Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - Steadfast Income REIT, Inc. | ex991cbreconsent12312017.htm |

| EX-32.2 - EXHIBIT 32.2 - Steadfast Income REIT, Inc. | ex322-sir12312017.htm |

| EX-32.1 - EXHIBIT 32.1 - Steadfast Income REIT, Inc. | ex321-sir12312017.htm |

| EX-31.2 - EXHIBIT 31.2 - Steadfast Income REIT, Inc. | ex312-sir12312017.htm |

| EX-31.1 - EXHIBIT 31.1 - Steadfast Income REIT, Inc. | ex311-sir12312017.htm |

| EX-23.1 - EXHIBIT 23.1 - Steadfast Income REIT, Inc. | ex231-sir12312017.htm |

| EX-21 - EXHIBIT 21 - Steadfast Income REIT, Inc. | ex21-sir12312017.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2017

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

Commission file number 000-54674

STEADFAST INCOME REIT, INC.

(Exact Name of Registrant as Specified in Its Charter)

Maryland | 27-0351641 | |

(State or Other Jurisdiction of | (I.R.S. Employer | |

Incorporation or Organization) | Identification No.) | |

18100 Von Karman Avenue, Suite 500 | ||

Irvine, California | 92612 | |

(Address of Principal Executive Offices) | (Zip Code) | |

(949) 852-0700

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.01 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | o | Accelerated filer | o | Non-accelerated filer | þ (Do not check if a smaller reporting company) | ||

Smaller reporting company | o | Emerging growth company | o | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

There is no established market for the registrant’s shares of common stock. There were approximately 74,757,916 shares of common stock held by non-affiliates at June 30, 2017, the last business day of the registrant’s most recently completed second fiscal quarter, for an aggregate market value of $870,929,726, assuming an estimated value per share of $11.65 per share.

As of March 20, 2018, there were 75,298,154 shares of the Registrant’s common stock issued and outstanding.

STEADFAST INCOME REIT, INC.

INDEX

Page | ||

Cautionary Note Regarding Forward-Looking Statements | ||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements of Steadfast Income REIT, Inc. (“we,” “our,” “us” or the “Company”) included in this annual report on Form 10-K that are not historical facts (including any statements concerning investment objectives, other plans and objectives of management for future operations or economic performance, or assumptions or forecasts related thereto) are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements are only predictions. We caution that forward-looking statements are not guarantees. Actual events or our investments and results of operations could differ materially from those expressed or implied in any forward-looking statements. Forward-looking statements are typically identified by the use of terms such as “may,” “should,” “expect,” “could,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “continue,” “predict,” “potential” or the negative of such terms and other comparable terminology.

The forward-looking statements included herein are based upon our current expectations, plans, estimates, assumptions and beliefs that involve numerous risks and uncertainties. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements. Factors that could have a material adverse effect on our operations and future prospects include, but are not limited to:

• | changes in economic conditions generally and the real estate and debt markets specifically; |

• | our ability to secure resident leases at favorable rental rates; |

• | our ability to execute on our value-enhancement strategy; |

• | risks inherent in the real estate business, including tenant defaults, potential liability relating to environmental matters and the lack of liquidity of real estate investments; |

• | risks related to owning investments with joint venture partners; |

• | our ability to identify and acquire multifamily properties; |

• | changes to our share repurchase program, distribution rate and other decisions; |

• | the fact we pay fees and expenses to our advisor and its affiliates that were not negotiated on an arm’s length basis and the fact that the payment of these fees and expenses increases the risk that our stockholders will not earn a profit on their investment in us; |

• | our ability to retain our executive officers and other key personnel of our advisor, our property manager and our affiliates; |

• | legislative or regulatory changes (including changes to the laws governing the taxation of real estate investment trusts, or REITs); |

• | our ability to generate sufficient cash flows to pay distributions to our stockholders; |

• | the availability of capital; |

• | changes in interest rates; and |

• | changes to U.S. generally accepted accounting principles, or GAAP. |

Any of the assumptions underlying forward-looking statements could be inaccurate. You are cautioned not to place undue reliance on any forward-looking statements included in this annual report. All forward-looking statements are made as of the date of this annual report and the risk that actual results will differ materially from the expectations expressed in this annual report will increase with the passage of time. Except as otherwise required by the federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements after the date of this annual report, whether as a result of new information, future events, changed circumstances or any other reason. In light of the significant uncertainties inherent in the forward-looking statements included in this annual report, including, without limitation, the risks described under “Risk Factors,” the inclusion of such forward-looking statements should not be regarded as a representation by us or any other person that the objectives and plans set forth in this annual report will be achieved.

i

PART I

ITEM 1. | BUSINESS |

Overview

Steadfast Income REIT, Inc. (which is referred to in this annual report, as the context requires, as the “Company,” “we,” “us” or “our”) was formed on May 4, 2009, as a Maryland corporation that has elected to be treated as, and currently qualifies as, a real estate investment trust, or REIT. We have invested in and manage a diverse portfolio of real estate investments, primarily in the multifamily sector, located throughout the United States. Substantially all of our business is conducted through Steadfast Income REIT Operating Partnership, L.P., a Delaware limited partnership formed on July 6, 2009, which we refer to as our “operating partnership.” We are the sole general partner of our operating partnership. As of December 31, 2017, we owned 48 multifamily properties comprised of a total of 12,156 apartment homes, an additional 21,130 square feet of rentable commercial space at two properties and a 10% interest in one unconsolidated joint venture that owns 12 multifamily properties comprised of a total of 3,301 apartment homes. For more information on our real estate portfolio, see “—Our Real Estate Portfolio” below.

On July 19, 2010, we commenced our initial public offering of up to 150,000,000 shares of common stock and up to 15,789,474 shares of common stock pursuant to our distribution reinvestment plan. Upon termination of our initial public offering on December 20, 2013, we had sold 73,608,337 shares of common stock for gross offering proceeds of $745,389,748, including 1,588,289 shares of common stock issued pursuant to our distribution reinvestment plan for gross offering proceeds of $15,397,232. Following the termination of our initial public offering, we continued to offer shares of our common stock pursuant to our distribution reinvestment plan until our board of directors determined to suspend our distribution reinvestment plan, effective December 1, 2014. On March 10, 2015, our board of directors determined an estimated value per share of our common stock of $10.35 as of December 31, 2014. On February 25, 2016, our board of directors determined an estimated value per share of our common stock of $11.44 as of December 31, 2015. On February 15, 2017, our board of directors determined an estimated value per share of our common stock of $11.65 as of December 31, 2016. On March 13, 2018, our board of directors determined an estimated value per share of our common stock of $10.84 as of December 31, 2017. See Item 5. “Market for Registrant’s Common Equity, Related Stockholder Matters and Purchase of Equity Securities—Market Information—Estimated Value Per Share” for further information regarding the estimated value per share.

Prior to the commencement of our public offering, we sold shares of our common stock in a private offering exempt from the registration requirements of the Securities Act of 1933, as amended, or the Securities Act. Upon termination of the private offering, we had sold 637,279 shares of common stock at $9.40 per share (subject to certain discounts) for net offering proceeds of $5,844,325.

We are externally managed by Steadfast Income Advisor, LLC, which we refer to as our “advisor,” pursuant to the Advisory Agreement, as amended, or the advisory agreement, by and among us, our operating partnership and our advisor. Subject to certain restrictions and limitations, our advisor manages our day-to-day operations and our portfolio of properties and real estate-related assets. Our advisor sources and presents investment opportunities to our board of directors and provides investment management services on our behalf. We retained our affiliate Steadfast Capital Markets Group, LLC, which we refer to as our “dealer manager,” to serve as the dealer manager for our initial public offering. Effective December 27, 2017, our dealer manager changed its name from “Steadfast Capital Markets Group, LLC” to “Stira Capital Markets Group, LLC.” The dealer manager was responsible for marketing our shares of common stock being offered pursuant to our initial public offering. The advisor, along with the dealer manager, also provides marketing, investor relations and other administrative services on our behalf.

1

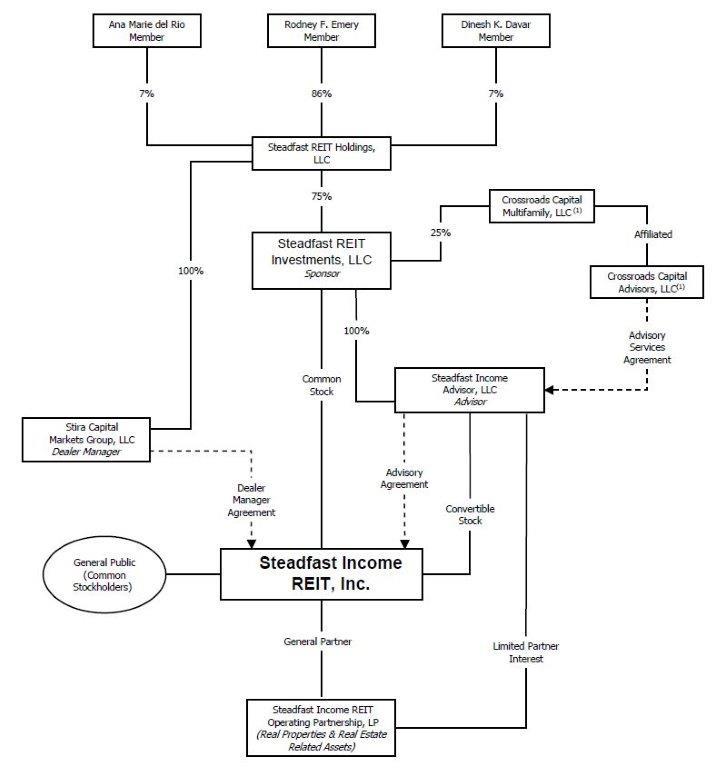

Our Structure

The chart below shows the relationships among our company and various affiliates.

2

______________

(1) Crossroads Capital Multifamily, LLC, or Crossroads Capital Multifamily, and Crossroads Capital Advisors, LLC, or Crossroads Capital Advisors, are affiliated entities, each being wholly-owned subsidiaries of Crossroads Capital Group, LLC.

Objectives and Strategies

Our primary investment objectives are to:

• | preserve, protect and return invested capital; |

• | pay attractive and stable cash distributions to stockholders; and |

• | realize capital appreciation in the value of our investments over the long term. |

We intend to use the cash flows from our operations to continue to invest in our real estate investments located throughout the United States. We have acquired, and actively manage, stabilized and income-producing properties with the objective of providing a stable and secure source of income for our stockholders and maximizing potential returns upon disposition of our assets through capital appreciation. We may make these investments directly or through joint ventures, in each case provided that the underlying real estate or real estate-related asset generally meets our criteria for direct investment.

2017 Highlights

During 2017, we:

• | invested $16,401,961 in improvements to our real estate assets; |

• | paid cash distributions of $54,369,877, which constituted a 7.0% annualized distribution rate to our stockholders based on a purchase price of $10.24 per share; |

• | generated cash flows from operations of $47,078,463; |

• | generated net operating income of $110,547,074; |

• | generated funds from operations, or FFO, of $44,485,775 (for further information on how we calculate FFO and a reconciliation of FFO to net income (loss), please refer to Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Funds From Operations and Modified Funds From Operations”); |

• | generated modified funds from operations, or MFFO, of $47,472,598 (for further information on how we calculate MFFO and a reconciliation of MFFO to net income (loss), please refer to Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Funds From Operations and Modified Funds From Operations”); |

• | disposed of 17 multifamily properties, including the contribution of 12 properties to the joint venture discussed below, for a gross sales price of $460,580,000, exclusive of closing costs for a gain on sales of real estate of $96,573,171; |

• | entered into a joint venture arrangement with Blackstone Real Estate Income Trust, Inc., or BX REIT, whereby we agreed to contribute a portfolio of 20 multifamily properties to BREIT Steadfast MF JV LP, or the joint venture, in exchange for cash and a 10% ownership interest in the joint venture. BX REIT, through its subsidiaries, owns a 90% interest in the joint venture and serves as the general partner of the joint venture. For more information on our joint venture with BX REIT, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Joint Venture Arrangement with Blackstone Real Estate Income Trust, Inc.”; and |

• | generated net income of $72,473,867. |

3

Plan of Liquidation

Pursuant to our Third Articles of Amendment and Restatement, or the charter, our board of directors is required to annually consider a resolution declaring that a proposed liquidation of us is advisable on substantially the terms and conditions set forth in the resolution, or the Plan of Liquidation, and direct that the proposed Plan of Liquidation be submitted for consideration at either an annual or special meeting of the stockholders. The adoption of a Plan of Liquidation and the submission to the stockholders may be postponed if a majority of directors, including a majority of independent directors, determine that a liquidation is not then in the best interest of the stockholders. On March 13, 2018, our board of directors, including a majority of the independent directors, determined that a liquidation is not in the best interests of the stockholders at this time, and, therefore, to postpone presenting a liquidation decision to stockholders. In accordance with our charter, the board of directors will reconsider whether to seek stockholder approval of our liquidation at least annually. The board of directors, pursuant to its fiduciary duties, continuously evaluates our long-term and short-term opportunities.

4

Our Real Estate Portfolio

As of December 31, 2017, we owned the 48 multifamily properties described below.

Property Name | Location | Number of Units | Average Monthly Occupancy(1) | Average Monthly Rent(2) | Purchase Date | Contract Purchase Price(3) | Mortgage Debt Outstanding | ||||||||||||||||

1 | Clarion Park Apartments(4) | Olathe, KS | 220 | 89.5 | % | $ | 832 | 6/28/2011 | $ | 11,215,000 | $ | 7,971,245 | |||||||||||

2 | Truman Farm Villas(5) | Grandview, MO | 200 | 99.0 | % | 743 | 12/22/2011 | 9,100,000 | 5,350,567 | ||||||||||||||

3 | EBT Lofts | Kansas City, MO | 102 | 89.2 | % | 1,064 | 12/30/2011 | 8,575,000 | 5,060,029 | ||||||||||||||

4 | Renaissance St. Andrews | Louisville, KY | 216 | 94.9 | % | 748 | 2/17/2012 | 12,500,000 | 8,357,513 | ||||||||||||||

5 | Spring Creek of Edmond | Edmond, OK | 252 | 93.3 | % | 844 | 3/9/2012 | 19,350,000 | 17,069,537 | ||||||||||||||

6 | Montclair Parc Apartments | Oklahoma City, OK | 360 | 94.7 | % | 849 | 4/26/2012 | 35,750,000 | 22,255,805 | ||||||||||||||

7 | Sonoma Grande Apartments | Tulsa, OK | 336 | 92.6 | % | 902 | 5/24/2012 | 32,200,000 | 20,920,589 | ||||||||||||||

8 | Estancia Apartments | Tulsa, OK | 294 | 94.9 | % | 919 | 6/29/2012 | 27,900,000 | 20,500,000 | ||||||||||||||

9 | Valley Farms Apartment Homes | Louisville, KY | 160 | 96.9 | % | 914 | 8/30/2012 | 15,100,000 | 9,421,511 | ||||||||||||||

10 | Hilliard Park Apartments | Columbus, OH | 201 | 93.0 | % | 1,030 | 9/11/2012 | 19,800,000 | 12,668,570 | ||||||||||||||

11 | Sycamore Terrace Apartments | Terre Haute, IN | 250 | 93.2 | % | 1,107 | 9/20/2012 & 3/5/2014 | 23,174,157 | 17,821,492 | ||||||||||||||

12 | Hilliard Summit Apartments | Columbus, OH | 208 | 94.7 | % | 1,191 | 9/28/2012 | 24,100,000 | 15,375,368 | ||||||||||||||

13 | Springmarc Apartments | San Marcos, TX | 240 | 92.9 | % | 1,098 | 10/19/2012 | 21,850,000 | 14,200,991 | ||||||||||||||

14 | Renaissance at St. Andrews Condominiums(6) | Louisville, KY | 30 | 96.7 | % | 750 | 10/31/2012 | 1,423,000 | — | ||||||||||||||

15 | Arrowhead Apartment Homes | Palatine, IL | 200 | 93.5 | % | 1,021 | 11/30/2012 | 16,750,000 | 11,527,640 | ||||||||||||||

16 | The Moorings Apartments | Roselle, IL | 216 | 94.4 | % | 1,144 | 11/30/2012 | 20,250,000 | 13,934,462 | ||||||||||||||

17 | Forty-57 Apartments | Lexington, KY | 436 | 95.0 | % | 923 | 12/20/2012 | 52,500,000 | 36,312,924 | ||||||||||||||

18 | Keystone Farms Apartments | Nashville, TN | 90 | 95.6 | % | 1,243 | 12/28/2012 | 8,400,000 | 5,723,070 | ||||||||||||||

19 | Riverford Crossing Apartments | Frankfort, KY | 300 | 95.0 | % | 903 | 12/28/2012 | 30,000,000 | 20,647,194 | ||||||||||||||

20 | Valley Farms North | Louisville, KY | 128 | 92.2 | % | 1,058 | 12/28/2012 | 14,607,032 | 9,469,959 | ||||||||||||||

21 | Montecito Apartments | Austin, TX | 268 | 90.7 | % | 981 | 12/31/2012 | 19,000,000 | 13,116,770 | ||||||||||||||

22 | Hilliard Grand Apartments | Dublin, OH | 314 | 94.6 | % | 1,240 | 12/31/2012 | 40,500,000 | 28,758,708 | ||||||||||||||

23 | The Hills at Fair Oaks | Fair Oaks Ranch, TX | 288 | 93.1 | % | 1,029 | 1/31/2013 | 34,560,000 | 23,441,688 | ||||||||||||||

24 | Library Lofts East(7) | Kansas City, MO | 118 | 87.3 | % | 1,059 | 2/28/2013 | 12,750,000 | 8,345,925 | ||||||||||||||

25 | Deep Deuce at Bricktown(8) | Oklahoma City, OK | 294 | 91.5 | % | 1,157 | 3/28/2013 | 38,271,000 | 24,260,315 | ||||||||||||||

5

Property Name | Location | Number of Units | Average Monthly Occupancy(1) | Average Monthly Rent(2) | Purchase Date | Contract Purchase Price(3) | Mortgage Debt Outstanding | ||||||||||||||||

26 | Retreat at Quail North | Oklahoma City, OK | 240 | 94.6 | % | $ | 942 | 6/12/2013 | $ | 25,250,000 | $ | 16,480,903 | |||||||||||

27 | Lodge at Trails Edge | Indianapolis, IN | 268 | 95.1 | % | 759 | 6/18/2013 | 18,400,000 | 11,798,975 | ||||||||||||||

28 | Arbors at Carrollton | Carrollton, TX | 131 | 94.7 | % | 987 | 7/3/2013 | 8,800,000 | 5,843,116 | ||||||||||||||

29 | Waterford on the Meadow | Plano, TX | 350 | 94.3 | % | 1,028 | 7/3/2013 | 23,100,000 | 15,520,062 | ||||||||||||||

30 | Tapestry Park Apartments | Birmingham, AL | 354 | 93.2 | % | 1,291 | 8/13/2013 & 12/1/2014 | 50,285,000 | 43,655,146 | ||||||||||||||

31 | Dawntree Apartments | Carrollton, TX | 400 | 93.0 | % | 990 | 8/15/2013 | 24,000,000 | 14,800,655 | ||||||||||||||

32 | Stuart Hall Lofts(9) | Kansas City, MO | 115 | 90.4 | % | 1,282 | 8/27/2013 | 16,850,000 | 16,008,257 | ||||||||||||||

33 | BriceGrove Park Apartments | Canal Winchester, OH | 240 | 93.8 | % | 868 | 8/29/2013 | 20,100,000 | 17,103,335 | ||||||||||||||

34 | Retreat at Hamburg Place | Lexington, KY | 150 | 92.7 | % | 1,011 | 9/5/2013 | 16,300,000 | 12,052,239 | ||||||||||||||

35 | Heights at 2121 | Houston, TX | 504 | 94.0 | % | 896 | 9/30/2013 | 37,000,000 | 38,272,259 | ||||||||||||||

36 | Villas at Huffmeister | Houston, TX | 294 | 92.9 | % | 1,149 | 10/10/2013 | 37,600,000 | 27,184,269 | ||||||||||||||

37 | Villas at Kingwood | Kingwood, TX | 330 | 96.7 | % | 1,240 | 10/10/2013 | 40,150,000 | 35,325,595 | ||||||||||||||

38 | Waterford Place at Riata Ranch | Cypress, TX | 228 | 92.5 | % | 1,075 | 10/10/2013 | 23,400,000 | 17,285,905 | ||||||||||||||

39 | Carrington Place | Houston, TX | 324 | 93.2 | % | 1,077 | 11/7/2013 | 32,900,000 | 27,323,636 | ||||||||||||||

40 | Carrington at Champion Forest | Houston, TX | 284 | 97.2 | % | 1,091 | 11/7/2013 | 33,000,000 | 24,920,866 | ||||||||||||||

41 | Carrington Park at Huffmeister | Cypress, TX | 232 | 94.0 | % | 1,157 | 11/7/2013 | 25,150,000 | 20,256,062 | ||||||||||||||

42 | Willow Crossing Apartments | Elk Grove, IL | 579 | 90.2 | % | 1,159 | 11/20/2013 | 58,000,000 | 57,665,058 | ||||||||||||||

43 | Echo at Katy Ranch | Katy, TX | 260 | 96.5 | % | 1,354 | 12/19/2013 | 35,100,000 | — | ||||||||||||||

44 | Heritage Grand at Sienna Plantation | Missouri City, TX | 240 | 94.2 | % | 1,151 | 12/20/2013 | 27,000,000 | 17,038,807 | ||||||||||||||

45 | Mallard Crossing | Loveland, OH | 350 | 95.4 | % | 1,073 | 12/27/2013 | 39,800,000 | 33,534,900 | ||||||||||||||

46 | Reserve at Creekside | Chattanooga, TN | 192 | 90.6 | % | 950 | 3/28/2014 | 18,875,000 | 14,217,203 | ||||||||||||||

47 | Mapleshade Park | Dallas, TX | 148 | 95.3 | % | 1,648 | 3/31/2014 | 23,325,000 | 19,265,284 | ||||||||||||||

48 | Oak Crossing | Fort Wayne, IN | 222 | 96.8 | % | 987 | 6/3/2014 | 24,230,000 | 17,721,534 | ||||||||||||||

12,156 | 93.8 | % | $ | 1,037 | $ | 1,208,240,189 | $ | 875,785,938 | |||||||||||||||

________________

(1) | At December 31, 2017, our portfolio was approximately 95.4% leased. As of December 31, 2017, no single tenant accounted for greater than 10% of our 2017 gross annualized rental revenues. |

(2) | Average monthly rent is based upon the effective rental income after considering the effect of vacancies, concessions and write-offs. |

6

(3) | The contract purchase price is comprised of the purchase price upon acquisition and the development and construction costs of apartment homes we constructed, as applicable. |

(4) | 100% of the units are required to be rented to tenants earning no more than 60% of the median income in the local area. |

(5) | Approximately 74% of the units are required to be rented to tenants earning no more than 60% of the median income in the local area. |

(6) | Renaissance at St. Andrews Condominiums, initially comprised of 29 apartment homes, was acquired by us on October 31, 2012. On May 20, 2016, we acquired one additional unit at the Renaissance at St. Andrews Condominiums for a purchase price of $48,000. |

(7) | Library Lofts East contains 16,680 rentable square feet of commercial space. As of December 31, 2017, the commercial space, which represents approximately 14.1% of the rentable square feet of Library Lofts East, was 100% occupied by two tenants. The lease terms of the two tenants occupying the commercial space expire between 2019 and 2025. The tenants pay an average annual rent of $192,998, or approximately $11.57 per square foot. |

(8) | Deep Deuce at Bricktown, comprised of 294 apartment homes, was acquired by us on March 28, 2013. On June 12, 2017, we acquired a land parcel adjacent to Deep Deuce at Bricktown for a purchase price of $51,000. |

(9) | Stuart Hall Lofts contains 4,450 rentable square feet of commercial space. As of December 31, 2017, the commercial space, which represents approximately 3.1% of the rentable square feet of Stuart Hall Lofts, was 100% occupied by one tenant. The lease term of the tenant occupying the commercial space expires in 2019. The tenant pays an average annual rent of $64,863, or approximately $14.58 per square foot. |

At December 31, 2017, our portfolio was approximately 93.8% occupied and the average monthly rent per leased multifamily home in our portfolio was $1,037. The weighted-average remaining lease term of our portfolio is less than one year. The weighted-average remaining lease term of our commercial office space leases is 2.66 years.

The following information generally applies to all of our properties:

• | we believe all of our properties are adequately covered by insurance and are suitable for their intended purposes; |

• | we have no plans for any material renovations, improvements or developments with respect to any of our properties; and |

• | our properties face competition in attracting new residents and retaining current residents from other multifamily properties in and around their respective submarkets. |

Joint Venture

As of December 31, 2017, we also owned a 10% interest in one unconsolidated joint venture that owns 12 multifamily properties comprised of a total of 3,301 apartment homes.

Debt Policy

We have used, and intend to use in the future, secured and unsecured debt. We believe that the careful use of borrowings will help us achieve our diversification goals and potentially enhance the returns on our investments. At December 31, 2017, our debt was approximately 58% of the value of our properties, as determined by the most recent valuations performed by an independent third-party appraiser as of December 31, 2017. We expect that our borrowings will be approximately 65% of the value of our properties. Under our charter we are prohibited from borrowing in excess of 300% of our net assets, which generally approximates to 75% of the aggregate cost of our assets. We may borrow in excess of this amount if such excess is approved by a majority of our independent directors and disclosed to stockholders in our next quarterly report, along with a justification for such excess. In such event, we will monitor our debt levels and take action to reduce any such excess as practicable. Our aggregate borrowings are reviewed by our board of directors at least quarterly. As of December 31, 2017, our aggregate borrowings were not in excess of 300% of the value of our net assets.

7

Employees

We have no paid employees. The employees of our advisor or its affiliates provide management, acquisition, advisory and certain administrative services for us.

Competition

We are subject to significant competition in seeking real estate investments and residents. We compete with many third parties engaged in real estate investment activities, including other REITs, specialty finance companies, savings and loan associations, banks, mortgage bankers, insurance companies, mutual funds, institutional investors, investment banking firms, lenders, hedge funds, governmental bodies and other entities. Many of our competitors have substantially greater financial and other resources than we have and may have substantially more operating experience than us. They also may enjoy significant competitive advantages that result from, among other things, a lower cost of capital.

We may also compete with Steadfast Apartment REIT, Inc., or Steadfast Apartment REIT, and Steadfast Apartment REIT III, Inc., or Steadfast Apartment REIT III, non-traded REITs sponsored by our sponsor that commenced their ongoing initial public offerings in December 2013 and February 2016, respectively, and have similar investment strategies as us. However, we expect any competition with Steadfast Apartment REIT or Steadfast Apartment REIT III for property acquisitions to be limited as our initial public offering terminated on December 20, 2013, and we have deployed all of the net offering proceeds raised in our initial public offering. Additionally, Steadfast Apartment REIT terminated its initial public offering on March 24, 2016, and has deployed all of its net offering proceeds raised in its initial public offering. However, we may compete with Steadfast Apartment REIT to the extent it raises additional capital or deploys proceeds from asset dispositions.

The multifamily property market in particular is highly competitive. This competition could reduce occupancy levels and revenues at our multifamily properties, which would adversely affect our operations. We face competition from many sources, including from other multifamily properties both in the immediate vicinity and the geographic market where our multifamily properties are and will be located. In addition, overbuilding of multifamily properties may occur, which would increase the number of multifamily homes available and may decrease occupancy and unit rental rates. Furthermore, multifamily properties we acquire most likely compete, or will compete, with numerous housing alternatives in attracting residents, including owner occupied single- and multifamily homes available to rent or purchase. Competitive housing in a particular area and the increasing affordability of owner occupied single- and multifamily homes available to rent or buy could adversely affect our ability to retain our residents, lease apartment homes and increase or maintain rental rates.

Regulations

Our investments are subject to various federal, state, and local laws, ordinances, and regulations, including, among other things, zoning regulations, land use controls, environmental controls relating to air and water quality, noise pollution, and indirect environmental impacts such as increased motor vehicle activity. We believe that we have all permits and approvals necessary under current law to operate our investments.

Income Taxes

We have elected to be taxed as, and currently qualify as, a REIT under the Internal Revenue Code of 1986, as amended, or the Internal Revenue Code, and have operated as such beginning with the taxable year ended December 31, 2010. To continue to qualify as a REIT, we must meet certain organizational and operational requirements, including a requirement to distribute at least 90% of our annual REIT taxable income to stockholders (which is computed without regard to the dividends paid deduction or net capital gain and which does not necessarily equal net income as calculated in accordance with GAAP). As a REIT, we generally will not be subject to federal income tax to the extent we distribute qualifying dividends to our stockholders. If we fail to qualify as a REIT in any taxable year, we would be subject to federal income tax on our taxable income at regular corporate income tax rates and generally would not be permitted to qualify for treatment as a REIT for federal income tax purposes for the four taxable years following the year during which qualification is lost, unless the Internal Revenue Service grants us relief under certain statutory provisions.

8

Financial Information About Industry Segments

Our current business consists of owning, managing, operating, leasing, acquiring, developing, investing in, and disposing of real estate assets. We internally evaluate all of our real estate assets as one industry segment, and, accordingly, we do not report segment information.

Available Information

We are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and, as a result, file periodic reports, proxy statements and other information with the Securities and Exchange Commission, or the SEC. Access to copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements and other filings with the SEC, including amendments to such filings, may be obtained free of charge from our website, http://www.steadfastreits.com. These filings are available promptly after we file them with, or furnish them to, the SEC. We are not incorporating our website or any information from the website into this annual report. The SEC also maintains a website, http://www.sec.gov, that contains our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Report on Form 8-K, proxy statements and other filings with the SEC. Access to these filings is free of charge.

ITEM 1A. | RISK FACTORS |

The following are some of the risks and uncertainties that could cause our actual results to differ materially from those presented in our forward-looking statements. The risks and uncertainties described below are not the only ones we face but do represent those risks and uncertainties that we believe are material to us. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also harm our business. References to “shares” and “our common stock” refer to the shares of common stock of Steadfast Income REIT, Inc.

General Investment Risks

From inception through December 31, 2017, we have experienced annual net losses and may experience similar losses in the future.

From inception through December 31, 2017, we incurred a net loss of $76,524,809. We cannot assure you that we will be profitable in the future or that we will recognize growth in the value of our assets.

There is no public trading market for shares of our common stock and we are not required to effectuate a liquidity event by a certain date. As a result, it will be difficult for you to sell your shares of common stock and, if you are able to sell your shares, you are likely to sell them at a substantial discount.

There is no current public market for the shares of our common stock and we have no obligation to list our shares on any public securities market or provide any other type of liquidity to our stockholders by a particular date. It may therefore be difficult for you to sell your shares of common stock. Even if you are able to sell your shares of common stock, the absence of a public market may cause the price received for any shares of our common stock sold to be less than what you paid or less than your proportionate value of the assets we own. We initially adopted a share repurchase program that allowed stockholders to sell to us their shares of common stock, subject to certain limitations. However, our share repurchase program was suspended effective November 20, 2014. We subsequently reinstated our share repurchase program effective July 1, 2015, subject to certain limitations on the amount of shares we will repurchase quarterly. Our board of directors may again in the future, amend, suspend, or terminate our share repurchase program upon 30 days’ notice. Additionally, our charter does not require that we consummate a transaction to provide liquidity to stockholders on any date certain. As a result, you must be prepared to hold your shares for an indefinite period of time.

9

We have paid a significant portion of our distributions to date from the proceeds of our public offering and cannot guarantee in the future that we will pay distributions solely from cash flow from operations. To the extent that we pay distributions from sources other than our cash flow from operations, we will have less funds available for investments, the overall returns to our stockholders may be reduced and subsequent stockholders will experience dilution.

Our organizational documents permit us to pay distributions from any source, including offering proceeds or borrowings (both of which may constitute a return of capital). From inception through December 31, 2017, 14.4% of distributions were funded from offering proceeds from our public offering, 78.6% of distributions were funded from cash flow from operations and 7.0% were funded from other sources. Of the $54,369,877 in total distributions we paid during the year ended December 31, 2017, 16.1% of such amounts were funded from sources other than cash flow from operations. To the extent we had funded distributions from the net proceeds of our public offering, we had less funds available for investment in real properties and real estate-related assets than if our distributions came solely from cash flow from operations, the overall returns to our stockholders may be reduced and subsequent investors will experience dilution. There is no limit on the amount of distributions we may fund from sources other than from cash flows from operations.

If the aggregate amount of cash we distribute to stockholders in any given year exceeds the amount of our earnings and profits generated during the year, the excess amount will either be (1) a return of capital or (2) a gain from the sale or exchange of property to the extent that a stockholder’s basis in our common stock equals or is reduced to zero as the result of our current or prior year distributions.

We face risks associated with the acquisition and value-enhancement of properties.

We may continue to acquire and renovate existing properties (which we refer to as “value-enhancement projects”). These activities are subject to various risks. We may not be successful in pursuing value-enhancement project opportunities. In addition, completed value-enhancement projects may not perform as well as expected. We are subject to other risks in connection with any acquisition and value-enhancement activities, including the following:

• | costs of a project may be higher than projected, potentially making the project unfeasible or unprofitable; |

• | we may not have funds available or be able to obtain financing for our value-enhancement projects on favorable terms, if at all; and |

• | occupancy rates and rents may not meet our projections and that project may not be profitable. |

If a value-enhancement project is unsuccessful, either because it is not meeting our expectations when operational or was not completed according to the value-enhancement project planning, the value of our investment in the project may decrease.

Disruptions in the financial markets and deteriorating economic conditions could adversely impact our ability to implement our investment strategy and achieve our investment objectives.

U.S. and global financial markets experienced extreme volatility and disruption from 2008 to 2010. There was a widespread tightening in overall credit markets, devaluation of the assets underlying certain financial contracts and increased borrowing by governmental entities. This turmoil in the capital markets resulted in constrained equity and debt capital available for investment in the real estate market, resulting in fewer buyers seeking to acquire real properties, increases in capitalization rates and lower property values. During the subsequent economic recovery, capital has been more available and the overall economy improved. However, the failure of a sustained economic recovery or future disruptions in the financial markets and deteriorating economic conditions could impact the value of our investments in properties. In addition, if potential purchasers of real properties have difficulty obtaining capital to finance property acquisitions, capitalization rates could increase and property values could decrease. Current economic conditions greatly increase the risks of our investments. See “—Risks Related to Investments in Real Estate.”

Financial regulatory reforms could have a significant impact on our business, financial condition and results of operations.

On July 21, 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act, or the Dodd-Frank Act, was signed into law. The Dodd-Frank Act represents a significant change in the American financial regulatory environment and impacts nearly every aspect of the U.S. financial services industry. The Dodd-Frank Act requires various federal agencies to adopt hundreds of new rules to implement the Dodd-Frank Act and to deliver to Congress numerous studies and reports that may

10

influence future legislation. The Dodd-Frank Act leaves significant discretion to federal agencies as to exactly how to implement the broad provisions of the Dodd-Frank Act. Some provisions of the Dodd-Frank Act have not been completely implemented and future implementation is uncertain in light of the transition of power in the U.S. federal government following the 2016 election. The changes resulting from the Dodd-Frank Act may impact the profitability of business activities, require changes to certain business practices, impose more stringent capital, liquidity and leverage requirements or otherwise adversely affect our business.

The geographic concentration of our portfolio may make us particularly susceptible to adverse economic developments in the real estate markets of those areas.

In addition to general, regional and national economic conditions, our operating results are impacted by the economic conditions of the specific markets in which we have concentrations of properties. As of December 31, 2017, of our $1,208,240,189 of real estate assets, 24.1% were located in the Houston metropolitan area. Any adverse economic or real estate developments in this market, such as business layoffs or downsizing, industry slowdowns, relocations of businesses, changing demographics and other factors, or any decrease in demand for multifamily property space resulting from the local business climate, could adversely affect our property revenue, and hence net operating income.

Non-traded REITs have been the subject of increased scrutiny by regulators and media outlets resulting from inquiries and investigations initiated by the Financial Industry Regulatory Authority, Inc., or FINRA, and the SEC. We could also become the subject of scrutiny and may face difficulties in raising capital in the future should negative perceptions develop regarding non-traded REITs. If we become the subject of scrutiny, even if we have complied with all applicable laws and regulations, responding to such scrutiny could be expensive and distracting to our management.

Our securities, like other non-traded REITs, were sold through the independent broker-dealer channel (i.e., U.S. broker-dealers that are not affiliated with money center banks or similar financial institutions). Governmental and self-regulatory organizations like the SEC and FINRA impose and enforce regulations on broker-dealers, investment banking firms, investment advisers and similar financial services companies. Self-regulatory organizations such as FINRA adopt rules, subject to approval by the SEC, that govern aspects of the financial services industry and conduct periodic examinations of the operations of registered investment dealers and broker-dealers.

In the past, FINRA has initiated investigations of broker-dealers with respect to the sales practices related to the sale of shares of non-traded REITS. These proceedings have resulted in increased regulatory scrutiny from the SEC regarding non-traded REITs. As a result of this increased scrutiny and accompanying negative publicity and coverage by media outlets, FINRA may impose additional restrictions on sales practices in the independent broker-dealer channel for non-traded REITs, and accordingly we may face increased difficulties in raising capital in the future. If we become the subject of scrutiny, even if we have complied with all applicable laws and regulations, responding to such scrutiny could be expensive and distracting our management.

In April 2016, FINRA adopted changes to rules relating to information required to be included on customer account statements by registered broker dealers. In order to assist broker dealers in complying with these rules, we are required to obtain independent valuations of our assets to determine an estimated per share value of our common stock more frequently than under prior regulations. Compliance with these new rules and future rule changes by FINRA could increase our operating expenses which could have an adverse effect on our results of operations.

A cybersecurity incident and other technology disruptions could negatively impact our business.

We use technology in substantially all aspects of our business operations. We also use mobile devices, social networking, outside vendors and other online activities to connect with our residents, suppliers and employees of our affiliates. Such uses give rise to potential cybersecurity risks, including security breach, espionage, system disruption, theft and inadvertent release of information. Our business involves the storage and transmission of numerous classes of sensitive and confidential information and intellectual property, including residents’ and suppliers’ personal information, private information about employees of our affiliates, and financial and strategic information about us. If we fail to assess and identify cybersecurity risks associated with our operations, we may become increasingly vulnerable to such risks. Additionally, the measures we have implemented to prevent security breaches and cyber incidents may not be effective. The theft, destruction, loss, misappropriation, or release of sensitive and/or confidential information or intellectual property, or interference with our information technology systems or the technology systems of third parties on which we rely, could result in business disruption,

11

negative publicity, brand damage, violation of privacy laws, loss of residents, potential liability and competitive disadvantage, any of which could result in a material adverse effect on our financial condition or results of operations.

Our board of directors determined an estimated value per share of $10.84 for shares of our common stock as of December 31, 2017. You should not rely on the estimated value per share as being an accurate measure of the current value of our shares of common stock.

On March 13, 2018, our board of directors determined an estimated value per share of our common stock of $10.84 as of December 31, 2017. Our board of directors’ objective in determining the estimated value per share was to arrive at a value, based on the most recent data available, that it believed was reasonable based on methodologies that it deemed appropriate after consultation with our advisor. However, the market for commercial real estate can fluctuate quickly and substantially and the value of our assets is expected to change in the future and may decrease. Also, our board of directors did not consider certain other factors, such as a liquidity discount to reflect the fact that our shares are not currently traded on a national securities exchange and the limitations on the ability to redeem shares pursuant to our share repurchase program.

As with any valuation methodology, the methodologies used to determine the estimated value per share were based upon a number of assumptions, estimates and judgments that may not be accurate or complete. Our assets have been valued based upon appraisal standards and the value of our assets using these methodologies are not required to be a reflection of market value under those standards and will not result in a reflection of fair value under GAAP. Further, different parties using different property-specific and general real estate and capital market assumptions, estimates, judgments and standards could derive a different estimated value per share, which could be significantly different from the estimated value per share determined by our board of directors. The estimated value per share does not represent the fair value of our assets less liabilities in accordance with GAAP as of December 31, 2017. The estimated value per share is not a representation or indication that: a stockholder would be able to realize the estimated value per share if he or she attempts to sell shares; a stockholder would ultimately realize distributions per share equal to the estimated value per share upon liquidation of assets and settlement of our liabilities or upon a sale of our company; shares of our common stock would trade at the estimated value per share on a national securities exchange; a third party would offer the estimated value per share in an arms-length transaction to purchase all or substantially all of our shares of common stock; or the methodologies used to estimate the value per share would be acceptable to FINRA or the Employee Retirement Income Security Act of 1974, or ERISA, with respect to their respective requirements. Further, the estimated value per share was calculated as of a moment in time and the value of our shares will fluctuate over time as a result of, among other things, future acquisitions or dispositions of assets (including acquisitions and dispositions of real estate investments since December 31, 2017), developments related to individual assets and changes in the real estate and capital markets.

The actual value of shares that we repurchase under our share repurchase program may be substantially less than what we pay.

We adopted a share repurchase program through which shares may be repurchased at varying prices depending on (1) the number of years the shares have been held, (2) the purchase price paid for the shares and (3) whether the redemptions are sought upon a stockholder’s death or disability. Effective November 20, 2014, our board of directors suspended our share repurchase program. Effective July 1, 2015, our board of directors reinstated our share repurchase program, subject to certain limitations on the amount of shares we will repurchase quarterly. The repurchase price is likely to differ from the price at which a stockholder could resell his or her shares. If the actual value of the shares that we repurchase is less than the repurchase price, the repurchase could be dilutive to our remaining stockholders. Even at lower repurchase prices, the actual value of the shares may be substantially less than what we pay and the repurchase may be dilutive to our remaining stockholders.

Because our charter does not require our listing or liquidation by a specified date, you should be prepared to hold our shares for an indefinite period of time.

Under our charter, if we had not determined to pursue a liquidity event by December 31, 2016, our charter required that we either (1) seek stockholder approval of our liquidation or (2) postpone presenting the liquidation decision to our stockholders if a majority of our board of directors, including a majority of the independent directors, determined that liquidation was not then in the best interests of our stockholders. If a majority of our board of directors, including a majority of the independent directors, determined that liquidation was not then in the best interests of our stockholders, our charter requires our board of directors to reconsider whether to seek stockholder approval of our liquidation at least annually. Our board of directors,

12

including a majority of the independent directors, determined that a liquidation is not in the best interests of the stockholders at this time and, therefore, to postpone presenting a liquidation decision to stockholders. In accordance with our charter, the board of directors will reconsider whether to seek stockholder approval of our liquidation at least annually. The board of directors, pursuant to its fiduciary duties, continuously evaluates opportunities, including possible liquidation events, of us.

Further postponement of a liquidity event or stockholder action regarding liquidation would only be permitted if a majority of our board of directors, including a majority of the independent directors, again determined that liquidation would not be in the best interests of our stockholders. If we sought and failed to obtain stockholder approval of our liquidation, our charter would not require us to consummate our liquidation and would not require our board of directors to reconsider whether to seek stockholder approval of our liquidation. There is no guarantee as to when our board of directors will pursue a liquidity event or submit a liquidation decision to our stockholders, if at all, and you should therefore be prepared to hold our shares for an indefinite period of time.

Payment of fees to our advisor and its affiliates reduces cash available for investment, which may result in our stockholders not receiving a full return of their invested capital.

Because a portion of the offering proceeds from the sale of our shares and cash flow generated from our operations were used to pay fees and expenses to our advisor and its affiliates, the amount of cash available for investments in real properties and real estate-related assets was reduced. As a result, stockholders will only receive a full return of their invested capital if we either: (1) sell our assets or our company for a sufficient amount in excess of the original purchase price of our assets or (2) the market value of our company after we list our shares of common stock on a national securities exchange is substantially in excess of the original purchase price of our assets.

If we internalize our management functions, your interest in us could be diluted and we could incur other significant costs associated with being self-managed.

Our board of directors may decide in the future to internalize our management functions. If we do so, we may elect to negotiate to acquire our advisor’s assets and personnel. At this time, we cannot anticipate the form or amount of consideration or other terms relating to any such acquisition. Such consideration could take many forms, including cash payments, promissory notes and shares of our common stock. The payment of such consideration could result in dilution of your interests as a stockholder and could have an adverse effect on our financial condition and ability to make distributions to our stockholders.

Additionally, while we would no longer bear the costs of the various fees and expenses we expect to pay to our advisor under the advisory agreement, our direct expenses would include general and administrative costs, including legal, accounting and other expenses related to corporate governance, SEC reporting and compliance. We would also be required to employ personnel and would be subject to potential liabilities commonly faced by employers, such as workers disability and compensation claims, potential labor disputes and other employee-related liabilities and grievances as well as incur the compensation and benefits costs of our officers and other employees and consultants that will be paid by our advisor or its affiliates. We may issue equity awards to officers, employees and consultants, which awards would decrease net income and funds from operations and may further dilute your investment. We cannot reasonably estimate the amount of fees to our advisor we would save or the costs we would incur if we became self-managed. If the expenses we assume as a result of an internalization are higher than the expenses we avoid paying to our advisor, our funds from operations would be lower as a result of the internalization than they otherwise would have been, potentially decreasing the amount of funds available to distribute to our stockholders.

Internalization transactions involving the acquisition of advisors have also, in some cases, been the subject of litigation. Even if these claims are without merit, we could be forced to spend significant amounts of money defending claims which would reduce the amount of funds available for us to invest or to pay distributions.

You are limited in your ability to have your shares of common stock repurchased pursuant to our share repurchase program. You may not be able to sell any of your shares of our common stock back to us, and if you do sell your shares, you may not receive the price you paid upon subscription.

Our share repurchase program may provide you with an opportunity to have your shares of common stock repurchased by us. No shares may be repurchased under our share repurchase program until after the first anniversary of the date of purchase of

13

such shares. Prior to the first determination of our estimated value per share following the completion of our offering stage, we repurchased shares of our common stock pursuant to our share repurchase program at a discount from the purchase price based upon how long such shares have been held. Following the first determination of our estimated value per share following the completion of our offering stage, shares of our common stock are repurchased at a price equal to a price based upon our estimated value per share as of our most recent appraisal.

Our share repurchase program contains certain restrictions and limitations, including those relating to the number of shares of our common stock that we can repurchase at any given time and limiting the repurchase price. Specifically, the share repurchase program limits the number of shares to be repurchased during any calendar year to no more than 5.0% of the weighted average number of shares of our common stock outstanding in the prior calendar year. Effective July 1, 2015, our board of directors amended our share repurchase program so that in no event would the value of the shares repurchased pursuant to the share repurchase program exceed $2,000,000 during the quarter beginning July 1, 2015, with each subsequent quarter not to exceed $1,000,000. On August 9, 2016, our board of directors approved and authorized an increase to the value of the shares that may be repurchased pursuant to the share repurchase program from $1,000,000 to $2,000,000, effective on the October 2016 repurchase date.

We have no obligation to repurchase shares if the repurchase would violate the restrictions on distributions under Maryland law, which prohibits distributions that would cause a corporation to fail to meet statutory tests of solvency. Our board of directors reserves the right to reject any repurchase request for any reason or no reason or to amend or terminate the share repurchase program at any time upon 30 days’ notice to our stockholders. Therefore, you may not have the opportunity to make a repurchase request prior to a potential termination of the share repurchase program and you may not be able to sell any of your shares of common stock back to us. Moreover, if you do sell your shares of common stock back to us pursuant to the share repurchase program, you may be forced to do so at a discount to the purchase price you paid for your shares.

Our success is dependent on the performance of our advisor and its affiliates.

Our ability to achieve our investment objectives and to pay distributions is dependent upon the performance of our advisor and its affiliates. Our advisor and its affiliates are sensitive to trends in the general economy, as well as the commercial real estate and credit markets. The most recent economic recession and accompanying credit crisis negatively impacted the value of commercial real estate assets, contributing to a general slow down in the real estate industry. The failure of a sustained economic recovery or renewed economic downturn could result in reductions in overall transaction volume and size of sales and leasing activities, which could put downward pressure on our advisor’s and its affiliates’ revenues and operating results. To the extent that any decline in revenues and operating results impacts the performance of our advisor and its affiliates, our financial condition and ability to pay distributions to our stockholders could also suffer.

Additionally, our advisor relies primarily on the fees it receives pursuant to the advisory agreement and capital from our sponsor to fund its operations and liabilities. If our advisor has insufficient cash from operations to meet its obligations under the advisory agreement and is unable to obtain financing, we would be adversely impacted.

Events in U.S. financial markets have had, and may continue to have, a negative impact on the terms and availability of credit and the overall national economy, which could have an adverse effect on our business and our results of operations.

The failure of large U.S. financial institutions in 2008 and the resulting turmoil in the U.S. financial sector has had a negative impact on the terms and availability of credit and the state of the economy generally within the United States. The tightening of the U.S. credit markets resulted in a lack of adequate credit. Some lenders continue to impose more stringent restrictions on the terms of credit, including shorter terms and more conservative loan-to-value underwriting than was previously customary. The negative impact of the tightening of the credit markets may limit our ability to finance the acquisition of properties and other real estate-related assets on favorable terms, if at all, and may result in increased financing costs or financing with increasingly restrictive covenants.

Additionally, decreasing home prices and mortgage defaults may again result in uncertainty in the real estate and real estate securities and debt markets. Until recently, the market for new issuances of commercial mortgage-backed securities, or CMBS, had been significantly reduced as a result of the recent turmoil in the financial markets and banks generally are providing limited debt financing with more stringent conditions for investments in real estate-related assets. As a result, the valuation of real estate-related assets has been volatile and is likely to continue to be volatile in the future. The volatility in markets may

14

make it more difficult for us to obtain adequate financing or realize gains on our investments which could have an adverse effect on our business and our results of operations.

We are uncertain of our sources for funding our future capital needs. If we do not have sufficient funds from operations to cover our expenses, repay maturing debt obligations or to fund improvements to our real estate and cannot obtain debt or equity financing on acceptable terms, our ability to cover our expenses, repay maturing debt obligations or to fund improvements to our real estate may be adversely affected.

We terminated our initial public offering on December 20, 2013. In the event that we develop a need for additional capital in the future for the repayment of maturing debt obligations, the improvement of our real properties or for any other reason, sources of funding may not be available to us. If we do not have sufficient funds from cash flow generated by our investments or out of net sale proceeds, or cannot obtain debt or equity financing on acceptable terms, our financial condition and ability to make distributions may be adversely affected.

If we cease to retain our advisor or one of its affiliates to perform substantial advisory services for us, we may be required to cease to conduct business under or use the name “Steadfast” or any derivative thereof.

Pursuant to the terms of the advisory agreement, if we cease to retain our advisor or one of its affiliates to perform substantial advisory services for us, we are required, upon receipt of written request from our advisor, to cease to conduct business under or use the name “Steadfast” or any derivative thereof and to change our name and the names of our subsidiaries to a name that does not contain the word “Steadfast” or any other word or words that might, in the reasonable discretion of our advisor, indicate some form of relationship between us and our advisor or its affiliates. If we are required to cease to conduct business under or use the name “Steadfast” or any derivative thereof, it could have an adverse effect on our ability to achieve our investment objectives.

Risks Relating to Our Organizational Structure

Maryland law and our organizational documents limit your right to bring claims against our officers and directors.

Maryland law provides that a director will not have any liability as a director so long as he or she performs his or her duties in accordance with the applicable standard of conduct. In addition, our charter provides that, subject to the applicable limitations set forth therein or under Maryland law, no director or officer will be liable to us or our stockholders for monetary damages. Our charter also provides that we will generally indemnify our directors, our officers, our advisor and its affiliates for losses they may incur by reason of their service in those capacities unless their act or omission was material to the matter giving rise to the proceeding and was committed in bad faith or was the result of active and deliberate dishonesty, they actually received an improper personal benefit in money, property or services or, in the case of any criminal proceeding, they had reasonable cause to believe the act or omission was unlawful. Moreover, we have entered into separate indemnification agreements with each of our directors and executive officers. As a result, we and our stockholders may have more limited rights against these persons than might otherwise exist under common law. In addition, we may be obligated to fund the defense costs incurred by these persons. However, our charter provides that we may not indemnify our directors, our advisor and its affiliates for loss or liability suffered by them or hold our directors or our advisor and its affiliates harmless for loss or liability suffered by us unless they have determined that the course of conduct that caused the loss or liability was in our best interests, they were acting on our behalf or performing services for us, the liability was not the result of negligence or misconduct by our non-independent directors, our advisor and its affiliates or gross negligence or willful misconduct by our independent directors, and the indemnification or agreement to hold harmless is recoverable only out of our net assets, including the proceeds of insurance, and not from the stockholders. As a result of these limitations on liability and indemnification provisions and agreements, we and our stockholders may be entitled to a more limited right of action than we would otherwise have if indemnification rights were not granted.

Risks associated with co-ownership arrangements with our co-venture partners, co-tenants or other partners.

As of December 31, 2017, we owned a 10% interest in the joint venture. In the future, we may enter into additional joint ventures or other co-ownership arrangements for the acquisition, development or improvement of communities as well as the acquisition of real estate-related investments. We may also purchase and develop communities in joint ventures or in partnerships, co-tenancies or other co-ownership arrangements with the sellers of the communities, affiliates of the sellers,

15

developers or other persons. Such investments may involve risks not otherwise present with other forms of real estate investment, including the possibility that our partner in an investment might be unable to or otherwise refuse to make capital contributions when due; that we may incur liabilities as the result of action taken by our partner; that our partner might at any time have economic or business interests or goals that are inconsistent with ours; and that our partner may be in a position to take action contrary to our instructions or requests. Frequently, we and our partner may each have the right to trigger a buy/sell arrangement, which could cause us to sell our interest, or acquire our partner’s interest, at a time when we otherwise would not have initiated such a transaction. Any of these events could have an adverse effect on our results of operations.

The limit on the percentage of shares of our common stock that any person may own may discourage a takeover or business combination that may benefit our stockholders.

Our charter restricts the direct or indirect ownership by one person or entity to no more than 9.8% of the value of our then outstanding capital stock (which includes common stock and any preferred stock we may issue) and no more than 9.8% of the value or number of shares, whichever is more restrictive, of our then outstanding common stock unless exempted by our board of directors. These restrictions may discourage a change of control of us and may deter individuals or entities from making tender offers for shares of our common stock on terms that might be financially attractive to stockholders or which may cause a change in our management. In addition to deterring potential transactions that may be favorable to our stockholders, these provisions may also decrease your ability to sell your shares of our common stock.

We may issue preferred stock or other classes of common stock, which issuance could adversely affect the holders of our common stock.

Investors in our common stock do not have preemptive rights to any shares issued by us in the future. We may issue, without stockholder approval, preferred stock or other classes of common stock with rights that could dilute the value of your shares of common stock. However, the issuance of preferred stock must also be approved by a majority of our independent directors not otherwise interested in the transaction, who will have access, at our expense, to our legal counsel or to independent legal counsel. The issuance of preferred stock or other classes of common stock may increase the number of stockholders entitled to distributions without simultaneously increasing the size of our asset base. Under our charter, we have authority to issue a total of 1,100,000,000 shares of capital stock, of which 999,999,000 shares are designated as common stock with a par value of $0.01 per share, 100,000,000 shares are designated as preferred stock with a par value of $0.01 per share, and 1,000 shares are designated as convertible stock with a par value of $0.01 per share. Our board of directors, with the approval of a majority of the entire board of directors and without any action by our stockholders, may amend our charter from time to time to increase or decrease the aggregate number of shares of capital stock or the number of shares of capital stock of any class or series that we have authority to issue. If we ever created and issued preferred stock with a distribution preference over common stock, payment of any distribution preferences of outstanding preferred stock would reduce the amount of funds available for the payment of distributions on our common stock. Further, holders of preferred stock are normally entitled to receive a preference payment in the event we liquidate, dissolve or wind up before any payment is made to our common stockholders, likely reducing the amount common stockholders would otherwise receive upon such an occurrence. In addition, under certain circumstances, the issuance of preferred stock or a separate class or series of common stock may render more difficult or tend to discourage a merger, tender offer or proxy contest, the assumption of control by a holder of a large block of our securities, or the removal of incumbent management.

Your investment will be diluted upon conversion of the convertible stock.

We have issued 1,000 shares of our convertible stock to our advisor. Under limited circumstances, each outstanding share of our convertible stock may be converted into shares of our common stock, which will have a dilutive effect to our stockholders. Our convertible stock will be converted into shares of common stock if (1) we have made total distributions on the then outstanding shares of our common stock equal to the price paid for those shares plus an 8.0% cumulative, non-compounded, annual return on that price, (2) we list our common stock for trading on a national securities exchange or enter into a merger whereby holders of our common stock receive listed securities of another issuer or (3) our advisory agreement is terminated or not renewed (other than for “cause” as defined in our advisory agreement). Upon any of these events, each share of convertible stock will be converted into a number of shares of common stock equal to 1/1000 of the quotient of (A) 10% of the amount, if any, by which (i) our “enterprise value” plus the aggregate value of the distributions paid to date on the then outstanding shares exceeds (ii) the aggregate purchase price paid by stockholders for those outstanding shares plus an 8.0% cumulative, non-compounded, annual return on the original issue price of the shares, divided by (B) our enterprise value divided by the number

16

of outstanding shares of our common stock on an as-converted basis as of the date of conversion. In the event of a termination or non-renewal of our advisory agreement for cause, the convertible stock will be redeemed by us for $1.00. Upon the issuance of our common stock in connection with the conversion of our convertible stock, your interests in us will be diluted.

The conversion of the convertible stock held by our advisor due upon termination of the advisory agreement and the voting rights granted to the holder of our convertible stock, may discourage a takeover attempt or prevent us from effecting a merger that otherwise would have been in the best interests of our stockholders.

If we engage in a merger in which we are not the surviving entity or our advisory agreement is terminated without cause, our advisor may be entitled to conversion of the shares of our convertible stock it holds and to require that we purchase all or a portion of the limited partnership interests in our operating partnership that it holds at any time thereafter for cash or our common stock. The existence of this convertible stock may deter a prospective acquirer from bidding on our company, which may limit the opportunity for stockholders to receive a premium for their stock that might otherwise exist if an investor attempted to acquire us through a merger.

The affirmative vote of two-thirds of the outstanding shares of convertible stock, voting as a single class, will be required (1) for any amendment, alteration or repeal of any provision of our charter that materially and adversely changes the rights of the convertible stock and (2) to effect a merger of our company into another entity, or a merger of another entity into our company, unless in each case each share of convertible stock (A) will remain outstanding without a material and adverse change to its terms and rights or (B) will be converted into or exchanged for shares of stock or other ownership interest of the surviving entity having rights identical to that of our convertible stock. In the event that we propose to merge with or into another entity, including another REIT, our advisor could, by exercising these voting rights, determine whether or not we are able to complete the proposed transaction. By voting against a proposed merger, our advisor could prevent us from effecting the merger, even if the merger otherwise would have been in the best interests of our stockholders.

We grant stock-based awards to our directors and may in the future grant such awards to our advisor’s employees and consultants pursuant to our long-term incentive plan, which will have a dilutive effect on your investment in us.

We have adopted a long-term incentive plan pursuant to which we are authorized to grant restricted stock, stock options, stock appreciation rights, restricted or deferred stock units, performance awards, dividend equivalents or other stock-based awards to directors, our advisor’s employees and consultants selected by our board of directors for participation in the plan. As of December 31, 2017, we have issued an aggregate of 94,000 shares of restricted stock to our independent directors pursuant to this plan. If we issue additional stock-based awards to eligible participants under our long-term incentive plan, the issuance of these stock-based awards will dilute your investment in our shares of common stock.