Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - Lonestar Resources US Inc. | lone-ex322_12.htm |

| EX-32.1 - EX-32.1 - Lonestar Resources US Inc. | lone-ex321_6.htm |

| EX-31.2 - EX-31.2 - Lonestar Resources US Inc. | lone-ex312_10.htm |

| EX-31.1 - EX-31.1 - Lonestar Resources US Inc. | lone-ex311_8.htm |

| EX-23.2 - EX-23.2 - Lonestar Resources US Inc. | lone-ex232_669.htm |

| EX-23.1 - EX-23.1 - Lonestar Resources US Inc. | lone-ex231_670.htm |

| EX-21.1 - EX-21.1 - Lonestar Resources US Inc. | lone-ex211_9.htm |

| EX-10.11 - EX-10.11 - Lonestar Resources US Inc. | lone-ex1011_921.htm |

| EX-10.8 - EX-10.8 - Lonestar Resources US Inc. | lone-ex108_767.htm |

| EX-10.7 - EX-10.7 - Lonestar Resources US Inc. | lone-ex107_766.htm |

| 10-K - 10-K - Lonestar Resources US Inc. | lone-10k_20171231.htm |

Exhibit 99.2

February 20, 2018

Lonestar Resources US Inc.

111 Boland Street, Suite 300

Fort Worth, TX 76107

Re: Lonestar Resources US Inc.

Estimate of Reserves and Revenues

2017 SEC Year-End Pricing

“As of” December 31, 2017

Ladies and Gentlemen:

At your request, W.D. Von Gonten & Co. (Von Gonten) has prepared estimates of future reserves and projected net revenues for certain property interests owned by Lonestar Resources US Inc. (Lonestar). The reserves and income data were estimated in accordance with the definitions and disclosure guidelines of the United States Securities and Exchange Commission (SEC), including the reserves definitions of Rule 4-10(a)(1)(33) of Regulation S-X. Our third party study, completed on February 20, 2018, and presented herein, was prepared for public disclosure by Lonestar in filings made with the SEC in accordance with Item 1202(a)(8) of Regulation S-K.

The properties evaluated by Von Gonten account for 100% of Lonestar’s total net Proved reserves “as of” December 31, 2017.

The results of the study are summarized as follows:

Purpose of Report –The purpose of this report is to be used in connection with Lonestar’s public disclosures with the SEC, in accordance with SEC rules and regulations.

Scope of Work – W.D. Von Gonten & Co. was engaged by Lonestar to estimate the remaining reserves and future production forecasts associated with the producing and undeveloped properties included in this report. Once reserves were estimated, future net revenues were determined utilizing a provided 2017 SEC Year-End pricing scenario.

Reporting Requirements – Securities and Exchange Commission (SEC) Regulation S-K, Item 102 and Regulation S-X, Rule 4-10, and Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 932, Extractive Activities – Oil and Gas requires oil and gas reserves information to be reported by publicly held companies as supplemental financial information. These regulations and standards provide for estimates of Proved reserves and revenues discounted at 10% and based on constant prices and costs.

The Securities and Exchange Commission Regulation S-X definitions of proved reserves are as follows:

Proved Reserves; Securities and Exchange Commission Regulation S-X §210.4-10(a)(22)

Proved oil and gas reserves are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible—from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations—prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time.

Developed Reserves-Securities and Exchange Commission Regulation S-X §210.4-10(a)(6)

Developed oil and gas reserves are reserves of any category that can be expected to be recovered: (i) Through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well; and (ii) Through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by means not involving a well.

Undeveloped Reserves-Securities and Exchange Commission Regulation S-X §210.4-10(a)(31)

Undeveloped oil and gas reserves are reserves of any category that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion. (i) Reserves on undrilled acreage shall be limited to those directly offsetting development spacing areas that are reasonably certain of production when drilled, unless evidence using reliable technology exists that establishes reasonable certainty of economic producibility at greater distances. (ii) Undrilled locations can be classified as having undeveloped reserves only if a development plan has been adopted indicating that they are scheduled to be drilled within five years, unless the specific circumstances justify a longer time. (iii) Under no circumstances shall estimates for undeveloped reserves be attributable to any acreage for which an application of fluid injection or other improved recovery technique is contemplated, unless such techniques have been proved effective by actual projects in the same reservoir or an analogous reservoir, or by other evidence using reliable technology establishing reasonable certainty.

Projections – The attached reserves and revenue projections are on a calendar year basis with the first time period being January 1, 2018 through December 31, 2018.

Lonestar Resources US Inc. – SEC Price Case – February 20, 2018 – Page 2

Property Discussion

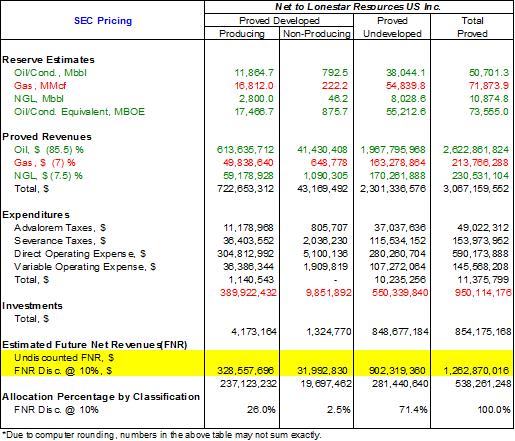

The Lonestar properties include producing and undeveloped locations located in Brazos, Dimmit, Fayette, Frio, Gonzales, Karnes, LaSalle, Lavaca, Robertson, and Wilson Counties, Texas. Lonestar currently owns interests in 238 Proved Developed Producing (PDP) wells, of which, 196 are horizontal Eagle Ford shale wells. Lonestar currently operates 175 of the total producing wells. As of December 31, 2017, the current gross production rates from all of the producing wells are approximately 7,600 barrels of oil and 12,100 Mcf of gas per day.

Currently, there are 170 Proved Undeveloped (PUD) locations to be completed in the Eagle Ford shale, of which, 162 will be operated by Lonestar. The first well is scheduled to start producing in March 2018.

Reserves Estimates

Producing and Non-Producing Properties – Reserve estimates for the PDP and Proved Non-Producing (PNP) properties were based on volumetric calculations, log analysis, decline curve analysis, and/or analogy to nearby production. Where applicable, these estimates were further supported by rate transit analysis and/or numerical reservoir simulation as part of a shale field study conducted by us independent of this report.

Undeveloped Properties – The undeveloped reserves were necessarily estimated using volumetric calculations, log analysis, core analysis, geophysical interpretation and reservoir simulation. In addition, W.D. Von Gonten & Co. has performed a field study of the Eagle Ford shale play independent of this report. Our conclusions from that field study have fortified our confidence in the producing and undeveloped reserves included herein.

Based on SEC reserves reporting requirements, only those undeveloped volumes scheduled to be drilled within five years of their initial recognition have been included within the Proved Undeveloped category of reserves.

Reserves and schedules of production included in this report are only estimates. The amount of available data, reservoir and geological complexity, reservoir drive mechanism, and mechanical aspects can have a material effect on the accuracy of these reserve estimates. Due to inherent uncertainties in future production rates, commodity prices, and geologic conditions, it should be realized that the reserve estimates, the reserves actually recovered, the revenue derived therefrom and the actual cost incurred could be more or less than the estimated amounts.

We consider the assumptions, data, methods, and procedures used in this report appropriate hereof, and we have used all such methods and procedures that we consider necessary and appropriate to prepare the estimates of reserves and future net revenues.

Product Prices

The estimated revenues shown herein were based on SEC Year-End pricing guidelines effective December 31, 2017. SEC pricing is determined by averaging the first day of each month’s closing price for the previous calendar year using published benchmark oil and gas prices. The provided scenario utilized for this report is a price of $51.34 per barrel of oil and $2.98 per MMBtu of gas. These prices were held constant throughout the life of the properties, as per SEC guidelines.

Pricing differentials were applied to all properties on an individual property basis in order to reflect prices actually received at the wellhead. Pricing differentials are typically utilized to account for transportation charges, geographical differentials, quality adjustments, any marketing bonuses or deductions, and any other factors that may affect the price actually received at the wellhead.

Lonestar Resources US Inc. – SEC Price Case – February 20, 2018 – Page 3

Lonestar provided historical pricing data for the twelve month time period ended November 2017. W.D. Von Gonten & Co. applied the historical averages extracted from the pricing data for this report. The natural gas liquids (NGL) price differential utilized in this evaluation was based on a comparison of the historical price received versus the average NYMEX oil price. The average realized prices, after applying the pricing adjustments, for the reserves included in this report are as set forth in the table below:

A gas volume shrinkage factor has been applied to each property. This shrinkage accounts for any line loss, generation of NGLs, and/or fuel usage before the actual sales point.

Operating Expenses and Capital Cost

|

Historical monthly operating expense data ranging from December 2016 through November 2017 for the properties were provided by Lonestar. W.D. Von Gonten & Co. applied a combination of fixed and variable monthly expenses to each individual property. |

Capital costs necessary to perform well completion operations and to develop undeveloped locations were supplied by Lonestar. Where available, these costs were verified from actual recent work in the area of interest and/or provided Authorities for Expenditures (AFEs).

All operating expenses and capital costs were held flat for the life of the properties in accordance with SEC guidelines.

Other Considerations

|

Abandonment Costs – Cost estimates regarding future plugging and abandonment procedures associated with these properties were supplied by Lonestar for the purposes of this report. As we have not inspected the properties personally, W.D. Von Gonten & Co. expresses no warranties as to the accuracy or reasonableness of this assumption. |

Additional Costs – Costs were not deducted for general and administrative expenses, depletion, depreciation and/or amortization (a non-cash item), or federal income tax.

Data Sources – Data furnished by Lonestar included basic well information, lease acreage maps, ownership interests, completion and drilling reports, pricing contracts, and daily production data. Public data sources such as IHS Energy and the U.S. Geological Survey (USGS) were used to gather any additional necessary data.

Context – We specifically advise that any particular reserve estimate for a specific property not be used out of context with the overall report. The revenues and present worth of future net revenues are not represented to be market value either for individual properties or on a total property basis. The estimation of fair market value for oil and gas properties requires additional analysis other than evaluating undiscounted and discounted future net revenues.

While the oil and gas industry may be subject to regulatory changes from time to time that could affect an industry participant’s ability to recover its oil and gas reserves, we are not aware of any such governmental actions which would restrict the recovery of the December 31, 2017 estimated oil and gas volumes. The reserves in this report can be produced under current regulatory guidelines. Actual future commodity prices may differ substantially from the utilized pricing scenario which may or may not extend or limit the estimated reserve and revenue quantities presented in this report.

Lonestar Resources US Inc. – SEC Price Case – February 20, 2018 – Page 4

We have not inspected the properties included in this report, nor have we conducted independent well tests. W.D. Von Gonten & Co. and our employees have no direct ownership in any of the properties included in this report. Our fees are based on hourly expenses and are not related to the reserves and revenue estimates produced in this report.

In summary, we consider the assumptions, data, methods and analytical procedures used in this report appropriate for the purpose hereof, and we have used all such methods and procedures that we consider necessary and appropriate to prepare the estimates of reserves herein. The Proved reserves included herein were determined in conformance with all applicable SEC rules and regulations, including all references to Regulation S-X and Regulation S-K, referred to herein collectively as the “SEC Regulations.” In our opinion, the Proved reserves presented in this report comply with the definitions, guidelines, and disclosure requirements as required by the SEC Regulations.

Thank you for the opportunity to assist Lonestar Resources US Inc. with this project.

|

Respectfully submitted, |

|

|

|

William D. Von Gonten, Jr., P.E. |

|

TX # 73244 |

|

|

|

Taylor D. Matthes |

|

|

|

|

|

|

Lonestar Resources US Inc. – SEC Price Case – February 20, 2018 – Page 5