Attached files

| file | filename |

|---|---|

| EX-31.1 - EX-31.1 - Solid Biosciences Inc. | d530438dex311.htm |

| EX-32.2 - EX-32.2 - Solid Biosciences Inc. | d530438dex322.htm |

| EX-32.1 - EX-32.1 - Solid Biosciences Inc. | d530438dex321.htm |

| EX-31.2 - EX-31.2 - Solid Biosciences Inc. | d530438dex312.htm |

| EX-23.1 - EX-23.1 - Solid Biosciences Inc. | d530438dex231.htm |

| EX-10.21 - EX-10.21 - Solid Biosciences Inc. | d530438dex1021.htm |

| EX-10.20 - EX-10.20 - Solid Biosciences Inc. | d530438dex1020.htm |

| EX-10.7 - EX-10.7 - Solid Biosciences Inc. | d530438dex107.htm |

| EX-2.3 - EX-2.3 - Solid Biosciences Inc. | d530438dex23.htm |

| EX-2.2 - EX-2.2 - Solid Biosciences Inc. | d530438dex22.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-38360

Solid Biosciences Inc.

(Exact name of Registrant as specified in its Charter)

| Delaware | 90-0943402 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 141 Portland Street, Fifth Floor Cambridge, MA |

02139 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (617) 337-4680

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, $0.001 par value per share |

The Nasdaq Stock Market LLC | |

| (Title of each class) | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐ NO ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☐ NO ☒

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). YES ☐ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ☐ NO ☒

As of June 30, 2017, the last business day of the Registrant’s most recently completed second fiscal quarter, the Registrant’s common stock was not publicly traded. The Registrant’s common stock began trading on the Nasdaq Global Select Market on January 26, 2018. As of March 15, 2018, the aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant was approximately $157.4 million, based upon the closing price on the Nasdaq Global Select Market reported for such date. Shares of common stock held by each of our officers and directors, together with their affiliated investment funds, and by each person who is known to own 10% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates of the Registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of Registrant’s common stock outstanding as of March 15, 2018 was 35,476,892.

Table of Contents

i

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K includes forward-looking statements, which involve risks and uncertainties. These forward-looking statements can be identified by the use of forward-looking terminology, including the terms “believe,” “estimate,” “project,” “anticipate,” “expect,” “seek,” “predict,” “aim,” “continue,” “possible,” “intend,” “may,” “might,” “will,” “could,” “would” or “should” or, in each case, their negative, or other variations or comparable terminology. These forward-looking statements include all matters that are not historical facts. They appear in a number of places throughout this Annual Report on Form 10-K. We derive many of our forward-looking statements from our operating budgets and forecasts, which are based upon many detailed assumptions. While we believe that our assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors, and, of course, it is impossible for us to anticipate all factors that could affect our actual results. All forward-looking statements are based upon information available to us on the date of this Annual Report on Form 10-K.

The forward-looking statements in this Annual Report on Form 10-K include, among other things, statements about:

| • | the timing, progress and results of preclinical studies and clinical trials for SGT-001 and our other product candidates; |

| • | our ability to resolve the full and partial clinical holds on SGT-001 and the requirements for and timing of any such resolutions; |

| • | our ability to obtain and maintain U.S. regulatory approval of SGT-001, and the timing and scope thereof; |

| • | our ability to obtain and maintain foreign regulatory approvals, and the timing and the scope thereof; |

| • | the size of the patient populations and potential market opportunity for SGT-001 and our other product candidates, if approved for commercial use; |

| • | our manufacturing capabilities and strategy, including the scalability and commercial viability of our manufacturing methods and processes; |

| • | our plans to develop and commercialize SGT-001 and our other product candidates, if approved; |

| • | the pricing and reimbursement of SGT-001 and any other product candidates we may develop, if approved; |

| • | the establishment of sales, marketing and distribution capabilities and entry into agreements with third parties to market and sell SGT-001 or our other product candidates, if approved; |

| • | the rate and degree of market acceptance and clinical utility of SGT-001 and any other product candidates we may develop and for which we may receive approval; |

| • | our expectations related to our use of capital resources; |

| • | our estimates regarding expenses, ongoing losses, future revenue, capital requirements and need for and ability to obtain additional financing; |

| • | our intellectual property position; |

| • | our competitive and market position; |

| • | developments relating to our competitors and our industry; and |

| • | the impact of laws and regulations on our operations. |

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We caution you that forward-looking

ii

Table of Contents

statements are not guarantees of future performance and that our actual results of operations, financial condition, business and prospects may differ materially from those made in or suggested by the forward-looking statements contained in this Annual Report on Form 10-K. In addition, even if our results of operations, financial condition, business and prospects are consistent with the forward-looking statements contained in this Annual Report on Form 10-K, those results may not be indicative of results in subsequent periods.

You should read this Annual Report on Form 10-K completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

As used in this Annual Report on Form 10-K, the terms “Solid,” “the Company,” “we,” “us” and “our” refer to Solid Biosciences Inc. unless the context indicates otherwise.

iii

Table of Contents

| Item 1. | Business. |

Overview

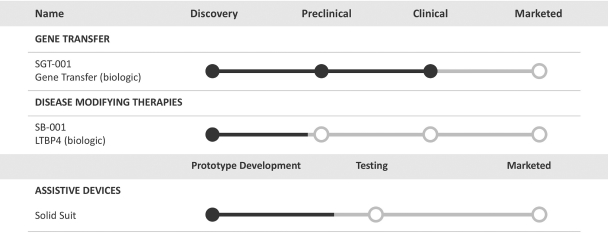

Our mission is to cure Duchenne muscular dystrophy, or DMD, a genetic muscle-wasting disease predominantly affecting boys, with symptoms that usually manifest between three and five years of age. DMD is a progressive, irreversible and ultimately fatal disease that affects approximately one in every 3,500 to 5,000 live male births and has an estimated prevalence of 10,000 to 15,000 cases in the United States alone. DMD is caused by mutations in the dystrophin gene, which result in the absence or near-absence of dystrophin protein. Dystrophin protein works to strengthen muscle fibers and protect them from daily wear and tear. Without functioning dystrophin and certain associated proteins, muscles suffer excessive damage from normal daily activities and are unable to regenerate, leading to the build-up of fibrotic, or scar, and fat tissue. There is no cure for DMD and, for the vast majority of patients, there are no satisfactory symptomatic or disease-modifying treatments. Our lead product candidate, SGT-001, is a gene transfer under development to restore functional dystrophin protein expression in patients’ muscles. Based on our preclinical program that included multiple animal species of different phenotypes and genetic variations, we believe the mechanism of action of SGT-001, if our clinical trials prove to be successful, has the potential to slow or even halt the progression of DMD, regardless of the type of genetic mutation or stage of the disease.

SGT-001 has been granted Rare Pediatric Disease Designation, or RPDD, in the United States and Orphan Drug Designations in both the United States and European Union. In November 2017, we initiated a Phase I/II clinical trial for SGT-001, called IGNITE DMD, and in February 2018 we dosed the first patient, a non-ambulatory adolescent. On March 14, 2018, we announced that IGNITE DMD was placed on full clinical hold following a serious adverse event reported in the clinical trial.

For patients suffering from DMD, symptoms usually begin to manifest between three and five years of age, when they fail to reach developmental milestones or experience motor function challenges, such as difficulty walking or climbing stairs. As the disease progresses, patients with DMD experience frequent falls; can no longer run, play sports or perform most daily functions; and are further weakened by physical activity. By their early teens, DMD patients typically lose their ability to walk and ultimately become dependent on a wheelchair for mobility. By their 20s, patients essentially become paralyzed from the neck down and require a ventilator to breathe. Though disease severity and life expectancy vary, a DMD patient’s quality of life dramatically decreases over time, with death typically occurring by early adulthood from either cardiac or respiratory complications.

Our founders, who are personally touched by the disease, created a biotechnology company purpose-built to accelerate the discovery and development of meaningful therapies for all patients affected by DMD. Through this disease-focused business model, our research team, led by experts in DMD biology and drug development, along with key opinion leaders in DMD, continuously evaluate emerging science to identify high-potential product candidates. Our selection process includes extensive diligence and initial pharmacology research with highly specific, predefined criteria, which provide us with confidence in our development program decisions. Through this data-driven selection process, we have evaluated a number of programs and identified gene therapy as a potentially beneficial approach for DMD, and thus initiated development of our lead product candidate SGT-001. We will continue to apply this rigorous approach and reject the majority of the candidates we evaluate in our effort to develop only programs that we believe have the greatest likelihood of becoming therapies for DMD patients.

Our product candidates

SGT-001 is our lead gene transfer candidate. Gene transfer, a type of gene therapy, is designed to address diseases caused by mutated genes through the delivery of functional versions of those genes, called transgenes. The transgenes are then utilized by the body to produce proteins that are absent or not functional prior to

1

Table of Contents

treatment, potentially offering long-lasting beneficial clinical effects. SGT-001 is designed to address the underlying genetic cause of DMD by delivering a synthetic transgene that produces dystrophin-like protein that is only expressed in muscles of the body, including cardiac and respiratory muscles. Our SGT-001 vector is derived from a naturally occurring, non-pathogenic virus called adeno-associated virus, or AAV, which was selected for its ability to efficiently enter skeletal, diaphragm and cardiac muscle tissues. The vector is designed to carry a synthetic dystrophin transgene construct, called microdystrophin, that retains the most critical components of the full-size dystrophin gene yet is small enough to fit within AAV packaging constraints. SGT-001 is designed to drive microdystrophin protein expression in affected muscles throughout the body. We have studied the efficacy, safety and durability of SGT-001 in multiple preclinical models and its functional benefits in DMD animal studies. In contrast to other therapeutic approaches that are designed to target specific mutations in the dystrophin gene, we believe SGT-001 is a mutation agnostic approach.

In the fourth quarter of 2017, we initiated a randomized, controlled, open-label, single-ascending dose Phase I/II clinical trial, called IGNITE DMD, to evaluate SGT-001 in ambulatory and non-ambulatory males with DMD aged four to 17 years. The primary objectives of IGNITE DMD are to assess the safety and tolerability of SGT-001, as well as efficacy as defined by microdystrophin protein expression. The clinical trial is also designed to assess muscle function and mass, respiratory and cardiovascular function, serum and muscle biomarkers associated with microdystrophin production, patient reported outcomes and quality of life measures, among other endpoints. IGNITE DMD is anticipated to enroll 16 to 32 patients with DMD, who will be randomly assigned to either an active treatment group or a delayed treatment group. It is planned so that adolescents aged 12 to 17 years will receive treatment and, at a later stage of the clinical trial, children aged four to 11 years will be dosed. Efficacy will be assessed by comparing microdystrophin protein expression in muscle biopsy before treatment and 12 months after treatment for each patient. Participants in the control group who continue to meet clinical trial criteria would receive active treatment after 12 months.

In March 2018, the U.S. Food and Drug Administration, or the FDA, placed IGNITE DMD on full clinical hold following our report of a serious adverse event in the clinical trial. On February 14, 2018, the first patient in IGNITE DMD, a non-ambulatory adolescent, received a dose of 5E13 vg/kg of SGT-001, the low dose in the clinical trial. Several days after administration the patient was hospitalized due to laboratory findings that included a decrease in platelet count followed by a reduction in red blood cell count and evidence of complement activation. The patient showed no signs or symptoms of coagulopathy (bleeding disorder), had no relevant changes from baseline in liver function tests and responded well to medical treatment.

We reported the serious adverse event to the FDA and, because it was unexpected, classified it as a Suspected Unexpected Serious Adverse Reaction, or SUSAR. We have halted enrollment and dosing in IGNITE DMD and are awaiting the formal clinical hold letter from the FDA.

Assuming successful resolution of the full clinical hold and based on data from the clinical trial, we will determine next steps for SGT-001 clinical development, including additional clinical trials that may include other patient populations, as well as the need for larger confirmatory clinical trials.

In addition, pursuant to a letter we received from the FDA in November 2017, we are not permitted to dose patients in the higher-dose group of IGNITE DMD due to a partial clinical hold. The hold relates to the number of vials and manufacturing lots utilized per patient, as well as manufacturing processes to support the higher-dose group. We have submitted our response to the FDA and are awaiting their feedback.

If successfully developed and approved, we intend to commercialize SGT-001 in the United States and European Union, and we may enter into licensing agreements or strategic collaborations to commercialize the product candidate in other markets.

2

Table of Contents

Taking into account the prevalence and incidence of DMD and the anticipated dosing requirements for gene transfer, we anticipate that there will be a need for a substantial supply of SGT-001 for clinical trials and, if approved, for commercial markets. Through significant targeted investments to address this challenge, we generated sufficient drug product supply to initiate our IGNITE DMD. We continue to develop our manufacturing process to meet future clinical and commercial production needs for SGT-001.

While we believe gene transfer may be able to slow or halt DMD disease progression, many patients would still suffer from the manifestations of the disease, such as tissue damage to their muscles, inflammation, cardiac dysfunction and fibrosis. As part of our disease-focused business model, we are also building a portfolio of complementary disease modifying therapies to address these manifestations. Our portfolio currently includes an initial disease modifying candidate, SB-001, a monoclonal antibody designed to reduce fibrosis and inflammation, as well as a number of emerging and complementary programs. We intend to commence preclinical activities for the SB-001 program in 2018.

In addition to developing our pipeline of product candidates, we believe it is critical to invest time and resources in tools and technologies designed to help us more effectively understand DMD, accurately monitor disease progression and assist patients in daily life. As part of this goal, we are developing biomarkers and sensors that may allow us to identify treatment targets faster, measure the therapeutic impact of potential product candidates better and reach decision points earlier. In addition, through our Solid Suit program, we are developing a line of soft, wearable assistive devices with the goal of providing functional and therapeutic benefits to DMD patients.

Our pipeline

We seek to protect our proprietary and intellectual property position through a combination of patents, trade secret laws, proprietary know-how, continuing technological innovation, and entering into non-disclosure, confidentiality and invention assignment agreements. We have exclusively licensed three issued U.S. patents, one pending U.S. non-provisional patent application, and seven issued patents and eleven pending patent applications in foreign jurisdictions. We have filed three pending U.S. provisional patent applications. We intend to continue building out our intellectual property protection to further strengthen our position in the DMD field.

Who we are

Solid Biosciences was founded in 2013 by our Chief Executive Officer, Ilan Ganot, our Chairman of the Board, Andrey Zarur, and our President, Gilad Hayeem, with the goal of developing meaningful therapies for patients with DMD. Solid is the English translation of Eytani, the Hebrew name of Ilan and Annie Ganot’s son,

3

Table of Contents

who was diagnosed with the disease in 2012. Our founders, unsatisfied with the existing therapeutic landscape, proceeded to raise funds to execute on our disease-focused business model. We assembled a passionate management team and scientific advisory board composed of individuals with extensive experience in DMD, gene therapy, product discovery, research and development, manufacturing, business strategy and finance.

In 2015, we began exclusively licensing the elements of the construct for SGT-001 and other elements of our gene transfer program from the University of Michigan, the University of Missouri and the University of Washington. Since then, we have continued to use our extensive network across the academic, business and patient communities to identify, vet and pursue high-potential complementary product candidates to address the needs of DMD patients.

Since our inception, we have raised private capital from a group of top-tier corporate and private investors. In addition, three leading U.K.-based DMD charities provided initial seed funding for our gene transfer program in return for equity in our company, and we have accepted additional contributions from several DMD charities to fund our early-stage research programs. In January 2018, we completed our initial public offering resulting in net proceeds of $129.3 million, after deducting underwriting discounts and commissions and offering expenses.

We operated as a Delaware limited liability company under the name Solid Biosciences, LLC until immediately prior to the effectiveness of our registration statement on Form S-1 on January 25, 2018, at which time we converted into a Delaware corporation pursuant to a statutory conversion and changed our name to Solid Biosciences Inc.

Mission

Our mission, which guides every aspect of our operations, is to cure DMD. Underscoring this mission, our disease-focused business model is founded on the following fundamental values:

| • | identify and develop meaningful therapies for all patients with DMD; |

| • | bring together the leading experts in DMD, science, technology, disease management and care; and |

| • | be guided by the needs of DMD patients. |

About Duchenne muscular dystrophy

DMD is an X-chromosome-linked, muscle-wasting disease, predominantly affecting boys. Progressive, irreversible and ultimately fatal, DMD occurs in approximately one in every 3,500 to 5,000 live male births and has an estimated prevalence of 10,000 to 15,000 cases in the United States alone. In DMD, mutations in the dystrophin gene result in the body’s inability to produce functioning dystrophin protein, which works to strengthen muscle fibers and protect them from daily wear and tear. Dystrophin protein also serves as the cornerstone of the dystrophin glycoprotein complex, or DGC, a group of proteins that links the inner and outer components of muscle cells to ensure proper muscle function.

Without dystrophin and the DGC, muscles suffer excessive damage from normal daily activities and are unable to regenerate, leading to the build-up of scar and fat tissue. More than 1,000 dystrophin gene mutations, which can be inherited or can occur spontaneously, have been identified in people with DMD.

For patients suffering from DMD, symptoms usually begin to manifest between three and five years of age, when they fail to reach developmental milestones or experience motor function challenges, such as difficulty walking or climbing stairs. Muscle wasting initially presents in the legs and pelvic area, then in the muscles of the shoulders, neck and arms. As the disease progresses, patients with DMD experience frequent falls, can no longer run, play sports or perform most daily functions, and are further weakened by physical activity. In addition to physical challenges, DMD also commonly involves cognitive difficulties and behavioral challenges.

4

Table of Contents

By their early teens, DMD patients typically lose their ability to walk and become dependent on a wheelchair for mobility. By their 20s, patients essentially become paralyzed from the neck down and require a ventilator to breathe. Though disease severity and life expectancy vary, a patient’s quality of life dramatically decreases over time, with death typically occurring by early adulthood from either cardiac or respiratory complications.

Need for effective therapies

There is no cure for DMD and, for the vast majority of patients, there are no satisfactory symptomatic or disease-modifying treatments.

Glucocorticoid treatment, the current standard-of-care, has been shown to temporarily improve muscle strength, prolong the period of ambulation and slow the progression of DMD. However, glucocorticoid use is associated with well-known adverse events, such as severe weight gain, stunted growth, weakening of bone structure and metabolic dysfunctions, among others. The most commonly used glucocorticoids include prednisone and deflazacort (EMFLAZA). Deflazacort has been commercially available in several countries outside of the United States and was approved in the United States for the treatment of DMD in 2017.

In recent years, certain regulators have conditionally approved two new therapies, eteplirsen (EXONDYS 51) and ataluren (Translarna), which target specific mutations in the dystrophin gene. These therapies are indicated for only a small portion of the DMD patient population, and their respective efficacy profiles still need to be fully understood.

Eteplirsen is an antisense oligonucleotide indicated for DMD patients who have a confirmed mutation of the dystrophin gene amenable to exon 51 skipping, which affects approximately 13% of DMD patients. Eteplirsen is administered as a weekly intravenous infusion. In 2016, eteplirsen was granted accelerated approval from the FDA based on an increase in dystrophin in skeletal muscle observed in some patients who received the therapy. However, the FDA concluded that a clinical benefit, including improved motor function, has not been established. Eteplirsen is still under review by regulatory authorities outside of the United States.

Ataluren is a small molecule indicated for the treatment of patients who have DMD resulting from nonsense mutations in the dystrophin gene, which also affect approximately 13% of DMD patients. In 2014, ataluren received conditional marketing authorization from the European Commission, and has since been approved in several other countries outside of the United States. Ataluren’s indication is currently limited to ambulatory patients five years of age and older. In February 2018, the FDA reiterated its denial of PTC Therapeutics, Inc.’s appeal of the complete response letter for the new drug application for ataluren.

Current best practices for treating DMD patients also dictate a multidisciplinary approach to disease management, which includes physical and occupational therapy to preserve strength, function and flexibility, orthopedic management to reduce the risk of scoliosis and other bone and joint problems, pulmonary, cardiac and gastrointestinal management, and psychosocial management to support behavior and learning.

Burden of disease

Despite recent therapeutic advances, DMD represents a significant societal and economic burden. The economic burden, estimated at $1.2 billion annually in the United States (excluding costly mortality and end-of-life care expenses), includes costs associated with hospital admissions, medication, frequent doctor visits and investment in assistive devices, as well as indirect costs related to productivity losses for the caregivers and costs due to pain, anxiety and social handicap. Of this amount, approximately 45% is represented by indirect costs. Only a small proportion of DMD patients are employed and many caregivers reduce their hours or stop working altogether to care for their children, who progressively require more help with everyday tasks, such as eating, dressing and using the bathroom. In some cases, patients also experience serious mental health issues that require additional support and treatment.

5

Table of Contents

Solid’s 360-degree solution

We aim to address the full spectrum of DMD disease manifestation, from its underlying genetic cause to other disorders that result from disease progression. We are advancing corrective therapies, disease-modifying therapies and assistive devices, as well as tools to accelerate drug development.

Gene transfer—A corrective therapy

Gene therapy is a therapeutic approach that aims to address diseases caused by gene mutations. A gene is a portion of deoxyribonucleic acid, or DNA, that provides the instructions for the body to construct proteins that perform functions needed for life. Genes are prone to mutations, which can either be inherited or occur spontaneously. While many mutations are harmless, some lead to the absence of crucial proteins, resulting in serious genetic diseases like DMD.

Gene transfer, a type of gene therapy, is designed to address diseases caused by mutated genes through the delivery of functional versions of those genes, called transgenes. The transgenes are then utilized by the body to produce proteins that are absent or not functional prior to treatment, potentially offering long-lasting beneficial effects.

We have focused our initial efforts on gene transfer because we believe it has the greatest potential to address the root cause of DMD: the absence or near-absence of dystrophin protein. If successful, we believe gene transfer can slow or stop the progression of DMD in a majority of patients, irrespective of their genetic mutation, by producing long-term, muscle-specific expression of a functional dystrophin-like protein.

Our gene transfer candidate, or vector, includes three components:

| • | a viral capsid—a protein shell utilized as a vehicle to deliver a transgene to cells in the body; |

| • | a transgene—a functional gene intended to produce a functional protein; and |

| • | a promoter—a specialized DNA sequence that directs cells to produce the protein in specific tissues. |

SGT-001

SGT-001, our lead gene transfer candidate, is designed to preserve muscle function in DMD patients after a single administration. The SGT-001 vector is comprised of a functional transgene and a muscle-specific promoter which are delivered via an AAV capsid.

The vector is modified to no longer self-replicate, yet retains its ability to effectively introduce new genetic material directly into patients’ cells. AAV vectors have been extensively studied in human clinical trials in multiple disease indications, including in clinical trials of high-dose, systemically delivered AAV gene therapies being conducted by third parties.

Capsid: The capsid of the SGT-001 vector is derived from a naturally occurring, non-pathogenic virus called AAV. There are several subtypes of AAV capsids that differ based on the proteins that make up their structure. These capsids have affinities for different sites in the body. We selected the AAV9 serotype capsid for clinical development based on our preclinical data, which demonstrated the capsid’s ability to enter skeletal, diaphragm and cardiac muscle tissues.

Transgene: Dystrophin, the largest gene in the body, exceeds the carrying capacity of AAV vectors. To overcome this challenge, we advanced development of the SGT-001 transgene, a synthetic, dystrophin-like gene that fits into AAV and has the ability to drive functional protein expression in skeletal, diaphragm and cardiac muscle tissue.

6

Table of Contents

The concept of a modified therapeutic dystrophin gene originated from research on Becker muscular dystrophy, or BMD, where researchers discovered that certain BMD patients had mutations in the dystrophin gene that drove expression of a functional form of dystrophin protein, allowing patients to live relatively normal lives. This discovery led scientists to engineer a number of synthetic, dystrophin transgene constructs, called microdystrophins, that retained only the most critical components of the full-size dystrophin gene yet were small enough to fit within AAV packaging constraints. There are several types of microdystrophins that differ based on the configuration of their components. Microdystrophins were subsequently demonstrated to functionally protect muscle in mouse models of DMD.

The SGT-001 microdystrophin construct, which is our lead clinical candidate for DMD, is based on three decades of development and optimization work at the University of Missouri and the University of Washington as well as other academic institutions. In preclinical studies, Jeffrey Chamberlain, Ph.D., from the University of Washington, and Dongsheng Duan, Ph.D., from the University of Missouri, identified a proprietary configuration of genetic components that, when administered systemically, produces functional microdystrophin protein expression that not only stabilizes muscle membranes and protects muscle against injury, but also simultaneously restores the localization of DGC to the muscle membrane, notably increasing neuronal nitric oxide synthase, or nNOS, concentration. In subsequent published studies, Dr. Duan demonstrated in animal models that, in comparison to earlier configurations, nNOS-restoring microdystrophins were more effective in improving muscle function and blood circulation.

Promoter: The expression of the SGT-001 microdystrophin transgene is regulated by a modified, synthetic muscle-specific promoter cassette called CK8, which is derived from the naturally occurring muscle creatine kinase promoter. Regulatory cassettes, such as CK8, are used to prompt gene expression specifically in muscle tissues. In comparison to other regulatory cassettes, we chose CK8 due to its small size and its ability to drive microdystrophin transgene expression in skeletal, diaphragm and cardiac muscle tissues. In our preclinical studies in small and large animal models, CK8 restricted microdystrophin transgene expression to these muscles.

SGT-001 preclinical program

Our comprehensive preclinical program for SGT-001 is comprised of studies that inform efficacy, durability and safety, as well as dose response and the kinetics of transgene expression. Our program includes three different animal species: mice, dogs and non-human primates, or NHPs. Our preclinical studies were performed by third-party collaborators over the last three years.

Well established mouse and dog disease models for DMD offered us the opportunity to better evaluate the potential translatability of SGT-001 to humans. While studies in dystrophic mice, such as the mdx mouse, provide important efficacy rationale, we chose to perform additional functional studies in dystrophic dogs because they exhibit a more severe dystrophic phenotype and progress similarly to human patients at earlier stages of the disease. Dog models enabled us to assess various endpoints, including biodistribution, expression, durability and function in a large animal species.

Because DMD is a disease defined by a lack of dystrophin protein, it is important to reliably detect microdystrophin expression in muscle after SGT-001 treatment. As part of our core preclinical program, we developed well characterized and well recognized analytic approaches to confirm transgene expression and localization, using the following assays:

| • | Immunofluorescence: A qualitative method to determine if a transgene is expressed and localized to muscle membrane. |

| • | Western blot: A recognized method to quantify dystrophin expression, which is a validated biomarker. |

| • | Mass spectrometry: A highly sensitive analytical method to quantify transgene expression. |

We also employed immunofluorescence to confirm if our microdystrophin construct restored the DGC, including key proteins such as sarcoglycan and nNOS.

7

Table of Contents

Efficacy in dystrophic mice

Multiple studies in both dystrophic, or mdx, and healthy, or wild-type, mice have demonstrated that a single intravenous administration of SGT-001 induces measurable levels of microdystrophin protein expression. In all studies, microdystrophin protein expression was measured using immunofluorescence, Western blot and mass spectrometry.

In an mdx dose-response study, a clear dose-dependent pattern of transgene expression was observed at day 28 by all three assays. As an example, at a dose of 1E14 vg/kg, transgene expression as quantified by positive immunoflouresence staining in the quadriceps and heart muscle tissues was 50% and 80%, respectively, of the full-length dystrophin levels quantified in healthy wild-type control muscles. Similar levels of microdystrophin expression were found in all mdx studies completed to date. Efficacy studies performed in dystrophic mice treated with SGT-001 demonstrated significant, dose-responsive improvements in both muscle morphology and multiple physiological parameters. In a blinded efficacy study performed in mdx mice dosed at approximately six weeks of age, SGT-001 treatment showed a statistically significant improvement in grip strength, which assesses arm and leg strength, at multiple doses.

In addition, using a treadmill exhaustion assay, the total distance run by the SGT-001-treated mdx mice was approximately two- to fifteen-fold longer compared to the untreated mice at all time points five-weeks post-dose.

At study termination, muscle force was measured ex vivo in the extensor digitorum longus muscle in all animals. SGT-001-treated mdx mice, dosed at either 2E14 or 4.5E14 vg/kg, exhibited a 1.3-fold increase in specific muscle force over untreated controls when compared to the untreated mdx mice.

In a second efficacy study employing a more severe dystrophic mouse model, or DBA/2J-mdx, a version of SGT-001 was administered at a dose of 1E15 vg/kg. Treated mice exhibited functional results that were similar to untreated wild-type animals. In the SGT-001-treated DBA/2J-mdx mice, the specific muscle force was similar to wild-type mice. Further, the treated animals were protected against muscle damage associated with eccentric contractions, a type of contraction related to muscle lengthening under load that is known to be highly damaging to dystrophic muscles. In contrast, untreated DBA/2J-mdx mice showed significantly reduced specific force and no protection against eccentric contraction induced muscle damage.

Efficacy in dystrophic dogs

Two independent studies in dystrophic dogs assessed durability of microdystrophin expression and efficacy, respectively. These studies were performed in two distinct dystrophic dog models (mixed breed dystrophic dogs, or cDMD, and Golden Retriever Muscular Dystrophy, or GRMD), collectively encompassing a number of genetic mutations that lead to the absence of dystrophin protein. This enabled us to assess SGT-001 across multiple mutations, which is more reflective of the composition of the DMD patient population. Both studies used a canine-optimized version of the microdystrophin gene.

In a long-term dose-ranging study, five three-month-old, juvenile cDMD dogs received an intravenous dose of either 5E13 vg/kg (n=1), 1E14 vg/kg (n=2), 3E14 vg/kg (n=1) or 5E14 vg/kg (n=1). In this study, muscle biopsies were collected from the skeletal muscles at one, three, six, 12, 16, 20, 24 and 30 months after injection. Robust transgene expression was detected by immunofluorescence at all time points and at all of the dose levels. In animals dosed with 1E14 vg/kg, approximately 70-90% of the muscle fibers were positive for microdystrophin. In treated muscle samples, transgene expression was associated with stabilization of the DGC, including nNOS. To date, all doses have been well tolerated and there has been no observed immune response to the transgene. This study is currently ongoing.

A blinded dose-ranging study in the GRMD model assessed the general safety and efficacy of the canine construct of SGT-001. The three dose levels (1E13, 1E14 and 2E14 vg/kg) were administered at three months of age and animals were followed for three months following administration. All doses were well tolerated and there was no observed immune response to the transgene.

8

Table of Contents

Dose-dependent transgene expression was detected in interim biopsies of skeletal muscles at day 28 and 45 and at the end of the study at day 91 in skeletal, diaphragm and cardiac muscles. A blinded histological evaluation of the muscle tissue revealed a reduction of dystrophic pathology at the higher dose levels. In the mid- and high-dose groups, all muscles biopsied at the end of the study exhibited improved pathology compared to low dose and untreated controls. Biodistribution studies demonstrated dose dependent transgene expression that was only detectable in the muscle tissues.

The observed dose response was detectable by both immunofluorescence and Western blot. Quantification by Western blot averaged less than 10% of wild-type in the low-dose (1E13 vg/kg) animals. In the mid-dose animals, the level of expression among the skeletal muscles ranged from an average of approximately 20% to approximately 50% of wild-type control muscles. At 2E14 vg/kg, the level of expression ranged from 30% to 70% of wild-type dystrophin. This data also correlates to quantification of microdystrophin via mass spectrometry.

Dose-dependent, sustained expression of microdystrophin not only correlated with histological improvements in muscle, but also provided statistically significant improvements in measures of muscle function. At day 90, muscle force generation was improved in both the 1E14 vg/kg and 2E14 vg/kg cohorts, indicating that the microdystrophin produced by SGT-001 is highly protective in a large animal dystrophic species.

The efficacy data collectively described above in both dystrophic mouse and dog models was incorporated into an overall nonclinical model to inform dose selection for our clinical program.

Manufacturing comparability

As part of our manufacturing process development, we have run comparability studies at each stage of our process scale-up. These comparability studies were carried out using in vivo mouse models to ensure that our drug product produced at different scales is comparable to each other.

Safety

As part of our preclinical program, we performed necessary good laboratory practices, or GLP, toxicology studies to establish the overall safety profile of SGT-001 in wild-type mice and NHPs. The data and our conclusions from these studies were included in our Investigational New Drug application, or IND, submission to the FDA. Systemic administration of SGT-001 was generally well tolerated in both species. We observed no evidence of test-article-related toxicity for up to 13 weeks after systemic administration of SGT-001 in either species that would prevent us from initiating clinical trials. In the NHP study, test-article-related effects were self-limited, mild chemistry and hematology changes with no microscopic correlates at the end of the study. There was a transient and asymptomatic increase in liver function enzymes observed in NHPs starting on day 9, which returned to normal levels by day 21. We believe there were no other relevant test-article-related adverse events associated with SGT-001 administration in either GLP study. In the NHP toxicology study, a single animal from the high dose cohort was euthanized after it did not recover from an anesthetic procedure. We believe this event was attributed to procedural errors. However, AAV vector cannot be completely ruled out as a contributing factor to the toxicity that gave rise to the event.

Clinical development of SGT-001

We are developing SGT-001 for the treatment of DMD through a single intravenous administration. In the fourth quarter of 2017, we announced the initiation of IGNITE DMD, a randomized, controlled, open-label, single-ascending dose Phase I/II clinical trial designed to evaluate SGT-001 in ambulatory and non-ambulatory males with DMD aged four to 17 years. The primary objectives of IGNITE DMD are to assess the safety and tolerability of SGT-001, as well as efficacy as defined by microdystrophin protein expression. The clinical

9

Table of Contents

trial is also designed to assess muscle function and mass, respiratory and cardiovascular function, serum and muscle biomarkers associated with microdystrophin production, patient reported outcomes and quality of life measures, among other endpoints. IGNITE DMD is anticipated to enroll 16 to 32 patients with DMD. Key inclusion criteria include: established clinical diagnosis of DMD and documented dystrophin gene mutation predictive of DMD phenotype; anti-AAV9 antibodies below pre-specified thresholds; stable cardiac and pulmonary function; and a stable daily dose of oral corticosteroids for 24 weeks. There is no enrollment restriction in the clinical trial protocol based on a patient’s underlying dystrophin gene mutation.

IGNITE DMD participants will be randomly assigned to either an active treatment group or a delayed treatment control group. The selection of our starting dose, 5E13 vg/kg, was based on safety and efficacy data observed in our preclinical studies. Dose escalation between cohorts and decisions regarding clinical trial progression will occur after review by the Data Safety Monitoring Board, or DSMB. It is planned so that adolescents aged 12 to 17 years will be treated initially, followed by children aged four to 11 years. Efficacy will be assessed by comparing microdystrophin protein expression in muscle biopsy before and 12 months after treatment for each patient. Other endpoints will be compared against the control group. We anticipate that the delayed treatment control group will be rolled into an active treatment phase after 12 months, as long as participants continue to meet clinical trial criteria. Long-term follow up will continue per regulatory guidelines.

In March 2018, the FDA placed IGNITE DMD on full clinical hold following our report of a serious adverse event in the clinical trial. On February 14, 2018, the first patient in IGNITE DMD, a non-ambulatory adolescent, received a dose of 5E13 vg/kg of SGT-001, the low dose in the clinical trial. Several days after administration the patient was hospitalized due to laboratory findings that included a decrease in platelet count followed by a reduction in red blood cell count and evidence of complement activation. The patient showed no signs or symptoms of coagulopathy (bleeding disorder), had no relevant changes from baseline in liver function tests and responded well to medical treatment.

We reported the serious adverse event to the FDA and, because it was unexpected, classified it as a Suspected Unexpected Serious Adverse Reaction, or SUSAR. We have halted enrollment and dosing in IGNITE DMD and are awaiting the formal clinical hold letter from the FDA.

Assuming successful resolution of the full clinical hold and data from the clinical trial, we will determine next steps for SGT-001 clinical development, including additional clinical trials that may include other patient populations, as well as the need for larger confirmatory clinical trials.

In addition to the full clinical hold on IGNITE DMD, we also must resolve a partial clinical hold on the higher-dose group in the clinical trial. Pursuant to a letter we received from the FDA in November 2017, we are not permitted to dose patients in the higher-dose group of the clinical trial until we decrease the number of vials and utilize no more than a single production lot per patient, as well as demonstrate that we have the appropriate manufacturing processes in place to support the higher-dose group. We have submitted our response to the FDA and are awaiting their feedback.

Manufacturing SGT-001

The prevalence and incidence of DMD, combined with average patient weight and anticipated dosing requirements for SGT-001, result in a substantial supply need for clinical trials and, if approved, for commercial markets. To address this challenge, we developed a manufacturing process that we believe will be scalable to meet clinical and commercial production needs for SGT-001.

Our suspension-based process is founded on seminal work by scientists at the University of Florida and has been optimized for manufacturability by our internal process development scientists with the support of our

10

Table of Contents

Contract Development Manufacturing Organizations, or CDMO, partners. The process consists of three steps. First, we produce two replication-incompetent Herpes Simplex Virus, or HSV, stocks, one containing our microdystrophin construct and the other containing the critical elements of the AAV9. We then use these two HSV stocks to coinfect suspension-adapted human embryonic kidney cells (HEK-293), which are then purified and concentrated in our downstream process to produce our gene transfer candidate. Our team has developed the analytical testing methods needed to support consistency and strict standards of quality and potency. We believe that this approach will increase our speed of development, ensure consistent quality and regulatory compliance, and reduce the risk of delay or unexpected production costs.

Current status and plans for clinical and commercial scale-up

We believe that our investment in our scalable manufacturing process over the last several years will allow us to minimize the need for changes throughout clinical development and upon commercialization, while ensuring supply at the high volume required at all stages. We intend to supply our clinical development program for SGT-001 with drug product produced at current good manufacturing practices, or cGMP, - compliant facilities located at partner CDMOs. We are currently operating at 250-liter scale. Our in-house scientists are continuing to work to increase the productivity and efficiency of our manufacturing process. In addition, we intend to establish the capability and capacity to supply SGT-001 at commercial scale from multiple sources, including potentially building our own GMP facility to ensure redundancy and reliability.

Complementary disease-modifying therapies

While we believe gene transfer may be able to slow or halt DMD disease progression, many patients would still suffer from the manifestations of the disease, such as tissue damage to their muscles, impaired muscle strength, inflammation, cardiac dysfunction and fibrosis. We are building a portfolio of complementary disease-modifying therapies designed to address these manifestations.

Our portfolio currently includes SB-001, our initial disease modifying candidate that is aimed at addressing fibrosis, as well as several emerging and complementary programs. We have chosen to focus our efforts on these programs following rigorous preclinical testing and our assessment of clinical potential given natural human modifiers. If initial preclinical studies are successful, we envision initiating additional studies for our disease-modifying programs in combination with SGT-001. We continue to assess additional emerging therapeutic approaches from academia and industry through our highly focused product candidate selection process to further build our portfolio.

SB-001 (LTBP4)

SB-001 is a monoclonal antibody intended to reduce fibrosis and inflammation. It is designed to target and stabilize the LTBP4 protein. LTBP4 is highly expressed in muscle and, when stable, prevents fibrosis and inflammation by inhibiting the activation of the TGF-beta pathway.

The rationale for targeting LTBP4 originated from observations in DMD natural history studies. Researchers found that subsets of patients with genetic variants in the LTBP4 gene maintained their ability to walk longer compared to patients in the study who did not. Researchers discovered that these genetic variants lead to reduced TGF-beta signaling. Elizabeth McNally, M.D., Ph.D., Director of the Center for Genetic Medicine at Northwestern University, hypothesized that stabilization of the LTBP4 protein in DMD patients could mimic the effect.

In order to assess the efficacy of potential human antibody clinical candidates in preclinical models, mice expressing the human version of LTBP4 were crossed with mdx mice to generate a DMD model that expressed human LTBP4 (hLTBP4:mdx). Preliminary studies showed that the hLTBP4:mdx animals treated with an anti-LTBP4 antibody showed significantly lower levels of fibrosis and inflammation due to the stabilization of the LTBP4 protein.

11

Table of Contents

In partnership with Dr. McNally and Adimab LLC, SB-001 development efforts are underway to optimize lead candidate human immunoglobulin G, or IgG, antibodies directed against LTBP4. Additional selection and characterization are being employed to obtain high affinity antibodies. We plan to conduct preclinical in vivo efficacy, biodistribution and safety studies utilizing these human antibodies in hLTBP4:mdx mice beginning in 2018, following final in vitro antibody characterization and scale-up of manufacturing efforts.

Tools to accelerate discovery and development

We believe it is critical to invest time and research into tools designed to help us more effectively measure disease progression and the therapeutic impact of our product candidates. We are focused on developing biomarkers and sensors that will allow us to identify treatment targets faster, better measure the therapeutic impact of potential product candidates and reach therapeutic decision points earlier.

Blood-based and imaging biomarkers

We are working to identify non-invasive blood-based and imaging biomarkers that could potentially reduce or eliminate the need for muscle biopsies in clinical trials, reducing stress on patients and allowing better evaluation of potential product candidates. We are developing a platform technology that may enable the non-invasive measurement of changes associated with increased dystrophin and dystrophin-like protein expression in DMD patients by using established imaging techniques. We are also currently using leading, robust platforms to perform extensive analysis on blood-based samples to establish molecular signatures based on various stages of DMD disease progression.

Sensor-less mobility tracking

We are working to develop naturalistic motor function measurement at home with an ambient measurement system, which is based on sensors such as Microsoft Kinect. This system uses infrared technology to detect body movement and is designed to collect mobility data for DMD patients without requiring wearable sensors. If successful, this new non-invasive technology would enable us to understand in greater detail the therapeutic impact of potential product candidates as they relate to everyday activities, and could provide information to establish and measure clinical endpoints in future clinical trials.

Assistive devices

Solid Suit

We are currently developing a line of soft, wearable assistive devices that may have both functional and therapeutic benefits, with the goal of helping patients perform day-to-day activities with greater ease and preserving their muscle function. We refer to these devices as the Solid Suit. This work is being done in collaboration with technology innovators and engineering and disease experts, and is informed by input from the patient community. The Solid Suit utilizes cutting-edge technologies to power soft, light-weight comfortable exoskeletons with the potential to offset muscle fatigue and augment muscle strength. We are developing the Solid Suit in three separate components, two of which are currently in prototype development.

Intellectual property

Our commercial success depends in part on our ability to obtain and maintain proprietary or intellectual property protection for our product candidates, including SGT-001, and other know-how, to operate without infringing, misappropriating or otherwise violating the intellectual property rights of others, and to prevent others from infringing, misappropriating or otherwise violating our intellectual property rights. We also rely on patents, trade secrets, know-how and continuing technological innovation to develop and maintain our proprietary and intellectual property position.

12

Table of Contents

As of March 15, 2018, we have filed three pending U.S. provisional patent applications and have exclusively licensed three issued U.S. patents, one pending U.S. non-provisional patent application, and seven granted patents and eleven pending patent applications in foreign jurisdictions. The issued U.S. patents are projected to expire between 2021 and 2028, excluding any patent term adjustments and any patent term extensions, and any U.S. patents that may issue from the pending U.S. non-provisional patent application and U.S. provisional patent applications (assuming U.S. non-provisional patent applications are timely filed with respect to such provisional patent applications and all other applicable requirements are satisfied) would be projected to expire between 2036 and 2039, excluding any patent term adjustments and any patent term extensions.

With respect to our gene transfer programs, we exclusively licensed patent families that relate to microdystrophin genes. With respect to SGT-001, we exclusively licensed one issued U.S. patent and one pending U.S. non-provisional patent application, which generally claim the structural elements of SGT-001 and the promoter sequence used in SGT-001. This issued U.S. patent is projected to expire in 2028, excluding any patent term adjustments and any patent term extensions. We also own one pending U.S. provisional patent application relating to SGT-001. Any U.S. patents that may issue from the pending U.S. non-provisional patent application and our pending U.S. provisional patent application (assuming a U.S. non-provisional patent application is timely filed with respect to such provisional patent application and all other applicable requirements are satisfied) would be projected to expire between 2036 and 2039, excluding any patent term adjustments and any patent term extensions. Substantive prosecution of our provisional patent application has not yet commenced at the U.S. Patent and Trademark Office, or USPTO. Our provisional patent application is not eligible to become an issued patent until, among other things, we file a non-provisional patent application within 12 months of the filing date of our provisional patent application. If we do not timely file the non-provisional patent application, we may lose our priority date with respect to our provisional patent application and any patent protection on the inventions disclosed in our provisional patent application. While we intend to file a non-provisional patent application, we cannot predict whether such future patent application will result in the issuance of a patent that effectively protects SGT-001, or if such issued patent or any of our licensor’s issued patents will effectively prevent others from commercializing competitive products. In any event, patent prosecution is a lengthy process, during which the scope of the claims initially submitted for examination by the USPTO offices are often significantly narrowed by the time they issue, if they issue at all.

With respect to SB-001, we do not currently own or in-license any issued patents or patent applications relating to such product candidate. We have an exclusive option to negotiate for licenses of certain patents and patent applications relating to SB-001 from Ikaika Therapeutics, LLC. If we exercise such option, Ikaika Therapeutics, LLC is only required to negotiate the terms of a potential license agreement with us for certain specified periods of time and we may be unable to enter into such a definitive license agreement within the required timeframe or under terms that are acceptable to us. If we are unable to enter into such a definitive license agreement, we will not have any license to such patents and patent applications.

The term of individual patents depends upon the legal term for patents in the countries in which they are obtained. In most countries, including the United States, the patent term is 20 years from the earliest filing date of a non-provisional patent application. In the United States, a patent’s term may be lengthened by patent term adjustment, which compensates a patentee for administrative delays by the USPTO in examining and granting a patent, or may be shortened if a patent is terminally disclaimed over an earlier filed patent. The term of a patent that covers a drug or biological product may also be eligible for patent term extension when FDA approval is granted, subject to certain limitations and provided statutory and regulatory requirements are met (for more information, please see “Business—U.S. patent term restoration and marketing exclusivity”). In the future, if and when our product candidates receive approval from the FDA or foreign regulatory authorities, we expect to apply for patent term extensions on issued patents we may obtain in the future covering those products, depending upon the length of the clinical trials for each product and other factors. There can be no assurance that any of our pending patent applications will issue or that we will benefit from any patent term extension or favorable adjustment to the term of any of our patents.

13

Table of Contents

As with other biotechnology and pharmaceutical companies, our ability to maintain and solidify our proprietary and intellectual property position for our product candidates will depend on our success in obtaining effective patent claims and enforcing those claims if granted. However, our owned and licensed pending patent applications, and any patent applications that we may in the future file or license from third parties may not result in the issuance of patents. We also cannot predict the breadth of claims that may be allowed or enforced in our patents. Any issued patents that we may receive in the future may be challenged, invalidated or circumvented. In addition, because of the extensive time required for clinical development and regulatory review of a product candidate we may develop, it is possible that, before any of our product candidates can be commercialized, any related patent may expire or remain in force for only a short period following commercialization, thereby limiting protection such patent would afford the respective product and any competitive advantage such patent may provide.

In addition to patents, we rely upon unpatented trade secrets and know-how and continuing technological innovation to develop and maintain our competitive position. We seek to protect our proprietary information, in part, by executing confidentiality agreements with our collaborators and scientific advisors, and non-competition, non-solicitation, confidentiality, and invention assignment agreements with our employees and consultants. We have also executed agreements requiring assignment of inventions with selected scientific advisors and collaborators. The confidentiality agreements we enter into are designed to protect our proprietary information and the agreements or clauses requiring assignment of inventions to us are designed to grant us ownership of technologies that are developed through our relationship with the respective counterparty. We cannot guarantee, however, that these agreements will afford us adequate protection of our intellectual property and proprietary information rights.

We also seek trademark protection in the United States and internationally where available and when appropriate. We currently own U.S. federal registrations for the marks SOLID, SOLID GT and SOLID BIOSCIENCES and a European Union registration for the mark SOLID GT.

Strategic partnerships and collaborations/licenses

We have certain obligations under licensing agreements with third parties that include annual maintenance fees and payments that are contingent upon achieving various development, commercial and regulatory milestones. Pursuant to many of these license agreements, we are required to make milestone payments if certain development, regulatory and commercial sales milestones are achieved, and may have certain additional research funding obligations. Also, pursuant to the terms of many of these license agreements, when and if commercial sales of a licensed product commence, we must pay royalties to our licensors on net sales of the respective licensed products.

University of Washington License Agreement

In 2015, we entered into a license agreement with the University of Washington, acting through UW CoMotion, under which we obtained an exclusive, royalty-bearing, sublicensable, worldwide license under certain patent applications owned by the University of Washington relating to novel micro-dystrophins to develop, manufacture, and commercialize products for use in the treatment of DMD and related disease indications caused by a lack of functional dystrophin. We have the right to grant sublicenses to third parties contingent upon written approval by the University of Washington prior to executing such sublicense, which approval may not be unreasonably withheld.

In consideration for the rights granted by the agreement, we paid a one-time, non-refundable license fee, which was recorded as a research and development expense in 2015. We are required to reimburse the University of Washington for costs incurred in applying for, prosecuting and maintaining patents and pay up to an aggregate of approximately $1 million upon the achievement of certain milestones. There were no milestones achieved as of December 31, 2016 and 2015. In October 2017, the first milestone was achieved under this agreement. The

14

Table of Contents

milestone payment was recorded as a research and development expense in the fourth quarter of 2017. We must also pay royalties of a low single digit percentage of future sales by us and our sublicensees of products developed under the licensed patent rights. In addition, we must pay an annual maintenance fee until certain milestones are achieved, at which time a minimum annual royalty requirement will replace such maintenance fee and will apply to us and our sublicensees.

We are obligated to use our commercially reasonable efforts, consistent with sound and reasonable business practices and judgment, to commercialize the inventions covered by the licensed patent rights and to make and sell products based on that patent as soon as practicable and maximize sales thereof.

The University of Washington controls the prosecution and maintenance of the licensed patents in consultation with us and at our expense. In countries in which we have not requested prosecution or maintenance of licensed patents, the University of Washington may prosecute and maintain such licensed patents at its own cost. We have the first right to enforce such licensed patents at our expense. However, we may not enter into any settlement in any manner relating to the licensed patents without the University of Washington’s prior written consent.

The license agreement remains in effect until the expiration of the last-to-expire patent licensed under the agreement. We may terminate the agreement at any time upon providing sixty days’ written notice to the University of Washington. The University of Washington may terminate the agreement upon our uncured, material breach of the agreement or if we enter into an insolvency-related event.

The University of Missouri License Agreement

In 2015, we entered into a license agreement with the Curators of the University of Missouri, or the University of Missouri, a public corporation of Missouri, under which we obtained an exclusive, royalty-bearing, sublicensable, worldwide license under certain patents and patent applications owned by the University of Missouri relating to a novel synthetic microdystrophin gene to make, sell and distribute products for use in the treatment of DMD and related disease indications resulting from a lack of functional dystrophin.

In consideration for the rights granted by the agreement, we paid a one-time, non-refundable license fee, which was recorded as a research and development expense in 2015. We are required to reimburse the University of Missouri for costs incurred in applying for, prosecuting and maintaining the licensed patents and pay up to an aggregate of approximately $1 million upon the achievement of certain milestones for each product developed based on the licensed patents. There were no milestones achieved as of December 31, 2016 and 2015. In October 2017, the first milestone was achieved under this agreement. The milestone payment was recorded as a research and development expense in the fourth quarter of 2017. We must pay a royalty of a low single digit percentage of future sales by us or our sublicensees of products developed using the licensed patents. In addition, we must pay an annual maintenance fee until certain milestones are achieved, after which time a minimum annual royalty will replace such maintenance fee.

Under the agreement, we granted the University of Missouri a non-exclusive, royalty-free, irrevocable, paid-up license, with the right to grant sublicenses to non-profit, academic, educational or governmental institutions, to practice and use improvements made by us using the licensed patent rights, solely for non-commercial research purposes.

We are obligated to use our reasonable best efforts to introduce products based on the licensed patent rights into the commercial market as soon as possible, consistent with sound and reasonable business practices and judgment, and thereafter to keep such products reasonably available to the public.

The University of Missouri controls the prosecution and maintenance of the licensed patents in consultation with us and at our expense. In countries in which we have not requested prosecution or maintenance of licensed

15

Table of Contents

patents, the University of Missouri may prosecute and maintain such licensed patents at its own cost. We have the first right to enforce such licensed patents at our expense. However, any settlement, consent judgment or other voluntary disposition of litigation that materially limits the scope, validity or enforceability of the licensed patent or admits fault or wrongdoing on the part of the University of Missouri must be pre-approved in writing by the University of Missouri.

The license agreement remains in effect until the expiration of the last-to-expire patent or the abandonment of the last to be abandoned patent application licensed under the agreement. The University of Missouri may terminate the agreement, or render the license granted thereunder non-exclusive, in individual countries if we and our sublicensees fail to achieve certain milestones. We may terminate the license agreement at any time upon providing six months’ written notice to the University of Missouri and paying a termination fee. Each of the University of Missouri and we may also terminate the agreement for an uncured default or breach of the agreement by the other party. Our ability to cure such breach only applies to the first two notices of such breach provided by the University of Missouri, and thereafter, the University of Missouri may terminate the agreement for our default or breach of the agreement upon thirty days’ written notice without an opportunity to cure such default or breach.

The University of Michigan License Agreement

In 2016, we entered into a license agreement with the Regents of the University of Michigan, or the University of Michigan, a constitutional corporation of Michigan, under which we obtained an exclusive, royalty-bearing, sublicensable, worldwide license to make, sell and distribute products under certain patents owned by the University of Michigan related to microdystrophin and utrophin spectrin-like nucleic acid sequences for any use that, but for this agreement, would comprise an infringement of a valid claim included in the licensed patent rights.

In consideration for the rights granted by the agreement, we paid a one-time license fee and a separate fee to cover past patent prosecution costs. We recorded the upfront license fee as a research and development expense in 2016. We are required to reimburse the University of Michigan for costs incurred in applying for, prosecuting and maintaining patents, and pay up to an aggregate of approximately $1 million upon the achievement of certain milestones. There were no milestones achieved as of December 31, 2017 and 2016. We must also pay royalties of a low single-digit percentage of future sales by us or our sublicensees of products developed using the licensed rights, with a minimum annual royalty after certain milestones are achieved. In addition, we must pay an annual maintenance fee in any year in which the minimum annual royalty is not reached.

Under the agreement, the University of Michigan reserves for itself and its affiliates the right to use the licensed rights for non-commercial research, public service, internal and educational purposes and the right to grant the same limited non-commercial rights to other non-profit research institutions.

We are obligated to use commercially reasonable efforts to bring one or more products based on the licensed patents to market through a diligence program for utilizing the licensed patents, to continue diligent marketing efforts throughout the term of the agreement, and to make reasonable amounts of such products commercially available, in each case consistent with prudent business practices and judgment.

The University of Michigan controls the prosecution and maintenance of the licensed patents in consultation with us and at our expense. In countries in which we have not requested prosecution or maintenance of licensed patents, the University of Michigan may prosecute and maintain such licensed patents at its own cost. We have the first right to enforce such licensed patents at our expense. However, we may only enter into a settlement with the advice and consent of the University of Michigan.

The license agreement remains in effect until the expiration of the last-to-expire patent licensed under the agreement. The University of Michigan may terminate the agreement upon our uncured material breach of the

16

Table of Contents

agreement, including failure to make required payments under the agreement or to achieve certain milestones, or if we become insolvent or bankrupt. We may terminate the license agreement at any time upon providing sixty days’ written notice to the University of Michigan.

Harvard College License Agreements

In 2016 and 2017, we entered into license agreements with the President and Fellows of Harvard College, or Harvard College, under which we obtained non-exclusive, royalty-bearing, sublicensable, worldwide licenses to use certain intellectual property owned by Harvard College to develop, manufacture, and commercialize products for use in the treatment of DMD.

In consideration for the rights granted by each agreement, we paid one-time, non-refundable license fees, which were recorded as a research and development expense in 2016 and 2017. We are required to pay an annual license maintenance fee until certain milestones are achieved, after which time the annual maintenance fee will increase annually. Such annual maintenance fees will further increase if we grant certain rights to a sublicensee or strategic partner with whom we collaborate on the development and commercialization of licensed products. The annual maintenance fees are creditable against royalty payments. We also must pay milestone payments within thirty days after achieving certain milestones. There were no milestones achieved as of December 31, 2017 and 2016 under either agreement. We must pay a royalty on future sales by us or our sublicensees of products developed using the licensed technology.

The license agreements each remain in effect for an initial term of fifteen years, with automatic three-year renewal periods thereafter unless one of the parties provides notice of non-renewal. We may terminate the license agreements at any time upon providing sixty days’ written notice to Harvard College. Harvard College may terminate the agreements in the event we become bankrupt or insolvent. Both Harvard College and we may also terminate the agreements for an uncured material breach of the agreements by the other party.

Other License Agreements