and esthetic light and heat based products and LED products.

We still market and sell our LHE® brand products, which were included in our Professional segment, through our subsidiary, Radiancy, Inc., or Radiancy. We are in the process of liquidating the remaining legacy inventory and assets of this business line, after which time we will no longer operate this business.

The proprietary LHE® brand technology combines the benefits of direct heat and a full-spectrum light source for a variety of clinical applications, including psoriasis care, acne treatment, skin tightening, skin rejuvenation, wrinkle reduction, collagen renewal, vascular and pigmented lesion treatments and hair removal. This technology was originally used primarily in our professional products, including capital equipment sold to physicians and skin care specialists worldwide. The technology was then adapted to our hand-held consumer line of products like no!no! Skin, a medical device for acne. Except for occasional sale of left over inventory, this business segment has basically ceased operations with the NEOVA sale September 23, 2016.

Sale of Prior Business

On March 31, 2016, we completed the sale to The Lotus Global Group, Inc. of all of the tangible and intangible assets of the Omnilux product line for $220 thousand ($110 thousand was received as a refundable deposit during December 2015 in advance and $110 thousand was received in April 2016), pursuant to the Agreement for Sale of Assets dated March 31, 2016. Management does not believe that the sale of the Omnilux product line represented a strategic shift for our company. As a result, the above transaction has not been reflected in the accompanying consolidated financial statements as discontinued operations (see Note 2, Discontinued Operations, to our consolidated financial statements). We recorded a loss on the disposal of those assets in the amount of $843 thousand for the year ended December 31, 2016.

On August 30, 2016, we entered into an Asset Purchase Agreement for the sale of our Neova product line. The sale was completed on September 15, 2016, resulting in immediate cash proceeds to us of $1.5 million and we recorded a loss of $1,731 thousand from the transaction during the third quarter ended September 30, 2016, and for the year ended December 31, 2016. The parties entered into several ancillary agreements as part of this transaction, including a Neova Escrow Agreement and a Neova Transition Services Agreement. Under the Neova Escrow Agreement, $250 thousand of the Purchase Price was placed into an escrow account held by U.S. Bank National Association as Escrow Agent. The funds were to remain in escrow until September 15, 2017, one year following the closing of the transaction. We received $158 thousand of these on December 13, 2017 and recognized an additional loss of $92 thousand on the sales of the Neova product line for the amount of funds withheld from the escrow account.

On October 4, 2016, we entered into an Asset Purchase Agreement with ICTV for the sale of our consumer division for $9.5 million, including $5 million in cash plus a $4.5 million royalty agreement. We also entered into a Transition Services Agreement, pursuant to which we agreed to provide ICTV with certain accounting, benefit, payroll, regulatory, IT support and other services for periods ranging from approximately three months to up to one year following the closing date, during which time ICTV would arrange to transition the services it receives to its own personnel.

This transaction was completed on January 23, 2017, (see Note 2 Discontinued Operations). We considered a number of factors before entering into the Asset Purchase Agreement, including, among other things, the price to be paid by ICTV, the strategic and financial benefits that the asset sale would provide to us, our extensive search process with respect to the sale of the business, the future business prospects of the business and the terms and conditions of the Asset Purchase Agreement. Ultimately, we concluded that the price offered by ICTV was a fair offer for the consumer products division.

On July 12, 2017, we entered into a Termination and Release Agreement under which the Asset Purchase Agreement described above was terminated and is of no further force and effect, except for certain surviving rights, obligations and covenants described in the Termination and Release Agreement. Pursuant to the Termination and Release Agreement, ICTV paid us $2 million in cash and we agreed that ICTV will have no further royalty or other payment obligations under the Asset Purchase Agreement. We derecognized the $4.5 million royalty receivable (which had been recognized on January 23, 2017) and recognized a total loss of $2 million in the nine-month period ended September 30, 2017, resulting in an adjustment of $2 million to the amount of the loss on the disposal of the asset. We had classified the assets of the consumer division as assets held for sale as of December 31, 2016.

12

As partial consideration for the releases provided by ICTV pursuant to the Termination and Release Agreement and in accordance with the terms therein, on July 12, 2017, we entered into a Bill of Sale and Assignment, which provides that we shall sell, assign, transfer, convey and deliver to ICTV, and ICTV purchase and accept from us, all of the right, title and interest, legal or equitable, in and to a deposit in the amount of $210 thousand held by a consumer division vendor, Sigmatron International, Inc., pursuant to an arrangement between us and Sigmatron International, Inc.

As part of the sale of the consumer product line, which transaction was determined to represent a complete liquidation of a foreign subsidiary, the cumulative translation adjustment of $3,228 thousand related to that foreign entity was reclassified from accumulated other comprehensive income (loss) and reported as part of gain or loss from the sale.

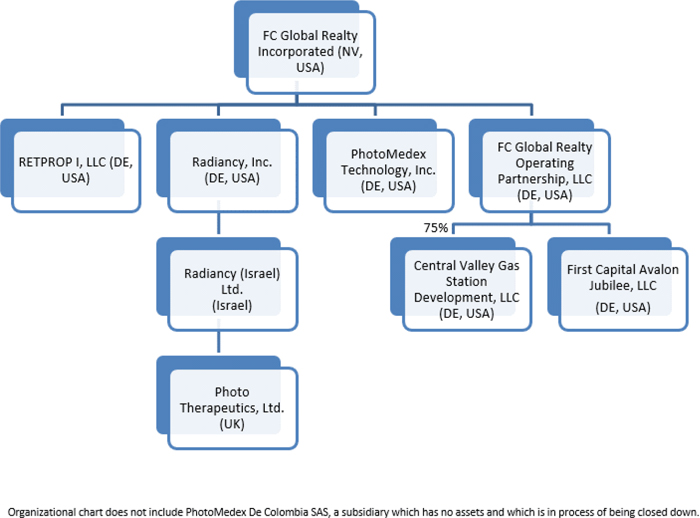

Organizational Chart

The following chart depicts our organizational structure following the sale of our prior business and the Contribution Transaction. All subsidiaries are wholly-owned unless otherwise indicated.

Our Real Estate Business

Our focus is to build our company into a leading real estate, asset management and development company, concentrating primarily on investments in high yield income producing assets and other opportunistic commercial properties via direct property ownership and asset management. Our objective is to generate long term net asset value growth while adhering to institutional best practices and a deep research process for all investments.

13

Income Producing Properties

For income producing properties, we intend to acquire assets that provide recurring income with the potential for income growth over the long-term. We believe there can be an attractive risk/reward profile to such properties based on the location and the underlying credit attributes of the tenants. In addition, we may invest in loans that are secured by income producing properties or ground leases on such properties. We believe that owning a diversified portfolio of actively managed properties and other real estate related investments can produce a consistent stream of income with long-term upside potential from income growth or redevelopment.

Real Estate Development

We look to invest in land assets that can be developed into income generating commercial, residential and hospitality properties, for-sale residential properties, or mixed-use development opportunities. Such properties may require extensive planning, and for these investments, we may partner with local developers, architects, and engineers to maximize the highest and best use. We focus on development properties where we believe the risk profile is misunderstood thus creating significant opportunity if we are able to turn the development into a stabilized operating property.

Competition

We believe the real estate business is very competitive. Our properties may compete with local sites in attracting skilled labor during the construction process and in attracting tenants and end-users upon completion. We compete with several types of real estate investors for acquisitions of properties, including real estate limited partnerships and private equity, REITs, developers, financial institutions, and individuals that own, manage, finance or develop properties. Many of these groups have larger operations and greater financial resources than we do.

We believe that our size and scale provide an opportunity to take advantage of smaller-tier assets that most traditional investors do not focus on due to size limitations, thus creating unique investment opportunities with attractive risk/reward profiles.

Investment Strategy

Our diversified investment strategy provides us with flexibility to invest across real estate asset classes and submarkets in the United States and globally. We will look to utilize our industry experience and relationships to identify the transactions which generate the most attractive risk / reward opportunities consistent with our strategy. We enforce a rigorous and repeatable underwriting process based on deep research and due diligence.

One of our core strategies is that we intend to find investments in secondary and tertiary markets with assets that require minimal capital expenditures but generate initial unlevered cash flow yields that are higher than those in primary markets. We look to acquire assets in submarkets where the population and employment trends are positive and where the underlying asset serves a key purpose to the local community.

A second component of our investment strategy will revolve around sourcing asset management opportunities for which we would operate as an asset manager of real estate properties. We are not currently structured as a REIT, thus we have the ability to retain earnings and to operate in real estate asset management, development and peripheral real estate activities, items that may be limited by REIT requirements. We will look to utilize our existing infrastructure to provide efficiencies of scale to owners of real estate assets as we grow our portfolio over time.

Our criteria for evaluating investments includes, but is not limited to, submarket location of the asset, economic and population growth fundamentals of the location, credit quality of the tenant, terms of the underlying leases, historical cash flow and capital expenditure needs at the property, ability to acquire financing secured by the property, tax and regulatory risks associated with the investment, environmental and structural attributes of the property, long-term viability of the asset, and potential redevelopment opportunities of the real estate.

We do extensive research on these investment attributes when preparing our investment memorandum. We compare the real estate acquisition we are making to other investments with similar risk profiles both inside and outside the direct real estate investment sector to best assess the merits of the opportunity.

14

Existing Portfolio

In 2017, we acquired (i) three vacant land sites intended for development as gas stations in northern California, (ii) a majority membership interest in a limited liability company that owns a vacant land site located in Northern California, and (iii) an interest in a limited liability company which owns property located in Los Lunas, New Mexico being developed as a single family residential development.

Our Intellectual Property

We do not have any material intellectual property rights relating to our real estate business. However, we do employ certain proprietary processes related to the real estate business which are protected as trade secrets of our company. We have not, at this time, registered any patents, trademarks or copyrights associated with our real estate business and do not expect to do so.

Our legacy global skin health business provided integrated disease management and aesthetic solutions to dermatologists, professional aestheticians and consumers. We protected our proprietary rights relating tour legacy business from unauthorized use by third parties to the extent that our proprietary rights were covered by valid and enforceable patents, trademarks, trade names or copyrights, or were effectively maintained as trade secrets.

Historically, our policy was to file patent applications and to protect certain technology, inventions and improvements that are commercially important to the development of our business. As patents expire and expose our inventions to public use, we sought to mitigate the impact of such expirations by seeking protection of improvements. We also relied on trade secrets, employee and third-party nondisclosure agreements and other protective measures to protect our intellectual property rights pertaining to our products and technology.

Our products and services were offered under trademarks and service marks, both registered and unregistered. We believe our trademarks encouraged customer loyalty and aided in the differentiation of our products from competitors’ products. In connection with the sales of our Neova product line and our consumer products division, we transferred the intellectual property associated with those product lines, including trademarks and trade names, to their respective purchasers. Accordingly, we had 20 trademarks, either registered or being registered, in markets around the world that we intend to maintain in support of our real estate business and our legacy capital equipment products. These include 9 trademarks issued in the U.S. and 11 trademarks issued in the rest of the world. We periodically reviewed the trademarks in our portfolio for usefulness with our then existing and anticipated product lines; as a result, certain trademarks which were no longer in use in our business were not renewed.

Research and Development

Our research and development expenditures relating to our legacy business operations were approximately $143 thousand in 2017 and $1.2 million in 2016. As of January 23, 2017, the research and development personnel were transferred to ICTV in connection with the closing of the sale of the consumer product line assets.

Government Regulation

Regulations Relating to Legacy Business

Regulations Relating to Products and Manufacturing

Our products are regulated by numerous governmental authorities, principally the U.S. Food and Drug Administration or the FDA and corresponding state and foreign regulatory agencies. Any medical device or cosmetic we distribute would be subject to pervasive and continuing regulation by the FDA. The U.S. Food, Drug and Cosmetics Act, and other federal and state laws and regulations govern the pre-clinical and clinical testing, design, manufacture, use, labeling and promotion of medical devices.

We have received approval from the European Union to affix the CE Mark to our LHE products. This certification is a mandatory conformity mark for products placed on the market in the European Economic Area, which is evidence that they meet all European Community, quality assurance standards and compliance with applicable European medical device directives for the production of medical devices. This will enable us to market our approved products in all of the member countries that accept the CE Mark. We also will be required to comply with additional individual national requirements that are in addition to those required by these nations. Our products have also met the requirements for marketing in various other countries.

15

Failure to comply with applicable regulatory requirements can result in fines, injunctions, civil penalties, recalls or seizures of products, total or partial suspensions of production, refusals by the U.S and foreign governments to permit product sales and criminal prosecution and could have a material adverse effect on our business, financial condition and results of operations.

Fraud and Abuse Laws

Because of the significant federal funding involved in Medicare and Medicaid, Congress and the states have enacted, and actively enforce, a number of laws whose purpose is to eliminate fraud and abuse in federal health care programs. Our business is subject to compliance with these laws.

Anti-Kickback Laws