Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - FENNEC PHARMACEUTICALS INC. | tv488216_ex99-1.htm |

| EX-32.1 - EXHIBIT 32.1 - FENNEC PHARMACEUTICALS INC. | tv488216_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - FENNEC PHARMACEUTICALS INC. | tv488216_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - FENNEC PHARMACEUTICALS INC. | tv488216_ex31-1.htm |

| EX-23.2 - EXHIBIT 23.2 - FENNEC PHARMACEUTICALS INC. | tv488216_ex23-2.htm |

| EX-23.1 - EXHIBIT 23.1 - FENNEC PHARMACEUTICALS INC. | tv488216_ex23-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _____ to _____

Commission File Number: 001-32295

FENNEC PHARMACEUTICALS INC.

(formerly ADHEREX TECHNOLOGIES INC.)

(Exact Name of Registrant as Specified in Its Charter)

| British Columbia, Canada (State or Other Jurisdiction of Incorporation or Organization) |

20-0442384 (I.R.S. Employer Identification No.) |

| PO Box 13628, 68 TW Alexander Drive Research Triangle Park, NC (Address of Principal Executive Offices) |

27709 (Zip Code) |

(919) 636-4530

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO þ

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO þ

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

YES þ NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company þ | Emerging growth company ¨ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO þ

The aggregate market value of the voting stock held by non-affiliates of the Registrant, computed by reference to the closing sales price of the Common Shares as reported by the OTCQB on June 30, 2017 (the last business day of the Registrant’s most recently completed second fiscal quarter) was $45,267,296 based upon a total of 7,128,708 shares held as of June 30, 2017 by persons believed to be non-affiliates of the Registrant (for purposes of this calculation, all of the Registrant’s officers, directors and 10% owners known to the Company are deemed to be affiliates of the Registrant).

As of March 16, 2018, there were 18,464,706 shares of the Registrant’s common shares outstanding.

FENNEC PHARMACEUTICALS INC.

2017 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements that involve significant risks and uncertainties. Our actual results, performance or achievements may be materially different from any results, performance or achievements expressed or implied by such forward-looking statements. Words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “estimate,” “project,” “plan,” and other similar words are one way to identify such forward-looking statements. Forward-looking statements in this Annual Report include, but are not limited to, statements with respect to (1) our anticipated sources and uses of cash and cash equivalents; (2) our anticipated commencement dates, completion dates and results of clinical trials; (3) our efforts to pursue collaborations with the government, industry groups or other companies; (4) our anticipated progress and costs of our clinical and preclinical research and development programs; (5) our corporate and development strategies; (6) our expected results of operations; (7) our anticipated levels of expenditures; (8) our ability to protect our intellectual property; (9) our ability to fully comply with domestic and international governmental regulation; (10) the anticipated applications and efficacy of our drug candidates; (11) the nature and scope of potential markets for our drug candidates; (12) future legal liability; and (13) our ability to attract and retain key employees. All statements, other than statements of historical fact, included in this Annual Report that address activities, events or developments that we expect or anticipate will or may occur in the future are forward-looking statements. We include forward-looking statements because we believe that it is important to communicate our expectations to our investors. However, all forward-looking statements are based on management’s current expectations of future events and are subject to a number of risks and uncertainties, as discussed below in Item 1A., “Risk Factors.” Although we believe the expectations reflected in the forward-looking statements are based upon reasonable assumptions, we can give no assurance that our expectations will be attained, and we caution you not to place undue reliance on such statements.

Our periodic and current reports are available, free of charge, after the material is electronically filed with, or furnished to, the SEC and EDGAR at http://www.sec.gov/edgar and the Canadian securities regulators on SEDAR, at www.sedar.com. The information provided on our website is not part of this Annual Report and is therefore not incorporated herein by reference.

| Item 1. | Business Overview |

Fennec Pharmaceuticals Inc. (“Fennec,” the “Company,” “we,” “us,” or “our”) is a biopharmaceutical company focused on the development of PEDMARKTM (a unique formulation of Sodium Thiosulfate (“STS”)) for the prevention of platinum-induced ototoxicity in pediatric cancer patients. We incorporated under the Canada Business Corporations Act ("CBCA”) in September 1996. Effective on August 25, 2011, the Company continued from the Canada Business Corporations Act to the Business Corporations Act (British Columbia) (the “Continuance”). The Continuance was approved by the shareholders of Fennec at the Company's June 2011 Annual and Special Meeting and by resolution of the Board of Directors on August 10, 2011. We have three wholly-owned subsidiaries: Oxiquant, Inc. and Fennec Pharmaceuticals, Inc., both Delaware corporations, and Cadherin Biomedical Inc., a Canadian company. With the exception of Fennec Pharmaceuticals, Inc., all subsidiaries are inactive.

On December 12, 2017, the Company announced the completion of an underwritten public offering of 2,352,950 common shares at a public offering price of $8.50 per share. In addition, Fennec issued an additional 135,670 common shares in connection with the partial exercise of the underwriters’ over-allotment option. The approximate total gross proceeds from the offering was $21.2 million.

On June 8, 2017, the Company completed the closing of a non-brokered private placement (the “Offering”) of 1,900,000 common shares for gross proceeds of $7.6 million. Each common share was issued at a price of $4.00.

Lead Product Candidate

The following is our only lead product candidate in the clinical stage of development:

| · | PEDMARKTM (a unique formulation of sodium thiosulfate (STS)) – sodium thiosulfate in a novel formulation, recently announced results of two Phase III clinical trials for the prevention of cisplatin induced hearing loss, or ototoxicity in children including the pivotal Phase III study SIOPEL 6 , “A Multicentre Open Label Randomised Phase 3 Trial of the Efficacy of Sodium Thiosulfate in Reducing Ototoxicity in Patients Receiving Cisplatin Chemotherapy for Standard Risk Hepatoblastoma,” and the proof of concept Phase III study “A Randomized Phase 3 Study of Sodium Thiosulfate for the Prevention of Cisplatin-Induced Ototoxicity in Children”. |

We continue to focus the Company’s resources on the development of PEDMARKTM.

PEDMARKTM

We have licensed from Oregon Health & Science University (“OHSU”) intellectual property rights for the use of PEDMARKTM as a chemoprotectant, and are developing PEDMARKTM as a protectant against the hearing loss often caused by platinum-based anti-cancer agents in children. Preclinical and clinical studies conducted by OHSU and others have indicated that PEDMARKTM can effectively reduce the incidence of hearing loss caused by platinum-based anti-cancer agents. We have received Orphan Drug Designation in the United States for the use of PEDMARKTM in the prevention of platinum-induced ototoxicity in pediatric patients.

| 1 |

Hearing loss among children receiving platinum-based chemotherapy is frequent, permanent and often severely disabling. The incidence of hearing loss in these children depends upon the dose and duration of chemotherapy, and many of these children require lifelong hearing aids. There is currently no established preventive agent for this hearing loss and only expensive, technically difficult and sub-optimal cochlear (inner ear) implants have been shown to provide some benefit. In addition, adults undergoing chemotherapy for several common malignancies, including ovarian cancer, testicular cancer, and particularly head and neck cancer and brain cancer, often receive intensive platinum-based therapy and may experience severe, irreversible hearing loss, particularly in the high frequencies.

The Company estimates based on data from Childhood and Adolescent Cancer Statistics (2014) and Automated Childhood Cancer Information System (ACCIS) that the annual incidence of pediatric solid tumor cases eligible for Platinum-Based therapy collectively in American and European markets is greater than 10,000.

Investigators at OHSU have conducted Phase I and Phase II studies which have shown that STS reduces the hearing loss associated with platinum-based chemotherapy. In one study at OHSU, the need for hearing aids to correct high frequency hearing loss was reduced from about 50% of patients being administered platinum-based chemotherapy to less than 5% of patients being administered platinum-based chemotherapy with STS.

STS has been studied by cooperative groups in two Phase III clinical studies of survival and reduction of ototoxicity, the Clinical Oncology Group (“COG”) Protocol ACCL0431 and the International Society of Pediatric Oncology (“SIOPEL 6”). The COG Protocol ACCL0431 enrolled one of five childhood cancers typically treated with intensive cisplatin therapy for localized and disseminated disease, including newly diagnosed hepatoblastoma, germ cell tumor, osteosarcoma, neuroblastoma, and medulloblastoma/PNET. SIOPEL 6 enrolled only hepatoblastoma patients with localized tumors.

In 2018, Fennec plans to pursue regulatory approval for PEDMARKTM based on the data from the pivotal SIOPEL 6 study along with the proof of principle data from COG ACCL0431. STS has received Orphan Drug Designation in the US in this setting and plans to pursue European Market Exclusivity for Pediatric Use ("PUMA") upon approval. Orphan Drug Designation will allow for 7.5 years of market exclusivity and PUMA will allow for 10 years of market exclusivity.

SIOPEL 6

In October 2007, we announced that our collaborative partner, the International Childhood Liver Tumour Strategy Group, known as SIOPEL, a multi-disciplinary group of specialists under the umbrella of the International Society of Pediatric Oncology, had launched a randomized Phase III clinical trial SIOPEL 6 to investigate whether STS reduces hearing loss in standard risk hepatoblastoma (liver) cancer patients receiving cisplatin as a monotherapy.

The study was initiated in October 2007 initially in the United Kingdom and completed enrollment at the end of 2014. 52 sites from 11 countries enrolled 109 evaluable patients. Under the terms of our agreement, SIOPEL conducts and funds all clinical activities and Fennec provides drug, drug distribution and pharmacovigilance, or safety monitoring, for the study. SIOPEL 6 was completed in December 2014 and the results of the trial were released in October 2017 at SIOP 2017.

The primary objectives of SIOPEL 6 are:

| · | To assess the efficacy of STS to reduce the hearing impairment caused by cisplatin. |

| · | To carefully monitor any potential impact of STS on response to cisplatin and survival. |

SIOPEL 6 - Results - October 2017

Background / Objectives:

Background: Bilateral high-frequency hearing loss is a serious permanent side-effect of cisplatin therapy, particularly debilitating when occurring in young children. STS has been shown to reduce cisplatin induced hearing loss. SIOPEL 6 is a phase III randomized trial to assess the efficacy of STS in reducing ototoxicity in young children treated with cisplatin (Cis) for Standard Risk Hepatoblastoma (SR-HB).

Design / Methods:

Methods: Newly diagnosed patients with SR-HB, defined as tumour limited to PRETEXT I, II or III, no portal or hepatic vein involvement, no intra-abdominal extrahepatic disease, AFP >100ng/ml and no metastases, were randomized to Cis or Cis+STS for 4 preoperative and 2 postoperative courses. Cisplatin 80mg/m2 was administered over 6 hours, STS 20g/m2 was administered intravenously over 15 minutes exactly 6 hours after stopping cisplatin. Tumour response was assessed after 2 and 4 preoperative cycles with serum AFP and liver imaging. In case of progressive disease (PD), STS was to be stopped and doxorubicin 60mg/m2 combined with cisplatin. The primary endpoint is centrally reviewed absolute hearing threshold, at the age of ≥3.5 years by pure tone audiometry.

| 2 |

Results:

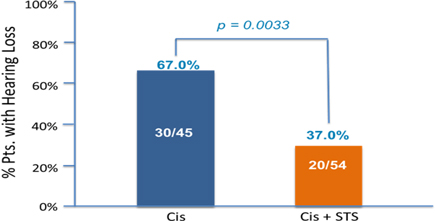

Results: One hundred and nine randomized patients (52 Cisplatin only ("Cis") and 57 Cis+STS) are evaluable. The combination of Cis+STS was generally well tolerated. With a follow up time of 52 months for the patients the 3 year Event Free Survival ("EFS") for Cis is 78.8% Cisplatin and 82.1% for the Cis + STS. The 3 year Overall Survival ("OS") is 92.3% for Cis and 98.2% for Cis + STS. Treatment failure defined as Progressive Disease ("PD") at 4 cycles was equivalent in both arms. Among the first 99 evaluable patients, hearing loss occurred in 30/45=67.0% under Cis and in 20/54=37.0% under Cis +STS, corresponding to a relative risk of 0.56(P=0.0033).

Conclusions:

This randomized phase III trial in SR-HB of cisplatin versus cisplatin plus sodium thiosulfate shows that the addition of sodium thiosulfate significantly reduces the incidence of cisplatin-induced hearing loss without any evidence of tumour protection.

COG ACCL0431

In March 2008, we announced the activation of a Phase III trial with STS to prevent hearing loss in children receiving cisplatin-based chemotherapy in collaboration with the Children’s Oncology Group (“COG ACCL0431”). The goal of this Phase III study was to evaluate in a multi-centered, randomized trial whether STS is an effective and safe means of preventing hearing loss in children receiving cisplatin-based chemotherapy for newly diagnosed germ cell, liver (hepatoblastoma), brain (medulloblastoma), nerve tissue (neuroblastoma) or bone (osteosarcoma) cancers. Eligible children, one to eighteen years of age, who were to receive cisplatin according to their disease-specific regimen and, upon enrollment in this study, were randomized to receive STS or not. Efficacy of STS was determined through comparison of hearing sensitivity at follow-up relative to baseline measurements using standard audiometric techniques. The Children’s Oncology Group is responsible for funding the clinical activities for the study and we are responsible for providing the drug, drug distribution and pharmacovigilance, or safety monitoring, for the study. The trial completed enrollment of 131 pediatric patients in the first quarter of 2012. The final results of COG ACCL0431 were published in Lancet Oncology in December 2016.

COG ACCL0431 - Results

COG Study ACCL0431, “A Randomized Phase III Study of Sodium Thiosulfate for the Prevention of Cisplatin-Induced Ototoxicity in Children,” finished enrollment of 131 patients of which 126 were eligible patients in Q1 2012. The patients had been previously diagnosed with childhood cancers.

The primary endpoint was to evaluate the efficacy of STS for prevention of hearing loss in children receiving cisplatin chemotherapy (hypothesis: 50% relative reduction in hearing loss).

Secondary endpoints included:

| · | Compare change in mean hearing thresholds. |

| · | Compare incidence of other Grade 3/4 toxicities (renal and hematological). |

| · | Monitor Event Free Survival (EFS) and Overall Survival (OS) in two groups. |

125eligible subjects were enrolled with germ cell tumor (32), osteosarcoma (29), neuroblastoma (26), medulloblastoma/pnet (26), hepatoblastoma (7) or other (5). Of these, 104 subjects (64 male and 29 <5 years old) were evaluable for the primary endpoint.

| 3 |

Subjects were randomized either to no treatment (control) or treatment with STS 16 grams/m2 IV over 15 minutes, 6 hours after each cisplatin dose. Hearing was measured using standard audiometry for age and data were reviewed centrally using American Speech-Language-Hearing Association criteria.

The proportion of subjects with hearing loss assessed at 4 weeks post the final cisplatin dose (primary endpoint):

| · | The proportion of hearing loss for STS vs. Control was 28.6% (14/49) vs. 56.4% (31/55), respectively (p=0.004). |

| · | In a predefined subgroup of patients less than 5 years old with 29 eligible subjects: STS vs. Control was 21.4% (3/14) vs. 73.3% (11/15), respectively (p=0.005). |

Conclusions:

| · | STS protects against cisplatin-induced hearing loss in children across a heterogeneous range of tumor types with even stronger efficacy in the protocol predefined subgroup of patients under five years old and is not associated with serious adverse events attributed to its use. |

| · | Further potential clinical use will be informed by the final results of SIOPEL 6 study. |

Intellectual Property

Patents are important to developing and protecting our competitive position. Our general policy is to seek patent protection in the United States, major European countries, Japan, Canada and other jurisdictions as appropriate for our compounds and methods. U.S. patents, as well as most foreign patents, are generally effective for 20 years from the date the earliest (priority) application was filed; however, U.S. patents that issue on applications filed before June 8, 1995 may be effective until 17 years from the issue date, if that is later than the 20 year date. In some cases, the patent term may be extended to recapture a portion of the term lost during the U.S. Food and Drug Administration (“FDA”) regulatory review or because of U.S. Patent and Trademark Office, or USPTO, delays in prosecuting the application. The duration of foreign patents varies similarly, in accordance with local law.

Currently, we have licensed from Oregon Health and Science University 1 U.S. and 9 foreign patents which expire in Europe. All patents expire in 2021, with an additional 2 patents pending.

In addition, periods of marketing exclusivity for STS may also be possible in the United States under orphan drug status and in Europe under European Market Exclusivity for Pediatric Use. We obtained U.S. Orphan Drug Designation for the use of STS in the prevention of platinum-induced ototoxicity in pediatric patients in 2004 which provides 7.5 years of market exclusivity upon approval. We plan to pursue European Market Exclusivity for Pediatric Use upon approval which would allow for 10 years of market exclusivity.

Our success is significantly dependent on our ability to obtain and maintain patent protection for our product candidate, both in the United States and abroad. The patent position of biotechnology and pharmaceutical companies, in general, is highly uncertain and involves complex legal and factual questions, which often results in apparent inconsistencies regarding the breadth of claims allowed and general uncertainty as to their legal interpretation and enforceability. Further, our principal candidate STS, is based on previously known compounds, and the candidates or products that we develop in the future may include or be based on the same or other compounds owned or produced by other parties, some or all of which may not be subject to effective patent protection. In addition, regimens that we may develop for the administration of pharmaceuticals, such as specifications for the frequency, timing and amount of dosages, may not be patentable. Accordingly, our patent applications may not result in patents being issued and issued patents may not afford effective protection. In addition, products or processes that we develop may turn out to be covered by third party patents, in which case we may require a license under such patents if we intend to continue the development of those products or processes.

Our patent position and proprietary rights are subject to certain risks and uncertainties. Please read the “Risk Factors” section of this Annual Report for information about certain risks and uncertainties that may affect our patent position and proprietary rights.

We also rely upon unpatented confidential information to remain competitive. We protect such information principally through confidentiality agreements with our employees, consultants, outside scientific collaborators, and other advisers. In the case of our employees, these agreements also provide, in compliance with relevant law, that inventions and other intellectual property conceived by such employees during their employment shall be our exclusive property.

Corporate Relationships

License Agreement with Oregon Health & Science University

On February 20, 2013, Fennec entered into a new exclusive license agreement with OHSU for exclusive worldwide license rights to intellectual property directed to STS and its use for chemoprotection, including the prevention of ototoxicity induced by platinum chemotherapy, in humans (the "New OHSU Agreement").

The term of the New OHSU Agreement expires on the date of the last to expire claim(s) covered in the patents licensed to us, unless earlier terminated as provided in the agreement. STS is currently protected by methods of use patents that we exclusively licensed from OHSU that expire in Europe, Canada and Australia in 2021 and are currently pending in the United States and Japan. The New OHSU Agreement is terminable by either Fennec or OHSU in the event of a material breach of the agreement by either party after 45 days prior written notice. Fennec has the right to terminate the New OHSU Agreement at any time upon 60 days prior written notice and payment of all fees due to OHSU under the New OHSU Agreement.

| 4 |

On May 18, 2015, Fennec negotiated an amendment ("Amendment 1") to the exclusive license agreement with OHSU. Amendment 1 expands the exclusive license agreement signed with OHSU on February 20, 2013 or New OHSU Agreement to include the use of N-acetylcysteine as a standalone therapy and/or in combination with STS for the prevention of ototoxicity induced by chemotherapeutic agents to treat cancers. Further, Amendment 1 adjusts select milestone payments entered in the OHSU Agreement including but not limited to the royalty rate on net sales for licensed products, royalty rate from sublicensing of the licensed technology and the fee payable upon the regulatory approval of a licensed product. The term of Amendment 1 under the OHSU Agreement expires on the date of the last to expire claim(s) covered in the patents licensed to Fennec or 8 years, whichever is later. In the event a licensed product obtains regulatory approval and is covered by the Orphan Drug Designation, the parties will in good faith amend the term of the agreement.

Competition

Competition in the biotechnology and pharmaceutical industries is intense. We expect that if our product candidate achieves regulatory approval for sale, it will compete on the basis of drug efficacy, safety, patient convenience, reliability, ease of manufacture, price, marketing, distribution, and patent protection, among other variables. Our competitors may develop technologies or drugs that are more effective, safer or more affordable than any we may develop.

There are a number of different approaches to the development of therapeutics for the treatment of cancer that are currently being used and studied. These approaches include: (i) surgery to excise the cancerous tissue; (ii) radiation therapy, which attacks cancerous cells but does not easily distinguish between healthy and diseased cells; (iii) chemotherapy, which works by preventing a cancerous cell from dividing or by killing cells that quickly divide; (iv) immunotherapy, which stimulates the body’s immune system to respond to the disease; and (v) hormone therapy, which may slow the growth of cancer cells or even kill them.

We are aware of a number of companies engaged in the research, development and testing of new cancer therapies or means of increasing the effectiveness of existing therapies, including, among many others, Amgen, AstraZeneca, Bayer, Bristol-Myers Squibb, Eli Lilly, Eisai, Merck KGaA, Novartis, Johnson & Johnson, Pfizer, Roche, Taiho and Sanofi-Aventis. Some of these companies have products that have already received, or are in the process of receiving, regulatory approval or are in later stages of clinical development than our product. Many of them have much greater financial resources than we do. Many of these companies have marketed drugs or are developing targeted cancer therapeutics which, depending upon the mechanism of action of such agents, could be viewed as competitors.

We are not aware of any commercially available agents that reduce the incidence of hearing loss associated with the use of platinum-based anti-cancer agents, for which purpose we are developing STS. There are several potential competitive agents with activity in preclinical or limited clinical settings. These include: D-methionine, an amino acid that has been shown to protect against hearing loss in experimental settings but was demonstrated to be inferior to STS in comparative studies; SPI-3005, an oral agent primarily being developed by Sound Pharmaceuticals for noise and age-related hearing loss but in early Phase II trials for chemotherapy related hearing loss, which mimics glutathione peroxidase and induces the intracellular induction of glutathione; N-acetylcysteine and amifostine, which have shown effectiveness (but less than STS) in experimental systems; and Vitamin E, salicylate and tiopronin, which have all demonstrated moderate activity in rat models to protect against cisplatin-induced ototoxicity, but no clinical trials have been performed. Cochlear implants, which are small electronic devices that are surgically placed in the inner ear to assist with certain types of deafness, are utilized to offer some relief but are often suboptimal.

Many of our existing or potential competitors have substantially greater financial, technical and human resources than we do and may be better equipped to develop, manufacture and market products. In addition, many of these competitors have extensive experience with preclinical testing and human clinical trials and in obtaining regulatory approvals. In addition, many of the smaller companies that compete with us have formed collaborative relationships with large, established companies to support the research, development, clinical trials and commercialization of any products that they may develop. We may rely on third parties to commercialize the products we develop, and our success will depend in large part on the efforts and competitive merit of these collaborative partners. Academic institutions, government agencies and other public and private research organizations may also conduct research, seek patent protection and establish collaborative arrangements for research, clinical development and marketing of products similar to those we seek to develop. These companies and institutions compete with us in recruiting and retaining qualified scientific and management personnel as well as in acquiring technologies complementary to our projects. The existence of competitive products, including products or treatments of which we are not aware, or products or treatments that may be developed in the future, may adversely affect the marketability of any products that we may develop.

| 5 |

Government Regulation

The production and manufacture of our product candidate and our research and development activities are subject to significant regulation for safety, efficacy and quality by various governmental authorities around the world. Before new pharmaceutical products may be sold in the U.S. and other countries, clinical trials of the product must be conducted and the results submitted to appropriate regulatory agencies for approval. Clinical trial programs must establish efficacy, determine an appropriate dose and regimen, and define the conditions for safe use. This is a high-risk process that requires stepwise clinical studies in which the candidate product must successfully meet predetermined endpoints. In the U.S., the results of the preclinical and clinical testing of a product are then submitted to the FDA in the form of a Biologics License Application or a New Drug Application. In response to these submissions, the FDA may grant marketing approval, request additional information or deny the application if it determines the application does not provide an adequate basis for approval. Similar submissions are required by authorities in other jurisdictions who independently assess the product and may reach the same or different conclusions.

The receipt of regulatory approval often takes a number of years, involves the expenditure of substantial resources and depends on a number of factors, including the severity of the disease in question, the availability of alternative treatments and the risks and benefits demonstrated in clinical trials. On occasion, regulatory authorities may require larger or additional studies, leading to unanticipated delay or expense. Even after initial approval from the FDA or other regulatory agencies has been obtained, further clinical trials may be required to provide additional data on safety and effectiveness. Additional trials are required to gain clearance for the use of a product as a treatment for indications other than those initially approved. Furthermore, the FDA and other regulatory agencies require companies to disclose clinical trial results. Failure to disclose such results within applicable time periods could result in penalties, including civil monetary penalties.

In Canada, these activities are subject to regulation by Health Canada’s Therapeutic Products Directorate, or TPD, and the rules and regulations promulgated under the Food and Drug Act. In the United States, drugs and biological products are subject to regulation by the FDA. The FDA requires licensing of manufacturing and contract research facilities, carefully controlled research and testing of products and governmental review and approval of results prior to marketing therapeutic products. Additionally, the FDA requires adherence to “Good Laboratory Practices” as well as “Good Clinical Practices” during clinical testing and “Good Manufacturing Practices” and adherence to labeling and supply controls. The systems of new drug approvals in Canada and the United States are substantially similar, and are generally considered to be among the most rigorous in the world.

Generally, the steps required for drug approval in Canada and the United States, specifically in cancer related therapies, include:

| · | Preclinical Studies: Preclinical studies, also known as non-clinical studies, primarily involve evaluations of pharmacology, toxic effects, pharmacokinetics and metabolism of a drug in animals to provide evidence of the relative safety and bioavailability of the drug prior to its administration to humans in clinical studies. A typical program of preclinical studies takes 18 to 24 months to complete. The results of the preclinical studies as well as information related to the chemistry and comprehensive descriptions of proposed human clinical studies are then submitted as part of the Investigational New Drug, application to the FDA, a Clinical Trial Application to the TPD, or similar submission to other foreign regulatory bodies. This is necessary in Canada, the United States and most other countries prior to undertaking clinical studies. Additional preclinical studies are conducted during clinical development to further characterize the toxic effects of a drug prior to submitting a marketing application. |

| · | Phase I Clinical Trials: Most Phase I clinical trials take approximately one year to complete and are usually conducted on a small number of healthy human subjects to evaluate the drug’s safety, tolerability and pharmacokinetics. In some cases, such as cancer indications, Phase I clinical trials are conducted in patients rather than healthy volunteers. |

| · | Phase II Clinical Trials: Phase II clinical trials typically take one to two years to complete and are generally carried out on a relatively small number of patients, generally between 15 and 50, in a specific setting of targeted disease or medical condition, in order to provide an estimate of the drug’s effectiveness in that specific setting. This phase also provides additional safety data and serves to identify possible common short-term side effects and risks in a somewhat larger group of patients. Phase II testing frequently relates to a specific disease, such as breast or lung cancer. Some contemporary methods of developing drugs, particularly molecularly targeted therapies, do not require broad testing in specific diseases, and instead permit testing in subsets of patients expressing the particular marker. In some cases, such as cancer indications, the company sponsoring the new drug may submit a marketing application to seek accelerated approval of the drug based on evidence of the drug’s effect on a “surrogate endpoint” from Phase II clinical trials. A surrogate endpoint is a laboratory finding or physical sign that may not be a direct measurement of how a patient feels, functions or survives, but is still considered likely to predict therapeutic benefit for the patient. If accelerated approval is received, the company sponsoring the new drug must continue testing to demonstrate that the drug indeed provides therapeutic benefit to the patient. |

| · | Phase III Clinical Trials: Phase III clinical trials typically take two to four years to complete and involve tests on a much larger population of patients suffering from the targeted condition or disease. These studies involve conducting controlled testing and/or uncontrolled testing in an expanded patient population, numbering several hundred to several thousand patients, at separate test sites, known as multi-center trials, to establish clinical safety and effectiveness. These trials also generate information from which the overall benefit-risk relationship relating to the drug can be determined and provide a basis for drug labeling. Phase III trials are generally the most time consuming and expensive part of a clinical trial program. In some instances, governmental authorities, such as the FDA, will allow a single Phase III clinical trial to serve as a pivotal efficacy trial to support a Marketing Application. |

| · | Marketing Application: Upon completion of Phase III clinical trials, the pharmaceutical company sponsoring the new drug assembles all the chemistry, preclinical and clinical data and submits it to the TPD or the FDA as part of a New Drug Submission in Canada or a New Drug Application, in the United States. The marketing application is then reviewed by the applicable regulatory body for approval to market the product. The review process generally takes twelve to eighteen months. |

| 6 |

Any clinical trials that we conduct may not be successfully completed, either in a satisfactory time period or at all. The typical time periods described above may vary substantially and may be materially longer. In addition, the FDA and its counterparts in other countries have considerable discretion to discontinue trials if they become aware of any significant safety issues or convincing evidence that a therapy is not effective for the indication being tested. It is possible the FDA and its counterparts in other countries may not (i) allow clinical trials to proceed at any time after receiving an Investigational New Drug, (ii) allow further clinical development phases after authorizing a previous phase, or (iii) approve marketing of a drug after the completion of clinical trials.

While European, U.S. and Canadian regulatory systems require that medical products be safe, effective, and manufactured according to high quality standards, the drug approval process in Europe differs from that in the United States and Canada and may require us to perform additional preclinical or clinical testing regardless of whether FDA or TPD approval has been obtained. The amount of time required to obtain necessary approvals may be longer or shorter than that required for FDA or TPD approval. European Union Regulations and Directives generally classify health care products either as medicinal products, medical devices or in vitro diagnostics. For medicinal products, marketing approval may be sought using either the centralized procedure of the European Agency for the Evaluation of Medicinal Products, or EMEA, or the decentralized, mutual recognition process. The centralized procedure, which is mandatory for some biotechnology derived products, results in an approval recommendation from the EMEA to all member states, while the European Union mutual recognition process involves country by country approval.

Good Clinical Practices

The FDA and other regulatory agencies promulgate regulations and standards, commonly referred to as current Good Clinical Practices for designing, conducting, monitoring, auditing and reporting the results of clinical trials to ensure that the data and results are accurate and that the trial participants are adequately protected. The FDA and other regulatory agencies enforce Good Clinical Practices through periodic inspections of trial sponsors, principal investigators and trial sites. If our study sites fail to comply with applicable Good Clinical Practices, the clinical data generated in our clinical trials may be deemed unreliable and relevant regulatory agencies may require us to perform additional clinical trials before approving our marketing applications.

Good Manufacturing Practices

The FDA and other regulatory agencies regulate and inspect equipment, facilities and processes used in the manufacture of pharmaceutical and biological products prior to approving a product. If, after receiving approval from regulatory agencies, a company makes a material change in manufacturing equipment, location or process, additional regulatory review and approval may be required. All facilities and manufacturing techniques that may be used for the manufacture of our products must comply with applicable regulations governing the production of pharmaceutical products known as "Good Manufacturing Practices."

Orphan Drug Act

Under the U.S. Orphan Drug Act, the FDA may grant orphan drug designation to drugs intended to treat a “rare disease or condition,” which generally is a disease or condition that affects fewer than 200,000 individuals in the U.S. If a product which has an orphan drug designation subsequently receives the first FDA approval for the indication for which it has such designation, the product is entitled to orphan exclusivity, i.e., the FDA may not approve any other applications to market the same drug for the same indication for a period of seven years following marketing approval, except in certain very limited circumstances, such as if the later product is shown to be clinically superior to the orphan product. Legislation similar to the U.S. Orphan Drug Act has been enacted in other countries, including within the European Union.

Pediatric Marketing Use Authorization

The PUMA approval is granted by the European Medicines Agency and is intended exclusively for pediatric (patients under 18 years of age) use. PUMA approval is valid in all countries within the European Economic Area. The PUMA process was established to make it more efficient for pharmaceutical companies to market drugs for children. New data for PUMA drugs are protected for 10 years and the applications are, in part, exempt from fees.

Other Laws

Our present and future business has been and will continue to be subject to various other laws and regulations. Various laws, regulations and recommendations relating to safe working conditions, laboratory practices, the experimental use of animals, and the purchase, storage, movement, import and export and use and disposal of hazardous or potentially hazardous substances, including radioactive compounds and infectious disease agents, used in connection with our research work are or may be applicable to our activities. Certain agreements entered into by us involving exclusive license rights may be subject to national or supranational antitrust regulatory control, the effect of which cannot be predicted. The extent of government regulation, which might result from future legislation or administrative action, cannot accurately be predicted.

Research and Development

Our research and development efforts have been focused on the development of PEDMARKTM since 2013.

| 7 |

We have established relationships with contract research organizations, universities and other institutions, which we utilize to perform many of the day-to-day activities associated with our drug development. Where possible, we have sought to include leading scientific investigators and advisors to enhance our internal capabilities. Research and development issues are reviewed internally by our executive management and supporting scientific team.

Research and development expenses totaled $1.9 million and $0.5 million for the fiscal years ended December 31, 2017 and 2016, respectively. The Company has increased its research and development expenses related to PEDMARKTM as a result of the Company drug manufacturing activities related to the preparation for registration batches.

Our product candidate still requires significant, time-consuming and costly research and development, testing and regulatory clearances. In developing our product candidate, we are subject to risks of failure that are inherent in the development of products based on innovative technologies. For example, it is possible that our product candidate will be ineffective or toxic, or will otherwise fail to receive the necessary regulatory clearances. There is a risk that our product candidate will be uneconomical to manufacture or market or will not achieve market acceptance. There is also a risk that third parties may hold proprietary rights that preclude us from marketing our product candidate or that others will market a superior or equivalent product. As a result of these factors, we are unable to accurately estimate the nature, timing and future costs necessary to complete the development of this product candidate. In addition, we are unable to reasonably estimate the period when material net cash inflows could commence from the sale, licensing or commercialization of such product candidate, if ever.

Employees

At December 31, 2017, we had three employees (our Chief Executive Officer, Chief Financial Officer and Controller). These employees are employed on a full-time basis and there are no part-time employees. The company uses independent contractors to perform certain daily operations of the company.

| Item 1A. | Risk Factors |

An investment in our common shares involves a significant risk of loss. You should carefully read this entire report and should give particular attention to the following risk factors. You should recognize that other significant risks may arise in the future, which we cannot reasonably foresee at this time. Also, the risks that we now foresee might affect us to a greater or different degree than currently expected. There are a number of important factors that could cause our actual results to differ materially from those expressed or implied by any of our forward-looking statements in this Annual Report. These factors include, without limitation, the risk factors listed below and other factors presented throughout this Annual Report and any other documents filed by us with the Securities and Exchange Commission, or the SEC, and the Canadian securities regulators on SEDAR which can be accessed at www.sedar.com.

Risks Related to Our Business

We have a history of significant losses and have had no revenues to date through the sale of our products. If we do not generate significant revenues, we will not achieve profitability.

To date, we have been engaged primarily in research and development activities. We have had no revenues through the sale of our products, and we do not expect to have significant revenues until we are able to either sell our product candidate after obtaining applicable regulatory approvals or we establish collaborations that provide us with up-front payments, licensing fees, milestone payments, royalties or other revenue. We have incurred significant operating losses every year since our inception on September 3, 1996. We reported a loss of approximately $7.0 million (including a non-cash loss on derivative liabilities of $0.13 million) for the year ended December 31, 2017, and reported a net loss of approximately $2.8 million (which included a non-cash gain on derivative liabilities of $0.05 million) for the year ended December 31, 2016. At December 31, 2017, we had an accumulated deficit of approximately $121.4 million. We anticipate incurring substantial additional losses due to the need to spend substantial amounts on activities required for regulatory approval of PEDMARKTM, commercial launch preparation of PEDMARKTM , anticipated research and development activities, and general and administrative expenses, among other factors. We have not commercially introduced any products. Our ability to attain profitability will depend upon our ability to fund and develop products that are safe, effective and commercially viable, to obtain regulatory approval for the manufacture and sale of our product candidate and to license or otherwise market our product candidate successfully. Any revenues generated from such product, assuming it is successfully developed, marketed and sold, may not be realized for a number of years. We may never achieve or sustain profitability on an ongoing basis.

PEDMARKTM is currently our only product candidate and there is no assurance that we will successfully develop PEDMARKTM into a commercially viable product.

Since our formation in September 1996, we have engaged in research and development programs. We have generated no revenue from product sales, do not have any products currently available for sale, and none are expected to be commercially available for sale until we have completed regulatory approval of PEDMARKTM. PEDMARKTM is currently our only product candidate. There can be no assurance that the research we fund and manage will lead PEDMARKTM or any future product candidate to become a commercially viable product. We have completed enrollment of two Phase III studies for PEDMARKTM. We anticipate substantial regulatory review prior to the commercialization of PEDMARKTM.

| 8 |

We anticipate the need for additional capital in the future and if we cannot raise additional capital, we will not be able to fulfill our business plan.

We need to obtain additional funding in the future in order to finance our business strategy, operations and growth. We may not be able to obtain additional financing in sufficient amounts or on acceptable terms when needed. If we fail to arrange for sufficient capital on a timely basis, we may be required to curtail our business activities until we can obtain adequate financing. Debt financing must be repaid regardless of whether or not we generate profits or cash flows from our business activities. Equity financing may result in dilution to existing shareholders and may involve securities that have rights, preferences, or privileges that are senior to our common shares or other securities. If we cannot raise sufficient capital when necessary, we will likely have to curtail operations and you may lose part or all of your investment.

If we do not maintain current or enter into new collaborations with other companies, we might not successfully develop our product candidate or generate sufficient revenues to expand our business.

We currently rely on scientific and research and development collaboration arrangements with academic institutions and other third party collaborators, including an exclusive worldwide license from OHSU for PEDMARKTM. We also rely on collaborators for testing PEDMARKTM, including SIOPEL and the Children’s Oncology Group.

The agreements with OHSU are terminable by either party in the event of an uncured breach by the other party. We may also terminate our agreement with OHSU at any time upon prior written notice of specified durations to the licensor. Termination of any of our collaborative arrangements could materially adversely affect our business. For example, if we are unable to make the necessary payments under these agreements, the licensor might terminate the agreement which might have a material adverse impact. In addition, our collaborators might not perform as agreed in the future.

Since we conduct a significant portion of our research and development through collaborations, our success may depend significantly on the performance of such collaborators, as well as any future collaborators. Collaborators might not commit sufficient resources to the research and development or commercialization of our product candidate. Economic or technological advantages of products being developed by others, among other factors, could lead our collaborators to pursue other product candidates or technologies in preference to those being developed in collaboration with us. The commercial potential of, development stage of and projected resources required to develop our drug candidate will affect our ability to maintain current collaborations or establish new collaborators. There is a risk of dispute with respect to ownership of technology developed under any collaboration. Our management of any collaboration will require significant time and effort as well as an effective allocation of resources. We may not be able to simultaneously manage a large number of collaborations.

Our product candidate is still in development. Due to the long, expensive and unpredictable drug development process, we might not ever successfully develop and commercialize our product candidate.

In order to achieve profitable operations, we, alone or in collaboration with others, must successfully fund, develop, manufacture, introduce and market our product candidate. The time necessary to achieve market success for any individual product is long and uncertain. Our product candidate and research programs are in clinical development and require significant, time-consuming and costly research, testing and regulatory clearances. In developing our product candidate, we are subject to risks of failure that are inherent in the development of therapeutic products based on innovative technologies. The results of preclinical and initial clinical trials are not necessarily predictive of future results. Our product candidate might not be economical to manufacture or market or might not achieve market acceptance. In addition, third parties might hold proprietary rights that preclude us from marketing our product candidates or others might market equivalent or superior products.

We may need to conduct additional human clinical trials to assess our product candidate. If these trials are delayed or are unsuccessful, our development costs will significantly increase and our business prospects may suffer.

Before obtaining regulatory approvals for the commercial sale of our product candidate, we must demonstrate, through preclinical studies with animals and clinical trials with humans, that our product candidate is safe and effective for use in each target indication. To date, we have performed only limited clinical trials. Much of our testing has been conducted on animals or on human cells in the laboratory, and the benefits of treatment seen in animals or on human cells in a laboratory setting may not ultimately be obtained in human clinical trials. As a result, we may need to perform significant additional research and development activities and conduct extensive preclinical and clinical testing prior to any application for commercial use. We may suffer significant setbacks in additional clinical trials, and the trials may demonstrate our product candidate to be unsafe or ineffective. We may also encounter problems in our clinical trials that will cause us to delay, suspend or terminate those clinical trials, which would increase our development costs and harm our financial results and commercial prospects. Identifying and qualifying patients to participate in clinical trials of our potential products is critically important to our success. The timing of our clinical trials depends on, among other things, the speed at which we can recruit patients to participate in testing our product candidate. We have experienced delays in some of our clinical trials and we may experience significant delays in the future. If patients are unwilling to participate in our trials because of competing clinical trials for similar patient populations, perceived risk or any other reason, the timeline for recruiting patients, conducting trials and obtaining regulatory approval of potential products will be delayed. Other factors that may result in significant delays include obtaining regulatory or ethics review board approvals for proposed trials, reaching agreement on acceptable terms with prospective clinical trial sites, and obtaining sufficient quantities of drugs for use in the clinical trials. Such delays could result in the termination of the clinical trials altogether.

| 9 |

Regulatory approval of our product candidate is time-consuming, expensive and uncertain, and could result in unexpectedly high expenses and delay our ability to sell our product.

Development, manufacture and marketing of our product is subject to extensive regulation by governmental authorities in the United States and other countries. This regulation could require us to incur significant unexpected expenses or delay or limit our ability to sell our product candidate. Our clinical studies might be delayed or halted, or additional studies might be required, for various reasons, including:

| · | there is a lack of sufficient funding; |

| · | the drug is not effective; |

| · | patients experience severe side effects during treatment; |

| · | appropriate patients do not enroll in the studies at the rate expected; |

| · | drug supplies are not sufficient to treat the patients in the studies; or |

| · | we decide to modify the drug during testing. |

If regulatory approval of our product is granted, it will be limited to those indications for which the product has been shown to be safe and effective, as demonstrated to the satisfaction of the FDA and foreign regulators through clinical studies. Furthermore, approval might entail ongoing requirements for post-marketing studies. Even if regulatory approval is obtained, labeling and promotional activities are subject to continual scrutiny by the FDA and state and foreign regulatory agencies and, in some circumstances, the Federal Trade Commission. FDA enforcement policy prohibits the marketing of approved products for unapproved, or off-label, uses. These regulations and the FDA’s interpretation of them might impair our ability to effectively market our product.

We and our third-party manufacturers are also required to comply with the applicable current FDA Good Manufacturing Practices regulations, which include requirements relating to quality control and quality assurance, as well as the corresponding maintenance of records and documentation. Further, manufacturing facilities must be approved by the FDA before they can be used to manufacture our product, and they are subject to additional FDA inspection. If we fail to comply with any of the FDA’s continuing regulations, we could be subject to reputational harm and sanctions, including:

| · | delays, warning letters and fines; |

| · | product recalls or seizures and injunctions on sales; |

| · | refusal of the FDA to review pending applications; |

| · | total or partial suspension of production; |

| · | withdrawals of previously approved marketing applications; and |

| · | civil penalties and criminal prosecutions. |

In addition, identification of side effects after a drug is on the market or the occurrence of manufacturing problems could cause subsequent withdrawal of approval, reformulation of the drug, additional testing or changes in labeling of the product.

We may be unable to effectively deploy the proceeds from our recent financings for the development of PEDMARKTM.

In December of 2017, the Company announced the completion of an underwritten public offering for gross proceeds of $21.2 million. In June of 2017, the Company announced the closing of a non-brokered private placement for gross proceeds of $7.6 million. Any inability on our part to manage effectively the deployment of this capital could limit our ability to successfully develop PEDMARKTM.

If our licenses to proprietary technology owned by others are terminated or expire, we may suffer increased development costs and delays, and we may not be able to successfully develop our product candidate.

The development of our drug candidate and the manufacture and sale of any products that we develop will involve the use of processes, products and information, some of the rights to which are owned by others. STS is licensed under agreements with OHSU. Although we have obtained licenses or rights with regard to the use of certain processes, products and information, the licenses or rights could be terminated or expire during critical periods and we may not be able to obtain, on favorable terms or at all, licenses or other rights that may be required. Some of these licenses provide for limited periods of exclusivity that may be extended only with the consent of the licensor, which may not be granted.

| 10 |

If we are unable to adequately protect or maintain our patents and licenses related to our product candidate, or if we infringe upon the intellectual property rights of others, we may not be able to successfully develop and commercialize our product candidate.

The value of our technology will depend in part upon our ability, and those of our collaborators, to obtain patent protection or licenses to patents, maintain trade secret protection and operate without infringing on the rights of third parties. Although we have successfully pursued patent applications in the past, it is possible that:

| · | some or all of our pending patent applications, or those we have licensed, may not be allowed; |

| · | proprietary products or processes that we develop in the future may not be patentable; |

| · | any issued patents that we own or license may not provide us with any competitive advantages or may be successfully challenged by third parties; or |

| · | the patents of others may have an adverse effect on our ability to do business. |

It is not possible for us to be certain that we are the original and first creator of inventions encompassed by our pending patent applications or that we were the first to file patent applications for any such inventions. Further, any of our patents, once issued, may be declared by a court to be invalid or unenforceable.

STS is currently protected by methods of use patents that we exclusively licensed from OHSU that expire in Europe in 2021 and are currently pending in the United States. In addition, periods of marketing exclusivity for STS may also be possible in the United States under orphan drug status. We obtained Orphan Drug Designation in the United States for the use of STS in the prevention of platinum-induced ototoxicity in pediatric patients in 2004; if it is subsequently approved, will have seven and a half years of pediatric exclusivity in the United States from the approval date. Refer to the “Description of Business” section of this Annual Report for a further description of the United States Orphan Drug Designation.

We may be required to obtain licenses under patents or other proprietary rights of third parties but the extent to which we may wish or need to do so is unknown. Any such licenses may not be available on terms acceptable to us or at all. If such licenses are obtained, it is likely they would be royalty bearing, which would reduce any future income. If licenses cannot be obtained on an economical basis, we could suffer delays in market introduction of planned products or their introduction could be prevented, in some cases after the expenditure of substantial funds. If we do not obtain such licenses, we would have to design around patents of third parties, potentially causing increased costs and delays in product development and introduction or precluding us from developing, manufacturing or selling our planned products, or our ability to develop, manufacture or sell products requiring such licenses could be foreclosed.

Litigation may also be necessary to enforce or defend patents issued or licensed to us or our collaborators or to determine the scope and validity of a third party’s proprietary rights. We could incur substantial costs if litigation is required to defend ourselves in patent suits brought by third parties, if we participate in patent suits brought against or initiated by our collaborators, or if we initiate such suits. We might not prevail in any such action. An adverse outcome in litigation or an interference to determine priority or other proceeding in a court or patent office could subject us to significant liabilities, require disputed rights to be licensed from other parties or require us or our collaborators to cease using certain technology or products. Any of these events would likely have a material adverse effect on our business, financial condition and results of operations.

Much of our technological know-how that is not patentable may constitute trade secrets. Our confidentiality agreements might not provide for meaningful protection of our trade secrets, know-how or other proprietary information in the event of any unauthorized use or disclosure of information. In addition, others may independently develop or obtain similar technology and may be able to market competing products and obtain regulatory approval through a showing of equivalency to our product that has obtained regulatory approvals, without being required to undertake the same lengthy and expensive clinical studies that we would have already completed.

The vulnerability to off-label use or sale of our product candidate that are covered only by “method of use” patents may cause downward pricing pressure on the product candidate if they are ever commercialized and may make it more difficult for us to enter into collaboration or partnering arrangements for the development of this product candidate.

STS is currently only covered by “method of use” patents, which covers the use of certain compounds to treat specific conditions, and are not covered by “composition of matter” patents, which would cover the chemical composition of the compound. Method of use patents provide less protection than composition of matter patents because of the possibility of off-label competition if other companies develop or market the compound for other uses. If another company markets a drug that we expect to market under the protection of a method of use patent, physicians may prescribe the other company’s drug for use in the indication for which we obtain approval and have a patent, even if the other company’s drug is not approved for such an indication. Off-label use and sales could limit our sales and exert pricing pressure on any product we develop covered only by method of use patents. Also, it may be more difficult to find a collaborator to license or support the development of our product candidate that is only covered by method of use patents.

| 11 |

If our third-party manufacturers breach or terminate their agreements with us, or if we are unable to secure arrangements with third party manufacturers on acceptable terms as needed in the future, we may suffer significant delays and additional costs.

We have no experience manufacturing products and do not currently have the resources to manufacture any products that we may develop. We currently have agreements with contract manufacturers for clinical supplies of PEDMARKTM, including drug substance providers and drug product suppliers, but they might not perform as agreed in the future or may terminate our agreements with them before the end of the required term. Significant additional time and expense would be required to effect a transition to a new contract manufacturer.

We plan to continue to rely on contract manufacturers for the foreseeable future to produce quantities of products and substances necessary for research and development, preclinical trials, human clinical trials and product commercialization, and to perform their obligations in a timely manner and in accordance with applicable government regulations. If we develop any product with commercial potential, we will need to develop the facilities to independently manufacture such product or products or secure arrangements with third parties to manufacture them. We may not be able to independently develop manufacturing capabilities or obtain favorable terms for the manufacture of our product. While we intend to contract for the commercial manufacture of our product candidate, we may not be able to identify and qualify contractors or obtain favorable contracting terms. We or our contract manufacturers may also fail to meet required manufacturing standards, which could result in delays or failures in product delivery, increased costs, injury or death to patients, product recalls or withdrawals and other problems that could significantly hurt our business. We intend to maintain a second source for back-up commercial manufacturing, wherever feasible. However, if a replacement to our future internal or contract manufacturers were required, the ability to establish second-sourcing or find a replacement manufacturer may be difficult due to the lead times generally required to manufacture drugs and the need for FDA compliance inspections and approvals of any replacement manufacturer, all of which factors could result in production delays and additional commercialization costs. Such lead times would vary based on the situation, but might be twelve months or longer.

We may lack the resources necessary to effectively market our product candidate, and we may need to rely on third parties over whom we have little or no control and who may not perform as expected.

We may not have the necessary resources to market our product candidate. If we develop any products with commercial potential, we will either have to develop a marketing capability, including a sales force, which is difficult and expensive to implement successfully, or attempt to enter into a collaboration, merger, joint venture, license or other arrangement with third parties to provide a substantial portion of the financial and other resources needed to market such products. We may not be able to do so on acceptable terms, if at all. If we rely extensively on third parties to market our products, the commercial success of such products may be largely outside of our control.

We conduct our business internationally and are subject to laws and regulations of several countries which may affect our ability to access regulatory agencies and may affect the enforceability and value of our licenses.

We have conducted clinical trials in the United States, Canada, Europe and the Pacific Rim and intend to, or may, conduct future clinical trials in these and other jurisdictions. There can be no assurance that any sovereign government will not establish laws or regulations that will be deleterious to our interests. There is no assurance that we, as a British Columbia corporation, will continue to have access to the regulatory agencies in any jurisdiction where we might want to conduct clinical trials or obtain regulatory approval, and we might not be able to enforce our license or patent rights in foreign jurisdictions. Foreign exchange controls may have a material adverse effect on our business and financial condition, since such controls may limit our ability to flow funds into or out of a particular country to meet obligations under licenses, clinical trial agreements or other collaborations.

Our cash invested in money market funds might be subject to loss.

Even though we believe we take a conservative approach to investing our funds, the nature of financial markets exposes us to investment risk, including the risks that the value and liquidity of our money market investments could deteriorate significantly and the issuers of the investments we hold could be subject to credit rating downgrades. While we have not experienced any loss or write down of our money market investments in the past, we cannot guarantee that such losses will not occur in future periods.

Risks Related to Our Industry

If we are unable to obtain applicable U.S. and/or foreign regulatory approvals, we will be unable to develop and commercialize our drug candidate.

The preclinical studies and clinical trials of our product candidate, as well as the manufacturing, labeling, sale and distribution, export or import, marketing, advertising and promotion of our product candidate, are subject to various regulatory frameworks in the United States, Canada and other countries. Any products that we develop must receive all relevant regulatory approvals and clearances before any marketing, sale or distribution. The regulatory process, which includes extensive preclinical studies and clinical testing to establish product safety and efficacy, can take many years and cost substantial amounts of money. As a result of the length of time, many challenges and costs are associated with the drug development process, and the historical rate of failures for drug candidates is extremely high. Changes in regulatory policy could also cause delays or affect regulatory approval. Any regulatory delays may increase our development costs and negatively impact our competitiveness and prospects. It is possible that we may not be able to obtain regulatory approval of our drug candidate or approvals may take longer and cost more to obtain than expected.

| 12 |

Regulatory approvals, if granted, may entail limitations on the uses for which any product we develop may be marketed, limiting the potential sales for any such products. The granting of product approvals can be withdrawn at any time, and manufacturers of approved products are subject to regular reviews, including for compliance with FDA Good Manufacturing Practices regulations. Failure to comply with any applicable regulatory requirement, which may change from time to time, can result in warning letters, fines, sanctions, penalties, recalling or seizing products, suspension of production, or even criminal prosecution.

Future sales of our product candidate may suffer if they fail to achieve market acceptance.

Even if our product candidate is successfully developed and achieves appropriate regulatory approval, it may not enjoy commercial acceptance or success. Our product candidate may compete with a number of new and traditional drugs and therapies developed by major pharmaceutical and biotechnology companies. Market acceptance is dependent on the product candidate demonstrating clinical efficacy and safety, as well as demonstrating advantages over alternative treatment methods. In addition, market acceptance is influenced by government reimbursement policies and the ability of third parties to pay for such products. Physicians, patients, or the medical community may not accept or utilize any products we may develop.

We face a strong competitive environment. Other companies may develop or commercialize more effective or cheaper products, which may reduce or eliminate the demand for our product candidate.

The biotechnology and pharmaceutical industry, and in particular the field of cancer therapeutics where we are focused, is very competitive. Many companies and research organizations are engaged in the research, development and testing of new cancer therapies or means of increasing the effectiveness of existing therapies, including, among many others, Amgen, AstraZeneca, Bayer, Bristol-Myers Squibb, Eli Lilly, Eisai, Merck KGaA, Novartis, Johnson & Johnson, Pfizer, Roche, Taiho and Sanofi-Aventis. Many of these companies have marketed drugs or are developing targeted cancer therapeutics, which depending upon the mechanism of action of such agents could be competitors.

Many of our existing or potential competitors have substantially greater financial, technical and human resources than we do and may be better equipped to develop, manufacture and market products. In addition, many of these competitors have extensive experience with preclinical testing and human clinical trials and in obtaining regulatory approvals. Also, some of the smaller companies that compete with us have formed collaborative relationships with large, established companies to support the research, development, clinical trials and commercialization of any products that they may develop. Academic institutions, government agencies and other public and private research organizations may also conduct research, seek patent protection and establish collaborative arrangements for research, clinical development and marketing of products similar to those we seek to develop. These companies and institutions compete with us in recruiting and retaining qualified scientific and management personnel as well as in acquiring technologies complementary to our projects.

We are likely to face competition in the areas of product efficacy and safety, ease of use and adaptability, as well as pricing, product acceptance, regulatory approvals and intellectual property. Competitors could develop more effective, safer and more affordable products than we do, and they may obtain patent protection or product commercialization before we do or even render our product candidate obsolete. The existence of competitive products, including products or treatments of which we are not aware, or products or treatments that may be developed in the future, may adversely affect the marketability of any product that we develop.

We may face product liability claims that could require us to defend costly lawsuits or incur substantial liabilities that could adversely impact our financial condition, receipt of regulatory approvals for our product candidate and our results of operation.

The use of our product candidate in clinical trials and for commercial applications, if any, may expose us to liability claims in the event that such product candidate causes injury or death or results in other adverse effects. These claims could be made by health care institutions, contract laboratories, and subjects participating in our clinical studies, patients or others using our product candidate. In addition to liability claims, certain serious adverse events could require interruption, delay and/or discontinuation of a clinical trial and potentially prevent further development of our product candidate. We carry clinical trial insurance but the coverage may not be sufficient to protect us from legal expenses and liabilities we might incur. Litigation is very expensive, even if we defend successfully against possible litigation. In addition, our existing coverage may not be adequate if we develop additional products, and future coverage may not be available in sufficient amounts or at reasonable cost. Further, it is possible that we may later reduce or terminate this coverage based on future availability of financial resources. Adverse liability claims may also harm our ability to obtain or maintain regulatory approvals.

| 13 |

We used hazardous materials and chemicals in our research and development, and our failure to comply with laws related to hazardous materials could materially harm us.