Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - TRANS WORLD CORP | twoc-20171231ex23147eef6.htm |

| EX-32 - EX-32 - TRANS WORLD CORP | twoc-20171231xex32.htm |

| EX-31.2 - EX-31.2 - TRANS WORLD CORP | twoc-20171231ex312f089ad.htm |

| EX-31.1 - EX-31.1 - TRANS WORLD CORP | twoc-20171231ex311d99a80.htm |

| EX-21 - EX-21 - TRANS WORLD CORP | twoc-20171231ex21e608d59.htm |

rkkkkkkkkks€

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2017

or

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File No.: 000-25244

TRANS WORLD CORPORATION

(Exact name of Registrant as specified in its charter)

|

Nevada |

|

13-3738518 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Identification No.) |

|

545 Fifth Avenue, Suite 940 |

|

|

|

New York, New York |

|

10017 |

|

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (212) 983-3355

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐ NO ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-X is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐ |

Accelerated filer ☐ |

Non-accelerated filer (Do not check if a smaller reporting company) ☐ |

|

Smaller reporting company ☒ |

|

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ☐ NO ☒

The aggregate market value of the Common Stock of the Registrant held by non-affiliates as of June 30, 2017, based upon the average bid and asked price of $5.75 as reported on the OTCQB on that date, was $51,054,313.00. As of March 22, 2018, there were 8,879,011 shares of Common Stock of the Registrant deemed outstanding.

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the Registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. YES ☐ NO ☐

Documents incorporated by reference: None.

TRANS WORLD CORPORATION

FORM 1O-K

|

|

|

|

|

|

|

|

|

Page |

|

PART I. |

|

|

|

|

|

1 | ||

|

|

|

1 | |

|

|

|

1 | |

|

|

|

2 | |

|

|

|

2 | |

|

|

|

2 | |

|

|

|

3 | |

|

|

|

3 | |

|

|

|

3 | |

|

|

|

4 | |

|

|

|

5 | |

|

|

|

6 | |

|

|

|

6 | |

|

|

|

6 | |

|

|

|

9 | |

|

|

|

9 | |

|

|

|

12 | |

|

|

12 | ||

|

|

18 | ||

|

|

19 | ||

|

|

|

20 | |

|

|

|

20 | |

|

|

|

20 | |

|

|

|

21 | |

|

|

21 | ||

|

|

21 | ||

|

|

|

|

|

|

|

|

|

|

|

|

22 | ||

|

|

|

22 | |

|

|

|

23 | |

|

|

|

23 | |

|

|

|

Sales of Unregistered Equity Securities; Use of Proceeds from Registered Securities |

23 |

|

|

25 | ||

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

27 | |

|

|

|

27 | |

|

|

|

27 | |

|

|

|

27 | |

|

|

|

28 | |

|

|

|

29 | |

|

|

|

30 |

The following discussion should be read in conjunction with the consolidated financial statements and notes thereto included elsewhere in this Annual Report on Form 10-K. This Annual Report on Form 10-K contains certain forward-looking statements including expectations of market conditions, challenges and plans, within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and is subject to the Safe Harbor provisions created by that statute. Reference is made to Part I, Item 1A “Risk Factors” and to Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Forward Looking Statements” for a discussion of the Registrant’s qualifications with respect to certain information presented in this Annual Report on Form 10-K.

All references to “$” or “USD” means U.S. dollars, “€” or “EUR” means euros, and “Kč” or “CZK” means Czech korunas. Unless noted otherwise, all USD equivalents of foreign currency amounts are converted at the year-end, December 31, 2017 exchange rates.

General Development of Business

Trans World Corporation (hereinafter referred to as “we,” “us,” the “Company,” or “TWC” or terms of similar import) was organized as a Nevada corporation in October 1993 for the acquisition, development and management of gambling establishments, to the extent permitted by applicable local laws, featuring live and mechanized gaming, including video gaming devices such as video poker machines, primarily in Louisiana.

In 1998, we revised our operating strategy by shifting our focus to the casino market in Europe. Furthermore, as a means of diversification of our business, we have also expanded our growth strategy to develop and/or acquire small-to-mid-size hotels of 80-250 rooms located in or near key metropolitan and/or resort areas in Europe, which may also include gambling operations.

Today, we own and operate three full-service casinos and five hotels, all of which are four-star rated, as per the ratings from the Hotelstars Union, under the patronage of HOTREC, the umbrella association of hotels, restaurants and cafés in Europe, and covers hotel associations of Austria, the Czech Republic and Germany. Our European operating units are organized under two reportable segments: a casino segment and a hotel segment. Both segments are operated through our wholly-owned European subsidiaries.

Our casinos are all in the Czech Republic (“CZ”) and are part of the casino segment, located in Ceska Kubice (“Ceska”), Hate (“Route 59”), and Dolni Dvoriste (“Route 55”). The Czech casinos, which conduct business under our registered brand name, American Chance Casinos (“ACC”), are situated at border locations and draw the majority of their customers from Germany and Austria.

ACC’s operating strategy centers on differentiating its products and services from its direct competitors. We operate our establishments with an emphasis on high customer service and attention to details. We strive to create gambling environments with casual and exciting atmospheres, highlighting entertainment, state-of-the-art equipment, and professional service to our customers.

Our hotels include the Hotel Savannah and Spa, a 79-room, four-star deluxe hotel, located in Hate, Czech Republic, and is part of our casino segment as it is physically attached to our Route 59 casino; Hotel Columbus, a 117-room, four-star property located in Seligenstadt, Germany; Hotel Auefeld, a 93-room four-star hotel located in Hannoversch Münden (“Hann. Münden”), Germany; Hotel Kranichhöhe, a 107-room four-star hotel located in Much, Germany; and Hotel Donauwelle, a 176-room, four-star property located in Linz, Austria. All three German hotels and the Austrian hotel comprise our hotel segment.

Two of our units, Hotel Savannah and Spa and the Route 59 casino, operate as complementary businesses and are referred to jointly herein as the “Route 59 Complex.” In addition to the gaming area, guest rooms, and the spa, which is

1

operated by an independent contractor, the Complex features eight banquet halls for meetings and special events as well as two full-service restaurants and two bars.

On December 21, 2016, our wholly-owned German subsidiary, Trans World Hotels Germany GmbH (“TWHG”) acquired the Lindner Sport & Aktivhotel Kranichhöhe, a 107-room hotel with extensive meeting space and recreational amenities located in Much, Germany, for a purchase price of €4.9 million, or $5.3 million at the acquisition date. The Company subsequently rebranded the hotel as Hotel Kranichhöhe. The assets acquired by TWHG include: the hotel building and its contents; three food and beverage outlets; 18 meeting rooms; a wellness center and spa; a fitness center with an indoor swimming pool; an adjoining tennis complex with two indoor courts and two outdoor courts; and a beach volleyball court. The hotel is located approximately two hours driving time from the Company’s Hotel Columbus in Seligenstadt, near Frankfurt, and approximately three hours driving time from its Hotel Auefeld in Hann. Münden. We are investing approximately $1.9 million to update and partially renovate this hotel, including the refurbishment of a majority of the hotel’s guestrooms, installation of air conditioning in those rooms, refurbishment of the property’s conference space, and renovation of the hotel’s lobby. Approximately $1.1 million was spent in 2017, with the remainder to be disbursed in 2018. The hotel was upgraded to a four-star rating on June 27, 2017.

On March 1, 2017, TWC, through its wholly-owned Czech subsidiary, Trans World Hotels & Entertainment, a.s. (“TWH&E”) and TWHG jointly acquired 100% of the shares of Hotel Donauwelle Betriebsgesellschaft M.B.H, which owned a four-star business hotel located in Linz, Austria. The hotel is situated on the banks of the Danube River in Linz, approximately 35 minutes driving time from our Route 55 Casino. The assets acquired included the ground lease rights through March 2062 to the plot upon which the hotel building stands, and the building contents. The hotel features 176 rooms, six meeting/banquet rooms, a 120-seat restaurant, a 40-seat bar, a 100-seat outdoor terrace, and a spa and gym room. The hotel was under management contract with Steigenberger Hotels AG until September 30, 2017, when the contract was terminated. TWC assumed active management on October 1, 2017 and renamed the hotel as “Hotel Donauwelle” (herein referred to as “Hotel Donauwelle”).

TWC’s hotel operating strategy centers on offering both business and leisure travelers attractive facilities, professional service, comfortable accommodations, and a wide range of amenities, including food and beverage services, conference space, and recreational facilities. The Company uses multiple channels to actively market its hotels to both business and leisure travelers. Further, management strives to foster strong relationships with local businesses and communities, which primarily support the hotels’ food and beverage, conference and banquet, and recreation facilities.

While our principal executive offices are located in New York City, we have no operating presence in the United States.

Our corporate offices are located at 545 Fifth Avenue, Suite 940, New York, New York 10017, our telephone number is (212) 983-3355, our website is www.transwc.com and the ACC website is www.acc.cz. Neither website is a part of this Form 10-K.

TWC is engaged in the acquisition, development and management of niche casino operations in Europe, which feature gaming tables and mechanized gaming devices, such as video slot machines, as well as the acquisition, development and management of small-to-mid-size, four-star hotels, which may include casino facilities. Our expansion into the hotel industry is founded on management’s belief that hotels in the small-to-mid-size class are complementary to our casino brand, that opportunities in one of these two industries often lead to, or are tied to, opportunities in the other industry, and that a more diversified portfolio of assets gives us greater stability and makes TWC more attractive to potential investors. TWC’s top management executives include individuals with extensive experience in both the casino and hotel industries.

Market Overview and Competition

Historically, casinos in Germany and Austria have been characterized by formal atmospheres and a sense of exclusivity. While this dynamic has changed across Europe over time, ACC was at the forefront of the movement

2

towards more relaxed casino atmospheres. This, coupled with our emphasis on integrating live entertainment into the gambling experience and creating strong customer loyalty programs, allowed us to become a preferred alternative for many of our patrons. Further, we have established ACC as a reputable casino company in the Czech Republic through our twenty plus years of operations that has featured high service standards, consistent professionalism and strict adherence to all local gaming regulations.

As of December 31, 2017, five casinos operate in direct competition with our Ceska casino. Our Route 59 and Route 55 casinos currently have two and three direct competitors, respectively. Some of these competitors are larger and have financial and/or other resources that are greater than ours.

While we do not consider our gambling business to be seasonal, it is occasionally impacted by extreme weather conditions (see also Item 1A “Risk Factors — Climate impact”) and major sporting events, such as the FIFA World Cup (“World Cup”) and the UEFA Euro Cup (“Euro Cup,”), as well as regulatory changes, which have and can negatively impact attendance at our casinos.

We compete for guests based primarily on brand name recognition and reputation, location, customer satisfaction, quality of service, amenities, quality of the gaming experience, quality of our accommodations, room rates, security and the ability of our customers to earn and redeem loyalty program points. We believe that increased gambling in other locations in or near the market areas in which we operate, coupled with the increase in popularity of internet gambling, could create additional competition for us and could adversely affect our casino operations and development plans. Further, the gambling industry in Eastern Europe faces competition from a variety of sources for discretionary consumer spending, including spectator sports and other entertainment and gambling options. Competitive gambling activities include traditional casinos, video lottery terminals, state-sponsored lotteries and other forms of legalized and illegal gambling. We anticipate competition in this area will become more intense as the industry consolidates and new web-based ventures enter the industry.

With respect to our hotel segment, in Germany, Hotel Columbus has six competitors in the Seligenstadt area and surrounding region that it serves, four of which are privately-owned and two of which are part of German hotel chains. Hotel Auefeld is the largest hotel in Hann. Münden and no hotel chains are represented in that market. However, Hotel Auefeld does compete with eight smaller, privately-owned, competitors in the Hann. Münden area. Hotel Kranichhöhe has one direct competitor in the city of Much and three competitors in the surrounding areas. Hotel Donauwelle has six direct competitors in Linz.

Owing to our quality product, adherence to high standards of hospitality and customer service, professionalism and strict compliance with all local hotel regulations and governances, we believe that we can compete effectively with these hoteliers.

Costs and Effects of Environmental Compliance

We incurred no material costs or effects due to environmental compliance for the years ended December 31, 2017 and 2016.

The Company does not engage in research and development other than internal market research for general business development, does not account for research expenditures separately under generally accepted accounting principles, and did not incur any separate research and development expense for 2017 or 2016.

Available Information - Internet Access

TWC is a “smaller reporting company” under the rules of the Securities and Exchange Commission (“SEC”). Copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are available free of charge on or through our website (www.transwc.com) as soon as reasonably practicable after we electronically file the material with the SEC. In addition, the public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site

3

(www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers (including the Company) that file electronically with the SEC.

Ceska — The Ceska casino, which is located approximately one hour’s driving time from Regensburg, Germany, was acquired through a lease in March 1998 in conjunction with the Company’s entry into the casino market in Europe. On November 23, 2011, TWC purchased the Ceska casino building, associated land and an adjacent outbuilding and related plot from the town of Ceska Kubice, from which TWC had been renting the facilities. The acquisition allowed us to undertake much needed capital improvements to the building, as competition in the Ceska area has increased dramatically in recent years. As of March 26, 2018, the two-story Ceska casino offered 13 gaming tables, including seven card tables and six roulette tables. The casino also features 118 video slot machines and a dedicated stage area for live performances. Amenities also include a separate dining facility and five luxurious hotel guest rooms. The address of our Ceska casino is Ceska Kubice 64, Ceska Kubice 345 32, Czech Republic.

Route 59 — Located approximately one hour’s driving time from Vienna, Austria, and opened in December 1999, Route 59 was constructed by the Company on land that had been acquired by TWC in conjunction with our entry into the European casino market in 1998. On February 22, 2016, we completed expansion and reconfiguration of the casino’s existing slot area and introduced 32 additional video slot machines. As of March 26, 2018, our Route 59 casino operated 24 gaming tables, consisting of 12 card tables and 12 roulette tables, as well as 214 video slot machines. Route 59 is located at 199 American Way, Hate-Chvalovice, Znojmo 669 02, Czech Republic.

Route 55 — Located approximately 35 minutes driving time from Linz, Austria, and opened in December 2004, Route 55 was constructed by the Company on a parcel of land that had been purchased by TWC in April 2002. As of March 26, 2018, the two-story Route 55 offered 22 tables, including 12 card tables and 10 roulette tables, as well as 192 video slot machines. On the mezzanine level, the casino features an Italian restaurant, an open buffet area, and three luxurious hotel guest rooms. Similar to the five guest rooms at Ceska, these rooms, when not used as accommodations for our VIP players and guests, are rented to other customers. Route 55 is located at Grenzubergang Wullowitz, Dolni Dvoriste 382 72, Czech Republic.

Hotel Savannah — As a complement to our Route 59 gaming operations, in January 2009, we opened Hotel Savannah, a 77-room, four-star deluxe hotel, attached to Route 59 by the hotel’s restaurant, on land that had been acquired by TWC in conjunction with our entry into the European casino market in 1998. In conjunction with opening the hotel, we also launched a full-service spa, the Spa at Hotel Savannah, which is attached to the hotel and is sub-contracted to a local operator who pays TWC a percentage of its gross revenues. The Spa features a large, 22 x 8 meter, indoor pool and Ayurvedic therapy facility. Hotel Savannah also features eight banquet halls for meetings and events. On March 26, 2017, we added two additional guest rooms to the hotel room inventory, which now totals 79 rooms. The

4

creation of the Route 59 Complex has attracted additional business to the casino, contributing incremental cash, and enhancing the Company’s overall results.

Hotel Columbus — We acquired Hotel Columbus, a four-star 117-room hotel, located in Seligenstadt, a town that is approximately 25 minutes equidistant from Frankfurt city center and the Frankfurt International Airport, in September 2014. Hotel Columbus features five meeting rooms; a restaurant and separate breakfast room, each with its own kitchen; two bars; a 37-space parking garage; and 43 surface lot parking places, including a satellite parking area located across the street from the Hotel. With the coming withdrawal of the United Kingdom from the European Union (“EU”), the city of Frankfurt is aggressively soliciting British financial institutions to relocate their European operations to the city. Hotel Columbus is located at Am Reitpfad 4, 63500 Seligenstadt-Froschhausen, Germany.

Hotel Auefeld — Hotel Auefeld, a 93-room, four-star hotel with extensive meeting space and recreational amenities located in Hann. Münden, Germany, was acquired in June 2015. The hotel features three food and beverage outlets; ten meeting rooms; an adjoining 13,000 square foot event hall; an adjoining tennis complex with four indoor courts; and several additional recreation areas. An independent townhouse comprised of one four-room and one six-room apartment was also included in the assets associated with the transaction. Hotel Auefeld is located at Hallenbadstrasse 33, 34346 Hann. Münden, Germany.

Hotel Kranichhöhe — Hotel Kranichhöhe is a 107-room, four-star hotel that includes extensive meeting space and recreational amenities and is located in Much, Germany. The hotel features three food and beverage outlets; 18 meeting rooms; a wellness center and spa; a fitness center with an indoor swimming pool; an adjoining tennis complex with two indoor courts and two outdoor courts; and a “beach” volleyball court. The Company intends to invest approximately $1.9 million to update and partially renovate the hotel. TWC spent approximately $1.1 million of this budget in 2017 toward the renovation, with the balance to be expensed in 2018. Hotel Kranichhöhe, which was upgraded to a four-star rated hotel on June 27, 2017, is located at Boevingen 129, 53804 Much, Germany.

Hotel Donauwelle — Hotel Donauwelle is a 176-room, four-star hotel, situated on the banks of the Danube River in Linz approximately 35 minutes driving time from our Route 55 Casino. The hotel includes six meeting/banquet rooms, a 120-seat restaurant, a 40-seat bar, a 100-seat outdoor terrace, and a spa and gym, as well as indoor and outdoor parking areas. As a condition to our acquisition of the property, the lender required TWC to invest a minimum of €2.5 million (50% of which has been escrowed with the lender) to renovate the hotel within the first twelve months after acquisition, an action that we had previously determined to be necessary to make the property competitive in the marketplace. Due to high business volume (i.e. high room occupancy), TWC asked for, and was granted, an extension to the end of August 2018 to complete its planned renovation of the property. The first of a two-part room renovation was completed in August 2017, with 84 remaining rooms slated to be completed in July through August 2018. Hotel Donauwelle is located at Am Winterhafen 13, 4020 Linz, in the State of Upper Austria, Austria.

Our casinos each offer a restaurant, lounge areas, multiple bars and free parking. Our Hotel Columbus, Hotel Auefeld and Hotel Donauwelle properties offer indoor and outdoor parking for a nominal fee, and our Hotel Kranichhöhe property offers outdoor parking for a nominal fee. All of our hotels offer restaurant and lounge areas, bars, and meeting rooms. Our Hotel Savannah, Hotel Auefeld and Hotel Kranichhöhe also offer extensive recreational facilities. With the exception of the long-term ground leases for the plots on which Hotel Auefeld and Hotel Donauwelle each stands, we own the land and buildings that comprise our casino and hotel assets.

In the highly competitive gaming and hospitality industries in which we operate, our trade names and logos are important to the success of our business. All of our casinos operate under the trademarked trade name “American Chance Casinos,” which we believe has become synonymous in our markets with our reputation for excellence in service, casual fun, international presence and state-of-the-art gaming equipment. In addition, the Hotel Savannah’s flowering tree logo has come to represent luxury and convenience for our overnight guests at our Route 59 Complex. The Company also maintains separate websites for our casinos and four hotels that provide users with updated information about news and events, and for the hotels, the ability to make room reservations online.

5

With the acquisitions of Hotel Kranichhöhe and Hotel Donauwelle in 2016 and 2017, respectively, our current operations consist of three casinos and five hotels, with four units located in the Czech Republic, three units located in Germany, and one unit in Austria. Our recent geographic and industry diversification is consistent with our long-range objective of positioning TWC as an international hotel and casino company.

TWC, the senior management of which is composed of individuals who have extensive experience in both the hotel and casino industries, continues to explore ways to expand the Company’s operations through the acquisition and/or development of complementary gaming and hotel business units, while continuing to maximize the potential of the Company’s existing operations. Future additions may include stand-alone operations, or complexes with integrated hotel and casino operations, such as our Route 59 Complex.

During the year ended December 31, 2017, we maintained and enhanced our marketing and promotional programs for our casinos, focusing primarily on internal and customer-oriented loyalty reward programs and greater use of social media and digital communication methods. In 2017, we strove to offer higher-value amenities and to provide, in the case of our casinos, live entertainment, in an ongoing effort to secure and enhance our competitive position in the markets that we serve. The casinos’ event calendars concentrated on key, player-tested, popular events and holidays, while simultaneously focusing on higher player-incentive games designed to reward existing players with redeemable points via our Player’s Loyalty Program, and thereby promote customer loyalty. In addition, we continued to be a benefactor in a number of community and social programs during the year as a way to further promote our image and make a positive contribution to the communities in which we operate. We also continued our popular, cultural-themed and holiday-related parties, which feature live entertainment, raffles and complimentary grand buffets. Further, we aggressively targeted key cities in our media campaigns, most notably Vienna, Linz and Regensburg and the areas surrounding these cities for our casinos and Hotel Savannah. With respect to our three German hotels and one Austrian hotel, we focused our sales efforts on targeting corporate business and other market segments from the surrounding areas and neighboring countries, and worked to cultivate existing and new local and regional business relationships.

We are subject to numerous foreign international, national and local government laws and regulations, including those relating to the operation of a casino business, the operation of our hotel business, the preparation and sale of food and beverages, building and zoning requirements, data privacy and general business license and permit requirements, in the various jurisdictions in which we own and operate our properties. Our ability to acquire and/or develop new casino and/or hotel properties and to remodel, refurbish or add to existing properties is also dependent on obtaining permits from local authorities. We are also subject to laws governing our relationships with employees, including minimum wage requirements, overtime, working conditions, hiring and firing, non-discrimination for disabilities and other individual characteristics, work permits and benefit offerings. Compliance with these various laws and regulations can affect the revenues and profits of the properties we own and could adversely affect our operations. We believe that our businesses are conducted in compliance with all applicable laws and regulations.

On June 7, 2016, the President of the Czech Republic signed the 2017 Gambling Act (186/2016 Coll.) (the “Gambling Act”) and the 2017 Gambling Tax Act (187/2016 Coll.) (the “2017 Gambling Tax Act”) (collectively referred to as the “Gambling Acts”). The Gambling Acts became law on June 15, 2016, when they were published in the official Collection of Laws, maintained by the Czech Ministry of the Interior. The 2017 Gambling Tax Act became effective on January 1, 2017, and raised the gaming tax rate on technical game (i.e. slot machine or electromechanical roulette or dice) revenues to a “minimum tax,” and raised the tax rate from 28% to 35%, and eliminated the per diem fixed fee of Kč 80 (approximately $3.76) on each slot machine.

The 2017 Gambling Act introduced many new changes, requirements and conditions, that will become effective at various times, some taking effect on the date of enactment, some on January 1, 2017 and certain provisions taking effect upon the renewal of the casino operator’s gambling licenses. TWC’s 10-year federal gambling license was scheduled to expire at the end of 2018, and its one-year slot operating license expired at the end of 2017, the timing of

6

which required the Company to reapply for both gambling licenses under the new legislation. Therefore, TWC took all the proper measures to conform to the underlying requirements for each basic gambling license, one to cover live games and the other to cover technical games (e.g. slots). On November 15, 2017 and December 28, 2017, TWC received from the Ministry of Finance (“MOF”) its gambling licenses for live games and technical games, respectively. Further, on December 29, 2017, TWC was granted premises licenses in the three municipalities in which it operates. The Company is also awaiting the Ministry of Finance of the Czech Republic’s final interpretation of certain new measures, some of which were clarified in August 2016. The Company is also awaiting clarification from the MOF whether a recertification of its casino management system (“CMS”) is required following any upgrades to the CMS. The notable changes and requirements of the 2017 Gambling Act are as follows:

|

· |

Upon the effective date of the Gambling Act, any gambling operator may apply for a gambling license if it meets all of the following conditions, having: (i) an office in the Czech Republic, in another EU Member state or in a state that is a party to the Agreement on the European Economic Area; (ii) an organizational chart that sets clear and comprehensive definitions of jurisdictions and decision-making powers; (iii) an established board of directors or similar control body; (iv) equity of at least of €2,000,000 (approximately $2.4 million); (v) a transparent and unobjectionable origin of its financial resources; and (vi) a transparent ownership structure. During the licensing process, confirmation of corporate ownership of the Czech entity and required documents (e.g. criminal and tax records, etc.) from all members of the board of directors and representatives from all levels of the company structure must be furnished to the MOF. |

|

· |

A basic, general gambling license from the MOF will be issued for a maximum of six (6) years and a gambling license (i.e. premises license) for each location at which live game and technical game operations are conducted will be issued from local municipality councils for a maximum of three (3) years. Previously, the MOF general gambling licenses for live games had been issued for ten (10) years and for one (1) year for technical games. Licenses can be issued and/or renewed if the Company meets the following pre-existing conditions: (i) the Company and its representatives maintain a clean criminal record and all necessary certifications; (ii) the Company and its representatives pay their taxes and other necessary charges on time; (iii) the Company stays in good standing; (iv) the Company confirms its ability to comply with all technical and supervisory standards required by the new law; and (v) the Company does not disturb public order. As of December 31, 2017 and the date hereof, TWC was, and is in, compliance with these conditions and thereby has received all required licenses to operate. |

|

· |

Individual municipalities and their local councils will be entitled to issue decrees to prohibit or restrict gambling operations, to set permissible hours of gambling operations and designate locations of operations within their respective jurisdictions. Previously, municipalities, by decree, were allowed to ban gambling operations or set the locations of gambling operations within their respective jurisdictions. As of December 31, 2017 and the date hereof, TWC was, and is, in good standing with all of the municipalities in which it operates. |

|

· |

Gambling operations will not be permitted in proximity to certain premises, such as schools, children’s leisure facilities, health and social care facilities, churches or religious societies. As of December 31, 2017 and the date hereof, TWC’s existing casinos were, and are, in compliance with this requirement. |

|

· |

Gambling operators will be required to follow certain self-restricting measures put in place by individual players. For instance, an operator must create an individual account for each player, which the player can use to manage his/her gaming expenditures and frequency of play, including a maximum number of casino visits per month. These accounts must also allow players to set individual limits on gambling activities, including setting maximum bets per day or per calendar month or a maximum amount of net loss per day or per calendar month. Each customer’s identity must be checked against the MOF’s central database of individuals excluded from participation in gambling activities (i.e. blacklisted). For foreign citizens living in the Czech Republic (expats), the individual account would be valid for only 90 days, following which a reapplication would be required to setup the account. Some of these provisions will not become effective until one year after the MOF has published a complete technical specification of its central database (gambling operation information system), but the self-restriction provisions for technical games became effective immediately after new gambling licenses were obtained. In order to meet these self-restricting measures, the Company implemented a casino management system in all of its three casinos in August 2017. |

|

· |

Gambling operators will also be required to ban from entry individuals flagged by the MOF and registered in its central database as blacklisted or noted as being “destitute” and on public assistance, bankrupt, subject to an |

7

order banning them from gambling under Czech criminal law, or compulsive gamblers. As noted above, this provision will not become effective until one year after the MOF has published a complete technical specification of its central database (gambling operation information system). No one under age 18 will be allowed on the casino floor. As of December 31, 2017 and the date hereof, TWC was, and is, in compliance with this age requirement. |

|

· |

Gambling operators will not be able to provide for free, or at reduced prices, any benefits to players, including food, beverages, tobacco products or “stimulating substances.” TWC has been in full compliance with this requirement since January 1, 2018, when its new gambling licenses became effective. |

|

· |

Gambling operators will be required to post a sign on each technical game warning that gambling is “harmful”, advising of the amount of the player’s net losses and how long the player has been playing, with a requirement that there be a 15-minute break after every two hours of continuous play. In the event a player takes the obligatory break earlier than the elapse of two hours of continuous play AND the break is at least 15 minutes, then a new two-hour play period would start. However, if the break is shorter than 15 minutes, then the break will not qualify as the obligatory 15-minute break, and would not constitute a restart of the two-hour play period. TWC is in full compliance with this requirement. |

|

· |

All customer transactions, such as exchanging money for gambling chips, must be logged and those records must be kept for 10 years, up from five years under the previous law. TWC extended its record archiving to 10 years to comply with this requirement. |

|

· |

The required retention period of all required real time color audio/visual surveillance recordings will increase from three months to 24 months. The Company has installed new surveillance systems in all its casinos that meet this requirement. |

|

· |

Maximum bets for technical games will be increased to Kč 1,000 (about $45) from the current amount of Kč 675 (about $32) and maximum win (or jackpot) per slot machine will be decreased to Kč 500,000 (approximately $23,500) from the current amount of Kč 675,000 (approximately $31,700). Slot and electromechanical machine vendors/suppliers will be required to incorporate these limit changes into all slots and technical games that they sell/service to the casinos. Further, a law on limitation of cash payments imposes a maximum daily transaction limit of Kč 270,000 (or approximately $12,700) on cash transactions. Any slot jackpot payouts exceeding this limit on any given day can only be paid either directly to the player’s bank account or in two per diem payments where the player can pick up the remainder amount on the following day. TWC was and is in full compliance with this requirement since January 1, 2018, when its new gambling licenses became effective. |

|

· |

Casinos must have a minimum of three live games tables and 30 technical games available during operating hours. For each additional live game table, a casino may operate an additional 10 slot or technical game machines. If a casino has more than 10 live game tables, there is no limit on the number of slot or technical game machines permitted. All of TWC’s existing casinos each have more than 10 live game tables in operation and are, thereby, already in compliance with this requirement. |

|

· |

A gaming bond equal to Kč 10 million (approximately $470,000) will be required to be paid by a casino operator to the MOF for each of its casino units. For operators owning multiple casinos, a minimum bond of Kč 20 million (approximately $940,000) is required, up to a maximum of Kč 50 million ($2.3 million) for any licensee, regardless of the number of casinos owned and operated beyond five casino units. Previously, only one gaming bond of Kč 22 million ($1.0 million) was required, which was used for all of the existing licenses. As a condition to acquiring new gaming licenses, the Company provided a new gaming bond of Kč 30 million ($1.4 million) to meet the new bond requirements for its three casinos, resulting in a net increase of Kč 8 million (approximately $381,000) from its existing bond. Therefore, the casino operator must initially pledge additional funds to secure the new bond requirement, which, for TWC, will amount to Kč 30 million ($1.4 million). TWC posted the additional bond payment in December 2017. On March 7, 2018, the old gaming bond was cancelled by the MOF and the funds were released free and clear to the Company. |

|

· |

Beginning January 1, 2017, any marketing advertisements were required to have a written warning label in Czech language about the damage gambling can do to gambling participants and that gambling participants must be older than 18 years of age. As of December 31, 2017 and the date hereof, TWC is in full compliance with this requirement. |

|

· |

Failure to comply with the new Gambling Act could result in a misdemeanor punishable by fines up to |

8

Kč 1.0 million (approximately $45,000) or an administrative offense punishable by an injunction against the prohibited practice, fines up to Kč 50 million ($2.3 million) and/or asset forfeiture to, or confiscation by, the Czech government, or prohibition of activities in the most serious cases.

We have been, and are currently, in compliance with all such conditions that are currently in effect. See also “Taxation,” below.

There can be no assurance that such licenses, approvals or findings of suitability will be obtained in the future or will not be revoked, suspended or conditioned, or that we will be able to obtain the necessary governmental approvals for our future activities.

Pursuant to Section 13(r) of the Exchange Act, if during 2017, TWC or any of its affiliates have engaged in certain transactions with Iran or with persons or entities designated under certain executive orders, we would be required to disclose information regarding such transactions in our Annual Report as required under Section 219 of the Iran Threat Reduction and Syria Human Rights Act of 2012, or ITRA. Certain of the Iran sanctions were lifted on January 16, 2016. During 2017, the Company did not engage in any of the law’s enumerated transactions with Iran or with persons or entities related to Iran.

Gaming Taxes

As noted above, we are subject to legislative changes that, at times, result in material adverse effects on our results of operations and financial condition.

On June 7, 2016, the President of the Czech Republic signed the Gambling Acts. The 2017 Gambling Tax Act became effective on January 1, 2017. The new law raised the gaming tax rate on technical game (i.e. slot machine or electromechanical roulette or dice) revenues to the greater of a “minimum tax,” or 35%, and eliminated the per diem fixed fee of Kč 80 ($3.76) on each slot machine.

This new “minimum tax” on technical games is equal to the product of: (x) the sum of all gambling positions of individual approved terminal devices (such as slot machines, electromechanical roulette and dice machines) permitted for the location of the gambling premises, times (y) Kč 9,200 (approximately $432). Therefore, if the aggregate tax amount collected from the 35% gaming tax on technical game revenues is lower than the computed “minimum tax,” then the casino operator must pay the “minimum tax” and not the aggregate tax amount collected from the 35% gaming tax. Otherwise, if the aggregate tax amount collected from the 35% gaming tax on technical game revenues is greater than the computed “minimum tax,” then the casino operator need only pay the aggregate tax amount collected from the 35% gaming tax and not the “minimum tax.” The gaming tax rate on live game (i.e. cards, roulette or dice) revenues remains

9

unchanged at 23%. Further, the 2017 Gambling Tax Act modified the tax revenue allocation between the federal government and local municipalities. A summary table of the 2017 Gambling Tax Act is shown below:

|

|

|

2017 Gambling Tax Act |

|

(in actual amounts) |

|

(Effective from January 1, 2017) |

|

Live Games |

|

23% gaming tax from revenue earned from live games (70% of tax allocated to the federal government; 30% of tax allocated to the local municipality). |

|

|

|

|

|

Slot and other technical games |

|

The greater of either: (a) the aggregate amount collected from 35% gaming tax from revenue earned from slot and other technical games (35% of tax allocated to the federal government; 65% of tax allocated to the local municipality), or (b) a "minimum tax," calculated as the product of the sum of all gambling positions of individual approved terminal devices referred to in the permit for the location of the gambling premises times Kč 9,200 (approximately $432). |

|

|

|

|

|

Net Income |

|

No change from the 19% corporate income tax noted below. |

On December 15, 2015, the President of the Czech Republic signed an amendment to the Gaming Law that increased gaming tax rates payable by all gaming operators, including TWC, effective January 1, 2016 (the “2016 Gaming Tax Amendment”). (See TWC’s Form 8-K, dated December 21, 2015). As a result of this amendment, gaming taxes on live game revenues increased from 20% to 23% and gaming taxes on slot revenues increased from 20% to 28%. In addition, the amendment increased the fee per slot machine per day to Kč 80 ($3.76) from Kč 55 ($2.58). The amendment became law on December 28, 2015, when it was published as Act No. 380/2015 Coll. in the official Collection of Laws, maintained by the Czech Ministry of the Interior.

10

|

|

|

2016 Gaming Tax Amendment |

|

(in actual amounts) |

|

(Effective from January 1, 2016 to December 31, 2016) |

|

Live Games |

|

23% gaming tax from revenue earned from live games (70% of tax allocated to the federal government; 30% of tax allocated to the local municipality). |

|

|

|

|

|

Slots |

|

28% gaming tax from revenue earned from slot games (20% of tax allocated to the federal government; 80% of tax allocated to the local municipality); and a per diem fixed fee of Kč 80 ($3.76) per slot machine (allocated to the federal government). |

|

|

|

|

|

Net Income |

|

No change from the 19% corporate income tax noted below. |

TWC’s gaming-related taxes and fees for the years ended December 31, 2017 and 2016 are summarized in the following table:

|

|

|

For the Year Ended |

|

||||

|

(amounts in thousands) |

|

2017 |

|

2016 |

|

||

|

|

|

|

|

|

|

|

|

|

Gaming revenues (excl. ancillary revenues) |

|

$ |

37,462 |

|

$ |

44,967 |

|

|

|

|

|

|

|

|

|

|

|

Gaming taxes |

|

$ |

11,754 |

|

$ |

12,398 |

|

|

Gaming taxes as % of gaming revenues (above) |

|

|

31.4 |

% |

|

27.6 |

% |

Gaming taxes are payable by the 25th day following the end of each calendar quarter, while corporate income tax is paid by June 30th of the subsequent year. Estimated quarterly income tax payments are also required since the third quarter of 2013. TWC was current on all of its Czech tax payments at December 31, 2017 and through the date of this report.

Corporate Income Taxes

Effective January 1, 2012, in conjunction with other changes to gaming tax rates, the Czech government instituted an effective corporate income tax, currently 19.0%, on all income, including gaming income. Prior to the law change, our Czech casino operations were subject only to gaming taxes. The income tax rate in Germany is approximately 30.0%. We have no gambling operations in Germany as of the date of the Annual Report. For the year ended December 31, 2017, the Company incurred a total net income tax expense of approximately $1.1 million, inclusive of a deferred income tax liability of $367,000. The prior year income tax expense of approximately $2.7 million included a deferred income tax benefit of $130,000. We did not incur any corporate income taxes in Germany from our hotel operations for the years ending December 31, 2017 and 2016, due to the consolidated losses arising from acquisition-related closing costs incurred in these two years.

On December 22, 2017, H.R. 1, originally known as the Tax Cuts and Jobs Act (the “TCJA”), was enacted in the United States. The TCJA made many significant changes to the U.S. federal income tax laws applicable to businesses and their owners, including stockholders of publicly traded corporations. Pursuant to this legislation, as of January 1, 2018, among other things, (i) the federal income tax rate applicable to corporations is reduced to 21%; (ii) the highest marginal individual income tax rate is reduced to 37% (through taxable years ending in 2025); (iii) the corporate alternative minimum tax is repealed; (iv) the backup withholding rate for U.S. stockholders is reduced to 24% and; (v) there is a migration from a “worldwide” system of taxation to a territorial system. The deduction of net interest expense is limited for all businesses; provided that certain businesses may elect not to be subject to such limitations and instead to depreciate their real property related assets over longer depreciable lives. The reduced 21% federal income tax rate applicable to corporations will apply to taxable earnings reported for the full 2018 fiscal year. As a result of this legislation, the Company remeasured its deferred tax assets and liabilities based on the rates at which they are expected to reverse in the future, which is generally 21%. The Company is still analyzing certain aspects of the TCJA and refining

11

its calculations, which could potentially affect the measurement of these balances or potentially give rise to new deferred tax amounts. The provisional amount recorded related to the remeasurement of the Company’s deferred tax balances was $2,810 which was offset fully by the provisional amount recorded related to the reversal of previously established valuation allowances against these deferred tax balances. In addition, the Company recognized $5,203 of tax expense related the deemed repatriation of foreign accumulated earnings.

We are still in the process of evaluating the income tax effect and other changes required by the TCJA that will be effective for our fiscal year 2018. Because we do not generate earnings in the United States, we have not paid U.S. corporate income taxes in 2017 or 2016.

Value Added Taxes

In conformity with the EU taxation legislation, the Czech Republic’s value added tax (“VAT”) has gradually increased from 5%, when that country joined the EU in 2004, to 21%, the effective rate since 2013. Unlike in other industries, VATs are not recoverable for gaming operations. The recoverable VAT under the hotel segment was not material for the years ended December 31, 2017 and 2016, respectively.

As of December 31, 2017, we had a total of 629 full and part-time employees, of which 83 work in Ceska; 168 in Route 59; 125 in Route 55; 45 in Hotel Savannah; 32 in Hotel Columbus; 48 in Hotel Auefeld; 56 in Hotel Kranichhöhe; 43 in Hotel Donauwelle; 24 in our shared services offices, located in our Ceska Casino; and five in the Company’s headquarters in New York City, New York. None of our employees are represented by a union nor are we a party to any labor contract.

We have described below what we currently believe to be the material risks and uncertainties in our business.

Before making an investment decision with respect to our Common Stock, you should carefully consider the risks and uncertainties described below, together with all of the other information included or incorporated by reference in this Annual Report on Form 10-K, including Item 7A. “Quantitative and Qualitative Disclosures About Market Risk.” We also face other risks and uncertainties beyond what is described below. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business. Further, past financial performance may not be a reliable indication of future performance and historical trends should not be used to anticipate results or trends in future periods. This Annual Report on Form 10-K is qualified in its entirety by these risk factors. If any of the following risks actually occur, our business, financial condition, results of operations and prospects could be materially and adversely affected. If this were to happen, the value of our Common Stock could decline significantly. You could lose all or part of your investment.

The proposed Merger may not be completed within the expected timeframe, or at all, and the failure to complete the Merger could adversely affect our business, operating results, liquidity and financial condition, and the price of our Common Stock.

On March 2, 2018, the Company entered into an Agreement and Plan of Merger (the ‘‘Merger Agreement’’) with FEC Overseas Investment (UK) Limited, a limited company formed under the laws of the United Kingdom (the “Parent”), and FEC Investment (US) Limited, a Nevada corporation and wholly-owned subsidiary of Parent and Far East Consortium Limited, a Cayman Islands limited company that is party solely for the limited purposes set forth in the Merger Agreement. The Merger Agreement is an executory contract subject to closing conditions beyond our control, and there is no guarantee that these conditions will be satisfied in a timely manner or at all. Completion of the Merger is subject to various conditions. If any of the conditions to the proposed Merger are not satisfied (or waived by the other party), the Merger may not be completed. In addition, we could be required to pay to the Parent a fee equal to $1,500,000 or transaction expenses up to $700,000 in the aggregate, if the Merger Agreement is terminated under certain limited circumstances more thoroughly described in the Merger Agreement. If we fail to complete the Merger our business,

12

operating results, liquidity and financial condition, and the price of our common stock, could be materially adversely affected.

Regulation and licensing

Our gambling operations are subject to regulation by each federal and local jurisdiction in which we operate. Each of our officers may be subject to strict scrutiny and approval from the gaming commission or other regulatory body of each jurisdiction in which we conduct gambling operations. Furthermore, the operations of our casinos are contingent upon maintaining all necessary regulatory licenses, permits, approvals, registrations, findings of suitability, orders and authorizations. The laws, regulations and ordinances requiring these licenses, permits and other approvals generally relate to the operations of the casinos, the payment of taxes, the responsibility, financial stability and character of the owners and managers of gambling operations, as well as persons financially interested or involved in gambling operations. All of our casinos are duly licensed by the MOF, and we are subject to ongoing regulation to maintain these operations.

Czech regulatory authorities have broad powers to request detailed financial and other information, to limit, condition, suspend or revoke a registration, gaming license or related approval and to approve changes in our operations. The suspension or revocation of any license which may be granted to us could significantly harm our business, financial condition, results of operations and prospects. Any change in the laws, regulations or licenses applicable to our business or a violation of any current or future laws or regulations applicable to our business or gaming licenses could require us to make substantial expenditures or could otherwise negatively affect our gambling operations.

Potential changes in legislation and regulation of our operations

Laws and regulations governing the conduct of gambling activities and the obligations of gaming companies in any jurisdiction in which we have or in the future may have gambling operations are subject to change and could impose additional operating, financial or other burdens on the way we conduct our business.

In early January 2016, the MOF imposed a ban on certain types of marketing and promotional events, under the stipulation that the operation of these promotional events were in violation of gaming law. The ban affected all casinos operating in the Czech Republic. In late September 2016, the MOF reversed its position and removed the ban for all casino operators. Although the temporary ban did not materially affect the Company’s casino operating results, any other similar actions by the MOF could have a negative impact on the Company’s business, operating results and prospects.

Moreover, legislation to prohibit, limit, or burden our gambling business have been introduced via the recent Gambling Acts and may be further introduced in the future in the Czech Republic or elsewhere where gambling has been legalized. In addition, from time to time, legislators and special interest groups (which may include our competitors) have proposed legislation that would expand, restrict or prevent gambling operations or which may otherwise adversely impact our operations in the jurisdictions in which we operate. Any expansion of gambling or restriction on or prohibition of our gambling operations, increase in gaming taxes, or enactment of other adverse regulatory changes could have a material adverse effect on our business, financial condition, operating results and prospects.

In addition to the Gambling Acts that were passed on June 7, 2016 and effective for the calendar year 2017 and forward, there may be other proposed legislation and/or amendments to these Gambling Acts that may further increase the constraints and limitations on our operations. We cannot, as of the date of this report, specifically predict any proposed legislation or its effect on the results of operations or financial condition or business prospects of the Company.

Taxation of gambling operations

Gambling operators are typically subject to significant taxes, which may increase at any time. Material increases in these taxes or fees have and would adversely affect our business, results of operations, financial condition and prospects. The Czech Republic currently has a number of laws related to various taxes imposed by governmental authorities. Applicable taxes include VAT, gaming tax, corporate income tax, and payroll (social) taxes. In December 2011, the Czech government passed sweeping gaming tax legislation that became effective in 2012. In this new tax law, the government eliminated the “charity contribution tax” scheme and, in lieu of it, changed the existing

13

revenue-based, tiered rate gaming tax structure to a flat 20% gaming tax on all gambling revenues, plus an applicable corporate income tax of 19% on adjusted net income derived from any revenue sources, including gambling. These tax law changes have negatively and materially impacted our results of operations since 2012.

In December 2015, the Czech government passed an amendment to the gaming tax law which effectively and significantly raised the gaming tax rates. The amendment was effective for the calendar year 2016 and forward. See also “Gaming Tax” section under “Taxation” above. These tax law changes, together with other legal compliance areas (for example, customs and currency control matters) are subject to review and investigation by a number of different Czech governmental authorities, which are authorized by law to impose fines, penalties and interest charges. These reviews may create additional tax risks that, if applied to TWC, could have a material adverse effect on our business, results of operations, financial condition and prospects.

On June 7, 2016, the President of the Czech Republic signed the Gambling Acts. The Gambling Acts became law on June 15, 2016, when they were published in the official Collection of Laws, maintained by the Czech Ministry of the Interior. The 2017 Gambling Tax Act became effective on January 1, 2017, raised the gaming tax rate on technical game (i.e. slot machine or electromechanical roulette or dice) revenues to a “minimum tax,” raised the tax rate from 28% to 35%, and eliminated the per diem fixed fee of Kč 80 ($3.76) on each slot machine. See “Taxation – Gaming Taxes,” above. This new tax law will have a material adverse effect on our net income for our fiscal year ended December 31, 2017.

General economic trends are unfavorable

The worldwide economic downturn in 2009 and the anemic economic growth that followed as well as the current debt and immigrant and terrorism crises in the EU has, and may, in the future, continue to have a negative impact on our financial performance. Lingering adverse economic conditions in local, regional, national and global markets could negatively impact our operations in the future. During periods of economic contraction like that recently experienced, certain costs can remain fixed or even increase, while revenues decline. The gambling services we provide are similar to other leisure activities in that they depend on personal discretionary expenditures, which are likely to decline during economic downturns. Continued adverse developments affecting economies throughout the world, and particularly in Europe, including a general tightening of the availability of credit, increasing interest rates, unemployment, deflation, political or economic turmoil, government debt crises, acts of war or terrorism, natural disasters, declining consumer confidence or significant declines or volatility in world stock markets could lead to a further reduction in discretionary spending on entertainment and leisure activities, which could adversely affect our business, financial condition, results of operations and prospects. In some cases, even the perception of an impending economic downturn or the continuation of a recessionary climate can be enough to discourage consumers from spending on leisure activities. We cannot predict at this time what the full effect and extent of the extended period of slow-growth in Europe will be on our business, financial condition, or results of operations.

We face significant competition

We operate in the highly competitive gaming industry with a large number of participants, many of which have financial and other resources that are greater than ours. The gaming industry faces competition from a variety of sources for discretionary consumer spending including spectator sports and other entertainment and gaming options, as well as home entertainment alternatives. Competitive gambling activities include traditional casinos, video lottery terminals, internet gaming, sports betting, state-sponsored lotteries and other forms of legalized and illegal gambling in the Czech Republic, Germany, Austria and in other jurisdictions. Moreover, these established gambling jurisdictions could award additional gaming licenses or permit the expansion of existing gambling operations. If additional gaming opportunities become available near our operations, such gaming opportunities could have a material, adverse impact on our business, financial condition, results of operations and prospects.

Additionally, internet gaming and wagering is growing rapidly and is affecting competition in our industry. Web-based businesses may offer consumers a wide variety of events to wager on, including other games, racetracks, sporting and even e-sporting events. Unlike most web-based gaming companies, we pay taxes in the jurisdictions in which we operate and our operations require ongoing capital expenditures for both their continued smooth operations, maintenance, renovation and growth. We could also face significantly greater costs in operating our business compared

14

to these “virtual” internet gaming companies. We cannot offer the same number of gaming options as internet-based gaming companies. Many internet-based gaming companies are located off-shore and avoid regulation under applicable Czech laws. These companies may divert wagering dollars from live wagering venues, such as our casinos. The continued growth and success of these on-line ventures could have a material, adverse impact on our business, financial condition, results of operations and prospects.

Our principal hotel competitors are other operators of full-service and select-service properties, including other major hospitality chains with well-established and recognized brands and integrated reservation systems. We also compete against smaller hotel chains and privately owned hotels. If we are unable to compete successfully, our revenues or profits may decline or our ability to maintain or increase our market share may be diminished. We compete for guests based primarily on location, customer satisfaction, room rates, quality of service, amenities, and quality of accommodations. Most of our competitors are larger than we are, based on the number of properties they manage, franchise or own, or based on the number of rooms or geographic locations where they operate. Many of our competitors also have recognizable brands, participate with online travel merchants and have a large number of members participating in their guest loyalty programs which may enable them to attract more customers and more effectively retain such guests. Our competitors generally also may have greater financial and marketing resources than we do, which could allow them to improve their properties and expand their marketing efforts in ways that could affect our ability to compete for guests effectively. If we are unable to successfully compete against competitors in our market areas, it will have a material adverse effect on our business, financial condition, results of operations and business prospects.

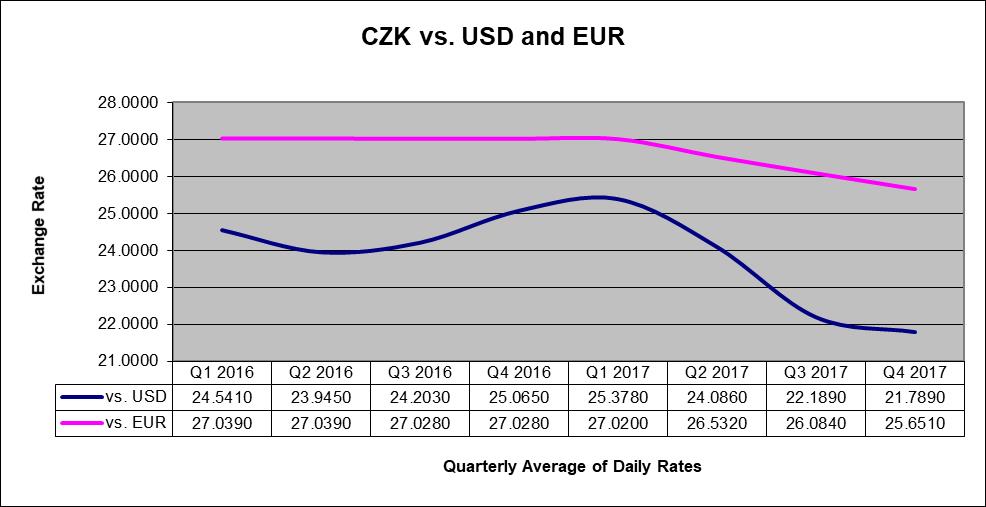

Fluctuations in currency exchange rates could adversely affect our business

Our facilities in the Czech Republic represent a significant portion of our business, and the revenue generated is generally denominated in EUR and the expenses incurred by these facilities are largely denominated in CZK, while revenues and expenses from our three hotels in Germany and one hotel in Austria are denominated in EUR. The potential depreciation in the value of either of these currencies against the USD would adversely impact the revenue and operating profit from our operations when translated into USD, which would have a corresponding effect on our consolidated results of operations. (See also “Item 7A. Quantitative and Qualitative Disclosure about Market Risk — Foreign Currency Exchange Rate Risk”). We do not currently hedge our exposure to fluctuations of these foreign currencies, and there is no guarantee that we will be able to successfully hedge any future foreign currency exposure, if we subsequently choose to do so in the future.

We are subject to the business, financial and operating risks inherent to the hospitality industry

Our hotel segment is subject to a number of business, financial and operating risks inherent to the hospitality industry, including:

|

· |

financing risks, including the risk of leverage and the corresponding risk of default on our existing indebtedness and potential inability to refinance or extend the maturities of our existing indebtedness; |

|

· |

levels of spending for business and leisure travel, as well as consumer confidence; |

|

· |

changes in consumer trends and preferences, particularly by younger consumers; |

|

· |

changes in taxes and governmental regulations that influence or set wages, prices, interest rates or construction and maintenance procedures and costs; |

|

· |

hostilities, including future terrorist attacks, or fear of hostilities that affect travel; |

|

· |

the degree and nature of our competition, including their marketing power, loyalty programs and integrated reservation systems, most of which may be more advanced and better financed than ours; |

|

· |

the costs and administrative burdens associated with complying with applicable laws and regulations; |

|

· |

the costs or desirability of complying with local practices and customs; |

|

· |

the availability and cost of capital necessary for us to fund acquisitions, investments, capital expenditures and service debt obligations; |

15

|

· |

delays in or cancellations of planned or future acquisition or development projects; |

|

· |

foreign exchange rate fluctuations; |

|

· |

changes in operating costs, including, but not limited to, interest rates, energy, food, workers’ compensation, benefits, insurance and unanticipated costs resulting from statutory requirements and/or force majeure events; |

|

· |

increases in cost for healthcare coverage for employees and potential government regulation in respect of health coverage; |

|

· |

shortages of labor or labor disruptions; |

|

· |

shortages of desirable locations for acquisition or development; |

|

· |

unrealistic purchase prices set by vendors; and |

|

· |

the ability of third-party internet travel intermediaries to attract customers for our properties. |

Any of these factors could substantially decrease customer stays, increase our costs of doing business or limit or reduce the prices we charge for our hospitality products or services, including the rates our properties charge for accommodations. These factors can also affect our ability to develop or acquire new properties or maintain and operate our existing properties. As a result, any of these factors can reduce our profits and limit our opportunities for growth. Many of these risk factors apply to our casino segment as well.

Need to diversify

Prior to 2014, all of our operations were primarily located in the Czech Republic. Therefore, any future adverse legislation in the Czech Republic may have an adverse impact on our Czech operations, financial results, financial condition and prospects. In an attempt to minimize this risk, we acquired Hotel Columbus in Seligenstadt, Germany, in September 2014, Hotel Auefeld in Hann. Münden, Germany, in June 2015, Hotel Kranichhöhe in Much, Germany, in December 2016, and Hotel Donauwelle in Linz, Austria, in March 2017. However, all of our operations are in the EU and are exposed to legislative risk from the Council of the European Union, as well as from the individual countries in which we operate.

Need for additional financing

Pursuant to our growth strategies, we may require additional debt and/or equity financing for the acquisition and development of new businesses or business units. We may also need to access the capital markets or otherwise obtain additional funds to finance acquisitions, the continuing maintenance, renovation, or re-theming of currently owned facilities or the development of new operations. There is no guarantee that we will be able to obtain such financing or funds in the future on favorable terms to us, or at all.

Dependence upon key personnel

Our ability to successfully implement our strategy of expansion, manage the existing casinos, and maintain a competitive position will continue to depend, in large part, on the services of Mr. Rami S. Ramadan, the Company’s President and Chief Executive Officer (“CEO”). The Company is also dependent upon other key employees, casino managers, and consultants, whom we retain from time to time.

International activities

Our operations are completely outside of the United States. Operating internationally involves additional risks including, but not limited to currency exchange rates, different legal or regulatory environments, political and economic risks relating to the stability or predictability of foreign governments, differences in the manner in which different cultures do business, difficulties in staffing and managing foreign operations, differences in financial reporting, operating difficulties, terrorism, different types of criminal threats and other factors. The occurrence of any of these risks, if severe enough, could have a material adverse effect on our business, financial condition, results of operations, and prospects.

16

Climate impact

The operations of our facilities are subject to disruptions or reduced patronage as a result of severe weather conditions, natural disasters and other casualty events, including loss of service due to casualty, forces of nature, mechanical or electrical or telecommunications failure, traffic and road conditions, extended or extraordinary maintenance, flood, wind, snow, ice or other severe weather conditions. As the majority of our casino clientele travel from German and Austrian border regions by automobile, we are highly dependent on the volume and frequency of these players’ visitations. Inclement weather conditions on the roads to our casinos can serve to substantially reduce the number of visitations, which occurred between December 2016 and February 2017. On the other hand, warm and favorable outdoor weather can also divert players to alternative activities, such as family outings. The frequency and strength of any of these aforementioned climate conditions could have a material adverse effect on our business, financial condition, results of operations, and prospects.

Liability insurance

We may not have sufficient insurance coverage in the event of a catastrophic property or casualty loss. We may also suffer disruption of our business in the event of a terrorist attack (at our premises or elsewhere), or other catastrophic property or casualty loss, or be subject to claims by third parties injured or harmed while visiting our locations. While we currently carry adequate general liability insurance and business interruption insurance, such insurance may not be sufficient to cover all losses in such event.

We do not currently have cyber insurance policies to provide supplemental coverage above the coverage of our general liability insurance policies. Despite various precautionary steps to protect our casinos and hotels from losses resulting from cyber-attacks, however, any occurrence of a cyber-attack could result in losses at our properties, which could affect our operations. To date, we are not currently aware of any cyber incidents that we believe to be material or that could have a material adverse effect on the business, financial condition, results of operations or prospects of the Company.

No dividends

We have not paid any dividends to date on our Common Stock. Currently, our plan is to retain future earnings, if and when generated, for investment in our current operations and for future project developments. Any future determination to pay dividends will be at the discretion of TWC’s Board of Directors (our “Board”) and will depend on our financial condition, capital requirements, restrictions contained in current or future financing instruments and such other factors as our Board deems relevant. See the “Dividend” section of Item 5. “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities — Dividends.”

Dilutive effect of options, restricted stock and deferred stock compensation

As of March 26, 2018, there were options outstanding to purchase 665,000 shares of our Common Stock, plus 734,232 shares issuable under the Company’s Deferred Compensation Plan and 25,000 shares of performance-tied restricted stock, which, if all were vested and exercised, would represent 13.8% of the 10,303,243 fully-diluted shares outstanding as of such date. The issuance of such securities would have a dilutive effect on any earnings per share that we may generate when the earnings per share are evaluated on a fully-diluted basis.

Possible adverse effect of issuance of preferred stock